Fundamentals of Financial Management, 11/eCreated by: Gregory A. Kuhlemeyer, Ph.D.

Carroll College, Waukesha, WI

14-2

Risk and Managerial Risk and Managerial Options in Capital BudgetingOptions in Capital BudgetingRisk and Managerial Risk and Managerial Options in Capital BudgetingOptions in Capital Budgeting

The Problem of Project Risk

Total Project Risk

Contribution to Total Firm Risk: Firm-Portfolio Approach

Managerial Options

The Problem of Project Risk

Total Project Risk

Contribution to Total Firm Risk: Firm-Portfolio Approach

Managerial Options

14-3

An Illustration of Total An Illustration of Total Risk (Discrete Distribution)Risk (Discrete Distribution)An Illustration of Total An Illustration of Total Risk (Discrete Distribution)Risk (Discrete Distribution)

ANNUAL CASH FLOWS: YEAR 1PROPOSAL APROPOSAL A

State ProbabilityProbability Cash FlowCash Flow

Deep Recession .05 $ -3,000

Mild Recession .25 1,000

Normal .40 5,000

Minor Boom .25 9,000

Major Boom .05 13,000

ANNUAL CASH FLOWS: YEAR 1PROPOSAL APROPOSAL A

State ProbabilityProbability Cash FlowCash Flow

Deep Recession .05 $ -3,000

Mild Recession .25 1,000

Normal .40 5,000

Minor Boom .25 9,000

Major Boom .05 13,000

14-4

Probability Distribution Probability Distribution of Year 1 Cash Flowsof Year 1 Cash FlowsProbability Distribution Probability Distribution of Year 1 Cash Flowsof Year 1 Cash Flows

Expected Value of Year 1 Expected Value of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))Expected Value of Year 1 Expected Value of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))

Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))

14-7

Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal AProposal A))

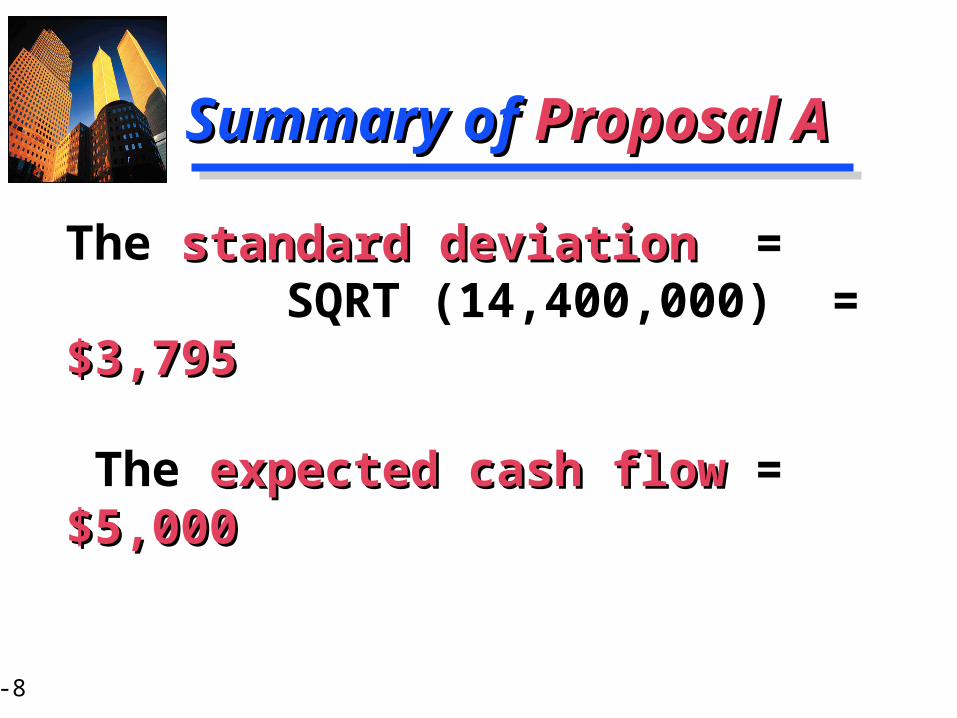

The standard deviation standard deviation = SQRT (14,400,000) = $3,795$3,795

The expected cash flow expected cash flow = $5,000$5,000

14-9

An Illustration of Total An Illustration of Total Risk (Discrete Distribution)Risk (Discrete Distribution)An Illustration of Total An Illustration of Total Risk (Discrete Distribution)Risk (Discrete Distribution)

ANNUAL CASH FLOWS: YEAR 1PROPOSAL BPROPOSAL B

State ProbabilityProbability Cash FlowCash Flow

Deep Recession .05 $ -1,000

Mild Recession .25 2,000

Normal .40 5,000

Minor Boom .25 8,000

Major Boom .05 11,000

ANNUAL CASH FLOWS: YEAR 1PROPOSAL BPROPOSAL B

State ProbabilityProbability Cash FlowCash Flow

Deep Recession .05 $ -1,000

Mild Recession .25 2,000

Normal .40 5,000

Minor Boom .25 8,000

Major Boom .05 11,000

14-10

Probability Distribution Probability Distribution of Year 1 Cash Flowsof Year 1 Cash FlowsProbability Distribution Probability Distribution of Year 1 Cash Flowsof Year 1 Cash Flows

.40

.05

.25

Pro

bab

ility

-3,000 1,000 5,000 9,000 13,000

Cash Flow ($)

Proposal BProposal B

14-11

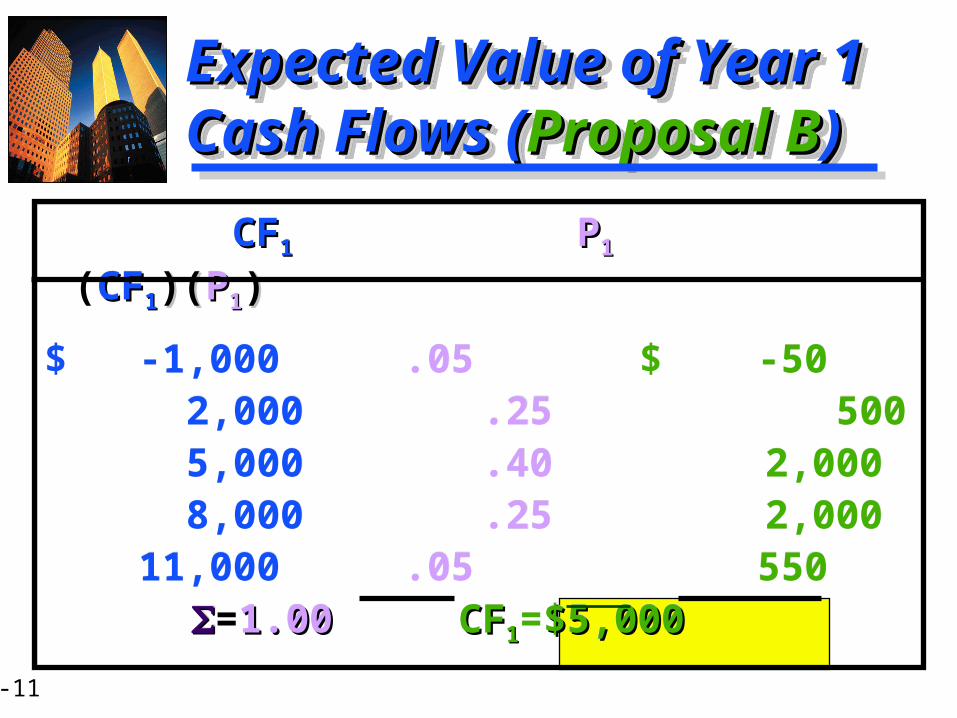

Expected Value of Year 1 Expected Value of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))Expected Value of Year 1 Expected Value of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))

Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))

14-13

Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))Variance of Year 1 Variance of Year 1 Cash Flows (Cash Flows (Proposal BProposal B))

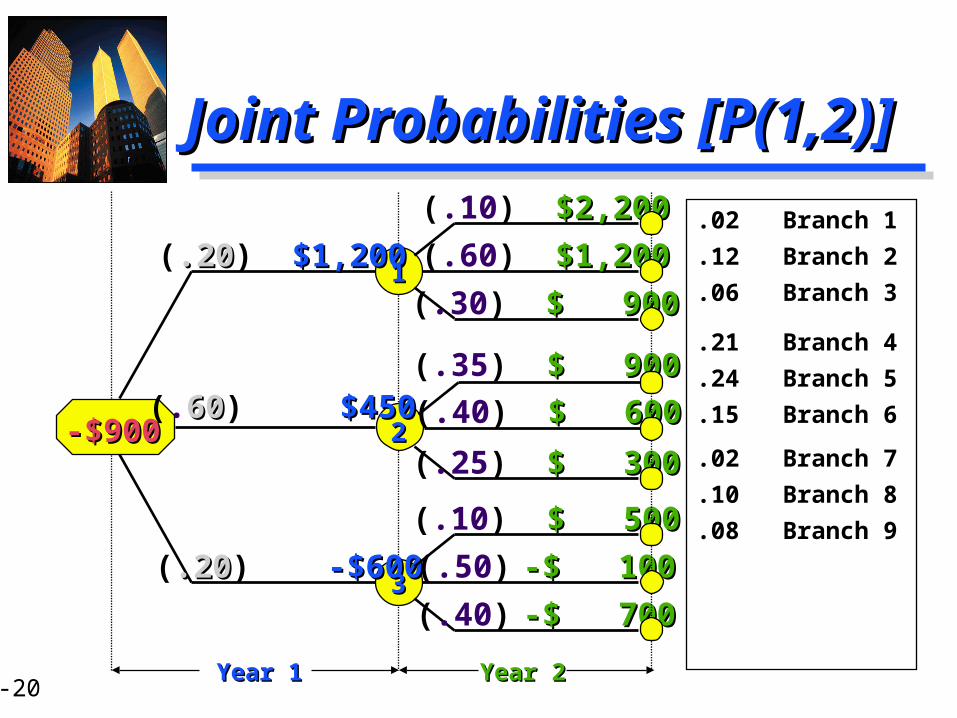

Project NPV Based on Project NPV Based on Probability Tree UsageProbability Tree Usage

The probability tree accounts for the distribution of cash flows.

Therefore, discount all cash flows at only the risk-freerisk-free rate of

return.

The NPV for branch i NPV for branch i of the probability tree for two

years of cash flows is

NPV = (NPVNPVii)(PPii)

NPVNPVii = CFCF11

(1 + RRff )11 (1 + RRff )22

CFCF22

- ICOICO

+

i = 1

z

14-22

NPV for Each Cash-Flow NPV for Each Cash-Flow Stream at 5% Risk-Free RateStream at 5% Risk-Free Rate

$ 2,238.32

$ 1,331.29

$ 1,059.18

$ 344.90

$ 72.79

-$ 199.32

-$ 1,017.91

-$ 1,562.13

-$ 2,106.35

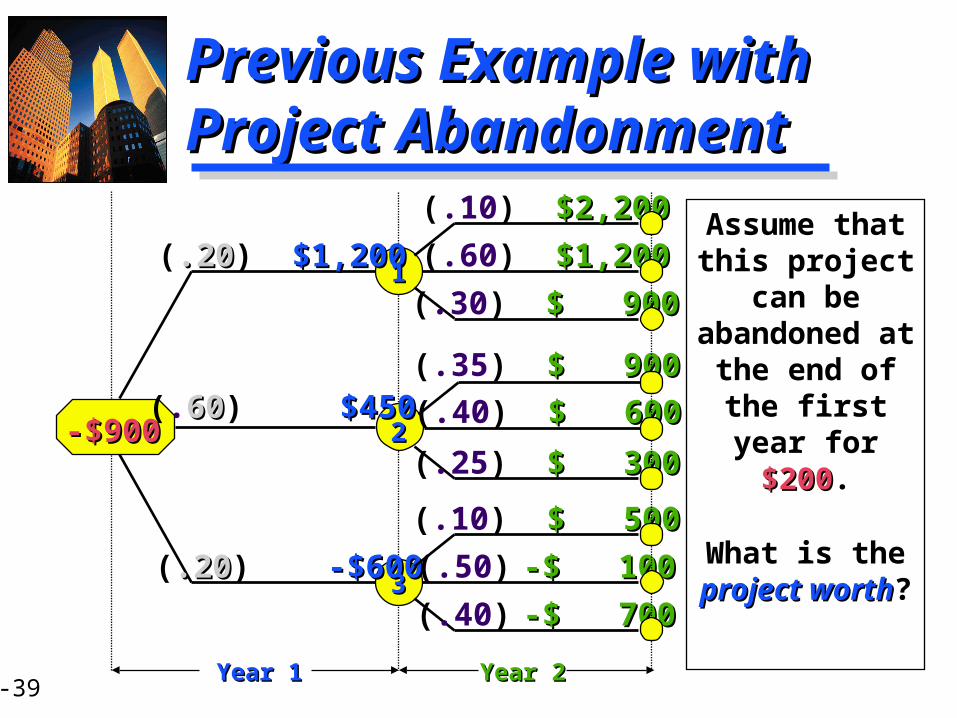

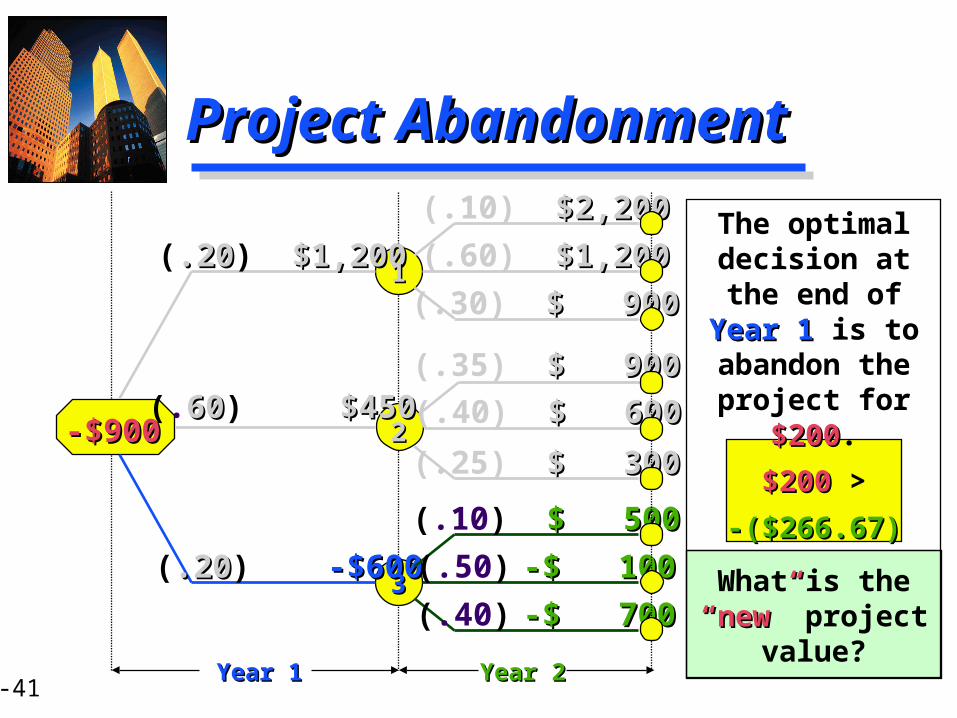

-$900-$900

(.20.20) $1,200$1,200

(.20.20) -$600-$600

(.6060) $450$450

Year 1Year 1

11

22

33

(.60) $1,200$1,200

(.30) $ 900$ 900

(.10) $2,200$2,200

(.35) $ 900$ 900

(.40) $ 600$ 600

(.25) $ 300 $ 300

(.10) $ 500$ 500

(.50) -$ 100-$ 100

(.40) -$ 700-$ 700

Year 2Year 2

14-23

NPV on the CalculatorNPV on the Calculator

Remember, we can use the cash flow registry

to solve these NPV problems quickly and

accurately!

14-24

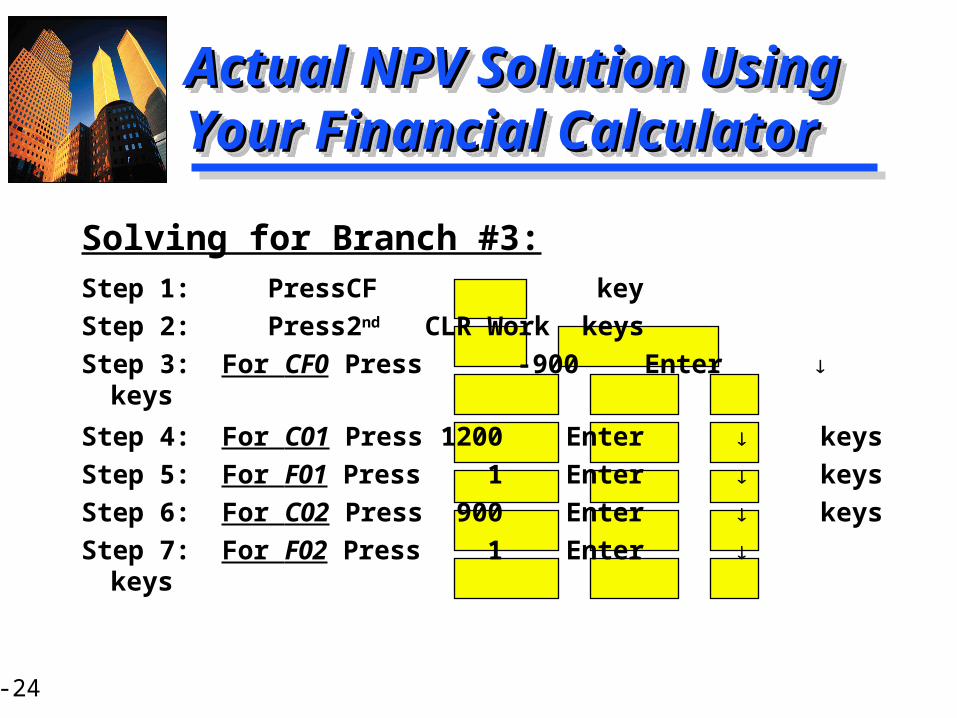

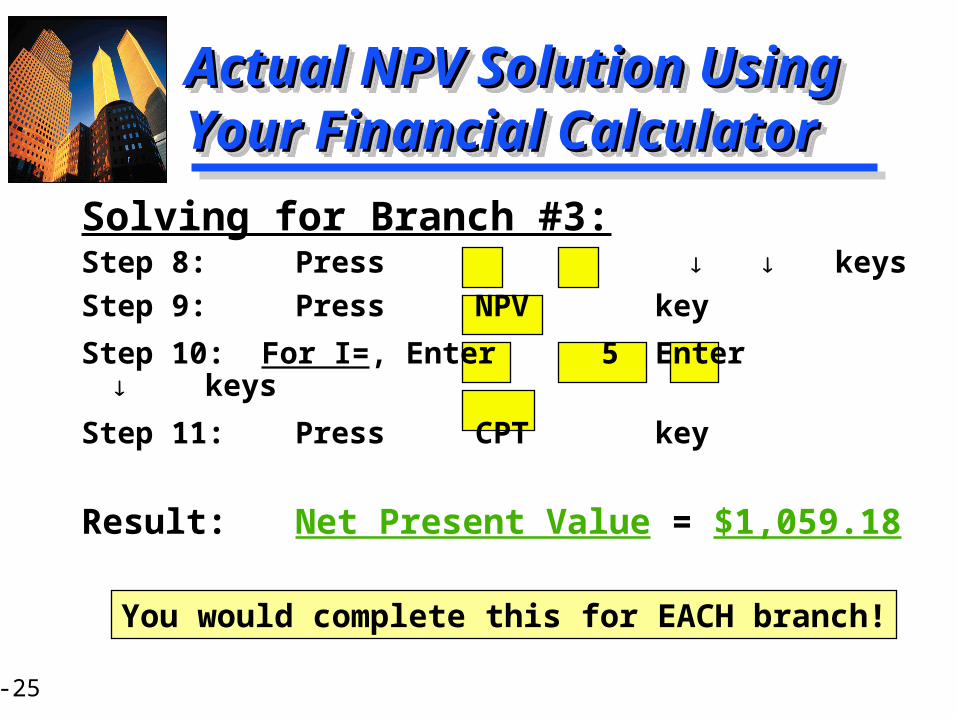

Actual NPV Solution Using Actual NPV Solution Using Your Financial CalculatorYour Financial CalculatorActual NPV Solution Using Actual NPV Solution Using Your Financial CalculatorYour Financial Calculator

Solving for Branch #3:Step 1: Press CF key

Step 2: Press 2nd CLR Work keys

Step 3: For CF0 Press -900 Enter keys

Step 4: For C01 Press 1200 Enter keys

Step 5: For F01 Press 1 Enter keys

Step 6: For C02 Press 900 Enter keys

Step 7: For F02 Press 1 Enter keys

14-25

Actual NPV Solution Using Actual NPV Solution Using Your Financial CalculatorYour Financial CalculatorActual NPV Solution Using Actual NPV Solution Using Your Financial CalculatorYour Financial Calculator

Solving for Branch #3:

Step 8: Press keys

Step 9: Press NPV key

Step 10: For I=, Enter 5 Enter keys

Step 11: Press CPT key

Result: Net Present Value = $1,059.18

You would complete this for EACH branch!

14-26

Calculating the Expected Calculating the Expected Net Present Value (Net Present Value (NPVNPV))

The resulting proposal value is dependent on the distribution and interaction of EVERY variable listed on slide 14-30.

14-32

Simulation ApproachSimulation Approach

Each proposal will generate an internal rate of internal rate of returnreturn. The process of generating many, many

simulations results in a large set of internal rates of return. The distributiondistribution might look like

the following:

INTERNAL RATE OF RETURN (%)

PR

OB

AB

ILIT

YO

F O

CC

UR

RE

NC

E

14-33

Combining projects in this manner reduces the firm risk due to diversificationdiversification.

Combining projects in this manner reduces the firm risk due to diversificationdiversification.

Contribution to Total Firm Risk: Contribution to Total Firm Risk: Firm-Portfolio ApproachFirm-Portfolio ApproachContribution to Total Firm Risk: Contribution to Total Firm Risk: Firm-Portfolio ApproachFirm-Portfolio Approach

CA

SH

FL

OW

TIME TIMETIME

Proposal AProposal A Proposal BProposal BCombination of Combination of

Proposals Proposals AA andand BB

14-34

NPVP = ( NPVj )

NPVP is the expected portfolio NPV,

NPVj is the expected NPV of the jth NPV that the firm undertakes,

m is the total number of projects in the firm portfolio.

NPVP = ( NPVj )

NPVP is the expected portfolio NPV,

NPVj is the expected NPV of the jth NPV that the firm undertakes,

m is the total number of projects in the firm portfolio.

Determining the Expected Determining the Expected NPV for a Portfolio of ProjectsNPV for a Portfolio of ProjectsDetermining the Expected Determining the Expected NPV for a Portfolio of ProjectsNPV for a Portfolio of Projects

m

j=1

14-35

PP = jk

jk is the covariance between possible

NPVs for projects j and k

jk = j k rrjk .

j is the standard deviation of project j,

k is the standard deviation of project k,

rjk is the correlation coefficient between projects j and k.

PP = jk

jk is the covariance between possible

NPVs for projects j and k

jk = j k rrjk .

j is the standard deviation of project j,

k is the standard deviation of project k,

rjk is the correlation coefficient between projects j and k.

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

m

j=1

m

k=1

14-36

E: Existing ProjectsE: Existing Projects

8 Combinations

EE EE + 1 EE + 1 + 2 EE + 2 EE + 1 + 3EE + 3 EE + 2 + 3

EE + 1 + 2 + 3

AA, BB, and CC are dominatingdominating combinations from the eight possible.

Combinations of Combinations of Risky InvestmentsRisky Investments

![[PPT]Edmonds Managerial Chapter 14 - Faculty Website …faculty.valenciacollege.edu/jrallis/acg2071/chap001.ppt · Web viewTitle Edmonds Managerial Chapter 14 Subject Statement of](https://static.documents.pub/doc/80x56/5b45c3a37f8b9ad1138bf412/pptedmonds-managerial-chapter-14-faculty-website-web-viewtitle-edmonds-managerial.jpg)

![[PPT]Edmonds Managerial Chapter 14 - Valencia Collegefaculty.valenciacollege.edu/jrallis/acg2071/Edmonds09No... · Web viewTitle Edmonds Managerial Chapter 14 Subject Statement of](https://static.documents.pub/doc/80x56/5b45c3a37f8b9ad1138bf403/pptedmonds-managerial-chapter-14-valencia-web-viewtitle-edmonds-managerial.jpg)