26

2

Energy market overview

CPFL Energia – Highlights and Results

Summary

3

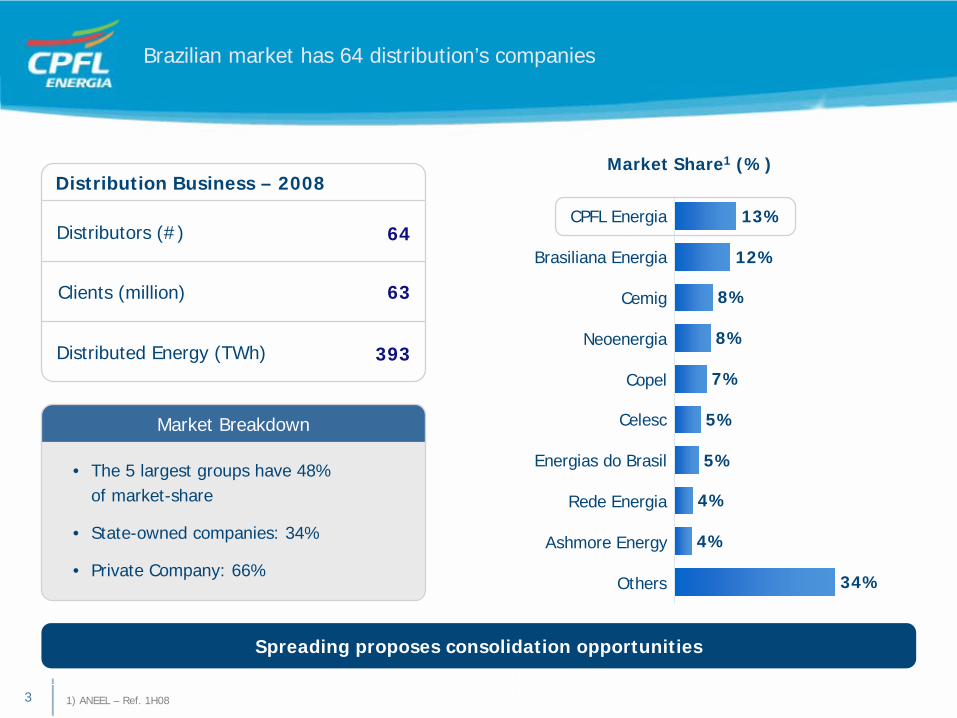

13%

12%

8%

8%

7%

5%

5%

4%

4%

34%

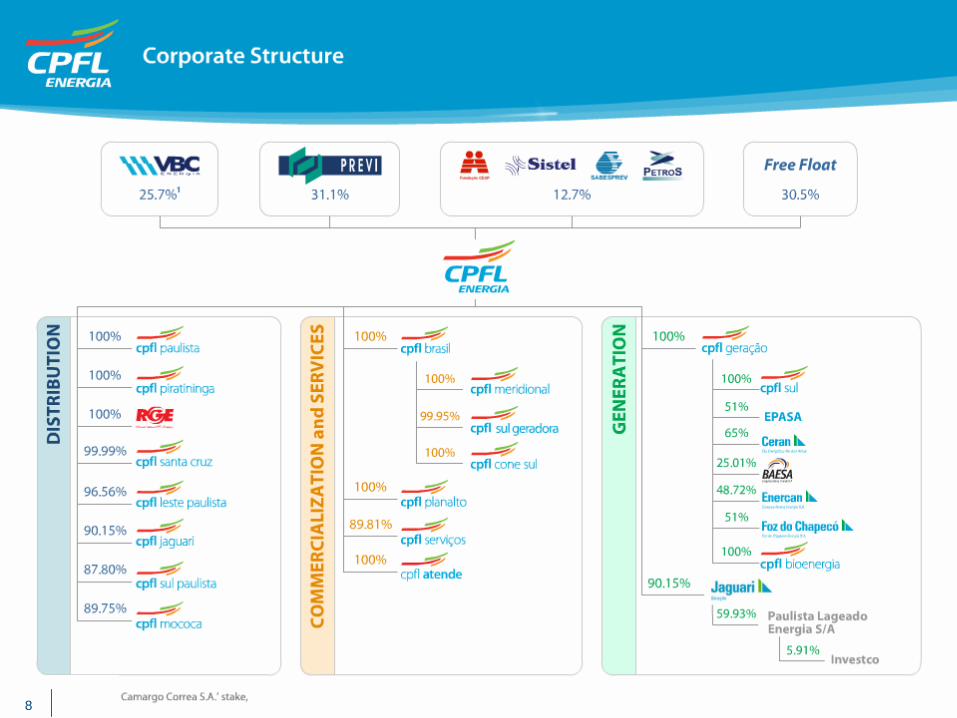

CPFL Energia

Brasiliana Energia

Cemig

Neoenergia

Copel

Celesc

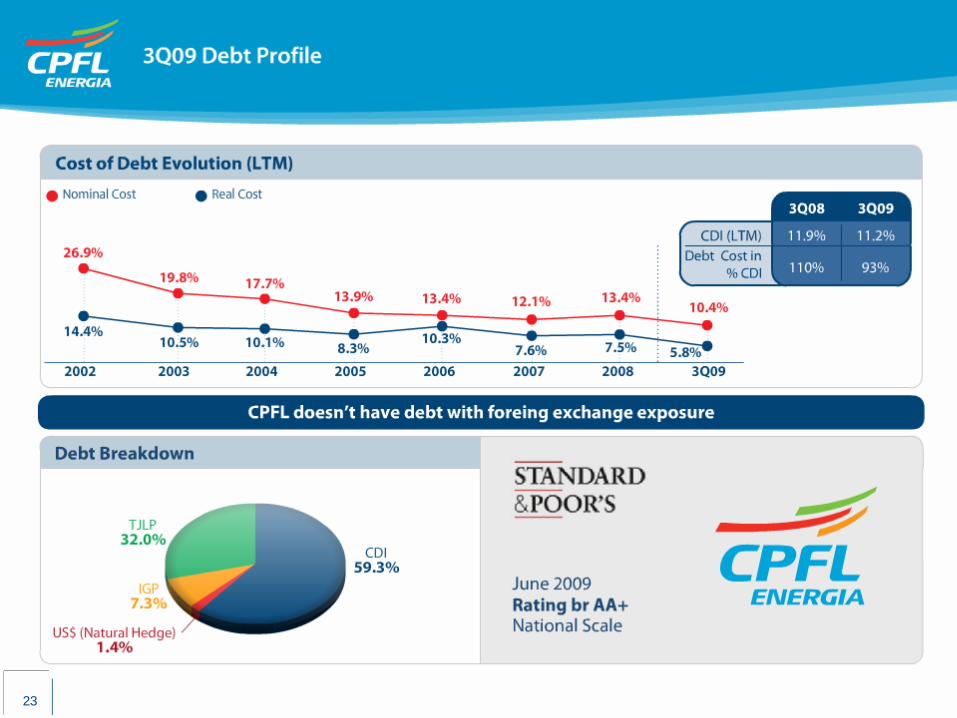

Energias do Brasil

Rede Energia

Ashmore Energy

Others

Market Share1 (%)

1) ANEEL – Ref. 1H08

Brazilian market has 64 distribution’s companies

Distribution Business – 2008

Distributors (#) 64

63Clients (million)

Distributed Energy (TWh) 393

Market Breakdown

• The 5 largest groups have 48%of market-share

• State-owned companies: 34%

• Private Company: 66%

Spreading proposes consolidation opportunities

4

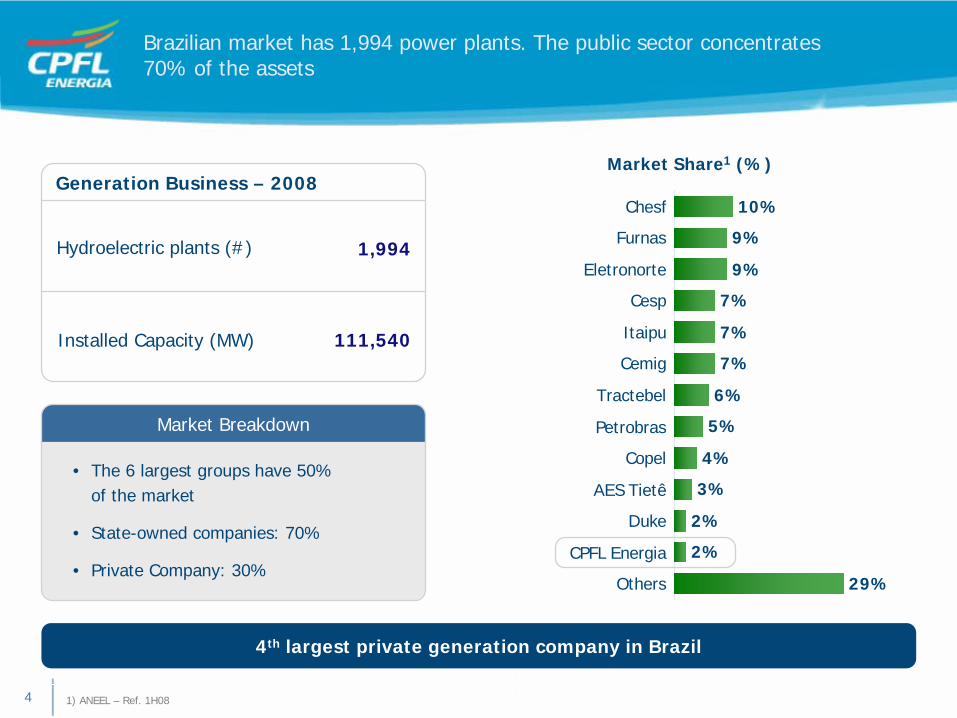

Market Share1 (%)

1) ANEEL – Ref. 1H08

Brazilian market has 1,994 power plants. The public sector concentrates 70% of the assets

Generation Business – 2008

Hydroelectric plants (#) 1,994

111,540Installed Capacity (MW)

Market Breakdown

• The 6 largest groups have 50% of the market

• State-owned companies: 70%

• Private Company: 30%

4th largest private generation company in Brazil

10%

9%

9%

7%

7%

7%

6%

5%

4%

3%

2%

2%

29%

Chesf

Furnas

Eletronorte

Cesp

Itaipu

Cemig

Tractebel

Petrobras

Copel

AES Tietê

Duke

CPFL Energia

Others

5

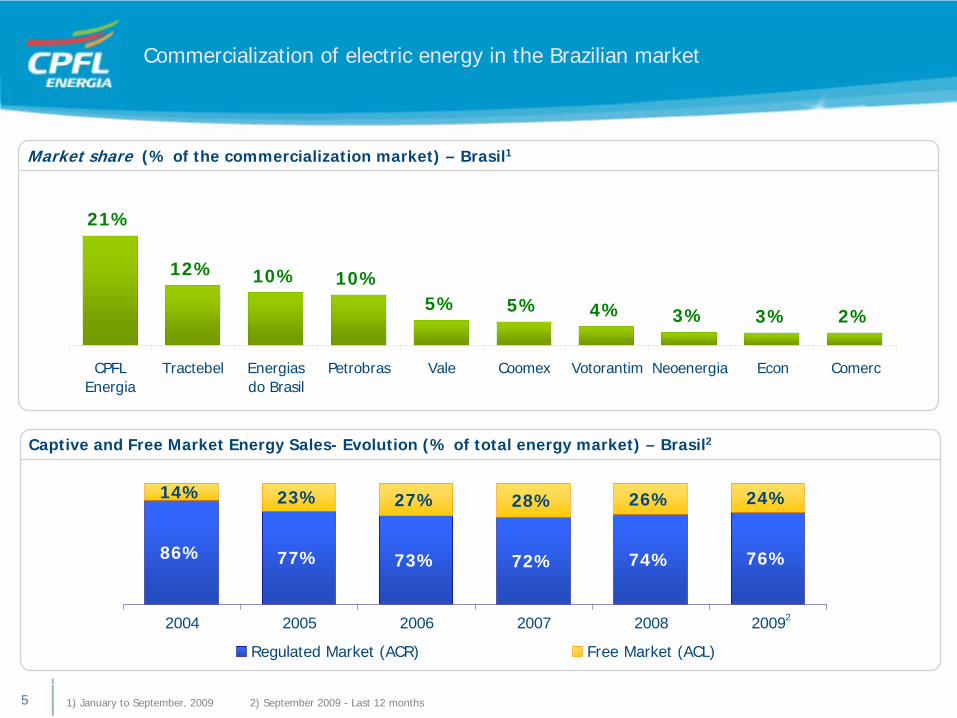

86% 77% 73% 72% 74% 76%

14% 23% 27% 28% 26% 24%

2004 2005 2006 2007 2008 2009

Regulated Market (ACR) Free Market (ACL)

2

Captive and Free Market Energy Sales- Evolution (% of total energy market) – Brasil2

Market share (% of the commercialization market) – Brasil1

21%

12% 10% 10%5% 5% 4% 3% 3% 2%

CPFLEnergia

Tractebel Energiasdo Brasil

Petrobras Vale Coomex Votorantim Neoenergia Econ Comerc

1) January to September, 2009 2) September 2009 - Last 12 months

Commercialization of electric energy in the Brazilian market

5

6

Energy market overview

CPFL Energia – Highlights and Results

Summary

7

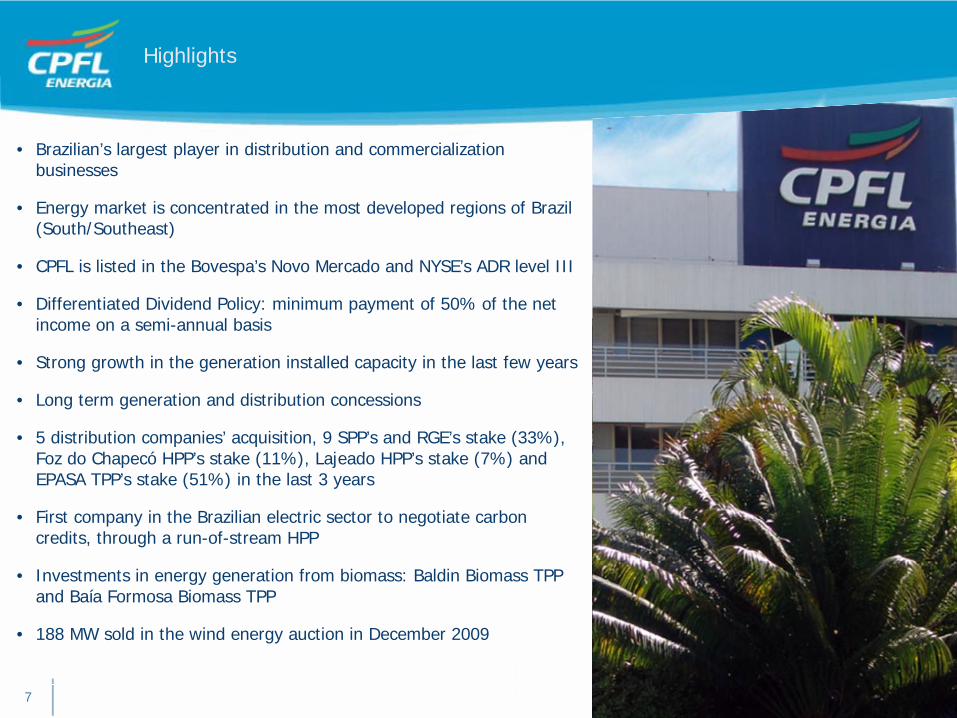

• Brazilian’s largest player in distribution and commercializationbusinesses

• Energy market is concentrated in the most developed regions of Brazil (South/Southeast)

• CPFL is listed in the Bovespa’s Novo Mercado and NYSE’s ADR level III

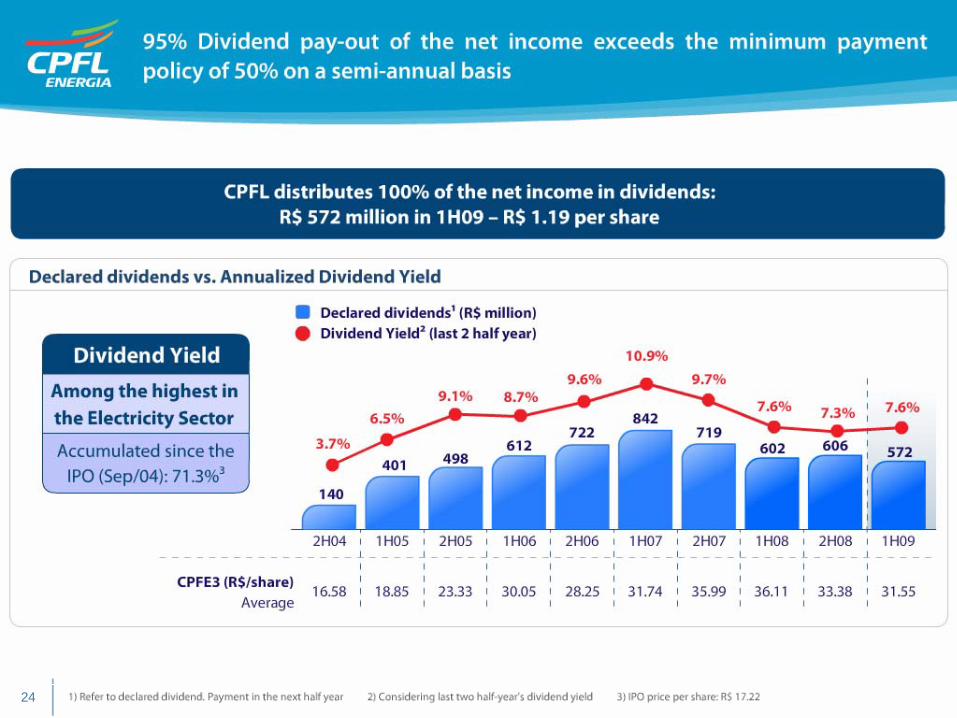

• Differentiated Dividend Policy: minimum payment of 50% of the net income on a semi-annual basis

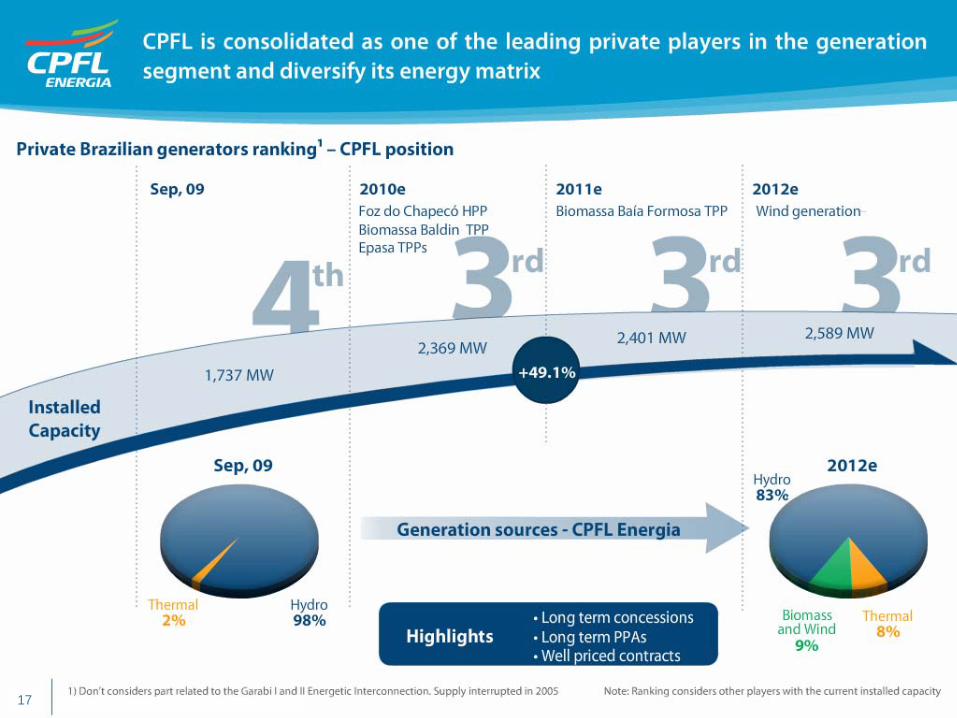

• Strong growth in the generation installed capacity in the last few years

• Long term generation and distribution concessions

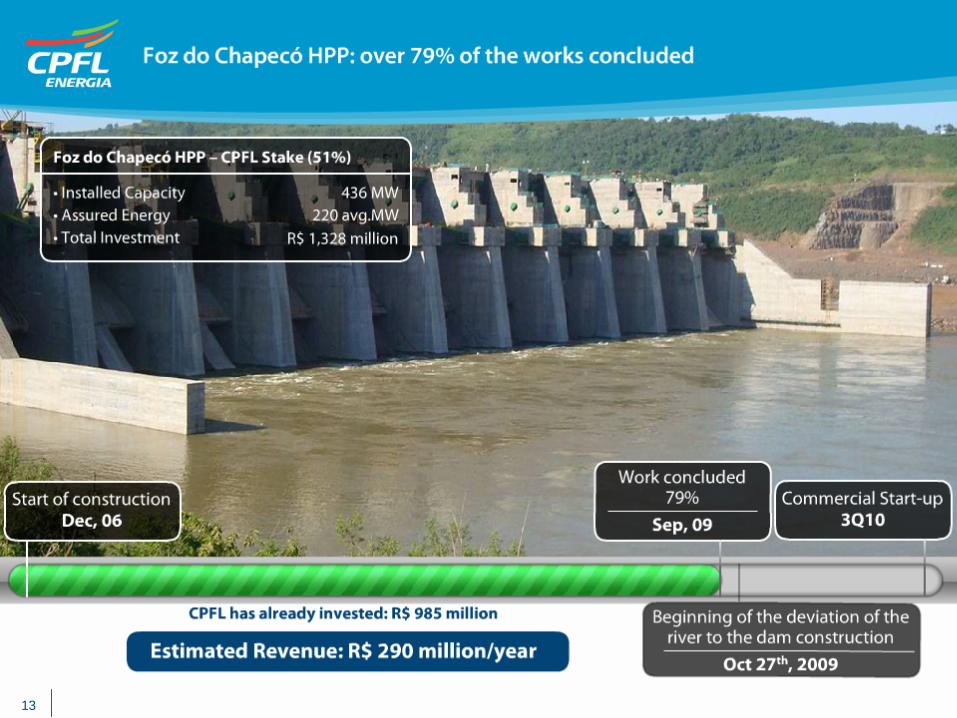

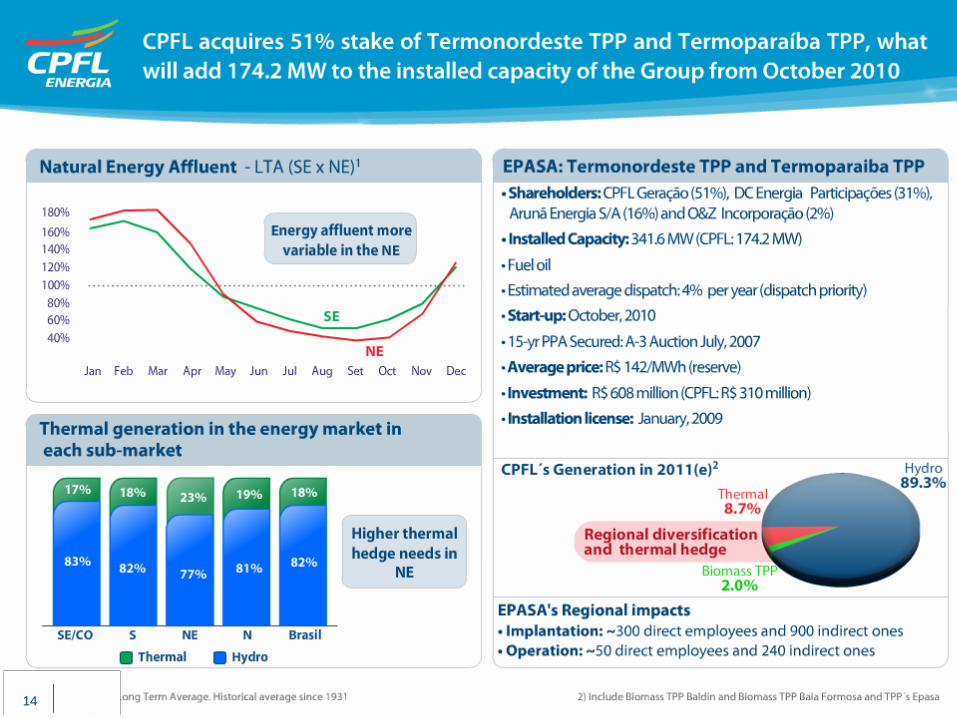

• 5 distribution companies’ acquisition, 9 SPP’s and RGE’s stake (33%), Foz do Chapecó HPP’s stake (11%), Lajeado HPP’s stake (7%) and EPASA TPP’s stake (51%) in the last 3 years

• First company in the Brazilian electric sector to negotiate carbon credits, through a run-of-stream HPP

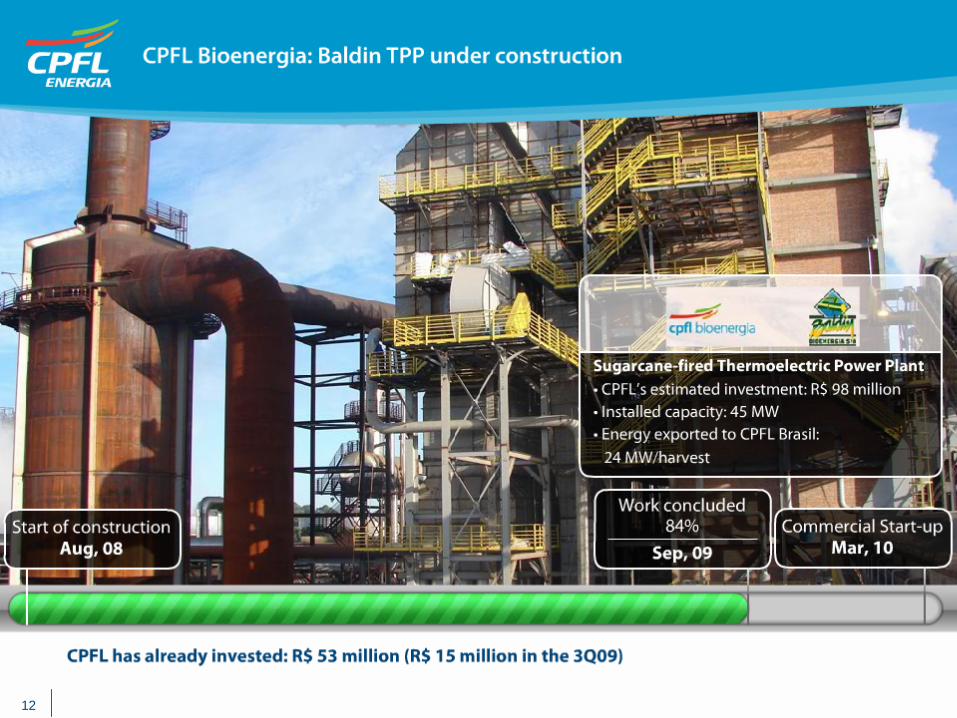

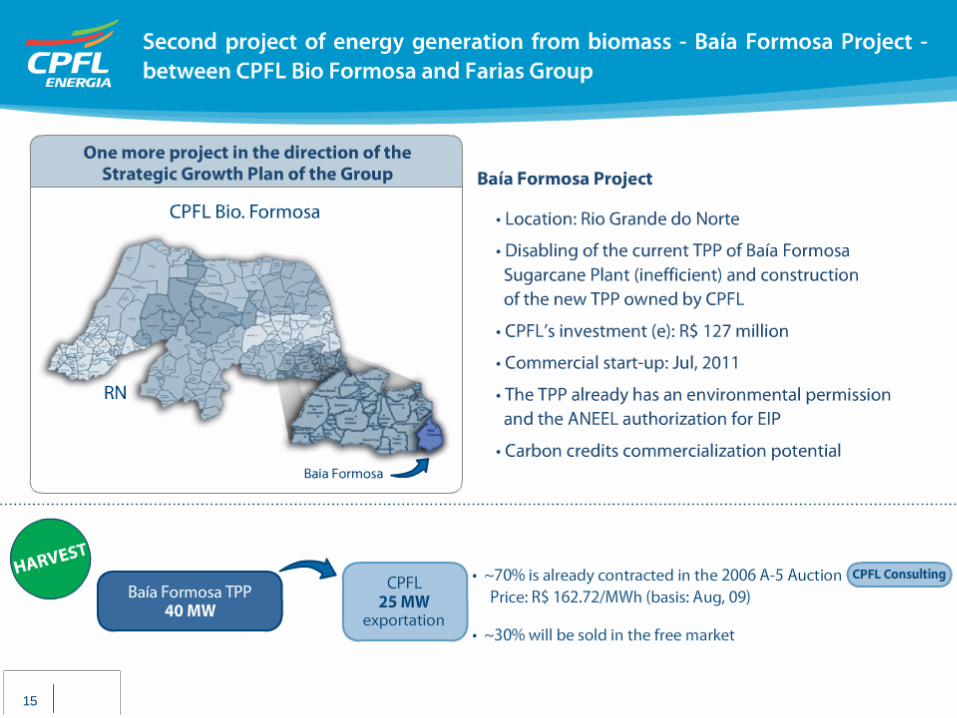

• Investments in energy generation from biomass: Baldin Biomass TPP and Baía Formosa Biomass TPP

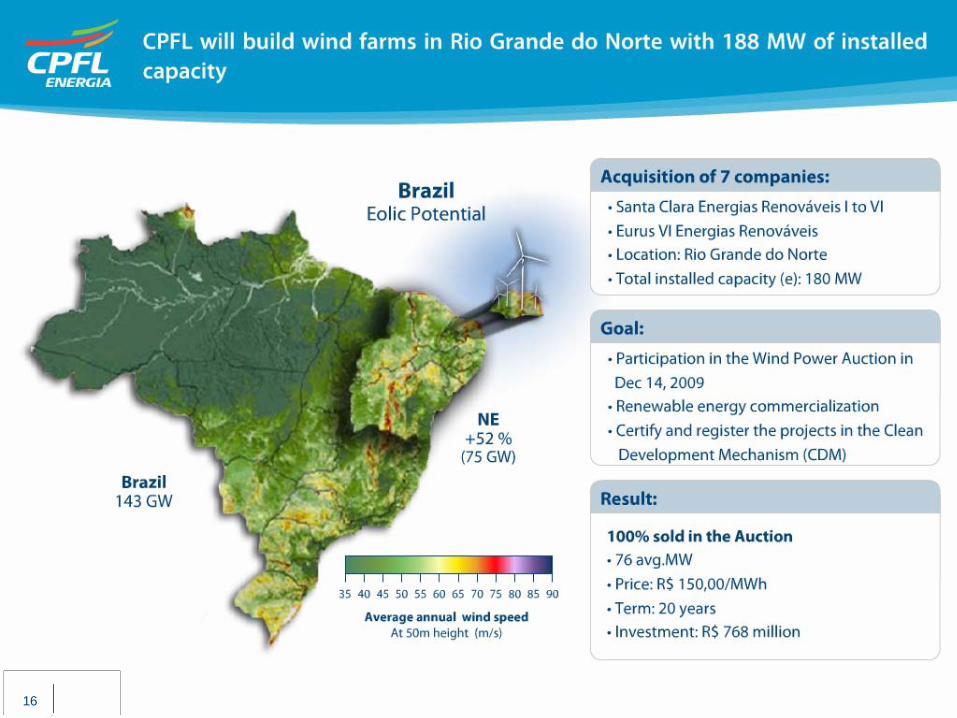

• 188 MW sold in the wind energy auction in December 2009

Highlights

88

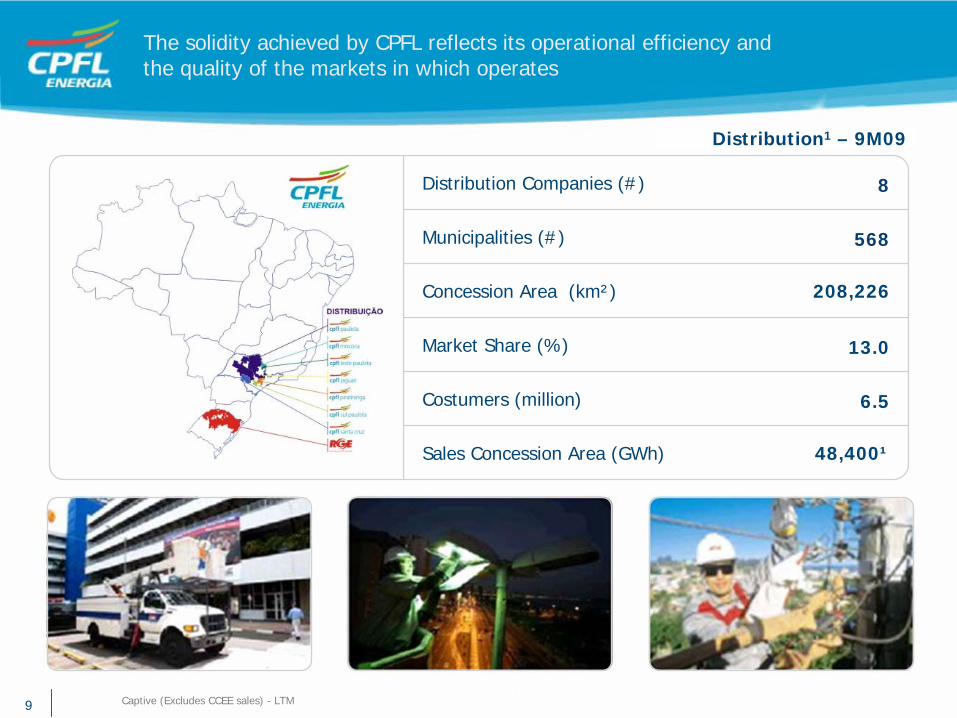

9 1) TUSD + Captive (Excludes CCEE sales) - LTM

The solidity achieved by CPFL reflects its operational efficiency and the quality of the markets in which operates

Distribution1 – 9M09

48,400¹Sales Concession Area (GWh)

6.5Costumers (million)

13.0Market Share (%)

208,226Concession Area (km²)

568Municipalities (#)

8Distribution Companies (#)

9

10

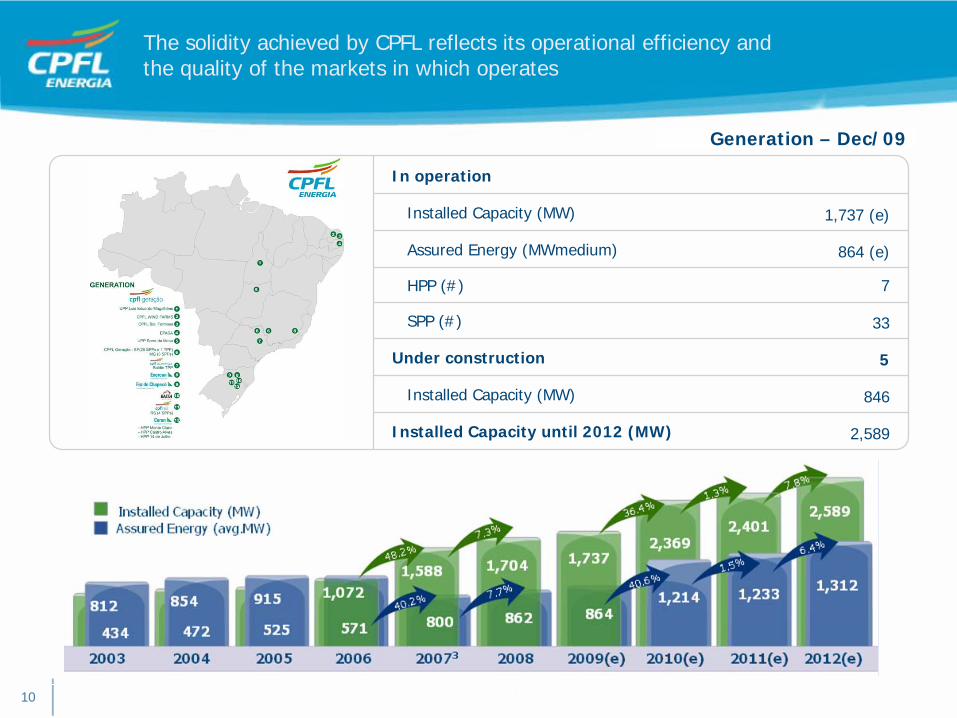

The solidity achieved by CPFL reflects its operational efficiency and the quality of the markets in which operates

2,589Installed Capacity until 2012 (MW)

846Installed Capacity (MW)

In operation

5Under construction

33SPP (#)

7HPP (#)

864 (e)Assured Energy (MWmedium)

1,737 (e)Installed Capacity (MW)

Generation – Dec/09

11

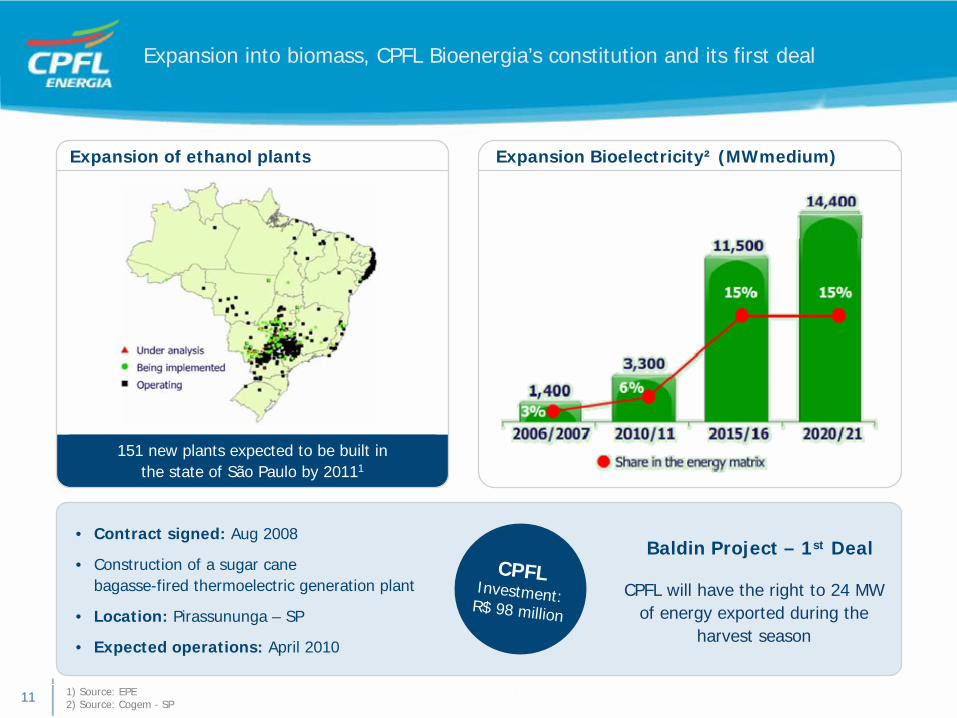

• Contract signed: Aug 2008

• Construction of a sugar cane bagasse-fired thermoelectric generation plant

• Location: Pirassununga – SP

• Expected operations: April 2010

CPFLInvestment:R$ 98 million

CPFL will have the right to 24 MW of energy exported during the

harvest season

Baldin Project – 1st Deal

1) Source: EPE2) Source: Cogem - SP

Expansion Bioelectricity² (MWmedium) Expansion of ethanol plants

Expansion into biomass, CPFL Bioenergia’s constitution and its first deal

151 new plants expected to be built inthe state of São Paulo by 20111

1212

1313

1414

1515

1616

1717

1818

1919

20

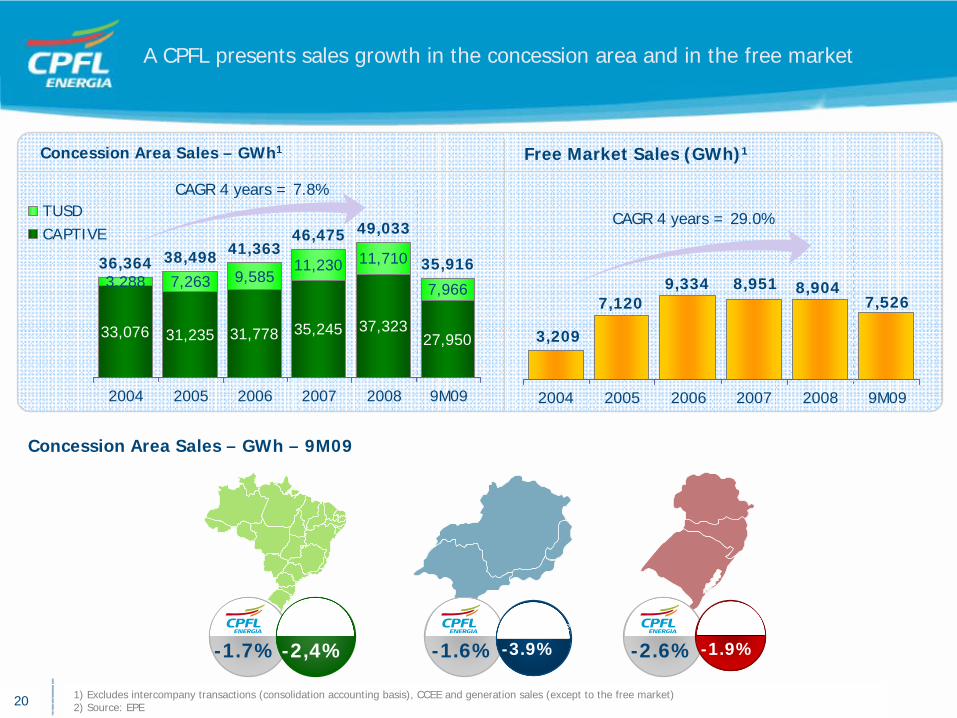

A CPFL presents sales growth in the concession area and in the free market

27,95033,076 31,235 37,32335,24531,778

7,966

11,7103,288

11,2309,5857,263

35,916

49,033

38,49836,364

46,47541,363

2004 2005 2006 2007 2008 9M09

TUSDCAPTIVE

7,5268,9048,9519,334

7,120

3,209

2004 2005 2006 2007 2008 9M09

Concession Area Sales – GWh1 Free Market Sales (GWh)1

CAGR 4 years = 7.8%

CAGR 4 years = 29.0%

1) Excludes intercompany transactions (consolidation accounting basis), CCEE and generation sales (except to the free market)2) Source: EPE

Concession Area Sales – GWh – 9M09

2020 1) Excludes intercompany transactions (consolidation accounting basis), CCEE and generation sales (except to the free market)2) Source: EPE

-1.7% -2,4%Brazil2

-1.6% -3.9%Southeast2

-2.6% -1.9%South2

21

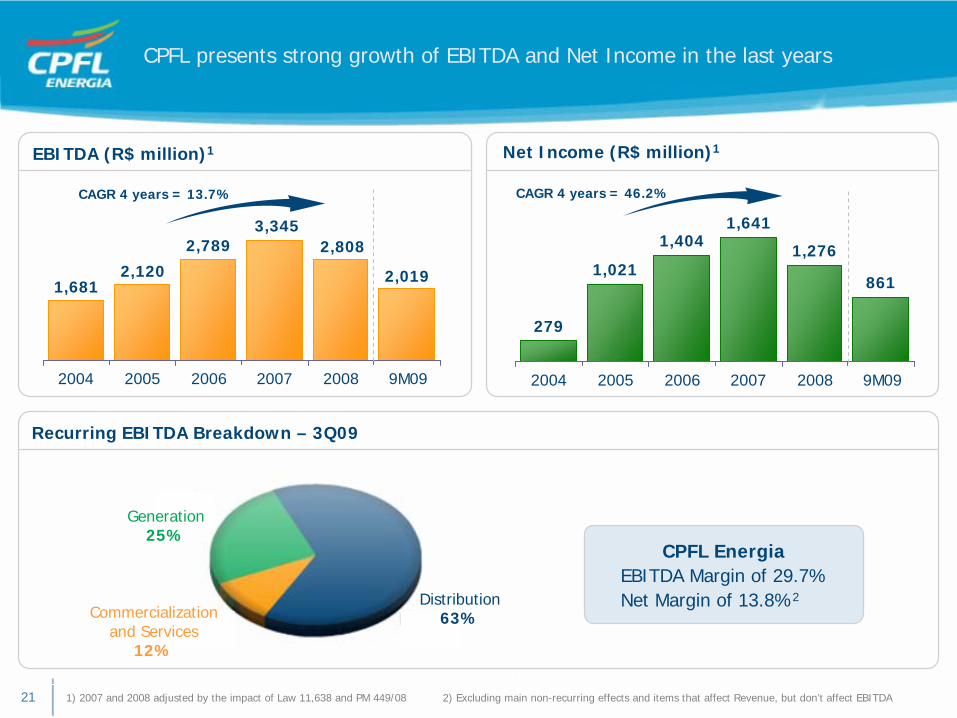

279

861

1,276

1,6411,404

1,021

2004 2005 2006 2007 2008 9M09

EBITDA (R$ million)1 Net Income (R$ million)1

2,019

2,8083,345

2,789

2,1201,681

2004 2005 2006 2007 2008 9M09

CAGR 4 years = 46.2%

Recurring EBITDA Breakdown – 3Q09

CAGR 4 years = 13.7%

1) 2007 and 2008 adjusted by the impact of Law 11,638 and PM 449/08 2) Excluding main non-recurring effects and items that affect Revenue, but don’t affect EBITDA

CPFL presents strong growth of EBITDA and Net Income in the last years

CPFL Energia EBITDA Margin of 29.7%Net Margin of 13.8%2

Commercializationand Services

12%

Distribution63%

Generation25%

2222

2323

24

2525