33

©2004 by Nelson, a division of Thomson Canada Limited 1 Chapter 7 Control

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | amice-west |

| View: | 231 times |

| Download: | 0 times |

©2004 by Nelson, a division of Thomson Canada Limited 1

Chapter 7

Control

©2004 by Nelson, a division of Thomson Canada Limited 2

What Would You Do?

Howmet opened a new plant in Laval

Aircraft parts market plummeted Layoffs were a possibility How can costs be cut to make up

for the sales shortage?

©2004 by Nelson, a division of Thomson Canada Limited 3

Learning Objectives:Basics of Control

After reading the next two sections, you should be able to:

1. describe the basic control process2. answer the question: Is control necessary or possible?

©2004 by Nelson, a division of Thomson Canada Limited 4

The Control Process Establish clear standards Compare actual to

standard performance Take corrective action, if

needed Control is a continuous,

dynamic process Three basic methods

©2004 by Nelson, a division of Thomson Canada Limited 5

Standards

Determine what should be benchmarked

Identify companies against which to benchmark standards

Collect data to determine other companies’ performance standards

©2004 by Nelson, a division of Thomson Canada Limited 6

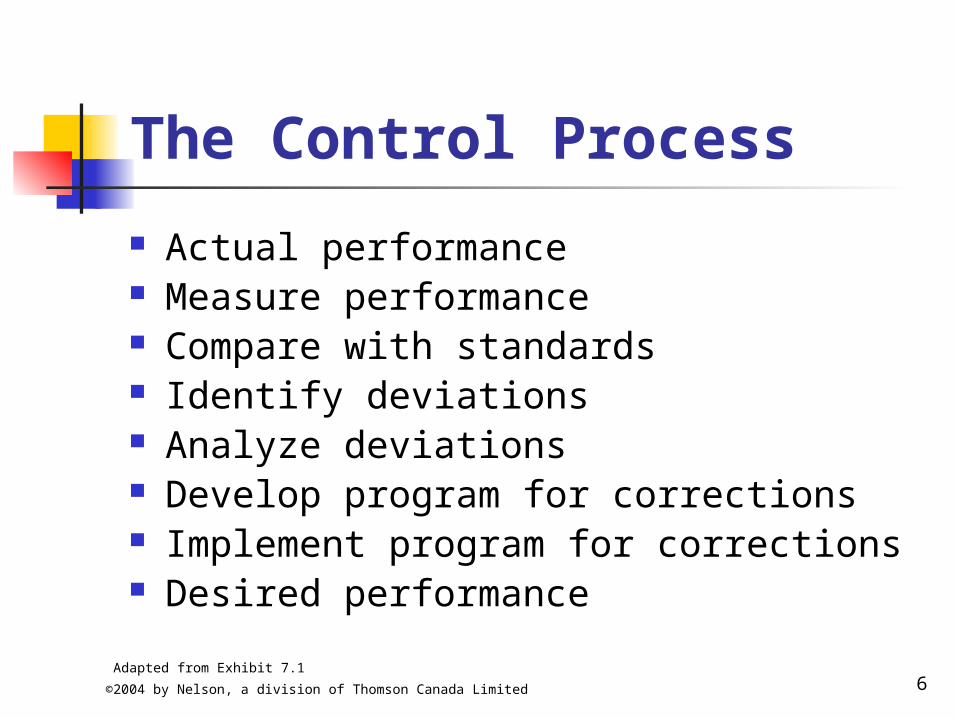

The Control Process

Actual performance Measure performance Compare with standards Identify deviations Analyze deviations Develop program for corrections Implement program for corrections Desired performance

Adapted from Exhibit 7.1

©2004 by Nelson, a division of Thomson Canada Limited 7

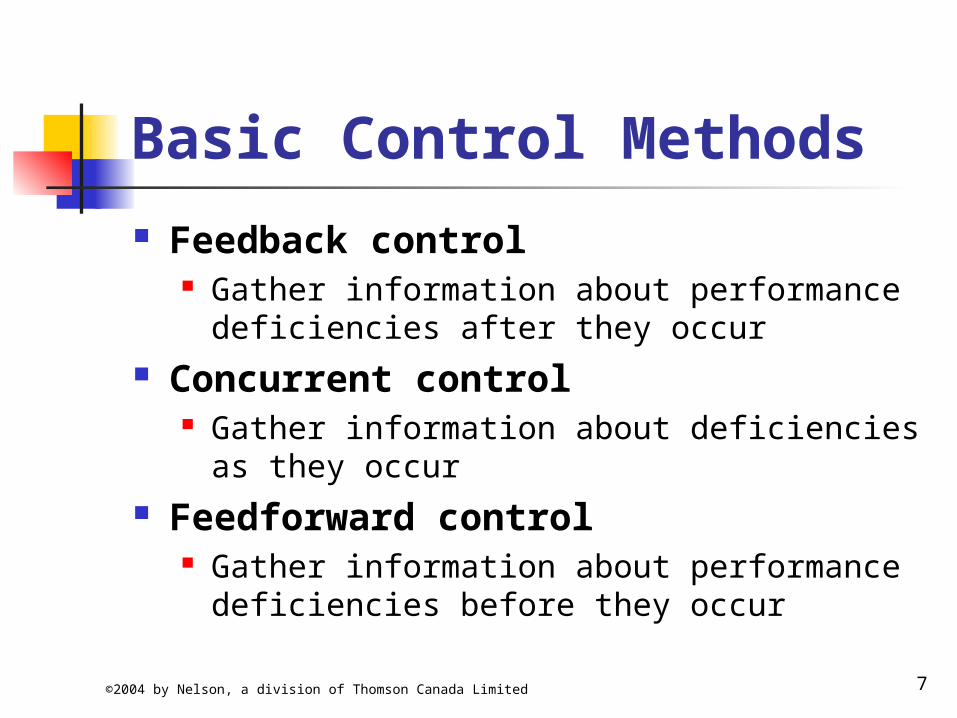

Basic Control Methods Feedback control

Gather information about performance deficiencies after they occur

Concurrent control Gather information about deficiencies as

they occur Feedforward control

Gather information about performance deficiencies before they occur

©2004 by Nelson, a division of Thomson Canada Limited 8

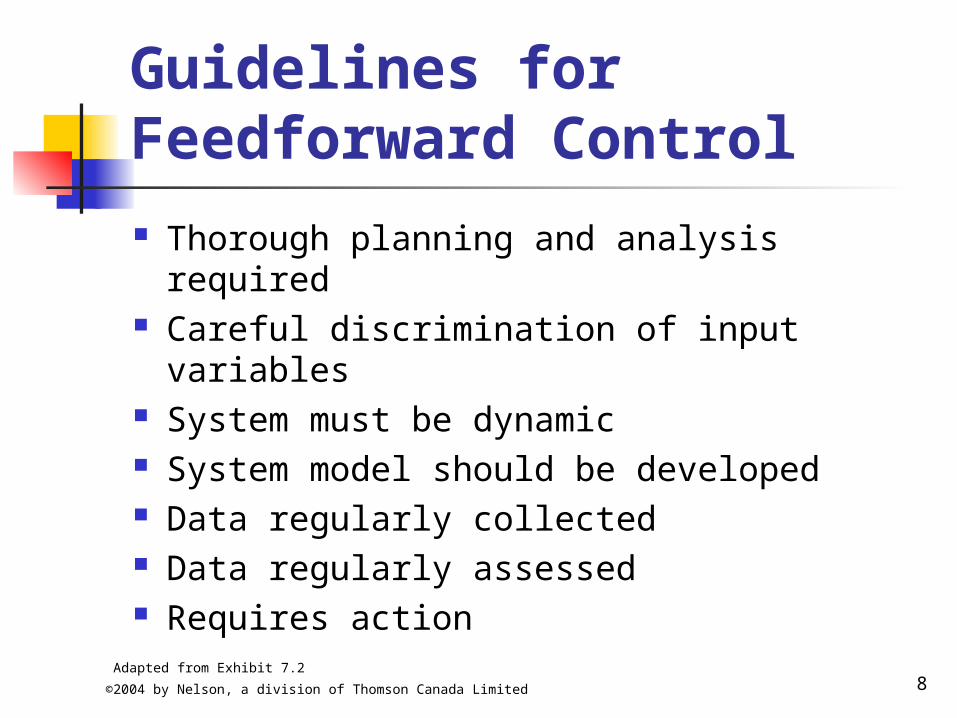

Guidelines for Feedforward Control Thorough planning and analysis

required Careful discrimination of input variables System must be dynamic System model should be developed Data regularly collected Data regularly assessed Requires action

Adapted from Exhibit 7.2

©2004 by Nelson, a division of Thomson Canada Limited 9

Is Control Necessary or Possible?

Is more control necessary? Is more control possible? Quasi-Control: When control isn’t

possible

©2004 by Nelson, a division of Thomson Canada Limited 10

Is More Control Necessary?

Degree of dependence the extent to which a company needs

a particular resource to accomplish its goals

Resource flows The extent to which a company has

easy access to critical resources

©2004 by Nelson, a division of Thomson Canada Limited 11

Is More Control Possible?

Cost of control direct costs of control unintended costs

Cybernetic feasibility the extent to which it is possible to

implement each step in the control process

if a step cannot be implemented, then control may not be possible

©2004 by Nelson, a division of Thomson Canada Limited 12

Quasi-Control: When Control Isn’t Possible

Reducing independence a choice to abandon or change goals when control over a critical resource

is not possible Restructure dependence

exchange dependence on one critical resource for dependence on another

©2004 by Nelson, a division of Thomson Canada Limited 13

Learning Objectives:How and What to Control

After reading the next two sections, you should be able to:

3. Discuss the various methods that managers can use to maintain

control4. Describe the behaviours, processes, and outcomes tat managers are choosing to control in today’s organizations

©2004 by Nelson, a division of Thomson Canada Limited 14

Control Methods

Bureaucratic Objective Normative Concertive Self-Control

©2004 by Nelson, a division of Thomson Canada Limited 15

Bureaucratic Control Top-down control Use rewards and punishments to

influence employee behaviour Use policies and rules to control

behaviour Bureaucratically controlled

companies are resistant to change and slow to respond to customers

©2004 by Nelson, a division of Thomson Canada Limited 16

Objective Control

Use of observable methods Behaviour control

regulate actions and behaviours of employees

Output control measure employee outputs coupled with use of rewards and

incentives

©2004 by Nelson, a division of Thomson Canada Limited 17

Normative Control

Company values and beliefs guide employee behaviour and decisions.Created by:

Careful selection of employees Role-modeling and retelling of stories

©2004 by Nelson, a division of Thomson Canada Limited 18

Concertive Control

Employees are guided by beliefs that are shaped and negotiated by work groups.Autonomous work groups

operate without managers Members responsible for controlling

work group process, outputs, and behaviour

©2004 by Nelson, a division of Thomson Canada Limited 19

Self-Control

Employees control their own behaviour

Employees make decisions within clear boundaries

Managers and employees set goals and monitor their own progress

©2004 by Nelson, a division of Thomson Canada Limited 20

When to Use Different Methods of Control

Use bureaucratic control when standard operating procedures needed necessary to establish limits

Use behaviour control when easier to measure activities than outputs “cause-effect” relationships are clear good measures of behaviour are available

Adapted from Exhibit 7.4

©2004 by Nelson, a division of Thomson Canada Limited 21

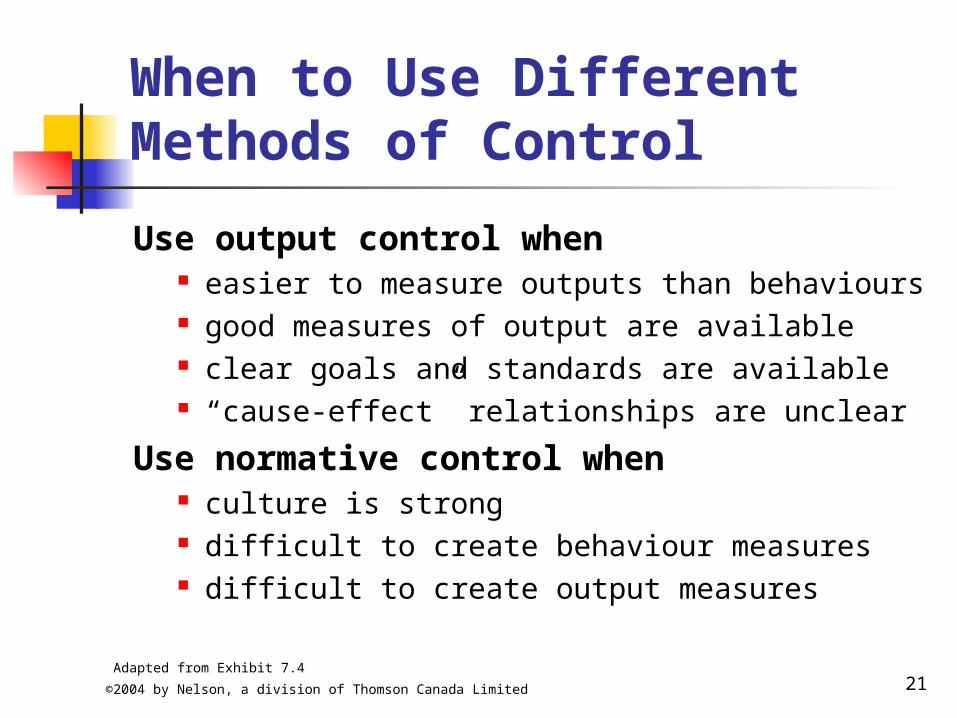

When to Use Different Methods of Control

Use output control when easier to measure outputs than behaviours good measures of output are available clear goals and standards are available “cause-effect” relationships are unclear

Use normative control when culture is strong difficult to create behaviour measures difficult to create output measures

Adapted from Exhibit 7.4

©2004 by Nelson, a division of Thomson Canada Limited 22

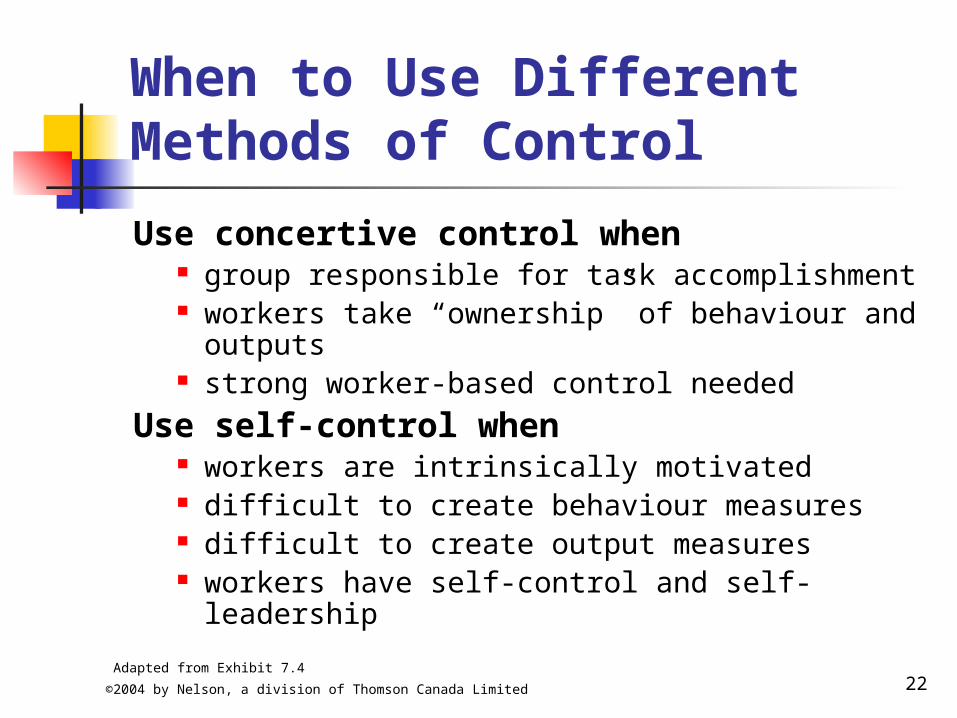

When to Use Different Methods of Control

Use concertive control when group responsible for task accomplishment workers take “ownership” of behaviour and

outputs strong worker-based control needed

Use self-control when workers are intrinsically motivated difficult to create behaviour measures difficult to create output measures workers have self-control and self-leadership

Adapted from Exhibit 7.4

©2004 by Nelson, a division of Thomson Canada Limited 23

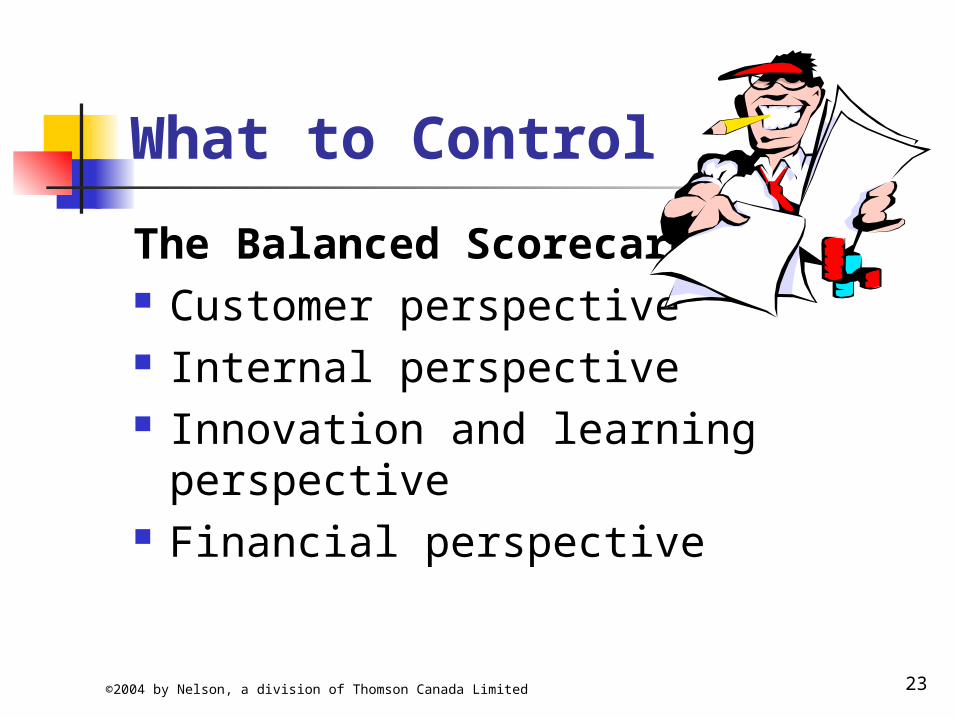

What to Control

The Balanced Scorecard Customer perspective Internal perspective Innovation and learning

perspective Financial perspective

©2004 by Nelson, a division of Thomson Canada Limited 24

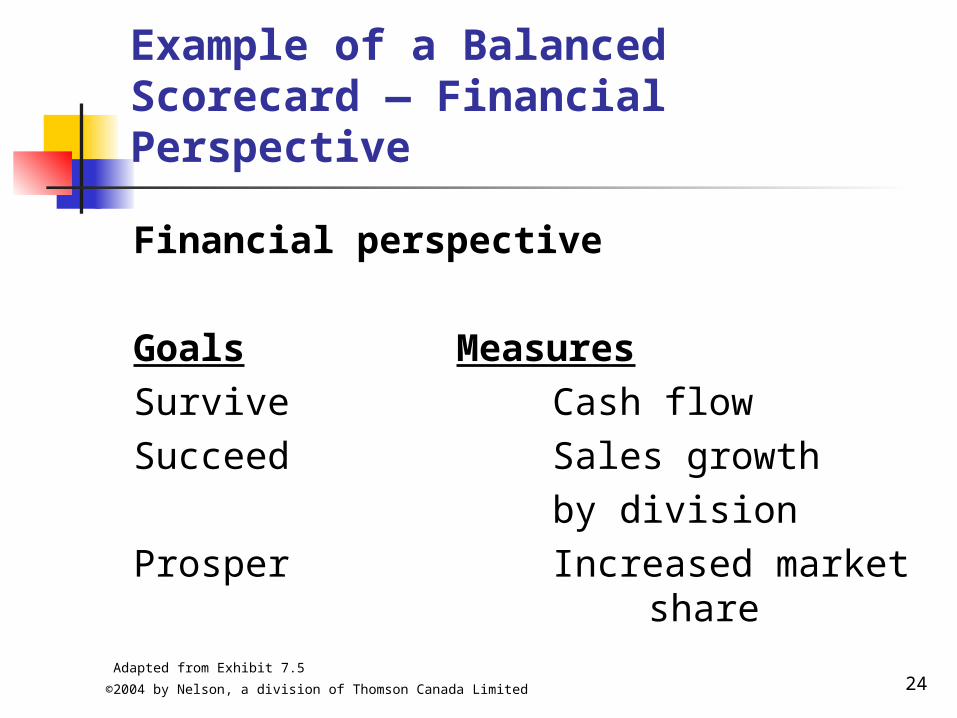

Example of a Balanced Scorecard — Financial Perspective

Financial perspective

Goals MeasuresSurvive Cash flowSucceed Sales growth

by divisionProsper Increased market

shareAdapted from Exhibit 7.5

©2004 by Nelson, a division of Thomson Canada Limited 25

Balanced Scorecard

Managers look beyond traditional financial measures

Managers set specific goals and measure performance in four areas

Helps minimize suboptimization

©2004 by Nelson, a division of Thomson Canada Limited 26

The Financial Perspective: Controlling Economic Value Added

The amount by which company profits exceed the cost of capital in a given year.Important because:

It shows if a business or profit centre is paying for itself

Focuses attention on specific departments

Encourage creative ways to improve organizational performance

©2004 by Nelson, a division of Thomson Canada Limited 27

The Customer Perspective: Controlling Customer Defections

Which customers are leaving and at what rate

Don’t rely completely on customer satisfaction surveys

Cost of replacing old customers with new ones is great

©2004 by Nelson, a division of Thomson Canada Limited 28

The Internal Perspective: Controlling Quality

Managers focus on quality.

Quality is measured as: excellence value conformance to expectations

©2004 by Nelson, a division of Thomson Canada Limited 29

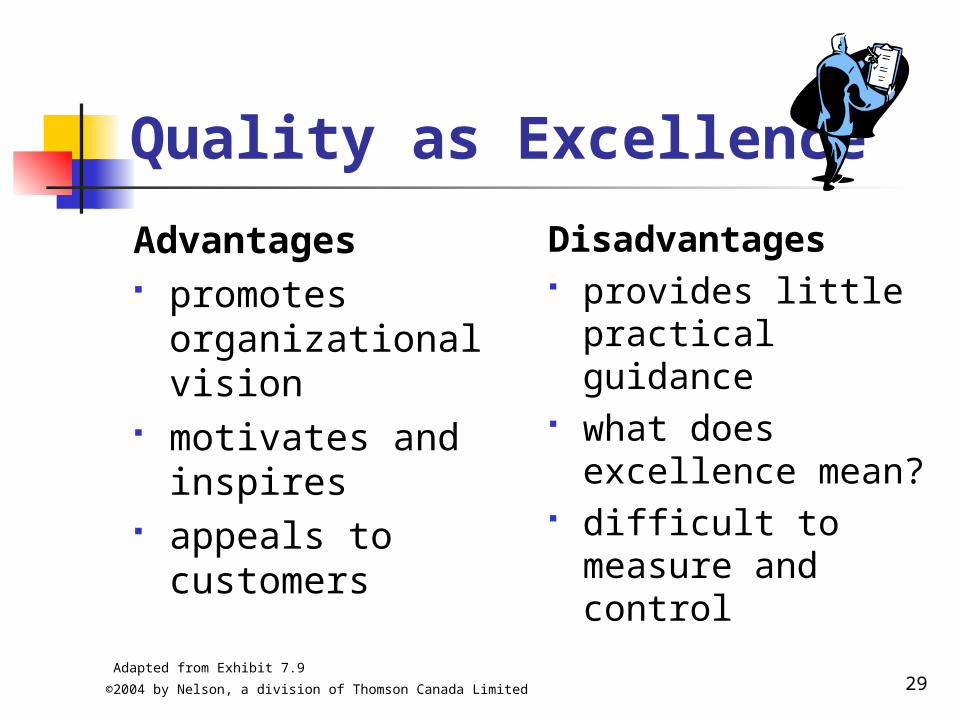

Quality as Excellence

Advantages promotes

organizational vision

motivates and inspires

appeals to customers

Disadvantages provides little

practical guidance what does

excellence mean? difficult to

measure and control

Adapted from Exhibit 7.9

©2004 by Nelson, a division of Thomson Canada Limited 30

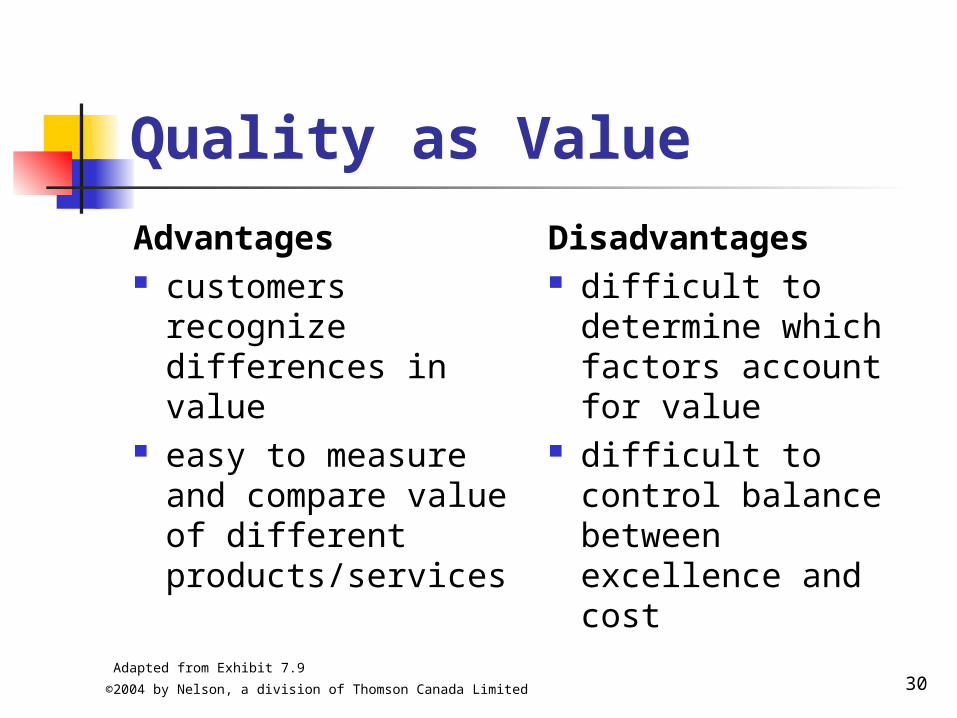

Quality as Value

Advantages customers

recognize differences in value

easy to measure and compare value of different products/services

Disadvantages difficult to

determine which factors account for value

difficult to control balance between excellence and cost

Adapted from Exhibit 7.9

©2004 by Nelson, a division of Thomson Canada Limited 31

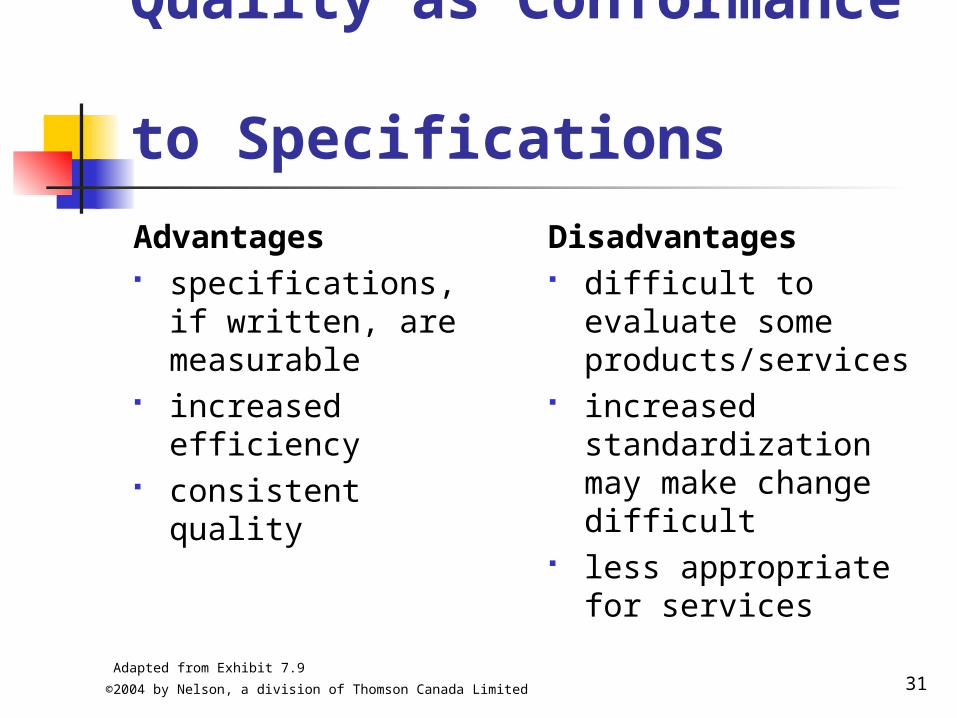

Quality as Conformance

to Specifications

Advantages specifications, if

written, are measurable

increased efficiency consistent quality

Disadvantages difficult to evaluate

some products/services

increased standardization may make change difficult

less appropriate for services

Adapted from Exhibit 7.9

©2004 by Nelson, a division of Thomson Canada Limited 32

The Innovation and Learning Perspective: Controlling Waste and Pollution

Four levels of waste minimization

Waste prevention and reduction Recycle and reuse Waste treatment Waste disposal

©2004 by Nelson, a division of Thomson Canada Limited 33

What Really Happened?

Focused on customer satisfaction Implemented Six Sigma system Quality and on-time delivery

improved dramatically Howmet is an industry model