22

JPMorgan European Smaller Companies Trust plc Half Year Report & Accounts for the six months ended 30th September 2012 Half Year Report 2012/13

JPMorgan European Smaller Companies Trust plcHalf Year Report & Accounts for the six months ended 30th September 2012

Half Year Report2012/13

European Smaller HY cover_European Smaller HY Cover 29/11/2012 17:09 Page 2

Features

Contents

About the Company

1 Half Year Performance 2 Chairman’s Statement 4 Investment Managers’ Report

Investment Review

6 List of Investments 7 Portfolio Analyses

Accounts

11 Income Statement 12 Reconciliation of Movements inShareholders’ Funds

13 Balance Sheet 14 Cash Flow Statement 15 Notes to the Accounts 17 Interim Management Report

Shareholder Information

18 Glossary of Terms and Definitions21 Information about the Company

Objective

Capital growth from smaller European companies (excluding the United Kingdom).

Investment Policies

– To invest in a diversified portfolio of smaller companies in Europe, excluding theUnited Kingdom.

– To manage liquidity and borrowings to increase potential returns to shareholders.The Board’s current policy is to be between 80% and 120% invested.

– To emphasise capital growth rather than income.

– To invest no more than 15% of gross assets in other UK listed investment companies(including investment trusts).

Risk

It should be noted that the Company invests in the shares of smaller companies,which tend to be more volatile than those of larger companies. The Company alsoemploys gearing to generate greater returns. The Company’s shares should thereforebe regarded as carrying greater than average risk.

Benchmark

HSBC Smaller European Companies (ex UK) Total Return Index in sterling terms.

Capital Structure

At 30th September 2012, the Company’s share capital comprised 35,926,923 ordinaryshares of 25p each.

Management Company

The Company employs JPMorgan Asset Management (UK) Limited (‘JPMAM’ or the‘Manager’) to manage its assets.

European Smaller HY cover_European Smaller HY Cover 29/11/2012 17:09 Page 3

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 1

Half Year Performance

–6.3%Share price total return1

–4.4%Net asset value total return2

Financial Data30th September 31st March %

2012 2012 change

Shareholders’ funds (£’000) 289,040 342,299 –15.6

Number of shares in issue 35,926,923 40,083,803 –10.4

Net asset value per share 804.5p 854.0p –5.8

Share price 665.5p 722.0p –7.8

Share price discount to net asset value per share 17.3% 15.5%

A glossary of terms and definitions is provided on page 18.1Source: Morningstar.2Source: J.P. Morgan.3Source: HSBC. The Company’s benchmark is the HSBC Smaller European Companies (ex UK) Total Return Index insterling terms.

–5.0%Benchmark total return3

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 1

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 20122

Chairman’s Statement

Performance

The economic backdrop for European investors has continued to be uncertain overthe first six months of the Company’s financial year. Quantitative easing in Europe andthe US encouraged investor confidence, only for this to fall away with continuedpolitical and economic uncertainty, particularly in the Eurozone. However, further tothe announcement in July that the European Central Bank was prepared to takeaction to support the Euro, equity market confidence has improved.

For the six months ended 30th September 2012, the Company produced a net assetvalue total return of –4.4%. Although a negative return, it outperformed the returnof –5.0% from the benchmark index, the HSBC Smaller European Companies (ex UK)Index. The share price total return was –6.3%, as the discount on the Company’sshares widened from 15.5% to 17.3% over the period.

Longer term performance remains positive, with a net asset value total return of+314.7% against the benchmark total return of +236.1% over the ten years ended30th September 2012.

In their report, the Investment Managers provide details of the key factors drivingperformance during the half year.

Revenue and Dividend

As detailed in my Chairman’s Statement for the year ended 31st March 2012, theBoard’s dividend policy is to pay out the vast majority of revenue available each year.However, shareholders are reminded that the management of the portfolio will notbe constrained to deliver income, given that the Company’s objective is to achievecapital growth. Gross revenue return for the six months to 30th September 2012 wasa little lower than the corresponding period in 2011 at £6.5 million (2011: £7.8 million).The Board has decided to maintain the interim dividend at 6.0 pence per share, whichwill be paid on 16th January 2013 to shareholders on the register as at 21st December2012.

Reverse Auction Tender Offer, Share Buybacks and Discount

During the six months ended 30th September 2012, a total of 4,156,880 shares wererepurchased for cancellation. 3,991,880 of those shares were repurchased as a resultof the reverse auction tender offer undertaken in July 2012, at a discount of 9%. Thetender offer met its principal objective of providing a liquidity event to shareholdersseeking a full or partial exit from the Company at a level determined by shareholders,whilst at the same time enhancing the net asset value for ongoing shareholders, whoalso received a final dividend of 11.0 pence in late August. The Company has notbought back any further shares since the tender offer, but the Board continues tomonitor closely the level of the discount.

Directorate

As detailed in the annual report, we were pleased to welcome Stephen White to theBoard on 1st April 2012. In July 2012, after nine years’ service, Michael Wrobel steppeddown as a Director. Due to new commitments, I will retire from the Board on

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 2

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 3

31st December 2012 and I wish Mrs Carolan Dobson, Chairman designate, everysuccess as she takes on the role from 1st January 2013. The Board has engaged theservices of an independent agency to assist in the appointment of a new Director anda further announcement will follow shortly.

Outlook

In spite of continued macro economic and political uncertainty, the Board believesthat the prospects for European small cap equities are more encouraging than theyhave been for some time and is confident that the Investment Managers’ bottom-upstock picking approach will continue to identify good investment opportunities forthe Company’s portfolio.

Paul ManducaChairman 30th November 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 3

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 20124

Investment Managers’ Report

Review

The confidence generated by the European Central Bank’s (‘ECB’) liquidity injection ofnearly €1 trillion into the banking system between December 2011 and February 2012began to wane at the start of the financial year. This came about as markets focusedincreasingly on the structural difficulties of the Euro project, namely that the ECB wasunwilling to act as lender of last resort in the same way as the Bank of England or theUS Federal Reserve Board.

With markets losing confidence in the Euro, bond yields in the two largest Eurozoneperiphery economies, Italy and Spain, reached unsustainable levels by the end ofJuly 2012. Equity markets fared poorly in this environment and looked set to worsen,when ECB President Draghi gave a now historic speech on 26th July where hefamously said: ‘Within our mandate, the ECB is ready to do whatever it takes topreserve the Euro. And believe me, it will be enough.’

Markets interpreted this to mean that the ECB was indeed prepared to act as lenderof last resort to prevent a break up of the Euro. Bond yields and equity marketsrapidly changed trajectory and by the end of September 2012 the large companyMSCI World Europe (ex UK) Index had virtually eradicated all losses, declining by0.9% in sterling terms. Smaller companies were unable to fare as well, thebenchmark HSBC Smaller European Companies (ex UK) Index falling by 5.0%.

Portfolio

The net asset value of the portfolio declined by 4.4% in the six months ended 30thSeptember 2012, slightly outperforming the benchmark index. This was due topositive asset allocation, namely the overweight position in Denmark andunderweight position in Sweden. The portfolio benefited from holdings in companieswhich had either a high level of recurring revenues or good visibility.

Top stock contributors over the six months included Danish hearing aid manufacturerGN Store Nord, French IT outsourcing company Atos Origin, Norwegian seismicsurvey provider TGS Nopec Geophysical, French food and pharma testing servicesprovider Eurofins and German industrial lubricants group Fuchs Petrolub. Negativestock contributors tended to be stock specific, including Dutch oil service companySBM (following write downs of some of its projects), Italian life insurance and assetmanager Mediolanum (on higher Italian bond yields), and Italian cementmanufacturer Buzzi Unicem and Italian scooter manufacturer Piaggio (on slowingeconomic growth).

Gearing at the end of the period was approximately 3.5%, although with improvingconfidence, we have raised the level at the time of writing to some 6%.

Given that global economic growth is likely to be limited in the near term, we arefocusing our stock picking efforts on companies that should be able to thrive despiteanaemic economies. Examples include French oil storage and energy distributionsupplier Rubis, Italian diagnostics company Diasorin, Swiss insurance companyHelvetia, Danish food ingredients manufacturer Christian Hansen and Irish gamblingcompany Paddy Power.

Francesco Conte

Jim Campbell

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 4

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 5

Outlook

We are more confident in markets than we have been for some time. The risk of aEurozone implosion has decreased significantly following President Draghi’s wordsand the setting up of a €700 billion European Stability Mechanism to help countriesin financial difficulties.

The economic plight of countries in the peripheral Eurozone, whilst harsh at thehuman level, is having the desired effects of improving primary and current accountdeficits, while at the same time forcing painful structural reforms which shouldultimately make these countries far more competitive.

The next step for the Euro integration project is the establishment of banking union.As with all grand Eurozone projects that require the giving up of sovereignty, it willnot be agreed overnight, but the resolve to move towards a closer union has nowbeen tested in many countries, both core and periphery, and each time it has notbeen found wanting.

Recent elections in Holland, one of the strongest core Eurozone countries, andGreece, the weakest of the periphery countries, resulted in pro-European coalitions,despite fears of anti-Eurozone electoral revolts. The German Constitutional Courtaccepted the legality of the establishment of the European Stability Mechanism, andgovernments in Italy, Spain, Portugal and Greece are pushing ahead with budgetaryausterity and reform despite electoral unpopularity.

On the macroeconomic front, the Eurozone may be slowing down, but it is by nomeans collapsing like it did in 2008/09. Macroeconomic data, while soft, is generallybetter than expected and the rate at which it is worsening is abating. In the US, thehousing market and the financial system are recovering quickly. Questions remainover the so-called US ‘fiscal cliff’, whereby expiration of certain tax cuts could lead toa sharp economic contraction, however it would seem to be in all parties’ interests tofind a solution, as they did with the earlier problem of the debt ceiling. Indicationsfrom the emerging markets of China, India and Brazil are that the worst of theslowdown is behind them.

On the microeconomic front, second and third quarter results, while generally weakin absolute terms, were largely in line with or better than analysts’ expectations.Those results confirmed that, in many cases, companies have solid balance sheetsand are able to pay attractive dividends.

The path ahead will not be smooth, because the world faces many challenges,however, central banks in the US and Europe have shown repeatedly that they arestrongly committed to the reflation of the global economy. So much cheap liquiditycombined with attractive valuations makes us confident that, despite expectedvolatility, the underlying trend for equity markets should remain positive over thecoming months.

Jim CampbellFrancesco ConteInvestment Managers 30th November 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 5

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 20126

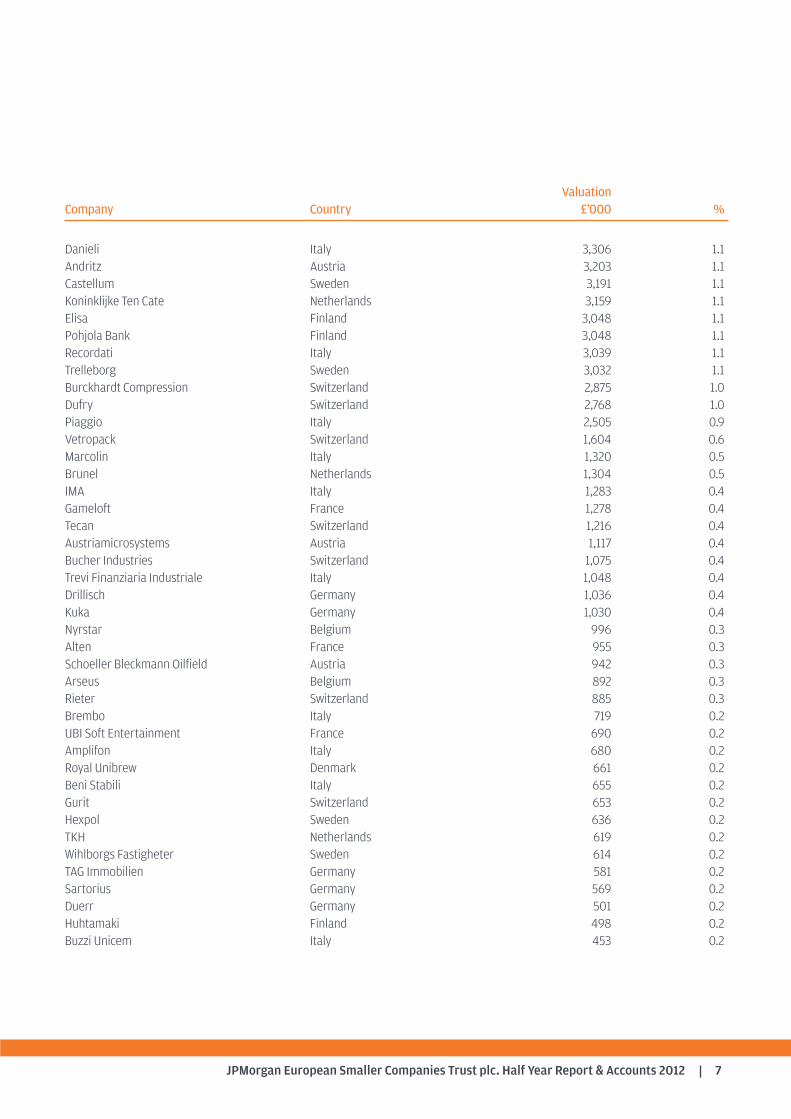

ValuationCompany Country £’000 %

TGS Nopec Geophysical Norway 9,140 3.2GN Store Nord Denmark 9,065 3.1Eurofins France 8,781 3.0DiaSorin Italy 7,836 2.7Finmeccanica Italy 7,700 2.7Nutreco Netherlands 7,600 2.6Atos Origin France 7,547 2.6Rubis France 7,538 2.6Kabel Deutschland Germany 7,501 2.6Wirecard Germany 7,487 2.6Flughafen Zurich Switzerland 7,244 2.5Freenet Germany 6,718 2.3Fuchs Petrolub Germany 6,712 2.3D’Ieteren Belgium 6,588 2.3GAM Switzerland 6,574 2.3Lottomatica Italy 6,226 2.2Symrise Germany 6,120 2.1Aker Solutions Norway 6,110 2.1Helvetia Switzerland 6,082 2.1Tecnicas Reunidas Spain 6,062 2.1Paddy Power Ireland 6,013 2.1Fred Olsen Energy Norway 6,006 2.1Gjensidige Forsikring Norway 5,992 2.1Chr.Hansen Denmark 5,890 2.0Unit 4 Agresso Netherlands 5,564 1.9MTU Aero Engines Germany 5,417 1.9Topdanmark Denmark 4,624 1.6Ipsos France 4,373 1.5Altran Technologies France 4,257 1.5Davide Campari Italy 4,212 1.5Gerry Weber International Germany 4,019 1.4Aalberts Industries Netherlands 3,994 1.4Viscofan Spain 3,950 1.4Elekta Sweden 3,937 1.4Sorin Italy 3,883 1.3Arcadis Netherlands 3,857 1.3Ackermans & van Haaren Belgium 3,622 1.3Azimut Italy 3,605 1.2Gerresheimer Germany 3,521 1.2Deutsche Wohnen Germany 3,479 1.2Kaba Switzerland 3,328 1.2

List of Investmentsat 30th September 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 6

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 7

ValuationCompany Country £’000 %

Danieli Italy 3,306 1.1Andritz Austria 3,203 1.1Castellum Sweden 3,191 1.1Koninklijke Ten Cate Netherlands 3,159 1.1Elisa Finland 3,048 1.1Pohjola Bank Finland 3,048 1.1Recordati Italy 3,039 1.1Trelleborg Sweden 3,032 1.1Burckhardt Compression Switzerland 2,875 1.0Dufry Switzerland 2,768 1.0Piaggio Italy 2,505 0.9Vetropack Switzerland 1,604 0.6Marcolin Italy 1,320 0.5Brunel Netherlands 1,304 0.5IMA Italy 1,283 0.4Gameloft France 1,278 0.4Tecan Switzerland 1,216 0.4Austriamicrosystems Austria 1,117 0.4Bucher Industries Switzerland 1,075 0.4Trevi Finanziaria Industriale Italy 1,048 0.4Drillisch Germany 1,036 0.4Kuka Germany 1,030 0.4Nyrstar Belgium 996 0.3Alten France 955 0.3Schoeller Bleckmann Oilfield Austria 942 0.3Arseus Belgium 892 0.3Rieter Switzerland 885 0.3Brembo Italy 719 0.2UBI Soft Entertainment France 690 0.2Amplifon Italy 680 0.2Royal Unibrew Denmark 661 0.2Beni Stabili Italy 655 0.2Gurit Switzerland 653 0.2Hexpol Sweden 636 0.2TKH Netherlands 619 0.2Wihlborgs Fastigheter Sweden 614 0.2TAG Immobilien Germany 581 0.2Sartorius Germany 569 0.2Duerr Germany 501 0.2Huhtamaki Finland 498 0.2Buzzi Unicem Italy 453 0.2

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 7

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 20128

ValuationCompany Country £’000 %

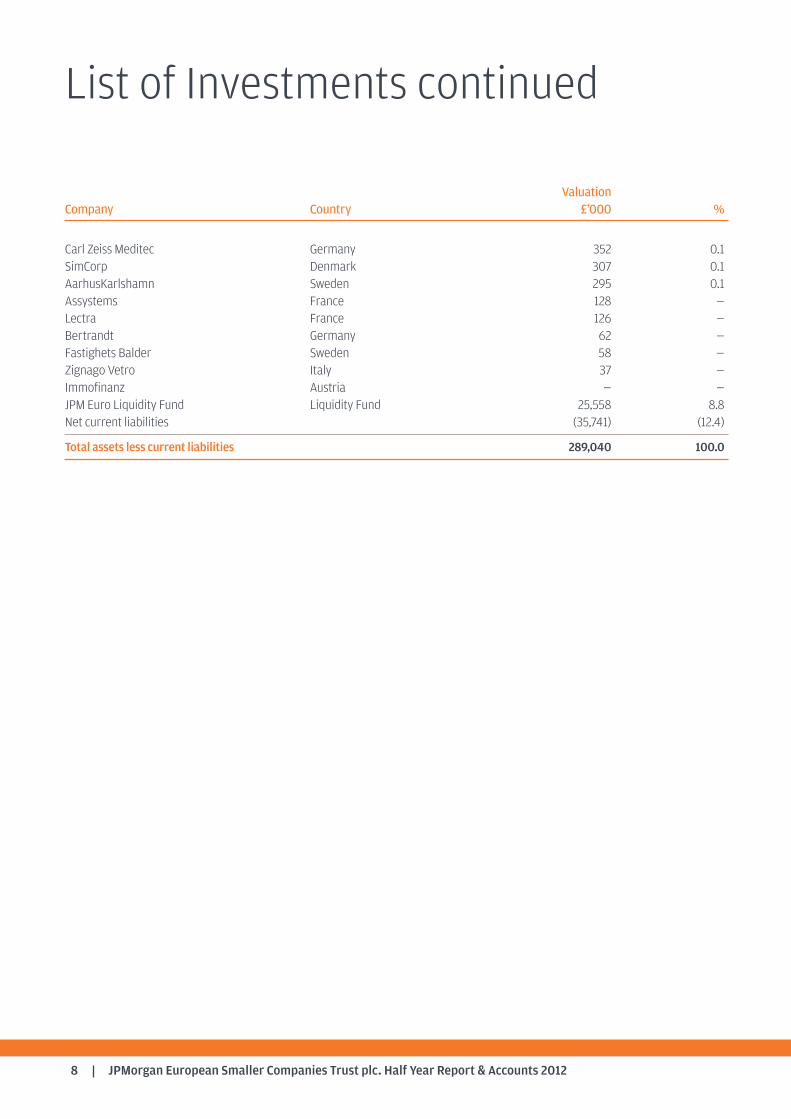

Carl Zeiss Meditec Germany 352 0.1SimCorp Denmark 307 0.1AarhusKarlshamn Sweden 295 0.1Assystems France 128 —Lectra France 126 —Bertrandt Germany 62 —Fastighets Balder Sweden 58 —Zignago Vetro Italy 37 —Immofinanz Austria — —JPM Euro Liquidity Fund Liquidity Fund 25,558 8.8Net current liabilities (35,741) (12.4)

Total assets less current liabilities 289,040 100.0

List of Investments continued

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 8

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 9

at 30th September 2012 at 31st March 2012Portfolio Benchmark Portfolio Benchmark

Geographical % % % %

Germany 19.1 14.4 13.6 14.2 Italy 16.8 10.9 14.4 10.1 France 12.1 11.9 20.3 13.0 Switzerland 12.0 11.5 12.8 11.5 Norway 9.5 6.5 6.1 6.5Netherlands 9.0 5.1 10.9 4.9Denmark 7.0 3.5 7.7 3.8 Belgium 4.2 4.5 2.3 4.6 Sweden 4.1 10.0 6.7 9.8Spain 3.5 6.3 5.3 6.3Finland 2.4 5.7 2.9 6.1 Ireland 2.1 2.0 1.8 2.1 Austria 1.8 3.1 0.2 3.0 Greece — 2.8 — 2.4 Portugal — 1.8 — 1.7

Total equities 103.6 100.0 105.0 100.0 Liquidity fund 8.8 — 4.4 —Net current liabilities (12.4) — (9.4) —

Total 100.0 100.0 100.0 100.0

Based on total assets less current liabilities of £289.0m (31st March 2012: £342.3m).

Portfolio Analyses

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 9

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 201210

at 30th September 2012 at 31st March 2012Portfolio Benchmark Portfolio Benchmark

Sector % % % %

Industrials 18.0 22.8 27.6 24.0Consumer Discretionary 15.6 14.4 11.0 16.2Health Care 15.1 9.1 5.9 8.2Financials 14.6 22.5 16.1 20.5Information Technology 10.4 7.7 7.8 8.0Energy 9.8 5.8 15.2 5.6Materials 8.0 7.8 13.5 8.3Consumer Staples 5.8 6.2 4.9 5.9Telecommunication Services 3.7 1.2 3.0 1.3Utilities 2.6 2.5 — 2.0

Total equities 103.6 100.0 105.0 100.0 Liquidity fund 8.8 — 4.4 —Net current liabilities (12.4) — (9.4) —

Total 100.0 100.0 100.0 100.0

Based on total assets less current liabilities of £289.0m (31st March 2012: £342.3m).

Portfolio Analyses continued

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 10

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 11

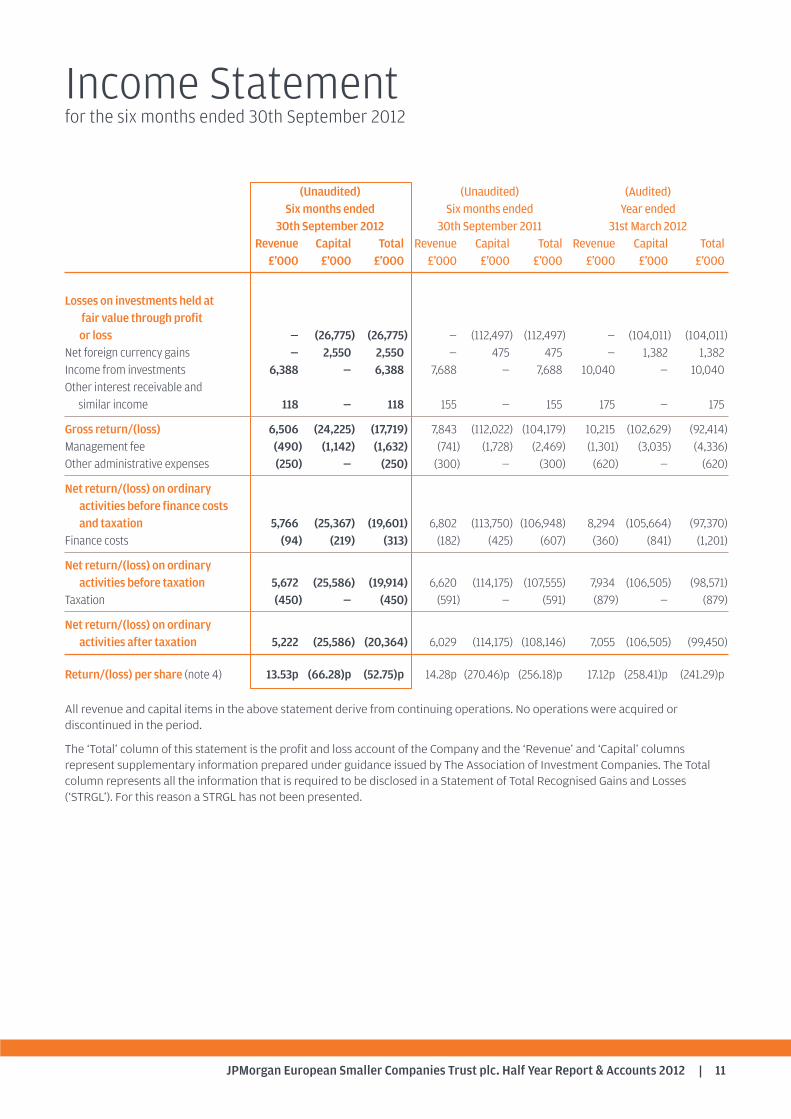

(Unaudited) (Unaudited) (Audited)Six months ended Six months ended Year ended

30th September 2012 30th September 2011 31st March 2012Revenue Capital Total Revenue Capital Total Revenue Capital Total£’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000

Losses on investments held atfair value through profit or loss — (26,775) (26,775) — (112,497) (112,497) — (104,011) (104,011)

Net foreign currency gains — 2,550 2,550 — 475 475 — 1,382 1,382Income from investments 6,388 — 6,388 7,688 — 7,688 10,040 — 10,040Other interest receivable and similar income 118 — 118 155 — 155 175 — 175

Gross return/(loss) 6,506 (24,225) (17,719) 7,843 (112,022) (104,179) 10,215 (102,629) (92,414)Management fee (490) (1,142) (1,632) (741) (1,728) (2,469) (1,301) (3,035) (4,336)Other administrative expenses (250) — (250) (300) — (300) (620) — (620)

Net return/(loss) on ordinaryactivities before finance costsand taxation 5,766 (25,367) (19,601) 6,802 (113,750) (106,948) 8,294 (105,664) (97,370)

Finance costs (94) (219) (313) (182) (425) (607) (360) (841) (1,201)

Net return/(loss) on ordinaryactivities before taxation 5,672 (25,586) (19,914) 6,620 (114,175) (107,555) 7,934 (106,505) (98,571)

Taxation (450) — (450) (591) — (591) (879) — (879)

Net return/(loss) on ordinaryactivities after taxation 5,222 (25,586) (20,364) 6,029 (114,175) (108,146) 7,055 (106,505) (99,450)

Return/(loss) per share (note 4) 13.53p (66.28)p (52.75)p 14.28p (270.46)p (256.18)p 17.12p (258.41)p (241.29)p

All revenue and capital items in the above statement derive from continuing operations. No operations were acquired ordiscontinued in the period.

The ‘Total’ column of this statement is the profit and loss account of the Company and the ‘Revenue’ and ‘Capital’ columnsrepresent supplementary information prepared under guidance issued by The Association of Investment Companies. The Totalcolumn represents all the information that is required to be disclosed in a Statement of Total Recognised Gains and Losses(‘STRGL’). For this reason a STRGL has not been presented.

Income Statementfor the six months ended 30th September 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 11

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 201212

Called up CapitalSix months ended share Share redemption Capital Revenue30th September 2012 capital premium reserve reserves reserve Total(Unaudited) £’000 £’000 £’000 £’000 £’000 £’000

At 31st March 2012 10,021 1,312 5,615 319,700 5,651 342,299Repurchase and cancellation of the Company’sown shares (1,039) — 1,039 (28,943) — (28,943)

Net (loss)/return on ordinary activities — — — (25,586) 5,222 (20,364)Dividends appropriated in the period — — — — (3,952) (3,952)

At 30th September 2012 8,982 1,312 6,654 265,171 6,921 289,040

Called up CapitalSix months ended share Share redemption Capital Revenue30th September 2011 capital premium reserve reserves reserve Total(Unaudited) £’000 £’000 £’000 £’000 £’000 £’000

At 31st March 2011 10,877 1,312 4,759 457,728 2,752 477,428Repurchase and cancellation of the Company’sown shares (636) — 636 (25,612) — (25,612)

Net (loss)/return on ordinary activities — — — (114,175) 6,029 (108,146)Dividends appropriated in the period — — — — (1,725) (1,725)

At 30th September 2011 10,241 1,312 5,395 317,941 7,056 341,945

Called up CapitalYear ended share Share redemption Capital Revenue31st March 2012 capital premium reserve reserves reserve Total(Audited) £’000 £’000 £’000 £’000 £’000 £’000

At 31st March 2011 10,877 1,312 4,759 457,728 2,752 477,428Repurchase and cancellation of the Company’sown shares (856) — 856 (31,523) — (31,523)

Net (loss)/return on ordinary activities — — — (106,505) 7,055 (99,450)Dividends appropriated in the year — — — — (4,156) (4,156)

At 31st March 2012 10,021 1,312 5,615 319,700 5,651 342,299

Reconciliation of Movements inShareholders’ Funds

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 12

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 13

(Unaudited) (Unaudited) (Audited)30th September 2012 30th September 2011 31st March 2012

£’000 £’000 £’000

Fixed assetsInvestments held at fair value through profit or loss 299,223 374,079 359,138Investments in liquidity funds held at fair value through profit or loss 25,558 — 15,003

Total investments 324,781 374,079 374,141

Current assetsDebtors 5,559 10,937 15,077Cash and short term deposits 7,152 15 568Derivative financial instruments: forward currency contracts held at fair value through profit or loss 2 1 —

12,713 10,953 15,645Creditors: amounts falling due within one year (48,454) (43,087) (47,487)

Net current liabilities (35,741) (32,134) (31,842)

Total assets less current liabilities 289,040 341,945 342,299

Net assets 289,040 341,945 342,299

Capital and reservesCalled up share capital 8,982 10,241 10,021Share premium 1,312 1,312 1,312Capital redemption reserve 6,654 5,395 5,615Capital reserves 265,171 317,941 319,700Revenue reserve 6,921 7,056 5,651

Equity shareholders’ funds 289,040 341,945 342,299

Net asset value per share (note5) 804.5p 834.8p 854.0p

Company registration number: 2431143

Balance Sheetat 30th September 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 13

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 201214

(Unaudited) (Unaudited) (Audited)Six months ended Six months ended Year ended

30th September 2012 30th September 2011 31st March 2012£’000 £’000 £’000

Net cash inflow from operating activities (note6) 4,123 4,772 3,807Net cash outflow from returns on investments and servicing of finance (339) (847) (1,411)

Tax recovered 84 73 203Net cash inflow from capital expenditure and financial investment 35,264 56,809 61,385

Dividend paid (3,952) (1,725) (4,156)Net cash outflow from financing (29,305) (60,232) (57,858)

Increase/(decrease) in cash in the period 5,875 (1,150) 1,970

Reconciliation of net cash flow to movement in net debt

Net cash movement 5,875 (1,150) 1,970Net loans drawn down in the period — 34,620 26,696Exchange movements 2,549 478 1,386

Movement in net funds in the period 8,424 33,948 30,052Net debt at the beginning of the period (41,106) (71,158) (71,158)

Net debt at the end of the period (32,682) (37,210) (41,106)

Represented by:Cash and short term deposits and bank overdrafts 7,152 15 568Debt falling due within one year (39,834) (37,225) (41,674)

Net debt at the end of the period (32,682) (37,210) (41,106)

Cash Flow Statementfor the six months ended 30th September 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 14

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 15

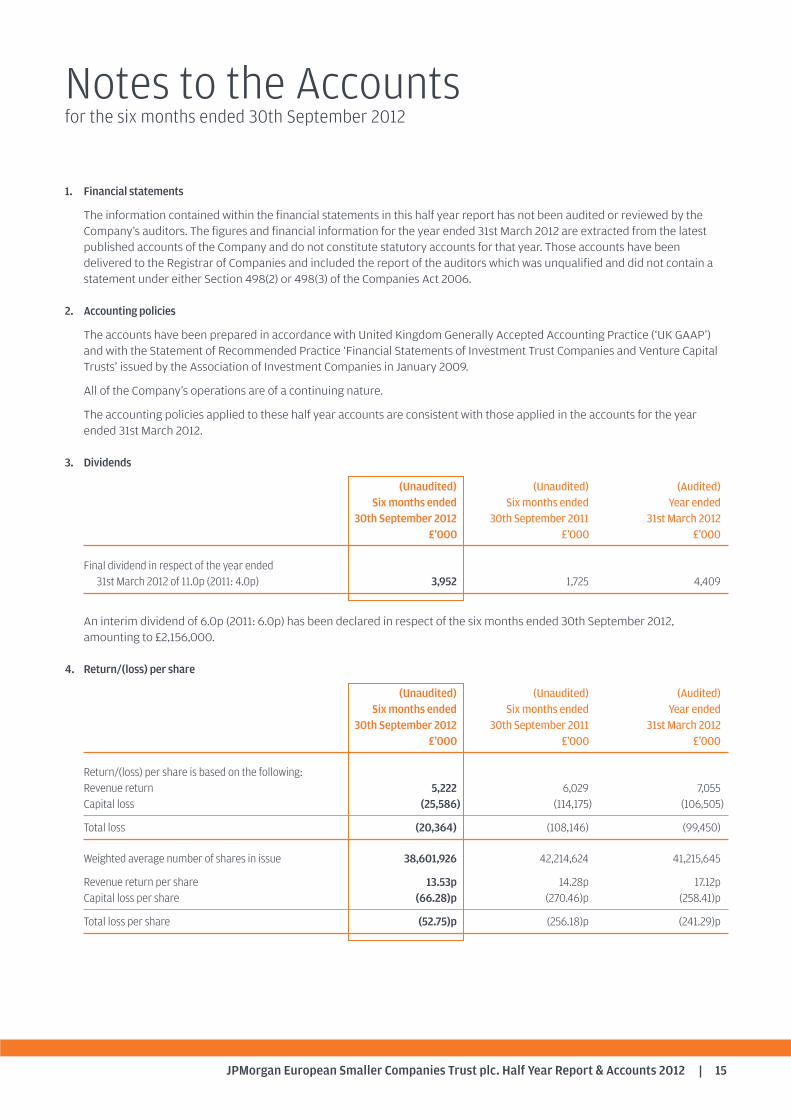

1. Financial statements

The information contained within the financial statements in this half year report has not been audited or reviewed by theCompany’s auditors. The figures and financial information for the year ended 31st March 2012 are extracted from the latestpublished accounts of the Company and do not constitute statutory accounts for that year. Those accounts have beendelivered to the Registrar of Companies and included the report of the auditors which was unqualified and did not contain astatement under either Section 498(2) or 498(3) of the Companies Act 2006.

2. Accounting policies

The accounts have been prepared in accordance with United Kingdom Generally Accepted Accounting Practice (‘UK GAAP’)and with the Statement of Recommended Practice ‘Financial Statements of Investment Trust Companies and Venture CapitalTrusts’ issued by the Association of Investment Companies in January 2009.

All of the Company’s operations are of a continuing nature.

The accounting policies applied to these half year accounts are consistent with those applied in the accounts for the yearended 31st March 2012.

3. Dividends

(Unaudited) (Unaudited) (Audited)Six months ended Six months ended Year ended

30th September 2012 30th September 2011 31st March 2012£’000 £’000 £’000

Final dividend in respect of the year ended 31st March 2012 of 11.0p (2011: 4.0p) 3,952 1,725 4,409

An interim dividend of 6.0p (2011: 6.0p) has been declared in respect of the six months ended 30th September 2012,amounting to £2,156,000.

4. Return/(loss) per share

(Unaudited) (Unaudited) (Audited)Six months ended Six months ended Year ended

30th September 2012 30th September 2011 31st March 2012£’000 £’000 £’000

Return/(loss) per share is based on the following:Revenue return 5,222 6,029 7,055Capital loss (25,586) (114,175) (106,505)

Total loss (20,364) (108,146) (99,450)

Weighted average number of shares in issue 38,601,926 42,214,624 41,215,645

Revenue return per share 13.53p 14.28p 17.12pCapital loss per share (66.28)p (270.46)p (258.41)p

Total loss per share (52.75)p (256.18)p (241.29)p

Notes to the Accountsfor the six months ended 30th September 2012

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 15

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 201216

5. Net asset value per share

The net asset value per share is calculated by dividing shareholders’ funds by the number of shares in issue at 30th September2012 of 35,926,923 (30th September 2011: 40,962,803 and 31st March 2012: 40,083,803).

6. Reconciliation of total loss on ordinary activities before finance costs and taxation to net cash inflow from operating activities

(Unaudited) (Unaudited) (Audited)Six months ended Six months ended Year ended

30th September 2012 30th September 2011 31st March 2012£’000 £’000 £’000

Total loss on ordinary activities before finance costs and taxation (19,601) (106,948) (97,370)

Less capital loss before finance costs and taxation 25,367 113,750 105,664Scrip dividends received as income (442) (786) (1,077)Decrease in accrued income 631 1,336 853(Increase)/decrease in other debtors (3) 40 18(Decrease)/increase in accrued expenses (36) (10) 1Overseas withholding tax (651) (882) (1,247)Management fee charged to capital (1,142) (1,728) (3,035)

Net cash inflow from operating activities 4,123 4,772 3,807

Notes to the Accounts continued

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 16

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 17

The Company is required to make the following disclosures inits half year report:

Principal risks anduncertainties

The principal risks and uncertainties faced by the Companyfall into the following broad categories: investment andstrategy; market; accounting, legal and regulatory; corporategovernance and shareholder relations; operational andfinancial. Information on each of these areas is given in theBusiness Review within the Annual Report and Accounts forthe year ended 31st March 2012.

Related parties’ transactions

During the first six months of the current financial year, notransactions with related parties have taken place which havematerially affected the financial position or the performance ofthe Company.

Going Concern

The Directors believe, having considered the Company’sinvestment objectives, risk management policies, capitalmanagement policies and procedures, nature of the portfolioand expenditure projections, that the Company has adequateresources, an appropriate financial structure and suitablemanagement arrangements in place to continue in operationalexistence for the foreseeable future. For these reasons, theyconsider there is reasonable evidence to continue to adopt thegoing concern basis in preparing the accounts.

Directors’ responsibilities

The Board of Directors confirms that, to the best of itsknowledge:

(i) the condensed set of financial statements containedwithin the half yearly financial report has beenprepared in accordance with the Accounting StandardsBoard’s Statement ‘Half-Yearly Financial Reports’ andgives a true and fair view of the assets, liabilities,financial position and net return of the Company asrequired by the UK Listing Authority Disclosure andTransparency Rules 4.2.4R; and

(ii) the interim management report includes a fair review ofthe information required by 4.2.7R and 4.2.8R of the UKListing Authority Disclosure and Transparency Rules.

For and on behalf of the BoardPaul ManducaChairman 30th November 2012

Interim Management Report

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 17

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 201218

Glossary of Terms and Definitions

Share price total return

Share price total return on a mid-market price to mid-marketprice basis, assuming that all dividends received werereinvested, without transaction costs, into the shares of theCompany at the time the shares were quoted ex-dividend.

Net asset value total return

Total return on net asset value (‘NAV’) per share, on a bid valueto bid value basis, assuming that all dividends paid out by theCompany were reinvested, without transaction costs, into theshares of the Company at the NAV per share at the time theshares were quoted ex-dividend.

In accordance with industry practice, dividends payable whichhave been declared but which are unpaid at the balance sheetdate are deducted from the NAV when calculating the net assetvalue total return.

Benchmark total return

Total return on the benchmark, on a mid-market value tomid-market value basis, assuming that all dividends receivedwere reinvested, without transaction costs, into the shares ofthe underlying companies at the time the shares were quotedex-dividend.

The benchmark is a recognised index of stocks which shouldnot be taken as wholly representative of the Company’sinvestment universe. The Company’s investment strategy doesnot follow or ‘track’ this index and consequently, there may besome divergence between the Company’s performance andthat of the benchmark.

Share price discount/premium to net asset value (‘NAV’) per share

If the share price of an investment trust is lower than theNAV per share, the shares are said to be trading at a discount.The discount is shown as a percentage of the NAV per share.The opposite of a discount is a premium. It is more commonfor an investment trust’s shares to trade at a discount than ata premium.

European Smaller_pp01_20_European Smaller_pp01_20 29/11/2012 16:30 Page 18

HistoryOn 24th April 1990, the Company acquired the undertakingand assets of Fleming European Fledgeling Fund Limited(the ‘Fund’) in exchange for the issue of its shares andwarrants. The Fund was an open-ended, unquoted investmentcompany based in Jersey and formed in June 1987 with thesame objectives and investment policies as the Company.

The Company adopted its present name in July 2010.

DirectorsPaul Manduca (Chairman) Anthony Davidson Federico Marescotti Carolan DobsonStephen White

Company NumbersCompany registration number: 2431143 London Stock Exchange number: 0341969 ISIN: GB0003419693 Bloomberg code: JESC LN

Market InformationThe Company’s net asset value (‘NAV’) is published daily, via theLondon Stock Exchange. The Company’s shares are listed onthe London Stock Exchange. The market price is shown daily inthe Financial Times, The Times, The Daily Telegraph, TheScotsman, The Independent, the Herald and on the JPMorganInternet site at www.jpmeuropeansmallercompanies.co.uk,where the share price is updated every fifteen minutes duringtrading hours.

Share TransactionsThe Company’s shares may be dealt in directly through astockbroker or professional adviser acting on an investor’sbehalf. They may also be purchased and held through theJ.P. Morgan Investment Account, J.P. Morgan ISA and J.P. MorganSIPP. These products are all available on the online wealthmanager service, J.P. Morgan WealthManager+ available atwww.jpmorganwealthmanagerplus.co.uk

Manager and Company SecretaryJPMorgan Asset Management (UK) Limited

Company’s Registered OfficeFinsbury Dials20 Finsbury StreetLondon EC2Y 9AQTelephone: 020 7742 4000

For company secretarial issues and administrative matters,please contact Jonathan Latter.

CustodianJPMorgan Chase Bank, N.A.25 Bank StreetCanary WharfLondon E14 5JP

RegistrarsEquiniti LimitedReference 1083Aspect HouseSpencer RoadLancingWest Sussex BN99 6DATelephone number: 0871 384 2325

Calls to this number cost 8p per minute from a BT landline.Other providers’ costs may vary. Lines open 8.30am to5.30pm Monday to Friday. The overseas helpline numberis +44 (0)121 415 7047.

Notifications of changes of address and enquiries regardingshare certificates or dividend cheques should be made inwriting to the Registrar quoting reference 1083.

Registered shareholders can obtain further details onindividual holdings on the internet by visitingwww.shareview.co.uk

Independent AuditorsPricewaterhouseCoopers LLP Chartered Accountants and Statutory Auditors7 More London RiversideLondon SE1 2RT

BrokersCenkos Securities plc 6.7.8 Tokenhouse Yard London EC2R 7AS

Savings Product AdministratorsFor queries on the J.P. Morgan Investment Account, J.P. MorganISA and J.P. Morgan SIPP, see contact details on the back coverof this report.

Information about the Company

Financial CalendarFinancial year end 31st March Final results announced May/June Half year end 30th September Half year results announced November Interim Management Statements announced January/July Annual General Meeting 16th July 2013Dividend July

A member of the AIC

JPMorgan European Smaller Companies Trust plc. Half Year Report & Accounts 2012 21

European Smaller HY cover_European Smaller HY Cover 29/11/2012 17:09 Page 21

J.P. Morgan HelplineFreephone 0800 20 40 20 or +44 (0)20 7742 9995

Your telephone call may be recorded for your security

www.jpmeuropeansmallercompanies.co.uk

European Smaller HY cover_European Smaller HY Cover 29/11/2012 17:09 Page 1

![Annual Report2012 [1370KB] - Dainippon Ink and Chemicals, Inc](https://static.documents.pub/doc/80x56/62038deeda24ad121e4ac47c/annual-report2012-1370kb-dainippon-ink-and-chemicals-inc.jpg)