34

©TNS 2012 2013 Economic Review, Trends & 2014 Forecast Ralf Matthaes Regional Managing Director Cambodia | Laos | Myanmar | Vietnam

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

2013 Economic Review, Trends & 2014 Forecast

Ralf Matthaes Regional Managing Director Cambodia | Laos | Myanmar | Vietnam

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

Contents

2

1 Economic overview 2012 - 2103

2 Recession impact

3 Retail impact

4 Marketing trends

5 2014 forecast

2012- Q.3 2013- Vietnam Macro Economic Overview

THE GOOD, THE BAD, THE UGLY

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

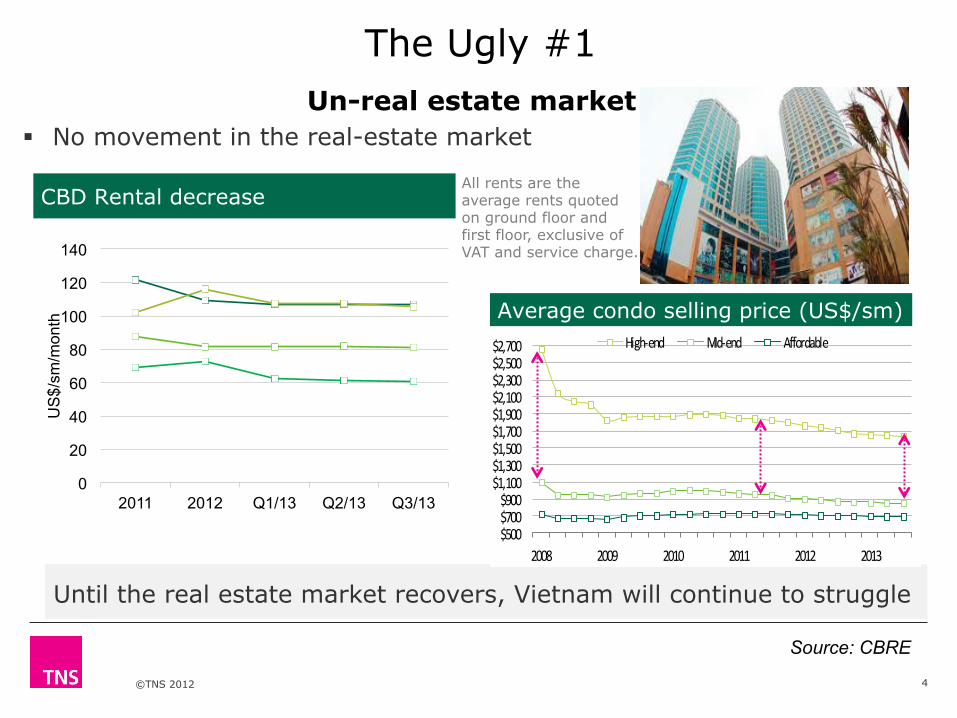

Un-real estate market § No movement in the real-estate market

Until the real estate market recovers, Vietnam will continue to struggle

4

The Ugly #1

0

20

40

60

80

100

120

140

2011 2012 Q1/13 Q2/13 Q3/13

US

$/sm

/mon

th

CBD Rental decrease

Average condo selling price (US$/sm)

$500$700$900

$1,100$1,300$1,500$1,700$1,900$2,100$2,300$2,500$2,700

2008 2009 2010 2011 2012 2013

High-‐end Mid-‐end Affordable

Source: CBRE

All rents are the average rents quoted on ground floor and first floor, exclusive of VAT and service charge.

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

5

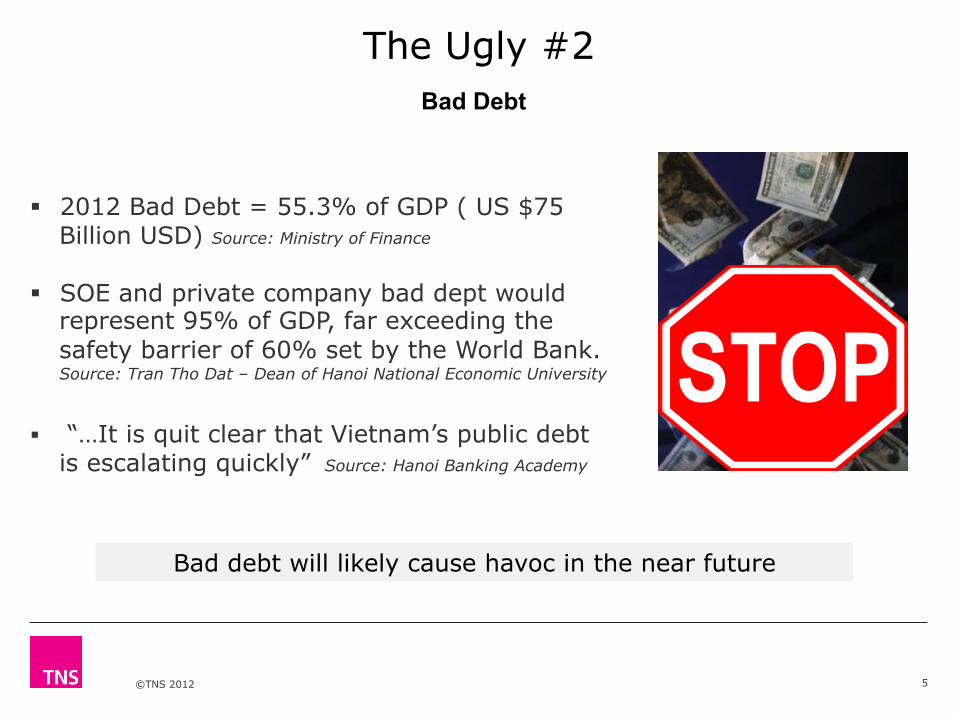

The Ugly #2

§ 2012 Bad Debt = 55.3% of GDP ( US $75

Billion USD) Source: Ministry of Finance

§ SOE and private company bad dept would represent 95% of GDP, far exceeding the safety barrier of 60% set by the World Bank. Source: Tran Tho Dat – Dean of Hanoi National Economic University

§ “…It is quit clear that Vietnam’s public debt

is escalating quickly” Source: Hanoi Banking Academy

Bad debt will likely cause havoc in the near future

Bad Debt

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

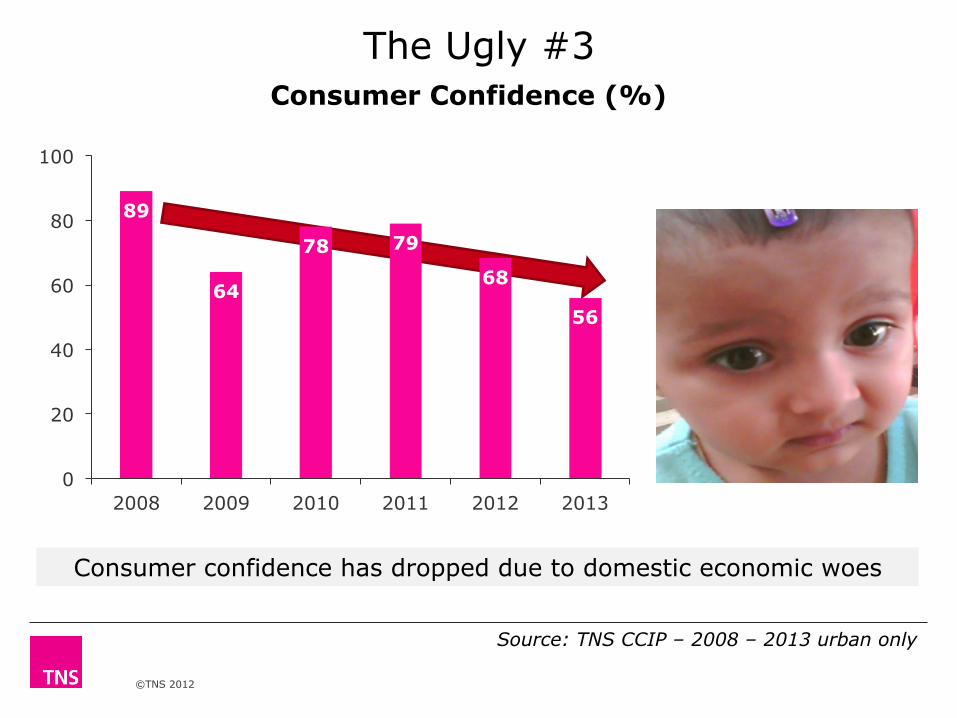

The Ugly #3

Source: TNS CCIP – 2008 – 2013 urban only

Consumer confidence has dropped due to domestic economic woes

Consumer Confidence (%)

89

64

78 79

68

56

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

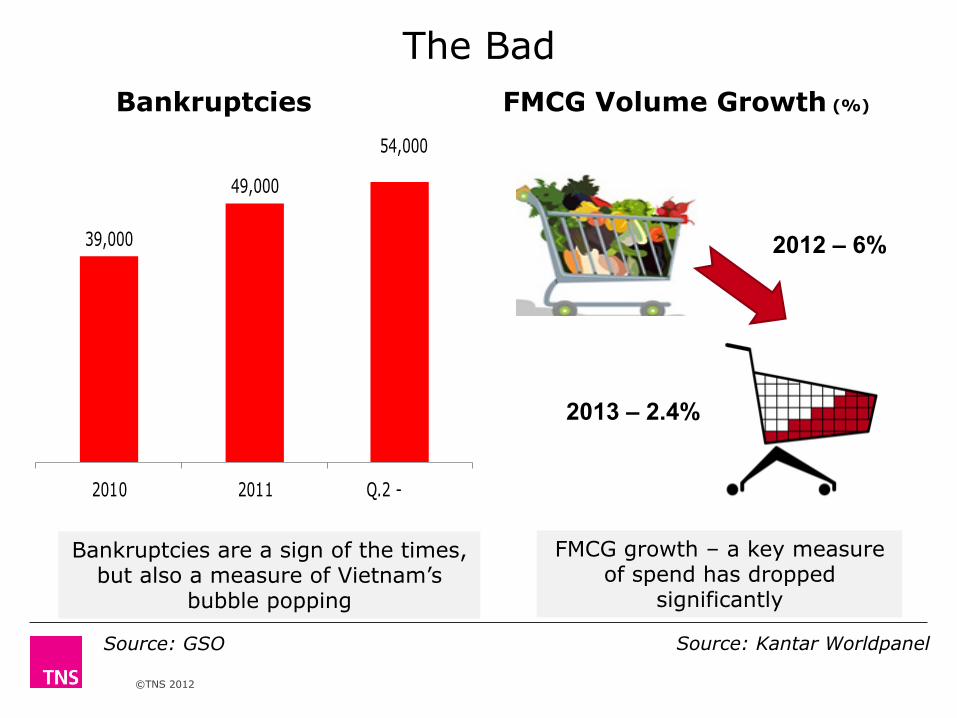

The Bad

Source: GSO

Bankruptcies are a sign of the times, but also a measure of Vietnam’s

bubble popping

Bankruptcies FMCG Volume Growth (%)

39,000

49,000

54,000

2010 2011 Q.2 - 2012

2012 – 6%

2013 – 2.4%

FMCG growth – a key measure of spend has dropped

significantly

Source: Kantar Worldpanel

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

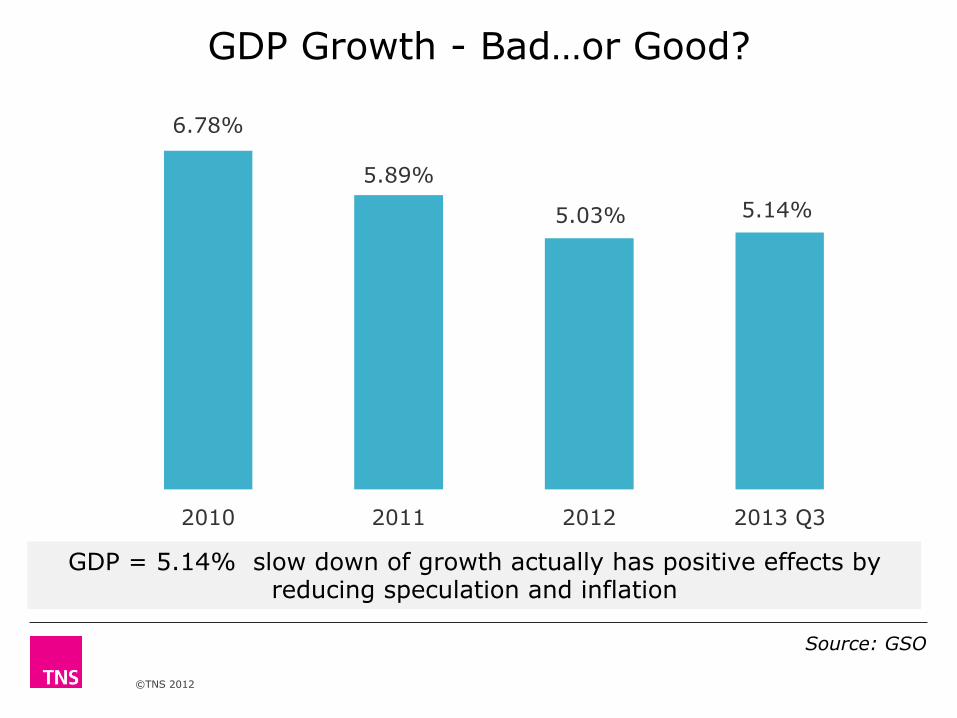

GDP Growth - Bad…or Good?

Source: GSO

GDP = 5.14% slow down of growth actually has positive effects by reducing speculation and inflation

6.78%

5.89%

5.03% 5.14%

2010 2011 2012 2013 Q3

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

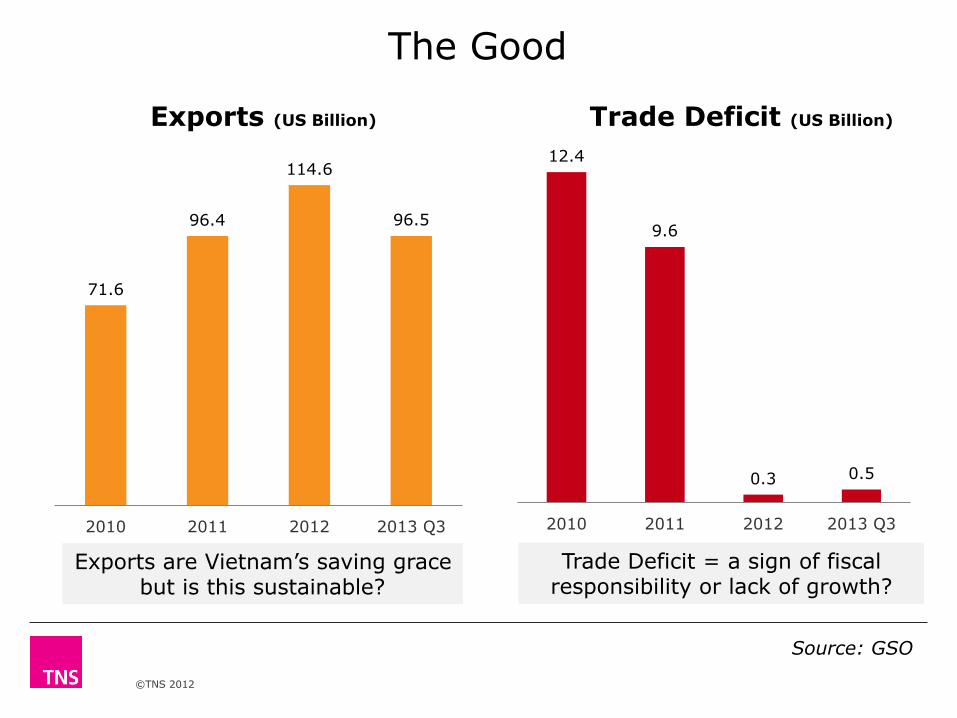

The Good

Source: GSO

Exports are Vietnam’s saving grace but is this sustainable?

Trade Deficit = a sign of fiscal responsibility or lack of growth?

71.6

96.4

114.6

96.5

2010 2011 2012 2013 Q3

12.4

9.6

0.3 0.5

2010 2011 2012 2013 Q3

Exports (US Billion) Trade Deficit (US Billion)

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

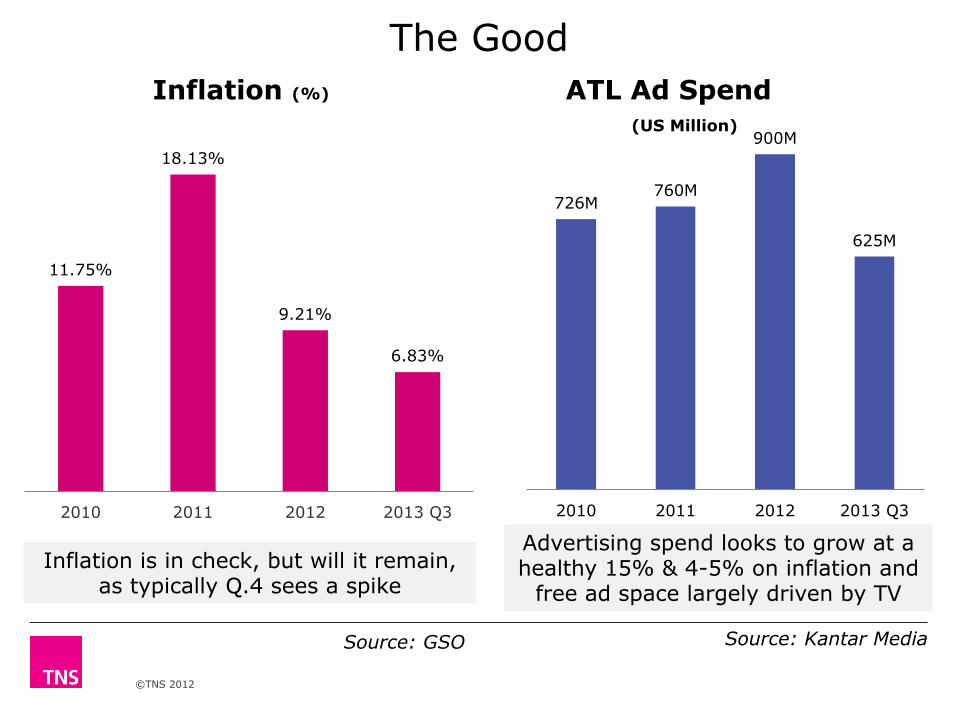

The Good

Inflation is in check, but will it remain, as typically Q.4 sees a spike

Source: GSO

Advertising spend looks to grow at a healthy 15% & 4-5% on inflation and

free ad space largely driven by TV

11.75%

18.13%

9.21%

6.83%

2010 2011 2012 2013 Q3

726M 760M

900M

625M

2010 2011 2012 2013 Q3

Inflation (%) ATL Ad Spend (US Million)

Source: Kantar Media

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

TNS Consumer Confidence Poll

© TNS

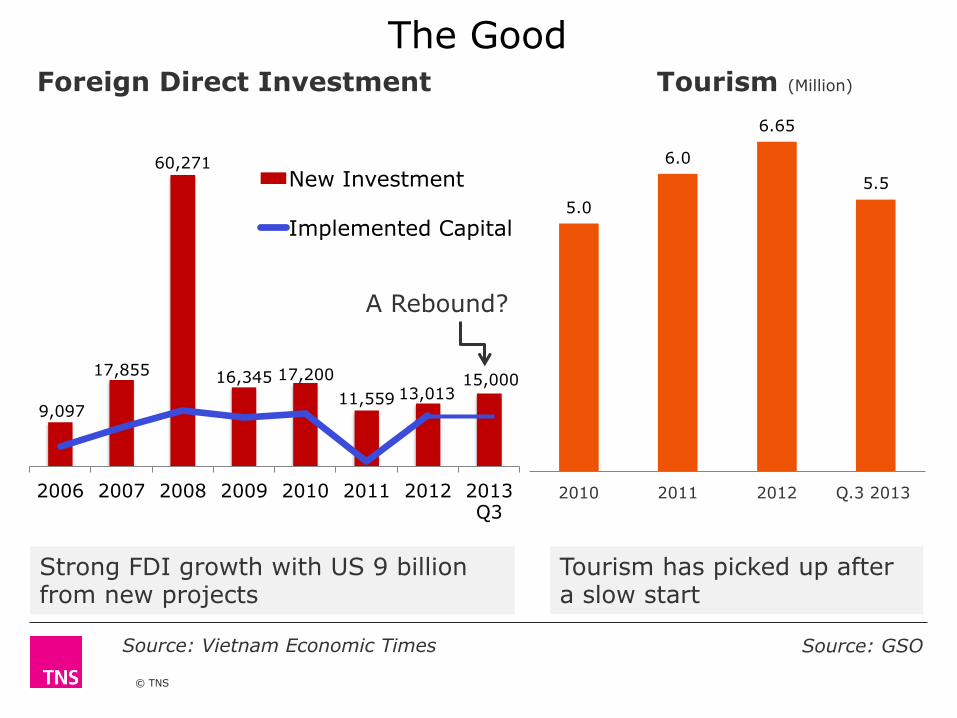

The Good

9,097

17,855

60,271

16,345 17,200 11,559 13,013

15,000

2006 2007 2008 2009 2010 2011 2012 2013 Q3

New Investment

Implemented Capital

A Rebound?

Strong FDI growth with US 9 billion from new projects

Foreign Direct Investment Tourism (Million)

5.0

6.0

6.65

5.5

2010 2011 2012 Q.3 2013

Tourism has picked up after a slow start

Source: Vietnam Economic Times Source: GSO

© TNS 2013

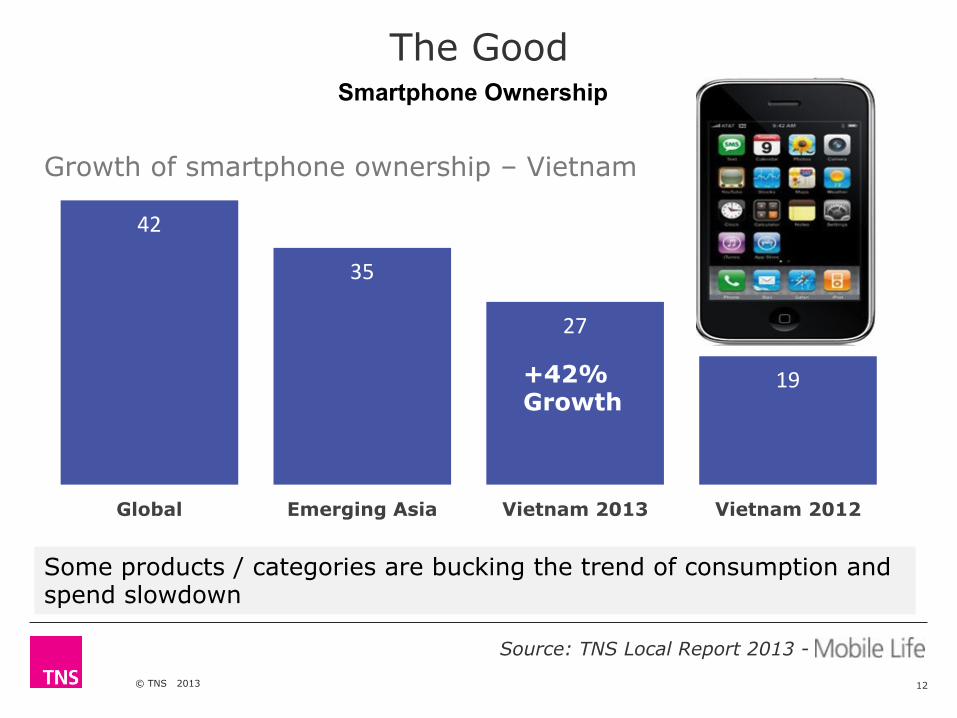

The Good

12

42

35

27

19

Global Emerging Asia Vietnam 2013 Vietnam 2012

Growth of smartphone ownership – Vietnam

Source: TNS Local Report 2013 -

+42% Growth

Some products / categories are bucking the trend of consumption and spend slowdown

Smartphone Ownership

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

TNS Consumer Confidence Poll

© TNS

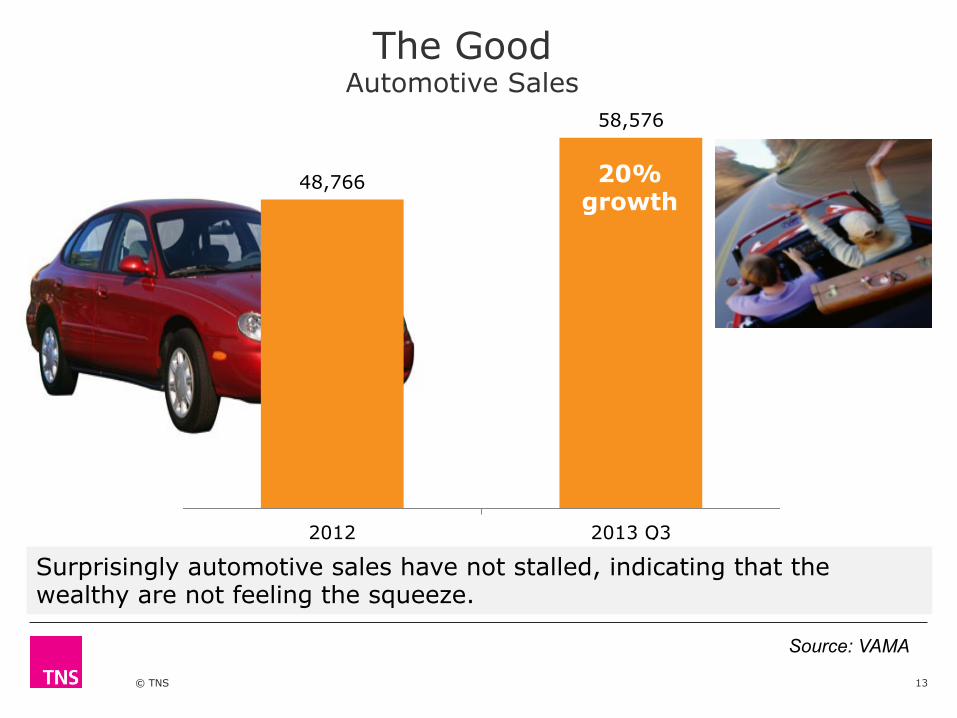

The Good Automotive Sales

13

Surprisingly automotive sales have not stalled, indicating that the wealthy are not feeling the squeeze.

48,766

58,576

2012 2013 Q3

20% growth

Source: VAMA

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

2013 YTD Economic indices scorecard

Ugly = 3 - Real Estate – Confidence – Bad debt Bad = 2 - Bankruptcies - FMCG growth Good = 8 - Modest shift towards recovery

Good time to invest for the future

However, 1st time since 2008 positives outweigh negatives

YTD 2013 is a mixed bag, some ugly, some bad, some good

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

RECESSION IMPACT

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

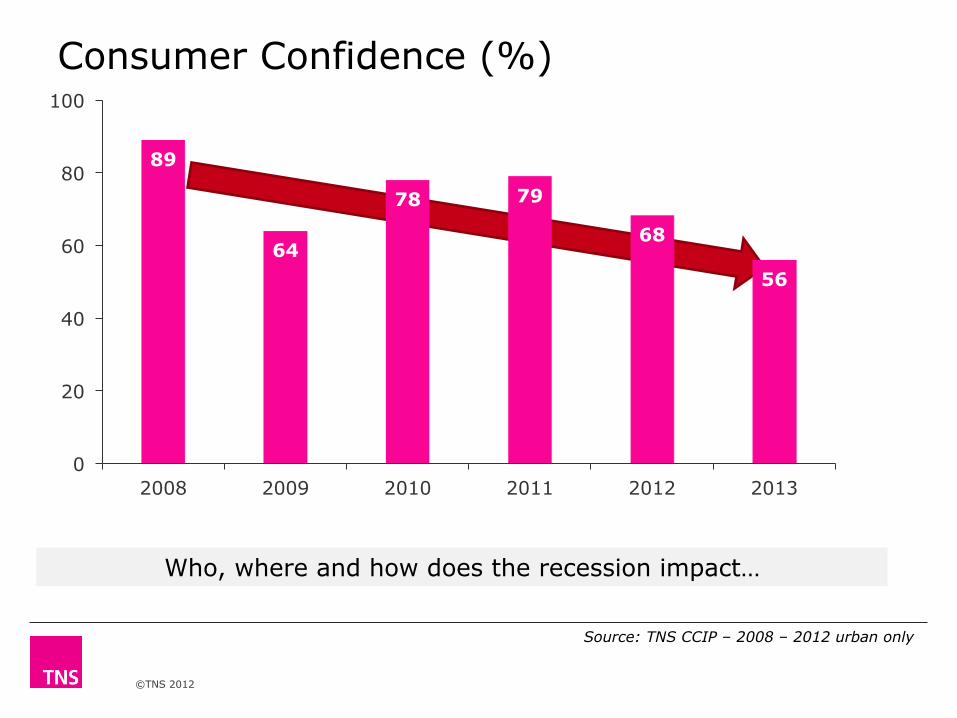

Source: TNS CCIP – 2008 – 2012 urban only

Who, where and how does the recession impact…

Consumer Confidence (%)

89

64

78 79

68

56

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

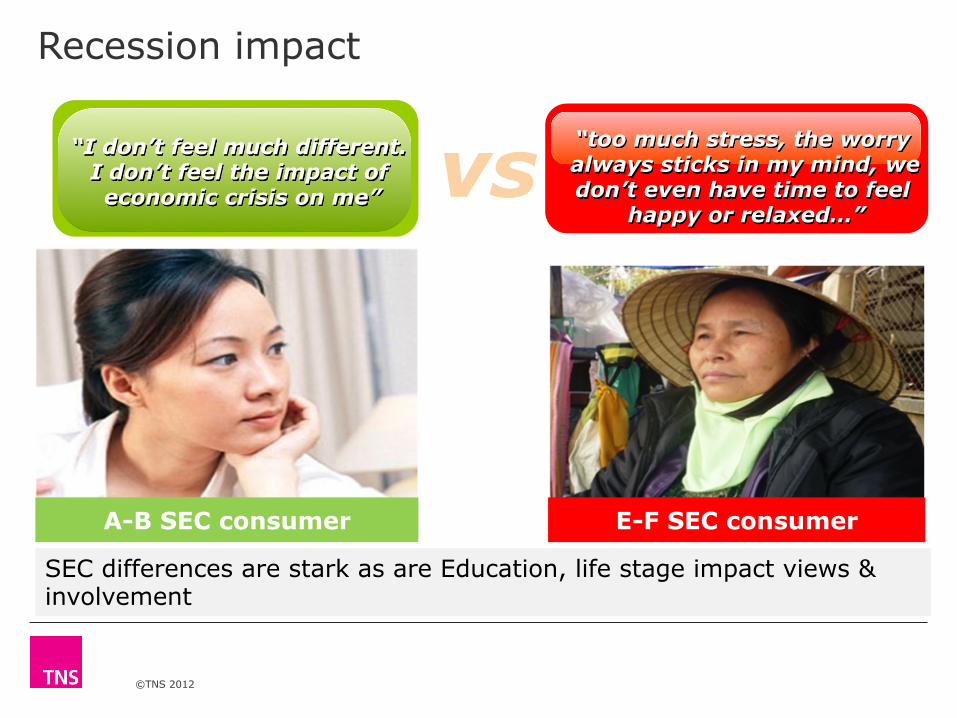

Recession impact “too much stress, the worry

always sticks in my mind, we don’t even have time to feel

happy or relaxed…”

“I don’t feel much different. I don’t feel the impact of economic crisis on me” vs

A-B SEC consumer E-F SEC consumer

SEC differences are stark as are Education, life stage impact views & involvement

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

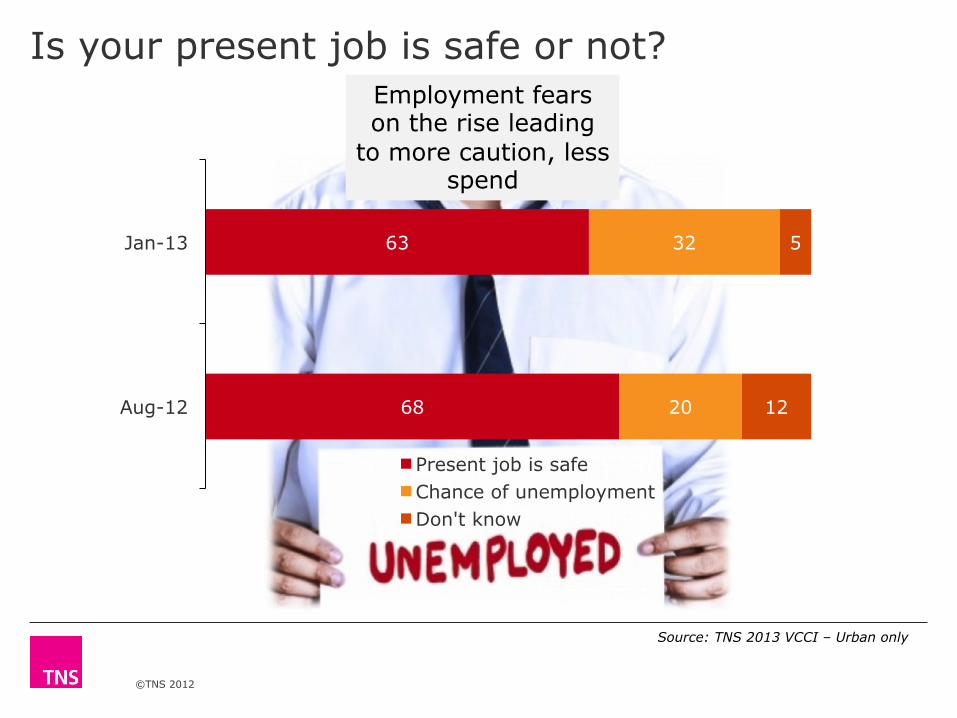

Is your present job is safe or not?

68

63

20

32

12

5

Aug-12

Jan-13

Present job is safe Chance of unemployment Don't know

Employment fears on the rise leading

to more caution, less spend

Source: TNS 2013 VCCI – Urban only

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

5

6

4

5

2

2

45

38

25

29

12

17

34

30

41

35

48

38

14

23

26

30

33

32

1

3

4

2

6

3 8

25

12

11

9

6

3

40

39

34

40

15

24

24

29

34

18

48

26

8

17

18

24

22

30

2

3

3

8

9

4

1

1

13

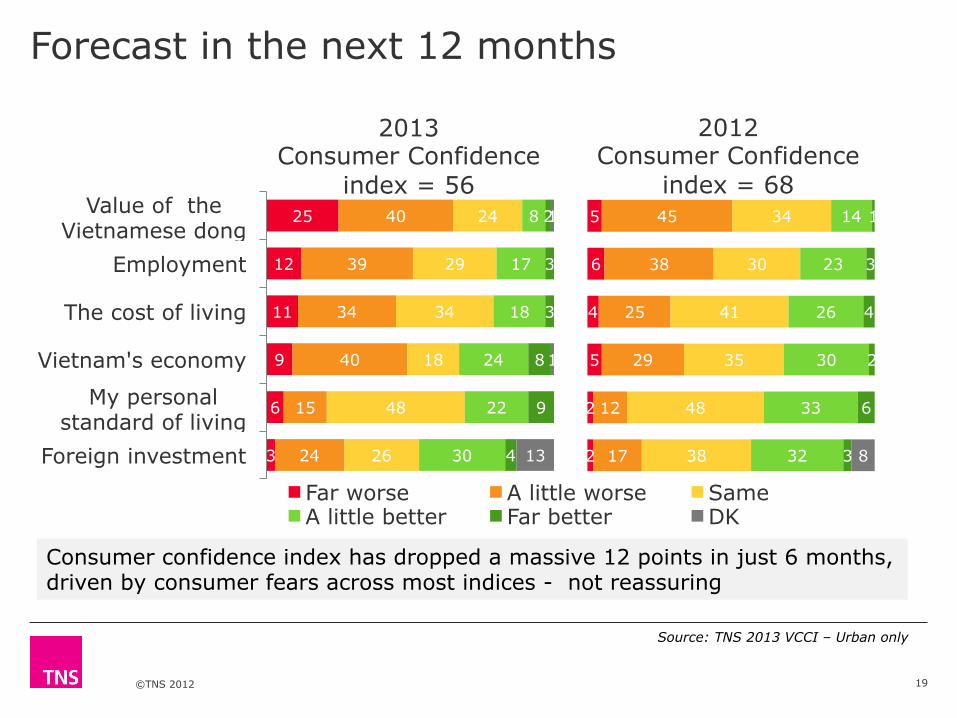

Value of the Vietnamese dong

Employment

The cost of living

Vietnam's economy

My personal standard of living

Foreign investment

Far worse A little worse Same A little better Far better DK

Forecast in the next 12 months

19

2013 Consumer Confidence

index = 56

2012 Consumer Confidence

index = 68

Source: TNS 2013 VCCI – Urban only

Consumer confidence index has dropped a massive 12 points in just 6 months, driven by consumer fears across most indices - not reassuring

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

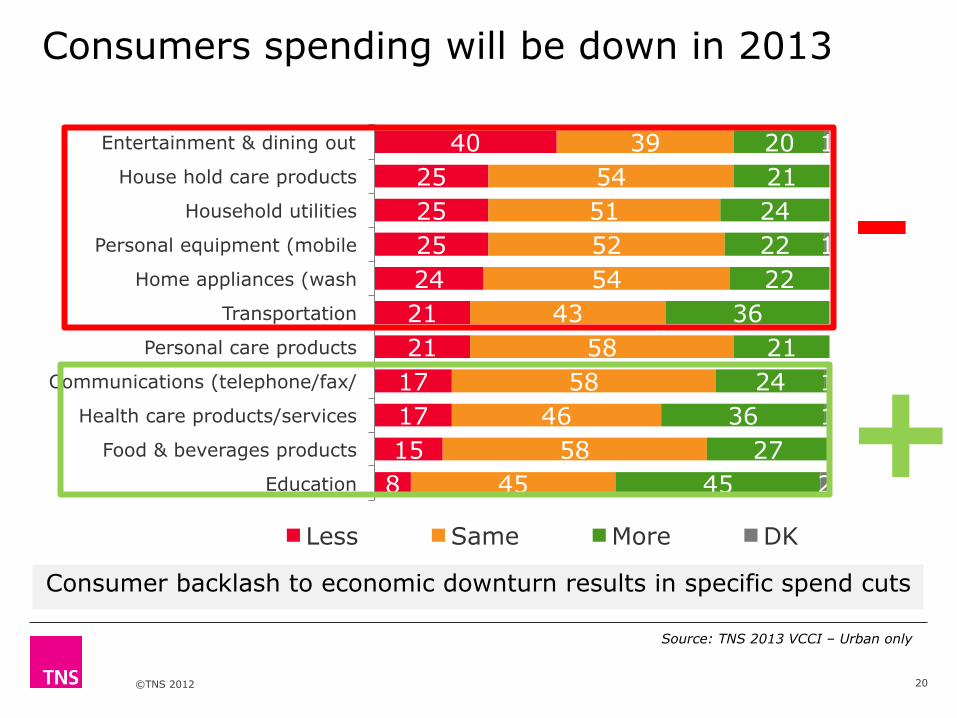

40 25 25 25 24 21 21

17 17 15 8

39 54 51 52 54

43 58

58 46

58 45

20 21 24 22 22

36 21

24 36

27 45

1

1

1 1

2

Entertainment & dining out

House hold care products

Household utilities

Personal equipment (mobile

Home appliances (wash

Transportation

Personal care products

Communications (telephone/fax/

Health care products/services

Food & beverages products

Education

Less Same More DK

- Consumers spending will be down in 2013

20

Consumer backlash to economic downturn results in specific spend cuts

Source: TNS 2013 VCCI – Urban only

+

RETAIL IMPACT

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

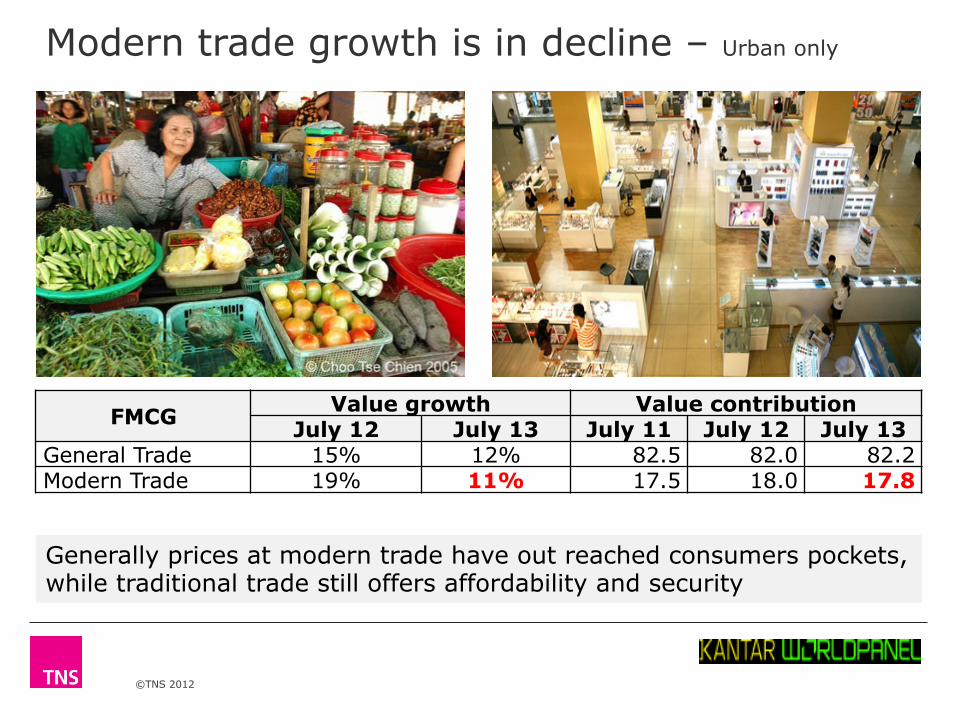

Modern trade growth is in decline – Urban only

Generally prices at modern trade have out reached consumers pockets, while traditional trade still offers affordability and security

FMCG Value growth Value contribution July 12 July 13 July 11 July 12 July 13

General Trade 15% 12% 82.5 82.0 82.2 Modern Trade 19% 11% 17.5 18.0 17.8

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

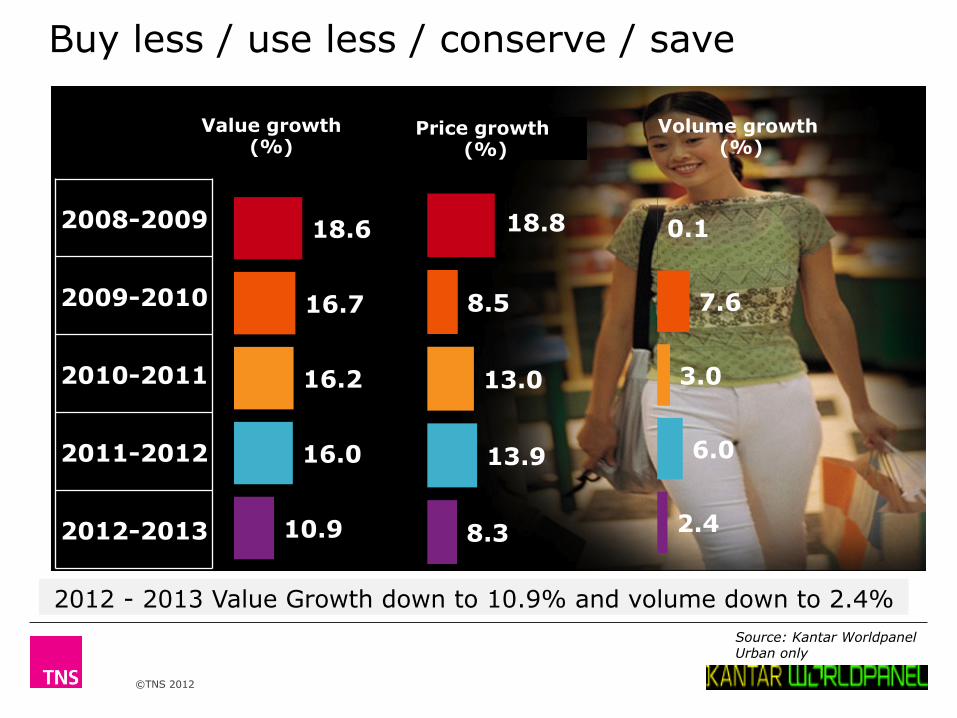

2012 - 2013 Value Growth down to 10.9% and volume down to 2.4%

Buy less / use less / conserve / save

2008-2009

2009-2010

2010-2011

2011-2012

2012-2013

18.6

16.7

16.2

16.0

10.9

Value growth (%)

18.8

8.5

13.0

13.9

8.3

0.1

7.6

3.0

6.0

2.4

Price growth (%)

Volume growth (%)

Source: Kantar Worldpanel Urban only

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

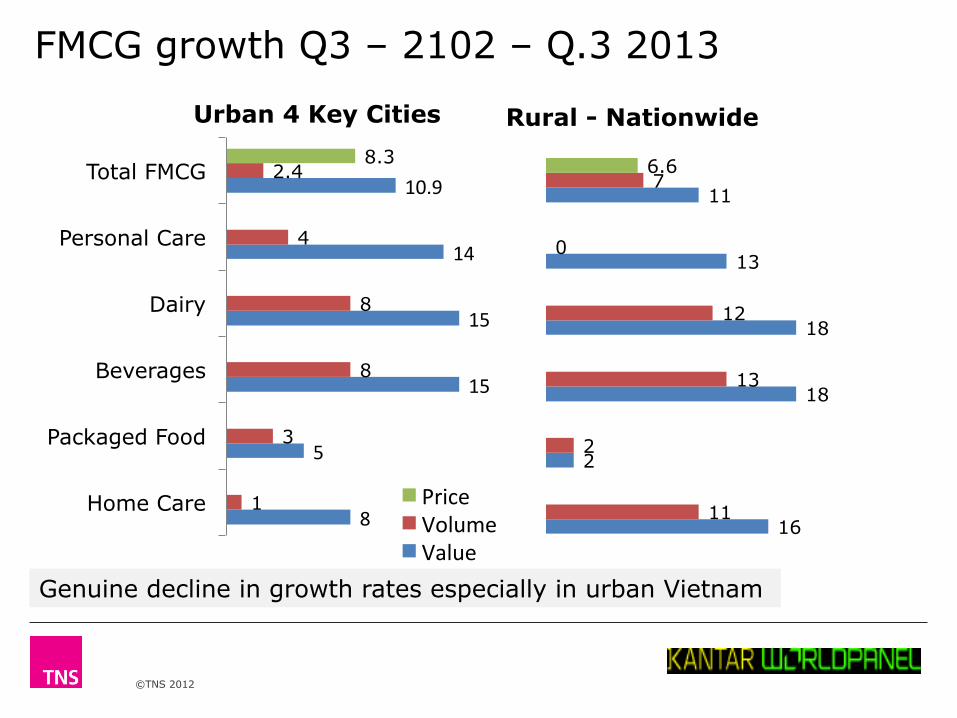

8

5

15

15

14

10.9

1

3

8

8

4

2.4 8.3

Home Care

Packaged Food

Beverages

Dairy

Personal Care

Total FMCG

Price Volume Value

16

2

18

18

13

11

11

2

13

12

0

7 6.6

Urban 4 Key Cities Rural - Nationwide

FMCG growth Q3 – 2102 – Q.3 2013

Genuine decline in growth rates especially in urban Vietnam

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

SIX MARKETING TRENDS

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

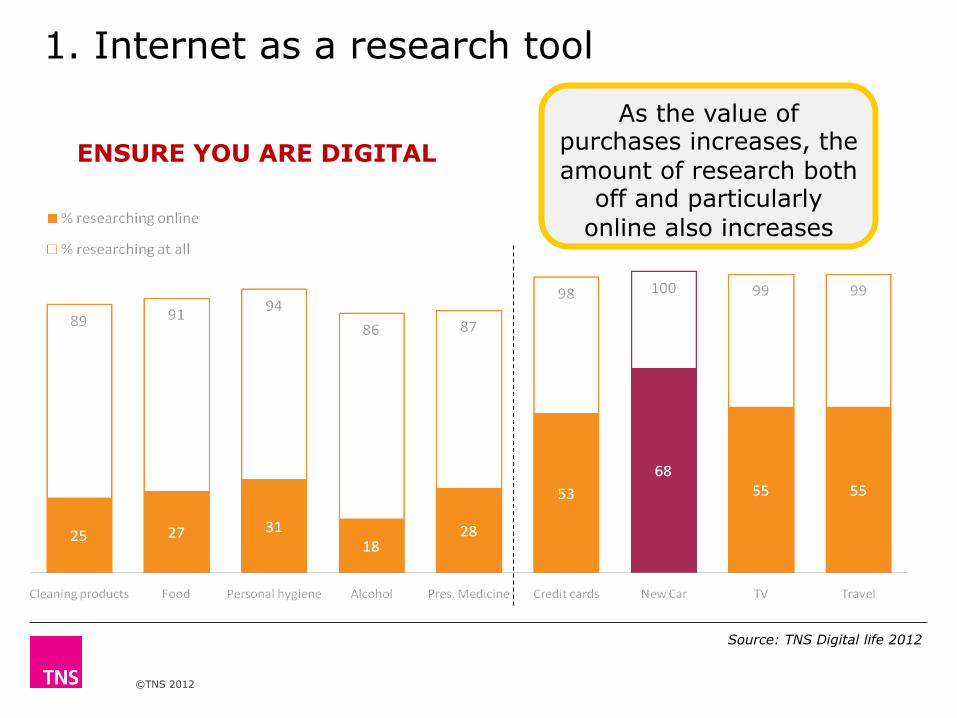

1. Internet as a research tool

Source: TNS Digital life 2012

As the value of purchases increases, the amount of research both

off and particularly online also increases

ENSURE YOU ARE DIGITAL

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

2. Mobile device as the everything hub

Absolutely!

DEVELOP YOUTH APPLICACTIOSN FOR

YOUR BUSINESS

As the availability of wireless broadband

expands & the cost of advanced mobile phones drop, the mobile device will

become the preferred hub for digital activity.

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

3. Authenticity matters

Yes! “I need to know the

companies where the products or services are

from so I have confidence to use them”

GUARANTEE QUALITY / SAFETY

Authenticity will become paramount for brands as they look to regain credibility and trust. Consumers have lost a great deal of faith in brands; they are searching for truths and clamouring for transparency.

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

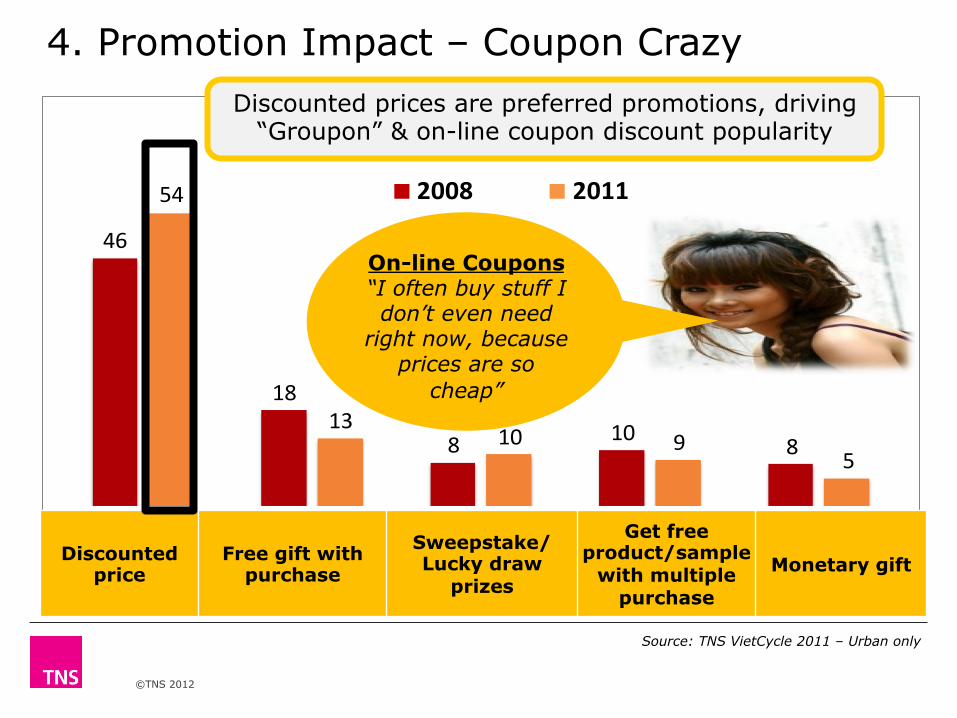

46

18

8 10 8

54

1310 9

5

2008 2011

Discounted price

Free gift with purchase

Sweepstake/Lucky draw

prizes

Get free product/sample

with multiple purchase

Monetary gift

4. Promotion Impact – Coupon Crazy

Source: TNS VietCycle 2011 – Urban only

On-line Coupons “I often buy stuff I don’t even need

right now, because prices are so

cheap”

Discounted prices are preferred promotions, driving “Groupon” & on-line coupon discount popularity

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

5.Brand innovation & new product launches

X-Men Manly

international standard ads

for men

Knorr All-in-one new multiple spices

for specific meals

Pro Beauty New Yogurt gives you

beautiful skin

Kent

Taste & strength control filter

Non to menthol

A good time to launch new products and innovations to keep consumers excited and stay ahead of competition

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

TNS Consumer Confidence Poll

© TNS

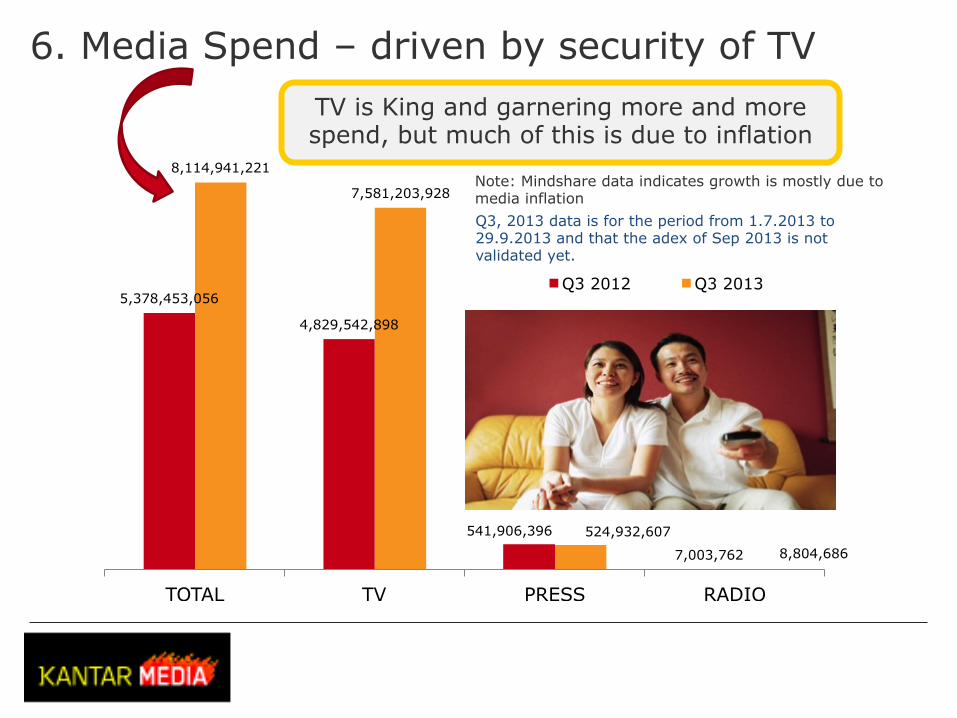

5,378,453,056

4,829,542,898

541,906,396

7,003,762

8,114,941,221

7,581,203,928

524,932,607 8,804,686

TOTAL TV PRESS RADIO

Q3 2012 Q3 2013

6. Media Spend – driven by security of TV

Note: Mindshare data indicates growth is mostly due to media inflation Q3, 2013 data is for the period from 1.7.2013 to 29.9.2013 and that the adex of Sep 2013 is not validated yet.

TV is King and garnering more and more spend, but much of this is due to inflation

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

TNS Consumer Confidence Poll

© TNS

Key insights and food for thought

32

§ Vietnam is experiencing a long overdue correction caused largely by the countries emergence from 3rd world existence, financial and real estate speculation and overall fiscal mismanagement and lack of transparency

§ The days of “build it they will come” are over - generic organic growth due to sheer emergence are in the past for most sectors

§ Targeted consumer engagement and building a reason to believe and develop trust are key proponents to success

§ Many Vietnamese companies are under capitalized, thus shifting investment focus back onto MNC’s and fleet of foot organizations

§ Size and length of business in Vietnam has impact on ability to grow. Many big companies are able to drowned out competition, so long as they invest and build their capabilities and capacity

§ New Investment in the market shall come from Japan, China and South East Asian countries, which needs to be harnessed for maximum impact

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

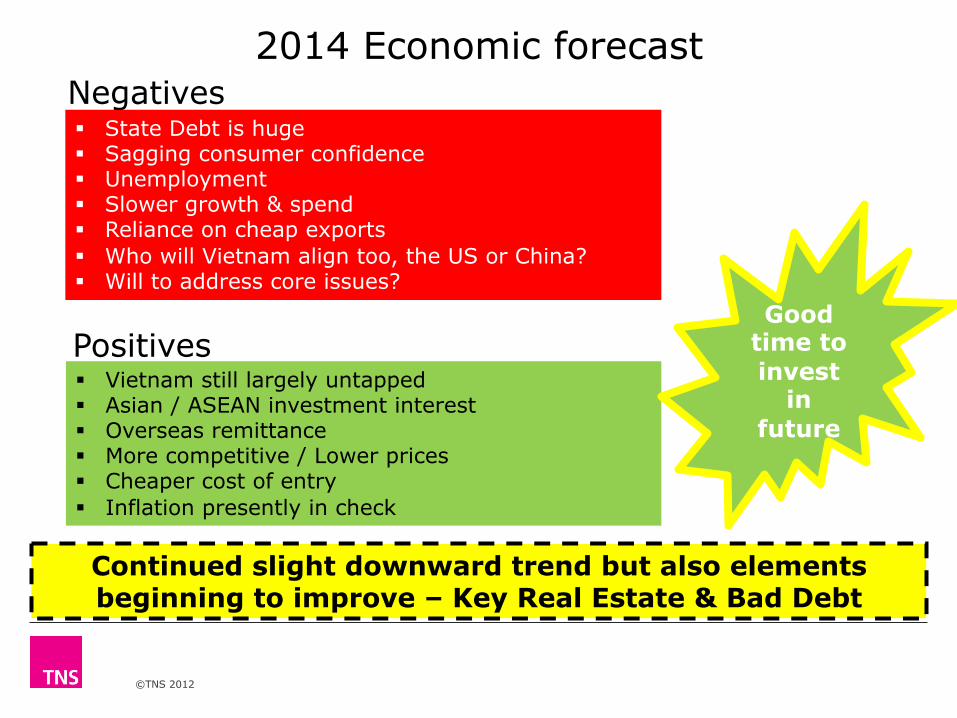

2014 Economic forecast

Continued slight downward trend but also elements beginning to improve – Key Real Estate & Bad Debt

Negatives

Positives

§ State Debt is huge § Sagging consumer confidence § Unemployment § Slower growth & spend § Reliance on cheap exports § Who will Vietnam align too, the US or China? § Will to address core issues?

§ Vietnam still largely untapped § Asian / ASEAN investment interest § Overseas remittance § More competitive / Lower prices § Cheaper cost of entry § Inflation presently in check

Good time to invest

in future

©TNS 2012

3.14 X AXIS

6.65 BASE MARGIN

5.95 TOP MARGIN

4.52 CHART TOP

11.90 LEFT MARGIN

11.90 RIGHT MARGIN

Complete Consumer Insights

§ Please do not hesitate to contact: § Ralf Matthaes § Regional Managing Director

[email protected] § Cambodia | Laos | Myanmar |

Vietnam

§ Vietnam site: www.tnsvietnam.vn § Global site: www.tnsglobal.com

§ Floor 3-4-5 Agrex Building 58 Vo Van Tan Street District 3, Ho Chi Minh City, Vietnam