40

ICF International | icfi.com © ICF SH&E 2013 MRO Market Forecast & Industry Dynamics October 15, 2013 Jonathan M. Berger Vice President ICF SH&E [email protected] Presented by:

| Date post: | 23-Oct-2015 |

| Category: |

Documents |

| Upload: | eduard-timoffeeff |

| View: | 221 times |

| Download: | 1 times |

ICF International | icfi.com © ICF SH&E 2013

MRO Market Forecast & Industry Dynamics

October 15, 2013

Jonathan M. Berger Vice President ICF SH&E [email protected]

Presented by:

ICF International | icfi.com © ICF SH&E 2013 1

Today’s Agenda:

1. MRO Market Forecast

2. MRO Industry Trends to Watch

joined ICF in 2011 joined ICF in 2012 joined ICF in 2007

2013 Airline E&M

North America

Montreal, Canada

ICF International | icfi.com © ICF SH&E 2013 2

MRO Market Forecast

ICF International | icfi.com © ICF SH&E 2013 3

North America

Europe

Asia Pacific

Latin America

Africa Middle East

NarrowbodyJet

Widebody Jet

Regional Jet

Turboprop

The current civil air transport fleet is in excess of 26K aircraft MRO MARKET FORECAST

Source: Flightglobal ACAS, ICF Analysis

2012 Global Air Transport Fleet

26,156 Aircraft

17%

50% 15%

18%

~8,300 32%

26%

24%

8%

5% 5%

26,156 Aircraft

ICF International | icfi.com © ICF SH&E 2013 4

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2012 2022

AfricaMiddle EastLatin AmericaAsia / PacificEuropeNorth America

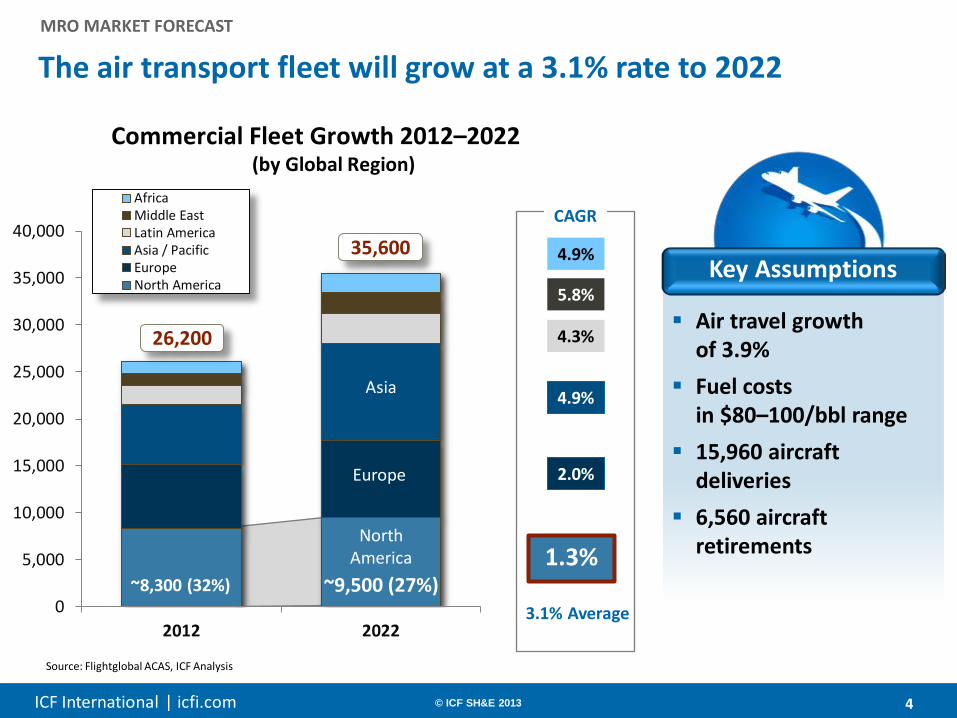

The air transport fleet will grow at a 3.1% rate to 2022 MRO MARKET FORECAST

Commercial Fleet Growth 2012–2022 (by Global Region)

Source: Flightglobal ACAS, ICF Analysis

4.3%

4.9%

2.0%

1.3%

5.8%

4.9%

26,200

35,600 CAGR

3.1% Average

Air travel growth of 3.9%

Fuel costs in $80–100/bbl range

15,960 aircraft deliveries

6,560 aircraft retirements

Key Assumptions

~8,300 (32%) ~9,500 (27%)

North America

Europe

Asia

ICF International | icfi.com © ICF SH&E 2013 5

The North American MRO market size in 2012 was $17.9 billion MRO MARKET FORECAST

2012 North American MRO Spend

$17.9B $17.9B

Source: ICF SH&E forecast Forecast in 2012 USD, exclusive of inflation. Includes turboprops

Engines

Components

Airframe

Line

Modifications

16%

17%

21%

41%

5% Narrowbody Jet

Widebody Jet

Regional Jet

Turboprop

50% 31%

15% 5%

ICF International | icfi.com © ICF SH&E 2013 6

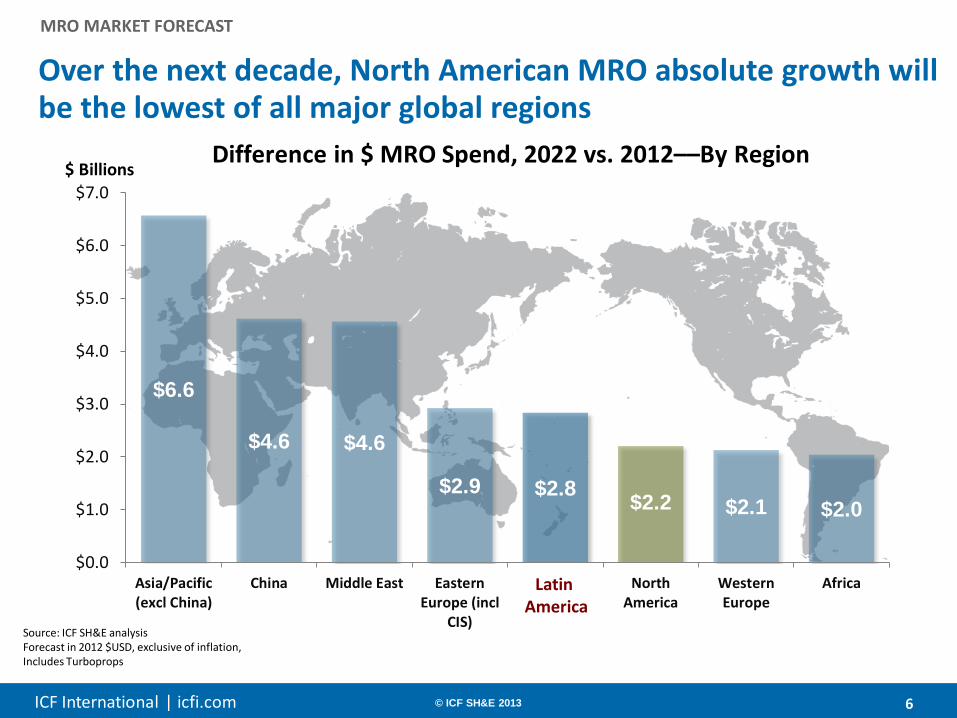

$6.6

$4.6 $4.6

$2.9 $2.8 $2.2 $2.1 $2.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

Asia/Pacific(excl China)

China Middle East EasternEurope (incl

CIS)

Latin America NorthAmerica

WesternEurope

Africa

Over the next decade, North American MRO absolute growth will be the lowest of all major global regions

MRO MARKET FORECAST

Difference in $ MRO Spend, 2022 vs. 2012––By Region $ Billions

Source: ICF SH&E analysis Forecast in 2012 $USD, exclusive of inflation, Includes Turboprops

Latin America

ICF International | icfi.com © ICF SH&E 2013 7

$0

$5

$10

$15

$20

$25

2012 2022

TurbopropRegional JetWidebody JetNarrowbody Jet

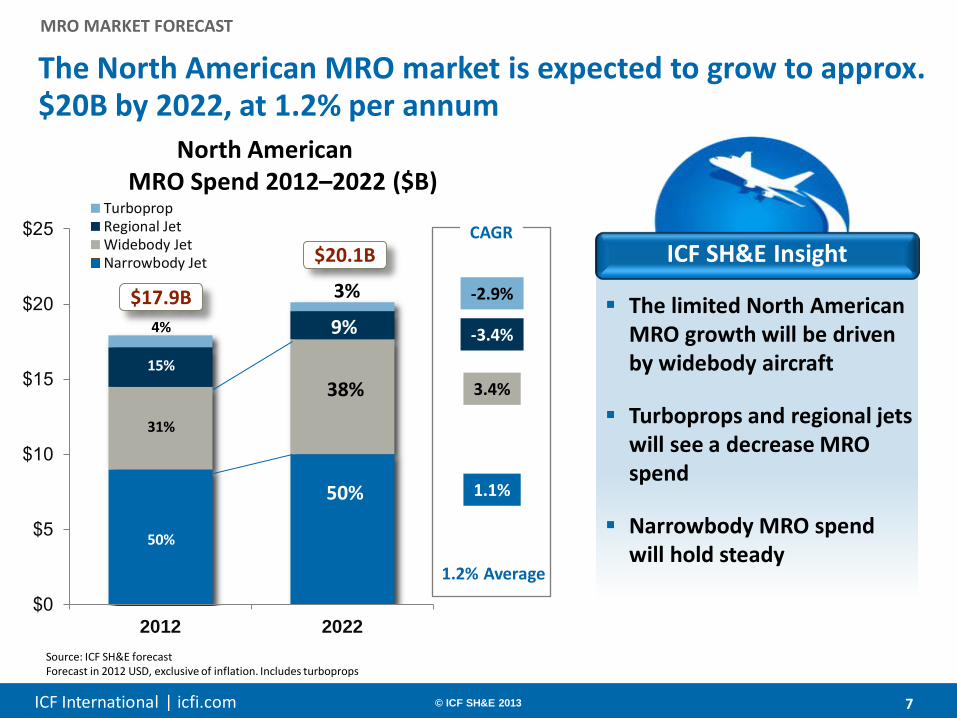

The North American MRO market is expected to grow to approx. $20B by 2022, at 1.2% per annum

MRO MARKET FORECAST

North American MRO Spend 2012–2022 ($B)

-2.9%

-3.4%

3.4%

1.1%

Source: ICF SH&E forecast Forecast in 2012 USD, exclusive of inflation. Includes turboprops

4%

15%

31%

50%

3%

9%

38%

50%

CAGR

1.2% Average

The limited North American MRO growth will be driven by widebody aircraft

Turboprops and regional jets will see a decrease MRO spend

Narrowbody MRO spend will hold steady

ICF SH&E Insight

$17.9B

$20.1B

ICF International | icfi.com © ICF SH&E 2013 8

MRO Industry Trends to Watch

ICF International | icfi.com © ICF SH&E 2013 9

Five key MRO industry trends to watch…

Source: ICF SH&E

MRO INDUSTRY TRENDS

Industry Trends

M&A in MRO

Surplus Parts

3-D Printing

Airframe MRO

Energy & Aviation

Convergence

ICF International | icfi.com © ICF SH&E 2013 10

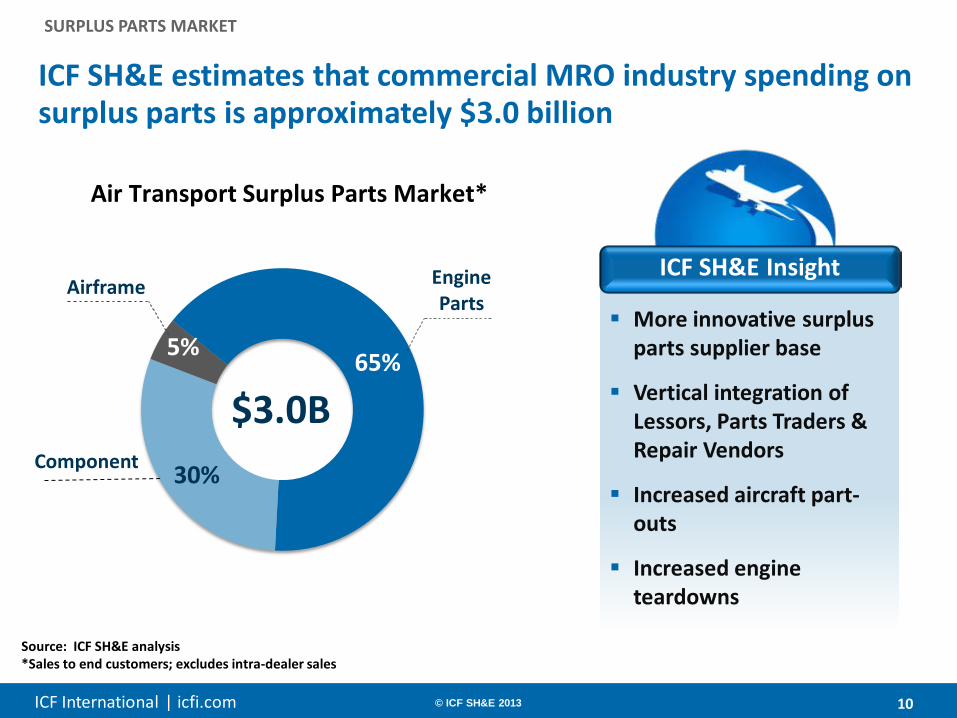

ICF SH&E estimates that commercial MRO industry spending on surplus parts is approximately $3.0 billion

SURPLUS PARTS MARKET

Engine Parts

Component

Airframe

5% 65%

30%

Air Transport Surplus Parts Market*

Source: ICF SH&E analysis *Sales to end customers; excludes intra-dealer sales

$3.0B

More innovative surplus parts supplier base

Vertical integration of Lessors, Parts Traders & Repair Vendors

Increased aircraft part-outs

Increased engine teardowns

ICF SH&E Insight

ICF International | icfi.com © ICF SH&E 2013 11

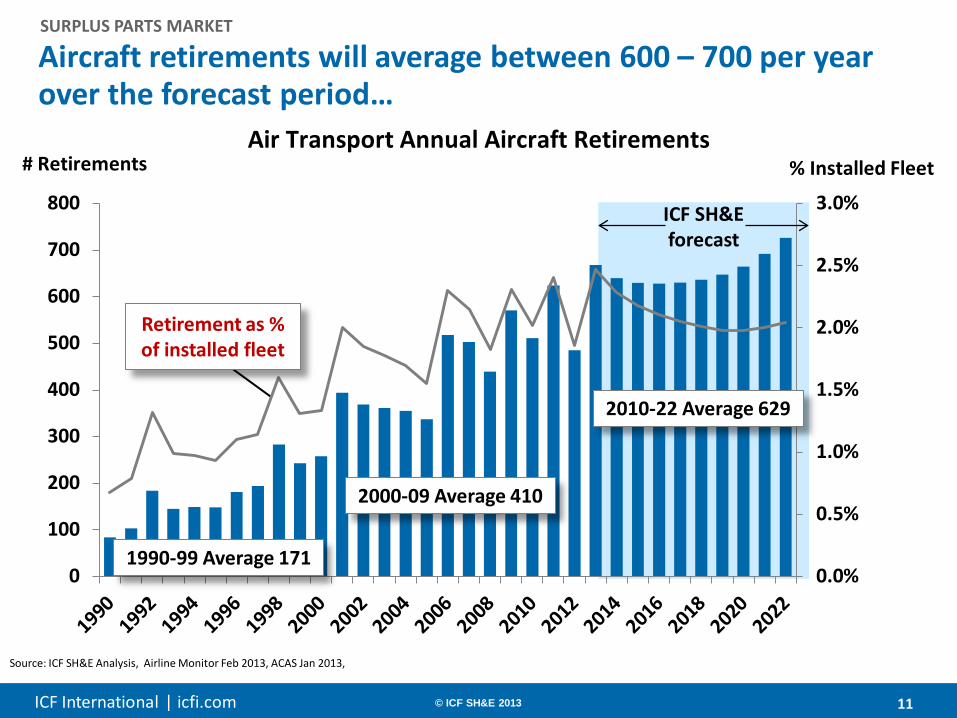

Aircraft retirements will average between 600 – 700 per year over the forecast period…

SURPLUS PARTS MARKET

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

100

200

300

400

500

600

700

800

Air Transport Annual Aircraft Retirements # Retirements

Retirement as % of installed fleet

% Installed Fleet

ICF SH&E forecast

Source: ICF SH&E Analysis, Airline Monitor Feb 2013, ACAS Jan 2013,

1990-99 Average 171

2000-09 Average 410

2010-22 Average 629

ICF International | icfi.com © ICF SH&E 2013 12

Surplus dealers now obtain over 80% of their inventory from parting-out aircraft…

SURPLUS PARTS MARKET

54%

82%

26%

8% 20% 10%

0%10%20%30%40%50%60%70%80%90%

100%

2007 2012

Aircraft Part-Out

Direct Purchase From Airline

Purchase From Surplus Dealer

2007 & 2012 Supplier Channels for Obtaining Surplus Materials

Source: ICFI SH&E Analysis

Leaner airline inventories

Improved material planning (and MRO IT capabilities)

Increased component pooling agreements

OEM after-market material control strategies

ICF SH&E Insight

ICF International | icfi.com © ICF SH&E 2013 13

Industry Trends

M&A in MRO

Energy & Aviation

Convergence

Airframe MRO

3-D Printing

Surplus Parts

Five key MRO industry trends to watch…

Source: ICF SH&E

MRO INDUSTRY TRENDS

ICF International | icfi.com © ICF SH&E 2013 14

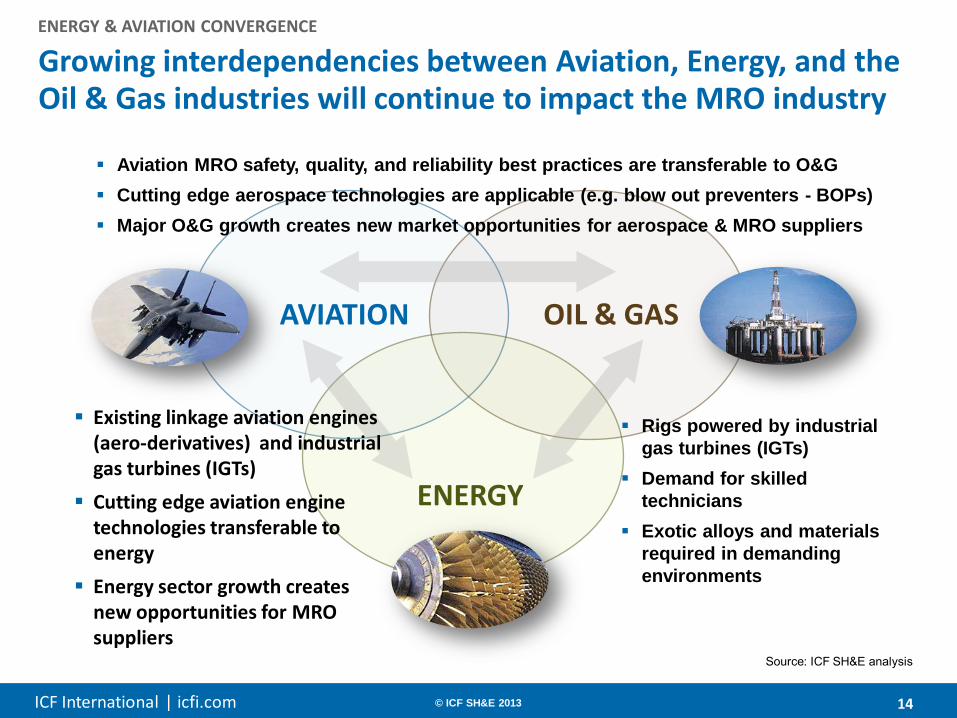

Growing interdependencies between Aviation, Energy, and the Oil & Gas industries will continue to impact the MRO industry

Source: ICF SH&E analysis

ENERGY & AVIATION CONVERGENCE

AVIATION OIL & GAS

ENERGY

Existing linkage aviation engines (aero-derivatives) and industrial gas turbines (IGTs)

Cutting edge aviation engine technologies transferable to energy

Energy sector growth creates new opportunities for MRO suppliers

Aviation MRO safety, quality, and reliability best practices are transferable to O&G Cutting edge aerospace technologies are applicable (e.g. blow out preventers - BOPs) Major O&G growth creates new market opportunities for aerospace & MRO suppliers

Rigs powered by industrial gas turbines (IGTs)

Demand for skilled technicians

Exotic alloys and materials required in demanding environments

ICF International | icfi.com © ICF SH&E 2013

Hydraulic fracturing (i.e. fracking) is leading to a significant shift away from coal to natural gas power generation…

012345678

$/M

MBt

u

Commodity Fuel Prices

Illinois 4lb Pennsylvania 4lbNYMEX Spec Henry Hub Gas

43% 35%

22% 30%

34% 34%

0

500

1,000

1,500

2,000

2,500

2011 Jan-Jun 2012 Jan-Jun

TWh

US Coal versus Gas Generation

Coal Generation Gas Generation Other Generation

-20% Coal

+34% Gas

-2% Other

-2% Total

Sources: ICF analysis, Bloomberg, EIA

ENERGY & AVIATION CONVERGENCE

Tumbling natural gas prices due to fracking have erased coal’s cost advantage

As a result, U.S. gas-powered power generation increased its market share from 22% to 30% in one year

The result: Greater industrial gas turbine (IGT) demand and utilization

ICF SH&E Insight

ICF International | icfi.com © ICF SH&E 2013 16

…and should underpin expansion of the industrial gas turbine (IGT) market, currently valued at approx. $20B

Source: ICF SH&E analysis, Forecast International

$0

$5

$10

$15

$20

$25

$30

Aeroengine IGT

2011 Global Gas Turbine Engine Production ($B)

Military

Aeroderivative

Used for Power Generation

Used for O&G and peak power generation

ENERGY & AVIATION CONVERGENCE

Lower natural gas prices are increasing demand IGT generation…and should underpin production market growth over the next decade

IGTs increasingly leverage leading aviation engine technologies developed for the aeroengine segment

ICF SH&E Insight

Civil Frame

ICF International | icfi.com © ICF SH&E 2013 17

Five key MRO industry trends to watch…

Source: ICF SH&E

Industry Trends

MRO INDUSTRY TRENDS

Airframe MRO

M&A in MRO

3-D Printing

Surplus Parts

Energy & Aviation

Convergence

ICF International | icfi.com © ICF SH&E 2013 18

Positive market forces are driving continued investment interest in the MRO industry…

M&A TRENDS IN THE MRO INDUSTRY

GROWTH INDUSTRY favorable market dynamics

D-E-F-E-N-S-E Avoid competitor from

acquiring first

MARKET SHARE Spread fixed costs over a large base

COST REDUCTION Leverage emerging market labor rates

DIVERSIFICATION Mitigate risk of industry

cyclicality

HORIZONTAL OR VERTICAL INTEGRATION Create synergies within

existing portfolio of products, services, and

customers

“OFF-SET” REQUIREMENT

Certain countries require reciprocal investment

GEOGRAPHIC EXPANSION increase global footprint &

customer base

ICF International | icfi.com © ICF SH&E 2013 19

M&A TRENDS IN THE MRO INDUSTRY

While peaking in 2007, MRO-related M&A transactions have shown steady growth…

Source: Jefferies’ Research

61

84 87

123

153

133

70 76 84

93

70

0

20

40

60

80

100

120

140

160

180

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013YTD

MRO-Related M&A Activity Cumulative Annual Total Transactions

ICF International | icfi.com © ICF SH&E 2013 20

M&A TRENDS IN THE MRO INDUSTRY

…also peaking in 2007, MRO related M&A EBITDA multiples appear to have stabilized

Source: Jefferies’ Research

9.0x 8.5x

12.5x

10.6x

13.1x

10.0x

8.0x

10.0x 9.2x

8.5x 9.0x

0x

2x

4x

6x

8x

10x

12x

14x

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013YTD

MRO-Related M&A Activity Average Transaction EBITDA Multiple

ICF International | icfi.com © ICF SH&E 2013 21

ICF SH&E anticipates strong growth in MRO related M&A activity to continue over the next few years…

M&A TRENDS IN THE MRO INDUSTRY

acquired SAS Components

acquired Vought Aircraft Industries and cabin repair specialist Aviation Network Services

acquired Aviall

acquired The Memphis Group

acquired DeCrane’s bizjet interior production

and completes Microtecnica acquisition

acquired M&M Hardware

acquired German galley

manufacturer Sell and finalizes Contour

Acquisition

acquired aircraft component

manufacturer South Bend Controls

acquired Aero Technology

acquired Goodrich

acquired UK-based Airinmar

acquired Aersospace Coatings

International (ACI), AMSafe acquired Satair

acquired safety equipment supplier

AmSafe acquired

Vector Aerospace

acquired Dansk Fly Elektronik acquired Aero

Maintenance Group (AMG)

acquired Finnair Engine shop

acquired Mechanical Enterprises (MEI)

acquired Connector Maker Switchcraft

Summary of active participants in MRO M&A

acquired Aveos Components

ICF International | icfi.com © ICF SH&E 2013 22

Five key MRO industry trends to watch…

Source: ICF SH&E

Industry Trends

MRO INDUSTRY TRENDS

Surplus Parts

Airframe MRO

3-D Printing

Energy & Aviation

Convergence

M&A in MRO

ICF International | icfi.com © ICF SH&E 2013 23

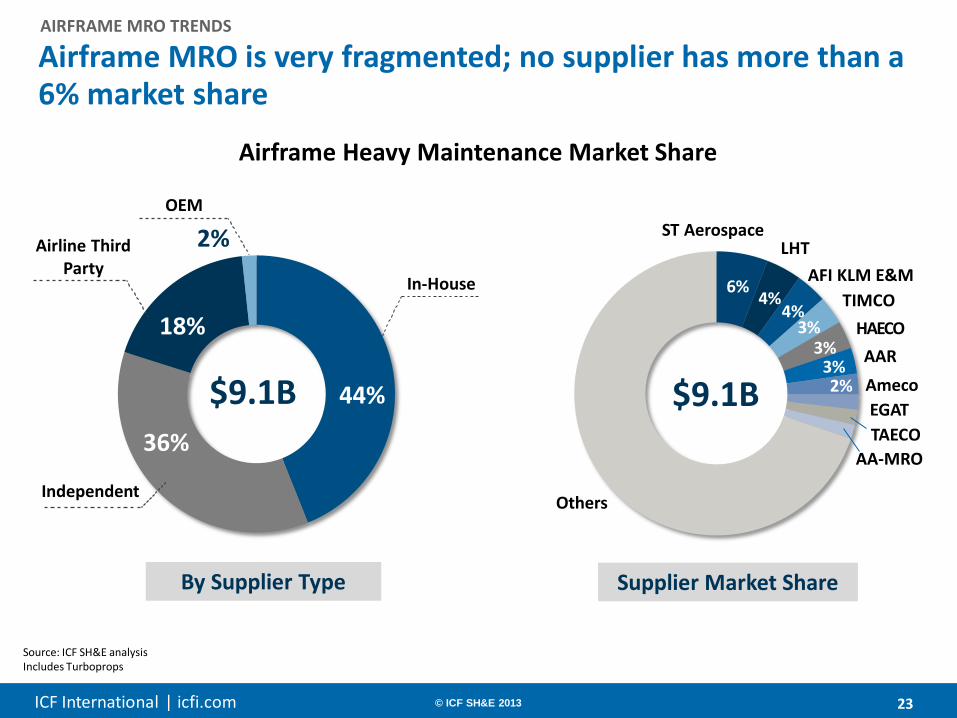

In-House

Independent

Airline Third Party

OEM

Airframe MRO is very fragmented; no supplier has more than a 6% market share

Airframe Heavy Maintenance Market Share

AIRFRAME MRO TRENDS

ST Aerospace LHT

AFI KLM E&M TIMCO

HAECO AAR Ameco EGAT TAECO

AA-MRO

Others

By Supplier Type

2%

44%

18%

36%

6% 4%

4% 3%

3% 3% 2% $9.1B

Source: ICF SH&E analysis Includes Turboprops

Supplier Market Share

$9.1B

ICF International | icfi.com © ICF SH&E 2013 24

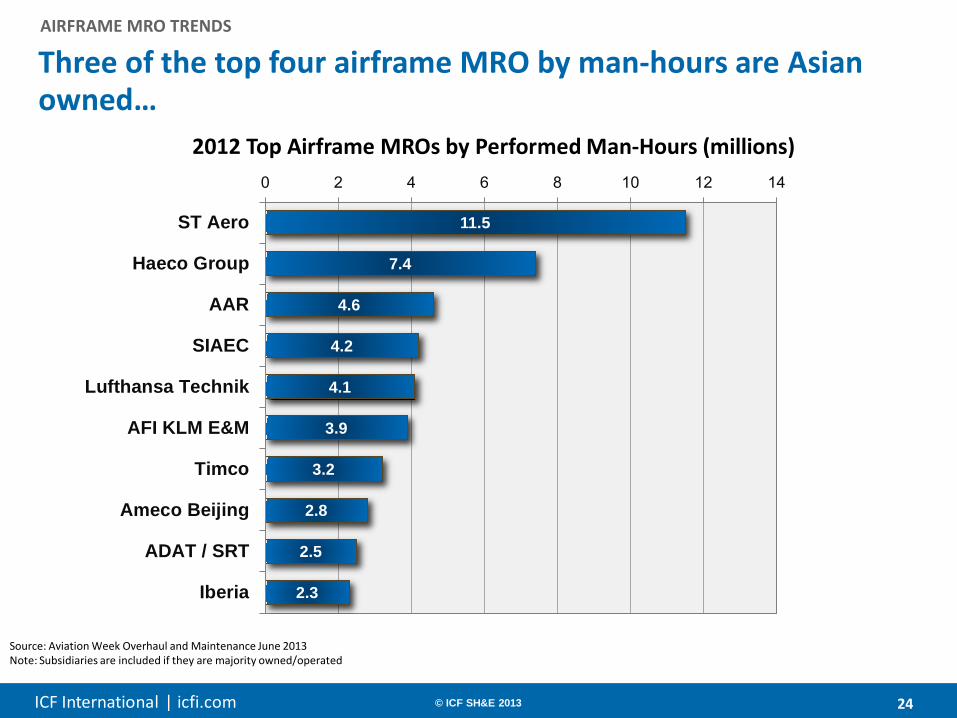

Three of the top four airframe MRO by man-hours are Asian owned…

AIRFRAME MRO TRENDS

11.5

7.4

4.6

4.2

4.1

3.9

3.2

2.8

2.5

2.3

0 2 4 6 8 10 12 14

ST Aero

Haeco Group

AAR

SIAEC

Lufthansa Technik

AFI KLM E&M

Timco

Ameco Beijing

ADAT / SRT

Iberia

2012 Top Airframe MROs by Performed Man-Hours (millions)

Source: Aviation Week Overhaul and Maintenance June 2013 Note: Subsidiaries are included if they are majority owned/operated

ICF International | icfi.com © ICF SH&E 2013 25

$10

$20

$30

$40

$50

$60

$70

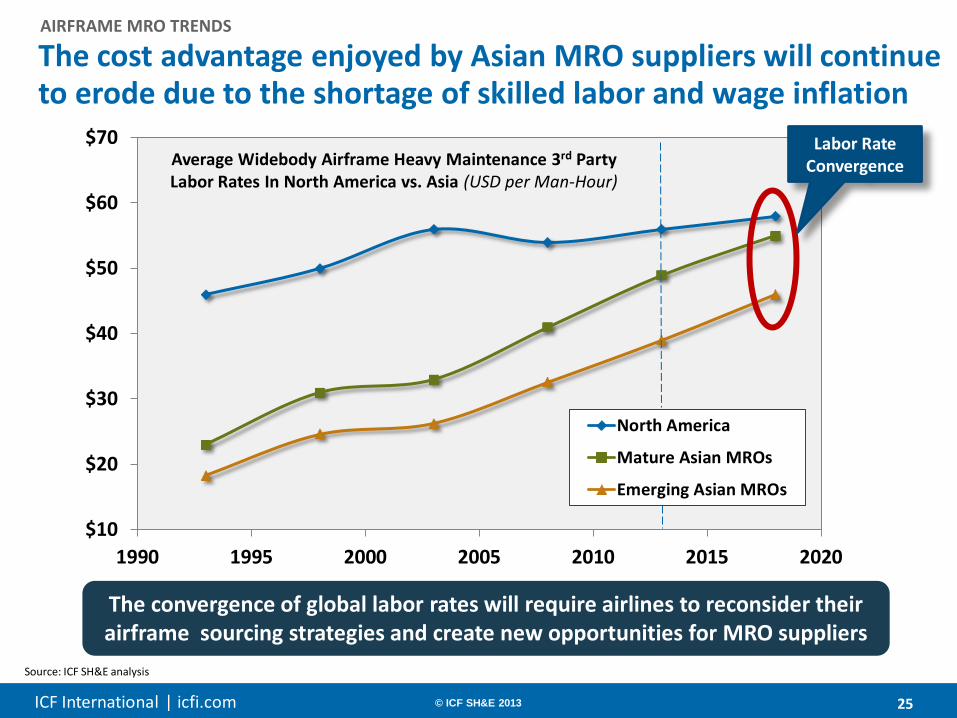

1990 1995 2000 2005 2010 2015 2020

North America

Mature Asian MROs

Emerging Asian MROs

Average Widebody Airframe Heavy Maintenance 3rd Party Labor Rates In North America vs. Asia (USD per Man-Hour)

The cost advantage enjoyed by Asian MRO suppliers will continue to erode due to the shortage of skilled labor and wage inflation

The convergence of global labor rates will require airlines to reconsider their airframe sourcing strategies and create new opportunities for MRO suppliers

Labor Rate Convergence

Source: ICF SH&E analysis

AIRFRAME MRO TRENDS

ICF International | icfi.com © ICF SH&E 2013 26

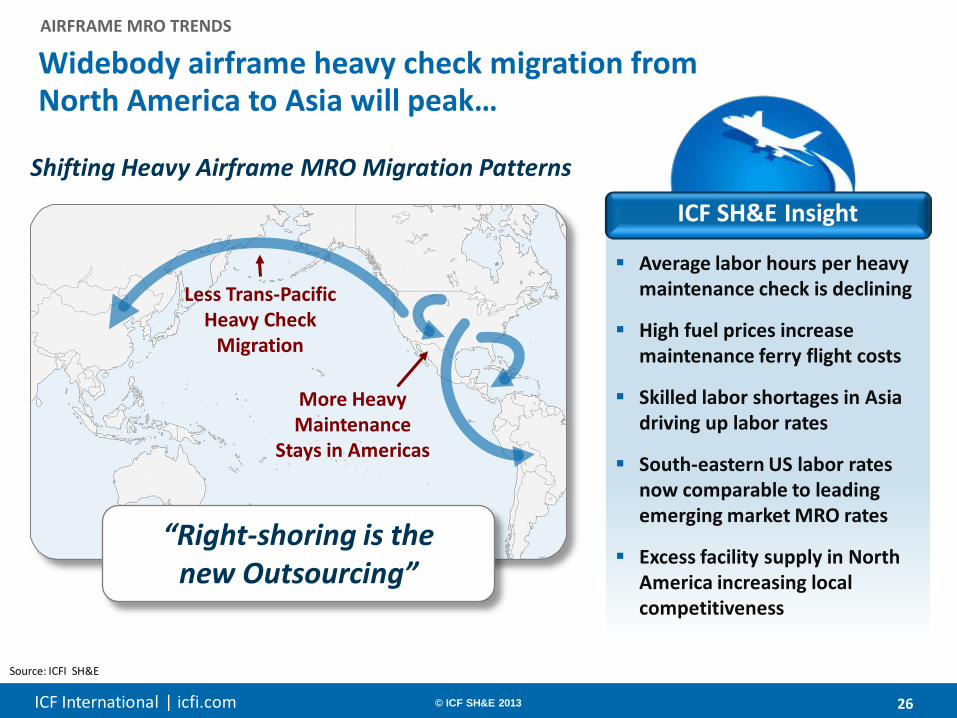

Widebody airframe heavy check migration from North America to Asia will peak…

Source: ICFI SH&E

Shifting Heavy Airframe MRO Migration Patterns

AIRFRAME MRO TRENDS

Average labor hours per heavy maintenance check is declining

High fuel prices increase maintenance ferry flight costs

Skilled labor shortages in Asia driving up labor rates

South-eastern US labor rates now comparable to leading emerging market MRO rates

Excess facility supply in North America increasing local competitiveness

ICF SH&E Insight

Less Trans-Pacific Heavy Check

Migration

More Heavy Maintenance

Stays in Americas

“Right-shoring is the new Outsourcing”

ICF International | icfi.com © ICF SH&E 2013 27

….and as a result, we will see continued investment activity in the airframe MRO sector

AIRFRAME MRO TRENDS

ICF International | icfi.com © ICF SH&E 2013 28

Five key MRO industry trends to watch…

Source: ICF SH&E

Industry Trends

MRO INDUSTRY TRENDS

3-D Printing

Energy & Aviation

Convergence

M&A in MRO

Surplus Parts

Airframe MRO

ICF International | icfi.com © ICF SH&E 2013 29

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

The GE Aviation-Parker Aerospace joint venture will 3-D print more than 30,000 LEAP-X fuel nozzles per year by 2017

ICF International | icfi.com © ICF SH&E 2013 30

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

HEICO is using 3-D printers to produce PMA part prototypes as well as tooling fixtures

ICF International | icfi.com © ICF SH&E 2013 31

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

Boeing is using 3-D printing to fabricate plastic interior parts for prototypes and test evaluation units

ICF International | icfi.com © ICF SH&E 2013 32

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

NASA has certified a 3-D printer to be used on the International Space Station in 2014

ICF International | icfi.com © ICF SH&E 2013 33

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

China’s AVIC heavy machinery is using large 3-D printed titanium parts for landing gear and other structural related parts.

ICF International | icfi.com © ICF SH&E 2013 34

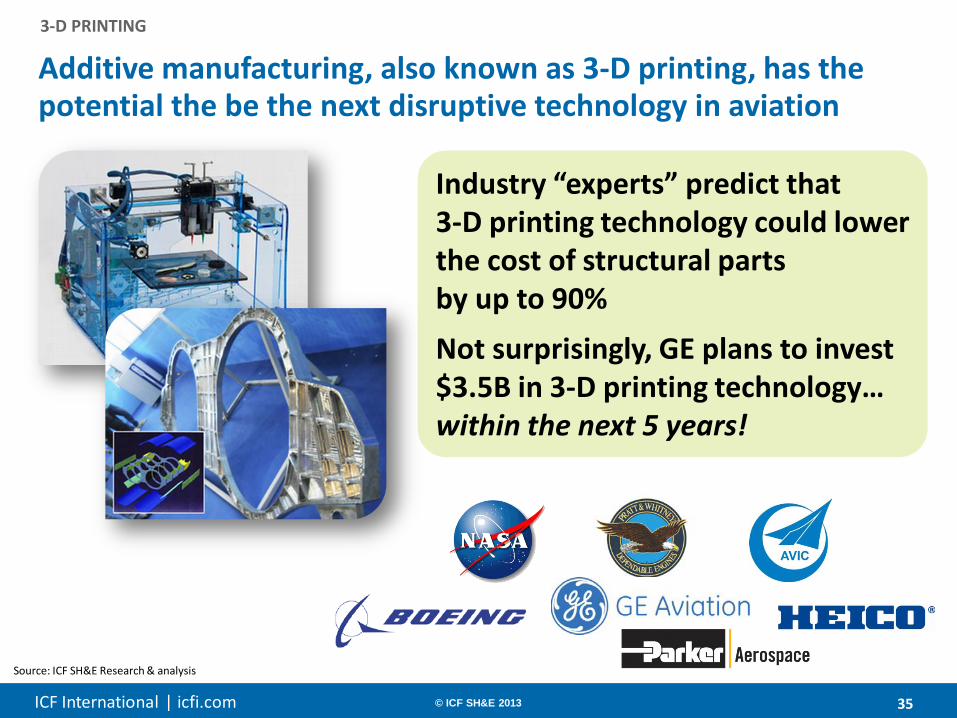

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

Pratt & Whitney will feature 25 different 3-D printed parts in its next generation GTF engine family

ICF International | icfi.com © ICF SH&E 2013 35

Additive manufacturing, also known as 3-D printing, has the potential the be the next disruptive technology in aviation

3-D PRINTING

Source: ICF SH&E Research & analysis

Industry “experts” predict that 3-D printing technology could lower the cost of structural parts by up to 90% Not surprisingly, GE plans to invest $3.5B in 3-D printing technology… within the next 5 years!

ICF International | icfi.com 36 © ICF SH&E 2013 36

Thank you!

MRO Market Research & Analysis

M&A Commercial Due Diligence

Aerospace Manufacturing Strategy

Aviation Asset Valuations & Appraisals

MRO Cost & Performance Benchmarking

MRO Information Technology (IT) Assessment

MRO Strategic Sourcing Support

Supply Chain Management

LEAN Continuous Process Improvement

Military Aircraft Sustainment

ICF SH&E’s MRO advisory services include the following:

ICF International | icfi.com © ICF SH&E 2013 37

ICF SH&E is one of the most experienced global aviation and aerospace consultancies

50 years in business (founded 1963) 100+ professional staff

− Dedicated exclusively to aviation and aerospace − Recruited from the industry

Specialized, focused expertise and proprietary knowledge Broad functional capabilities More than 8,000 private sector and public sector assignments Backed by parent company ICF International ($937M revenue) Global presence –– seven major offices

New York • Boston • Ann Arbor • London • Singapore • Beijing • Hong Kong

Airports • Airlines • Aerospace & MRO • Asset Advisory • Safety & Security

ICF International | icfi.com © ICF SH&E 2013 38

ICF International delivers professional services and technology solutions in three focus areas, which ICF SH&E draws upon, further expanding its service offerings and technology solutions

One of ICF's founders and its first president was a Tuskegee Airman. C.D. "Lucky" Lester flew more than 90 missions and earned the Distinguished Flying Cross. In 1969, "Lucky" and 3 DoD analysts founded the organization that is now ICF International.

$937M Revenues 4,500+ Employees ICFI NASDAQ

Energy Environment Transportation

Health, Social Programs, and Consumer/Financial

Public Safety and Defense

ICF International | icfi.com © ICF SH&E 2013 39

Jonathan M. Berger Vice President

icfi.com