57

3 - 1 Copyright 2003 Pearson Education Canada Inc. CHAPTER 3 Professio nal Ethics

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | barrie-rogers |

| View: | 225 times |

| Download: | 2 times |

3 - 1Copyright 2003 Pearson Education Canada Inc.

CHAPTER 3Professional

Ethics

3 - 2Copyright 2003 Pearson Education Canada Inc.

professional ethics

personal morals= ?

3 - 3Copyright 2003 Pearson Education Canada Inc.

professional ethics

personal morals=

3 - 4Copyright 2003 Pearson Education Canada Inc.

function of

?

professional ethics

personal morals=

3 - 5Copyright 2003 Pearson Education Canada Inc.

function of: - nature of the profession- collective morals- regulatory & legal constraints

professional ethics

personal morals=

3 - 6Copyright 2003 Pearson Education Canada Inc.

function of: - nature of the profession- collective morals- regulatory & legal constraints

functionof:

?

professional ethics

personal morals=

3 - 7Copyright 2003 Pearson Education Canada Inc.

function of: - nature of the profession- collective morals- regulatory & legal constraints

function of:- religious faith- family’s values- morals of peers- experiences- personality: selfish/altruistic

professional ethics

personal morals=

3 - 8Copyright 2003 Pearson Education Canada Inc.

personal

professional ethics

The profession hopes that individualThe profession hopes that individualpractitioners will absorb the profession’spractitioners will absorb the profession’s ethics into their personal morals.ethics into their personal morals.

morals

3 - 9Copyright 2003 Pearson Education Canada Inc.

Basic ethics principlesBasic ethics principlesare universal, regardless of religiousaffiliation, culture, background, etc.

3 - 10Copyright 2003 Pearson Education Canada Inc.

Basic ethics principlesBasic ethics principlesEXAMPLE: Our class finds itself on a desert island with no hope of escape. What societal rules do we need?

3 - 11Copyright 2003 Pearson Education Canada Inc.

Basic ethics principlesBasic ethics principles- be honest- have integrity- keep your promises- be faithful and loyal- be fair- care for others- respect others- be a responsible citizen- pursue excellence- be accountable

3 - 12Copyright 2003 Pearson Education Canada Inc.

Why do people Why do people obeyobey rules? rules?

3 - 13Copyright 2003 Pearson Education Canada Inc.

Why do people Why do people obeyobey rules? rules?

- personal integrity “I said I would obey the rules,and I will.”

3 - 14Copyright 2003 Pearson Education Canada Inc.

Why do people Why do people obeyobey rules? rules?

- personal integrity“I said I would obey the rules, And I will.”

- utilitarianism “If we all obey the rules, we willall benefit.”

3 - 15Copyright 2003 Pearson Education Canada Inc.

Why do people Why do people obeyobey rules? rules?

- personal integrity“I said I would obey the rules, and I will.”

- utilitarianism “If we all obey the rules, we willall benefit.”

- fear of consequences“If I break the rules, I may be punished.”

3 - 16Copyright 2003 Pearson Education Canada Inc.

Why do people Why do people fail to obeyfail to obey rules? rules?

3 - 17Copyright 2003 Pearson Education Canada Inc.

- lack of personal integrity

Why do people Why do people fail to obeyfail to obey rules? rules?

3 - 18Copyright 2003 Pearson Education Canada Inc.

- lack of personal integrity- selfishness

Why do people Why do people fail to obeyfail to obey rules? rules?

3 - 19Copyright 2003 Pearson Education Canada Inc.

- lack of personal integrity- selfishness- rationalization

“everyone does it” “it’s not illegal” “I won’t get caught”

Why do people Why do people fail to obeyfail to obey rules? rules?

3 - 20Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethical dilemma?with an ethical dilemma?

3 - 21Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethical dilemma?with an ethical dilemma?

- obtain relevant facts

3 - 22Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethical dilemma?with an ethical dilemma?

- obtain relevant facts- identify ethical issues

3 - 23Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethics dilemma?with an ethics dilemma?

- obtain relevant facts- identify ethical issues- determine stakeholders

3 - 24Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethics dilemma?with an ethics dilemma?

- obtain relevant facts- identify ethical issues- determine stakeholders- identify alternatives

3 - 25Copyright 2003 Pearson Education Canada Inc.

What do you do when confronted What do you do when confronted with an ethics dilemma?with an ethics dilemma?

- obtain relevant facts- identify ethical issues- determine stakeholders- identify alternatives- identify consequences of alternatives on stakeholders

3 - 26Copyright 2003 Pearson Education Canada Inc.

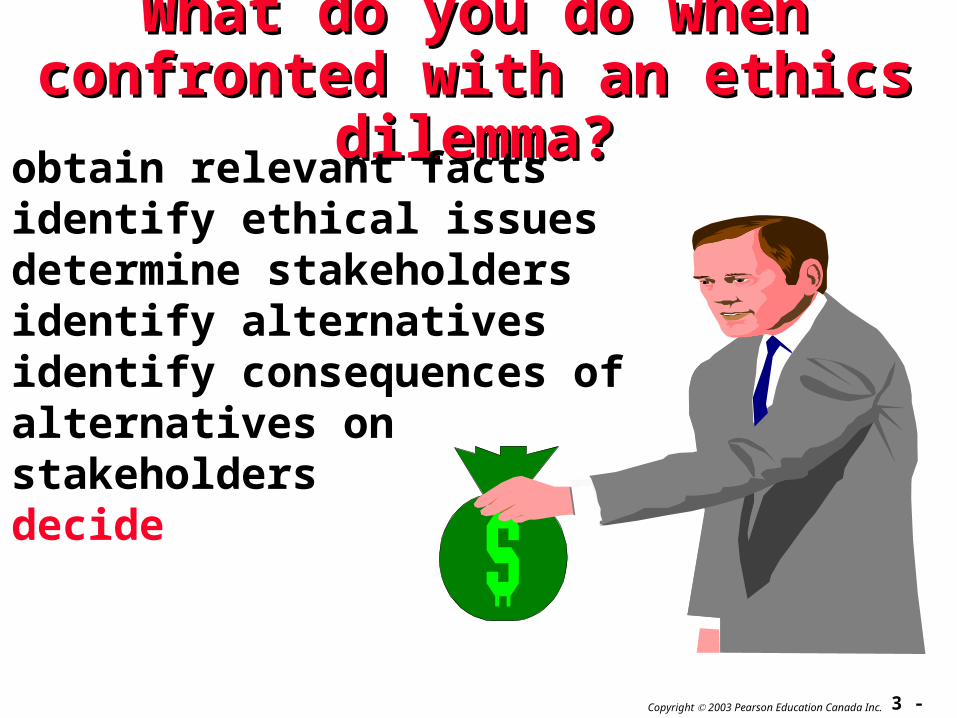

What do you do when confronted What do you do when confronted with an ethics dilemma?with an ethics dilemma?

- obtain relevant facts- identify ethical issues- determine stakeholders- identify alternatives- identify consequences of alternatives on stakeholders- decide

3 - 27Copyright 2003 Pearson Education Canada Inc.

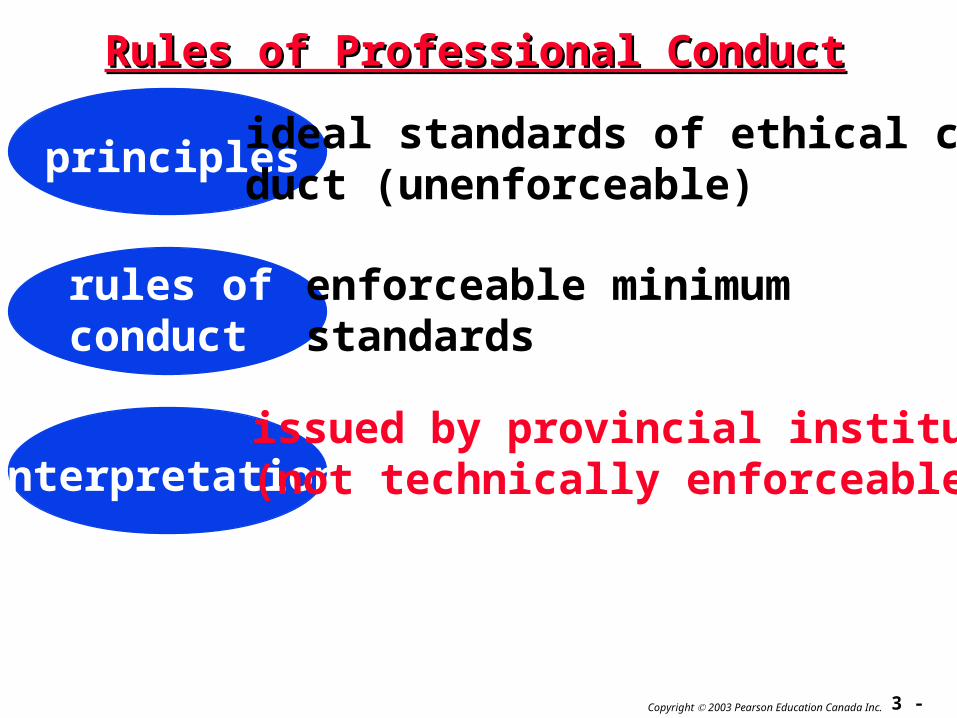

Rules of Professional ConductRules of Professional Conduct

principlesideal standards of ethical con-duct (unenforceable)

3 - 28Copyright 2003 Pearson Education Canada Inc.

Rules of Professional ConductRules of Professional Conduct

principles

rules ofconduct

enforceable minimum standards

ideal standards of ethical con-duct (unenforceable)

3 - 29Copyright 2003 Pearson Education Canada Inc.

Rules of Professional ConductRules of Professional Conduct

principles

rules ofconduct

interpretationsissued by provincial institutes(not technically enforceable)

ideal standards of ethical con-duct (unenforceable)

enforceable minimum standards

3 - 30Copyright 2003 Pearson Education Canada Inc.

Rules of Professional Rules of Professional ConductConduct

IndependenceIndependenceA member in public accounting mustbe independent in the performanceof certain professional services (audits,reviews, other attestation functions;not tax returns, compilations, manage-ment consulting).

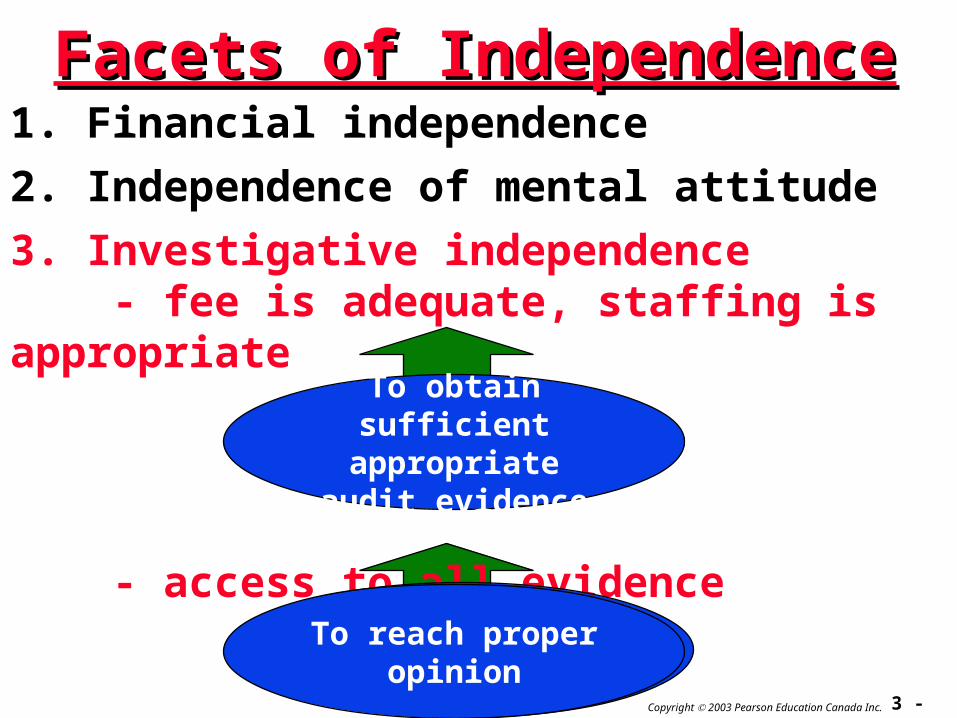

3 - 31Copyright 2003 Pearson Education Canada Inc.

Facets of IndependenceFacets of Independence1. Financial independence - not having a financial interest in the client

3 - 32Copyright 2003 Pearson Education Canada Inc.

Facets of IndependenceFacets of Independence1. Financial independence

2. Independence of mental attitude - professional skepticism

3 - 33Copyright 2003 Pearson Education Canada Inc.

1. Financial independence

2. Independence of mental attitude

3. Investigative independence - fee is adequate, staffing is appropriate

- access to all evidence

Facets of IndependenceFacets of Independence

To obtain sufficient appropriate audit

evidence

To reach proper opinion

To reach proper opinion

3 - 34Copyright 2003 Pearson Education Canada Inc.

Facets of IndependenceFacets of Independence1. Financial independence

2. Independence of mental attitude

3. Investigative independence

4. Reporting independence

Ensures report is acted on

3 - 35Copyright 2003 Pearson Education Canada Inc.

Confidential Client InformationConfidential Client Information

A member in public practice shall notdisclose any confidential client (oremployer) information without thespecific consent of the client (oremployer). Confidential / inside infor-mation can’t be used to benefit themember.

3 - 36Copyright 2003 Pearson Education Canada Inc.

Confidential Client InformationConfidential Client InformationA member in public practice shall notdisclose any confidential client informa-tion without the specific consent of the client.

What are the What are the exceptionsexceptions??

3 - 37Copyright 2003 Pearson Education Canada Inc.

A member in public practice shall notdisclose any confidential client informa-tion without the specific consent of the client...

What are the What are the exceptionsexceptions??- subpoena or summons (court)

Confidential Client InformationConfidential Client Information

3 - 38Copyright 2003 Pearson Education Canada Inc.

A member in public practice shall notdisclose any confidential client informa-tion without the specific consent of the client...

What are the What are the exceptionsexceptions??- subpoena or summons (court)- disciplinary proceedings

Confidential Client InformationConfidential Client Information

3 - 39Copyright 2003 Pearson Education Canada Inc.

A member in public practice shall notdisclose any confidential client informa-tion without the specific consent of the client...

What are the What are the exceptionsexceptions??- subpoena or summons (court)- disciplinary hearings- practice inspections

Confidential Client InformationConfidential Client Information

3 - 40Copyright 2003 Pearson Education Canada Inc.

Integrity and Due CareIntegrity and Due Care

In the performance of any professionalservice, a member shall maintain integrity (reputation for honesty) and use due care (application of appropriatelevel of care and skill for comparabletrained professional).

3 - 41Copyright 2003 Pearson Education Canada Inc.

CompetenceCompetence

A member shall maintain his / herprofessional competence. Undertakeonly those professional services that themember or the member’s firm can rea-sonably expect to be completed withprofessional competence.

3 - 42Copyright 2003 Pearson Education Canada Inc.

Adherence to GAAS & GAAPAdherence to GAAS & GAAP

- A member shall comply with the pro- fessional standards in the CICA Handbook.

3 - 43Copyright 2003 Pearson Education Canada Inc.

- A member shall comply with the pro- fessional standards in the CICA Handbook. - A member shall not be associated with false or misleading financial infor- mation.

Adherence to GAAS & GAAPAdherence to GAAS & GAAP

3 - 44Copyright 2003 Pearson Education Canada Inc.

Advertising & SolicitationAdvertising & Solicitation

- Solicitation of another’s client is prohibited.

3 - 45Copyright 2003 Pearson Education Canada Inc.

Advertising & SolicitationAdvertising & Solicitation

- Solicitation of another’s client is prohibited.

- Advertising which is not in good taste is prohibited.

3 - 46Copyright 2003 Pearson Education Canada Inc.

Breaches of Rules of Breaches of Rules of Professional ConductProfessional Conduct

A member who is aware of a breach by another member must report the breach tothe disciplinary committee after advising themember of the intent to make a report.

3 - 47Copyright 2003 Pearson Education Canada Inc.

Contingent FeesContingent Fees

A member in public practice shall not chargea fee contingent on the outcome of an audit,review or compilation.

3 - 48Copyright 2003 Pearson Education Canada Inc.

Contingent FeesContingent Fees

For what typesof engagements may

contingent fees bepermitted?

3 - 49Copyright 2003 Pearson Education Canada Inc.

Contingent FeesContingent Fees

business and consulting services

For what typesof engagements may

contingent fees bepermitted?

3 - 50Copyright 2003 Pearson Education Canada Inc.

Communication withCommunication withPredecessor AuditorPredecessor Auditor

Any circumstanceswhich should prevent

successorfrom accepting?

A member shall communicate with thepredecessor auditor prior to acceptingan appointment.

3 - 51Copyright 2003 Pearson Education Canada Inc.

If public accountants comply with all If public accountants comply with all of the Rules of Conduct, are they of the Rules of Conduct, are they

assured that they have not violated assured that they have not violated anyany accounting ethics rules? accounting ethics rules?

3 - 52Copyright 2003 Pearson Education Canada Inc.

If public accountants comply with all If public accountants comply with all of the Rules of Conduct, are they of the Rules of Conduct, are they

assured that they have not violated assured that they have not violated anyany accounting ethics rules? accounting ethics rules?

YES!

3 - 53Copyright 2003 Pearson Education Canada Inc.

Who must comply with the Who must comply with the Rules of Professional Rules of Professional

Conduct?Conduct?all

accountants?

all publicaccountants?

3 - 54Copyright 2003 Pearson Education Canada Inc.

Not all rules are applicable formembers not in public practice.

allmembers

Who must comply with the Who must comply with the Rules of Professional Rules of Professional

Conduct?Conduct?

3 - 55Copyright 2003 Pearson Education Canada Inc.

What happens if a member What happens if a member violates the Rules of violates the Rules of

Professional Conduct?Professional Conduct?

ROPC

3 - 56Copyright 2003 Pearson Education Canada Inc.

- someone may know of the violation and report it to the Institute

VIOLATION!

What happens if a member What happens if a member violates the Rules of violates the Rules of

Professional Conduct?Professional Conduct?

3 - 57Copyright 2003 Pearson Education Canada Inc.

- someone may know of the violation and report it to the Institute

- the Institute may investigate and may prescribe discipline; possible sanctions include required CPE, publication, fines, suspension, or expulsion

What happens if a member What happens if a member violates the Rules of violates the Rules of

Professional Conduct?Professional Conduct?