Completion Report Project Number: 35242-013 Loan Numbers: 2188-BAN/2189-BAN(SF) Grant: 0019 July 2019 Bangladesh: Gas Transmission and Development Project This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

Transcript

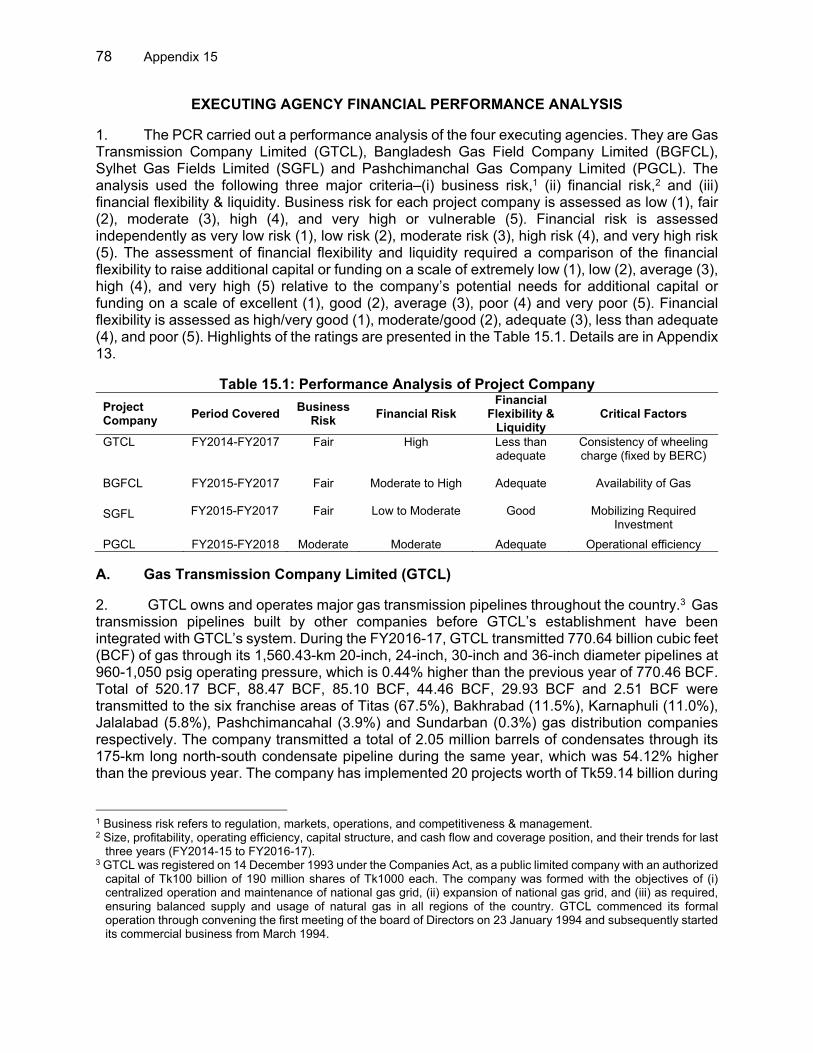

Completion Report

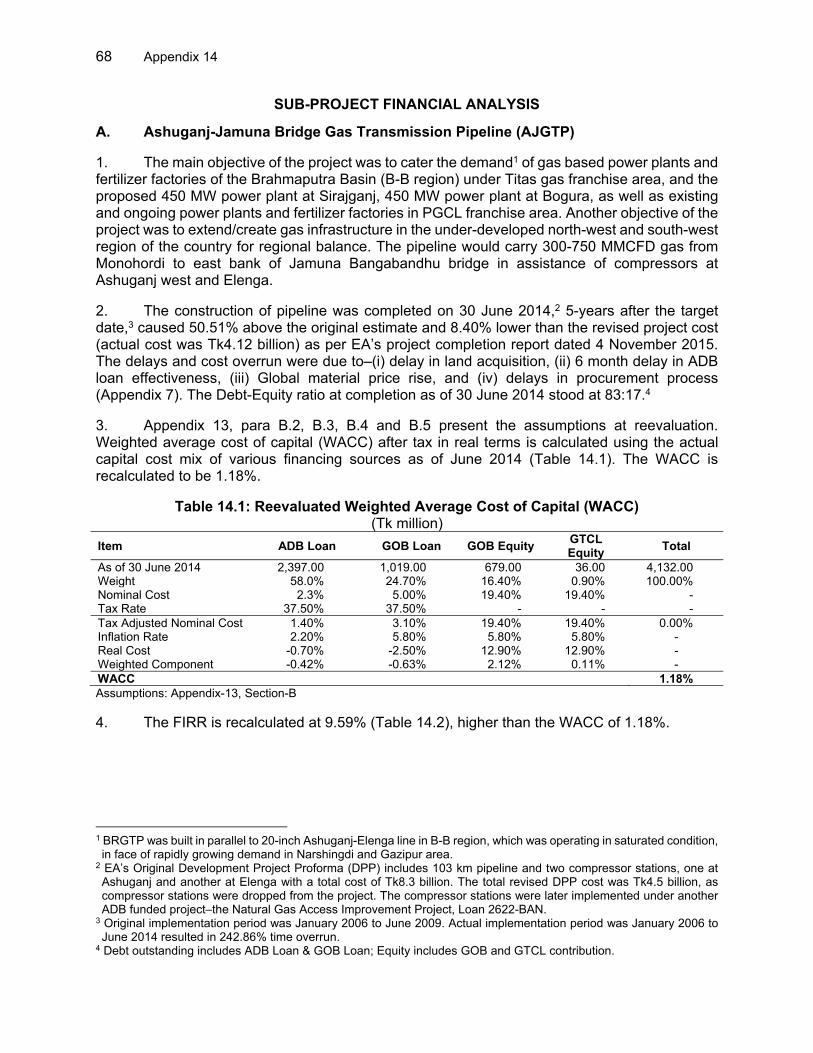

Project Number: 35242-013 Loan Numbers: 2188-BAN/2189-BAN(SF) Grant: 0019 July 2019

Bangladesh: Gas Transmission and Development Project This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

CURRENCY EQUIVALENTS

Currency unit – taka (Tk) At Appraisal At Project Completion (16 May 2005) (31 December 2016)

Tk1.00 = $0.06 $0.01 $1.00 = Tk64.45 Tk78.70

ABBREVIATIONS

ADB – Asian Development Bank BAPEX – Bangladesh Petroleum Exploration and Production Company Limited BERC – Bangladesh Energy Regulatory Commission BGFCL – Bangladesh Gas Fields Company Limited CCPP – combined cycle power plant CNG – compressed natural gas DMF – design and monitoring framework EMP – environmental management plan EMR – environmental management report EMRD – Energy and Mineral Resources Division EVC – electronic volume corrector GTCL – Gas Transmission Company Limited GTP – gas transmission pipeline HCU – Hydrocarbon Unit LNG – liquefied natural gas O&M – operation and maintenance OCR – ordinary capital resources PGCL – Pashchimanchal Gas Company Limited PCR – project completion report RRP – report and recommendation of the President SCADA – supervisory control and data acquisition SDR – special drawing rights SGFL – Sylhet Gas Fields Limited TGTDCL – Titas Gas Transmission and Distribution Company Limited WACC – weighted average cost of capital

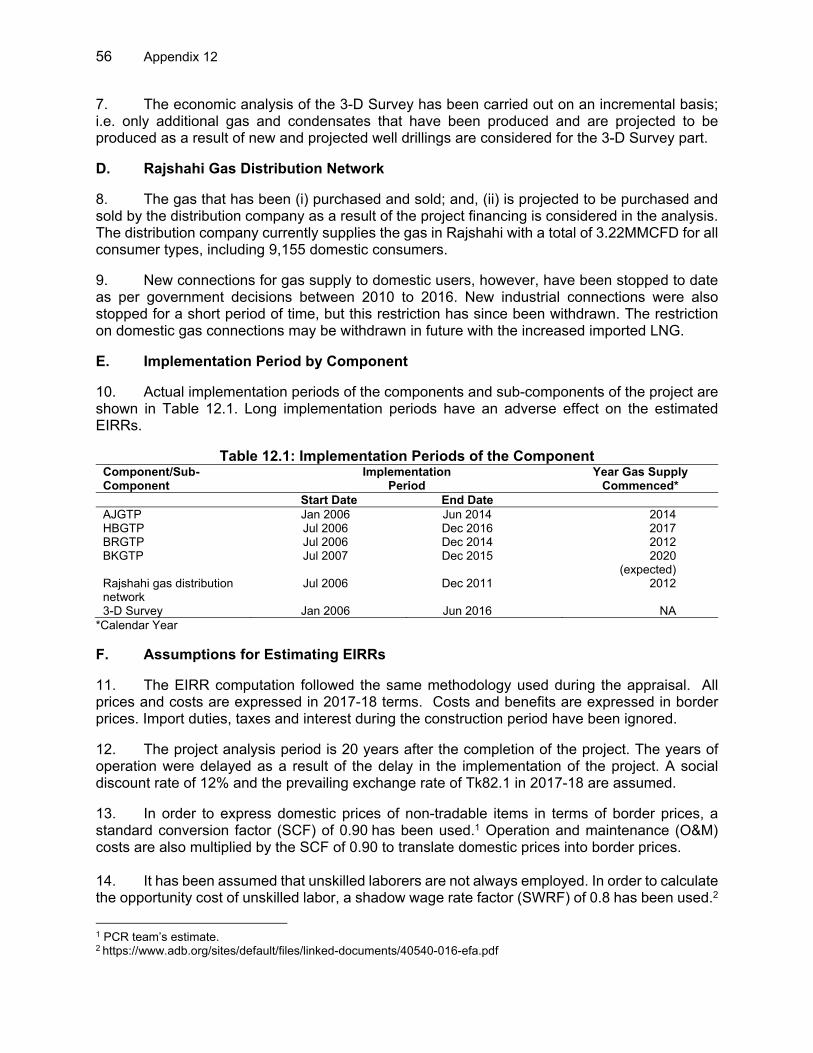

WEIGHTS AND MEASURES BCF – billion cubic feet km – kilometer MMBTU – million British thermal unit MCF – million cubic feet MMCFD – million cubic feet per day MW – megawatt TCF – trillion cubic feet

NOTES (i) The fiscal year (FY) of the government and its agencies ends on 30 June. FY before a

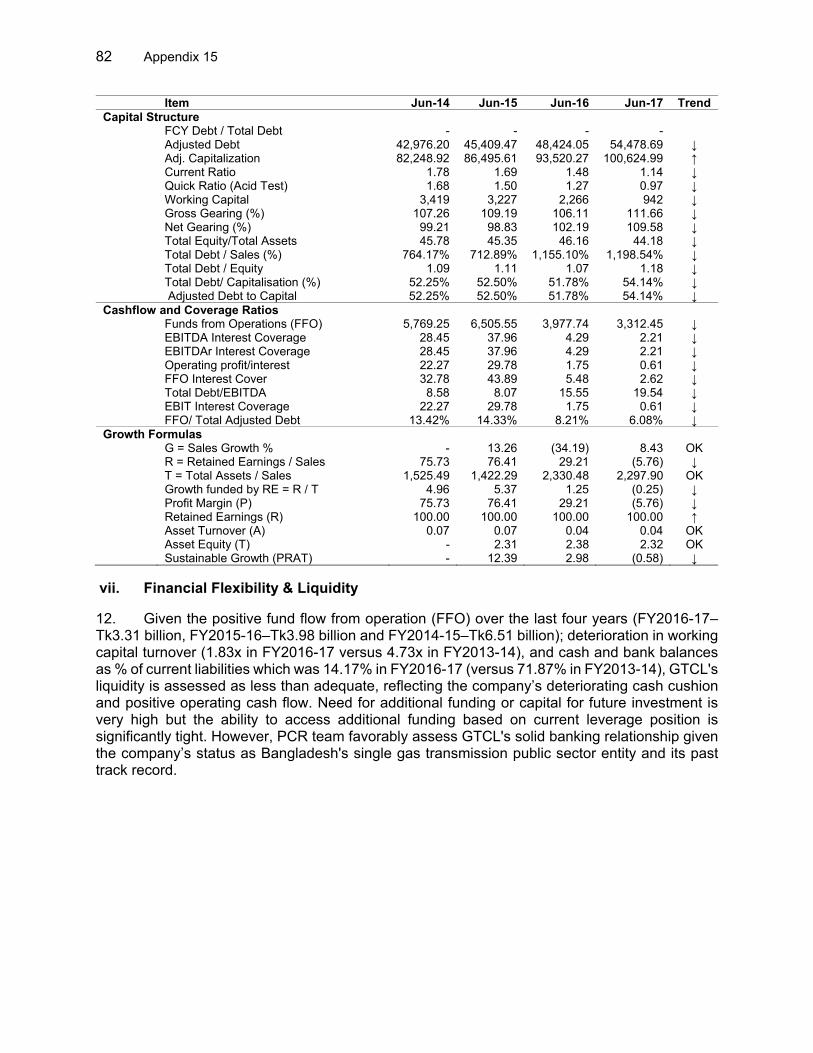

calendar year denotes the year in which the fiscal year ends, e.g., FY2018 ends on 30 June 2018.

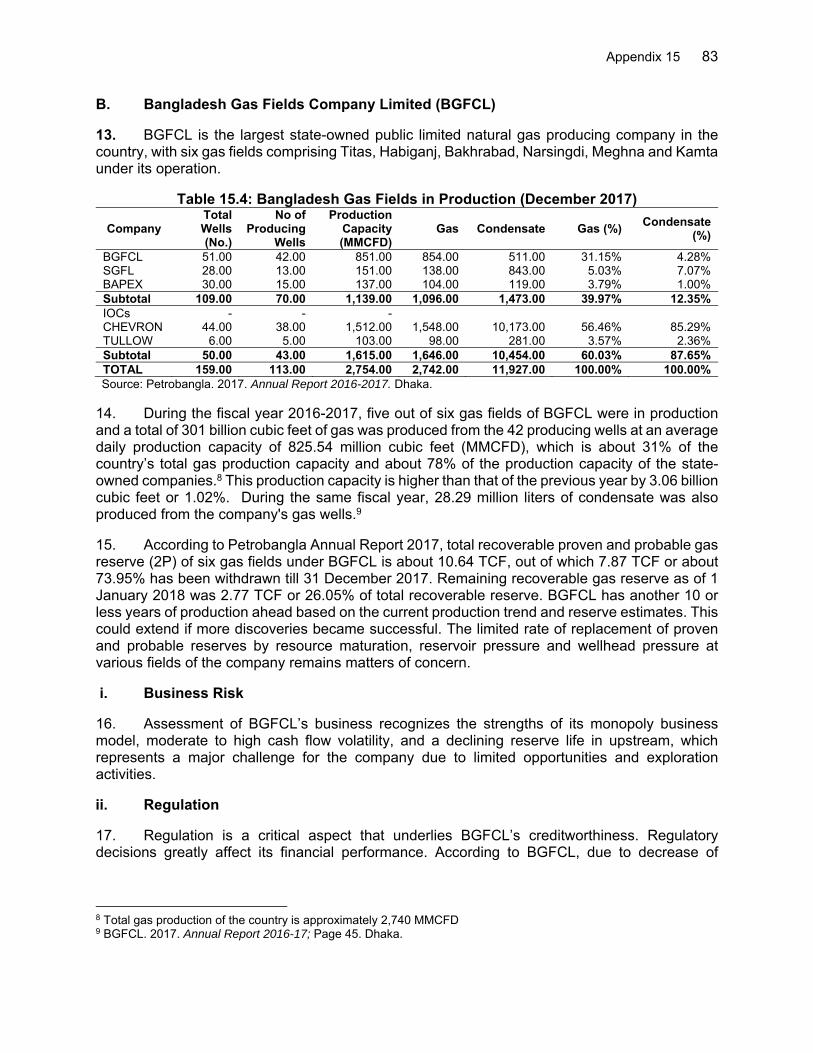

(ii) In this report, "$" refers to US dollars.

Vice-President Shixin Chen, Vice President, Operations 1 Director General Hun Kim, South Asia Department (SARD) Director

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS Page

BASIC DATA i MAP vii I. PROJECT DESCRIPTION 1 II. DESIGN AND IMPLEMENTATION 2

A. Project Design and Formulation 2 B. Project Outputs 3 C. Project Costs and Financing 7 D. Disbursements 7 E. Project Schedule 7 F. Implementation Arrangements 8 G. Consultant Recruitment and Procurement 8 H. Gender Equity 9 I. Safeguards 9 J. Monitoring and Reporting 10

III. EVALUATION OF PERFORMANCE 11 A. Relevance 11 B. Effectiveness 12 C. Efficiency 12 D. Sustainability 13 E. Development Impact 14 F. Performance of the Borrower and the Executing Agency 14 G. Performance of Cofinancier 14 H. Performance of the Asian Development Bank 14 I. Overall Assessment 14

IV. ISSUES, LESSONS, AND RECOMMENDATIONS 15 A. Issues and Lessons 15 B. Recommendations 15

APPENDIXES

1. Design and Monitoring Framework 16

2. Project Cost at Appraisal and Actual 19

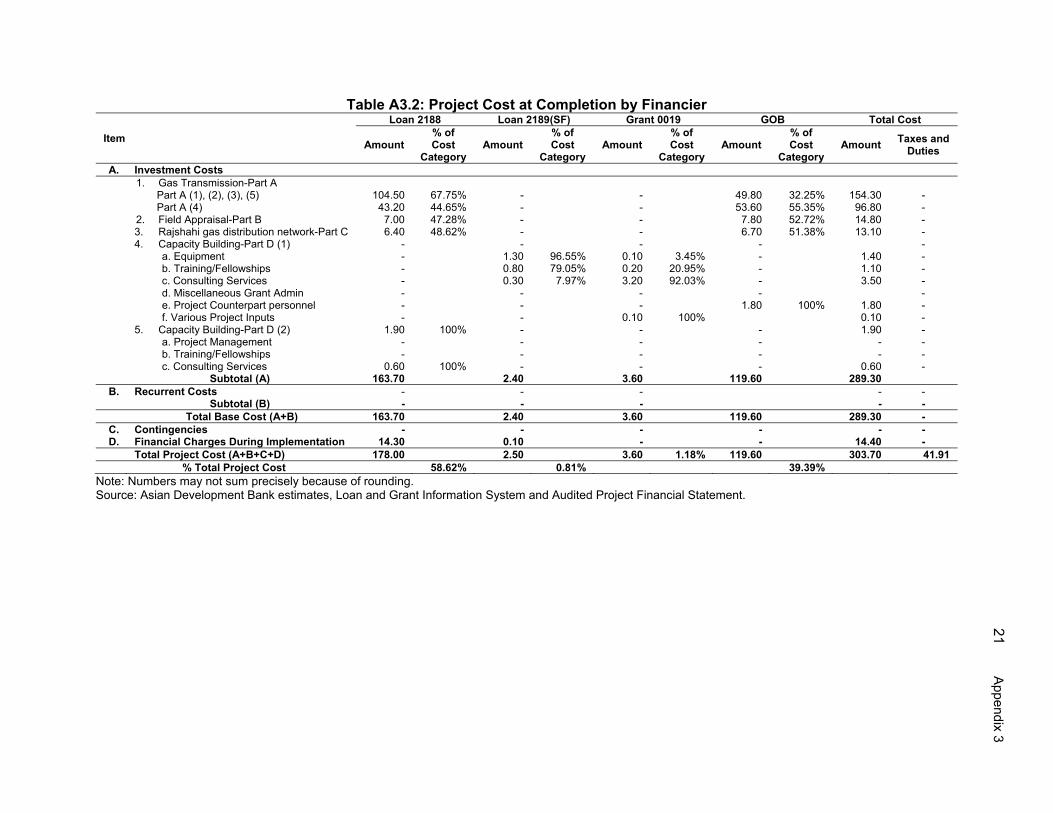

3. Project Cost by Financier 20

4. Disbursement of ADB Loan Proceeds 22

5. Implementation Schedule: Planned versus Actual 23

6. Contract Awards of ADB Loan Proceeds 24

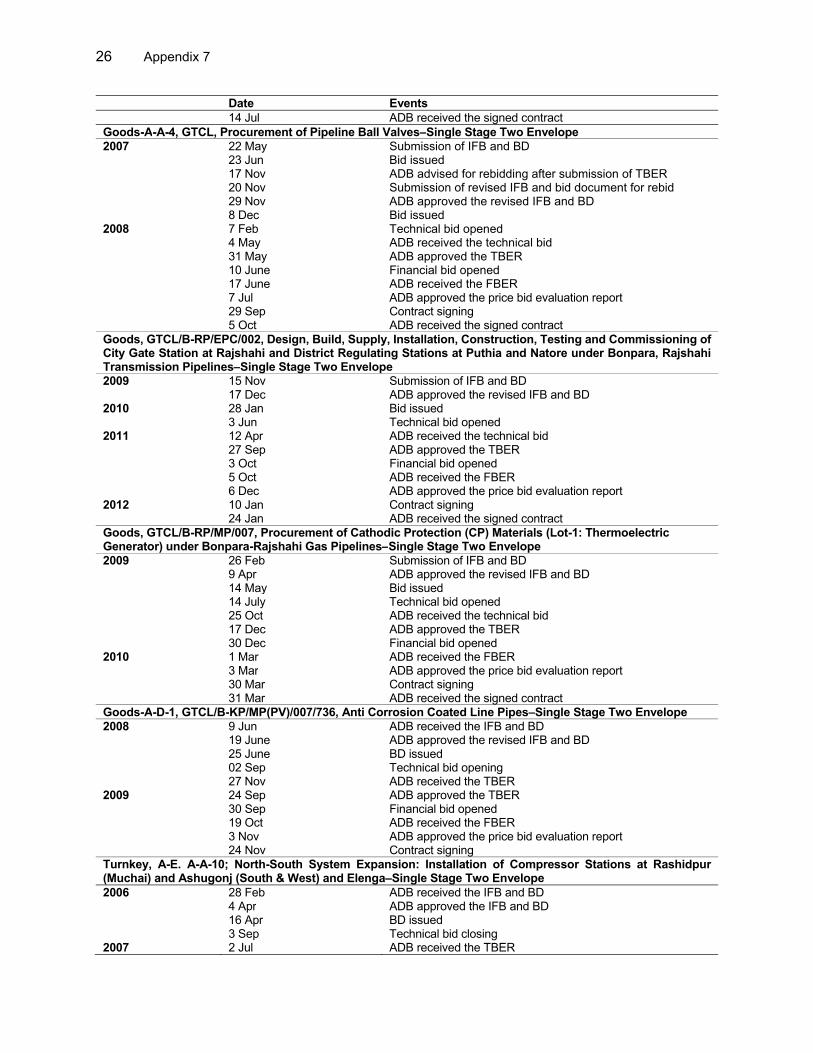

7. Chronology of Main Events 25

8. Implementation of Safeguards 30

9. Status of Compliance with Loan Covenants 32

10. Weighting Factors to Determine Project Effectiveness 45

1. Country Bangladesh 2. Loan number and financing source 2188-BAN(OCR)/2189-BAN(SF)

Grant number 0019-BAN 3. Project title Gas Transmission and

Development Project 4. Borrower People’s Republic of Bangladesh 5. Executing agency Part-A: Gas Transmission Company

Limited (GTCL), Part-B: Bangladesh Gas Fields Company Limited (BGFCL) and the Sylhet Gas Fields Limited (SGFL) with Bangladesh Petroleum Exploration Company Limited (BAPEX) as implementing agency, Part-C: Pashchimanchal Gas Company Limited (PGCL), and Part-D: Petrobangla (including Grant 0019) in coordination with the Energy and Mineral Resources Division (EMRD) of the Ministry of Power, Energy and Mineral Resources and other concerned entities.

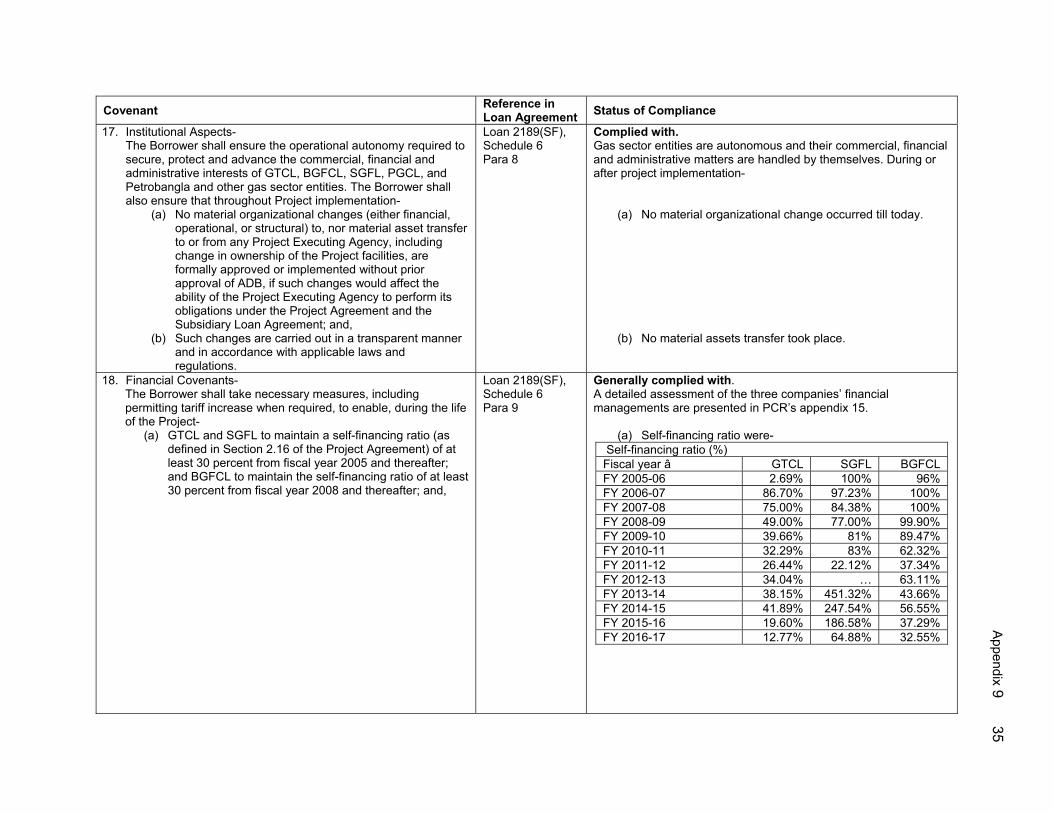

6. Amount of loan and grant

Loan 2188-BAN US$225,000,000 Loan 2189-BAN(SF) SDR3,401,000 Grant 0019-BAN US$5,000,000

7. Financing modality Project Lending B. Loan and Grant Data

1. Appraisal

– Date started 16 May 2005 – Date completed 23 May 2005

2. Loan and grant negotiations

– Date started 19 September 2005 – Date completed 20 September 2005

3. Date of Board approval

– Loan 2188, Loan 2189 & Grant 0019 27 October 2005

4. Date of agreement – Loan 2188-BAN 18 June 2006 – Loan 2189-BAN (SF) 18 June 2006 – Grant 0019 11 October 2006

ii

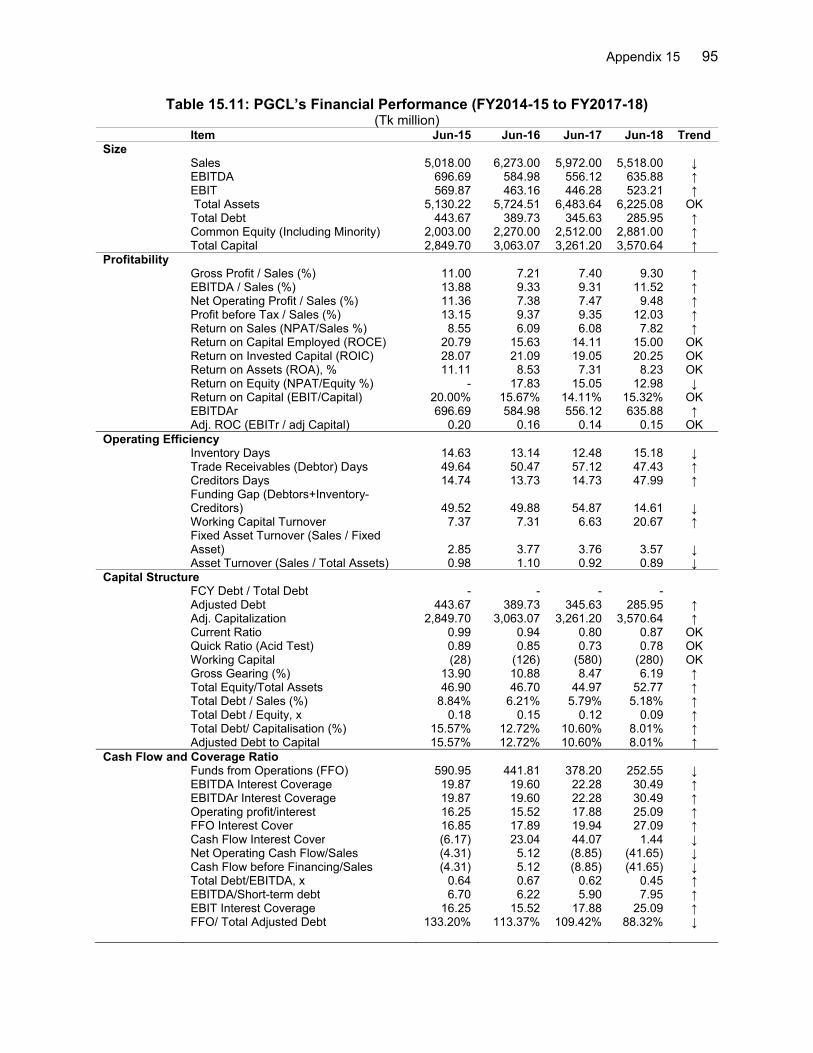

5. Date of loan or grant effectiveness Loan 2188-BAN

– In loan agreement 16 September 2006 (90 days) – Actual 28 November 2006 – Number of extensions 4

Loan 2189-BAN(SF)

– In loan agreement 16 September 2006 (90 days) – Actual 28 November 2006 – Number of extensions 4

Grant 0019

– In loan agreement 11 October 2006 – Actual 11 October 2006

6. Project completion date

Loan 2188-BAN – Appraisal 31 December 2010 – Actual 31 December 2016

Loan 2189-BAN(SF)

– Appraisal 31 December 2010 – Actual 31 December 2012

Grant 0019

– Appraisal 11 October 2011 – Actual 10 October 2013

7. Loan or grant closing date

Loan 2188-BAN – In loan agreement 31 December 2010 – Actual 31 December 2016 – Number of extensions 3

Loan 2189-BAN(SF)

– In loan agreement 31 December 2010 – Actual 31 December 2012 – Number of extension 1

Grant 0019

– In agreement 11 October 2011 – Actual 10 October 2013 – Number of extensions 2

8. Financial closing date

Actual – Loan 2188-BAN 18 May 2017 – Loan 2189-BAN(SF) 4 June 2013 – Grant 0019 13 February 2014

iii

9. Terms of loan Loan 2188-BAN

– Interest rate London Interbank offered rate (LIBOR) and 0.60%

– Maturity (number of years) 20 years – Grace period (number of years) 5 years

Loan 2189-BAN(SF)

– Interest rate 1% during grace period, thereafter 1.5% fixed

– Maturity (number of years) 32 years – Grace period (number of years) 8 years

10. Terms of Relending

Loan 2188-BAN – Interest rate 5% per annum – Maturity (number of years) 15 years – Grace period (number of years) 5 years – Second-step borrower (i) GTCL

(ii) SGFL (iii) BGFCL (iv) PGCL (v) Petrobangla

Loan 2189-BAN(SF)

– Interest rate 1% during grace period, thereafter 1.5% fixed

– Maturity (number of years) 32 years – Grace period (number of years) 8 years – Second-step borrower Petrobangla

11. Disbursements

a1. Dates: Loan 2188-BAN Initial Disbursement

30 April 2007 Final Disbursement

7 April 2017 Time Interval 119.80 months

Effective Date 28 November 2006

Actual Closing Date 18 May 2017

Time Interval 125.20 months

a2. Dates: Loan 2189-BAN(SF)

Initial Disbursement 28 January 2010

Final Disbursement 14 December 2012

Time Interval 34.50 months

Effective Date 28 November 2006

Actual Closing Date 4 June 2013

Time Interval 78.20 months

a3. Dates: Grant 0019

Initial Disbursement 27 May 2009

Final Disbursement 21 January 2014

Time Interval 55.00 months

Effective Date 11 October 2006

Actual Closing Date 13 February 2014

Time Interval 88.00 months

iv

b1. Amount: Loan 2188-BAN ($ million)

Category Original

Allocation (1)

Increased during

Implementation (2)

Canceled during

Implementation (3)

Last Revised

Allocation (4=1+2-3)

Amount Disbursed

(5)

Undisbursed Balance

(6=4-5)

1a. Part A (A1-A3, A5) 120.57 16.02 104.55 104.55 0 1b. Part A (A4) 43.93 0.71 43.22 43.22 0 2. Part B 12.36 5.37 6.99 6.99 0 3. Part C 8.57 2.22 6.35 6.35 0 4. Part D(II) 1.60 0.35 0 1.95 1.95 0 5. Project management 1.00 1.00 0 0 0 6. Training and fellowships 2.30 2.30 0 0 0 7. Consulting services 4.44 3.80 0.64 0.64 0 8. Interest and

commitment charge 16.80 2.47 14.33 14.33 0

9. Unallocated 13.43 13.43 0 0 0 Total in USD 225.00 0.35 47.32 178.03 178.03 0

Note. $26.801 million was cancelled on 19 August 2013 and $20.16 million on 18 May 2017.

b2. Amount: Loan 2189-BAN(SF) (SDR million)

Category

Original Allocation

(1)

Increased during

Implementation (2)

Canceled during

Implementation (3)

Last Revised

Allocation (4=1+2-3)

Amount Disbursed

(5)

Undisbursed Balance

(6=4-5)

1. Equipment 1.06 0.21 0.85 0.85 0 2. Training and fellowship 0.52 0.01 0.53 0.53 0 3. Consulting services 1.61 1.43 0.18 0.18 0 4. Interest 0.09 0.06 0.03 0.03 0 5. Unallocated 0.12 0.12 0 0 0 Total in SDR 3.40 0.01 1.82 1.59 1.59 0 Total in USD 5.00 0.17 2.71 2.46 2.46 0 Note. SDR1.08 million (equivalent $2.70 million) was cancelled on 4 June 2013.

b3. Amount: Grant 0019-BAN ($ million)

Category

Original Allocation

(1)

Increased during

Implementation (2)

Canceled during

Implementation (3)

Last Revised

Allocation (4=1+2-3)

Amount Disbursed

(5)

Undisbursed Balance

(6=4-5)

1. Equipment 0.40 0.30 0.10 0.10 0 2. Training and fellowship 0.70 0.50 0.20 0.20 0 3. Consulting services 2.40 0.80 0 3.20 3.20 0 4. Miscellaneous grant

administration 0.10 0.10 0 0 0

5. Project counterpart personnel

0.30 0.30 0 0 0

6. Various project input 1.10 1.00 0.10 0.10 Total in USD 5.00 0.80 2.20 3.60 3.60 0 C. Project Data

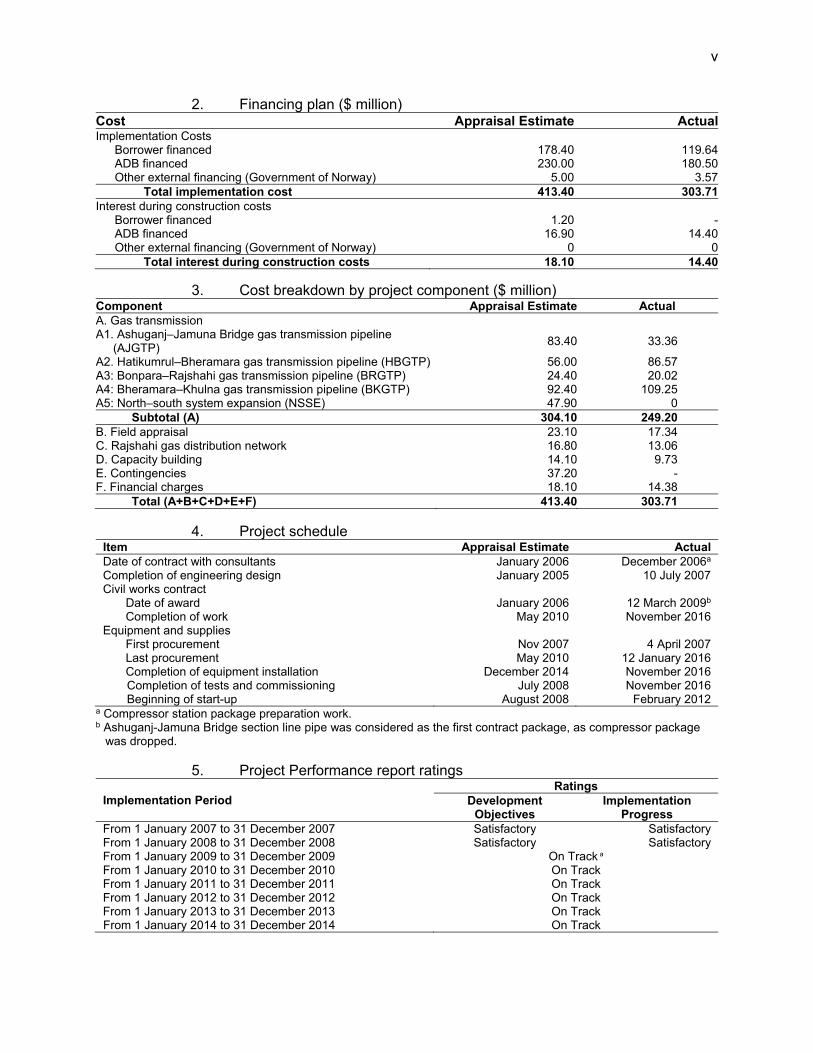

1. Project cost ($ million) Cost Appraisal Estimate Actual Foreign exchange cost 235.00 180.12 Local currency cost 178.40 123.60 Total 413.40 303.71

v

2. Financing plan ($ million) Cost Appraisal Estimate ActualImplementation Costs Borrower financed 178.40 119.64 ADB financed 230.00 180.50 Other external financing (Government of Norway) 5.00 3.57

Total implementation cost 413.40 303.71Interest during construction costs Borrower financed 1.20 - ADB financed 16.90 14.40 Other external financing (Government of Norway) 0 0

Total interest during construction costs 18.10 14.40

3. Cost breakdown by project component ($ million) Component Appraisal Estimate Actual A. Gas transmission A1. Ashuganj–Jamuna Bridge gas transmission pipeline

(AJGTP) 83.40 33.36

A2. Hatikumrul–Bheramara gas transmission pipeline (HBGTP) 56.00 86.57 A3: Bonpara–Rajshahi gas transmission pipeline (BRGTP) 24.40 20.02 A4: Bheramara–Khulna gas transmission pipeline (BKGTP) 92.40 109.25 A5: North–south system expansion (NSSE) 47.90 0

Subtotal (A) 304.10 249.20 B. Field appraisal 23.10 17.34 C. Rajshahi gas distribution network 16.80 13.06 D. Capacity building 14.10 9.73 E. Contingencies 37.20 - F. Financial charges 18.10 14.38

Total (A+B+C+D+E+F) 413.40 303.71

4. Project schedule Item Appraisal Estimate Actual Date of contract with consultants January 2006 December 2006a Completion of engineering design January 2005 10 July 2007 Civil works contract Date of award January 2006 12 March 2009b

Completion of work May 2010 November 2016 Equipment and supplies First procurement Nov 2007 4 April 2007 Last procurement May 2010 12 January 2016 Completion of equipment installation December 2014 November 2016

Completion of tests and commissioning July 2008 November 2016 Beginning of start-up August 2008 February 2012

a Compressor station package preparation work. b Ashuganj-Jamuna Bridge section line pipe was considered as the first contract package, as compressor package

was dropped.

5. Project Performance report ratings

Implementation Period Ratings

Development Objectives

Implementation Progress

From 1 January 2007 to 31 December 2007 Satisfactory Satisfactory From 1 January 2008 to 31 December 2008 Satisfactory Satisfactory From 1 January 2009 to 31 December 2009 On Track a From 1 January 2010 to 31 December 2010 On Track From 1 January 2011 to 31 December 2011 On Track From 1 January 2012 to 31 December 2012 On Track From 1 January 2013 to 31 December 2013 On Track From 1 January 2014 to 31 December 2014 On Track

vi

Implementation Period Ratings Development

Objectives Implementation

Progress From 1 January 2015 to 31 December 2015 On Track From 1 January 2016 to 31 December 2016 On Track

a ADB performance rating system changed during this time. D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons

No. of Person-

Days

Specialization of Members

Fact-finding 26 Feb–10 Mar 2005 4 10 b, g, h, a Appraisal mission 16–23 May 2005 3 6 b, g. a, Consultation mission 9–12 Oct 2005 2 4 b, d Loan inception mission 10–18 Jul 2006 3 7 g, e, b, d Review mission 1 11–15 Feb 2007 2 5 g, d Special project administration mission 17–19 Dec 2007 2 3 g, c Review mission 2 14–23 Sep 2008 1 8 g, f Review mission 3 (handover mission) 2–11 Feb 2009 2 8 g, c Review mission 4 17 Feb –11 Mar 2010 2 17 c, e Review mission 5 24 Oct–4 Nov 2010 2 10 d, e Review mission 6 5–18 Aug 2011 2 12 d, e Safeguard review mission 5-10 Mar 2011 2 5 g, h Review mission 7 14 Feb–4 Mar 2012 2 17 d, e Review mission 8 11–30 May 2013 4 17 d, g, h, e Review mission 9 1–18 Feb 2014 4 16 d, e, g, h, c Review mission 10 14–28 Nov 2016 3 13 d, e, c Project completion report mission 9–17 Dec 2018 3 6 d, e, h

a = counsel, b = economist, c = procurement consultant or specialist, d = project officer, e = analyst, f = staff consultant, g = specialist, h = safeguards officer.

vii

MAP

I. PROJECT DESCRIPTION 1. In 2005, the per capita gross domestic product of Bangladesh was $484, and the poverty rate was 40%. Only 44% of population had access to electricity at a per capita consumption of 171 kWh, one of the lowest in South Asia.1 Inadequate energy supply was a key constraint on economic development. Natural gas—although pivotal in the economy since 1973 and shared 70% of the country’s primary energy in 2005—was under-used compared to the immense potential of domestic reserves.2 Insufficient investment, inadequate infrastructure, low extraction, lack of commercial orientation in tariffs, and poor maintenance all drove the underdevelopment of country’s gas sector. Bangladesh needed investment in the gas sector to grow the economy and reduce poverty. 2. In 2005, the country’s natural gas demand was 1,350 million cubic feet per day (MMCFD) and projected to reach 2,420 MMCFD in 2015 and 3,785 MMCFD in 2025, with an annual growth of 7%–8%.3 At project appraisal, there was a net 105 MMCFD demand–supply gap for gas, with forecast to reach 249 MMCFD in 2016 and 4,421 MMCFD in 2025. To meet growing demand, in 2002 the Asian Development Bank (ADB) helped Petrobangla4 develop a $3 billion investment plan for 2002–2020 for the gas sector—for exploration, field development, transmission, and distribution—aligned with the national gas sector reform roadmap (GSRR).5 ADB designed the Gas Transmission and Development Project as part of Petrobangla’s investment plan. 3. On 27 October 2005, ADB approved the Gas Transmission and Development Project, 6 which comprised:

(i) Loan 2188-BAN for $225 million from ADB’s ordinary capital resources (OCR); (ii) Loan 2189-BAN(SF) for $5 million equivalent (SDR3.4 million) from ADB’s Special

Funds (SF); and (iii) Grant 0019-BAN for $5 million from the Government of Norway, administered by

ADB under a cofinancing arrangement. 4. The loan agreements were signed on 18 June 2006 and declared effective on 28 November 2006; the grant agreement was signed and declared effective on 11 October 2006. Project implementation closed physically on 31 December 2016, and financially on 18 May 2017. The projected impact was the increased pace of economic development and the projected outcome was the enhanced use of natural gas by residential, industrial, and commercial users. Project outputs included (i) improved and expanded gas transmission and distribution networks in the project area; (ii) gas field appraisal to update estimated reserves and determine exact

1 World Bank. Indicators. https://data.worldbank.org/indicator/. 2 Proven recoverable gas reserves from 22 fields were estimated at 20.4 trillion cubic feet (TCF) in 2005, of which 5.09 TCF were extracted. Excluding the 9 TCF estimated underdeveloped and undiscovered reserves, 15.31 TCF of recoverable reserve remained.

3 From 2002 to 2004, national gas consumption grew at an annual rate of 8%, preceded by steady annual growth rate of 7% in the previous decade.

4 Petrobangla is a department under the Ministry of Power, Energy and Mineral Resources and is responsible for the exploration and development of the oil, gas, and mineral resources of the country. 5 Government of Bangladesh, Ministry of Power, Energy and Mineral Resource, Energy and Mineral Resource Division. 2005. Gas Sector Reform Roadmap. GSRR was adopted in 2005 for a period of 5 years. It aimed to support an investment plan for 2002–2020. The roadmap covered: (i) institutional and financial restructuring of gas sector companies to ensure long term financial sustainability, (ii) strengthening public–private partnership in the gas sector aimed to create an environment for private sector led growth, (iii) transforming gas companies to diversify ownership involving private investors, (iv) restructuring and unbundling gas sector institutions and enterprises; and (v) market oriented energy pricing reflecting energy parity, eliminating noneconomic factors and levies. It was approved as a national plan in 2009. 6 ADB. 2005. Report and Recommendation of the President to the Board of Directors: Proposed Loans Gas Transmission and Development Project (Bangladesh). Manila.

2

location for future drilling activities; (iii) enhanced financial performance, governance, and efficiency indicators of the gas sector utilities through the GSRR’s capacity building and implementation; and (iv) improved air quality.

II. DESIGN AND IMPLEMENTATION A. Project Design and Formulation 5. The project design and formulation were aligned with the poverty reduction strategy paper prepared by the government and development partners in 2005. The strategy emphasized (i) enhancing gas production to properly use reserves and promote industrialization and (ii) expanding gas transmission infrastructure to less developed regions for balanced regional development and equitable distribution of benefits. The strategy targeted halving the poverty rate from 50% in 2000 to 25% in 2015. To attain the target, Bangladesh needed to accelerate poverty reduction at 3.3% during 2000–2015, which required raising annual economic growth from 5% in 2005 to 6%–7%, sustained over the next 15 years. 6. The project and the GSRR were part of Petrobangla’s $3 billion investment plan for 2002–2020 (para. 2) to develop Bangladesh’s gas resources—which provided almost 90% of input to power generation—and infrastructure to meet the rapidly growing commercial energy demand. The project envisaged necessary development of the natural gas sector and infrastructure and targeted replacing expensive and polluting fossil and biomass fuels with less polluting natural gas for industrial and commercial sectors. Considering the project’s well identified scope, its linkage with Petrobangla’s long-term investment plan and necessary reform agenda through GSRR, ADB chose a project lending modality. 7. The project design was consistent with ADB’s country strategy and program, 2004–2006 to promote domestic gas resources to replace imported fossil fuels and restructure the gas sector, allow full autonomy to gas sector entities, and deregulate and depoliticize tariff setting.7 Project covenants assured GSRR and loss reduction plan implementation. The project was consistent with ADB’s energy policy (1995) supporting balanced infrastructure investment, financially robust and efficient operations, deregulated energy markets, and private sector development.8 8. At appraisal, project implementation arrangements involved relevant agencies and planned necessary review processes. Thus, project design and formulation remained sound and adequate for the foreseen needs at appraisal for future gas transmission, distribution, sector reform, loss reduction, field appraisal, and capacity development. However, there were some changes in project scope during implementation due to the excessive increase in bid prices (paras. 10, 14 and 40). A major challenge during implementation was the severe gas supply shortage in the country amid the rapidly growing demand, as a series of drillings were unsuccessful starting from 2009. The energy crisis was experienced when construction of facilities under the project was already in full swing. To manage the situation, the 2010 National Power System Master Plan focused on expanding the gas network with more efficient power stations and constructing deep-sea ports to import liquified natural gas (LNG). The government formulated the Bangladesh Gas Act 2010 and Gas Development Fund Policy 2012 to enhance field exploration and equitable distribution. The government’s Seventh Five-Year Plan, 2016–2020 and 2016 Power System Master Plan targeted at least 33% power generation with natural gas by 2041, importing 4,000 MMCFD natural gas by 2041. The government has signed two long term LNG sales and purchase agreement with RasGas of Qatar and Oman Trading International in

7 ADB. 2004. Country Strategy and Program Update Bangladesh: 2004–2006. Manila. 8 ADB. 1995. Bank Policy for Energy Sector. Manila.

3

2011 on a government to government basis. In July 2018, Bangladesh began importing 500 MMCFD of LNG with the country’s first floating storage regassification unit (FSRU). Second FSRU for another 500 MMCFD LNG import capacity started to operate partially from early 2019. While the imported LNG helped meet growing industrial and commercial demand in the greater Chattogram division, most of the 2,700 MMCFD indigenous natural gas from the eastern region of the country is being transmitted to cater greater Dhaka and the western region’s demand. The transmission of indigenous natural gas requires networks developed by the project; hence, the project remains relevant at completion. While the gas supply shortage was unforeseen, the government is addressing the problem through several initiatives. The infrastructure established under the project will support gas supply from imports and indigenous sources. B. Project Outputs 9. The project had four outputs with eight indicators and, through its various parts (A–D), achieved seven out of eight (Appendix 1).9 Under output 1, improving gas transmission and the distribution network system, executed by Gas Transmission Company Limited (GTCL), the project achieved two out of three indicators: it (i) constructed 345 kilometers (km) of gas transmission line with an aggregate 342 MMCFD gas throughput (part A, components A1–A4), and (ii) constructed 270 km of gas distribution network (part C). The third indicator, installation of compressors at Ashuganj and Muchai (component A5) was dropped. Under output 2, the field appraisal, the project carried out seismic surveys in five gas fields as targeted (part B). Under output 3, enhancing the capacity of gas sector utilities, the project (part D) implemented the GSRR and helped (i) reduce system losses, (ii) efficiently operate and manage gas entities with the appropriate debt service and self-financing ratios, and (iii) achieve approval of policies such as the Bangladesh Gas Act of 2010, the Gas Development Fund Policy of 2012, and other regulations to streamline processes and attract private investment in liquified petroleum gas and LNG. Under output 4, air quality, the project installed distribution networks that helped households to shift from firewood to gas burners, which improved the ambient and indoor air quality (part C).

1. Part A: Gas Transmission Expansion and Reinforcement 10. A1: Ashuganj west–Jamuna Bridge east bank gas transmission pipeline. The project completed: (i) a 50.5 km, 30-inch-diameter transmission pipeline (appraisal estimate 51 km) in two sections from Monohardi to Dhanua through Narshingdi and Gazipur; and Elenga to Jamuna Bridge east bank through Tangail; (ii) a 1.004 km river crossing at Brahmaputra and Shitalakhya; and (iii) a metering and manifold station at Dhanua. Commercial operation began on 30 June 2014. The Ashuganj–Jamuna gas transmission pipeline (GTP) carries gas up to 342 MMCFD, against the appraisal estimate of 390 MMCFD.10 The project completed all scopes under this component except the compressor station at Ashuganj (west) and Elenga for throughput of 390 MMCFD, which was dropped because of an excessively high bid compared to the engineer’s estimate. It was later financed by another ADB project (para. 14). The project directly benefited commercial and industrial customers of Gazipur and Narshingdi and provided gas to four power plants totaling 1 gigawatt generation capacity at Sirajganj. Network use is expected to increase to full capacity once gas supply from the second FSRU reaches to 500 MMCFD within 2019. 11. A2: Hatikumrul–Ishwardi–Bheramara gas transmission pipeline. The project constructed 79.83 km (97% of the target 87 km) for Hatikumrul–Bheramara GTP with a 30-inch-

9 The outputs presented is based on the components outlined in RRP. The MAP shows the completed infrastructures. 10 The gas flow was recorded up to 420 MMCFD in 2014 but fell to 142 MMCFD after construction of a parallel 36-inch-

diameter 140 km pipeline from Bibiana gas field to Dhanua with government funding in 2015. The new pipeline affected Ashuganj–Jamuna GTP from 2015 to 2018, but use resumed from late 2018, after the LNG import began.

4

diameter pipe—larger than appraisal design (24-inch-diameter). It has increased the cost by $30 million. It included five river crossings at the Goja, Atrai, Borai, Khalishdanga, and Padma rivers. The pipeline and city gate station at Bheramara was completed in May 2013 but commercial operation was delayed until 27 November 2016 because of the delays in Padma river crossing. At Padma river, the first contractor failed in horizontal directional drilling because of hard rocks and, after failing in two attempts, it abandoned the site. A new contractor completed the job in November 2016 after a delay of 3 years. GTCL commissioned the city gate station at Bheramara for 68 MMCFD gas from May 2017, against the estimate of 235 MMCFD. Its capacity will be utilized once the LNG import reaches 1,000 MMCFD. Project beneficiaries include Bheramara 410 megawatt (MW) combined cycle power plant (CCPP), four ready-made garment factories, one battery and plastic factories in the Ishwardi export processing zone, several compressed natural gas (CNG) refueling stations, and residential customers of Ishwardi and Bheramara. 12. A3: Bonpara–Rajshahi gas transmission pipeline. The project constructed 53 km of 12.75-inch-diameter pipeline (106% of target 50 km of 12-inch-diameter); commercial operation began on 8 February 2012. The component included the Nandagoja river crossing, Rajshahi city gate station, and district regulating stations at Natore and Puthia. It connected Natore and the divisional cities of Rajshahi with natural gas for the first time. From 2012, the pipeline carried only 3–5 MMCFD gas against the target of 25–30 MMCFD. Suspension of new gas connections, unforeseen at appraisal, hampered the industrialization in project area, resulting in low gas uses.11 13. A4: Bheramara–Khulna gas transmission pipeline. The project constructed 162.5 km of 20-inch-diameter Bheramara–Khulna GTP (98% of target 165 km) on 31 July 2012. Six river crossings with length of 2.5 km, across Kumar, Nabaganga-I, Nabaganga-II, Chitra, Buribhairab and Begabati rivers were completed in December 2012. Major beneficiaries of the facilities include two ADB-funded projects–the Khulna CCPP, which is commissioned in June 2016, and Rupsha 800 MW CCPP, expected to start in June 2022. Utilization of pipeline has not yet started because of the delays in distribution pipeline construction (under another ADB project) connecting Khulna city gate station to Khulna 225 MW CCPP.12 The contract for construction of pipeline from Khulna city gate station to Khulna CCPP is awarded in January 2019 and is under implementation. It is expected that the pipeline will start to supply gas from 2020 and reach full utilization (75–125 MMCFD at appraisal) by 2022. 14. A5: North–south system expansion. This component comprised of installing two gas turbine compressors at Ashuganj south and Muchai with throughputs of 370–890 MMCFD. Two consecutive biddings for procurement in 2006 and 2008 had failed. The first round of bid was canceled due to a perceived integrity violation. ADB advised to rebid it. Second round of bid was failed due to the increase in steel price in international market and design change—both caused excessively high bids.13 In April 2009 the EMRD requested ADB for additional financing for compressor stations. Given the lead time for processing of additional financing, ADB advised

11 Due to the nationwide supply crisis from 2009, the Government intermittently suspended new gas connections in

2010–2014. Commercial and industrial connections resumed in 2014. Residential connections are permanently suspended from 16 July 2016.

12 Construction of 12 km Khulna city gate station to Khulna 225MW CCPP pipeline is part of ADB Loan 2622-BAN. 13 The cost estimate in first bid on 16 April 2006 was $41 million for compressor capacities—1,050 MMCFD at Ashuganj

and 1,100 MMCFD at Muchai. Rebid in 2008 increased compressor capacities—1,500 MMCFD for Ashuganj; 1,160 MMCFD for Muchai and added a 500 MMCFD compressor at Elenga based on revised demand forecast. Elenga compressor station’s original design was 209 MMCFD. The lowest received bid on 9 February 2009 was $147.9 million against the estimate of $55 million. Similar high price trend was also observed in contemporary contract for package A-B-1, awarded on 11 March 2009 at $46.2 million against estimate of $23 million, and the contract for package A-A-1, awarded on 12 March 2009 at $ 26.8 million against the estimate of $14.7 million.

5

transferring the compressor stations to another ADB project being processed.14 Hence, both gas compressor stations were dropped from the project. ADB provided its concurrence to drop the compressor stations on 23 September 2009.15 The contracts for Ashuganj (south and west) compressor stations for throughput of 1,500 and Elenga for 500 MMCFD were awarded on 21 October 2011 under Loan 2622-BAN; the stations were commissioned in June 2016. Chevron Bangladesh Ltd. (a private oil and gas company) constructed the Muchai compressor station for 1,160 MMCFD throughput under a production sharing contract, commissioned in March 2012.16

15. Supervisory control and data acquisition (SCADA) system under components A2–A4 was procured in a single package—western zone SCADA package—and completed in November 2015. The system interfaced with GTCL’s existing SCADA system, financed by JICA, and enabled GTCL to access the real time gas transmission data from Dhaka from August 2018.

16. Overall, under output 1, the project constructed a 345.8 km pipeline, 98% of the target 353 km, with throughput capacity up to 342 MMCFD, 95% of the target of 360 MMCFD (Table 1).

Table 1: Gas Transmission Lines Capacity Expansion at Appraisal and Completion At Appraisal At Completion

17. As targeted, the project’s part B completed appraisal of five gas fields (1,250 square km) in April 2014, with 4 years’ delay. The component’s two executing agencies—Bangladesh Gas Fields Limited (BGFCL) and Sylhet Gas Fields Limited (SGFL)—procured 3-D survey equipment and provided it to the implementing agency, Bangladesh Petroleum Exploration and Production Company Limited (BAPEX), for survey, instead of contracting to an external firm. BAPEX completed the field survey and data interpretation in 2007–2012. As a result, the project proposed drilling 30 new gas wells (Titas-11 and Bakhrabad-3 under BGFCL; Rashidpur-9, Kailastilla-4 and Sylhet gas field-3 under SGFL)—12 wells were drilled successfully in subsequent years.17 Instead of foreign training, the project arranged on-the-job training at local levels from international experts.18 BAPEX used the equipment procured and expertise gained under the project for revision of data interpretation in 2016 for precise determination of drilling locations.

14 ADB. 2010. Bangladesh: Natural Gas Access Improvement Project. 15 ADB approved cancellation of compressors on post facto on 8 October 2013. Subsequently, ADB review mission on

13–16 December 2009 recorded gas turbine compressor stations to be funded by the ensuing Loan 2622-BAN. 16 The contract value for the Ashuganj and Elenga compressor stations was $122 million; the contract value for the

Muchai compressor station was $52.8 million. 17 Seven out of 12 drillings were successful and added 114 MMCFD gas to the national grid. Four drillings were carried

out under ADB project from Loan 2622. 18 BAPEX invited expressions of interest three times, but the single responsive proposal was much higher than estimate.

6

3. Part C: Rajshahi Gas Distribution Network

18. The project’s part C completed 270.16 km of distribution pipelines of 1- to 8-inch-diameter (over 85% of the target 280–320 km), including a 34 km ring main of 8-inch-diameter pipeline and accessories, in July 2012.19 Pashchimanchal Gas Company Limited (PGCL) executed the project component, providing Rajshahi city with piped gas for the first time and connecting a total of 9,155 households (228% of the appraisal target of 4,000 households) when the temporary suspension on new domestic connection was relaxed (footnote 11).20 Starting July 2012, the project connected 11 industries, 2 captive power plants (2 MW and 2.4 MW) and one CNG station, against the target of 150 commercial and 75 industrial connections. Part C supplies 3.22 MMCFD gas against the target 20 MMCFD. Gas supply shortage and the government’s continued suspension on new connections hampered industrial development and led to low capacity use. Table 2 summarizes the gas distribution network at appraisal and at completion.

Table 2: Rajshahi Gas Distribution Network at Appraisal and Completion At Appraisal At Completion

Component Pipeline Length

(km)

Gas Connections

(Nos.)

Gas Throughput

(MMCFD)

Pipeline Length

(km)

Gas Connections

(Nos.)

Gas Throughput

(MMCFD) Rajshahi gas distribution network

280.00 4,225.00 20.00 270.16 9,167.00 3.22

km = kilometer, MMCFD = million cubic feet per day

4. Part D: Capacity Building 19. Part D helped enhance financial performance, governance and institutional efficiency of the executing and implementing agencies—Petrobangla, BAPEX, and Titas Gas Transmission and Distribution Company Ltd (TGTDCL)—through capacity building and implementing the GSRR (footnote 5). It implemented four capacity building components (D1–D4). 20. D1: Institutional strengthening of hydrocarbon unit (HCU). Grant 0019 funded the HCU work plan. As planned, nine consulting firms were recruited. The terms of references were updated to accommodate gas production augmentation services. Though delayed, the HCU became a permanent technical arm of EMRD on 1 January 2014, which is a major achievement. 21. D2: BAPEX data center upgrade. The BAPEX data center was upgraded in May 2011 and digitized old data in 2012; the upgraded center digitally preserves geological, geophysical, and well data of the gas fields. 22. D3: Development of institutional capacity of gas sector entities. 154.8 person-weeks of training (71% of 218 person-weeks at appraisal) were provided to 340 gas sector staff. Training included engineering design; operation and maintenance of processing plants and transmission and distribution pipelines; exploration of geophysics; 3-D seismic acquisition, processing and interpretation; reservoir engineering and management; compressor station planning and management; techno-commercial engineering; and decision making and executive management. 23. D4: System loss reduction of Titas Gas Transmission and Distribution Company. In 2009, 604 turbine and rotary meters with electronic volume correctors (EVC) and five mobile on-site meter calibration units were procured; by June 2011, 575 rotary meters with EVC were installed. However, TGTDCL does not bill gas consumption based on the EVC meters, except for the industries and CNG fueling stations, and does not use corrected readings from the installed 19 The RRP presents the length as 320 km, the DMF as 200 km, and the project administration manual as 280 km. 20 9,155 newly connected households included 9,103 non-metered and 52 metered, comprising 14,638 dual burners.

7

EVC meters to compute system loss for household customers. Because of the prevailing low tariff for metered gas compared to the connection-based tariff, TGTDCL would lose revenue if the EVC meters were used.21 TGTDCL uses the EVC meters only for the bulk customers whose tariff are consumption based. As envisaged the project completed the other components such as, system operation strengthening, loss control, customer services upgrade, and human resources development by October 2010. The project trained 140 TGTDCL staff with specialized on-the-job training in the Bangladesh Petroleum Institute. TGTDCL’s performance is noted to have improved. C. Project Costs and Financing 24. The total project cost at completion is $303.71 million, 26.53% below the estimated $413.4 million at appraisal (Appendix 2). Part A, the transmission component, cost 18% below the appraisal cost. Component A2 costs 54.5% more than at appraisal, whereas components A1, A3 and A4 cost 18.76% below in aggregate. Cancellation of four compressor stations (A1 and A5) reduced the ADB’s finance by $55 million; whereas Padma river crossing and use of 87 km of 30-inch-diameter pipe instead of 24-inch in A2 increased the cost by $30.57 million. At completion, the actual cost of A2 reached $86.57 million against $56 million at appraisal. ADB financed $50.82 million against $30 million at appraisal to A2. Part B, field appraisal, cost 25.24% below; Part C, gas distribution, 22.25% below; and Part D, capacity building, 31% below the appraisal costs. 25. At appraisal, ADB’s financing ratio was 54.43% from Loan 2188 (OCR) and 1.21% from Loan 2189 (SF). At completion, ADB’s share stood at 59.43% (OCR 58.62%; SF 0.81%). Share of Norwegian grant to capacity building (part D1) was 1.18%. Appendix 3 presents the original and actual loans and grant allocation by financers. Borrowers request for reallocation of Loan 2188 and Grant 0019 were approved on 8 October 2013.

D. Disbursements 26. The disbursement schedule at appraisal was realistic and consistent with the investment proposal. The disbursement period extended from the original 49 months to 121 months because of the 72-month delay in project implementation. At completion, partial cancellations of two loans and one grant totaled $50.91 million (22% of total loans and grant)—$46.97 million from Loan 2188, $2.54 million from Loan 2189(SF) and $1.4 million from Grant 0019. At government’s request, $26.80 million was partially canceled on 19 August 2013 from Loan 2188; the remaining loan was canceled at account closure. Appendix 4 shows the projected and actual disbursements. ADB’s loans cumulatively disbursed $180.5 million (78.48% of loan), and the Norwegian grant disbursed $3.6 million (72% of grant). Approximately 98% of ADB financing was disbursed via commitment letter— from Loan 2188 (OCR). Remaining 2% was disbursed via direct payment—from Loan 2189(SF) and Grant 0019. E. Project Schedule 27. Signing of the loans and grant agreements were delayed by eight months due to change in the government in 2005. It took another four months for effectiveness. Loan 2188 was physically closed on 31 December 2016, Loan 2189(SF) on 31 December 2012, and Grant 0019 on 10 October 2013. Loan 2189(SF) was extended once and Grant 0019 twice, and their accounts were closed on 13 February 2014, after more than three years. Loan 2188 was extended three times and financially closed on 18 May 2017, after six and a half years. Project delays resulted from rebidding of 26 packages (parts A to C), difficulties in acquiring right of ways (A2), delays in 21 Domestic gas is generally priced per connection at flat rate. TGTDCL incurs revenue loss if it bills with EVC meters,

as most household consumers use less volume of gas than the allocated. However, it is noted, with the revisions in domestic gas tariff in 2015, 2017 and 2018, the JICA-funded consumption-based prepaid meters succeeded.

8

Padma river crossing work (para. 11), delays in consultant recruitment (parts B and D) and delays in land acquisition (parts A and C). GTCL’s defective SCADA system and server breakdown delayed the western zone SCADA work (part A). SCADA installation began only after the existing system was repaired in November 2011. The interfacing was finally completed in 2015. Delays in consultant recruitment for BAPEX data center upgrade also delayed the closing of Loan 2189(SF). The government’s technical assistance project proforma for grants required revision during the implementation as it did not provision the VAT and advance income tax. To prepare a detailed action plan for part D the government of Norway fielded international consultant in July 2007 separate from the grant. The action plan was endorsed by EMRD and ADB in July 2008. Change in executing agency for capacity development component also delayed the project. Overall, the project faced 72 months delay (Appendix 5). F. Implementation Arrangements 28. The project implementation arrangement at appraisal was adequate, except for part D (Table 3). For component D1 (HCU capacity development), to ensure proper line of command, ADB changed the executing agency at the government’s request from Petrobangla to EMRD on 23 October 2007. For D2–D4, Petrobangla coordinated with BAPEX for the data center upgrade (D2), and with TGTDCL for the gas sector loss reduction plan (D3) and institutional capacity development of gas sector entities (D4). The project established 13 project management units (PMUs), against five planned at appraisal—five PMUs under part A, one for each component (A1–A5); three PMUs under part B, one for each agency; one PMU under part C; and four PMUs for part D.22 PMUs recruited the project management and safeguards implementation specialists.

Table 3: Project Implementation Arrangements: Planned versus Actual Component EA/IA at Appraisal EA/IA at Implementation A. Gas transmission GTCL GTCL B. Field appraisal SGFL & BGFCL, with BAPEX as IA SGFL & BGFCL, with BAPEX as IA C. Rajshahi gas distribution network PGCL PGCL D1. Capacity development of HCU Petrobangla and EMRD EMRD with HCU as IA D2. Upgrading BAPEX data center BAPEX Petrobangla with BAPEX as IA D3. TGTDCL system loss reduction Petrobangla Petrobangla with TGTDTCL as IA D4. Institutional capacity

development Petrobangla Petrobangla

BAPEX = Bangladesh Petroleum Exploration and Production Company, BGFCL = Bangladesh Gas Fields Company Limited, EA = executing agency, EMRD = Energy and Mineral Resources Division, HCU = hydrocarbon unit, IA = implementing agency, GTCL = Gas Transmission Company Limited, PGCL = Pashchimanchal Gas Company Limited, SGFL = Sylhet Gas Fields Limited, TGTDTCL = Titas Gas Transmission and Distribution Company Limited.

G. Consultant Recruitment and Procurement 29. At appraisal, the procurement plan envisaged 30 international competitive bidding packages (25 for GTCL, 1 for SGFL and BGFCL, 2 for PGCL, and 1 each for Petrobangla and EMRD). It also included 19 limited international bidding packages (14 for GTCL, 1 each for SGFL and BGFCL, 1 for PGCL, and 3 for Petrobangla and EMRD) and one shopping package by GTCL. The plan included quality- and cost-based selection to recruit four consulting firms (one for SGFL and BGFCL and one each for GTCL, Petrobangla, and EMRD) and individual consultants for the HCU (part D1). At completion, the project procured 66 contracts with international competitive bidding (41 for GTCL, 7 for BGFCL, 9 for PGCL, and 3 for SGFL), included 8 turnkey and 58 supply contracts. Two consulting firms were recruited following quality- and cost-based selection: one for field appraisal, later executed at the executing agency’s expense, and one for compressor

22 The PMU for the compressor station package (A5) continued under new project (Loan 2622: BAN).

9

station implementation, including technical support for bidding.23 To support studies and trainings, the project recruited individual consultants instead of a firm (para. 20). ADB’s prior approval were secured for all changes in methods and packages. Appendix 6 presents the contract awards at appraisal and at completion. Chronology of major procurement events is in Appendix 7. 30. Twenty-six procurement packages under GTCL (components A1–A2), BGFCL, and PGCL required rebidding due to lack of competition, international market price increases, and packaging issues (one package in part B required goods from six different manufacturers, bidders could not succeed as they failed to consolidate bids). Contract execution was hampered by supplier’s failure to complete the job because of increase in price of materials (component A1). Technical failures of the induction bend (component A2) caused replacement of materials during warranty period. Outdated cost estimates, changes in specification during implementation and unforeseen price increases in the international market forced cancellation of four gas compressor stations. Lowest bid value for the compressors was more than twice of the estimates (footnote 13). Good technical due diligence and robust cost estimate would have avoided procurement delays and cost overrun. H. Gender Equity 31. Though categorized as no gender element at appraisal, certain positive benefits to women and children were observed at project implementation. The project provided gas connections to 9,155 households comprising 14,638 cooking stoves and one textile factory with 85% women employees in Rajshahi creating positive impact on the quality of life for women and children. By replacing firewood and kerosene with cleaner gas, project helped improve health of women and children. It reduced the time spent in cooking that gave them more time for productive work. I. Safeguards 32. Environment. The project was categorized B for environmental safeguards, as the impact on environment was expected to be less significant and mitigation measures were readily available. The initial environmental examinations and environmental management plans were prepared for all components following the ADB environment policy (2002), environmental assessment guidelines (2003), the government of Bangladesh’s environment conservation act (1995), environmental impact assessment guidelines for industries, and related national policies and legislations. A summary initial environmental examination for entire project was prepared and disclosed per ADB environment policy 2002. On the government side, an environmental impact assessment was prepared and environmental clearance certificate was obtained from department of environment, as the government decided to consider the project a part of “exploration, extraction and distribution of mineral resources,” falling under item 65 in the red category list of Bangladesh environmental conservation rules (1997). 33. At implementation, environmental management clauses were incorporated in the bidding documents for eight civil works packages that required specific environmental safeguard measures. Both PGCL and GTCL, who implemented the civil works, recruited consultants for environmental monitoring and training. Consultants prepared environmental monitoring reports for both PGCL and GTCL (Appendix 8) and organized a training workshop on environment for PGCL engineers and officials. The project used suitable technology such as horizontal directional drilling to minimize construction effects and avoid significant adverse impacts on navigation, fisheries, and other aquatic resources in fourteen river crossings. During site visits, the PCR mission noted good environmental health and safety practices at the project sites, including

23 ADB did not finance the consulting firm for field appraisal since only one technically responsive firm emerged even

after three consecutive expressions of interest. The scope was reduced, and the executing agency funded it.

10

monthly safety reporting systems, mock fire drills, availability of first aid boxes, and no record of accidents. Because the natural gas replaces alternative fuels including high speed diesel for power plants and industries, it is expected to have mitigated greenhouse gas emissions. The project is expected to reduce carbon dioxide emissions by 61,351,249 tons over the period up to 2037.24 Delay in project categorization, long implementation period and dropping of the compressors have led to nondisclosure of some reports in ADB website—they were subsequently traced and found satisfactory. The overall environmental safeguards compliance is rated satisfactory. 34. Social safeguards. The project was categorized A for involuntary resettlement and C for indigenous peoples. The policy framework and entitlements are based on ADB’s involuntary resettlement policy (1995).25 At appraisal, GTCL and PGCL prepared six resettlements plans to mitigate permanent and temporary socioeconomic impacts. The project involved land acquisition and temporary requisition in parts A, B, and C (Appendix 8). Under part A, the component causing maximum social impact, four resettlement plans (RP) stipulated permanent acquisition of 351.55 hectares and temporary requisition of 628.5 hectares of lands, affecting 1,249 households. Under Part B, field appraisal activities caused temporary effects for 15 days—RP anticipated 270 hectares of land having only short-term impact on crops affecting 800 households. The RP for part C (gas distribution pipeline) required 3 hectares land acquisition. 35. At project closure, all six RPs were implemented (Appendix 8). The project hired a nongovernment organization to monitor implementation of RPs as per loan covenant. GTCL and PGCL disclosed the external monitor’s comprehensive reports on RP implementation on the ADB website. With support from the local government, BAPEX delivered crop compensation under part B. At closure, no unresolved grievances needed resolution. The delays in land acquisition (Appendix 8) occurred because of the complexity of acquisition process, as natural gas transmission projects require permanent acquisition of a 20- to 30-feet wide strip and temporary acquisition of another 40-feet wide strip throughout the pipelines. These affects thousands of landowners and requires substantial time to complete. The overall social safeguards compliance for the project is rated satisfactory. J. Monitoring and Reporting 36. The project fully complied with 40 out of 41 covenants (Appendix 9). The project partially complied with one covenant on air quality improvement monitoring under the project performance monitoring system. Due to lack of baseline and current data, the project did not measure air quality improvement and instead used the secondary data. All executing agencies submitted the semiannual environmental monitoring reports, except for part B, where the impact was temporary. All executing agencies submitted the quarterly progress reports and social monitoring reports to ADB on time. No covenants were modified, suspended, or waived during implementation. However, changes in PMU staffs and project delays caused some gaps in reports disclosure. 37. Submission of annual audited project financial statements and audited entity financial statements were timely, but some discrepancies exist with the data from loan and financial information system which is being reconciled. Project review missions regularly monitored the financial and physical implementation progress against the implementation schedule and compliance with the covenants. Further follow up is needed to resolve some audit observations. 24 Carbon dioxide emissions were calculated following the guidelines of the United Nations Framework Convention on

Climate Change (https://unfccc.int/resource/docs/publications/09_resource_guide3.pdf). 25 Summary resettlement plan (Appendix 14, p. 52) in ADB. 2005. Report and Recommendation of the President to the

Board of Directors on a Proposed Loan and Grant to the People’s Republic of Bangladesh for Gas Transmission and Development Project. Manila.

11

III. EVALUATION OF PERFORMANCE A. Relevance 38. The project is rated relevant. The design and formulation were consistent with the poverty reduction strategy paper of 2005 (para. 4) for enhancing natural gas production and distribution to promote industrialization and ensure equitable distribution of benefits. The depth of development coordination has prevented overlaps in support among development partners. At completion, the project is aligned with the government’s Seventh Five-Year Plan, 2016–202026 that targeted higher, sustainable, and inclusive growth through continued focus on natural gas infrastructure, including LNG import facilities. Similarly, the project at appraisal was aligned with ADB’s country strategy and program, 2004–2006 and continued to align with ADB’s country partnership strategy, 2016–2020, which prioritized easing infrastructure constraints in key sectors like energy.27 The project remains consistent with ADB’s energy policy (2009).28 The project played a vital role in improving the energy infrastructure, connecting the energy-starved western region and catering need for energy in the rapidly growing industrial and commercial zones around Dhaka by constructing 345-km transmission pipelines and 270-km distribution pipelines. At appraisal, the existing pipeline in the Brahmaputra basin from Ashuganj to Elenga (B-B line) was operating in saturated condition. The Ashuganj–Jamuna Bridge GTP, built in parallel to B-B line, strengthened the national gas grid backbone, now capable of serving the regional gas demand up to 420 MMCFD. The Hatikumrul–Bheramara GTP and Bonpara–Rajshahi GTP deliver gas to the south-western zone, a future industrial hub. The network will harness its full potential once the import of LNG, begun in 2018, is fully realized (para. 8). On upstream exploration, a sub-surface 3-D survey provided a solid basis for adding proven gas reserves up to 3 TCF. The western zone SCADA system interfaces with the pre-existing SCADA network so GTCL can access countrywide real time data remotely. While utilization of some project outputs was affected by the gas supply shortage, the government’s current interventions and future plans for the energy sector show that the facilities established under the project would play a crucial role as the country’s demand for energy continues to increase (para. 8). 39. The project lending modality was appropriate (para. 5) given the defined scope of investments. Synergies between the hard and soft components were ensured with their alignment with Petrobangla’s investment plan and the GSRR. The project design and monitoring framework (DMF) though could have benefited from having a more logical linkage of results, realistic and measurable indicators and relevant baseline data (DMF output 4). Applying lessons and recommendations from the previous project PCR, the project included a system loss reduction plan aligned to the GSRR and pursued a reform agenda, including autonomy of Bangladesh Energy Regulatory Commission (BERC) and HCU functionality.29 The government’s power system master plan of 2016 targets 33% of electricity generation fueled by gas by 2041. The Bangladesh Gas Act (2010) and Gas Development Fund Policy (2012) both emphasized new exploration, production, and transmission infrastructure. The project remained relevant at completion and will continue to be relevant after project completion (para. 8). 40. The implementation arrangement was adjusted to improve management and coordination of project components (para. 28). The project scope was modified with cancellation of compressor stations (para. 10 and 14). The canceled compressor component constituted only 13.3% of the

26 Government of Bangladesh, Planning Commission. 2015. Seventh Five Year Plan FY2016–FY2020: Accelerating

Growth, Empowering Citizens. Dhaka. 27 ADB. 2016. Country Partnership Strategy: Bangladesh, 2016–2020. Manila; 28 ADB. 2009. Energy Policy. Manila. 29 ADB. 2005. Project Completion Report: Third Natural Gas Development Project. Manila.

12

total project cost and financed by another ADB project. The Rajshahi gas distribution network under part C achieved more than 85% of its physical target, but capacity use was low because of low industrialization due to shortage of indigenous gas supply during 2010–2014 (footnote 11). B. Effectiveness 41. The project is rated effective. The outcome and outputs envisioned at appraisal were substantially achieved (Appendixes 1 and 10). The country’s gas consumption increased from 1,400 MMCFD in 2005 to 1,925 MMCFD in 2010 and 2,450 MMCFD in 2015, against the outcome target 1,760 MMCFD in 2014. Outcome indicator 1 was fully achieved by year 2010 (109% of the target). The country’s gas consumption in 2018 reached about 3,200 MMCFD, 170% of the outcome target. The population using natural gas as a primary fuel (outcome indicator 2) increased from 6% in 2005 to 10% in 2015, against the target of 10% by 2012. Suspension on gas connections and shortage of gas lowered the use of project assets (footnote 11). 42. Parts A and B of the project directly contributed to outcome indicators 1 and 2. In 2019, 342 MMCFD gas (11.4% of national consumption) flowed through the Ashuganj–Elenga pipeline, which is 95% of the outcome target (addition of 360 MMCFD). Field appraisal and a 3-D survey (part B) eventually resulted in additional gas production of 114 MMCFD (4.2% of total indigenous gas production). The project constructed 345 km of new transmission pipelines (98% of the output 1 target of 353 km). Under part C, 270 km of distribution pipelines in Rajshahi and adjoining area (96% of the target 280 km) were constructed. Under part B, five gas fields of 1,250 square km (100% of the target) were 3-D surveyed. 43. The capacity building component (part D) strengthened the gas sector utilities’ financial performance, governance, and efficiency. GTCL, SGFL and BGFCL generally achieved the debt service coverage ratio of 1.2 from 2005 onwards. The project helped implement the GSRR (Appendix 11), which became a policy roadmap for Petrobangla from 2009. The project enhanced private sector participation—in 2019, the private sector produced 58.32% of domestic gas under production sharing contracts. System loss fell to 1.82% in 2010 against the target 2% and remained below 2% thereafter. Implementation of GSRR led to the functionality of BERC and the formulation of the Bangladesh Gas Act (2010) and Petroleum Act (2016). The outcome will be visible in 2021, once the LNG import reaches its full potential. Implementation of environmental and social safeguard management plans was satisfactory (paras. 33 and 35). C. Efficiency 44. The project is rated efficient. The economic reevaluation was conducted following ADB guidelines, consistent with the approach adopted at appraisal.30 Because the project comprised distinct parts, separate economic analyses were carried out for each part and subsequently aggregated and weighted to reflect the significance and size of the subprojects. Despite a 72-month implementation delay, the economic internal rate of return (EIRR) at project completion is 39.8% in aggregate (Appendix 12). The aggregate EIRR, though lower than at appraisal’s 56.6%, it is higher than the benchmark 12%.31 The reevaluated EIRR has been assessed as robust. The sensitivity analysis shows the EIRR would remain unchanged if O&M cost increased by 10%. The EIRR would drop to 38.0% if the benefit decreased by 10%. Likewise, the EIRR would drop to 38.9% if the gas costs increased by 10%. If all three events took place simultaneously, the EIRR would drop to 35.1%. Table 4 shows the EIRR at appraisal and at completion. 30 ADB. 2017. Guidelines for the Economic Analysis of Projects. Manila. 31 RRP para. 49 states the EIRR at appraisal was 28.1%. In its Appendix 12, Table A12.1, the O&M costs were noted

to be grossly overestimated. This resulted in the low value of EIRR. The supplementary appendix to RRP has calculated the EIRR of 56.6%. For comparison, the PCR considered the EIRR at appraisal to be 56.6%.

13

Table 4: Comparison of EIRR at Appraisal and Completion

Components EIRR (%)

At Appraisal At Completion Part A A1 and A5. AJGTP and NSSE

57.30

84.00

A2. HBGTP 33.50 26.80 A3. BRGTP 25.00 9.90 A4. BKGTP 28.00 21.30 Overall part A: Gas transmissiona 57.10 37.90 Part B: Field appraisal 42.60 48.90 Part C: Rajshahi gas distribution network NA 13.10 Overall 56.60 39.80 AJGTP = Ashuganj–Jamuna Bridge gas transmission pipeline, BKGTP = Bheramara–Khulna gas transmission pipeline, BRGTP = Bonpara–Rajshahi gas transmission pipeline, EIRR = economic internal rate of return, HBGTP = Hatikumrul–Bheramara gas transmission pipeline, NSSE = north–south system expansion. a Includes the Rajshahi gas distribution network. The EIRR for Part C is also computed separately above.

45. Due to multiple reasons (para. 27), the project was delayed. Pipeline use remains low because the gas supply through Bheramara–Khulna GTP has not started as of June 2019. Full capacity use is expected from 2022 (para. 13). Nevertheless, the economic benefits far outweigh the cost of project factoring the delays as discussed above. The project used 73.46% of resources allocated by all financiers suggesting efficient use of resources. D. Sustainability 46. The project is rated likely sustainable. The aggregate reevaluated FIRR following ADB guidelines on financial management is 3.20%,32 which is higher than the aggregate weighted average cost of capital (WACC) of 1.46% (Appendix 13), but lower than the FIRR of 12.0% at appraisal. Because the reevaluated FIRR exceeds the WACC, it confirms the investment was robust. However, implementation delay, low pipeline use, and higher O&M costs reduced the revenue of Bonpara–Rajshahi transmission and Rajshahi distribution pipelines during FY2014–2018, resulting in negative FIRR (Appendix 14). Imported LNG and commissioning of the Rupsha 800 MW CCPP will ensure full utilization of the south-western Bheramara–Khulna GTP by 2022. 47. The institutional sustainability of gas utilities, namely, GTCL, PGCL, BGFCL, and SGFL were assessed based on their business and financial risks, and financial flexibility and liquidity (Appendix 15). Overall, their business risks are assessed to be insignificant. However, because tariffs are highly regulated, their revenue risk continues, for example, delays in approving new tariffs caused significant margin and cash flow pressure during the analysis period of FY2015–2017. Implementation of the GSRR and ADB’s continued policy dialogue with the government are supporting BERC on the formulation of market-based gas tariff, which is expected to start after the 1,000 MMCFD LNG import plan fully materializes by end of 2019. Although financial performances were mixed, the country’s stable and stronger economic outlook indicates gas companies will continue with investments as their credit metrics remain robust, supported by positive operating cash flow. But despite the positive cash flow, gas utilities need to focus on controlling the O&M costs. This is being monitored by the BERC. Implementation of GSRR, the Bangladesh Gas Act (2010), the Gas Development Fund Policy (2012), establishment of HCU, and formulation of gas sector master plan are expected to uphold the business and financial sustainability of gas sector entities. Gas system loss reduction plan achieved its targets (Appendix 16). There are no foreseen environmental and social risks in the project. The quality of assets created are deemed sound and likely to withstand normal weather patterns and other adversities.

32 ADB. 2005. Financial Management and Analysis of Projects. Manila.

14

E. Development Impact

48. Overall developmental impact is assessed satisfactory. The project improved the gas supply around greater Dhaka. Transmission pipelines up to Khulna and Rajshahi have ensured adequate gas supply to the existing, ongoing, and upcoming power plants at Sirajganj, Rajshahi, Bheramara, and Khulna. Access to gas has increased to 8% against a target of 10% by 2012, and further increased to 13% in 2017.33 Domestic gas production reached 2,700 MMCFD in 2015. Power generation capacity increased from approximately 6,000 MW in 2005 to 19,000 MW in 2018, with 56% fueled by gas. In 2019, natural gas contributes 62% of primary energy. Access to electricity is over 90%, up from 40% at appraisal. Gross domestic product growth reached 7.6% in 2018 from 5.5% at appraisal. Thus, project has fostered the accelerated economic activities. F. Performance of the Borrower and the Executing Agency 49. The performance of the borrower and executing agencies is rated satisfactory. The executing agencies established the PMUs on time with proper resources. The government funded 39% of the project cost, close to the appraisal estimate of 43%. GTCL has put all its efforts to complete the delayed Padma river crossing. Likewise, the EMRD fully owned the capacity development activities. All EAs have submitted the quarterly progress reports and annual audited project financial statements as required. They prepared the PCRs on time. However, their financial management could have been better as some audit and reconciliation issues continued. G. Performance of Cofinancier

50. Performance of the government of Norway was satisfactory. It worked closely with ADB and the government, participated in reviews and timely transferred its cofinancing share to ADB. H. Performance of the Asian Development Bank

51. ADB’s performance was satisfactory. It responded timely to the needs of executing agencies including changes in specifications in part A2, financing arrangements for compressor stations (footnote 15), and extension of loans and grant (para. 27) to complete the delayed components. ADB reviewed and approved the procurement documents in time and provided guidance to executing agencies through review missions and meetings. ADB promptly canceled $49.5 million loan and $1.4 million grant at government’s request. Project performance remained satisfactory or on-track for the entire period from 2007 to 2016. However, some audit observations and reconciliation issues were persisted over the years. The financial management could have been better. The project missed to fully comply with the environment safeguard report disclosure (Appendix 8). The DMF’s output 4 (improved air quality) should have been placed at outcome level, and it lacked baseline data and methodology of monitoring. After the cancellation of compressor stations, the relevant output indicator should have been revised. I. Overall Assessment 52. Overall, the project is successful based on the ratings of relevance, effectiveness, efficiency, and sustainability. The project is relevant as it financed important natural gas infrastructure and reforms for equitable distribution of benefits and economic growth as per the government and ADB policies. It is effective as both the outcome indicators are fully achieved, and except the installation of compressor stations all eight output indicators are substantially

33 The increase in access to gas is one of the project’s contributions to ADB’s results framework. Other results indicators

include (i) 2,794,510 tons of carbon dioxide emission reduction as of December 2018, (ii) 345 km of gas transmission lines installed, and (iii) 270 km of gas distribution lines installed.

15

achieved. It is efficient with an EIRR of 39.8% despite the substantial delays. The project is likely sustainable as the reevaluated FIRR of 3.20% is higher than the WACC of 1.46%. The higher utilization of the pipelines in near future will further improve the financial benefits of the project.

Table 5: Overall Ratings Criteria Rating Relevance Relevant Effectiveness Effective Efficiency Efficient Sustainability Likely sustainable Overall Assessment Successful Development impact Satisfactory Borrower and executing agencies Satisfactory Performance of ADB Satisfactory

IV. ISSUES, LESSONS, AND RECOMMENDATIONS

A. Issues and Lessons 53. Large consumers in Khulna region have not received the gas due to the delays in constructing the associated facilities, such as distribution pipelines. Effective coordination among the EMRD, Power Division, and Ministry of Industries would have ensured optimum use of assets. 54. With the increased LNG supply and depletion of domestic gas, some compressors are likely to be underutilized in future. A comprehensive study of long-term availability of domestic gas may have given better options and avoided the possibility of stranding of the assets. 55. The resettlement process started in 2007 and finished only in 2014. Advance readiness actions on land acquisition could have improved the resettlement process efficiency. 56. The project suffered because of rebidding 26 packages, 39.4% of total packages (Appendix 7). Robust technical due diligence and comprehensive cost estimates based on the international market were needed for better procurement and implementation. 57. Emphasis on financial management requirements by the borrower’s auditors, project authorities and ADB is required for continued compliance with the financial covenants. B. Recommendations 58. Further action or follow-up. ADB should continue assistance to BERC for improved tariff mechanisms for sector sustainability. With LNG imports, a dynamic gas tariff reflecting international prices is recommended. ADB should continue its policy dialogue for sector reform and implementation of the gas sector master plan, support to HCU, and help the country respond to private sector development. Before investment ADB should assess the adequacy of gas supply. 59. Robust design and specification, realistic cost estimates and packaging, strategic procurement planning, flexible procurement to accommodate uncertainties in international prices of materials and equipment, and advance project readiness action for land acquisition are recommended. Safeguard categories and baseline data should be firmed up at the design stage. 60. Future Monitoring. Borrower’s reconciliation between ADB’s disbursements record (LFIS and GFIS) and aggregated project audited financial statements to complete by 30 October 2019. 61. Timing of the project performance evaluation report. As of August 2019, the facilities have not utilized their capacity fully. The project performance evaluation may begin after 2020.

16 Appendix 1

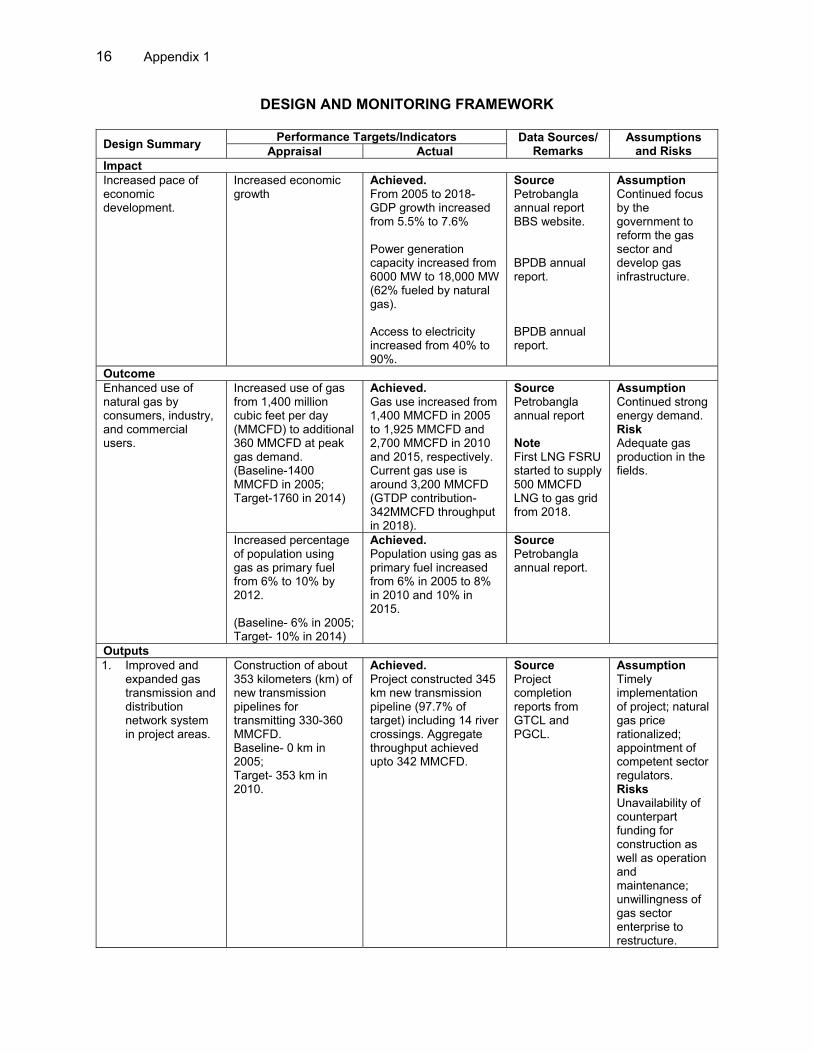

DESIGN AND MONITORING FRAMEWORK

Design Summary Performance Targets/Indicators Data Sources/

Remarks Assumptions

and Risks Appraisal Actual Impact Increased pace of economic development.

Increased economic growth

Achieved. From 2005 to 2018- GDP growth increased from 5.5% to 7.6% Power generation capacity increased from 6000 MW to 18,000 MW (62% fueled by natural gas). Access to electricity increased from 40% to 90%.

Assumption Continued focus by the government to reform the gas sector and develop gas infrastructure.

Outcome Enhanced use of natural gas by consumers, industry, and commercial users.

Increased use of gas from 1,400 million cubic feet per day (MMCFD) to additional 360 MMCFD at peak gas demand. (Baseline-1400 MMCFD in 2005; Target-1760 in 2014)

Achieved. Gas use increased from 1,400 MMCFD in 2005 to 1,925 MMCFD and 2,700 MMCFD in 2010 and 2015, respectively. Current gas use is around 3,200 MMCFD (GTDP contribution- 342MMCFD throughput in 2018).

Source Petrobangla annual report Note First LNG FSRU started to supply 500 MMCFD LNG to gas grid from 2018.

Assumption Continued strong energy demand. Risk Adequate gas production in the fields.

Increased percentage of population using gas as primary fuel from 6% to 10% by 2012. (Baseline- 6% in 2005; Target- 10% in 2014)

Achieved. Population using gas as primary fuel increased from 6% in 2005 to 8% in 2010 and 10% in 2015.

Source Petrobangla annual report.

Outputs 1. Improved and

expanded gas transmission and distribution network system in project areas.

Construction of about 353 kilometers (km) of new transmission pipelines for transmitting 330-360 MMCFD. Baseline- 0 km in 2005; Target- 353 km in 2010.

Achieved. Project constructed 345 km new transmission pipeline (97.7% of target) including 14 river crossings. Aggregate throughput achieved upto 342 MMCFD.

Source Project completion reports from GTCL and PGCL.

Assumption Timely implementation of project; natural gas price rationalized; appointment of competent sector regulators. Risks Unavailability of counterpart funding for construction as well as operation and maintenance; unwillingness of gas sector enterprise to restructure.

Appendix 1 17

Design Summary Performance Targets/Indicators Data Sources/

Remarks Assumptions

and Risks Appraisal Actual Installation of

compressors at Ashuganj and Muchai with throughputs of 370-890 MMCFD. Baseline- 0 in 2005; Target- 4 in 2010.

Not achieved under this project.1 The component was transferred and completed under subsequent ADB project (Loan 2622-BAN) for a throughput of 2000 MMCFD (footnote 15).

Source Government’s project completion report of ADB Loan 2622-BAN.

Construction of new gas distribution network of about 200 km in the Rajshahi area in western Bangladesh. Baseline- 0 km in 2005; Target- 200 km in 2010.

Substantially Achieved. 270 km distribution pipelines constructed (135% of target) and commissioned in 2011.

Source PGCL’s project completion report

2. Field appraisal of gas fields to update estimated gas reserves and determine exact location for future exploration activities

Five three-dimensional seismic survey reports from Bakhrabad, Kailastila, Rashidpur, Sylhet, and Titas. Baseline- 0 in 2005; Target- 5 in 2010

Achieved. Seismic surveys were carried out in 5 gas fields covering 1250 square KM area from 2012 to 2013. Data interpretation report prepared from 5 gas fields (100% of target) was submitted in 2014.

Source Project completion reports from BGFCL and SGFL.

3. Enhanced financial performance, governance and efficiency indicators of the gas sector utilities through capacity building and implementation of the GSRR to attract private sector investment

Formulation and implementation of the GSRR, a program to reduce system losses to 6% in 2005, 4% by 2007, and 2% by 2010.

Achieved. GSRR was formulated in 2005 and approved in 2009. System loss was brought to 1.82% by 2010 and kept less than 2% onwards. Please refer to Appendix 11 for GSRR agenda achievement and Appendix 16 for updates on gas system loss reduction plan.

Source TGTDCL’s annual Report.

Efficient operation and management of gas entities. Debt service coverage ratio of 1.2 from 2007 and self- financing ratio of 30% from 2008 onwards.

Achieved. Please refer to covenant 18 of Appendix 9.

Source Petrobangla annual Report

Introduction of policies and regulations to streamline processes and attract private sector investment.

Achieved. Bangladesh Gas Act was approved in 2010. Gas Development Fund Policy was approved in 2012. Compressor station at Muchai was constructed by

Source Petrobangla annual Report

1 ADB dropped the compressor stations package from the loan on 23 November 2009. The scope change was approved

by ADB post facto vide memo dated 8 October 2013. However, DMF was not updated to reflect the change in scope.

18 Appendix 1

Design Summary Performance Targets/Indicators Data Sources/

Remarks Assumptions

and Risks Appraisal Actual Cheveron Bangladesh Limited under Production sharing contract with Petrobangla. Govt. introduced policies and regulations to streamline processes and attract private sector investment for LPG and LNG sector (para 39; Appendix 11).

4. Improved air quality. Baseline to be determined during project implementation.

Baseline - None Achieved. Baseline was not determined during project processing or at implementation. But overall air quality improved. Connection of 9,155 households with 14,638 gas stoves in Rajshahi area replaced the firewood for cooking and contributed to improved ambient and indoor air quality. Approximately 2,794,510 tons of CO2 emission has been estimated to have avoided till 2018. 61,351,249 tons of CO2

emission reduction is expected by up to 2037

Source PCR Appendix 12.

BBS = Bangladesh Bureau of Statistics, BGFCL= Bangladesh Gas Fields Company Ltd, BPDB = Bangladesh Power Development Board, GDP = gross domestic product, GSRR = gas sector reform roadmap, GTCL = Gas Transmission Company Ltd., GTDP = Gas Transmission And Development Project, LNG = liquefied natural gas, LPG = liquefied petroleum gas, MMCFD = million cubic feet per day, PGCL = Pashchimanchal Gas Company Ltd., PSC = production sharing contract, SGFL = Sylhet Gas Fields Company Ltd.

19 A

ppendix 2

PROJECT COST AT APPRAISAL AND ACTUAL

Table A2.1: Estimated Project Cost at Appraisal and at Actual completion ($'000)

Item Appraisal Estimate Actual

Foreign Currency

Local Currency

Total Cost Foreign

Currency Local

Currency Total Cost