November 2, 2008 US Technology Strategy Independent Insight: IT Spending Survey 2009 under the knife – expect -1% global decline Expect global slowing in IT spending Balancing developed market declines of -5% for 2009 against emerging market growth of 7% we triangulate to a -1% decline globally. This compares to 6% estimated global growth in 2008 and 9% in 2007. CIO feedback underscores spending contraction Our reading on total IT spending is the lowest in the history of the survey (since 2002). Our total IT spending index came in at 38.8, down from 51.0 in our prior survey, implying meaningful contraction. 4Q budget flush severely capped Fifty-two percent of respondents have seen budgets decrease for 2008 in the past three months, likely pressuring any sort of 4Q budget flush. Forty-one percent of our survey believes spending will be less in 4Q versus recent years. Services pressured; caution on Indian IT Services ticks up Results for services mark a new low point. Appetite for offshore services remains well below trend, and we remain cautious on the space, with both TCS (TCS.BO) and Wipro (WIT, WIPR.BO) rated Sell. Software weakens; Microsoft the exception Software spending intentions dropped to just in line with overall budget commentary, having been flagged as more resilient prior. Applications are most at risk, SAP (SAP) drops out of the top group, and we remain sellers of salesforce.com (CRM) and NetSuite (N). Microsoft (MSFT) enterprise products driving relatively better expectations of spending; in mobile arena, catching up to RIM (RIMM). Networking softer; Cisco positive, best-of-breeds pressured Networking spending intentions softened in line with the overall reining-in of spending intentions. We remain on the sidelines for most stocks in this area. The notable exception is Cisco (CSCO), where share gains partially mute the impact of weaker spending. THIS IS THE 43 RD ISSUE IN OUR IT SPENDING SURVEY SERIES. OUR SURVEY PANEL IS MADE UP OF 100 MANAGERS WITH STRATEGIC DECISION-MAKING AUTHORITY AT MULTINATIONAL FORTUNE 1000 COMPANIES. Sarah Friar (415) 249-7436 | [email protected]Goldman, Sachs & Co. James Covello (212) 902-1918 | [email protected]Goldman, Sachs & Co. Derek R. Bingham (415) 249-7435 | [email protected]Goldman, Sachs & Co. The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. The Goldman Sachs Group, Inc. Global Investment Research

Transcript

November 2, 2008

Goldman Sachs Global Investment Research 1

November 2, 2008

US Technology Strategy

Independent Insight: IT Spending Survey

2009 under the knife – expect -1% global decline

Expect global slowing in IT spending

Balancing developed market declines of -5% for 2009 against emerging

market growth of 7% we triangulate to a -1% decline globally. This

compares to 6% estimated global growth in 2008 and 9% in 2007.

CIO feedback underscores spending contraction

Our reading on total IT spending is the lowest in the history of the

survey (since 2002). Our total IT spending index came in at 38.8, down

from 51.0 in our prior survey, implying meaningful contraction.

4Q budget flush severely capped

Fifty-two percent of respondents have seen budgets decrease for 2008

in the past three months, likely pressuring any sort of 4Q budget flush.

Forty-one percent of our survey believes spending will be less in 4Q

versus recent years.

Services pressured; caution on Indian IT Services ticks up

Results for services mark a new low point. Appetite for offshore

services remains well below trend, and we remain cautious on the

space, with both TCS (TCS.BO) and Wipro (WIT, WIPR.BO) rated Sell.

Software weakens; Microsoft the exception

Software spending intentions dropped to just in line with overall

budget commentary, having been flagged as more resilient prior.

Applications are most at risk, SAP (SAP) drops out of the top group,

and we remain sellers of salesforce.com (CRM) and NetSuite (N).

Microsoft (MSFT) enterprise products driving relatively better

expectations of spending; in mobile arena, catching up to RIM (RIMM).

The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

The Goldman Sachs Group, Inc. Global Investment Research

November 2, 2008

Goldman Sachs Global Investment Research 2

Table of contents

2009 IT spending forecast down 1% globally: Negative in developed economies; growth still evident in emerging markets 2

End-market demand: Almost every vertical likely to soften in 2009 given broad-based nature of macroeconomic declines 7

Latest IT Spending Survey results: Indices continue sharp retreat, now indicating contraction 8

Segment focus: Professional services and hardware tend to be a top focus for spending cuts 12

Vendor focus: Who is gaining share of the shrinking budget? 13

Sub-sector focus: Hardware 17

Sub-sector focus: Software 21

Sub-sector focus: Services 23

Sub-sector focus: Networking 27

Respondent overview 32

Disclosures 34

2009 IT spending forecast down 1% globally: Negative in developed economies; growth still evident in emerging markets

• We estimate IT spending in developed economies will contract 5% in 2009. We

triangulate on the outlook for economic growth, capital spending, and corporate

profits – as well as our latest IT Spending Survey results – to conclude that tech

spending in the developed economies (the United States, Western Europe, and Japan)

is likely to decline by about 5% in 2009. This compares to 4% expected growth in 2008

and 7% growth in 2007.

• We expect 2009 emerging economy IT spending growth of 7%. The Goldman Sachs

Economic Research outlook for capital spending in emerging economies for 2009 is

growth of about 7%. We assume IT spending should trend about in line with this

estimate. The 2009 outlook for emerging markets compares to 10% expected growth in

2008 and 12% growth in 2007.

• Developed market declines offset by emerging market growth leads us to our

forecast of -1% global IT spending growth for 2009. We estimate that developed

economies account for about 65% of total IT spending, with emerging economies

making up the balance. The weighted global spending forecast thus comes to

contraction of about 1% in 2009, compared to our estimate of 6% global spending

growth in 2008 and 9% growth in 2007.

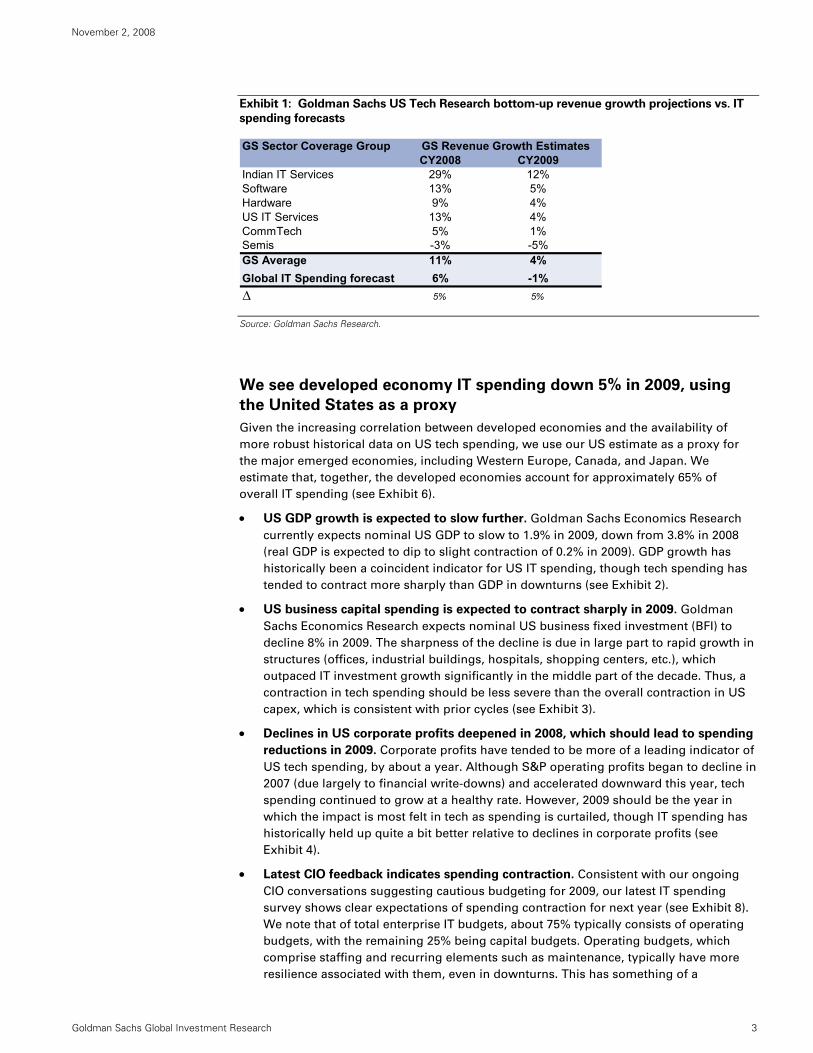

Aligning bottom-up with top-down analysis

Aligning with this IT spending forecast, each coverage group within Goldman Sachs US

Technology Research is forecasting a significant deceleration in growth in CY2009 from

the growth rates seen in CY2008 (see Exhibit 1). We note it is difficult to triangulate exactly

from a global IT spending forecast to our individual sector and company coverage growth

rates. However, directionally we are in synch, having the same delta between our forecast

and overall IT spending expectations in both CY2008 and CY2009. The delta is likely driven

by some bias on the size and quality of companies under coverage, some M&A that does

not get removed in our bottom-up builds, and finally the overall capital spending data we

use does not cover some of the more ratable and recurring revenue streams such as

software maintenance, for example.

November 2, 2008

Goldman Sachs Global Investment Research 3

Exhibit 1: Goldman Sachs US Tech Research bottom-up revenue growth projections vs. IT

spending forecasts

GS Sector Coverage Group GS Revenue Growth EstimatesCY2008 CY2009

Indian IT Services 29% 12%Software 13% 5%Hardware 9% 4%US IT Services 13% 4%CommTech 5% 1%Semis -3% -5%GS Average 11% 4%Global IT Spending forecast 6% -1%∆ 5% 5%

Source: Goldman Sachs Research.

We see developed economy IT spending down 5% in 2009, using

the United States as a proxy

Given the increasing correlation between developed economies and the availability of

more robust historical data on US tech spending, we use our US estimate as a proxy for

the major emerged economies, including Western Europe, Canada, and Japan. We

estimate that, together, the developed economies account for approximately 65% of

overall IT spending (see Exhibit 6).

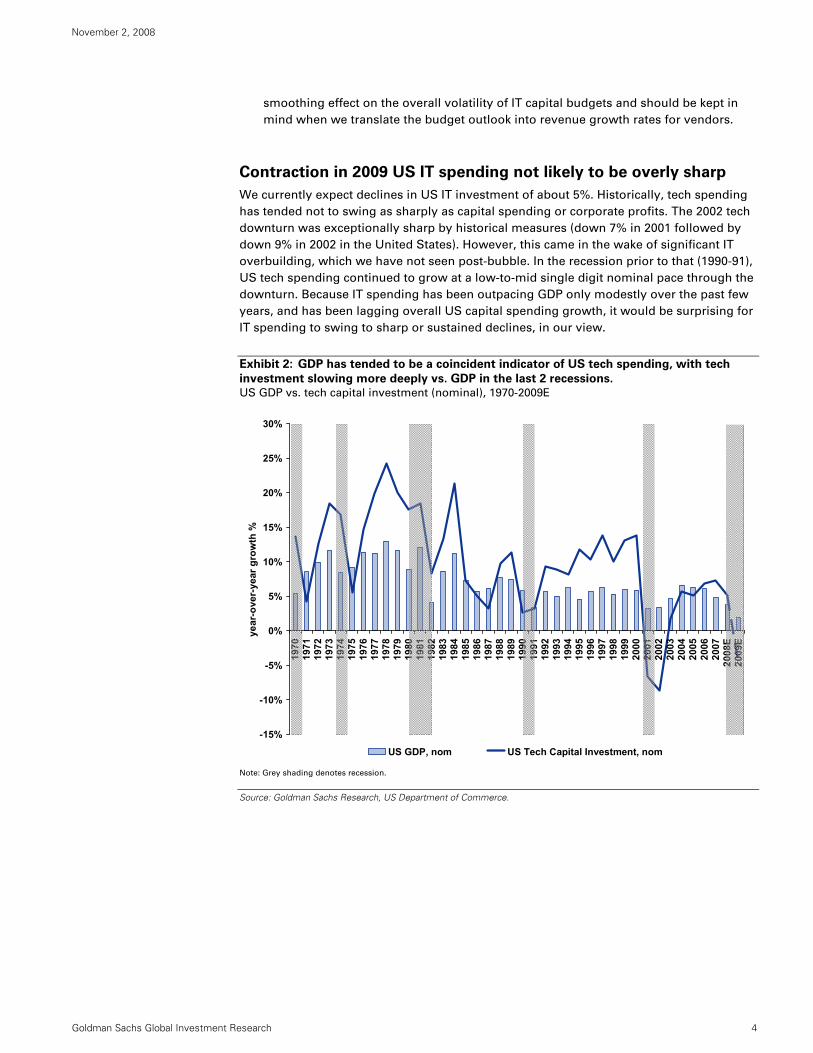

• US GDP growth is expected to slow further. Goldman Sachs Economics Research

currently expects nominal US GDP to slow to 1.9% in 2009, down from 3.8% in 2008

(real GDP is expected to dip to slight contraction of 0.2% in 2009). GDP growth has

historically been a coincident indicator for US IT spending, though tech spending has

tended to contract more sharply than GDP in downturns (see Exhibit 2).

• US business capital spending is expected to contract sharply in 2009. Goldman

Sachs Economics Research expects nominal US business fixed investment (BFI) to

decline 8% in 2009. The sharpness of the decline is due in large part to rapid growth in

structures (offices, industrial buildings, hospitals, shopping centers, etc.), which

outpaced IT investment growth significantly in the middle part of the decade. Thus, a

contraction in tech spending should be less severe than the overall contraction in US

capex, which is consistent with prior cycles (see Exhibit 3).

• Declines in US corporate profits deepened in 2008, which should lead to spending

reductions in 2009. Corporate profits have tended to be more of a leading indicator of

US tech spending, by about a year. Although S&P operating profits began to decline in

2007 (due largely to financial write-downs) and accelerated downward this year, tech

spending continued to grow at a healthy rate. However, 2009 should be the year in

which the impact is most felt in tech as spending is curtailed, though IT spending has

historically held up quite a bit better relative to declines in corporate profits (see

Exhibit 6: We estimate developed economies make up about 65% of IT spending

Estimated share of worldwide IT spending by geography, 2009E

North America30%

Western Europe27%

Japan8%

Asia/Pacific16%

Latin America7%

Middle East and Africa7%

Central & Eastern Europe5%

Source: Goldman Sachs Research, Gartner.

November 2, 2008

Goldman Sachs Global Investment Research 7

End-market demand: Almost every vertical likely to soften in 2009 given broad-based nature of macroeconomic declines

Exhibit 7: Normalized vertical end demand: Financials, communications, manufacturing,

and government are the “Big 4,” making up almost two-thirds of IT spending

Financials and manufacturing likely to see the sharpest contraction in 2009 based on feedback

from CIO conversations

Financial services, 21%

Communications, 16%

Manufacturing, 14%Government, 11%

Business services, 8%

Technology, 6%

Retail, 5%

Healthcare, 5%

Transportation, 3%

Energy & utilities, 3%

Education, 2%Other, 6%

Source: Goldman Sachs Research estimates.

Our conversations with CIOs across many verticals, as well as with management teams in

our coverage, have emphasized the broad-based nature of the current downturn, both by

vertical and by geography. Healthcare is perhaps the only vertical that still appears to be

spending at a more normalized clip, but given its small overall size within IT spending this

is unlikely to be a “needle-mover,” except at the micro level for companies particularly

exposed in that arena.

• Financials: We expect significant spending pressure. As is already well known, we

have seen tightening spending in 2008 by US and European financials companies. In

the US, most financials CIOs with whom we have spoken are planning on IT spending

being down in the range of 10-20% for 2009, with some even suggesting more than

this. We do not expect a rebound from the sector until companies can assess how the

credit and broader macro outlooks are unfolding.

• Communications: Having been one of the healthiest, comms are likely to curtail

spending in 2009. We expect the communications vertical to see about a 7% decline

in capital spending in 2009 globally given macro headwinds and following a few big

years of investment. Comms capital spending growth in 2008 was about 5% in the

United States with about 22% growth in the rest of the world (17% growth in total).

Wireline build-outs to facilitate triple-play broadband and rich audio/visual delivery in

both the home and enterprise will continue to be a focus but will slow for now.

November 2, 2008

Goldman Sachs Global Investment Research 8

• Manufacturing: Capital spending plans remain highly in flux in this vertical. However,

Goldman Sachs analysts’ best estimate is for overall capital spending to be flat to

down 10% from low to mid-single-digit growth in 2008. We expect companies to

remain conservative about the emerged economies in setting 2009 spending targets,

but would expect relatively stronger investment in international markets.

• Government: Spending is likely to soften quite a bit as well. On the local level, we

expect a more pronounced slowdown after stronger spending growth over the past

few years. Tax receipts are set to fall as housing and income impacts feed through the

local economies. At the Federal civilian level, the continuing resolution provides

authorization in civilian agencies to continue spending at 2008 levels. However, this

does impede new program starts. On the Federal DoD side, spending remains intact

and is fully funded. With an administration change, regardless of party, we would not

expect any material change in the near term as the DoD budget has already been put

into law, and the continuing resolution on the Federal Civilian is in effect through

March 2009.

• Technology and Retail: Expect spending to drop as the impact from reduced

consumer spending flows through business models. Currently, Goldman Sachs

analysts expect negative capital expenditure growth from both verticals.

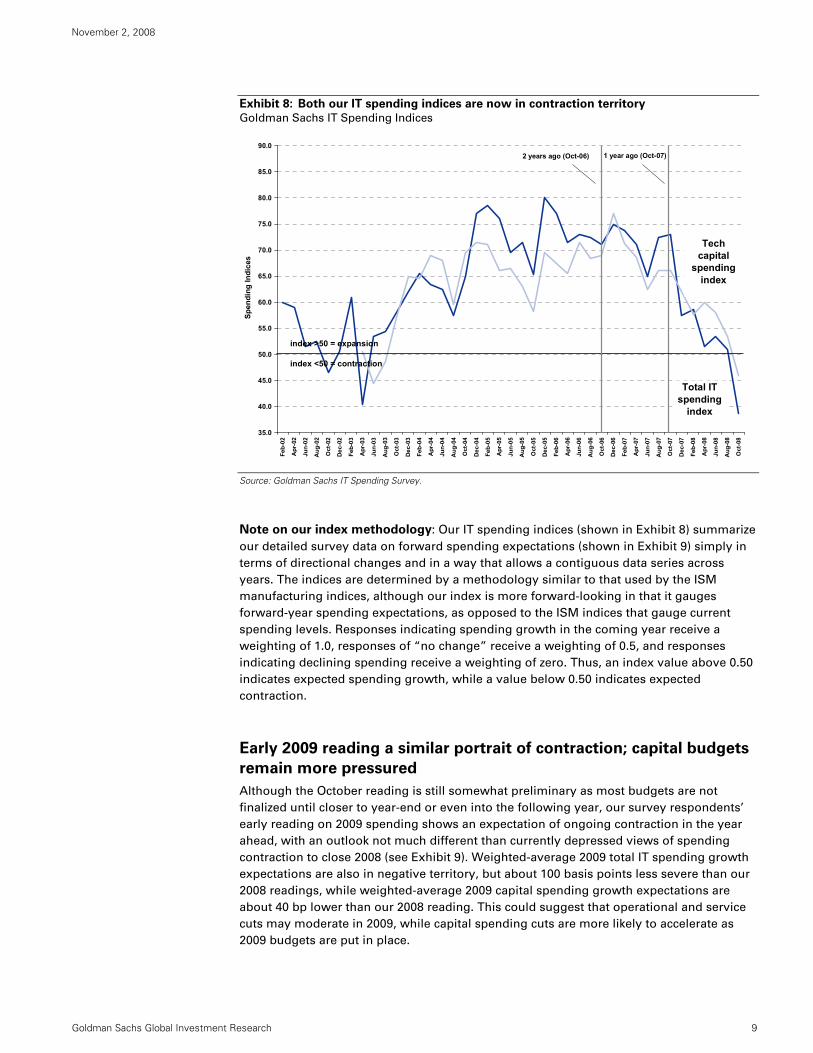

Latest IT Spending Survey results: Indices continue sharp retreat, now indicating contraction

Our IT spending indices, which measure indications of spending growth versus

spending contraction, have reached multi-year lows, now implying year-over-year

spending contraction. Our total IT spending index (which includes salaries, services,

depreciation, occupancy, etc.) came in at 38.8, down from 51.0 in our prior survey in

August, implying meaningful contraction. This reading on total IT spending is the lowest in

the history of our survey (since 2002). Our tech capital spending index (representing

spending only on new equipment and software) dropped to 45.9, versus 53.5 in our prior

survey, also dipping into contraction territory (see Exhibit 8). We note that our respondents

continue to indicate that capital spending is holding up somewhat better than overall

spending, consistent with anecdotal feedback putting contingent labor, professional and

data services at the top of the list of cut-backs. However, this likely reverses next year as

capital budgets are targeted for the next round of cost reductions. Interviews for our latest

survey were conducted in mid-October.

November 2, 2008

Goldman Sachs Global Investment Research 9

Exhibit 8: Both our IT spending indices are now in contraction territory

Goldman Sachs IT Spending Indices

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

Feb-

02

Apr

-02

Jun-

02

Aug

-02

Oct

-02

Dec

-02

Feb-

03

Apr

-03

Jun-

03

Aug

-03

Oct

-03

Dec

-03

Feb-

04

Apr

-04

Jun-

04

Aug

-04

Oct

-04

Dec

-04

Feb-

05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb-

06

Apr

-06

Jun-

06

Aug

-06

Oct

-06

Dec

-06

Feb-

07

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb-

08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Spen

ding

Indi

ces

index >50 = expansion

index <50 = contraction

Total IT spending

index

Tech capital

spending index

1 year ago (Oct-07)2 years ago (Oct-06)

Source: Goldman Sachs IT Spending Survey.

Note on our index methodology: Our IT spending indices (shown in Exhibit 8) summarize

our detailed survey data on forward spending expectations (shown in Exhibit 9) simply in

terms of directional changes and in a way that allows a contiguous data series across

years. The indices are determined by a methodology similar to that used by the ISM

manufacturing indices, although our index is more forward-looking in that it gauges

forward-year spending expectations, as opposed to the ISM indices that gauge current

spending levels. Responses indicating spending growth in the coming year receive a

weighting of 1.0, responses of “no change” receive a weighting of 0.5, and responses

indicating declining spending receive a weighting of zero. Thus, an index value above 0.50

indicates expected spending growth, while a value below 0.50 indicates expected

contraction.

Early 2009 reading a similar portrait of contraction; capital budgets

remain more pressured

Although the October reading is still somewhat preliminary as most budgets are not

finalized until closer to year-end or even into the following year, our survey respondents’

early reading on 2009 spending shows an expectation of ongoing contraction in the year

ahead, with an outlook not much different than currently depressed views of spending

contraction to close 2008 (see Exhibit 9). Weighted-average 2009 total IT spending growth

expectations are also in negative territory, but about 100 basis points less severe than our

2008 readings, while weighted-average 2009 capital spending growth expectations are

about 40 bp lower than our 2008 reading. This could suggest that operational and service

cuts may moderate in 2009, while capital spending cuts are more likely to accelerate as

2009 budgets are put in place.

November 2, 2008

Goldman Sachs Global Investment Research 10

Exhibit 9: Early indications from our Survey panel on 2009 spending suggest ongoing contraction of a similar

magnitude to current activity Underlying detail on our spending indices

Total IT Spending

21%

12%

15%

24%

15%

6% 5%

12%14%

10%

35%

21%

7%

0%0%

5%

10%

15%

20%

25%

30%

35%

40%

More than10% lower

5-10% lower Down lessthan 5%

About thesame

Up less than5%

5-10%higher

More than10% higher

% o

f Res

pond

ents

2008 2009

IT Capital Spending

20%

11%

6%

34%

13%

8% 7%

17%

13% 13%

39%

13%

3% 4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

More than10% lower

5-10% lower Down lessthan 5%

About thesame

Up less than5%

5-10%higher

More than10% higher

% o

f Res

pond

ents

2008 2009

Source: Goldman Sachs IT Spending Survey.

Exhibit 10: What is your current expectation of US economic conditions in 2009 relative to

2008?

Oct-08 Oct-07 Oct-06Stronger 11% 18% 25%Weaker 56% 38% 29%About the same 33% 43% 46%

Source: Goldman Sachs IT Spending Survey.

Clearly, CIO views on the economy are driving their views on budget decisions.

November 2, 2008

Goldman Sachs Global Investment Research 11

Fourth quarter budget flush likely capped, as even 2008 budgets

come under the knife

Exhibit 11: How have your IT budget expectations for 2008 changed in the past three

months?

18%

10%

24%

39%

6%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Down greater than 10%

Down 5-10%

Down 0-5%

Unchanged

Up 0-5%

Up 5-10%

% of respondents

Source: Goldman Sachs IT Spending Survey.

Exhibit 12: Which of the following best characterizes your spending intentions through

the end of the current calendar year?

Oct-08 Oct-07 Oct-06 Oct-05Our end-of-year IT spending activity will be similar to recent years 42% 57% 67% 55%Our end-of-year IT spending activity will be greater than recent years 17% 28% 24% 24%Our end-of-year IT spending activity will be less than recent years 41% 15% 9% 21%

Source: Goldman Sachs IT Spending Survey.

Volatile pricing index recovers somewhat but remains at depressed

levels

Our panel suggests pricing discounts remain fairly aggressive. Vendors seem to be

remaining flexible with respect to pricing in an effort to buoy demand in the current

environment (see Exhibit 13). In general, we believe that this favors larger solution

providers who can offer attractive pricing and payment terms on bundles of products

relative to smaller “best-of-breed” vendors who may lack similar flexibility. From an

investment perspective, we believe that this benefits companies such as Cisco, IBM,

and Oracle. Pricing is more likely to be an issue for more focused “best-of-breeds”

such as Aruba Networks, Lexmark, NetSuite, Network Appliance, Riverbed,

salesforce.com, and TIBCO.

52% of respondents have seen budgets decrease for 2008 in the past three months, likely dampening any sort of 4Q budget flush.

In addition, responses paint a tempered view directly on 4Q budget activity.

November 2, 2008

Goldman Sachs Global Investment Research 12

Exhibit 13: Our pricing index is based on respondents’ indications of increasing or

decreasing discounting by vendors to close business

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

Apr-04

Jun-04

Aug-04

Oct-04

Dec-04

Feb-05

Apr-05

Jun-05

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-06

Aug-06

Oct-06

Dec-06

Feb-07

Apr-07

Jun-07

Aug-07

Oct-07

Dec-07

Feb-08

Apr-08

Jun-08

Aug-08

Oct-08

Pric

ing

Inde

x

IT Pricing Index

Higher index value = firmer pricing, benefiting vendors

Lower index value = softer pricing / more discounting

Source: Goldman Sachs IT Spending Survey.

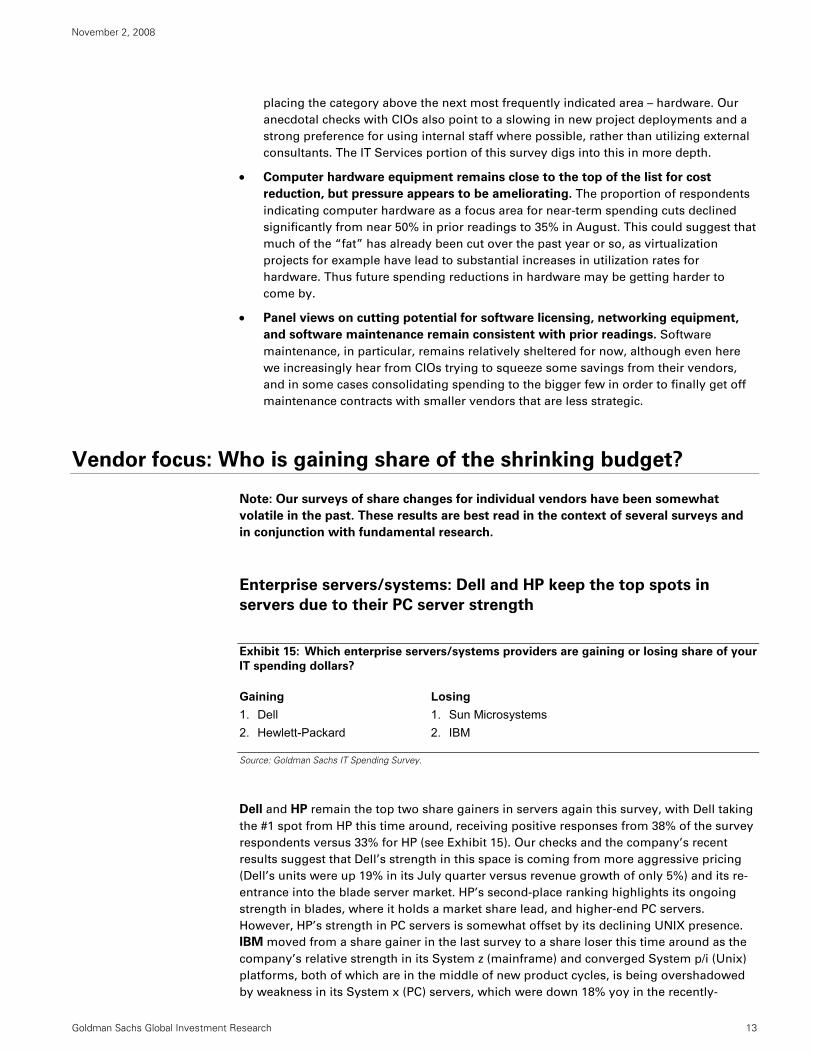

Segment focus: Professional services and hardware tend to be a top focus for spending cuts

We alternate how often we ask questions and hence the segment focus was not updated in

this current round of questions. However, to put the next section on vendor focus in

perspective we are reprising the data from our August survey on how each segment tends

to be viewed by our CIO population as they look for cost reduction (see Exhibit 14).

Exhibit 14: In terms of where your organization sees the greatest potential for cost

reduction in your IT organization, please specify the areas in which you expect to see the

greatest proportion of cost reduction over the next 12 months. Answer all that apply.

In a relatively short 12-month period, our survey respondents expect to dramatically

increase the percentage of their PC servers that are virtualized. On a weighted average

basis, 34% of PC servers should be virtualized a year from now, more than double the 15%

that are virtualized today. More striking, 45% of our respondents expect to virtualize over

30% of their servers, up from just 7% today, suggesting a much more aggressive

penetration of virtualization compared to what we have seen to date. Our sense is that

total cost of ownership (TCO) reductions will be a key driver of the acceleration in server

virtualization deployments as CIOs are forced to cut capital spending and reign in

management, administrative, and power/cooling costs. In our VMware initiation (“Still the

aggressor, but slowing growth & valuation a drag”; published August 11, 2008), our base-

case analysis showed a 30% reduction in TCO, while a higher compression ratio of

physical to virtual servers would allow the savings to increase to 45%-50%. Avoidance of

PC server purchases is the largest source of savings, followed by reduced management

and support costs which more than offset the incremental investment in the server

virtualization software/support itself and storage.

November 2, 2008

Goldman Sachs Global Investment Research 19

Despite the emergence of new competition, VMware should

maintain a large lead over the next two years

Exhibit 22: Who do you currently view as your primary server virtualization providers /

enablers? What do you expect 2 years from now?

82

13

50 1 1 3

79

16 15

2 1 1 3

0

10

20

30

40

50

60

70

80

90

VMware Citrix(XenSource)

Microsoft Oracle Sun Red Hat Incumbentsystems

managementprovider

# of

resp

onde

nts

Current In 2 years

Source: Goldman Sachs IT Spending Survey.

VMware should continue to dominate the market for server virtualization software over the

next two years, with 79 of our respondents selecting the company as their primary

provider in this high-priority segment, roughly the same number as today. Our checks

continue to be overwhelmingly positive for VMware from both a product and support point

of view. While Microsoft and Citrix have become more competitive in the hypervisor

space, VMware’s suite of advanced management tools and its large number of third-party

software partners set it apart from the competition. At the same time, it appears that

customers will begin to add additional server virtualization solutions into their

environments, with both Citrix and, more dramatically, Microsoft gaining share. In the

next two years, just over 30% of our survey respondents expect to deploy server

virtualization from Citrix and Microsoft, up from 18% today.

November 2, 2008

Goldman Sachs Global Investment Research 20

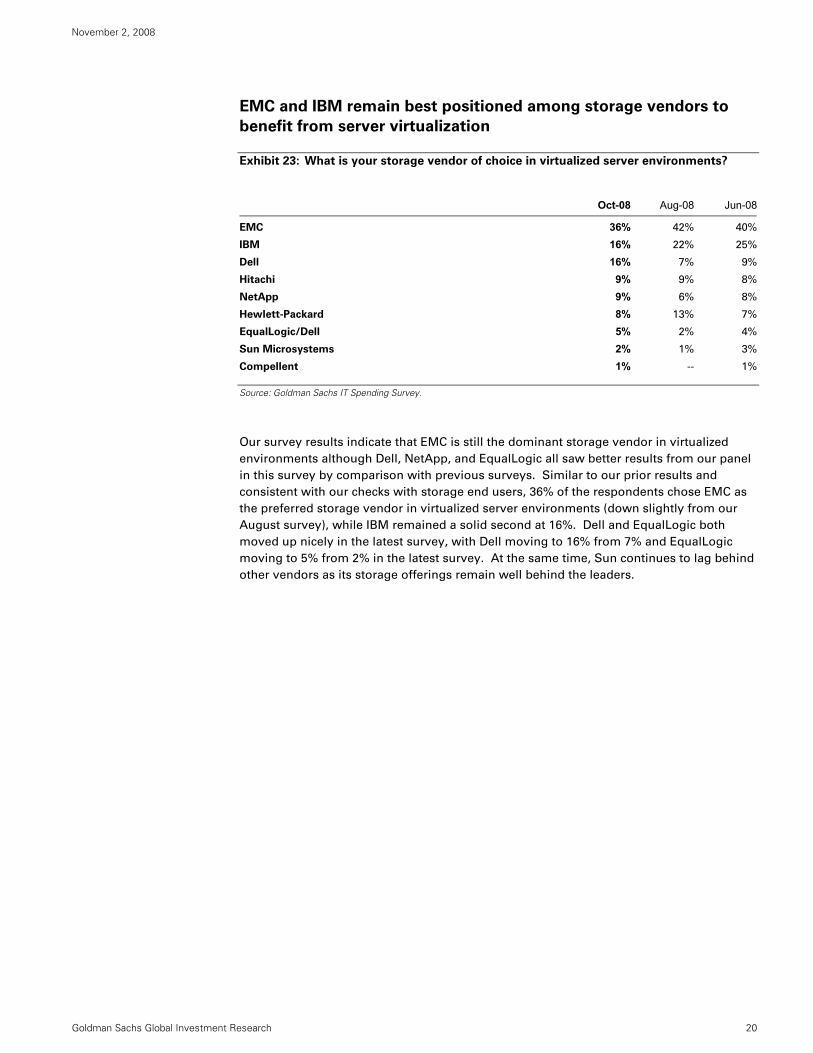

EMC and IBM remain best positioned among storage vendors to

benefit from server virtualization

Exhibit 23: What is your storage vendor of choice in virtualized server environments?

Oct-08 Aug-08 Jun-08

EMC 36% 42% 40%

IBM 16% 22% 25%

Dell 16% 7% 9%

Hitachi 9% 9% 8%

NetApp 9% 6% 8%

Hewlett-Packard 8% 13% 7%

EqualLogic/Dell 5% 2% 4%

Sun Microsystems 2% 1% 3%

Compellent 1% -- 1%

Source: Goldman Sachs IT Spending Survey.

Our survey results indicate that EMC is still the dominant storage vendor in virtualized

environments although Dell, NetApp, and EqualLogic all saw better results from our panel

in this survey by comparison with previous surveys. Similar to our prior results and

consistent with our checks with storage end users, 36% of the respondents chose EMC as

the preferred storage vendor in virtualized server environments (down slightly from our

August survey), while IBM remained a solid second at 16%. Dell and EqualLogic both

moved up nicely in the latest survey, with Dell moving to 16% from 7% and EqualLogic

moving to 5% from 2% in the latest survey. At the same time, Sun continues to lag behind

other vendors as its storage offerings remain well behind the leaders.

November 2, 2008

Goldman Sachs Global Investment Research 21

Sub-sector focus: Software

Software spending weakened; now in-line with overall budget

expectations

Exhibit 24: In terms of your overall software spending, what do you expect to be the most

likely scenario over the next 12 months?

5%

23%

34%

16%

22%

14%

26%

33%

12%

15%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Up more than 10%

Up 1 to 10%

Same / flat

Down 1 to 10%

Down more than 10%

% of respondents

Oct-08 Aug-08

Source: Goldman Sachs IT Spending Survey.

We are beginning a bi-monthly tracker for software spending. In this second installment,

28% of our respondents are expecting increased software spending over the next year,

well down from the 40% reading in the last survey. This compares to 38% expecting a

decrease, up from 27% in our last survey. Clearly shifting lower, software now ranks about

in line with the overall expectations for IT spending in 2009. However, the change in

sentiment from the last survey is worrying, and suggests that even with the stickiness of

elements such as maintenance and support requirements, software will be cut as budgets

are cut.

Analysis by Goldman Sachs’ Software Research Team, led by Sarah Friar, Sasa Zorovic, and Derek Bingham.

November 2, 2008

Goldman Sachs Global Investment Research 22

Microsoft stronger than overall expectations; new product cycles

likely helping

Exhibit 25: In terms of your level of spending with Microsoft, what do you expect to be

the most likely scenario over the next 12 months?

Up 21 to 50% 3%

Up 11 to 20% 5%

Up 1 to 10% 33%

Same / flat 37%

Down 1 to 10% 5%

Down 11 to 20% 13%

Down 21 to 50% 5%

Source: Goldman Sachs IT Spending Survey.

Among applicable respondents, 41% indicate an expectation of spending growth with

Microsoft over the coming year vs. 23% indicating contraction, a somewhat stronger ratio

of increases to decreases than for software spending as a whole (in the prior exhibit). This

is consistent Microsoft’s lift in the overall software share gainers and laggards. Overall,

we would expect Microsoft to continue to consolidate share, and upgrade cycles such as

Windows Server 2008, SQL Server, and traction with SharePoint Server should continue to

provide momentum to the company’s Server and Tools division – the key area we think

CIOs are responding to in the survey. See Exhibit 26.

Exhibit 26: In the next twelve months, please indicate how you expect your spending will

change for the following Microsoft products, if applicable.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Forefront Security Offerings

System Center (managementofferings)

Search

Exchange Server

Dynamics Apps (including CRM)

Office

Vista

Communications Server

SharePoint Server

Windows Server (including Hyper-V)

SQL Server

Increase No Change Reduce

Source: Goldman Sachs IT Spending Survey.

November 2, 2008

Goldman Sachs Global Investment Research 23

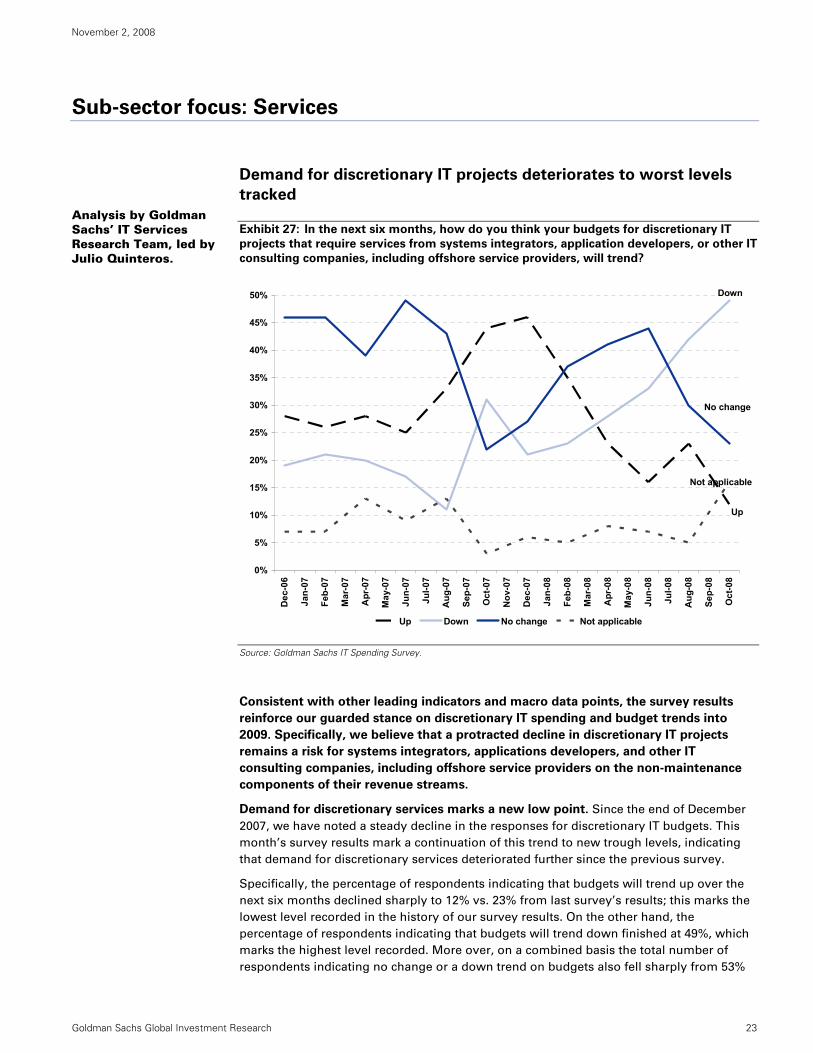

Sub-sector focus: Services

Demand for discretionary IT projects deteriorates to worst levels

tracked

Exhibit 27: In the next six months, how do you think your budgets for discretionary IT

projects that require services from systems integrators, application developers, or other IT

consulting companies, including offshore service providers, will trend?

Not applicable

Up

Down

No change

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%D

ec-0

6

Jan-

07

Feb-

07

Mar

-07

Apr

-07

May

-07

Jun-

07

Jul-0

7

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

Oct

-08

Up Down No change Not applicable

Source: Goldman Sachs IT Spending Survey.

Consistent with other leading indicators and macro data points, the survey results

reinforce our guarded stance on discretionary IT spending and budget trends into

2009. Specifically, we believe that a protracted decline in discretionary IT projects

remains a risk for systems integrators, applications developers, and other IT

consulting companies, including offshore service providers on the non-maintenance

components of their revenue streams.

Demand for discretionary services marks a new low point. Since the end of December

2007, we have noted a steady decline in the responses for discretionary IT budgets. This

month’s survey results mark a continuation of this trend to new trough levels, indicating

that demand for discretionary services deteriorated further since the previous survey.

Specifically, the percentage of respondents indicating that budgets will trend up over the

next six months declined sharply to 12% vs. 23% from last survey’s results; this marks the

lowest level recorded in the history of our survey results. On the other hand, the

percentage of respondents indicating that budgets will trend down finished at 49%, which

marks the highest level recorded. More over, on a combined basis the total number of

respondents indicating no change or a down trend on budgets also fell sharply from 53%

Analysis by Goldman Sachs’ IT Services Research Team, led by Julio Quinteros.

November 2, 2008

Goldman Sachs Global Investment Research 24

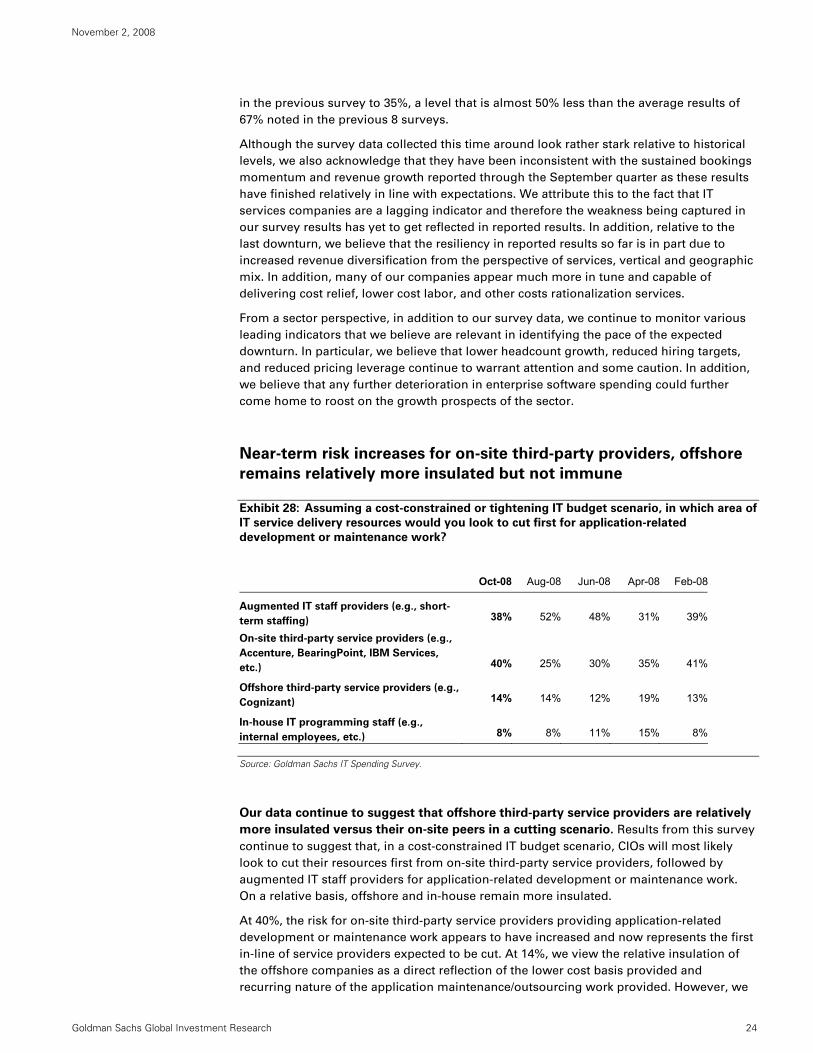

in the previous survey to 35%, a level that is almost 50% less than the average results of

67% noted in the previous 8 surveys.

Although the survey data collected this time around look rather stark relative to historical

levels, we also acknowledge that they have been inconsistent with the sustained bookings

momentum and revenue growth reported through the September quarter as these results

have finished relatively in line with expectations. We attribute this to the fact that IT

services companies are a lagging indicator and therefore the weakness being captured in

our survey results has yet to get reflected in reported results. In addition, relative to the

last downturn, we believe that the resiliency in reported results so far is in part due to

increased revenue diversification from the perspective of services, vertical and geographic

mix. In addition, many of our companies appear much more in tune and capable of

delivering cost relief, lower cost labor, and other costs rationalization services.

From a sector perspective, in addition to our survey data, we continue to monitor various

leading indicators that we believe are relevant in identifying the pace of the expected

downturn. In particular, we believe that lower headcount growth, reduced hiring targets,

and reduced pricing leverage continue to warrant attention and some caution. In addition,

we believe that any further deterioration in enterprise software spending could further

come home to roost on the growth prospects of the sector.

Near-term risk increases for on-site third-party providers, offshore

remains relatively more insulated but not immune

Exhibit 28: Assuming a cost-constrained or tightening IT budget scenario, in which area of

IT service delivery resources would you look to cut first for application-related

development or maintenance work?

Oct-08 Aug-08 Jun-08 Apr-08 Feb-08

Augmented IT staff providers (e.g., short-

term staffing) 38% 52% 48% 31% 39%

On-site third-party service providers (e.g.,

Accenture, BearingPoint, IBM Services,

etc.) 40% 25% 30% 35% 41%

Offshore third-party service providers (e.g.,

Cognizant) 14% 14% 12% 19% 13%

In-house IT programming staff (e.g.,

internal employees, etc.) 8% 8% 11% 15% 8%

Source: Goldman Sachs IT Spending Survey.

Our data continue to suggest that offshore third-party service providers are relatively

more insulated versus their on-site peers in a cutting scenario. Results from this survey

continue to suggest that, in a cost-constrained IT budget scenario, CIOs will most likely

look to cut their resources first from on-site third-party service providers, followed by

augmented IT staff providers for application-related development or maintenance work.

On a relative basis, offshore and in-house remain more insulated.

At 40%, the risk for on-site third-party service providers providing application-related

development or maintenance work appears to have increased and now represents the first

in-line of service providers expected to be cut. At 14%, we view the relative insulation of

the offshore companies as a direct reflection of the lower cost basis provided and

recurring nature of the application maintenance/outsourcing work provided. However, we

November 2, 2008

Goldman Sachs Global Investment Research 25

continue to believe that the more discretionary application development work, which

makes up 40% of revenue remains relatively exposed and is the source behind the rapid

decrease in revenue growth for most offshore vendors.

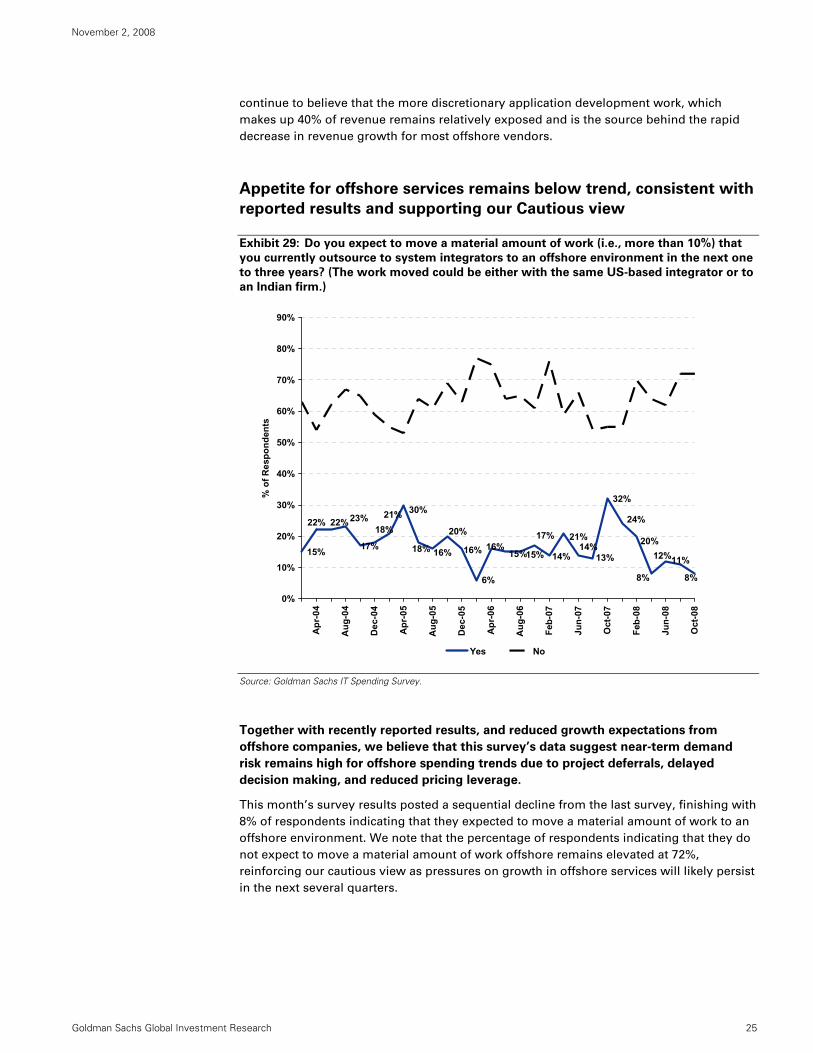

Appetite for offshore services remains below trend, consistent with

reported results and supporting our Cautious view

Exhibit 29: Do you expect to move a material amount of work (i.e., more than 10%) that

you currently outsource to system integrators to an offshore environment in the next one

to three years? (The work moved could be either with the same US-based integrator or to

an Indian firm.)

32%

6%

15% 15%15%

20%

16%

21%23%22%22%

20%

8%

16% 16%21%

24%

18%

30%

18%

17%12%

8%

11%13%14%

17%

14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Oct

-08

Jun-

08

Feb-

08

Oct

-07

Jun-

07

Feb-

07

Aug

-06

Apr

-06

Dec

-05

Aug

-05

Apr

-05

Dec

-04

Aug

-04

Apr

-04

% o

f Res

pond

ents

Yes No

Source: Goldman Sachs IT Spending Survey.

Together with recently reported results, and reduced growth expectations from

offshore companies, we believe that this survey’s data suggest near-term demand

risk remains high for offshore spending trends due to project deferrals, delayed

decision making, and reduced pricing leverage.

This month’s survey results posted a sequential decline from the last survey, finishing with

8% of respondents indicating that they expected to move a material amount of work to an

offshore environment. We note that the percentage of respondents indicating that they do

not expect to move a material amount of work offshore remains elevated at 72%,

reinforcing our cautious view as pressures on growth in offshore services will likely persist

in the next several quarters.

November 2, 2008

Goldman Sachs Global Investment Research 26

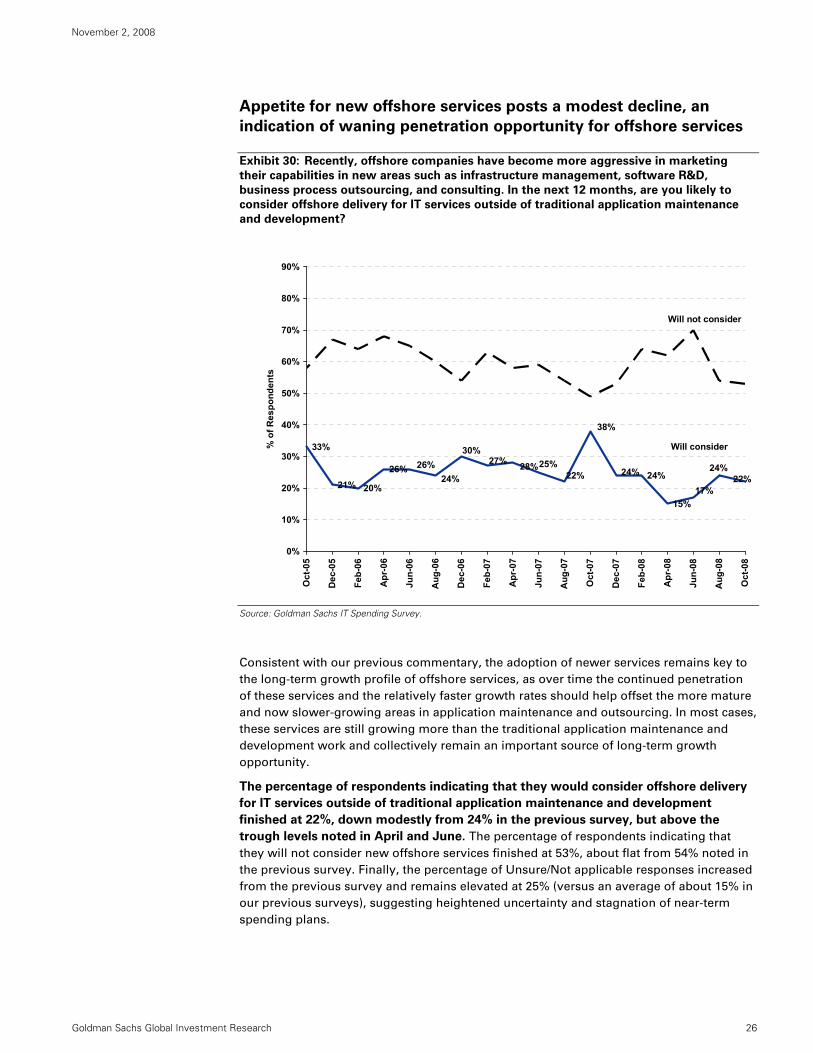

Appetite for new offshore services posts a modest decline, an

indication of waning penetration opportunity for offshore services

Exhibit 30: Recently, offshore companies have become more aggressive in marketing

their capabilities in new areas such as infrastructure management, software R&D,

business process outsourcing, and consulting. In the next 12 months, are you likely to

consider offshore delivery for IT services outside of traditional application maintenance

and development?

15%

24%26%

20%21%

33%

17%22%

24%22%

25%30%

27%24%

38%

28%24%

26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Oct

-08

Aug

-08

Jun-

08

Apr

-08

Feb-

08

Dec

-07

Oct

-07

Aug

-07

Jun-

07

Apr

-07

Feb-

07

Dec

-06

Aug

-06

Jun-

06

Apr

-06

Feb-

06

Dec

-05

Oct

-05

% o

f Res

pond

ents

Will consider

Will not consider

Source: Goldman Sachs IT Spending Survey.

Consistent with our previous commentary, the adoption of newer services remains key to

the long-term growth profile of offshore services, as over time the continued penetration

of these services and the relatively faster growth rates should help offset the more mature

and now slower-growing areas in application maintenance and outsourcing. In most cases,

these services are still growing more than the traditional application maintenance and

development work and collectively remain an important source of long-term growth

opportunity.

The percentage of respondents indicating that they would consider offshore delivery

for IT services outside of traditional application maintenance and development

finished at 22%, down modestly from 24% in the previous survey, but above the

trough levels noted in April and June. The percentage of respondents indicating that

they will not consider new offshore services finished at 53%, about flat from 54% noted in

the previous survey. Finally, the percentage of Unsure/Not applicable responses increased

from the previous survey and remains elevated at 25% (versus an average of about 15% in

our previous surveys), suggesting heightened uncertainty and stagnation of near-term

spending plans.

November 2, 2008

Goldman Sachs Global Investment Research 27

Sub-sector focus: Networking

Network equipment spending resumed its downward trend in

October following the rebound in August

Exhibit 31: In terms of your overall network equipment spending, what do you expect to

be the most likely scenario over the next 12 months?

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dec-03

Feb-04

Apr-04

Jun-04

Aug-04

Oct-04

Dec-04

Feb-05

Apr-05

Jun-05

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-06

Aug-06

Jan-07

Feb-07

Apr-07

June-0

7

Aug-07

Oct-07

Dec-07

Feb-08

Apr-08

Jun-08

Aug-08

Oct-08

% o

f Res

pond

ents

Down

Up

Flat

Unsure

Source: Goldman Sachs IT Spending Survey.

As in past surveys, we asked our respondents about their plans for overall network

equipment spending over the next 12 months. The responses reflect a deteriorating

environment, with a meaningful drop in the percentage of respondents who expect their

spending to increase from 53% in August to 48% in October. In addition, the percentage of

respondents who expect their spending to decline increased from 13% to 19%. The

findings from the survey are consistent with our belief that given the increased probability

that we are now in a recession, overall network spending will likely decline in the United

States over the next several quarters. The findings are consistent with our below-

consensus estimates for companies in our coverage with significant enterprise networking

exposure, such as Cisco, Juniper, Riverbed, and Aruba Networks. We recommend that

investors remain on the sidelines for all these stocks except for Cisco, where we believe

the impact to estimates will be partially muted by the company’s continued share gains, as

CIOs continue to consolidate their spending around their largest, and most strategic

vendors.

Analysis by Goldman Sachs’ Networking Research Team, led by Simona Jankowski and Thomas Lee.

November 2, 2008

Goldman Sachs Global Investment Research 28

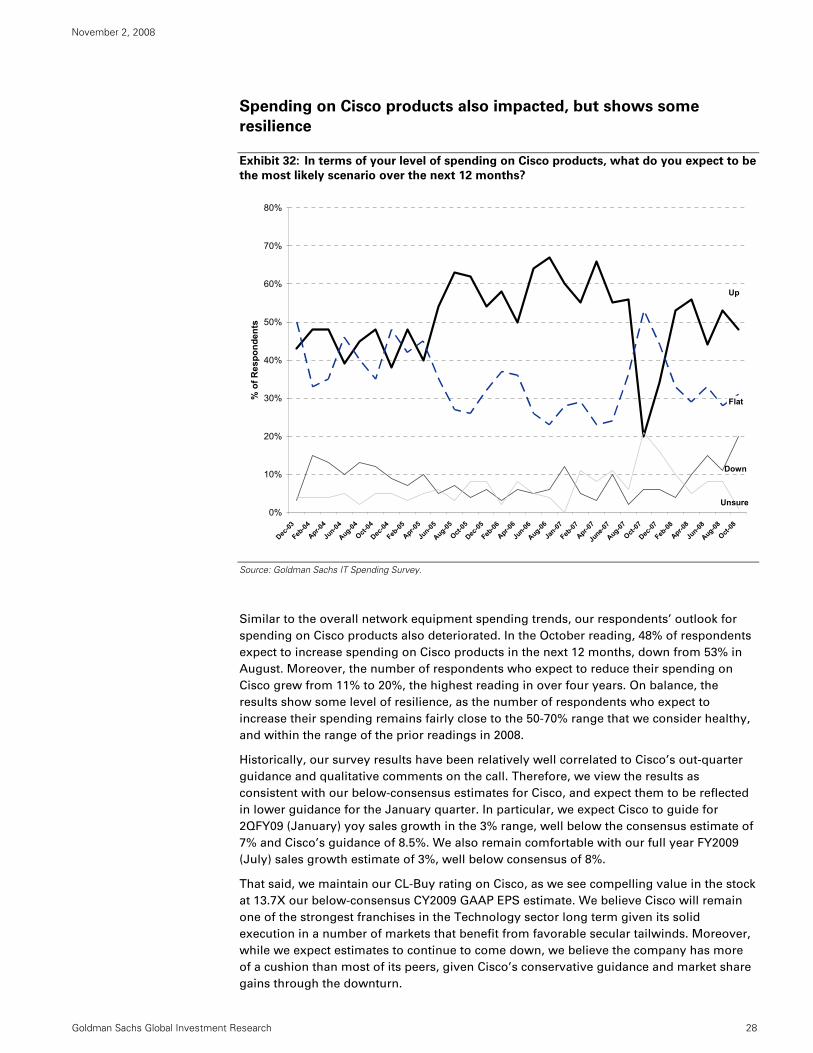

Spending on Cisco products also impacted, but shows some

resilience

Exhibit 32: In terms of your level of spending on Cisco products, what do you expect to be

the most likely scenario over the next 12 months?

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dec-03

Feb-04

Apr-04

Jun-04

Aug-04

Oct-04

Dec-04

Feb-05

Apr-05

Jun-05

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-06

Aug-06

Jan-07

Feb-07

Apr-07

June-0

7

Aug-07

Oct-07

Dec-07

Feb-08

Apr-08

Jun-08

Aug-08

Oct-08

% o

f Res

pond

ents

Down

Up

Flat

Unsure

Source: Goldman Sachs IT Spending Survey.

Similar to the overall network equipment spending trends, our respondents’ outlook for

spending on Cisco products also deteriorated. In the October reading, 48% of respondents

expect to increase spending on Cisco products in the next 12 months, down from 53% in

August. Moreover, the number of respondents who expect to reduce their spending on

Cisco grew from 11% to 20%, the highest reading in over four years. On balance, the

results show some level of resilience, as the number of respondents who expect to

increase their spending remains fairly close to the 50-70% range that we consider healthy,

and within the range of the prior readings in 2008.

Historically, our survey results have been relatively well correlated to Cisco’s out-quarter

guidance and qualitative comments on the call. Therefore, we view the results as

consistent with our below-consensus estimates for Cisco, and expect them to be reflected

in lower guidance for the January quarter. In particular, we expect Cisco to guide for

2QFY09 (January) yoy sales growth in the 3% range, well below the consensus estimate of

7% and Cisco’s guidance of 8.5%. We also remain comfortable with our full year FY2009

(July) sales growth estimate of 3%, well below consensus of 8%.

That said, we maintain our CL-Buy rating on Cisco, as we see compelling value in the stock

at 13.7X our below-consensus CY2009 GAAP EPS estimate. We believe Cisco will remain

one of the strongest franchises in the Technology sector long term given its solid

execution in a number of markets that benefit from favorable secular tailwinds. Moreover,

while we expect estimates to continue to come down, we believe the company has more

of a cushion than most of its peers, given Cisco’s conservative guidance and market share

gains through the downturn.

November 2, 2008

Goldman Sachs Global Investment Research 29

Incrementally negative for RIM: Interest in Microsoft-based devices

accelerating with iPhone steadily improving

We asked our respondents about their plans to deploy wireless email devices over the next

12 months. The October results were incrementally negative for RIM on three fronts.

• Interest in BlackBerry only deployments decreased significantly since August. The

percentage of respondents expecting to offer only BlackBerry devices to their

employee base declined significantly to 32% from 44% in August.

• Interest in Microsoft-enabled devices increased significantly since August. The

percentage of respondents who are currently using BlackBerry devices but will also

enable Microsoft-based devices increased considerably to 26% from 16% in August.

These results are consistent with our checks that an increasing number of enterprises

are looking at Microsoft as a potential second source of their wireless email

deployment, due to their desire to diversify their wireless e-mail supplier base.

Additionally, with a number of key smartphone vendors adopting Microsoft as their

business OS (HTC, Motorola, Palm), we believe lower smartphone ASPs (driven by a

wider availability of devices) could be another reason why enterprises are taking a

greater interest in Microsoft-enabled devices.

• iPhone adoption continues to gain traction. Interest in the Apple iPhone continued

to increase as 10% of our respondents said they will enable iPhone devices alongside

BlackBerry compared to 8% in August and 4% in June. This is also consistent with our

anecdotal checks which reveal that some enterprises may be looking to enable the

iPhone as part of their wireless device fleets.

Lastly, unlike the last few surveys, we saw a much greater number of respondents that

were NA/Unsure (10% vs 0% in August/June) about their plans for email device

deployment over the next 12 months. We believe this is likely attributed to the level of

uncertainty that CIOs have about their current IT budgets given the present macro

environment. CIOs may look curtail spending on new wireless email devices by either

lengthening the replacement cycle and/or delaying purchases for new wireless email

devices.

While the IT survey results have negative implications for RIM’s enterprise business, we

continue to believe that RIM will still maintain a strong position in this segment though it

may cede some of its dominant share in North America to Microsoft-based devices and the

iPhone over the next few years. We believe the decrease in share will more than likely be

offset by an overall increase in penetration of wireless e-mail in enterprises, which

currently stands at only 5% of a base of 600 million enterprise e-mail accounts. As the

overall market penetration expands, in particular outside North America, we expect RIM

will continue to benefit from strong growth in that segment despite having to share some

of the incremental market growth with Microsoft/Apple.

November 2, 2008

Goldman Sachs Global Investment Research 30

Exhibit 33: What wireless email devices do you plan to deploy over the next 12 months?

0%

4%

8%

3%

6%

6%

4%

23%

46%

0%

5%

10%

5%

6%

6%

8%

16%

44%

10%

2%

6%

2%

5%

7%

10%

26%

32%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

NA/Unsure

We do not plan to deploy anywireless email devices over the next

12 months

We currently use a combination ofdevices

We currently use Microsoft-baseddevices but will also enable iPhone

We currently use Microsoft-baseddevices but will also enable

BlackBerry

Microsoft-based devices only

We currently use BlackBerry but willalso enable iPhone

We currently use BlackBerry but willalso enable Microsoft-based devices

BlackBerry only

% of total responses

June August October

Source: Goldman Sachs IT Spending Survey.

Enterprise outlook for RIM remains weak

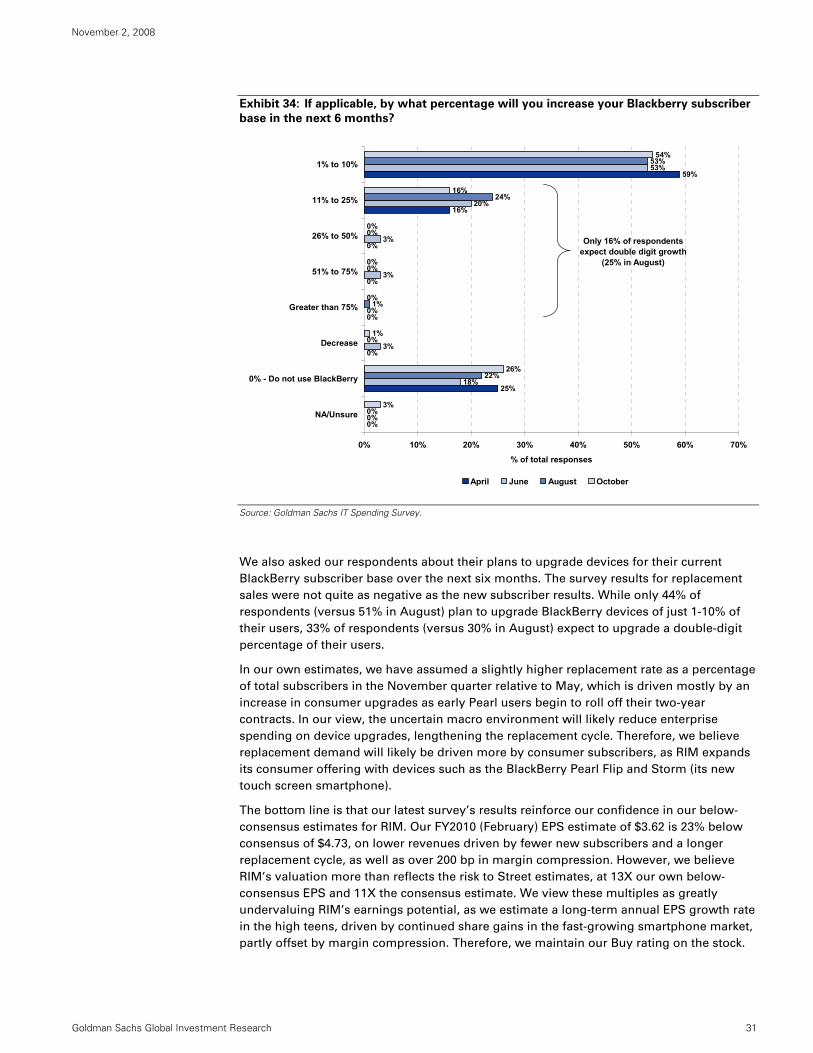

We asked our respondents about their plans to increase their BlackBerry subscriber base

over the next six months. The survey results suggest a negative outlook, as 16% of our

respondents (versus 25% in the August survey) expect their subscriber base to grow

double digits over the next six months. The distribution of responses within that

percentage continues to be unfavorable, with 0% of subscribers (down from 1% in August

and 6% in June) expecting to increase their subscriber base by over 26%. We believe our

November quarter estimates are inline with the survey results as we are forecasting RIM’s

enterprise subscribers to grow only 1% qoq, compared to 8% in the August quarter.

Similar to the above question, we believe the current macro headwinds are causing

increased uncertainty with CIOs, as 3% of respondents were unsure about their 6-month

outlook, compared to 0% in the prior three readings.

November 2, 2008

Goldman Sachs Global Investment Research 31

Exhibit 34: If applicable, by what percentage will you increase your Blackberry subscriber

base in the next 6 months?

0%

25%

0%

0%

0%

0%

16%

59%

0%

18%

3%

0%

3%

3%

20%

53%

0%

22%

0%

1%

0%

0%

24%

53%

3%

26%

1%

0%

0%

0%

16%

54%

0% 10% 20% 30% 40% 50% 60% 70%

NA/Unsure

0% - Do not use BlackBerry

Decrease

Greater than 75%

51% to 75%

26% to 50%

11% to 25%

1% to 10%

% of total responses

April June August October

Only 16% of respondents expect double digit growth

(25% in August)

Source: Goldman Sachs IT Spending Survey.

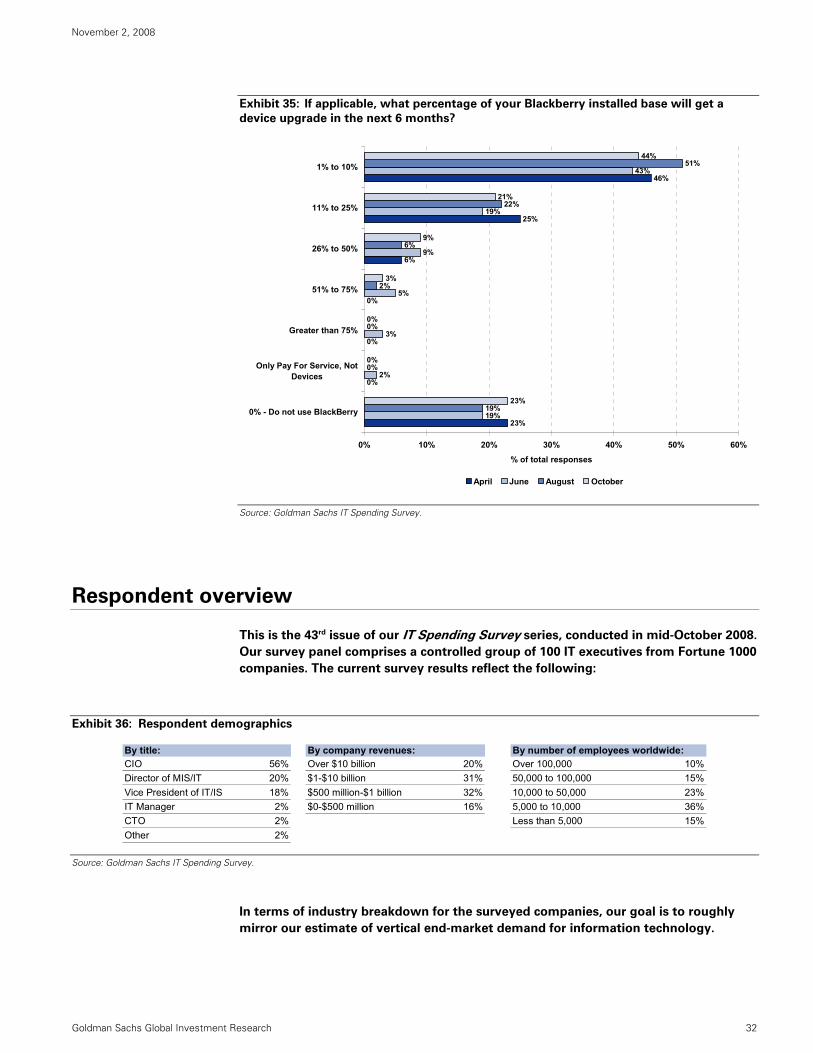

We also asked our respondents about their plans to upgrade devices for their current

BlackBerry subscriber base over the next six months. The survey results for replacement

sales were not quite as negative as the new subscriber results. While only 44% of

respondents (versus 51% in August) plan to upgrade BlackBerry devices of just 1-10% of

their users, 33% of respondents (versus 30% in August) expect to upgrade a double-digit

percentage of their users.

In our own estimates, we have assumed a slightly higher replacement rate as a percentage

of total subscribers in the November quarter relative to May, which is driven mostly by an

increase in consumer upgrades as early Pearl users begin to roll off their two-year

contracts. In our view, the uncertain macro environment will likely reduce enterprise

spending on device upgrades, lengthening the replacement cycle. Therefore, we believe

replacement demand will likely be driven more by consumer subscribers, as RIM expands

its consumer offering with devices such as the BlackBerry Pearl Flip and Storm (its new

touch screen smartphone).

The bottom line is that our latest survey’s results reinforce our confidence in our below-

consensus estimates for RIM. Our FY2010 (February) EPS estimate of $3.62 is 23% below

consensus of $4.73, on lower revenues driven by fewer new subscribers and a longer

replacement cycle, as well as over 200 bp in margin compression. However, we believe

RIM’s valuation more than reflects the risk to Street estimates, at 13X our own below-

consensus EPS and 11X the consensus estimate. We view these multiples as greatly

undervaluing RIM’s earnings potential, as we estimate a long-term annual EPS growth rate

in the high teens, driven by continued share gains in the fast-growing smartphone market,

partly offset by margin compression. Therefore, we maintain our Buy rating on the stock.

November 2, 2008

Goldman Sachs Global Investment Research 32

Exhibit 35: If applicable, what percentage of your Blackberry installed base will get a

device upgrade in the next 6 months?

23%

0%

0%

0%

6%

25%

46%

19%

2%

3%

5%

9%

19%

43%

19%

0%

0%

2%

6%

22%

51%

23%

0%

0%

3%

9%

21%

44%

0% 10% 20% 30% 40% 50% 60%

0% - Do not use BlackBerry

Only Pay For Service, NotDevices

Greater than 75%

51% to 75%

26% to 50%

11% to 25%

1% to 10%

% of total responses

April June August October

Source: Goldman Sachs IT Spending Survey.

Respondent overview

This is the 43rd issue of our IT Spending Survey series, conducted in mid-October 2008.

Our survey panel comprises a controlled group of 100 IT executives from Fortune 1000

companies. The current survey results reflect the following:

Exhibit 36: Respondent demographics

By title: By company revenues: By number of employees worldwide:CIO 56% Over $10 billion 20% Over 100,000 10%Director of MIS/IT 20% $1-$10 billion 31% 50,000 to 100,000 15%Vice President of IT/IS 18% $500 million-$1 billion 32% 10,000 to 50,000 23%IT Manager 2% $0-$500 million 16% 5,000 to 10,000 36%CTO 2% Less than 5,000 15%Other 2%

Source: Goldman Sachs IT Spending Survey.

In terms of industry breakdown for the surveyed companies, our goal is to roughly

mirror our estimate of vertical end-market demand for information technology.

November 2, 2008

Goldman Sachs Global Investment Research 33

Exhibit 37: Respondents by vertical industry vs. our estimates of end-demand share

Source: Goldman Sachs IT Spending Survey, Goldman Sachs Research estimates.

Our survey captures the most significant IT spending verticals.

November 2, 2008

Goldman Sachs Global Investment Research 34

Reg AC

We, Sarah Friar, James Covello and Derek R. Bingham, hereby certify that all of the views expressed in this report accurately reflect our personal

views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly

or indirectly, related to the specific recommendations or views expressed in this report.

Investment profile

The Goldman Sachs Investment Profile provides investment context for a security by comparing key attributes of that security to its peer group and

market. The four key attributes depicted are: growth, returns, multiple and volatility. Growth, returns and multiple are indexed based on composites

of several methodologies to determine the stocks percentile ranking within the region's coverage universe.

The precise calculation of each metric may vary depending on the fiscal year, industry and region but the standard approach is as follows:

Growth is a composite of next year's estimate over current year's estimate, e.g. EPS, EBITDA, Revenue. Return is a year one prospective aggregate

of various return on capital measures, e.g. CROCI, ROACE, and ROE. Multiple is a composite of one-year forward valuation ratios, e.g. P/E, dividend

yield, EV/FCF, EV/EBITDA, EV/DACF, Price/Book. Volatility is measured as trailing twelve-month volatility adjusted for dividends.

Quantum

Quantum is Goldman Sachs' proprietary database providing access to detailed financial statement histories, forecasts and ratios. It can be used for

in-depth analysis of a single company, or to make comparisons between companies in different sectors and markets.

Disclosures

Coverage group(s) of stocks by primary analyst(s)

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Company-specific regulatory disclosures

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Distribution of ratings/investment banking relationships

Goldman Sachs Investment Research global coverage universe

Rating Distribution Investment Banking Relationships

Buy Hold Sell Buy Hold Sell

Global 26% 57% 17% 52% 47% 37%

As of October 1, 2008, Goldman Sachs Global Investment Research had investment ratings on 3,165 equity securities. Goldman Sachs assigns

stocks as Buys and Sells on various regional Investment Lists; stocks not so assigned are deemed Neutral. Such assignments equate to Buy, Hold

and Sell for the purposes of the above disclosure required by NASD/NYSE rules. See 'Ratings, Coverage groups and views and related definitions'

below.

Price target and rating history chart(s)

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Regulatory disclosures

Disclosures required by United States laws and regulations

See company-specific regulatory disclosures above for any of the following disclosures required as to companies referred to in this report: manager

or co-manager in a pending transaction; 1% or other ownership; compensation for certain services; types of client relationships; managed/co-

managed public offerings in prior periods; directorships; market making and/or specialist role.

The following are additional required disclosures: Ownership and material conflicts of interest: Goldman Sachs policy prohibits its analysts,

professionals reporting to analysts and members of their households from owning securities of any company in the analyst's area of coverage.

November 2, 2008

Goldman Sachs Global Investment Research 35

Analyst compensation: Analysts are paid in part based on the profitability of Goldman Sachs, which includes investment banking revenues. Analyst as officer or director: Goldman Sachs policy prohibits its analysts, persons reporting to analysts or members of their households from serving as

an officer, director, advisory board member or employee of any company in the analyst's area of coverage. Non-U.S. Analysts: Non-U.S. analysts

may not be associated persons of Goldman, Sachs & Co. and therefore may not be subject to NASD Rule 2711/NYSE Rules 472 restrictions on

communications with subject company, public appearances and trading securities held by the analysts. Distribution of ratings: See the distribution

of ratings disclosure above. Price chart: See the price chart, with changes of ratings and price targets in prior periods, above, or, if electronic format

or if with respect to multiple companies which are the subject of this report, on the Goldman Sachs website at

http://www.gs.com/research/hedge.html. Goldman, Sachs & Co. is a member of SIPC(http://www.sipc.org).

Additional disclosures required under the laws and regulations of jurisdictions other than the United States

The following disclosures are those required by the jurisdiction indicated, except to the extent already made above pursuant to United States laws

and regulations. Australia: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian

Corporations Act. Canada: Goldman Sachs Canada Inc. has approved of, and agreed to take responsibility for, this research in Canada if and to the

extent it relates to equity securities of Canadian issuers. Analysts may conduct site visits but are prohibited from accepting payment or

reimbursement by the company of travel expenses for such visits. Hong Kong: Further information on the securities of covered companies referred

to in this research may be obtained on request from Goldman Sachs (Asia) L.L.C. India: Further information on the subject company or companies

referred to in this research may be obtained from Goldman Sachs (India) Securities Private Limited; Japan: See below. Korea: Further information

on the subject company or companies referred to in this research may be obtained from Goldman Sachs (Asia) L.L.C., Seoul Branch. Russia: Research reports distributed in the Russian Federation are not advertising as defined in Russian law, but are information and analysis not having

product promotion as their main purpose and do not provide appraisal within the meaning of the Russian Law on Appraisal. Singapore: Further

information on the covered companies referred to in this research may be obtained from Goldman Sachs (Singapore) Pte. (Company Number:

198602165W). Taiwan: This material is for reference only and must not be reprinted without permission. Investors should carefully consider their

own investment risk. Investment results are the responsibility of the individual investor. United Kingdom: Persons who would be categorized as

retail clients in the United Kingdom, as such term is defined in the rules of the Financial Services Authority, should read this research in conjunction

with prior Goldman Sachs research on the covered companies referred to herein and should refer to the risk warnings that have been sent to them

by Goldman Sachs International. A copy of these risks warnings, and a glossary of certain financial terms used in this report, are available from

Goldman Sachs International on request.

European Union: Disclosure information in relation to Article 4 (1) (d) and Article 6 (2) of the European Commission Directive 2003/126/EC is

available at http://www.gs.com/client_services/global_investment_research/europeanpolicy.html

Japan: Goldman Sachs Japan Co., Ltd. Is a Financial Instrument Dealer under the Financial Instrument and Exchange Law, registered with the Kanto Financial Bureau (Registration No. 69), and is a member of Japan Securities Dealers Association (JSDA) and Financial Futures Association of Japan (FFJAJ). Sales and purchase of equities are subject to commission pre-determined with clients plus consumption tax. See company-specific disclosures as to any applicable disclosures required by Japanese stock exchanges, the

Japanese Securities Dealers Association or the Japanese Securities Finance Company.

Ratings, coverage groups and views and related definitions

Buy (B), Neutral (N), Sell (S) -Analysts recommend stocks as Buys or Sells for inclusion on various regional Investment Lists. Being assigned a Buy

or Sell on an Investment List is determined by a stock's return potential relative to its coverage group as described below. Any stock not assigned as

a Buy or a Sell on an Investment List is deemed Neutral. Each regional Investment Review Committee manages various regional Investment Lists to

a global guideline of 25%-35% of stocks as Buy and 10%-15% of stocks as Sell; however, the distribution of Buys and Sells in any particular coverage

group may vary as determined by the regional Investment Review Committee. Regional Conviction Buy and Sell lists represent investment

recommendations focused on either the size of the potential return or the likelihood of the realization of the return.

Return potential represents the price differential between the current share price and the price target expected during the time horizon associated

with the price target. Price targets are required for all covered stocks. The return potential, price target and associated time horizon are stated in

each report adding or reiterating an Investment List membership.

Coverage groups and views: A list of all stocks in each coverage group is available by primary analyst, stock and coverage group at

http://www.gs.com/research/hedge.html. The analyst assigns one of the following coverage views which represents the analyst's investment outlook

on the coverage group relative to the group's historical fundamentals and/or valuation. Attractive (A). The investment outlook over the following 12

months is favorable relative to the coverage group's historical fundamentals and/or valuation. Neutral (N). The investment outlook over the

following 12 months is neutral relative to the coverage group's historical fundamentals and/or valuation. Cautious (C). The investment outlook over

the following 12 months is unfavorable relative to the coverage group's historical fundamentals and/or valuation.

Not Rated (NR). The investment rating and target price, if any, have been removed pursuant to Goldman Sachs policy when Goldman Sachs is

acting in an advisory capacity in a merger or strategic transaction involving this company and in certain other circumstances. Rating Suspended (RS). Goldman Sachs Research has suspended the investment rating and price target, if any, for this stock, because there is not a sufficient

fundamental basis for determining an investment rating or target. The previous investment rating and price target, if any, are no longer in effect for

this stock and should not be relied upon. Coverage Suspended (CS). Goldman Sachs has suspended coverage of this company. Not Covered (NC). Goldman Sachs does not cover this company. Not Available or Not Applicable (NA). The information is not available for display or is not applicable.

Not Meaningful (NM). The information is not meaningful and is therefore excluded.

Ratings, coverage views and related definitions prior to June 26, 2006

Our rating system requires that analysts rank order the stocks in their coverage groups and assign one of three investment ratings (see definitions

below) within a ratings distribution guideline of no more than 25% of the stocks should be rated Outperform and no fewer than 10% rated

Underperform. The analyst assigns one of three coverage views (see definitions below), which represents the analyst's investment outlook on the

coverage group relative to the group's historical fundamentals and valuation. Each coverage group, listing all stocks covered in that group, is

available by primary analyst, stock and coverage group at http://www.gs.com/research/hedge.html.

Definitions

November 2, 2008

Goldman Sachs Global Investment Research 36

Outperform (OP). We expect this stock to outperform the median total return for the analyst's coverage universe over the next 12 months. In-Line (IL). We expect this stock to perform in line with the median total return for the analyst's coverage universe over the next 12 months. Underperform (U). We expect this stock to underperform the median total return for the analyst's coverage universe over the next 12 months.

Coverage views: Attractive (A). The investment outlook over the following 12 months is favorable relative to the coverage group's historical

fundamentals and/or valuation. Neutral (N). The investment outlook over the following 12 months is neutral relative to the coverage group's

historical fundamentals and/or valuation. Cautious (C). The investment outlook over the following 12 months is unfavorable relative to the coverage

group's historical fundamentals and/or valuation.

Current Investment List (CIL). We expect stocks on this list to provide an absolute total return of approximately 15%-20% over the next 12 months.

We only assign this designation to stocks rated Outperform. We require a 12-month price target for stocks with this designation. Each stock on the

CIL will automatically come off the list after 90 days unless renewed by the covering analyst and the relevant Regional Investment Review

Committee.

Global product; distributing entities

The Global Investment Research Division of Goldman Sachs produces and distributes research products for clients of Goldman Sachs, and pursuant

to certain contractual arrangements, on a global basis. Analysts based in Goldman Sachs offices around the world produce equity research on

industries and companies, and research on macroeconomics, currencies, commodities and portfolio strategy.

This research is disseminated in Australia by Goldman Sachs JBWere Pty Ltd (ABN 21 006 797 897) on behalf of Goldman Sachs; in Canada by

Goldman Sachs Canada Inc. regarding Canadian equities and by Goldman Sachs & Co. (all other research); in Germany by Goldman Sachs & Co.

oHG; in Hong Kong by Goldman Sachs (Asia) L.L.C.; in India by Goldman Sachs (India) Securities Private Ltd.; in Japan by Goldman Sachs Japan Co.,

Ltd.; in the Republic of Korea by Goldman Sachs (Asia) L.L.C., Seoul Branch; in New Zealand by Goldman Sachs JBWere (NZ) Limited on behalf of

Goldman Sachs; in Singapore by Goldman Sachs (Singapore) Pte. (Company Number: 198602165W); and in the United States of America by

Goldman, Sachs & Co. Goldman Sachs International has approved this research in connection with its distribution in the United Kingdom and

European Union.

European Union: Goldman Sachs International, authorised and regulated by the Financial Services Authority, has approved this research in

connection with its distribution in the European Union and United Kingdom; Goldman, Sachs & Co. oHG, regulated by the Bundesanstalt für

Finanzdienstleistungsaufsicht, may also be distributing research in Germany.

General disclosures in addition to specific disclosures required by certain jurisdictions

This research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public information that we

consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. We seek to update our research as

appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large

majority of reports are published at irregular intervals as appropriate in the analyst's judgment.

Goldman Sachs conducts a global full-service, integrated investment banking, investment management, and brokerage business. We have

investment banking and other business relationships with a substantial percentage of the companies covered by our Global Investment Research

Division.

Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and our

proprietary trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, our

proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views

expressed in this research.

We and our affiliates, officers, directors, and employees, excluding equity analysts, will from time to time have long or short positions in, act as

principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research.

This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be

illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of

individual clients. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and,

if appropriate, seek professional advice, including tax advice. The price and value of the investments referred to in this research and the income from

them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may

occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments.

Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all

investors. Investors should review current options disclosure documents which are available from Goldman Sachs sales representatives or at

http://www.theocc.com/publications/risks/riskchap1.jsp. Transactions cost may be significant in option strategies calling for multiple purchase and

sales of options such as spreads. Supporting documentation will be supplied upon request.

Our research is disseminated primarily electronically, and, in some cases, in printed form. Electronic research is simultaneously available to all

clients.

Disclosure information is also available at http://www.gs.com/research/hedge.html or from Research Compliance, One New York Plaza, New York,

NY 10004.

Copyright 2008 The Goldman Sachs Group, Inc.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The Goldman Sachs Group, Inc.

November 2, 2008

Goldman Sachs Global Investment Research 37

US Technology Strategy