51

8-1 ©2011 Pearson Education, Inc. Publishing as Prentice Hall

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | juliet-carpenter |

| View: | 217 times |

| Download: | 1 times |

8-1©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-2

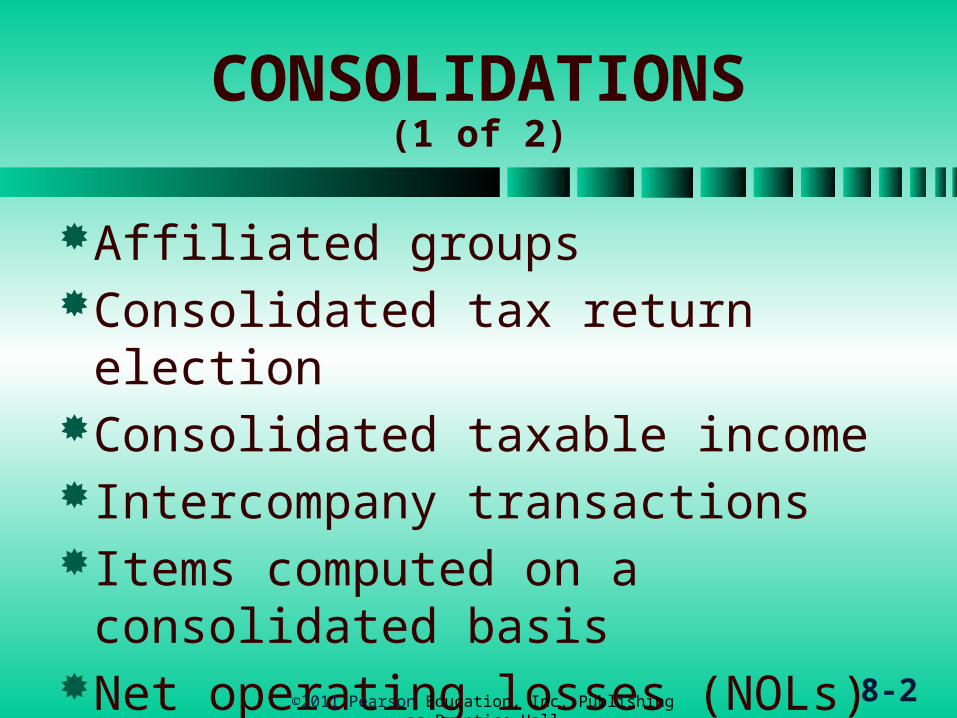

CONSOLIDATIONS(1 of 2)

Affiliated groupsConsolidated tax return electionConsolidated taxable incomeIntercompany transactionsItems computed on a

consolidated basisNet operating losses (NOLs)

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-3

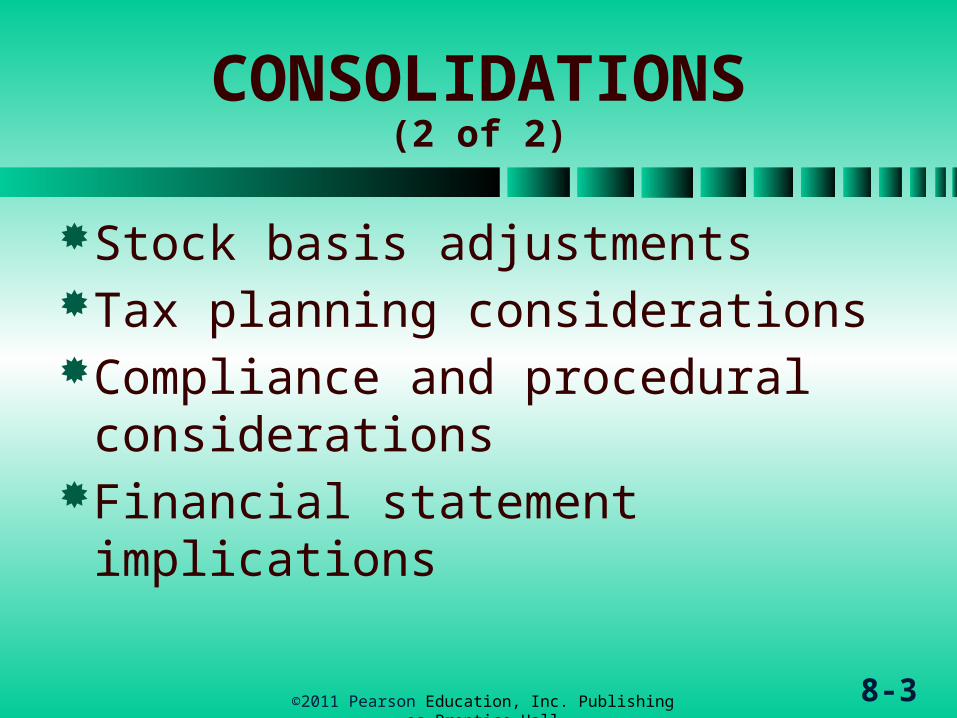

CONSOLIDATIONS(2 of 2)

Stock basis adjustmentsTax planning considerationsCompliance and procedural

considerationsFinancial statement implications

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-4

Affiliated GroupsStock Ownership Requirement

Parent must directly own 80% of voting power & 80% of total value of stock of at least one subsidiary

Parent & other group members must own 80% of the voting power & 80% of value of each corporation to be included in the group©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-5

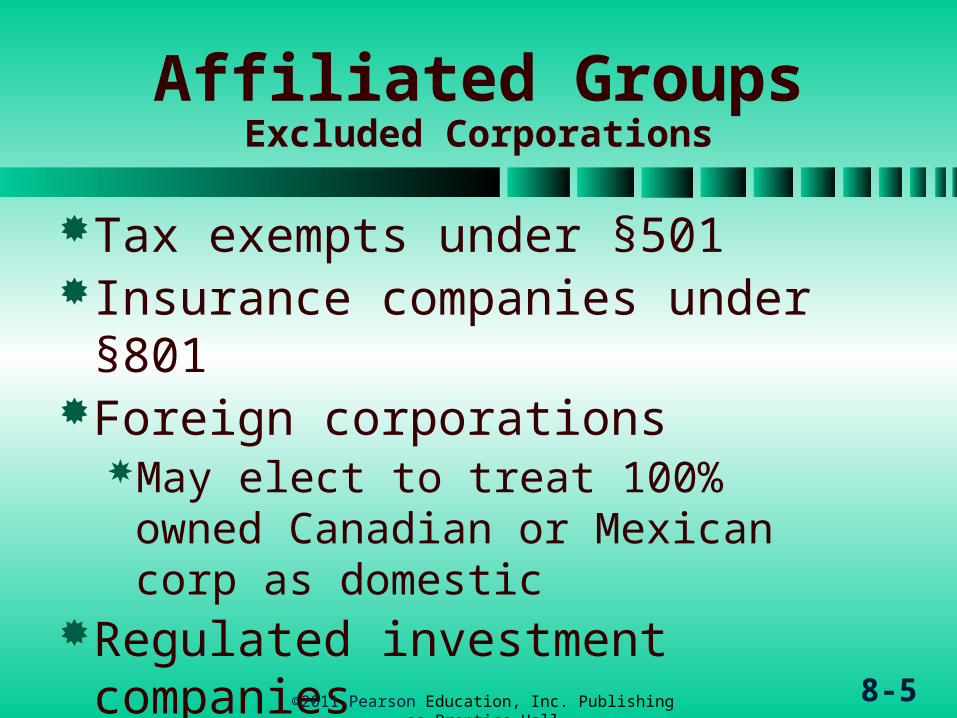

Affiliated GroupsExcluded Corporations

Tax exempts under §501Insurance companies under

§801Foreign corporations

May elect to treat 100% owned Canadian or Mexican corp as domestic

Regulated investment companies

Real estate investment trustsS corporations

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-6

Affiliated GroupsComparison with Controlled Group

Definitions (1 of 2)

Brother-sister controlled groups cannot file consolidated returns

Parent-subsidiary controlled groups and parent-subsidiary portion of combined controlled groups can file consolidated returns

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-7

Affiliated GroupsComparison with Controlled Group

Definitions (2 of 2)

Differences between rulesStock ownership for affiliated

group is ≥80% of voting power AND value

Attribution rules more strict for affiliated groups

Excluded corporations differAffiliated group definition tests

done on each day of the year, not just 12/31

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-8

Consolidated Tax ReturnElection (1 of 2)

§§1501-1504Very generalPrimarily define affiliated groups

eligible to file consolidated returnStatutory and interpretative

Regs used to determine consolidated tax liability and filing requirements

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-9

Consolidated Tax ReturnElection (2 of 2)

Termination of consolidated filingTermination of affiliated groupGood cause request to

discontinueEffects of former members

Gains and losses deferred on intercompany transactions may have to be recognized under acceleration rule

Consolidated return attributes must be allocated among former group members

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-10

Consolidated Taxable Income

Accounting Periods and Methods

Accounting periodsConsolidated return must conform

to parent’s tax yearAccounting methods

Each group member’s method used for separate filing is used for consolidated return

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-11

Consolidated Taxable Income

Calculation (1 of 2)

1. Compute each member’s income

2. Adjust each member’s income Adjustments made to take into

account special consolidated treatment

3. Remove any item that is reported on a consolidated basis

Resulting amount is separate taxable income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-12

Consolidated Taxable Income Calculation (2 of 2)

4. Combine separate taxable income (STI) of each member

Resulting amount is combined TI

5. Adjust combined taxable income for items reported on a consolidated basis

Resulting amount is consolidated taxable income (or NOL)

See Table 1

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-13

Intercompany Transactions

(1 of 3)

Transactions between corporations that are members of the same affiliated group immediately after the transaction

Matching ruleConsolidated group treats

intercompany item as if both companies were divisions of a single company©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-14

Intercompany Transactions

(2 of 3)

Acceleration ruleWhen a member leaves the group,

any transaction involving the departing member is fully taken into account

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-15

Intercompany Transactions

(3 of 3)

Examples include:Property transactionsPerformance of servicesLicensing of technologyRenting of propertyLending of moneySubsidiary’s distribution to parent

Dividend or redemption©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-16

Property Transactions(1 of 2)

Group members recognize gain or loss on intercompany property transfers in computing separate taxable income

Intercompany gain or loss excluded from consolidated income until a later event triggers recognition

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-17

Property Transactions(2 of 2)

Examples of recognition events:Buyer claims depreciation,

amortization or depletion on purchased asset

Amortization of capitalized services

Departure from the group by either buyer or seller

Parent starts a separate return year

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-18

Other IntercompanyTransactions

Both parties report their side of the transaction in determining separate taxable income

Net effect upon consolidation is zero

If parties use different methods or tax years, adjustments to match income and expense are required

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-19

Items Computed on a Consolidated Basis (1 of 2)

Charitable contribution deduction

Net §1231 gain or lossCapital gains and lossesDividends received deductionU.S. production activities

deduction©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-20

Items Computed on a Consolidated Basis (2 of 2)

Regular tax liabilityAMT liabilityTax creditsEstimated tax payments

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-21

Charitable Contribution Deduction

The affiliated group’s charitable contribution deduction is computed on a consolidated basisSum the individual contributions10% limitation based on adjusted

consolidated taxable incomeSame as adjusted taxable income for

a corporationCarryover the excess for 5 years

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-22

Capital Gains and Losses

Determined in manner similar as for single corporation

Departing members’ capital lossesRules similar to NOL treatmentDeparting member allocated a

portion of capital loss carryoverSRLY limitation for carrybacks from

separate return year©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-23

Dividends Received Deduction

Dividends received from other group members are excluded from consolidated income

Dividends-received deduction applied on a consolidated basis for dividends from non-group member corporations

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-24

U.S. Production Activities Deduction (1 of 3)

The affiliated group’s U.S. production activities deduction (CPAD) is computed on a consolidated basisLesser of

Consolidated productive activities income OR

Consolidated taxable income before CPAD deduction

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-25

U.S. Production Activities Deduction (2 of 3)

For purposes of computing CPAD, definition of affiliated group stock ownership threshold is 50% instead of 80%Lower threshold may require

inclusion of corps in this deduction that are not part of the consolidated return

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-26

U.S. Production Activities Deduction (3 of 3)

Production activities income computed on consolidated basis and then deduction allocated to corps based on relative amount of qualified production activities income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-27

Regular Tax Liability

Multiply consolidated taxable income by the appropriate tax rate(s) in §11If affiliated group chooses files

separate tax returns, reduced tax rates on lower income apply only one time regardless of number of members in group

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-28

Corporate AMT Liability

AMT prepared on a consolidated basis for all group members

Computation parallels determination of group’s consolidated taxable income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-29

Tax Credits

Affiliated groups may claim all tax credits available to corporationsDetermined on a consolidated

basis

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-30

Estimated Payments

1st two years option to make on separate or consolidated basis

After 2nd year must be on consolidated basis

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-31

Consolidated NOLs

Current year NOLsCarryovers of consolidated

NOLsCarryback to separate return

yearCarryforward to separate return

yearSpecial loss limitations©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-32

Current Year NOLs(1 of 2)

All members’ income/losses combined

Loss from one member offsets income from another member

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-33

Current Year NOLs(1 of 2)

Carrybacks and carryforwards done on consolidated basis if group has not changed its membersCarryback 2 yrs and forward 20

yearsTaxpayer can elect to carryback

NOL from 2008 or 2009 3, 4, or 5 years ©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-34

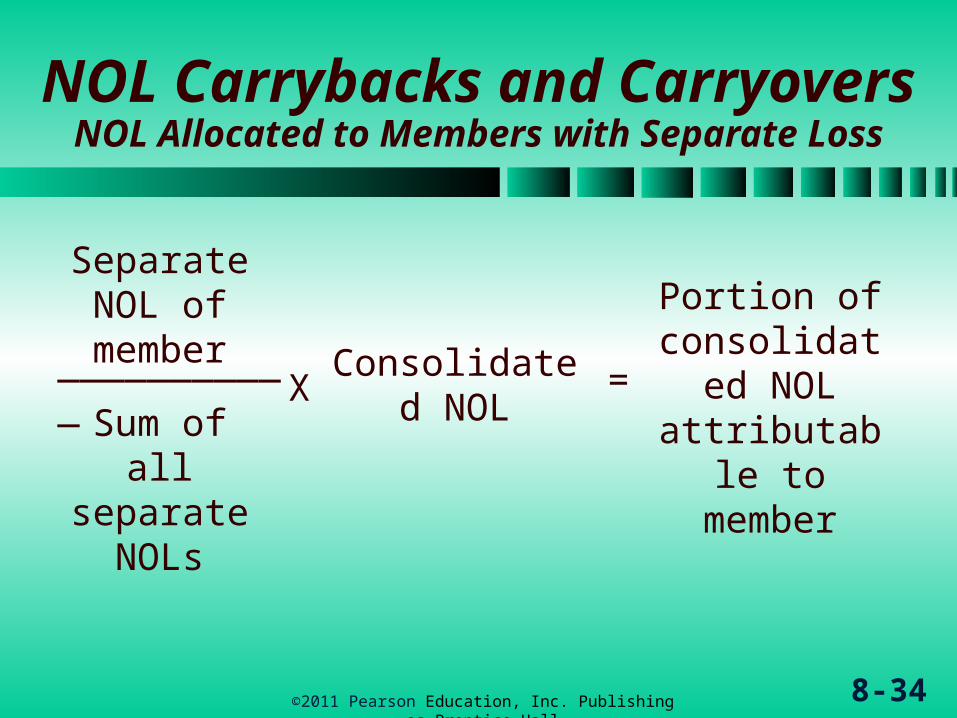

NOL Carrybacks and Carryovers

NOL Allocated to Members with Separate Loss

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Separate NOL of

member___________

Sum of all separate

NOLs

Consolidated NOLX =

Portion of consolidate

d NOL attributable to member

8-35

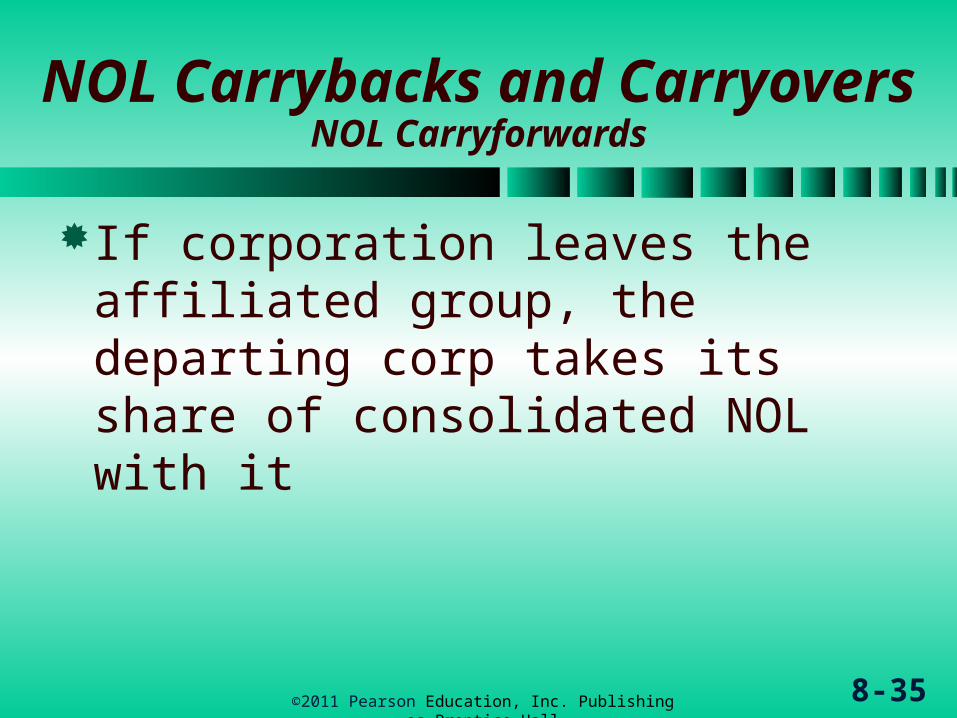

NOL Carrybacks and Carryovers

NOL Carryforwards

If corporation leaves the affiliated group, the departing corp takes its share of consolidated NOL with it

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-36

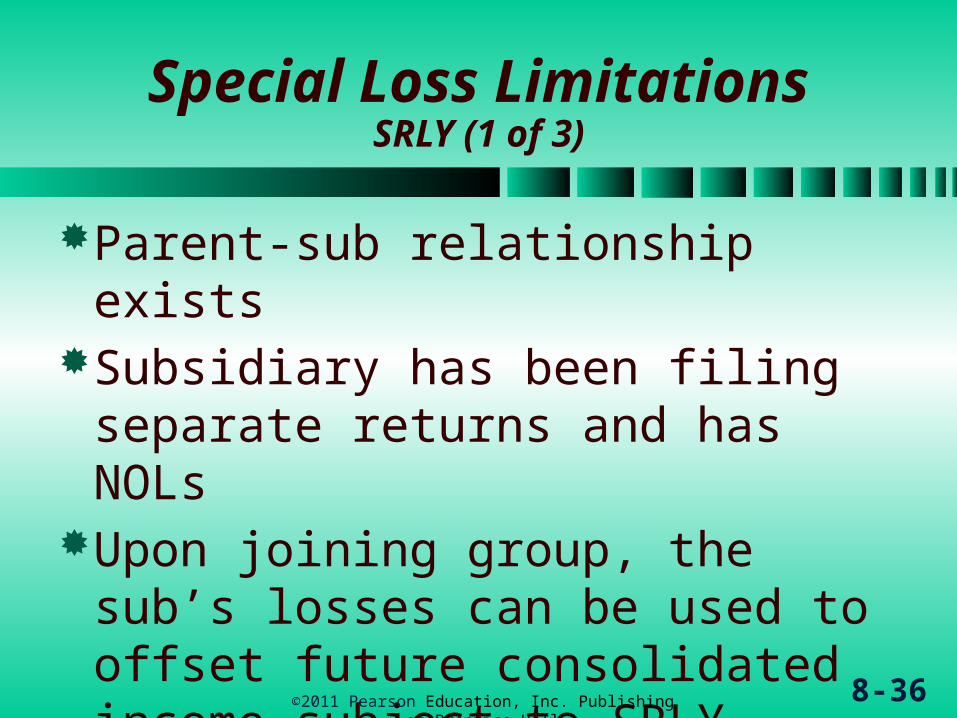

Special Loss LimitationsSRLY (1 of 3)

Parent-sub relationship existsSubsidiary has been filing

separate returns and has NOLsUpon joining group, the sub’s

losses can be used to offset future consolidated income subject to SRLY limitations

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-37

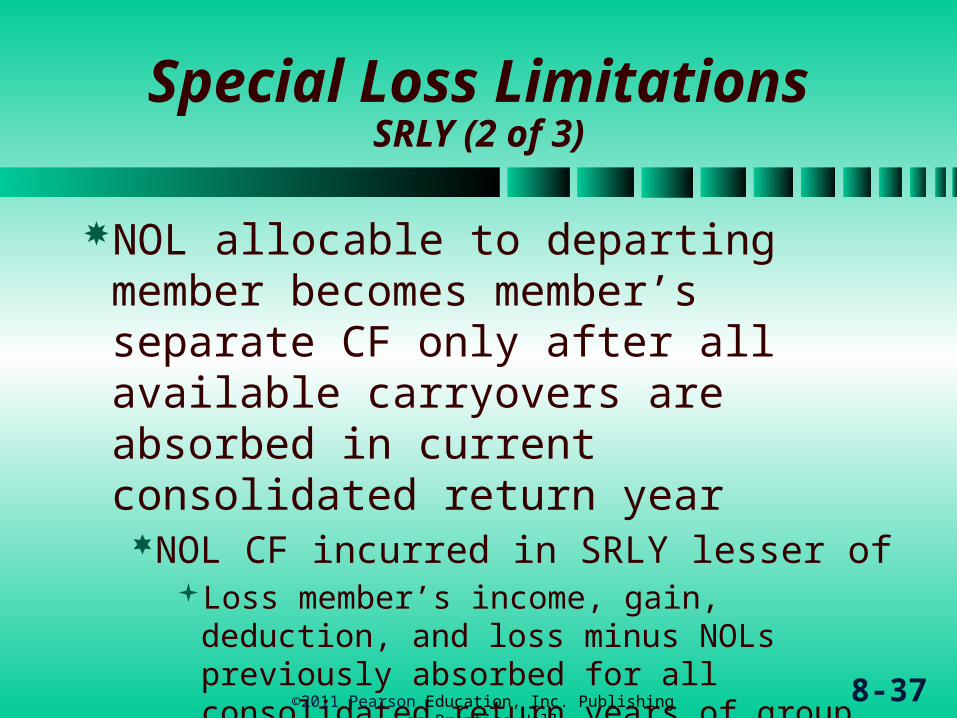

Special Loss LimitationsSRLY (2 of 3)

NOL allocable to departing member becomes member’s separate CF only after all available carryovers are absorbed in current consolidated return yearNOL CF incurred in SRLY lesser of

Loss member’s income, gain, deduction, and loss minus NOLs previously absorbed for all consolidated return years of group,

Consolidated taxable income, orAmount of the NOL carryover©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-38

Special Loss LimitationsSRLY (3 of 3)

SRLY carryover cannot be used when member’s cumulative contribution < $0

SRLY rules also apply to carrybacks for corporations who leave group and later carryback NOLs to consolidated years

In a reverse acquisition, SRLY limitation applies the acquiring corp’s NOLs

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-39

Special Loss Limitations §382 (1 of 2)

§382 limitation applied when unrelated corp (or group) added as a subsidiary and has NOLs

Limitation determines dollar amount of loss carryforward from new sub (or sub group) that can be applied to reduce consolidated taxable income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-40

Special Loss Limitations §382 (2 of 2)

Loss limitation Value of loss group x federal

interest rateLoss group value is value of all

common & pref stock owned by outsiders immediately before change of ownership

SRLY NOL creates deferred tax assetMay be subject to a valuation

allowance

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-41

Stock Basis Adjustments(1 of 2)

Annually, basis for investment in a subsidiary corporation is adjusted

Adjustment parallels the “equity” method of accounting for investments but uses tax numbers instead of book income numbers

Adjustments listed on page 35©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-42

Stock Basis Adjustments(2 of 2)

Large negative basis adjustments can reduce a sub’s stock basis to $0Negative basis adjustments when

sub’s basis is $0 creates an excess loss account

Subsequent positive adjustments reduce (or eliminate) the excess loss account©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-43

Tax Planning Considerations

Advantages of Consolidating (1 of 2)

Losses in one member offset gains in another in the current year

Intragroup dividends are eliminated

Combined credits and deductions may avoid carryovers

Intragroup gains are deferredConsolidated AMT may reduce

the negative effects of AMT adjustments

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-44

Tax Planning Considerations

Advantages of Consolidating (2 of 2)

Parent corp (& upper tier corps) increase its bases in subsidiary stock investments for sub’s taxable income, eliminating double taxation

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-45

Tax Planning Considerations

Disadvantages of Consolidating

Election binding on subsequent years

Members must use same tax year

Intragroup losses are deferredIntragroup losses may reduces

the limitation on certain deductions and credits

Additional administrative cost©2011 Pearson Education, Inc. Publishing as

Prentice Hall

8-46

Compliance and Procedural

Considerations (1 of 2)

Basic election and returnFile Form 1120

Including Form 851 affiliations schedule

Subs’ consent to election use Form 1122

Must provide a columnar schedule reconciling consolidated income with members’ separate incomes

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-47

Compliance and Procedural

Considerations (1 of 2)

Parent corp acts as agent for groupParent can request IRS consent to

treat intercompany transactions on a separate entity basis

Tax treatment of affiliated groups for state income tax purposes of varies from state to state

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-48

Financial Statement Implications

Intercompany Transactions (1 of 2)

Discussion based on 100%-owned sub

Intercompany dividendsEliminated for both tax and book

whether filing separately or consolidated

Intercompany salesDefers intercompany income for

book and tax if filing consolidated returnDeferred amounts may differ

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-49

Financial Statement Implications

Intercompany Transactions (2 of 2)

Intercompany sales (continued)If filing separate returns

Seller recognizes income for tax purposes, but not for financial stmt purposes

Group recognizes deferred tax asset on difference between profit deferred in consolidated financial stmts and taxes paid on seller’s separate tax return

©2011 Pearson Education, Inc. Publishing as Prentice Hall

8-50

Financial Statement Implications

SRLY Losses

NOL from SRLY creates deferred tax assetPossibly subject to a valuation

allowance

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Comments or questions about PowerPoint Slides?Contact Dr. Richard Newmark at University of Northern Colorado’s

Kenneth W. Monfort College of [email protected]

8-51©2011 Pearson Education, Inc. Publishing as Prentice Hall