DOCUMENT RESUME ED 373 248 CE 067 082 TITLE Financing the Business. Unit 11. Level 3. Instructor Guide. PACE: Program for Acquiring Competence in Entrepreneurship. Third Edition. Research & Development Series No. 303-11. INSTITUTION Ohio State Univ., Columbus. Center on Education and Training for Employment. PUB DATE 94 NOTE 61p.; For the complete set, i.e., 21 units, each done at three levels, see CE 067 029-092. Supported by the International Consortium for Entrepreneurship Education, the Coleman Foundation, and the Center for Entrepreneurial Leadership Inc. AVAILABLE FROM Center on Education and Training for Employment, 1900 Kenny Road, Columbus, OH 43210-1090 (order no. RD303-11 IG, instructor guide $4.50; RD303-11 M, student module, $3; student module sets, level 1--RD301M, level 2--RD302M, level 3--RD303M, $45 each; instructor guide sets, level 1--RD301G, level 2--RD302G, level 3--RD303G, $75 each; 3 levels and resource guide, RD300G, $175). PUB TYPE 71iides Classroom Use Teaching Guides (For T..acher) (052) Guides Classroom Use Instructional Materials (For Learner) (051) EDRS PRICE MF01/PC03 Plus Postage. DESCRIPTORS Administrators; Behavioral Objectives; Business Administration; Business Education; *Competency Based Education; Credit (Finance); *Entrepreneurship; *Financial Aid Applicants; Financial Needs; *Financial Support; Learning Activities; Managerial Occupations; Master Plans; Postsecondary Education; Secondary Education; Self Employment; *Small Businesses; Strategic Planning; Teaching Guides IDENTIFIERS *Program for Acquiring Competence Entrepreneurship ABSTRACT This instructor guide for a unit on business finance in the PACE (Program for Acquiring Competence in Entrepreneurship) curriculum includes the full text of the student module and lesson plans, instructional suggestions, and other teacher resources. The competencies that are incorporated into this module are at Level 3 of learning--starting and managing one's own business. Included in the instructor's guide are the following: unit objectives, guidelines for using PACE, lists of teaching suggestions for each unit objective/subobjective, model assessment responses, and overview of the three levels of the PACE program. The following materials are contained in the student's guide: activities to be completed in preparation for the unit, unit objectives, student reading materials, individual and group learning activities, case study, discussion questions, assessment questions, and references. These four objectives are addressed: determine options for financing one's business; discuss the financial information included in a business plan; justify one's financial projections; and explain the use of a loan application package. (YLB)

Transcript

DOCUMENT RESUME

ED 373 248 CE 067 082

TITLE Financing the Business. Unit 11. Level 3. InstructorGuide. PACE: Program for Acquiring Competence inEntrepreneurship. Third Edition. Research &Development Series No. 303-11.

INSTITUTION Ohio State Univ., Columbus. Center on Education andTraining for Employment.

PUB DATE 94

NOTE 61p.; For the complete set, i.e., 21 units, each doneat three levels, see CE 067 029-092. Supported by theInternational Consortium for EntrepreneurshipEducation, the Coleman Foundation, and the Center forEntrepreneurial Leadership Inc.

AVAILABLE FROM Center on Education and Training for Employment, 1900Kenny Road, Columbus, OH 43210-1090 (order no.RD303-11 IG, instructor guide $4.50; RD303-11 M,student module, $3; student module sets, level1--RD301M, level 2--RD302M, level 3--RD303M, $45each; instructor guide sets, level 1--RD301G, level2--RD302G, level 3--RD303G, $75 each; 3 levels andresource guide, RD300G, $175).

PUB TYPE 71iides Classroom Use Teaching Guides (For

IDENTIFIERS *Program for Acquiring Competence Entrepreneurship

ABSTRACTThis instructor guide for a unit on business finance

in the PACE (Program for Acquiring Competence in Entrepreneurship)curriculum includes the full text of the student module and lessonplans, instructional suggestions, and other teacher resources. Thecompetencies that are incorporated into this module are at Level 3 oflearning--starting and managing one's own business. Included in theinstructor's guide are the following: unit objectives, guidelines forusing PACE, lists of teaching suggestions for each unitobjective/subobjective, model assessment responses, and overview ofthe three levels of the PACE program. The following materials arecontained in the student's guide: activities to be completed inpreparation for the unit, unit objectives, student reading materials,individual and group learning activities, case study, discussionquestions, assessment questions, and references. These fourobjectives are addressed: determine options for financing one'sbusiness; discuss the financial information included in a businessplan; justify one's financial projections; and explain the use of a

loan application package. (YLB)

Co

csic)

UNIT 11LEVEL 3

Program for AcquiringCompetence inEntrepreneurship

CENTER ON EDUCATIONAND IMMO FON ENPLOYNDIT

COLLEGE OF EDUCATIONTmE OHO STATE ulaveftsiry

Objectives:

Research I lhaclopment Series Ni..

Determine options for financing your business.

Discuss the financial information included in a busi-ness plan.

Justify your financial projections.

t.)

Explain the use of a loan application package.U S DE rARTMENT OF EDUCATION

Flit;CATIONAL RESOURCES INFORMATIONCENTER fERICI

Of If,. rirwIment h.l heen rovioluCodrorp,Orl from the pnrcnn nr nrcprul.ilinn

Mn lt c.h.11,ue. have hvon made I'rourrifluction quality

Prunt, of view (1111111010n, 'dated in (Si',drcumonl not nor °vainly represent

0E111 molion nr prau y

PERMISSION TO REPRODUCE THISMATERIAL HAS BEEN GRANTED BY

C 6-ft

TO THE EDUCATIONAL RESOURCESINFORMATION CENTER (ERIC)

INSTRUCTOR GUIDE

Unit 11

Financing the BusinessLevel 3

HOW TO USE PACE

Use the objectives as a pretest. If a studentis able to meet the objectives, ask him orher to read and respond to the assessmentquestions in the back of the module.

Duplicate the glossary from the ResourceGuide to use as a handout.

Use the teaching outlines provided in theInstructor Guide for assistan "e in focusingyour teaching delivery. '1 .; left side ofeach outline page lists objectives with thecorresponding headings (margin questions)from the unit. Space is provided for you toadd your own suggestions. Try to increasestudent involvement in as many ways aspossible to foster an interactive learningprocess.

When your students are ready to do theActivities, assist them in selecting thosethat you feel would be the most beneficialto their growth in entrepreneurship.

Assess your students on the unit contentwhen they indicate they are ready. Youmay choose written or verbal assessmentsaccording to the situation. Model re-sponses are provided for each module ofeach unit. While these are suggestedresponses, others may be equally valid.

2BEST COPY AVAILABLE

Objectives Teaching Suggestions

1. DETERMINE OPTIONS FORFINANCING YOUR BUSINESS

How are the financing needs deter-mined for the business?

What is special about financing amanufacturing business?

What is special about financing aservice business?

What is special about financing afranchise business?

How do you determine which fi-nancing sources to use?

How do you construct a plan ofaction to satisfy your financingneeds?

Ask students to list sources of information used by entrepreneursto estimate start-up costs and operating expenses. Using a chalk-board or overhead, show the sources enumerated by your stu-dents and add others to complete the list.

Ask students to define the concept of work-in-process inventory.Use a simple example to show how accountants compute thework-in-process inventory. Also, define inventory turnover.

Ask students to explain in their own words how service busi-nesses differ from manufacturing businesses regarding financialanalysis.

First, have students give examples of franchises and explainwhat characterizes this form of debt financing. Then, use anoverhead or chalkboard to list sources of information on fran-chising.

Use the five-step procedure presented in this section to showhow financing needs for a small business are determined.

Use the outline "Checklist for Financing Your Business" pre-sented in this section to discuss the plan of action for satisfyingfinancing needs.

Objectives Teaching Suggestions

2. DISCUSS THE FINANCIALINFORMATION INCLUDEDIN A BUSINESS PLAN

What are operating expenses?

How are operating expense ratiosused?

How do you determine the financ-ing needed to start your business?

What is involved in estimating an-nual sales volumes?

How do you estimate start-upcosts and monthly operatingexpenses?

How do you determine the totalcash needed to start the business?

How do you prepare to arrange thefinancing?

Ask students to define the concept of operating expenses and togive examples.

Use Figure 1 in this section to review financial ratio analysis.Make sure students understand the meaning of the ratios andknow how to compute them. Use numerical examples to checkthe knowledge of your students.

Invite a local entrepreneur to speak about his/her experience re-garding methods of estimating financing needs.

Refer to the above suggestion. Ask the entrepreneur to usenumerical examples like the one presented in Figure 2 toestimate sales volume.

Use Figure 3 to explain the process of estimating these two im-portant financial components included in the business plan.

Refer to the above suggestion.

Engage students in a discussion on how entrepreneurs shouldprepare financial statements to convince lenders and investorsabout the worthiness of their business.

4

Objectives Teaching Suggestions

How do you prepare a projectedincome statement?

How do you prepare a projectedcashflow statement?

How do you prepare your personalbalance sheet?

3. JUSTIFY YOUR FINANCIALPROJECTIONS

Can you justify your financial pro-jections?

4. EXPLAIN THE USE OFA LOAN APPLICATIONPACKAGE

How do you prepare a loanapplication package?

Follow the step-by-step procedure presented in this section toexplain how to develop a projected income statement.

Refer to the above suggestion. Make sure students understandthe computations in the tables presented in Figures 5 and 6 (i.e.,how to compute gross income, net income, pre-operating cash-flow, monthly cumulative cashflow, etc.).

Use this opportunity to ask students to prepare a personal bal-ance sheet. Use the example provided in Figure 7 as a startingpoint.

Engage students in a discussion on how to justify financial pro-jections in the business plan. Highlight the importance of clearlystating assumptions on sales growth, cost of goods sold, expectedcashflow timing, accounts receivable collection, etc.

Use the loan application package outline presented in this unit asa ramp toward a more extensive discussion on completing a loanapplication. Acquaint students with the information contained insuch applications. Refer to the Bank One Loan Application Kitpresented in this unit.

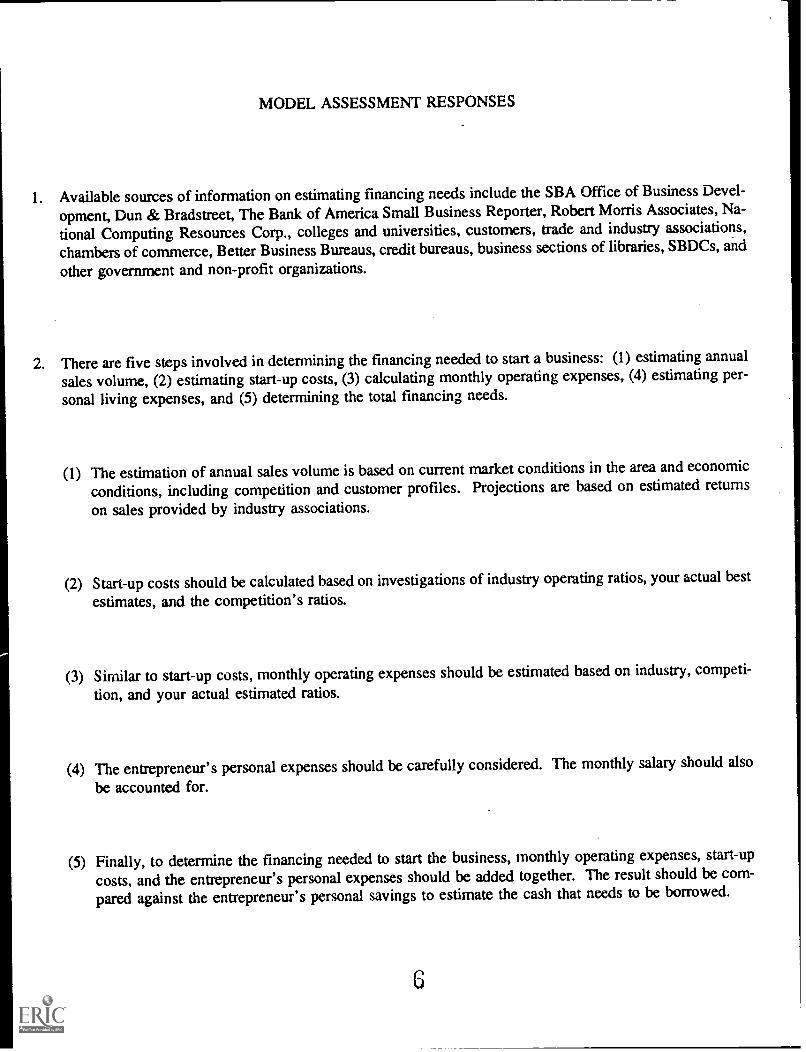

MODEL ASSESSMENT RESPONSES

1. Available sources of information on estimating financing needs include the SBA Office of Business Devel-

opment, Dun & Bradstreet, The Bank of America Small Business Reporter, Robert Morris Associates, Na-tional Computing Resources Corp., colleges and universities, customers, trade and industry associations,chambers of commerce, Better Business Bureaus, credit bureaus, business sections of libraries, SBDCs, and

other government and non-profit organizations.

2. There are five steps involved in determining the financing needed to start a business: (1) estimating annualsales volume, (2) estimating start-up costs, (3) calculating monthly operating expenses, (4) estimating per-

sonal living expenses, and (5) determining the total financing needs.

(1) The estimation of annual sales volume is based on current market conditions in the area and economic

conditions, including competition and customer profiles. Projections are based on estimated returns

on sales provided by industry associations.

(2) Start-up costs should be calculated based on investigations of industry operating ratios, your actual best

estimates, and the competition's ratios.

(3) Similar to start-up costs, monthly operating expenses should be estimated based on industry, competi-

tion, and your actual estimated ratios.

(4) The entrepreneur's personal expenses should be carefully considered. The monthly salary should also

be accounted for.

(5) Finally, to determine the financing needed to start the business, monthly operating expenses, start-up

costs, and the entrepreneur's personal expenses should be added together. The result should be com-pared against the entrepreneur's personal savings to estimate the cash that needs to be borrowed.

6

3. Three steps involved in preparing a projected income statement include: (1) listing the estimated monthlygross sales, (2) listing the cost of goods sold for the monthly projected sales, (3) subtracting the cost ofgoods sold from estimated gross sales to obtain gross profit, (4) itemizing monthly operating expenses,(5) totaling monthly operating expenses, and (6) subtracting total monthly operating expenses from grossprofit to calculate the net profit.

To prepare a projected cashflow statement, one needs to (1) add together cash-on-hand and loans to deter-mine the total amount of cash available to start the busines,, (2) subtract start-up costs from the totalamount of cash available to project actual cash left over, (3) itemize sources of cash, (4) add sources ofcash, (5) itemize cash disbursements, (6) total cash disbursements, (7) subtract cash disbursements fromsources of cash to calculate the monthly cash balance. Monthly cumulative cashflow is computed by addingtogether the previous month cumulative cashflow and the monthly cashflow balance.

4. To justify financial projections, the entrepreneur needs to clearly state assumptions on sales growth, costof goods sold, operating expenses, cashflow timing, accounts receivable collection, supplier reliability, andother assumptions that underlie financial projections in the business plan.

5. The five basic parts in a loan application package are: (1) basic application information, (2) loan request,(3) applicant's personal information, (4) business information, and (5) financial projections.

(1) The basic application information refers to personal data of the applicant and general data on the busi-ness, including the type, size, type of ownership of the business, as well as the amount invested in thebusiness by the entrepreneur.

(2) The loan request section includes the purpose, amount, and terms of the loan, as well as the business'sdebt to equity ratio, information on collateral, any intended use of borrowed money, etc.

(3) The applicant's personal information includes the resume, credit references, personal balance sheet, andpast two or three years of income tax statements.

(4) The business information section covers the business plan, life and casualty insurance coverage, li-censes and permits, lease and agreements, and other information pertaining to the business plan.

(5) The financial projections include projected monthly income and cashfiow statements, as well as a first-

year projected balance sheet.

Program for AcquirinCompetence inEntrepreneurship

Incorporates the needed competencies for creating and operating a small business at three levels of learning, with experiences andoutcomes becoming progressively more advanced.

Level 1 Understanding the creation and operation of a business.Level 2 Planning for a business in your future.Level 3 Starting and managing your own business.

Self-contained Student Modules include: specific objectives, questions supporting the objectives, complete content in form of answersto the questions, case studies, individual activities, group activities, module assessment references. Instructor Guides include the full textof each student module and lesson plans, instructional suggestions, and other resources. PACE,Third Edition, Resource Guide includesteaching strategies, references, glossary of terms, and a directory of entrepreneurship assistance organizations.

For information on PACE or to order, contact the Publications Department at theCenter on Education and Training for Employment, 1900 Kenny Road, Columbus, Ohio 43210-1090

(614) 292-4353, (800) 848-4815.

Support for PACE, Third Edition provided in whole or in part by:

International Consortium for Entrepreneurship Educationand

International Enterprise AcademyCenter on Education and Training for Employment

The Ohio State University

The Coleman Foundation

Center for Entrepreneurial Leadership Inc.

9 Ewing Marion Kauffman Foundation

Your Potentialas an

Entrepreneur

Help forthe

Entrepreneur

LegalIssues

Nature ofN.) Small Business

Types ofOwnership

Financingthe Business

BushessOpportunities

MarketingAnalysis

Business Human

Management Resources

Record FinancialKeeping Analysis

Location

Global Markets

UNIT 11LEVEL 3

TheBusiness Plan

PricingStrategy

Promotion

CustomerCredit

CENTER ON EDUCATIONAND TRAINING FOR EMPLOYMENT

COLLEGE OF EDUCATIONTHE OHIO STATE UNIVERSITY

is

Selling

RiskManagement

Operations

Program:for AcquiringCompetence mEntrepreneurship

Research & Development Series No. 303-11

FINANCING THE BUSINESS

BEFORE YOU BEGIN . . .

1. Consult the Resource Guide for instructions if this is your first PACE unit.

2. Read What are the Objectives for this Unit on the following page. If you thinkyou can meet these objectives now, consult your instructor.

3. These objectives were met in Level 1 and Level 2:

Level 1

Discuss the personal risks involved in financing a business.

Explain the difference between operating expenses and start-up costs.

Describe methods of financing a new business.

Discuss the importance of having a good credit rating.

Level 2Discuss the factors t, consider in financing a business.

Explain how to determine the different types of costs.

Compare the advantages and disadvantages of different sources offinancing.

4. Look for these business terms as you read this unit. If you need help with themeanings, ask your instructor for a copy of the PACE Glossary contained in theResource Guide.

Convertible debenture FlooringDebt-to-equity ratio Indirect collection financingDebt with warrants Inventory turnover/stock turnsDirect term-loan Policy loanFarmer's Home Administration Savings and loan association (S&L)

discuss the financial information included in a business plan,

justify your financial projections, and

explain the use of a loan application package.

WHAT IS THIS UNIT ABOUT?

Financing is the lifeblood of a business.Without capital, a business cannot begin,grow, or ever hope to become successful.Now that you have decided to start a busi-ness, here are the two most crucial questionsyou must ask:

What are my business's realistic finan-cial needs?

How do I satisfy these needs?

12

3

The information in this unit will help youanswer these two extremely important ques-tions. The first part of the unit presentsinformation you can use to investigate andstudy your business's financial needs. Thenyou will explain how to prepare estimates ofyour business's capital needs and the neces-sary financial statements. After you haveexamined the preparation and justification ofthe projected income and cashflow state-ments, you will study the production and useof the loan application package.

By applying the material presented in thisunit, you should be able to determine theamount of the financial lifeblood your busi-ness needs and to select the most appropriatesources for supplying it.

4

HOW ARE THE FINANCINGNEEDS DETERMINED FORTHE BUSINESS?

Making a profit is necessary if a business isto succeed. Therefore, carefully investigatethe financing needs of your business. Notonly must you estimate how much it willcost to start-up your business, but you mustalso provide figures on how much moneywill be required to operate it during the firstyear. Money needs will vary according tothe type of businesswhether it is manufac-turing, wholesaling, retailing, or servicethekind of merchandise or service offered, theincome level of your customers, your per-sonal trade connections, the location of yourbusiness, and many other factors.

When determining costs, there is no substi-tute for first-hand knowledge about yourprospective business enterprise. It is farbetter for you to spend a few hours and dol-lars now to make this initial investigationthan to wait and learn through trial anderror. Therefore, secure all the informationyou need from other people in the same or asimilar business, from trade associations,government agencies, libraries, and fromother likely sources, such as professionalbusiness consultants, accountants, andlawyers. Many of these sources may bewithin your own community.

The following sources can be contactedeither by mail or by referring to theirpublications in your local library:

Small Business AdministrationOffice of Business DevelopmentWashington, DC 20416

or call the SBA Small Business AnswerDesk 1-800-368-5855. (Ask for SmallBusiness DirectoryPublications andVideotapes for St 'rig and Managing aSuccessful Small Business.)

Dun & Bradstreet99 Church StreetNew York, NY 10007

The Bank of AmericaSmall Business ReporterDepartment 3120P.O. Box 37000San Francisco, CA 94137

Robert Morris AssociatesPhiladelphia National Bank Bldg.Philadelphia, PA 19107

National Computing Resources Corporation3095 Kettering Blvd., 15t FloorDayton, OH 45439(Ask for the annual "Expense in Retailing"

publication.)

Here are some other organizations or indi-viduals that should be contacted:

Colleges and universities

Your own present or potential customers

Trade associations

Chambers of commerce

Better Business Bureaus

13

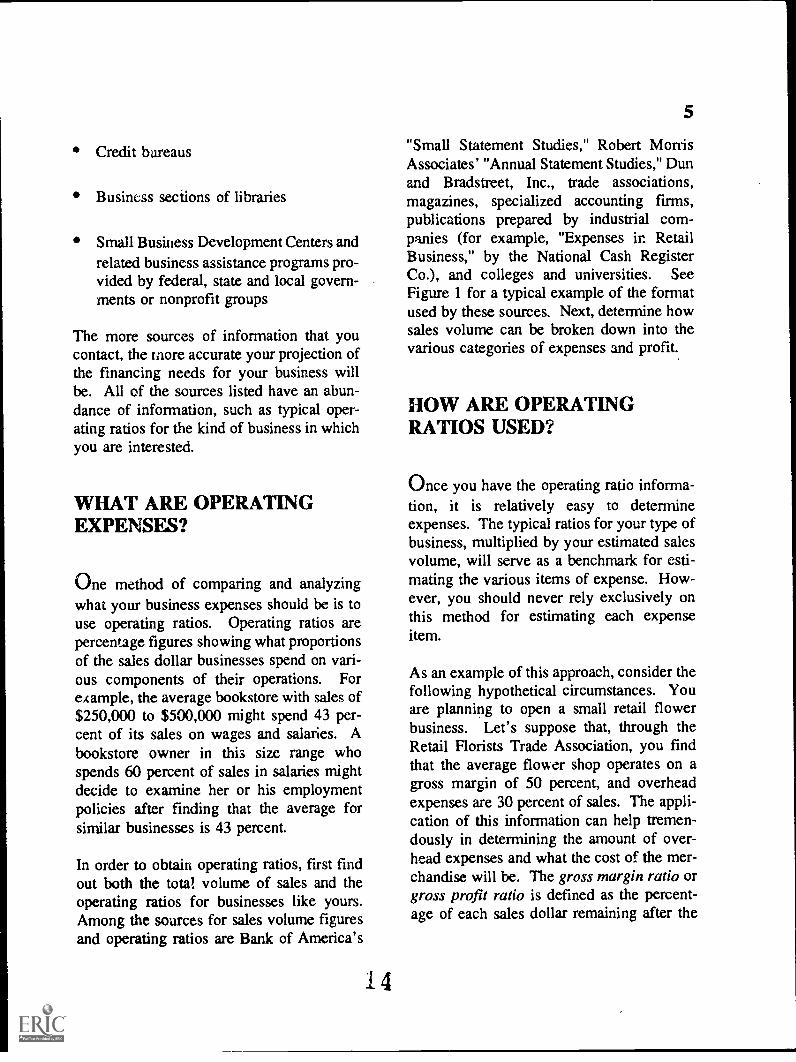

Credit bureaus

Business sections of libraries

Small Business Development Centers andrelated business assistance programs pro-vided by federal, state and local govern-ments or nonprofit groups

The more sources of information that youcontact, the more accurate your projection ofthe financing needs for your business willbe. All of the sources listed have an abun-dance of information, such as typical oper-ating ratios for the kind of business in whichyou are interested.

WHAT ARE OPERATINGEXPENSES?

One method of comparing and analyzingwhat your business expenses should be is touse operating ratios. Operating ratios arepercentage figures showing what proportionsof the sales dollar businesses spend on vari-ous components of their operations. Forexample, the average bookstore with sales of$250,000 to $500,000 might spend 43 per-cent of its sales on wages and salaries. Abookstore owner in this size range whospends 60 percent of sales in salaries mightdecide to examine her or his employmentpolicies after finding that the average forsimilar businesses is 43 percent.

In order to obtain operating ratios, first findout both the total volume of sales and theoperating ratios for businesses like yours.Among the sources for sales volume figuresand operating ratios are Bank of America's

4

5

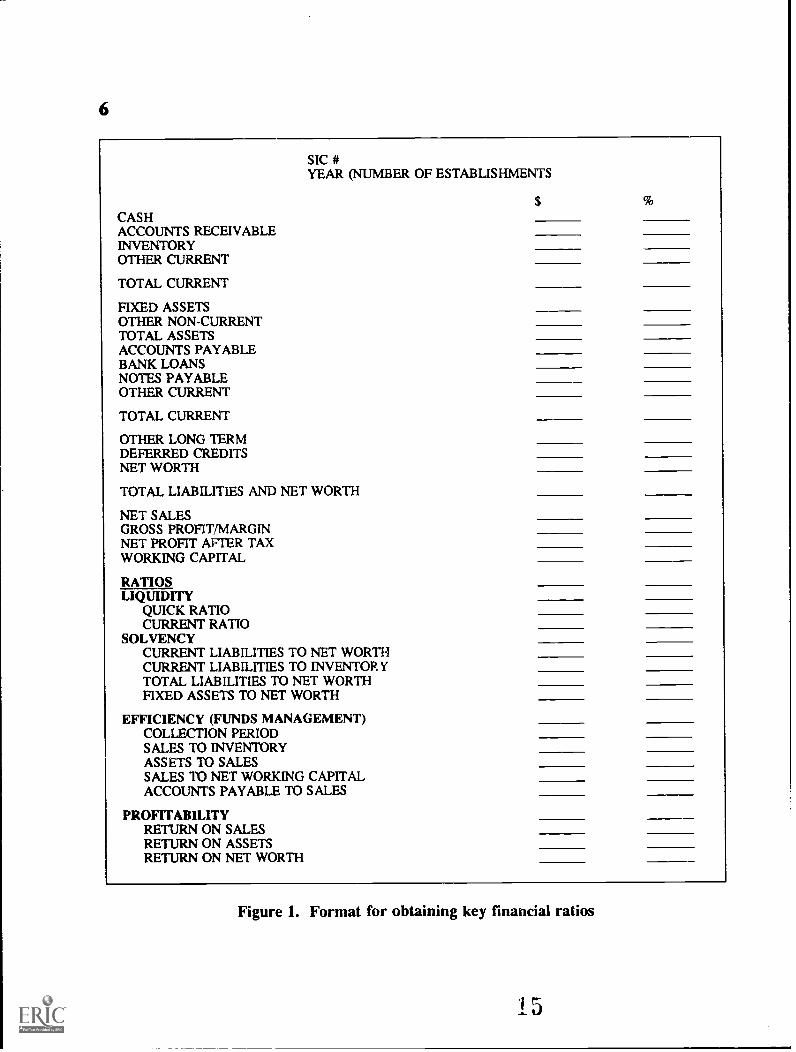

"Small Statement Studies," Robert MorrisAssociates' "Annual Statement Studies," Dunand Bradstreet, Inc., trade associations,magazines, specialized accounting firms,publications prepared by industrial com-panies (for example, "Expenses in RetailBusiness," by the National Cash RegisterCo.), and colleges and universities. SeeFigure I for a typical example of the formatused by these sources. Next, determine howsales volume can be broken down into thevarious categories of expenses and profit.

HOW ARE OPERATINGRATIOS USED?

Once you have the operating ratio informa-tion, it is relatively easy to determineexpenses. The typical ratios for your type ofbusiness, multiplied by your estimated salesvolume, will serve as a benchmark for esti-mating the various items of expense. How-ever, you should never rely exclusively onthis method for estimating each expenseitem.

As an example of this approach, consider thefollowing hypothetical circumstances. Youare planning to open a small retail flowerbusiness. Let's suppose that, through theRetail Florists Trade Association, you findthat the average flower shop operates on agross margin of 50 percent, and overheadexpenses are 30 percent of sales. The appli-cation of this information can help tremen-dously in determining the amount of over-head expenses and what the cost of the mer-chandise will be. The gross margin ratio orgross profit ratio is defined as the percent-age of each sales dollar remaining after the

6

SIC #YEAR (NUMBER OF ESTABLISHMENTS

CASHACCOUNTS RECEIVABLEINVENTORYOTHER CURRENT

TOTAL CURRENT

FIXED ASSETSOTHER NON-CURRENTTOTAL ASSETSACCOUNTS PAYABLEBANK LOANSNOTES PAYABLEOTHER CURRENT

TOTAL CURRENT

OTHER LONG TERMDEFERRED CREDITSNET WORTH

TOTAL LIABILITIES AND NET WORTH

NET SALESGROSS PROFIT/MARGINNET PROFIT AFTER TAXWORKING CAPITAL

RATIOSLIQUIDITY

QUICK RATIOCURRENT RATIO

SOLVENCYCURRENT LIABILITIES TO NET WORTHCURRENT LIABILITIES TO INVENTORYTOTAL LIABILITIES TO NET WORTHFIXED ASSETS TO NET WORTH

EFFICIENCY (FUNDS MANAGEMENT)COLLECTION PERIODSALES TO INVENTORYASSETS TO SALESSALES TO NET WORKING CAPITALACCOUNTS PAYABLE TO SALES

PROFITABILITYRETURN ON SALESRETURN ON ASSETSRETURN ON NET WORTH

Figure 1. Format for obtaining key financial ratios

1 5

business has paid for its goods (i.e., thepercentage of sales in excess over the cost ofsales). Similarly, gross profit (or grossmargin) is the difference between the salesrevenue and the cost of sales.

To apply this information you will have toestimate your first year's sales. If you esti-mate $100,000 in sales your first year, this iswhat you would find:

$100,000 in sales x 50% = $50,000 gross margin

$100,000 in sales x 30% = $30,000 in overheadexpenses

$ 50,000 gross margin - $30,000 in overheadexpenses = $20,000 net profit before taxes

Note that the cost of sales is usually a directcost incurred by the business. However, theoverhead cost is generally considered an in-direct cost (we assume that the debt expenseis also included in the overhead).

Furthermore, if you found that the averagerate of inventory turnover for retail flowershops was 10 times annually, you could alsofigure the average dollar inventory youwould need. Since you estimated your grossmargin to be $50,000 on sales of $100,000,the cost of the flowers you sold were$50,000. Now, using the following formula,you can determine the average amount ofinventory you need to have on hand.

Cost of merchandise (flowers) sold =Average rate of inventory turnover

Average Inventory to Have in Stock

$50.000 = $5,00010

One of the first considerations in financingyour business is to determine how much

7

money is needed for inventory, accounts re-ceivable, and, of course, for cash. All ofthese will comprise your current assets. Toa large extent, your investment in current as-sets will depend upon what you anticipateyour current liabilities to be on the openingday of business. A rule of thumb is thatcurrent assets should be twice that of currentliabilities.

In estimating inventory requirements for awholesale or retail business, talk to prospec-tive suppliers. Such an estimate should bechecked against the typical ratio of inventoryin relation to sales, if you have such a ratiofor your business. For example, assume thatnet sales in your type of business are typi-cally six times the inventory. Then for an-nual net sales of $375,000, your inventoryshould be $62,500.

You should make this type of calculation toestablish a maximum dollar figure for inven-tory and not go above it. Otherwise, you oryour suppliers might be over enthusiasticabout the amount of merchandise you shouldstock for your initial inventory.

WHAT IS SPECIALABOUT FINANCINGA MANUFACTURINGBUSINESS?

The procedure for estimating the moneyneeded to start a swill factory is similar, butyou will need to determine the costs for bothproduction capacity (plant and equipment)and your raw material and work-in-progressinventory.

16

8

For example, suppose you wish to manufac-ture an automotive part and hope to make anannual net profit of $20,000. Yearly sales of$500,000 will be necessary, computed at a 4percent profit. How many units must beproduced to attain this volume?

Assume you plan to manufacture one partthat will sell for an average of $20. Toreach a sales volume of $500,000, you mustsell 25,000 units. This means an average of500 units per week for 50 weeks. You arenow in a position to determine how muchmachinery, equipment, and floor space willbe required to produce 500 units per week.

How much down payment for the equipmentwill be necessary? Should you lease someof the equipment? How many operators willbe needed? You must add estimates of thecosts for materials, wages, rent, sales, office,and other expenses for a period necessary toproduce enough units for one complete turn,that is, the annual production (25,000 unitsin this case) divided by the expected numberof stock turns per year. This will provide arough estimate of the investment you willhave to make in acquiring and producinginventory.

WHAT IS SPECIAL ABOUTFINANCING A SERVICEBUSINESS?

Estimating the money r.:.eded to start aservice establishment will involve a com-bination of the methods used for merchan-dising and manufacturing businesses. To theextent that the service business carries goodsfor sale, estimates could be made in themanner outlined for wholesale and retail

concerns. To the extent that the businesssells labor or machine work, money neededfor equipment and wages could be estimatedin a similar fashion as for a factory.

WHAT IS SPECIAL ABOUTFINANCING A FRANCHISEDBUSINESS?

"Holiday Inn," "Kentucky Fried Chicken,"and "McDonald's" are all familiar franchis-ing organizations. The capital required topurchase an outlet of many of the large, suc-cessful franchise organizations can rangefrom hundreds of thousands to several mil-lion dollars. Yet some franchise outlets canstill be purchased for a thousand dollars.Those franchises that require the least start-up cash are in the business aids and serviceareasareas that are expected to have rapidgrowth.

Franchising offers a means of becoming anentrepreneur, being your own boss, and pro-fiting from being a part of a big businesswith national or regional advertising, large-scale purchasing power, and exclusive distri-bution of name brands. If you can providethe capital, franchising may be the way toown your own business and make a respec-table profit.

Information on Franchising. If you areconsidering opening a franchise, you shouldcheck several resources. Write for annualreports and other brochures from the parentcompany. Ask to be sent disclosure state-ments. The sources below, among others,should be consulted prior to making acommitment to work with a franchisingcompany:

Franchising Opportunities, availablefrom International Franchise Association,1350 New York Avenue, NW, Suite 900,Washington, D.C. 20005

Franchising in the Economy, availablefrom IFA Education Foundation, Inc. andHorwath International, IFA provides cur-rent information on trends and statisticalcomparisons in the franchising business.

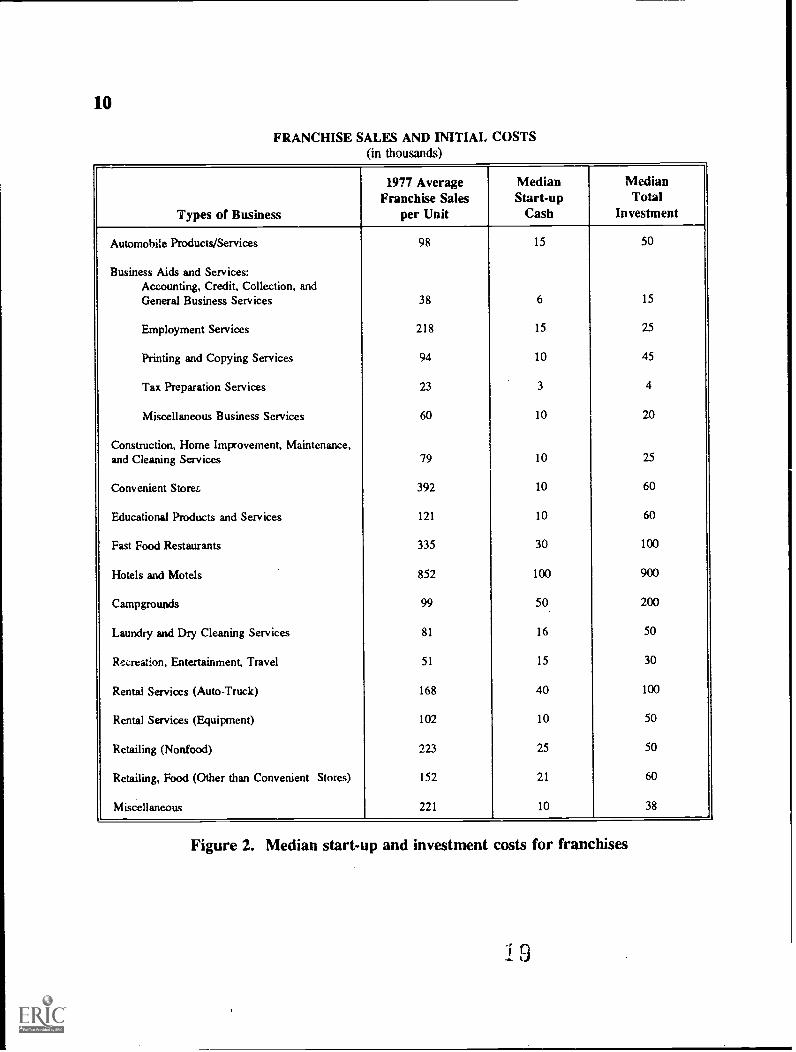

Figure 2 illustrates the format utilized byone publication to describe the expected in-vestment, sales, and industry statistics youwill need to evaluate in determining thestart-up costs and potential viability of afranchise opportunity. These types of sta-tistics are repeated for each industry groupand franchising company for several thou-sand different companies. Some of the ser-vice businesses can be started with a rela-tively small total investment. Tax prepara-tion businesses are a good example. Otherbusinesses, like fast-food restaurants, mayrequire large investments of $300,000 ormore.

HOW DO YOU DETERMINETHE FINANCING NEEDED TOSTART YOUR BUSINESS?

If you have been thorough in your investiga-tion, you should have sufficient information

9

aboutindustry averages, operating ratios, andother general factors affecting the type andamount of financing that your particular typeof business requires. It is also advantageousfor you to have also talked with bankers,suppliers, competitors, and other knowledge-able people in or related to your industry.

Now is the time to put what you have learn-ed to work. Using the information you havegathered, the next section will assist you indetermining your financing needs on a step-by-step basis. The first step involves esti-mating your sales. The second step is esti-mating start-up costs. The third step is cal-culating monthly operating expenses. Thefourth step is figuring personal living ex-pense requirements. The fifth step is addingthe start-up, operating, and personal livingexpenses together to determine the total fi-nancing needed to put your business intooperation.

WHAT IS INVOLVED INESTIMATING ANNUALSALES VOLUME?

The first step in determining the financingyou need is to estimate sales volume foryour first year of operation. Your estimatedsales volume becomes the target or the goalfor all of your expenses in time, effort, andmoney. Your annual sales goal provides theparameter or means by which you can keepyour estimate of financing realistic. Thereshould be a very definite relationship be-tween sales and expenses.

IS

10

FRANCHISE SALES AND INITIAL COSTS(in thousands)

Types of Business

1977 AverageFranchise Sales

per Unit

MedianStart-up

Cash

MedianTotal

Investment

Automobile Products/Services 98 15 50

Business Aids and Services:Accounting, Credit, Collection, andGeneral Business Services 38 6 15

Employment Services 218 15 25

Printing and Copying Services 94 10 45

Tax Preparation Services 23 3 4

Miscellaneous Business Services 60 10 20

Construction, Home Improvement, Maintenance,and Cleaning Services 79 10 25

Convenient Storer. 392 10 60

Educational Products and Services 121 10 60

Fast Food Restaurants 335 30 100

Hotels and Motels 852 100 900

Campgrounds 99 50 200

Laundry and Dry Cleaning Services 81 16 50

Rfxreation, Entertainment, Travel 51 15 30

Rental Services (Auto-Truck) 168 40 100

Rental Services (Equipment) 102 10 50

Retailing (Nonfood) 223 25 50

Retailing, Food (Other than Convenient Stores) 152 21 60

Miscellaneous 221 10 38

Figure 2. Median start-up and investment costs for franchises

9

There are many factors to consider whenestimating sales volume. You must estimatethe total amount of business in the area, andthe number and ability of competitors nowsharing that business. Your own ability tocompete for the customers' dollars will alsoimpact on sales volume.

One approach to determining your indepen-dent estimate is to start with the income youdesire. Suppose you hope to earn annualprofits of $15,000. Your research revealsthat the rate of net profit on sales for thetype of business you plan to operate is4 percent. To bring an annual return of$15,000, a sales of $375,000 ($15,000divided by 4%) is required. This is a salesgoal not a realistic projection. To determineif this level of sales is reasonable, crosscheck it against several other methods. Forexample, your industry association may pro-vide average sales per square foot for retaillocations. Once you know the size of yourstore you can compute expected sales forcomparison with your goal.

In reaching your final estimate of sales, becautious. A new business generally growsslowly at the start. If you overestimatesales, you are likely to invest too much inequipment and initial inventory and commityourself to heavier operating expenses thanyour actual sales volume will justify. Youwill have to estimate the number of custom-ers and their buying habits by conductingsome market research. You may obtain as-sistance in this research for making yoursales estimate from wholesalers, trade asso-ciations, your banker, and other businesspeople. The counsel of others can be com-pared with your independent estimate ofwhat you believe is needed to make theeffort worthwhile to you.

11

HOW DO YOU ESTIMATESTART-UP COSTS ANDMONTHLY OPERATINGEXPENSES?

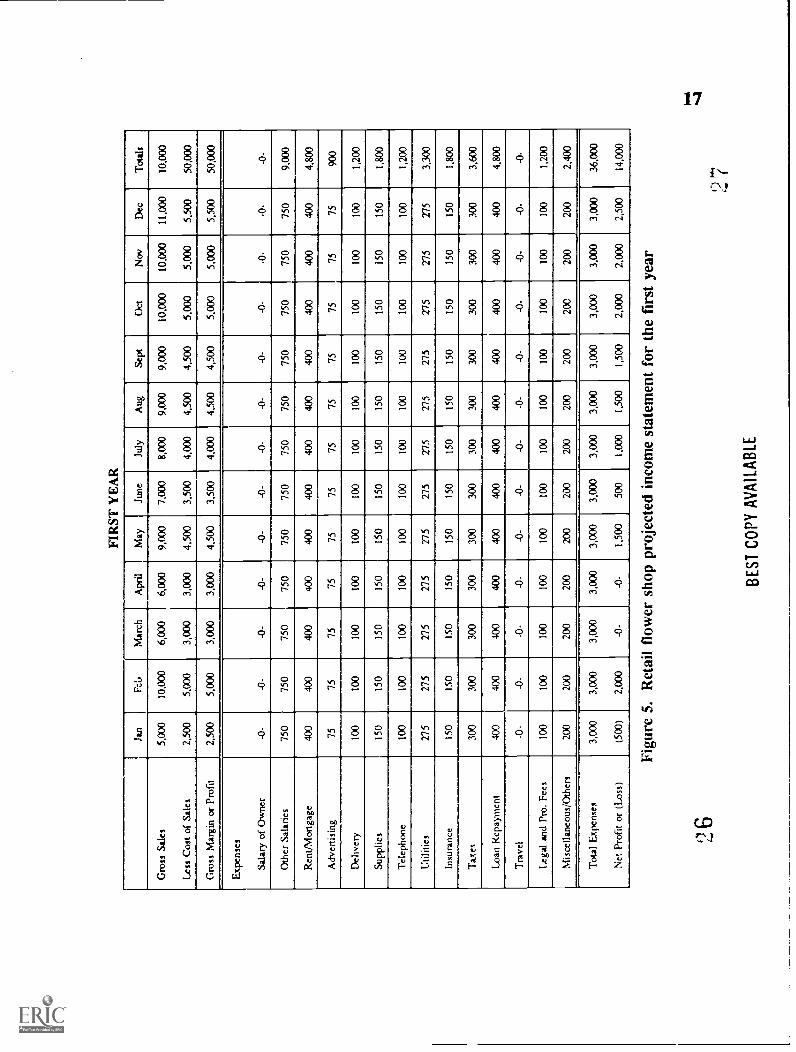

The investigation you completed of the ex-pense and sales structure of your businessshould now enable you to make educatedestimates of your start-up costs and monthlyoperating expenses. The worksheet inFigure 3 provides a logical approach forgetting your estimates on paper and a meansof comparing your figures with industrynorms.

The expense and start-up cost worksheet isdivided into five columns and a set of cate-gory labels describing a listing of the variousstart-up costs and monthly operating ex-penses you have. In each column, youshould write in the figures you have dis-covered or calculated in your investigation.

Column one shows the results of your inves-tigations of industry operating ratios ex-pressed as a percentage of sales. Column

three is your best estimate of the actualmonthly expenses your business will facebased upon price quotes, your judgement,business colleagues, and the corrnet:tion.Competition in this case does not necessarilymean the strongest firm against which youwill compete. Rather, it means a business ofa similar size that has been engaged in thetype of sales or services that you want toestablish. It will be difficult to developaccurate data from you competition, but it isessential that you conduct the best surveyyou can to develop your estimates.

Column two is simply calculated by divid-ing each estimate by monthly sales and

12

expressing the result as a percentage. Youcan now directly compare the industry-wideoperating ratios with your own projectedoperating ratios. You will need to explaincarefully any wide differences between yourestimates and the industry norms. For exam-ple, if your rent costs are much lower thanthe industry average, you may wonder ifyour location is of sufficient quality tosupport the number of customers you plan tohave.

As an illustration, Figure 3 has been com-pleted based upon research indicating salesof $100,000 per year or $8,333/monthly.Assume that this figure is lower than theindustry norms for first year sales, but youhave elected to accept your own more con-servative estimates to avoid planning forhigher operating and start-up costs for plan-ned inventory, etc. Your industry sourcesalso have indicated that your sales during thefirst four months will average several thou-sand dollars less than the annual average.

As you can see from the example in Figure3, the prospective owner of the retail flowershop has used the worksheet to determinethe money needed to start the business. Tobe sure there is enough cash on hand tocover monthly operating expenses for threemonths, the owner will need $9,000. This,added to the $18,775 of start-up costs, showsa total need of $27,775 to get the retailflower shop open and operating.

Entrepreneurs should also remember to con-sider their personal living expenses whendetermining the total financing needed tostart the business. In some situations, anentrepreneur will have to take money fromthe business each month to pay for all orpart of the personal living expenses. If thisis the case, it is critical that the amount

needed be known and at least that much ispaid to the owner as a salary.

The business owner's living expenses arehandled in numerous ways. Sometimes theowner will continue to hold a regular payingjob in order to receive a steady paycheckuntil the new business is large enough tosupport the entrepreneur. Other times, theincome of the owner's spouse is sufficient,and it is not necessary to consider personalliving expenses when determining how muchcash is needed to get the business going.Then, too, some entrepreneurs will have sev-eral months of personal living expensessaved to use until the business has grownenough to take a salary.

The personal living expenses worksheet inFigure 4 is an effective means of determin-ing the entrepreneur's costs of living. Witha total figure in mind, the business ownercan then calculate how the expenses will behandled. The entrepreneur who started theflower shop did not take a salary. This wasto keep monthly operating expenses (and,consequently, the cash needed to start thebusiness) as low as possible. Also, this waspractical because the entrepreneur's spouseearned enough income to pay all of theirpersonal living expenses. In the example,personal living expense worksheet illustratesthis situation. According to the flower shopentrepreneur, personal living expenses to-talled $1,775 per month. The spouse's takehome pay was $1,815.

Both of the worksheets discussed here arealso available as computer spreadsheets.

Salary of ownerOther salariesRent/mortgageAdvertisingDelivery expensesSuppliesTelephoneUtilitiesInsuranceTaxesLoan repaymentTravelLegal and Professional feesMiscellaneous/Others

Total

Projected Monthly Sales Income (in thousands)

FriendCompetitionAverageYours

Jan

67

6.55

Feb

11

14

12.510

Mar

712

9.56

Apr

7

10

8.56

May Jun

89

8.57

Jul

9998

Aug,

999

9

So

1011

10.5

9

Oct

911

1010

Nov Dec

1012

11

11

10101010

101211

9

Figure 3. Start-up costs and operating expense worksheet

14

DETAILED PERSONAL BUDGET

Based on average monthdoes not cover purchase of any new items except emergency replacements.

DETAILED BUDGET

Regular Monthly Payments

Rent or House Payments(including taxes)

Car Payments (including insurance)

Appliances/TV Payments

$ 350

Food Expense

Food-At Home

Food-Away from Home

TOTAL

Personal Expense

$ 150

50175

65$ 200

Home Improvement Loan Payments 0

Personal Loan Payments 35Clothing, Cleaning,Laundry, Shoe Repair 65

Health Plan Payments 55 Drugs 15

Life Insurance Premium 110 Doctors and Dentists 30

Other Insurance Premiums 50 Education 0

Miscellaneous Payments 50 Dues 0

TOTAL $ 890 Gifts and Contributions 10

Household Operating Expense Travel 0

Telephone 60 Newspapers, Magazines, Books 15

Gas and Electricity 140 Auto Upkeep, Gas, and Parking 150

Water 25 Spending Money, Allowances 100

Other Household Expenses,Repairs, Maintenance 75

TOTAL $ 385

Total Personal Living Expenses $1,775TOTAL $ 300

Spouse's Net Monthly Pay $1,815

Figure 4. Personal living expenses worksheet

With the completion of this step (figuringthe amount needed to cover personal livingexpenses), the procedure for determining thetotal amount of cash needed to start the busi-ness is nearly completed.

HOW DO YOU DETERMINETHE TOTAL CASH NEEDEDTO START THE BUSINESS?

The fifth and final step simply involvesadding the total needed for monthly oper-ating expenses and start-up costs from thesecond worksheet (Figure 3) with the totalneeded to pay for personal living expenses(Figure 4). In the flower shop example, thetotal cash needed was $27,775 since thespouse's income was sufficient to handle allthe personal living expenses.

HOW DO YOU PREPARE TOARRANGE THE FINANCING?

Over the past seven years, the flower shopowner has saved $10,000 to start the busi-ness. The question now is where the re-maining $17,775 will come from. Sincesharing ownership in the business is notdesirable, debt financing through some typeof loan may be most realistic. With this inmind, the flower shop owner knows thatcommercial lenders will want financial state-ments projecting the activity of the business.In addition, a statement reflecting the per-sonal financial position of the entrepreneur isfrequently required. If an entrepreneur doesnot have his or her own personal finances ingood condition, lenders will question vvoeth-

,)4

15

er the finances of the business can be hand-led properly. Therefore, the projected in-come statement, projected cashflow state-ment, and personal balance sheet must beprepared.

HOW DO YOU PREPAREA PROJECTED INCOMESTATEMENT?

To lend money to a business just beingstarted, most lenders require a projection ofthe monthly income for the first year. Thisstatement provides an estimate of when thebusiness will begin to make money and howmuch it will make. This is important to thelender, since loan repayments generally aremade from business profits.

The projected income statement is fairlyeasy to construct if you have used the work-sheets previously presented to estimate salesand monthly operating expenses. The fol-lowing steps make the development of theprojected income statement simple.

Step 1. List your estimated gross sales on amonthly basis.

Step 2. List the costs of the merchandise (orservice) you estimate will be soldmonthly.

Step 3. Subtract the cost: 'f the merchan-dise (or service) rrom your esti-mated gross sales. The resultingfigure is your gross margin orprofit.

Step 4. Itemize the monthly operating ex-penses.

1

16

Step 5. Total the monthly operating ex-penses.

Step 6. Subtract the monthly operating ex-penses from the gross margin orprofit. The resulting figure is thenet income for the month. Lossesare shown by putting parenthesesaround the number. For example a$500 loss would be listed as ($500).

The projected income statement for the retailflower shop is provided in Figure 5. As youcan see, the owner is projecting a $500 lossthe first month of operation. Sales are esti-mated to be much higher during February,the second month, because of Valentine'sDay. Therefore, a $2,000 profit is estimatedfor the month. The third and fourth monthsshow an equal amount of gross margin orprofit and expenses, so there is neither aprofit nor a loss, i.e., the business breakseven. A profit is estimated for the remain-ing months of the first year and, subsequent-ly, a $14,000 total profit for the first year.

HOW DO YOU PREPAREA PROJECTED CASHFLOW STATEMENT?

Will you be able to pay the suppliers intime to receive the discount? When duringthe year will contracts be bringing in cash?To answer these questions, you need to pro-ject your cashflow. The cashflow projectiongives you a picture of the amount of cashthat will come into and go out of your busi-ness. If you sell on credit, not all sales willproduce cash. Also, your firm's income andexpenses are not going to be constant eachmonth. Therefore, it is necessary to predict

the month-by-month pattern in which cashwill actually come in and go out. You canthen anticipate, for example, if you will needa loan to cover expenses and can begin mak-ing arrangements to obtain one early.

Like the projected income statement, theprojected cashflow statement uses much ofthe financial information that you have pre-viously calculated. The net income youhave projected, plus any additional disburse-ments or expenditures, are the two majorcomponents. The step-by-step procedure forpreparing the projected cashflow statement isas follows.

Step 1. Add together any cash on hand andloans you have to determine the to-tal amount of cash you have to startthe business.

Step 2. Subtract the start-up costs to projectthe actual amount of cash left overto start the business. (Steps 1 and 2were completed in the preoperatingcolumn.)

Step 3. For each month of the first year ofoperation, add the estimated profitor loss that you have previouslydetermined.

Step 4. Determine other cash expendituresor disbursements and list them.

Step 5. Total the disbursements.

Step 6. Subtract the total disbursementsfrom the cash received during eachmonth. This is the net cashflow.

FIR

ST Y

EA

R

Jan

Fcl

,M

arch

Apr

ilM

ayJu

neJu

lyA

ugS

ept

Oct

Nov

Dec

Tot

als

Gro

ss S

ales

Less

Cos

t of S

ales

5,00

0

2,50

0

10,0

00

5,00

0

6,00

0

3,00

0

6,00

0

3,00

0

9,00

0

4,50

0

7,00

0

3,50

0

8,00

0

4,00

0

9,00

0

4,50

0

9,00

0

4,50

0

10,0

00

5,00

0

10,0

00

5,00

0

11,0

00

5,50

0

10,0

00

50,0

00

Gro

ss M

argi

n or

Pro

fit2,

500

5,00

03,

000

3.00

04,

500

3,50

04,

000

4,50

04,

500

5,00

05,

000

5,50

050

,000

Exp

ense

s

Sal

ary

of O

wne

r-0

--0

--0

--0

--0

--0

--0

--0

--0

--0

--0

--0

--0

-

Oth

er S

alar

ies

750

750

750

750

750

750

750

750

750

750

750

750

9,00

0

Ren

t/Mor

tgag

e40

040

040

040

040

040

040

040

040

040

040

040

04,

800

Adv

ertis

ing

7575

7575

7575

7575

7575

7575

900

Del

iver

y10

010

010

010

010

010

010

010

010

010

010

010

01,

200

Sup

plie

s15

015

015

015

015

015

015

015

015

015

015

015

01,

800

Tel

epho

ne10

010

010

010

010

010

010

010

010

010

010

010

01,

200

Util

ities

275

275

275

275

275

275

275

275

275

275

275

275

3,30

0

Insu

ranc

e15

015

015

015

015

015

015

015

015

015

015

015

01,

800

Tax

es30

030

030

030

030

030

030

030

030

030

030

030

03,

600

Loan

Rep

aym

ent

400

400

400

400

400

400

400

400

400

400

400

400

4,80

0

Tra

vel

-0-

-0-

-0-

-0-

-0-

-0-

-0-

-0-

-0-

-0-

-0-

-0-

Lega

l and

Pro

. Fee

s10

010

010

010

010

010

010

010

010

010

010

010

01,

200

Mis

cella

neou

s /O

ther

,20

020

020

020

020

020

020

020

020

020

020

020

02,

400

Tot

al E

xpen

ses

Net

Pro

fit o

r (L

oss)

3,00

0

(500

)

3,00

0

2,00

0

3,00

0

-0-

3,00

0

-0-

3,00

0

1,50

0

3,00

0

500

3,00

0

1.00

0

3,00

0

1,50

0

3,00

0

1,50

0

3,00

0

2,00

0

3,00

0

2,00

0

3,00

0

2,50

0

36,0

00

14,0

00

26

Figu

re 5

.R

etai

l flo

wer

sho

p pr

ojec

ted

inco

me

stat

emen

t for

the

firs

t yea

r

BE

ST

CO

PY

AV

AIL

AB

LE

18

Step 7. Add the net cashflow to the cumula-tive cashflow, which is the totalamount of cash left over from theprevious months. This gives youthe total amount of cash you haveaccumulated.

As an example, the projected cashflow state-ment for the retail flower shop is presentedin Figure 6. The 'ntrepreneur's $10,000 insavings is added to the $17,775 in start-upcosts that will be expended in opening thebusiness is subtracted. If you recall, thestart-up costs for this business were esti-mated at $18,775. However, since $500 wasfor cash and $500 was for accounts receiv-able, and since these two items were notspent but were actually put into the cash ac-count of the business, they were taken out ofthe start-up costs disbursement. This left thebusiness with $10,000 in cash to begin oper-ating the business.

Each month the entrepreneur is estimatingsome additional disbursement beyond month-ly operating expenses. In January it is $150.Although these disbursements are not specif-ically labeled in this example, there shouldbe a specific purpose intended for themoney. The $150 in January might be foradditional grand opening expenses. The$3,000 in September is to buy a used van fordeliveries. Extra holiday personnel may beneeded in December, and $1,750 is desig-nated to pay these people. As you can see,it is important to plan your cash disburse-ments on a monthly basis to determine theimpact they will have on your cashflow.

You may have a negative cashflow in somemonths. This occurs when you spend morecash than you take in during the month.You will notice this is the case in January,March, April, and September. This is feasi-

ble for the flower shop owner because therewill be sufficient cash accumulated to makeup the difference. If this were not the case,some type of loan or credit arrangementmight be necessary.

HOW CAN YOU JUSTIFYYOUR FINANCIALPROJECTIONS?

Projections are based upon uncertain as-sumptions about the future. You will needto prepare for the arguments that will beraised against your proposals by those youapproach for financing. The best counterargument is to include answers to the basicquestions in your original presentation.Remember, lenders or investors are primarilyinterested in assuring that they are repaid.Four types of answers should be includedwithin your financial plan as follows:

1. Provide clearly stated assumptions uponwhich you base your projections of

sales,

cost of goods sold,

expenses,

cashflow timing,

accounts receivable collections, and

supplier reliability.

FIR

ST Y

EA

R

Pre-

oper

atin

gJa

nFe

bM

arch

Apr

ilM

ayJu

neJu

lyA

ugus

tSe

ptO

ctN

ovD

ec

SO4.

1=3

of C

ash

Cas

h on

Han

dS1

0,00

0

Loa

n17

,775

Net

Pro

fit

(500

)2,

000

-0-

-0-

1,50

050

01,

000

1,50

01,

500

2,00

02,

000

2,50

0

Tot

al27

,775

(500

)2,

000

-0-

-0-

1,50

050

01,

000

1,50

01,

500

2,00

02,

000

2,50

0

Dis

burs

emen

ts

Star

t-up

Cos

tsO

wne

r's D

raw

17,7

75

Inco

me

Tax

1,50

0

Oth

ers

(bey

ond

mon

thly

oper

atin

gex

pens

es)

150

200

100

100

300

100

200

300

3,00

030

030

01,

750

Tot

al17

,775

150

200

100

1,60

030

010

020

030

03,

000

300

300

1,75

0

Net

Cas

h Fl

ow10

,000

(650

)1,

800

(100

)(1

,600

)1,

200

400

800

1,20

0(1

,500

)1,

700

1,70

075

0

Cum

ulat

ive

Cas

h Fl

ow10

,000

9,35

011

,150

11,0

509,

450

10,6

5011

,050

11,8

5013

.050

11,5

5013

250

14,9

5015

,700

Figu

re 6

. Ret

ail f

low

er s

hop

proj

ecte

d ca

shfl

ow f

or th

e fi

rst y

ear

*Net

pro

fit i

s ca

rrie

d ov

er f

rom

the

proj

ecte

d pr

ofit-

and-

loss

sta

tem

ent.

rS

29

20

2. Provide complete documentation whichexplains how you developed each costestimate or projection. For example,

copies of quotes from suppliers,

references to specific industry operat-ing ratio reports, and/or

results of surveys you have made ofcustomers and competitors.

3. Provide a realistic discussion of the"downside" risks of the proposed busi-ness. Frankly discuss those areas whereyou are not sure exactly what will hap-pen during the projection period.

For each risk that you identify, developan alternative plan that will allow thebusiness to keep operating (and repayingany loans.)

4. Develop a clear, concise discussion ofthe "safety" margin you have built in toyour projections. Use the lowest salesand highest cost estimates. Use "conser-vative" assumptions in preparing yourprojections.

When your plan is "justified" to your satis-faction, you should present it to a businessadvisor or counselor who has no financial orother stake in your business. Small BusinessDevelopment Center or SCORE counselorsare excellent at providing an objective sec-ond opinion and critique of your plan. It iscritical that you experience this type of criti-cism prior to presenting the plan to an inves-tor or lender. You can expect to receivestrong criticism on your first effortslater

versions will be much better justified andrealistic in the eyes of potential lenders.

HOW DO YOU PREPAREYOUR PERSONALBALANCE SHEETS?

Your personal balance sheet provides anypotential lender with an overall view of yourfinancial position. A sufficiently large networth, will make you more appealing as aloan applicant. An entrepreneur with a weakfinancial position and a large number ofdebts may not meet the standards of thelenders.

The personal balance sheet includes a sum-mary of your assets, what you own that hascash value, and your liabilities or debts. Theexample in Figure 7 is of an entrepreneurstarting the flower shop.

Preparing your personal balance sheet in-volves a few simple steps.

Step 1. Determine the value of all your as-sets. These would be the items youown that have cash value. Listthem on the balance sheet.

Step 2. Total the value of your assets.

Step 3. List all of your debts.

Step 4. Total the amount of your debts andliabilities.

Step 5. Deduct your total liabilities fromyour total assets. This is your networth.

31

21

ASSETS: Everything you own with cash value.

Cash money you have on hand and in the bank $ 975.00Savings account $10,000.00Stocks, bonds, other securitiesAccounts/notes receivable

TOTAL ASSETS $87,373.00LESS TOTAL LIABILITIES $39,460.00

NET WORTH $47,913.00

Figure 7. Personal balance sheet for retail flower shop owner

SOURCE: 'eprinted with permission from Bank of American NT&SA, "Steps to Starting adusiness," Vol. 10, No. 10, Small Business Reporter.

22

The financial position of the entrepreneurstarting the flower business is solid. Theassets include cash, personal savings, lifeinsurance, an automobile, real estate, andpersonal property. The liabilities are fairlylimited, with the biggest loan being themortgage on the real estate. There is about$2.22 worth of assets for every $1.00 of lia-bility. It is evident that the entrepreneur hashandled his or her personal financial affairswell. This will certainly help impress acommercial or government lender, andshould help obtain the necessary debt fi-nancing to get the flower shop started.

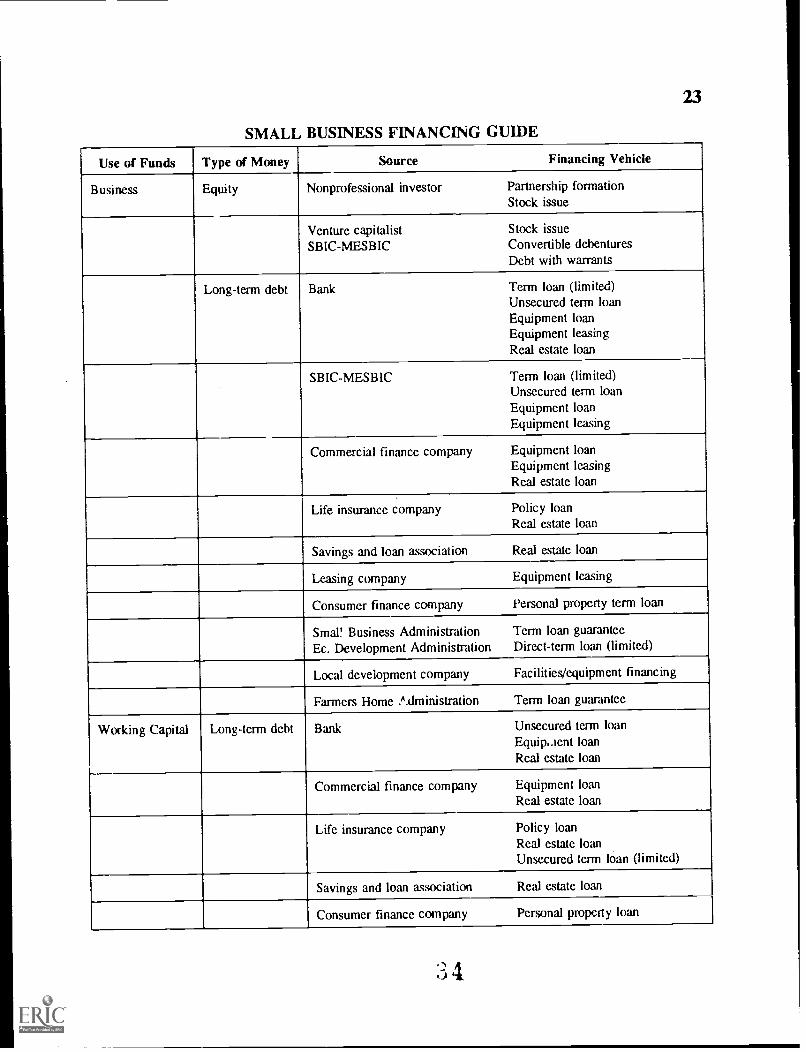

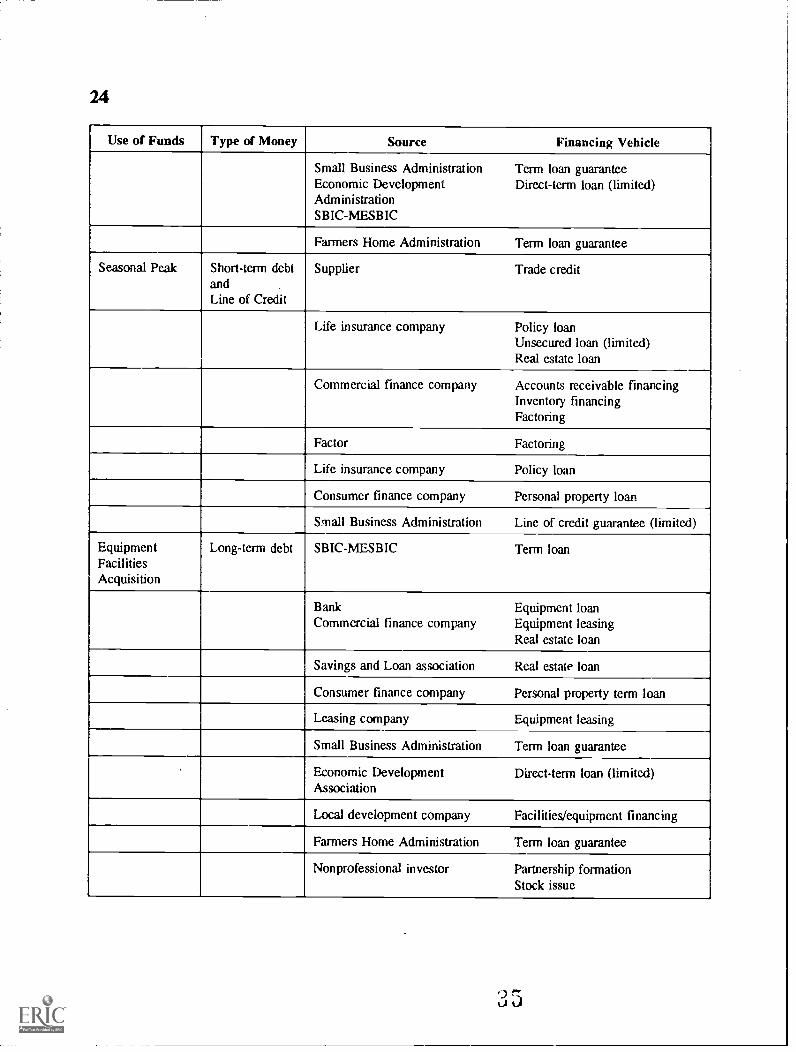

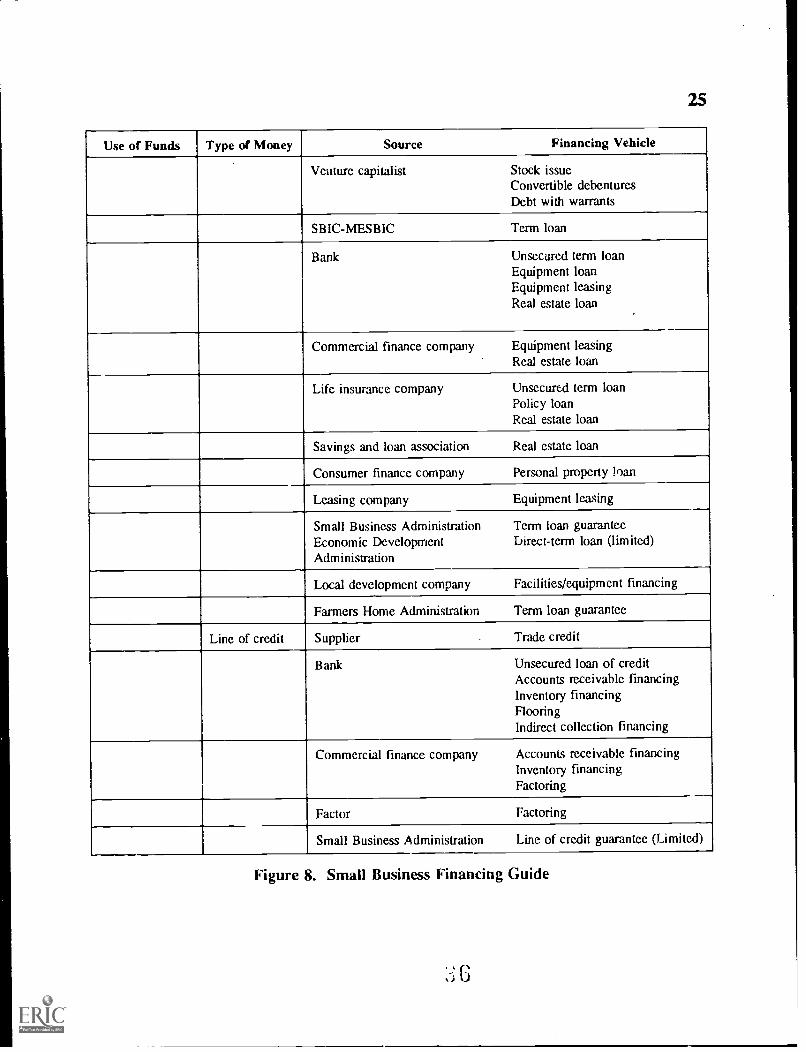

HOW DO YOU DETERMINEWHICH FINANCINGSOURCES TO USE?

With the financial statements prepared, youare now ready to zero in on the specific fi-nancing sources you wish to use. The mixof sources that the entrepreneur will even-tually use is based upon the interaction ofseveral variables. Some of these variablesare as follows:

The amount and timing of the moneyneeded

Current economic conditions and prevail-ing interest rates

The credit record of the entrepreneur

The specific purpose that the financingwill be used for

The type of business being started andits prospect for success

An aspiring entrepreneur should study thesituation carefully. It may be wise to dis-cuss the matter with your local banker, SBAoffice, or Small Business Development Cen-ter consultant. The Small Business Financ-ing Guide presented in Figure 8 may behelpful, as well.

33

23

SMALL BUSINESS FINANCING GUIDE

Use of Funds Type of Money Source Financing Vehicle

Business Equity Nonprofessional investor Partnership formationStock issue

Use of Funds Type of Money Source Financing Vehicle

Venture capitalist Stock issueConvertible debenturesDebt with warrants

SBIC-MESBIC Term loan

Bank Unsecured term loanEquipment loanEquipment leasingReal estate loan

Commercial finance company Equipment leasingReal estate loan

Life insurance company Unsecured term loanPolicy loanReal estate loan

Savings and loan association Real estate loan

Consumer finance company Personal property loan

Leasing company Equipment leasing

Small Business AdministrationEconomic DevelopmentAdministration

Term loan guaranteeDirect-term loan (limited)

Local development company Facilities/equipment financing

Farmers Home Administration Term loan guarantee

Line of credit Supplier Trade credit

Bank Unsecured loan of creditAccounts receivable financingInventory financingFlooringIndirect collection financing

Commercial finance company Accounts receivable financingInventory financingFactoring

Factor Factoring

Small Business Administration Line of credit guarantee (Limited)

Figure 8. Small Business Financing Guide

26

HOW DO YOU PREPARE ALOAN APPLICATIONPACKAGE?

The choice of financing sources you qualifyfor and decide to use will essentially dictatethe contents of your loan application pack-age. Whereas some lenders may request avery detailed presentation, otherswho mayalready know youmay ask for less infor-mation.

The breadth, depth, and quality of your loanapplication package will dramatically affectyour chances for approval. It is vital to puttogether a package that presents you, yourideas, and your business plan in an impres-sive manner.

The following is an outline of a businessloan application package.

Loan Application Package Outline

I. Basic Application Information

A. Applicant's name, address, and tele-phone number

B. Business name, address, and telephonenumber

C. Type of businessD. Size of businessE. Type of ownershipF. Applicant's financial contribution to

business

II. Loan Request

A. Purpose of loanB. AmountC. Terms, including desired interest rateD. Debt/equity ratioE. CollateralF. Specific use of motley borrowed

III. Applicant's Personal Information

A. Resume, including education, workexperience, and business background.

B. Credit referencesC. Personal balance sheetD. Past two to three years' income tax

statements

IV. Business Information

A. Business planB. Life and casualty insurance coverageC. Business licenses or permitsD. Lease/facilities agreementE. Other supporting information

V. Financial Projections

A. Projected monthly income statementfor at least one year

B. Projected cashflow statement for atleast one year

C. Some lenders may also ask for a pro-jected balance sheet for the first year

The above outline should help you under-stand what kind of information lenders re-quire to approve loans. Loan applicationpackages should be filled out by entrepre-neurs in a most logical and accurate waypossible. It is this package, along with thebusiness plan that convinces the banker orother lenders to offer a loan.

To better acquaint yourself and understandthe requirements of a loan application, referto the Bank One Business Loan Kit preced-ing the Activity section.

HOW DO YOU CONSTRUCTA PLAN OF ACTION TOSATISFY YOUR FINANCINGNEEDS?

Determining and satisfying the financingneeds of your business takes a great deal ofthought, planning, and organizing. You needto develop and execute a complete plan ofaction. The following Checklist for Financ-ing Your Business should help you as youdevise your plan. The checklist items are

27

organized by the steps you need to take toarrange your financing. To determinewhether you are being thorough in complet-ing the financial steps, ask yourself eachquestion on the checklist. If you have com-pleted the activity, put a check mark (4)beside the item. If you answer no to thequestion, leave the line blank. Then, askyourself if the item is applicable to yoursituation. If it is, you should plan to com-plete the activity. If it is not, put N/Abeside the question and go on to the nextitem. After completing all the checklistitems, your financing plan should be readyto go.

Checklist for Financing your Business

Step 1. Investigate Your Financial Needs

Have you obtained specific informationon operating ratios and start-up costsfrom trade associations, the SBA, fi-nancial service companies, and othersources?

Have you talked with others, includingcompetitors in your field?

Have you talked with your banker, sup-pliers, and other knowledgeable sourcesabout your financing needs?

Have you determined what is uniqueabout financing your particular type ofbusiness?

Step 2. Determine the Type and Amountof Financing You Need

Have you used the information gatheredin your investigation?

Have you used operating ratios to esti-mate your financial needs?

Have you used actual quotations ofprices for inventory and equipmentneeds?

Have you estimated your sales volumefor the first year?

Have you determined what type of start-up costs and monthly operating expensesyou will have?

Have you completed Start-up Costs andOperating Expenses Work sheet (Figure3)?

Have you determined where the moneywill come from to cover your personalliving expenses while you start thebusiness?

28

Have you used the Personal Living Ex-pense Work sheet (Figure 4) to deter-mine your monthly personal budget?

Step 3. Prepare to Arrange the FinancingYou Need

Have you determined how much you arepersonally going to invest in the busi-ness?

Have you determined how much addi-tional financing you are going to need,beyond your personal investment, to getthe business started?

Have you prepared a projected incomestatement (Figure 5)?

Have you prepared a projected cashflowstatement (Figure 6)?

Have you prepared a personal balancesheet (Figure 7)?

Have you received a "second opinion"from an objective professional businessadvisor or counselor?

Step 4. Determine which Financing to Use

Have you considered the advantages anddisadvantages of the equity financingalternatives?

Have you considered the advantages anddisadvantages of the debt financing alter-natives?

Have you considered which sources offinancing you qualify for?

Have you determined the type and formof financing that best suits the needs ofyour business?

Have you determined the priority for ap-proaching and using your potential fi-nancing sources?

Step 5. Prepare the Loan ApplicationPackage

Have you discussed loan application pro-cedures with potential lenders?

Have you determined the information re-quired for the loan application package?

Have you determined what collateral youwill use?

Have you gathered and organized the in-formation needed for your loan applica-tion package?

Have you completed your loan applica-tion package and had it reviewed andchecked by another person?

Step 6. Present the Loan ApplicationPackage and Negotiate the Fi-nancing Needed to Start YourBusiness

Securing financing for your business is onlythe beginning. But, solid financing is essen-tial for a good beginning. The process canbe complicated, and at times a little over-whelming. Therefore, make sure you arewell-advised and choose carefully.

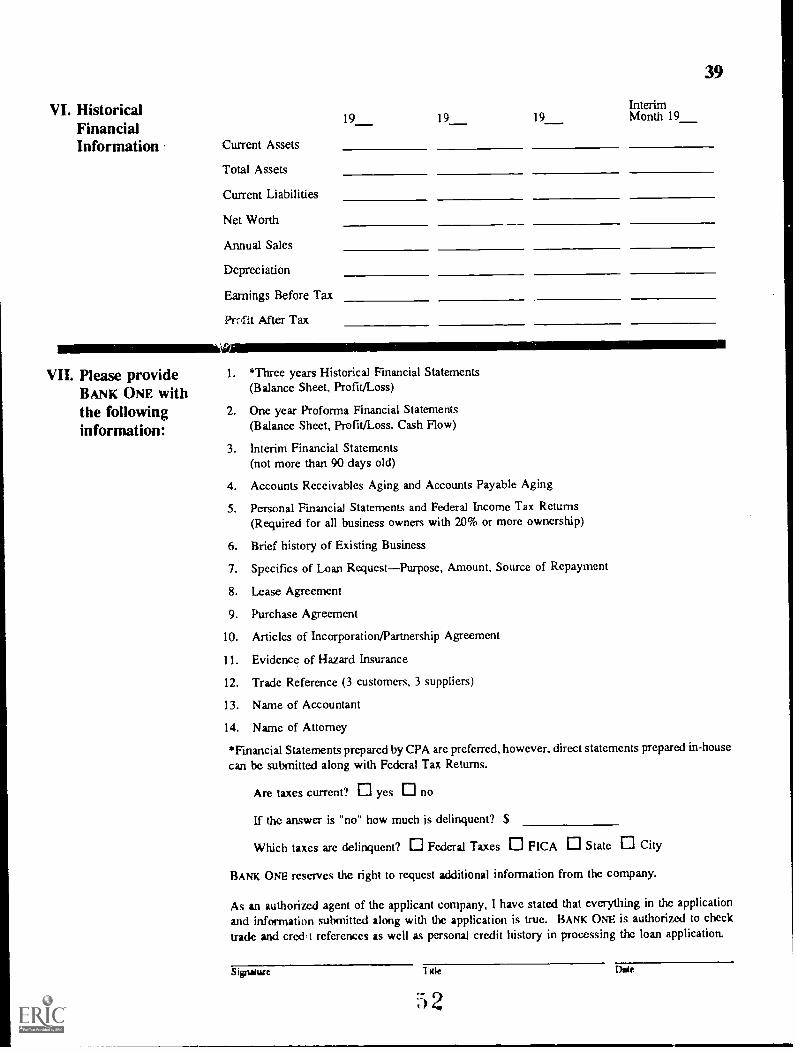

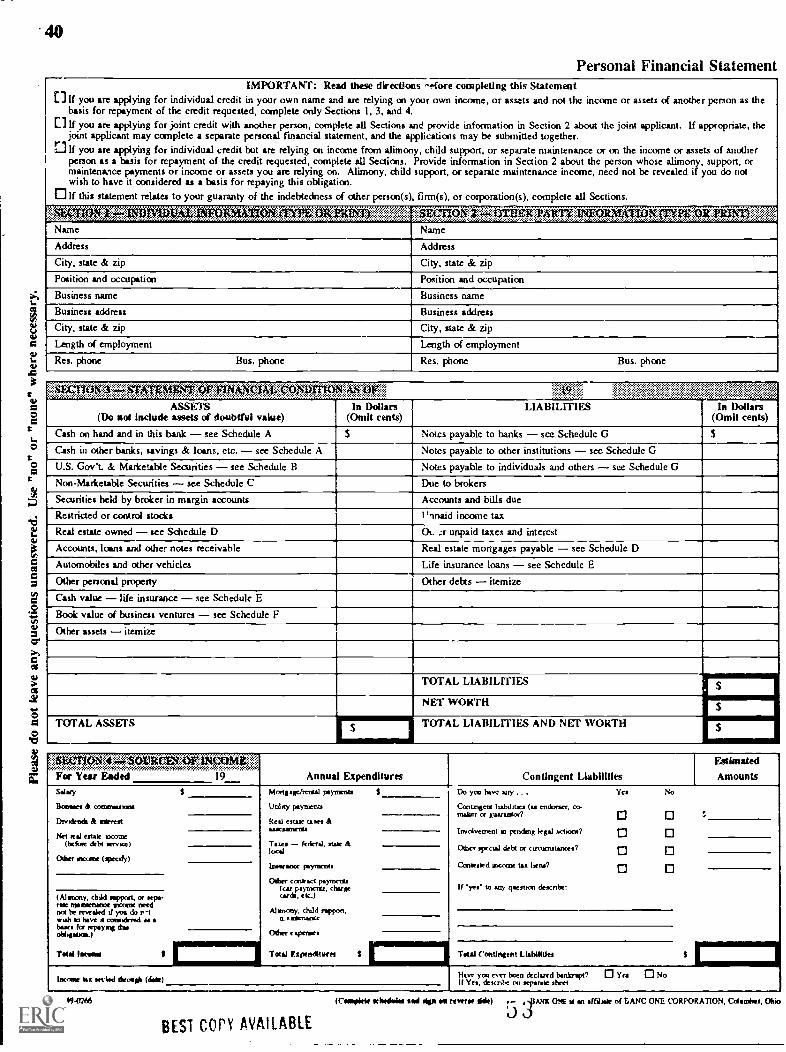

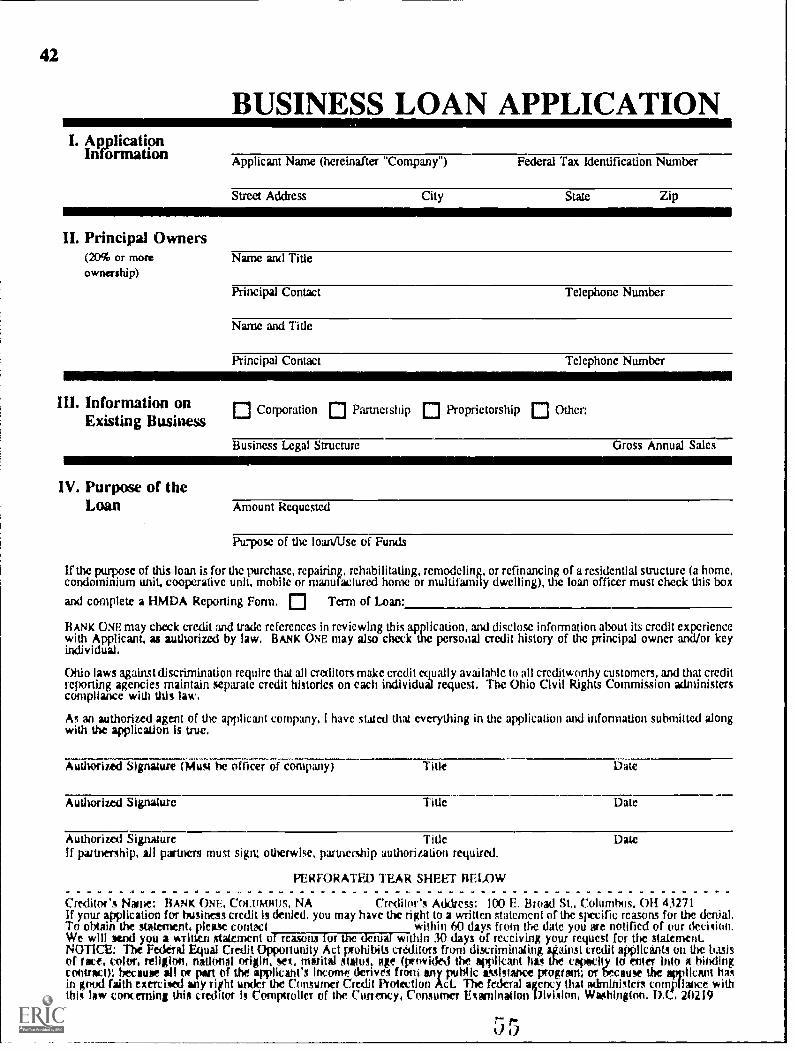

BUSINESS LOAN KIT

BANK ONE*

*All Bank One materials are used with permission.

10

29

30

Dear Applicant:

THANK YOU FOR CONSIDERING BANK ONE for your business financialneeds. We put together this business loan kit to help you get started indeveloping your company's overall business strategy.

SECTION I of the Business Loan Kit is the business plan. For the start-upbusiness, we have prepared a series of questions that will assist you indeveloping clear and precise business objectives. The answers to thesequestions will help you to complete the next stepthe actual business planand projections. If you have already established a business plan, you maywant to review this section to ensure that your present plan has addressed allpertinent areas.

SECTION II of the Business Loan Kit is the actual loan application. Thisshould be completed once you have developed your business plan. You willfind that much of this information is needed to complete the loan applicationform. Please be sure to complete the entire application before submitting itto your Business Banking Group Officer. In addition, we have enclosed aglossary of terms that may be helpful to you when completing the businessplan and application.

We thank you again for considering BANK ONE, and we look forward tohearing from you soon.

Sincerely,

Business Banking Group Officers

Section I THE BUSINESS PLAN

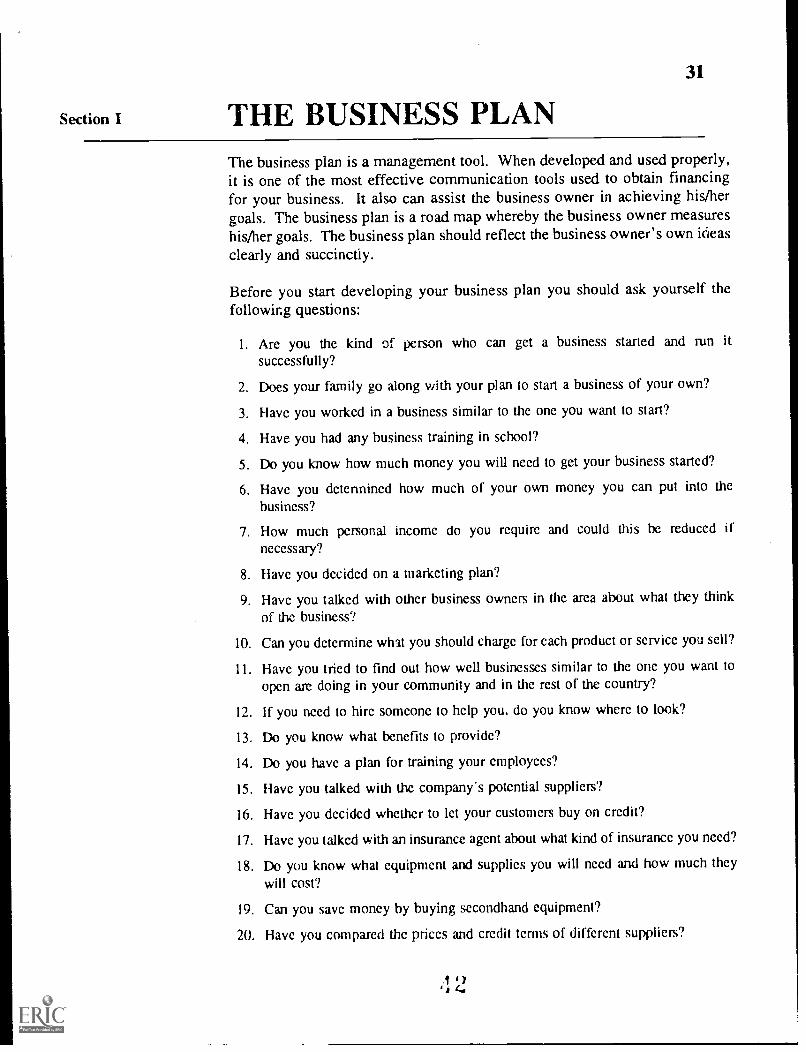

31

The business plan is a management tool. When developed and used properly,it is one of the most effective communication tools used to obtain financingfor your business. It also can assist the business owner in achieving his/hergoals. The business plan is a road map whereby the business owner measureshis/her goals. The business plan should reflect the business owner's own ideasclearly and succinctly.

Before you start developing your business plan you should ask yourself thefollowing questions:

1. Are you the kind of person who can get a business started and run it

successfully?

2. Does your family go along with your plan to start a business of your own?

3. Have you worked in a business similar to the one you want to start?

4. Have you had any business training in school?

5. Do you know how much money you will need to get your business started?

6. Have you determined how much of your own money you can put into thebusiness?

7. How much personal income do you require and could this be reduced ifnecessary?

8. Have you decided on a marketing plan?

9. Have you talked with other business owners in the area about what they thinkof the business?

10. Can you determine what you should charge for each product or service you sell?

11. Have you tried to find out how well businesses similar to the one you want toopen are doing in your community and in the rest of the country?

12. If you need to hire someone to help you. do you know where to look?

13. Do you know what benefits to provide?

14. Do you have a plan for training your employees?

15. Have you talked with the company's potential suppliers?

16. Have you decided whether to let your customers buy on credit?

17. Have you talked with an insurance agent about what kind of insurance you need?

18. Do you know what equipment and supplies you will need and how much theywill cost?

19. Can you save money by buying secondhand equipment?

20. Have you compared the prices and credit terms of different suppliers?

32

Business Plan Outline The previous questions should help you in developing your business plan.Once you have formulated your answers, you should begin developing yourbusiness plan. The following is an outline to be used in developing yourbusiness plan.

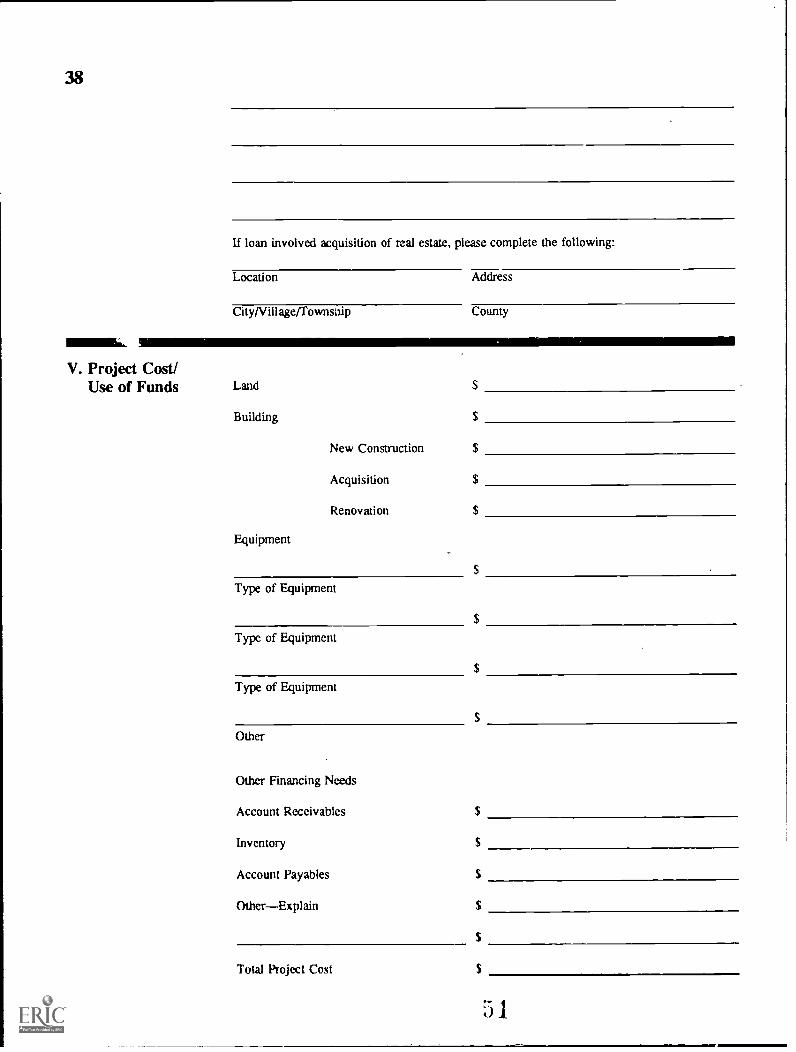

I. Cover LetterA. Dollar amount requestedB. Terms and timingC. Type and amount of collateralD. Purpose and source of repayment

II. SummaryA. Business description

1. Name2. Location and plant description3. Product4. Market and competition5. Management and business goals

B. Summary of financial needs and application of funds

HI. Products or ServicesA. Description of product lineB. Proprietary position: patents, copyrights, legal and technical considerationC. Product comparison

IV. Manufacturing Process (if applicable)A. MaterialsB. Source of supplyC. Production methods

V. Market AnalysisA. Description of total marketB. Industry trendsC. Target marketD. Competition

VI. Marketing StrategyA. Overall strategyB. Pricing policyC. Methods of selling, distributing, and servicing

VII. Management PlanA. Form of business organizationB. Board of Directors (Owner or Partners)C. Officers: organization chart and responsibilitiesD. Resumes of key personnelE. Staffing plan/number of employeesF. Facilities plan/planned capital improvementsG. Operating plan/schedule of work for next 1-2 years

VIII. Financial DataA. Financial statements (three years to present)B. Three-year financial projections (first year by months, remaining years annually)

I. Profit and loss statements2. Cash Flow charts3. Balance sheets

C. Explanation of projectionsD. Explanation of use and impact of new funds

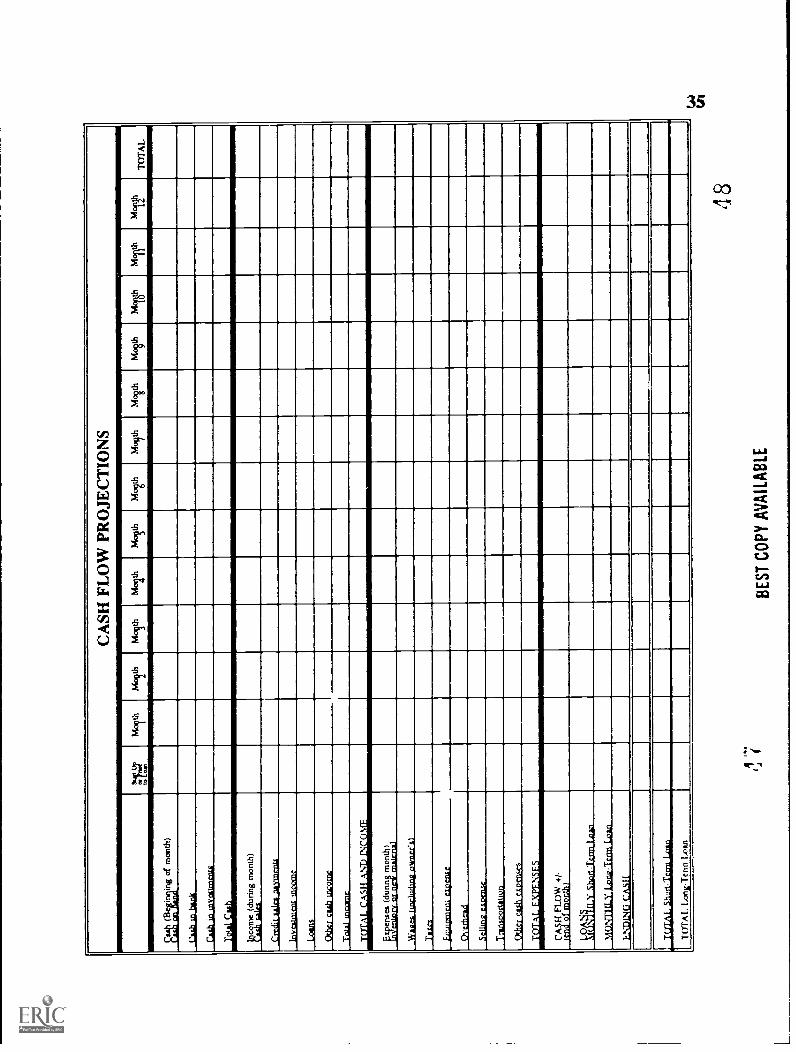

Projections

33

When preparing projected financial statements for your business plan you muststart with basic assumptions for income and expenses. These assumptions forincome and expenses should be detailed in your business plan with supportingdocumentation derived from the market study and the market strategy in thebusiness plan. The projected financial statements should indicate economicchanges in your business cycle. For instance, if your business is seasonal,sales during a specific period will be greater than another period. Yourfinancial projects should indicate the fluctuation in sales and expenses.

There are three types of financial statements:

Profit/Loss Statement

The profit/loss statement will take your income minus expenses andequal either a profit or a loss.

For the first year the projected profit/loss statement should be doneon a monthly basis. Thereafter, the second and third year may bedone on a quarterly basis.

Cash Flow Statement

The projected cash flow statements will show the cash generated andcollected from the business operations. This statement will utilize thesame income and expense as the profit/loss statement, however, ittakes last month/quarter previous cash and adds that into total cash/receipts for the new month/quarter. Timing differences resulting fromaccounts receivable turnover and the ongoing need for cash to fundexpenses will indicate your business need for working capital.

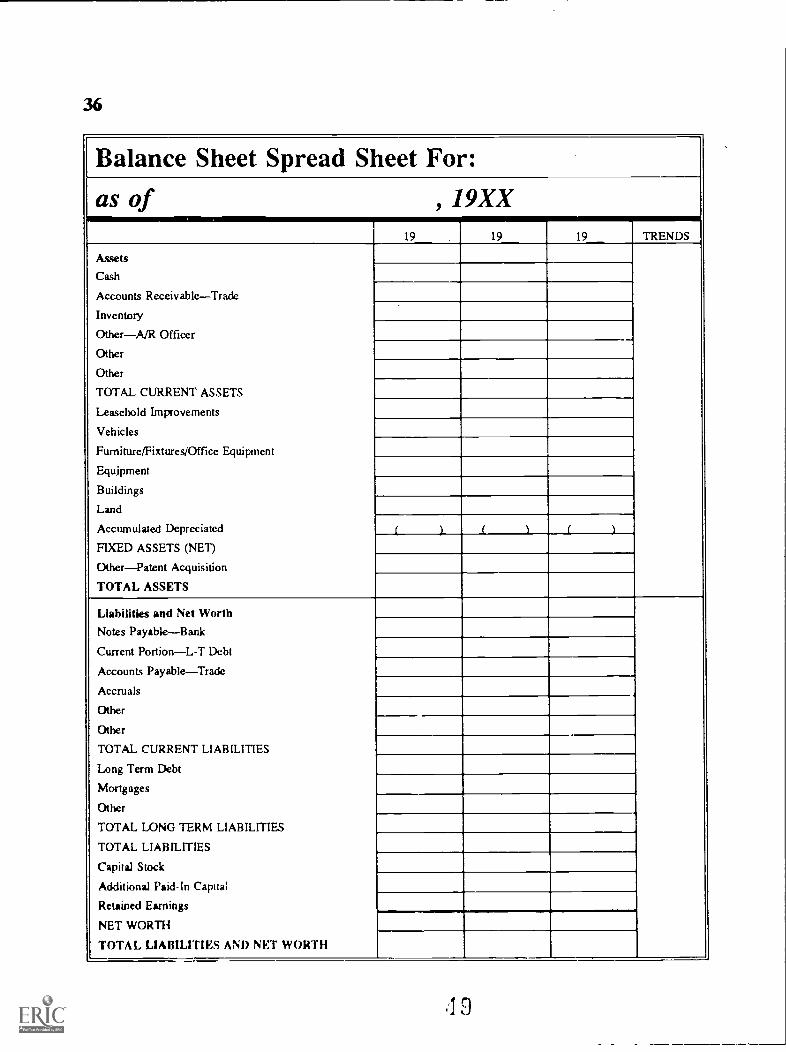

Balance Sheet

The balance sheet records the total assets, liabilities, and equity of abusiness on a specific day.

The projected balance sheet is done every twelve months. If yourcompany's business year end is December 31, then your proformabalance sheet reflects the assets, liabilities, and equity on that date.The projected balance sheet should reconcile with the projected profit/loss and cash flow statements.

Included in this kit are forms to be used in the financial forecastingof your business. A rule of thumb when forecasting; "be asconservative and as realistic as possible." Remember, your businessplan should provide you with all the supporting documentation whenforecasting,

45

PRO

JEC

TE

D P

RO

FIT

AN

D L

OSS

ST

AT

EM

EN

T

Mon

th1

Mon

th 2M

onth

3M

onth

4M

onth

5M

onth 6

Mon

th7

Mon

th8

Mon

th9

Mon

th10

Mon

th11

Mon

th12

TO

TA

L

Tot

al N

et S

ales

Cos

t of

Sale

s

GR

OSS

PR

OFI

T.

Con

trol

labl

e E

xpen

ses

Sala

ries

Pa r

oll T

axes

Secu

nty

Adv

ertis

ing

Aut

omob

ile

Due

s an

d Su

bscr

iptio

ns

Leg

al a

nd A

ccou

ntin

g

Off

ice

Suie

s

Tel

epho

ne

Util

ities

Mis

crtla

neou

s

Tot

al C

ontr

olla

ble

Es

nses

Fixe

d E

xpen

ses

De

ciat

icn

Insu

ranc

e

Ren

t.

Tax

es a

nd L

icen

ses

Inte

rest

on lo

ans

_int

ents

Tot

al F

ixed