14

A comparison between Islamic finance and conventional finance forms for SMEs in Egypt: the case study (Abu Dhabi Islamic Bank and Banque Misr) By/ Reham Mostafa Mohammed

A comparison between Islamic finance and

conventional finance forms for SMEs in

Egypt: the case study (Abu Dhabi Islamic

Bank and Banque Misr)

By/ Reham Mostafa Mohammed

•1) Definition of SMEs.

•2) Importance of SMEs.

•3) Obstacles faced by SMEs.

•4) Comparison between Abu Dhabi and Banque Misr

•-Briefly talk about establishment of Abu Dhabi and Banque Misr & forms of finance.

•- Customer Deposits

•- Total Assets.

Introduction

•The whole world has become interested in SMEs particularly developing countries. And this is because of their social and economic benefits. SMEs create job opportunities for youth under the age of thirty-five, increase GDP and decrease the unemployment rate. Egypt's GDP annual growth has reached 2.30 % (2016) and the

unemployment rate has reached 12.6 % (2016).

In upper Egypt, the unemployment rate has reached 23.2% (2016).

According to World Bank studies Formal SMEs contribute up to 45 percent of total employment and up to 33 percent of national income (GDP) in emerging economies. These numbers are significantly higher when informal SMEs are included. According to estimates, 600 million jobs will be needed in the next 15 years to absorb the growing global workforce, mainly in Asia and Sub-Saharan Africa. In emerging markets, most formal jobs are with SMEs, which also create 4 out of 5 new positions.

•However, access to finance is a key constraint to SME growth; without it, many SMEs languish and stagnate. There are many problems faced by SMEs such as lack of administrative experience, lack of marketing

knowledge and high taxes but financing is still the main problem.

•Thus, Islamic banks were established to contribute to close the gap of SMEs financing according to Sharia.

•The difference between Islamic banks and conventional banks is that Islamic banks do not seek to generate profits without taking into consideration social benefits also Islamic banks do not apply interests.

Definition of SMEs

•According to European Union

•But according to Egypt

Turnover Employees Company category

10 million € ≥ < 50 Small

50 million € ≥ < 250 Medium

Employees Company category

< 10 Small

<50 Medium

Importance of SMEs

•1) Create jobs, Providing foreign exchange, either by

• - The production of export opportunities for commodities.

• - The production of alternative goods imports

•2) Attract savings and channel them towards investment and production and thus increase income.

•3) Constitute a solid ground for the national economy in the face of negative effects. And setbacks such as inflation and recession, due to the limited vulnerability to economic fluctuations

Obstacles faced by SMEs

•1) Lack of Financial Resources.

•2)Lack of Administrative Experience.

•3) The absence of programs to upgrade the quality of the production of these projects.

•4) Low technological level.

•5) The high cost of production prices of raw materials in some countries for other countries thus losing much on foreign competition.

Abu Dhabi Islamic Bank and Banque Misr

•Banque Misr founded in 1920, the economic ideology of national Mohammed Talaat Harb Pasha, which is the first Egyptian bank owned 100% of the Egyptians. the establishment of many companies in various economic areas and those areas textile, insurance, transportation..

Abu Dhabi Islamic Bank is the Emirati Bank was established on 13 Muharram 1418 AH, corresponding to May 20, 1997 AD as a public company, and that was at the Emiri No. 9 for the year 1997 decree issued by His Highness Sheikh Khalifa bin Zayed Al Nahyan. The bank has begun to provide a range of banking products and services with high-level, as services funding and services of various bank accounts

Forms of Islamic finance in Abu Dhabi Islamic bank

•Murabaha is an Islamic financing structure in which an

intermediary buys a property with the free and clear title

•Murabaha is not an interest-bearing loan, which is considered riba (or excess) and is an acceptable form of credit sale under Sharia (Islamic religious law). Similar in structure to a rent-to-own arrangement, the intermediary retains ownership of the property until the loan is paid in full.

•Mudaraba is a partnership where capital is provided, in cash or assets by one party - the fund provider - and labor is provided by the other party – mudarib

•A loan is a form of conventional finance in Banque Misr but Murabaha and Mudaraba are the forms of finance in Abu Dhabi Islamic Bank and this is the main difference between Banque Misr and Abu Dhabi Islamic Bank

Banque Misr programs for SMEs

•For small enterprises

•Newly established companies

• Be a paid-up capital of LE 50 thousand to 5 million pounds of industrial facilities and to 3 million pounds of non-industrial

•B) existing companies

• The Bank finances small businesses in order to all the individual enterprises and companies of people and companies money in all industrial, commercial and service activities, which are sales of 10 million pounds, and even less than 20 million pounds, according to the needs of each client and interest rates (5%) (a simple return decreasing), according to the initiative of the bank Egyptian Central

Financing medium-sized enterprises

•Newly established companies • Be a paid-up capital of more than 5 million pounds to 10 million pounds of

industrial facilities and more than 3 million pounds to 5 million pounds of

non-industrial

•Existing companies

•The Bank finances medium-sized companies and to all the individual enterprises and companies of people and companies money in all industrial, commercial and service activities, which are sales of 20 million pounds, and even less than 100 million pounds, according to the needs of each client

• Bank provides financing for medium and long-term to medium businesses regular operating in the fields of industry and agriculture, according to the initiative in the Central Bank of Egypt and a yield of lending (7%) to finance machinery or equipment or new production lines for a maximum of 10 years and a maximum of 20 million pounds, provided they do not benefit from this initiative The last bank

Customer deposits (Abu Dhabi Islamic bank and banque Misr)

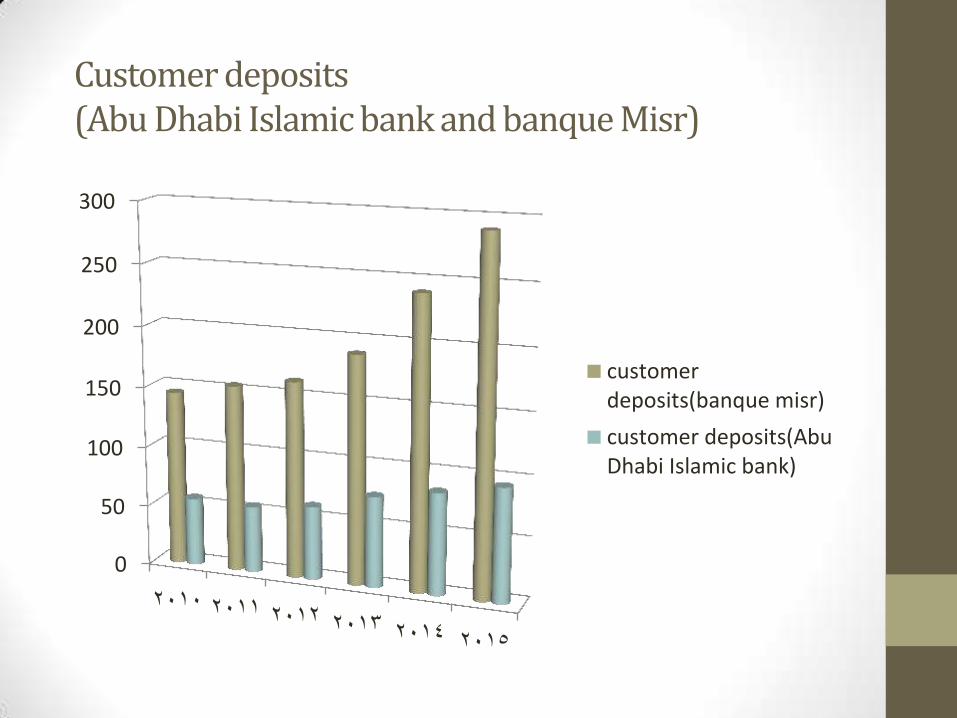

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015

customerdeposits(banque misr)

customer deposits(AbuDhabi Islamic bank)

Total assets

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015

total assets(banqueMisr)

total assets(Abu DhabiIslamic bank)