42

CyRCE: JavierM árquez Diez-Canedo. M arch 2002 A CreditRisk defaultm odelthat m easures concentration,single obligorlim its and bank capital adequacy.

CyRCE:

Javier M árquez Diez-Canedo.M arch 2002

A Credit Risk default m odel thatm easures concentration, singleobligor lim its and bank capitaladequacy.

I. I. IntroductionIntroduction

II.II. CyRCE m odelCyRCE m odel

III.III. System ic Credit Risk analysisSystem ic Credit Risk analysis

Index

Introduction

One of the m ain concerns of regulators is having a proper

assessm ent of the solvency of the Financial System .

It is im portant to have an adequate picture of the level of risk of the

Financial System as a whole, where risk is concentrated, and the

individual banks’ contribution to overall risk.

This represents a technically form idable problem for several

reasons:

Inform ation

Credit risk m ethodologies:

No accepted paradigm

Num erical techniques w ith heavy com putational requirem ents

How to draw the picture?

Existing Credit Risk M ethodologies

Big inform ation requirem ents.

Substantial com putational effort to obtain loss distribution.

No explicit relation betw een credit risk and

• Capital adequacy

• Concentration

• Single obligor lim its

I. I. IntroductionIntroduction

II.II. CyRCE m odelCyRCE m odel

III.III. System ic Credit Risk analysisSystem ic Credit Risk analysis

Index

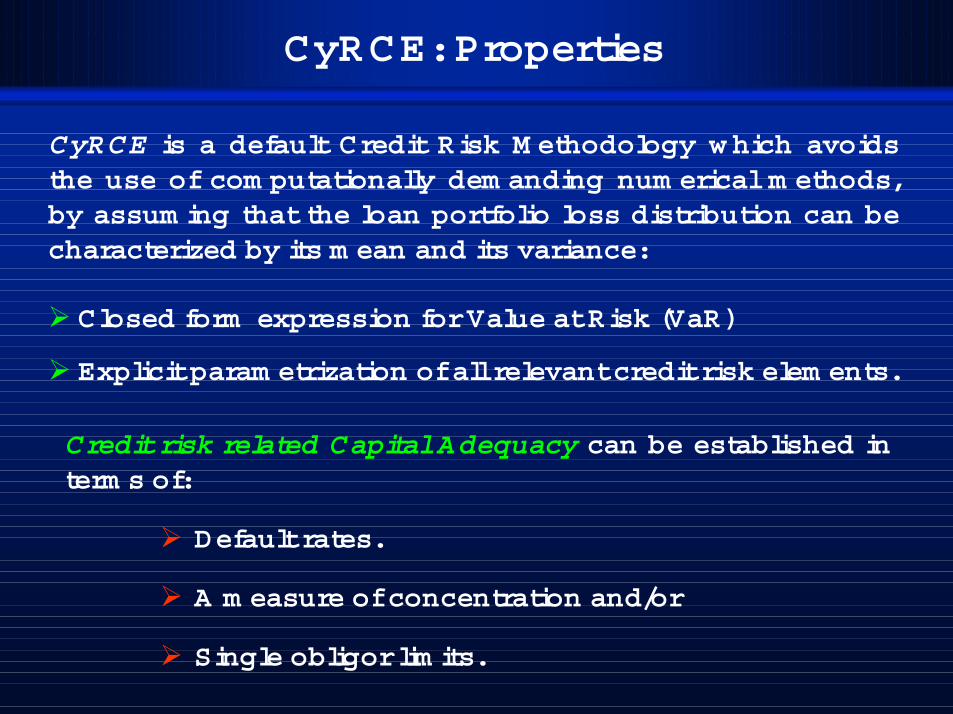

CyRCE: Properties

CyRCE is a default Credit Risk M ethodology which avoidsthe use of com putationally dem anding num erical m ethods,by assum ing that the loan portfolio loss distribution can becharacterized by its m ean and its variance:

Closed form expression for Value at Risk (VaR)

Explicit param etrization of all relevant credit risk elem ents.

Credit risk related Capital Adequacy can be established interm s of:

Default rates.

A m easure of concentration and/or

Single obligor lim its.

The m odel is “built up” from a verysim ple case where all loans havei.i.d default probabilities, andextended to a general situationwhere default probabilities of loanscan differ, be correlated and theportfolio can be segm entedarbitrarily to detect riskyconcentration segm ents.

CyRCE: Capital Adequacy and Credit Risk

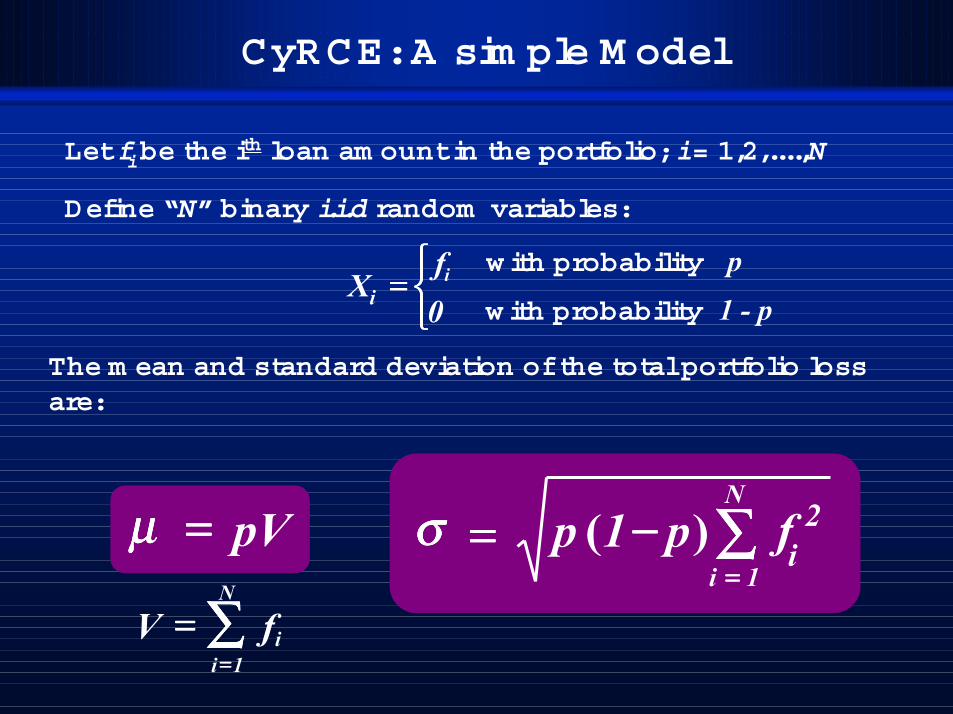

Let fi be the ith loan am ount in the portfolio; i = 1,2,....,N

Define “N” binary i.i.d random variables:

CyRCE: A sim ple M odel

Xi

====0fi

w ith probability 1 - p w ith probability p

The m ean and standard deviation of the total portfolio lossare:

pV====µµµµ

∑∑∑∑====

====N

1iifV

==== ∑∑∑∑====

N

1i

2if−−−− p1p )(σσσσ

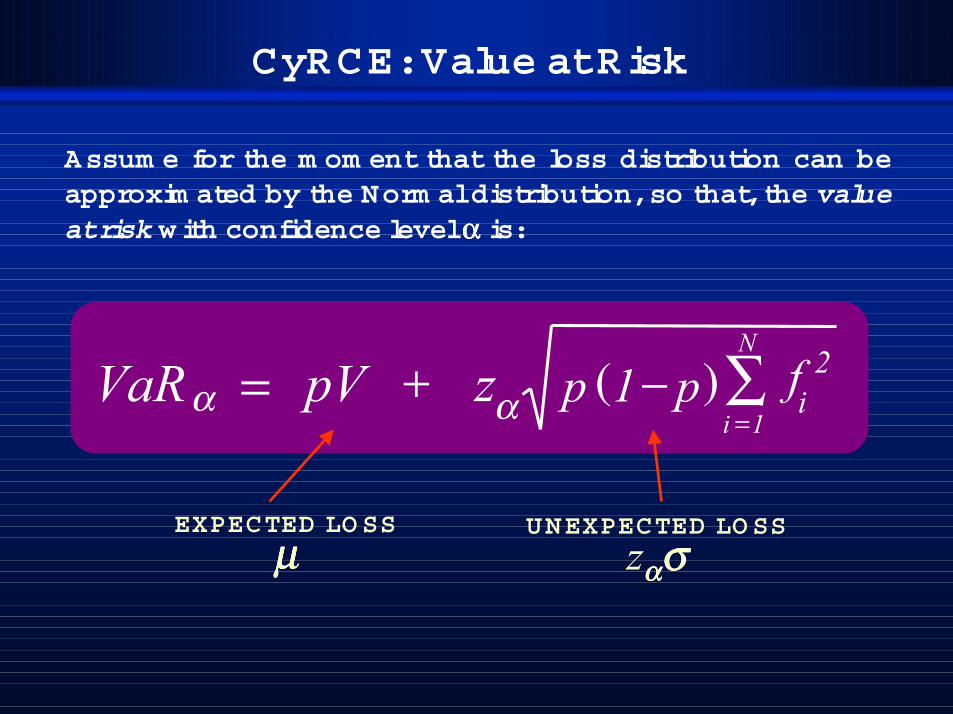

CyRCE: Value at Risk

Assum e for the m om ent that the loss distribution can beapproxim ated by the Norm al distribution, so that, the valueat risk with confidence level αααα is:

+=VaRα zα ∑=

N

1i

2if− p1p )(pV

EXPECTED LOSS

µµµµUNEXPECTED LOSS

zαααασσσσ

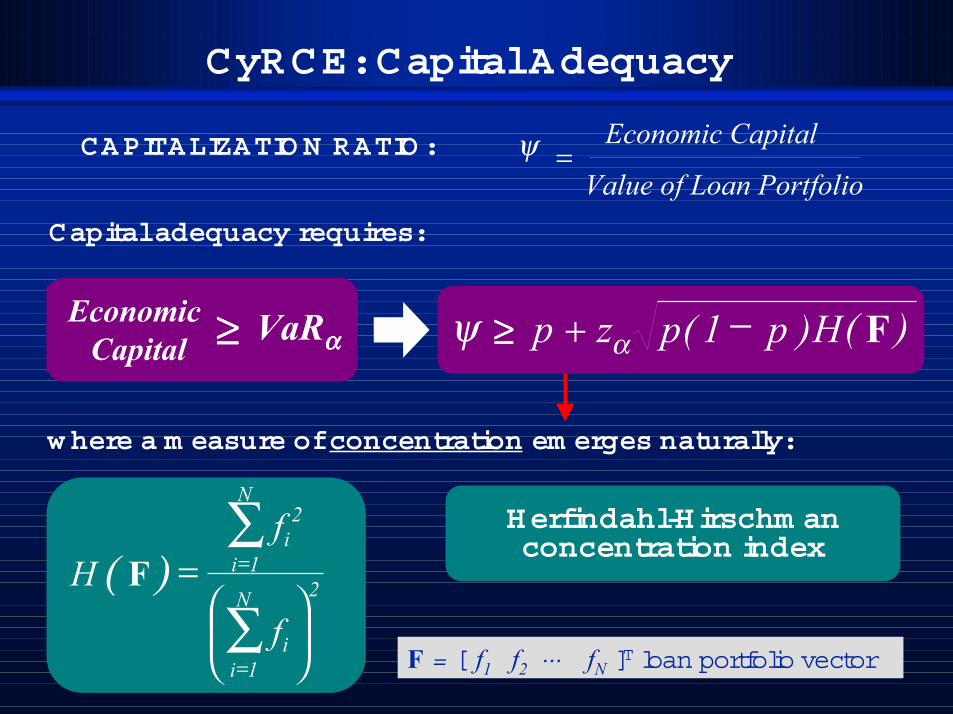

CyRCE: Capital Adequacy

CAPITALIZATIO N RATIO :

Value of Loan Portfolio

Economic Capital=ψ

VaRααααEconomic Capital ≥≥≥≥

Capital adequacy requires:

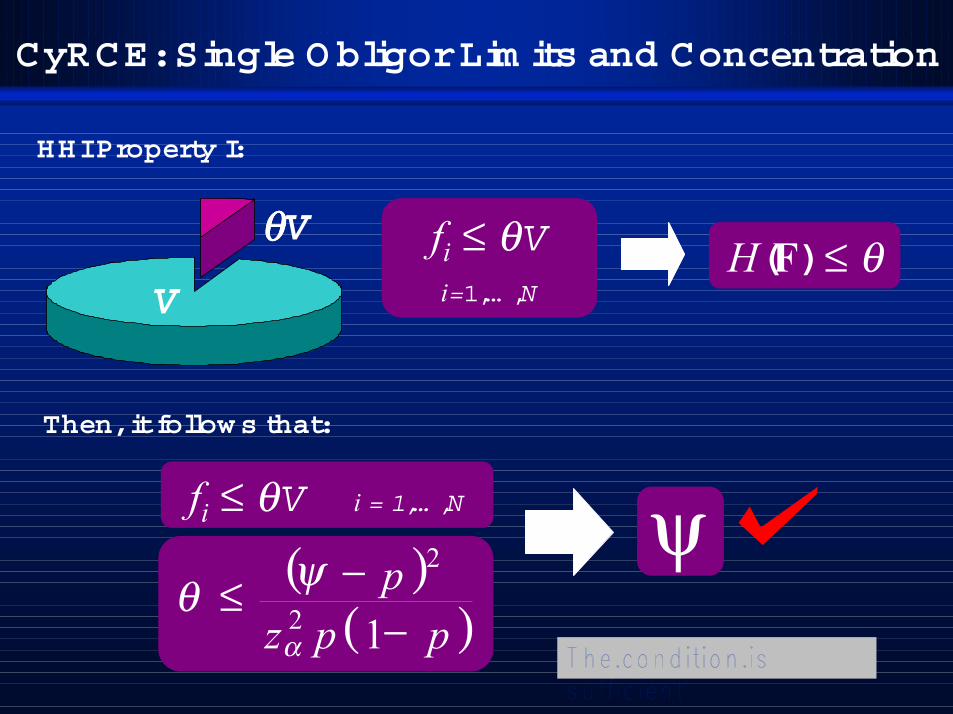

FH)p1(pzp −+≥≥≥≥ αψ ( )

( ) 2N

1ii

N

1i

2i

f

fH

=

∑

∑

=

= FHerfindahl-Hirschm anconcentration index

F = [ f1 f2 ⋅⋅⋅ fN ]T loan portfolio vector

w here a m easure of concentration em erges naturally:

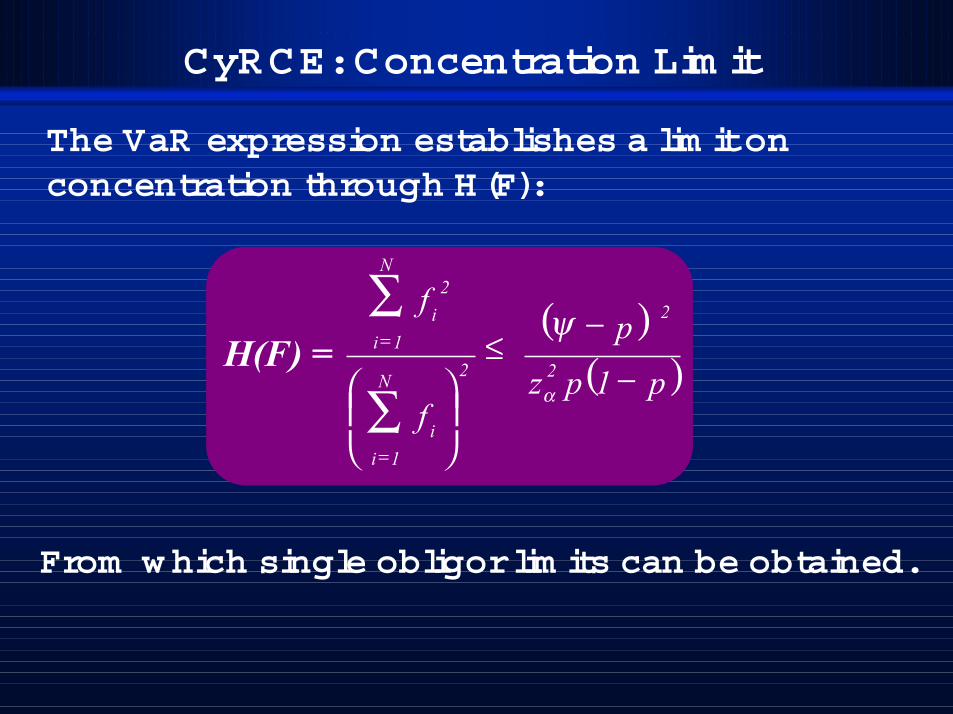

CyRCE: Concentration Lim it

The VaR expression establishes a lim it onconcentration through H(F):

( )( )p1pz

p

f

f

2

2

2N

1ii

N

1i

2i

−

−≤

∑

∑

=

=

α

ψH(F) =

From which single obligor lim its can be obtained.

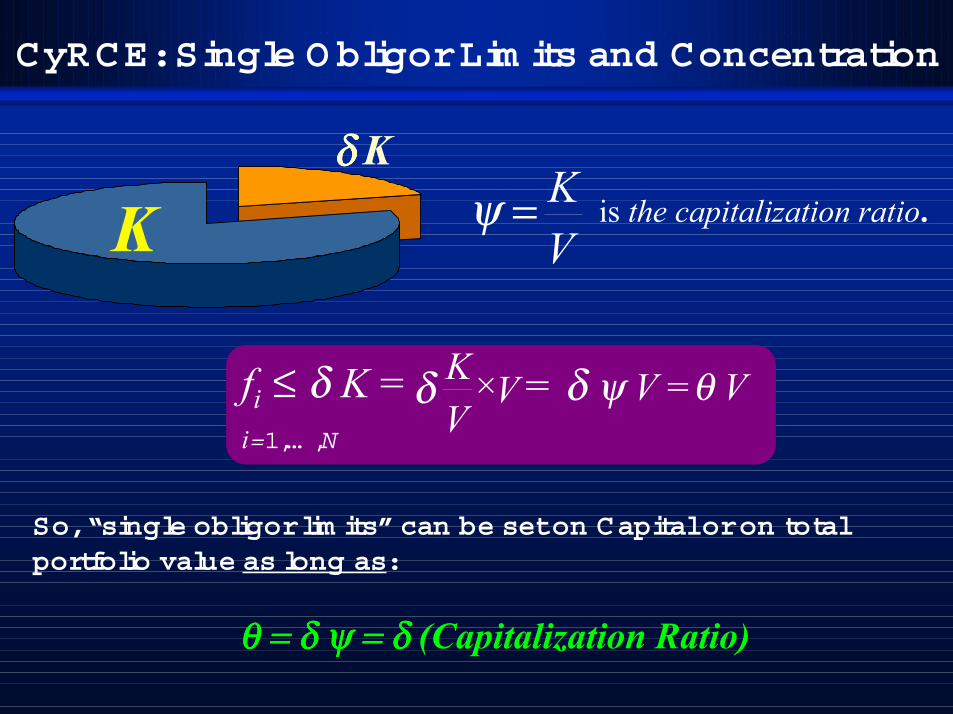

CyRCE: Single Obligor Lim its and Concentration

Kδδδδ

K

θ = δ ψ = δ θ = δ ψ = δ θ = δ ψ = δ θ = δ ψ = δ (Capitalization Ratio)

is the capitalization ratio.VK=ψ

fi ≤ δ K =i=1,… ,N

VVKδ × = δ ψ V =θ V

So, “single obligor lim its” can be set on Capital or on totalportfolio value as long as:

CyRCE: Single Obligor Lim its and Concentration

ψ

H(F) ≤ θ

Then, it follows that:

V

Vθθθθ fi ≤ θVi=1,… ,N

( )( )ppz

p−

−≤ 12

2

α

ψθ

fi ≤ θV i = 1,… ,N

HHI Property I:

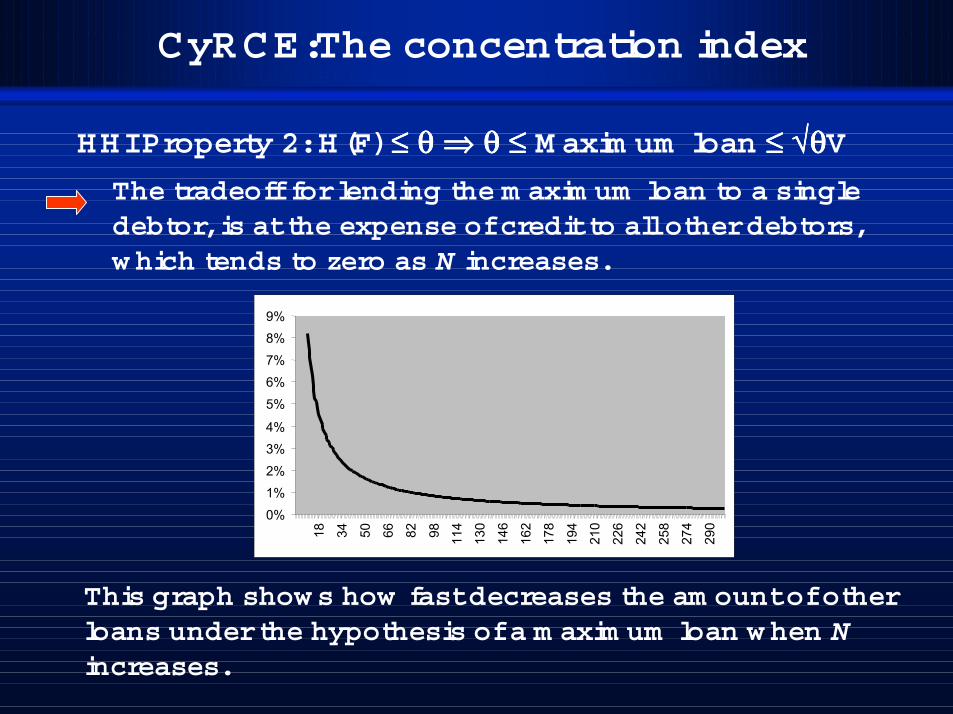

The tradeoff for lending the m axim um loan to a singledebtor, is at the expense of credit to all other debtors,w hich tends to zero as N increases.

1%

3%

5%

7%

9%18 34 50 66 82 98 11

4

130

146

162

178

194

210

226

242

258

274

290

0%

2%

4%

6%

8%

This graph shows how fast decreases the am ount of otherloans under the hypothesis of a m axim um loan w hen Nincreases.

CyRCE:The concentration index

HHI Property 2: H(F) ≤≤≤≤ θθθθ ⇒⇒⇒⇒ θθθθ ≤≤≤≤ M axim um loan ≤≤≤≤ √θ√θ√θ√θV

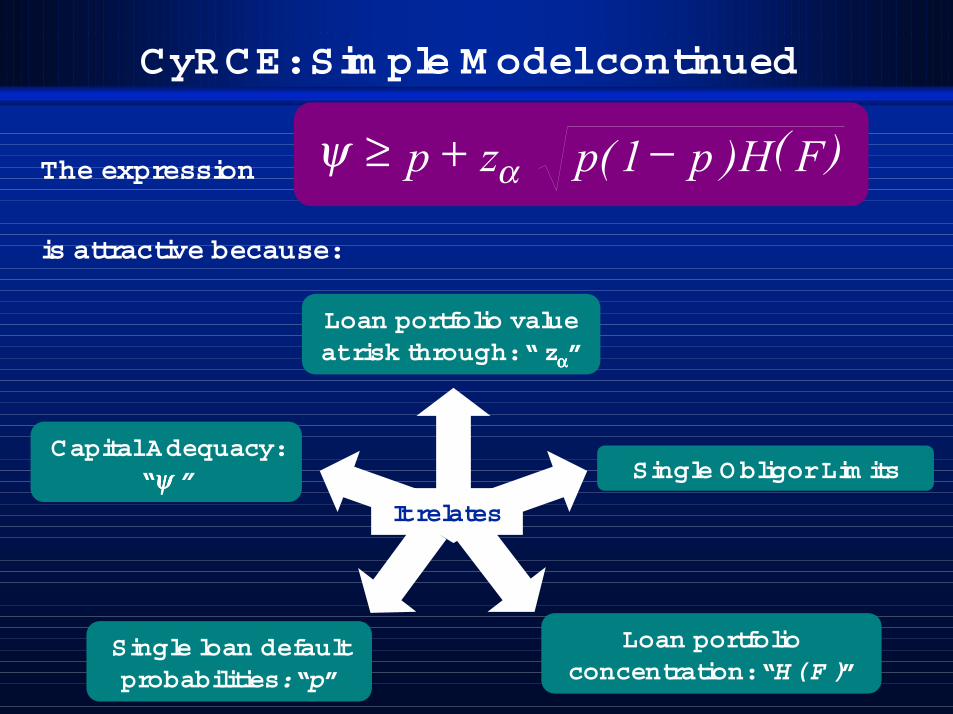

CyRCE: Sim ple M odel continued

Loan portfolio valueat risk through: “ zαααα”

Loan portfolioconcentration: “H( F )”

Capital Adequacy:“ψψψψ ”

Single loan defaultprobabilities: “p”

FH)p1(pzp −+≥ αψ ( )

is attractive because:

Single Obligor Lim its

It relates

The expression

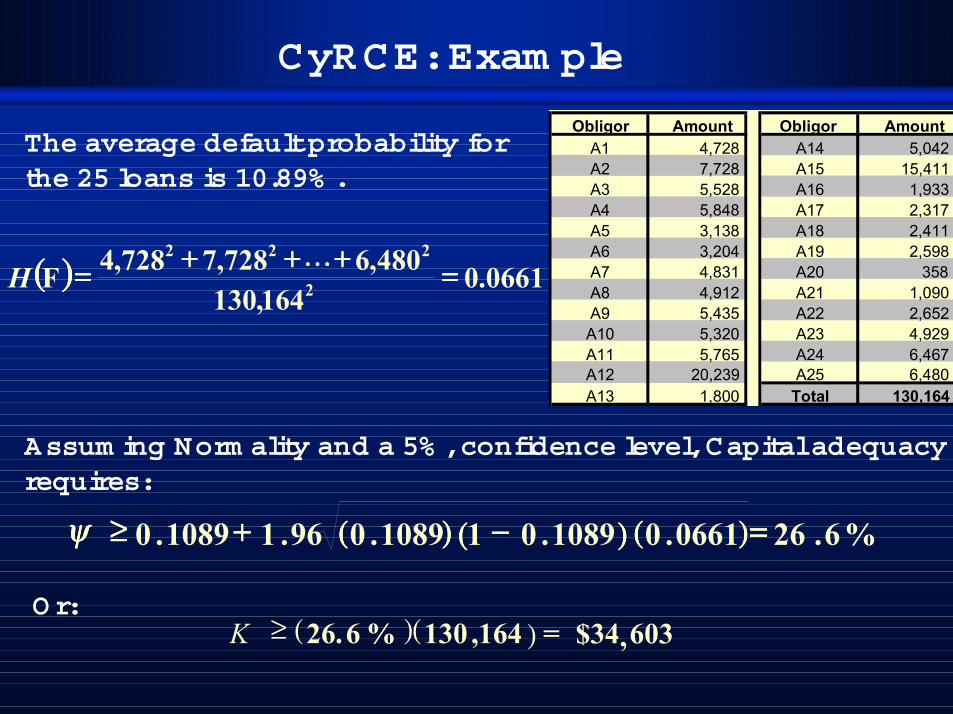

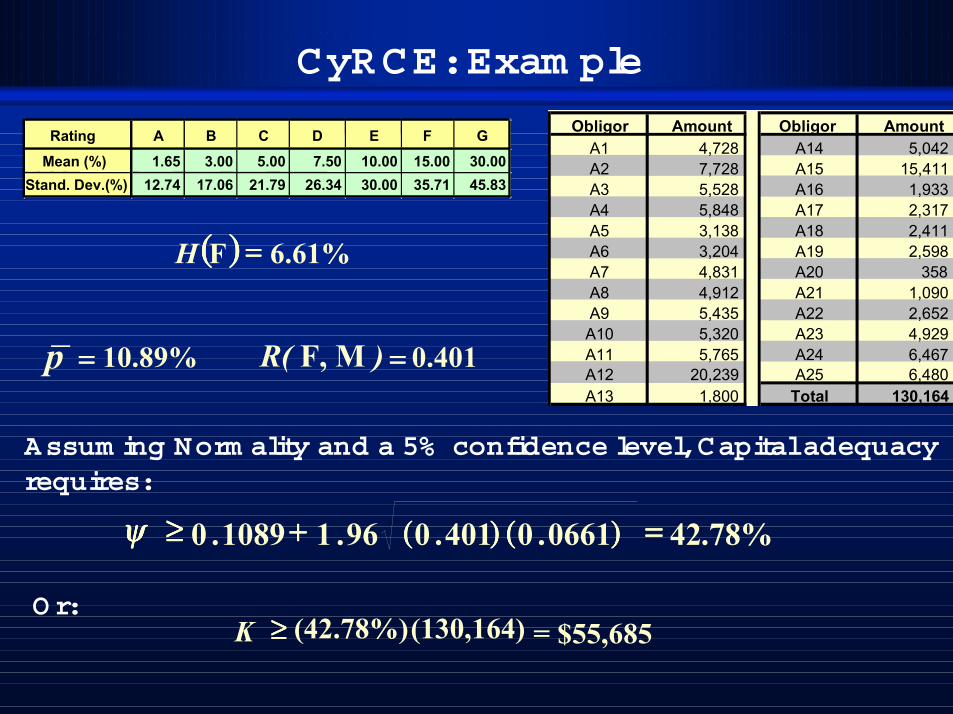

Obligor Amount Obligor AmountA1 4,728 A14 5,042 A2 7,728 A15 15,411 A3 5,528 A16 1,933 A4 5,848 A17 2,317 A5 3,138 A18 2,411 A6 3,204 A19 2,598 A7 4,831 A20 358 A8 4,912 A21 1,090 A9 5,435 A22 2,652 A10 5,320 A23 4,929 A11 5,765 A24 6,467 A12 20,239 A25 6,480 A13 1,800 Total 130,164

CyRCE: Exam ple

The average default probability forthe 25 loans is 10.89% .

(((( )))) 0661.0164,130

480,6728,7728,42

222====++++++++++++==== LLLLFH

,( , )164130( )%6.26 603$34=≥K

Assum ing Norm ality and a 5% , confidence level, Capital adequacyrequires:

O r:

. %62696.11089.0 ====)))).(((( 06610.(((( ))))10890 (((( ))))1089.01 −−−−++++≥≥≥≥ψψψψ

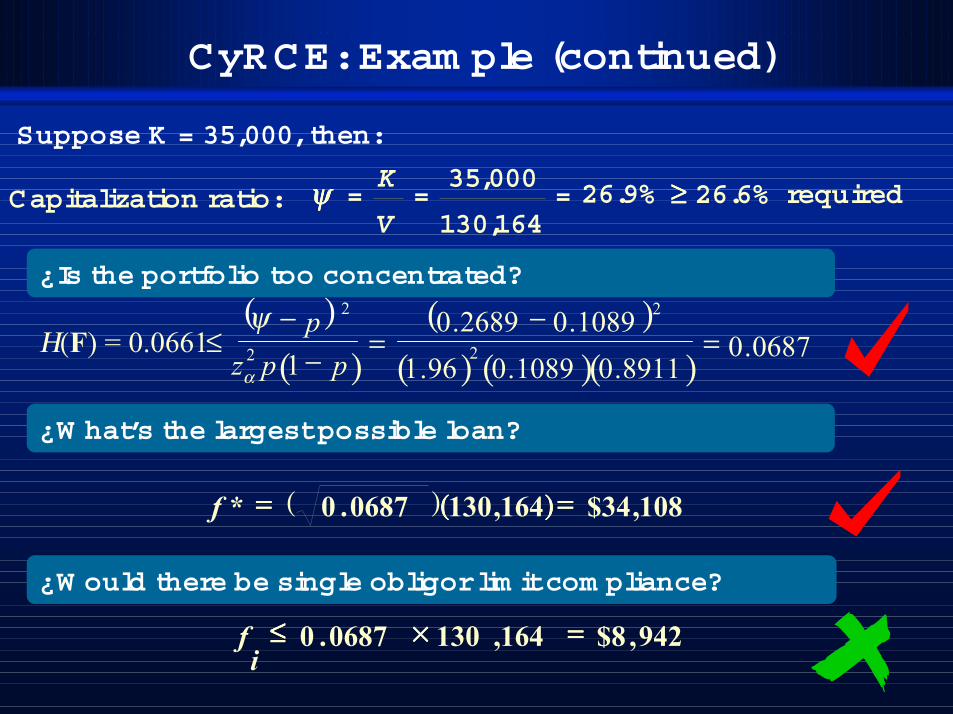

CyRCE: Exam ple (continued)

Capitalization ratio:

Suppose K = 35,000, then:

26.9%164,130

000,35===

V

Kψψψψ ≥≥≥≥ 26.6% required

¿Is the portfolio too concentrated?

¿W hat’s the largest possible loan?

(((( ))))164,130( )0687.0* 108 ,$34========f

¿W ould there be single obligor lim it com pliance?

( )( ( ) ( )( ) 0687.0

1089.02689.0 2

=−

=≤2− pψ( )) 0. 8911.1089096.1

21 − pp2zα

Η(F) = 0.0661

942 ,$8164,1300687.0 ====××××≤≤≤≤i

f

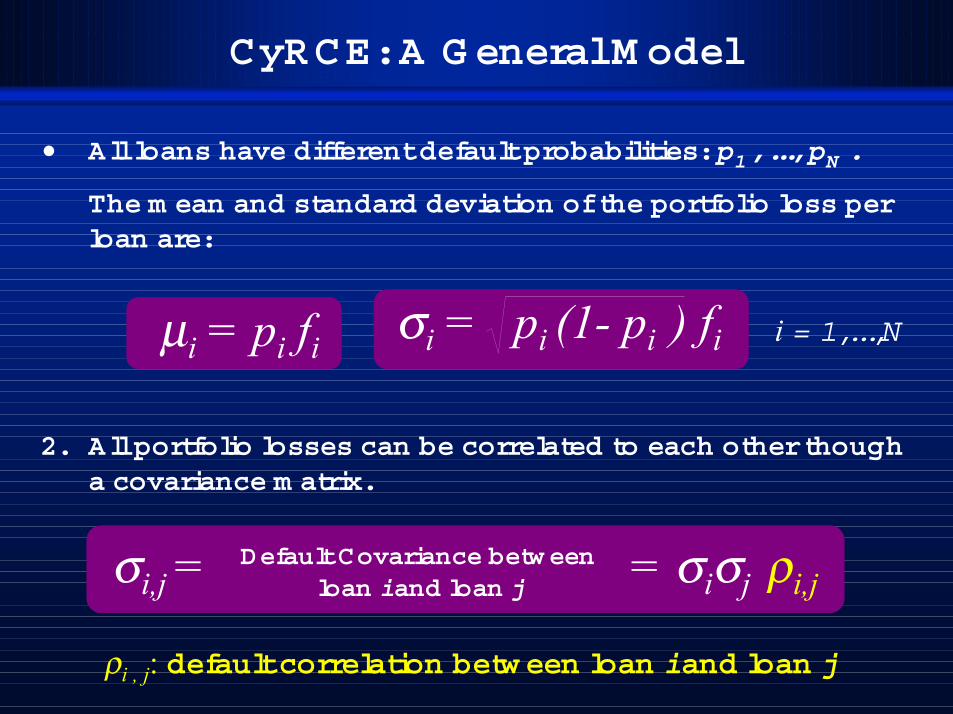

CyRCE: A General M odel

• All loans have different default probabilities: p1 , ..., pN .

The m ean and standard deviation of the portfolio loss perloan are:

2. All portfolio losses can be correlated to each other thougha covariance m atrix.

ρi , j: default correlation between loan i and loan j

= σiσj ρi,jDefault Covariance between

loan i and loan jσi,j =

µi = pi fi i = 1,...,Nσi = pi (1- pi ) fi

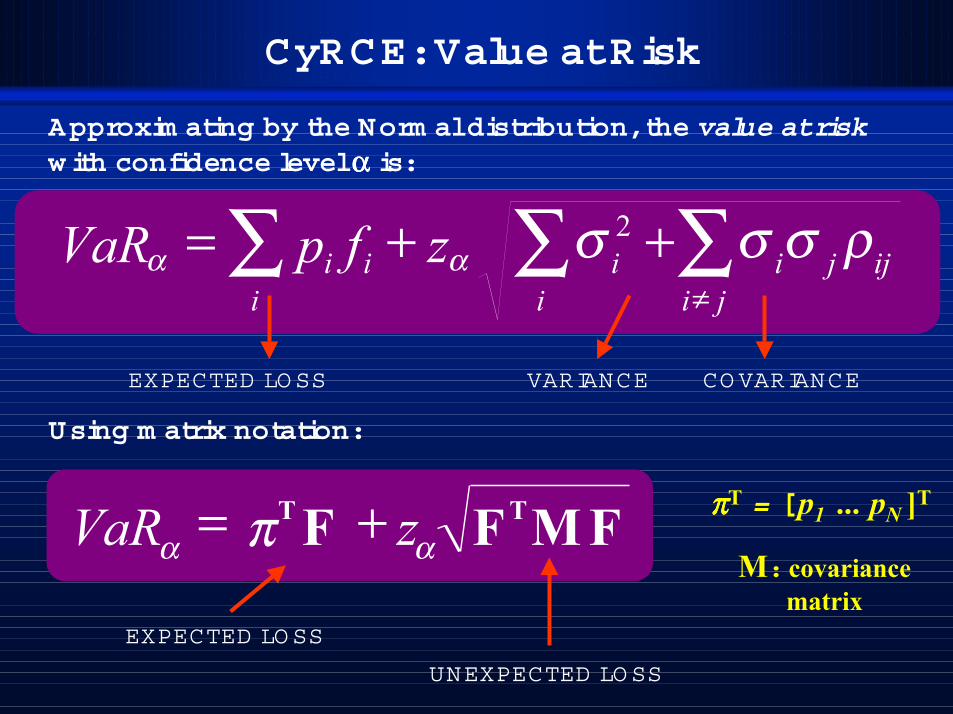

CyRCE: Value at Risk

∑∑∑≠

++=ji

ijjii

ii

ii zfpVaR ρσσσαα2

+= z FMFTαVaRα

T Fπ

EXPECTED LOSS

UNEXPECTED LO SS

Approxim ating by the Norm al distribution, the value at riskw ith confidence level αααα is:

Using m atrix notation:

M: covariancematrix

ππππT = [ p1 ... pN ]T

EXPECTED LOSS VARIANCE CO VARIANCE

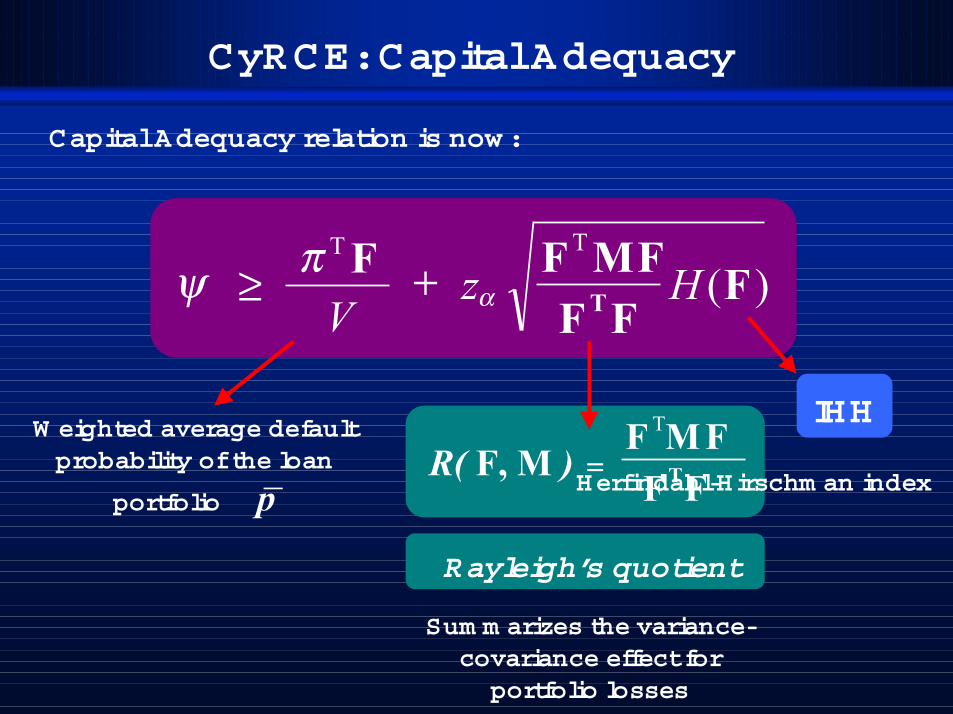

CyRCE: Capital Adequacy

Capital Adequacy relation is now :

T

T

FHFF

MFz )(αψ +≥T

VFπ F

Sum m arizes the variance-covariance effect forportfolio losses

R( F, M ) = T

T

FFMF F

Rayleigh’s quotient

IHHW eighted average defaultprobability of the loan

portfolio p_ Herfindahl-Hirschm an index

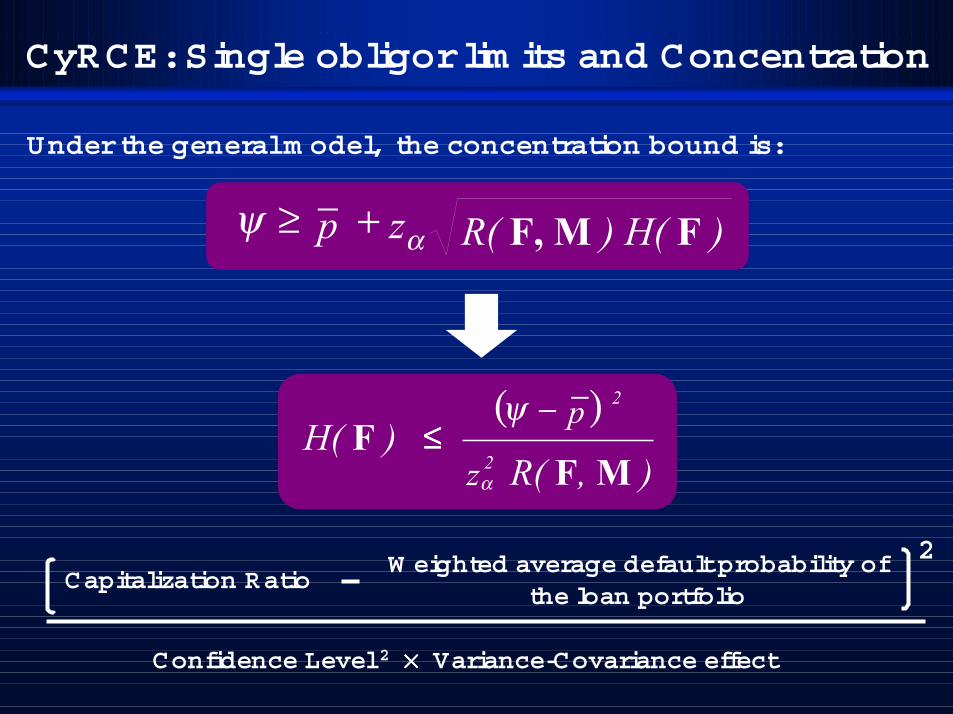

Under the general m odel, the concentration bound is:

CyRCE: Single obligor lim its and Concentration

R( F, M ) H( F )+≥ zαψ p_

R( F, M )≤≤≤≤

z 2α

H( F )p( ) 2−ψ −

Capitalization RatioW eighted average default probability of

the loan portfolio

2

Confidence Level 2 ×××× Variance-Covariance effect

CyRCE: Exam ple

Assum ing Norm ality and a 5% confidence level, Capital adequacyrequires:

O r:

Rating A B C D E F GMean (%) 1.65 3.00 5.00 7.50 10.00 15.00 30.00

Stand. Dev.(%) 12.74 17.06 21.79 26.34 30.00 35.71 45.83

(((( )))) 6.61%====FH

p_

==== 10.89% R( F, M ) 0.401====

)))).(((( 06610.(((( ))))401096.11089.0 . %7842====++++≥≥≥≥ψψψψ

(42.78%) $55,685=≥≥≥≥K (130,164)

Obligor Amount Obligor AmountA1 4,728 A14 5,042 A2 7,728 A15 15,411 A3 5,528 A16 1,933 A4 5,848 A17 2,317 A5 3,138 A18 2,411 A6 3,204 A19 2,598 A7 4,831 A20 358 A8 4,912 A21 1,090 A9 5,435 A22 2,652 A10 5,320 A23 4,929 A11 5,765 A24 6,467 A12 20,239 A25 6,480 A13 1,800 Total 130,164

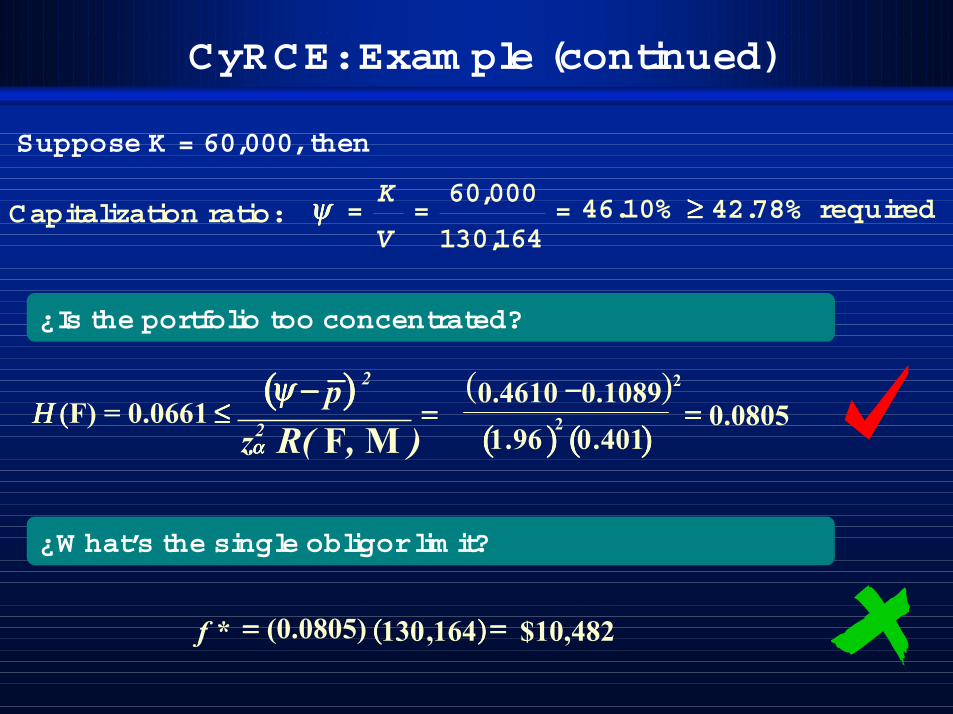

CyRCE: Exam ple (continued)

Suppose K = 60,000, then

Capitalization ratio: 46.10%164,130

000,60===

V

Kψψψψ ≥≥≥≥ 42.78% required

¿Is the portfolio too concentrated?

¿W hat’s the single obligor lim it?

0.0805====( 0.10890.4610 )2−−−−

====≤≤≤≤(((((((( )))))))) .401096.1 2Η Η Η Η ((((F) = 0.0661

R( F, M )z2αααα

p(((( )))) 2−−−−ψψψψ −−−−

(((( ))))164,130(0.0805) $10,482====* ==== f

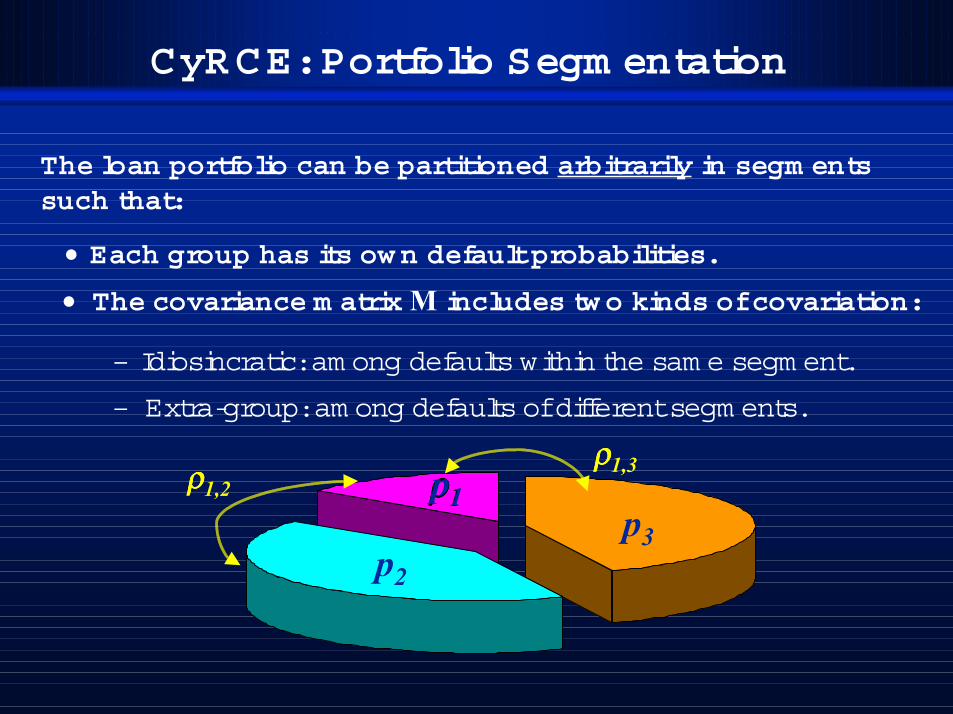

CyRCE: Portfolio Segm entation

The loan portfolio can be partitioned arbitrarily in segm entssuch that:

ρρρρ1,3ρρρρ1,2

– Extra-group: am ong defaults of different segm ents.

ρρρρ1

• The covariance m atrix M includes tw o kinds of covariation:

– Idiosincratic: am ong defaults within the sam e segm ent.

p1

p2

p3

• Each group has its ow n default probabilities.

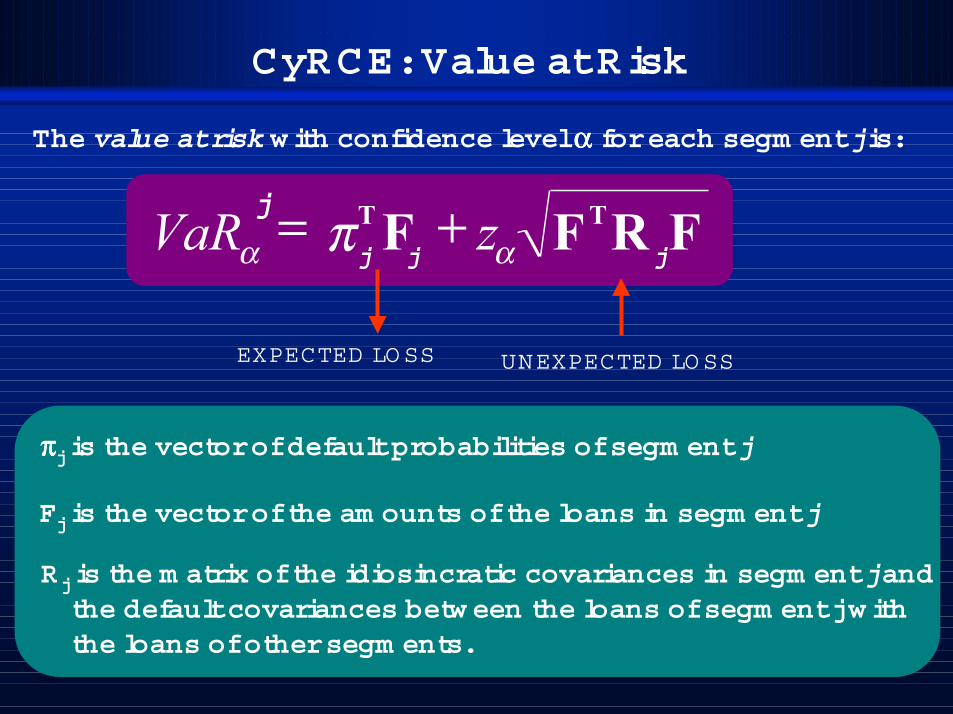

CyRCE: Value at Risk

The value at risk with confidence level αααα for each segm ent j is:

+= z FRFTαVaRα

T Fπj

j j j

ππππj is the vector of default probabilities of segm ent j

Rj is the m atrix of the idiosincratic covariances in segm ent j andthe default covariances betw een the loans of segm ent j w iththe loans of other segm ents.

Fj is the vector of the am ounts of the loans in segm ent j

EXPECTED LO SS UNEXPECTED LO SS

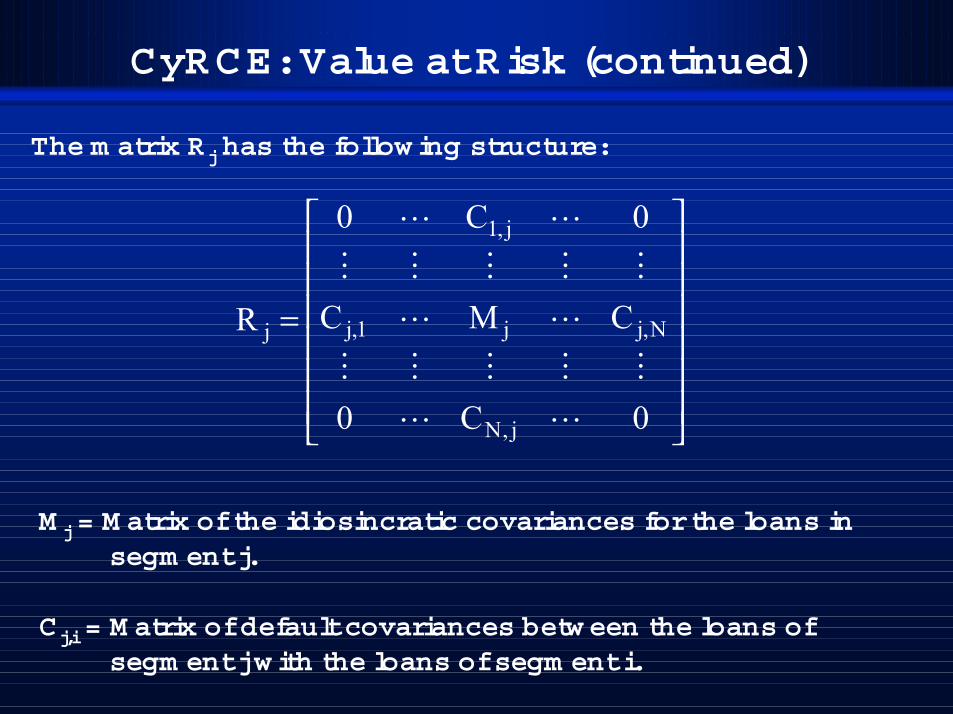

CyRCE: Value at Risk (continued)

=

0C0

CMC

0C0

R

j,N

N,jj1,j

j,1

j

LL

MMMMM

LL

MMMMM

LL

The m atrix Rj has the follow ing structure:

M j = M atrix of the idiosincratic covariances for the loans insegm ent j.

Cj,i = M atrix of default covariances betw een the loans ofsegm ent j w ith the loans of segm ent i.

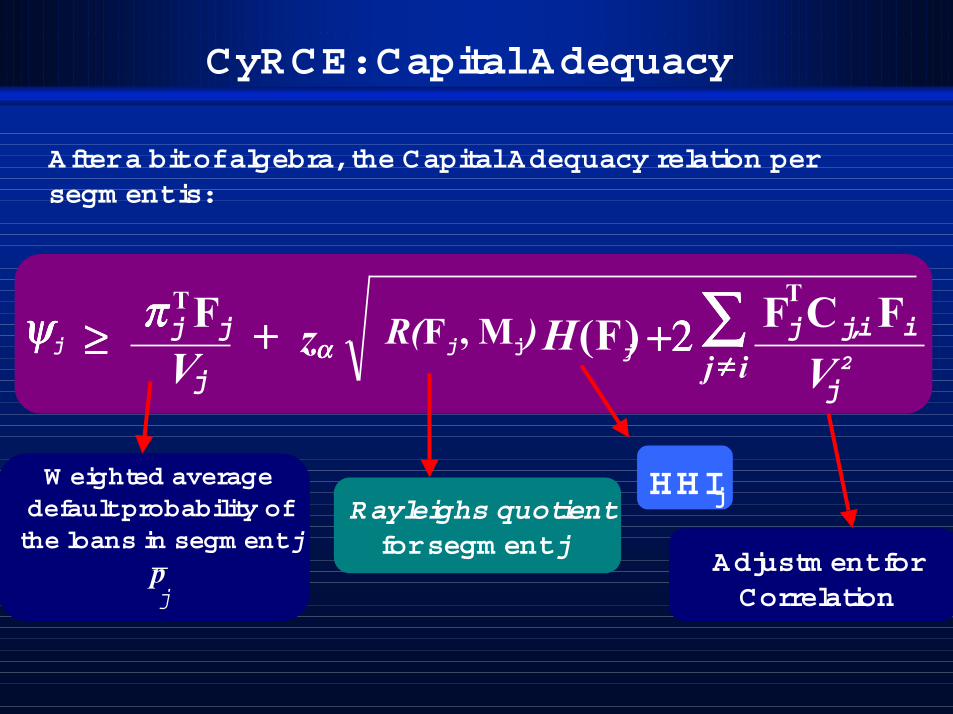

CyRCE: Capital Adequacy

After a bit of algebra, the Capital Adequacy relation persegm ent is:

z FjH )(ααααψψψψj ++++≥≥≥≥T

VFππππ R(Fj , Mj )j j

j

+2+2+2+2 ∑∑∑∑≠≠≠≠ ij

FjTCj,iFiVj2

W eighted averagedefault probability ofthe loans in segm ent j

p_

j

Rayleighs quotientfor segm ent j

HHIj

Adjustm ent forCorrelation

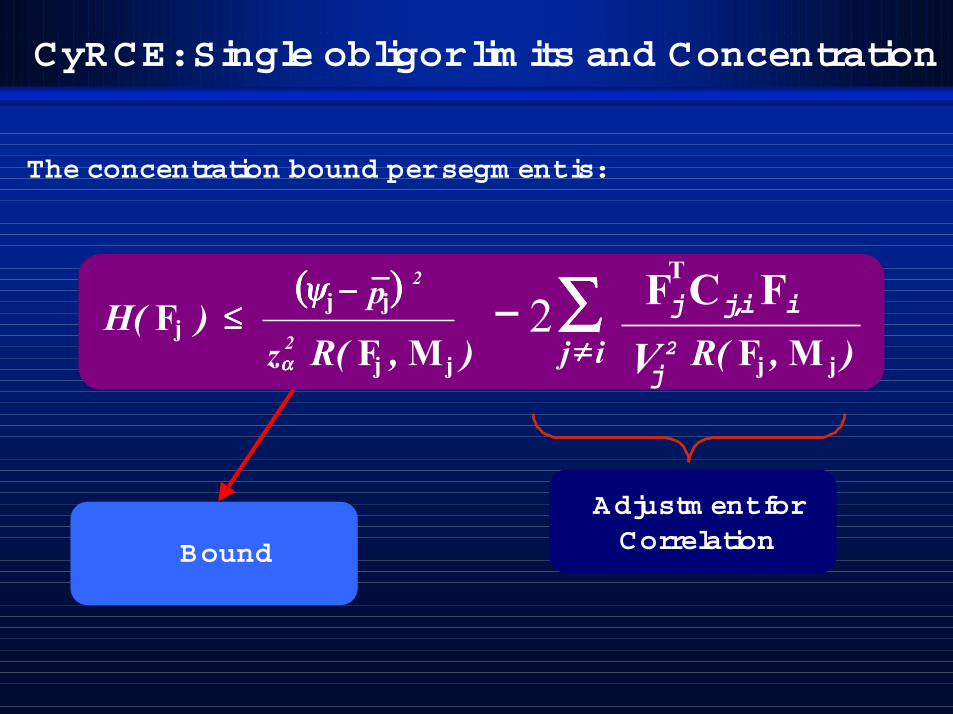

CyRCE: Single obligor lim its and Concentration

The concentration bound per segm ent is:

R( F , M )≤≤≤≤

z 2αααα

H( F )p(((( )))) 2−−−−ψψψψ −−−−

jj

j

j j

- 2∑∑∑∑≠≠≠≠ ij

FjTCj,iFi

Vj2 R( F , M )j j

Bound

Adjustm ent forCorrelation

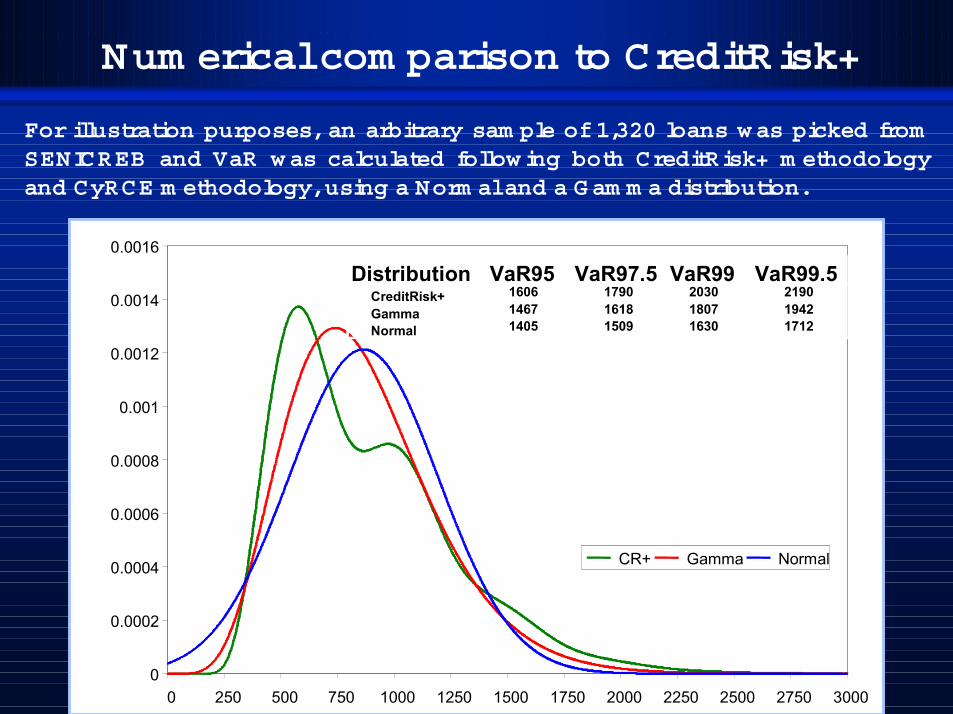

Num erical com parison to CreditRisk+

For illustration purposes, an arbitrary sam ple of 1,320 loans was picked fromSENICREB and VaR was calculated follow ing both CreditRisk+ m ethodologyand CyRCE m ethodology, using a Norm al and a Gam m a distribution.

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012

0.0014

0.0016

0 250 500 750 1000 1250 1500 1750 2000 2250 2500 2750 3000

CR+ Gamma Normal

Distribution VaR95 VaR97.5 VaR99 VaR99.5CreditRisk+ 1606 1790 2030 2190Gamma 1467 1618 1807 1942Normal 1405 1509 1630 1712

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012

0.0014

0.0016

0 250 500 750 1000 1250 1500 1750 2000 2250 2500 2750 3000

CR+ Gamma NormalCR+ Gamma Normal

Distribution VaR95 VaR97.5 VaR99 VaR99.5CreditRisk+ 1606 1790 2030 2190Gamma 1467 1618 1807 1942Normal 1405 1509 1630 1712

I. I. IntroductionIntroduction

II.II. CyRCE m odelCyRCE m odel

•• System ic Credit Risk analysisSystem ic Credit Risk analysis

III.IIII.I PositionPosition

III.II VaR analysisIII.II VaR analysis

Index

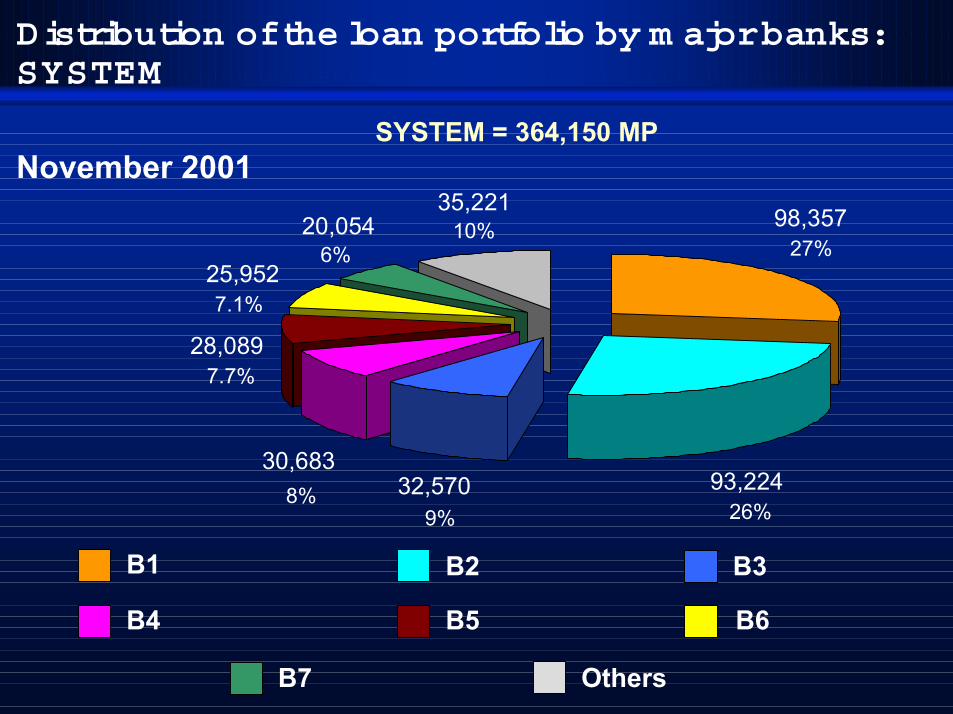

Distribution of the loan portfolio by m ajor banks:SYSTEM

November 2001

27%

26%9%8%

7.7%

7.1%

6%10% 98,357

93,22432,57030,683

28,089

25,952

20,05435,221

SYSTEM = 364,150 MP

B1 B2

B4

B3

B5 B6

B7 Others

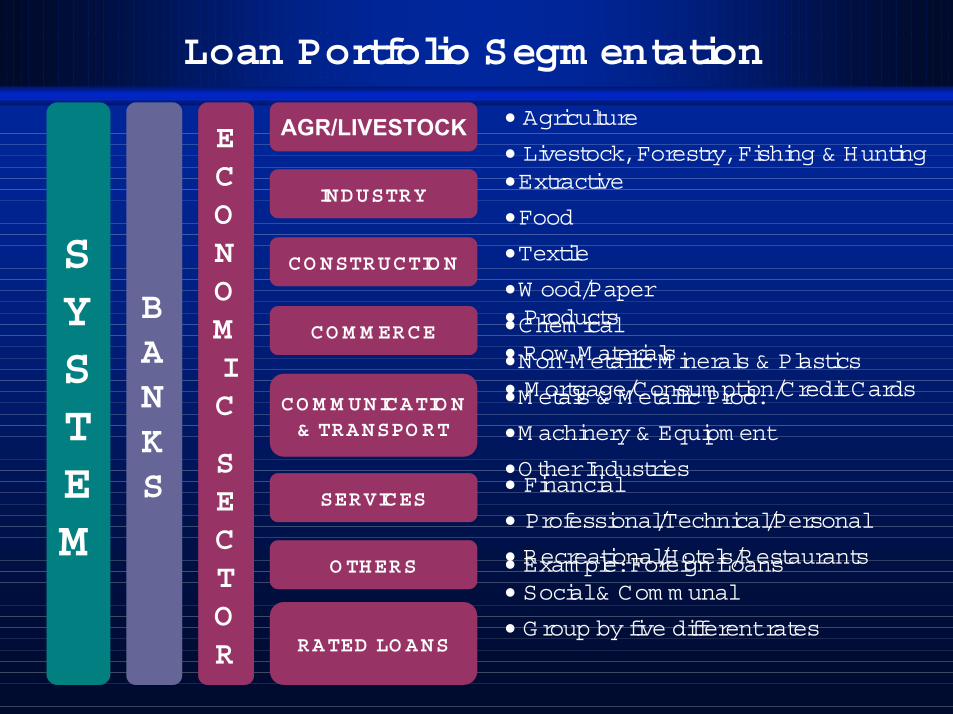

Loan Portfolio Segm entation

BANKS

CONSTRUCTIO N

INDUSTRY• Extractive

• Food

• Textile

• W ood/Paper

• Chem ical

• Non-M etallic M inerals & Plastics

• M etals & M etallic Prod.

• M achinery & Equipm ent

• Other Industries

CO M M ERCE• Products

• Row M aterials

• M ortgage/Consum ption/Credit Cards

SERVICES• Financial

• Professional/Technical/Personal

• Recreational/Hotels/Restaurants

• Social & Com m unal

AGR/LIVESTOCK • Agriculture

• Livestock, Forestry, Fishing & Hunting

CO M M UNICATIO N& TRANSPO RT

O THERS

RATED LO ANS

• Exam ple: Foreign Loans

• G roup by five different rates

SYSTEM

ECONOMIC

SECTOR

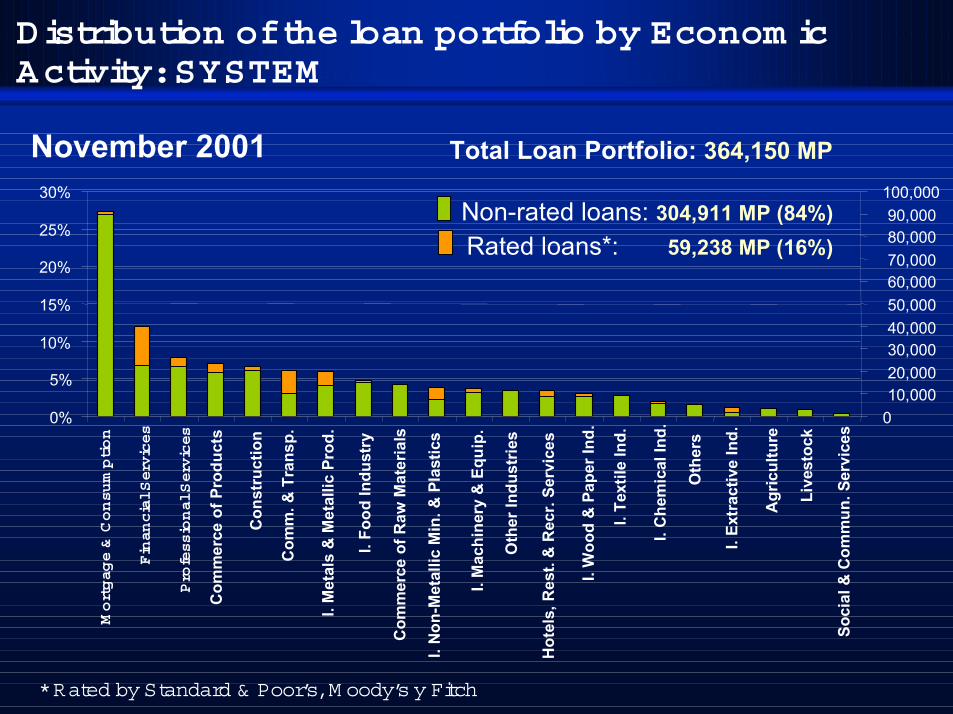

Distribution of the loan portfolio by Econom icActivity: SYSTEM

November 2001Mortgage & Consumption

Financial Services

Professional Services

Com

mer

ce o

f Pro

duct

s

Con

stru

ctio

n

Com

m. &

Tra

nsp.

I. M

etal

s &

Met

allic

Pro

d.

I. Fo

od In

dust

ry

Com

mer

ce o

f Raw

Mat

eria

ls

I. N

on-M

etal

lic M

in. &

Pla

stic

s

I. M

achi

nery

& E

quip

.

Oth

er In

dust

ries

Hot

els,

Res

t. &

Rec

r. Se

rvic

es

I. W

ood

& P

aper

Ind.

I. Te

xtile

Ind.

I. C

hem

ical

Ind.

I. Ex

trac

tive

Ind.

Agr

icul

ture

Live

stoc

k

Soci

al &

Com

mun

. Ser

vice

s

Oth

ers

Non-rated loans: 304,911 MP (84%) Rated loans*: 59,238 MP (16%)

* Rated by Standard & Poor’s, M oody’s y Fitch

0%

5%

10%

15%

20%

25%

30%

010,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000

Total Loan Portfolio: 364,150 MP

I. I. IntroductionIntroduction

II.II. CyRCE m odelCyRCE m odel

•• System ic Credit Risk analysisSystem ic Credit Risk analysis

III.IIII.I PositionPosition

III.II VaR analysisIII.II VaR analysis

Index

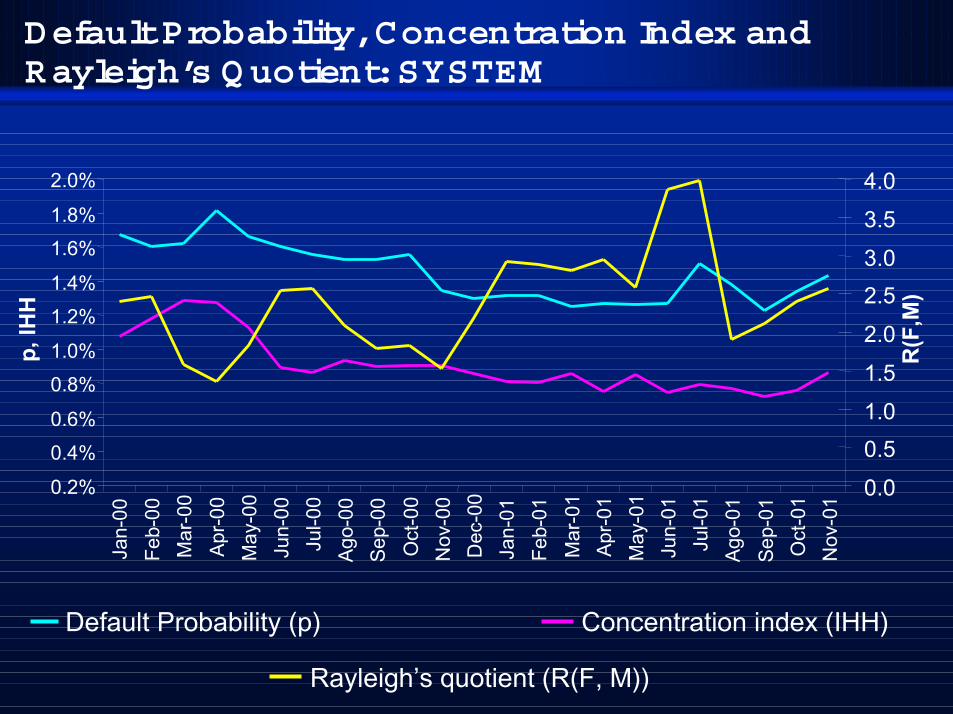

Default Probability, Concentration Index andRayleigh’s Q uotient: SYSTEM

0.2%

0.4%0.6%

0.8%1.0%

1.2%1.4%

1.6%1.8%

2.0%

Jan-

00Fe

b-00

Mar

-00

Apr-0

0M

ay-0

0Ju

n-00

Jul-0

0Ag

o-00

Sep-

00O

ct-0

0N

ov-0

0D

ec-0

0Ja

n-01

Feb-

01M

ar-0

1Ap

r-01

May

-01

Jun-

01Ju

l-01

Ago-

01Se

p-01

Oct

-01

Nov

-01

p, IH

H

0.0

0.51.01.5

2.0

2.53.0

3.54.0

R(F

,M)

Concentration index (IHH)Default Probability (p)

Rayleigh’s quotient (R(F, M))

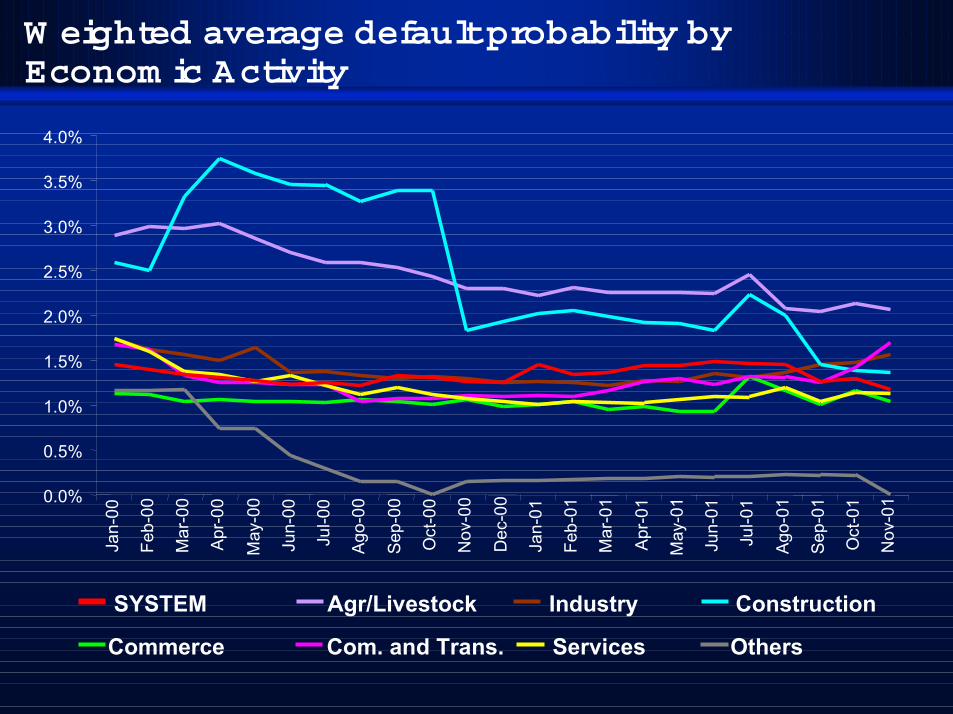

W eighted average default probability byEconom ic Activity

SYSTEM Agr/Livestock Industry Construction

Commerce Com. and Trans. Services Others

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%Ja

n-00

Feb-

00

Mar

-00

Apr-0

0

May

-00

Jun-

00

Jul-0

0

Ago-

00

Sep-

00

Oct

-00

Nov

-00

Dec

-00

Jan-

01

Feb-

01

Mar

-01

Apr-0

1

May

-01

Jun-

01

Jul-0

1

Ago-

01

Sep-

01

Oct

-01

Nov

-01

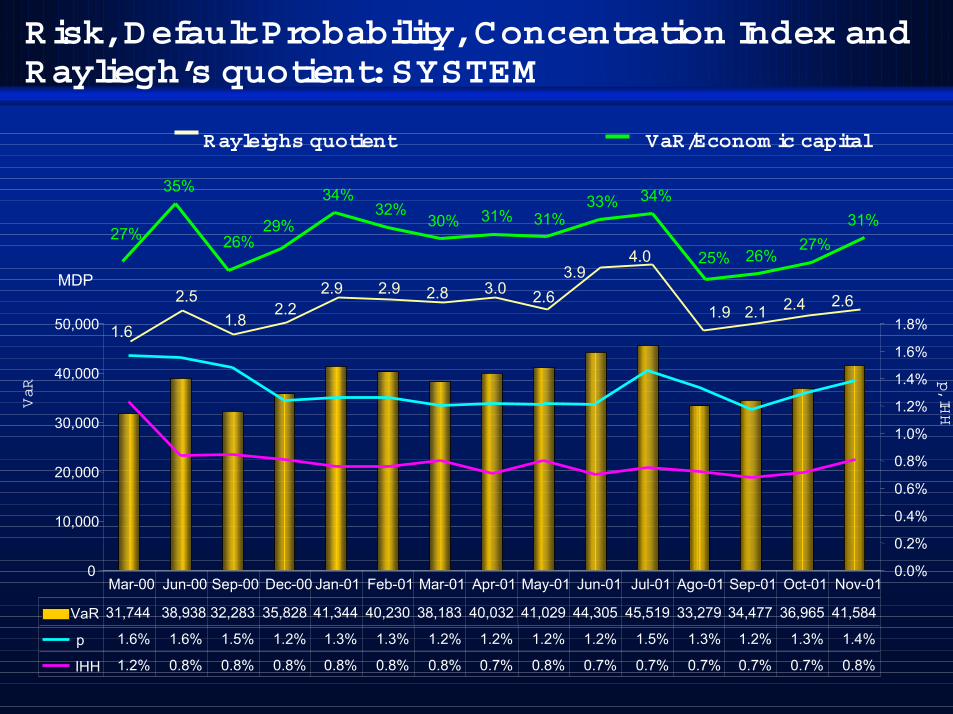

Risk, Default Probability, Concentration Index andRayliegh’s quotient: SYSTEM

VaR/Econom ic capital

27%

35%

26%29%

34%32%

30% 31% 31%33% 34%

25% 26%27%

31%

0

10,000

20,000

30,000

40,000

50,000

MDP

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

VaR 31,744 38,938 32,283 35,828 41,344 40,230 38,183 40,032 41,029 44,305 45,519 33,279 34,477 36,965 41,584

p 1.6% 1.6% 1.5% 1.2% 1.3% 1.3% 1.2% 1.2% 1.2% 1.2% 1.5% 1.3% 1.2% 1.3% 1.4%

IHH 1.2% 0.8% 0.8% 0.8% 0.8% 0.8% 0.8% 0.7% 0.8% 0.7% 0.7% 0.7% 0.7% 0.7% 0.8%

Mar-00 Jun-00 Sep-00 Dec-00 Jan-01 Feb-01 Mar-01 Apr-01 May-01 Jun-01 Jul-01 Ago-01 Sep-01 Oct-01 Nov-01

1.6

2.51.8

2.22.9 2.9 2.8 3.0 2.6

3.94.0

1.9 2.1 2.4 2.6

Rayleighs quotient

VaR p

, IHH

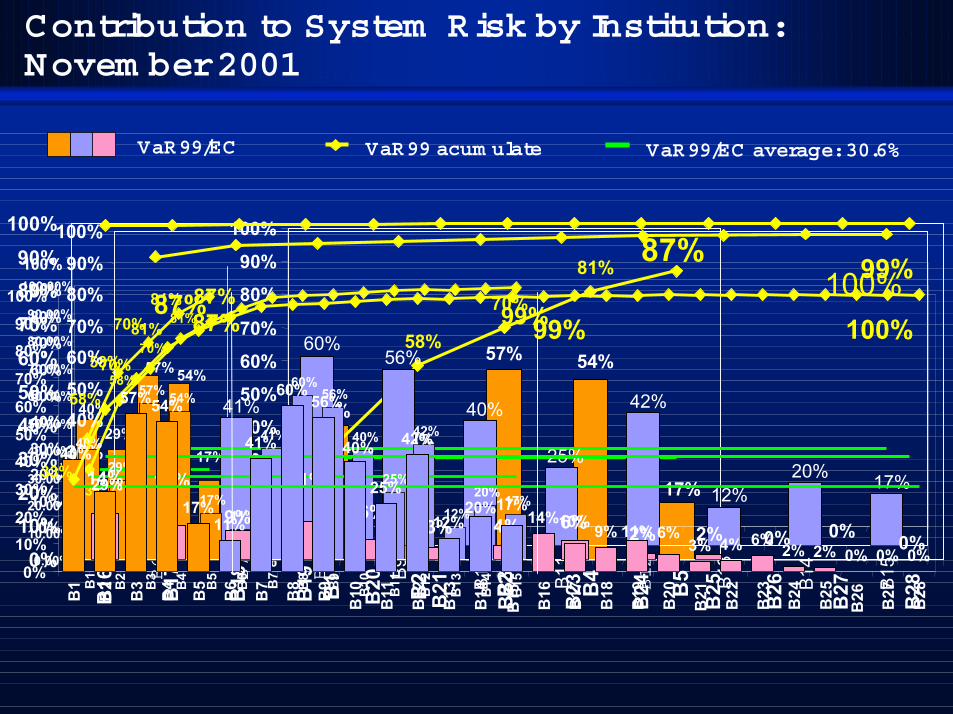

Contribution to System Risk by Institution:Novem ber 2001

VaR99/EC VaR99 acum ulate VaR99/EC average: 30.6%

54%57%

29%40%

17%33%

58%

70%

81%

0%10%20%

30%40%50%60%70%

80%90%

100%

B1

B2 B3

B4

B5

87%

40%29%

57% 54%

17%

81%70%

33%

58%

87%

0%10%20%30%40%50%60%70%80%90%

100%

B1

B2

B3 B4

B5

B6

B7

B8 B9 B10

B11

20%12%

42%

25%

40%

56%60%

41%

11%17%

99%

0%10%20%30%40%50%60%70%80%90%

100%

B12

B13

B14

B15

29%

57% 54%

17%11%

41%

60%56%

40%

25%

42%

12%20% 17%

40%

87%

58%

99%

33%

70%

81%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

B1

B2

B3

B4

B5

B6 B7

B8

B9

B10

B11

B12

B13

B14

B15

6%

14% 10%

9%

11%

3% 4% 6% 2% 2% 0% 0% 0%0%

10%20%30%40%50%60%70%80%90%

100%

B16 B17

B18

B19

B20

B21

B22

B23

B24

B25

B26

B27

B28

100%

57%54%

17%11%

41%

60%

25%

42%

12% 14%9%

3% 4% 6% 2% 2% 0% 0% 0%6%11%10%

17%

40%

29%

40%

20%

56%

87%

58%

33%

70%

81%

0%10%20%30%40%50%60%70%80%90%

100%

B1

B2

B3 B4

B5

B6

B7

B8

B9

B10

B11

B12

B13

B14

B15 B16 B17

B18

B19

B20

B21 B22

B23 B24

B25

B26 B27

B28

100%99%

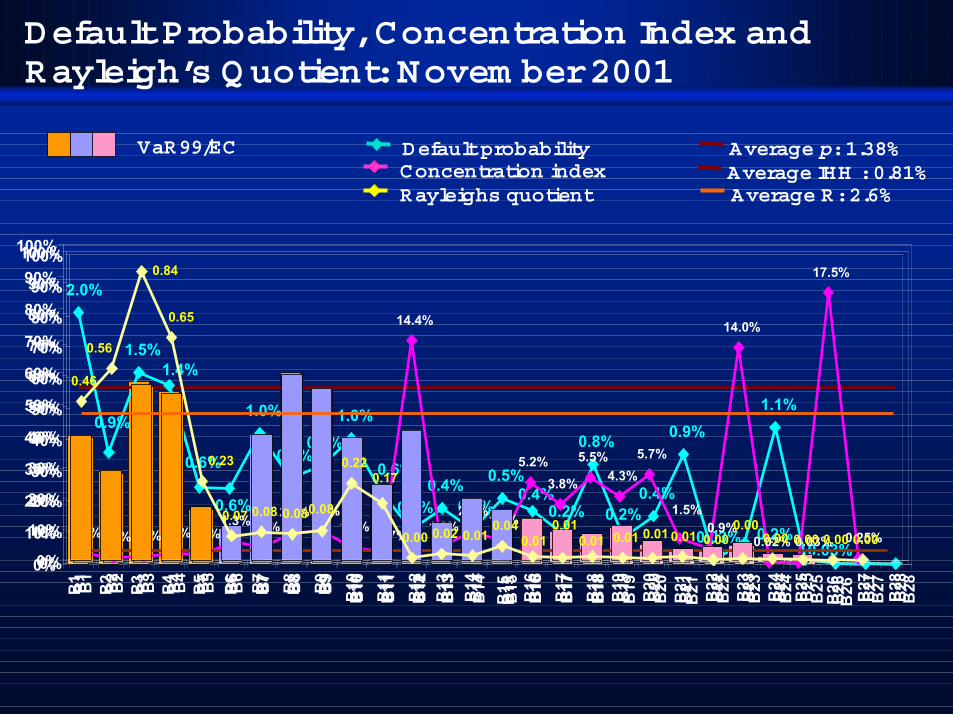

Default Probability, Concentration Index andRayleigh’s Q uotient: Novem ber 2001

VaR99/EC Average p: 1.38% Default probability

2.0%

0.9%

1.5%1.4%

0.6%

0.6%

1.0%

0.7%0.8%

1.0%

0.6%

0.3%0.4%

0.3%

0.5%0.4%

0.2%

0.8%

0.2%0.4%

0.9%

0.2%

1.1%

0.03%0.03%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

B1

B2

B3 B4

B5

B6

B7

B8

B9

B10

B11

B12 B13

B14

B15

B16

B17

B18

B19 B20

B21 B22

B23

B24

B25

B26 B27

B28

Average IHH : 0.81% Concentration index

0.6%0.3%0.4%0.6%0.5%1.3%1.0%

2.0%2.0%1.0% 0.7%

14.4%

1.0%2.0%1.4%

5.2%3.8%

5.5%4.3%

5.7%

0.9%

14.0%

17.5%

0.03% 0.25%0.02%

1.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

B1

B2 B3

B4

B5

B6 B7

B8

B9

B10

B11 B12

B13

B14

B15 B16

B17

B18 B19 B20

B21 B22

B23

B24 B25

B26 B27

B28

Rayleighs quotient Average R: 2.6%

0.46

0.56

0.84

0.65

0.23

0.07 0.08 0.080.08

0.220.17

0.00 0.02 0.010.04

0.010.01

0.01 0.01 0.01 0.01 0.000.00

0.00 0.00 0.00 0.000%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

B1

B2

B3

B4 B5

B6

B7

B8

B9

B10

B11

B12

B13 B14

B15 B16

B17

B18

B19 B20

B21 B22 B23

B24

B25

B26 B27

B28

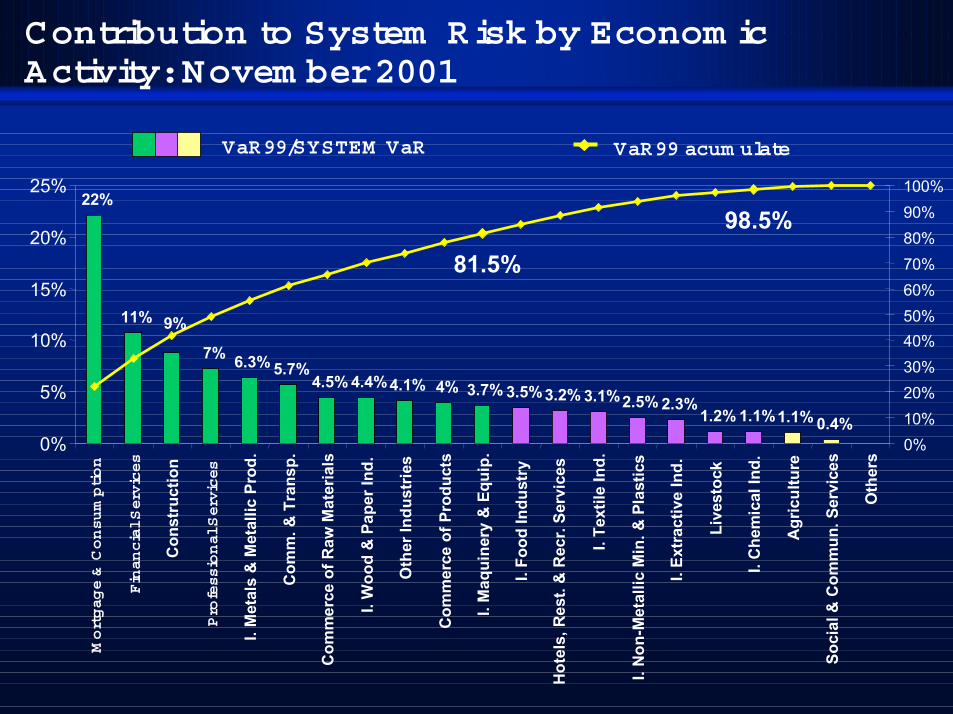

Contribution to System Risk by Econom icActivity: Novem ber 2001

VaR99 acum ulate VaR99/SYSTEM VaR

4.1% 3.7% 3.5%3.2% 3.1%2.5% 2.3%1.2% 1.1%1.1% 0.4%

6.3% 5.7%4.4%4.5%

22%

11% 9%

7%

4%

98.5%

81.5%

0%

5%

10%

15%

20%

25%

Mortgage & Consumption

Financial Services

Con

stru

ctio

n

Professional Services

I. M

etal

s &

Met

allic

Pro

d.

Com

m. &

Tra

nsp.

Com

mer

ce o

f Raw

Mat

eria

ls

I. W

ood

& P

aper

Ind.

Oth

er In

dust

ries

Com

mer

ce o

f Pro

duct

s

I. M

aqui

nery

& E

quip

.

I. Fo

od In

dust

ry

Hot

els,

Res

t. &

Rec

r. Se

rvic

es

I. Te

xtile

Ind.

I. N

on-M

etal

lic M

in. &

Pla

stic

s

I. Ex

trac

tive

Ind.

Live

stoc

k

I. C

hem

ical

Ind.

Agr

icul

ture

Soci

al &

Com

mun

. Ser

vice

s

Oth

ers

0%10%20%30%40%50%60%70%80%90%100%

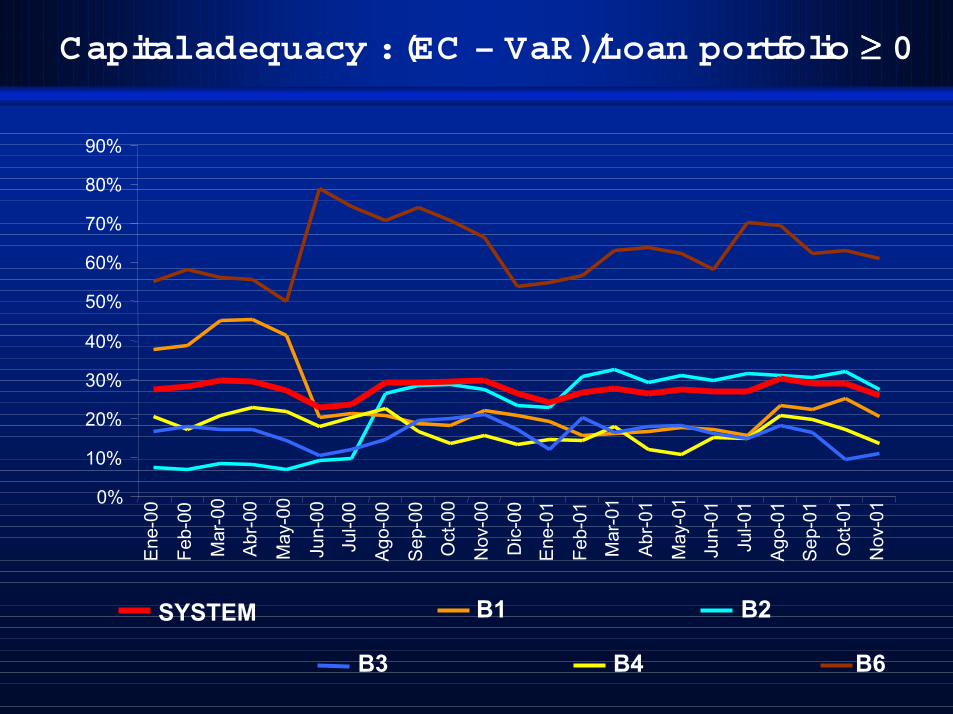

Capital adequacy : (EC – VaR)/Loan portfolio ≥≥≥≥ 0

B2 B1

B4 B6B3

SYSTEM

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%En

e-00

Feb-

00

Mar

-00

Abr-0

0

May

-00

Jun-

00

Jul-0

0

Ago-

00

Sep-

00

Oct

-00

Nov

-00

Dic

-00

Ene-

01

Feb-

01

Mar

-01

Abr-0

1

May

-01

Jun-

01

Jul-0

1

Ago-

01

Sep-

01

Oct

-01

Nov

-01

END