Century CenturyLink Link A Leading Rural Telecom Provider in A Leading Rural Telecom Provider in Kansas Kansas KCC Broadband & Telecom Roundtable KCC Broadband & Telecom Roundtable – March 11, 2011 March 11, 2011 1 Presented by John Idoux Presented by John Idoux - CenturyLink Governmental Affairs CenturyLink Governmental Affairs

Transcript

CenturyCenturyLinkLink

A Leading Rural Telecom Provider inA Leading Rural Telecom Provider in KansasKansas

KCC Broadband & Telecom Roundtable KCC Broadband & Telecom Roundtable –– March 11, 2011 March 11, 2011

1

KCC Broadband & Telecom Roundtable KCC Broadband & Telecom Roundtable –– March 11, 2011 March 11, 2011

Presented by John Idoux Presented by John Idoux -- CenturyLink Governmental AffairsCenturyLink Governmental Affairs

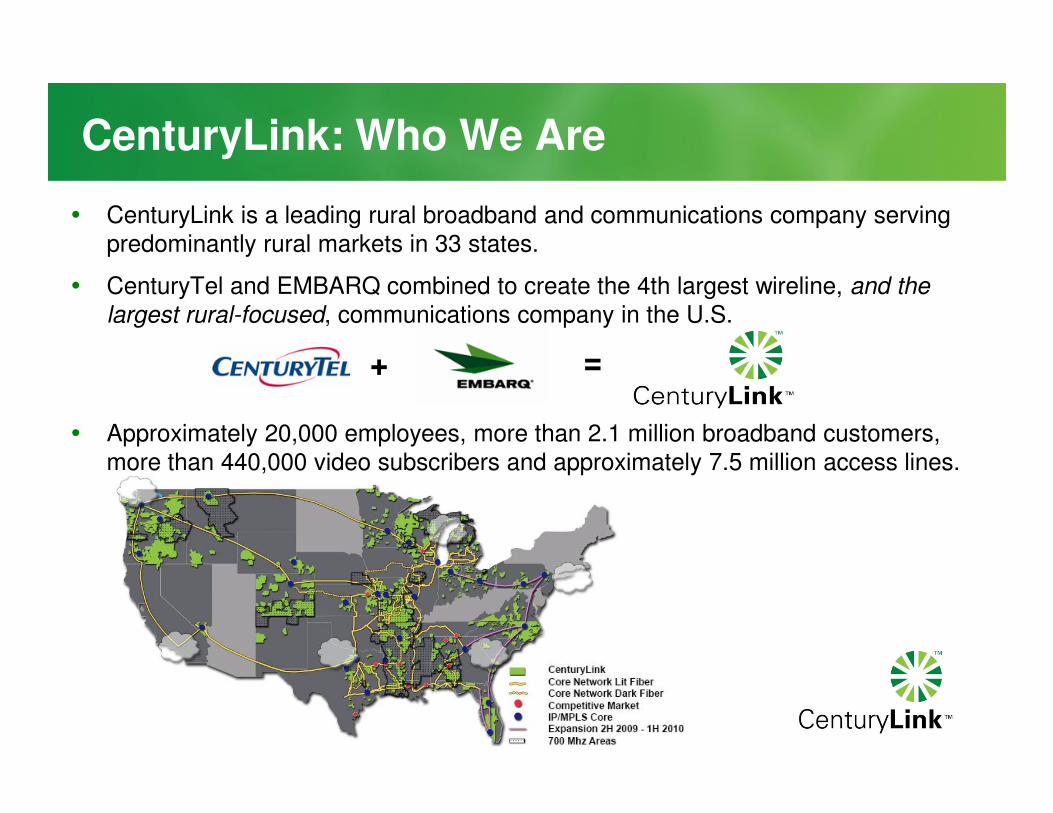

CenturyLink: Who We Are

� CenturyLink is a leading rural broadband and communications company serving predominantly rural markets in 33 states.

� CenturyTel and EMBARQ combined to create the 4th largest wireline, and the

largest rural-focused, communications company in the U.S.

+ =

� Approximately 20,000 employees, more than 2.1 million broadband customers, more than 440,000 video subscribers and approximately 7.5 million access lines.

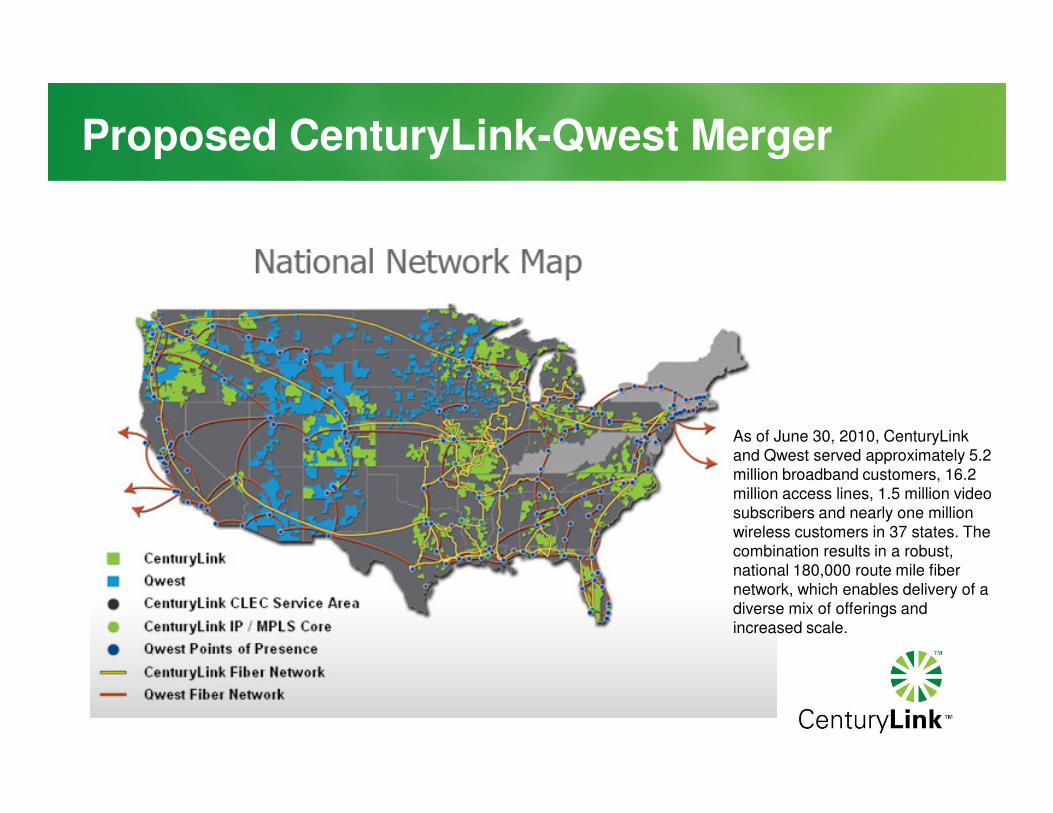

Proposed CenturyLink-Qwest Merger

As of June 30, 2010, CenturyLink and Qwest served approximately 5.2 million broadband customers, 16.2 million access lines, 1.5 million video subscribers and nearly one million wireless customers in 37 states. The combination results in a robust, national 180,000 route mile fiber network, which enables delivery of a diverse mix of offerings and increased scale.

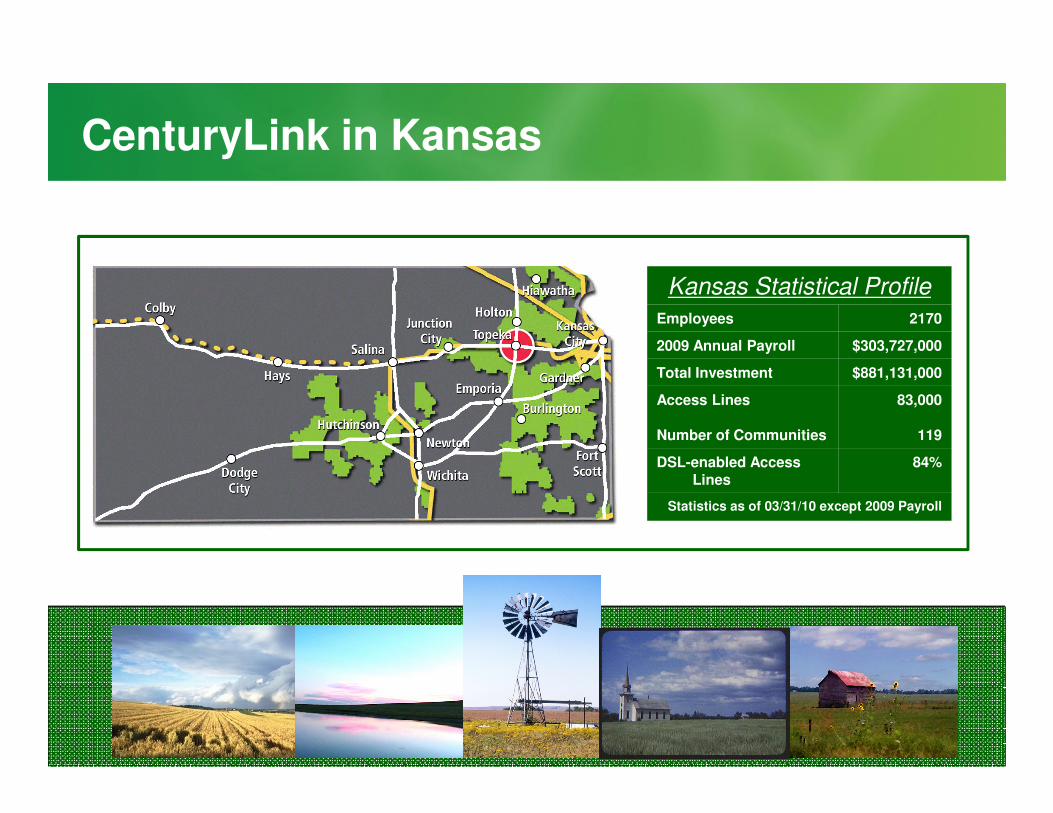

CenturyLink in Kansas

Kansas Statistical Profile

Employees 2170

2009 Annual Payroll $303,727,000

Total Investment $881,131,000

Access Lines 83,000Access Lines

Number of Communities

83,000

119

DSL-enabled Access Lines

84%

Statistics as of 03/31/10 except 2009 Payroll

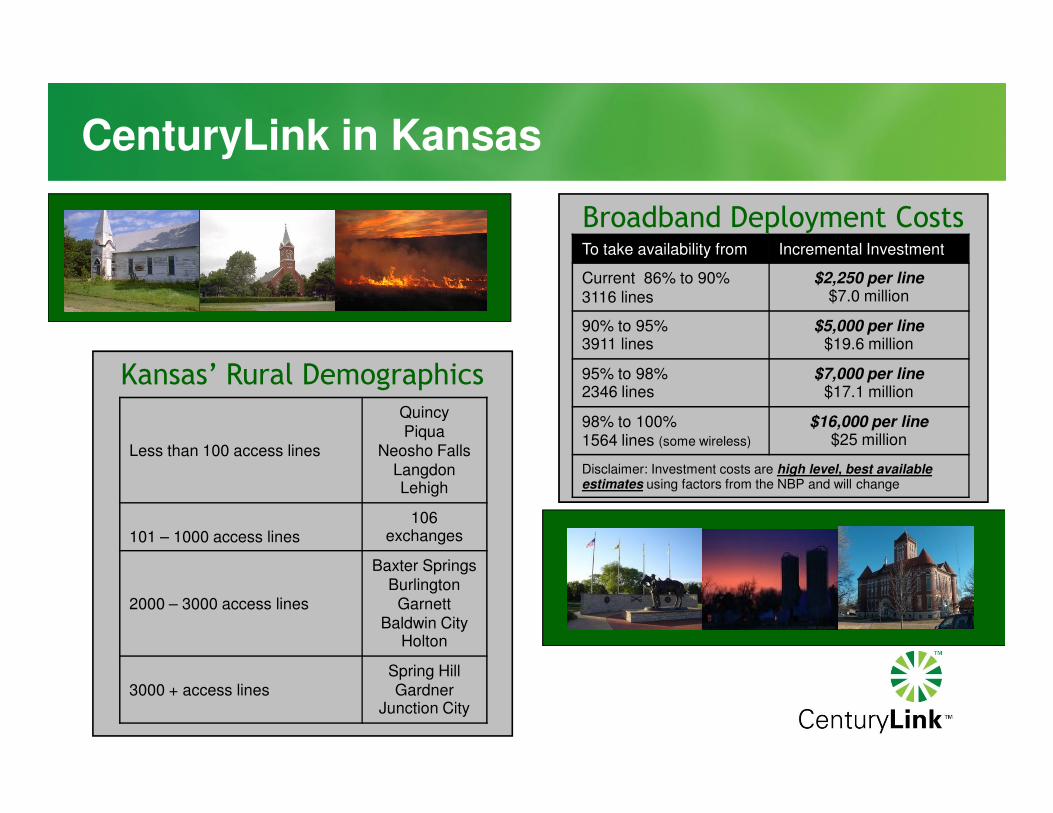

Kansas’ Rural DemographicsQuincy

CenturyLink in Kansas

Broadband Deployment CostsTo take availability from Incremental Investment

Current 86% to 90% 3116 lines

$2,250 per line$7.0 million

90% to 95%3911 lines

$5,000 per line$19.6 million

95% to 98%2346 lines

$7,000 per line$17.1 million

Less than 100 access lines

QuincyPiqua

Neosho FallsLangdonLehigh

101 – 1000 access lines106

exchanges

2000 – 3000 access lines

Baxter SpringsBurlington

GarnettBaldwin City

Holton

3000 + access linesSpring HillGardner

Junction City

98% to 100%1564 lines (some wireless)

$16,000 per line$25 million

Disclaimer: Investment costs are high level, best available estimates using factors from the NBP and will change

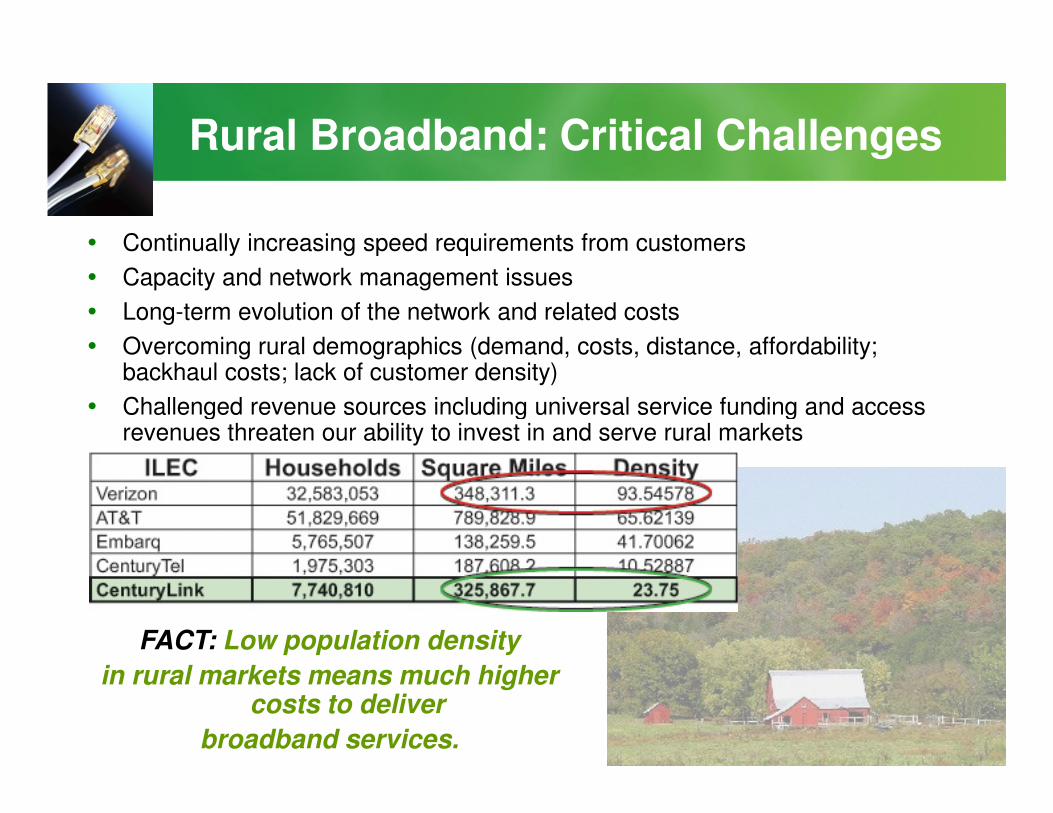

Rural Broadband: Critical Challenges

� Continually increasing speed requirements from customers

� Capacity and network management issues

� Long-term evolution of the network and related costs

� Challenged revenue sources including universal service funding and access � Challenged revenue sources including universal service funding and access revenues threaten our ability to invest in and serve rural markets

FACT: Low population density

in rural markets means much higher costs to deliver

broadband services.

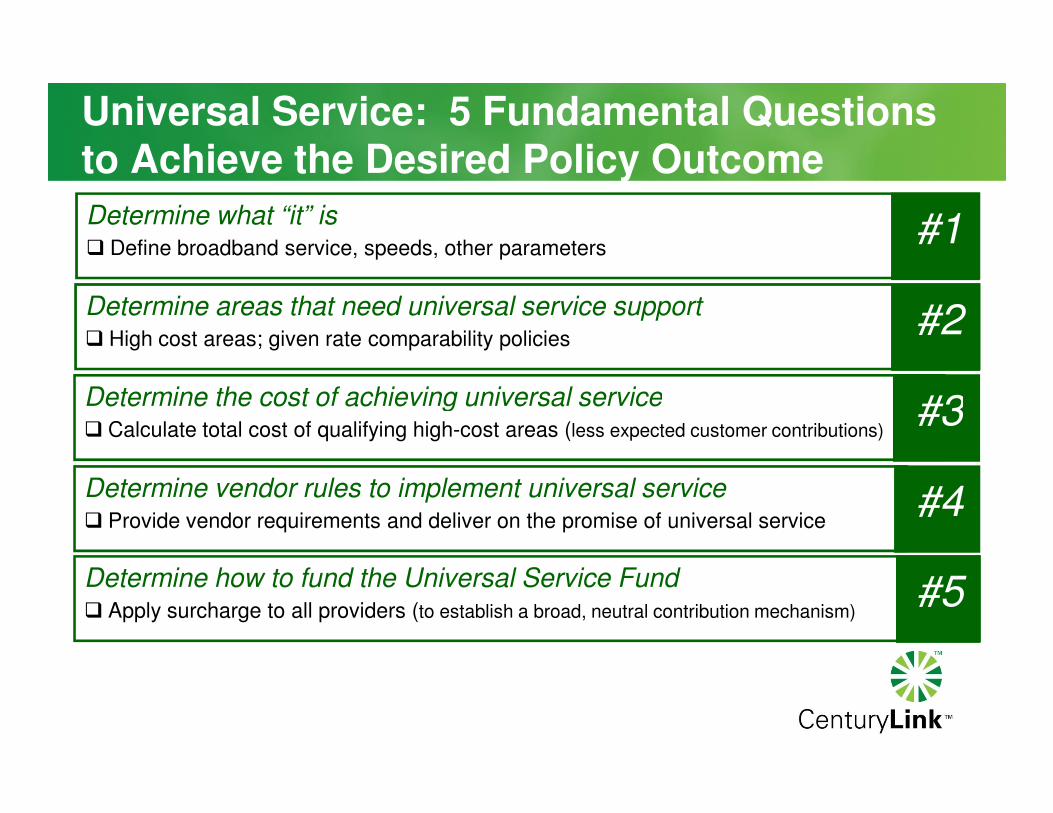

Universal Service: 5 Fundamental Questions to Achieve the Desired Policy Outcome

Determine what “it” is� Define broadband service, speeds, other parameters

#1

Determine areas that need universal service support� High cost areas; given rate comparability policies

#2

Determine the cost of achieving universal service #3Determine the cost of achieving universal service� Calculate total cost of qualifying high-cost areas (less expected customer contributions)

#3

Determine vendor rules to implement universal service� Provide vendor requirements and deliver on the promise of universal service

#4

Determine how to fund the Universal Service Fund� Apply surcharge to all providers (to establish a broad, neutral contribution mechanism)

#5

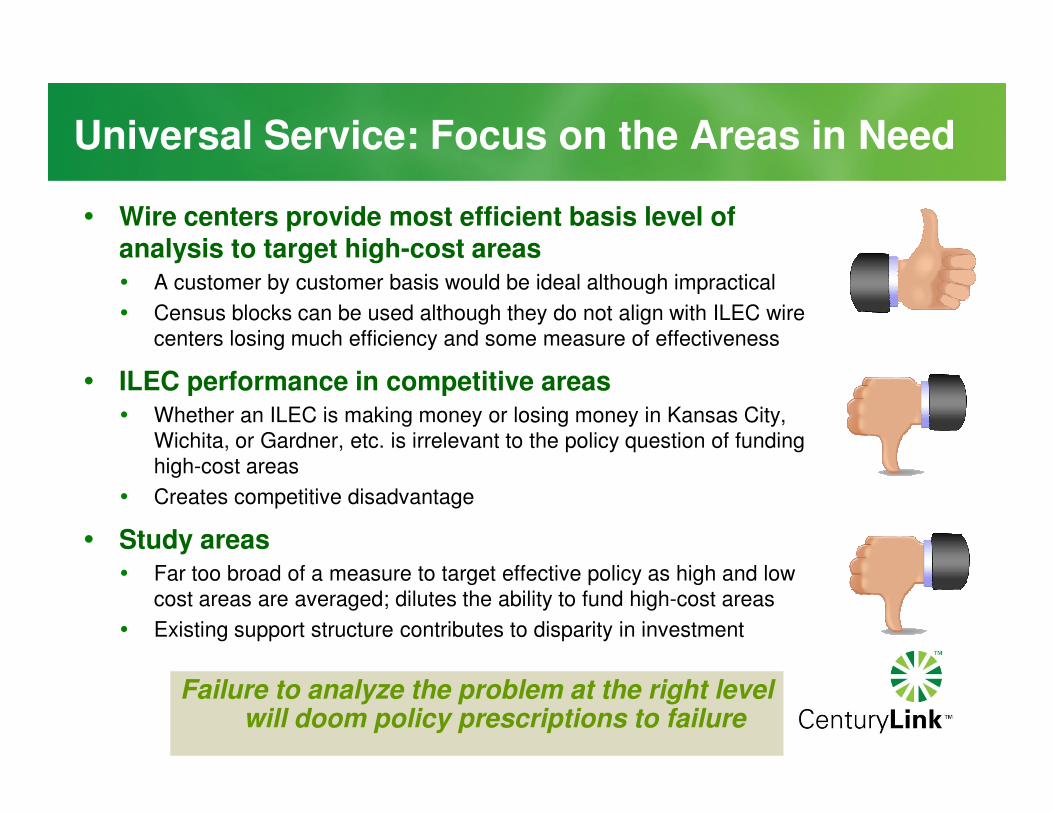

Universal Service: Focus on the Areas in Need

� Wire centers provide most efficient basis level of analysis to target high-cost areas� A customer by customer basis would be ideal although impractical

� Census blocks can be used although they do not align with ILEC wire centers losing much efficiency and some measure of effectiveness

� ILEC performance in competitive areas� Whether an ILEC is making money or losing money in Kansas City, � Whether an ILEC is making money or losing money in Kansas City,

Wichita, or Gardner, etc. is irrelevant to the policy question of funding high-cost areas

� Creates competitive disadvantage

� Study areas� Far too broad of a measure to target effective policy as high and low

cost areas are averaged; dilutes the ability to fund high-cost areas

� Existing support structure contributes to disparity in investment

Failure to analyze the problem at the right level will doom policy prescriptions to failure

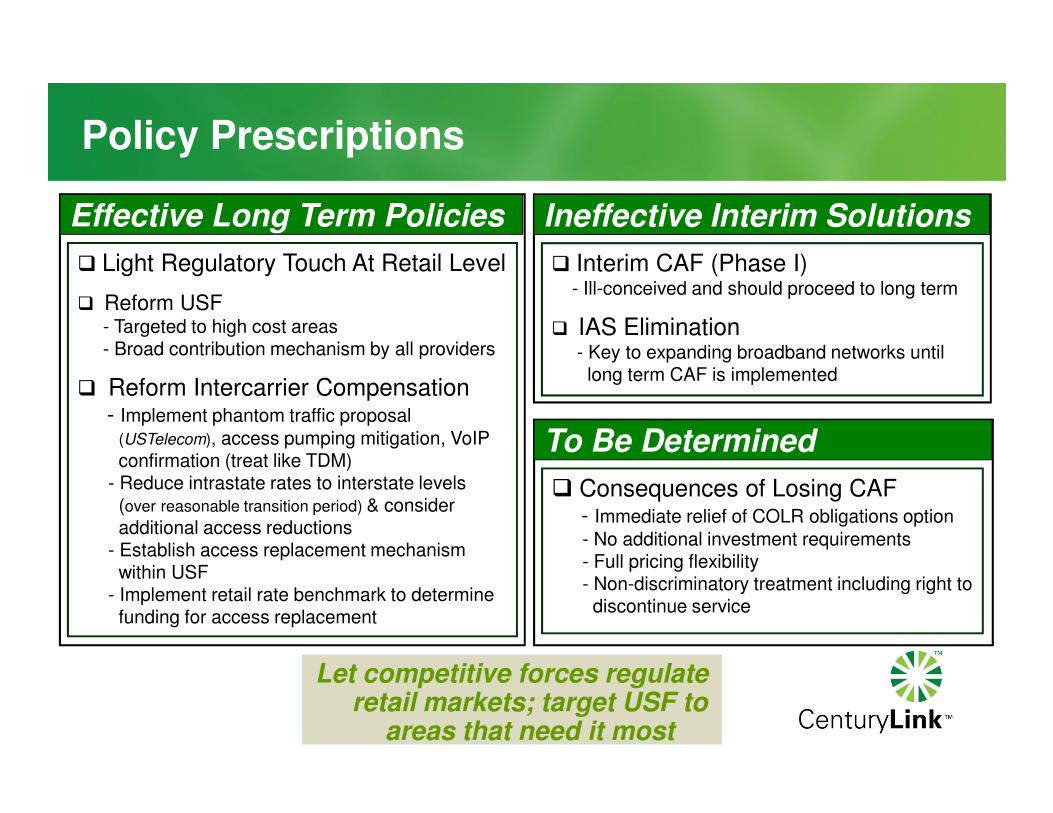

Policy Prescriptions

Effective Long Term Policies

� Light Regulatory Touch At Retail Level

� Reform USF- Targeted to high cost areas- Broad contribution mechanism by all providers

- Establish access replacement mechanism within USF

- Implement retail rate benchmark to determinefunding for access replacement

To Be Determined

� Consequences of Losing CAF- Immediate relief of COLR obligations option- No additional investment requirements- Full pricing flexibility- Non-discriminatory treatment including right todiscontinue service