A Practical Guide to Successful SEPA Migration Providing a list of software and service providers PPI AG Informationstechnologie Moorfuhrtweg 13, 22301 Hamburg Wall 55, 24103 Kiel Peter-Müller-Str. 10, 40468 Düsseldorf Wilhelm-Leuschner-Straße 79, 60329 Frankfurt/Main

Transcript

A Practical Guide to Successful SEPA MigrationProviding a list of software and service providers

PPI AG InformationstechnologieMoorfuhrtweg 13, 22301 Hamburg Wall 55, 24103 KielPeter-Müller-Str. 10, 40468 Düsseldorf Wilhelm-Leuschner-Straße 79, 60329 Frankfurt/Main

3

The harmonisation of the Single Euro Payments Area, or SEPA, is now in its final phase. Under the SEPA Migration Regulation, all countries that participate in the euro are required to start using the new SEPA instruments for payments in euros – and to discontinue the present national instruments for credit transfers and direct debits – by 1 February 2014.

We know from discussions with a variety of clients that many of you would like further support from your bank throughout migration to SEPA. This is confirmed by the extraordinary demand for our publication, “The Ultimate Guide to SEPA Migration”. As a result, we have asked PPI AG to compile this guide, which is designed to provide additional practical assistance to ease the transition.

Over recent years PPI has supported numerous clients on the road to successful SEPA implementation – now you can take advantage of our experience.

Section 1 of the guide provides an overview of the impact of SEPA on business operations, on the departments affected and on IT systems. In addition, it gives practical tips on identifying the functional, organisational and technological gaps that have been created by SEPA.

Section 2 contains advice on how to close these gaps— by taking advantage of some of the third-party products and services available on the market. It gives an overview of all the service providers known to us and recommendations as to the criteria you should apply in selecting your provider. Please note, however, that this guide does not provide – nor does it claim to provide – an exhaustive list of all providers.

Section 3 provides support for project planning and illustrates the make-up, phases and length of a typical SEPA project.

Finally, the Appendix contains additional information, including details of the various providers in Europe.

We look forward to continuing our dialogue and wish you all a smooth and efficient SEPA migration.

Preliminary remarks

Thomas ReherMichael Spiegel

Michael SpiegelGlobal Head of Trade Finance and Cash Management Corporates, Deutsche Bank AG

Thomas ReherMember of the Management Board, PPI AG

4

Table of contents

Preliminary remarks 3

1 Impact of SEPA on business operations and IT 71.1 Business areas affected 71.2 Impact on the payment process 8

1.3 Impact on systems and IT 101.3.1 New functionalities 101.3.2 Data content and structures 101.3.3 Data formats 111.3.4 Data conversion 11

2 Commercially available SEPA conversion support products 132.1 Introduction 132.2 Overview of SEPA products and services offered by external providers 132.3 SEPA software 15

2.3.1 Selection process 152.3.2 Long-listing: an overview of providers 162.3.3 Short-listing and final selection 162.3.4 Mandate management requirements 17

2.3.4.1 Functionality 172.3.4.2 Integration in the system and process landscape 19

2.3.5 IBAN/BIC converter requirements 202.3.5.1 Functionalities 202.3.5.2 Integration in the system and process landscape 20

2.3.6 XML converter requirements 212.3.6.1 Functionalities 212.3.6.2 Integration in the system and process landscape 21

6 List of SEPA software and SEPA testing providers 356.1 Contact and general information 356.2 Services and solutions offering 44

7 Examples of SEPA impact on individual business areas 47

8 Make-or-Buy decision parameters 52

9 Appendix 549.1 References 549.2 Table of figures 54

6

7

1.1 Business areas affected

With its new payment file formats and account identifiers, and the changes to the procedural rules for credit transfers and direct debits, SEPA now affects all areas of your business:– in which euro payments are made (e.g. payroll accounting)– in which euro payments-in, for example account statement

information, are processed (e.g. accounts)– which collect or use address and account identification data

(e.g. sales and marketing, supplier management)– which use documents containing account details

(e.g. creditor management)

– which exchange payments and information with banks and payment institutions in national formats

– which are responsible for liquidity control within the business (treasury, cash management)

– which manage risk and compliance within the business.

As a general rule, a SEPA project will necessitate modifications to your IT infrastructure, master data and business processes as well as the forms used in your business.

Figure 1 shows the most important business areas and the impact SEPA will have on them. Further examples are provided in the Appendix.

SEPA has a particularly significant impact on the payment process, affecting payments-out and payments-in in different ways. Since electronic account statements are now available in XML format as “camt” messages, it may, under certain circumstances, be necessary to make changes to the way debits and credits are booked.

The new “end-to-end ID” – mandatory information that must be forwarded on a one-on-one basis by all the parties involved in the payment chain from payer to recipient – can now be used to allocate an entry to a payment order. An identifier of this kind typically contains a unique invoice or order number and thus provides new potential for optimising account reconciliation.

1.2.1 Outgoing payments

The process concerning outgoing payments comprises all the actions necessary to create a payment file, send it to the bank and book it.

Figure 2 and Figure 3 show examples of the types of modifications required for credit transfers and direct debits.

Figure 2

Modifications to credit transfers out

Prepare paymentObtain/modify basic data

– Modify or obtain account identification data

– Modify data elements (e.g. payment reference)

Create payment

– Modify submission times where required

– Modify data formats

Submit payment

– Modify submission times where required

Reconcile/book payment

– Modify account reconciliation

– Modify account statement processing

– Modify R transaction processing

9

1.2.2 Incoming payments

All countries participating in the euro will need to have converted from national payment traffic formats to the XML format by February 2014. This will make it even easier to reconcile and book payments-in and will facilitate transactions thanks to the structured information contained in the new messages. For example, it will be possible to use the creditor reference (or payment reference) in account statements in XML format: so-called “camt” messages.

In addition, a number of changes are required in relation to direct debits. They relate in particular to the processing of R-transactions, as SEPA return processes are considerably more differentiated and structured than previous charge back processes. This will enable further automation of transaction processing within your business.

Figure 3

Changes in the direct debit process

Obtain/modify basic data

– Modify or obtain account identification data

– Modify data elements (e.g. payment reference)

– Obtain additional data (e.g. contact address for non-standard payer)

– Obtain creditor ID– Migrate direct debit

authorisations (existing) or obtain direct debit mandates (new business)

Prepare payment

– Modify submission times

– Modify data formats

– Supply additional data for payment run

Prepare payment

– Send pre-notification

– Integrate new check routines (e.g. mandate validity)

Submit payment

– Modify submission times

Reconcile/book payment

– Modify account reconciliation

– Modify account statement processing

– Modify R transaction processing

10

These changes will affect a significant number of IT systems, including not only those that generate or process payment files, but also any downstream systems which provide necessary data and cross-sectional systems used for document management, for example. In addition, external interfaces to customers, suppliers and other partners will also require modification.

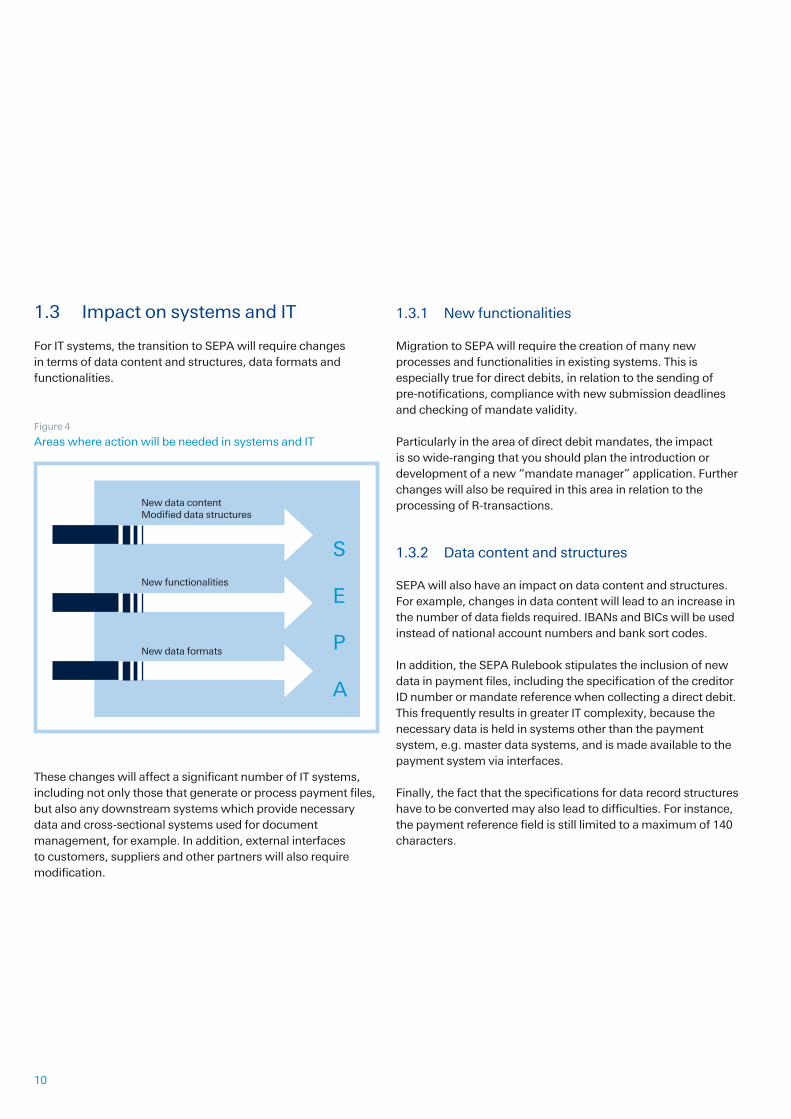

1.3.1 New functionalities

Migration to SEPA will require the creation of many new processes and functionalities in existing systems. This is especially true for direct debits, in relation to the sending of pre-notifications, compliance with new submission deadlines and checking of mandate validity.

Particularly in the area of direct debit mandates, the impact is so wide-ranging that you should plan the introduction or development of a new “mandate manager” application. Further changes will also be required in this area in relation to the processing of R-transactions.

1.3.2 Data content and structures

SEPA will also have an impact on data content and structures. For example, changes in data content will lead to an increase in the number of data fields required. IBANs and BICs will be used instead of national account numbers and bank sort codes.

In addition, the SEPA Rulebook stipulates the inclusion of new data in payment files, including the specification of the creditor ID number or mandate reference when collecting a direct debit. This frequently results in greater IT complexity, because the necessary data is held in systems other than the payment system, e.g. master data systems, and is made available to the payment system via interfaces.

Finally, the fact that the specifications for data record structures have to be converted may also lead to difficulties. For instance, the payment reference field is still limited to a maximum of 140 characters.

1.3 Impact on systems and IT

For IT systems, the transition to SEPA will require changes in terms of data content and structures, data formats and functionalities.

Figure 4

Areas where action will be needed in systems and IT

New functionalities

New data formats

New data contentModified data structures

S

E

P

A

11

1.3.3 Data formats

The data formats for national payment traffic files are also changing, being superseded by the XML format.

Since XML files create a comparatively higher data load due to their data structures, this change may even have an impact on the technical infrastructure. Estimates suggest that, following the introduction of the XML format, requirements for memory, capacity and computing power will increase at least three-fold in comparison with the German DTA format. Where applicable, it will therefore also be necessary to increase the line capacities for the transfer of payment files to the banks.

1.3.4 Data conversion

When converting account identification data or data formats you can opt for either one-off or recurrent data conversion. In the case of one-off conversion, both inventory data and new data in the systems have to be converted to the new specifications. In the case of recurrent conversion, the data is converted continuously using an intermediary software application at the input/output interface.

12

13

2 Commercially available SEPA conversion support products

2.1 Introduction

Once the gap analysis described in Section 1 is complete, every business will need to decide whether it wishes to close any gaps identified, either by using solutions developed in-house, or commercially available products and services (this is addressed in the “Make-or-Buy” decision and is detailed in Section 8).

Over recent years a market featuring a range of companies providing such external solutions has developed in Europe. The products and services they offer range from SEPA migration support services to software products designed to perform specific tasks.

The next section classifies the various companies providing these solutions. Section 2.3 provides practical hints on how to find the best software provider for your needs. Other SEPA services are described in Section 2.4.

Section 3 provides information on how to integrate the selection and implementation of external solutions into your SEPA project. NB – Other extensive changes will also be required involving the integration of your own resources (cf. Section 1 and Appendix: Examples of SEPA impact on individual business areas of a company) irrespective of whether you choose to use external solutions or providers.

Figure 5

Services offered by external providers

2.2 Overview of SEPA products and services offered by external providers

This section provides an overview of the services and specific SEPA software products available in the market.

Following migration to SEPA, it may be useful in individual cases to take advantage of the potential created by the standardisation of payment traffic. If you choose to do so, it is advisable either to replace the entire payment traffic platform, centralise payment traffic processing or outsource certain parts of the process as applicable (refer to "The Ultimate Guide to SEPA Migration" [1], p. 7 et seq.)

Section 6 contains a list of suppliers and the software products and services they offer; it also identifies sector and region-specific focuses.

The information contained in the list is based on a market analysis carried out by PPI, and on information supplied by the providers themselves. However, we cannot provide any guarantee that the information included is correct, complete or up-to-date.

Software

– Mandate management– IBAN/BIC conversion– XML conversion

Services

– Project management– Testing

Commercially available SEPA products and services

14

The providers can, in principle, be divided into the following categories:

International full service providersThis group comprises firms offering – at the bare minimum – most of the products and services listed above to clients in more than one EU country (in one or more sectors).

Regional full service providersThese companies provide their services in only one, or a small number, of EU countries. Their range of products and services includes the majority of those listed above (in one or more sectors).

International specialistsThe international specialists are those with a market presence in more than one EU country, but with a limited range of services.

Regional specialistsRegional specialists are firms with a market presence in only one, or a small number, of EU countries, but with a limited service offering.

We have classified the listed providers as shown in the table below:

Figure 6

Overview of providers

Sco

pe

of s

ervi

ces

Sp

ecia

lised

ser

vice

sFu

ll se

rvic

e

Country coverage

Regional International

– C1 Fin Con GmbH– Cedricom S.A.– Consolut International AG– ENERGY4U GmbH– Lusis S.A.– PPI Informationstechnologie AG– Stellwerk Consulting GmbH– Vericos GmbH– Volante Technologies Ltd

– allevo S.R.L.– ALSYON Technologies – KPMG International – Polinflex Solutions– PwC Group– SAP AG & Co.KG– Sterci Group S.A.– Steria Limited– SWIFT Group– XMLdation Ltd

– Adesso AG– Bank-Verlag GmbH– Cogon AG– CPG Finance Systems GmbH– DataLog Finance S.A.– DIMO Gestion S.A.– e-Finances SARL– GENEVA-ID GmbH– Ibidem GmbH– SIA SpA– van den Berg AG

– IBM Corp.– Incentage AG– msg systems AG– NEOFI Solutions S.A.– NTT Data Group– Omikron GmbH & Co.KG– Projektfabrik GmbH– SBC Systems GmbH– Sentenial Ltd– Simplex GTP Ltd.– Sungard Data Systems– TESSI S.A.– Unisys Group– XCOM AG

15

2.3 SEPA software

The market for SEPA software solutions is currently very dynamic, with a real boom in new solutions sparked by the EU’s passing of the SEPA Migration End Date Regulation in March 2012. The market is largely new and its products are developing quickly.

2.3.1 Selection process

If you wish to select a provider, you should opt for a structured, two-stage selection process using the long- and short-listing method detailed in sections 2.3.2 and 2.3.3.

Figure 7

Provider selection process

~ 1 week ~ 3 – 5 week ~ 3 – 4 week

Selection of no more than 8 to 10 providers from the Vendor Guide

Reduction to no more than 4 providers in a workshop

– Provider A– Provider B– Provider C– Provider D

– Individual presentations

– Indicative offers from providers

Final negotiation with provider C

Long listSelect providers for short list Short list

Evaluation of short list candidates

Selected provider

16

2.3.2 Long-listing: an overview of providers

Section 6 provides a list of all SEPA software providers known to us at the present time, who agreed to be named in this guide. You can use this list to choose candidates for your own long-list.

In order to provide additional guidance, each provider is classified according to a specific set of criteria. The categories were chosen on the basis of the providers’ answers to the following questions.

Functional scope of the softwareWhat software do they offer, i.e. mandate management, IBAN/BIC conversion or XML conversion?

Use of the softwareHow can you use the software, i.e. via a licence, as Software as a Service (SaaS) or on an Application Service Provider (ASP) model?

Software maturityHow mature is the software?

Software integration capabilitiesCan the software be integrated in open system environments and/or in mainframe environments?

RegionsIn which regions and markets are the provider and its solutions primarily available?

SectorsWhich sectors are covered?

2.3.3 Short-listing and final selection

To whittle down the number of long-listed candidates and derive the short-list, you will need a set of more business-specific criteria. To determine these criteria, we recommend that you organise a workshop that should be attended by representatives from the following business areas:– any specialist areas involved– relevant IT areas– IT architecture (in relation to integration)– purchasing.

It would also be useful to involve the relevant staff in the final decision-making process. To do this, you may wish to fine-tune the criteria according to individual factors specific to your business. Experience shows that the criteria should be neither too detailed nor contain too much technical specification. The following parameters have been found to provide a sound basis for decision making:– Provider – Credit-worthiness – Current position (e.g. mergers, etc.) – Practical experience/references – Availability of necessary resources – Quality of offer documents – Personal impression– Commercial evaluation – Price/performance ratio (what does the solution include/

exclude?) – Internal integration costs– Solution evaluation – Does it meet the functional requirements? – Does it meet the technical/integration capability

requirements?

At this stage – if you have yet to do so – you should ask all potential providers to formally present their solutions and make a serious offer.

Sections 2.3.4 to 2.3.6 provide further recommendations which may prove useful in assessing your functional and technical requirements.

17

Figure 8

Overview of basic mandate management functions

2.3.4 Mandate management requirements

2.3.4.1 FunctionalityMandate management involves the storage, administration and archiving of mandates. A mandate management application must therefore support the setting-up, amendment, blocking and deletion of mandates.

The core functions of mandate management include the addition of current mandate information to a payment run with SEPA direct debits.

Fig. 8 gives an overview of the most important basic mandate management functions. Some of the requirements listed are explained in greater detail below.

Framework functions– Issue mandate ID– Print out mandate– eMandate

Basic functions– Set up, modify, update, delete– Check, store– Archive

Information – Record of mandate at a particular point in time– Status information

Update status– Determine status: active/non-active mandate– Establish direct debit type: first, recurrent, one-off or last direct debit– Check deadline depending on direct debit type

Direct debit run– Check the validity of the mandate– Add mandate data to direct debits– Record status modifications for returns

18

Setting up a new mandateExisting collection authorisations/direct debit details (mass data) can be migrated in SEPA formats to the mandate manager, which then reuses this information in accordance with the SEPA Rulebook.

The mandate manager allows a new mandate to be set up by internal dialogue or by reference to external systems. It must also be possible to store different mandate statuses in the system.

In addition, the system should be able to manage both individual contract and consolidated mandates.

Modifying a mandateIn the mandate manager, you can track all modifications made to a mandate at any time and over its entire lifetime. Written documentation ensures that it is possible to account for the new information at any time.

In principle, all fields of a mandate can be modified. However, it is important to note that whenever the identity of a debtor or creditor is updated, you will need to obtain a new mandate.

To ensure end-to-end checking, it is important to ensure that modifications are dated. This makes it possible to determine what mandate information is/was valid at any time in the mandate management process. With the mandate manager it is possible to show the current and future statuses of a mandate over various time periods.

Please remember that mandate modifications involving the identity of the debtor or bank details, for example, require a new pre-notification. The relevant data on this is documented in the mandate manager.

Plausibility checkingThe mandate manager checks that all details are complete. If they are not, the relevant procedures for blocking the mandate are triggered automatically.

Access to mandate informationIt should be possible to integrate a mandate manager into existing authorisation structures fairly easily. An important prerequisite for successful integration is the ability, in principle, to create “View”, “Acquire”, “Modify” and “Delete” functions in accordance with the principle of dual control.

ArchivingThe creditor must be able to provide an end-to-end record of the mandate and any modifications which have been made to it. For this reason a data archive function should be implemented.

Other functionsIn addition, a mandate management system should also support the following functions:– Updating of mandate content in accordance with the

requirements set out in the SEPA Rulebook and national specifications whenever changes are made

– Ways of evaluating mandates, e.g. displaying all mandates for one creditor

– Termination of mandates which remain unused for more than 36 months, except in the case of framework mandates, as this would result in the termination of all contracts with the customer

– Creation of a mandate form (in the relevant contract language and English) from the mandate manager

– Use of electronic mandates where applicable

19

2.3.4.2 Integration in the system and process landscapeThe integration of a mandate manager into your IT architecture will depend on the specifications used in your business. In any event, it is recommended that you include the following requirements:– Multi-client capability to support the creation of different

group companies if required – Availability: 24 hours a day, 7 days a week

In addition, depending on the complexity of the existing IT architecture, you have the choice of either integrating a central mandate management system into the overall system landscape, or implementing several mandate managers for specific systems.

With individual mandate managers, for example, it is possible to use a combination of SAP mandate managers for the SAP module and other mandate management systems for other areas of your business. However, with this type of arrangement, uniform data storage is likely to be more complex than with a central mandate management system.

Central mandate management systems control mandate data and create direct debits for a range of applications. The fundamental advantages of such centralisation are the reduced space requirement and the central checking capability (for the dual issue of mandate references, for example). It is also easier to display evaluations with a central mandate management system.

The example below shows how a central mandate manager can be integrated into a system landscape:

Figure 9

Mandate manager interfaces

Master data

Mainframe applications

Front end

Peripheral systems

Clearing

Mandate management

Mandate database

Other requirements

Archiving

Mandate modification

Plausibility check

New mandate set-up

Access mandate information

Mandate management

20

Due to the high degree of integration and potential other factors, the introduction of a mandate management system creates a range of challenges. These include:– the high number of stakeholders in the business (both

specialist departments and IT)– the integration of customer processes into mandate

management (setting-up, modifying and deleting mandates, complaints, etc.)

– the integration of the mandate manager into business partner and customer systems

– the interaction between the various systems involved in the payment traffic process, e.g. ERP, electronic banking and client-specific systems

– the different technical platforms (Host, Java, etc.)– the limited availability of technical expertise– the migration of all direct debit collection authorisations to

SEPA mandates– the conversion of account numbers and bank sort codes to

IBANs/BICs– pre-notifications for contract holders and, where appropriate,

non-standard payers– the storage and archiving of mandates (physical and

electronic)

2.3.5 IBAN/BIC converter requirements

2.3.5.1 FunctionalitiesAn IBAN converter calculates the correct IBAN from the bank sort code and the account number. These two components are converted into an IBAN using a database and a computation process. The relevant BIC is determined from an index of bank sort codes.

Please note that, as a general rule, each country has a different IBAN structure. In addition, most converters do not provide a 100% conversion rate, because under some configurations – for example, in the case of merged banks – the IBAN cannot always be determined correctly on the basis of algorithms. However, providers and some central banks are aware of the problem of incorrect conversions, and work on appropriate solutions is ongoing.

In addition, you should note that, for liability reasons, converter solutions do not guarantee 100% correct results.

2.3.5.2 Integration in the system and process landscape IBAN converters can be used as a one-off process as part of a full conversion. Apart from the introduction of the IBAN and BIC fields, there are almost no other integration costs since the existing database can be exported and the new one imported. It is simply necessary to modify the import interfaces accordingly.

Before converting account numbers and bank sort codes, we recommend that you cleanse the master data to ensure that only current bank details are converted to existing bank sort codes. This will result in a higher conversion rate, and additional funds and time should be earmarked for this activity.

Rather than being restricted to single use, IBAN converters can also be integrated into the normal operation of a business so that conversion takes place as and when required. In this instance, the output data used (account numbers and bank sort codes) will have to be corrected (where necessary) in advance, in order to avoid delays and failed payments. In addition, it is

21

Figure 10

Converter interfaces

essential to analyse supplier and target systems in order to determine any modifications that may be required. The necessary interfaces may, for example, be based on the following services:– WEB services– Remote Function Calls (RFC)– Message Queues (MQ).

2.3.6 XML converter requirements

2.3.6.1 FunctionalitiesExperience has shown that even after SEPA implementation, various systems in a company will continue to supply credit transfers and direct debits in national formats (e.g. DTA format in Germany). For this reason, it will also be necessary in future to provide a converter for XML files. This converter must be capable of both, converting outgoing files from national formats (e.g. the German DTA) or global formats (e.g. IDOC, CSV or EDIFACT) into XML files and converting incoming XML files into the non-XML formats used by your customers. When

structuring files, it is therefore vital to consider any business idiosyncrasies in order to reduce the number of different data formats in use, as well as to avoid data loss.

In addition, the converter should also be able to abbreviate the payment reference for the SEPA format. A good solution here would be an administrable logic function that automatically represents long expressions as abbreviations (for example by abbreviating “invoice number” to “IN”).

2.3.6.2 Integration in the system and process landscape The XML converter should ideally be integrated into normal business operation to enable conversion to take place as and when required. This means that supplier and target systems have to be analysed in order to determine the need for any modifications.

The conversion of both account numbers to IBAN/BIC format and of XML files can be integrated into the system landscape as follows:

IT system landscape

Mandatedatabase

Conversion

IBAN/BIC

Nationalformats/

XML

Other requirements

Archiving

Mandate modification

Plausibility check

New mandate set-up

Access mandate information

Mandate management

Mandate management

22

2.3.7 Software usage options

The software operation model will generally be specified by a business’s existing IT strategy or existing payment traffic solutions. In any event, the operating model is a decision-making criterion in terms of evaluation for the future solution. Most providers offer the following usage options:

LicensingProviders license software and permit its operation within a company’s own system infrastructure. In some cases they provide maintenance and support under the terms of a service level agreement. The charge for this service takes the form of royalties, maintenance fees, etc.

Software as a Service (SaaS)The SaaS model is based on the principle that both the software and the IT infrastructure are operated by an external IT service provider and are used as a service by the customer. The service user does not therefore install its own software. To use the service, the user simply needs an Internet connection to the

external IT service provider. Access to the software is generally via a web browser. To use and operate the service, the user pays a charge based on usage (generally per user and per month/data record).

This model can be useful for conversions where the customer contracts a service provider to convert inventory on a one-off basis.

Application Service Provider (ASP) servicesAn Application Service Provider (ASP) offers its application over a public network, such as the Internet or a private data network. The ASP takes care of all administration tasks including backups, the installation of patches, etc. The ASP facility normally includes all services (e.g. user support) related to the application. With this system the software required is not purchased, but leased for use over the data network. ASP services allow companies to outsource entire areas of administration and/or other individual business processes, thereby freeing them up to concentrate on their core activities.

23

2.4 SEPA services

2.4.1 SEPA project management

The scope and intensity of a SEPA project depend on many factors. Support is available from external service providers and management consultants throughout the process. In addition to project management functions, they can also take on practical tasks such as the elaboration and fine-tuning of technical specifications.

By using the wealth of SEPA expertise available you can significantly increase the speed and quality of migration – as long as you have scrutinised the credentials of your provider first.

As capability and credentials are so important, it is recommended that you pay particular attention to the following areas when selecting a service provider:– SEPA expertise and SEPA references

of both the service provider and the particular project consultant

– the consultant’s availability– SEPA-specific project tools, e.g. SEPA checklists– the price/performance ratio.

However, a significant increase in demand for experienced consultants has led to price escalation and may well result in a shortage of available qualified consultants. For example, a representative survey of German insurance companies revealed that 67% of firms questioned wish to buy-in support from external personnel for their migration to SEPA (see “SEPA Readiness Index” [2]).

2.4.2 SEPA testing

Like any system modification, the conversion of a system to SEPA has to be tested before commissioning, which means it is necessary to establish concrete requirements for test procedures and benchmarks for the corresponding quality assurance. A key point in this respect is real payment traffic with banks (business client/bank interface) as there are new SEPA formats to be set-up, and the bank may supply new “camt” formats.

As part of this testing process, banks offer a wide range of accompanying services that vary between providers. The primary task at the client/bank interface is to ensure that the data formats supplied and processed by both parties are syntactically and semantically correct. This can be done by means of format testing.

However, these tests are not able to recreate the complete process chain and, as a result, many banks recommend that SEPA transactions be tested using real payment data in so-called “productive tests”. This is the only way of reliably checking whether end-to-end processing (including R-transactions) is operating smoothly.

In light of this recommendation, businesses often find it necessary to find a test partner able to simulate the role of the bank and payment traffic recipient. The objective is for the business to test its new systems – including data transfer – on a fully functioning external interface before a productive test. In so doing, it is advisable to simulate R transactions as well as positive cases, as these transfers have to be treated in a particular manner in the specialist/technical processes downstream. It should also be noted that the test products currently on the market offer conversion from national formats to SEPA and vice versa, but do not support the end-to-end testing that is also required.

24

25

3 SEPA project roadmap

A SEPA implementation project can typically be divided into the following phases:– Preliminary study– Detailed design/project initialisation– Implementation– Testing– Completion

The content of the individual phases is described in the table below, which also shows how to integrate the selection and implementation of external solutions into your SEPA project.

Figure 11

The phases of a SEPA project

Preliminary study Detailed design Implementation Testing Completion

– Identify need for modification in terms of: organisation, processes, systems, documents

– Take basic technical/specialist decisions, e.g. Make or Buy

– Where applicable, carry out selection procedure for external solutions

– Evaluate need for modification

– Plan implementation phase

– Technical specifications for measures identified (e.g. technical specification for mandate manager, training specification for staff)

– Data processing and testing specifications for systems to be modified/integrated

– Validate results of preliminary study

– Prepare for implementation phase

– Development (if in-house)

– Customising (third party software)

– Modification of client models and processes

– Installation– Implementation of

detailed improvements

– Interface development and modification

– Documentation– Data migration

– Integration test– Technical

acceptance test– Training– Deployment

– Finishing touches/end of project

– Disposal/removal of old systems as required

26

ScheduleThe roadmap below shows the typical sequence of individual project phases for a company starting work in the first quarter

of 2013. As you are no doubt aware, the latest project completion date is the statutory migration end date of 1 February 2014.

Figure 12

Typical SEPA project schedule

2013 2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

EffortEven if you use some or all of the external solutions specified in Section 2, you will still need to make a large number of changes independently, using proprietary resources.

The effort required to complete a SEPA implementation project depends on a number of factors. These include, in particular, company size, sector, the number of business areas involved, geographical location and the specialist, technical and political particularities of the specific case.

Experience has shown that businesses require two to three months to carry out a preliminary study involving a core team of 2–3 people.

The average number of people making up the core team for the implementation phase ranges from 3–5, and goes up to 10–20 when further specialists employed on an ad hoc basis, such as developers or legal experts, are counted.

In total, a SEPA migration project takes between at least 200, and up to some 20,000, working days. While it may seem high, this latter figure is perfectly conceivable for companies such as large insurance groups with a high number of direct debits (see “SEPA: Will European Firms be Ready for the Changeover?” [3]). Challenges and roadblocksThere are various challenges and roadblocks at various stages of the migration process that require additional effort to overcome. These include:– Building up the necessary SEPA expertise– Availability – or perhaps lack thereof – of the necessary

internal resources– Time lost due to asymmetrical prioritisation of the SEPA

project across the numerous specialist departments affected– Insufficient analysis of existing systems and processes,

which may be dependent on other ongoing projects– Lack of integration and testing specifications

Success factorsThe following requirements are, therefore, crucial in guaranteeing successful SEPA enablement:– Implementation of a central, hierarchical project control and

management structure (in terms of specialist, technical, organisational and budgetary factors)

– Prioritisation of SEPA project activities, including clear and rapid escalation and decision-making mechanisms in the event of conflict

– Close involvement of external partners (in particular software suppliers and banks)

28

29

PPI AG has already supported many businesses in their implementation of SEPA standards and selection of SEPA software. Thanks to its comprehensive practical experience it is able to offers clients the following skills:

Market knowledge: PPI AG has specialised in the fields of consulting, software and eBanking products for more than 25 years.

Market overview: PPI AG has broad knowledge and experience of the European conversion services market and mandate management system providers, and is therefore able to offer targeted support for your selection process.

Specific SEPA project tools: These capabilities enable PPI AG to provide clients with fast, business-specific conversion support.

Regulatory insight and understanding: PPI AG has devised interpretation aids for all unresolved SEPA-related issues and continually tracks current developments and decisions.

SEPA testing service: PPI AG offers a cost-effective SEPA testing service and permits complete end-to-end testing for SCT/SDD collectors.

4 Where can I get further help?

31

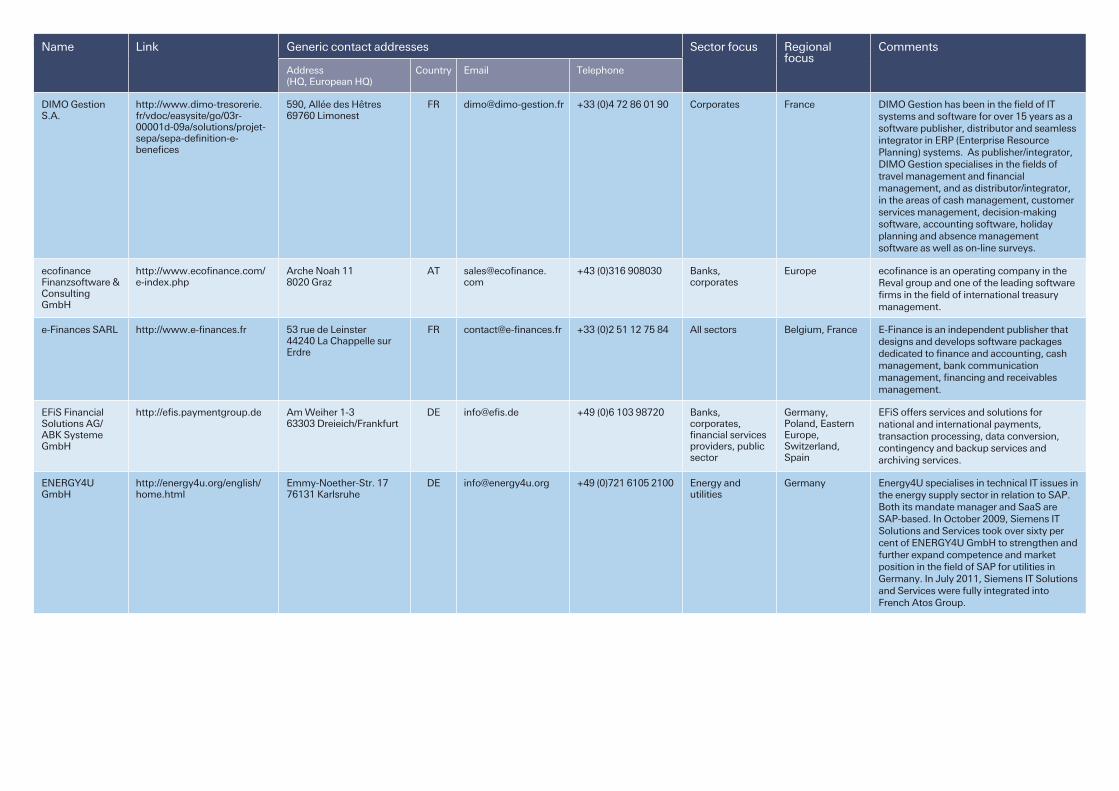

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

Adesso AG http://www.adesso.de/en/unternehmen/unternehmensprofil/index.html

Europe ATOS is an international information technology company delivering high-tech transactional services, consulting and technology services, systems integration and managed services.

Germany C1 Fin Con is a software house with a focus on software development, and IT and business consulting. It offers mandate management and SEPA conversion through its partnership with payment services provider van den Berg AG.

Capgemini Service SAS

http://www.capgemini-consulting.com

Tour Europlaza 20, avenue André Prothin 92927 Paris

+33 (0)1 49 67 3000 Consumer prod-ucts and retail; energy, utilities, chemicals; finan-cial services; life sciences; manu-facturing; public sector; telecom-munication, me-dia and entertain-ment

Europe Capgemini Consulting provides consulting, technology and outsourcing services. Capgemini offers software solutions via its partner company Clear2Pay, which supports banks and financial organizations in their provision of payment services. Software is available on Software-as-a-Service (SaaS) basis only.

France Cedricom is a developer and marketer of financial management solutions for the exchange of banking data and flow of paperless cheques. Its products include a converter for French account numbers to BIC/IBAN and CFONB formats to XML.

127 - 137 rue d’Aguesseau 92100 Boulogne Billancourt

FR [email protected] +33 (0)1 49 09 22 00 Insurance companies, healthcare and life sciences

Europe Cegedim is a global technology and services company, supplying services, technological tools, specialised software, data flow management services and databases. Cegedim has developed Cegedim Global Payments, a service dedicated to management fund flows, in particular the migration to SEPA direct debit (SDD) through a software package MA€A, available in license or Software-as-a-Service (SaaS).

5 List of SEPA consultancy firms

31

Name Link Generic contact addresses Sector focus Regional focus

Financial services providers, tele-communications, manufacturing, healthcare, gov-ernment and public utilities

Belgium, Germany, France, Ireland, Netherlands, Austria, Portugal, Spain, UK

The Canadian CGI Group took over British/Dutch service provider Logica in 2012. Its business portfolio includes management and technology consulting, systems integration, infrastructure and application management, and business process outsourcing. CGI offers a complete suite of SEPA services through CGI SEPA services.

Consolut provides advice and support in all maters connected with SAP and DCW. The company offers support for SEPA implementation within the SAP-system, including review and analysis of system requirements, customisation, review of master data, functionality tests and user training.

Computer Sciences Corporation (CSC)

http://www.csc.com 3170 Fairview Park Drive Falls Church, VA 22042

USA [email protected] +1 (703) 876 1000 All sectors Europe Computer Sciences Corporation provides consulting and information technology (IT) services to industry and government. The company provides consulting, systems design and integration, IT and business process outsourcing, applications software, and Web and application hosting. CSC’s PTDS/SEPA Systems is a standard, but customisable software with a Web front end that enables banks to get ready for SEPA, requiring minimal investment.

DE [email protected] +49 (0)40 27892 0 Insurance companies and financial services providers

Germany A software development and consultancy firm, GENEVA-ID is a provider of software to insurance companies and brokers.

Hanse Orga AG http://www.hanseorga.de/en/services/sepa-consulting/

Oldesloer Straße 63 22457 Hamburg

DE [email protected] +49 (0)40 5148080 All sectors Germany, France, Netherlands, Scandinavia

The Hanse Orga group provides specialist software solutions for financial supply chain management in SAP. Hanse Orga specialises in SAP-based solutions in the field of payment traffic, SEPA and mandate management.

Ibidem GmbH http://www.ibidem.de/leistungen/zahlungsverkehr/sepa.html

Germany Ibidem is a software and IT consulting company specialising in payment transaction solutions, financial services, messaging and enterprise application integration.

3233

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

IBM Corp. http://www.ibm.com/us/en/ 1 New Orchard RoadArmonk, NY 10504

USA [email protected] +1 (904) 499 1900 All sectors Europe IBM is a globally active US IT and consultancy firm, and a provider in the field of payment processing and securities transactions.

KPMG International Cooperative (“KPMG International”)

All sectors Europe msg systems is an international group of companies specialising in IT consultancy and solutions. It offers SEPA testing services exclusively in collaboration with a partner firm. IBAN/BIC and XML converters available on request.

Europe NEOFI Solutions is a software and IT consultancy firm specialising in data integration, cash management, SEPA and eBanking. It provides a mandate manager - a Windows application which requires Windows Microsoft Net Framework - exclusively in collaboration with a partner firm.

NTT Data Group http://emea.nttdata.com 2 Royal Exchange London, EC3V 3DG

UK [email protected] +44 (0)20 7283 8944 All sectors Europe NTT Data is a provider in the field of payments with expertise in consultancy and the implementation of service solutions involving SEPA, foreign and treasury and SWIFT payments to clients in the banking, insurance and corporate sectors.

Polinflex Solutions

http://www.polinflex.pl/servicesEU.html

30-638 Cracow Czarnogorska 3 m 7

PL [email protected] +48 (0)604 06 80 04 All sectors Europe Polinflex Solutions is a software provider and consultancy firm which does not offer SEPA solutions.

Germany, France Alongside its IT consultancy services, PPI AG also specialises in the development and production of IT solutions for credit risk management and eBanking.

Europe PwC specialises in auditing, tax advice and business/management consultancy.

3233

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

SBC Systems GmbH

http://sepa.sbc-systems.de/?tag=sbc-systems-gmbh

Taunusstraße 6 60329 Frankfurt am Main

DE [email protected] +49 (0)69 9 77 69 659 All sectors Europe SBC is a software house specialising in the development of software solutions for the payment traffic sector. It also provides consulting, coaching, IT project, software and training services.

Simplex GTP Ltd. http://www.simplexgtp.com/ First Floor 60 Gresham Street London EC2V 7BB

Europe Simplex is a European consultancy for Straight Through Processing and business process re-engineering, in both banking and securities. In 2004 Simplex launched the UK’s first independent SWIFT Service Bureau and building on this, the company created a sophisticated global transaction processing platform based on best-of-breed solutions. Simplex is a trusted global transaction platform provider and a major ‘white-label’ managed services payments provider to large global transaction banks.

DE [email protected] +49 (0)22 34 69 67 18 All sectors Germany The company specialises in SAP consultancy in the fields of accounting and risk management.

Sterci Group S.A. http://www.sterci.com/solutions/banks.html

Europe The Sterci Group is a financial messaging solutions company, providing an integrated portfolio of business solutions. Its services cover transactional banking, multi-bank connectivity, full data integration, reconciliation, cash management, zero balancing and market data management. In addition, Sterci has expertise in the replacement of legacy messaging systems, covering all major legacy platforms.

Steria Limited www.steria.com Three Cherry Trees Lane Hemel Hempstead, Hertfordshire HP2 7AH

UK [email protected] +44 (0)845 601 8877 All sectors Europe Steria provides business and IT consultancy/development and a range of individualised SEPA products and services including SEPA training, impact analysis, SEPA Cockpit for SAP, Ready4SEPA and RightTesting™ SEPA.

SWIFT Group http://www.swift.com/products_services/industry_initiatives/sepa/overview?rdct=t

+32 (2)655 31 11 All sectors Europe SWIFT is an international cooperative owned by its member financial institutions which operates a telecommunications network for the exchange of financial information for corporate clients such as banks, stock exchanges and brokers. SWIFT is also the official registration authority for the BIC and national IBAN formats.

3435

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

TESSI Technologies S.A.

http://www.tessi.fr 177 cours de la Libération 38029 Grenoble Cedex 2

The company’s product portfolio includes IT consultancy and the development of software solutions for SEPA including a converter for French account numbers to BIC/IBAN and CFONB formats to XML.

Unisys Group http://www.unisys.com 801 Lakeview Drive, Suite 100 Blue Bell, PA 19422

USA

+1 (215) 986 4011 UK +44 (0)20 7526 6100 DE +49 (0)6196 99 0

All sectors Benelux, Germany, Austria

Unisys is a global US software company with a product portfolio including outsourcing services, system integration, consulting, infrastructure and maintenance services, and IT solutions.

Europe Alongside its IT consultancy activities, XCOM AG specialises in the development of software products and IT services with its own range of eBanking, eBrokerage and eBusiness solutions.

3435

6 List of SEPA software and SEPA testing providers6.1 Contact and general information

Name Link Generic contact addresses Sector focus Regional focus

Belgium, Germany, France, Ireland, Netherlands, Switzerland, UK

ACE is a global provider of specialist payments and message processing products and solutions. Its software solution, PelicanPay, processes corporate SEPA compliant e-payments and e-collections.

Adesso AG http://www.adesso.de/en/unternehmen/unternehmensprofil/index.html

+33 (0)1 39 76 20 08 All sectors Europe ALSYON Technologies develops and provides corporate payment and banking communication management software. It offers conversion services from French account numbers to BIC/IBAN and CFONB formats to XML.

Europe ATOS is an international information technology company delivering high-tech transactional services, consulting and technology services, systems integration and managed services.

Europe Accuity, part of BankersAccuity, is a provider of data, software and services that maximise payment efficiency and facilitate compliance of transactions. Accuity focuses on banking data and its conversion and verification. The company offers solutions designed to integrate this data in existing environments and systems.

37

Name Link Generic contact addresses Sector focus Regional focus

Germany A wholly-owned subsidiary of the Federal Association of German Banks (Bundesverband deutscher Banken), Bank-Verlag GmbH provides IT systems for banks and financial services providers.

Germany C1 Fin Con is a software house with a focus on software development, and IT and business consulting. It offers mandate management and SEPA conversion through its partnership with payment services provider van den Berg AG.

Capgemini Service SAS

http://www.capgemini-consulting.com

Tour Europlaza 20, avenue André Prothin 92927 Paris

+33 (0)1 49 67 3000 Consumer prod-ucts and retail; energy, utilities, chemicals; finan-cial services; life sciences; manu-facturing; public sector; telecom-munication, me-dia and entertain-ment

Europe Capgemini Consulting provides consulting, technology and outsourcing services. Capgemini offers software solutions via its partner company Clear2Pay, which supports banks and financial organizations in their provision of payment services. Software is available on Software-as-a-Service (SaaS) basis only.

France Cedricom is a developer and marketer of financial management solutions for the exchange of banking data and flow of paperless cheques. Its products include a converter for French account numbers to BIC/IBAN and CFONB formats to XML.

127 - 137 rue d’Aguesseau 92100 Boulogne Billancourt

FR [email protected] +33 (0)1 49 09 22 00 Insurance companies, healthcare and life sciences

Europe Cegedim is a global technology and services company, supplying services, technological tools, specialised software, data flow management services and databases. Cegedim has developed Cegedim Global Payments, a service dedicated to management fund flows, in particular the migration to SEPA direct debit (SDD) through a software package MA€A, available in license or Software-as-a-Service (SaaS).

Financial services providers, tele-communications, manufacturing, healthcare, gov-ernment and public utilities

Belgium, Germany, France, Ireland, Netherlands, Austria, Portugal, Spain, UK

The Canadian CGI Group took over British/Dutch service provider Logica in 2012. Its business portfolio includes management and technology consulting, systems integration, infrastructure and application management, and business process outsourcing. CGI offers a complete suite of SEPA services through CGI SEPA services.

37

Name Link Generic contact addresses Sector focus Regional focus

Europe Clear2Pay is a payments technology company focused on the delivery of globally applicable solutions for secure, timely and streamlined payments processing. Clear2Pay’s Open Payment Framework (OPF), a library of component building blocks, offers SCT and SDD payment solutions and format conversion tools, as well as SEPA Mandate Management and SEPA implementation testing in collaboration with a partner firm.

Cogon AG http://www.cogon.de/ index.php5?Page= Std&Content=SEPA

Walther-von-Cronberg-Platz 2 60594 Frankfurt am Main

DE [email protected] +49 (0)69 247530 100 All sectors Germany, Austria, Switzerland

Cogon AG is a software company offering eBanking and cash management solutions in German-speaking countries.

CPG Finance Systems GmbH

http://www.cpg.de Landsberger Straße 110 80339 Munich

DE [email protected] +49 (0)89 68 09 70 0 Banks, public sector, insurance companies

Germany, Austria CPG Finance Systems GmbH is best known as a provider of high-quality payment solution CBPay. CBPay, which stands for Cross Border Payment, is a comprehensive solution for domestic and international cross-border payments used by financial services providers in different industries. CPG offers a number of SEPA solutions for mandate management and conversion of SCT and SDD into the DTA format to support in-house systems, such as BIC and IBAN.

Computer Sciences Corporation (CSC)

http://www.csc.com 3170 Fairview Park Drive Falls Church, VA 22042

USA [email protected] +1 (703) 876 1000 All sectors Europe Computer Sciences Corporation provides consulting and information technology (IT) services to industry and government. The company provides consulting, systems design and integration, IT and business process outsourcing, applications software, and Web and application hosting. CSC’s PTDS/SEPA Systems is a standard, but customisable software with a Web front end that enables banks to get ready for SEPA, requiring minimal investment.

+33 (0)1 44 08 80 10 Corporates France DataLog designs, develops and markets cash management software packages. These software packages are intended to ensure the dynamic and secured management of cash flows in the fields of payment pooling and cash pooling, cash reporting, intra-group payment netting, treasury management and account reconciliation.

FR [email protected] +33 (0)4 72 86 01 90 Corporates France DIMO Gestion has been in the field of IT systems and software for over 15 years as a software publisher, distributor and seamless integrator in ERP (Enterprise Resource Planning) systems. As publisher/integrator, DIMO Gestion specialises in the fields of travel management and financial management, and as distributor/integrator, in the areas of cash management, customer services management, decision-making software, accounting software, holiday planning and absence management software as well as on-line surveys.

Europe ecofinance is an operating company in the Reval group and one of the leading software firms in the field of international treasury management.

e-Finances SARL http://www.e-finances.fr 53 rue de Leinster 44240 La Chappelle sur Erdre

FR [email protected] +33 (0)2 51 12 75 84 All sectors Belgium, France E-Finance is an independent publisher that designs and develops software packages dedicated to finance and accounting, cash management, bank communication management, financing and receivables management.

EFiS Financial Solutions AG/ ABK Systeme GmbH

http://efis.paymentgroup.de Am Weiher 1-3 63303 Dreieich/Frankfurt

DE [email protected] +49 (0)6 103 98720 Banks, corporates, financial services providers, public sector

EFiS offers services and solutions for national and international payments, transaction processing, data conversion, contingency and backup services and archiving services.

Germany Energy4U specialises in technical IT issues in the energy supply sector in relation to SAP. Both its mandate manager and SaaS are SAP-based. In October 2009, Siemens IT Solutions and Services took over sixty per cent of ENERGY4U GmbH to strengthen and further expand competence and market position in the field of SAP for utilities in Germany. In July 2011, Siemens IT Solutions and Services were fully integrated into French Atos Group.

3839

Name Link Generic contact addresses Sector focus Regional focus

FR [email protected] +33 (0)1 41461002 Corporates Europe exalog is a specialist provider of Software-as-a-Service (web-based applications). The company designs, implements and operates its own solutions, with a focus on treasury management, electronic banking and e-declaration of social data. exalog solutions meet SEPA requirements, allowing its clients to carry out SEPA credit transfers (SCT) and SEPA direct debits (SDD) using exalog’s cash flow management applications and direct debits management tool.

Experian PLC http://www.experian.co.uk Experian Payments SWIFT Park Rugby CV21 1DZ

+44 (0)845 266 6602 Banks, healthcare, public sector, insurance companies

Europe Experian is a global information services company, providing data and analytical tools to clients around the world. The Group helps businesses to manage credit risk, prevent fraud, target marketing offers and automate decision making. Experian also helps individuals to check their credit report and credit score, and protect against identity theft. Experian’s IBAN and BIC validation software, or web service Bank Wizard, can check the accuracy of BBAN or IBAN and BIC details and reformat data at the point of entry, ensuring capture and processing of only valid bank account details, and only valid data is submitted for payment. For a one-off conversion, the Experian Data Conversion Service supports compliance with the latest SEPA legislation by generating IBANs from validated BBANs and adding BICs where required.

DE [email protected] + 49 (0)2408 60770 0 Banks, financial service providers, corporates and the German public sector

Germany, Luxembourg, Austria, Switzerland

GEVA is a software company specialising in the development, integration and distribution of payment transaction solutions.

4041

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

Hanse Orga AG http://www.hanseorga.de/en/services/sepa-consulting/

Oldesloer Straße 63 22457 Hamburg

DE [email protected] +49 (0)40 5148080 All sectors Germany, France, Netherlands, Scandinavia

The Hanse Orga group provides specialist software solutions for financial supply chain management in SAP. Hanse Orga specialises in SAP-based solutions in the field of payment traffic, SEPA and mandate management.

Ibidem GmbH http://www.ibidem.de/leistungen/zahlungsverkehr/sepa.html

Germany Ibidem is a software and IT consulting company specialising in payment transaction solutions, financial services, messaging and enterprise application integration.

IBM Corp. http://www.ibm.com/us/en/ 1 New Orchard RoadArmonk, NY 10504

+1 (904) 499 1900 All sectors Europe IBM is a globally active US IT and consultancy firm, and a leading provider in the field of payment processing and securities transactions.

Incentage AG www.incentage.com Mülistrasse 18 CH-8320 Fehraltorf

Germany, Luxembourg, Austria, Switzerland, Scandinavia, UK, Central and Eastern Europe

Incentage offers straight-through-processing and messaging solutions. The company provides software solutions in the fields of systems integration, project management and SWIFT integration.

Lusis S.A. http://www.lusis.com 5, Cité Rougemont 75009 Paris

France Lusis is a specialist software house providing IT solutions in the fields of payment systems, CRM, energy, communications and transport. It offers a number of converters albeit limited to certain formats/countries.

All sectors Europe msg systems is an international group of companies specialising in IT consultancy and solutions. It offers SEPA testing services exclusively in collaboration with a partner firm. IBAN/BIC and XML converters available on request.

Europe NEOFI Solutions is a software and IT consultancy firm specialising in data integration, cash management, SEPA and eBanking. It provides a mandate manager - a Windows application which requires Windows Microsoft Net Framework - exclusively in collaboration with a partner firm.

NTT Data Group http://emea.nttdata.com 2 Royal Exchange London, EC3V 3DG

UK [email protected] +44 (0) 20 7283 8944 All sectors Europe NTT Data is a provider in the field of payments with expertise in consultancy and the implementation of service solutions involving SEPA, foreign and treasury and SWIFT payments to clients in the banking, insurance and corporate sectors.

4041

Name Link Generic contact addresses Sector focus Regional focus

Germany, France Alongside its IT consultancy services, PPI AG also specialises in the development and production of IT solutions for credit risk management and eBanking.

+49 (0)6227 7 47474 All sectors Europe SAP is a provider of enterprise software and software-related services. Its areas of expertise include the development of software for all business processes, e.g. accounting, controlling, sales and marketing, purchasing, production, stock keeping and human resources. Its SEPA module is specially designed for SAP environments. Rather than special SEPA software, SAP provides a service which makes the existing SAP solution SEPA-ready.

SBC Systems GmbH

http://sepa.sbc-systems.de/?tag=sbc-systems-gmbh

Taunusstraße 6 60329 Frankfurt am Main

DE [email protected] +49 (0)69 9 77 69 659 All sectors Europe SBC is a software house specialising in the development of software solutions for the payment traffic sector. It also provides consulting, coaching, IT project, software and training services.

Sentenial Ltd http://www.sentenial.com/ Unit 16F Maynooth Business Campus Maynooth Co. Kildare

Europe Sentenial specialises in the provision of SEPA payment traffic solutions for banks and businesses. It carries out SEPA testing in conjunction with XMLDation in Ireland only.

SIA SpA http://www.sia.eu/Engine/RAServePG.php/P/267410011713

Via Gonin 36 20147 Milan

IT [email protected] +39 (0)2 60842307 Banks, corporates, public sector

Italy SIA is an infrastructure service provider and IT service business specialising in the field of payments, e-money, network services and capital markets. Its SEPA services are available as services only.

Europe Simplex is a European consultancy for Straight Through Processing and business process re-engineering, in both banking and securities. In 2004 Simplex launched the UK’s first independent SWIFT Service Bureau and building on this, the company created a sophisticated global transaction processing platform based on best-of-breed solutions. Simplex is a trusted global transaction platform provider and is the major ‘white-label’ managed services payments provider to some of the largest global transaction banks.

Sterci Group S.A. http://www.sterci.com/solutions/banks.html

Europe The Sterci Group is a financial messaging solutions company, providing an integrated portfolio of business solutions. Its services cover transactional banking, multi-bank connectivity, full data integration, reconciliation, cash management, zero balancing and market data management. In addition, Sterci has an unrivalled expertise in the replacement of legacy messaging systems, covering all major legacy platforms.

USA [email protected] +1 (800) 825 2518 Corporates Europe SunGard is an international provider of mission-critical software and IT services to virtually every segment of the financial services industry. AvantGard Payments helps streamline payments processing through data consolidation, workflow and approval routing via the Payment Factory and then facilitates connectivity for payment execution through SWIFTNet, exchanges and an online Portal for payment processing. It also complies with payment industry standards and regulations, including SEPA.

SWIFT Group http://www.swift.com/products_services/industry_initiatives/sepa/overview?rdct=t

+32 (2) 655 31 11 All sectors Europe SWIFT is an international cooperative owned by its member financial institutions which operates a telecommunications network for the exchange of financial information for corporate clients such as banks, stock exchanges and brokers. SWIFT is also the official registration authority for the BIC and national IBAN formats.

TESSI Technologies S.A.

http://www.tessi.fr 177 cours de la Libération 38029 Grenoble Cedex 2

The company’s product portfolio includes IT consultancy and the development of software solutions for SEPA including a converter for French account numbers to BIC/IBAN and CFONB formats to XML.

4243

Name Link Generic contact addresses Sector focus Regional focus

Comments

Address (HQ, European HQ)

Country Email Telephone

Unisys Group http://www.unisys.com 801 Lakeview Drive, Suite 100 Blue Bell, PA 19422

USA +1 (215) 986 4011 UK +44 (0)20 7526 6100 Germany +49 (0)6196 99 0

All sectors Benelux, Germany, Austria

Unisys is a global US software company with a product portfolio including outsourcing services, system integration, consulting, infrastructure and maintenance services, and IT solutions.

van den Berg AG http://www.vdb.de/en Im Straßer Feld 3 52134 Herzogenrath

Germany van den Berg provides software solutions for electronic payment transactions, ranging from development through sales and installation to support. Its SEPA testing services are offered exclusively in collaboration with a partner firm.

Germany V ericos provides consultancy and software development services with a focus on the insurance sector. Its product portfolio includes project management, IT architecture and IT process skills. Both its SEPA testing and hosting services are provided in collaboration with a partner firm.

Volante Technologies Ltd

http://www.volantetech.com 9 Devonshire Square London EC2M 4YF

UK Volante is a software company specialising in data management. Volante provides integration solutions for low-latency environments, service oriented architectures, vendor data consolidation, complex event processing, SWIFT message integration and other complex data challenges. Its metadata-based technology also enables enterprise data governance and model-driven initiatives. Its testing services and ASP are offered exclusively in cooperation with partner firms.

Europe Alongside its IT consultancy activities, XCOM AG specialises in the development of software products and IT services with its own range of eBanking, eBrokerage and eBusiness solutions.

XMLdation Ltd http://xmldation.com/en Kalevantie 2 33100 Tampere

GEVA Business Solutions GmbH 1 1 1 1 1 1 1 high 1 1

Hanse Orga AG 1 0 1 1 1 1 0 high 1 1

6.2 Services and solutions offering

45

Name Scope of software applies (1), does not apply (0)

Usage options applies (1), does not apply (0)

Solution maturity

Integration capability applies (1), does not apply (0)

Mandate management

IBAN/BIC converter

XML converter

Testing Sales licence SaaS ASP high medium low

Mainframe OSy

Ibidem GmbH 1 1 1 1 1 1 1 high 1 1

IBM Corp. 1 1 1 1 1 1 1 high 1 1

Incentage AG 1 1 1 1 1 1 0 high 1 1

Lusis S.A. 0 1 1 0 1 1 1 high 1 1

msg systems AG 1 0 0 1 1 0 0 high 1 1

NEOFI Solutions S.A. 1 1 1 1 1 0 1 high 0 0

NTT Data Group 1 1 1 1 0 1 1 high 1 1

Omikron Systems GmbH & Co.KG 1 1 1 1 1 1 1 high 0 1

PPI Informationstechnologie AG 0 0 1 1 1 1 1 high 1 1

Projektfabrik GmbH 1 1 1 0 1 1 1 high 1 1

SAP AG & Co.KG 1 0 1 1 1 1 1 high 1 1

SBC Systems GmbH 1 1 1 1 1 1 1 high 1 1

Sentenial Ltd 1 1 1 1 0 1 1 high 1 1

SIA SpA 1 1 1 1 0 0 1 high 1 1

Simplex GTP Ltd. 1 1 1 1 1 1 1 high 1 1

Sterci Group S.A. 0 0 1 1 1 1 1 high 0 1

SunGard Data Systems Inc. 1 1 1 1 1 1 1 high 1 1

SWIFT Group 0 1 0 1 1 0 0 high 1 1

TESSI Technologies S.A. 1 1 1 1 1 1 1 high 0 1

Unisys Group 1 1 1 1 1 1 1 high 1 1

van den Berg AG 1 1 1 1 1 1 1 high 1 1

Vericos GmbH 1 0 0 1 1 0 1 high 1 1

Volante Technologies Ltd 0 1 1 1 1 1 1 high 1 1

XCOM AG 1 1 1 1 1 1 1 high 1 1

XMLdation Ltd 0 0 1 1 0 1 0 high 0 1

47

Sales and marketing departments will need to ensure that IBANs and BICs are ready to be exchanged with customers. These codes should appear on all relevant business documents, including letterheads, invoices and delivery notes. The same applies to online sales and marketing portals, EDI processes and other electronic systems which support the sales and marketing function.

When using direct debit collections it is important to ensure that the new mandate forms are used, and that sales and marketing staff are able to assist customers in completing them.

7 Examples of SEPA impact on individual business areas

For payroll payments all personnel accounts will have to be upgraded to include the new IBAN and BIC account identifiers. Payments must be made with the corresponding Category Purpose Codes (e.g. SALA).

Sales and marketing Human Resources

Figure 13 Figure 14

Business area Modification

Customer support Systems

Processes

Data

Documents

Business area Modification

Payroll accounting Systems

Processes

Data

Documents

Affected by SEPA Not affected by SEPA

48

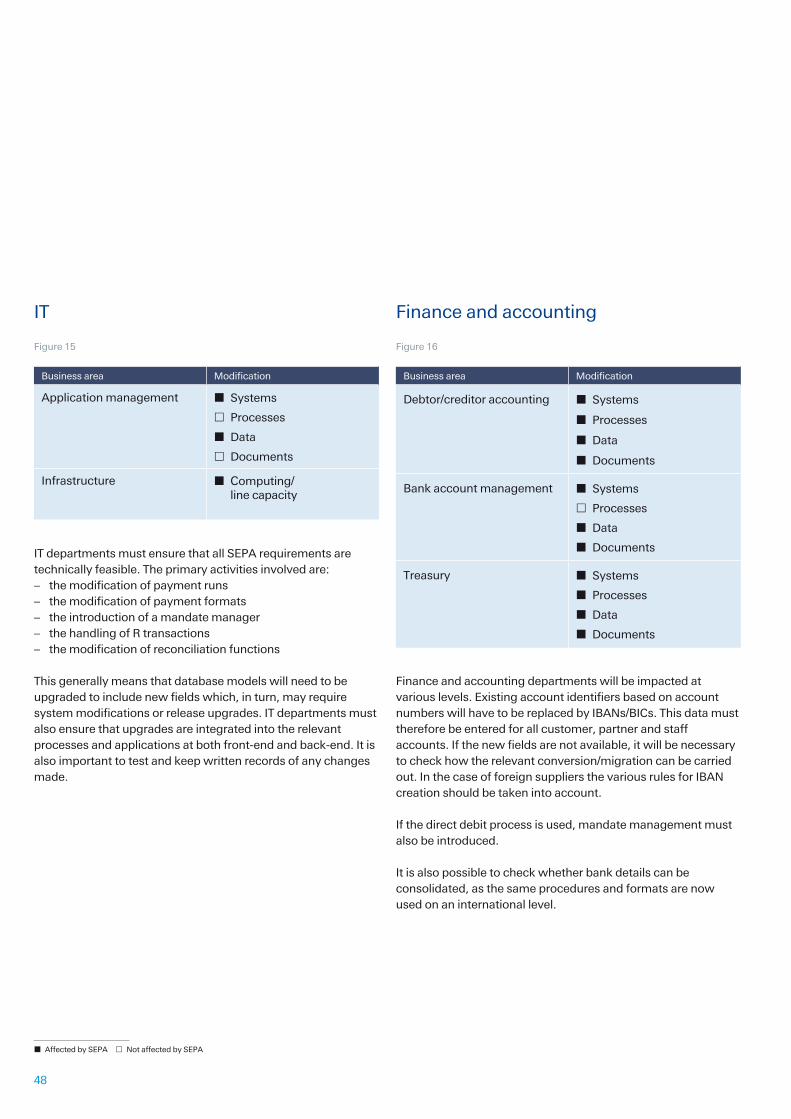

IT departments must ensure that all SEPA requirements are technically feasible. The primary activities involved are:– the modification of payment runs– the modification of payment formats– the introduction of a mandate manager– the handling of R transactions– the modification of reconciliation functions

This generally means that database models will need to be upgraded to include new fields which, in turn, may require system modifications or release upgrades. IT departments must also ensure that upgrades are integrated into the relevant processes and applications at both front-end and back-end. It is also important to test and keep written records of any changes made.

Finance and accounting departments will be impacted at various levels. Existing account identifiers based on account numbers will have to be replaced by IBANs/BICs. This data must therefore be entered for all customer, partner and staff accounts. If the new fields are not available, it will be necessary to check how the relevant conversion/migration can be carried out. In the case of foreign suppliers the various rules for IBAN creation should be taken into account.

If the direct debit process is used, mandate management must also be introduced.

It is also possible to check whether bank details can be consolidated, as the same procedures and formats are now used on an international level.

IT Finance and accounting

Figure 15 Figure 16

Business area Modification

Application management Systems

Processes

Data

Documents

Infrastructure Computing/line capacity

Business area Modification

Debtor/creditor accounting Systems

Processes

Data

Documents

Bank account management Systems

Processes

Data

Documents

Treasury Systems

Processes

Data

Documents

Affected by SEPA Not affected by SEPA

49

General service departments will need to check which master data requires modification.

Under certain circumstances it may be necessary to add IBANs and BICs to forms.

In addition to contracts affected by the direct debit process, legal and compliance departments will also need to add the new IBAN/BIC account identifiers to all contracts that contain payment/account information.

New processes sometimes contain other/new compliance risks, in relation to anti-fraud and anti-money laundering measures, for example.

General services Legal/Compliance

Figure 17 Figure 18

Business area Modification

Contract and general terms of business management

Systems

Processes

Data

Documents

Business area Modification

Purchasing Systems

Processes

Data

Documents

Real estate management Systems

Processes

Data

Documents

Travel expense management Systems

Processes

Data

Documents

Affected by SEPA Not affected by SEPA

50

It will also be necessary to check all insurance policies and update them where necessary. In addition, insurance policy debit positions will have to be modified to comply with pre-notification and submission deadlines.

A mandate management element will have to be added to the current direct debit process. It will therefore have to be possible to maintain the relevant mandate information in all systems. As a result, all processes including applications, sales, data and partner maintenance, even bank communications, will be affected.

A SEPA investment can be dealt with in the same way as any other IT investment, that is to say by asking whether the new system should be developed using internal resources (Make) or procured externally (Buy).

The Make-or-Buy decision is thus, first and foremost, a fundamental decision and a question of approach.

In addition, the decision to choose one option rather than the other should not only be based on general criteria, such as cost, quality, timeframe, availability of resources and risk, but should also take into account your IT strategy.

In the case of SEPA, and against the backdrop of the SEPA Migration End Date Regulation and its deadline of February 2014, timeframe is a particularly important criterion. For example, you may consider not converting your ERP or treasury systems to IBAN or XML immediately, but rather use an external solution for a transitional period.

Figure 20

SEPA Make-or-Buy comparison

Make Buy

– Generally easier to customise

– Developing a solution in-house builds up and retains SEPA expertise within the company (not dependent on external parties)

– Individual IT environment is so complex that third-party software is difficult to integrate

– No approval for third-party software in-house

– The functionalities of SEPA software are not unique features and will not generate more business

– The market offers appropriate solutions

– (Scarce) internal resources could be better used in the implementation/testing of the new processes and integration

– Experience shows that the effort needed to integrate a well-designed, bought-in solution is only marginally higher than what would be required to develop an in-house solution

– Provider assumes responsibility for the significant modifications to the Rulebooks expected in the first few years of operation

53

Strategic Make-or-Buy issues

Investment amountHow high is the investment amount?

EfficiencyHow efficiently can your business develop the product in comparison with a service provider? How specialised is your staff in the field of payment traffic? What expertise is the external provider offering?

FeasibilityHow easy is it to find another service provider?

Relative sourcing positionIs it easier for your business to find a service provider than it is for the competition?

Strategic impactWill your decision to make or buy increase or decrease your competitive advantage?