48

A STEP TO HAPPINESS ANNUAL REPORT ͳ 2013

A STEP TO HAPPINESS

ANNUAL REPORT 2013

01 SUPERVISORY BOARD REPORT

02 MANAGEMENT REPORT

03 IMPORTANT HIGHLIGHTS

04 SOCIAL PROJECTS

05 OUR BORROWERS

06 FUNDERS ABOUT CRYSTAL

07 FINANCIAL STATEMENTS

08 INSTITUTIONAL PROFILE

Page 1

Page 7

Page 16

Page 21

Page 23

Page 30

Page 34

Page 40

www.crystal.ge

We are pleased to report about another successful year for Crys-tal. The company grew in size and in quality allowing us to serve a greater number of clients.

“A step to happiness” became a mo o helping Crystal’s growing team to be focused on the company’s most important individuals – the clients. Our belief is that every interac on with Crystal, every loan, is a step in improving client’s life, thus contribu ng to an in-dividual happiness.

Crystal has always been a transparent company for all its stake-holders. Fairness, transparency and high quality in service provi-sion became an obvious compara ve advantage for Crystal. With-out external regulatory pressures, we realised that transparency in prices, avoiding over-indebtedness, consumer-friendly product design and use of a plain language in communica on with clients can be a game-changer and merely the right way of conduc ng a business.

For its high ins tu onal standards and strong commitment to re-sponsible lending, in August 2013 Crystal received the most es-teemed global industry recogni on - the MIX granted the company a S.T.A.R. MFI (Socially Responsible and Transparent MFI) cer fi cate naming Crystal among fi rst three S.T.A.R. MFIs worldwide.

As a socially responsible company, we have been rewarded by funders, refl ected in the volume of and condi ons for borrowing. In 2013, Crystal a racted more than USD 12.5 million of debt fi nance mainly from interna onal microfi nance investment vehicles.

SUPERVISORY BOARD REPORT

1

Last year helped us to consolidate Crystal’s organisa onal culture. The business model and the way of doing things brought tangible posi ve results in terms of client reten on, client and staff sa sfac- on levels, a rac ve pace of growth and return.

GROWTH AND EFFICIENCY

In 2013, the Georgian economy demonstrated a moderate growth of 3.2%. Nevertheless, the microfi nance sector assets grew by about 25%. The sector is represented by 62 MFIs and several com-mercial banks, which increases the level of compe on.

Meanwhile, Crystal’s gross loan por olio grew by 57% reaching USD 25.8 million. We disbursed USD 36.7 million – a 72% increase year-on-year basis. A number of ac ve loans increased by 58% reaching 27,094.

In 2013, Crystal expanded its geographic outreach by opening 6 new branches and entering 3 new regions of East Georgia. For the year end, the company operated the network of well-equipped 22 branches in Georgia’s 8 regions.

It is par cularly important that in spite of such a spacious growth, a por olio quality remained one of the best in the sector with a year-end PAR>30 of 0.5%; the ra o of restructured loans was 0.6% and the loan write-off s made 0.6%.

Last year, a reduc on of interest rates was quite apparent. This was due to the increasing compe on and historically low refi nancing rate set but the Na onal Bank of Georgia. While access to local currency fi nance remains a challenge for MFIs, Crystal managed to adjust its interest rates reducing the por olio yield by 3% to stay

2

in-tact with market trends. This could have an impact on return and profi tability, but focus on effi ciency helped the management to keep up to the profi t targets.

Effi ciency was and remains to be one of the key management ob-jec ves. In 2013, Crystal reduced the opera ng cost ra o by one percent (year-end at 21%), but developments we have ini ated are going to produce a desirable impact in the medium and long-term perspec ve. Crystal’s new strategic plan 2020 includes a vision and specifi c measures for increasing the effi ciency through a scale, be er-designed opera ons, loan offi cer and branch produc vity as well as the use of technology.

HUMAN CAPACITY A HAPPY COMPANY

Crystal is a step to happiness not only for clients, but also for its team, which grew in 2013 by 54% brining together 249 commit-ted professionals. Last year’s achievements were remarkable for ins lling the confi dence among the management and staff . Crystal managed to maintain a high mo va on environment, keeping its staff turnover rates to very low.

The emphasis on healthy life-style, adequate work hours and work-ing condi ons, internal accountability, eff ec ve communica on across the company, training and career opportuni es as well as feeling of being part of a responsible enterprise are important com-ponents of success.

Encouragement of ideas, personal freedom, openness and fairness clearly proved eff ec ve in unleashing human poten al of the com-pany. “Innova on is life” – a snap slogan by one of the senior man-agers, which can now be seen on T-shirts, electronic forums and on the cover of the in-house magazine, became a mantra for the 3

team. This indeed drives crea ve process making Crystal a dis nct company.

Crystal implemented some very important internal ins tu onal im-provements, established a training center, introduced new model of sales and distribu on, conducted internal and external client sur-veys and ini ated modernisa on of IT systems. Crystal successfully implemented a range of social projects, including Summer School, aimed at students from local universi es in order to improve pro-fessional skills and increase their employability.

Supervisory Board has been ac ve as always, providing the man-agement with clear direc on, support and oversight as well as cri -cally important freedom for fulfi lling team’s management objec- ves. There are fi ve commi ees within the Supervisory Board such

as Assets and Liabili es, Risk, Internal Audit, Social and Strategy Commi ees. In 2013, we have made a further progress in foster-ing corporate governance standards by introducing more eff ec ve performance appraisal and self-assessment process, rigorous risk management, qualita vely new planning and repor ng rou nes.

FUTURE STEPS

Crystal is set for a substan al growth due to its leadership, team and systems. We aim to increase the market share becoming a medium-size microfi nance ins tu on. This development is partly dependant on our ability to raise funds, especially in Georgian Lari. The short-term objec ves are the increase in produc vity and ef-fi ciency, development of sales teams and channels as well as par al automa on of business processes. This will ensure high-quality in services as well as adequate fi nancial and social returns.

4

A STEP TO HAPPINESS

Crystal’s Vision: To become a leading microfi nance institution in Georgia, renowned for the quality of its

service, its innovative business model, its cohesive corporate philosophy, its focus on regional development

and its commitment to social responsibility.

5

CORE VALUES OF CRYSTAL:

LOAN PORTFOLIO

In 2013 gross loan por olio of Crystal reached USD 25.8 million (GEL 44.8 million) which represents 57% annual growth. More than USD 36.7 million (GEL 61.2 million) has been disbursed during the year, which exceeds disbursements of the previous year by 72%. Number of ac ve loans made up 27,094 (58% annual growth). The total number of disbursed loans is 35,285 (69% growth).

7

MANAGEMENT REPORT

GROSS LOAN PORTFOLIO

PORTFOLIO QUALITY

Despite such a dynamic growth, por olio quality of the company remains one of the best in the sector. By the end of 2013, PAR>301

made up just 0.48%; the ra o of total restructured loans is 0.60%, whereas write-off ra o equaled to 0.60%.

The main reason of having such a stable por olio quality over the last 3-4 years is establishing strong internal control and risk man-agement systems, intensive training for fi eld staff in order to raise their qualifi ca on, focus on small loans, eff ec ve diversifi ca on of loan products and strong devo on to responsible lending stand-ards.8

1Por olio at Risk for loan delinquencies of more than 30 days

ACTIVE LOANS

9

PORTFOLIO STRUCTURE

It is noteworthy that around 65% of Company’s loan por olio is invested in rural and non-urban areas, which represent main focus and target market of Crystal.

10

LOAN PRODUCTS

Crystal off ers mul -currency loans up to GEL 50 000 ($ 30,000) for any fi nancial need and purpose of the borrower. Loans are dis-bursed for start-up and exis ng businesses, small farmers, hous-ing, educa on, household and consump on. In 2013 company dis-bursed more than 350 start-up loans.

11

Pawn shop 8.8%

Trade 17.4%

Consumer 12.5%

Service 22.4%

Agriculture 35.4%

Manufacture 3.4%

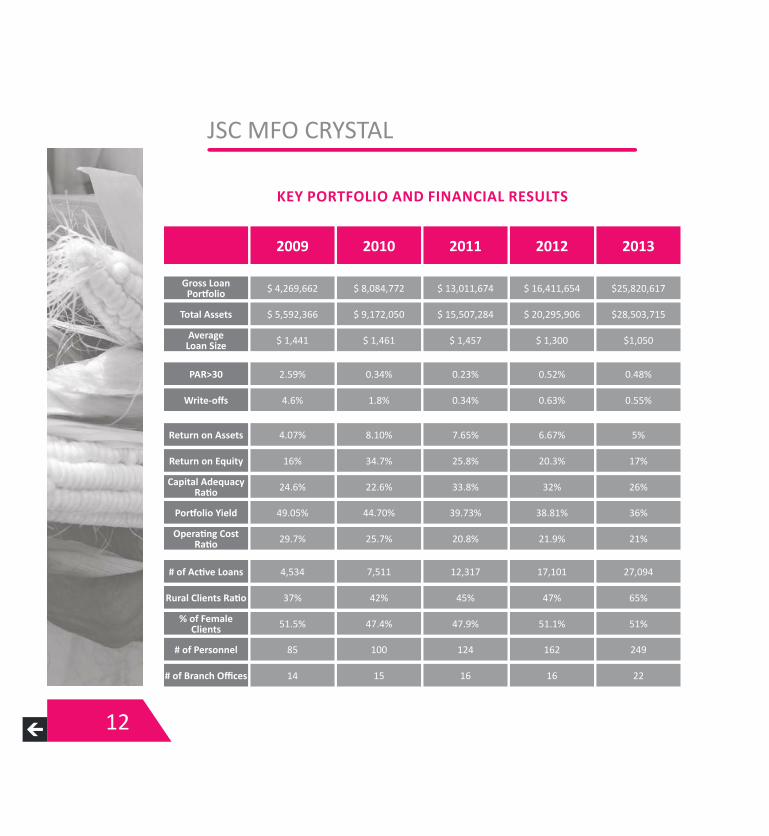

KEY PORTFOLIO AND FINANCIAL RESULTS

12

Gross Loan Por olio

Return on Assets

# of Ac ve Loans

Total Assets

Return on Equity

Rural Clients Ra o

Por olio Yield

# of Personnel

PAR>30

Average Loan Size

Capital Adequacy Ra o

% of Female Clients

Opera ng Cost Ra o

# of Branch Offi ces

Write-off s

2009

$ 4,269,662

4.07%

4,534

$ 5,592,366

16%

37%

49.05%

85

2.59%

$ 1,441

24.6%

51.5%

29.7%

14

4.6%

2010

$ 8,084,772

8.10%

7,511

$ 9,172,050

34.7%

42%

44.70%

100

0.34%

$ 1,461

22.6%

47.4%

25.7%

15

1.8%

2011

$ 13,011,674

7.65%

12,317

$ 15,507,284

25.8%

45%

39.73%

124

0.23%

$ 1,457

33.8%

47.9%

20.8%

16

0.34%

2012

$ 16,411,654

6.67%

17,101

$ 20,295,906

20.3%

47%

38.81%

162

0.52%

$ 1,300

32%

51.1%

21.9%

16

0.63%

2013

$25,820,617

5%

27,094

$28,503,715

17%

65%

36%

249

0.48%

$1,050

26%

51%

21%

22

0.55%

GEOGRAPHIC AREA

Crystal operates through a network of 22 branch offi ces located in regions and serving both rural and urban clients. Cash desks are now opera onal in all offi ces simplifying loan repayment for cli-ents, who in addi on can access currency exchange, money trans-fer, interna onal remi ance and u lity payment services. Crystal is also linked to the na onal cash kiosk networks sca ered across the country (more than 5,000 points) allowing clients to repay the loan without travelling to the branch.

13

FUNDING

2013 was successful for Crystal in terms of fundraising and a rac- on of new funding sources. During the year, Crystal managed to

obtain more than USD 12.5 million debt investment, mainly from interna onal fi nancial ins tu ons. Crystal thoroughly managed its liabili es, repaying totally 4.2 million in 2013. The chart below shows a list of Crystal’s debt funders as of December 31, 2013.

14

Commerzbank AG

KFW

DWM

MEF

responsAbility

Symbio cs

Incofi n

IFAD

Oikocredit

$1 000 000$1 800 000

$515 243

$2 000 000

$2 500 000

$3 000 000

$1 000 000$1 416 806

$2 000 000

$2 417 785

$1 000 000

$954 962$1 000 000

MCE

FUNDING SOURCES

15

Communica on with Staff : In 2013, Crystal’s team grew by as much as 54%. This process went smoothly due to the ever-evolving internal communica on and Human Resource Management systems. One of the most important elements of Crystal’s HR policy is openness in communica on and ac ve engagement with staff . It is not only about eff ec vely keeping people informed about the mission, goals and objec ves, but it is equally important to listen to and engage with the staff .

Crystal built layers of physical and electronic forums and rou nes helping to facilitate a good dialogue and eff ec ve transfer of knowl-edge across the company. This is essen al for the company with growing number of branches.

Communica on with staff provided the management with much be er feel for the market, it also helped staff to share fully the values promoted and goals set by the management. Finally, Crystal team proved to be unique source of crea ve and innova ve ideas.

16

IMPORTANT HIGHLIGHTS

Crystal started publishing quarterly staff magazine “Digest”, high-ligh ng company and individual achievements, which got very pop-ular among the staff .

Training and Development: Crystal successfully implemented sev-eral internal ins tu onal improvements, establishing a new Train-ing Centre and introducing new incen ve mechanisms for staff .

Crystal successfully implemented Summer School project, aimed to train students of economic and fi nancial courses from local univer-si es in order to improve their professional skills and provide them with greater employment opportuni es. Overwhelming majority of summer school graduates became Crystal’s employees. The project increased Crystal’s visibility and recogni on in Kutaisi, where fi rst summer school project was implemented. 17

Georgian Lari and Long-Term Financing: Crystal is diligent in protect-ing clients from assuming currency risks. Being focused on agro and MSME loans, the majority of Crystal’s clientele requires Georgian Lari loans, whereas majority of Crystal’s liabili es is in US Dollars.

Funders suppor ng Crystal through local currency funds in 2013 have been KfW, DWM and Oikocredit.

Long-term subordinated loan from KfW allowed Crystal to provide Georgian Lari loans of up to 4 year maturity to its agro-clients. It is noteworthy, that in parallel of the loan, KfW provided 3-year technical assistance package. Consul ng company Business and Finance Consul ng carried on valuable work to strengthen Crys-tal’s capacity to serve agricultural clients. BFC improved agro-loan screening procedure and provided Crystal with necessary training and technical support.

Another source of local currency fi nance is Georgian Banks: TBC Bank and Basis Bank. Crystal uses back-to-back loans to naturally hedge its foreign currency mismatch. Although, this raises the cost of borrowing subsequently aff ec ng profi tability, Crystal manage-ment is confi dent in the fairness and posi ve impact of this policy for clients.

18

Crystal’s Role in Microfi nance Sector Development: In 2013, Archil Ba-kuradze, Chairman of the Supervisory Board of Crystal, has been elected as a Chairman of the Board of the Geor-gian Microfi nance Associa on. The Associa on became ac ve in fostering be er microfi nance regula on, im-proving the visibility of the sector as well as raising performance standards of par cipa ng ins tu ons. The Associa on has adopt-ed the Code of Ethics, providing basis for protec on of consumer rights and encouraging socially responsible behavior of companies.

Malkhaz Dzadzua, CEO of Crystal was elected as the Chairman of the Associa on’s Ethics and Social Impact Commi ee. The main objec ve of the Commi ee is to promote ethical business stand-ards and responsible business conduct among its member organi-sa ons, covering about 70% of the industry.

Tamar Zamtaradze, Crystal’s Marke ng and PR Manager, was elect-ed as a Chair of the Marke ng and Public Rela ons Commi ee of the Georgian Microfi nance Associa on.

19

saqarTvelos mikrosafinanso asociacia

Association

20

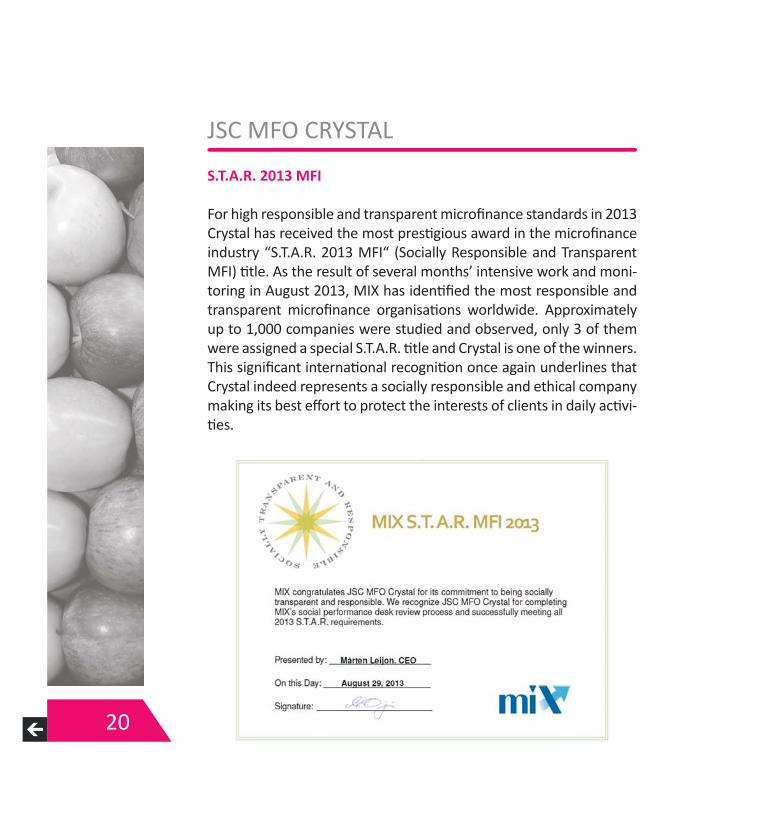

S.T.A.R. 2013 MFI

For high responsible and transparent microfi nance standards in 2013 Crystal has received the most pres gious award in the microfi nance industry “S.T.A.R. 2013 MFI“ (Socially Responsible and Transparent MFI) tle. As the result of several months’ intensive work and moni-toring in August 2013, MIX has iden fi ed the most responsible and transparent microfi nance organisa ons worldwide. Approximately up to 1,000 companies were studied and observed, only 3 of them were assigned a special S.T.A.R. tle and Crystal is one of the winners. This signifi cant interna onal recogni on once again underlines that Crystal indeed represents a socially responsible and ethical company making its best eff ort to protect the interests of clients in daily ac vi- es.

21

In 2013 Crystal con nued its ac ve involvement in social projects. These are examples of our social ac vi es:

June 1 - Celebra ng the Interna onal Children’s Day, Crystal’s branch managers gained informa on about needs of local children from so-cially vulnerable families, day centers and orphan houses and paid visits to mark this special day.

SOCIAL PROJECTS

www.crystal.ge

22

“Catharsis” - It has been 4 years since Crystal’s coopera on with In-terna onal Humanitarian Union “Catharsis” started. Crystal is spon-soring free charity dinners to elder people. In 2013, the agreement was signed according to which Crystal hosts the elder benefi ciaries of “Catharsis” with free charity dinners four mes a year.

www.crystal.ge

Thanks to the loan from Crys-tal, I managed to arrange irriga- onal system for greenhouse.

As the business went on well, I took another, larger loan; this me for improving the package

of the greenhouse. During this period I increased agricultural income: cucumber, tomato, greens produc on was added

to my nut business, and I employee two persons seasonally. At the moment I am Crystal’s third circle client and now I am thinking of changing a polyethylene tape into glass material that is more eco-nomic and environmentally friendly. Thus, thanks to Crystal’s high-quality service and wise fi nancial planning I not only managed to survive through our family’s extremely harsh economic condi ons, but also was able to start and develop my small greenhouse busi-ness.

23

OUR BORROWERS

Mr. Shota Seper ladzeOzurge , vil. Dzimi

Eliso is an internally displaced person (IDP) from Abkhazia. Having lost her husband and brother during an ethnic con-fl ict in the 90s, Eliso used to live alone in Kutaisi. Recently, she has received a small apartment through the governmental aid.

Eliso started her own micro business with GEL 2,000 loan from Crystal: she equipped a “garage” (gi ed to her by rela ves) with all necessary u li es for poultry breeding and bought 200 chickens, food and medicines. Today her business is successful enough; Eliso manages stable sales of poultry as well as eggs in the local markets. She has repaid the fi rst loan completely and is going to increase scale of her business with ongo-ing support of Crystal. Now Eliso feels to be fi nancially secured for making her long me dream come true: be an independent woman, adopt a child and become a mother.

24

Ms. Eliso LobjaniaKutaisi

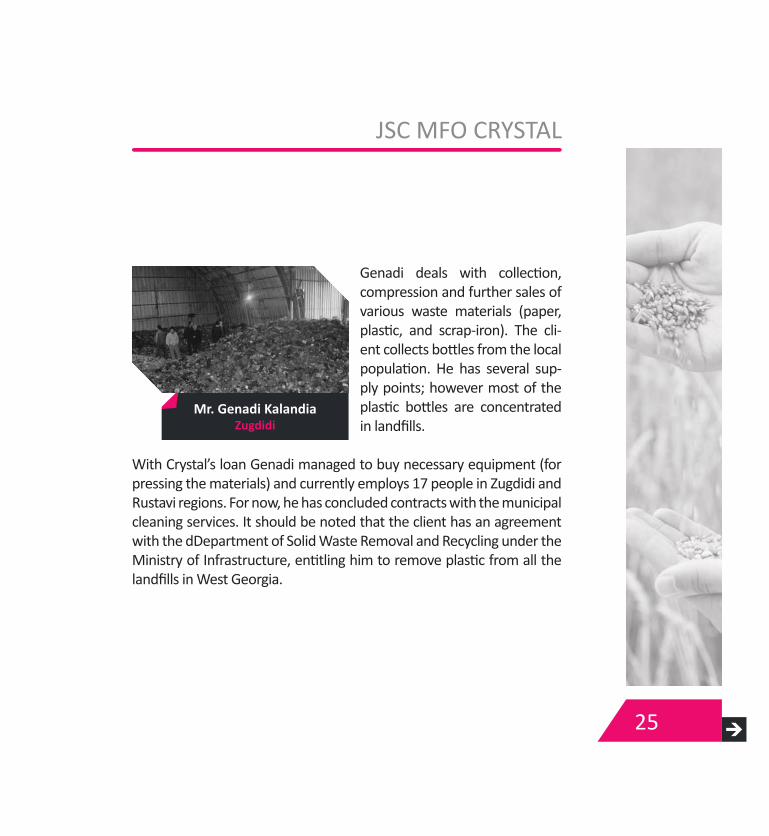

Genadi deals with collec on, compression and further sales of various waste materials (paper, plas c, and scrap-iron). The cli-ent collects bo les from the local popula on. He has several sup-ply points; however most of the plas c bo les are concentrated in landfi lls.

With Crystal’s loan Genadi managed to buy necessary equipment (for pressing the materials) and currently employs 17 people in Zugdidi and Rustavi regions. For now, he has concluded contracts with the municipal cleaning services. It should be noted that the client has an agreement with the dDepartment of Solid Waste Removal and Recycling under the Ministry of Infrastructure, en tling him to remove plas c from all the landfi lls in West Georgia.

25

Mr. Genadi KalandiaZugdidi

26

SUPERVISORY BOARD

EXECUTIVE BOARD

Clare TitcombChair of RiskCommi ee

Nikoloz LoladzeChairman of Social and

IA Commi ees

Archil BakuradzeChairman of SB and Chairman of ALCO

Aleem RemtulaChairman of Strategy

Commi ee

Malkhaz DzadzuaChief Execu ve Offi cer

David BendelianiChief Financial Offi cer

Manuchar ChitaishviliChief Administra ve

Offi cer

Kakha GabeskiriaChief Opera onal

Offi cer

27

SENIOR MANAGEMENT

Mirian Lomidze Treasurer

Sophio KhublavaChief Accountant

Vladimer ZhorzholianiIT Manager

Nikoloz GegeshidzeHead of Legal Department

Zviad ZambakhidzeLogis cs Manager

Davit Mindiashvili East Regional Manager

Nino Sebiskveradze Social Responsibility

Offi cer

Revaz Kharabadze Human Resources

ManagerKoba Mikautadze Head of Cash Desk

Khatuna Zibzibadze Non-Credit Products

Manager

Giorgi Megeneishvili Risk Manager

Paata GhvinjiliaWest Regional Manager

Svetlana Tavadze-Dundua

West-Central Regional Manager

Tamar ZamtaradzeHead of PR

and Marke ng Giorgi Phaikidze

Head of Internal Audit

28 Miranda LominadzeOzurge Branch

Manager

Mamuka Ra a Tsalenjikha Branch

Manager

Vakhtang SartaniaZugdidi-2 Branch

Manager

Levan RogavaZugdidi-1 Branch

Manager

Bakur Tsurtsumia Chkhorotsku Branch

Manager

Giorgi Nardaia Khobi Branch Manager

Vakhtang BabiluaSenaki Branch Manager

Shorena LomidzeMartvili Branch

Manager

Demna PhichkhaiaPo Branch Manager

Nino JokhadzeKutaisi 1 Branch

Manager

Otar RomanashviliLanchkhu Branch

Manager

SENIOR MANAGEMENT

29Sulkhan JorbenadzeSagarejo Branch

Manager

Nikoloz JaniashviliTsnori Branch

Manager

Artur NazarianMarneuli Branch

Manager

Zviad GiorgadzeKutaisi 2 Branch

Manager Zviad Jeladze

Vani Branch ManagerMedea ChukhuaSamtredia Branch

Manager Manana Jishkariani Khoni Branch Manager

Davit Kubuluri Kareli Branch Manager

Maka MetreveliTbilisi Branch Manager

Tedi JavakhishviliGori Branch Manager

Ekaterine GabuniaDushe Branch

Manager

SENIOR MANAGEMENT

30

FUNDERS ABOUT CRYSTAL

Developing World Markets is proud to be a supporter and provider of debt and equity fi nancing to Crystal over the past 4 years. Crystal’s solid track record of fi nancial per-formance and outreach to rural clients is a testament to the organisa on’s strong man-agement and commitment to the economic development of the people of Georgia.

Through its investments in Crystal, DWM is fulfi lling its core purpose of improving lives at the base of the world’s economic pyramid by harnessing the power of capital markets.

Bogdan Tatarchevskiy, Vice President, Rela onship Manager for EECADeveloping World Markets

At responsAbility, we consider Crystal Fund as one of our strongest partners in Georgia. The ins tu on has managed to develop sig-nifi cantly since we started to fund it in 2010 and we always have been impressed by its strong governance, processes, and commit-ment to its social mission.

31

Our rela onship with the Crystal Fund man-agement team has always been excellent and we par cularly value their transparency and responsiveness. In 2012, responsAbility provided 3 loans to the ins tu on and we are proud to support Crystal Fund’s con n-ued growth and development.”

Antoine Prédour, Investment Offi cerresponsAbility Social Investments AG

Oikocredit’s coopera on with MFO Crystal dates back to 2006, when the fi rst of several loans from Oikocredit was extended to Crys-tal based on our belief in their opera ons and mission. Crystal remains a unique MFI, based out of and focused on Western Geor-gia, with good all-round performance, also during cri cal periods.

It is a pleasure to work with this well-posi- oned MFI with suppor ve shareholders,

commi ed and professional managers and a good product range as well as an ac ve focus on further mainstreaming social objec ves into their opera ons. We are glad to have Crystal among our long term partners and look forward to con nuing this rela onship and expanding our coopera on in the future

Amber O’Connell, Microfi nance Offi cerOikocredit

32

Incofi n Investment Management started working with MFO Crystal early 2011 through its Rural Impulse Fund I (RIF). We value Crys-tals providing rural entrepreneurs in Georgia with fi nancial services; not only with credits but also FX exchange and remi ances ser-vices. Crystal has proven to be able to be fi -nancially sustainable but also working with respect for its clients, for example through transparent pricing and clear loan agree-ments. This made Crystal an ideal candidate for our RIF fund.

In 2012, with the support of FMO, we were able to co-fi nance a capacity development technical assistance project on topics includ-ing corporate governance, strategic planning and middle management strengthening. This TA project was successfully implement-ed and well received by Crystal. Hence, it was no surprise that we recently (early 2013) strengthened our frui ul rela on with Crys-tal through RIF again.

We congratulate Crystal with the results of a challenging 2012, and are confi dent Crystal has a solid base for 2013 and beyond.

Marcel Gerrits, senior investment manager Incofi n IM

33

MicroCredit Enterprises has enjoyed a strong partnership with Crystal since 2010. We have been consistently impressed with Crystal’s excellent management team and dedicated shareholders, as well as Crystal’s commit-ment to its mission of working with Georgia’s underserved, despite the challenging operat-ing environment in Western Georgia.

Crystal has always conducted itself in a trans-parent and pro-client manner, further under-scoring the organisa on’s focus on the well-being of its clients. MicroCredit Enterprises is proud to work with Crystal, and we look forward to a con nued partnership going forward.

Ayesha Wagle, Senior Vice PresidentMicroCredit Enterprises

Independent Auditors’ Report

To the Shareholders and the Execu ve BoardJSC Microfi nance Organisa on Crystal

We have audited the accompanying fi nancial statements of JSC Microfi nance Organisa on Crystal (the “Company”), which comprise the statement of fi -nancial posi on as at 31 December 2013, and the statements of profi t or loss and other comprehensive income, changes in equity and cash fl ows for the year then ended, and notes, comprising a summary of signifi cant accoun ng policies and other explanatory informa on.

Management’s Responsibility for the Financial Statements

Management is responsible for the prepara on and fair presenta on of these fi nancial statements in accordance with Interna onal Financial Repor ng Standards, and for such internal control as management determines is nec-essary to enable the prepara on of fi nancial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these fi nancial statements based on our audit. We conducted our audit in accordance with Interna onal Standards on Audi ng. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the fi nancial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the fi nancial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the fi nancial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal con-trol relevant to the en ty’s prepara on and fair presenta on of the fi nancial

34

FINANCIAL STATEMENTS

35

statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the ef-fec veness of the en ty’s internal control. An audit also includes evalua ng the appropriateness of accoun ng policies used and the reasonableness of accoun ng es mates made by management, as well as evalua ng the overall presenta on of the fi nancial statements.

We believe that the audit evidence we have obtained is suffi cient and appro-priate to provide a basis for our audit opinion.

Opinion

In our opinion, the fi nancial statements present fairly, in all material respects, the fi nancial posi on of the Company as at 31 December 2013, and its fi nan-cial performance and its cash fl ows for the year then ended in accordance with Interna onal Financial Repor ng Standards.

Emphasis of Ma er

We draw a en on to the fact that the corresponding fi gures presented, ex-cluding the adjustments described in note 3 (j) to the fi nancial statements, are based on the fi nancial statements of the Company as at and for the year ended 31 December 2012, which were audited by other auditors whose report dated 25 February 2013 expressed an unmodifi ed opinion on those statements. As part of our audit of the 2013 fi nancial statements, we have audited the adjustments described in note 3 (j) to the fi nancial statements that were applied to restate the 2012 fi nancial statements. In our opinion, such adjustments are appropriate and have been properly applied. We were not engaged to audit, review, or apply any procedures to the 2012 fi nancial statements of the Company other than with respect to the adjustments and, accordingly, we do not express an opinion or any other form of assurance on the 2012 fi nancial statements taken as a whole.

36

37

38

39

40

INSTITUTIONAL PROFILE

JSC Microfi nance Organisa on “Crystal” supports the development of micro, small businesses and agriculture in Georgia. Crystal is registered as a microfi nance organisa on at the Na onal Bank of Georgia.

The Mission of Crystal is to off er a wide range of high quality fi nancial services to micro and small entrepreneurs through-out Georgia.

The vision of Crystal is to become a leading microfi nance in-s tu on known for: quality of service, innova ve business model, cohesive corporate philosophy, focus on regional de-velopment and commitment to social responsibility.

The core values of Crystal are: Responsibility, Transparency, Access, Partnership and Professionalism.

In 1995, a group of Internally Displaced Persons from Abkhazia established IDP-focused local NGO Charity Humanitarian Centre “Abkhaze ” (CHCA). In 1998, a pilot micro-lending program with a start-up loan capital grant of $10,000 was established. Nowadays, Crystal manages up to $26 million loan por olio; $28 million total assets; $7.3 million equity capital and through the network of 22 branch offi ces serves around 27,000 ac ve borrowers in 8 regions of Georgia.

Crystal off ers a wide range of fi nancial services to its customers, including micro, agricultural, SME, educa onal and housing loans as well as currency exchange, money transfer, interna onal remit-tances and u lity payment services.

Crystal is funded by well-known interna onal fi nancial ins tu ons, such as: EBRD, KfW, Commerzbank, IFAD, responsAbility SICAV, De-veloping World Markets, MicroVest, Oikocredit, Incofi n, Symbiot-ics, Micro Credit Enterprises, Blue Orchard and other fi nancial com-panies. In October 2011, US investment bank “Developing World Markets” (DWM) became the fi rst ins tu onal investor and share-holder of Crystal.

For its high ins tu onal standards and commitment to social re-sponsibility and transparency, Crystal received several interna on-al recogni ons, including S.T.A.R. MFI 2013 status by MIX, Pla num Award (highest grade) for its social performance repor ng from MIX Market (2012); CGAP’s Financial Transparency Award (2006); in 2011 Crystal was globally recognised by the Smart Campaign for Client Protec on Principles in microfi nance industry for its “plain language loan contract”.

In December 2012 Crystal obtained “BBB” Microfi nance Ins tu- onal Ra ng Grade with “Stable” outlook by Microfi nanza ra ng

agency. This grade was 3 steps higher than to the previous ra ng (B-), which demonstrates the signifi cant improvements in govern-ance and management and organisa onal growth of Crystal.

For further informa on, please, visit www.crystal.ge 41

Short Biographies of Supervisory Board and Management

Clare Titcomb is a member of the JSC MFO Supervisory Board of Crystal and chair of the company’s Risk Commi ee. Clare has been a board member of Crystal for six years. Clare is an English solicitor and currently works as a senior associate lawyer for DLA Piper in Ukraine. Previously Clare worked for DLA Piper in Georgia where she advised on some of the leading private equity, project fi nance and capital markets deals in the region, including Georgia’s debut sovereign bond issue and fi rst corporate IPO on an interna onal stock exchange. Before joining DLA Piper, Clare spent 4 years with CMS Cameron McKenna LLP, working both in the London offi ce and with its corporate and banking departments in Central and Eastern Europe, including a 6 month client secondment to the corporate banking division of Lloyds TSB in the City of London.

Aleem Remtula is DWM’s investor nominee director on the Super-visory Board of JSC MFO Crystal. He has been on the Board of Crys-tal since DWM’s equity investment in 2011 and leads the Compa-ny’s Strategy Commi ee. Aleem has a decade of impact inves ng experience with socially responsible, double and triple bo om line venture capital and private equity funds in the U.S. and Europe. He is a Vice President on DWM’s private equity team covering Central and South Asia and the Caucasus. Aleem received his MBA from Harvard Business School and his BA in Economics and Finance from Princeton University.

42

Nikoloz Loladze is a Member of the Supervisory Board of Crys-tal. He is a social entrepreneur and development consultant with more than 10 years of experience in economic development work. Nikoloz is a founder and board member of a number of prominent business and not-for-profi t organisa ons in Georgia. In his capacity as a governance expert, Nikoloz is an advisor and board member of a number of business and not-for-profi t organisa ons, includ-ing Georgian Stock Exchange, JSC Brokerage Company Caucasus Capital Group, JSC Mobile Finance Eurasia, UK-Georgia Professional Network, Anchor Consul ng LLC, etc. In recent years he has been ac vely involved in civil society and government capacity-building ini a ves focused on be er - more transparent and accountable - Public Financial Management in Georgia. Nikoloz also frequently works as a business development consultant (corporate govern-ance, business planning, fi nancial modelling, market research) to various commercial enterprises in Georgia. Nikoloz holds postgrad-uate qualifi ca ons in Management (Warwick, UK), and Physics (Tbi-lisi, Georgia), as well as cer fi cates in Project Management, Policy Analysis, and Public Administra on.

Archil Bakuradze is the Chairman of the Supervisory Board of JSC MFO Crystal, leading the company’s Assets and Liabili es Commit-tee. Archil has been involved in Crystal’s management and govern-ance since founding it in 1998. He currently serves as Chairman of the Georgian Microfi nance Associa on. He is a Founder of JSC “Mobile Finance Eurasia”, mobile fi nance company. As part of his commitment to civil society, Archil holds non-execu ve posi ons

43

44

in the Business and Economic Centre in the Parliament of Geor-gia, Charity Humanitarian Center “Abkhaze ” and Queen Ketevan Founda on. For his contribu on to the Internally Displaced People, in 2003 he received the interna onal award from the Dutch Refu-gee Founda on (S ch ng Vluchteling). Archil Bakuradze holds a BA in Economics from the Georgian Ins tute of Sub-tropic Agriculture and MBA degree from the Lancaster University. He is UK FCO Ch-evening scholar and a fellow of the John Smith Memorial Trust.

Malkhaz Dzadzua has been Chief Execu ve Offi cer (CEO) of Crys-tal since its establishment. He has extensive experience in micro-fi nance, fund raising, strategic and opera onal management. He began his career in 1995 as a volunteer with a local NGO in Kutaisi, Georgia. Since 1997 he has been ac vely involved in microfi nance, star ng as a loan offi cer and then progressing to more senior po-si ons. In 2005-2007 he worked as fi rst elected Chairman of the Supervisory Board of the Georgian MFI Associa on.

Kakha Gabeskiria has been Chief Opera ng Offi cer (COO) of Crys-tal since August 2009. Kakha brings vigorous knowledge of micro-fi nance sector and a decade of credit management experience. Formerly, leading Procreditbank’s credit opera ons in key loca ons of West Georgia, Kakha has acquired immense experience of port-folio growth and credit management. He hold a Bachelor’s degree in Economics from the Georgia University of Sub-tropic Agriculture. Kakha par cipated in various courses on microfi nance manage-ment. His career in microfi nance started with the role of a loan offi cer in Crystal (CHCA Micro-lending Program) back in year 2000.

David Bendeliani is Chief Financial Offi cer (CFO) of JSC MFO Crys-tal. He was the Financial Manager of CHCA from 1997. He has been head of Crystal’s fi nancial department from its establishment. He currently manages the fi nance staff of Crystal, coordina ng ac-coun ng, fi nancial control, planning, budge ng, assets and liability management, tax management, repor ng and rela onship with banks and fi nancial ins tu ons. He holds a degree in Accoun ng and Financial Analysis from the Tbilisi State University. David was a lecturer of Financial Accoun ng and Audit in the Georgian Univer-sity of Sub-tropic Agriculture from 1995 ll 2005.

Manuchar Chitaishvili has served as Chief Administra ve Offi cer from October 2012. Since 2006 he worked as Head of Internal Au-dit Department. Currently he reports to the Supervisory Board. He is the lawyer by educa on (Kutaisi State University) and holds a Masters Degree in Public Administra on from Georgian Ins tute of Public Aff airs. Manuchar took part in microfi nance management and internal audit courses in Kazakhstan and Greece. In the past he worked in the Georgia Young Lawyers Associa on as a coordina-tor of legal projects before working as Head of Staff for the Kutaisi Mayor’s Offi ce. Manuchar has worked as a Lecturer of Jurispru-dence in the Kutaisi State University.

45

JSC MFO “CRYSTAL”72 Queen Tamar StreetKutaisi, 4600, GeorgiaTel: +995 431 253 343

www.crystal.ge