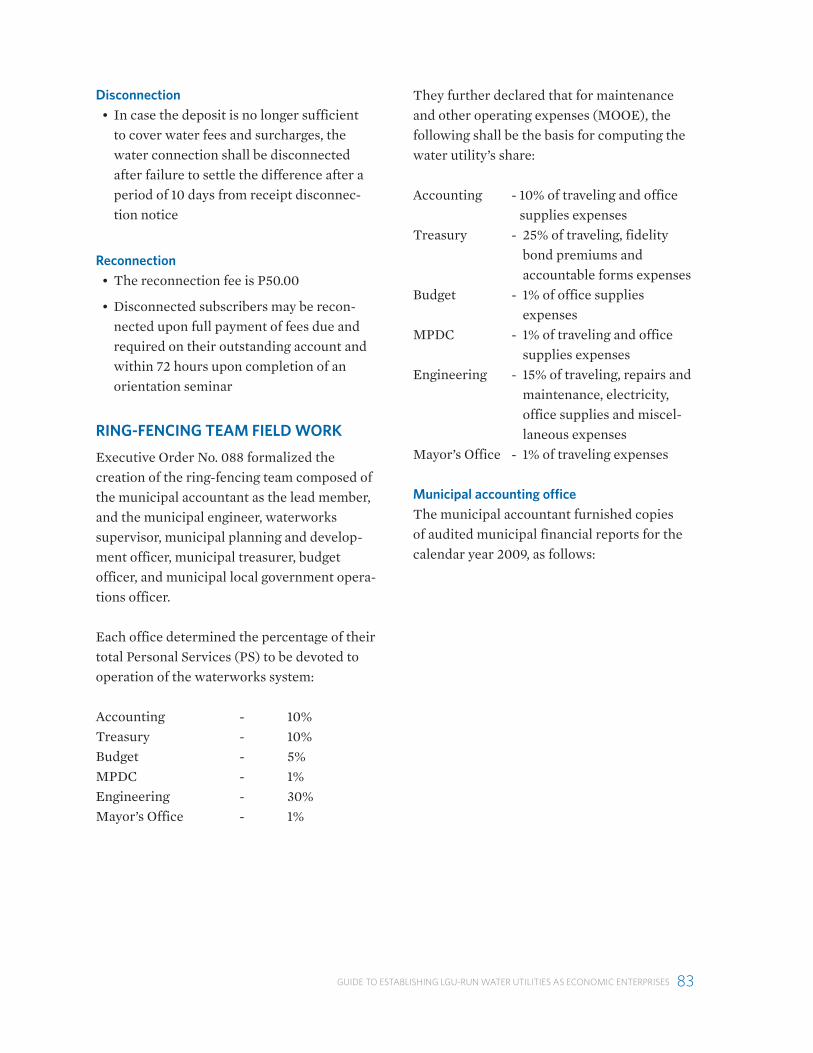

129

About Philippine Water Revolving Fund (PWRF) Support Program

The PWRF Support Program (PWRF-SP) is a collaborative undertaking of Government of the Philippines partners, USAID, Japan International Cooperation Agency (JICA), LGU Guarantee Corporation (LGUGC), and private financing institutions (PFIs) through the Bankers Association of the Philippines. The Program’s GOP partners are led by the Department of Finance and the Development Bank of the Philippines.

The PWRF Support Program operates around the following main objectives:• Establish the co-financing facility and develop a long-term financing strategy and mechanism with broader private sector participation;• Strengthen water project financing and enable other conditions necessary for optimizing PWRF-SP’s positive impact on the sector, including

corollary regulatory reforms; • Assist water districts and local government units in developing a pipeline of bankable water projects; and• Assist water districts and local government units with reforms in utility governance.

The PWRF Support Program has established a co-financing facility that combines ODA/JICA resources with PFI funds for creditworthy water service providers, using a financial structure that allows affordable loan terms without sacrificing the viability of PFIs. PFIs have access to credit risk guarantees provided by LGUGC and USAID’s Development Credit Authority. PWRF-SP has also assisted in financing policy formulation, regulatory reform, project development and capacity building of water utilities to improve management and operations.

PWRF-SP has actively supported utility reform initiatives, such as the ring-fencing of LGU and cooperative-run utilities. Together the PWRF-SP, Water and Sanitation Project (WSP) of World Bank, Department of Interior and Local Government (DILG) and Cooperative Development Authority (CDA) collaborated on developing knowledge products and helping build capacity of LGUs and cooperatives in ring-fencing of water utility accounts and operations.

The PWRF Support Program is implemented by Development Alternatives, Inc. in association with The Community Group International LLC, Resource Mobilization Advisors, and CEST, Inc.

Guide to Establishing LGU-Run Water

This guide was published with assistance from the USAID Philippine Water Revolving Fund (PWRF) Support Program. The views expressed here do not necessarily reflect those of USAID or the United States Government.

Utilities as Economic Enterprises

Acknowledgements

The PWRF Support Program thanks the Water and Sanitation Program (WSP) of the World Bank and the Public-Private Infrastructure Advisory Facility (PPIAF) for allowing use of the Guide to Ring-Fencing of Local Government-Run Water Utilities prepared by the Small Water Utilities Improvement and Financing (SWIF) Project in the development of this guide. In particular, Chapters 2 and 3 of this Guide are quoted directly from the Guide to Ring-Fencing, which discusses the critical first step—that of segregating the water utility accounts—in the establishment of a discrete economic enterprise for a LGU-run water utility. Thus the two guidebooks are complementary and provide a uniform approach for completing the process of establishing a utility distinct from the overall LGU operation, accountable for its performance and has disposition of its funds.

This Guide benefited from a peer review by accountants and finance specialists from the municipalities of Jagna, Alburquerque and Antequera in the province of Bohol; and from local resource institutes: Ateneo de Naga University Center for Local Governance, Batangas State University, Catanduanes State Colleges, UP Los Baños College of Public Affairs, Father Saturnino Urios University, GenTwoFifteen Development Foundation Inc., Holy Name University Center for Local Governance, University of Northern Philippines, the Local Government Academy, and WSP.

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAMvi

viiGUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

contents

Abbreviations and Acronyms 1

1. Developing the Guide 3

1.1 Ring-fencing approach 4

1.2 Ring-fencing towards corporatization 5

1.3 Ring-fencing pilot experiences 5

1.4 Organization of the guide 7

2. Accounts Reconstruction 9

2.1 Preparatory activities 9

2.2 Steps in the Accounts Reconstruction 12

3. Maintenance of ring-fenced books of accounts 35

3.1 Parallel books 35

3.2 Bookkeeping 36

3.3 System of allocating shared expenses 37

3.4 Accounting and financial reporting system 37

3.5 Monitoring and evaluation 40

4. Evaluation of Water Utility Performance 41

4.1 Benchmarking key performance indicators 41

4.2 Conference with local officials 44

4.3 Strategic business planning 45

5. Financial Management Guidelines for the Utility 47

5.1 Formulation 47

5.2 Review 55

5.3 Institutionalization 55

5.4 Implementation 57

6. Separate Bank Account for the Utility 59

6.1 Rationale 59

6.2 Authority 59

6.3 Cashbook 59

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAMviii

7. Separate Budget for the Utility 63

7.1 Budget preparation 63

7.2 Budget authorization 65

7.3 Budget review 65

7.4 Budget execution 65

7.5 Budget accountability 65

8. LGU-Run Water Utility as Economic Enterprise 71

8.1 Corporatization 71

8.2 Creation of a water utility economic enterprise 71

8.3 Restructuring the water utility’s organization 74

8.4 Zero-subsidy and/or positive surplus 76

8.5 Performance contracting 77

Appendix 1 79

Appendix 2 101

Appendix 3 117

List of Boxes

Box 1. Testimonies of local chief executives of pilot LGUs 7

Box 2. Books of accounts and chart of accounts under the ring-fencing system

and the NGAS 35

Box 3. Subsidiary ledgers for major controlling accounts in the general ledger 38

Box 4. Key performance indicators and formulas 43

Box 5. Pro-forma for water utility operation budget proposal 63

Box 6. Important dates in the local planning budget calendar 64

List of Exhibits

Exhibit 1. Benchmarking results for water utilities in small towns 3

Exhibit 2. Comparative analysis of performance of ring-fenced

water utilities for 2008–2009 6

Exhibit 3. Executive order creating a ring-fencing team 10

Exhibit 4. Inventory count sheet 13

Exhibit 5.1 Useful lives of tangible assets that may be considered part of inventory 21

Exhibit 5.2. Estimated useful lives of property, plant and equipment 23

Exhibit 6. Schedule of aging of receivables 26

Exhibit 7. Sample ring-fencing financial management guidelines 50

Exhibit 8. SB resolution adopting the financial management guidelines 56

Exhibit 9. Cashbook - Cash in Bank 60

ixGUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Exhibit 10. Cashbook - Cash in Treasury 61

Exhibit 11. Quarterly report of income 67

Exhibit 12. Quarterly financial report of operations 68

Exhibit 13. Quarterly physical report of operations 69

Exhibit 14. Statement of receipts and expenditures 70

List of Figures

Figure 1. Water utility economic enterprise program 5

Figure 2. Discussion points in conference with local officials 44

Figure 3. FMG review and adoption process 57

Figure 4. Organization chart of a typical LGU-run water utility 76

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAMx

1GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

ADCOM Additional compensationAIP Annual Investment PlanAve AverageBOM Budget Operations ManualCO Capital outlayCoops CooperativesDILG Department of the Interior

and Local GovernmentECC Employees compensation

contributionFF Furniture and fixturesFMG Financial management

guidelinesGFI Government financing

institutionsIEC Information, education and

communicationIRA Internal Revenue AllotmentJEV Journal entry voucherKPI Key performance indicatorsLCE Local Chief ExecutiveLDC Local Development CouncilLDIP Local Development

Investment PlanLFC Local Finance CommitteeLGC Local Government CodeLGOO Local Government Operations

OfficerLGU Local government unitLPDC Local Planning and

Development OfficerLWUA Local Water Utilities

AdministrationMandE Monitoring and evaluation

MDFO Municipal Development Fund Office

MOOE Maintenance and other operating expenses

MPC Multipurpose cooperativeNGAS New Government Accounting

SystemNRW Non-revenue waterNWRB National Water Resources

BoardOandM Operations and maintenanceOME Other machineries and

equipmentOR Official receiptsPERA Personal Expenses Relief

Allowance PFI Private financing institutionsPGB Policy Governing BodyPI Public infrastructuresPS Personal servicesPWRF-SP Philippine Water Revolving

Fund Support ProgramRA Representation allowanceRWSAs Rural Waterworks Systems

AssociationsSB Sangguniang BayanTA Transportation allowanceUSAID United States Agency for

International DevelopmentWATSAN Water and sanitationWD Water districtsWSP Water and Sanitation ProgramWSPs Water service providers

Abbreviations and Acronyms

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM2

3

SECTION ONE

Many local government units provide water supply services as part of their

regular operations. This means the budget for operating the water utility is included in the LGU’s overall budget, and all revenue from providing water services go to the general fund. Tasks involving water supply services are often added on to the regular workload of the local engineer, accountant, or treasurer. Since accounts are not ring-fenced and the water supply function is not governed as a sustainable entity, the performance of the water utility is generally poor and service coverage is inadequate.

One way to address this concern is to improve the governance system of LGU-run utilities to compel as well as empower them to become accountable for their performance, budget disposition, and revenues generated. The Local Government Code (LGC) already provides the enabling mechanism; short of creating an autonomous corporation, LGUs can establish economic enterprises that operate on commer-cial principles to generate revenues adequate to sustain their operations and, ultimately, invest-ment needs. Economic enterprises are allowed to maintain separate accounts and dedicated personnel.

Exhibit 1. Benchmarking results for water utilities in small towns

KPI/utility modelIdeal/

industrystandard

Benchmarking results

LGURWSAs/

CoopsWD Private Ave

Sample size 10 9 18 8 45

Coverage (%) 100 57 66 69 66 65

Availability (hours) 24 18 20 23 22 21

Consumption (lpcd) >100 96 127 120 144 120

NRW (%) 20 36 16 26 26 29

Operating ratio < 1 1.18 0.87 0.70 0.74 0.85

Accounts receivable (months) < 1 2.3 2.6 1.3 1.7 1.8

Average tariff (P/m3) - 7.22 7.99 17.82 15.37 13.06

Collection efficiency (%) 98 91 99 99 102 98

Staff/1000 connections 4 9 6.6 6.8 5.8 7.0

Source: Philippines Towns Water Utilities Databook 2004 published in December 2006 by WSP

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM4

The process of establishing a water utility as an economic enterprise starts with the critical step of segregating utility accounts. In this regard, the Guide to Ring-Fencing of Local Government-Run Water Utilities developed in 2009 by the Water and Sanitation Program of The World Bank will be a very useful reference. It initially addresses account-ing issues, particularly regarding income recognition and subsidy level determina-tion. It provides a uniform approach to the reconstruction of water utility accounts, maintenance of parallel books of accounts and separate records, and preparation of periodic ring-fenced financial reports. The Guide to Ring-Fencing will be helpful to LGUs in gener-ating the following outputs: beginning ledger balances, reconstructed financial statements, and separate books of accounts.

However, the end-goal of ring-fencing is establishing a public utility and economic enterprise that has its own budget, fund management system, management policies and human resource policies. Picking up from where the WB Guide to Ring-Fencing leaves off, this Guide covers the remaining steps and requirements prescribed by the LGC and other government regulations in establishing an economic enterprise that

operates as a business concern. On 4 May 2011, the Department of the Interior and Local Government (DILG) issued Memorandum Circular (MC) 2011-65 encouraging LGUs to adopt ring-fencing as a mechanism to improve the performance of LGU-run water utilities and to pursue utility reform. It cites these two complementary Guidebooks as key reference materials. MC 2011-65 is shown in Appendix 3.

1.1 RING-FENCING APPROACH

Ring-fencing is a financial and management arrangement whereby activities and financial accounts associated with a particular business are fenced off from the general accounts of the entity. This approach can be particularly helpful to LGUs because the financial informa-tion and records of the LGU-run water utility are merged with the general fund account of the LGU.

Ring fencing of LGU-run water utilities essen-tially involves identifying and isolating the utility’s activities, assets, costs and revenues, and obligations for goods and services; transforming the water utility into a viable and sustainable public utility and economic enterprise; and utilizing the utility’s resources primarily for operations and maintenance, as well as capital investments.

The need to ring-fence LGU-run water utilities became apparent from results of the

benchmarking survey done by WSP Philippines together with NWRB, DILG, and LWUA.

Data gathered from 45 water utilities revealed that LGU-run water utilities were the poorest

performers among water service providers in terms of financial and operational performance.

They posted the (a) lowest average service coverage; (b) lowest water availability per day; (c)

least amount of water delivered to consumers; (d) lowest average tariff per cubic meter; (e)

lowest revenue collection efficiency; (f) highest average operating ratio; (g) highest staff/1000

connections ratio; and (h) very low capital per expenditure connection.

5GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

1.2 RING-FENCING TOWARDS CORPORATIZATION

Corporatization, as used in this Guide, refers to an LGU-run water utility that is ring-fenced and practices corporate governance and commercial principles in running the utility as a business. It involves a situation where the water utility attains viable and self-sustaining operations without the need for LGU subsidies. Corporatization describes a water utility that has been established as an economic enterprise thus generating revenues that can sufficiently finance its operations and maintenance costs and capital investments. Should it generate excess revenues, these can be plowed back to the LGU general fund. This is the goal of ring-fencing.

The ring-fencing of the water utility opera-tions consists of two (2) phases. Phase 1, known as the Accounts Reconstruction Phase,

Figure 1. Water utility economic enterprise program

Full ring-fencing

At least 12 months after accounts reconstruction

Ring-fencing transition period activities:• Parallel books of accounts

maintained• Revenues recorded when realized• All costs accounted for, including

shared costs• Separate record of property, plant

and equipment• Periodic ring-fenced financial

reports prepared • Financial management guidelines

implemented*• Separate bank account

established*• Separate budget prepared*• Business plan prepared*

*Needs local Sanggunian Resolution

Full-blown economic enterprise

Water utility operating as a self-sustaining public utility and economic enterprise

• Retains excess income for operations and improvements

• Implements performance contracting

Accounts reconstruction

Within 3 months

Reconstruction of water utility accounts

Income statement adjusted based on accrual and full costing

Balance sheet beginning balances set-up

involves the preparatory activities for ring-fencing and the reconstruction of water utility accounts. It also involves the maintenance of books parallel to the LGU General Fund accounts, the preparation of periodic financial reports, the formulation and implementa-tion of financial management guidelines, the opening of a separate bank account, provision of a separate budget, and the preparation of the business plan for the water utility. This process will take approximately 18 months depending on the capacity of the utility and the commitment of the LGU. See Figure 1 above for details of activities in Phase 1 and Phase 2.

1.3 RING-FENCING PILOT EXPERIENCES

The PWRF-SP implemented a technical assis-tance program that included training on ring-fencing, the pilot testing of accounts recon-struction in selected LGUs and multipurpose

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM6

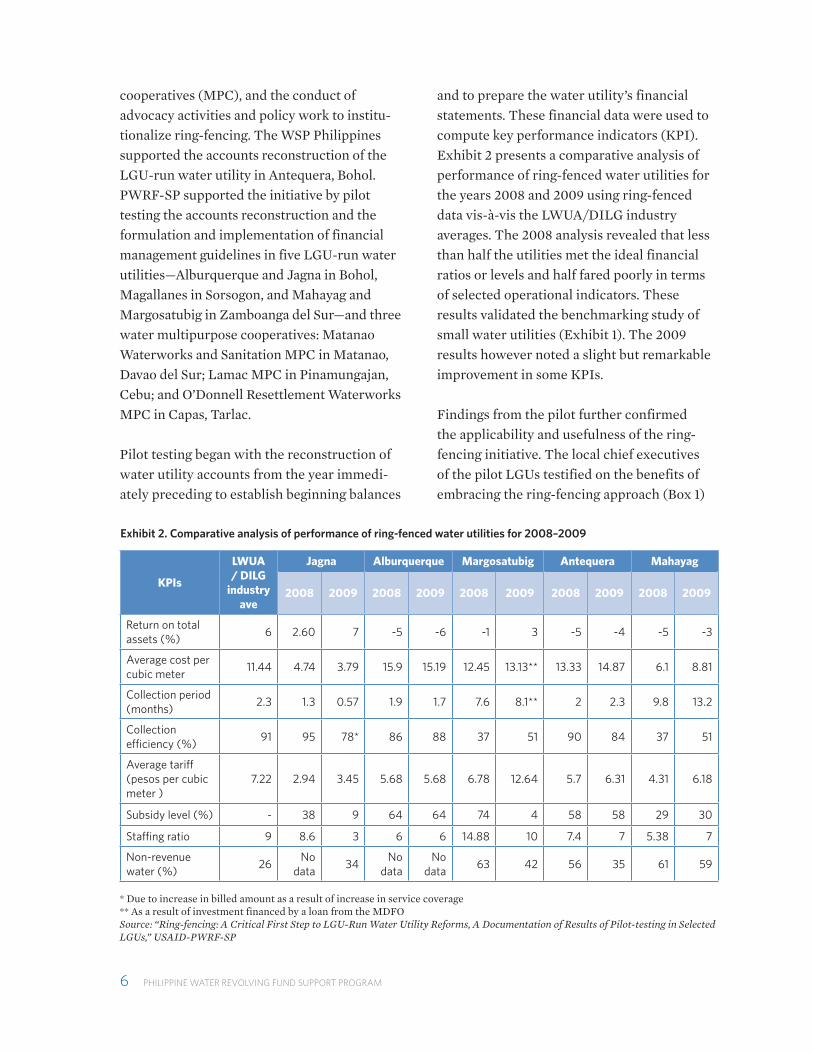

cooperatives (MPC), and the conduct of advocacy activities and policy work to institu-tionalize ring-fencing. The WSP Philippines supported the accounts reconstruction of the LGU-run water utility in Antequera, Bohol. PWRF-SP supported the initiative by pilot testing the accounts reconstruction and the formulation and implementation of financial management guidelines in five LGU-run water utilities—Alburquerque and Jagna in Bohol, Magallanes in Sorsogon, and Mahayag and Margosatubig in Zamboanga del Sur—and three water multipurpose cooperatives: Matanao Waterworks and Sanitation MPC in Matanao, Davao del Sur; Lamac MPC in Pinamungajan, Cebu; and O’Donnell Resettlement Waterworks MPC in Capas, Tarlac.

Pilot testing began with the reconstruction of water utility accounts from the year immedi-ately preceding to establish beginning balances

Exhibit 2. Comparative analysis of performance of ring-fenced water utilities for 2008–2009

and to prepare the water utility’s financial statements. These financial data were used to compute key performance indicators (KPI). Exhibit 2 presents a comparative analysis of performance of ring-fenced water utilities for the years 2008 and 2009 using ring-fenced data vis-à-vis the LWUA/DILG industry averages. The 2008 analysis revealed that less than half the utilities met the ideal financial ratios or levels and half fared poorly in terms of selected operational indicators. These results validated the benchmarking study of small water utilities (Exhibit 1). The 2009 results however noted a slight but remarkable improvement in some KPIs.

Findings from the pilot further confirmed the applicability and usefulness of the ring-fencing initiative. The local chief executives of the pilot LGUs testified on the benefits of embracing the ring-fencing approach (Box 1)

KPIs

LWUA / DILG

industry ave

Jagna Alburquerque Margosatubig Antequera Mahayag

2008 2009 2008 2009 2008 2009 2008 2009 2008 2009

Return on total assets (%)

6 2.60 7 -5 -6 -1 3 -5 -4 -5 -3

Average cost per cubic meter

11.44 4.74 3.79 15.9 15.19 12.45 13.13** 13.33 14.87 6.1 8.81

Collection period (months)

2.3 1.3 0.57 1.9 1.7 7.6 8.1** 2 2.3 9.8 13.2

Collection efficiency (%)

91 95 78* 86 88 37 51 90 84 37 51

Average tariff (pesos per cubic meter )

7.22 2.94 3.45 5.68 5.68 6.78 12.64 5.7 6.31 4.31 6.18

Subsidy level (%) - 38 9 64 64 74 4 58 58 29 30

Staffing ratio 9 8.6 3 6 6 14.88 10 7.4 7 5.38 7

Non-revenue water (%)

26No

data34

No data

No data

63 42 56 35 61 59

* Due to increase in billed amount as a result of increase in service coverage** As a result of investment financed by a loan from the MDFOSource: “Ring-fencing: A Critical First Step to LGU-Run Water Utility Reforms, A Documentation of Results of Pilot-testing in Selected LGUs,” USAID-PWRF-SP

7GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

in their respective water utilities. The pilot test also revealed areas for improvement as follows:1. Large amounts of collectibles were noted

but not reported in the LGU’s financial statements. Water revenues are booked only when bills are actually collected. As a result, unpaid water bills are not monitored and the aging of receivables is often left undone.

2. Utilities are highly dependent on the Internal Revenue Allotment, and their capital and OandM expenses are highly subsidized. Among the pilot LGUs, the estimated annual subsidy ranges from P735,000 to P3.75 million.

3. Budgeted funds of water utilities are commingled with those of other economic enterprises such as public markets, terminals, and cemeteries. This makes the tracking of financial and budgetary perfor-mance difficult.

4. There are not enough trained staff to provide customer service and to keep track of the individual customer accounts. This may be due to high staff turnover rate brought about by frequent changes in the administration and highly politicized hiring and firing policies. When the utility is attached to one of the LGU offices, staff members have multiple tasks and the responsibility of handling water utility records and accounts becomes second priority.

5. There are no written financial and opera-tional policies. Personnel are not properly supervised. No one directs the operations of the water utility.

6. Political interference, usually in the form of personnel accommodations or condonation of payments, contributes to inefficiencies.

Box 1. Testimonies of local chief executives of pilot LGUs

Honorable Mayor Exuperio Lloren of Jagna pointed out that ring-fencing enabled them “to gauge the viability of our water utility and determine proper actions to enhance our service delivery.”

Hon. Mayor Abelardo Arambulo of Magallanes stated that ring-fencing showed the many things that still need to be done to enhance water service operations in their locality. He said that the ring-fencing “has made it easier for us to determine the appropriate level of tariff.”

Hon. Mayor Cirilo Jalad of Alburquerque acknowledged that findings from the ring-fencing pilot have helped them identify a plan of action to improve their waterworks operation.

Hon. Mayor George Minor of Margosatubig said that “ring-fencing the waterworks accounts made it easier for us to monitor and track the financial performance of our utility. It opened our eyes to unnecessary subsidies that we are providing.”

Hon. Mayor Paulino Fanilag of Mahayag realized that their collection plan was inefficient and the subsidy appropriated to operate the utility was immense.

Hon. Mayor Cecelia Rebosura of Antequera, indicated that, after ring-fencing, they realigned their waterworks organization and undertook reforms, such as increasing the tariff.

Source: “Proceedings of the Workshop on Ring-fencing of Water Utility Accounts,” USAID-PWRF-SP, October 2009

1.4 ORGANIZATION OF THE GUIDE

This Guide aims to provide a uniform approach for LGU-run water utilities in executing the remaining steps and processes after successful reconstruction of water utility accounts and maintenance of separate books of accounts to achieve the goal of ring-fencing.

Specifically, the Guide• Takes off at the completion of Accounts

Reconstruction and maintenance of parallel books of accounts

• Expounds on steps and procedures in the conduct of activities at the transi-tion stage: formulation and adoption of

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM8

financial management guidelines, opening of separate bank account, preparation of separate budget, and maintenance of parallel books of accounts

• Clarifies guidelines and processes for the water utility to reach “corporatization,” or the establishment of the water utility as a sustainable economic enterprise

• Provides set of sample problems and suggested solutions to simulate the Accounts Reconstruction and other activities

To provide a better grasp of the whole ring-fencing system, this Guide is organized based on the water utility economic enterprise program. Following the phases of ring-fencing, the eight sections contained in this guide are:

Section 1 Developing the guideTaking into consideration the pilot testing experiences, the ring-fencing approach moves forward from accounts reconstruction to estab-lishing the water utility as an economic enter-prise. This section showcases the foundation of the ring-fencing concept and the eventual development of the complementary guide.

Section 2 Accounts reconstructionThis section reviews the step-by-step approaches in reconstructing the water utility accounts that have merged with the General Fund account of the LGU. Examples culled from suggested solutions (Appendix 2) are provided for each significant step.

Section 3 Maintenance of ring-fenced books of accountsThis section expounds on the systems and processes necessary to fully implement ring-fencing of water utility accounts. A detailed discussion focuses on the maintenance of

ring-fenced accounts alongside the LGU’s General Fund books of accounts.

Section 4 Evaluation of water utility performanceBenchmarking is considered in this section. It presents financial and operational analyses with relevant input on the decision making process.

Section 5 Financial management guidelines for the utilityThis section illustrates the formulation of financial management guidelines for the water utility as a separate economic entity. It discusses in detail important processes for instituting the financial management policy.

Section 6 Setting up a separate bank account This section focuses on setting up a separate bank account for water utility funds. It discusses how maintaining a separate bank account is essential to transforming the water utility into a viable, bankable and sustainable economic enterprise.

Section 7 A separate budget for the utilityOne internal control measure is the main-tenance of a separate budget. This section presents important considerations in preparing a separate budget for the water utility.

Section 8 A public utility and economic enterpriseThis section provides guidelines on the estab-lishment of the water utility as a public utility and economic enterprise. It suggests uniform approaches and highlights conditions in the establishment of a financially viable and self-sustaining water utility economic enterprise. Appendices 1 and 2 contain a practice set of simulation problems and suggested solutions for the Accounts Reconstruction Phase.

9

SECTION TWO

This section of the Guide provides an overview of ring-fencing as introduced

in the Guide to Ring-Fencing of Local Government-Run Water Utilities developed by the Water and Sanitation Program (WSP) of the World Bank in 2009. It integrates concepts and methodologies obtained from pilot testing experiences.

The ring-fencing concept operates within the ambit of Section 313 of the Local Government Code (RA 7160) and the New Government Accounting System (NGAS) Sections 105 to 110, which allows the creation of special accounts for public utilities to be maintained under the general fund. The methodologies introduced in the ring-fencing approach enhanced some of these accounting procedures, such as using a subsidiary ledgering system for waterworks. They reinforced the preparation of separate financial statements for the special account maintained for the waterworks system. A subcode 04 (waterworks system) has been assigned under NGAS for this purpose.

2.1 PREPARATORY ACTIVITIES

A number of preparations need to be made before an LGU can adopt the ring-fencing approach. First, local officials should draw a

utility reform agenda and identify programs or strategies to that effect. Given the fact that local government accounting follows the one-fund approach in which all financial transactions are commingled in the General Fund, all water utility reform programs therefore will neces-sitate implementation of ring-fencing as the first step.

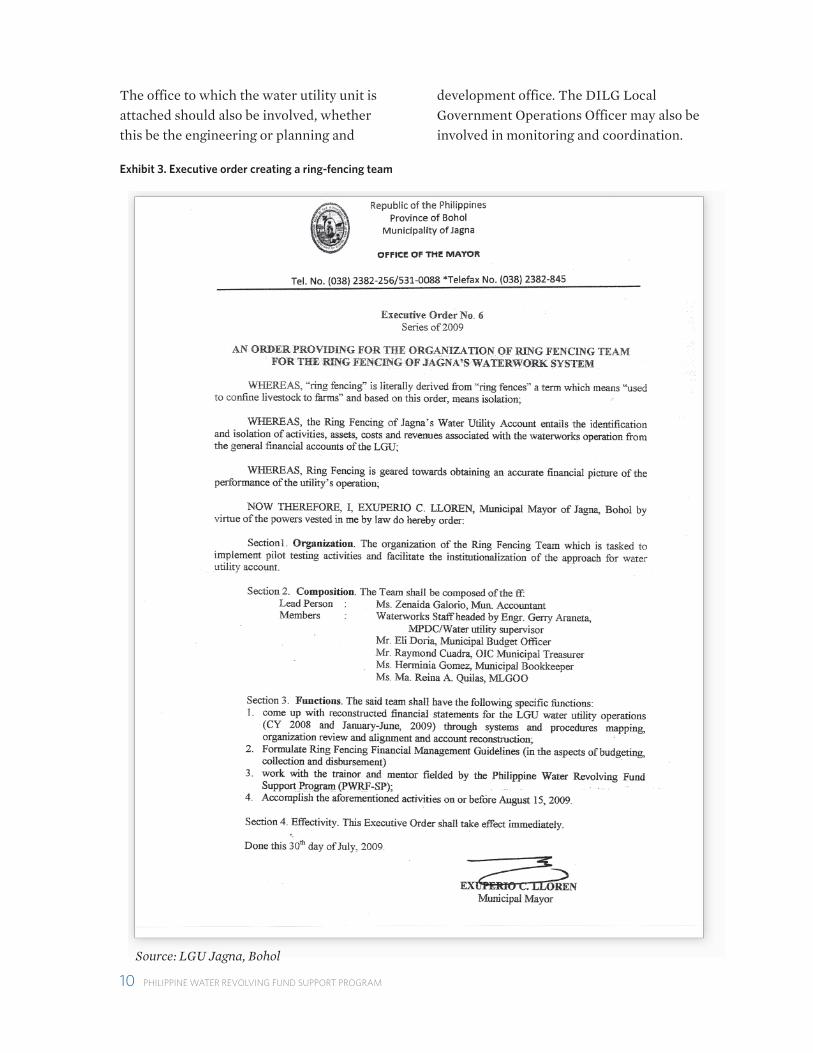

2.1.1 Affirmation of LGU commitment to ring-fencingFirst the LGU must commit itself to adopting the ring-fencing approach for water utility operation and management through the issuance of an executive order by the Local Chief Executive (LCE) or a resolution by the local Sanggunian adopting the ring-fencing system and creating the ring-fencing team (Exhibit 3). A ring-fencing team is needed to make sure all involved units and personnel will participate in the process. This will ensure collaboration and support among concerned officers to install, implement and complete the ring-fencing process.

The ring-fencing team should be composed of the LGU’s key financial management officers, such as the accountant, treasurer, budget officer, and chairman on appropriations.

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM10

The office to which the water utility unit is attached should also be involved, whether this be the engineering or planning and

Exhibit 3. Executive order creating a ring-fencing team

development office. The DILG Local Government Operations Officer may also be involved in monitoring and coordination.

Source: LGU Jagna, Bohol

11GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

2.1.2 Basic information gatheringThe ring-fencing team will need to gather basic information about the water utility to better understand existing conditions, systems and procedures. This involves gathering forms, records and reports used and prepared by the utility and other LGU units involved in water utility operations.

Water utility profileAs a minimum, information gathering and profiling should cover the following information:

1. Name of the utility 2. Brief history or background (year the utility

was formed or when operations started, system source and type, utility in-charge, etc.)

3. Vision and mission statements, goals and objectives

4. Coverage area (total no. of barangays in the administrative and service areas, total population of barangays served, other water service providers present)

5. Connections (active, inactive, disconnected, public taps, metered and non-metered connections)

6. Production levels (annual volume produced, annual volume billed, treatment facility type, if any)

7. Customer service (average number of hours of water availability per day; frequency of bacteriological, physical and chemical tests; water meter maintenance)

8. Personnel (permanent, casual, contractual)9. Waterworks assets (land, building,

machinery, tools and equipment, infrastructure)

10. Tariff structure (flat or graduated rates)

Water utility documents, forms, records and reportsDocuments, forms, records and reports for the last two years or for the year immediately preceding should be obtained to facilitate reconstruction of accounts.

1. Billing and collection reports, such as meter reading list, file copy of water bills, customer master list, report of collection and deposits

2. Customer accounts receivables, such as customer ledger cards or index cards, customer logbooks, account receivable ledgers and subsidiary ledgers

3. Staffing list and salary schedules, including the payroll

4. Operation and maintenance expense reports

5. Subsidiary records or ledgers for property, plant and equipment

6. Registries for infrastructure and grants/donations

7. Trial balance and, if separate financial reports are prepared for the water utility, copies of Statement of Income and Expenses, Balance Sheet and Cash Flow Statement or similar reports

8. Operations policies, such as a local ordinance or Sangguniang Bayan (SB) resolutions and Local Revenue Code

9. Monthly data sheet (as prescribed by the NWRB) for LGUs under consensual agreement

2.1.3 Review of organization and functionsAnother important activity is to review how the utility is organized, including its staffing structure. Creating a simple organizational chart will help the ring-fencing team to understand the organization’s systems and procedures. Understanding the different processes in water service provision, through

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM12

activity analysis and perhaps even utilizing a simple flowcharting tool, is valuable preparation for the installation of the ring-fencing system.

2.2 STEPS IN THE ACCOUNTS RECONSTRUCTION

The reconstruction of the utility’s financial accounts should follow these 13 major steps. We use the case of Matubig Waterworks System (see Appendix 1) as a sample problem to illustrate steps and suggested solutions.

Step 1. Set up the books of accounts The books of accounts shall be composed of journals and ledgers required by NGAS for LGUs, such as the Cash Receipts Journal, Cash Disbursements Journal, Check Disbursements Journal, General Journal, General Ledger and Subsidiary Ledger. LGU-run water utilities should also set up a Bill Register, a special journal to record water bills issued, and Customer Ledger Cards, a special subsid-iary ledger for maintaining customer records.

Step 2. Establish the balance sheet accounts’ beginning balancesAfter deciding on the cut-off date (or January 1) of the immediately preceding year, the beginning balances of the balance sheet accounts can be established.

Cash accounts. The cash accounts normally consist of data on Cash – Collecting Officer, Petty Cash Fund, and Cash in Bank.

An example of determining the beginning balance of Cash in Bank as of January 1, 2009 can be seen in Example 1.

Cash in bank (from loan proceeds) 25,844,515.00 Advances to contractors -Add/less: Mobilization (3,876,677.25) Recoupment of mobilization 1,550,670.90 2008 progress payments (11,053,905.82) 2008 BIR remittances (1,063,036.59) (14,442,948.76) Cash in bank balance 11,401,566.24

Receivables accounts. The receivables accounts common to water utilities are Accounts Receivable, Allowance for Doubtful Accounts, Due from Other Funds, and Other Receivables.A sample solution for determining the beginning balance of accounts receivable (AR) and cor-responding allowance for doubtful accounts (assumed at 2% of ending AR balance) as of January 1, 2009 can be seen in Example 2.

Inventory accounts. The inventory accounts usually consists of Office Supplies Inventory, Accountable Forms Inventory, Gasoline, Oil and Lubricants Inventory, Spare Parts Inventory,

Example 1. Example of determining the beginning balance of Cash in Bank as of January 1, 2009

13GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Unpaid water bills, 2007 649,465.00 Issued water bills, 2008 2,923,523.60 Collection from water bills, 2008 (2,680,107.00)Unpaid water bills, 2008 (accounts receivable) 892,881.60

Allowance for doubtful accounts2% of unpaid water bills = P892,881.60 x 2% = P17,857.63

Exhibit 4. Inventory count sheet

Inventory Count Sheet

Sheet no.: Counted by:

Item no. Description Location Quantity Acquisition cost Total cost

Example 2. A sample solution for determining the beginning balance of accounts receivable (AR) and corresponding allowance for doubtful accounts (assumed at 2% of ending AR balance) as of January 1, 2009

Construction Materials Inventory, and Other Supplies Inventory. Prepare an inventory count sheet (Exhibit 4) for each inventory account.

Property, plant and equipment accounts. System assets are recorded in the LGU books of accounts as Public Infrastructure – Artesian Wells, Reservoirs, Pumping Stations and Conduits, while non-system assets are recorded as Property, Plant and Equipment (PPE). The PPE accounts consist of Land and Land Improvements, Buildings, Office Equipment, Furniture and Fixtures, Machineries and Equipment, Transportation Equipment, and Other Property, Plant and Equipment.

An example on the determination of property, plant and equipment beginning balance as of January 1, 2009 is presented in Example 3. It shall follow the same format as the schedule of depreciation to obtain the corresponding beginning balance of accumulated depreciation as of the same cut-off date.

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM14

Ass

et d

escr

ipti

onA

cqui

siti

on

date

Acq

uisi

tion

co

stSa

lvag

e va

lue

Dep

reci

able

co

stEs

tim

ated

Use

ful L

ife

Ann

ual

depr

ecia

tion

Year

s in

us

e as

of

12/3

1/0

8

Acc

umul

ated

de

prec

iati

on12

/31/

08

RES

ERV

OIR

S

Gro

und

conc

rete

tank

- B

rgy

Sila

ng20

05

228

,561

.00

22,8

56.10

205,

704

.90

40

5,14

2.62

315

,427

.87

Gro

und

conc

rete

tank

- B

rgy

Osl

ao19

9615

0,0

00

.00

15,0

00

.00

135,

00

0.0

04

03,

375.

00

124

0,5

00

.00

Gro

und

conc

rete

tank

- B

rgy

Pono

ng19

9422

0,0

00

.00

22,0

00

.00

198

,00

0.0

04

04

,950

.00

1469

,30

0.0

0

Gro

und

conc

rete

- B

rgy

Banb

anon

198

925

0,0

00

.00

25,0

00

.00

225,

00

0.0

04

05,

625.

00

1910

6,87

5.0

0

Elev

ated

con

cret

e ta

nk -

Brg

y M

agta

ngal

e19

9775

,00

0.0

07,

500

.00

67,5

00

.00

40

1,687

.50

1118

,562

.50

Gro

und

Con

cret

e -

Brgy

Lin

ongg

anan

1994

120

,00

0.0

012

,00

0.0

010

8,0

00

.00

40

2,70

0.0

014

37,8

00

.00

Gro

und

conc

rete

tank

- B

rgy

Jubg

an20

04

335,

00

0.0

033

,50

0.0

030

1,50

0.0

04

07,

537.

504

30,15

0.0

0

Gro

und

conc

rete

tank

- B

rgy

Am

onta

y20

02

228

,471

.00

22,8

47.

1020

5,62

3.90

40

5,14

0.6

06

30,8

43.

59

Gro

und

Inta

ke ta

nk -

Brg

y Ba

ybay

200

58

9,0

71.0

08

,90

7.10

80

,163.

904

02,

00

4.10

36,

012

.29

Sub-

tota

l1,

696,

103.

00

169,

610

.30

1,52

6,4

92.7

038

,162

.32

355,

471

.25

PUM

PIN

G E

QU

IPM

ENT

Dee

p w

ell 1

50 ft

w/

3HP

subm

ersi

ble

pum

p -

Brgy

Sila

ng20

04

210

,00

0.0

021

,00

0.0

018

9,0

00

.00

1018

,90

0.0

04

75,6

00

.00

Dee

p w

ell 1

20 ft

w/

1.5H

P su

bmer

sibl

e pu

mp

- Br

gy O

slao

1995

75,0

00

.00

7,50

0.0

067

,50

0.0

010

6,75

0.0

010

67,5

00

.00

Dee

p w

ell 1

80

ft w

/ 1.

5HP

subm

ersi

ble

pum

p -

Brgy

Pon

ong

1994

170

,00

0.0

017

,00

0.0

015

3,0

00

.00

1015

,30

0.0

010

153,

00

0.0

0

Dee

p w

ell 6

0 ft

w/

1.5

HP

subm

ersi

ble

pum

p -

Brgy

Ba

nban

on19

9363

,00

0.0

06,

300

.00

56,7

00

.00

105,

670

.00

1056

,70

0.0

0

Dee

p w

ell 1

60 ft

w/

2HP

subm

ersi

ble

pum

p -

Brgy

M

agta

ngal

e20

01

120

,00

0.0

012

,00

0.0

010

8,0

00

.00

1010

,80

0.0

07

75,6

00

.00

Dee

p w

ell 2

00

ft w

/ 1H

P su

bmer

sibl

e pu

mp

- Br

gy

Lino

ngga

nan

200

217

5,0

00

.00

17,5

00

.00

157,

500

.00

1015

,750

.00

694

,50

0.0

0

Dee

p w

ell 2

50 ft

w/

1.5

HP

subm

ersi

ble

pum

p -

Brgy

Ju

bgan

200

532

5,0

00

.00

32,5

00

.00

292,

500

.00

1029

,250

.00

387

,750

.00

Dee

p w

ell 2

00

ft w

/ 1.

5HP

subm

ersi

ble

pum

p -

Brgy

A

mon

tay

200

122

0,0

00

.00

22,0

00

.00

198

,00

0.0

010

19,8

00

.00

713

8,6

00

.00

Dee

p w

ell 2

00

ft w

/ 1.

5HP

subm

ersi

ble

pum

p -

Brgy

Ba

ybay

200

517

7,54

5.0

017

,754

.50

159,

790

.50

1015

,979

.05

34

7,93

7.15

Dee

p w

ell 1

00

ft w

/ 1.

5 H

P su

bmer

sibl

e pu

mp

- Br

gy D

iaz

200

38

3,0

00

.00

8,3

00

.00

74,7

00

.00

107,

470

.00

537

,350

.00

Subm

ersi

ble

pum

p 3H

P -

Brgy

Hon

rado

Spr

ing

200

225

4,0

00

.00

25,4

00

.00

228

,60

0.0

010

22,8

60.0

06

137,

160

.00

Dee

p w

ell w

/ 1H

P su

bmer

sibl

e pu

mp

– Br

gy B

razi

l19

9828

,00

0.0

02,

80

0.0

025

,20

0.0

010

2,52

0.0

010

25,2

00

.00

Sub-

tota

l1,

900

,54

5.0

019

0,0

54.5

01,

710

,490

.50

171,

04

9.0

599

6,8

97.1

5

Exam

ple

3. P

PE D

epre

ciat

ion

Sche

dule

15GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

TR

AN

SMIS

SIO

N a

nd D

IST

RIB

UT

ION

MA

INS

Dis

trib

utio

n lin

e 1

1994

500

,00

0.0

050

,00

0.0

04

50,0

00

.00

3015

,00

0.0

014

210

,00

0.0

0

Dis

trib

utio

n lin

e 2

1998

1,025

,00

0.0

010

2,50

0.0

092

2,50

0.0

030

30,7

50.0

010

307,

500

.00

Dis

trib

utio

n lin

e 3

200

01,

500

,00

0.0

015

0,0

00

.00

1,35

0,0

00

.00

304

5,0

00

.00

836

0,0

00

.00

Dis

trib

utio

n lin

e 4

200

382

9,18

0.6

582

,918

.07

746,

262.

5930

24,8

75.4

25

124

,377

.10

Tran

smis

sion

line

- B

rgy

Pono

ng20

05

100

,210

.00

10,0

21.0

090

,189.

00

303,

00

6.30

39,

018

.90

Tran

smis

sion

line

- B

rgy

Banb

anon

200

476

,977

.00

7,69

7.70

69,2

79.3

030

2,30

9.31

49,

237.

24

Pipe

s -

Brgy

Mac

opa

200

669

,250

.00

6,92

5.0

062

,325

.00

302,

077

.50

24

,155.

00

Sub-

tota

l4

,10

0,6

17.6

54

10,0

61.7

73,

690

,555

.89

123,

018

.53

1,0

24,2

88

.24

WA

TER

TR

EAT

MEN

T E

QU

IPM

ENT

Wat

er c

hlor

inat

or20

07

17,2

92.3

51,7

29.2

415

,563

.1210

1,55

6.31

11,

556.

31

Sub-

tota

l17

,292

.35

1,72

9.24

15,5

63.1

21,

556.

311,

556.

31

OFF

ICE

FUR

NIT

UR

E an

d FI

XT

UR

ES

Off

ice

tabl

es (

5 un

its)

200

224

,250

.00

2,4

25.0

021

,825

.00

54

,365

.00

521

,825

.00

Filin

g ca

bine

t20

01

6,93

5.50

693.

556,

241.9

55

1,24

8.3

95

6,24

1.95

Stee

l cab

inet

200

711

,24

5.50

1,124

.55

10,12

0.9

55

2,0

24.19

12,

024

.19

Stan

d fa

n20

05

821

.65

82.

1773

9.4

95

147.

93

44

3.69

Des

k fa

n20

04

695

69.5

625.

55

125.

14

500

.4

Cei

ling

fan

200

692

8.8

92.8

88

35.9

25

167.

182

334

.37

Sub-

tota

l4

4,8

76.4

54

,487

.65

40

,38

8.8

18

,077

.76

31,3

69.6

0

OFF

ICE

EQU

IPM

ENT

Type

wri

ter

1998

19,4

74.0

01,9

47.

40

17,5

26.6

05

3,50

5.32

517

,526

.60

Sub-

tota

l19

,474

.00

1,94

7.4

017

,526

.60

3,50

5.32

17,5

26.6

0

OT

HER

MA

CH

INER

Y a

nd E

QU

IPM

ENT

Plum

bing

tool

s20

08

55,0

00

.00

5,50

0.0

04

9,50

0.0

05

9,90

0.0

00

-

Sub-

tota

l55

,00

0.0

05,

500

.00

49,

500

.00

9,90

0.0

00

.00

TOTA

LS7,

833

,90

8.4

578

3,39

0.8

67,

050

,517

.62

355,

269.

292,

427

,10

9.15

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM16

Construction in progress accounts. The only construction in progress accounts for water utilities are Artesian Wells, Reservoirs, Pumping Stations and Conduits and Other Infrastructures.

As an example, the computation of the Construction in Progress beginning balance at January 1, 2009 can be seen in Example 4.

First billing at 33.94% - P 8,771,628.39Second billing at 58.76% - 6,414,608.62Total value of accomplishment - P15,186,237.01

Example 4. Computation of the Construction in Progress beginning balance at January 1, 2009

Guarantee deposits payable2009 total deposits from water customers (Note 5) - P 119,500.00Less: 2009 collections on guarantee deposits - 27,600.002009 beginning balance - P 91,900.00

Loans payable – domesticTotal loan amount - P25,844,515.00Less: Quarter payments in 2008: 2nd quarter - P 497,009.91 3rd quarter - P 497,009.91 4th quarter - P 497,009.91 - 1,491,029.73Loan balance as of Dec. 31, 2008 - P24,353,485.28

Other payables10% Retention money on contracts 1st progress billing - P 877,162.84 2nd progress billing - 641,460.86Total - P1,518,623.70

Example 5. Examples of determining beginning balances of current and long-term liabilities

Liability accounts. The current liability accounts of a water utility usually arise from supplies purchased on credit and payroll transactions, particularly on remittable amounts to government agencies, like GSIS, HDMC, PHIC and BIR. The current liabilities consist of Accounts Payable, Notes Payable, Interest Payable, Due to BIR, Due to GSIS, Due to Pag-ibig, Due to PhilHealth, Due to NGAs, Guaranty Deposits Payable, and Other Payables. The long-term liabilities consist of Loans Payable Domestic, and Other Long-term Payables.

The following computations are examples of determining beginning balances of current and long-term liabilities.

Government equity. The government equity account represents the LGU’s (the owner’s) capital contribution. This can be obtained by getting the difference between total assets and total liabilities, as shown in Example 6.

17GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Government equityASSETS Amount Cash in bank 11,401,566.24 Accounts receivables 892,881.60 Allowance for doubtful accounts (17,857.63) Office equipment 19,474.00 Accumulated depreciation (17,526.60) Furniture and fixtures 44,876.45 Accumulated depreciation (31,369.60) Other machinery and equipment 55,000.00 Accumulated depreciation - Artesian wells, reservoir, pumping stations and conduits 7,714,558.00 Accumulated depreciation (2,378,212.94) Construction in progress - artesian wells, reservoirs, pump… 15,186,237.01 Advances to contractors 2,326,006.35 TOTAL ASSETS 35,195,632.88 LESS: LIABILITIES Guaranty deposits payable 91,900.00 Due to BIR - Loans payable – Domestic 24,353,485.28 Other payables 1,518,623.70 TOTAL LIABILITIES 25,964,008.98

Government equity 9,231,623.90

Example 6. Government equity

Step 3. Determine revenues for the year.Despite the NGAS provision on the use of accrual basis for revenues, many if not all LGUs still record most of its revenues following the cash basis of accounting (with the exception of the internal revenue allotment [IRA] which is reported based on the Statement of Allotment Release Order received by the LGU from the Department of Budget and Management). The ring-fencing approach reinforces the accrual basis for revenue recognition since this method is more practical for water utilities—the necessary supporting data are concrete, reliable and readily available in the form of issued water bills. Since the amount of water consumption is clearly supported and recorded in water bills and billable at the stated amount at a specified

due date, recording of revenues therefore must originate from issuance of water bills and not upon collection of payment.

Under the accrual basis of accounting, receiv-ables are set up for the amount of unpaid water bills at the end of the accounting period. Recognizing receivables is useful for monitor-ing the collection effort, measure collection efficiency, manage customer accounts, and secure fund availability to commit expendi-tures for business operations.

Water consumption is the major source of revenue for the water utility but there are other sources which are realized only upon actual collection. These types of revenue are therefore recorded on a cash basis.

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM18

Considering the variety of income sources, the ring-fencing approach further recommends the use of specific account titles to appro-priately describe the nature of waterworks income. These account titles are to be main-tained in parallel to the NGAS’ only income account for waterworks’ revenues called “Income from Waterworks System.”

The waterworks revenues would normally include the following:

1. Water Sales Revenue. This account refers to the income arising from water consumption as evidenced by issued water bills. This is recorded on accrual basis of accounting.

In our example, the Matubig Waterworks System should record its water sales revenue based on the 2009’s summary of water bills in the amount of P4,504,367.00, equal to the total annual water bills issued.

2. Other Business Income. This is a control-ling account that consists of collections from all services provided by the water-works system for a fee. These are recorded following the cash basis of accounting and are evidenced by official receipts. Subsidiary ledgers shall be maintained for the following sub-accounts:

a. New connection fees - income from making new service connections

b. Reconnection fees - income from reconnections

c. Other service fees - income from operations which cannot be classified in other business income accounts, such as tapping fee, inspection fee, and metering fee

Example: Based on the summary of collec-tions prepared by the revenue collection

officer of Matubig Waterworks System, the total Other Business Income of the utility is composed of the following:

Application fee = P110,400.00Reconnection fee = 150.00Other service fee = 348,294.45Other business income = P458,844.45

3. Fines and Penalties-Business Income. This accounts for the total fines and penalties charged on late payments of water bills and recorded using the modified accrual accounting basis; the amounts can be obtained from the customers’ ledgers and/or official receipts

Step 4. Determine expenses for the yearBasically, expenses in LGUs are classified into Personal Services (PS) and Maintenance and Other Operating Expenses (MOOE). PS includes salaries, allowances, benefits and other personal service expenses. MOOE includes all non-salary expenditures such as the cost of chemicals, pump electricity, plumbing materials and supplies, minor repairs and maintenance, and all other expenses incurred in the ordinary course of providing water services.

Under the ring-fencing approach, expenses of the water utility are determined using the full cost accounting method, i.e., all related costs or expenses in water service provision whether directly or indirectly incurred by the utility will be accounted for in the books of accounts. Hence, the PS and MOOE are further classified into Dedicated Expenses and Shared Expenses.

Example 7. Other Business Income

19GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Dedicated expensesDedicated expenses are costs incurred by the utility itself or expenses directly attributable to water service operations. These costs normally consist of salaries, wages, and fringe benefits for waterworks personnel, repairs and maintenance of transmission and distribution networks, cost of electricity for waterworks pumps, cost of chemicals used in water treatment, and other expenses whose vouchers originate from the waterworks unit.

Example: In the case of Matubig Waterworks System, its allotment and appropriation showed the following items below. The fully utilized allotments become the basis for determining dedicated expenses for the utility.

Dedicated personal servicesPersonal services Salaries and wages - Permanent 975,648.00Salaries and wages - Casual 308,400.00PERA 83,000.00ADCOM 144,000.00Cash gift 120,000.00Year-end bonus 81,304.00Life and retirement insurance contribution 117,077.76Pag-Ibig contribution 19,572.00PhilHealth contribution 11,700.00ECC contribution 8,471.40Other personnel benefits 72,500.00Total 1,941,673.16

Dedicated maintenance and other operating expensesMOOE Electricity 478,634.00Repairs and maintenance 302,583.40Miscellaneous expense 159,417.00Total 940,634.40

Shared expensesShared expenses are costs incurred by other LGU offices, units, or departments that provide support services to the water utility or all expenses that are indirectly attributable to water service operations charged against the operations of other offices or units. Being a part of the LGU, the water utility’s transactions follow accounting and budgeting processes used by the LGU, with costs normally including a share in operation and maintenance expenses of the local finance units. Some shared staff include the budget officer who is in charge of budget preparation and release, the treasurer who maintains and controls cash availability, the accountant who certifies the appropri-ate obligation of every financial transaction, the local planning and development officer and/or engineer in the management of water operations, human resource officer who handles staffing, even the electrician or sanitary inspector, whose time and resources also go to the water service provision.

Example 8. Dedicated expenses

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM20

Example 9.1. Shared personal services

Sharing percentage 1% 1% 30% 10% 10% 5%

Personal services Mayor MPDC Engineering Treasury Accounting Budget

Salaries and wages – Permanent

3,400.80 3,420.72 102,621.60 35,062.80 32,558.40 17,103.60

PERA - 60.00 1,800.00 600.00 600.00 300.00

ADCOM 180.00 180.00 5,400.00 1,800.00 1,800.00 900.00

RA 846.60 601.80 18,054.00 6,018.00 6,018.00 3,009.00

TA 846.60 601.80 18,054.00 6,018.00 6,018.00 3,009.00

Cash gift 150.00 150.00 4,500.00 1,500.00 1,500.00 750.00

Year-end bonus 283.40 285.06 8,551.80 2,921.90 2,713.20 1,425.30

Life and retirement insurance contribution

408.10 410.49 12,314.59 4,207.54 3,907.01 2,052.43

Pag-Ibig contribution 68.04 68.52 2,055.60 702.00 651.60 342.60

PhilHealth contribution 42.00 42.00 1,260.00 435.00 405.00 202.50

ECC contribution 12.00 12.00 360.00 120.00 120.00 60.00

Other personnel benefits 60.00 60.00 1,800.00 600.00 600.00 300.00

Total 6,297.54 5,892.39 176,771.59 59,985.24 56,891.21 29,454.43

Example 9.2. Shared maintenance and other operating expenses

Sharing percentage 1% 1% 15% 25% 10% 1%

MOOEs Mayor MPDC Engineering Treasury Accounting Budget

Travelling 1,094.87 195.00 4,986.00

Office supplies 78.00 3,620.00 112.00

Accountable forms 1,647.25

Electricity 6,486.30

Fidelity bond premiums 6,933.75

Repairs and maintenance 17,154.45

Miscellaneous expense 429.45

Total 1,094.87 273.00 24,070.20 8,581.00 8,606.00 112.00

Therefore, there will be Dedicated PS, Dedicated MOOE, Shared PS and Shared MOOE. The dedicated expenses are recorded at cost while the shared expenses are accounted for using the system of allocation (Section 3.3).The local budget or the Statement or Registry of Appropriation, Allotment and Obligation is the basis for determining shared expenses.

Example: The Matubig Waterworks System uses man-hours as the basis for allocating shared costs. The water utility’s share in the PS and MOOE of LGU offices providing support services are as follows:

21GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Step 5. Determine the depreciation expenseIn consonance with full cost accounting, depreciating all property, plant and equipment (PPE), including public infrastructure-artesian wells, reservoirs, pumping stations and conduits is a major step in the ring-fencing approach. This step is a slight departure from the NGAS. Adopting the ring-fencing approach means treating the artesian wells, reservoirs, pumping stations and conduits as PPE and therefore subject to depreciation. Depreciating artesian wells, reservoirs, pumping stations and conduits is also a way of determining the total value of water utility operations; a basis for allocating funds for future replacement, rehabilitation or improvement of water facilities; and a factor in setting the appropriate tariff.

NGAS guidelines using the straight line method with 10% salvage value on depreciating PPE will be followed. A separate depreciation schedule shall be prepared. The annual depreciation expense of the water utility will include the depreciable amount of artesian wells, reservoirs, pumping stations and conduits and other PPE accounts. In determining the economic life of assets, reference should be made to COA Circular 2005-002 dated 14 April 2005 adopting International Accounting Standards No. 16 in depreciating those assets considered as part of inventory and to the NWRB’s estimated useful lives in depreciating PPE, including artesian wells, reservoirs, pumping stations and conduits (see Exhibits 5.1 and 5.2).

Exhibit 5.1 Useful lives of tangible assets that may be considered part of inventory

Description Useful life (years)

A. Office supplies

1 Blackboard/whiteboard 5

2 Copy holder, clamp type with adjustable arm 5

3 Cutter 5

4 Desk tray 3

5 Eraser – blackboard 3

6 Mechanical pencil 2

7 Mini calculators 3

8 Pen 2

9 Pencil sharpener 3

10 Puncher 5

11 Ruler 3

12 Scissors 3

13 Sharpener 3

14 Staple wire remover 2

15 Stapler 2

16 Tape dispenser 3

D. Textbooks and instructional materials

75 Textbooks 5

76 Instructional materials 2

F. Other supplies

Computer peripherals

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM22

Description Useful life (years)

108 Computer cover 2

109 Computer screen 5

110 Diskette storage 2

111 Mouse 2

112 Mouse pad 2

113 Printer cable 5

114 Printer head 5

115 Printer sharing device 5

116 Surge protector 5

Common janitorial supplies

117 Dust pan 2

118 Mop handle 2

119 Pail 2

120 Trash can 5

121 Wastebasket 5

Other inventory items

122 Tea set 3

123 Cups and saucers 3

124 Desk tray 3

125 Dinner plates 3

126 Emergency light 3

127 Rugs, carpets and mats 5

128 Spoon and forks 5

129 Stool 5

130 Pitcher and glass confectionary 3

Hardware and construction supplies

131 Hammer 5

132 Saw 5

133 Plane 5

134 Paint roller 1

135 Paint brush 1

136 Chisel 5

137 Long nose pliers 5

Electrical supplies

138 Extension cord 2

G. School chairs, desks and tables (wood)

139 Chairs 5

140 Desks 5

141 Tables 5

H. Monobloc furniture

142 Chairs 5

143 Tables 5

23GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Property, plant and equipment Useful life (years)

Deep wells and pumphouses (Artesian wells)

Deepwell casing 15

Pump assembly 10

Motor for submersible pump 5

Motor control for deep well pump 7

Pump house-mixed materials 10

Pump house-reinforced concrete 40

Booster station (pumping stations)

Pump house-mixed materials 10

Pump house-reinforced concrete 40

Pump assembly 20

Motor for booster and line turbine 5

Motor control for booster station 20

Reservoirs

Concrete reservoir 40

Steel overhead tank 25

Steel tank on ground concrete 30

Chlorinating equipment 10

Pipelines (conduits)

Cast/ductile iron pipes 60

Steel pipes with cement lining 40

Steel pipes cylinder type 20

Asbestos and plastic pipes 30

Flow meters

Water meters 7

Service connections 5

Valves and chambers 30

Fire hydrants 20

Building 40

Building improvements 10

Office furniture and fixtures 10

Office equipment 5

Vehicles 5

Tools and equipment 5

Exhibit 5.2. Estimated useful lives of property, plant and equipment

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM24

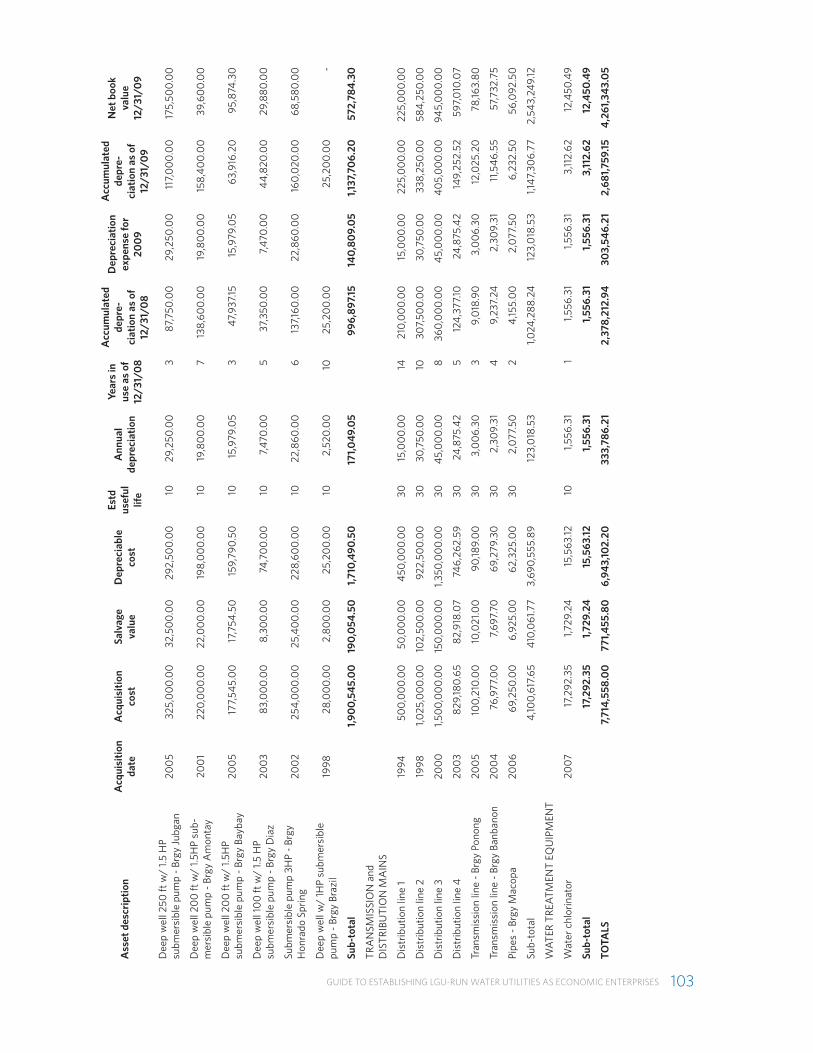

In determining the depreciation expense for the year, simply add more columns to the schedule of depreciation shown in Example 3—one column for the number of years in use, say as of 12/31/2009, and another for the amount of depreciation for the year.

Example 10. The case of Matubig Waterworks System’s PPEs, the depreciation for the year 2009 is as follows:

Asset descriptionAcquisition

cost

Estd useful

life

Annual depreciation

Years in use as of 12/31/09

Depreciation expense for

2009

RESERVOIRS

Ground concrete tank - Brgy Silang 228,561.00 40 5,142.62 4 5,142.62

Ground concrete tank - Brgy Oslao 150,000.00 40 3,375.00 13 3,375.00

Ground concrete tank - Brgy Ponong 220,000.00 40 4,950.00 15 4,950.00

Ground concrete - Brgy Banbanon 250,000.00 40 5,625.00 20 5,625.00

Elevated concrete tank - Brgy Magtangale 75,000.00 40 1,687.50 12 1,687.50

Ground concrete - Brgy Linongganan 120,000.00 40 2,700.00 15 2,700.00

Ground concrete tank - Brgy Jubgan 335,000.00 40 7,537.50 5 7,537.50

Ground concrete tank - Brgy Amontay 228,471.00 40 5,140.60 7 5,140.60

Ground intake tank - Brgy Baybay 89,071.00 40 2,004.10 4 2,004.10

Sub-total 1,696,103.00 38,162.32 38,162.32

PUMPING EQUIPMENT

Deep well 150 ft w/ 3HP submersible pump - Brgy Silang

210,000.00 10 18,900.00 5 18,900.00

Deep well 120 ft w/ 1.5HP submersible pump - Brgy Oslao

75,000.00 10 6,750.00 10Fully

depreciated

Deep well 180 ft w/ 1.5HP submersible pump - Brgy Ponong

170,000.00 10 15,300.00 10Fully

depreciated

Deep well 60 ft w/ 1.5 HP submersible pump - Brgy Banbanon

63,000.00 10 5,670.00 10Fully

depreciated

Deep well 160 ft w/ 2HP submersible pump - Brgy Magtangale

120,000.00 10 10,800.00 8 10,800.00

Deep well 200 ft w/ 1HP submersible pump - Brgy Linongganan

175,000.00 10 15,750.00 7 15,750.00

Deep well 250 ft w/ 1.5 HP submersible pump - Brgy Jubgan

325,000.00 10 29,250.00 4 29,250.00

Deep well 200 ft w/ 1.5HP submersible pump - Brgy Amontay

220,000.00 10 19,800.00 8 19,800.00

Deep well 200 ft w/ 1.5HP submersible pump - Brgy Baybay

177,545.00 10 15,979.05 4 15,979.05

Deep well 100 ft w/ 1.5 HP submersible pump - Brgy Diaz

83,000.00 10 7,470.00 6 7,470.00

Submersible pump 3HP - Brgy Honrado Spring

254,000.00 10 22,860.00 7 22,860.00

Deep well w/ 1HP submersible pump - Brgy Brazil

28,000.00 10 2,520.00 10Fully

depreciated

Sub-total 1,900,545.00 171,049.05 140,809.05

25GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Asset descriptionAcquisition

cost

Estd useful

life

Annual depreciation

Years in use as of 12/31/09

Depreciation expense for

2009

TRANSMISSION and DISTRIBUTION MAINS

Distribution line 1 500,000.00 30 15,000.00 15 15,000.00

Distribution line 2 1,025,000.00 30 30,750.00 11 30,750.00

Distribution line 3 1,500,000.00 30 45,000.00 9 45,000.00

Distribution line 4 829,180.65 30 24,875.42 6 24,875.42

Transmission line - Brgy Ponong 100,210.00 30 3,006.30 4 3,006.30

Transmission line - Brgy Banbanon 76,977.00 30 2,309.31 5 2,309.31

Pipes - Brgy Macopa 69,250.00 30 2,077.50 3 2,077.50

Sub-total 4,100,617.65 123,018.53 123,018.53

WATER TREATMENT EQUIPMENT

Water chlorinator 17,292.35 10 1,556.31 2 1,556.31

Sub-total 17,292.35 1,556.31 1,556.31

OFFICE FURNITURE and FIXTURES

Office tables (5 units) 24,250.00 5 4,365.00 5Fully

depreciated

Filing cabinet 6,935.50 5 1,248.39 5Fully

depreciated

Steel cabinet 11,245.50 5 2,024.19 2 2,024.19

Stand fan 821.65 5 147.9 4 147.90

Desk fan 695 5 125.1 5 125.10

Ceiling fan 928.8 5 167.18 3 167.18

Sub-total 44,876.45 8,077.76 2,464.37

OFFICE EQUIPMENT

Typewriter 19,474.00 5 3,505.32 5Fully

depreciated

Sub-total 19,474.00 3,505.32 0.00

OTHER MACHINERY and EQUIPMENT

Plumbing tools 55,000.00 5 9,900.00 1 9,900.00

Sub-total 55,000.00 9,900.00 9,900.00

TOTALS 7,833,908.45 355,269.29 315,910.58

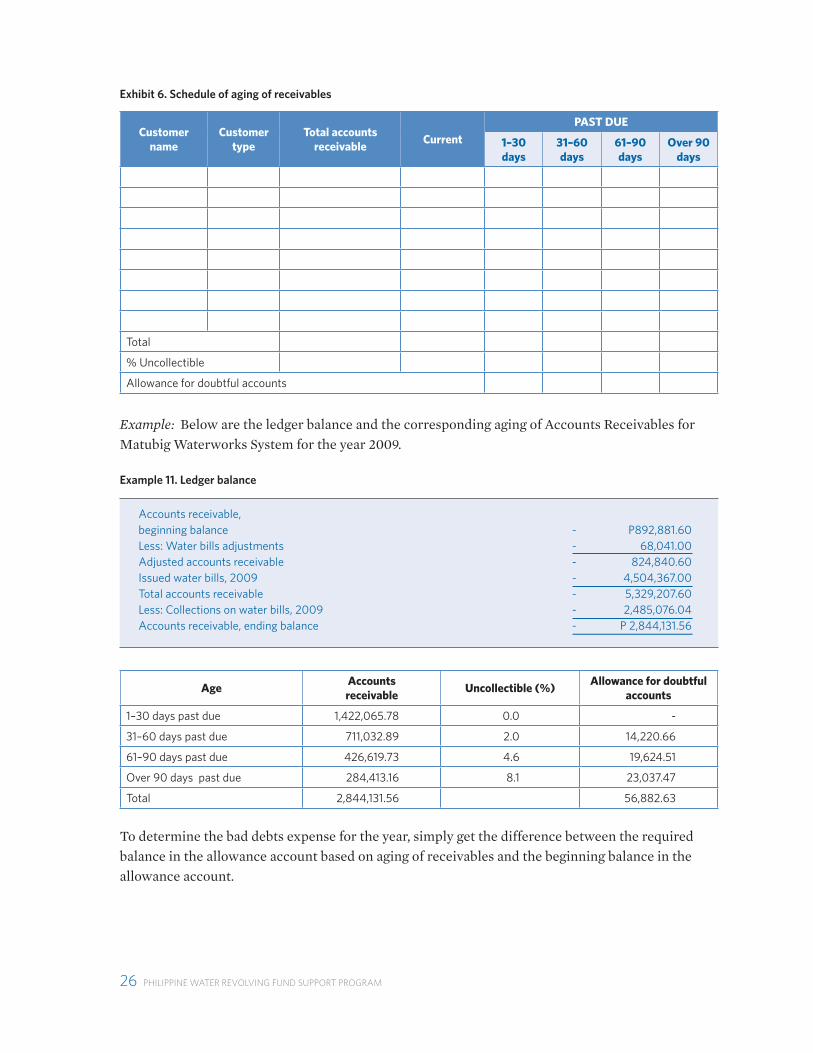

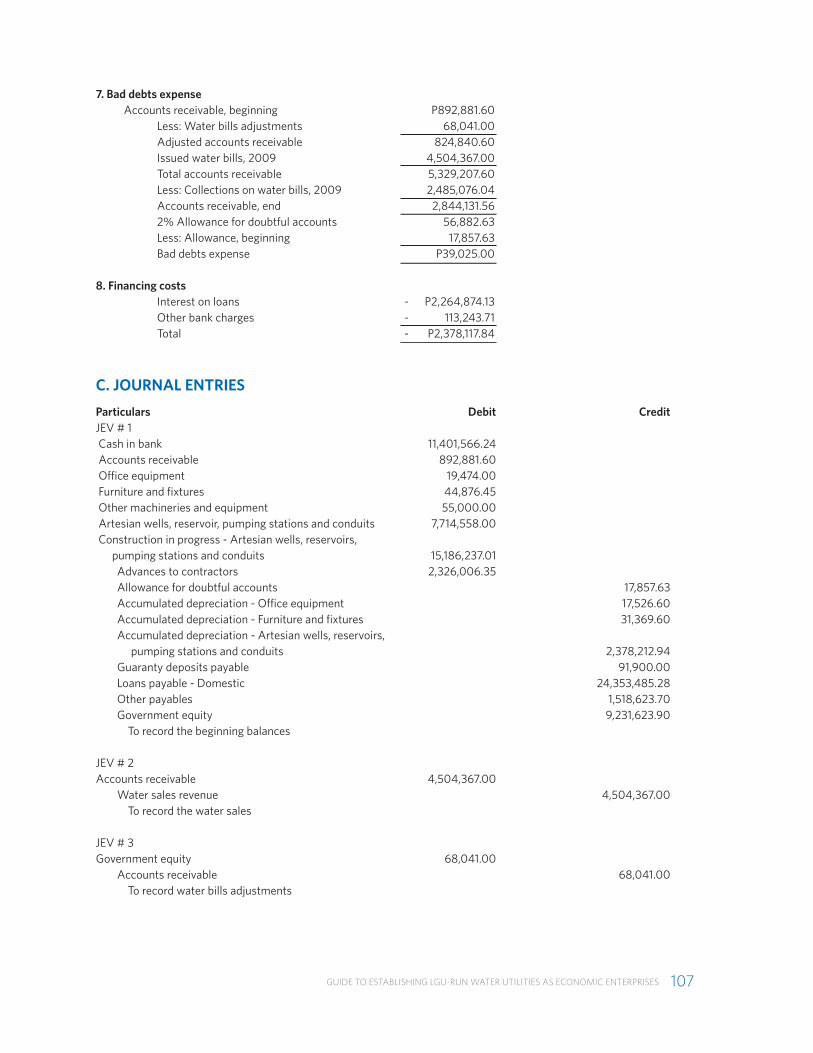

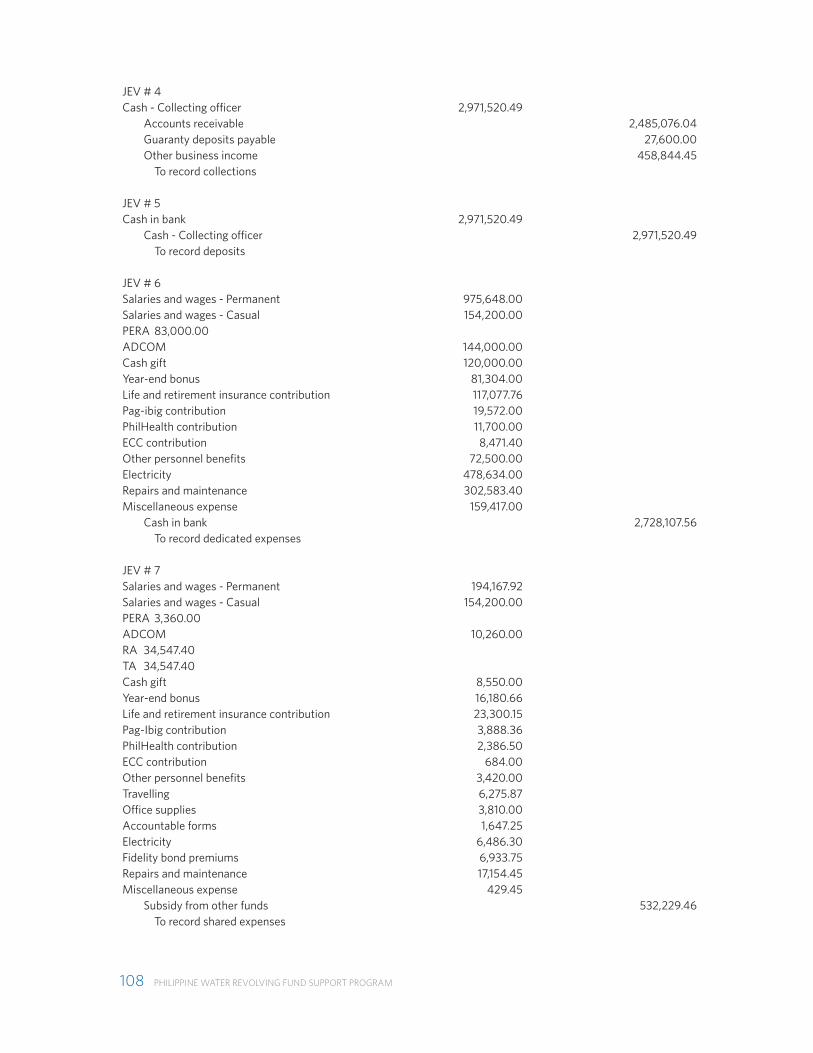

Step 6. Determine the bad debts expenseCommensurate to the accrual method of recognizing water service incomes, the allowance for uncollectible accounts will also be determined at the end of the accounting period. The allowance represents the amount of accounts receivable estimated to be uncollectible or the non-collection of long overdue water bills using the aging of accounts receivable. A schedule of aging of receivables (Exhibit 6) will be prepared to support the estimates.

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM26

Customer name

Customer type

Total accounts receivable

Current

PAST DUE

1–30 days

31–60 days

61–90 days

Over 90 days

Total

% Uncollectible

Allowance for doubtful accounts

Exhibit 6. Schedule of aging of receivables

Example: Below are the ledger balance and the corresponding aging of Accounts Receivables for Matubig Waterworks System for the year 2009.

AgeAccounts receivable

Uncollectible (%)Allowance for doubtful

accounts

1–30 days past due 1,422,065.78 0.0 -

31–60 days past due 711,032.89 2.0 14,220.66

61–90 days past due 426,619.73 4.6 19,624.51

Over 90 days past due 284,413.16 8.1 23,037.47

Total 2,844,131.56 56,882.63

Accounts receivable, beginning balance - P892,881.60Less: Water bills adjustments - 68,041.00Adjusted accounts receivable - 824,840.60Issued water bills, 2009 - 4,504,367.00Total accounts receivable - 5,329,207.60Less: Collections on water bills, 2009 - 2,485,076.04Accounts receivable, ending balance - P 2,844,131.56

To determine the bad debts expense for the year, simply get the difference between the required balance in the allowance account based on aging of receivables and the beginning balance in the allowance account.

Example 11. Ledger balance

27GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Step 7. Determine the financing expenseSome LGU waterworks systems are financed by loans from government financing institutions (GFIs) or private financing institutions (PFIs). The corresponding interests that accrue for the accounting period will be reported as expense for the year. Other financing expenses come from bank charges, commitment fees, documentary stamps expenses and other finance charges.

Step 8. Prepare the trial balanceThe trial balance reflects the summary of all ledger balances and becomes the basis for the prepara-tion of ring-fenced financial statements.

Example 14 on the following page shows a sample trial balance worksheet for the case of Matubig Waterworks System.

Interest on loans - P2,264,874.13Other bank charges - 113,243.71Total - P2,378,117.84

Example 13. Common Financing Costs

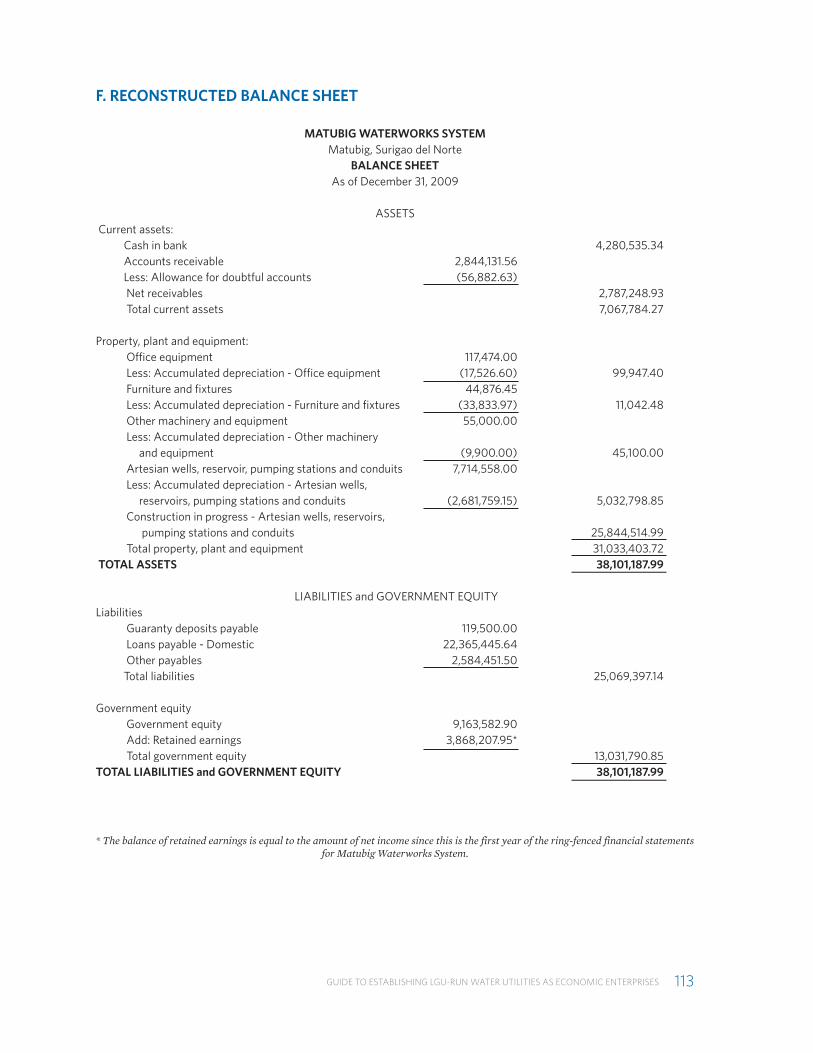

Step 9. Prepare the reconstructed financial statementsThe ring-fenced financial statements consist of the Income Statement, Balance Sheet and Cash Flow Statement. The income statement presents the operation results of the water utility for the year. The balance sheet presents the utility’s financial condition, showing total assets, liabilities, and equity of the LGU in the waterworks system. The cash flow statement shows how changes in the balance sheet and income statement accounts affect the utility’s cash position in a particular year. Using the direct method, compare total cash outflows with total cash inflows. Examples of recon-structed financial statements are shown in Example 15.

Example 12. Bad debts expense

Allowance for doubtful accounts - P56,882.63Less: Allowance, beginning - 17,857.63Bad debts expense - P39,025.00

PHILIPPINE WATER REVOLVING FUND SUPPORT PROGRAM28

Acc

ount

titl

esT

RIA

L BA

LAN

CE

INC

OM

E ST

AT

EMEN

TBA

LAN

CE

SHEE

T

DEB

ITC

RED

ITD

EBIT

CR

EDIT

DEB

ITC

RED

IT

Cas

h in

ban

k

4,2

80

,535

.34

4,2

80

,535

.34

Acc

ount

s re

ceiv

able

2,8

44

,131.

56

2

,84

4,13

1.56

Allo

wan

ce fo

r do

ubtf

ul a

ccou

nts

56,

88

2.63

5

6,8

82.

63

Off

ice

equi

pmen

t

11

7,4

74.0

0

117,

474

.00

Acc

umul

ated

dep

reci

atio

n -

offic

e eq

uipm

ent

17,

526.

60

17,

526.

60

Furn

iture

and

fixt

ures

4

4,8

76.4

5

4

4,8

76.4

5

Acc

umul

ated

dep

reci

atio

n -

Furn

iture

and

fixtu

res

33,

833

.97

33,

833

.97

Oth

er m

achi

nery

and

equ

ipm

ent

55,

00

0.0

0

55,

00

0.0

0

Acc

umul

ated

dep

reci

atio

n -

Oth

er m

achi

nery

and

equi

pmen

t

9,9

00

.00

9

,90

0.0

0

Art

esia

n w

ells

, res

ervo

ir, p

umpi

ng s

tatio

ns

and

cond

uits

7

,714

,558

.00

7,7

14,5

58.0

0

Acc

umul

ated

dep

reci

atio

n -

Art

esia

n w

ells

,

rese

rvoi

rs, p

umpi

ng s

tatio

ns a

nd c

ondu

its

2

,68

1,759

.15

2

,68

1,759

.15

Con

stru

ctio

n in

pro

gres

s -

Art

esia

n w

ells

,

rese

rvoi

rs, p

umpi

ng s

tatio

ns a

nd c

ondu

its

25

,84

4,5

14.9

9

25,8

44

,514

.99

Gua

rant

y de

posi

ts p

ayab

le

119,

500

.00

11

9,50

0.0

0

Loan

s pa

yabl

e -

Dom

estic

22,3

65,4

45.

64

22

,365

,44

5.6

4

Oth

er p

ayab

les

2

,58

4,4

51.5

0

2

,58

4,4

51.5

0

Gov

ernm

ent e

quity

9,

163,

582.

909,

163,

582.

90

Wat

er s

ales

reve

nue

4

,50

4,3

67.0

0

4

,50

4,3

67.0

0

Oth

er b

usin

ess

inco

me

458

,84

4.4

5

458

,84

4.4

5

Sala

ries

and

wag

es -

Per

man

ent

1

,169,

815

.92

1,1

69,8

15.9

2

Sala

ries

and

wag

es -

Cas

ual

308

,40

0.0

0

3

08

,40

0.0

0

PERA

8

6,36

0.0

0

8

6,36

0.0

0

AD

CO

M

154

,260

.00

154

,260

.00

RA

34

,54

7.4

0

3

4,5

47.

40

Exam

ple

14. T

rial

Bal

ance

Wor

kshe

et

29GUIDE TO ESTABLISHING LGU-RUN WATER UTILITIES AS ECONOMIC ENTERPRISES

Acc

ount

titl

esT

RIA

L BA

LAN

CE

INC

OM

E ST

AT

EMEN

TBA

LAN

CE

SHEE

T

DEB

ITC

RED

ITD

EBIT

CR

EDIT

DEB

ITC

RED

IT

TA