23

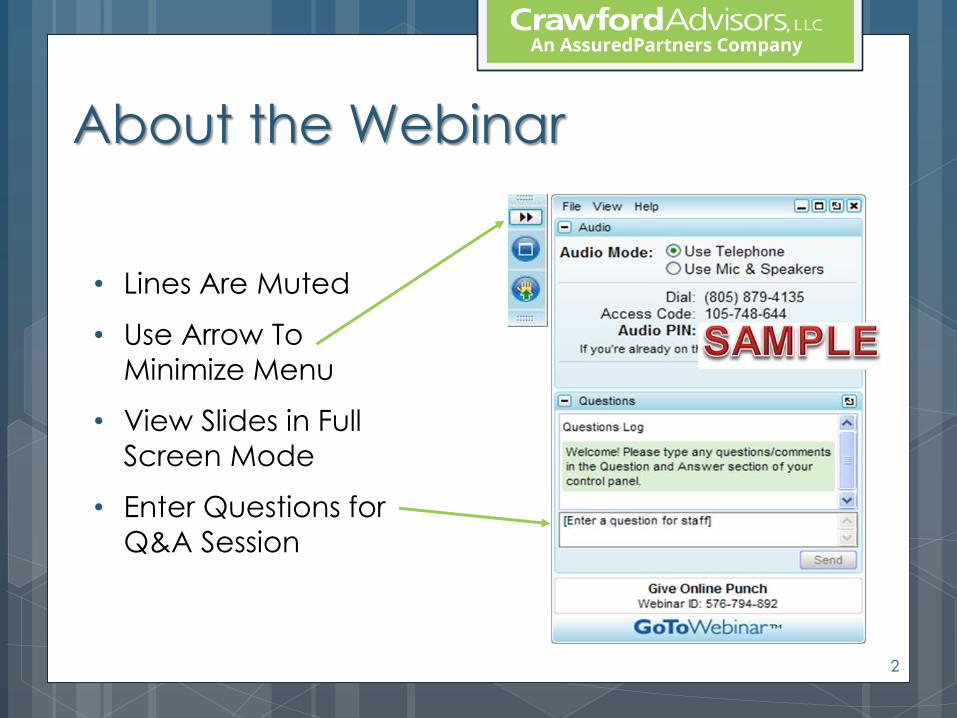

About the Webinar

• Lines Are Muted

• Use Arrow To

Minimize Menu

• View Slides in Full

Screen Mode

• Enter Questions for

Q&A Session

2

Today’s Speaker

Patrick Haynes Education Temple University School of Law, LL.M. Rutgers University School of Law, J.D. Rutgers University School of Business, M.B.A. Rutgers University College of Arts & Sciences, B.A.

As Crawford Advisors’ GC and Vice President –

Compliance, Mr. Haynes advises employers and plan

sponsors in a variety of health and welfare benefit plan

compliance matters, including, but not limited to, tax

qualification and other Internal Revenue Code issues,

PPACA, ERISA, COBRA and HIPAA portability, security

and privacy issues. Mr. Haynes lectures frequently and

has published many articles on health and welfare

benefit plan compliance topics.

Practice Areas

Employee Benefits & Exec

Comp, ERISA, COBRA,

HIPAA, §125, and §§ 105,

106, 129, 132

Admitted to Practice • U.S. Supreme Court • Federal and State

Courts of • New Jersey

• Pennsylvania • Connecticut • District of Columbia

3

Topics Raised by Your Questions 1 Wellness Programs:

• EEOC Final Regulations

• Wellness penalties / rewards / maximums

2 IRS Tax Guidance

• Taxes for wellness rewards

• Taxes for gift cards, gym memberships, etc.

3 SBCs - 2017 Updates & Changes Affecting Your Next

Renewal

4 HIPAA Privacy & Security

5 HSA, FSA, HRA – best approach

6 Grab Bag

4

Wellness Changes You’ve been reading our blog updates (E.g. May

17, 2016) and have been considering what these

wellness changes mean for your next renewal (for

renewals on or after 1/1/2017).

Changes for 1/1/2017 - EEOC Final ADA Rules-

relates only to the Employee (Wellness rules)

30% differential based upon the cost of self-only

coverage

• Limit is calculated based on self-only cost

(even if enrolled in family coverage)

5

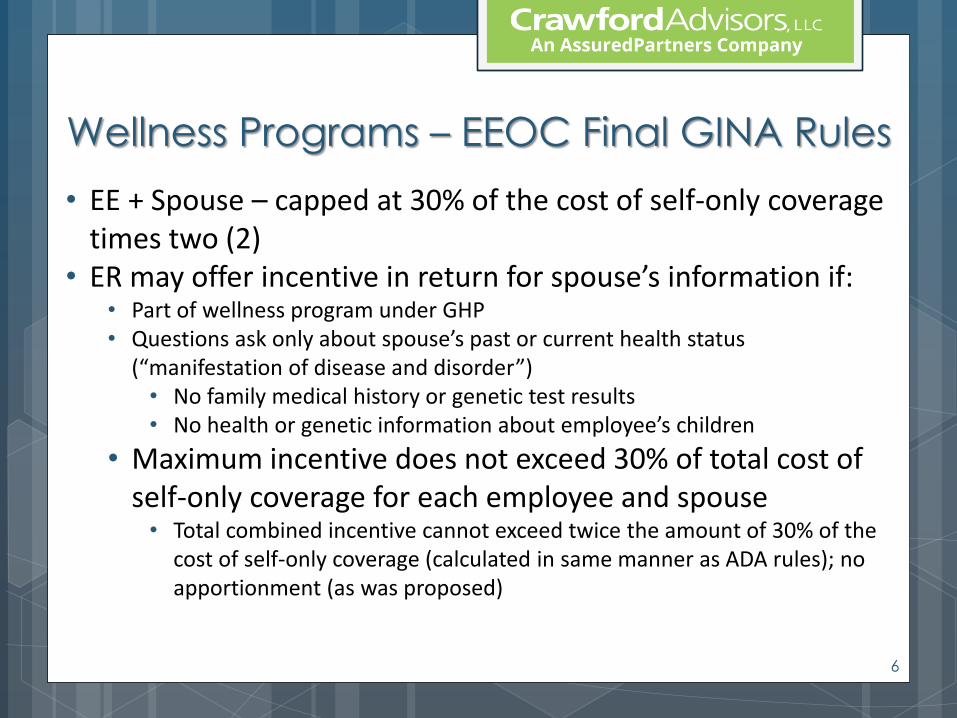

Wellness Programs – EEOC Final GINA Rules

• EE + Spouse – capped at 30% of the cost of self-only coverage times two (2)

• ER may offer incentive in return for spouse’s information if: • Part of wellness program under GHP • Questions ask only about spouse’s past or current health status

(“manifestation of disease and disorder”) • No family medical history or genetic test results • No health or genetic information about employee’s children

• Maximum incentive does not exceed 30% of total cost of self-only coverage for each employee and spouse • Total combined incentive cannot exceed twice the amount of 30% of the

cost of self-only coverage (calculated in same manner as ADA rules); no apportionment (as was proposed)

6

Use of a New Notice – Warning Style Notice

to Employee Plan Participants

NOTICE REGARDING WELLNESS PROGRAM [Name of wellness program] is a voluntary wellness program available to all

employees. The program is administered according to federal rules permitting employer-sponsored wellness programs that seek to improve employee health or prevent disease, including the Americans with Disabilities Act of 1990, the Genetic Information Nondiscrimination Act of 2008, and the Health Insurance Portability and Accountability Act, as applicable, among others. If you choose to participate in the wellness program you will be asked to complete a voluntary

health risk assessment or “HRA” that asks a series of questions about your health-related activities and behaviors and whether you have or had certain medical conditions (e.g., cancer, diabetes, or heart disease). You will also be asked to complete a biometric screening, which will include a blood test for [be specific about the conditions for which blood will be tested]. You are not required to complete the HRA or to participate in the blood test or other medical

examinations.

However, employees who choose to participate in the wellness program will receive an incentive of [indicate the incentive] for [specify criteria]. Although you are not required to complete the HRA or participate in the biometric screening, only employees who do so will receive [the incentive].

7

Incentives

Incentives to an Employee who answers disability-related questions or undergoes medical examinations as part of a wellness program in order to earn a reward or avoid a penalty, are limited to the following:

• 30% of the total cost for self only coverage • 30% of the lowest cost self only coverage plan if multiple plans

are offered • 30% of the cost that a 40-year-old non-smoker would pay for

self-only coverage under the second lowest cost Silver Plan on the State or federal health care Exchange

• Spouses participation may not exceed 30% of the total cost of self-only coverage (same for EEs)

8

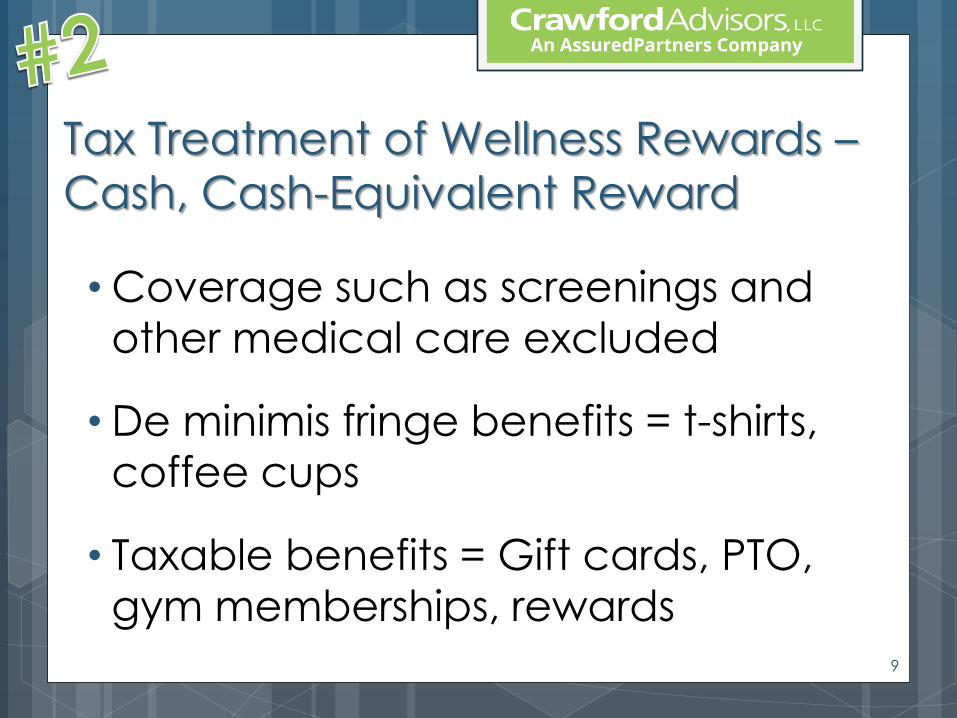

Tax Treatment of Wellness Rewards –

Cash, Cash-Equivalent Reward

• Coverage such as screenings and

other medical care excluded

• De minimis fringe benefits = t-shirts,

coffee cups

• Taxable benefits = Gift cards, PTO,

gym memberships, rewards 9

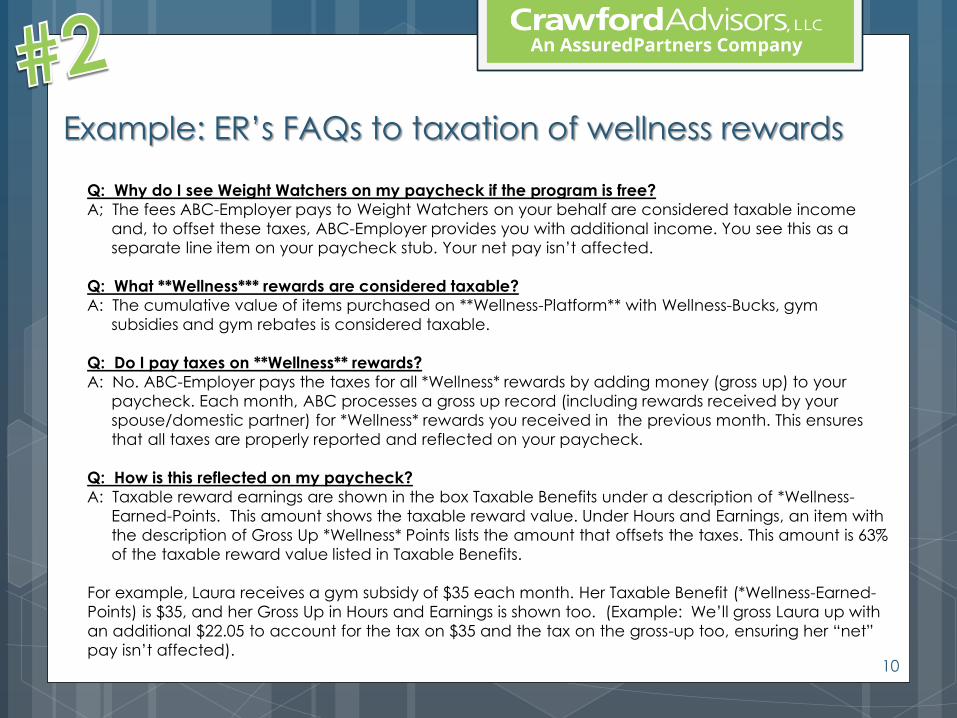

Example: ER’s FAQs to taxation of wellness rewards

Q: Why do I see Weight Watchers on my paycheck if the program is free?

A; The fees ABC-Employer pays to Weight Watchers on your behalf are considered taxable income

and, to offset these taxes, ABC-Employer provides you with additional income. You see this as a

separate line item on your paycheck stub. Your net pay isn’t affected.

Q: What **Wellness*** rewards are considered taxable?

A: The cumulative value of items purchased on **Wellness-Platform** with Wellness-Bucks, gym

subsidies and gym rebates is considered taxable.

Q: Do I pay taxes on **Wellness** rewards?

A: No. ABC-Employer pays the taxes for all *Wellness* rewards by adding money (gross up) to your

paycheck. Each month, ABC processes a gross up record (including rewards received by your

spouse/domestic partner) for *Wellness* rewards you received in the previous month. This ensures

that all taxes are properly reported and reflected on your paycheck.

Q: How is this reflected on my paycheck?

A: Taxable reward earnings are shown in the box Taxable Benefits under a description of *Wellness-

Earned-Points. This amount shows the taxable reward value. Under Hours and Earnings, an item with

the description of Gross Up *Wellness* Points lists the amount that offsets the taxes. This amount is 63%

of the taxable reward value listed in Taxable Benefits.

For example, Laura receives a gym subsidy of $35 each month. Her Taxable Benefit (*Wellness-Earned-

Points) is $35, and her Gross Up in Hours and Earnings is shown too. (Example: We’ll gross Laura up with

an additional $22.05 to account for the tax on $35 and the tax on the gross-up too, ensuring her “net”

pay isn’t affected).

10

QUIZ….

11

A. T-shirts

B. Screenings

C. Gift cards

D. Gym memberships

E. C and D

Which of the following are taxable to

your employees?

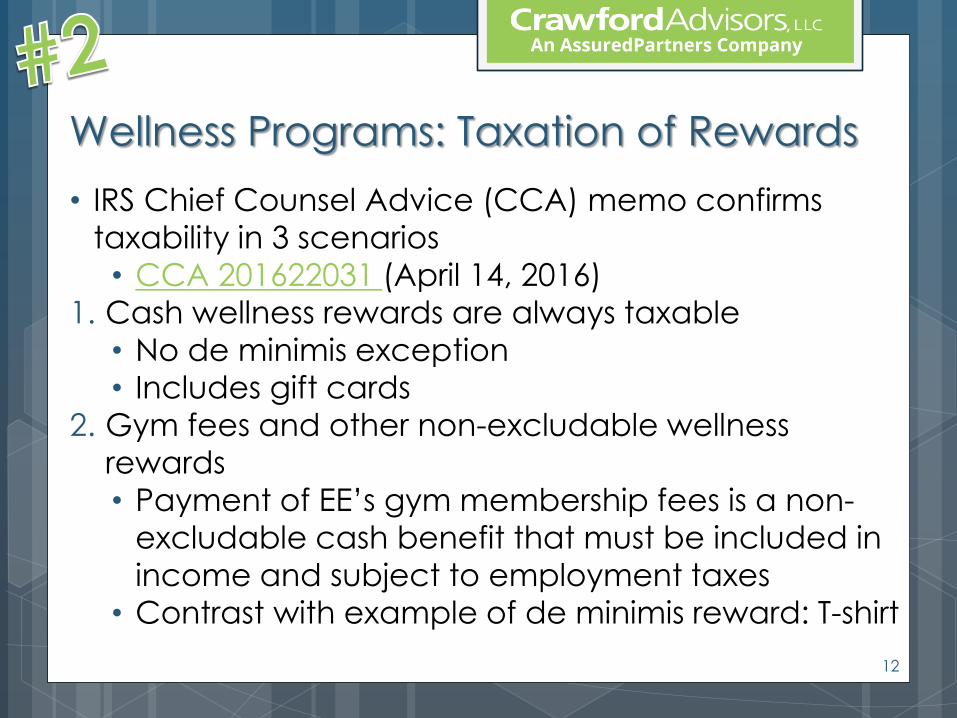

• IRS Chief Counsel Advice (CCA) memo confirms

taxability in 3 scenarios

• CCA 201622031 (April 14, 2016)

1. Cash wellness rewards are always taxable

• No de minimis exception

• Includes gift cards

2. Gym fees and other non-excludable wellness

rewards

• Payment of EE’s gym membership fees is a non-

excludable cash benefit that must be included in

income and subject to employment taxes

• Contrast with example of de minimis reward: T-shirt

Wellness Programs: Taxation of Rewards

12

3. No double-dipping • Imagine - salary reductions taken pre-tax as

“wellness program premiums,” and then returned to the EE as a “premium reimbursement” or “reward”

under the wellness program (e.g., for completing a health risk assessment) • CCA memo confirms that the return of these

amounts to the EE (even if called a wellness

program reward) is taxable income • IRS notes that Rev. Rul. 2002-3 previously

addressed the reimbursement of pretax

premiums, and applies here as well

Wellness Programs: Taxation of Rewards

Tip: There are still fly-by-night brokers/agents selling these plans today. Be careful! 13

• Final SBC template and related materials • Released April 2016; use for first open enrollment period

beginning on or after 4/1/2017

• Changes include: • Streamlined content, E.g., the removal of Q&A about

Coverage Examples, which reduced the template to five (5)

pages (SBC limit remains 8 pages/4 double-sided pages)

• An additional cost example for a foot fracture treated in an

emergency room.

• Updated claims/pricing data for the coverage example

calculator

• Adding disclosures about MEC and MV, including specific

language explaining significance

• Rewording part of the “Important Questions” section

• Underlining any uniform glossary terms used in SBC (may use

hyperlinks in electronic SBCs)

2017 Updates/Changes #3

14

• May 2016 FAQ clarifies flat-fee for electronic copies of

PHI

• Flat fee of up to $6.50 fee is one method for assessing

fees for electronic copies; it is not a limit on

calculating actual cost or average cost under the

other two permitted methods

• Can use different methods for different requests

• Remember (from March 2016 Q&A guidance):

• Costs are limited to: (1) labor to create and deliver

copies; (2) supplies; (3) labor for explanation or

summary (if agreed); and (4) postage

• Always must inform requestor in advance of

approximate fee for requested copies

HIPAA Privacy & Security: HHS FAQ

15

• Resolution agreements continue, including:

• Improper disclosure/disposal of x-rays, PHI: $750,000

• Provider sent x-rays to vendor without BAA

• Disclosure of patient PHI during TV filming: $2.2 million

• Hospital allowed TV crew “virtually unfettered”

access, filming patients without authorization

• Phase 2 audits have begun

• Phase 2 audit protocol released in April

• Updates to audit webpage, including link to pre-

screening questionnaire: http://www.hhs.gov/hipaa/for-

professionals/compliance-enforcement/audit/index.html

• Protocol topics include risk analyses, BAAs, access to

PHI, and periodic security updates

HIPAA Privacy & Security: Enforcement

16

• Written Risk Assessment? • Track all PHI created, received, stored, exchanged?

• HIPAA BAA with all vendors, carriers, claims payers,

consultants?

• HR or IT policies? HIPAA? GLBA? Other privacy regs? • Personnel Files

• Evidence of Insurability

• STD/FMLA paperwork

• Emails / Faxes from EEs, Spouses, Dependents • Payroll software

• Access to HR records

• HR-offices, PCs, printers, faxes – building and electronic

access? • Record retention (onsite & offsite and cloud-based)

HIPAA Privacy & Security: Preparation

17

http://www.crawfordadvisors.com/wp-content/uploads/2016/05/2017_HSA_limits.pdf

HSA, HCFSA, HRA – best approach?

18

2016: $2,600

For 2017, Non-ALEs (smaller

than 50 FTEs) – can offer a

stand-alone-HRA. See the new

21st Century Cures Act.

• Mental health parity

• DOL released non-exhaustive list of NQTLs (Non-

Quantitative Treatment Limitations) that could

violate MHPA/ MHPAEA provisions (if plan does not

impose similar limits on medical and surgical benefits)

• Examples • Preauthorization and pre-service notification

requirements • Fail-first, probability of improvement, and patient

noncompliance provisions

• Written treatment plan

• Residential, geographical, and licensure requirements

Grab Bag – including other Federal Mandates for GHPs

19

• Agency FAQs: Mental health parity; WHCRA

• Mental health parity (3 FAQs) • Parity in quantitative limitations and financial requirements

cannot be calculated across insurer’s book of business; must

be as plan-specific as possible (given available data)

• Explains plan documents that individuals can request (under

ERISA and MHPAEA disclosure rules) to assess a plan’s

MHPAEA compliance for NQTLs

• Confirms MHPAEA applies to medication-assisted treatment

for opioid use disorder

• WHCRA (1 FAQ)

• Clarifies scope of reconstructive surgery coverage • DOL Checklist for Mental Health Parity

• Warning Signs- Plan or Policy Non-Quantitative Treatment Limitations (NQTLs) that Require Additional Analysis to Determine Mental Health Parity Compliance

• https://www.dol.gov/sites/default/files/ebsa/laws-and-regulations/laws/mental-health-parity/warning-signs-plan-or-policy-nqtls-that-require-additional-analysis-to-determine-mhpaea-compliance.pdf

Other Federal Mandates for GHPs

20

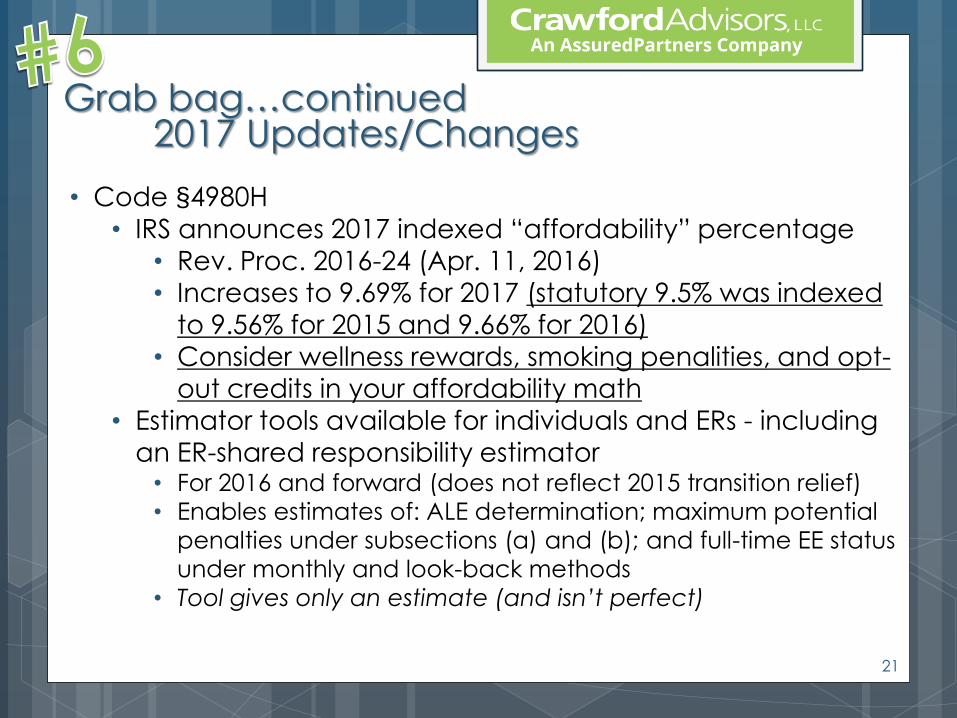

• Code §4980H

• IRS announces 2017 indexed “affordability” percentage

• Rev. Proc. 2016-24 (Apr. 11, 2016)

• Increases to 9.69% for 2017 (statutory 9.5% was indexed

to 9.56% for 2015 and 9.66% for 2016) • Consider wellness rewards, smoking penalities, and opt-

out credits in your affordability math

• Estimator tools available for individuals and ERs - including

an ER-shared responsibility estimator • For 2016 and forward (does not reflect 2015 transition relief)

• Enables estimates of: ALE determination; maximum potential

penalties under subsections (a) and (b); and full-time EE status

under monthly and look-back methods

• Tool gives only an estimate (and isn’t perfect)

Grab bag…continued 2017 Updates/Changes

21

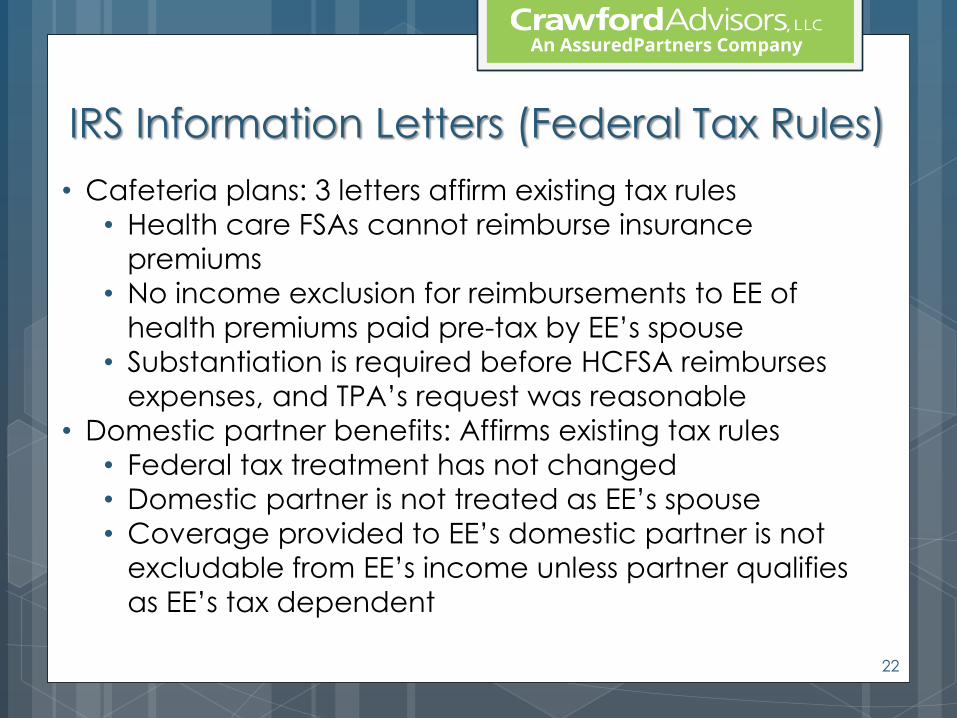

• Cafeteria plans: 3 letters affirm existing tax rules

• Health care FSAs cannot reimburse insurance

premiums

• No income exclusion for reimbursements to EE of

health premiums paid pre-tax by EE’s spouse

• Substantiation is required before HCFSA reimburses

expenses, and TPA’s request was reasonable

• Domestic partner benefits: Affirms existing tax rules

• Federal tax treatment has not changed

• Domestic partner is not treated as EE’s spouse

• Coverage provided to EE’s domestic partner is not

excludable from EE’s income unless partner qualifies

as EE’s tax dependent

IRS Information Letters (Federal Tax Rules)

22

If you have any further questions about the information discussed in this

webinar please feel free to contact us at:

Crawford Advisors, LLC

• HQ: 200 International Circle | Suite 4500 | Hunt Valley, MD 21031

• 1813 Sweetbay Drive | Suite 10 | Salisbury, MD 21804

• 201 King of Prussia Road | Suite 650 | Radnor, PA 19087

• 280 Granite Run Drive | Suite 250 | Lancaster, PA 17601

• 2975 W. Executive Parkway | Lehi, UT 84043

(800) 451-8519 | www.crawfordadvisors.com

Download Slides – www.crawfordadvisors.com/webinars/

Questions & Requests – [email protected]

Questions…

23