37

Academe – Industry Collaboration through the Global Competitiveness Assessment Tool (GCAT) November 5, 2011 NICP, Gen San

| Date post: | 09-Jul-2018 |

| Category: |

Documents |

| Upload: | truonghuong |

| View: | 213 times |

| Download: | 0 times |

Academe – Industry Collaboration through the Global Competitiveness

Assessment Tool (GCAT)

November 5, 2011

NICP, Gen San

The Philippines’ IT-BPO industry has grown rapidly since Road Map 2010 was launched in 2007

Philippine IT-BPO industry size

2006-2009; US$ billion x% YoY Growth

1 Philippines IT-BPO market as percentage of global offshore services market, in revenue terms

Sources: BPAP; Everest analysis

# FTEs

(~„000) 240 300 370 423 525

Global

share1 5% 6% 6% 7% 8%

Impact over 5 years

Contribution

to GDP

4%–5% of annual GDP

Employment

generation

Largest private sector

new job creator

300,000 direct

Up to 0.7 million–

1.0 million indirect jobs

Foreign

exchange

earnings

Significant export

impact

Third-largest export

earner on net value

add basis

Growth of

Next Wave

Cities™

Catalyzed growth of

10+ Next Wave Cities™

adding over 50,000

jobs

~50%

~26%

~14%

~20%

The industry is showing initial signs of diversification beyond traditional areas of strength

Philippine IT-BPO service segments

US$ billion

Philippine IT-BPO source markets

US$ billion

Note: 2006 Split per ICT Survey of IT and ITES; 2010 estimates from Everest-O2P survey

Sources: BPAP; Everest-O2P survey

Voice BPO

Non

Voice

BPO

IT/ESO

3.2 8.9 100% =

U.S.

UK/EU

APAC

3.2 8.9 100% =

Domestic

Philippines has become COE for BPO due to depth of talent available in this sector

Current Services: - Accounting and bookkeeping - Legal Transcription - Account maintenance - Litigation Support - Accounts receivable collection - Content Development - Accounts payable processing -Contract Summarization -Fund adm/reconciliation - Editing, Sub-titling, Translation - Payroll processing - Publishing - Retail banking support -Health Services revenue cycle - Asset management - Travel Services Back Office - Financial analysis and auditing - Credit/Loan processing - Inventory control and purchasing - Health Insurance - Expense and revenue reporting - General Insurance - Financial reporting - Sales and marketing - Human resources administration - Tax reporting - Customer Management - Financial leasing - Credit card administration - Transaction management - Factoring and stock brokering - Sourcing and Procurement - Revenue management - Logistics - Transaction processing - Disaster recovery - Business data processing - Business Intelligence - Database management - Network management - Supply chain management - Warehouse and inventory Mgmt

Arising Services: (KPO) - Market Research and Analysis

- Intellectual Property Management

- Account Risk Management

-Equities/Portfolio research & analysis

3 Copyright ©2010: Business Processing Association of the Philippines. All rights reserved.

It has also spread beyond NCR as credible Tier-2/3 destinations emerge

2007

2010E

Distribution of FTEs by delivery location

Percentage, FTEs; 2007: ~297K; 2010: ~530K FTEs

* Others includes inter-alia Cavite, Baguio, Cagayan de Oro, Davao, Dumaguete, Iloilo, Lipa and Malolos / Bulacan

Sources: BPAP; Everest analysis

Key takeaways

Expansion into Next Wave

towns has increased with

~80,000 FTEs spread

across Tier-2/3 towns

across the country

Rapid growth in

employability across Next

Wave Cities has increased

pool of talent supply in

Philippines

The global offshore services market is growing at a healthy but slower pace, and will more than double by 2016

Global offshore services market size

US$ billion

~2.3 ~2.7 ~3.4 ~3.6 ~7.6 Number of

offshore jobs

(millions)

~3.8

Sources: Everest analysis; NASSCOM

62-74 76-88

94-106 98-110

256-268

IT/ESO

BPO 20-24

42-50

26-30

50-58

34-38

60-68

35-39

63-71 120-124

136-144

105-125

40-45

65-80

CAGR:

~15 %

CAGR:

10-15 %

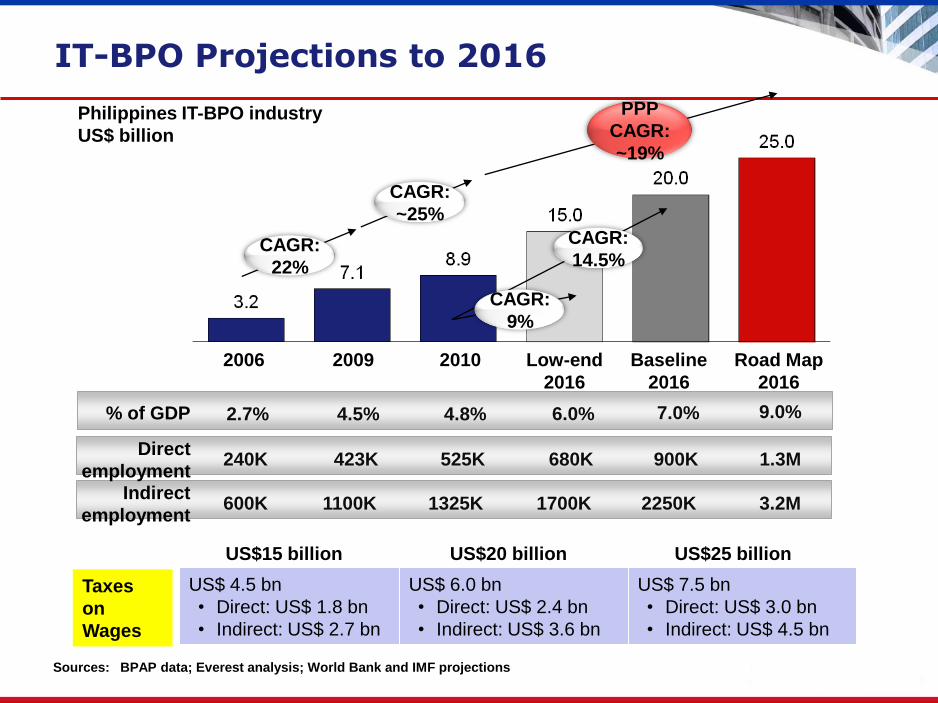

IT-BPO Projections to 2016

Sources: BPAP data; Everest analysis; World Bank and IMF projections

Philippines IT-BPO industry

US$ billion

1325K 2250K Indirect

employment 600K 1100K 3.2M

% of GDP 2.7% 4.8% 7.0% 4.5% 9.0%

1700K

6.0%

2006 2010 2009 Road Map

2016

Baseline

2016

CAGR:

22%

CAGR:

~25%

CAGR:

14.5%

PPP

CAGR:

~19%

Low-end

2016

CAGR:

9%

525K 900K Direct

employment 240K 423K 1.3M 680K

US$ 4.5 bn

• Direct: US$ 1.8 bn

• Indirect: US$ 2.7 bn

US$ 6.0 bn

• Direct: US$ 2.4 bn

• Indirect: US$ 3.6 bn

US$ 7.5 bn

• Direct: US$ 3.0 bn

• Indirect: US$ 4.5 bn

US$15 billion US$20 billion US$25 billion

Taxes

on

Wages

Talent: 2016 talent requirements will reverse the current demand-supply situation by 2011

Effective addressable

supply

440

1,300

2009 Future

employment

(2016E)

3X increase

IT-BPO industry employment

„000s FTEs

Annual Demand and Supply projections of entry-level industry talent –

Philippines IT-BPO

„000 FTEs

Talent demand („Target scenario‟)

Effective addressable Talent supply (as-is)

Source: Everest analysis

Global Competitiveness Assessment Test (GCAT)

(formerly known as BPAP National Competency Test)

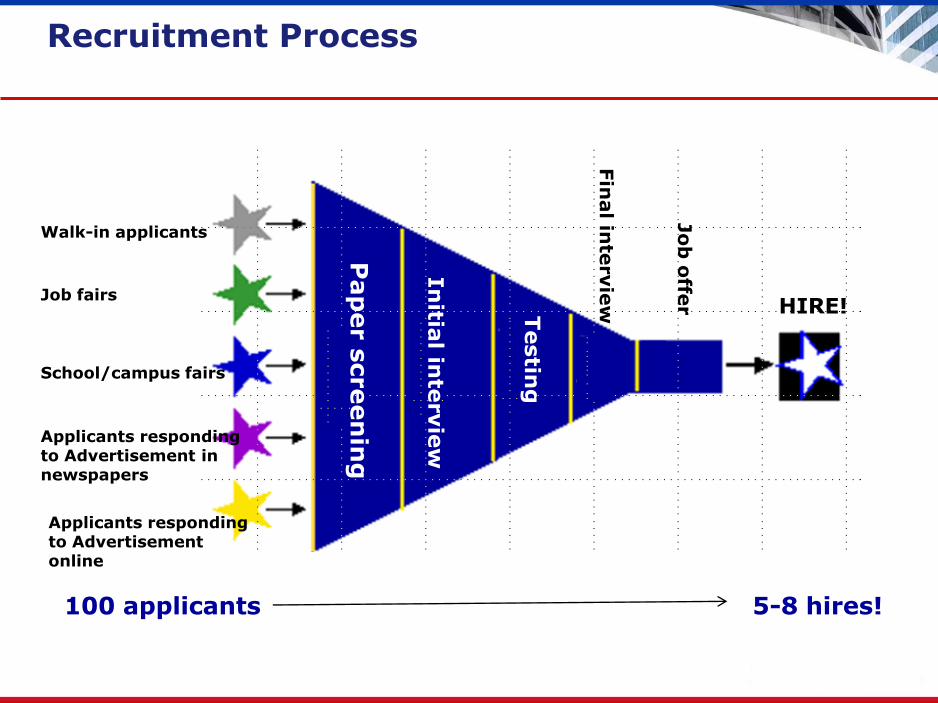

Recruitment Process

Pap

er s

creen

ing

Testin

g

Fin

al in

tervie

w

Job

offe

r

In

itial in

tervie

w

HIRE!

Walk-in applicants

Job fairs

School/campus fairs

Applicants responding to Advertisement in newspapers

100 applicants 5-8 hires!

Applicants responding to Advertisement online

• Hiring qualified people remains the biggest issue facing business

process outsourcing industry today.

• Job mismatch – what does this really mean? The students lack the

required competencies needed for them to get hired.

• What are these competencies, particularly in the IT-BPO industry?

How can we improve competencies if we don’t articulate to the

academe what we are looking for?

Rationale

What is GCAT?

• Industry-initiated assessment program

• Proactively generates industry-ready talents for

the Philippine IT-BPO industry

• Standardizes the competency assessment

system for applicants in the IT-BPO sector

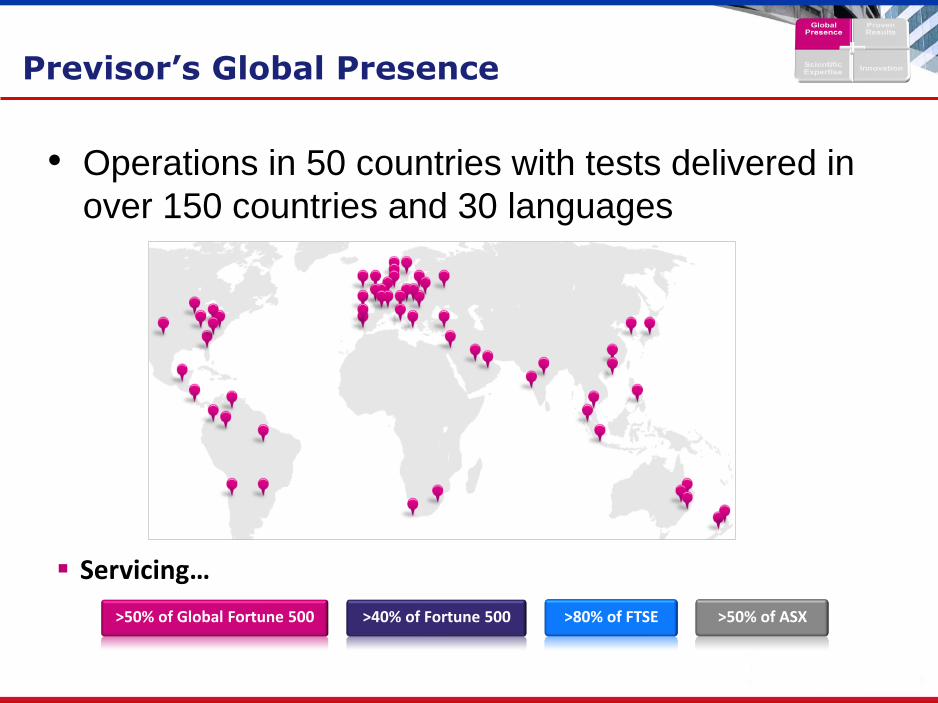

The PreVisorTM Solution

“Best of Breed” - 80+ years

combined experience

Over 45 million tests delivered

138 of Fortune 500 use

PreVisor

Extensive experience in most

industries and job types

• Operations in 50 countries with tests delivered in

over 150 countries and 30 languages

>50% of Global Fortune 500 >40% of Fortune 500 >80% of FTSE >50% of ASX

Servicing…

Previsor’s Global Presence

Companies using Previsor

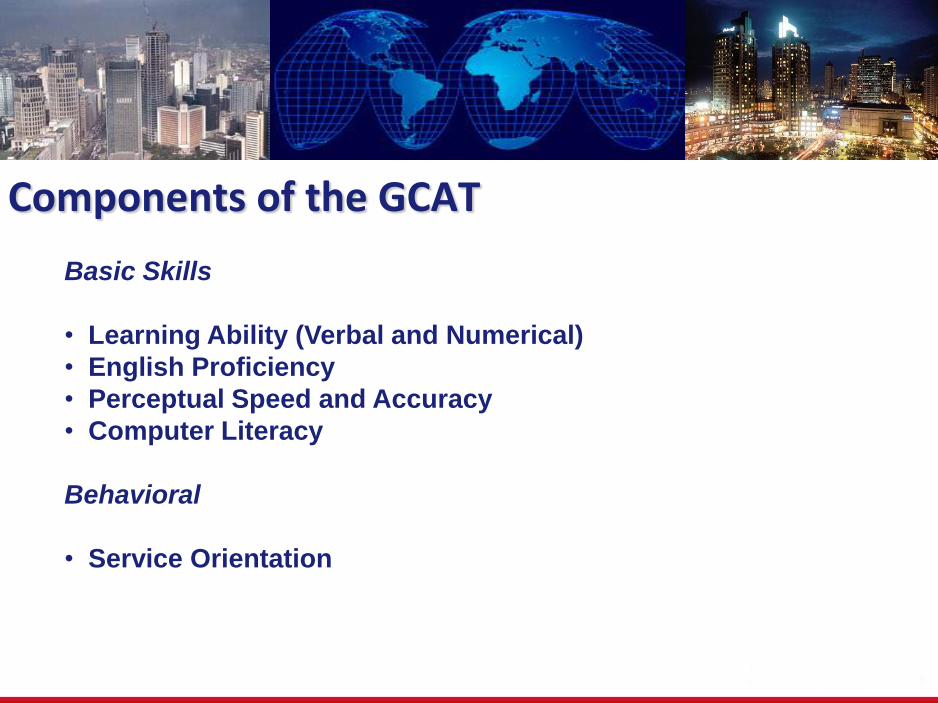

Basic Skills

• Learning Ability (Verbal and Numerical)

• English Proficiency

• Perceptual Speed and Accuracy

• Computer Literacy

Behavioral

• Service Orientation

Components of the GCAT

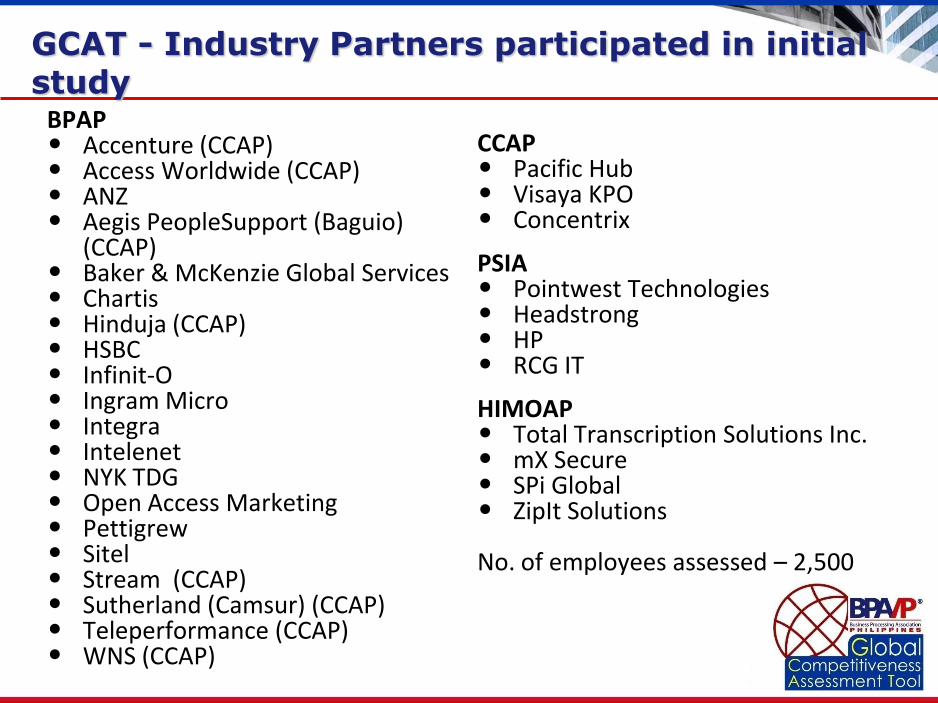

GCAT - Industry Partners participated in initial study

BPAP • Accenture (CCAP) • Access Worldwide (CCAP) • ANZ • Aegis PeopleSupport (Baguio)

(CCAP) • Baker & McKenzie Global Services • Chartis • Hinduja (CCAP) • HSBC • Infinit-O • Ingram Micro • Integra • Intelenet • NYK TDG • Open Access Marketing • Pettigrew • Sitel • Stream (CCAP) • Sutherland (Camsur) (CCAP) • Teleperformance (CCAP) • WNS (CCAP)

CCAP • Pacific Hub • Visaya KPO • Concentrix

PSIA • Pointwest Technologies • Headstrong • HP • RCG IT

HIMOAP • Total Transcription Solutions Inc. • mX Secure • SPi Global • ZipIt Solutions

No. of employees assessed – 2,500

Colleges and Universities participated in 2010-2011 GCAT (NCR)

• Centro Escolar University – Makati • Centro Escolar University – Manila • De La Salle – College of St. Benilde • Emilio Aguinaldo College – Manila • FEU Diliman • FEU Morayta • Jose Rizal University • Lyceum Manila

• Mapua Intramuros • Mapua Makati • National Teachers’ College • STI (Caloocan, Fairview,

Pasay,) • University of Makati • University of Sto. Tomas

BAGUIO • AMA • Saint Louis University • University of Cordilleras • STI – Baguio BULACAN • Centro Escolar University –

Malolos • STI (Balagtas, Baliuag) PAMPANGA • Angeles University Foundation • Holy Angel University • University of the Assumption

LAGUNA/CAVITE/ BATANGAS • De La Salle University –

Dasmarinas • Emilio Aguinaldo College – Cavite • Lyceum Laguna • St. Michael’s College of Laguna • STI (Calamba, San Pablo,

Tagaytay)

Colleges and Universities participated in 2010-2011 GCAT (Luzon)

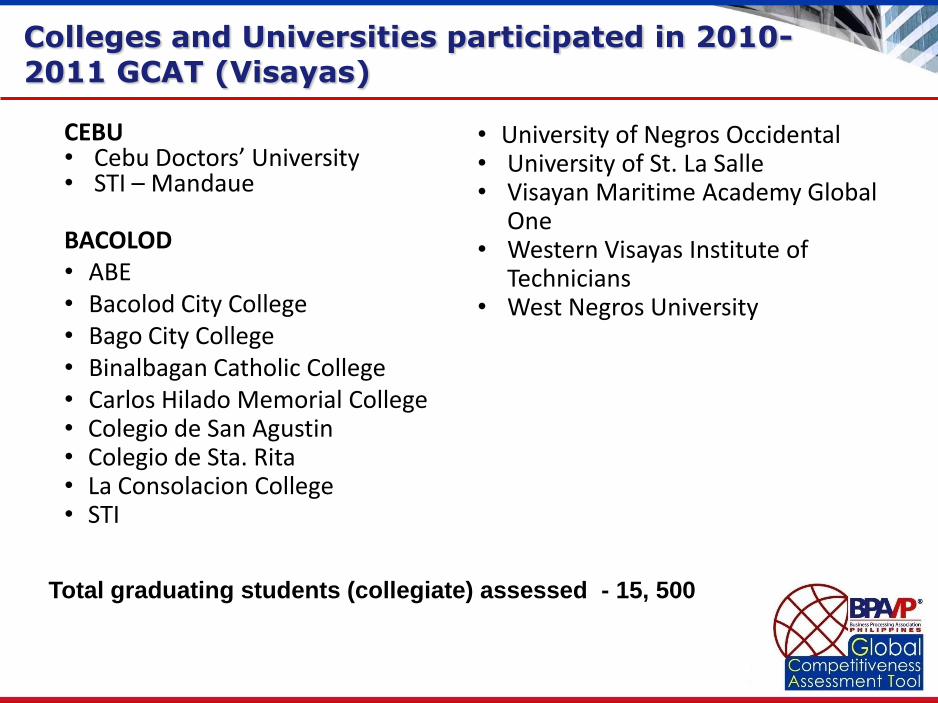

Total graduating students (collegiate) assessed - 15, 500

CEBU • Cebu Doctors’ University • STI – Mandaue BACOLOD

• ABE • Bacolod City College • Bago City College • Binalbagan Catholic College • Carlos Hilado Memorial College • Colegio de San Agustin • Colegio de Sta. Rita • La Consolacion College • STI

• University of Negros Occidental • University of St. La Salle • Visayan Maritime Academy Global

One • Western Visayas Institute of

Technicians • West Negros University

Colleges and Universities participated in 2010-2011 GCAT (Visayas)

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

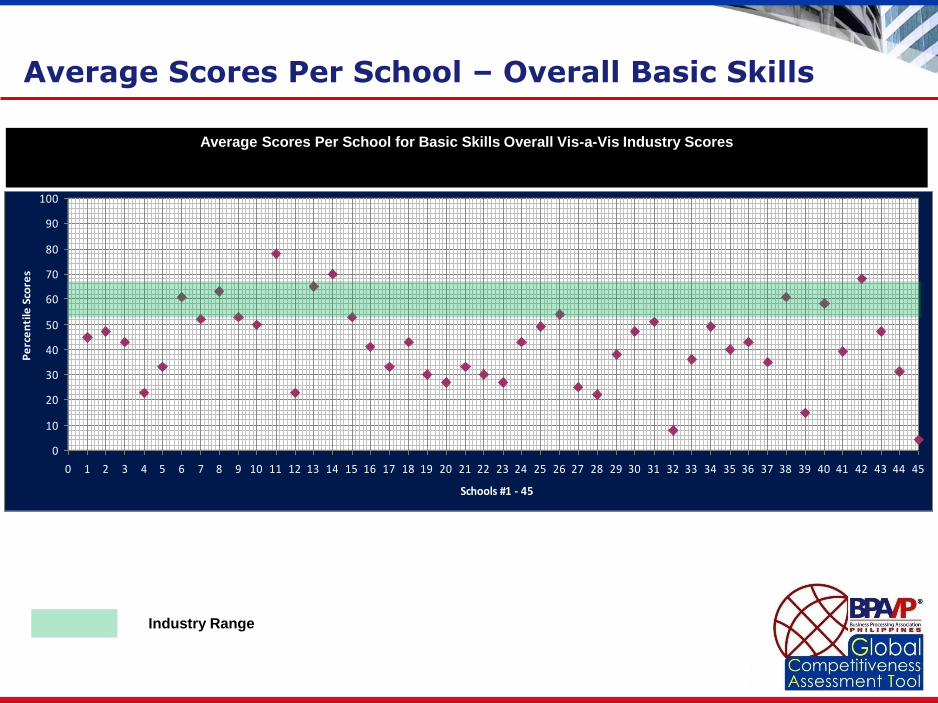

Average Scores Per School for Basic Skills Overall Vis-a-Vis Industry Scores

Industry Range

Average Scores Per School – Overall Basic Skills

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Learning Ability Vis-a-Vis Industry Scores

Average Scores Per School – Learning Ability

* Effective use of verbal reasoning, numerical and analytical reasoning; ability

to learn work-related tasks, information, processes, policies; ability to

perform when working with relatively complex information such as report,

correspondence, and research.

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

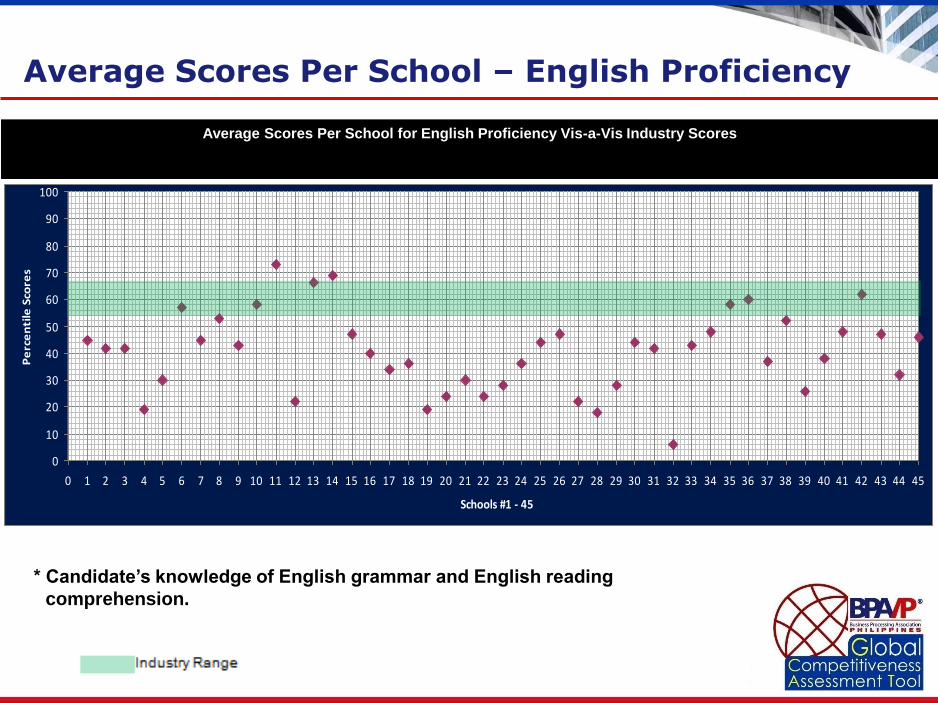

Average Scores Per School for English Proficiency Vis-a-Vis Industry Scores

Average Scores Per School – English Proficiency

* Candidate‟s knowledge of English grammar and English reading

comprehension.

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Computer Literacy Vis-a-Vis Industry Scores

Average Scores Per School – Computer Literacy

* Timed; simulations asking candidates to open, close, save, delete, and

rename files, to access and search the Internet, to send e-mails with

attachments, and to perform other basic Microsoft Windows tasks.

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Perceptual Speed and Accuracy Vis-a-Vis Industry Scores

Average Scores Per School – Perceptual Speed and Accuracy

* Visual comparison test which measure the candidate‟s ability to efficiently

compare information and detect errors.

Key Findings

• Two lowest scores in the competency exam:

– Learning ability

– English proficiency

• Learning ability includes analytical skills and critical

thinking

• English proficiency – interventions at the collegiate level

may not be enough to address current gap between

what is now versus what the industries need

Note: Spoken English is not currently assessed by GCAT

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Behavioral Component Overall Vis-a-Vis Industry Scores

Average Scores Per School – Overall Behavioral Skills

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Communication Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) – Communication*

* Communication: explaining service, keeping the customers informed in language they can

understand and listen to.

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Learning Orientation Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) –Learning Orientation*

* Learning orientation: willingness to learn product and service information

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Courtesy Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) – Courtesy*

* Courtesy: politeness, respect, consideration, access and friendliness of personnel

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Empathy Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) – Empathy*

* Empathy: Knowing the customer and making the effort to understand the customers‟

needs

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

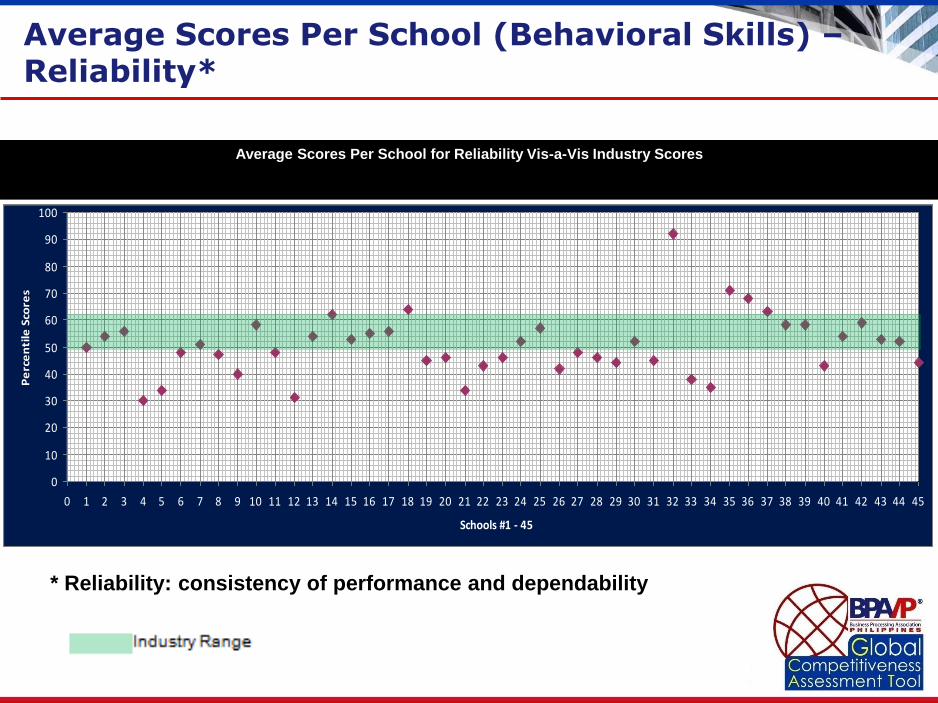

Average Scores Per School for Reliability Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) – Reliability*

* Reliability: consistency of performance and dependability

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Schools #1 - 45

Pe

rce

nti

le S

core

s

Average Scores Per School for Responsiveness Vis-a-Vis Industry Scores

Average Scores Per School (Behavioral Skills) – Responsiveness*

* Responsiveness: willingness and readiness of employees to provide service

Key Findings

• Scores on Service Orientations show intrinsic Filipino

culture of service

• Responsiveness and reliability – components with

highest scores

• Learning orientation and communication – could still be

further improved

0

10

20

30

40

50

60

Learning Ability

English proficiency

Perceptual Speed

Computer literacy

Co

mp

ete

ncy

Sco

res

GCAT Results

Year 2

Year 1

BNCT baseline

Desired Outcome with GCAT (for Schools over time)

• Schools can use GCAT to measure improvement year on year • Industry scores may change over time

GCAT: How Can it Help You?

Thank you!

49