Volume 13, Number 1 Print ISSN: 1544-1458 Online ISSN: 1939-6104 ACADEMY OF STRATEGIC MANAGEMENT JOURNAL SHAWN CARRAHER OXFORD JOURNAL DISTINGUISHED RESEARCH PROFESSOR EDITOR The Academy of Strategic Management Journal is owned and published by Jordan Whitney Enterprises, Inc.. Editorial Content is controlled by the Allied Academies, a non-profit association of scholars, whose purpose is to support and encourage research and the sharing and exchange of ideas and insights throughout the world.

Transcript

Volume 13, Number 1 Print ISSN: 1544-1458 Online ISSN: 1939-6104

ACADEMY OF STRATEGIC MANAGEMENT JOURNAL

SHAWN CARRAHER OXFORD JOURNAL DISTINGUISHED RESEARCH PROFESSOR

EDITOR

The Academy of Strategic Management Journal is owned and published by Jordan Whitney Enterprises, Inc.. Editorial Content is controlled by the Allied Academies, a non-profit association of scholars, whose purpose is to support and encourage research and the sharing and exchange of ideas and insights throughout the world.

Page ii

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Authors execute a publication permission agreement and assume all liabilities. Neither Jordan Whitney Enterprises, Inc. nor Allied Academies is responsible for the content of the individual manuscripts. Any omissions or errors are the sole responsibility of the authors. The Editorial Board is responsible for the selection of manuscripts for publication from among those submitted for consideration. The Publishers accept final manuscripts in digital form and make adjustments solely for the purposes of pagination and organization.

The Academy of Strategic Management Journal is owned and published by Jordan Whitney Enterprises, Inc., PO Box 1032, Weaverville, NC 28787, USA. Those interested in communicating with the Journal, should contact the Executive Director of the Allied Academies at [email protected].

Copyright 2014 by Jordan Whitney Enterprises, Inc., USA

Page iii

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

EDITORIAL REVIEW BOARD

Peter Antoniou California State University San Marcos

Stephanie Huneycutt Bardwell Christopher Newport University

James Bishop New Mexico State University

ThomasBox Pittsburg State University

Marty Bressler Southeast Oklahoma State University

Steve Brown Eastern Kentucky University

Richard Caldarola Troy State University

Eugene Calvasina Southern University

Shawn Carraher Minot State University

Robert Carton Western Carolina University

Beth Castiglia Felician College

John James Cater Louisiana State University

Ronald Cheek University of Louisiana at Lafayette

Iain Clelland Radford University

Meredith Downes Illinois State University

Thomas Garsombke Claflin University

Edward Haberek Briarwood College

Paul Jacques Western Carolina University

Raghu Korrapati Walden University

Rick Koza Chadron State College

Catherine Levitt California State University at Los Angeles

Chris Lockwood Northern Arizona University

Lee Makamson Hampton University

Terry Maris Ohio Northern University

James Maxwell Indiana State University

David McCalman University of Central Arkansas

Page iv

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

EDITORIAL REVIEW BOARD

James McLaurin American University of Sharjah

Mohsen Modarres Humboldt State University

Chynette Nealy University of Houston-Downtown

John Kalu Osir Washington State University

Mildred Golden Pryor Texas A&M University-Commerce

Oswald Richards Lincoln University

Stanley Ross Bridgewater State College

Robert Scully Barry University

Claire Simmers Saint Joseph's University

Prasanna Timothy Karunya Institute of Technology & Sciences

Jennifer Villa New Mexico State University

Page v

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

TABLE OF CONTENTS EDITORIAL REVIEW BOARD .................................................................................................. III LETTER FROM THE EDITOR .................................................................................................. VII A PRELIMINARY EXAMINATION OF SUSTAINABLE DISCLOSURES ON FORTUNE 500 COMPANY WEBSITES ......................................................................................................... 1

Michelle B. Kunz, Morehead State University Janet M. Ratliff, Morehead State University Marlene Blankenbuehler, Morehead State University Traci Bard, Morehead State University

DOES COMPANY SIZE AFFECT MISSION STATEMENT CONTENT? .............................. 21

Darwin L. King, St. Bonaventure University Carl J. Case, St. Bonaventure University Kathleen M. Premo, St. Bonaventure University

SIX SIGMA IMPLEMENTATION BY INDIAN MANUFACTURING SMES - AN EMPIRICAL STUDY ............................................................................................................ 35

A. Raghunath, Centre For Research, Anna University, Chennai R.V. Jayathirtha, Bullseye Consulting Group, Bangalore

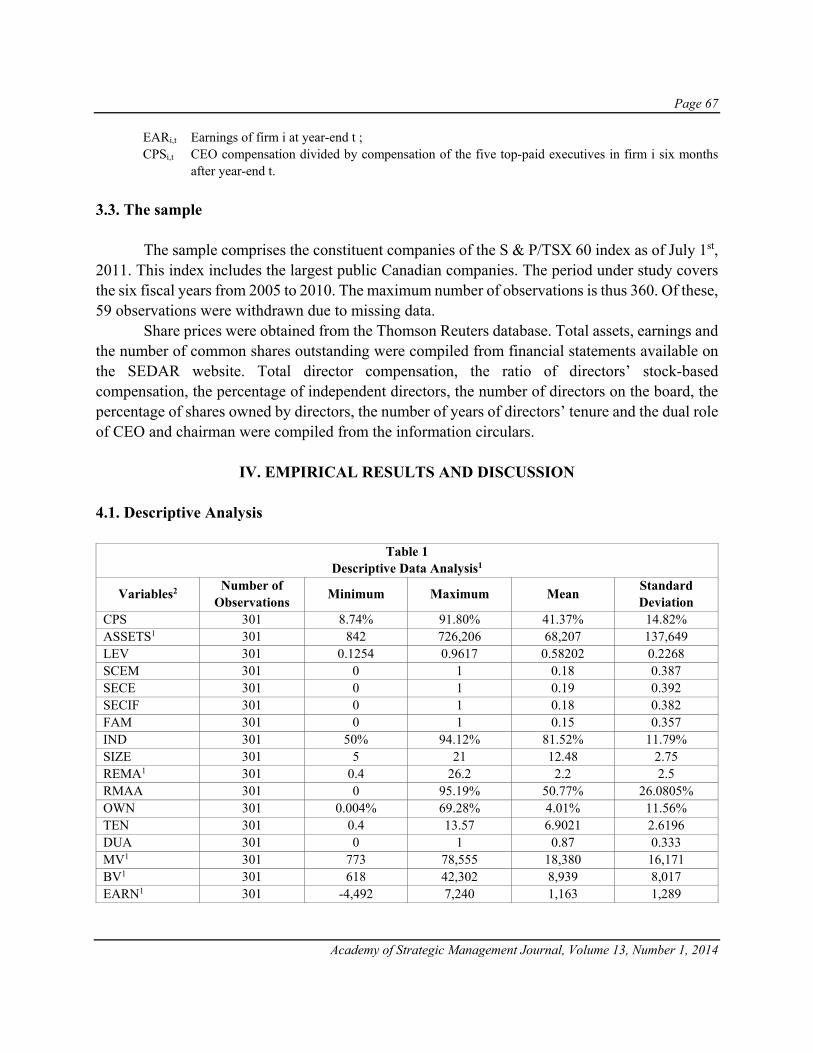

CEO’S SHARE OF TOP-MANAGEMENT COMPENSATION, CHARACTERISTICS OF THE BOARD OF DIRECTORS AND FIRM-VALUE CREATION .......................................... 57

Sébastien Deschênes, University of Moncton Mohamed Zaher Bouaziz, University of Moncton Tania Morris, University of Moncton Miguel Rojas, University of Moncton Hamadou Boubacar, University of Moncton

RESOURCE VALUE AS A SOURCE OF NEGOTIATING POWER: DETERMINANTS OF ALLIANCE FUNDING AMOUNTS IN THE US BIOTECH INDUSTRY. .............................. 75

Paul Forshey, High Point University

Page vi

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

SERVANT LEADERSHIP, HUMANE ORIENTATION, AND CONFUCIAN DOCTRINE OF JEN .................................................................................................................... 97

Mary Jo Hirschy, Taylor University Doris Gomez, Regent University Kathleen Patterson, Regent University Bruce E. Winston, Regent University

DETERMINANTS OF INTERFIRM RIVALRY OR COOPERATION: IMPLICATIONS FOR MANAGEMENT .................................................................................. 113

William T. Jackson, University of South Florida St. Petersburg Terry Nelson, University of Alaska, Anchorage Lei Gao, University of Memphis Jeffrey A. Krug, Loyola University New Orleans Peter Wright, University of Memphis

BOARD HETEROGENEITY: DOUBLE-EDGED SWORD? FOCUSING ON THE MODERATING EFFECTS OF RISK ON HETEROGENEITY-PERFORMANCE LINKAGE .................................................................................................... 129

Kong-Hee Kim, St. Cloud State University

Page vii

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

LETTER FROM THE EDITOR Welcome to the Academy of Strategic Management Journal. The Journal is owned and published by Jordan Whitney Enterprises, Inc.. The Editorial Board and the Editors are appointed by the Allied Academies, Inc., a non profit association of scholars whose purpose is to encourage and support the advancement and exchange of knowledge, understanding and teaching throughout the world. The editorial mission of the Journal is to advance the field of strategic management. To that end, the journal publishes theoretical and empirical manuscripts pertaining to the discipline. The manuscripts contained in this volume have been double blind refereed. The acceptance rate for manuscripts in this issue, 25%, conforms to our editorial policies. Our editorial review policy maintains that all reviewers will be supportive rather than destructive, helpful versus obtrusive, mentoring instead of discouraging. We welcome different points of view, and encourage authors to take risks with their research endeavors. The Editorial Policy, background and history of the organization, and calls for conferences are published on our web site. In addition, we keep the web site updated with the latest activities of the organization. Please visit our site at www.alliedacademies.org and know that we welcome hearing from you at any time.

Shawn Carraher Oxford Journal Distinguished Research Professor

Page viii

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Page 1

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

A PRELIMINARY EXAMINATION OF SUSTAINABLE DISCLOSURES ON FORTUNE 500 COMPANY

WEBSITES

Michelle B. Kunz, Morehead State University Janet M. Ratliff, Morehead State University

Marlene Blankenbuehler, Morehead State University Traci Bard, Morehead State University

ABSTRACT

An exploratory study of the sustainable information posted on Fortune 500 corporate

websites found differences in the sustainable actions of these companies based upon industry, and the size of the firm. Findings of the study also indicate that more than three-fourths of the companies examined engage in one or more sustainable actions. Additionally, researchers present suggestions for future analysis and review of publicly available corporate sustainability information and present questions for consideration in future research.

BACKGROUND

Sustainability has been termed an emerging megatrend (Lubin & Esty, 2010), as the environmental issues have steadily increased in the list of issues corporate executives consider when reporting corporate standing, as well as finding ways to create value for stakeholders. Furthermore, Holden (2012) cites a 2011 McKinsey survey that indicated one third of respondents indicated the top reason for pursuing sustainability initiatives was to lower operations costs and improve efficiency. This is also supported by Heffes (2010) as she reports that sustainability and green initiatives have a place in corporate strategy, but corporate executives still have difficulty conveying to their stakeholders how such actions create value. Finally, Stafford and Hartman (2013) echo these sentiments, stating that today’s corporations recognize the value of increasing sustainability. The authors cite reduced costs and risks, preservation of resources, goodwill among regulators, stockholders, customers and other stakeholders. Thus business understands how sustainability will benefit the corporation, but still need to convey these benefits to stakeholders. Corporations recognize that it is imperative they meet stakeholder expectations, while addressing sustainability, however Ballou, Heitger, Landed and Adams, (2006) also emphasize business must demonstrate how sustainability also creates social and environmental value. In order to operationalize these efforts, essentially organizations are systematically implementing eco-effective management practices that are strategic in nature (Huppes & Ishikawa, 2005). Burnett, Skousen and Wright (2011) found empirical evidence to support the proposition that sustainable

Page 2

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

corporate effort goes beyond just environmental impact, to create long-term value for shareholders and the firm as well.

The push to provide information regarding sustainable actions and corporate social responsibility can be traced back to the social movements of the 1960s and 1970s (Kleine & von Hauff, 2009). In 1987 the Brundtland Report (Casimir & Dutilh, 2003) introduced the concept of sustainable development, stating that the needs of the present should be met without compromising the ability of future generations to meet their needs. By 1992, the United Nations Conference for Environment and Development was globally accepted (Kleine & von Hauff, 2009). Research in the area also has a history dating back to the 1970s (Montiel, 2008). Articles at that time addressed corporate social responsibility (CSR), while a couple decades later corporate sustainability (CS) began to appear. More recently, 2000-2005, articles that focused on environmental management (EM), were greater than the number of CSR and CS articles combined. Additionally, the Academy of Management implemented initiatives in this direction, including special issues of the Academy of Management Review and the Academy of Management Journal. As these topics merge and take a permanent place on the business agenda, it necessary to examine how corporations are disseminating information about their sustainable activities. In fact, there were 7,700 companies in 130 countries that voluntarily signed the UN global compact in 2008 (Lozano, 2012), and by 2010 this number had increased to 10,000 companies in 130 countries ("Overview of the UN Global Compact," 2011).

DEFINITION OF TERMS

In 1996, The International Organization for Standardization defined a corporate environmental policy as a “statement by the organization of its intentions and principles in relation to its overall environment performance”(Ramus & Montiel, 2005) . In turn, this provided the framework necessary to set environmental objectives and targets and allow corporations to commit to implementation of proactive policies aimed at sustainability. Yet today, confusion exists in terminology and definition of sustainability and related issues. Sustainability, environmental sustainability, sustainable development, corporate social responsibility, as well as corporate responsibility and corporate sustainability are all used, with similar, while varying definitions (Roca & Searcy, 2012). In some instances, terms are used interchangeably, and definitions can be as varied as the terminology used. Dilling (2010) indicated that there is no globally accepted definition of CSR or sustainability reporting. To add to this confusion, while many consider sustainability from the ecological or environmental perspective, others address sustainability from the “triple bottom line” approach, with the three dimensions of economic/financial, environmental and social responsibility (Montiel, 2008). Montiel continues by positing that CSR and CS are converging, with environmental issues a subset of CSR. Thus, corporate social responsibility could or would include an environmental/corporate sustainability component. This perspective of sustainability as a component included in corporate social responsibility is supported by others as

Page 3

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

well (Dilling, 2010; Katrinli, Gunay, & Biresselioglu, 2011; Matthews & Rusinko, 2010; Shih-Fang & Her-Jiun, 2007). Sustainability is part of the corporate vision for companies in which it is integrated across the business functions of the organization (Lubin & Esty, 2010), and as such may be integrated into annual reports or other reporting mechanisms of the corporate reporting function. To further add to the confusion, corporate reports also use various names, such as corporate responsibility or social responsibility, as well as sustainability report (Roca & Searcy, 2012).

CORPORATE EXAMPLES

Sustainability efforts have been implemented and integrated across many companies (Lubin & Esty, 2010). Some examples include: DuPont’s attempt to become more eco-efficient through “zero waste” and increased future earnings by removing businesses with large eco-footprints from their operations. Coca-Cola for example, created new packaging which was modified to be more light-weight and saves the company tens of millions of dollars. By 2015 their new vending machines are to be HFC-free, reducing greenhouse gas emissions by 99%. Walmart launched Sustainability 360 initiative with goals of creating zero waste, cutting greenhouse gas emissions, purchasing 100% renewable energy, and selling products that sustain the environment and world resources. Companies are adopting sustainability approaches that create more efficient operations, positively affect the bottoms line, and engage outsiders to consider sustainability (Lubin & Esty, 2010).

The technology industry seems to be leading the charge, while banking and the oil and gas industries are poor performers. However, the report which identified the top 25 Global Corporate Reputation index included companies from across the board. Some of those identified as good corporate citizens were: Adidas, Apple, Avon, Bosch, Canon, Coca-Cola, Danone, Electrolux, Ford, Google, Heinz, Honda, Lego, McDonald’s, Microsoft, Nestle, Mike, Nokia, Phillips, Puma, Sharp, Sony, Toshiba, Via and Volkswagen. Other corporations identified for their sustainability efforts include Campbell’s Soup (Kruschwitz, 2012a), Dell (Kruschwitz, 2012b), Johnson & Johnson (Borkowski, Welsh, & Wentzel, 2010), as well as Coca-Cola’s water stewardship program (Walsh & Dowding, 2012). Wal-Mart has invested heavily in sustainability, both within the corporation itself, both in-store as well as in productions facilities (Ladd, 2010). Furthermore, Wal-Mart has been aggressive in promoting sustainability in the processes of suppliers worldwide.

Intel is the largest purchaser of green power in the U.S (Kruschwitz, 2012c). According to Intel, sustainability creates value in four ways: brand value, operational excellence and cost savings, revenue and new market opportunities, and risk management. Intel realizes sustainability efforts may increase costs but has been willing to spend more on green energy as a way to increase future demand and long-term value for their company. To deal with sustainability–related issues, Dell has created a hub within the company (Kruschwitz, 2012b). Four individuals report to a director of sustainability. The areas in which they focus include: 1) environmental strategy, 2) social strategy, 3) operational strategies, and 4) services organization which focuses on

Page 4

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

performance and bottom-line effects. One goal reached by Dell included reducing power consumption of desktops and laptops by 40%. Also, packaging goals of the company follow three C’s created by the company: 1) cube, reduce the size of the package, 2) content – make the materials used more sustainable, and 3) curb – package materials are recyclable or compostable. Greif, a leading manufacturer of industrial packaging indicates four keys to their sustainability agenda: 1) attention to sustainability by top management, 2) approach to sustainability collaboration, 3) business model innovation, and 4) new internal organizational structures (Kiron, Kruschwitz, Reeves, & Goh, 2013). In a survey created by Greif to analyze the response to sustainability within its business model, results indicated that 48% of the companies changed their business model, 46% said the sustainability activities added to profits. Additionally, of the half of survey respondents who made three to four changes to their business model, they profited from their sustainability activities in comparison to only 37% of those who only changed one aspect of their business model. Lastly, Timberland positions sustainability as the triple bottom line by focusing on what they refer to as the four pillars (Kruschwitz, 2013). These pillars include building sustainable living environments at their factories, community service and greening communities, corporate footprint, and product footprint.

Companies implementing corporate sustainability are creating stronger sustainability efforts that go beyond eco-efficiency and pollution control (Young & Tilley, 2006). Kraft collaborated with a company called TerraCycle that rewards consumers for returning non-recyclable packaging. Kraft wanted to divert packaging that was unable to be recycled from going to landfills. By working with TerrCycle they were able to raise their brands’ profile and influence consumers to make better choices (Kruschwitz, 2012d). Kraft Foods Group, Inc. employs business teams worldwide to reduce the Kraft’s global environmental impact (Kruschwitz, 2012d). Efforts include sustainable agriculture practices which have been used for almost two decades, with coffee. In addition, the company has committed to invest in sustainable cocoa farming in Ghana. Furthermore, the company has taken action to reduce CO2 emissions, decrease needed water for processes, reduced waste, as well as the poundage of packaging and removed 60 million road miles from the transportation and distribution network.

Some corporations embrace sustainability after pressure from consumers (Fromartz, 2009). Nike is one example, after criticism of the labor practices of suppliers put pressure on the company. The company’s response to these concerns led to further questions about Nike’s product design and manufacturing processes. This resulted in a goal of zero waste as one of several long-term goals for 2020, and a product line (named Considered), and production and design standards (named Considered Design) which reduce waste, cut energy use and slash the use of solvent. While Wal-Mart still has detractors of the corporation’s stand on sustainability, it all began when consumer pressure in 2005, led to the development of Wal-Mart’s Sustainability Index (Merchant, 2009), a complex plan to measure the sustainability of every product it sells. This effort resulted in collaboration with suppliers and supply chain partners to move toward zero waste initiatives. The goal is to provide consumers with a scorecard for over 100 product categories. According to

Page 5

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

the Wal-Mart corporate website, the goal was to have this available by the end of 2012 ("Sustainability Index," 2012).

CONSUMER INTEREST

For many companies, communicating the company’s focus on sustainability by addressing corporate actions has become a significant part of the corporate agenda (Reilly, 2009). Greening efforts that lead to aggressive cost cutting and reduction of the carbon footprint can help companies be successful and at the same time produce a healthy revenue stream (Ladd, 2010). Consumers also want to know about green products, and corporate practices. However, corporate communications must feel authentic, especially concerning sustainability actions (Watson, 2011). The so-called “green consumer” prefers green products and services (Oates et al., 2008), and therefore values truthful information from companies about their sustainable practices.

While business understands the sustainable imperative, research (Stafford & Hartman, 2013) indicates only about 5% of consumer purchasing is truly environmentally conscious. Thus corporations need to address how they can appeal to consumers, and impact consumer choice behaviors. By providing transparent information to consumers, perhaps in easily and frequently accessed information sources, i.e. the corporate webpage, more consumers can be convinced of the importance of sustainability. Approximately one-fifth of US adults believe a majority of businesses are committed to improving the environment by implementing sustainable business practices and/or offering environmentally-friendly products and services (Loch & Buhay, 2012). This percentage of concerned US consumers has increased from 16 and 17 percent in 2010 and 2011, respectively. While consumers may not believe corporations are committed to becoming sustainable, the majority (71%) are interested in learning what companies are doing regarding sustainable actions.

A series of annual Harris Interactive surveys report changing trends in consumer attitudes and actions. In 2008, ("SCA Survey Conducted by Harris Interactive(R) Shows That Despite a Weakened Economy, U.S. Consumers Willing to Spend Green to Go Green," 2008) consumers indicated that they were willing to pay more for environmentally-friendly products such as: hybrid cars, organic, fair trade or locally sourced food, green/organic cleaning supplies, and products made from recycled materials. On the average, consumers indicated they were willing to spend 17-19% more on green products. Additional findings indicate that consumers are better informed about what makes products and services environmentally-friendly, indicating use of product ingredients, third-party seal of approval, and an environmental statement on the product package. The 2011 (Steinberg, 2011) poll found that fewer US adults were likely to engage in “green actions, ” less likely to express green attitudes, as well as to have adopted typical environmental activities such as purchasing Energy Start appliances, recycling electronics, switching from bottled to tap water or purchasing a hybrid or more fuel-efficient car. Despite these lower numbers, a small

Page 6

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

group of committed US adults are more likely to describe themselves as conservationists, “green,” and environmentalists, than they were the previous year.

The 2012 poll (Steinberg, 2012) found a continued decrease in the likelihood of consumers to incorporate sustainable actions in their daily lives, as well as fewer of them likely to describe themselves as environmentally-conscious. Only about 1 in 3 Americans say they are concerned about the planet, and what will be left for future generations. However, as with the 2011 poll, a higher percentage of a minority of Americans continue to describe themselves as conservationists, “green” or environmentalists. Pollsters surmise that over the past several years, the economic environment has had a significant impact on consumer attitudes and actions. Unfortunately, some of these failures may be costing consumers more of their dollars, as actions such as buying in bulk and recycling, could in fact save them money, as well as leaving a cleaner/sustainable planet for future generations.

Another 2012 survey ("SCA Survey Finds Two-Thirds of American Adults Purchase Green Products," 2012) seems to contradict the negative findings of the Harris polls. This survey found that more than two-thirds (69%) of Americans purchase green products, and almost half of those who do, make these purchases because they believe it is better for the environment. Forty-two percent of those surveyed believe the green movement is just getting started. Perhaps even more important to corporate executives, more than 80% of these consumers consider themselves to be knowledgeable about which companies and brands have a strong history of sustainability, and consider the history of a company’s sustainable actions when making a purchase.

ONLINE INFORMATION

The corporate website is the most frequently used medium to engage CSR communication (Morhardt, Baird, & Freeman, 2002). Eighty percent of Fortune 500 companies mentioned their involvement in corporate socially responsibility actions. Furthermore, brand web sites are the best means of influencing attitudes and perceptions. Rowbottom and Lymer (2009) also suggest the need to use the corporate web site to communicate and legitimize sustainable activities. These authors indicate the UK companies have the highest level of reporting in the world. Sustainability practices and strategies are also being reported on thousands of global organization corporate websites (Sobhani, Amran, & Zainuddin, 2012). Posting sustainability reports online provides easy access for consumers, and is cost-effective for corporations (Morhardt, 2010). Furthermore, KLD Research Analytics, Inc. has developed social responsibility indexing based upon environmental communication and reporting of corporate best practices, to assist investors desirous of investing in socially responsible companies.

KLD Research Analytics, Inc. created a methodology, which includes companies in its social responsibility indices that have been researched and screened to assist investors who are socially responsible in selecting companies also included in that category (Delmas & Blass, 2010). The analysis of reporting and transparency indicators was based on information available on the

Page 7

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

firm’s website and environmental/social responsibility reports. Toyota for example includes their sustainability report on their web pages for anyone to view (Ketola, 2010). Since 2001 BP has disclosed sustainability and operation information in their Health, Safety, and Environment (HSE) charting tool and in annual reports posted on their website. Shell created a separate link on their website that included additional information that was not included in their sustainability report (Dragomir, 2012). Also, Intel has created a specific website called ExploreIntel.com, which provides year-round real-time reporting of CSR activities (Kruschwitz, 2012c). Constant and repeated communication of environmental and social importance of sustainability must be emphasized to reach and change the culture throughout an organization (Epstein, Buhovac, & Yuthas, 2010).

PURPOSE

The purpose of this paper is to examine what the Fortune 500 companies are reporting on their websites regarding their environmental sustainability activities. After determining the current state of sustainability reporting, we will develop a proposal for future, more detailed research. Several research studies that analyzed annual reports as well as sustainability reports vary by industry, and could be correlated to the industry in which the company engages. Oil and gas, chemical and non-chemical manufacturing companies were more likely to adopt environmental policies than service industries (Ramus & Montiel, 2005). However, oil and gas companies were not likely to implement a policy reducing use of fossil fuels. Another study, (Roca & Searcy, 2012) determined the number of indicators reported differed by industry, with engineering, construction, chemical, banks, as well as oil and gas sectors reported a high number of indicators. Conversely, finance, retail and the food industry reported few indicators in their annual reports and/or accountability reports. Hubbard (2011) also indicates the U.S. food industry is far behind in what they include in sustainability reports. In fact, Hubbard states that overall, the US is far behind Europe in sustainability reporting. He concluded that most US companies are more concerned with presenting a positive image, that sustainability reports are more marketing documents rather than true sustainability reports, and determined a great deal of the information would be classified as greenwash. In addition to the impact of industry, Morehardt, Baird and Freeman, (2002) found the adoption of an environmental policy is associated with firm size, and that large, well-financed firms are more likely to adopt an environmental policy.

Based upon these findings, this research is an exploratory study designed to examine what types of sustainable activities companies report on their website. We established eight categories of sustainable actions companies might report: adapting methods of producing their products (product) to be a sustainable product; changing methods and operations of production (production) to be more sustainable and environmentally responsible; implementing facility design and operations changes to be more environmentally sustainable (plant); being innovative and proactive with members of the supply chain and logistics operations to increase sustainable practices (supply

Page 8

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

chain); facilitating recycling actions across the organization (recycle); providing the means and opportunity for their customers and consumers to recycle or otherwise act in a more environmentally sustainable way (consumer); using social and community engagement to encourage consumers to be more environmentally responsible (social); and finally, if the website material was deemed to be more promotional and image building, rather than providing actual procedures that are sustainable the site was labeled as greenwashing (greenwash). Since both the size of the corporation and the relevant industry appear to be influential in sustainability reporting, the companies were placed in quintiles, based upon Fortune 500 ranking, and categorized by industry. The companies are classified by Fortune into 65 different industries, many with only five or fewer companies. For the purpose of this analysis, published industry categories were collapsed into twelve more generalized categories. Finally, the number of different types of sustainable activities reported by the individual corporations was summed into a new variable (Green), with a range of 1-7. Research Questions

The research questions this study attempts to answer are:

1. What sustainable actions are Fortune 500 companies reporting? a. (product, production, plant, supply chain, recycle, consumer, social, greenwash)

2. How many of the Fortune 500 companies report one or more of these sustainable actions? 3. Does the industry in which the company operates influence what sustainable actions they report? 4. Does size of the firm (Fortune 500 ranking) influence what sustainable actions the companies report?

PRELIMINARY METHODOLOGY

The corporate websites for each company listed on the 2011 Fortune 500 list were

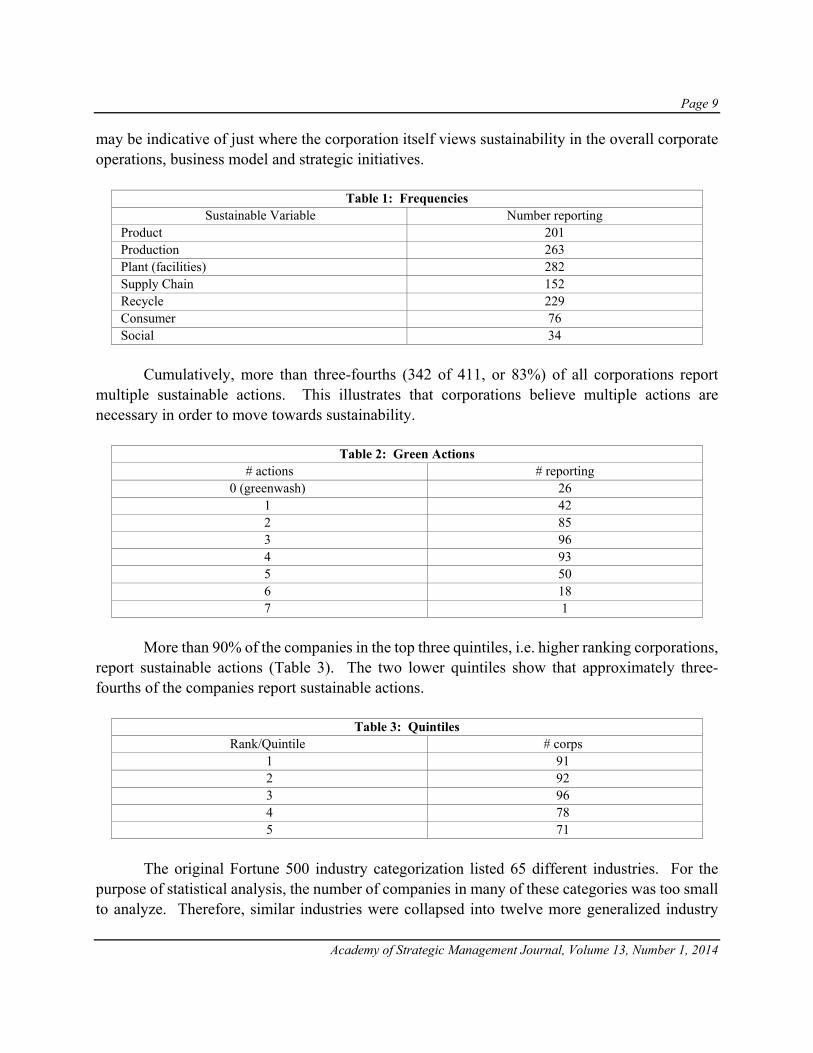

reviewed by three trained data collectors. Each data collector analyzed the corporate website for publicly posted information regarding sustainable activities. This was usually posted under corporate information, and in some cases termed sustainability policy, or was found in social responsibility. After all data were collected individually, a fourth researcher compared the responses and determined a point of agreement. If the three data collectors’ reviews were consistent, then this was deemed correct; if however there were difference, these sites were re-analyzed by the fourth researcher, in consultation with the data collector and reconciled. A total of 411 companies had information posted about their sustainable actions. As noted in Table 1, very few corporations included actions that provided consumers an opportunity to be sustainable, as well as using social means to encourage sustainable actions. However, when it came to the plant or facilities, or actual production operations, over one half of corporations’ efforts were found to be in these initiatives closely followed by recycling efforts and the product itself. These results

Page 9

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

may be indicative of just where the corporation itself views sustainability in the overall corporate operations, business model and strategic initiatives.

Table 1: Frequencies Sustainable Variable Number reporting

Product 201 Production 263 Plant (facilities) 282 Supply Chain 152 Recycle 229 Consumer 76 Social 34

Cumulatively, more than three-fourths (342 of 411, or 83%) of all corporations report

multiple sustainable actions. This illustrates that corporations believe multiple actions are necessary in order to move towards sustainability.

More than 90% of the companies in the top three quintiles, i.e. higher ranking corporations,

report sustainable actions (Table 3). The two lower quintiles show that approximately three-fourths of the companies report sustainable actions.

Table 3: Quintiles Rank/Quintile # corps

1 91 2 92 3 96 4 78 5 71

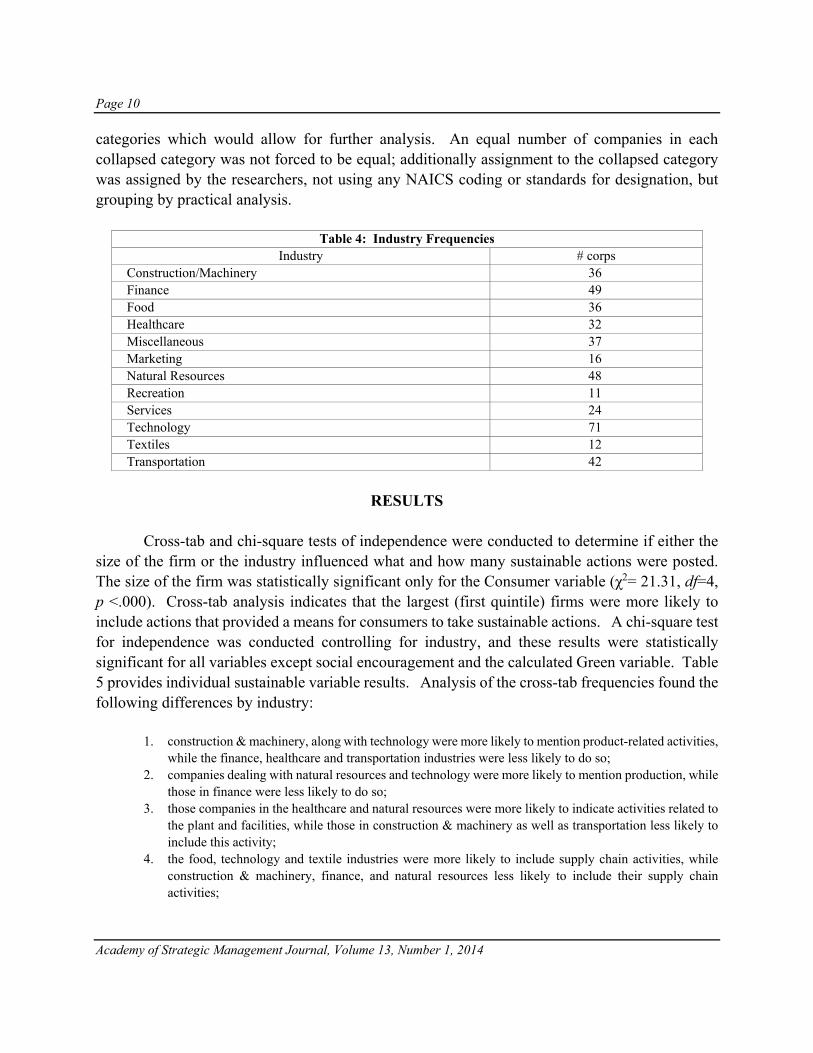

The original Fortune 500 industry categorization listed 65 different industries. For the

purpose of statistical analysis, the number of companies in many of these categories was too small to analyze. Therefore, similar industries were collapsed into twelve more generalized industry

Page 10

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

categories which would allow for further analysis. An equal number of companies in each collapsed category was not forced to be equal; additionally assignment to the collapsed category was assigned by the researchers, not using any NAICS coding or standards for designation, but grouping by practical analysis.

Cross-tab and chi-square tests of independence were conducted to determine if either the

size of the firm or the industry influenced what and how many sustainable actions were posted. The size of the firm was statistically significant only for the Consumer variable (χ2= 21.31, df=4, p <.000). Cross-tab analysis indicates that the largest (first quintile) firms were more likely to include actions that provided a means for consumers to take sustainable actions. A chi-square test for independence was conducted controlling for industry, and these results were statistically significant for all variables except social encouragement and the calculated Green variable. Table 5 provides individual sustainable variable results. Analysis of the cross-tab frequencies found the following differences by industry:

1. construction & machinery, along with technology were more likely to mention product-related activities, while the finance, healthcare and transportation industries were less likely to do so;

2. companies dealing with natural resources and technology were more likely to mention production, while those in finance were less likely to do so;

3. those companies in the healthcare and natural resources were more likely to indicate activities related to the plant and facilities, while those in construction & machinery as well as transportation less likely to include this activity;

4. the food, technology and textile industries were more likely to include supply chain activities, while construction & machinery, finance, and natural resources less likely to include their supply chain activities;

Page 11

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

5. the finance, services and textile industries were more likely to recycle, while the construction & machinery, natural resources, technology and transportation industries were less likely to recycle;

6. the technology industry was more likely to provide means to allow consumers to be sustainable, while the construction & machinery, healthcare, marketing, services and transportation industries less likely to provide means for consumers to be sustainable.

Recent reports indicate sustainability is on the corporate agenda (Epstein et al., 2010;

Heffes, 2010), with more than one quarter (28%) of corporate executives planning to increase focus on green initiatives, and upper management realizes the advantage of sustainability initiatives. Furthermore, environmental sustainability can be a source of competitive advantage (Matthews & Rusinko, 2010; Nidumolu, Prahalad, & Rangaswami, 2009; Ross, 2010). In addition, Nidumolu, Prahalad and Rangaswami (2009) purport that sustainability is rooted in organizational and technological innovation, as sustainable practices and activities lower costs because companies reduce the inputs they need as well as generating additional revenues from better products. Additionally, Ladd (2010) posits that companies generally make more money when they “do the right thing.” Pollution is waste, and therefore inefficient. It’s simply not profitable to be inefficient. There seems to be a sense among Americans that suggests the public wants changes that are green but tend to be less demanding, referred to as “lighter greens” and others who are more demanding about green initiatives are called “true greeners” (Oates et al., 2008).

FUTURE RESEARCH Reporting Indexes and Databases

There are several reporting agencies/groups which provide guidelines and statistics for sustainability reports. For example, CRD Analytics maintains the Global Sustainability 50 Index (Ladd, 2010). The Roberts Environmental Center publishes the Pacific Sustainability Index (Lee & Pati, 2012), which analyzes the effect of environmental and social performance of a form on the firm’s overall performance measures, as well as providing “scoring” of various industries. Within

Page 12

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

the environmental area of assessment the center reports on accountability, management, vision and policy, along with resource utilization and emissions data by industry sector. Lee & Pati (2012) focused on the triple bottom line, financial, environmental and societal performance, and reported that information from the REC data indicates enhancement of corporate sustainability efforts helps explain firm performance, because there was a strong evidence of a direct relationship between environmental and social sustainability factors in the Pacific Sustainability Index and market performance. The most dominant reporting regulations are those of the Global Reporting Initiative (GRI) (Ballou et al., 2006), which was launched in 1997, with the goal of enhancing the quality, rigor and utility of sustainability reporting. There were nearly 1000 international companies from more than 60 countries that had registered with the GRI by 2006. The GRI is an independent global organization that has established the de facto standards for sustainability reporting (D'Aquila, 2012). Dilling (2010) recently examined the characteristics of corporations that provide high quality sustainability reports, using the GRI 2007 G3 report list. The G3 is the third and latest version of the GRI Sustainability Reporting guidelines and framework for voluntary corporate sustainability reports. Findings indicate that corporations which publish a G3 report have certain characteristics, related to location, sector or industry, profitability and growth. D ’Aquila (2012) also reported that KPMG’s International Survey of Corporate Responsibility Reporting found that in 2001 95% of Fortune Global 250 corporations incorporated their social responsibility information in the corporate annual report. By 2008, KPMG reported that 80% of Global Fortune 250 corporations issued standalone documents for CSR reports in addition to the annual report (Bell & Lundblad, 2011). By 2011, KPMG reported that the number of multinational corporations providing CSR reports has continued to increase since its last survey in 2008 and goes on to say that what once was considered to be a nice activity has become almost mandatory for most multinational companies regardless of where they operate around the world. Thus, the KPMG International Corporate Responsibility Reporting Survey 2011 is recognized as the world’s largest and most comprehensive survey of Corporate Responsibility (CR) reporting trends ever published ("KPMG International Survey of Corporate Responsibility Reporting 2011," 2011). The CorporateRegister.com is the largest global repository of sustainability report (Burnett et al., 2011; Hubbard, 2011), with more than 21,000 corporate reports on file. In addition to all of these reporting agencies, and to illustrate the increasing importance of sustainability, in 1999, The Dow Jones Sustainability Group Indexes (DJSGI) was the first global index created to track the financial performance of leading sustainability driven companies worldwide (Shih-Fang & Her-Jiun, 2007).

The fact that several reporting agencies maintain either a repository of corporate sustainability reports, or index of such companies, leads to a possible research venture which could investigate which index or report listing include corporations appearing on the Fortune 500 list. The specific research questions posed to answer are:

1) Which Fortune 500 companies appear in the GRI Sustainability Disclosure Database

(http://database.globalreporting.org)?

Page 13

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

2) Which Fortune 500 companies appear in the CorporateRegister.com database? 3) Which Fortune 500 companies have been rated on the Pacific Sustainability Index on the Roberts

Environmental Center website? 4) Is there consistency in the individual reports of corporations which appear on one or more of these

databases?

Level of “Greenness” or Sustainability

Corporate sustainability may be addressed from the perspective of “stages of development” (Kashmanian, Wells, & Keenan, 2011; Nidumolu et al., 2009). The early stage of sustainable action at the corporate level is implemented based upon compliance with regulations. As time progresses, the corporation focuses on reduction of consumption, in particular non-renewable resources. Consumption is considered a prominent aspect of sustainability (Oates et al., 2008). As sustainability becomes more integrated within the organization and operations, manufacturing processes, value chain/supply chain are revised to integrate sustainable practices. The concept spreads across the organization, designing sustainable products and services, and becomes integrated across all business functions, becoming part of the business model. The integration of sustainability across the organization leads to engaging consumers and suppliers to do the same. As a result, in the short-term, the focus is on improving efficiency expands and results in increased revenues, as well as the establishment of a publicly available sustainability policy. This provides a direction or sustainability path for the company, as well as identifying where the company has made a commitment to improve performance, in the long run with consideration given to future product offering; which could result in the goal of achieving a competitive advantage over other companies. The importance of the life-cycle stage of products takes into consideration all stages of the environmental impact the product creates.

A similar, but somewhat different approach to the stages of corporate sustainability commitment is presented by Lubin and Esty (2010), based loosely on the four principles of value creation. These authors propose that the path to riding the sustainability wave is comprised of four stage of value creation. The first stage is to do old things in new ways by outperforming competitors on regulatory compliance and environmental-related costs and risk management. The second stage is to do new things in new ways, which means firms engage in widespread redesign of products, processes as well as optimizing natural resources efficiencies and risk management across their value chain. The third stage transforms the core business, as sustainable innovations provide new revenues and growth. Finally, the fourth stage created a new business model as well as differentiation. In this highest stage of sustainable development, firms can exploit the trend as a source of differentiation in the business model, brand, employee engagements, which fundamentally repositions the company and redefines its strategy for competitive advantage. A more sophisticated matrix describing the level of economic sustainability has been developed by Baumgartner and Ebner (2010). Again, the overall schema is developed upon a four-tier level of sustainability, beginning, elementary, satisfying, and sophisticated. However, the authors also

Page 14

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

then develop a matrix which addresses actions across the organization, from innovation and technology, sustainability reporting, to product and process actions, to waste and emissions.

Future research might examine the sustainability actions and classify the corporations by level of “greenness” based upon one or more of these “classification systems.” After reviewing the above literature, it would seem logical to develop a four-stage system, from a basic, legal and regulatory perspective, to a fully integrated, corporate-wide strategy which provides competitive advantage and a new corporate perspective. This review should answer this proposed research question: 5) Is the stage of sustainable adoption influenced by industry, and/or size of the corporation (based upon rank), on the Fortune 500 list?

Any future research should further refine the industry classification used for analysis. While the individual industry classifications are the most useful, they are also too individualized for statistical analysis. While the industry classifications used in the preliminary study were useful for initial data analysis, perhaps aligning categories with those used in the Pacific Sustainability Index would be a place to start, but additional categorization may be needed. As with all research which addresses a changing environment, developing a longitudinal study could provide insights how corporations continue to respond to sustainable initiatives. Accessibility of Website Information

Wheeler and Elkington (2001) predict that the future of corporate environmental reporting will be interactive and online, given the “wired” environment in which we live. Using online communication with stakeholders, including investors, consumers and employees provides flexibility across the corporation as well as large complex business entities. Morhardt (2010) analyzed and scored the environmental and social performance reports on corporate internet sites. While the content of the information presented is important, how easily accessible the information is to the website visitor impacts both access and perception of corporate intentions. Future research might examine how easily the information can be found. Specific questions to answer are:

6) How many clicks (pages deep) from the home page? 7) What title/subject is used to identify the sustainability information 8) Is there a section on the website for sustainability?

a. or is the information contained inside an annual corporate report, such as a Corporate Sustainability Report?

CONCLUSION

MIT Sloan Management Review and Boston Consulting Group have jointly conducted annual surveys of managers and top executives from world-wide corporations asking them about their sustainable business practices (Berns et al., 2009a, 2009b; Dawar & Stornelli, 2013; Haanaes et al., 2011; Hopkins, Haanaes, et al., 2011; Hopkins, Kruschwitz, et al., 2011; Hopkins et al.,

Page 15

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

2009; Kiron, Kruschwitz, Haanaes, & von Streng Velken, 2012; Kiron et al., 2013; Kruschwitz & Velken, 2011). The first survey in 2009, (Berns et al., 2009a, 2009b) found that the large majority (92%) of the executives reported their companies were addressing sustainability, and continuing to do so, despite the economic downturn; less than 25% of the respondents indicated their company had decreased commitment to sustainability. In fact, some sectors such as the automotive industry had actually increased efforts. The majority of actions reported were addressing what was necessary to meet regulatory requirements, and more than 70% of the companies had not developed a clear business case for sustainability. The second survey in 2010 (Haanaes et al., 2011; Hopkins, Haanaes, et al., 2011; Hopkins, Kruschwitz, et al., 2011), found that again, sustainability efforts had survived the economic climate with 59% of the respondents indicated they were increasing their commitment to sustainability. While the study divided the corporations into Embracers and Cautious Adopters, all were seeing the benefits of a sustainable strategy as improving resource efficiency and waste management. In fact, the study noted that members of the C-suite were not embracing the movement based upon environmental concerns, but rather because they perceive sustainability to be essential to being competitive. The report found substantial difference between the two groups, Embracers and Cautious Adopters. The Embracers corporations see great potential in sustainable strategies: deliver new customers, increase market share, and profit margins. Embracers tend to be large global or regional companies, with only nine percent of small companies categorized as Embracers. The companies that fall within this category also tend to resource-intensive industries. This group of companies are also growing and in growth markets, where investment in sustainability come easily. This second study, also found a larger number of those Cautious Adopters, as almost two-thirds (63%) indicated they would be increasing investments in sustainability in 2011. Thus, sustainability continued to have an increased importance corporate strategy and practice. One finding in this annual survey found significant variance across industries. The automotive, chemical, commodities, conglomerate/multi-industry, consumer products, industrial good/machinery retail, and technology/telecommunications industries report indicated their company’s commitment to sustainability had increased over the last year, and would increase in the next year. For some industries, such as chemical and resource-based operations, sustainability is a matured concept. Others, such as the automotive and consumer goods companies, will indicate competitive advantage as the basis for sustainability, while they in fact are no more likely to actually present a business case that supports such actions. The conclusion of the second survey identified specific differences between the embracers, or top performers from the lower-performing, cautious adopters. Top performers innovate more, and achieve competitive differentiation, while placing an emphasis on the long-term. These corporations and their respective leadership are far more convinced that sustainable actions lead to profitability, and they quantify sustainability-related benefits across the board. Embracers assign managers dedicated to sustainability, and rely on leaders as well as non-leadership employees to drive sustainability within and across the corporation. They consider risks,

Page 16

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

intangibles and qualitative factors more formally, and are more confident about the business case for sustainability.

In addition to analyzing what role sustainability played in business actions, this second study also cited several instances of the influence consumers have in the role of corporate sustainability. This second study found that both large and small companies have built sustainability into the brand. Examples of large corporations include General Electric, Walmart and Toyota. Smaller companies include Patagonia and Interface Global. Regardless of which corporate label from the study was applied, across the study, executives cited improved brand reputation, and brand equity as a continued importance for sustainable actions. Beth Spring, executive vice president at Clorox, believe consumer megatrends provided big growth opportunities which reinvigorated Brita water pitchers and filters, and the launch of Green Works, an all-natural clearing product line, as well as the acquisition of Burt’s Bees, an all-natural personal care line (Hopkins, Kruschwitz, et al., 2011).

The third annual survey (Kiron et al., 2012; Kruschwitz & Velken, 2011) reported sustainability has neared a tipping point. More than two-thirds (70%) of the companies surveyed have placed sustainability permanently on their agenda, and many have done so in the past six years. This year, two-thirds of the respondents indicated sustainability was necessary to be competitive in today’s marketplace. Even with this positive perspective of sustainability, it only ranks in eighth place on the corporate agenda. A third category, or group of corporations, was identified in this third survey: Harvesters. Harvesters are profiting from sustainability, and in front others. In these organizations, sustainability relies on the longevity and robustness of the company’s agenda, and ultimately depends upon how well sustainability is embedded in the business processes. Harvesters differ on four points: organizations support, operations, collaborations, and willingness to change the company’s business model, in response to sustainable considerations. There are managerial differences for Harvesters as well: they are 50% more likely to have a CEO committed to sustainability, twice as likely to have a separate sustainability reporting process as well as a separate function for sustainability. They are also more likely to have a Chief Sustainability Officer, as well as having a person in each business unit who is responsible for sustainability. Harvesters accounted for 31% of the respondents, and exist in every industry covered by the survey. Again, this third survey found the role customers play in the corporate sustainability agenda. In fact, 41% of all respondents indicated that customer preferences for sustainable products and services as a reason for changing business models. However, customers are not always willing to pay more for these products, possibly as a result of the recent economic conditions.

Clearly, sustainability has become a part of corporate operations and strategy, and emphasis is expected to increase. In addition, it appears consumers continue to express concern for the environment, as well as the role their consumption plays in growing sustainable efforts. Therefore, continued observation and review of corporate actions, the reporting of these actions and research associated with these actions will remain important to corporate success.

Page 17

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Establishing corporate sustainability fosters the corporation’s influence on the public perception of the corporate commitment to sustainability (Kashmanian, Wells, & Keenan, 2011). By informing the public and business community of their corporate actions and commitment to sustainbility, companies are encouraging individul and corporate responsibility. Engaging society provides the opportunity to ensure a sound environment and prospersou future (Casimir & Dutilj, 2003).

REFERENCES Ballou, B., Heitger, D. L., Landes, C. E., & Adams, M. (2006). The future of corporate sustainability reporting. Journal

of Accountancy, 202(6), 65-67,70-74. Baumgartner, R. J., & Ebner, D. (2010). Corporate sustainability strategies: Sustainability profiles and maturity levels.

Sustainable Development, 18(2), 76. Bell, J., & Lundblad, H. (2011). A comparison of ExxonMobil's sustainability reporting to outcomes. The Journal of

Applied Business and Economics, 12(1), 17-29. Berns, M., Townsend, A., Khayat, Z., Balagopal, B., Reeves, M., Hopkins, M., & Kruschwitz, N. (2009a). The

business of sustainability: Findings and insights from the first annual business of sustainability survey and the global thought leaders' research project (pp. 1-84). North Holywood, CA: Massachusetts Institute of Technology.

Berns, M., Townsend, A., Khayat, Z., Balagopal, B., Reeves, M., Hopkins, M., & Kruschwitz, N. (2009b). The business of sustainability: Imperatives, advantages, and actions (pp. 1-35). Boston, MA: Boston Consulting Group, Inc.

Borkowski, S. C., Welsh, M. J., & Wentzel, K. (2010). Johnson & Johnson: A model for sustainability reporting. Strategic Finance, 92(3), 29-37.

Burnett, R. D., Skousen, C. J., & Wright, C. J. (2011). Eco-effective management: An empirical link between firm value and corporate sustainability. Accounting & the Public Interest, 11, 1-15.

Casimir, G., & Dutilh, C. (2003). Sustainability: A gender studies perspective*. International Journal of Consumer Studies, 27(4), 316-325.

D'Aquila, J. (2012). Integrating sustainability into the reporting process and elsewhere. The CPA Journal, 82(4), 16-21,24.

Dawar, N., & Stornelli, J. (2013). Rebuilding the relationship between manufacturers and retailers. MIT Sloan Management Review, 54(2), 83-90.

Delmas, M., & Blass, V. D. (2010). Measuring corporate environmental performance: the trade-offs of sustainability ratings. Business Strategy and the Environment, 19(4), 245.

Dilling, P. F. A. (2010). Sustainability reporting in a global context: What are the characteristics of corporations that provide high quality sustainability reports - an empirical analysis. The International Business & Economics Research Journal, 9(1), 19-30.

Dragomir, V. D. (2012). The disclosure of industrial greenhouse gas emissions: A critical assessment of corporate sustainability reports. Journal of Cleaner Production, 29-30, 222-237.

Epstein, M. J., Buhovac, A. R., & Yuthas, K. (2010). Implementing Sustainability: The Role of leadership and organizational culture. Strategic Finance, 91(10), 41-47.

Fromartz, S. (2009). The mini-cases: 5 companies, 5 strategies, 5 transformations. MIT Sloan Management Review, 51(1), 41-45.

Haanaes, K., Arthur, D., Balagopal, B., Kong, M. T., Velken, I., & Hopkins, M. S. (2011). First look: The second annual sustainability & innovation survey. MIT Sloan Management Review, 52(2), 77-83.

Page 18

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Heffes, E. M. (2010). Sustainability's place on corporate 'to-do' lists. Financial Executive, 26(2), 9-9. Holden, G. (2012). The state of sustainability. Research Technology Management, 55(6), 7-9. Hopkins, M. S., Haanaes, K., Balagopal, B., Velken, I., Kruschwitz, N., & Arthur, D. (2011). New sustainability study:

The embracers seize advantage. MIT Sloan Management Review, 52(3), 23-35. Hopkins, M. S., Kruschwitz, N., Haanaes, K., Kong, M. T., Arthur, D., & Reeves, M. (2011). Sustainability: The

'embracers' seize advantage. MIT Sloan Management Review, 52(3), 3-27. Hopkins, M. S., Townend, A., Khayat, Z., Balagopal, B., Reeves, M., & Berns, M. (2009). The business of

sustainability: What it means to managers now. MIT Sloan Management Review, 51(1), 20-26. Hubbard, G. (2011). The quality of the sustainability reports of large international companies: An analysis.

International Journal of Management, 28(3), 824-848. Huppes, G., & Ishikawa, M. (2005). Why eco-efficiency? Journal of Industrial Ecology, 9(4), 2-5. Kashmanian, R. M., Wells, R. P., & Keenan, C. (2011). Corporate environmental sustainability strategy: Key

elements. Journal of Corporate Citizenship(44), 107-130. Katrinli, A., Gunay, G., & Biresselioglu, M. E. (2011). The convergence of corporate social responsibility and

corporate sustainability: Starbucks corporation's practises. The Business Review, Cambridge, 17(1), 164-171. Ketola, T. (2010). Five leaps to corporate sustainability through a corporate responsibility portfolio matrix. Corporate

Social - Responsibility and Environmental Management, 17(6), 320. Kiron, D., Kruschwitz, N., Haanaes, K., & von Streng Velken, I. (2012). Sustainability nears a tipping point. MIT

Sloan Management Review, 53(2), 69-74. Kiron, D., Kruschwitz, N., Reeves, M., & Goh, E. (2013). The benefits of sustainability-driven innovation. MIT Sloan

Management Review, 54(2), 69-73. Kleine, A., & von Hauff, M. (2009). Sustainability-driven implementation of corporate social responsibility:

Application of the integrative sustainability triangle. Journal of Business Ethics, 85, 517-533. KPMG International Survey of Corporate Responsibility Reporting 2011. (2011). In KPMG.com (Ed.): KPMG

International Cooperative. Kruschwitz, N. (2012a). How an abundance mentality and a CEOs fierce resolve kickstarted CSR at campbell soup.

MIT Sloan Management Review, 54(1), 1-3. Kruschwitz, N. (2012b). How Dell turned bamboo and mushrooms into environmental-friendly packaging. MIT Sloan

Management Review, 54(1), 1-5. Kruschwitz, N. (2012c). Integrating sustainability into strategy, governance and employee engagement. MIT Sloan

Management Review, 53(4), 1-3. Kruschwitz, N. (2012d). Why Kraft Foods cares about fair trade chocolate. MIT Sloan Management Review, 54(1), 1-

4. Kruschwitz, N. (2013). New ways to engage employees, suppliers and competitors in CSR. MIT Sloan Management

Review, 54(2), 1-3. Kruschwitz, N., & Velken, I. (2011). First look: highlights from the third annual sustainability global executive survey.

MIT Sloan Management Review, 53(1), 87-89. Ladd, S. (2010). Corporate "greening". Financial Executive, 26(2), 36-41. Lee, J., & Pati, N. (2012). New insights on the operational links between corporate sustainability and firm performance

in service industries. International Journal of Business Insights & Transformation, 4, 80-93. Loch, R., & Buhay, M. C. (2012). 2012 Gibbs & Soell sense & sustainability study: Perspectives on corporate

sustainability among consumers and executives. In I. Gibbs & Soell (Ed.). Lozano, R. (2012). Orchestrating organisational changes for corporate sustainability. Greener Management

International(57), 43-64. Lubin, D. A., & Esty, D. C. (2010). The sustainability imperative. Harvard Business Review, 88(5), 42-50. Matthews, J. O., & Rusinko, C. A. (2010). Linking sustainability and financial valuation: Six necessary conditions.

Journal of Investing, 19(3), 128-135,126,128.

Page 19

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Merchant, B. (2009). Walmart's sustainability index: The greenest thing ever to happen to retail? Retrieved January 29, 2013, from http://www.treehugger.com/corporate-responsibility/walmarts-sustainability-index-the-greenest-thing-ever-to-happen-to-retail.html

Montiel, I. (2008). Corporate social responsibility and corporate sustainability separate pasts, common futures. Organization & Environment, 21(3), 245-269.

Morhardt, J. E. (2010). Corporate social responsibility and sustainability reporting on the internet. Business Strategy & the Environment (John Wiley & Sons, Inc), 19(7), 436-452.

Morhardt, J. E., Baird, S., & Freeman, K. (2002). Scoring corporate environmental and sustainability reports using GRI 2000, ISO 14031 and other criteria. Corporate Social - Responsibility and Environmental Management, 9(4), 215-215.

Nidumolu, R., Prahalad, C. K., & Rangaswami, M. R. (2009). Why sutainability is now the key driver of innovation. Harvard Business Review, 87(9), 56-64.

Oates, C., McDonald, S., Alevizou, P., Kumju, H., Young, W., & McMorland, L.-A. (2008). Marketing sustainability: Use of information sources and degrees of voluntary simplicity. Journal of Marketing Communications, 14(5), 351-365.

. Overview of the UN Global Compact. (2011, December 1) Retrieved February 5, 2013, from http://www.unglobalcompact.org/AboutTheGC/index.html

Ramus, C. A., & Montiel, I. (2005). When are corporate environmental policies a form of greenwashing? Business and Society, 44(4), 377-414.

Reilly, A. H. (2009). Communicating sustainability initiatives in corporate reports: Linking implications to organizational change. S.A.M. Advanced Management Journal, 74(3), 33-43,32.

Roca, L. C., & Searcy, C. (2012). An analysis of indicators disclosed in corporate sustainability reports. Journal of Cleaner Production, 20(1), 103-118.

Ross, L. (2010). Accounting For Sustainability. Financial Management, 31-32. Rowbottom, N., & Lymer, A. (2009). Exploring the use of online corporate sustainability information. Accounting

Forum, 33(2), 176-186. SCA survey conducted by Harris Interactive® shows that despite a weakened economy, U.S. consumers willing to

spend green to go green. (2008, April 21) Retrieved January 28, 2012, from http://www.prnewswire.com/news-releases/sca-survey-conducted-by-harris-interactiver-shows-that-despite-a-weakened-economy-us-consumers-willing-to-spend-green-to-go-green-57470917.html

SCA survey finds two-thirds of American adults purchase green products. (2012). Tork News. Retrieved from http://betterbusiness.torkusa.com/green-business-survey-tork-bbc/

Shih-Fang, L., & Her-Jiun, S. (2007). Is corporate sustainability a value-increasing strategy for business? Corporate Governance: An International Review, 15(2), 345-358.

Sobhani, F. A., Amran, A., & Zainuddin, Y. (2012). Sustainability disclosure in annual reports and websites: a study of the banking industry in Bangladesh. Journal of Cleaner Production, 23(1), 75-85.

Stafford, E. R., & Hartman, C. L. (2013). Promoting the value of sustainably minded purchase behaviors. Marketing News, 47, 28-33.

Steinberg, K. (2011, January 10). Fewer Americans "going green" Retrieved January 28, 2012, from http://www.harrisinteractive.com/NewsRoom/HarrisPolls/tabid/447/mid/1508/articleId/667/ctl/ReadCustom%20Default/Default.aspx

Steinberg, K. (2012, April 18). Fewer Americans "thinking green" Retrieved January 28, 2012, from www.harrisinteractive.com/NewsRoom/HarrisPolls/tabid/447/ctl/ReadCustom Default/mid/1508/ArticleId/1009/Default.aspx

. Sustainability Incex. (2012) Retrieved February 1, 2013, from http://corporate.walmart.com/global-responsibility/environment-sustainability/sustainability-index

Page 20

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Walsh, H., & Dowding, T. J. (2012). Sustainability and the coca-cola company: The global water crisis and coca-cola's business case for water stewardship. International Journal of Business Insights & Transformation, 4, 106-118.

Watson, M. (2011). Doing well by doing good: Ray C. Anderson as evangelist for corporate sustainability. Business Communication Quarterly, 74(1), 63-67.

Wheeler, D., & Elkington, J. (2001). The end of the corporate environmental report? Or the advent of cybernetic sustainability reporting and communication. Business Strategy and the Environment, 10(1), 1-14.

Young, W., & Tilley, F. (2006). Can businesses move beyond efficiency? The shift toward effectiveness and equity in the corporate sustainability debate. Business Strategy and the Environment, 15(2), 402-415.

Page 21

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

DOES COMPANY SIZE AFFECT MISSION STATEMENT CONTENT?

Darwin L. King, St. Bonaventure University

Carl J. Case, St. Bonaventure University Kathleen M. Premo, St. Bonaventure University

ABSTRACT

Mission statements are probably the most important communication issued by a firm to all

of its many stakeholders. Missions provide the reason why the firm is in existence. This paper is a continuation of the mission statement research that the authors have conducted over the last twelve years. Previous studies have reviewed mission statements from the largest corporations in countries including Canada, United Kingdom, France, Germany, Australia, Japan, China, Brazil, and India. This study considers United States’ businesses only. The intent of the authors is to determine if the size of the company affects the content of the mission statement.

The authors have conducted research on mission statements in 2001, 2008, 2010, 2011, and 2012 that has been published in various Allied Academies’ journals. The majority of the articles have appeared in the Academy of Strategic Management Journal (ASMJ). The mission statement comparisons have emphasized two distinct areas, namely, the stakeholders mentioned in the mission statements and the named goals and objectives of the company. The stakeholders and goals/objectives emphasis is continued in this paper.

The authors again used the Fortune 500 list to determine the largest firms in the United States. In this study, the largest 100 firms are compared with the last 100 companies in the Fortune 500 list (numbers 401-500). The authors hope to determine if size does affect the stakeholders and goals/objectives mentioned in the firm’s mission statement. Stakeholders identified included communities, customers, employees, stockholders/stakeholders, and suppliers/partners. Identified goals and objectives included affordability of products or services, following core values, striving for diversity, maintaining efficient operations, concern for the environment, maintaining ethical operations, striving for global operations, maintaining innovation, maintaining a leadership position, an emphasis on profitability/profits, desire to produce a quality product or service that provided value to customers, producing a safe product, an emphasis on teamwork, and the desire to gain the trust of stakeholders. Significant differences were identified in the mission statement content of these two groups of firms and are discussed in this paper.

INTRODUCTION For at least the last 40 years, the company’s mission statement has served as the primary

communication tool to explain to all stakeholders what the firm is all about. It states the reason for the firm’s existence. Peter Drucker, who is often considered the “father of management,” wrote extensively about mission statements. He felt that missions are the “foundation for priorities,

Page 22

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

strategies, plans, and work assignments” (Drucker, 1974). Drucker felt that mission statements differentiated firms and gave them their own personality. Drucker felt that the mission statement should serve as the foundation for the creation of company strategies and policies. If the emphasis in the mission statement was on customers, it was only logical that the firm’s policies and strategies should emphasize that stakeholder’s importance.

Drucker established the Leader to Leader Institute that emphasized the importance of the mission statement. Drucker felt that mission statements should be short and to the point. He suggested that the mission statement should be only 3 or 4 sentences in length. He believed that these few sentences should address four aspects about the firm including who are we, what do we do, what do we stand for, and why do we do what we do. This is a lot to expect from a single paragraph of only 3 or 4 sentences. Drucker felt that a good mission statement should specifically name the firm’s most important stakeholders.

Fred David believes that mission statements should include the firm’s basic purpose, its unique qualities or strengths, its values, its core stakeholders, and its major goals or objectives (David, 2005). Although they are known by many names including creed statements, statements of belief, and statements of business purpose, these critical communications must inform all stakeholders about the nature and character of the company. David also believes that mission statements must explain the organization’s “reason for being” (David, 2009). In this process, he feels that mission statements should clearly state who the firm seeks to serve, so the naming of stakeholders is especially important. Many authors feel that the goals and objectives of the firm must mirror the content of the mission statement (Robbins & Coulter, 2012). Robbins & Coulter feel that the mission statements must disclose the organization’s purpose or reason for being. This serves as a guidebook to all employees of the company in the process of establishing corporate policies and strategies. Other authors including Annie McKee feel that the mission statement provides the focus for the firm (McKee, 2012). Without a well written mission statement, the organization, in effect, has lost its compass. McKee emphasizes that the mission statement should describe what the firm considers important, what it does, and what it stands for. She, along with many other authors, feels that mission statements should be used by managers in the process of establishing and following short and long term objectives. Another author on mission statements, Jeffery Abrahams, has researched over 300 of the largest U.S. firms’ statements (Abrahams, 1999). Following this analysis, he felt that a good mission statement reflects the values of the firm and provides stakeholders with a statement of purpose. Others, including Samuel and S. Trevis Certo, believe that the mission statement is a critical part of the strategic management process (S. & S.T. Certo, 2012).

Many authors feel that the strategic management process requires a carefully constructed mission statement to provide direction to all employees and managers. Hitt, Black, and Porter support this belief and stress that an effective mission statement must describe the central purpose of the company (M.A. Hitt, J.S. Black & L.W. Porter, 2012). Rarick and Vitton feel that mission statements should include important aspects of the company including company core philosophy, customer markets served, major products or services produced, and concern for the environment and the communities in which the firm operates (Rarick and Vitton, 1995).

Page 23

Academy of Strategic Management Journal, Volume 13, Number 1, 2014

Other authors including Thompson, et.al. emphasize that mission statements should clearly describe the current business and purpose of the firm (Thompson, et.al. 2012). These authors feel that a well written mission statement gives the company its unique identity. Another group of authors, Schermerhorn, et. al., feel that well written mission statements describe who the firm seeks to serve and what is the overall organizational purpose (Schermerhorn, et.al.). Finally, Wheelen and Hunger argue that an efficient and effective mission statement describes the fundamental or unique purpose of the organization (Wheelen and Hunger, 2010). They feel that this provides the unique personality of the firm that sets the company apart from all others.

Following a brief summary of previous mission statement research, the authors summarize the similarities and differences among the top 100 Fortune firms and those that are listed on the Fortune 500 list in positions from 401 to 500. There are many significant differences from the largest companies and those that are significantly smaller in size. Finally, the appendix contains a listing of the 200 firms used in this study.

PREVIOUS MISSION STATEMENT RESEARCH The authors began their mission statement research twelve years ago. Five of the authors’ mission statement articles have been published in the Academy of Managerial Communications Journal (King, 2001) and the Academy of Strategic Management Journal (King, Case & Premo, 2010), (King, Case & Premo, 2011), (King, Case & Premo, 2012) and (King, Case & Premo, 2013). This mission statement research has increased in size over the years with the most current study involving a review of ten countries’ mission statements. These five research projects are briefly summarized in the following paragraphs.