CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES TRUE-FALSE—Conceptual Answer No. Description T 1. When to use lower-of-cost-or-market. F 2. Lower-of-cost-or-market and conservatism. F 3. Purpose of the “floor” in LCM. T 4. Lower-of-cost-or-market and consistency. F 5. Reporting inventory at net realizable value. T 6. Valuing inventory at net realizable value. T 7. Valuation using relative sales value. F 8. Definition of a basket purchase. F 9. Recording purchase commitments. T 10. Loss on purchase commitments. F 11. Recording noncancelable purchase contract. T 12. Gross profit method. F 13. Gross profit percentage. T 14. Disadvantage of gross profit method. F 15. Conventional retail method. F 16. Definition of markup. T 17. Accounting for abnormal shortages. F 18. Computing inventory turnover ratio. T 19. Average days to sell inventory. T 20 LIFO retail method. MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Knowledge of lower-of-cost-or-market valuations. d 22. Appropriate use of LCM valuation. c 23. Definition of "market" under LCM. b 24. Definition of "ceiling." a 25. Definition of "designated market value." c 26. Application of lower-of-cost-or-market valuation. d 27. Effect of inventory write-down. d S 28. Recording inventory loss under direct method.

Transcript

CHAPTER 9

INVENTORIES: ADDITIONAL VALUATION ISSUES

TRUE-FALSE—ConceptualAnswer No. Description

T 1. When to use lower-of-cost-or-market.F 2. Lower-of-cost-or-market and conservatism.F 3. Purpose of the “floor” in LCM.T 4. Lower-of-cost-or-market and consistency.F 5. Reporting inventory at net realizable value.T 6. Valuing inventory at net realizable value.T 7. Valuation using relative sales value.F 8. Definition of a basket purchase.F 9. Recording purchase commitments.T 10. Loss on purchase commitments. F 11. Recording noncancelable purchase contract.T 12. Gross profit method.F 13. Gross profit percentage.T 14. Disadvantage of gross profit method.F 15. Conventional retail method.F 16. Definition of markup.T 17. Accounting for abnormal shortages.F 18. Computing inventory turnover ratio.T 19. Average days to sell inventory.T 20 LIFO retail method.

MULTIPLE CHOICE—ConceptualAnswer No. Description

d 21. Knowledge of lower-of-cost-or-market valuations.d 22. Appropriate use of LCM valuation.c 23. Definition of "market" under LCM.b 24. Definition of "ceiling."a 25. Definition of "designated market value."c 26. Application of lower-of-cost-or-market valuation.d 27. Effect of inventory write-down.d S28. Recording inventory loss under direct method.c S29. Recording inventory at net realizable value.b 30. Net realizable value under LCM.d 31. Definition of "net realizable value."a 32. Valuation of inventory at net realizable value.d 33. Appropriate use of net realizable value.a 34. Material purchase commitments.a 35. Loss recognition on purchase commitments.b P36. Reporting purchase commitments loss.

Test Bank for Intermediate Accounting, Twelfth Edition

d S37. Gross profit method assumptions.d 38. Appropriate use of the gross profit method.b 39. Appropriate use of the gross profit method.d 40. Advantage of retail inventory method.c 41. Conventional retail inventory method.a 42. Assumptions of the retail inventory method.d 43. Appropriate use of the retail inventory method.b 44. Markdowns and the conventional retail method.a 45. Markups and the conventional retail method.b *46. Knowledge of the cost ratio for retail inventory methods.a S47. Information needed in retail inventory method.d S48. Reasons for using retail inventory method.b P49. Inventory cost flow assumptions.a P50. Computing average days to sell inventory.c 51. Inventory turnover ratio.c *52. Dollar-value LIFO retail method.

a 53. Value inventory at LCM.b 54. Lower-of-cost-or-market.b 55. Lower-of-cost-or-market.c 56. Determining net realizable value.c 57. Determining net realizable value.b 58. Relative sales value method.b 59. Relative sales value method.c 60. Relative sales method of inventory valuation.c 61. Entry for purchase commitment loss.c 62. Recognizing loss on purchase commitments.b 63. Recognizing loss on purchase commitments.a 64. Estimating ending inventory using gross profit method.a 65. Estimating ending inventory using gross profit method.d 66. Calculate cost of goods sold given a markup on cost.d 67. Calculate merchandise purchases given a markup on cost.a 68. Calculate total sales from cost information.a 69. Markup on cost equivalent to a markup on selling price.b 70. Estimate ending inventory using gross profit method.c 71. Calculate ending inventory using gross profit method

. b 72. Calculate ending inventory using gross profit method.a 73. Estimate cost of inventory destroyed by fire.a 74. Determine items to be included in inventory.b 75. Calculate cost of retail ratio to approximate LCM.b 76. Calculate ending inventory at retail.a 77. Calculate cost to retail ratio approximating LCM.b 78. Calculate cost of inventory lost using retail method.b *79. Calculate ending inventory at cost using LIFO retail.c *80. Determine cost to retail ratio using LIFO retail.a 81. Calculate ending inventory at retail.

a 82. Calculate ending inventory at retail.c 83. Average days to sell inventory.c 84. Average days to sell inventory.b 85. Calculate inventory turnover ratio.d 86. Determine cost to retail ratio to approximate LCM.d 87. Calculate ending inventory at retail.a 88. Calculate ending inventory using conventional retail.c *89. Determine cost to retail ratio using LIFO cost.a *90. Calculate ending inventory cost using dollar-value LIFO.b *91. Calculate cost of ending inventory using LIFO retail.a *92. Calculate ending inventory cost using dollar-value LIFO.

P These questions also appear in the Problem-Solving Survival Guide.S These questions also appear in the Study Guide.* This topic is dealt with in an Appendix to the chapter.

MULTIPLE CHOICE—CPA AdaptedAnswer No. Description

d 93. Recognizing a loss due to LCM.b 94. Appropriate use of replacement costs in LCM.b 95. Identification of the designated market value.a 96. Estimate cost of inventory lost by theft.a 97. Determine cost of ending inventory using retail method.d 98. Determine cost of ending inventory using retail method.a *99. Calculate ending inventory using LIFO retail.

1. Describe and apply the lower-of-cost-or-market rule.

2. Explain when companies value inventories at net realizable value.

3. Explain when companies use the relative sales value method to value inventories.

4. Discuss accounting issues related to purchase commitments.

5. Determine ending inventory by applying the gross profit method.

6. Determine ending inventory by applying the retail inventory method.

7. Explain how to report and analyze inventory.

*8. Determine ending inventory by applying the LIFO retail methods.

9 - 4

Inventories: Additional Valuation Issues

*SUMMARY OF LEARNING OBJECTIVES BY QUESTIONS

Item Type Item Type Item Type Item Type Item Type Item Type Item TypeLearning Objective 1

1. TF 21. MC 25. MC 53. MC 94. MC 102. E2. TF 22. MC 26. MC 54. MC 95. MC 103. E3. TF 23. MC 27. MC 55. MC 100. E 104. E4. TF 24. MC S28. MC 93. MC 101. E 109. E

Learning Objective 25. TF S29. MC 31. MC 33. MC 57. MC6. TF 30. MC 32. MC 56. MC

Learning Objective 37. TF 8. TF 58. MC 59. MC 60. MC 105. E

Learning Objective 49. TF 11. TF 35. MC 61. MC 63. MC

10. TF 34. MC P36. MC 62. MCLearning Objective 5

12. TF 38. MC 66. MC 70. MC 74. MC 108. E13. TF 39. MC 67. MC 71. MC 96. MC 110. P14. TF 64. MC 68. MC 72. MC 106. E

S37. MC 65. MC 69. MC 73. MC 107. ELearning Objective 6

15. TF 41. MC 45. MC 75. MC 81. MC 88. MC 111. P16. TF 42. MC 46. MC 76. MC 82. MC 97. MC17. TF 43. MC S47. MC 77. MC 86. MC 98. MC40. MC 44. MC S48. MC 78. MC 87. MC 109. E

Learning Objective 718. TF P49. MC 51. MC 84. MC19. TF P50. MC 83. MC 85. MC

Learning Objective *820. TF 79. MC 90. MC 99. MC 113. P 116. P46. MC 80. MC 91. MC 109. E 114. P52. MC 89. MC 92. MC 112. P 115. P

Test Bank for Intermediate Accounting, Twelfth Edition

TRUE-FALSE—Conceptual

1. A company should abandon the historical cost principle when the future utility of the inventory item falls below its original cost.

2. The lower-of-cost-or-market method is used for inventory despite being less conservative than valuing inventory at market value.

3. The purpose of the “floor” in lower-of-cost-or-market considerations is to avoid overstating inventory.

4. Application of the lower-of-cost-or-market rule results in inconsistency because a company may value inventory at cost in one year and at market in the next year.

5. GAAP requires reporting inventory at net realizable value, even if above cost, whenever there is a controlled market with a quoted price applicable to all quantities.

6. A reason for valuing inventory at net realizable value is that sometimes it is too difficult to obtain the cost figures.

7. In a basket purchase, the cost of the individual assets acquired is determined on the basis of their relative sales value.

8. A basket purchase occurs when a company agrees to buy inventory weeks or months in advance.

9. Most purchase commitments must be recorded as a liability.

10. If the contract price on a noncancelable purchase commitment exceeds the market price, the buyer should record any expected losses on the commitment in the period in which the market decline takes place.

11. When a buyer enters into a formal, noncancelable purchase contract, an asset and a liability are recorded at the inception of the contract.

12. The gross profit method can be used to approximate the dollar amount of inventory on hand.

13. In most situations, the gross profit percentage is stated as a percentage of cost.

14. A disadvantage of the gross profit method is that it uses past percentages in determining the markup.

15. When the conventional retail method includes both net markups and net markdowns in the cost-to-retail ratio, it approximates a lower-of-cost-or-market valuation.

16. In the retail inventory method, the term markup means a markup on the original cost of an inventory item.

17. In the retail inventory method, abnormal shortages are deducted from both the cost and retail amounts and reported as a loss.

9 - 6

Inventories: Additional Valuation Issues

18. The inventory turnover ratio is computed by dividing the cost of goods sold by the ending inventory on hand.

19. The average days to sell inventory represents the average number of days’ sales for which a company has inventory on hand.

*20. The LIFO retail method assumes that markups and markdowns apply only to the goods purchased during the period.

True False Answers—ConceptualItem Ans. Item Ans. Item Ans. Item Ans.1. T 6. T 11. F 16. F2. F 7. T 12. T 17. T3. F 8. F 13. F 18. F4. T 9. F 14. T 19. T5. F 10. T 15. F 20. T

MULTIPLE CHOICE—Conceptual

21. Which of the following is true about lower-of-cost-or-market?a. It is inconsistent because losses are recognized but not gains.b. It usually understates assets.c. It can increase future income.d. All of these.

22. The primary basis of accounting for inventories is cost. A departure from the cost basis of pricing the inventory is required where there is evidence that when the goods are sold in the ordinary course of business theira. selling price will be less than their replacement cost.b. replacement cost will be more than their net realizable value.c. cost will be less than their replacement cost.d. future utility will be less than their cost.

23. When valuing raw materials inventory at lower-of-cost-or-market, what is the meaning of the term "market"?a. Net realizable valueb. Net realizable value less a normal profit marginc. Current replacement costd. Discounted present value

24. In no case can "market" in the lower-of-cost-or-market rule be more thana. estimated selling price in the ordinary course of business.b. estimated selling price in the ordinary course of business less reasonably predictable

costs of completion and disposal.c. estimated selling price in the ordinary course of business less reasonably predictable

costs of completion and disposal and an allowance for an approximately normal profit margin.

9 - 7

Test Bank for Intermediate Accounting, Twelfth Edition

d. estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal, an allowance for an approximately normal profit margin, and an adequate reserve for possible future losses.

25. Designated market valuea. is always the middle value of replacement cost, net realizable value, and net realizable

value less a normal profit margin.b. should always be equal to net realizable value.c. may sometimes exceed net realizable value.d. should always be equal to net realizable value less a normal profit margin.

26. Lower-of-cost-or-marketa. is most conservative if applied to the total inventory.b. is most conservative if applied to major categories of inventory.c. is most conservative if applied to individual items of inventory.d. must be applied to major categories for taxes.

27. An item of inventory purchased this period for $15.00 has been incorrectly written down to its current replacement cost of $10.00. It sells during the following period for $30.00, its normal selling price, with disposal costs of $3.00 and normal profit of $12.00. Which of the following statements is not true?a. The cost of sales of the following year will be understated.b. The current year's income is understated.c. The closing inventory of the current year is understated.d. Income of the following year will be understated.

S28. When the direct method is used to record inventory at marketa. there is a direct reduction in the selling price of the product that results in a loss being

recorded on the income statement prior to the sale.b. a loss is recorded directly in the inventory account by crediting inventory and debiting

loss on inventory decline.c. only the portion of the loss attributable to inventory sold during the period is recorded

in the financial statements.d. the market value figure for ending inventory is substituted for cost and the loss is

buried in cost of goods sold.

S29. Recording inventory at net realizable value is permitted, even if it is above cost, when there are no significant costs of disposal involved anda. the ending inventory is determined by a physical inventory count.b. a normal profit is not anticipated.c. there is a controlled market with a quoted price applicable to all quantities.d. the internal revenue service is assured that the practice is not used only to distort

reported net income.

30. When inventory declines in value below original (historical) cost, and this decline is considered other than temporary, what is the maximum amount that the inventory can be valued at?a. Sales priceb. Net realizable valuec. Historical costd. Net realizable value reduced by a normal profit margin

9 - 8

Inventories: Additional Valuation Issues

31. Net realizable value isa. acquisition cost plus costs to complete and sell.b. selling price.c. selling price plus costs to complete and sell.d. selling price less costs to complete and sell.

32. If a unit of inventory has declined in value below original cost, but the market value exceeds net realizable value, the amount to be used for purposes of inventory valuation isa. net realizable value.b. original cost.c. market value.d. net realizable value less a normal profit margin.

33. Inventory may be recorded at net realizable value ifa. there is a controlled market with a quoted price.b. there are no significant costs of disposal.c. the inventory consists of precious metals or agricultural products.d. all of these.

34. If a material amount of inventory has been ordered through a formal purchase contract at the balance sheet date for future delivery at firm prices,a. this fact must be disclosed.b. disclosure is required only if prices have declined since the date of the order.c. disclosure is required only if prices have since risen substantially.d. an appropriation of retained earnings is necessary.

35. The credit balance that arises when a net loss on a purchase commitment is recognized should bea. presented as a current liability.b. subtracted from ending inventory.c. presented as an appropriation of retained earnings.d. presented in the income statement.

P36. In 2006, Lucas Manufacturing signed a contract with a supplier to purchase raw materials in 2007 for $700,000. Before the December 31, 2006 balance sheet date, the market price for these materials dropped to $510,000. The journal entry to record this situation at December 31, 2006 will result in a credit that should be reporteda. as a valuation account to Inventory on the balance sheet.b. as a current liability.c. as an appropriation of retained earnings.d. on the income statement.

S37. Which of the following is not a basic assumption of the gross profit method?a. The beginning inventory plus the purchases equal total goods to be accounted for.b. Goods not sold must be on hand.c. If the sales, reduced to the cost basis, are deducted from the sum of the opening

inventory plus purchases, the result is the amount of inventory on hand.d. The total amount of purchases and the total amount of sales remain relatively

unchanged from the comparable previous period.

9 - 9

Test Bank for Intermediate Accounting, Twelfth Edition

38. The gross profit method of inventory valuation is invalid whena. a portion of the inventory is destroyed.b. there is a substantial increase in inventory during the year.c. there is no beginning inventory because it is the first year of operation.d. none of these.

39. Which statement is not true about the gross profit method of inventory valuation?a. It may be used to estimate inventories for interim statements.b. It may be used to estimate inventories for annual statements.c. It may be used by auditors.d. None of these.

40. A major advantage of the retail inventory method is that ita. provides reliable results in cases where the distribution of items in the inventory is

different from that of items sold during the period.b. hides costs from competitors and customers.c. gives a more accurate statement of inventory costs than other methods.d. provides a method for inventory control and facilitates determination of the periodic

inventory for certain types of companies.

41. An inventory method which is designed to approximate inventory valuation at the lower of cost or market isa. last-in, first-out.b. first-in, first-out.c. conventional retail method.d. specific identification.

42. The retail inventory method is based on the assumption that thea. final inventory and the total of goods available for sale contain the same proportion of

high-cost and low-cost ratio goods.b. ratio of gross margin to sales is approximately the same each period.c. ratio of cost to retail changes at a constant rate.d. proportions of markups and markdowns to selling price are the same.

43. Which statement is true about the retail inventory method?a. It may not be used to estimate inventories for interim statements.b. It may not be used to estimate inventories for annual statements.c. It may not be used by auditors.d. None of these.

44. When the conventional retail inventory method is used, markdowns are commonly ignored in the computation of the cost to retail ratio becausea. there may be no markdowns in a given year.b. this tends to give a better approximation of the lower of cost or market.c. markups are also ignored.d. this tends to result in the showing of a normal profit margin in a period when no

markdown goods have been sold.

9 - 10

Inventories: Additional Valuation Issues

45. To produce an inventory valuation which approximates the lower of cost or market using the conventional retail inventory method, the computation of the ratio of cost to retail shoulda. include markups but not markdowns.b. include markups and markdowns.c. ignore both markups and markdowns.d. include markdowns but not markups.

*46. When calculating the cost ratio for the retail inventory method,a. if it is the conventional method, the beginning inventory is included and markdowns

are deducted.b. if it is the LIFO method, the beginning inventory is excluded and markdowns are

deducted.c. if it is the LIFO method, the beginning inventory is included and markdowns are not

deducted.d. if it is the conventional method, the beginning inventory is excluded and markdowns

are not deducted.

S47. Which of the following is not required when using the retail inventory method?a. All inventory items must be categorized according to the retail markup percentage

which reflects the item's selling price.b. A record of the total cost and retail value of goods purchased.c. A record of the total cost and retail value of the goods available for sale.d. Total sales for the period.

S48. Which of the following is not a reason the retail inventory method is used widely?a. As a control measure in determining inventory shortagesb. For insurance informationc. To permit the computation of net income without a physical count of inventoryd. To defer income tax liability

P49. Which of the following statements is false regarding an assumption of inventory cost flow?a. The cost flow assumption need not correspond to the actual physical flow of goods.b. The assumption selected may be changed each accounting period.c. The FIFO assumption uses the earliest acquired prices to cost the items sold during a

period.d. The LIFO assumption uses the earliest acquired prices to cost the items on hand at

the end of an accounting period.

P50. The average days to sell inventory is computed by dividinga. 365 days by the inventory turnover ratio.b. the inventory turnover ratio by 365 days.c. net sales by the inventory turnover ratio.d. 365 days by cost of goods sold.

51. The inventory turnover ratio is computed by dividing the cost of goods sold bya. beginning inventory.b. ending inventory.c. average inventory.d. number of days in the year.

9 - 11

Test Bank for Intermediate Accounting, Twelfth Edition

*52. When using dollar-value LIFO, if the incremental layer was added last year, it should be multiplied bya. last year's cost ratio and this year's index.b. this year's cost ratio and this year's index.c. last year's cost ratio and last year's index.d. this year's cost ratio and last year's index.

Multiple Choice Answers—ConceptualItem Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.

21. d 26. c 31. d 36. b 41. c *46. b 51. c22. d 27. d 32. a 37. d 42. a 47. a *52. c23. c 28. d 33. d 38. d 43. d 48. d24. b 29. c 34. a 39. b 44. b 49. b25. a 30. b 35. a 40. d 45. a 50. a

Solutions to those Multiple Choice questions for which the answer is “none of these.”

38. The gross profit percentage applicable to the goods in ending inventory is different from the percentage applicable to the goods sold during the period.

43. Many answers are possible.

MULTIPLE CHOICE—Computational

53. Marr Corporation has two products in its ending inventory, each accounted for at the lower of cost or market. A profit margin of 30% on selling price is considered normal for each product. Specific data with respect to each product follows:

In pricing its ending inventory using the lower-of-cost-or-market, what unit values should Marr use for products #1 and #2, respectively?a. $40.00 and $65.00.b. $46.00 and $65.00.c. $46.00 and $60.00.d. $45.00 and $54.00.

54. Paul Konerko Company sells product 2005WSC for $20 per unit. The cost of one unit of 2005WSC is $18, and the replacement cost is $17. The estimated cost to dispose of a unit is $4, and the normal profit is 40%. At what amount per unit should product 2005WSC be reported, applying lower-of-cost-or-market?a. $8.b. $16.c. $17.d. $18.

9 - 12

Inventories: Additional Valuation Issues

55. Remington Company sells product 1976NLC for $40 per unit. The cost of one unit of 1976NLC is $36, and the replacement cost is $34. The estimated cost to dispose of a unit is $8, and the normal profit is 40%. At what amount per unit should product 1976NLC be reported, applying lower-of-cost-or-market?a. $16.b. $32.c. $34.d. $36.

56. Joe Crede Corporation sells its product, a rare metal, in a controlled market with a quoted price applicable to all quantities. The total cost of 5,000 pounds of the metal now held in inventory is $250,000. The total selling price is $600,000, and estimated costs of disposal are $10,000. At what amount should the inventory of 5,000 pounds be reported in the balance sheet?a. $240,000.b. $250,000.c. $590,000.d. $600,000.

57. Pettengal Corporation sells its product, a rare metal, in a controlled market with a quoted price applicable to all quantities. The total cost of 5,000 pounds of the metal now held in inventory is $150,000. The total selling price is $350,000, and estimated costs of disposal are $5,000. At what amount should the inventory of 5,000 pounds be reported in the balance sheet?a. $145,000.b. $150,000.c. $345,000.d. $350,000.

58. Jermaine Dye Corporation acquired two inventory items at a lump-sum cost of $50,000. The acquisition included 3,000 units of product LF, and 7,000 units of product 1B. LF normally sells for $15 per unit, and 1B for $5 per unit. If Dye sells 1,000 units of LF, what amount of gross profit should it recognize?a. $1,875b. $5,625.c. $10,000.d. $11,875.

59. Williamson Corporation acquired two inventory items at a lump-sum cost of $40,000. The acquisition included 3,000 units of product CF, and 7,000 units of product 3B. CF normally sells for $12 per unit, and 3B for $4 per unit. If Williamson sells 1,000 units of CF, what amount of gross profit should it recognize?a. $1,500.b. $4,500.c. $8,000.d. $9,500.

9 - 13

Test Bank for Intermediate Accounting, Twelfth Edition

60. At a lump-sum cost of $48,000, Sealy Company recently purchased the following items for resale:

Item No. of Items Purchased Resale Price Per UnitM 4,000 $2.50N 2,000 8.00O 6,000 4.00

The appropriate cost per unit of inventory is:M N O

61. During 2006, Reese Co., a manufacturer of chocolate candies, contracted to purchase 100,000 pounds of cocoa beans at $4.00 per pound, delivery to be made in the spring of 2007. Because a record harvest is predicted for 2007, the price per pound for cocoa beans had fallen to $3.10 by December 31, 2006.

Of the following journal entries, the one which would properly reflect in 2006 the effect of the commitment of Reese Co. to purchase the 100,000 pounds of cocoa isa. Cocoa Inventory.............................................................. 400,000

Loss on Purchase Commitments.................................... 90,000Accounts Payable............................................... 400,000

c. Estimated Loss on Purchase Commitments................... 90,000Estimated Liability on Purchase Commitments... 90,000

d. No entry would be necessary in 2006

62. AJ Corporation, a manufacturer of ethnic foods, contracted in 2007 to purchase 500 pounds of a spice mixture at $5.00 per pound, delivery to be made in spring of 2008. By 12/31/07, the price per pound of the spice mixture had risen to $5.60 per pound. In 2007, AJ should recognizea. a loss of $2,500.b. a loss of $300.c. no gain or loss.d. a gain of $300.

63. DT Corporation, a manufacturer of Mexican foods, contracted in 2007 to purchase 1,000 pounds of a spice mixture at $5.00 per pound, delivery to be made in spring of 2008. By 12/31/07, the price per pound of the spice mixture had dropped to $4.60 per pound. In 2007, DT should recognizea a loss of $5,000.b. a loss of $400.c. no gain or loss.d. a gain of $400.

9 - 14

Inventories: Additional Valuation Issues

64. The following information is available for October for Jordan Company.

A fire destroyed Jordan’s October 31 inventory, leaving undamaged inventory with a cost of $3,000. Using the gross profit method, the estimated ending inventory destroyed by fire isa. $17,000.b. $77,000.c. $80,000.d. $100,000.

65. The following information is available for October for Horton Company.

A fire destroyed Horton’s October 31 inventory, leaving undamaged inventory with a cost of $6,000. Using the gross profit method, the estimated ending inventory destroyed by fire isa. $34,000.b. $154,000.c. $160,000.d. $200,000.

Use the following information for questions 66 and 67.

Sloan Company, a wholesaler, budgeted the following sales for the indicated months:

June July August Sales on account $1,800,000 $1,840,000 $1,900,000Cash sales 180,000 200,000 260,000Total sales $1,980,000 $2,040,000 $2,160,000

All merchandise is marked up to sell at its invoice cost plus 20%. Merchandise inventories at the beginning of each month are at 30% of that month's projected cost of goods sold.

66. The cost of goods sold for the month of June is anticipated to bea. $1,440,000.b. $1,500,000.c. $1,520,000.d. $1,650,000.

67. Merchandise purchases for July are anticipated to bea. $1,632,000.b. $2,076,000.c. $1,700,000.d. $1,730,000.

9 - 15

Test Bank for Intermediate Accounting, Twelfth Edition

68. Gomez Company had a gross profit of $360,000, total purchases of $420,000, and an ending inventory of $240,000 in its first year of operations as a retailer. Gomez’s sales in its first year must have beena. $540,000.b. $660,000.c. $180,000.d. $600,000.

69. A markup of 40% on cost is equivalent to what markup on selling price?a. 29%b. 40%c. 60%d. 71%

70. Miller, Inc. estimates the cost of its physical inventory at March 31 for use in an interim financial statement. The rate of markup on cost is 25%. The following account balances are available:

Inventory, March 1 $220,000Purchases 172,000Purchase returns 8,000Sales during March 300,000

The estimate of the cost of inventory at March 31 would bea. $84,000.b. $144,000.c. $159,000.d. $112,000.

71. On January 1, 2007, the merchandise inventory of Colaw, Inc. was $800,000. During 2007 Colaw purchased $1,600,000 of merchandise and recorded sales of $2,000,000. The gross profit rate on these sales was 25%. What is the merchandise inventory of Colaw at December 31, 2007?a. $400,000.b. $500,000.c. $900,000.d. $1,500,000.

72. For 2007, cost of goods available for sale for Vale Corporation was $900,000. The gross profit rate was 20%. Sales for the year were $800,000. What was the amount of the ending inventory?a. $0.b. $260,000.c. $180,000.d. $160,000.

73. On April 15 of the current year, a fire destroyed the entire uninsured inventory of a retail store. The following data are available:

Sales, January 1 through April 15 $300,000Inventory, January 1 50,000Purchases, January 1 through April 15 250,000Markup on cost 25%

9 - 16

Inventories: Additional Valuation Issues

The amount of the inventory loss is estimated to bea. $60,000.b. $30,000.c. $75,000.d. $50,000.

74. The inventory account of Lance Company at December 31, 2007, included the following items:

Inventory AmountMerchandise out on consignment at sales price

(including markup of 40% on selling price) $15,000Goods purchased, in transit (shipped f.o.b. shipping point) 12,000Goods held on consignment by Lance 13,000Goods out on approval (sales price $7,600, cost $6,400) 7,600

Based on the above information, the inventory account at December 31, 2007, should be reduced bya. $20,200.b. $22,600.c. $32,200.d. $32,000.

75. Flynn Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year:

If the ending inventory is to be valued at the lower-of-cost-or-market, what is the cost to retail ratio?a. $177,500 ÷ $250,000b. $177,500 ÷ $258,500c. $175,000 ÷ $260,000d. $177,500 ÷ $248,500

Use the following information for questions 76 through 80.

The following data concerning the retail inventory method are taken from the financial records of Stone Company.

Test Bank for Intermediate Accounting, Twelfth Edition

76. The ending inventory at retail should bea. $74,000.b. $60,000.c. $64,000.d. $42,000.

77. If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost to retail ratio should be based on goods available for sale at (1) cost and (2) retail, respectively ofa. $279,000 and $410,000.b. $279,000 and $396,000.c. $279,000 and $390,000.d. $273,000 and $390,000.

78. If the foregoing figures are verified and a count of the ending inventory reveals that merchandise actually on hand amounts to $54,000 at retail, the business hasa. realized a windfall gain.b. sustained a loss.c. no gain or loss as there is close coincidence of the inventories.d. none of these.

*79. Assuming no change in the price level if the LIFO inventory method were used in conjunction with the data, the ending inventory at cost would bea. $42,600.b. $42,000.c. $40,800.d. $43,200.

*80. Assuming that the LIFO inventory method were used in conjunction with the data and that the inventory at retail had increased during the period, then the computation of retail in the cost to retail ratio woulda. exclude both markups and markdowns and include beginning inventory.b. include markups and exclude both markdowns and beginning inventory.c. include both markups and markdowns and exclude beginning inventory.d. exclude markups and include both markdowns and beginning inventory.

81. Gooch Corporation had the following amounts, all at retail:

Beginning inventory $ 3,600 Purchases $120,000Purchase returns 6,000 Net markups 18,000Abnormal shortage 4,000 Net markdowns 2,800Sales 72,000 Sales returns 1,800Employee discounts 1,600 Normal shortage 2,600

What is Gooch’s ending inventory at retail?a. $54,400.b. $56,000.c. $57,600.d. $58,400

9 - 18

Inventories: Additional Valuation Issues

82. Dryer Corporation had the following amounts, all at retail:

Beginning inventory $ 3,600 Purchases $100,000Purchase returns 6,000 Net markups 18,000Abnormal shortage 4,000 Net markdowns 2,800Sales 72,000 Sales returns 1,800Employee discounts 1,600 Normal shortage 2,600

What is Dryer’s ending inventory at retail?a. $34,400.b. $36,000.c. $37,600.d. $38,400

83. Dye Corporation’s computation of cost of goods sold is:

Beginning inventory $ 60,000Add: Cost of goods purchased 405,000Cost of goods available for sale 465,000Ending inventory 90,000Cost of goods sold $375,000

The average days to sell inventory for Dye area. 58.4 days.b. 67.6 days.c. 73.0 days.d. 87.6 days.

84. Ace Corporation’s computation of cost of goods sold is:

Beginning inventory $ 60,000Add: Cost of goods purchased 405,000Cost of goods available for sale 465,000Ending inventory 80,000Cost of goods sold $385,000

The average days to sell inventory for Ace area. 56.9 days.b. 63.1 days.c. 66.4 days.d. 75.8 days.

85. The 2007 financial statements of Wert Company reported a beginning inventory of $80,000, an ending inventory of $120,000, and cost of goods sold of $600,000 for the year. Wert’s inventory turnover ratio for 2007 isa. 7.5 times.b. 6.0 times.c. 5.0 times.d. 4.3 times.

9 - 19

Test Bank for Intermediate Accounting, Twelfth Edition

Use the following information for questions 86 through 90.

Trent Co. uses the retail inventory method. The following information is available for the current year.

86. If the ending inventory is to be valued at approximately lower of average cost or market, the calculation of the cost ratio should be based on cost and retail ofa. $300,000 and $430,000.b. $300,000 and $428,000.c. $373,000 and $550,000.d. $378,000 and $552,000.

87. The ending inventory at retail should bea. $160,000.b. $150,000.c. $144,000.d. $140,000.

88. The approximate cost of the ending inventory by the conventional retail method isa. $95,900.b. $94,920.c. $98,000.d. $102,480.

*89. If the ending inventory is to be valued at approximately LIFO cost, the calculation of the cost ratio should be based on cost and retail ofa. $378,000 and $552,000.b. $378,000 and $532,000.c. $300,000 and $410,000.d. $300,000 and $430,000.

*90. Assuming that the LIFO inventory method is used, that the beginning inventory is the base inventory when the index was 100, and that the index at year end is 112, the ending inventory at dollar-value LIFO retail cost isa. $80,460.b. $92,757.c. $95,900.d. $102,480.

9 - 20

Inventories: Additional Valuation Issues

Use the following information for questions 91 and 92.

Baker Company, which uses the retail LIFO method to determine inventory cost, has provided the following information for 2007:

*91. Assuming stable prices (no change in the price index during 2007), what is the cost of Baker's inventory at December 31, 2007?a. $128,100.b. $138,100.c. $136,000.d. $132,300.

*92. Assuming that the price index was 105 at December 31, 2007 and 100 at January 1, 2007, what is the cost of Baker's inventory at December 31, 2007 under the dollar-value-LIFO retail method?a. $133,690.b. $138,915.c. $140,305.d. $131,800.

Multiple Choice Answers—ComputationalItem Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.

53. a 59. b 65. a 71. c 77. a 83. c *89. c54. b 60. c 66. d 72. b 78. b 84. c *90. a55. b 61. c 67. d 73. a *79. b 85. b *91. b56. c 62. c 68. a 74. a *80. c 86. d *92. a57. c 63. b 69. a 75. b 81. a 87. d58. b 64. a 70. b 76. b 82. a 88. a

9 - 21

Test Bank for Intermediate Accounting, Twelfth Edition

MULTIPLE CHOICE—CPA Adapted

93. Teel Distribution Co. has determined its December 31, 2007 inventory on a FIFO basis at $250,000. Information pertaining to that inventory follows:

Teel records losses that result from applying the lower-of-cost-or-market rule. At December 31, 2007, the loss that Teel should recognize isa. $0.b. $5,000.c. $20,000.d. $25,000.

94. Under the lower-of-cost-or-market method, the replacement cost of an inventory item would be used as the designated market valuea. when it is below the net realizable value less the normal profit margin.b. when it is below the net realizable value and above the net realizable value less the

normal profit margin.c. when it is above the net realizable value.d. regardless of net realizable value.

95. The original cost of an inventory item is above the replacement cost and the net realizable value. The replacement cost is below the net realizable value less the normal profit margin. As a result, under the lower-of-cost-or-market method, the inventory item should be reported at thea. net realizable value.b. net realizable value less the normal profit margin.c. replacement cost.d. original cost.

96. Gore Company's accounting records indicated the following information:

Inventory, 1/1/07 $ 600,000Purchases during 2007 3,000,000Sales during 2007 3,800,000

A physical inventory taken on December 31, 2007, resulted in an ending inventory of $700,000. Gore's gross profit on sales has remained constant at 25% in recent years. Gore suspects some inventory may have been taken by a new employee. At December 31, 2007, what is the estimated cost of missing inventory?a. $50,000.b. $150,000.c. $200,000.d. $250,000.

9 - 22

Inventories: Additional Valuation Issues

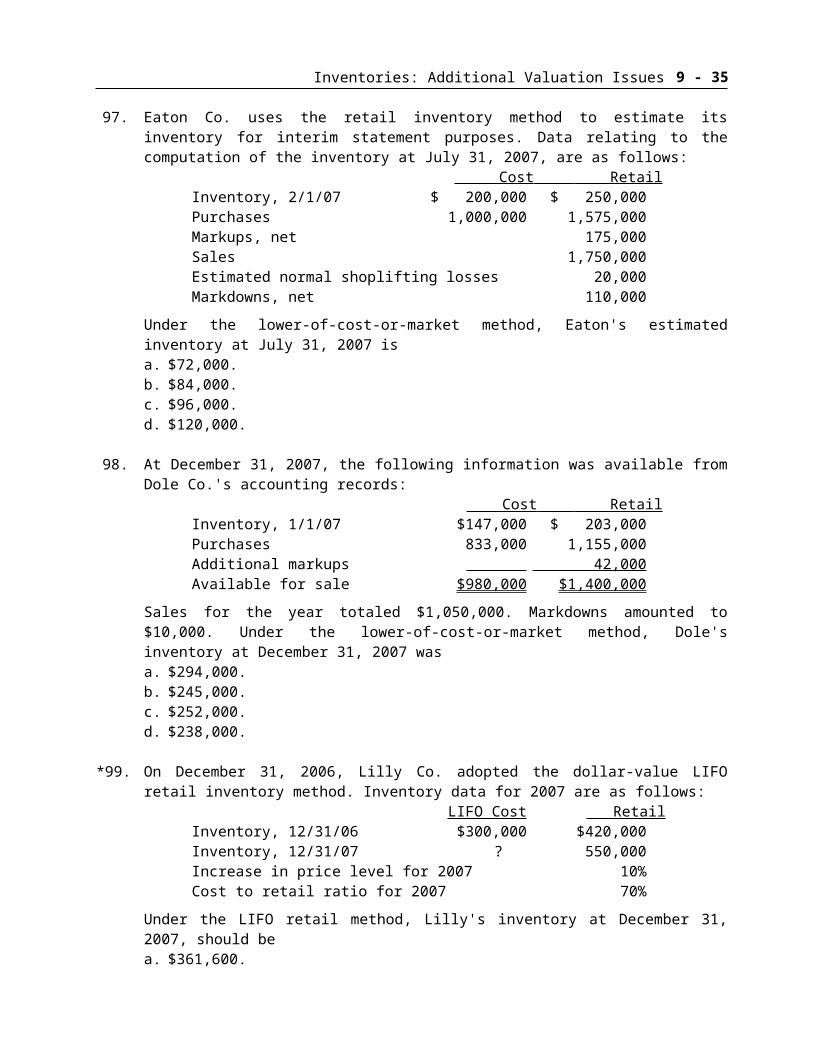

97. Eaton Co. uses the retail inventory method to estimate its inventory for interim statement purposes. Data relating to the computation of the inventory at July 31, 2007, are as follows:

Cost Retail Inventory, 2/1/07 $ 200,000 $ 250,000Purchases 1,000,000 1,575,000Markups, net 175,000Sales 1,750,000Estimated normal shoplifting losses 20,000Markdowns, net 110,000

Under the lower-of-cost-or-market method, Eaton's estimated inventory at July 31, 2007 isa. $72,000.b. $84,000.c. $96,000.d. $120,000.

98. At December 31, 2007, the following information was available from Dole Co.'s accounting records:

Cost Retail Inventory, 1/1/07 $147,000 $ 203,000Purchases 833,000 1,155,000Additional markups 42,000Available for sale $980,000 $1,400,000

Sales for the year totaled $1,050,000. Markdowns amounted to $10,000. Under the lower-of-cost-or-market method, Dole's inventory at December 31, 2007 wasa. $294,000.b. $245,000.c. $252,000.d. $238,000.

*99. On December 31, 2006, Lilly Co. adopted the dollar-value LIFO retail inventory method. Inventory data for 2007 are as follows:

LIFO Cost Retail Inventory, 12/31/06 $300,000 $420,000Inventory, 12/31/07 ? 550,000Increase in price level for 2007 10%Cost to retail ratio for 2007 70%

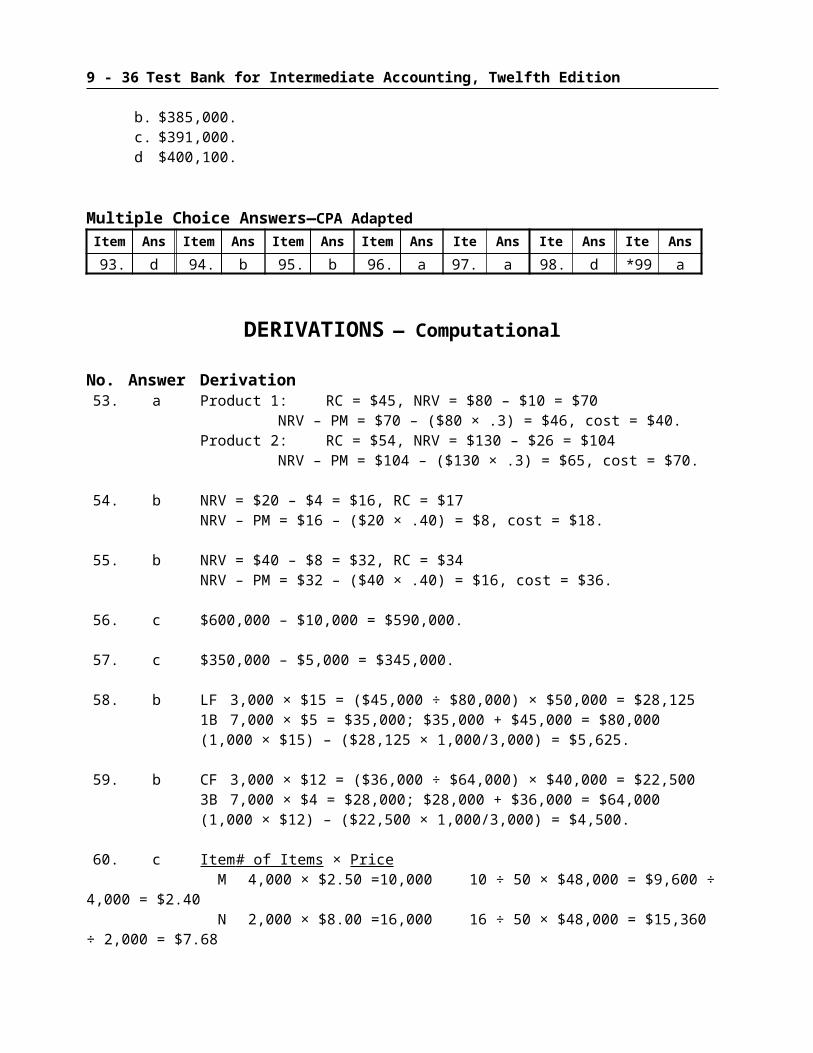

Under the LIFO retail method, Lilly's inventory at December 31, 2007, should bea. $361,600.b. $385,000.c. $391,000.d $400,100.

Multiple Choice Answers—CPA AdaptedItem Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.

93. d 94. b 95. b 96. a 97. a 98. d *99. a

9 - 23

Test Bank for Intermediate Accounting, Twelfth Edition

Determine the proper unit inventory price in the following independent cases by applying the lower of cost or market rule. Circle your choice.

1 2 3 4 5 Cost $8.00 $10.50 $12.00 $6.00 $7.20Net realizable value 8.85 10.00 12.20 4.25 6.90Net realizable value less normal profit 8.15 9.00 11.40 3.75 6.00Market replacement cost 7.90 10.10 12.50 4.00 5.40

Solution 9-100Case 1 $ 8.00 Case 4 $4.00Case 2 $10.00 Case 5 $6.00Case 3 $12.00

Ex. 9-101—Lower-of-cost-or-market.

Determine the unit value that should be used for inventory costing following "lower of cost or market value" as described in ARB No. 43.

A B C D E F Cost $2.35 $2.48 $2.25 $2.54 $2.34 $2.43Replacement cost 2.26 2.55 2.20 2.52 2.32 2.46Net realizable value 2.50 2.50 2.50 2.50 2.50 2.50Net realizable value less normal profit 2.30 2.30 2.30 2.30 2.30 2.30

Solution 9-101Case A $2.30 Case D $2.50Case B $2.48 Case E $2.32Case C $2.25 Case F $2.43

Ex. 9-102—Lower-of-cost-or-market.

Assume in each case that the selling expenses are $8 per unit and that the normal profit is $5 per unit. Calculate the limits for each case. Then enter the amount that should be used for lower of cost or market.

InstructionsUsing the lower-of-cost-or-market approach applied on an individual-item basis, compute the inventory valuation that should be reported for each product on December 31, 2007.

At 12/31/06, the end of Feeney Company's first year of business, inventory was $4,100 and $2,800 at cost and at market, respectively.

Following is data relative to the 12/31/07 inventory of Feeney:

9 - 28

Inventories: Additional Valuation Issues

Ex. 9-104 (cont).

Original Net Net Realizable AppropriateCost Replacement Realizable Value Less Inventory

Item Per Unit Cost Value Normal Profit Value A $ .65 $ .45B .45 .40C .70 .75D .75 .65E .90 .85

Selling price is $1.00/unit for all items. Disposal costs amount to 10% of selling price and a "normal" profit is 30% of selling price. There are 1,000 units of each item in the 12/31/07 inventory.

Instructions(a) Prepare the entry at 12/31/06 necessary to implement the lower-of-cost-or-market procedure

assuming Feeney uses a contra account for its balance sheet.(b) Complete the last three columns in the 12/31/07 schedule above based upon the lower-of-

cost-or-market rules.(c) Prepare the entry(ies) necessary at 12/31/07 based on the data above.(d) How are inventory losses disclosed on the income statement?

Solution 9-104(a) Loss Due to Market Decline of Inventory.................................... 1,300

Allowance to Reduce Inventory to Market...................... 1,300

(b) Original Net Net Realizable AppropriateCost Replacement Realizable Value Less Inventory

Item Per Unit Cost Value Normal Profit Value A $ .65 $ .45 $ .90 $ .60 $ .60B .45 .40 .90 .60 .45C .70 .75 .90 .60 .70D .75 .65 .90 .60 .65E .90 .85 .90 .60 .85

$3.45 $3.25*

*$3.25 × 1,000 = $3,250

(c) Allowance to Reduce Inventory to Market.................................. 1,300Cost of Goods Sold......................................................... 1,300

Loss Due to Market Decline of Inventory.................................... 200Allowance to Reduce Inventory to Market...................... 200

(Cost of inventory at 12/31/07 = $7,250)

ORA student can record a recovery of $1,100.

(d) Inventory losses can be disclosed separately (below gross profit in operating expenses) or they can be shown as part of cost of goods sold.

9 - 29

Test Bank for Intermediate Accounting, Twelfth Edition

Ex. 9-105 – Relative sales value method.

Adler Realty Company purchased a plot of ground for $800,000 and spent $2,100,000 in developing it for building lots. The lots were classified into Highland, Midland, and Lowland grades, to sell at $100,000, $75,000, and $50,000 each, respectively.

InstructionsComplete the table below to allocate the cost of the lots using a relative sales value method.

No. of Selling Total % of Apportioned Cost Grade Lots Price Revenue Total Sales Total Per Lot Highland 20 $ $ $ $Midland 40 $ $Lowland 100 $ $

160 $ $

Solution 9-105 No. of Selling Total % of Apportioned Cost

Grade Lots Price Revenue Total Sales Total Per Lot Highland 20 $100,000 $ 2,000,000 20% $ 580,000 $29,000Midland 40 $75,000 3,000,000 30% 870,000 $21,750Lowland 100 $50,000 5,000,000 50% 1,450,000 $14,500

160 $10,000,000 $2,900,000

Ex. 9-106—Gross profit method.

An inventory taken the morning after a large theft discloses $60,000 of goods on hand as of March 12. The following additional data is available from the books:

Inventory on hand, March 1 $ 84,000Purchases received, March 1 – 11 63,000Sales (goods delivered to customers) 120,000

Past records indicate that sales are made at 50% above cost.

InstructionsEstimate the inventory of goods on hand at the close of business on March 11 by the gross profit method and determine the amount of the theft loss. Show appropriate titles for all amounts in your presentation.

Solution 9-106Beginning Inventory $ 84,000Purchases 63,000Goods Available 147,000Goods Sold ($120,000 ÷ 150%) 80,000Estimated Ending Inventory 67,000Physical Inventory 60,000Theft Loss $ 7,000

9 - 30

Inventories: Additional Valuation Issues

Ex. 9-107—Gross profit method.

On January 1, a store had inventory of $48,000. January purchases were $46,000 and January sales were $90,000. On February 1 a fire destroyed most of the inventory. The rate of gross profit was 25% of cost. Merchandise with a selling price of $5,000 remained undamaged after the fire. Compute the amount of the fire loss, assuming the store had no insurance coverage. Label all figures.

Solution 9-107Beginning Inventory $ 48,000Purchases 46,000Goods available 94,000Cost of sale ($90,000 ÷ 125%) (72,000)Estimated ending inventory 22,000Cost of undamaged inventory ($5,000 ÷ 125%) (4,000)Estimated fire loss $18,000

Ex. 9-108—Gross profit method.

Reese Co. prepares monthly income statements. Inventory is counted only at year end; thus, month-end inventories must be estimated. All sales are made on account. The rate of mark-up on cost is 20%. The following information relates to the month of May.

Accounts receivable, May 1 $21,000Accounts receivable, May 31 27,000Collections of accounts during May 90,000Inventory, May 1 45,000Purchases during May 58,000

InstructionsCalculate the estimated cost of the inventory on May 31.

Solution 9-108Collections of accounts $ 90,000Add accounts receivable, May 31 27,000Deduct accounts receivable, May 1 (21,000)Sales during May $ 96,000

Inventory, May 1 $ 45,000Purchases during May 58,000Goods available 103,000Cost of sales ($96,000 ÷ 120%) (80,000)Estimated cost of inventory, May 31 $ 23,000

9 - 31

Test Bank for Intermediate Accounting, Twelfth Edition

Ex. 9-109—Comparison of inventory methods.

In the cases cited below, five different conditions are possible when X is compared with Y. These possibilities are as follows:

a. X equals Y d. X is equal to or greater than Yb. X is greater than Y e. X is equal to or less than Yc. X is less than Y

InstructionsIn the space provided show the relationship of X and Y for each of the following independent statements.

_____ 1. "Cost or market, whichever is lower," may be applied to (1) the inventory as a whole or to (2) categories of inventory items. Compare (X) the reported value of inventory when procedure (1) is used with (Y) the reported value of inventory when procedure (2) is used.

_____ 2. Prices have been rising steadily. Physical turnover of goods has occurred approxi-mately 4 times in the last year. Compare (X) the ending inventory computed by LIFO method with (Y) the same ending inventory computed by the moving average method.

_____ 3. The retail inventory method has been used by a store during its first year of operation. Compare (X) markdown cancellations with (Y) markdowns.

_____ 4. Prices have been rising steadily. At the beginning of the year a company adopted a new inventory method; the physical quantity of the ending inventory is the same as that of the beginning inventory. Compare (X) the reported value of inventory if LIFO was the new method with (Y) the reported value of inventory if FIFO was the new method.

_____ 5. Prices have been rising steadily. Physical turnover of goods has occurred five times in the last year. Compare (X) unit prices of ending inventory items at moving average pricing with (Y) those at weighted average pricing.

Solution 9-109 1. d 2. c 3. e 4. c 5. b

9 - 32

Inventories: Additional Valuation Issues

PROBLEMS

Pr. 9-110—Gross profit method.

On December 31, 2007 Carr Company's inventory burned. Sales and purchases for the year had been $1,400,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2007) was $170,000; in the past Carr's gross profit has averaged 40% of selling price.

InstructionsCompute the estimated cost of inventory burned, and give entries as of December 31, 2007 to close merchandise accounts.

Solution 9-110Beginning inventory $ 170,000Add: Purchases 980,000Cost of goods available 1,150,000Sales $1,400,000Less 40% (560,000) 840,000Estimated inventory lost $ 310,000

When you undertook the preparation of the financial statements for Vancey Company at January 31, 2007, the following data were available:

At Cost At Retail Inventory, February 1, 2006 $70,800 $ 98,500Markdowns 35,000Markups 63,000Markdown cancellations 20,000Markup cancellations 10,000Purchases 219,500 294,000Sales 345,000Purchases returns and allowances 4,300 5,500Sales returns and allowances 10,000

InstructionsCompute the ending inventory at cost as of January 31, 2007, using the retail method which approximates lower of cost or market. Your solution should be in good form with amounts clearly labeled.

9 - 33

Test Bank for Intermediate Accounting, Twelfth Edition

Totals 440,000Deduct markdowns (net) 15,000Sales price of goods available 425,000Sales less sales returns 335,000Ending inventory, 1/31/07 at retail $ 90,000Ending inventory at cost: Ratio of cost to retail =

The records of Irvin Stores included the following data:Inventory, May 1, at retail, $14,500; at cost, $10,440Purchases during May, at retail, $42,900; at cost, $31,550Freight-in, $2,000; purchase discounts, $250Additional markups, $3,800; markup cancellations, $400; net markdowns, $1,300Sales during May, $46,500

InstructionsCalculate the estimated inventory at May 31 on a LIFO basis. Show your calculations in good form and label all amounts.

*Solution 9-112 Cost Retail Ratio

Inventory, May 1 $10,440 $14,500 .72Purchases 31,550 42,900Freight-in 2,000Purchase discounts (250)Net markups 3,400Net markdowns (1,300)Totals excluding beginning inventory 33,300 45,000 .74Goods available $43,740 59,500Sales (46,500)Inventory, May 31 $13,000Estimated inventory, May 31 ($13,000 × .72) $ 9,360

Cabel Department Store wishes to use the retail LIFO method of valuing inventories for 2007. The appropriate data are as follows:

At Cost At Retail December 31, 2006 inventory (base layer) $1,150,000 $2,100,000Purchases (net of returns, allowances, markups, and markdowns) 2,100,000 3,500,000Sales 2,870,000Price index for 2007 105

InstructionsComplete the following schedule (fill in all blanks and show calculations in the parentheses):

Computation of Retail Inventory for 2007 Cost Retail Ratio

Inventory, December 31, 2006 $1,150,000 $2,100,000Purchases (net of returns, allowances,

markups, and markdowns) %

Total available $

____________________________________

Inventory, December 31, 2007, at retail $

Adjustment of Inventory to LIFO Basis Cost Retail

Ending inventory at base year prices $ ( )

Beginning inventory at base year prices $

Increase at base year prices $

Increase at 2007 retail ( ) $

Increase at 2007 cost ( )

Inventory, December 31, 2007, at LIFO cost $

*Solution 9-113Computation of Retail Inventory for 2007 Cost Retail RatioInventory, December 31, 2006 $1,150,000 $2,100,000Purchases (net of returns, allowances, markups, and

markdowns) 2,100,000 3,500,000 60%Total available $3,250,000 5,600,000Less: Sales 2,870,000

9 - 35

Test Bank for Intermediate Accounting, Twelfth Edition

Inventory, December 31, 2007, at retail $2,730,000

*Solution 9-113 (cont.)

Adjustment of Inventory to LIFO Basis Cost Retail Ending inventory at base year prices

($2,730,000 ÷ 1.05) $2,600,000Beginning inventory at base year prices $1,150,000 2,100,000Increase at base year prices $ 500,000

Increase at 2007 retail ($500,000 × 1.05) $ 525,000Increase at 2007 cost ($525,000 × 60%) 315,000Inventory, December 31, 2007 at LIFO cost $1,465,000

InstructionsAssuming that there was no change in the price index during the year, compute the inventory at December 31, 2007, using the LIFO retail inventory method.

*Solution 9-114Miller Variety Store

LIFO Retail ComputationDecember 31, 2007

At Cost At Retail RatioInventory, January 1, 2007 $136,000 $ 220,000Purchases 480,000 700,000Freight-in 80,000Net markups 160,000Net markdowns (60,000)Total (excluding beginning inventory) 560,000 800,000 70%Total (including beginning inventory) $696,000 1,020,000Less sales 720,000Inventory, Dec. 31, 2007, at retail $ 300,000

Ending inventory deflated ($330,000 ÷ 1.10) $ 300,000Base inventory $155,000 (250,000)Layer added $ 50,000New layer at end of year dollars ($50,000 × 1.10 × .64) 35,200Estimated inventory at dollar value, LIFO $190,200

*Pr. 9-116—Retail LIFO.

Horne Book Store uses the conventional retail method and is now considering converting to the LIFO retail method for the period beginning 1/1/07. Available information consists of the following:

Test Bank for Intermediate Accounting, Twelfth Edition

Loss from breakage — 500 — -0-Applicable price index — 100 — 110*Pr. 9-116 (cont.)

Following is a schedule showing the computation of the cost of inventory on hand at 12/31/06 based on the conventional retail method.

Cost Retail RatioInventory 1/1/06 $ 12,500 $ 22,500Purchases (net) 250,000 347,500Net markups — 5,000Goods available $262,500 375,000 70%Sales (net) (309,000)Net markdowns (2,500)Loss from breakage (500)Inventory 12/31/06 at retail $ 63,000Inventory 12/31/06 at LCM ($63,000 × 70%) $ 44,100

Instructions(a) Prepare the journal entry to convert the inventory from the conventional retail to the LIFO

retail method. Show detailed calculations to support your entry.

(b) Prepare a schedule showing the computation of the 12/31/07 inventory based on the LIFO retail method as adjusted for fluctuating prices. Without prejudice to your answer to (a) above, assume that you computed the 1/1/07 inventory (retail value $49,000) under the LIFO retail method at a cost of $34,000.

*Solution 9-116(a) Cost Retail

Goods available $262,500 $375,000Less: Beginning inventory (12,500) (22,500)

Net markdowns (2,500)Cost to retail $250,000 $350,000

Inventory.................................................................................... 900Adjustment to Record Inventory at Cost......................... 900

(b) Cost Retail RatioInventory $ 34,000 $ 49,000Purchases 245,000 345,000Net markups 10,000Net markdowns (5,000)Total 245,000 350,000 70%Total goods available $279,000 399,000Sales (311,000)Ending inventory at retail—end of year dollars $ 88,000