Addressing Environmental Liabilities When Buying Land or Business Addressing Environmental Liabilities When Buying Land or Business Loren Larson, Caltha LLP www.calthacompany.com Loren Larson, Caltha LLP www.calthacompany.com

Transcript

Addressing Environmental Liabilities When Buying Land or Business

Addressing Environmental Liabilities When Buying Land or Business

CERCLA (Superfund)Federal law that can require current landowner

to bear full burden of costs to remediate (clean up) site, even if contamination was caused by a previous landowner.

Also includes all past contributors to a contamination issue at another location.

CERCLA (Superfund)Federal law that can require current landowner

to bear full burden of costs to remediate (clean up) site, even if contamination was caused by a previous landowner.

Also includes all past contributors to a contamination issue at another location.

Evolution of Environmental Risk Management Evolution of Environmental Risk Management

Tools to manage property liabilities

Tools to manage property liabilities

Insurance coverage

Purchase agreements/escrow

Release from liability issued by agency

Avoidance

Management

Insurance coverage

Purchase agreements/escrow

Release from liability issued by agency

Avoidance

Management

Release from liability through agency

Release from liability through agency

Release from liability through agency

Release from liability through agency

Required an ASTM Phase 1

Required recent sampling data demonstrating impacts had occurred

Required a commitment to cooperate with agency in future clean up

“Covent Not To Sue” issued by State

based on existing information and conditions

property use restriction

Required an ASTM Phase 1

Required recent sampling data demonstrating impacts had occurred

Required a commitment to cooperate with agency in future clean up

“Covent Not To Sue” issued by State

based on existing information and conditions

property use restriction

Limits on property useLimits on property use

Soil contaminationSoil contamination

Exposure and risks managedExposure and risks managed

Cleansoil

Residual liabilityResidual liability

Contamination identified on title

Contamination stigma

Property use restrictions

If area is disturbed, then

Sampling/risk reevaluation

Reassessment by agency

Costs to remediate to new conditions

Contamination identified on title

Contamination stigma

Property use restrictions

If area is disturbed, then

Sampling/risk reevaluation

Reassessment by agency

Costs to remediate to new conditions

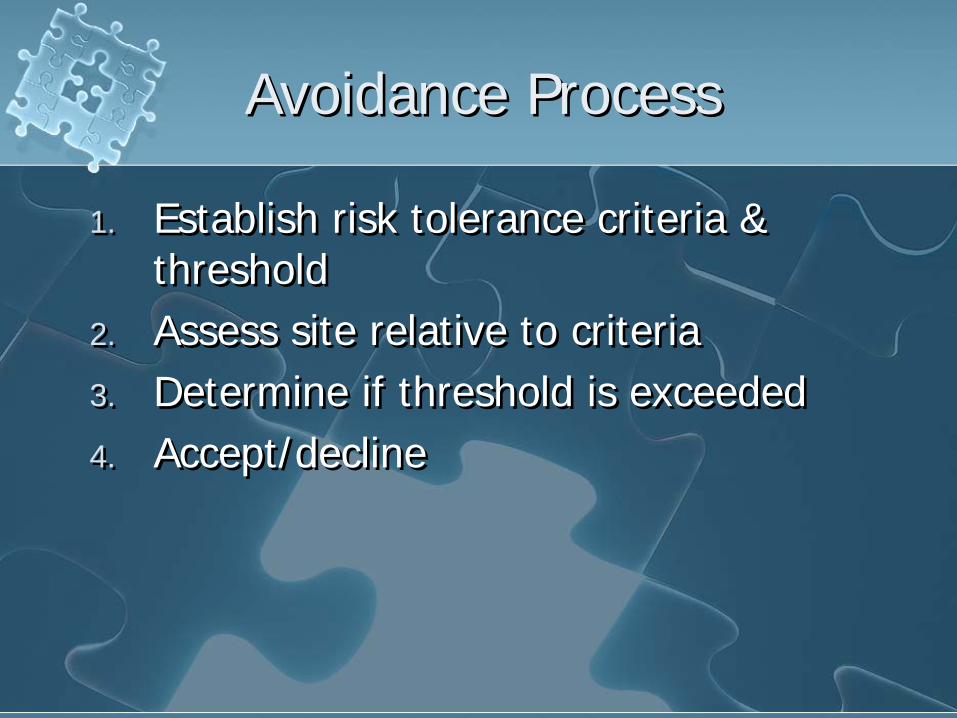

Avoidance ProcessAvoidance Process

1. Establish risk tolerance criteria & threshold

2. Assess site relative to criteria3. Determine if threshold is exceeded4. Accept/decline

1. Establish risk tolerance criteria & threshold

2. Assess site relative to criteria3. Determine if threshold is exceeded4. Accept/decline

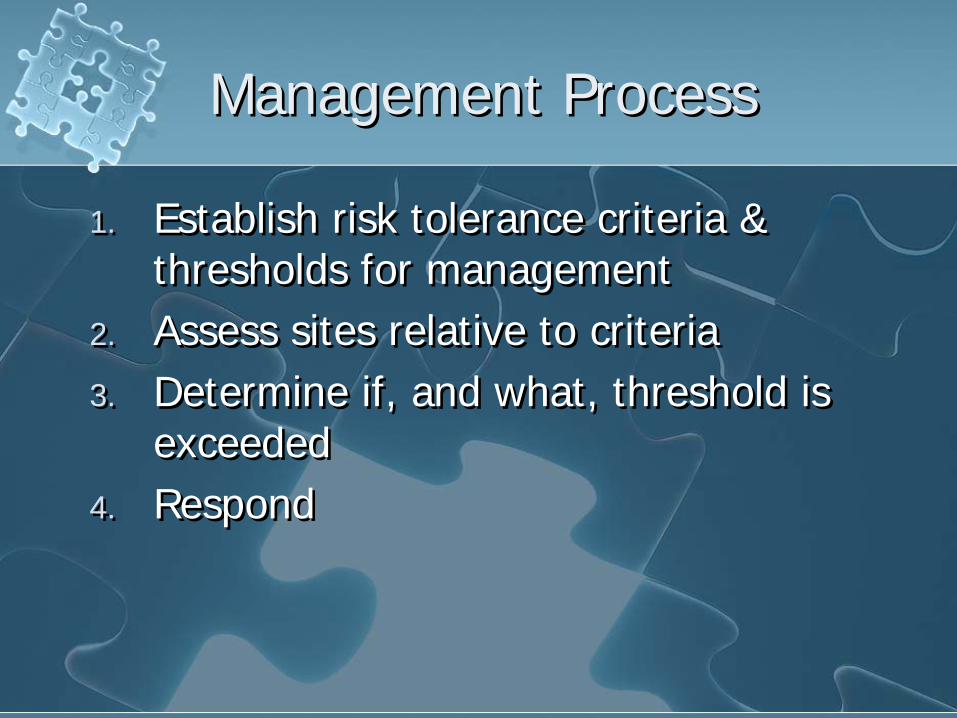

Management ProcessManagement Process

1. Establish risk tolerance criteria & thresholds for management

2. Assess sites relative to criteria3. Determine if, and what, threshold is

exceeded 4. Respond

1. Establish risk tolerance criteria & thresholds for management

2. Assess sites relative to criteria3. Determine if, and what, threshold is

exceeded4. Respond

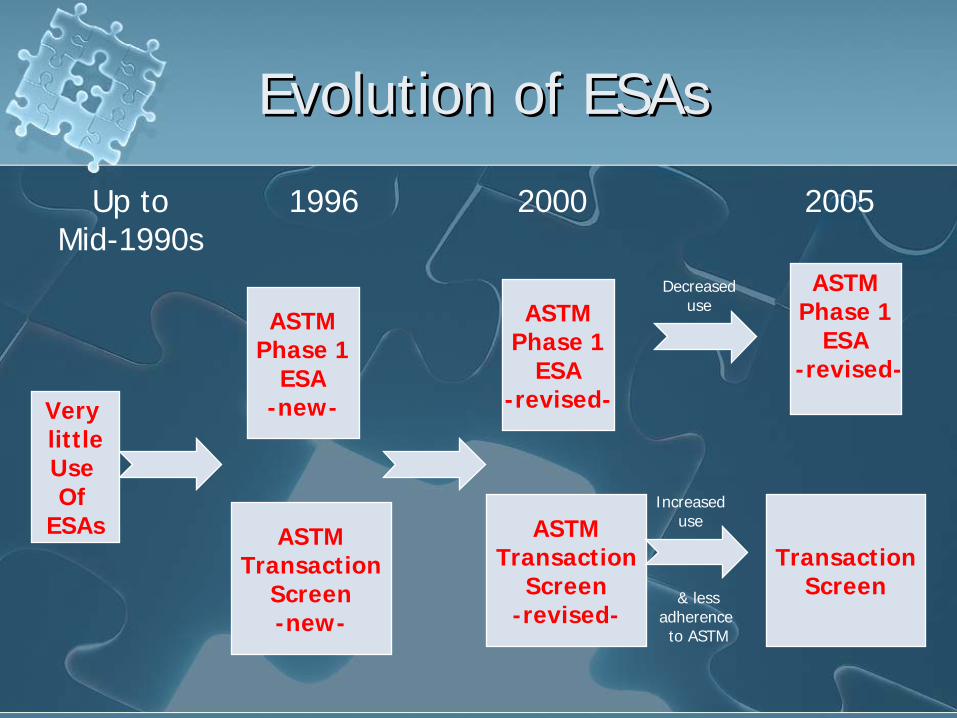

Evolution of ESAsEvolution of ESAs

Very littleUse Of

ESAs

Up toMid-1990s

ASTMPhase 1

ESA-revised-

ASTMTransaction

Screen-revised-

1996 2000 2005

TransactionScreen

ASTMPhase 1

ESA-revised-

Decreaseduse

Increaseduse

& lessadherence to ASTM

ASTMPhase 1

ESA-new-

ASTMTransaction

Screen-new-

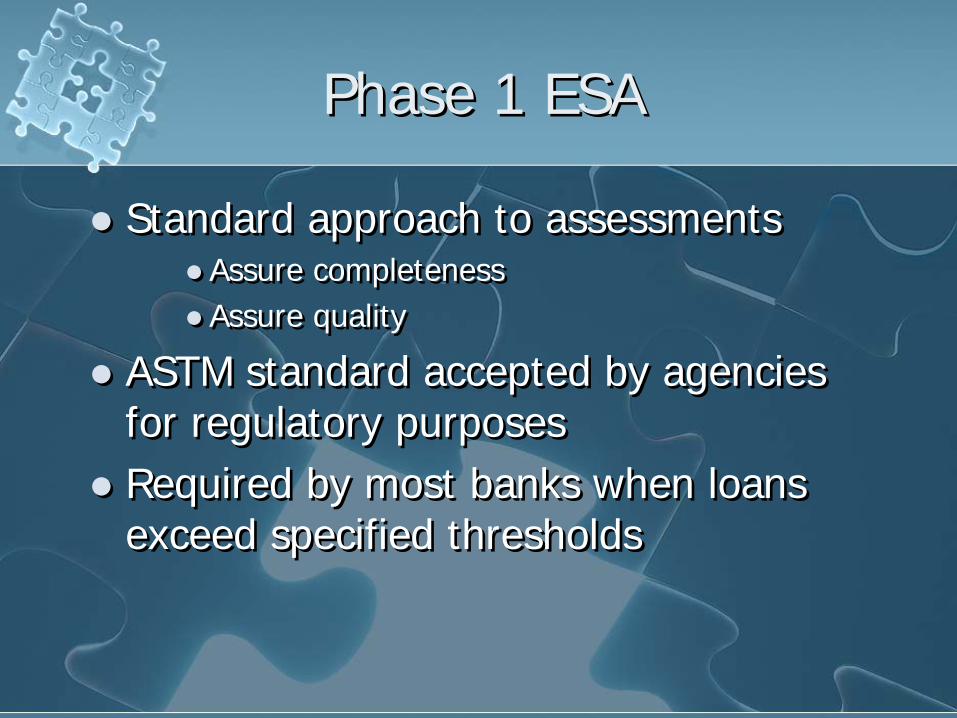

Phase 1 ESAPhase 1 ESA

Standard approach to assessments

Assure completeness

Assure quality

ASTM standard accepted by agencies for regulatory purposes

Required by most banks when loans exceed specified thresholds

Standard approach to assessments

Assure completeness

Assure quality

ASTM standard accepted by agencies for regulatory purposes

Required by most banks when loans exceed specified thresholds

Phase 1 ESAPhase 1 ESA

Purpose:“ …assemble information about

Recognized Environmental Conditions or business-related environmental risks in connection with the Subject Property or other neighboring properties.

Purpose:“ …assemble information about

Recognized Environmental Conditions or business-related environmental risks in connection with the Subject Property or other neighboring properties.

Phase 1 ESAPhase 1 ESA

Recognized Environmental Conditions:“ … the presence or likely presence of any

hazardous substance or petroleum products on the property under conditions that indicate an existing, past or material threat of release.”

“… The term does not include de minimis conditions that generally do not represent a material risk of harm to public health or the environment and would generally not be subject to enforcement action. “

Recognized Environmental Conditions:“ … the presence or likely presence of any

hazardous substance or petroleum products on the property under conditions that indicate an existing, past or material threat of release.”

“… The term does not include de minimis conditions that generally do not represent a material risk of harm to public health or the environment and would generally not be subject to enforcement action. “

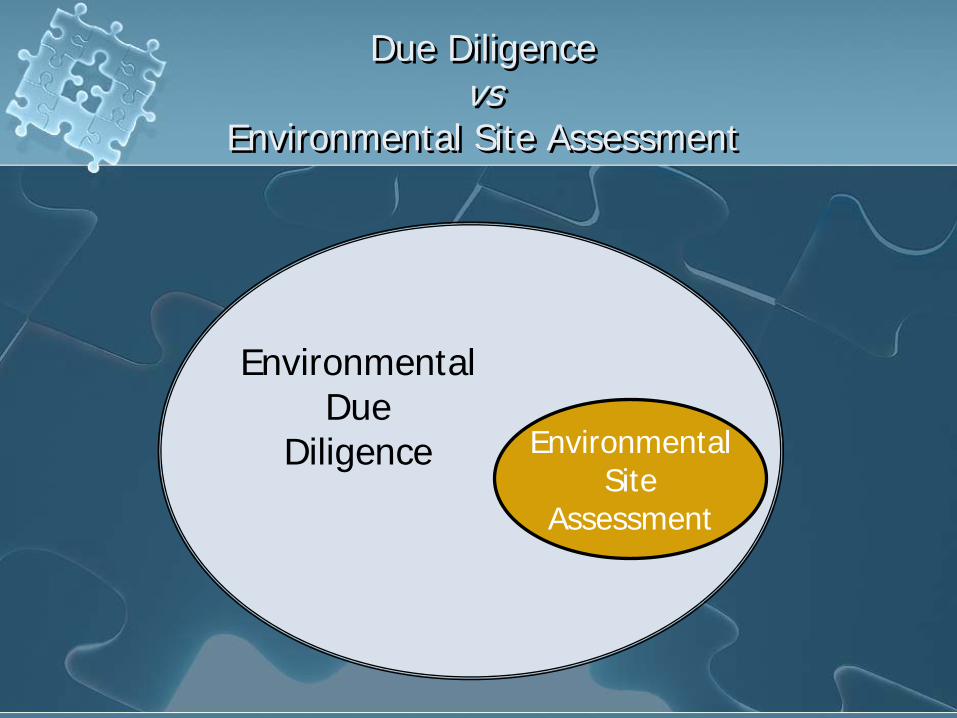

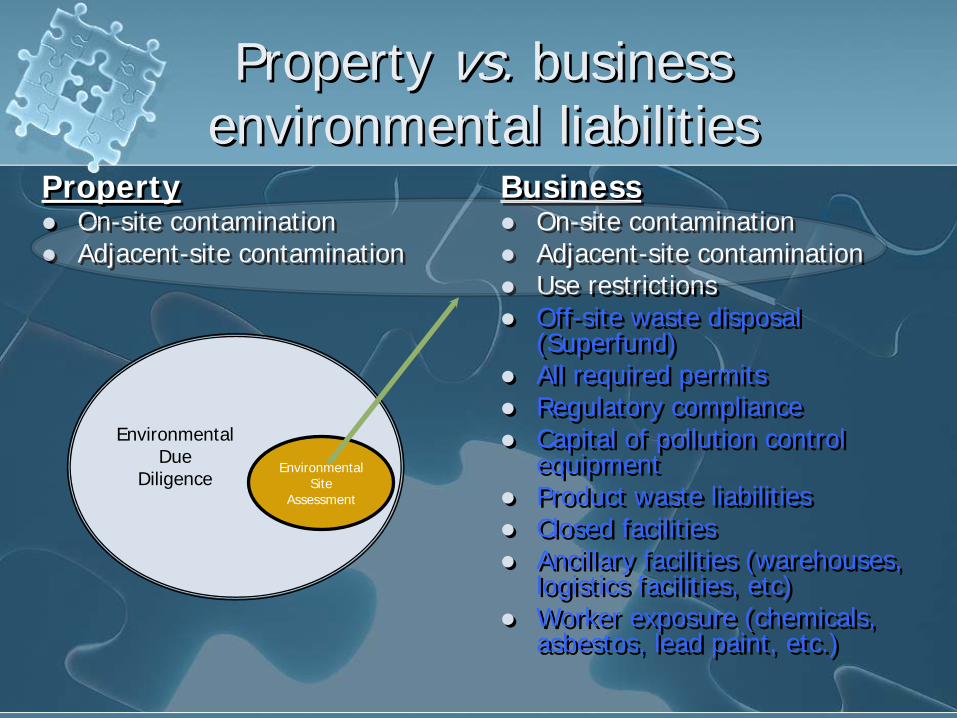

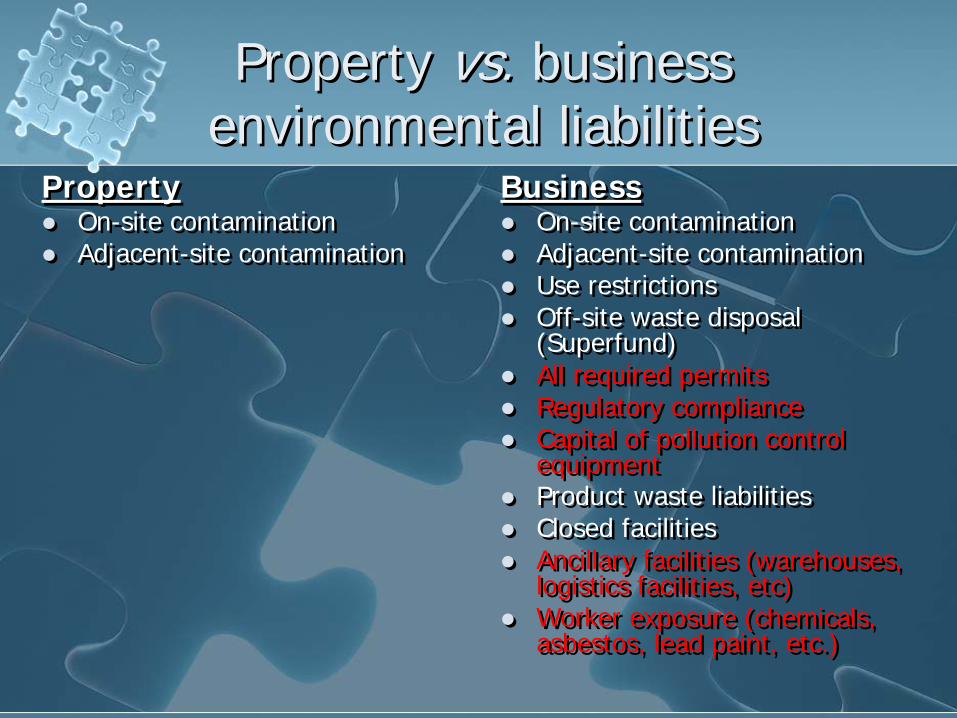

Property vs. business environmental liabilities Property vs. business

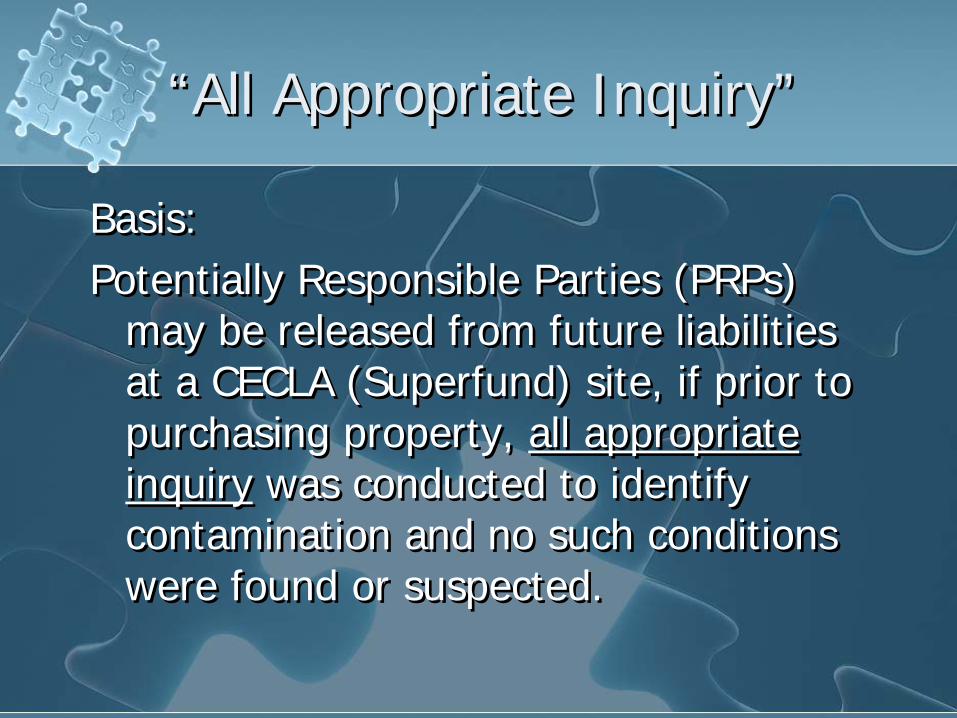

may be released from future liabilities at a CECLA (Superfund) site, if prior to purchasing property, all appropriate inquiry was conducted to identify contamination and no such conditions were found or suspected.

Basis:Potentially Responsible Parties (PRPs)

may be released from future liabilities at a CECLA (Superfund) site, if prior to purchasing property, all appropriate inquiry was conducted to identify contamination and no such conditions were found or suspected.

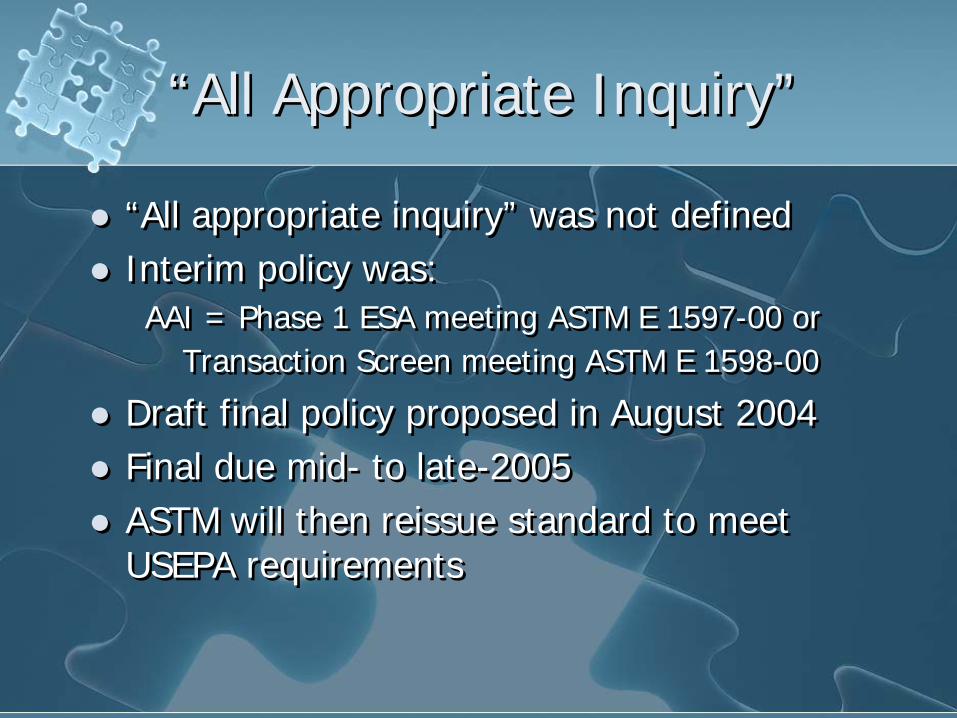

Interim policy was:AAI = Phase 1 ESA meeting ASTM E 1597-00 or

Transaction Screen meeting ASTM E 1598-00

Draft final policy proposed in August 2004

Final due mid- to late-2005

ASTM will then reissue standard to meet USEPA requirements

“All appropriate inquiry” was not defined

Interim policy was:AAI = Phase 1 ESA meeting ASTM E 1597-00 or

Transaction Screen meeting ASTM E 1598-00

Draft final policy proposed in August 2004

Final due mid- to late-2005

ASTM will then reissue standard to meet USEPA requirements

Highlights to USEPA Proposed Requirements

Highlights to USEPA Proposed Requirements

Transaction screens will no longer met requirements for “all appropriate inquiry”

Transaction screens will no longer met requirements for “all appropriate inquiry”

Evolution of ESAsEvolution of ESAs

Very littleUse Of

ESAs

Up toMid-1990s

ASTMPhase 1

ESA-revised-

ASTMTransaction

Screen-revised-

1996 2000 2005

TransactionScreen

ASTMPhase 1

ESA-revised-

Decreaseduse

Increaseduse

& lessadherence to ASTM

ASTMPhase 1

ESA-new-

ASTMTransaction

Screen-new-

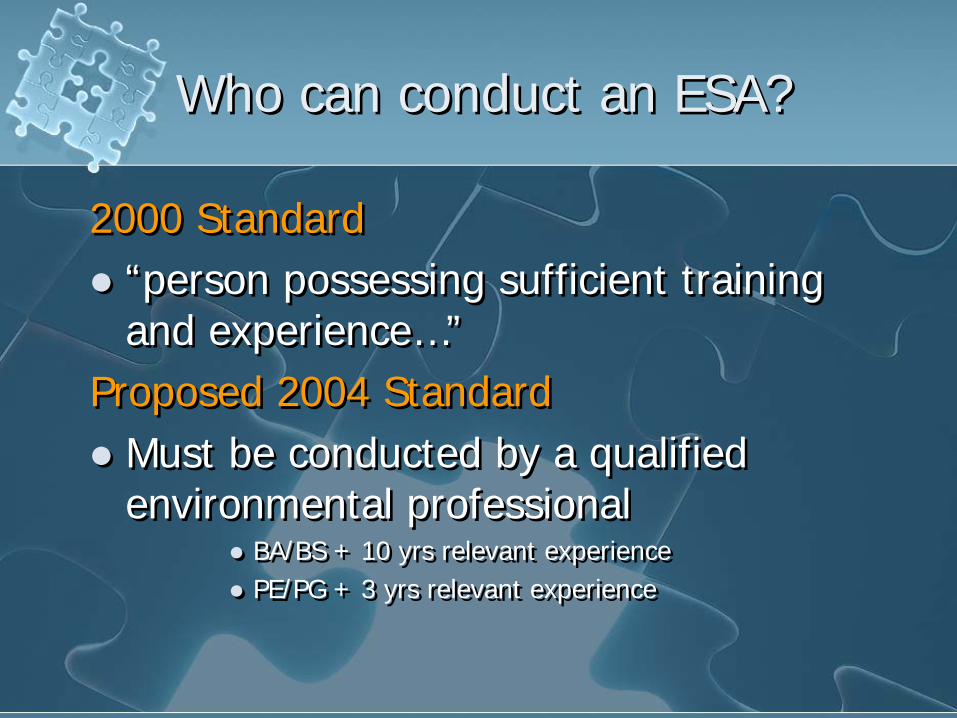

Who can conduct an ESA?Who can conduct an ESA?

2000 Standard

“person possessing sufficient training and experience…”

Proposed 2004 Standard

Must be conducted by a qualified environmental professional

BA/BS + 10 yrs relevant experience

PE/PG + 3 yrs relevant experience

2000 Standard

“person possessing sufficient training and experience…”

Proposed 2004 Standard

Must be conducted by a qualified environmental professional

BA/BS + 10 yrs relevant experience

PE/PG + 3 yrs relevant experience

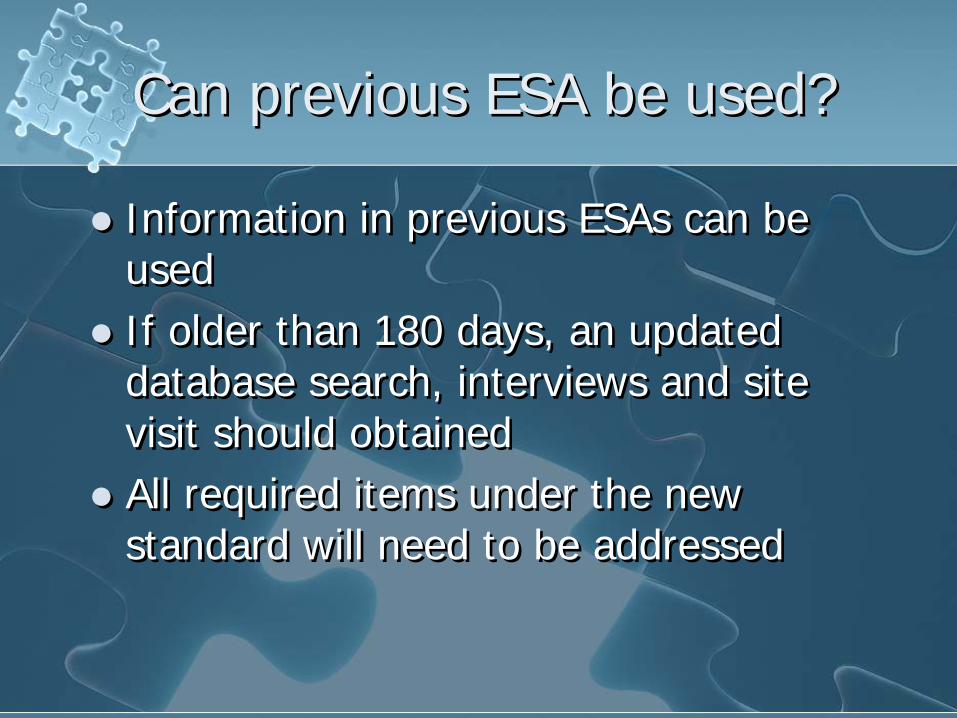

Can previous ESA be used?Can previous ESA be used?

Information in previous ESAs can be used

If older than 180 days, an updated database search, interviews and site visit should obtained

All required items under the new standard will need to be addressed

Information in previous ESAs can be used

If older than 180 days, an updated database search, interviews and site visit should obtained

All required items under the new standard will need to be addressed

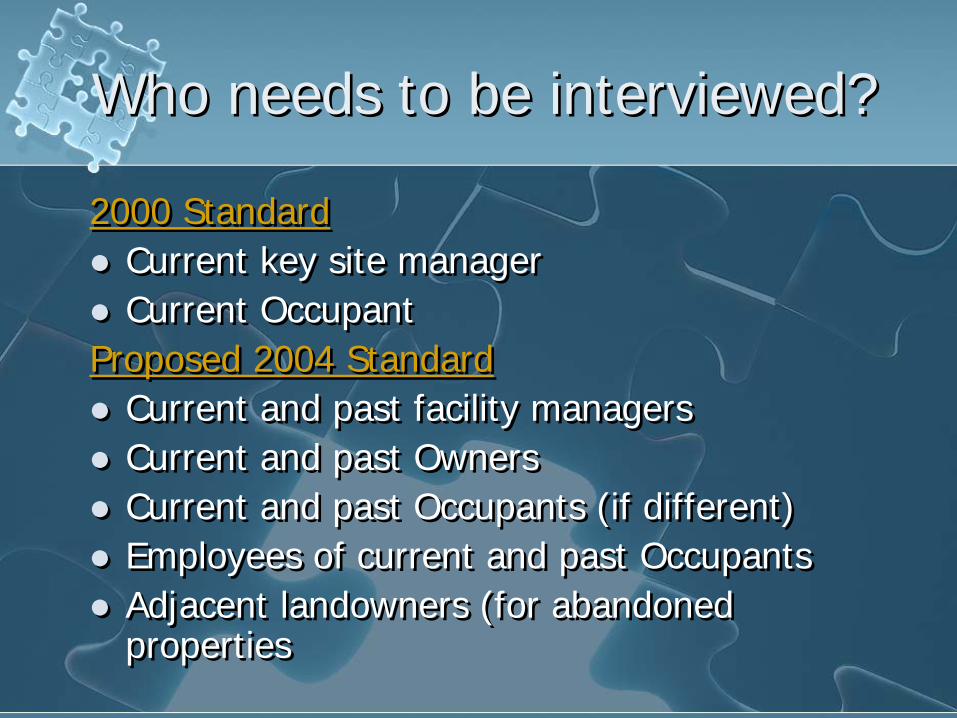

Who needs to be interviewed?Who needs to be interviewed?

2000 Standard

Current key site manager

Current OccupantProposed 2004 Standard

Current and past facility managers

Current and past Owners

Current and past Occupants (if different)

Employees of current and past Occupants

Adjacent landowners (for abandoned properties

2000 Standard

Current key site manager

Current OccupantProposed 2004 Standard

Current and past facility managers

Current and past Owners

Current and past Occupants (if different)

Employees of current and past Occupants

Adjacent landowners (for abandoned properties

Who needs to be interviewed?Who needs to be interviewed?

Issues

Finding past facility managers, occupants and employees

Confidential transactions

Identifying and contacting neighbors

Issues

Finding past facility managers, occupants and employees

Confidential transactions

Identifying and contacting neighbors

What historic records need to be reviewed?

What historic records need to be reviewed?

2000 Standard

USER must search environmental liens or land use limitations

Proposed 2004 Standard

Requires Preparer review of title records to confirm absence of environmental liens and use restrictions

2000 Standard

USER must search environmental liens or land use limitations

Proposed 2004 Standard

Requires Preparer review of title records to confirm absence of environmental liens and use restrictions

Property ValueProperty Value

2000 Standard

Requires USER to evaluate difference between purchase price and price of comparable properties

Proposed 2004 Standard

Preparer must evaluate fair market value if property were not contaminated

2000 Standard

Requires USER to evaluate difference between purchase price and price of comparable properties

Proposed 2004 Standard

Preparer must evaluate fair market value if property were not contaminated

Property ValueProperty Value

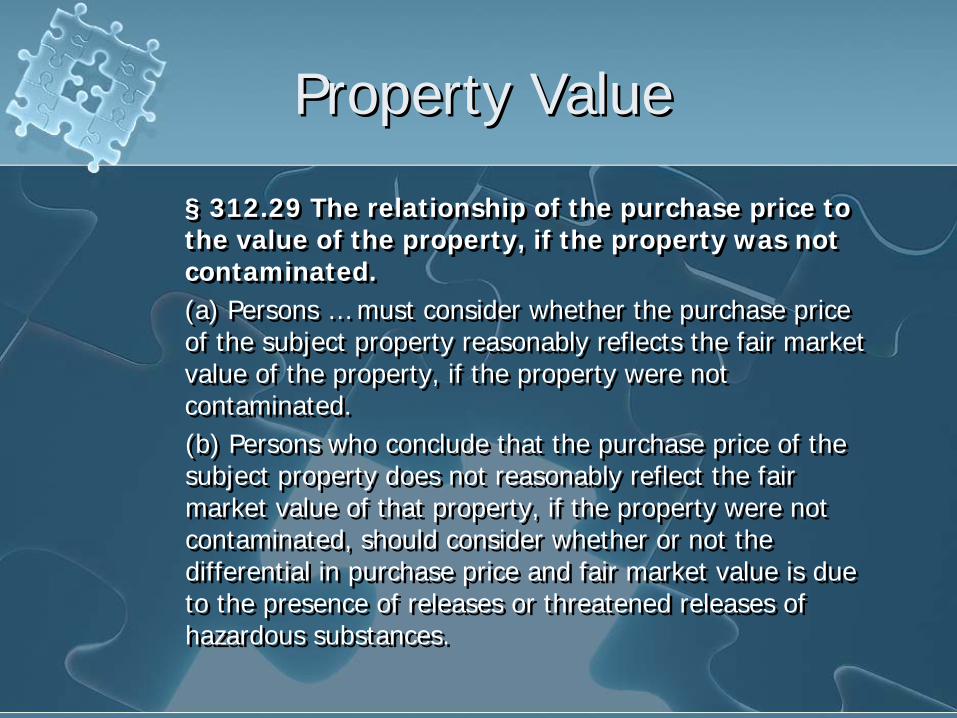

§ 312.29 The relationship of the purchase price to the value of the property, if the property was not contaminated. (a) Persons … must consider whether the purchase price of the subject property reasonably reflects the fair market value of the property, if the property were not contaminated. (b) Persons who conclude that the purchase price of the subject property does not reasonably reflect the fair market value of that property, if the property were not contaminated, should consider whether or not the differential in purchase price and fair market value is due to the presence of releases or threatened releases of hazardous substances.

§ 312.29 The relationship of the purchase price to the value of the property, if the property was not contaminated.(a) Persons … must consider whether the purchase price of the subject property reasonably reflects the fair market value of the property, if the property were not contaminated. (b) Persons who conclude that the purchase price of the subject property does not reasonably reflect the fair market value of that property, if the property were not contaminated, should consider whether or not the differential in purchase price and fair market value is due to the presence of releases or threatened releases of hazardous substances.

Property ValueProperty Value

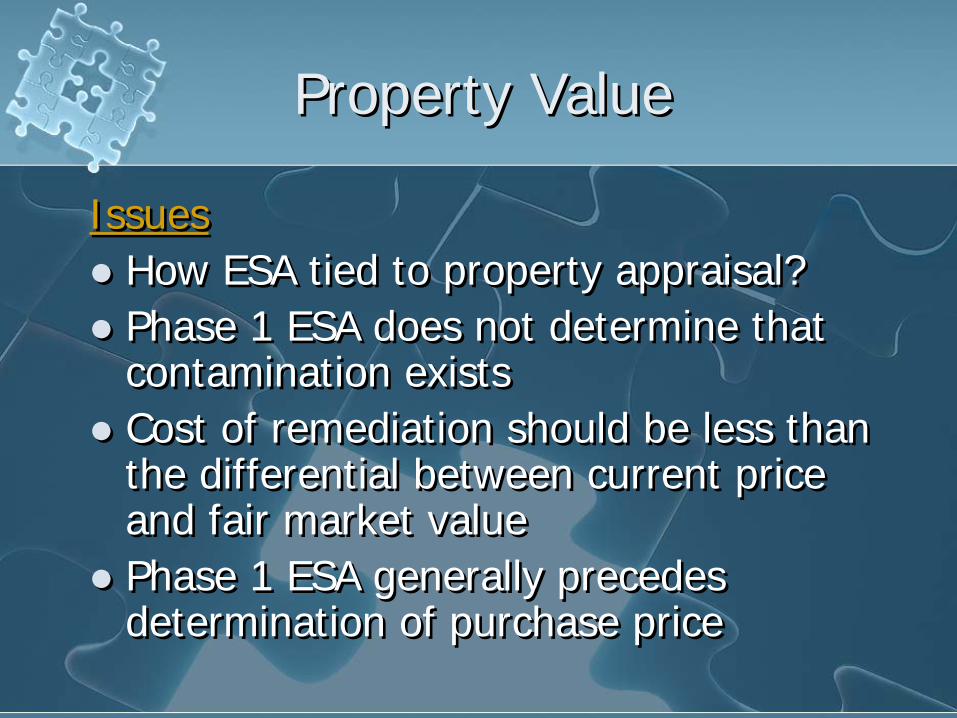

Issues

How ESA tied to property appraisal?

Phase 1 ESA does not determine that contamination exists

Cost of remediation should be less than the differential between current price and fair market value

Phase 1 ESA generally precedes determination of purchase price

Issues

How ESA tied to property appraisal?

Phase 1 ESA does not determine that contamination exists

Cost of remediation should be less than the differential between current price and fair market value

Phase 1 ESA generally precedes determination of purchase price

ESA “Rules of Thumb” for realtors ESA “Rules of Thumb” for realtors