Independent Auditors’ Reports as Required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards and Government Auditing Standards and Related Information ADELPHI UNIVERSITY For the years ended August 31, 2016 and 2015

Transcript

Independent Auditors’ Reports as Required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles,

and Audit Requirements for Federal Awards and Government Auditing Standards and Related Information

ADELPHI UNIVERSITY

For the years ended August 31, 2016 and 2015

C O N T E N T S

Page(s)

Report of Independent Certified Public Accountants 1 - 2

Consolidated Financial Statements:

Consolidated Statements of Financial Position as of August 31, 2016 and 2015 3

Consolidated Statement of Activities for the year ended August 31, 2016 (with summarized comparative

financial information for the year ended August 31, 2015) 4

Consolidated Statement of Activities for the year ended August 31, 2015 5

Consolidated Statements of Cash Flows for the years ended August 31, 2016 and 2015 6

Notes to Consolidated Financial Statements 7 - 26

Schedule of Expenditures of Federal Awards for the year ended August 31, 2016 27

Notes to Schedule of Expenditures of Federal Awards for the year ended August 31, 2016 28

Report of Independent Certified Public Accountants on Internal Control over Financial Reporting and

on Compliance and Other Matters Required by Government Auditing Standards 29 - 30

Report of Independent Certified Public Accountants on Compliance for Each Major Federal

Program and on Internal Control over Compliance Required by the Uniform Guidance 31 - 32

Schedule of Findings and Questioned Costs for the year ended August 31, 2016 33 - 34

Summary Schedule of Prior Year Audit Findings and Corrective Action Plan 35

REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS

To the Board of Trustees of

Adelphi University:

Report on the financial statements

We have audited the accompanying consolidated financial statements of Adelphi University and subsidiary

(collectively, the “University”), which comprise the consolidated statements of financial position as of August 31,

2016 and 2015, and the related consolidated statements of activities and cash flows for the years then ended, and

the related notes to the consolidated financial statements.

Management’s responsibility for the financial statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in

accordance with accounting principles generally accepted in the United States of America; this includes the design,

implementation, and maintenance of internal control relevant to the preparation and fair presentation of

consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We

conducted our audits in accordance with auditing standards generally accepted in the United States of America

and the standards applicable to financial audits contained in Government Auditing Standards issued by the

Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or

error. In making those risk assessments, the auditor considers internal control relevant to the University’s

preparation and fair presentation of the consolidated financial statements in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

University’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by

management, as well as evaluating the overall presentation of the consolidated financial statements.

Grant Thornton LLP 445 Broad Hollow Road, Suite 300 Melville, NY 11747-3601

T 631.249.6001 F 631.249.6144 GrantThornton.com linkd.in/GrantThorntonUS twitter.com/GrantThorntonUS

Grant Thornton LLP U.S. member firm of Grant Thornton International Ltd

2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit

opinion.

Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the

financial position of Adelphi University and subsidiary as of August 31, 2016 and 2015, and the changes in their

net assets and their cash flows for the years then ended in accordance with accounting principles generally accepted

in the United States of America.

Other matters

Supplementary information Our audits were conducted for the purpose of forming an opinion on the consolidated financial statements as a

whole. The schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations

(CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal

Awards, is presented for purposes of additional analysis and is not a required part of the consolidated financial

statements. Such supplementary information is the responsibility of management and was derived from and relates

directly to the underlying accounting and other records used to prepare the consolidated financial statements. The

information has been subjected to the auditing procedures applied in the audits of the consolidated financial

statements and certain additional procedures. These additional procedures included comparing and reconciling

the information directly to the underlying accounting and other records used to prepare the consolidated financial

statements or to the consolidated financial statements themselves, and other additional procedures in accordance

with auditing standards generally accepted in the United States of America. In our opinion, the supplementary

information is fairly stated, in all material respects, in relation to the consolidated financial statements as a whole.

Other reporting required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report, dated November 28, 2016,

on our consideration of the University’s internal control over financial reporting and on our tests of its compliance

with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of

that report is to describe the scope of our testing of internal control over financial reporting and compliance and

the results of that testing, and not to provide an opinion on the effectiveness of internal control over financial

reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the University’s internal control over financial reporting and compliance.

Melville, New York

November 28, 2016

ADELPHI UNIVERSITY

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

AS OF AUGUST 31, 2016 AND 2015

The accompanying notes are an integral part of these consolidated financial statements

3

NOTES 2016 2015

ASSETS

Cash and Short-Term Investments, at fair value 2 27,645,286$ 22,885,222$

Accounts Receivable, net 3 1,781,985 2,052,545

Grants Receivable 1 336,359 625,145

Prepaid Expenses and Other Assets 7,913,581 8,035,180

Contributions Receivable, net 1, 4 5,857,663 6,203,627

Student Loans Receivable, net 5 6,721,412 6,525,165

Investments, at fair value 1, 6 164,847,667 178,458,191

Amounts Held in Trust 1, 8 2,048,743 1,644,820

Land, Buildings, and Equipment, net 1, 9 256,128,755 241,043,264

TOTAL ASSETS 473,281,451$ 467,473,159$

LIABILITIES AND NET ASSETS

LIABILITIES

Accounts Payable and Accrued Expenses 1,10 24,061,223$ 21,912,594$

Deferred Revenues 1 33,327,691 29,848,014

U.S. Government Grants Refundable 5 5,802,724 5,647,384

Long-Term Debt 11 123,553,249 126,127,554

Total Liabilities 186,744,887 183,535,546

COMMITMENTS AND CONTINGENCIES 15

NET ASSETS

Unrestricted Net Assets: 1, 7

Operations and Designated 201,767 78,458

Long-Term Investment 124,318,868 124,721,011

Plant 110,483,470 110,002,330

Total Unrestricted Net Assets 235,004,105 234,801,799

Temporarily Restricted Net Assets 1, 7 20,318,668 18,552,520

Permanently Restricted Net Assets 1, 7 31,213,791 30,583,294

Total Net Assets 286,536,564 283,937,613

TOTAL LIABILITIES AND NET ASSETS 473,281,451$ 467,473,159$

ADELPHI UNIVERSITY

CONSOLIDATED STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED AUGUST 31, 2016 (WITH SUMMARIZED COMPARATIVE FINANCIAL INFORMATION FOR THE YEAR ENDED AUGUST 31, 2015)

The accompanying notes are an integral part of this consolidated financial statement

CHANGE IN NET ASSETS, before transfers and amounts designated 10,630,746 (52,510) 10,578,236 1,322,761 (11,798,140) 102,857 1,766,148 630,497 2,499,502 (8,809,644)

TRANSFERS

Mandatory Transfer for Debt Service (7,724,994) - (7,724,994) - 7,724,994 - - - - -

Matching and Other Contributions (25,096) - (25,096) 25,096 - - - - - -

CHANGE IN NET ASSETS, before transfers and amounts designated 12,685,399 (68,740) 12,616,659 (9,016,707) (11,967,093) (8,367,141) (3,202,946) 2,760,443 (8,809,644)

TRANSFERS

Mandatory Transfer for Debt Service (7,492,083) - (7,492,083) - 7,492,083 - - - -

Matching and Other Contributions (29,967) - (29,967) 29,967 - - - - -

CHANGE IN NET ASSETS, before amounts designated 68,894 (68,740) 154 (8,986,740) 619,445 (8,367,141) (3,202,946) 2,760,443 (8,809,644)

AMOUNTS DESIGNATED

Faculty Research (68,894) 68,894 - - - - - - -

CHANGE IN NET ASSETS, before postretirement changes - 154 154 (8,986,740) 619,445 (8,367,141) (3,202,946) 2,760,443 (8,809,644)

Postretirement Changes Other than Net Periodic Benefit Costs 10 - - - - - - - - -

CHANGE IN NET ASSETS - 154 154 (8,986,740) 619,445 (8,367,141) (3,202,946) 2,760,443 (8,809,644)

NET ASSETS, BEGINNING OF YEAR - 78,304 78,304 133,707,751 109,382,885 243,168,940 21,755,466 27,822,851 292,747,257

NET ASSETS, END OF YEAR -$ 78,458$ 78,458$ 124,721,011$ 110,002,330$ 234,801,799$ 18,552,520$ 30,583,294$ 283,937,613$

UNRESTRICTED

ADELPHI UNIVERSITY

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED AUGUST 31, 2016 AND 2015

The accompanying notes are an integral part of these consolidated financial statements

6

2016 2015

Cash Flows from Operating Activities:

Change in Net Assets 2,598,951$ (8,809,644)$

Adjustments to Reconcile Change in Net Assets to Net Cash Flows

Provided by Operating Activities:

Nonoperating Items:

Realized Gain on Investments (5,550,562) (8,808,817)

Contributions and Investment Income Restricted for Long-Term Investment (1,946,942) (2,316,717)

Noncash Items:

Depreciation, Accretion, and Amortization 7,418,473 7,499,002

Amortization of Bond Premium (192,188) (181,956)

Net Unrealized (Gain) Loss on Investments (3,635,168) 17,003,989

Loss on Disposals of Equipment 26,581 12,738

Cancellations of Notes Receivable 143,436 207,176

Increase (Decrease) in Allowance for Doubtful Accounts 24,631 (52,201)

Change In Operating Assets and Liabilities:

Decrease (Increase) in Accounts Receivable 245,929 (152,544)

Decrease (Increase) in Grants Receivable 288,786 (121,382)

Decrease (Increase) in Prepaid Expenses and Other Assets 121,599 (1,987,017)

Decrease (Increase) in Contributions Receivable 400,972 (698,877)

Increase in Amounts Held in Trust (403,923) (131,111)

Increase in Accounts Payable and Accrued Expenses 2,014,769 2,047,611

Increase in Deferred Revenues 3,479,677 761,321

Increase (Decrease) in U.S. Government Grants Refundable 155,340 (18,778)

Net Cash Flows Provided by Operating Activities 5,190,361 4,252,793

Cash Flows from Investing Activities:

Proceeds from Sale of Investments 46,756,574 54,949,381

Purchase of Investments (24,015,328) (32,804,789)

Student Notes Receivable:

New Loans Made (1,219,539) (1,152,335)

Principal Collected 879,856 864,091

Expenditures for Plant Facilities (22,298,802) (39,688,409)

Net Cash Flows Provided by (Used in) Investing Activities 102,761 (17,832,061)

Cash Flows from Financing Activities

From Borrowings:

Proceeds from Issuance of Bonds, Net of Bond Issuance Costs - 35,794,812

Use of Proceeds of Bonds and Return on Proceeds of Bonds - 23,843,492

Retirement of Debt (2,480,000) (36,101,599)

Proceeds from Contributions and Investment Earnings Restricted for:

Investment in Endowment 1,684,177 1,711,363

Plant Improvements 261,218 603,907

Student Loan Funds 1,547 1,447

Net Cash Flows (Used in) Provided by Financing Activities (533,058) 25,853,422

Net Increase in Cash and Short-Term Investments 4,760,064 12,274,154

Cash and Short-Term Investments:

Beginning of Year 22,885,222 10,611,068

End of Year 27,645,286$ 22,885,222$

Supplemental Disclosures:

Interest Paid 5,602,402$ 4,897,087$

Assets Acquired through Capital Lease 40,465$ - $

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

7

1. Summary of Significant Accounting Policies

a. Nature of Operations

Adelphi University (the “University”) is an independent not-for-profit institution of higher education with

programs at the undergraduate and graduate levels. The University’s main campus is located in Garden City,

New York. The University is tax exempt under Section 501(c)(3) of the Internal Revenue Code.

Black Cat Advertising, a wholly-owned subsidiary of the University, began operations in 2004 and is

consolidated in the accompanying financial statements. All intercompany transactions have been eliminated

in consolidation.

b. Basis of Presentation

The consolidated financial statements of the University have been prepared in accordance with accounting

principles generally accepted in the United States of America (“US GAAP”) using the accrual basis of

accounting.

The University maintains its accounts in accordance with the principles and practices of “fund accounting”.

Fund accounting is the procedure by which resources are classified for accounting purposes in accordance

with activities or objectives specified by donors, in accordance with regulations, restrictions, or limitations

imposed by sources outside the institution, or in accordance with directions by the Board of Trustees

(the “Board”).

The University follows the provisions of ASC 958, “Not-For-Profit Entities.” ASC 958 specifies that

financial statements provided by not-for-profit organizations include statements of financial position,

activities, and cash flows and that net assets be classified as unrestricted, temporarily restricted or

permanently restricted based on the existence or absence of donor-imposed restrictions. A description of the

three net asset classifications is as follows:

Unrestricted net assets include the following:

Operations: Operations include the revenues and expenses associated with the principal educational mission

of the University.

Amounts Designated: The amounts designated to support (i) certain research activities (ii) related changes

in personnel and (iii) strategic planning initiatives.

Long-Term Investment: Long-term investment includes Board designations to funds functioning as

endowment, cumulative realized and unrealized gains on board-designated endowment funds, and the

University’s required matching contribution on government student loan funds.

Plant: Plant net assets include: (i) transfers from operations designated by the University to fund future

capital projects and debt service payments; (ii) amounts held in trust for payment of outstanding long-term

debt; (iii) the deficit of construction expenditures in excess of fundraising; and (iv) amounts invested in land,

buildings and equipment net of accumulated depreciation. Contributions restricted for the acquisition of land,

buildings and equipment are reported as temporarily restricted revenues. These contributions are reclassified

to unrestricted net assets upon acquisition of the assets. In the accompanying consolidated statements of

activities, expenses represent primarily interest on debt service and depreciation.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

8

Temporarily restricted net assets generally result from contributions whose use by the University is limited

by donor-imposed stipulations that can be fulfilled by actions of the University pursuant to those stipulations

and/or that expire by the passage of time. When donor restrictions expire, that is, when a restriction is fulfilled

or a time restriction ends, temporarily restricted net assets are reclassified to unrestricted net assets and

reported in the accompanying consolidated statements of activities as net assets released from restrictions.

When a temporarily restricted contribution is received and the restriction is fulfilled in the same period, the

corresponding revenue is recorded as unrestricted in the accompanying consolidated statements of activities.

Permanently restricted net assets generally represent the historical cost of contributions whose use is

limited by donor-imposed stipulations requiring that the original principal be maintained permanently by the

University. Generally, the donors of these assets permit the University to use all or part of the investment

return on these assets for specific purposes or general university operations. Such assets primarily include

the University’s permanent endowment funds.

c. Deferred Revenues

The University derives its revenue primarily from student tuition and fees. Revenue is recorded on the accrual

basis of accounting. Deferred revenues primarily represent payments received from students relating to

registrations for the following fall semester. Such amounts are recognized as revenue during the subsequent

fiscal year.

On February 4, 2013, the University entered into a transaction, whereby the University provided a 360 month

assignment of its interest in and rent revenue associated with five operating leases between the University

and certain cell phone providers. The University, in providing the 360 month assignment, received

$3,000,000, which has been recorded as deferred revenue within the consolidated statements of financial

position and will be amortized into revenue over the life of the assignment. The total amount of revenue with

a related interest expense component recognized for the years ended August 31, 2016 and 2015 totaled

$165,186 and $204,910, respectively, and has been recorded in the caption other sources within the

accompanying consolidated statements of activities.

d. Land, Buildings and Equipment, Net

Land, buildings and equipment, net, are based on the following valuations:

Land and improvements - at appraised value in 1958, plus subsequent improvements at cost.

Buildings - at approximate fair value in accordance with a survey by the Home Insurance Company made

in February 1967, plus a six percent estimate for excavations, foundations and underground facilities;

additions subsequent to February 1967 are recorded at cost.

Equipment and Library Books - recorded at cost.

Donated assets are stated at fair value as of the date of the gift.

The University follows the guidance of ASC 360, “Accounting for the Impairment or Disposal of Long-lived

Assets.” The University reviews long-lived assets for possible impairment whenever events or changes in

circumstances indicate that the carrying amount of an asset may not be recoverable. Some factors the

University considers important, which could trigger an impairment review, include: (i) significant

underperformance compared to expected historical or projected future operating results; (ii) significant

changes in the University’s use of the acquired assets or the strategy for its overall business; and

(iii) significant negative industry or economic trends.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

9

Depreciation on land, buildings and equipment has been computed on the straight-line basis over the

estimated useful lives of the assets as follows:

Buildings and additions 75 years

Building improvements and renovations 15 years

Furniture and equipment 5-10 years

Software 5 years

Library books 20 years

Depreciation, accretion and amortization expense on assets for the years ended August 31, 2016 and 2015

amounted to $7,418,473 and $7,499,002, respectively. Upon retirement or disposal, the asset cost and related

accumulated depreciation and amortization are eliminated from the respective accounts and the resulting gain

or loss, if any, is included in the accompanying consolidated statements of activities. During the years ended

August 31, 2016 and 2015, the University disposed of fully depreciated assets totaling approximately

$500,000 and $4,500,000, respectively.

e. Amounts Held in Trust

Amounts held in trust are recorded at fair value. Amounts held for agency funds totaled $677,146 and

$480,755 at August 31, 2016 and 2015, respectively. The corresponding liability for the amounts held for

agency funds are included in accounts payable and accrued expenses within the accompanying consolidated

statements of financial position.

The University provides a 457(b) deferred compensation plan (the “Plan”) primarily for a select group of

management and highly compensated employees. The University is the custodian of the Plan and records

both an asset and a corresponding liability for the amounts included within the Plan. As of August 31, 2016

and 2015, amounts recorded for this plan totaled $1,371,597 and $1,164,065, respectively. The

corresponding liability for the amounts included within the Plan are included in accounts payable and accrued

expenses within the accompanying consolidated statements of financial position.

f. Investments

Investments consist primarily of equities, publicly traded fixed income funds and alternative investments.

Purchases and sales of securities are reflected on a trade-date basis. Gains and losses on sales of securities

are based on average cost and are recorded in the consolidated statements of activities in the period in which

the securities are sold. Dividends are accrued based on the ex-dividend date. Interest is recognized as earned.

All investment securities are exposed to various risks such as interest rate, market, and credit risks. Due to

the level of risk associated with certain investment securities, it is at least reasonably possible that changes

in the values of investment securities will occur in the near term and such changes could materially affect the

amounts reported in the consolidated statements of financial position.

g. Fair Value Measurements

The fair values of all financial instruments, other than contributions receivable, investments, long-term debt

and loans receivable from students under government loan programs, approximate carrying values because

of the short maturity of these instruments.

A reasonable estimate of the fair value of loans receivable from students under government loan programs

cannot be made because the notes are not saleable and can only be assigned to the U.S. Government or its

designees.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

10

The fair value of long-term debt approximates the carrying value since the interest rates charged, as disclosed

in Note 11, approximate the University’s current borrowing rate for similar instruments. For all other

financial instruments, the carrying amounts as disclosed in the accompanying consolidated financial

statements approximate fair value.

The University follows Fair Value Measurements guidance which establishes a framework for measuring

fair value, expands disclosures about fair value measurements and provides a consistent definition of fair

value, which focuses on an exit price between market participants in an orderly transaction. The guidance

also prioritizes, within the measurement of fair value, the use of market-based information over entity-specific

information and establishes a three-level hierarchy for fair value measurements based on the transparency of

information used in the valuation of an asset or liability as of the measurement date. Assets and liabilities

measured and reported at fair value are classified and disclosed in one of the following categories:

Level 1 - Quoted prices are available in active markets for identical assets or liabilities as of the reporting

date. The type of investments in Level 1 include listed equities held in the name of the University, and

exclude listed equities and other securities held indirectly through commingled funds.

Level 2 - Pricing inputs, including broker quotes, are generally those other than exchange quoted prices in

active markets. Level 2 assets and liabilities include debt securities with quoted market prices that are traded

less frequently than exchange-traded instruments. This category generally includes certain U.S. government

and agency mortgage-backed securities, and corporate-debt securities.

Level 3 - Pricing inputs are unobservable for the asset or liability and include situations where there is little,

if any, market activity for the asset or liability. The inputs into the determination of fair value require

significant management judgment or estimation. Investments that are included in this category generally

include privately held investments and partnership interests.

h. New Accounting Pronouncements

In 2015, the Financial Accounting Standards Board (“FASB”) issued guidance amending the requirement to

categorize within the fair value hierarchy all investments for which fair value is measured using the net asset

value per share as a practical expedient. The amendments within this update must be applied retrospectively

to all periods presented. As such, the University has adopted this guidance for the years ended August 31,

2016 and 2015. This new guidance only amended disclosure requirements and did not have any impact on

the University’s consolidated statements of financial position or consolidated statements of activities for the

years presented (Note 6).

Also in 2015, the FASB issued guidance to simplify the presentation of debt issuance costs by requiring debt

issuance costs related to a recognized debt liability to be presented as a direct deduction from the carrying

amount of that debt liability. The amendments within this update must be applied retrospectively to all

periods presented. As such, the University has adopted this guidance for the years ended August 31, 2016

and 2015 (Note 11).

i. Concentration of Credit Risk

Cash and investments are exposed to various risks, such as interest rate, market and credit risks. To minimize

such risks, the University maintains its cash in various bank deposit accounts which, at times, may exceed

federally insured limits, and in a diversified investment portfolio. At August 31, 2016 and 2015, the

University’s cash and investments were placed with high credit quality financial institutions and, accordingly,

the University does not expect nonperformance.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

11

j. Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make estimates

and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets

and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during

the reporting period. Significant estimates include the allowance for accounts receivable, valuation of

alternative investments, actuarial assumptions related to the postretirement plan, useful lives of plant assets

and certain accrued liabilities. Actual results could differ from those estimates.

k. Contributions and Government Grants and Contracts

Contributions, including unconditional promises to give, are reported as revenue in the period received.

Contributions are recorded at fair value, net of estimated uncollectible amounts. Conditional contributions

are recognized as revenue when the conditions on which they depend have been substantially met.

Fundraising costs of $2,286,015 and $2,375,076 have been included in institutional support expenses in the

accompanying consolidated statements of activities for the years ended August 31, 2016 and 2015,

respectively.

Revenues from government grants and contracts for specific programs are recognized in the period when

expenditures have been incurred in compliance with the respective contract. Amounts received in advance

are recorded as deferred revenue. Contracts awarded for the acquisition of long-lived assets are reported as

unrestricted revenue during the fiscal year in which the assets are acquired. Governmental grants and

contracts are subject to audit and potential disallowance. It is management’s opinion that any potential

disallowances will not have a material effect on the accompanying consolidated financial statements.

l. Tuition Discounting

The University maintains a policy of offering qualified applicants admission to the University without regard

to financial circumstances. The University provides institutional financial aid to those admitted on the basis

of merit or need in the form of direct grants or employment during the academic year. Tuition and fees have

been reduced by institutional directed grants in the amount of $54,681,053 and $52,493,809 for the years

ended August 31, 2016 and 2015, respectively.

m. Temporarily Restricted and Permanently Restricted Net Assets

Temporarily restricted net assets, at August 31, 2016 and 2015, were available for the following purposes:

2016 2015

Education 6,297,615$ 4,833,096$

Endowment Cumulative Gain on Donor Restricted Net Assets 9,668,742 9,414,166

Annuity Trust Agreements 2,386,692 2,315,059

Building Renovations 1,965,619 1,990,199

20,318,668$ 18,552,520$

Permanently restricted net assets, at August 31, 2016 and 2015, consisted of the following:

Endowment - Corpus 31,106,300$ 30,477,349$

Loan Fund 107,491 105,945

31,213,791$ 30,583,294$

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

12

n. Conditional Asset Retirement Obligations

The University recognizes the cost associated with the eventual remediation and abatement of asbestos

located within its facilities. The cost of the abatement was estimated using historical construction and

renovation documents.

The University recognized accretion expense relating to these obligations of $93,395 and $89,709 for the

years ended August 31, 2016 and 2015, respectively. These obligations were reduced by remediation costs

of $82,158 and $75,861 for the years ended August 31, 2016 and 2015, respectively. The obligation

amounted to $1,595,811 and $1,531,061 at August 31, 2016 and 2015, respectively, and is included within

accounts payable and accrued expenses in the accompanying consolidated statements of financial position.

o. Income Taxes

The University follows ASC 740-10 which clarifies the accounting for uncertainty in tax positions taken or

expected to be taken in a tax return, including issues relating to financial statement recognition and

measurement. This section provides that the tax effects from an uncertain tax position can be recognized in

the financial statements only if the position is “more-likely-than-not” to be sustained if the position were to

be challenged by a taxing authority. The assessment of the tax position is based solely on the technical merits

of the position, without regard to the likelihood that the tax position may be challenged.

The University is exempt from federal income taxation by virtue of being an organization described in Section

501(c)(3) of the Internal Revenue Code. Nevertheless, the University may be subject to tax on income

unrelated to its exempt purpose, unless that income is otherwise excluded by the Code. The tax years ended

August 31, 2013, 2014, 2015 and 2016 are still open to audit for both federal and state purposes. Management

has determined that there are no material uncertain tax positions within its consolidated financial statements.

p. Reclassification

Certain information in the fiscal 2015 consolidated financial statements has been reclassified to conform to the

fiscal 2016 presentation.

2. Cash and Short-Term Investments

Cash and short-term investments include cash and cash equivalents with an original maturity of three months or

less at the time of purchase, and other short-term investments maturing within a year of the consolidated statement

of financial position date. As of August 31, 2016 and 2015, cash and short-term investments consisted of the

following:

2016 2015

Cash and Cash Equivalents 27,089,700$ 19,677,526$

Certificates of Deposit (Short-Term Investments) 555,586 3,207,696

27,645,286$ 22,885,222$

Investment income on cash and short-term investments, included in unrestricted net assets, amounted to $224,193

and $114,061 for the years ended August 31, 2016 and 2015, respectively.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

13

3. Accounts Receivable, net

Accounts receivable primarily consist of amounts due from students and are recorded net of an allowance for

doubtful accounts of $825,000 and $800,000 at August 31, 2016 and 2015, respectively. The carrying value of

receivables has been reduced by an appropriate allowance for uncollectible accounts, based on historical collection

experience, and therefore, approximates net realizable value. Receivables are written off in the period in which

they are deemed to be uncollectible. Accounts receivable are expected to be collected within one year.

4. Contributions Receivable, net

Contributions receivable consisted of the following:

2016 2015

Amounts expected to be collected:

Within 1 year 1,017,205$ 1,169,801$

1 to 5 years 2,491,507 2,545,258

Thereafter 75,000 336,000

3,583,712 4,051,059

Less: allowance for doubtful pledges (18,225) (18,225)

Less: discount to present value (rates ranging from 0.4% - 4.7%) (109,601) (170,893)

3,455,886 3,861,941

Bequests 150,000 175,000

Charitable Remainder Trusts 2,251,777 2,166,686

5,857,663$ 6,203,627$

The University is a beneficiary of irrevocable charitable remainder trusts held by others. At the dates these

charitable remainder trusts are either established or the University becomes aware of their existence, contribution

revenue and receivables are recognized at the present value of the estimated future benefits to be received when

the trust assets are distributed, at discount rates ranging from approximately 1.2% to 6.2%. The receivable is

adjusted during the term of the trusts for changes in the value of assets, accretion of the discount, and other changes

in the estimates of future benefits. The income (loss) on the investments within charitable remainder trusts for the

years ended August 31, 2016 and 2015 amounted to $55,008 and ($107,125), respectively, and is included in

investment income (loss) in the accompanying consolidated statements of activities. The University’s interest in

the charitable remainder trusts is considered to be Level 3 under the fair value hierarchy.

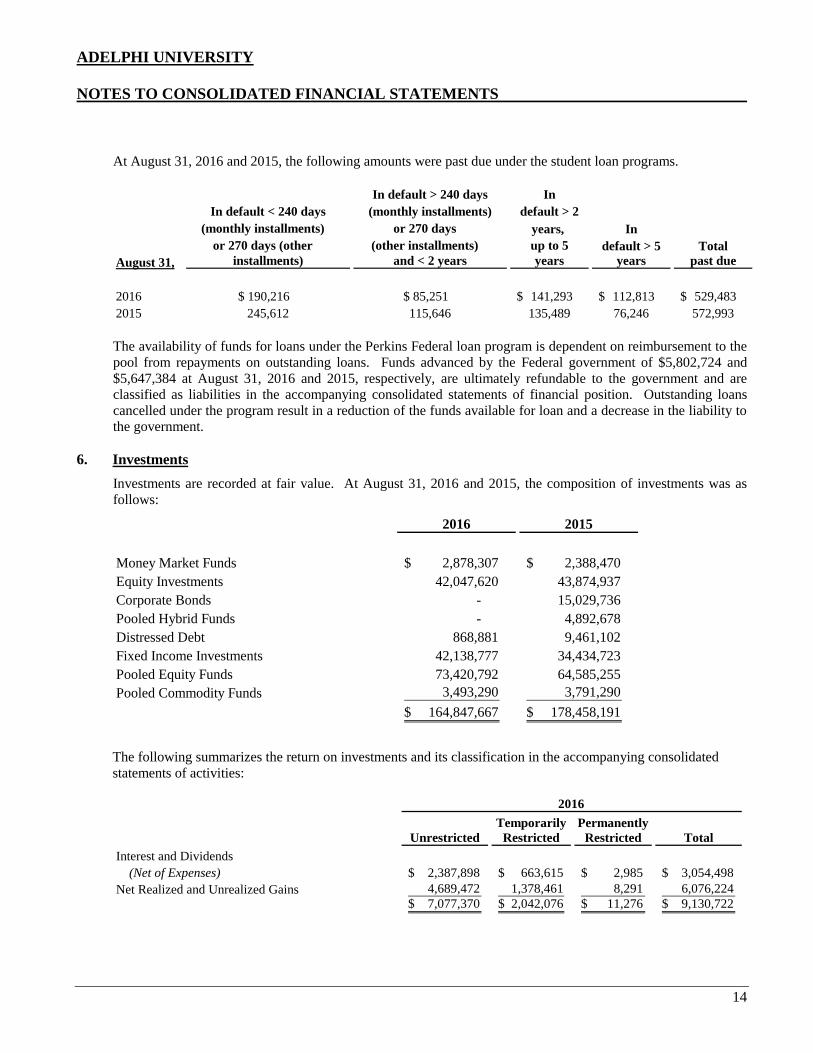

5. Student Loans Receivable, net and U.S. Government Grants Refundable

The University makes uncollateralized loans to students based on financial need under the Perkins Federal loan

program, Nursing Student Loan program and the Nurse Faculty Student Loan program. Student loans are funded

through Federal government loan programs or institutional resources. At August 31, 2016 and 2015, student loans

represented approximately 1.5% and 1.4% of total assets, respectively. At August 31, 2016 and 2015, gross student

loans receivable for Federal government programs totaled $6,893,212 and $6,695,865, respectively. Of these

amounts, as of August 31, 2016 and 2015, $4,295,035 and $4,617,351, respectively, were not in repayment status.

Amounts due under the Federal loan programs are guaranteed by the government and therefore, no reserves are

placed on any past due balances under the program. The University does have an allowance for doubtful accounts of approximately $173,000 relating to the institutional share of these loan programs for each of the years ended

August 31, 2016 and 2015.

ADELPHI UNIVERSITY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

14

At August 31, 2016 and 2015, the following amounts were past due under the student loan programs.

In default > 240 days In

In default < 240 days (monthly installments) default > 2

(monthly installments) or 270 days years, In

or 270 days (other (other installments) up to 5 default > 5 Total

August 31, installments) and < 2 years years years past due

a. Noncancelable Lease Agreements and Other Contracts

The University is obligated under noncancelable operating lease agreements for the rental of off-campus

facilities, some of which contain escalation clauses; equipment rentals; and other contracts. Minimum annual

commitments under the operating leases and other contracts are as follows at August 31, 2016:

Total

2017 $ 3,936,668

2018 4,472,636

2019 4,327,584

2020 4,091,178

2021 3,520,225

Thereafter 9,175,928

$ 29,524,219

Year Ending

August 31,

Rental expense for operating leases amounted to $3,703,979 and $3,086,992 for the years ended August 31,

2016 and 2015, respectively.

b. Litigation

The University is presently a defendant in several lawsuits arising from the normal conduct of its affairs.

Management of the University is of the opinion that settlements, if any, of the aforementioned litigation not

covered by insurance will not have a material adverse impact on the accompanying consolidated financial

statements of the University.

16. Subsequent Events

The University evaluated its August 31, 2016 consolidated financial statements for subsequent events through

November 28, 2016, the date the consolidated financial statements were issued. The University is not aware of

any subsequent events which would require recognition or disclosure in the consolidated financial statements.

27

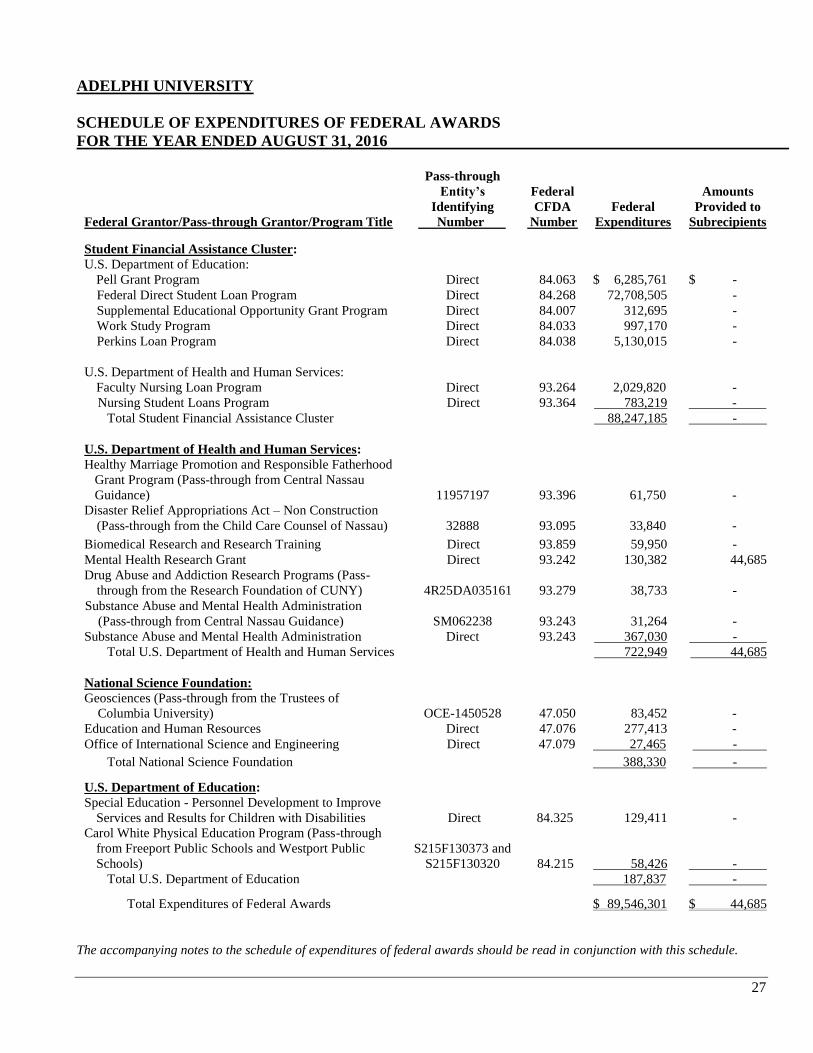

ADELPHI UNIVERSITY

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

FOR THE YEAR ENDED AUGUST 31, 2016

Pass-through

Federal Grantor/Pass-through Grantor/Program Title

Entity’s

Identifying

Number

Federal

CFDA

Number

Federal

Expenditures

Amounts

Provided to

Subrecipients

Student Financial Assistance Cluster:

U.S. Department of Education:

Pell Grant Program Direct 84.063 $ 6,285,761 $ -

Federal Direct Student Loan Program Direct 84.268 72,708,505 -

Supplemental Educational Opportunity Grant Program Direct 84.007 312,695 -

Work Study Program Direct 84.033 997,170 -

Perkins Loan Program Direct 84.038 5,130,015 -

U.S. Department of Health and Human Services:

Faculty Nursing Loan Program Direct 93.264 2,029,820 -

Nursing Student Loans Program Direct 93.364 783,219 -

Total Student Financial Assistance Cluster 88,247,185 -

U.S. Department of Health and Human Services:

Healthy Marriage Promotion and Responsible Fatherhood

Grant Program (Pass-through from Central Nassau

Guidance)

11957197

93.396

61,750

-

Disaster Relief Appropriations Act – Non Construction

(Pass-through from the Child Care Counsel of Nassau) 32888 93.095 33,840 -

Biomedical Research and Research Training Direct 93.859 59,950 -

Mental Health Research Grant Direct 93.242 130,382 44,685

Drug Abuse and Addiction Research Programs (Pass-

through from the Research Foundation of CUNY) 4R25DA035161 93.279 38,733 -

Substance Abuse and Mental Health Administration

(Pass-through from Central Nassau Guidance)

SM062238

93.243

31,264

-

Substance Abuse and Mental Health Administration Direct 93.243 367,030 -

Total U.S. Department of Health and Human Services 722,949 44,685

National Science Foundation:

Geosciences (Pass-through from the Trustees of

Columbia University)

OCE-1450528

47.050

83,452

-

Education and Human Resources Direct 47.076 277,413 -

Office of International Science and Engineering Direct 47.079 27,465 -

-

Total National Science Foundation 388,330 -

U.S. Department of Education:

Special Education - Personnel Development to Improve

Services and Results for Children with Disabilities

Direct

84.325 129,411

-

Carol White Physical Education Program (Pass-through

from Freeport Public Schools and Westport Public

Schools)

S215F130373 and

S215F130320

84.215 58,426

-

Total U.S. Department of Education 187,837 -

Total Expenditures of Federal Awards $ 89,546,301 $ 44,685

The accompanying notes to the schedule of expenditures of federal awards should be read in conjunction with this schedule.

28

ADELPHI UNIVERSITY

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

FOR THE YEAR ENDED AUGUST 31, 2016

1. BASIS OF PRESENTATION

The accompanying schedule of expenditures of federal awards (the “Schedule”) presents the federal grant expenditures

of Adelphi University and subsidiary (collectively, the “University”) for the year ended August 31, 2016. The schedule

was prepared using the accrual basis of accounting and is in accordance with the requirements of Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards. Therefore, some amounts presented in this Schedule may differ from amounts presented in or used

in the preparation of the consolidated financial statements. In addition, the University did not elect to utilize the federal

minimum indirect cost rate (i.e. 10%).

2. LOAN PROGRAMS

The federal student loan programs listed below are administered directly by the University, and balances and transactions

related to these programs are included in the University’s consolidated financial statements. Loan activities and balances

consist of the following:

Federal CFDA Balance at Loans Payments Balance at

Number September 1, 2015 Issued Received August 31, 2016

Perkins Loan Program 84.038 4,380,015$ 750,000$ (768,312)$ 4,361,703$

Faculty Nursing Loan Program 93.264 1,739,581 290,239 (134,389) 1,895,431

Nursing Student Loan Program 93.364 576,269 206,950 (147,324) 635,895

6,695,865$ 1,247,189$ (1,050,025)$ 6,893,029$

During the year ended August 31, 2016, the University processed $72,708,505 of new loans under the Federal Direct

Student Loan Program which superseded and replaced the Federal Family Education Loan Program as of July 1, 2010,

(it also includes Federal Parents’ Plus Loans for Undergraduate Students and Graduate Plus Loans for Graduate

Students). It is not practical to determine the balance of loans outstanding to students of the University under these

programs.

29

REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS ON INTERNAL

CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER

MATTERS REQUIRED BY GOVERNMENT AUDITING STANDARDS

To the Board of Trustees of

Adelphi University:

We have audited, in accordance with auditing standards generally accepted in the United States of America and

the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller

General of the United States, the consolidated financial statements of Adelphi University and subsidiary

(collectively, the “University”), which comprise the consolidated statement of financial position as of August 31,

2016, and the related consolidated statements of activities and cash flows for the year then ended, and the related

notes to the consolidated financial statements, and have issued our report thereon dated November 28, 2016.

Internal control over financial reporting

In planning and performing our audit of the consolidated financial statements, we considered the University’s

internal control over financial reporting (“internal control”) to design audit procedures that are appropriate in the

circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of

expressing an opinion on the effectiveness of internal control. Accordingly, we do not express an opinion on the

effectiveness of the University’s internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or

employees, in the normal course of performing their assigned functions, to prevent, or detect and correct,

misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal

control, such that there is a reasonable possibility that a material misstatement of the University’s financial

statements will not be prevented, or detected and corrected, on a timely basis. A significant deficiency is a

deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet

important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section

and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant

deficiencies. Given these limitations, during our audit we did not identify any deficiencies in the University’s

internal control that we consider to be material weaknesses. However, material weaknesses may exist that have

not been identified.

Grant Thornton LLP 445 Broad Hollow Road, Suite 300 Melville, NY 11747-3601

T 631.249.6001 F 631.249.6144 GrantThornton.com linkd.in/GrantThorntonUS twitter.com/GrantThorntonUS

Grant Thornton LLP U.S. member firm of Grant Thornton International Ltd

30

Compliance and other matters

As part of obtaining reasonable assurance about whether the University’s consolidated financial statements are

free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations,

contracts, and grant agreements, noncompliance with which could have a direct and material effect on the

determination of financial statement amounts. However, providing an opinion on compliance with those

provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of

our tests disclosed no instances of noncompliance or other matters that are required to be reported under

Government Auditing Standards.

Intended purpose

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the

results of that testing, and not to provide an opinion on the effectiveness of the University’s internal control or on

compliance. This report is an integral part of an audit performed in accordance with Government Auditing

Standards in considering the University’s internal control and compliance. Accordingly, this report is not suitable

for any other purpose.

Melville, New York

November 28, 2016

31

REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS ON

COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND ON INTERNAL

CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE

To the Board of Trustees of

Adelphi University:

Report on compliance for each major federal program

We have audited the compliance of Adelphi University and subsidiary (collectively, the “University”) with the

types of compliance requirements described in the U.S. Office of Management and Budget’s OMB Compliance

Supplement that could have a direct and material effect on its major federal program for the year ended August 31,

2016. The University’s major federal program is identified in the summary of auditor’s results section of the

accompanying schedule of findings and questioned costs.

Our audit of, and opinion on, the University’s compliance for its major federal program does not include the

compliance requirements governing Federal Perkins loan processing and student refunds under the Student

Financial Assistance cluster, because the University engaged Heartland ECSI and Higher One, Inc. to perform

these compliance activities. These third-party servicers have obtained a compliance examination from other

practitioners in accordance with the U.S. Department of Education’s Audit Guide, Audits of Federal Student

Financial Assistance Programs at Participating Institutions and Institution Servicers.

Management’s responsibility

Management is responsible for compliance with federal statutes, regulations, and the terms and conditions of its

federal awards applicable to the University’s federal programs.

Auditor’s responsibility

Our responsibility is to express an opinion on compliance for the University’s major federal program based on our

audit of the types of compliance requirements referred to above. We conducted our audit of compliance in

accordance with auditing standards generally accepted in the United States of America; the standards applicable

to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United

States; and the audit requirements of Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform

Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance).

Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable

assurance about whether noncompliance with the types of compliance requirements referred to above that could

have a direct and material effect on a major federal program occurred. An audit includes examining, on a test

basis, evidence about the University’s compliance with those requirements and performing such other procedures

as we considered necessary in the circumstances.

Grant Thornton LLP 445 Broad Hollow Road, Suite 300 Melville, NY 11747-3601

T 631.249.6001 F 631.249.6144 GrantThornton.com linkd.in/GrantThorntonUS twitter.com/GrantThorntonUS

Grant Thornton LLP U.S. member firm of Grant Thornton International Ltd

32

We believe that our audit provides a reasonable basis for our opinion on compliance for the major federal program.

However, our audit does not provide a legal determination of the University’s compliance.

Opinion on each major federal program

In our opinion, the University complied, in all material respects, with the types of compliance requirements

referred to above that could have a direct and material effect on its major federal program for the year ended

August 31, 2016.

Report on internal control over compliance

Management of the University is responsible for establishing and maintaining effective internal control over

compliance with the types of compliance requirements referred to above. In planning and performing our audit

of compliance, we considered the University’s internal control over compliance with the types of compliance

requirements that could have a direct and material effect on its major federal program to design audit procedures

that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for its major

federal program and to test and report on internal control over compliance in accordance with the Uniform

Guidance, but not for the purpose of expressing an opinion on the effectiveness of internal control over

compliance. Accordingly, we do not express an opinion on the effectiveness of the University’s internal control

over compliance.

As described in our Report on Compliance for Each Major Federal Program above, this Report on Internal Control

Over Compliance does not include the results of the other auditors’ testing of internal control over compliance

that is reported on separately by those auditors.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance

does not allow management or employees, in the normal course of performing their assigned functions, to prevent,

or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely

basis. A material weakness in internal control over compliance is a deficiency, or a combination of deficiencies,

in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a

type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely

basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies,

in internal control over compliance with a type of compliance requirement of a federal program that is less severe

than a material weakness in internal control over compliance, yet important enough to merit attention by those

charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph

of this section and was not designed to identify all deficiencies in internal control over compliance that might be

material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any

deficiencies in the University’s internal control over compliance that we consider to be material weaknesses.

However, material weaknesses may exist that have not been identified.

The purpose of this Report on Internal Control Over Compliance is solely to describe the scope of our testing of

internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance.

Accordingly, this report is not suitable for any other purpose.

Melville, New York

February 13, 2017

33

ADELPHI UNIVERSITY

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE YEAR ENDED AUGUST 31, 2016

SECTION I - SUMMARY OF AUDITOR’S RESULTS

Consolidated Financial Statements

Type of auditor’s report issued: Unmodified

Internal control over financial reporting:

• Material weakness(es) identified? yes X no

• Significant deficiencies identified that are not considered to be

material weakness(es)? yes X none reported

• Noncompliance material to consolidated financial statements noted? yes X no

Federal Awards

Internal control over the major federal program:

• Material weakness(es) identified? yes X no

• Significant deficiencies identified that are not considered to be material

weakness(es)? yes X none reported

Type of auditor’s report issued on compliance for the major federal program: Unmodified

Any audit findings disclosed that are required to be reported

in accordance with 2 CFR 200.516(a) of the Uniform Guidance? yes X no

Identification of the major federal program:

Federal Grantor/Pass-through Program Title or Cluster

Federal

CFDA Number

Student Financial Assistance Cluster:

U.S. Department of Education:

Pell Grant Program 84.063

Federal Direct Student Loan Program 84.268

Supplemental Educational Opportunity Grant Program 84.007

Work Study Program 84.033

Perkins Loan Program

U.S. Department of Health and Human Services:

84.038

Faculty Nursing Loan Program 93.264

Nursing Student Loans Program 93.364

Dollar threshold used to distinguish between type A and type B programs: $750,000

Auditee qualified as low-risk auditee? X yes no

34

ADELPHI UNIVERSITY

SCHEDULE OF FINDINGS AND QUESTIONED COSTS (continued)

FOR THE YEAR ENDED AUGUST 31, 2016

SECTION II - FINANCIAL STATEMENT FINDINGS

No matters reported.

SECTION III - FEDERAL AWARD FINDINGS AND QUESTIONED COSTS