27

Economy & Civil Construction Outlook Adrian Hart, Senior Manager Infrastructure & Mining

| Date post: | 25-Jan-2017 |

| Category: |

Business |

| Upload: | informa-australia |

| View: | 551 times |

| Download: | 0 times |

Economy & Civil Construction Outlook Adrian Hart, Senior Manager Infrastructure & Mining

Presentation Outline

Key Messages, Implications & Risks

Economic State of Play & Outlook

National Civil Construction Outlook

State Comparisons

Implications: Findings from the CCFWA Infrastructure Report 2015

Key Messages

National economy to continue growing below trend – but stronger

growth expected later this decade

Mining investment bust still has 2-3 years to run, impacting on the

economy and civil construction work. We have not hit bottom yet.

Vast differences in the economic and civil construction outlook

between the “resources” and “non-resources” states

Vast differences in the outlook between segments of the

construction industry, and within the civil construction market

Implications

For businesses: to plan and prepare for the substantial shifts in

construction work taking place over next 3-5 years, regionally and

by segment. Be aware of the drivers, opportunities and risks.

Where possible, use the current downturn to lock in lower costs

(interest rates, rents, wages, overheads) to be in the best shape

for the next upswing in the cycle.

For governments and infrastructure providers: to recognise the

best time to deliver projects and how to fund them. Use long term

planning to avoid unnecessary booms and busts in activity.

We need a political “New Deal” for infrastructure investment

Risks

Global: economic conditions end up worse than expected, driving

down commodity prices and resources investment even more

The $A stays too high for too long – even US$0.70 is high given

the appreciation of the US dollar against other currencies

Domestic: Public investment continues its decline (since 2010)

due to either a lack of productive infrastructure projects, or lack

of consensus on how to fund them

Political noise and electioneering stymie confidence and

spending in the economy

World Economic Growth

-4%

-2%

0%

2%

4%

6%

87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

World OECD Australia

Year ended December Source: BIS Shrapnel, OECD, Consensus

Annual growth in Real GDP

Value of Australian exports by region

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

88 90 92 94 96 98 00 02 04 06 08 10 12 14

South Korea

European Union

USA

India

Year ended December Source: ABS

Percent of annual Australian exports

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

88 90 92 94 96 98 00 02 04 06 08 10 12 14

Greater China

Japan

Other East Asia

Year ended December Source: ABS

Percent of annual Australian exports

China’s Real GDP Growth

+ 0.3+ 0.4+ 0.5

+ 0.5+ 0.6

+ 0.8+ 1.0

+ 0.7+ 0.7

+ 1.0+ 1.0

+ 0.8+ 0.9

+ 1.0+ 1.0

+ 1.0

+ 1.1

0

4

8

12

16

20

0

4

8

12

16

20

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Tho

usa

nd

s

Source: BIS Shrapnel, OECD, Consensus

$ Trillion, Real GDP (in constant PPP, $US 2008)

Annual change in Real GDP ($T)

$4.4 trillioneconomy in 2000

$17.8 trillioneconomy in 2017

Size of Australian economy in 2014(in constant PPP, $US 2008)

0%

2%

4%

6%

8%

10%

12%

14%

00 05 10 15 17

Year ended December

Percent

Annual GDP growth (%)

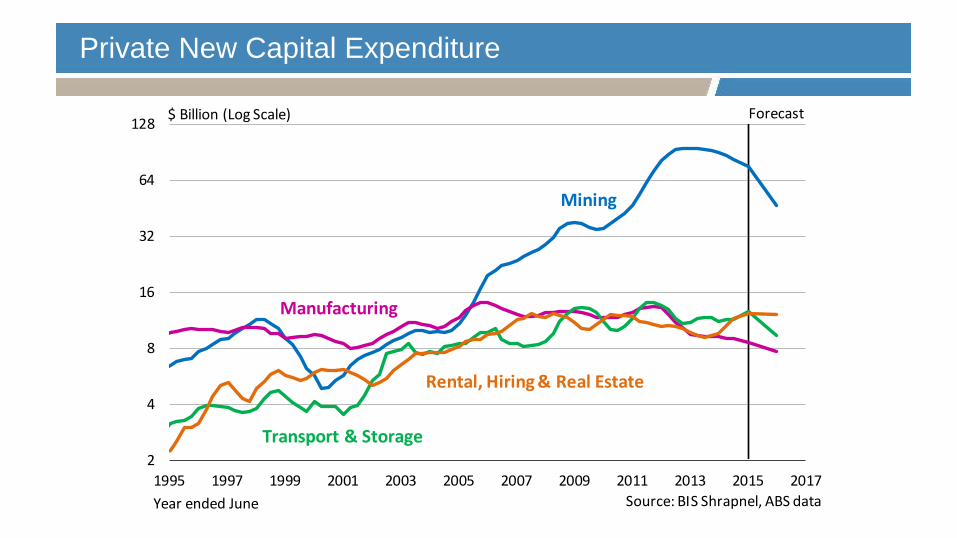

Private New Capital Expenditure

2

4

8

16

32

64

128

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Mining

Forecast$ Billion (Log Scale)

Rental, Hiring & Real Estate

Manufacturing

Transport & Storage

Year ended June Source: BIS Shrapnel, ABS data

Government Investment to pick up – but when?

0

3

6

9

12

15

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

NSW VIC

QLD WA

SA Other

Year ended June Source: BIS Shrapnel, ABS

$ Billion (in constant prices), value of work done

Phases of construction in Australia

Housing boom/bust

Private funding boom

Resources boom

Public funding boom

0

50

100

150

200

250

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Year ended June

Engineering Construction

Non-Residential Building

Residential Building

Source: BIS Shrapnel, ABS

$ Billion

Construction – Australia Value of Work Done

0

50

100

150

200

250

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Year ended June

Engineering Construction

Non-Residential Building

Residential Building

Source: BIS Shrapnel, ABS

$ Billion

Engineering Construction – Australia Value of Work Done

0

30

60

90

120

150

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Privately funded

Publicly funded

Total

Year ended June Source: BIS Shrapnel, ABS

$ Billion (in constant prices), value of work done

Mining and Heavy Industry Construction – Australia Value of Work Done

0

10

20

30

40

50

60

70

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Other heavy industry

Other minerals (includes iron ore)

Coal

Bauxite, alumina and aluminium

Oil and gas

Year ended June Source: BIS Shrapnel, ABS

Forecast$ Billion (in constant prices), value of work done

Construction – Australia Value of Work Done by State

0

10

20

30

40

50

60

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Source: BIS Shrapnel, ABS

$ Billion

Year ended June

NSW

QLD

VIC

WA

SA NT

ACT TAS

Challenges & Implications – From CCFWA Infrastructure Report 2015

End of resources boom requires new drivers for growth:

“Restoring full employment and growth after the end of the China resources boom … requires real

currency depreciation supported by public investment in productive infrastructure and

uninhibited productivity-raising reform.” – Ross Garnaut (2015)

“Monetary policy alone can't deliver everything we need and expecting too much from it can lead,

in time, to much bigger problems… Meanwhile, as often remarked, infrastructure spending has a role

to play in sustaining growth and also in generating confidence.” – Glenn Stevens (2015)

“Robust demand growth from advanced economies has not yet emerged despite continued very low

interest rates and easing of brakes to the recovery … in this context an increase in public

infrastructure investment, particularly for advanced economies with clearly identified infrastructure

needs and efficient public investment processes, could provide a boost to demand in the short

term and help raise potential output in the medium term.” – IMF World Economic Outlook (2014)

Challenges & Implications – From CCFWA Infrastructure Report 2015

Do we have clearly identified infrastructure needs? Do we have an

infrastructure deficit?

ABN Amro & Citigroup 2008 – Australian investment task between $450 - 770 billion

Engineers Australia 2010 – changes in investment needed to retain adequacy requirements

Infrastructure Australia 2013 – Australian infrastructure backlog measured at $300 billion

Property Council of Australia 2014 – WA infrastructure deficit measured at $60 billion

Infrastructure Australia 2015 – National Infrastructure Audit

Australia’s population to grow to 30.5 million by 2031

75% of this growth focused in Sydney, Melbourne, Brisbane and Perth

Biggest infrastructure gaps are in urban transport and regional water

Economic cost of congestion in Perth to rise to $15.9 billion per annum by 2031

Challenges & Implications – From CCFWA Infrastructure Report 2015

How can we fund infrastructure provision?

Private sector – when benefits of infrastructure provision can be captured

Public sector approaches:

User charges – can be politically difficult for some sectors such as roads

Capital recycling – all costs should be considered, including future regulation

Tax reforms – including road pricing, value catchment, betterment levies – not stamp duties!

Debt financing – raises servicing costs, but can be both efficient and equitable

Challenges for public sector funding

Choosing the most productive projects – requires transparent CBA and better industry data

Reforming procurement processes to lower costs as per Productivity Commission (2014)

Utilising a mix of funding mechanisms including debt – don’t lock out valid solutions

Requires a political “New Deal” in terms of advocacy for tax reform and debt funding

Challenges & Implications – From CCFWA Infrastructure Report 2015

Can we really use more debt for infrastructure provision?

Do we have a debt problem?

Public debt in Australia is not relatively high in Australia – but household debt is!

Commonwealth public debt around 16% of GDP, total public debt closer to 35%

114th largest public debt to GDP ratio, generally half that of our major trading partners

G20 public debt to GDP ratios averaging around 100% (not good either!)

IMF: Australia identified as having one of the world’s largest measure of “fiscal space”

Morgan Stanley: Australia could boost debt by $80 billion without losing AAA credit rating

Household debt has risen sharply to 100% of GDP from 30% in the early 1990s.

Costs of funding infrastructure through debt

Additional interest costs, even at record low rates

Potential loss of creditworthiness (credit rating) which could push up repayment costs

(Very real) risk of not choosing productive projects

Risk of confusing productive and unproductive debt – requires tax and spending reform!

Australia’s public debt position compared to our peers

0-20% of GDP

20-40% of GDP

40-75% of GDP

75%+ of GDP

Rank / Country

1 Japan 227.70 227.7

3 Greece 174.50 174.5

5 Italy 134.10 134.1

7 Portugal 131.00 131.0

9 Ireland 118.90 118.9

11 Singapore 106.70 106.7

15 Spain 97.60 97.6

16 France 95.50 95.5

20 Canada 92.60 92.6

24 United Kingdom 86.60 86.6

35 Germany 74.70 74.7

39 United States 71.20 71.2

67 India 51.30 51.3

112 New Zealand 35.30 35.3

113 Switzerland 34.70 34.7

114 Australia 34.50 34.5

129 Norway 29.60 29.6

133 Indonesia 23.90 23.9

137 China 22.40 22.4

144 Chile 16.50 16.5

159 Kuwait 6.80 6.8

163 Libya 2.90 2.9

164 Saudi Arabia 1.60 1.6

Net Debt as

Share of GDP

Source: IMF Datamapper

Source: CIA The World Factbook

Commonwealth net debt and interest payments as share of GDP

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

-5%

0%

5%

10%

15%

20%1

986

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15e

20

16f

20

17f

20

18f

20

19f

Net Debt (LHS) Interest Payments (RHS)

Debt expected to peak

at levels similar to 1996

as a share of GDP.

Record low interest rates

mean servicing costs will

peak at a level 40% lower

than 1996.

Public debt would need to

rise by another $180

billion to match servicing

costs from 1996 as a

share of GDP.

Public sector net debt as share of GDP

Public debt as a share

of GDP remains well

below historical

averages, despite

rising since 2008

(Circled area matches

period of previous

slide)

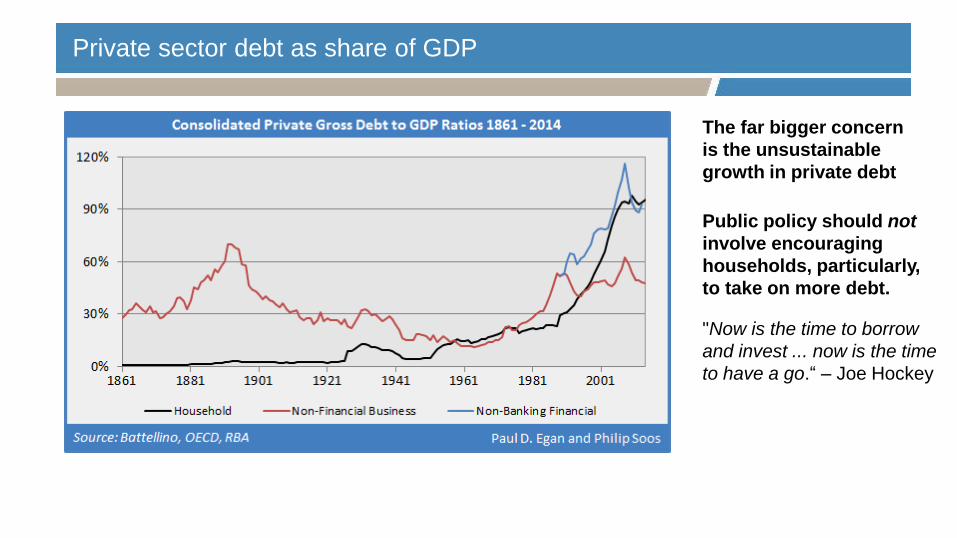

Private sector debt as share of GDP

The far bigger concern

is the unsustainable

growth in private debt

Public policy should not

involve encouraging

households, particularly,

to take on more debt.

"Now is the time to borrow

and invest ... now is the time

to have a go.“ – Joe Hockey

Fiscal Space – Distance to Debt Limit

246

241.1

228.1

224.5

222.9

214.5

209.5

202

196.7

193

191.1

188.8

171.7

167.9

165.1

158.1

156.6

151.1

149.8

145.3

132.6

124.3

116.9

115.2

105.5

58.8

0

0

0

0

0 50 100 150 200 250

Norway

South Korea

New Zealand

Hong Kong

Luxembourg

Australia

Taiwan

Switerland

Denmark

Singapore

Israel

Sweden

Finland

Germany

United States

Netherlands

Austria

Malta

Canada

Iceland

United Kingdom

Belgium

France

Spain

Ireland

Portugal

Japan

Italy

Greece

Cyprus

Fiscal Space: Distance to Debt Limit (Percentage Points)

Source: Moodys Analytics, IMF

Challenges & Implications

Benefits of using debt for infrastructure provision

Intergenerational equity: costs of infrastructure provision are spread across multiple generations,

to match the benefits accruing to future generations from infrastructure provision.

Economic efficiency (in special circumstances): the economic returns (output benefits) to

infrastructure provision exceed the costs and in some cases can even drive a decline in the public

debt to GDP ratio (IMF).

Gross multiplier impact of a boost to civil construction: 2.17

Initial Civil Construction Broader Economic Annual Interest Costs ($M) @

Boost ($M) Impact ($M) 2.5% 3.0% 3.5%

$250 $542 6.3 7.5 8.8

$500 $1,084 12.5 15.0 17.5

$750 $1,518 18.8 22.5 26.3

$1,000 $2,169 25.0 30.0 35.0

Challenges & Implications

The IMF has specifically endorsed debt funding for infrastructure in

Australia

“Increasing public investment (financed by more borrowing rather than offsetting measures) would

support aggregate demand and ensure against downside risks. It would also employ resources

released by the mining sector, catalyse private investment, boost productivity, take advantage of

record-low borrowing rates, and maintain the government’s net worth. Indeed, IMF research

suggests that economies like Australia—with an output gap, accommodative monetary policy,

and fiscal space—benefit most from debt-financed infrastructure investment, with the growth

boost largely containing the impact on the (low) debt-to-GDP ratio.” – IMF (2015)

But depends on the following factors:

Selecting the best projects through transparent CBA

Having spare industry capacity (keeping costs of procurement low)

Taking advantage of low interest rates and fiscal space may require:

Establishing consensus with State and Federal Governments on debt and tax/spend reform

Separation of “Opex” and “Capex” spending in the Budget

A political “New Infrastructure Deal”?