290

AGL AUTONOMOUS GROUP LEARNING Dr. Bob Boland Boland1

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | brent-stanley |

| View: | 213 times |

| Download: | 0 times |

AGL

AUTONOMOUS

GROUP

LEARNING

Dr. Bob Boland

Boland1

6/1 AUTONOMOUS GROUP

LEARNING (AGL)

NO. 6 - DISCOUNTED CASH FLOW FOR CAPITAL INVESTMENT ANALYSIS

PART I

Copyright: RGAB/2005/1

1.0 INTRODUCTION

6/2 ABBREVIATIONS

AGI AUTONOMOUS GROUP LEARNING IND INDIVIDUAL SC SMALL GROUP CSG COMBINED SMALL GROUP MG MAIN GROUP CIA CAPITAL INVESTMENT ANALYSIS PL PROGRAM LEARNING L LECTURE D DISCUSSION CH CHAPTER

STOP DO NOT LOOK AHEAD UNTIL SPECIFICALLY REQUESTED TO DO SO.

6/3 1.1 SPECIFIC LEARNING OBJECTIVES

(a) Understand the language and concepts of

DCF for Capital Investment Analysis (CIA)

(b) Develop creativity and confidence in applying

DCF techniques to practical business problems.

(c) Appreciate the need for a creative system

of long term planning for capital investment

involving: Search, Analysis, Decision and Audit.

(d) Communicate effectively with technical and

specialist staff.

(e) Motivate further study in the future.

6/3 AGL - AUTOMATED GROUP LEARNING

The AGL method is designed to achieverapid individual learning, using specialmaterials and the stimulus of groups activity,without a formal instructor.

The groups use the materials to find theanswers to all the questions and problems.

6/4 GROUP ARRANGEMENTS

The work will be done:

I - Individually.

SG - Small Groups which change twice daily.

CSJ - Combined Small Group - two groups working together.

MG - Main Group - for lectures.

6.5a 1.4 SMALL GROUPS

INITIAL SMALL GROUP NAMES PROVIDEDBY THE ORGANIZER.

MAKE A NOTE OF YOUR GROUP AND THENAMES OF THE OTHER MEMBERS

6/6 1.5 LEARNING MATERIALS

(a) Retained by members:

TextbookNotebook for recording every key pointCourse DiaryProgram Learning

Glossary

(b) Used by members but not retained:

Daily Work Packs for Parts I and II including: introduction, cases,. solutions and key learning points to be noted.

6/6 a 1.5 LEARNING MATERIALS

NOTE:

Use your notebook

Do not mark the Daily Work Pack which must behanded back to the Organiser.

Do not "look ahead" in the work pack untilspecifically asked to do so.

6/7 1.6 METHOD

Plan to complete fully every task in the time allowed.

A pattern of learning methods will include:

(a) Program learning(b) Case analysis(c) Role assignments(6) Lectures(e) Quizzes (f) Learning patterns(g) Homework readings and exercises(h) CAI(I) Learning recall tape..

6/8 1.7a LEARNING PATTERNS

LEARNING OBJECTIVESLanguage and Concepts

Capital Budgeting

Measures of Investment

CIA Systems

Communication with Specialists

DCF Technique before and after tax

= CONFIDENCE

6/9 1.7b LEARNING PATTERNS

GROUP ARRANGEMENTS

IndividualIndividual

Small GroupSmall Group

Combined Small GroupCombined Small Group

Main GroupMain Group

6/10 1.7c LEARNING PATTERNS

METHODS

READINGS CASES EXERCISES QUIZ PROGRAM LEARNING INDIVIDUAL WORK SG WORK CSG WORK MG WORK

= CONFIDENCE

6/11 1.7d DISCOUNT TABLE A

PV of 1.00 received ONCE ONLY in years 1-10.

Year 0% 10% 20% 30%0 1.0 1.0 1.0 1.01 1.0 0.9 0.8 0.82 1.0 0.8 0.7 0.63 1.0 0.8 0.6 0.44 1.0 0.7 0.5 0.45 1.0 0.6 0.4 0,2Sub. 5.0 3.8 3,0 2.4 as in B - Sub-total 6 1.0 0,6 0.3 0.47 1.0 0,5 0.3 0.98 1.0 0.5 0.2 0.19 1.0 0.4 0.2 0.110 1.0 0.3 0.2 0.1Total 10.0 6.1 4.2 3.l as in B - Sub-total

6/12 1.7e DISCOUNT TABLE B

PV OF 1.00 RECEIVED EVERY YEAR IN YEARS 1-1O

Year 0% 10% 20% 30%

1 1.0 0.9 0.8 0.72 2.0 1.7 1.5 1.43 3.0 2.5 2.1 1.84 4.0 3.2 2.6 2.25 5.0 3.8 3.0 2.4 as in A6 6,0 4.4 3.3 2.67 7.0 4.9 3.6 2.88 8.0 5.4 3 8 2.99 9.0 5.8 4.0 3.010 10.0 6.1 4.2 3.1 as in A

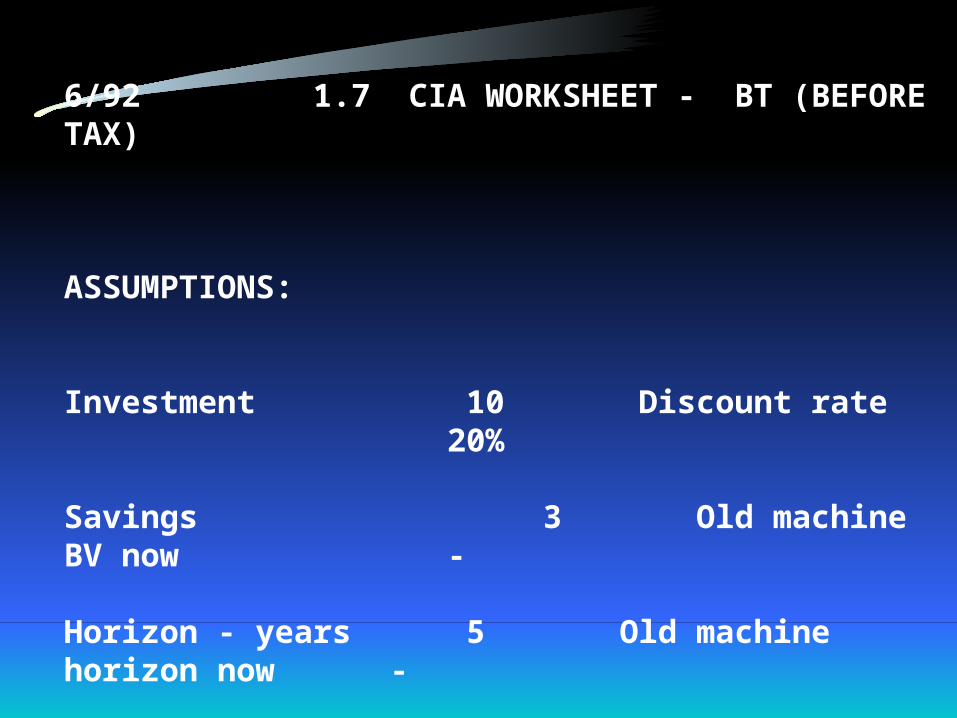

6/92 1.7 CIA WORKSHEET - BT (BEFORE TAX)

ASSUMPTIONS:

Investment 10 Discount rate 20%

Savings 3 Old machine BV now -

Horizon - years 5 Old machine horizon now -

Terminal value nil Old machine TV now -

Tax Rate -

6/93 1.7 CIA WORKSHEET - BT

Annual savings 3

Less depreciation: New machine 10/5 years 2 Old machine / years Incremental depreciation 2 Taxable income 1Tax @ % -After tax income 1

Add back depreciation 2

Annual cash flow 3

6/94 1.7 CIA WORKSHEET - BT

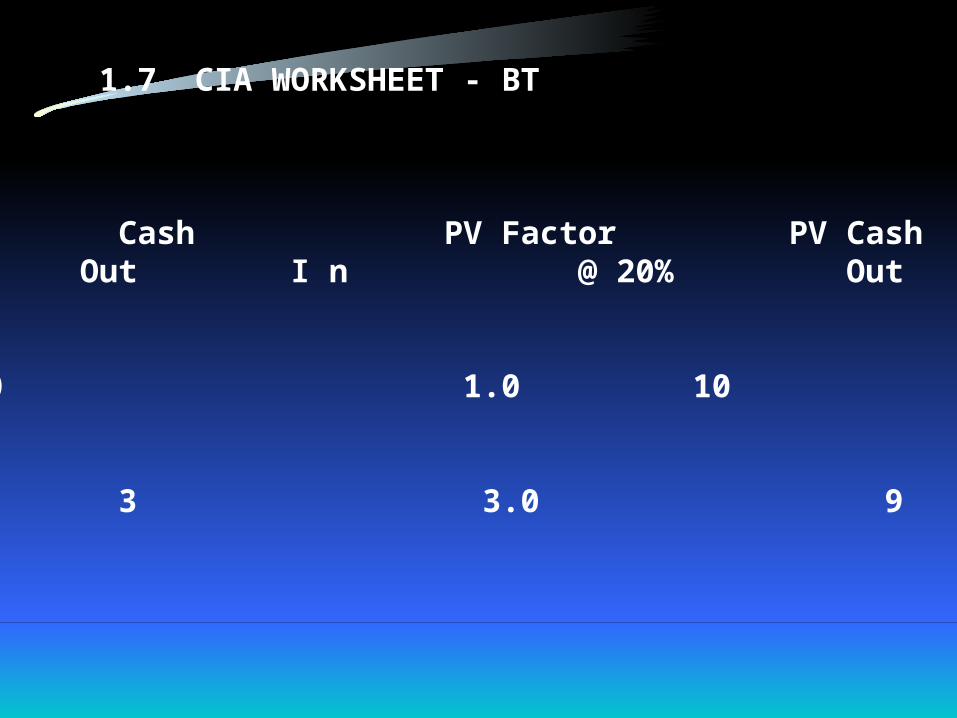

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 10 1.0 10

1- 5 3 3.0 9

6/95 1.7 CIA WORKSHEET - BT

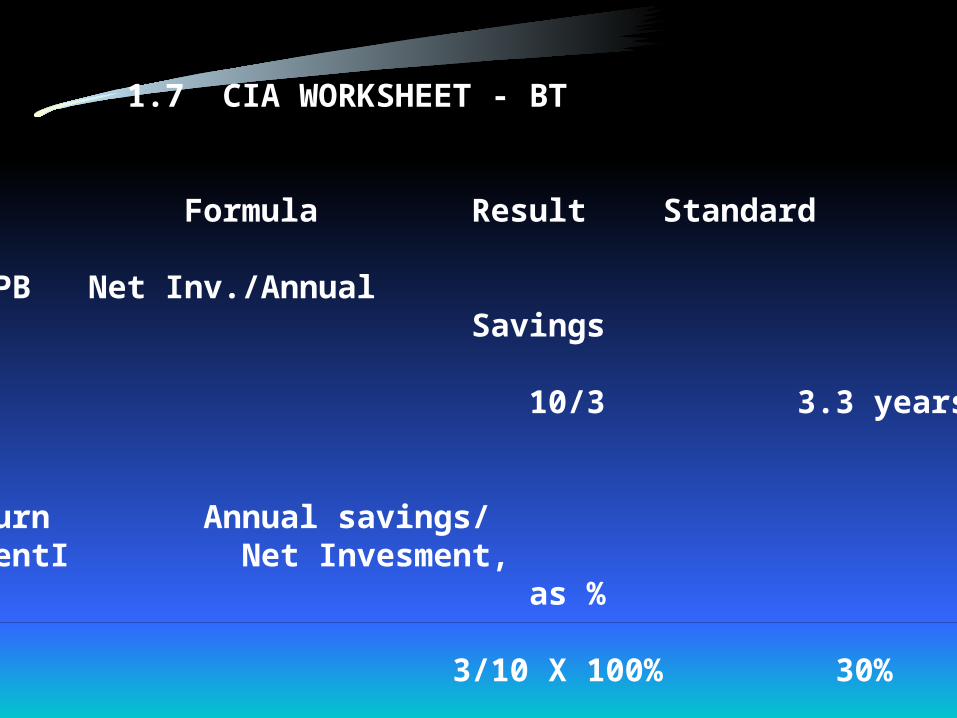

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

10/3 3.3 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

3/10 X 100% 30% 20%

6/95a 1.7 CIA WORKSHEET - BT

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

9 - 10 - 1 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

later later 1.0 +

6/95c 1.7 CIA WORKSHEET - BT

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

later

Refer to Table B with horizon of 8 years to give an actual DR later 20%

2.0 QUIZ -

... JUST FOR FUN ...

3.0 PROGRAM LEARNING

4.0 LECTURE -

BASICS OF CIA

6/17 ASSIGNMENT 4.0 - LECTURE - BASICS OF CIA

4.1 FINANCIAL MANAGEMENT

Financial Management deals with four major problems:

(a) How large should a firm seek to be?

(b) What rate of growth - sales, assets, profit, etc. ?

(c) To what extent should instability in sales and profit be avoided?

(d) What kind of assets should the firm acquire? (This is Capital Investment analysis!!)

6/18 4.2 CAPITAL INVESTMENT ANALYSIS (CIA)

This analysis of capital projects is often known as:

Capita! budgeting, or Capital investment analysis Capital expenditure analysis DCF analysis Project appraisal, or Return on investment analysis

6/18a 4.2 CAPITAL INVESTMENT ANALYSIS (CIA)

CIA means: Invest Now in Year 0 … for benefits later in Years 1-10 plus

The AGL approach to CIA:

Part I - Basics Measures of Investment before tax

Part II - Capital Budgeting Systems Measures of Investment after tax.

6/19 4.3 CAPITAL INVESTMENT DECISIONS

Key decisions! Large amounts ! Long time penods.

(a) Policy

(b) Law

(c) Economics (Return on Investment)

CIA deals mainly with (c)!

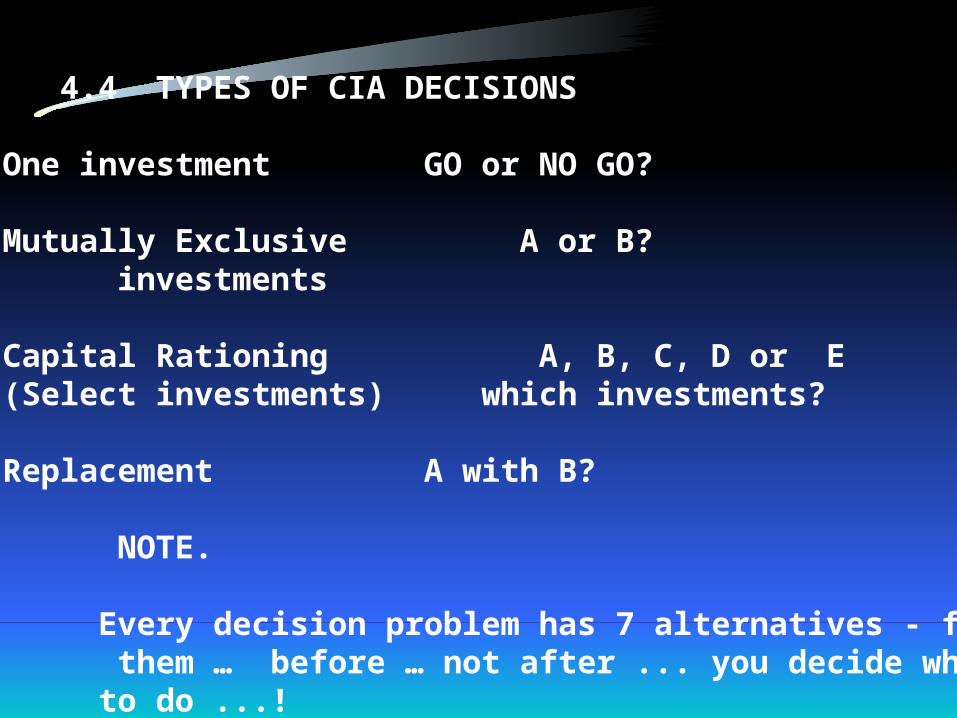

6/20 4.4 TYPES OF CIA DECISIONS

One investment GO or NO GO?

Mutually Exclusive A or B? investments

Capital Rationing A, B, C, D or E(Select investments) which investments?

Replacement A with B?

NOTE.

Every decision problem has 7 alternatives - find them … before … not after ... you decide what to do ...!

6/21 4.5 CASH FLOW - CASH PROFILE

(a) All investment decisions may be reduced to a cash out (Year 0) and cash in (Years I- 10) in a Cash Profile:

Year Cash Out Cash ln 0 1 000

1-10 500 p. a.

(b) Impossible to evaluate CIA decisions without taking account of: different horizons and cash flows over time. Cash has a cost in relation to time.

6/22 4.6 DISCOUNTED CASH FLOW (DCF)

DCF recognises that future cash inflows and must:

(a) Repay the initial investment (Year 0), and

(b) Provide compound interest on the balance of investment outstanding.

DCF relates money to interest but not to INFLATION.

6/23 4.7 DISCOUNT TABLES

Discount tables are compound interest tables worked backwards.

Tables of PV (Present Value) of an Amount at an Interest (Discount) Rate (%) over a Time Period (Horizon) (years 0 - 50).

PV Tables: Table A - PV of 1,00 received only once Table B - PV of 1.00 received every year

NOTE: Exercise the discount tables to achieve a "feel" for the numbers.

6/24 4.8 ASSUMPTIONS

CIA depends upon the six basic assumptions on the worksheet: 1. Investment

2. Annual savings3. Horizon4. Tax rate5. Discount rate

6. Terminal values

NOTE: The new Gross Investment is reduced by TerminalValue of the old replaced equipment to compute the Net Investment. Book values are not cash flows and are therefore not relevant (except for tax purposes).

6/25 4.9 DCF JARGON

PV - Present Value - Value today (Year 0)

NPV Net Present Value - Excess of PV of Savings (Year 1-10) over the PV of Investment (Year 0)

PVF - Present Value Factor - Number in the discount table for a discount rate over a horizon penod.

6/26 4.10 SIMPLE MEASURES OF INVESTMENT

Measure each investment against a standard:

(a) Payback - period of years

Measures risk and cash recovery. Net Investment/Annual savings before depreciation and tax

(b) Simple Return dn Investment (SRI) - % return

Highly misleading measure. Gross Annual Savings/Net Investment x 100%

6/26a 4.10 SIMPLE MEASURES OF INVESTMENT

(c) DCF - Net Present Value (NPV)

Excess of PV of savings over PV of Investment for a Discount Rate over a Horizon period. NPV is computed:

Annual cash flow - say 40

PV Factor (Table B 20% 10 Years) - 4.2

PV of Savigs 40 times 4.2 168

Less: PV of Investment 120

Net Present Value +48

Note: NPV of an acceptable investment is 0 or more.

6/27 4.11 OVERALL

CIA is part of Financial Management concerned with investment NOW for benefit LATER.

For DCF analysis of CIA project we determine:

(a) Assumptions

(b) Cash Flow

(c) Cash Profile

(d) Measures of Investment

(e) Non-quantitative factors

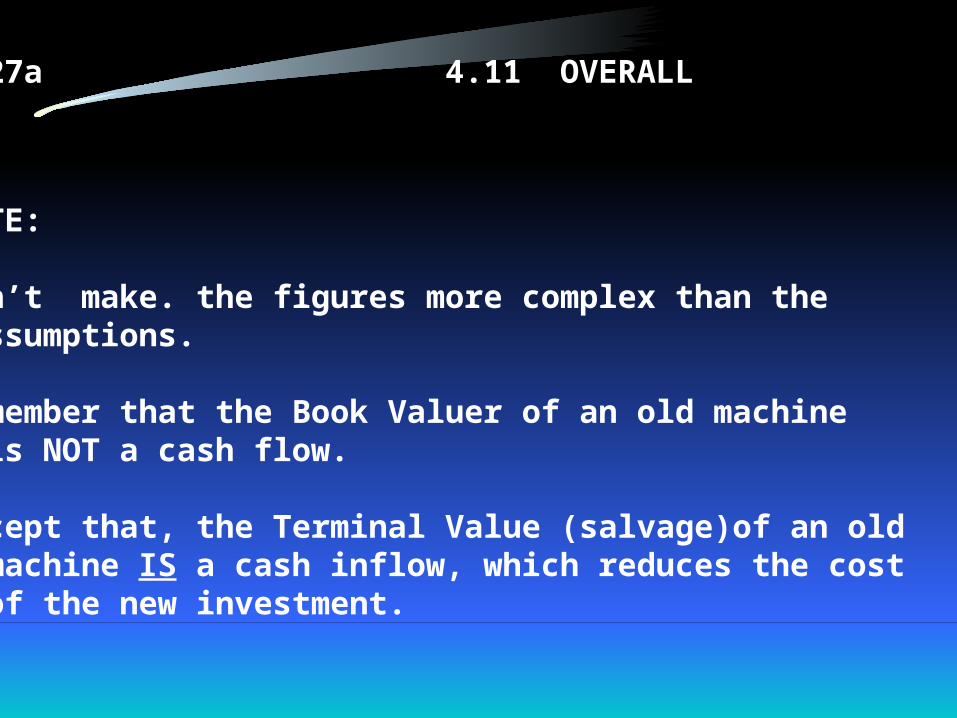

6/27a 4.11 OVERALL

NOTE:

Don’t make. the figures more complex than the assumptions.

Remember that the Book Valuer of an old machine is NOT a cash flow.

Accept that, the Terminal Value (salvage)of an old machine IS a cash inflow, which reduces the cost of the new investment.

6/29 4.12 LEARNING PATTERNS

ASSUMPTIONS AND GARBAGE

Poor Assumptions = GARBAGE!!!

Discounted Assumptions = Computerized Discountred Garbage!!!

Question: Why is a CIA Yield of 15.656% Garbage?Answer?Not yet!

Answer: Because CIA assumptions about the future can never be that accurate …15% … plus or minus …

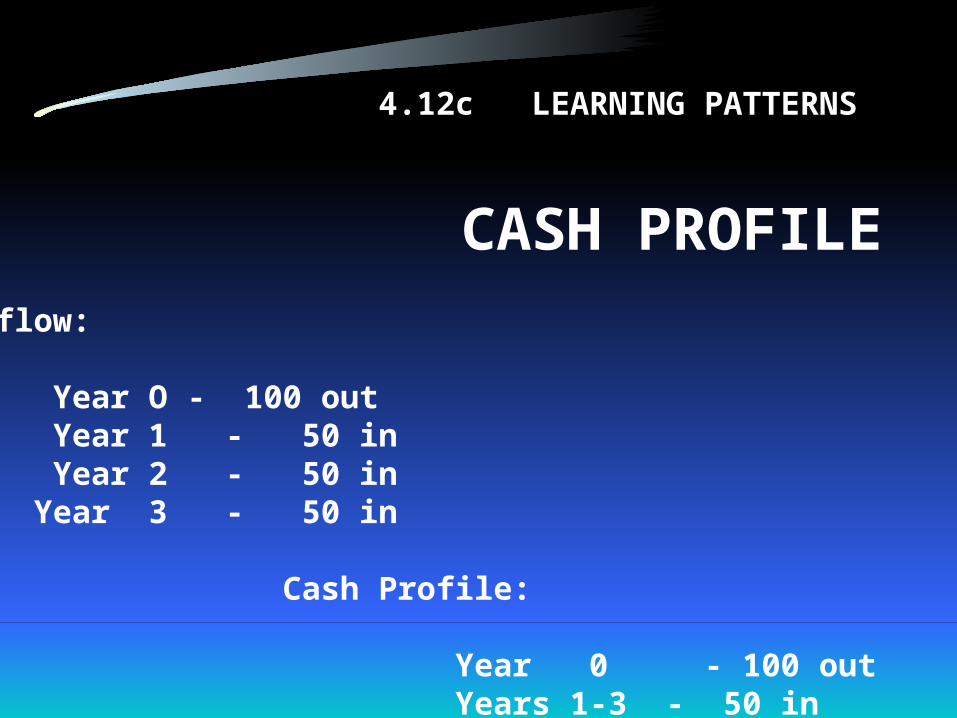

6/30 4.12c LEARNING PATTERNS

CASH PROFILE

Cash flow:

Year O - 100 out Year 1 - 50 in Year 2 - 50 in Year 3 - 50 in

Cash Profile:

Year 0 - 100 out Years 1-3 - 50 in

6/31 4.12d LEARNING PATTERNS

PRESENT VALUES

Discount Rate YR 1 YR 2 YR 3 YR 4

0% 1.00 1.00 1.00 1.00

20% .80 1.50 2.10 2.60

Table A B B B

Note: Cash flow in early years has a higher present value.

6/32 4.12e LEARNING PATTERNS

INVESTMENT GROSS AND NET

Gross Investment 200

Less:

Salvage vlaue of old machine 80

Net |Investment 120

Note: Old machine book value is not a cash flow.

6/33 4.12f LEARNING PATTERNS

PAYBACK

INVESTMENT 100

ANNUAL SAVINGS 20

PAYBACK 5 years

HORIZON? WHO CARES?

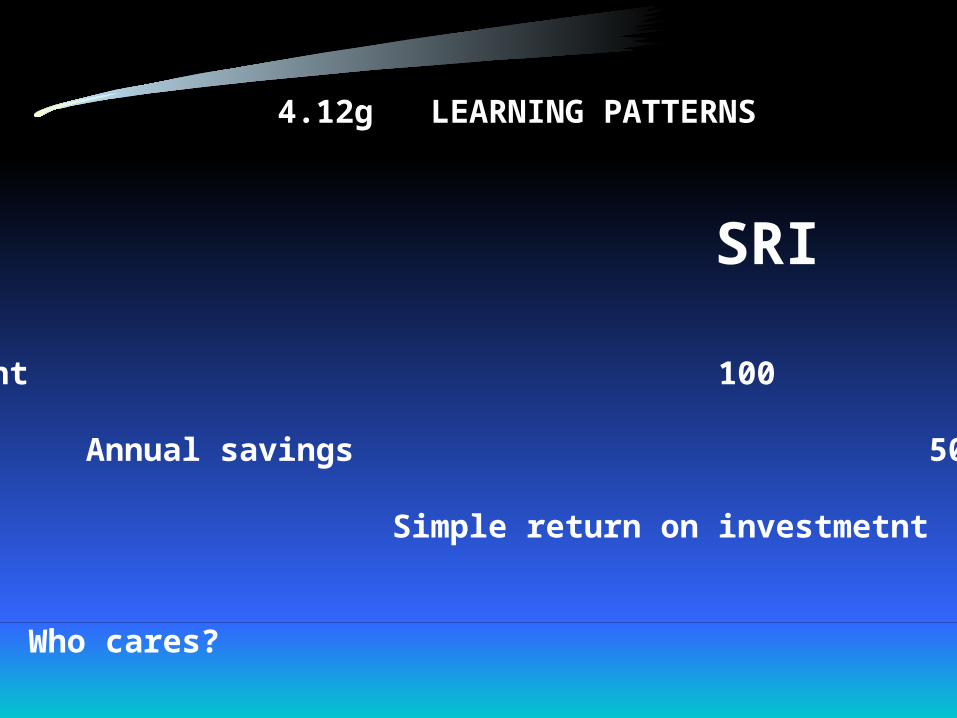

6/35 4.12g LEARNING PATTERNS

SRI

Investment 100

Annual savings 50 Simple return on investmetnt 50%

Horizon? Who cares?

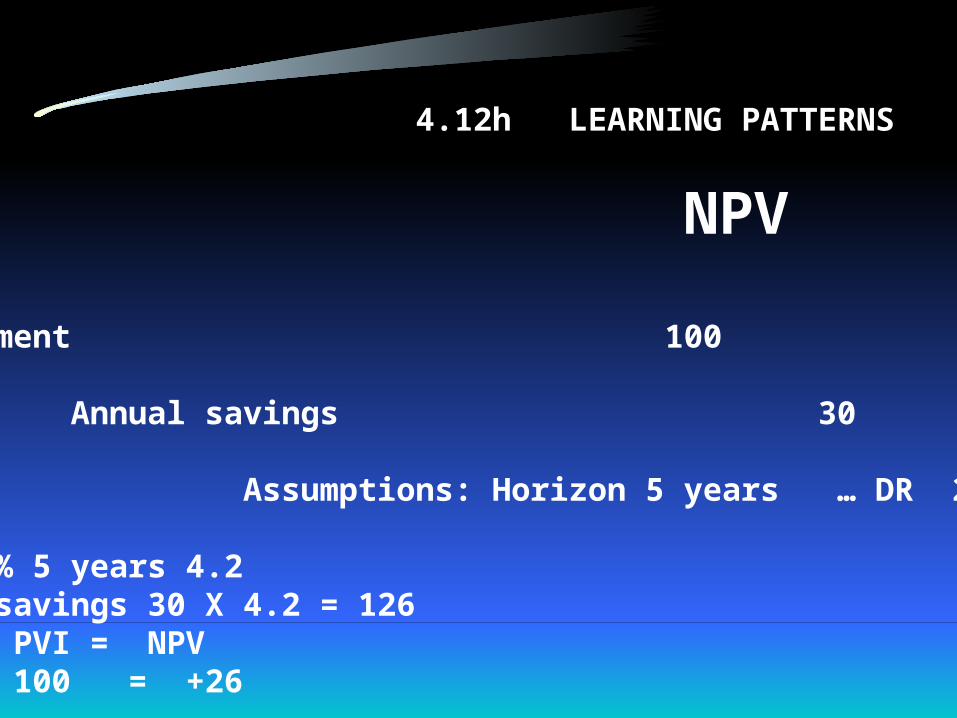

6/36 4.12h LEARNING PATTERNS

NPV

Investment 100

Annual savings 30

Assumptions: Horizon 5 years … DR 20% …!!

PVF 20% 5 years 4.2PV of savings 30 X 4.2 = 126 PVS - PVI = NPV126 - 100 = +26

6/37 4.13 CIA WORKSHEET

ASSUMPTIONS:

Investment 200 Discount rate 20%

Savings 30 Old machine BV now -

Horizon - years 10 Old machine horizon now -

Terminal value nil Old machine TV now -

Tax Rate ignored

6/38 4.13 ANNUAL CASH FLOW

Annual savings 30

Less depreciation: New machine 200/10 years 20 Old machine / years Incremental depreciation 20 Taxable income 10Tax @ % -After tax income 10

Add back depreciation 20

Annual cash flow 30

6/39 4.13 OLD MACHINE EFFECT ON NEW INVESTMENT

Old machine net book value now -

Less: old machine terminal value now 100

Tax loss -

Old machine tax shield @ % -

Old machine terminal value now 100

Toral reduction of the new investment in Year 0 100

6/39 4.13 CASH PROFILE

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 200 1.0 200

1-10 30 4.2 126

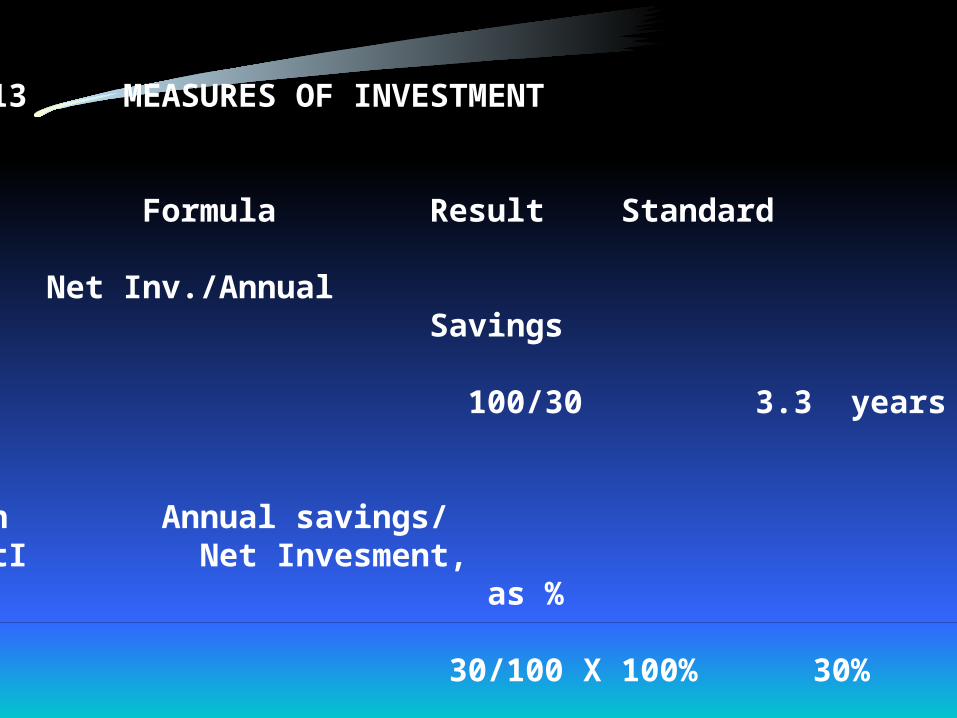

6/40 4.13 MEASURES OF INVESTMENT

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

100/30 3.3 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

30/100 X 100% 30% 20%

6/40a 4.13 MEASURES OF INVESTMENT

Measure Forrmula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

126 -100 26 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment later

5.0 CASE STUDY IN SG & CSG

6.0 LECTURE

ON THE CASE

6/41 6. 0 - LECTURE - MAZARELLA CO.

6. 1 STORY OF THE CASE

Engineering company has a policy of replacing plant using as measures of iInvestment:

Payback 3 years or SRI 25%

Chief Engineer seeks to compare old Measures of Investment with new DCF measure "Net Present Value" to see whether replacement is justified.

6/42 6. 2 ALTERNATIVES TO PURCHASE OF A NEW MACHINE

There are always many alternatives to buying a new equipment including:

(1) Time - buy later (2) Quantity - buy one or more or none (3) Source - buy differently (4) Efficiency - improve internal efficiency instead (5) Do nothing (6) Do without all machines (7) Lease or hire purchase (8) Repair or overhaul existing machines etc.

6/42a 6. 2 ALTERNATIVES TO PURCHASE OF A NEW MACHINE

NOTE: Always do AA - Alternative Analysis early! Seek all alternatives before analysing any one, avoid "Emotional Investment; in one course of action.

9/43 6.3 MEASURES OF INVESTMENT

(a) Payback measures "cash availability and risk" but fails to consider the savings after the payback period or the time value of money.

(b) SRI fails to consider horizon or time value of money.

(c) Net Present Value (NPV) includes all these factors and may be rigorously computed once the assumptions are agreed.

(d) DCF does not "decide", it merely provides a quantitative measure towards good intuitive decision making.

6/44 6. 5 PROJECT B

The CIA Worksheet indicates:

Measure of Investment Amount Standard Decision

Payback 4,4 yrs. 3 yrs. No SRI 23% 20 % Yes NPV -6 0 or + No

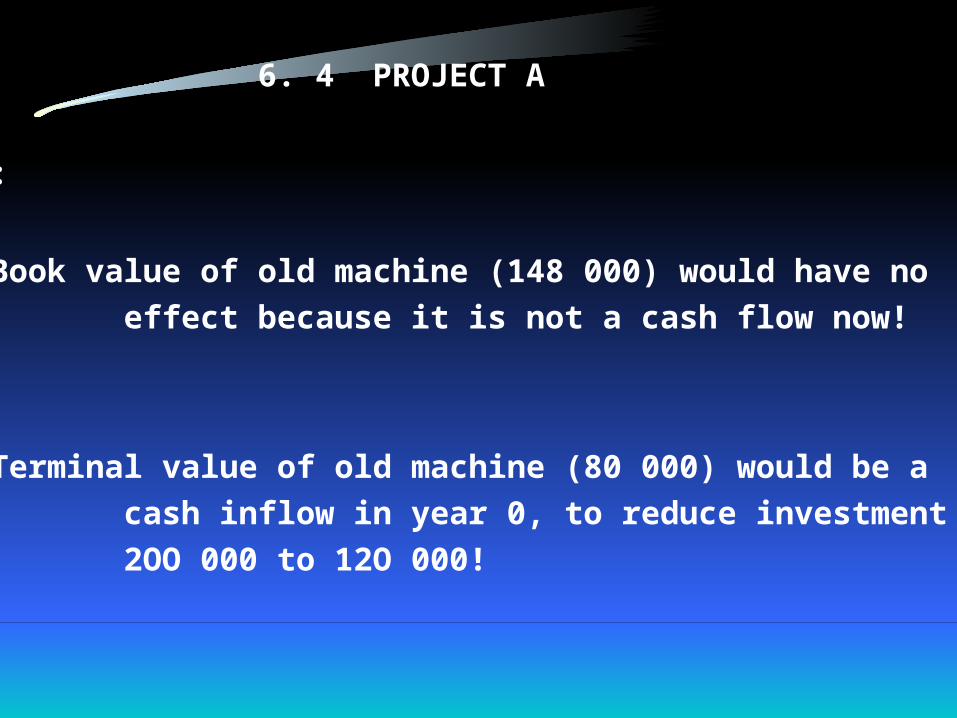

6/45 6. 4 PROJECT A

NOTE:

(a) Book value of old machine (148 000) would have no effect because it is not a cash flow now!

(b) Terminal value of old machine (80 000) would be a cash inflow in year 0, to reduce investment from 2OO 000 to 12O 000!

6/46 NOTES

(c) Annual deprecation is computed as new machine depreciation (2OO divided by 5 years) 40 , less the existing old machine depreciation (148 divided by 4 years) 36, to give Incremental Depreciation of 4. No effect of the final cash flow until we actually introduce taxes into the comutations!

6/47 6. 7 DECISION AND JUSTIFICATION

A purely quantitative analysis using the DCF Measure of NPV indicates the following decisions:

Project NPV DecisionA - 50 NoB - 5 NoC +30 Yes

subject, of course, to possible better alternatives, better opportunities and the usual non-quantitative factors.

An NPV of zero or more indicates an acceptable returnon investment above the discount (hurdle) rate.

6/48 6. 8 LEARNING POINTS

(a) CIA involves investment now (year 0) for benefits over the horizon (years 1-10).

(b) All CIA may be reduced to a cash profile of "cash in and cash out" over the horizon, brought to a present value by DCF.

(c) CIA assumptions are : investment, annual savings, horizon, tax rate, discount rate, and terminal values.

(d) Check assumptions before accepting any measures of investment.

6/48a

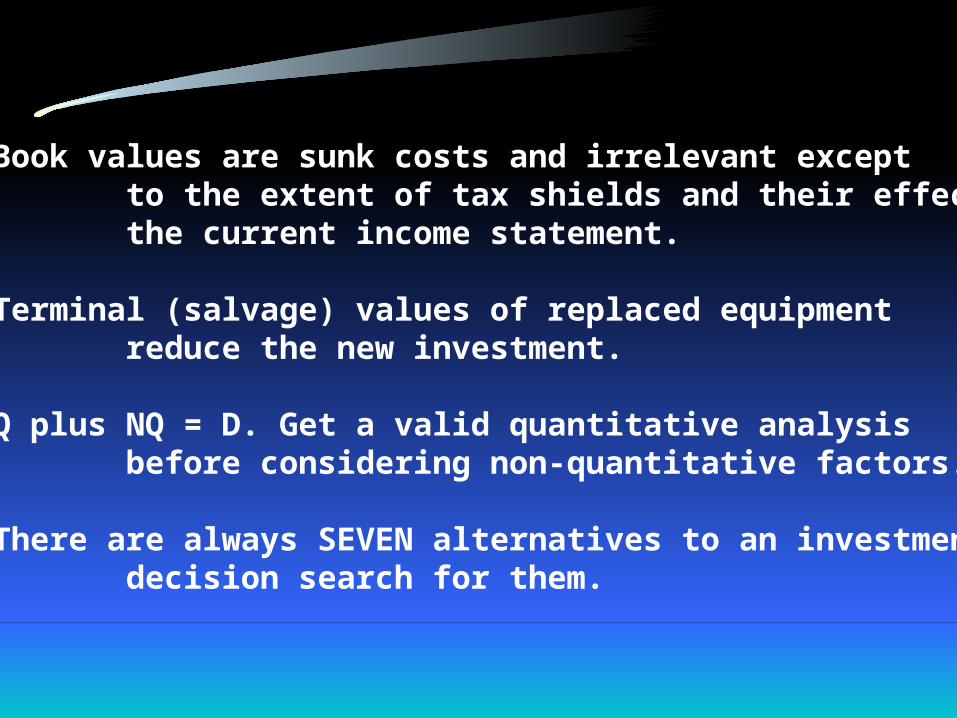

(e) Book values are sunk costs and irrelevant except to the extent of tax shields and their effect upon the current income statement.

(f) Terminal (salvage) values of replaced equipment reduce the new investment.

(g) Q plus NQ = D. Get a valid quantitative analysis before considering non-quantitative factors.

(h) There are always SEVEN alternatives to an investment decision search for them.

6/48b

(i) Payback is a crude measure of cash availability that ignores the time value of money.

(j) SRI is a crude measure which ignores the horizon.

(k) Net Present Value (NPV) should be zero or positive for the investment to be acceptable.

(l) Keep all calculations simple and don't pretend to be too "accurate" despite very broad assumptions.

(m) In a CIA Worksheet we set out the assumptions - the rest is simple arithmetic!

6/49 6.9a LEARNING PATTERNS

AA - ALTERNATIVE ANALYSIS

Buy or don't buy Machine A?

How many alternatives

I, 2, 3, 4, 5, 6, 7 ?

NOTE: Do it early to avoid the dreaded El.

6/50 6.9b INVESTMENT GROSS AND NET

New GROSS investment 200

Old machine:

Net Book Value now 160 Terminal Value now 100

New NET investment: (a) 200 ? (b) 460 ? (c) 260 ? (d) 100 ? Wait a moment … decide … then press … Not yet ... Answer: (d)

6/51 6.9c PAYBACK AND SRI

A B C

PB 100/20 PB 60/20 PB 40/20= 5 yrs. = 3 yrs. = 2 yrs.

SRI 20 % SRI 33% SRI 50 %

6/51 6.9c PAYBACK AND SRI

A B C

PB 100/20 PB 60/20 PB 40/20 = 5 yrs. = 3 yrs. = 2 yrs.

SRI 20 % SRI 33% SRI 50 %

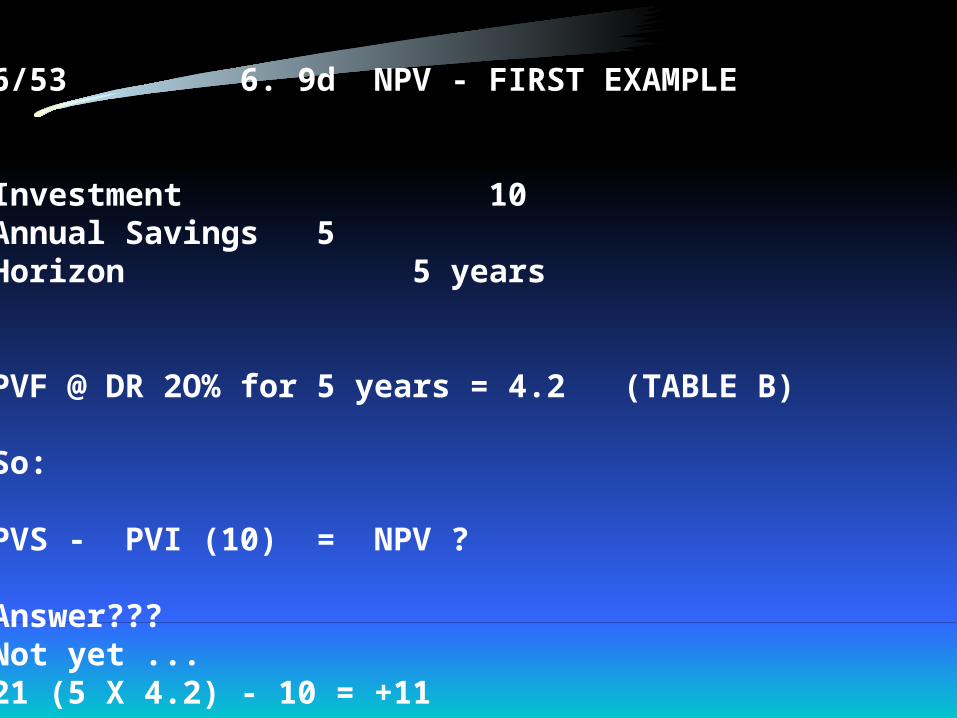

6/53 6. 9d NPV - FIRST EXAMPLE

Investment 10Annual Savings 5Horizon 5 years

PVF @ DR 2O% for 5 years = 4.2 (TABLE B)

So:

PVS - PVI (10) = NPV ?

Answer???Not yet ...21 (5 X 4.2) - 10 = +11

6/54 CIA ASSUMPTIONS

1. I 6. DR

2. S 7. OLD BV

3. H (key !!!) 8. OLD H

4. TV 9. OLD TV

5. TAX 10. SIMPLICITY!!!

6/55 CIA WORKSHEET - PROJECT B

ASSUMPTIONS:

Investment 40 Discount rate 20%Savings 9 Old machine BV now - Horizon - years 8 Old machine horizon now - Terminal value nil Old machine TV now -Tax Rate ignored

6/56 ANNUAL CASH FLOW

Annual savings 9

Less depreciation: New machine 40/8 years 5 Old machine / years Incremental depreciation 5 Taxable income 4Tax @ % -After tax income 4

Add back depreciation 5

Annual cash flow 9

6/56a LD MACHINE EFFECT ON NEW INVESTMENT

Old machine net book value now -

Less: old machine terminal value now -

Tax loss -

Old machine tax shield @ % -

Old machine terminal value now -

Toral reduction of the new investment in Year 0 -

6/57 6.9b CASH PROFILE

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 40 1.0 40

1-8 9 3.8 34

6/58 6.9h MEASURES OF INVESTMENT

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

40/9 4.4 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

9/40 X 100% 23% 20%

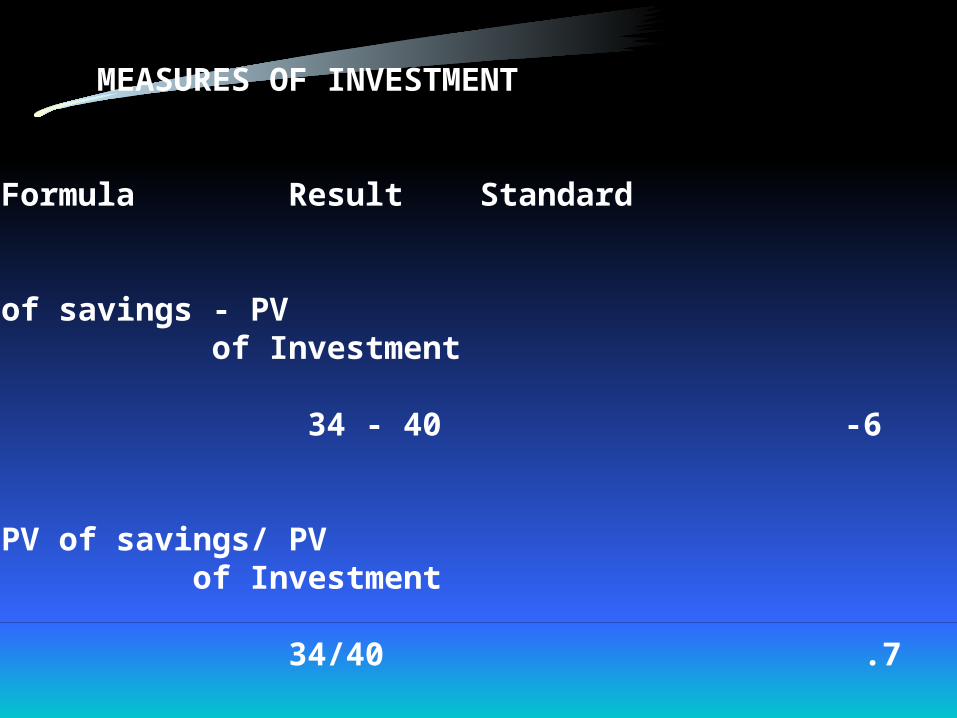

6/58a 6.9h MEASURES OF INVESTMENT

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

34 - 40 -6 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

34/40 .7 1.0 +

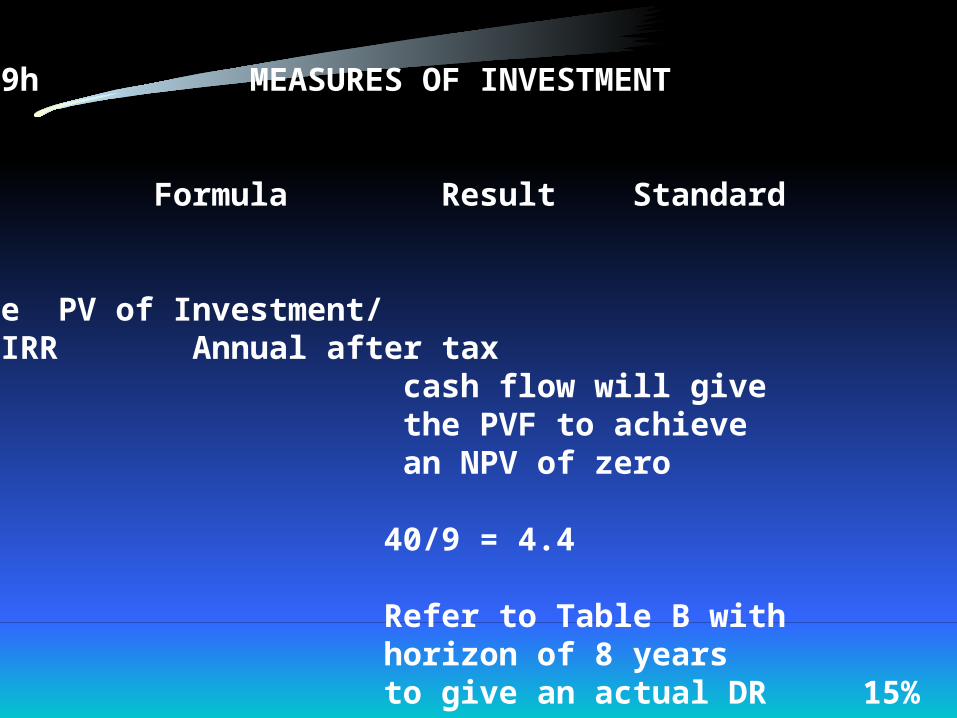

6/58b 6.9h MEASURES OF INVESTMENT

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

40/9 = 4.4

Refer to Table B with horizon of 8 years to give an actual DR 15% 20%

7.0 PROGRAM LEARNING

8.0 LECTURE

MEASURES OF INVESTMENT

6/59 8.0 LECTURE - MEASURES OF INVESTMENT

8.1 CAPITAL INVESTMENT DECISIONS

Good capital investment decisions are intuitive.

Depend upon quantitative Q and non-quantative data NQ.

DCF merely aids intuition.

6/60 8.2 DISCOUNT RATES

DCF is simply old fashioned Compound Interestcalculations, reduced to present value at the year 0with an interest (discount) rate.

The Discout Rate (DR is called the:

a. In vestment Opportunity Rate, or

b. Hurdle Rate, or

c. Minimum Rate of Return, or

d. Cost of Capital or the average rate of return on investment to achieve EVA (Economic Value Added)

6/60a DISCOUNT RATES

Note:

Setting the required discount rate is a key management decision.

Distinguish “Investment Decisions” - CIA

from

“Financing Decisions” - related to general financialmanagement of the company.

6/61 RELEVANT COST ANALYSIS

Define the investment decision carefully and select onlythe relevant cash flows.

Relevant cash flows:

a. Outflows - relevant costs, differential costs, incremental costs, oppoprtunity costs, new investment costs.

but not: sunk costs, book costs, fixed costs, exchange of cash for inventory or bank loans.

b. Inflows - contribution (sales less variable costs and taxes) cost reductions and terminal values

but not: net profits and not bank loans.

6/62 8.4 ALTERNATIVE ANALYSIS

Search for all alternatives before becoming emotionally involved in any particular investment or decision.

Do this at early stage of analysis.

Avoid "Emotional Investment".

6/63 8. 5 PFD - PROVISION FOR DISASTER

Before making a CIA decision make a PFD analysisinvestigating fully all possible outcomes which could destroy the value of the investment.

AA (Alternative Analysis) and PFD ensure that we analyse not just a "good alternative" but the "bestalternative" in the total environment.

6/63 8. 6 MEASURES OF INVESTMENT - NPV

Net Present Value measures the excess of savings over investment at present value (year 0).

If the NPV is equal to zero or greater the investment returns more than the required discount rate and the decision is YES.

6/64 8. 7 MEASURES OF INVESTMENT = PI

The Profitability Index measures the excess of savingsover investment in the form of an index number of plusor minus 1.

Profitability Index (PI): PVS/PVI

If the Profitability Index is greater than or equal to 1, thedecision is YES! Usefiul for comparing projects.

6/64 8. 8 MEASURES OF INVESTMENT - YIELD

The Yield or Internal Rate of Return measures the actual return (%) of the investment.

Yield is calculated by trial and error to find the discount rate which brings Net Present Value to zero.

Iif Yield (%) exceeds the required discount ("hurdle")rste, the investment decision is YES!

Yield is easily communicated to Management.

6/67 8.9 SIMPLE COMPUTATION OF YIELD

For an even cash flow the Yield may be simply computed:

Investment 1200Annual Cash Flow 400Horizon 5 years

Required PV Factor 1200/400 = 3,0

PV of Cash Flow 400 x 3, 0 = 1200Net Present Value (PVS - PVI) = 0

Table B gives a PVF of 3.0 for 5 years at. 20 %

Therefore the Yield of an Investment of 1200 with Annual Cash Flow 400 over Horizon 5 years is ... 20%

6/68 8.10 MEASURES OF INVESTMENT - RELATED

(a) Payback measures net investment against annual savings.

(b) Simple return on investment is useless.

(c) DCF returns are related to a discount rate and horizon:

PVS PVI = NPV PVS PVI = Pi If NPV = 0

then the discount rate is the same as the Yield

6/69 8.11 THE DICH APPROACH TO CIA

Think abouteach CIA problem in terms of:

D - Decision and CriteriaI - InvestmentC - Cash FlowH - Horizon and Terminal Values

NOTE: Remember also : NQ factors of short and long term planning, policy, government and politicalinfluences, liquidity, infleucne on current net profit,and better opportunities in the future,which may be more important than the Q!

6/70 8.12a LEARNING PATTERNS

DISCOUNT RATES

Financing InvestmentDecisions Decisions

CIA Hurdle Rate Cost of Capital Investment Opportunity Rate

Equity ? Go or No Go ?Debt ?

6/71 8.12b RELEVANT CASH PROFILE

OUT - COSTS IN - CONTRIBUTIONS

RELEVANT:

Variable Incremental RevenueSalvage Less: Variable cost Differential taxes = ContributionOpportunity Cost reductions

NOT RELEVANT

Sunk LoansFixed Other

6/72 8.l2c DCF MEASURES OF INVESTMENT

PVS - PVI = NPV

PVS/PVI = PI

YIELD IS THE DISCOUNT RATE …

WHICH MAKES PVS - PVI = 0

6/73 8.12d PVS - PVI = NPV

DR PVI PVS NPV

30 % 10 3 -7 25 % 10 7 -3 20 % 10 10 0 NPV 0 15 % 10 14 +3 10 % 10 17 +7 NPV ++

NOTE: What is the YIELD?

Not yet ...

Answer: 10%

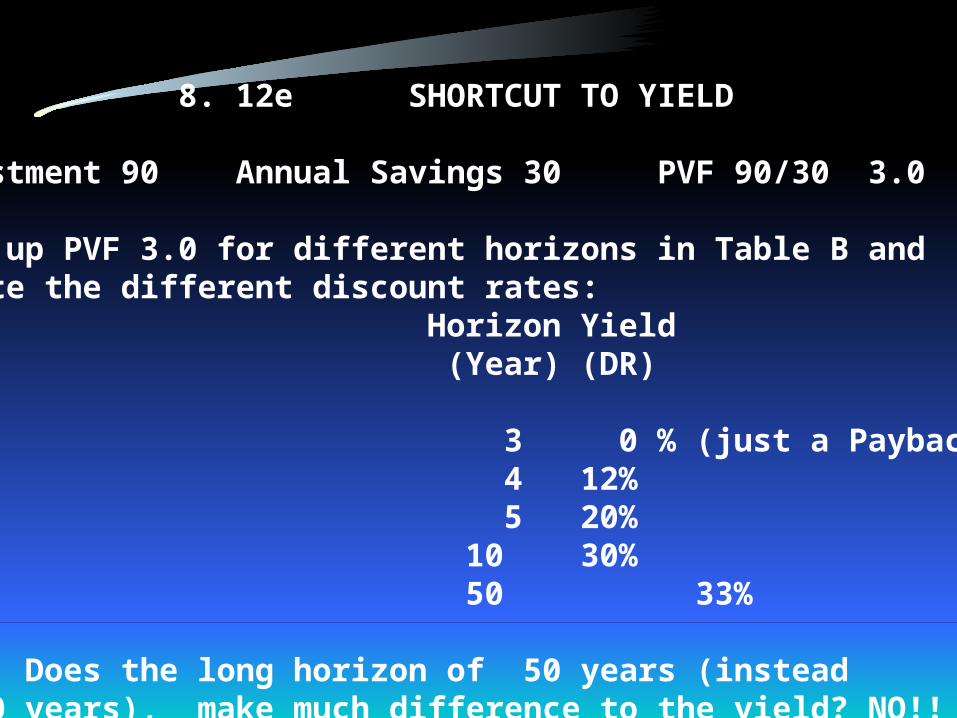

6/74 8. 12e SHORTCUT TO YIELD

Investment 90 Annual Savings 30 PVF 90/30 3.0

Look up PVF 3.0 for different horizons in Table B andlocate the different discount rates: Horizon Yield (Year) (DR)

3 0 % (just a Payback) 4 12% 5 20% 10 30% 50 33%

NOTE: Does the long horizon of 50 years (insteadof 10 years), make much difference to the yield? NO!!

6/75 8.12f DCF MEASURES RELATED

IF PVS = PVI THEN WHAT IS:

NPV ? PI ? YIELD ?

Answers coming ...Not yet ...

Answers: 0, 1, same as DR

6/76 6.9b CASH PROFILE

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 20 1.0 20

1-10 3 4.2 13

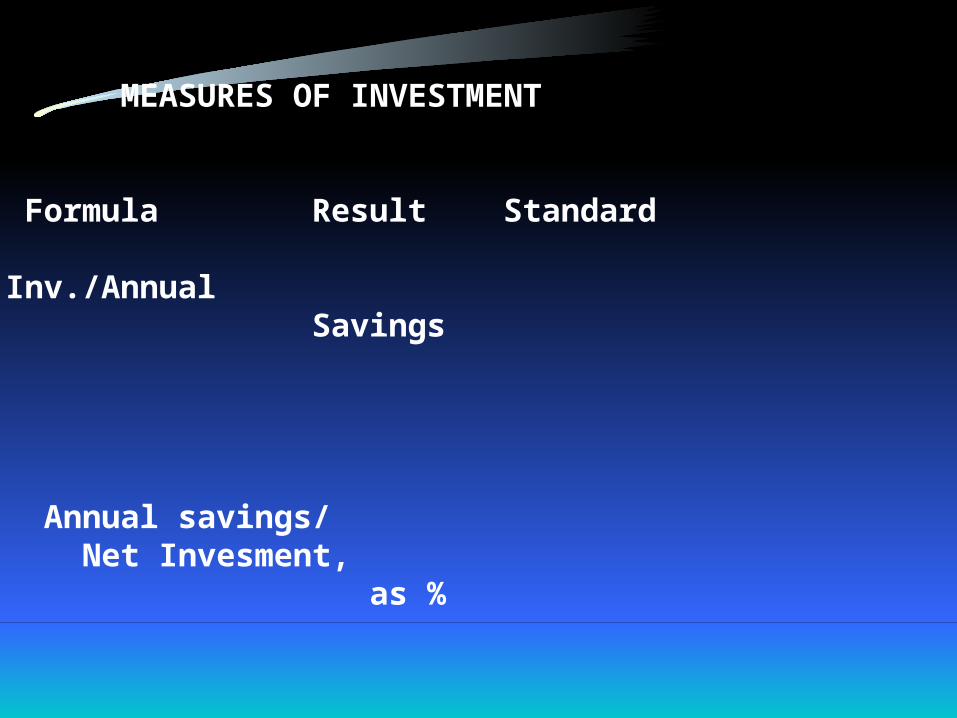

6/76a 8.12g CASH PROFILE

Year Cash PV Factor PV Cash Out I n @ 8% Out In

0 20 1.0 20

1-10 3 6.6 20

6/77 8.12g MEASURES OF INVESTMENT

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

20%

6/77a 8.12g MEASURES OF INVESTMENT

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

13 -20 -7 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

13/20 .7 1.0 +

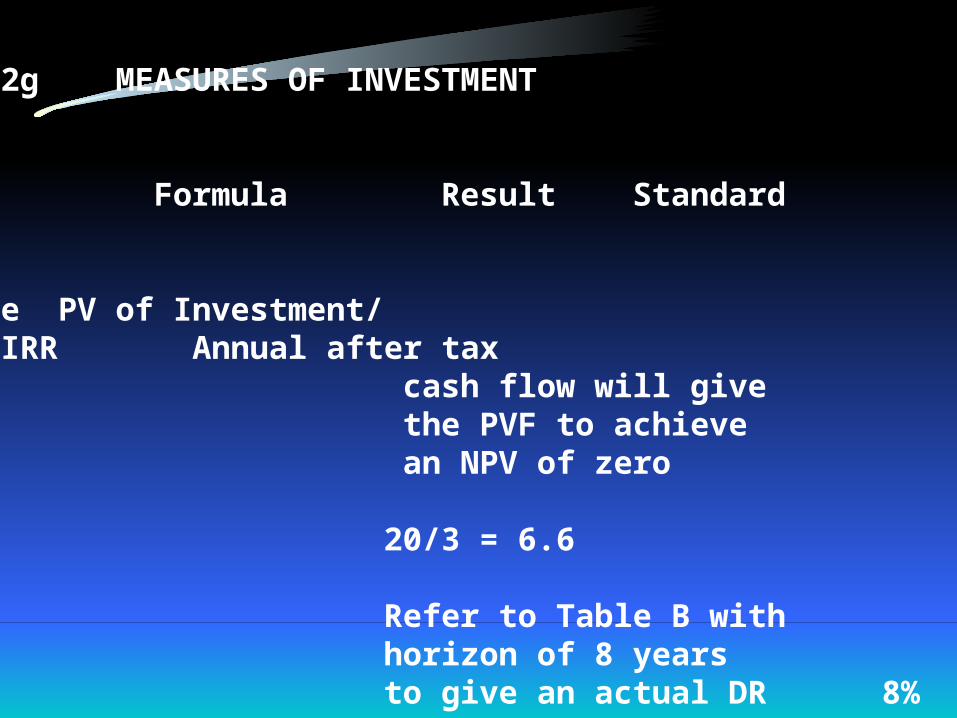

6/77b 8.12g MEASURES OF INVESTMENT

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

20/3 = 6.6

Refer to Table B with horizon of 8 years to give an actual DR 8% 20%

9.0 CASE STUDY

10.0 LECTURE

ON THE CASE

6/78 10. 0 - LECTURE - SPECIAL SUPPLY COMPANY

10.1 STORY OF THE CASE

Controller of company with liquidity crisis, must set

coming year's capital budget for Product Group X

carefully, by choosing alternative proposals to meet

the 100 000 limit.

6/79 10.2 NON-QUANTITANVE FACTORS

Non-quantitative factors to be considered in the capital Budget include:

- short and long term company planning

- government and political influences

- reliability of underlying assumptions

- all other alternatives

- postponement of projects to take better opportunities in the future

- immediate liquidity crisis

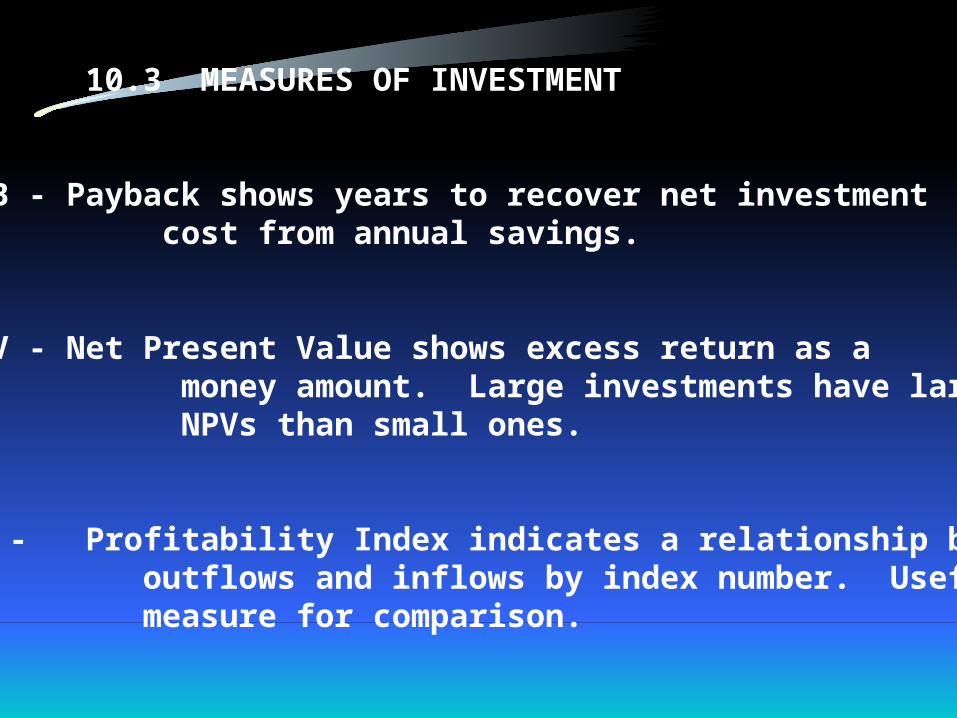

6/80 10.3 MEASURES OF INVESTMENT

(a) P B - Payback shows years to recover net investment cost from annual savings.

(b) NPV - Net Present Value shows excess return as a money amount. Large investments have larger NPVs than small ones.

(c) PI - Profitability Index indicates a relationship between outflows and inflows by index number. Useful measure for comparison.

6/80a 10.3 MEASURES OF INVESTMENT

(d) YIELD - Is the Internal Rate of Return expressed as a %.

(e) SRI - Simple Return on Investment could be computed in too many different ways - useless!

NOTE: Overall we prefer Payback and Yield for easy communication to Management although PI could be useful for comparison too!

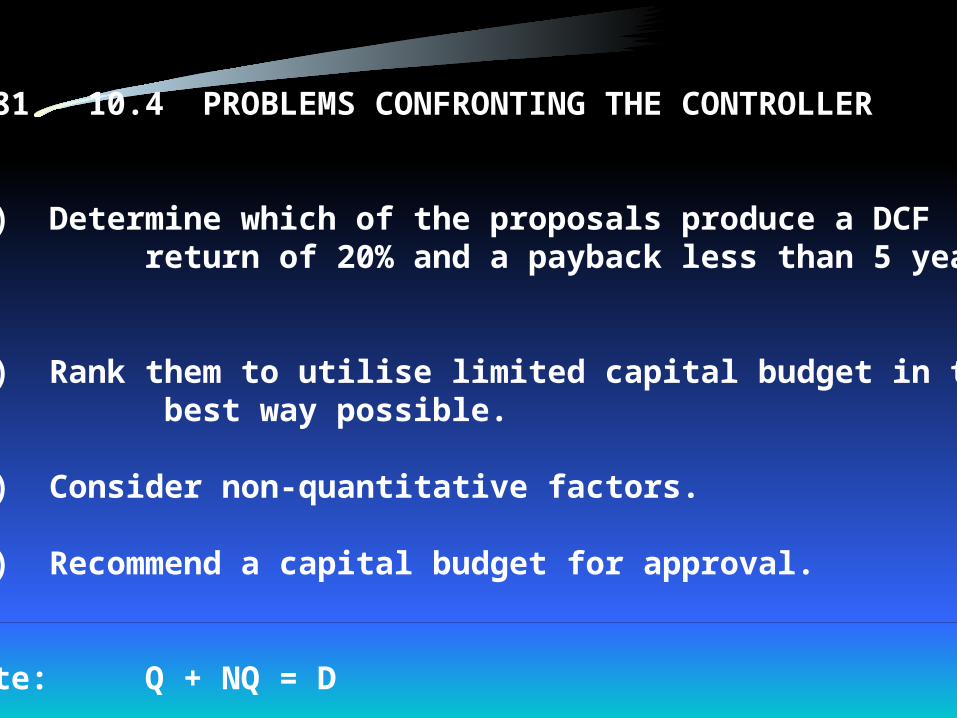

6/81 10.4 PROBLEMS CONFRONTING THE CONTROLLER

(a) Determine which of the proposals produce a DCF return of 20% and a payback less than 5 years.

(b) Rank them to utilise limited capital budget in the best way possible.

(c) Consider non-quantitative factors.

(d) Recommend a capital budget for approval.

Note: Q + NQ = D

6/82 CIA ERRORS IN PROJECT 2

Three errors of CIA in Project 2 were:

(a) Net Investment 70 not 100, because new investment reduced by the terminal value of the old machine 30.

(b) Cash Flow 30 (not 50) because fixed costs not relevant cash flow.

(c) PVF at discount rate 20 % for 10 years is 4. 2 not 3. 0.

NOTE: See CIA revised Worksheet.

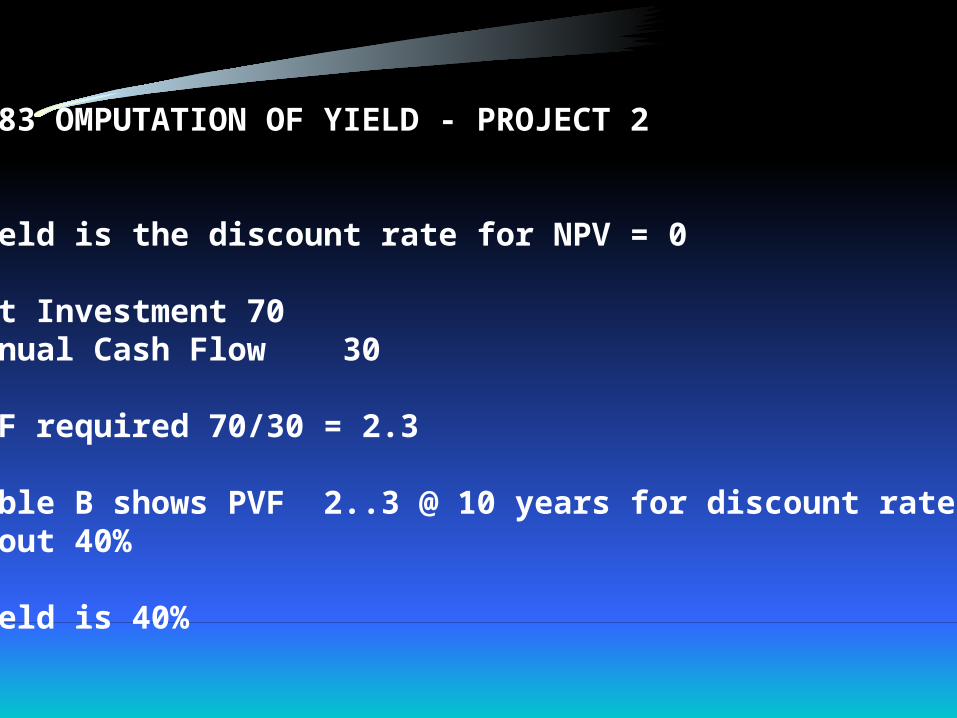

6/83 OMPUTATION OF YIELD - PROJECT 2

Yield is the discount rate for NPV = 0

Net Investment 70Annual Cash Flow 30

PVF required 70/30 = 2.3

Table B shows PVF 2..3 @ 10 years for discount rateabout 40%

Yield is 40%

6/84 10.7 DECISION AND JUSTIFICATION

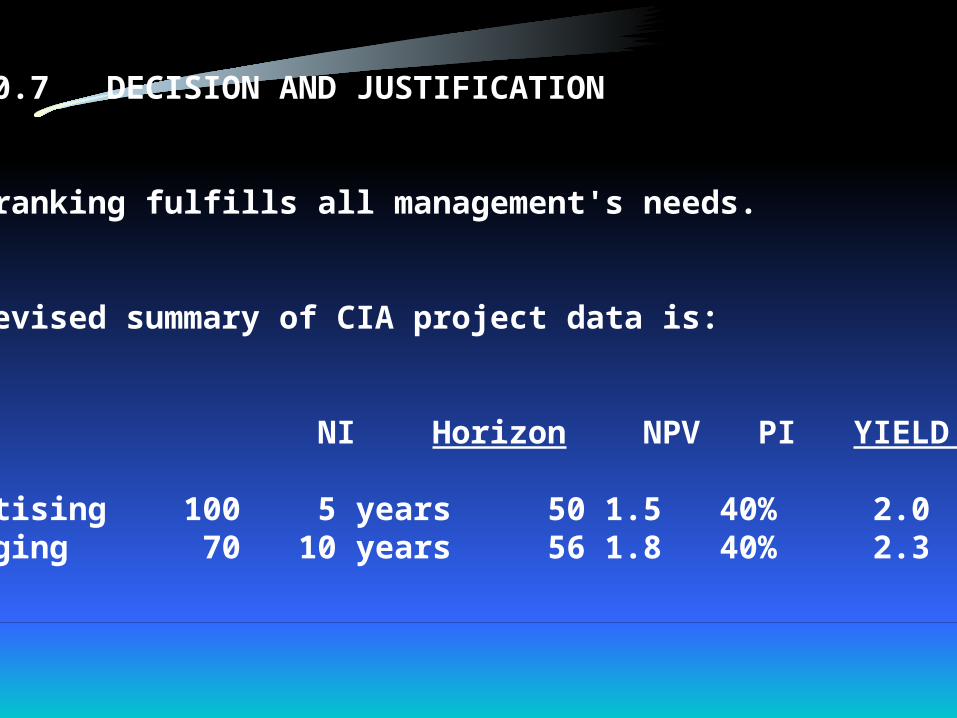

(a) No ranking fulfills all management's needs.

(b) A revised summary of CIA project data is:

Project NI Horizon NPV PI YIELD PB

1. Advertising 100 5 years 50 1.5 40% 2.02. Packaging 70 10 years 56 1.8 40% 2.3

6/84a 10.7 DECISION AND JUSTIFICATION

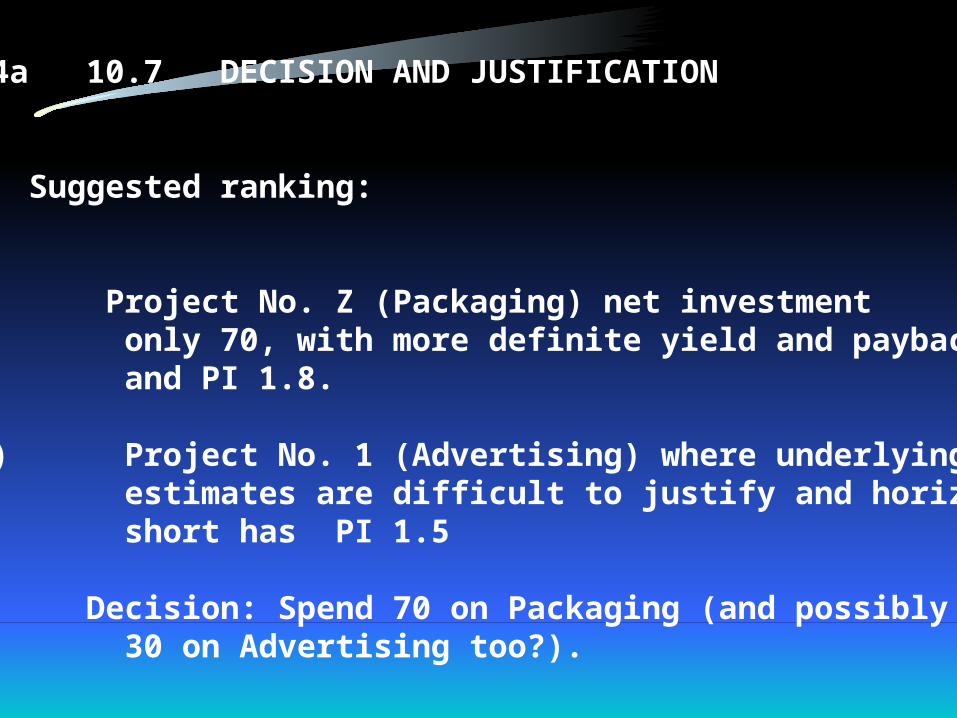

(c) Suggested ranking:

(i) Project No. Z (Packaging) net investment only 70, with more definite yield and payback, and PI 1.8.

(ii) Project No. 1 (Advertising) where underlying estimates are difficult to justify and horizon short has PI 1.5

(d) Decision: Spend 70 on Packaging (and possibly 30 on Advertising too?).

6/85 10.8 LEARNING POINTS

(a) Strategic and other NQ factors may be more important than Q features of a CIA project.

(b) Ranking of CIA projects depends on both Q and NQ factors.

(c) Payback indicates cash availability but fails to consider DCF and the full horizon and terminal values.

(d) Net Present Value should be zero or positive - large investments tend to have large NPVS.

6/85a 10.8 LEARNING POINTS

(e) Yield that should exceed "hurdle" rate; it is simple and communicates well to management.

(f) Profitability index provides useful comparative data of outflow to inflow.

(g) Book value of replaced equipment is a sunk cost but the terminal value reduces the new investment.

(h) Fixed costs are not usually relevant cash flows.

6/85b 10.8 LEARNING POINTS

(i) Excessive accuracy in CIA is misleading; work only in 000’s.

(j) CIA involves assumptions followed by systematic analysis.

(k) DICH - Decision and Criteria, Investment, Cash Flow, Horizon and Terminal Values followed by Cash Profile and Measures of Investment.

(l) Liquidity problems influence management to prefer short term payback to long term profitability.

6/86 10.9a NQ FACTORS

Long term PlanningCapital BudgetsProfit Levels this year - will they be critical to survival?StrategyPersonal FactorsRisky AssumptionsLawManagement ValuesPast HistoryEconomy and Social FactorsLiquidityGovernment RelationsOrganisationSub-optimization etc.

6/87 10.9b LEARNING PATTERNS

SUNK COSTS AND RELEVANT COSTS

Past Future

Sunk & Book Variable & Opportunity Values Costs

NOT RELEVANT RELEVANT

6/88 10.9c YIELD COMPUTATION

NET INVESTMENT 70

Annual After Tax Cash Flow 30

PVF REQUIRED 70/30 = 2. 3

In Table B, look up for the 10 year horizon to finda PVF of 2.3 … and see a yield of 40%

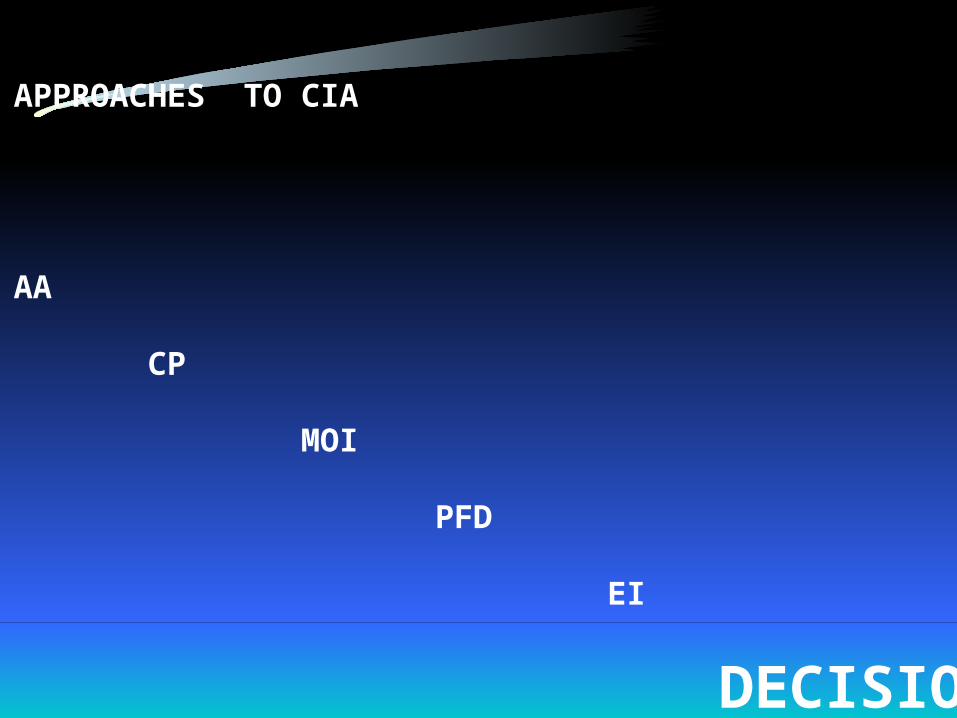

6/89 10.9d APPROACHES TO CIA

DICH

AA

CP

MOI

PFD

EI

DECISION

6/90 10.9c MEASURES FOR RANKING INVESTMENTS

FOR RANKING TOOL AGAINST Easy PVS - PVI = NPV Definite AN AMOUNT Larger I gives Value larger NPV?

Definite PVS/PVI=PI Relates input AN INDEX Materiality? to output

6/91 10.9c OTHER MEASURES FOR RANKING INVESTMENTS

FOR RANKING TOOL AGAINST

Return YIELD Reinvestment?Communication AN INDEX Materiality?

Communication PAYBACK DCF?Cash Recovery NO. OF YEARS Horizon?Liquidity

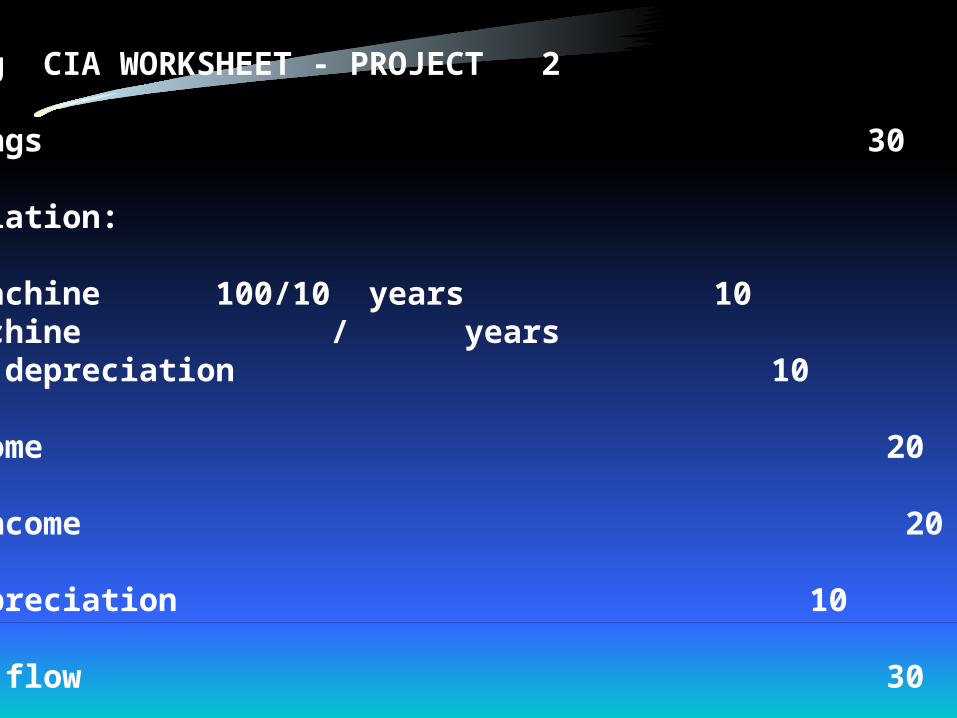

6/92 10.9g CIA WORKSHEET - PROJECT 2

ASSUMPTIONS:

Investment 100 Discount rate 20%Savings 30 Old machine BV now - Horizon - years 10 Old machine horizon now - Terminal value nil Old machine TV now 30Tax Rate ignored

6/93 10.9g CIA WORKSHEET - PROJECT 2

Annual savings 30

Less depreciation: New machine 100/10 years 10 Old machine / years Incremental depreciation 10 Taxable income 20Tax @ % -After tax income 20

Add back depreciation 10

Annual cash flow 30

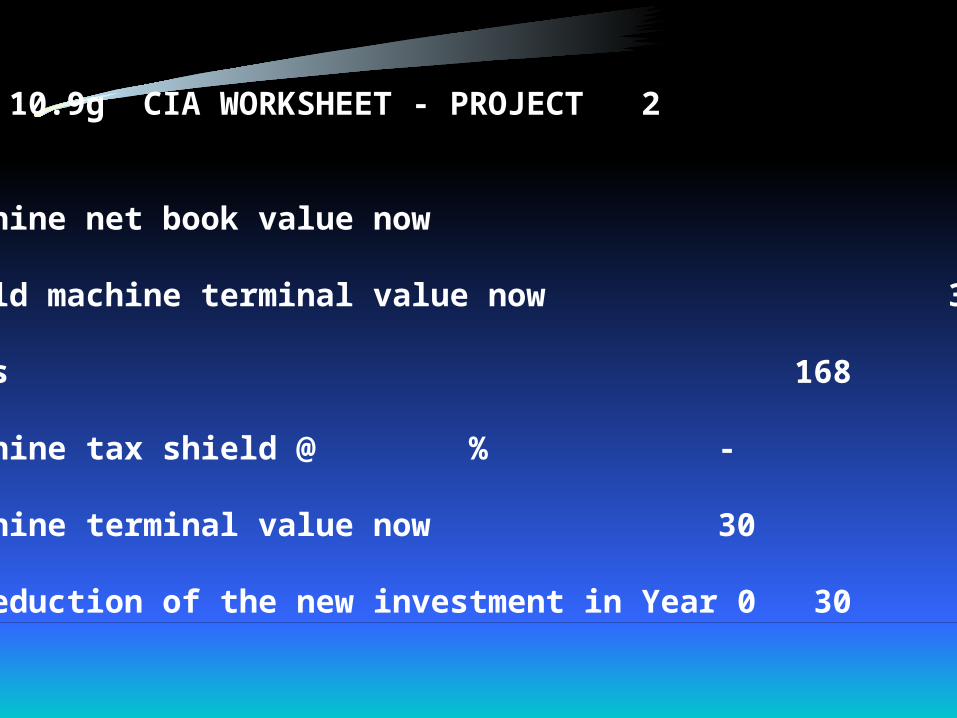

6/93a 10.9g CIA WORKSHEET - PROJECT 2

Old machine net book value now 198

Less: old machine terminal value now 30

Tax loss 168

Old machine tax shield @ % -

Old machine terminal value now 30

Toral reduction of the new investment in Year 0 30

6/94 10.9g CIA WORKSHEET - PROJECT 2

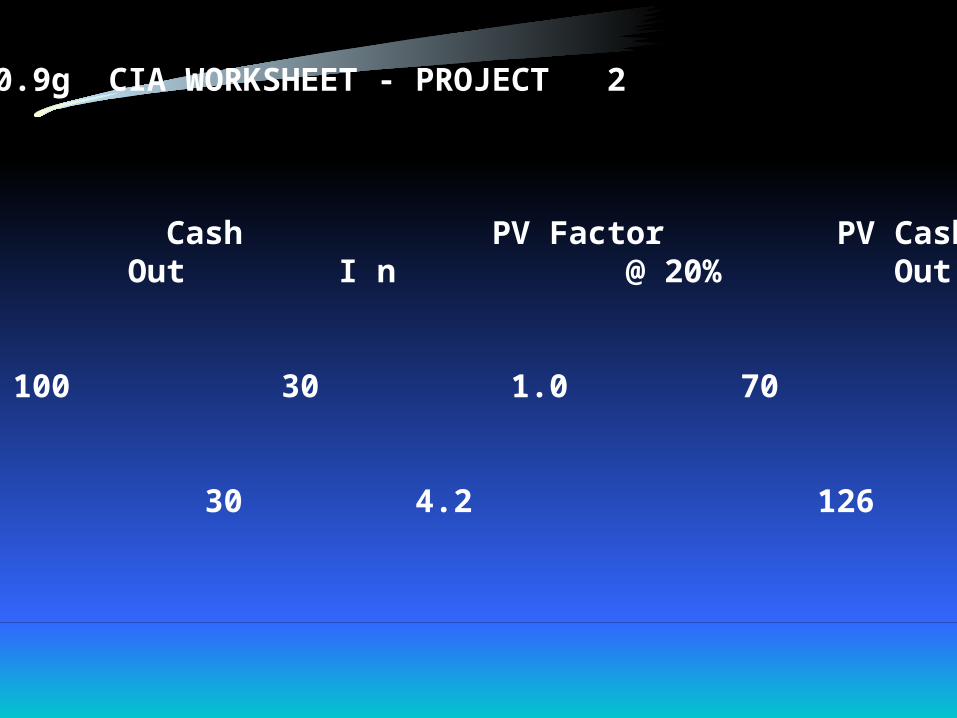

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 100 30 1.0 70

1-10 30 4.2 126

6/95 10.9g CIA WORKSHEET - PROJECT 2

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

70/30 2.3 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

30/70 X 100% 43% 20%

6/95a 10.9g CIA WORKSHEET - PROJECT 2

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

126-70 56 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

126/70 1.8 1.0 +

6/95c 10.9g CIA WORKSHEET - PROJECT 2

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

70/30 = 2.3

Refer to Table B with horizon of 8 years to give an actual DR 40% 20%

11.0 SUMMARY LECTURE

FOR PART I

(HOORAY)

6/96 11.0 SUMMARY LECTURE FOR PART I

11.1 INVESTMENT

Cash Flow in and out for:

Machinery, Land, Buildings, Research and Development,Training, Advertising, Shares, Inventory, Receivables etc., etc., etc.

Invest now (Year 0) for benefit later (years 1-10) plus.

6/97 11.2 JARGON

CIA - Capital Investment AnalysisDCF - Discounted Cash FlowI - InvestmentPV - Presemt Value (Year 0)PVI - PV Investment (Year 0)PVS - PV Savings (Years 1-5

reduced to Year 0)

PYF - PV Factor (0,0)PB - Payback (Years)TV - Terminal ValueS - Savings (Years 1-5)H - Horizon (Years)

6/97a 11.2 JARGON

COC - Cost of CapitalEVA - Economic Value AddedSVA - Share Vakue Added

BT - Before TaxAT - After Tax

DR - Discount Rate (%)ROI - Return on Investment (%)BOR - Borrowing Opportunity Rate (%)IOR - Investment Opportunity Rate (%)NPV - Net Present Value (Year C)PI - Profitability Index

Yield - Internal Rate of Return

6/98 113 CAPITAL INVESTMENT

(a) JustificatioN:

Law Policy Economics (apply CIA)

(b) Types of Decisions: New projects - Go or No Co? Mutually Exclusive ProjeCtS - choose A or B? Capital Rationing - choose A B C D E or F - fit a limited budget? Replacement - replace C with D?

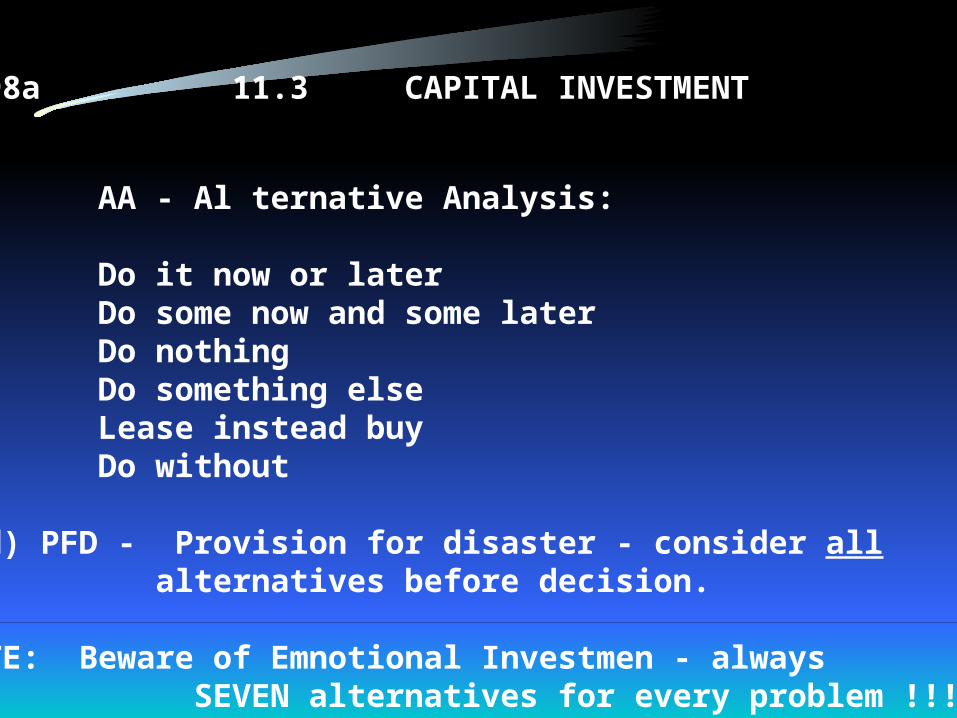

6/98a 11.3 CAPITAL INVESTMENT

© AA - Al ternative Analysis:

Do it now or later Do some now and some later Do nothing Do something else Lease instead buy Do without

(d) PFD - Provision for disaster - consider all alternatives before decision.

NOTE: Beware of Emnotional Investmen - always SEVEN alternatives for every problem !!!

6/99 11.4 RELEVANT CASH FLOWS

Specify the decision very carefully.

Ignore sunk costs and fixed costs.

Include only those cash flows that change with thedecision, such as:

variable, incremental, differentail and opportunity costs, that ...: “Ring or could ring, the cast register".

Compute cash profiles (cash in and out).

6/100 11.5 CASH PROFILE

Year(a) Horizontal Form 0 1 2 3

Investment 1000 Savings 400 400 400

(b) Vertical Form Year In Out Investment 0 1000 Savings 1-3 400

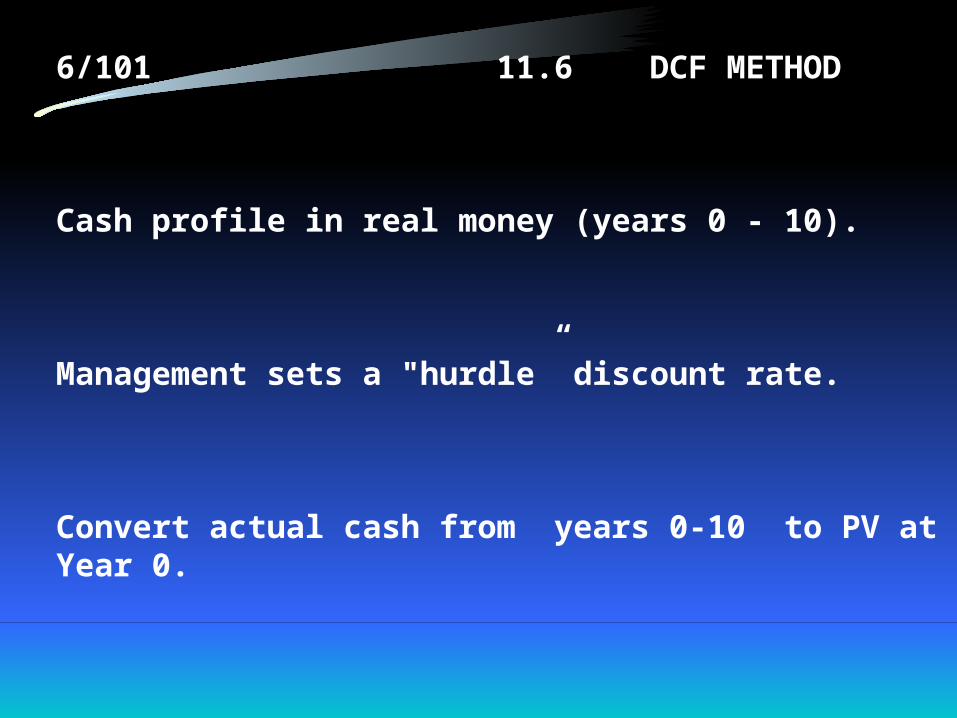

6/101 11.6 DCF METHOD

Cash profile in real money (years 0 - 10).

Management sets a "hurdle” discount rate.

Convert actual cash from years 0-10 to PV at Year 0.

6/101a 11.6 DCF METHOD

NOTE:

The Hurdle Rate" or Investment Opportunity Rate isset by complex analysis of the average "Cost of Capital"of the business.

It is a key decision worthy of the highest level of management expertise. What rate does your company use? Why?

Investments which yield above the CoC increase the company value and thus achieve … EVA … and … hopefully … SVA.

6/102 11.7 MEASURES OF INVESTMENT

Measure Result

Payback (I/AS) years

NPV (PVS - PY!) + cash

PI (PVS/PVI) index 1 or more

Yield (NPV = 0) % return

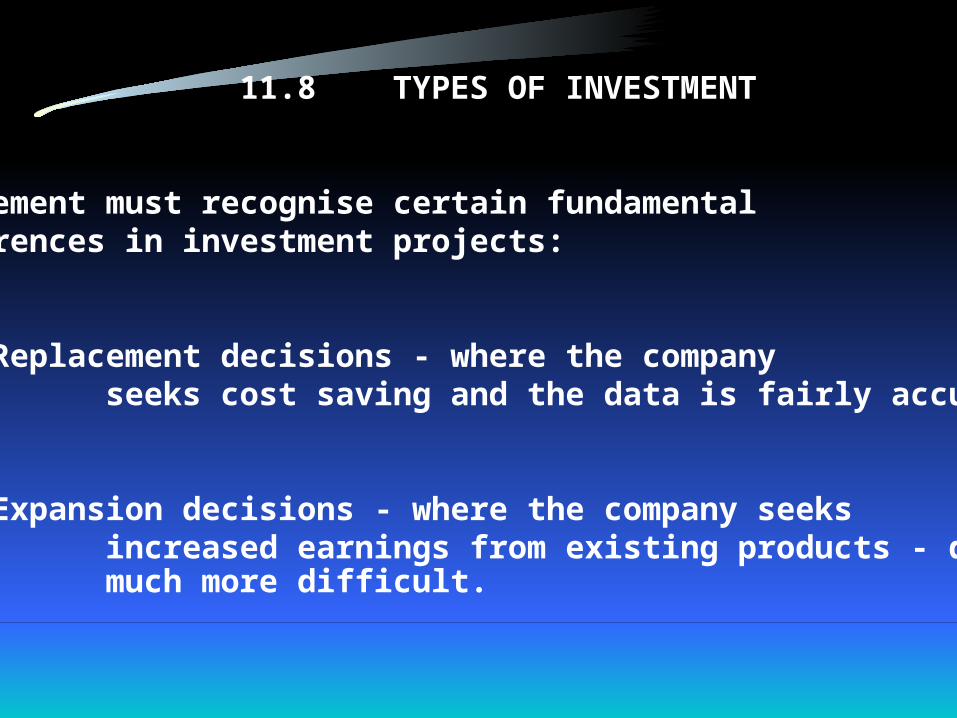

6/103 11.8 TYPES OF INVESTMENT

Management must recognise certain fundamentaldifferences in investment projects:

(a) Replacement decisions - where the company seeks cost saving and the data is fairly accurate.

(b) Expansion decisions - where the company seeks increased earnings from existing products - data much more difficult.

6/103a 11.8 TYPES OF INVESTMENT

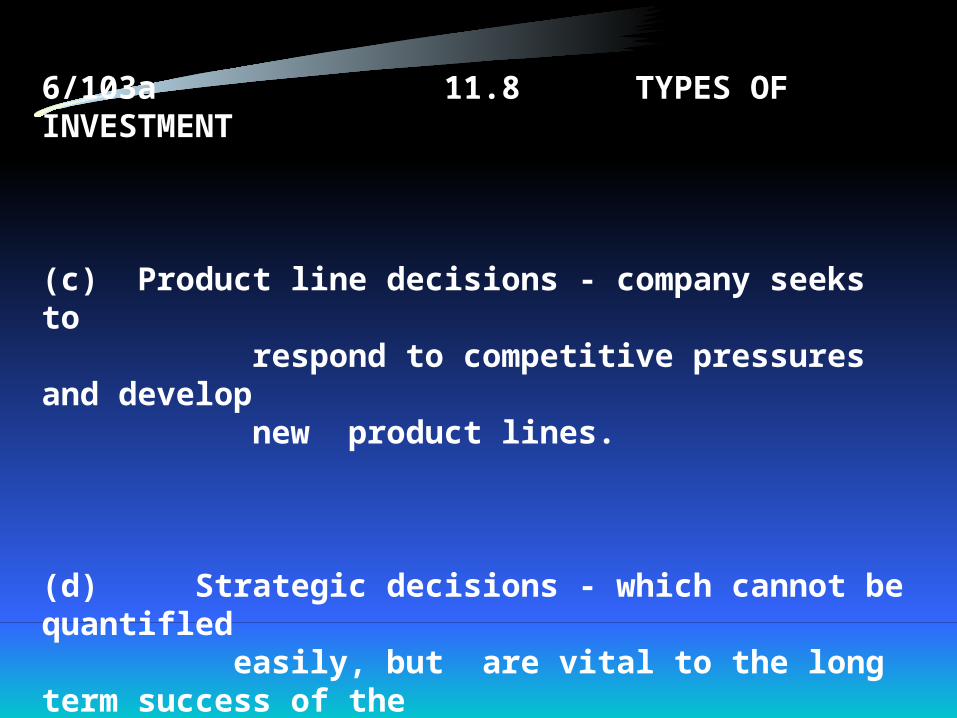

(c) Product line decisions - company seeks to respond to competitive pressures and develop new product lines.

(d) Strategic decisions - which cannot be quantifled easily, but are vital to the long term success of the company.

NOTE: Therefore CIA depends more on NQ than Q.

6/104 11.9 DICH

D - Decision and Criteria

I - Investment

C - Cash Flow - in and out)

H - Horizon and Terminal Value

followed by: Cash Pofiles and Measures of Investment.

6/105 11.10 OVERALL

Good capital investment decisions are intuitive.

Depend mainly upon non-quantitative factors.

DCF and quantitative data is only an AID to goodbusiness intuition.

Do AA (alternative analysis) and PFD (provision fordisaster) early enough to avoid emotional investrnentin a poor alternative!

Don't apply DCF to small investments and don't tryj to be too “pseudo accurate”.

6/106 11.11 CIA WORKSHEET - BEFORE TAX

ASSUMPTIONS:

Investment 200 Discount rate 20%Savings 60 Old machine BV now 168 Horizon - years 5 Old machine horizon now 11 Terminal value nil Old machine TV now -Tax Rate ignored

6/107 11.11 CIA WORKSHEET - BEFORE TAX

Annual savings 60

Less depreciation: New machine 200/5 years 40 Old machine 168 /11 years 15 Incremental depreciation 25 Taxable income 35Tax @ % -After tax income 35

Add back depreciation 25

Annual cash flow 60

6/107a 11.11 CIA WORKSHEET - BEFORE TAX

Old machine net book value now 168

Less: old machine terminal value now -

Tax loss 168

Old machine tax shield @ % -

Old machine terminal value now -

Total reduction of the new investment in Year 0 -

6/108 11.11 CIA WORKSHEET BEFORE TAX

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 200 1.0 200

1-5 60 3.0 180

6/109 11.11 CIA WORKSHEET - BEFORE TAX

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

200/60 3.3 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

60/200 X 100% 30% 20%

6/110 11.11 CIA WORKSHEET - BEFORE TAX

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

180-200 -20 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

180/200 .9 1.0 +

6/109a 11.11 CIA WORKSHEET - BEFORE TAX

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

200/60 = 3.3

Refer to Table B with horizon of 5 years to give an actual DR 15% 20%

6/110 11.11 CIA WORKSHEET - AFTER TAX

ASSUMPTIONS:

Investment 200 Discount rate - after tax 10%Savings 60 Old machine BV now 168 Horizon - years 5 Old machine horizon now 11 Terminal value nil Old machine TV now -Tax Rate 50%

6/111 11.11 CIA WORKSHEET - AFTER TAX

Annual savings 60

Less depreciation: New machine 200/5 years 40 Old machine 168 /11 years 15 Incremental depreciation 25 Taxable income 35Tax @ % 17After tax income 18

Add back depreciation 25

Annual cash flow 43

6/111a 11.11 CIA WORKSHEET - AFTER TAX

Old machine net book value now 168

Less: old machine terminal value now -

Tax loss 168

Old machine tax shield @ 50 % 84

Old machine terminal value now -

Total reduction of the new investment in Year 0 84

6/112 11.11 CIA WORKSHEET - AFTER TAX

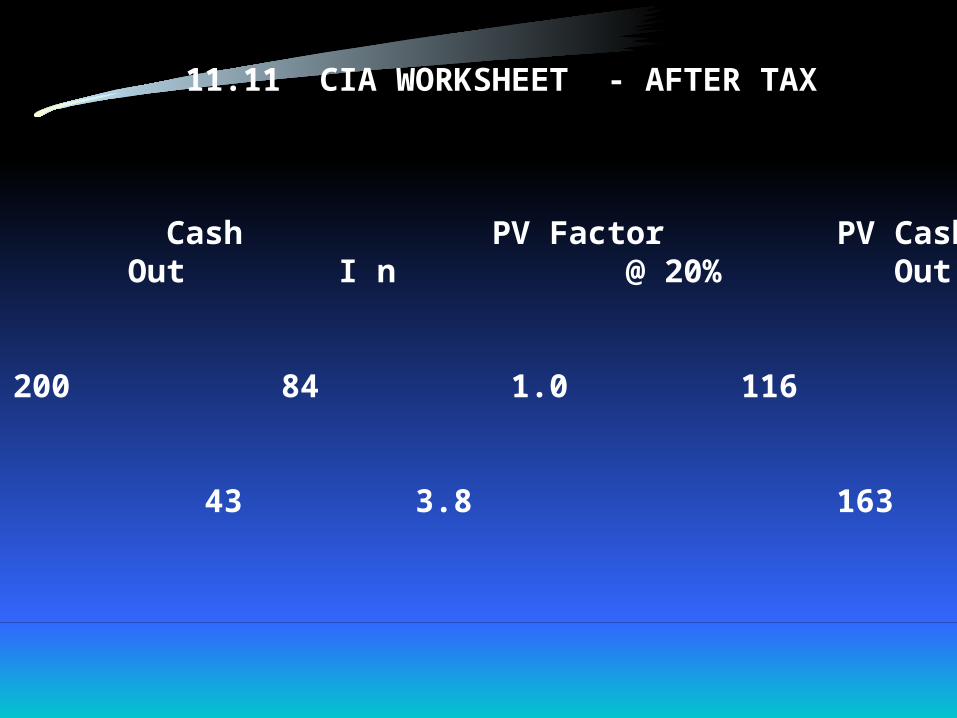

Year Cash PV Factor PV Cash Out I n @ 20% Out In

0 200 84 1.0 116

1-10 43 3.8 163

6/113 11.11 CIA WORKSHEET - AFTER TAX

Measure Formula Result Standard

Payback - PB Net Inv./Annual Savings

200/60 3.3 years 3 years

Simple Return Annual savings/ on InvestmentI Net Invesment,- SRI as %

60/200 X 100% 30% 20%

6/113a 11.11 CIA WORKSHEET - AFTER TAX

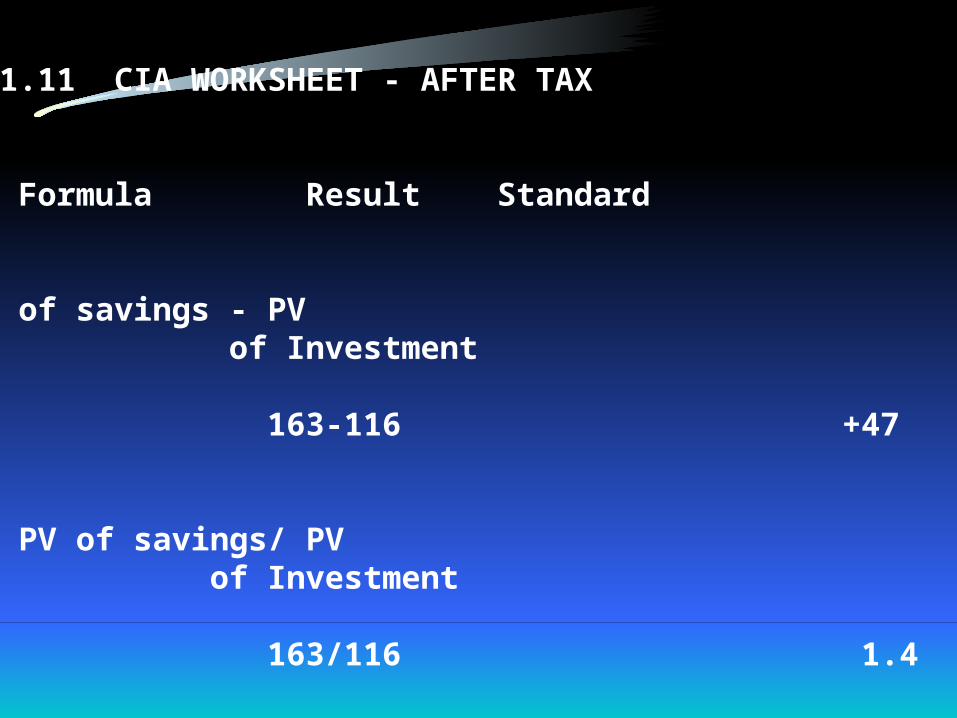

Measure Formula Result Standard

Net PresntVakue - NPV PV of savings - PV of Investment

163-116 +47 zero or +

ProfitabilityIndex - PI PV of savings/ PV of Investment

163/116 1.4 1.0 +

6/114 11.11 CIA WORKSHEET - AFTER TAX

Measure Formula Result Standard

YieldInternal Rate PV of Investment/of Return - IRR Annual after tax cash flow will give the PVF to achieve an NPV of zero

116,43 = 2.7

Refer to Table B with horizon of 5 years to give an actual DR 25% 10%

6/116 11.11 LEARNING PATTERNS

JARGON

PV - PVI, PVS, NPV, PVF

CF - AT, I, ST, TV

% - DR, ROI, BOR, IOR, IRR, Y, COC

6/115a 11.11 LEARNING PATTERNS

AA & PFD

AA … 7 always 7 ...

EI

PFD - politics, death, delay, technology, economy

6/117 11.11 LEARNING PATTERNS

DECISIONS Investment decisions:

A Go or no go … ?

A or B Mutually exclusive …?

A B C Rationinbg out a limited budget …?

A for B Replacement … or not … now or later …?

Note: Distinguish investment from financing decisions … lease or buy …?

6/118 11.11 LEARNING PATTERNS

DEPRECIATIONNew investment:

Cost 1000Horizon 10 yearsDepreciation 100 p.a.

Old machine:

Net book value 600Reamaing horizon 10 years Depreciation 60 p.a.

Incrtemental depreciation which affects the tax onannual savings 40 p.a.

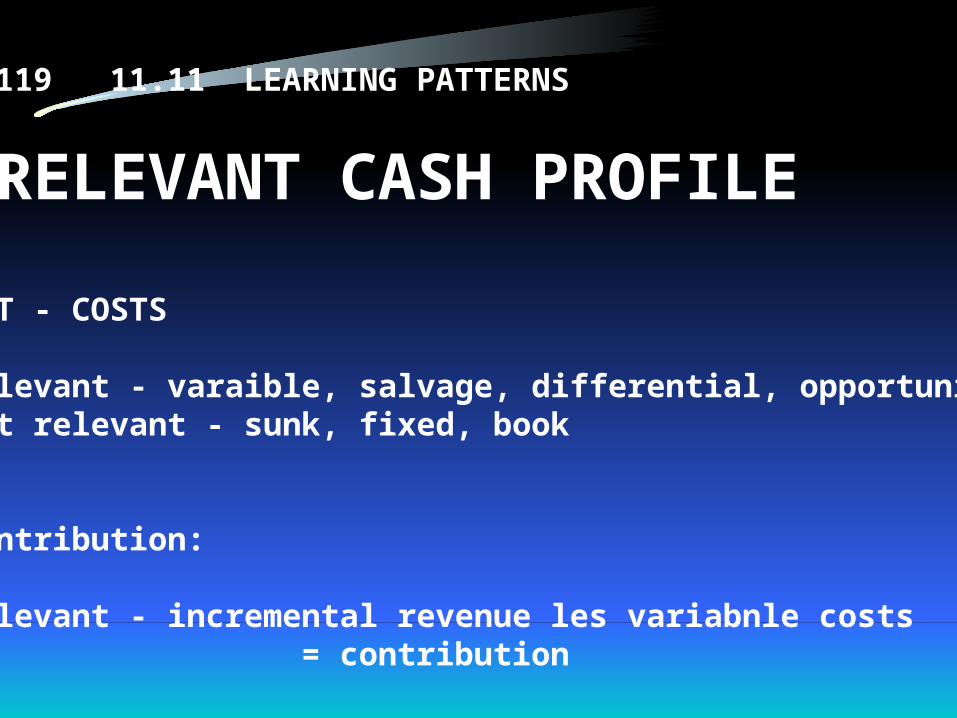

6/119 11.11 LEARNING PATTERNS

RELEVANT CASH PROFILE

OUT - COSTS

Relevant - varaible, salvage, differential, opportunityNot relevant - sunk, fixed, book

Contribution:

Relevant - incremental revenue les variabnle costs = contribution

6/120 11.11 LEARNING PATTERNS

DCF MEASURES

PVS - PVI = NPV

PVS/PVI = PI

PVS - PVI = 0 … at the Yield DR

6/1121 11.11 LEARNING PATTERNS

NPVDR NPV

30% negative25% negative20% zero15% positive10% positive

The Yield is … %?Not yetAnswer: 20%

6/122 11.11 LEARNING PATTERNS

YIELD SHORTCUTInvestment 90Savings 30PV factor 3.0

Look up in Table B for the horizon period … and get the Yield %!

Note: Savings in years 11-50 do not improve the yield very much ... shame …

6/123 11.11 LEARNING PATTERNS

DCF MEASURES RELATEDIf PVS = PVI then the :

NPV = … ?PI = … ?Yield = … ?

Not yet

Answers: 0, 1, DR

6/124 11.11 LEARNING PATTERNS

CIA DECISIONS

Coconuts - big investments for long horizons = keys to survival

Peanuts - small investments for short horizons = not too important

Always: Q + NQ = D

Note: DCF gives a good Q … but does not decide …

6/125 11.11 LEARNING PATTERNS

DICHD - DECISION & CRITERIAI - INVESTMENTC - CASH FLOWH - HORIZON & TERMINAL VALUE

ASSUMPTIONS, CASH FLOW, OLD MACHINE, CASH PROFILE, PB, SRI, NPV, PI, Y

Q + NQ = D

Watch out for: AA, EI, PFD, coconuts and peanuts!

6/126 11.12 END OF PART I - HOORAY!!!

This ends Part I of out program.

Thank you for working so hard.

Part II begins almost immediately, and it is

“DOWNHILL ALL THE WAY …”

AGL

AUTONOMOUS

GROUP

LEARNING

Dr. Bob Boland

Boland1

6/1 AUTONOMOUS GROUP

LEARNING (AGL)

NO. 6 - DISCOUNTED CASH FLOW FOR CAPITAL INVESTMENT ANALYSIS

PART II

1.0 REVIEW OF PART I AND SHORT QUIZ

(… just for fun …)

2.0 PROGRAM LEARNING

3.0 LECTURE - EFFECTS OF TAX ON CIA

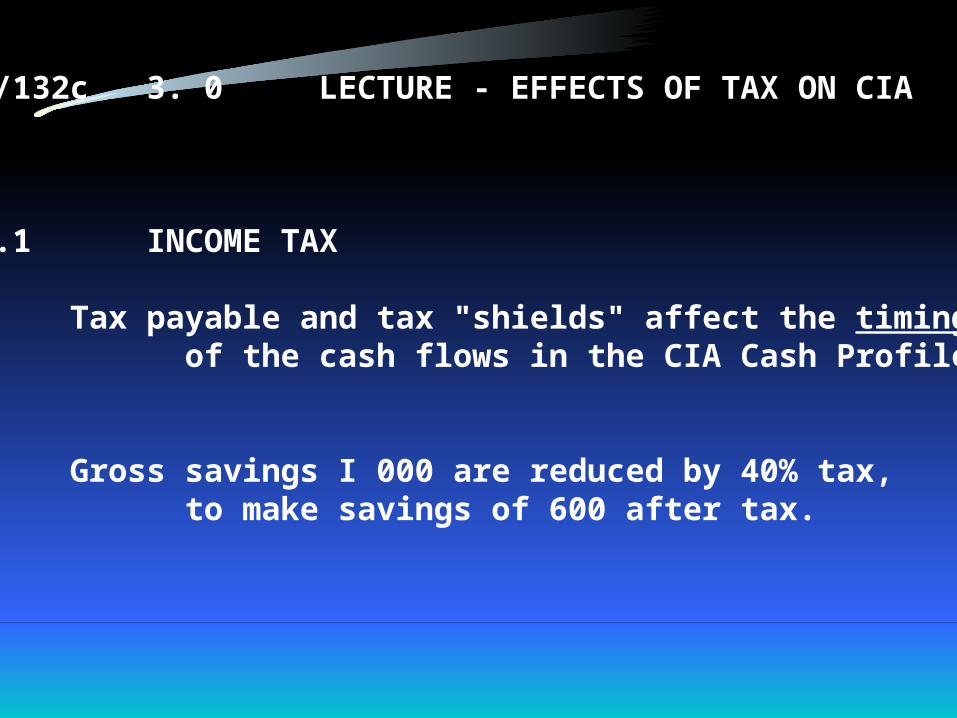

6/132c 3. 0 LECTURE - EFFECTS OF TAX ON CIA

3.1 INCOME TAX

Tax payable and tax "shields" affect the timing of the cash flows in the CIA Cash Profile.

Gross savings I 000 are reduced by 40% tax, to make savings of 600 after tax.

6/132d 3.2 DEPRECIATION

(a) Cost of a fixed asset is a capital expenditure; it is allocated as depreciation expense over the working life (horizon) of the asset.

(b) For simplicity we use "straight line depreciation" but other methods are equally applicable.

(c) Depreciation is not a cash flow after Year 0 but provides a tax shield in Years 1 - 10.

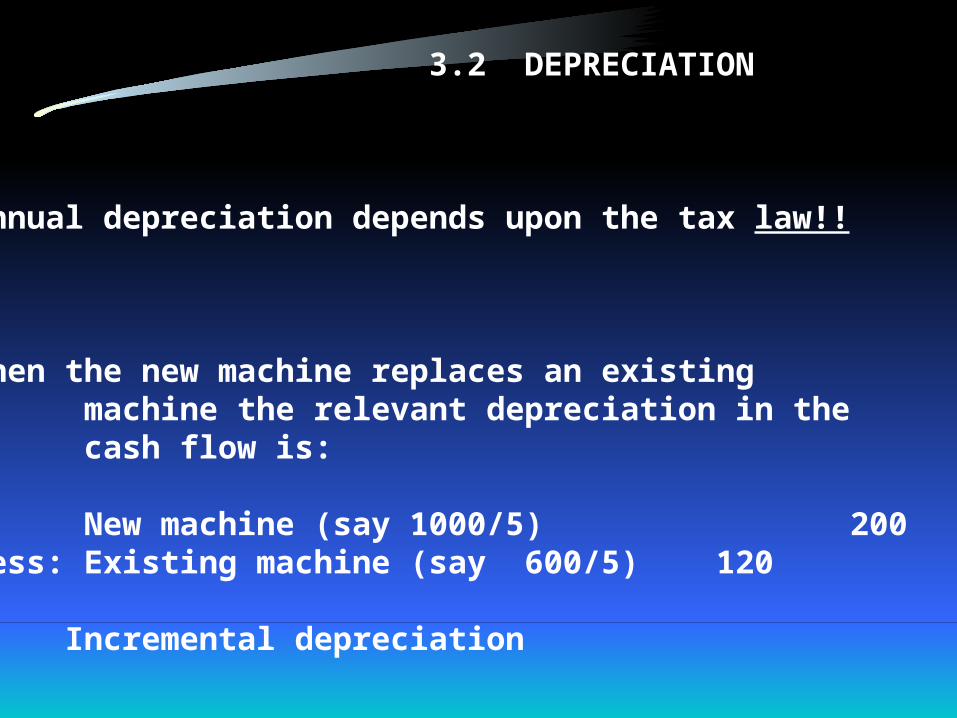

6/132e 3.2 DEPRECIATION

(d) Annual depreciation depends upon the tax law!!

(e) When the new machine replaces an existing machine the relevant depreciation in the cash flow is:

New machine (say 1000/5) 200Less: Existing machine (say 600/5) 120

Incremental depreciation 80

6/133 3.3 TAX SHIELDS

If equipment is sold or scrapped, any loss is a relief fortax purposes.

Thus, if equipment with a book value of 200 is sold fornothing, there is a book loss which provides a tax shieldimmediately of 40%; tax shield 40% x 200 = 80 cash inflow.

The loss on disposal is reduced by any terminal value;thus if a book value of 200 is sold for 200, there is noprofit or loss and thus no tax shield.

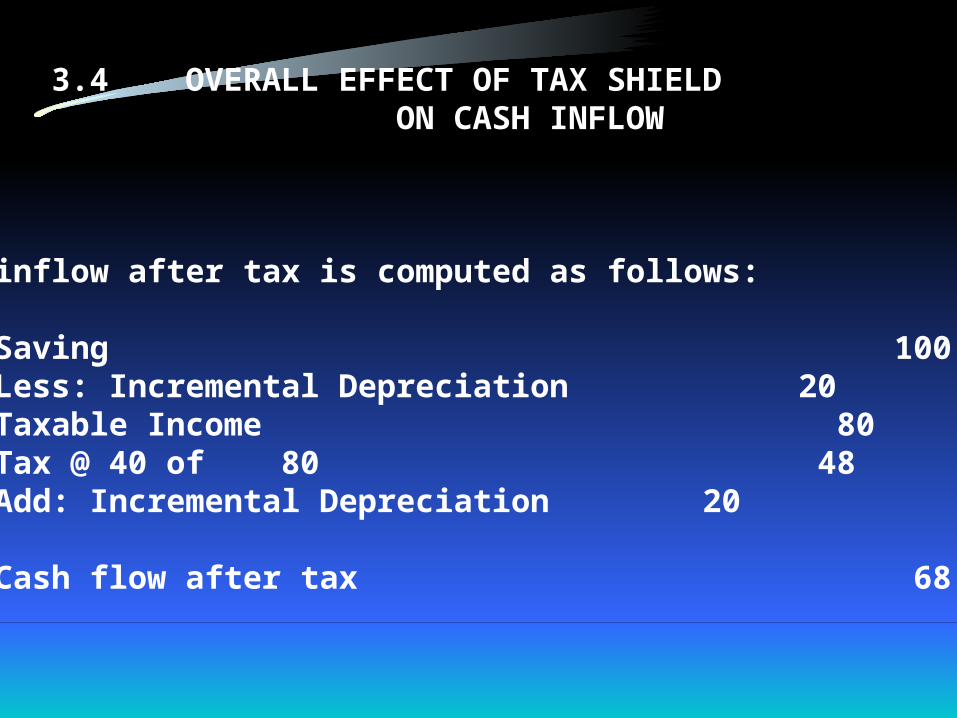

6/134 3.4 OVERALL EFFECT OF TAX SHIELD ON CASH INFLOW

Cash inflow after tax is computed as follows:

Saving 100Less: Incremental Depreciation 20Taxable Income 80Tax @ 40 of 80 48Add: Incremental Depreciation 20

Cash flow after tax 68

6/134 3.4 OVERALL EFFECT OF TAX SHIELD ON CASH INFLOW

or alternatively:

Saving 100Less: Tax @ 40% 40

60

Add: Incremental depreciation tax shield 20 @ 40% 8

Cash flow after tax 68

Note: Both methods provide the same result:savings 100 less tax of 32 = cash flow after tax of 68.

6/135 3.5 TAX SHIELD ON BOOK LOSSES

Where equipment is scrapped any book loss providesa tax shield now (year 0). The advantage of the tax shieldin year 0 instead of over the remaining life of the machineis a time advantage:

Examples: 1 2 3Net Book Value 100 100 100Terminal Value - 20 100Book Loss 100 80 - ___ ___ ___ Tax Shield on loss @ 40% 40 32 -Add Terminal Value - 20 100

Total benefit NOW whichreduces the investment inthe new machine 40 52 100

6/136 3.6 PROBLEMS OF DIFFERENT WORKING LIVES

Difficult to compare mutually exclusive projects with different horizons (i. e. 20 years or 15 years).

Simple solution is to choose the shorter horizon(15 years) and introduce a Terminal Value for the longerproject (20 years) as a cash inflow in year 15.

Alternatively use the "Yield" method and to identify thebest return.

Other theoretical methods may be too complicated orrequire difficulty assumptions.

6/137 3. 7 QUANTITATIVE AND NON-QUANTITATIVE FACTORSN + NQ = D

Quantify for rigorous analysis but consider also the NQ factors. If the Q is poor we may still invest; converselyeven good Q, we may still decide not to invest.

Need a range of Q’s to test the sensitivity of results todifferent assumptions; try different:

- discount rates- horizons- terminal values- levels of cash flow

NOTE: Horizon is the @e assumption.

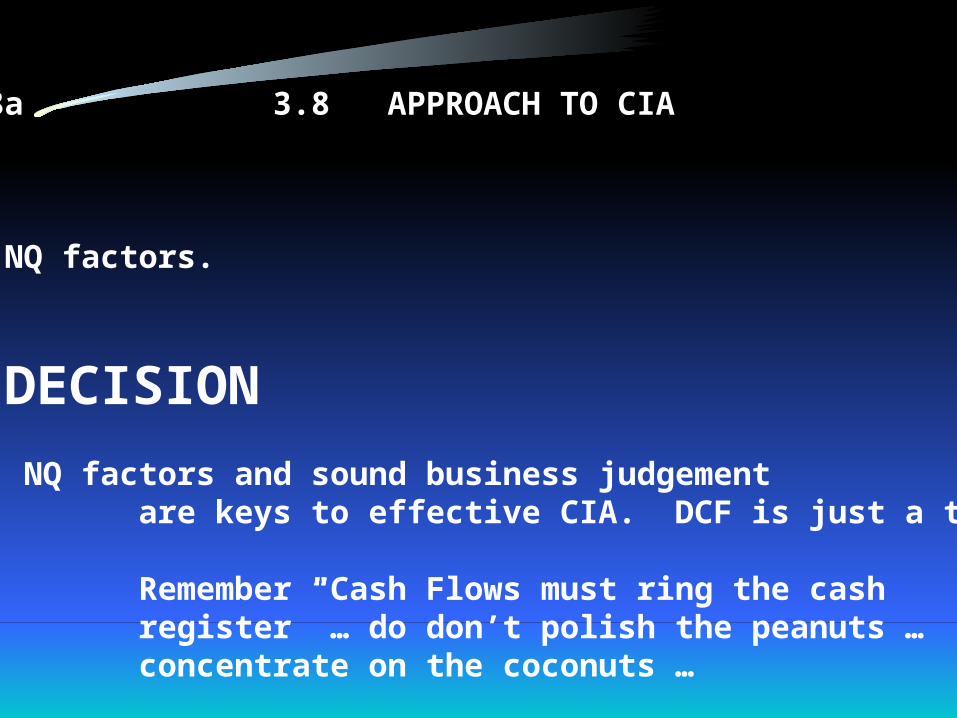

6/138 3.8 APPROACH TO CIA

(a) DICH - Decision Investment Cash Flow Horizon and Terminal Values

(b) AA (Alternative Analysis) and PFD (Provision for Disaster).

(c) Cash Profile = Actual cash to present value cash.

(d) Measures of investment: Payback, Net Present Value, Profitability Index and Yield.

6/138a 3.8 APPROACH TO CIA

(e) NQ factors.

(f) DECISION

NOTE: NQ factors and sound business judgement are keys to effective CIA. DCF is just a tool.

Remember "Cash Flows must ring the cash register” … do don’t polish the peanuts … concentrate on the coconuts …

6/139 3.9a DEPRECIATION

Strainght line method :

100 - depn. 20 20 20 20 20

Diminishing balance method:

100 - depn. 30 21 15 10 7

6/140 3.9b ANNUAL AFTER TAX CASH FLOW

APPROACH I APPROACH IISavings - Cash In 100 Savings - Cash In 100Depreciation 20 Tax 40% 40Taxable Income 80 60

Tax 40 % - Cash Out 32 Depn tax shield 20 X 40% 8 Sub total 48 Depeciation 20Cash Flow after tax 68 68

6/141 3. 9c TERMINAL VALUES AND TAX SHIELDS

1 2 3

Old Machine Net Book Value 100 100 100Terminal Value 80 80 0

Book Loss 20 60 100

Tax Shield - 40 % 8 24 40Terminal Value 80 40 0 Reduction of new investment 88 64 40

6/142 3.9d COMPARING DIFFERENT WORKING LIVES

Machine A 10 years

Machine B 15 years - make a cut off at 10 years and take a terminal value and a tax shield

6/143 3.9e LEARNING PATTERNS

DICH ANALYSIS

PFD DICH AA

Cash Profiles After Tax

Measures of Investment NQ Factors

DECISION

6/144 3.9f CIA DECISIONS

Q + NQ = D

4.0 CASE STUDY

5.0 LECTURE -

ON THE CASE

6/145 5.0 LECTURE - SCOTT MORTON COMPANY

5.1 STORY OF THE CASE

hree years ago SMC bought four machines with a 15year working life, for use on a major contract held bythe company for the previous 10 years.

Now consider replacing them with one automatic machine for 180 000 with a possible 15 year horizon, financing the cost mai from the bank. Is financing relevant to CIA?

General Manager justifies the investment by payback and SRI.

Should the company buy the automatic machine now?

6/146 5.2 GENERAL MANAGER’S JUSTIFICATION

(a) No, not justified by payback and SRI alone; fails to consider "time value of money", terminal values, tax shields and the effect of fixed costs.

(b) Alternatives available:

- Buy the machine now and scrap 4 old machines- Buy the machine now and scrap 3 old machines- Buy the machine later- Buy another machine- Don't buy anything- Lease- Overhaul the old machine- Subcontract the work- Give up the contract

6/147 5. 3 NQ FACTORS AND PFD

(a) The following NQ factors are relevant:

- Overall manufacturing policy- Labour problems- Reliability- Supplier relationships- Materiality- Better machines later, etc.

6/147a 5. 3 NQ FACTORS AND PFD

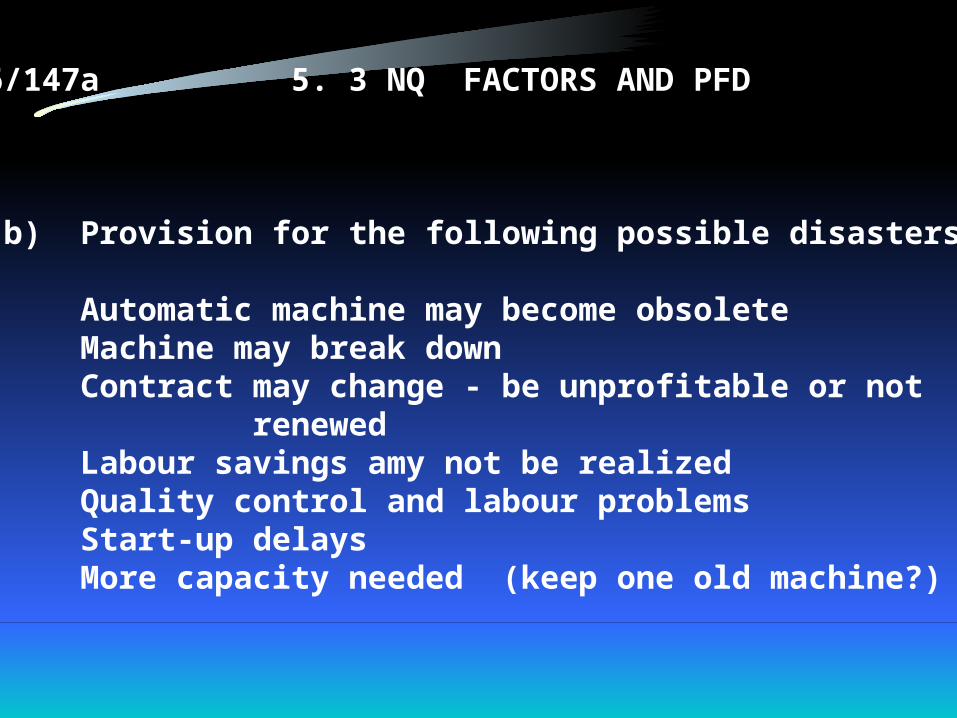

(b) Provision for the following possible disasters:

- Automatic machine may become obsolete- Machine may break down- Contract may change - be unprofitable or not renewed- Labour savings amy not be realized- Quality control and labour problems- Start-up delays- More capacity needed (keep one old machine?)

6/147b 5. 3 NQ FACTORS AND PFD

(b) Provision for the following possible disasters:

… but on the other hand:

- Greater capacity than three machines- Avoid labour troubles- Provide many NQ benefits- Have a long life- And OVERALL may be strategically necessary

6/148 5.4 RELEVANT DATA

(a) Bank loan not relevant - merely financing; not CIA problem (really! )

(b) Terminal value of old machine 60 000 reduces the new mac investment from 180 000 to 120 000 net.

(c) Loss on scrapping the old machine (120 000 - 60 000) 60 00 provides a tax shield of 40% - 24 000 which reduces the gross investment from 120 000 to net investment of 96 000.

6/148a 5.4 RELEVANT DATA

(d) Floor space savings are fixed costs - not relevant since no cash flow (does not "ring the cash register".

(e) Horizon. Initially try 15 years but reduce it due to risk. Try 7 years as more reasonable estimate.

6/149 5.5 INCREMENTAL DEPRECIATION AND CIA WORKSHEET

Relevant depreciation is the (additional) incrementaldepreciation as follows:

New machine 180 000 15 years = 12 000 p. a. Old machine 120 000 12 years = 10 000 p. a.

Incremental depreciation 2 000 p. a.

Note: Comparison with different horizons can be a little complex; thus it is easier to consider always the same minimum horizon and to make adjustment for a terminal values accordingly.

6/149a 5.5 INCREMENTAL DEPRECIATION AND CIA WORKSHEET

CIA Worksheets show following results:

Horizon Horizon15 years 7 years

Gross Payback 3 years 3 yearsNPV + 15 -3PI 1.1 1.0Yield 18 % 15%

NOTE: Yield not substantially changed due to taxshield on book loss in year 7, since Tax Law only allowsdepreciation tax shield of 1/15 annually for 15 years.

6/150 5.6 PLAN OF ACTION

(a) Do not buy the machine now. Wait and see ...

(b) Justification.

Automatic machine achieves yield of only 15 % ata 7 year horizon yet old machine lasted only 3 years.

High risk of project due to possible obsolescence,breakdown and contract failure.

Better alternative available?

6/150a 5.6 PLAN OF ACTION

(c) Search alternative machines or delay decision until long term contract is signed, or possibly lease the machine or sub-contract.

(d) Set up a CIA system to consider all alternatives and to do a PFD before making a decision.

NOTE: NPV of -3 IS A PEANUT DIFFERENCE, SO TREAT IT AS ZERO!

6/151 5.7 LEARNING POINTS

(a) Bank loans for financing equipment are not relevart to the investment problem!

(b) New investment is reduced by the terminal value of old machine.

(c) Book loss on old equipment provides a tax shield to reduce the new investment.

(d) New investment much achieve the required Yield after tax to reach EVA.

6/151a 5.7LEARNING POINTS

(e) Depreciation is a non-cash expense relevant for tax purposes.

(f) Depreciation tax shield on the taxable cash flow is only for the incremental depreciation based on the tax law.

(g) Horizon is the key assumption - don't forget terminal values and tax shields on book losses!

(h) Test CIA using different assumptions to produce a range of computations.

6/151b 5.7LEARNING POINTS

(i) DICH followed by Cash Profile and Measures of Investment.

(j) Q + NQ = D but NQ is the key!

(k) Compute figures in 000s (thousands! big assumptions do not justify small figures - avoid "fraudulent pseudo accuracy".

(1) Don't let the figures make the decision - they merely support good business judgement.

(m) Seek not merely a good investment opportunity but the best alternative to achieve required objectives.

6/152 5.8b LEARNING PATTERNS

BENEFIT OF SCRAPPING OLD MACHINE NOW

Net Book Value 120Terminal Values 60Book Loss 60

TAX SHIELD @ 40% of 60 24Terminal Value 60

Total Benefit - to reduce the new Investment 84

NOTE: Only incremental depreciation is relevant to the annual cash flow in the Cash Profile.

6/153 5.8 LEARNING PATTERNS

SAVINGS AFTER TAXSavings 30 Savings 30

IncrementalDepreciation 2 Tax 12

Taxable savings 28 18 Tax 40 % 11 Depn. Sub-total 17 Tax Shield 1Add back depn. 2

Cash flow AT 19 19

6/154 5.8 LEARNING PATTERNS

NQ FACTORS

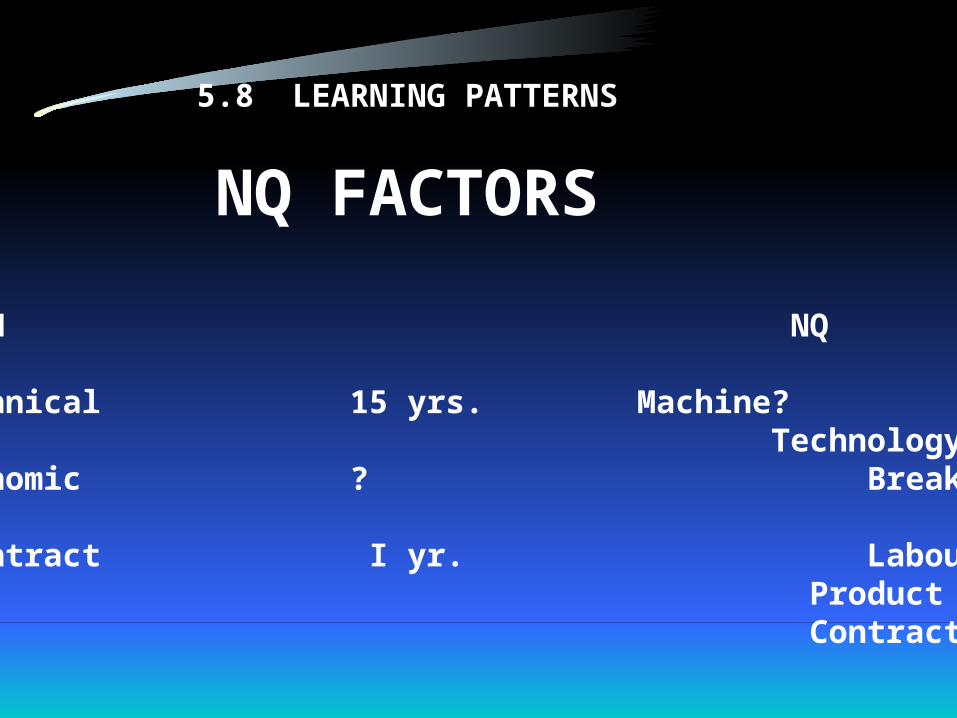

HORIZON NQ

- Technical 15 yrs. Machine? Technology?

- Economic ? Breakdown?

- Contract I yr. Labour? Product Contract

6/155 5.8 LEARNING PATTERNS

MEASURES OF INVESTMENT

PB SRI

PI NPV YIELD

6/156 5.8 LEARNING PATTERNS

CIA DECISION

Yield & PB

Assumptions

NQ Factors

AA?

PFD?

Decision by Management

6/157 5.8 LEARNING PATTERNS

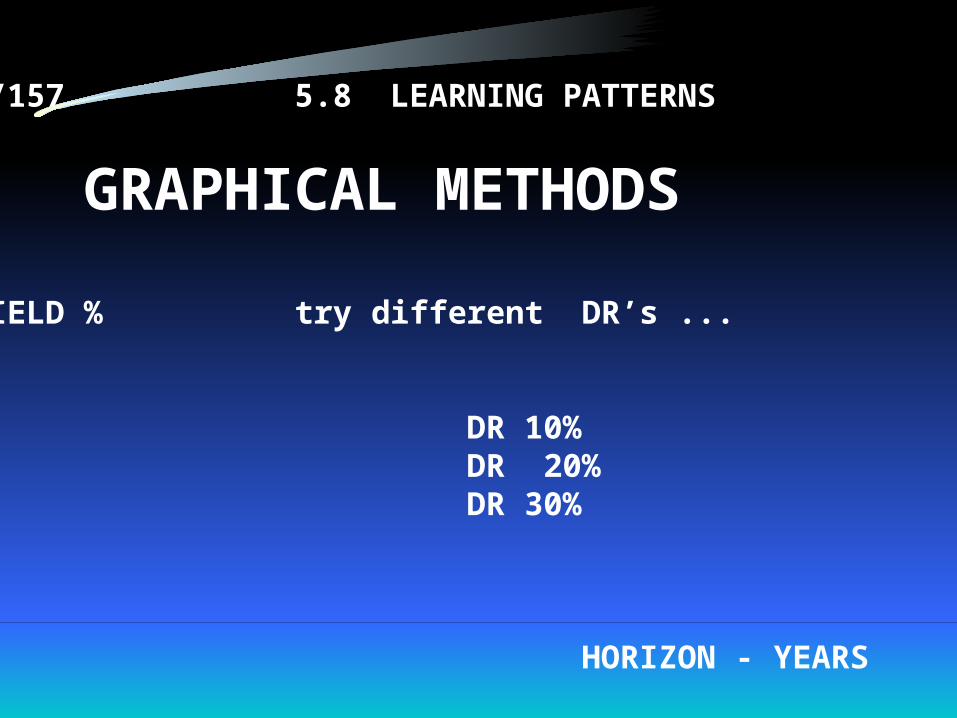

GRAPHICAL METHODS

YIELD % try different DR’s ...

DR 10% DR 20% DR 30%

HORIZON - YEARS

6/158 5.8 LEARNING PATTERNS

GRAPHICAL METHODS

YIELD % seek the minimum life to achieve the required DR ...

HORIZON - YEARS

6.0 BILL BROWN

7.0 PROGRAM LEARNING

8.0 LECTURE - CAPITAL

BUDGETING SYSYEMS

6/159 8.0 LECTURE - CAPITAL BUDGETING SYSTEMS

8.1 THE SYSTEMATIC APPROACH

(a) Search

(b) Long range planning and short range capital budgets.

(c) Research and analysis - determine relevant data.

(d) Criteria - set basis for Go or No Go decision.

(e) Audit - systematic comparison of project estimates and subsequent reality. Basis for reviewing past decisions and making new ones. Psychological effect upon managers making new estimates.

6/159a 8.0 LECTURE - CAPITAL BUDGETING SYSTEM

8.1 THE SYSTEMATIC APPROACH

(f) Disinvestment policy - important!

(g) System of forms and procedures (Controller' s job!

NOTE:

Distinguish "investment" problems (is it worhtwhile to invest) from "financing" problem how to finance it!

6/160 8. 2 LONG RANGE PLAN

For CIA in the framework of a long planning horizonwe need:

(a) Forecast of general economic activity.

(b) Projection of the firm's physical sales volume.

(c) Forecasting of the facilities and personnel needed.

(d) Projection of routine machine replacement (best analysed by operational research techniques).

(e) Ranking of major projects including plans to deal with long run changes in the economy or the Organisation.

6/161 8. 3 SHORT RANGE CAPITAL BUDGET

Forces managers to look ahead and plan.

Forces top management to look at cash flow, earnings, depreciation allowances and dividend policy.

Should accomplish:

(a) tie in with a long range capital budget. (b) forecast of cash flows for each investment project.

Fits projects into a general framework, consistent with the company objectives.

6/162 8.4 RISK

Involved in all projects - never certainty!

Never good data - valid assumptions.

Approach to risk in CIA:

(a) Use conservative estimates.(b) Use higher IOR'S.(c) Use probability and "expected value" techniques.(d) Use shorter horizons.(e) Use graphical methods to show sensitivity of measures of investment to underlying assumptions.

NOTE: See HBR articles on the Hertz ad other Models using probability etc.

8/163 8. 5 APPROACH TO "LEASE OR BUY" PROBLEMS

Complex problem with no "correct" DCF solutions!

BUY - NPV of the cost to buy is: Original Investment less the PV of the tax shield.

LEASE - NPV of the cost to lease is: PV of the after tax lease payments.

Determine Cash Profiles at various discount rates and assumptions. Don't believe the results too easily!!

Sophisticated analysis is not justified for poor data.NQ factors are the key! If short of cash ... lease!

6/164 8. 6 CRITICISM OF CIA MEASURES

(a) Payback and SRI ignore time value of money.

(b) Payback ignores all cash flows after payback period.

(c) All measures involve assumptions about re-investing annual proceeds.

(d) Yield does not indicate size of projects whereas NPV does

(e) To communicate to management use: YIELD and PAYBACK.

6/165 8.7 PROBLEM OF ASSUMPTIONS

All CIA depends upon assumptions. Prepare high, low and expected assumptions. Key assumption is HORIZON!

Use CIA techniques appropraite to the data. Normallycompute all data in thousands - don’t “polish peanuts!!”.

Set the assumptions and then do:

AA, PFD, Cash Profile, Measures of Investment, NQ factors, Decision and Audit.

NOTE: Watch out for your personal EI (EmotionalInvestment) … in a poor alternative!

6/166 8.8 DICH

D - Decision and Criteria

I - Investment

C - Cash flow after tax

H - Horizon and terminal values

6/167 8. 9 MANIPULATION - “CREATIVITY”

CIA data may be manipulated like any other accountingdata. To "improve" the DCF return, we may:

reduce investment or increase savings shorten time of savings or increase horizon reduce tax -rate or increase terminal values deduct irrelevant salvage values combine projects ands cover a bad one with a good one!

Insist that CIA assumptions be stated and justified; besure they are valid and always seek alternative assumptions.

CIA sets the shape of the company for years ahead we must get it "right".

6/168 8.10 CIA AND THE CURRENT NET PROFIT

Invest "now for benefit later" but don't ignore effect of "irrelevant losses" on the actual profits this year … management may get fired!

Choose a mix of investments that provides both short term and long term profit for the company.

CIA book losses may not be relevant cash flow but they may be too big to ignore in their effect on thecurrent year net profit!!

6/169 8.11 LEARNING PATTERNS

CAPITAL BUDGETING SYSTEM

Long Range Short RangePlanning Capital Budget(5 years)

Search Analysis

CriteriaDecisionAudit

Forms & PossibleProcedures Disinvestment

6/170 8.11 LEARNING PATTERNS

PROVIDING FOR RISK

HORIZONS GRAPHS

ESTIMATES HIGH - LOW SENSITIVITY

HURDLE RATES ANALYSIS

PROBABILITIES CASH CAUTION

6/171 8.11 LEARNING PATTERNS

LEASE v BUY

CASH PROFILES - ACTUAL, BOR, IOR

SENSITIVITY AND NQ FACTORS

DISNTINGUISH - FINANCIAL v OPERATING LEASES

USE BOR INSTEAD OF IOR … AS NECESSARY ...

6/172 8.11 LEARNING PATTERNS

ASSUMPTIONS

GOOD ASSUMPTIONS ARE THE KEY TO CIA TO BE SURE THAT IT IS :

EFFICIENT - DOING THINGS RIGHT

AND ALSO …

EFFECTIVE - DOING THE RIGHT THINGS

6/173 8.1l LEARNING PATTERNS

DICH Good DICH involves:

AssumptionsAACash Profiles - Real Money into PV MoneyMeasure s of Investment - PB, NPV, PI, YIELDQ + NQ = D PFD

to give r ranges of decision for management Intuition …

6/174 8.ll LEARNING PATTERNS

CIA MANIPULATION

How to turn an estimated yield of 8% into the “required” hurdle rate of 15% and thus get approval to do it …

Change the estimates for ... Investment? Savings? Horizon? Volumes? Terminal Values? Tax Rates? .. or simply combine it with a "good" project?

Alternatively - justify it by Law or Policy or Expense it!

Note: Never call it “M” … call it “Creativity” ...

9.0 CASE STUDY

10.0 LECTURE

ON THE CASE

6/175 10.0 LECTURE - CAPE CHEMICAL CO.

10.1 STORY OF THE CASE

Company needs increased product X701 provided eitherby purchase or investment in new machine.

Factory manager' s analysis indicates acceptableinvestment of 42% against Controller yield of 10%.

General Manager wants to know what to do about theCapital Budgeting System and this project.

6/176 10. 2 CAPITAL BUDGETING SYSTEM

Company needs proper system since CIA involveskey major expenditures over long time periods; system must relate projects not to short term but tolong term planning; one year budgets are only usefulas part of a long term plan.

Suggest:

(a) Measures of Investment - DCF essential for analysis of major projects; compute results in 000's only.

6/176a 10. 2 CAPITAL BUDGETING SYSTEM

(b) Planning - set up Total Business Plan for 5 years, researc ing the environment, setting policies, key decisions and an budgets. Replan every year for 5 years ahead; ensure tha system motivates a creative search for new CIA projects.

(c) Hurdle Rate - set minimum acceptance rate for CIA projec to ensure improvement of long term profitability of the firm; rate should be "Average Cost of Capital" or different (high rates to allow for risk. EVA and SVA are vital.

6/176b 10. 2 CAPITAL BUDGETING SYSTEM

(d) Ranking projects systematically only after Q and NQ factors have been considered. Use yield and Payback as major criteria for the Q

(e) Search-for new projects to provide both the short term and long term profitability for the company.

(f) Do AA and PFD regularly as a required routine … .

6/177 10. 3 AUDIT

CIA post-completion audits are vital to:

(a) Check out the capital investment estimates against reality.

(b) Check original assumptions.

(c) Improve future CIA.

NOTE Such audits are vital … but often very embarassing to senior managers … I wonder why …?

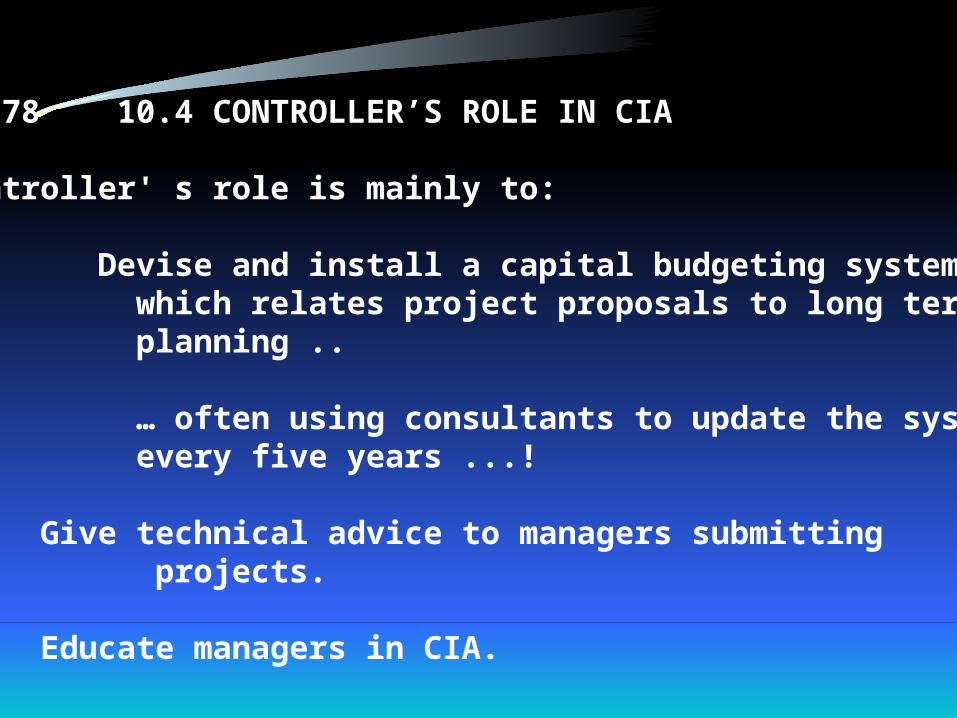

6/178 10.4 CONTROLLER’S ROLE IN CIA

Controller' s role is mainly to:

(a) Devise and install a capital budgeting system which relates project proposals to long term planning ..

… often using consultants to update the system every five years ...!

(b) Give technical advice to managers submitting projects.

(c) Educate managers in CIA.

6/178a 10.4 CONTROLLER’S ROLE IN CIA

(d) Check out CIA proposals.

(e) Make post completion audits of CIA projects.

(f) Help to develop a creative approach toward CIA throughout the company.

6/179 10.5 COMPUTERS

Simple standard computer packages available for CIA.

Keep all data simple! ! Don't believe the computer too easily!

Make alternative computations for each project usingvarious assumptions.

NOTE: Beware of garbage! Discounted garbage! And even worse, computerised discounted garbage!(CIA based on wrong assumptions. )

6/180 10. 6 ALTERNATIVES AND CRITICISM OF FACTORY MANAGER’S COMPUTATION

(a) Many alternatives available: buy, do not buy, delay buying, buy product, lease equipment, don't expand, work double shift, etc.

(b) Several errors in the assumptions and method:

- Depreciation is not a cash flow - relevant only for tax shield. - Calculation does not include DCF. - Relevant production is 100 000 not 600 000.

(c) Lease v. buy analysis could also be made.

6/181 EQUIPMENT DECISION AND JUSTIFICATION

(a) Q facvtor - CIA Worksheet shows the the equipment is not justified:

Payback 3 yearsNet Present Value -1Profitability Index .8Yield +/- 10% (standard 15%)

(b) NQ factors - better alternatives probably available (AA), horizon may be less than 7 years, possible quality problem etc, (PFD).

(c) Subject to NQ factors DO NOT BUY the equipment now … wait and seek a better alternative.

6/182 10.8 LEARNING POINTS

(a) Need for rigorous capital budgeting system which relates projects and capital budgets to long term planning.

(b) One year capital budget must be related to long term plan.

© CIA search and audit are vital parts of the capital budgeting system.

(d) Post-completion audits of projects essential for many reasons.

6/182a 10.8LEARNING POINTS

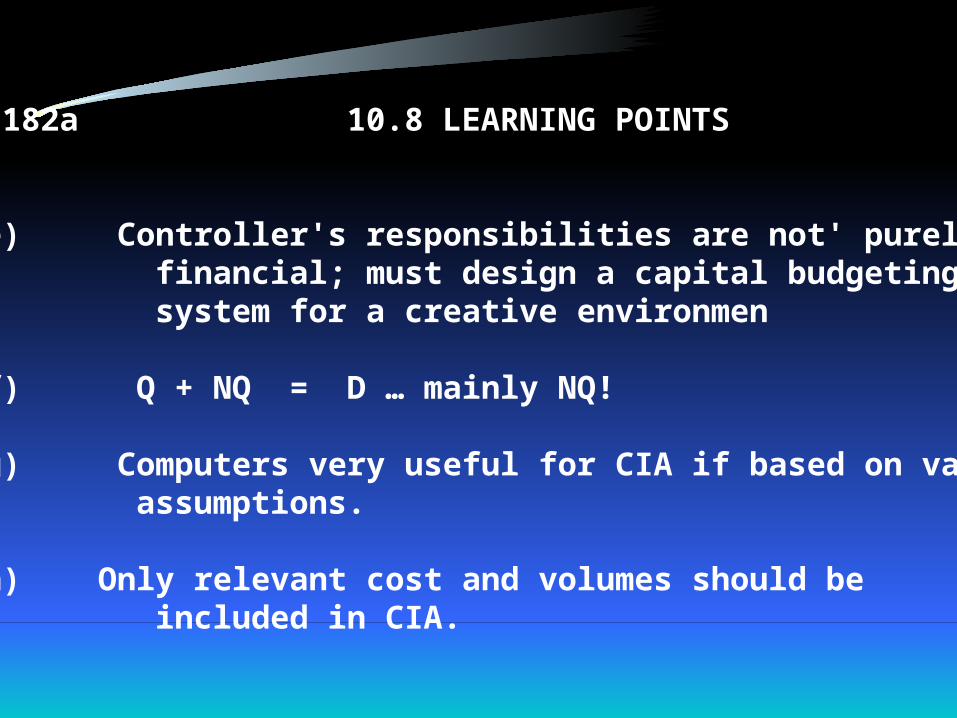

(e) Controller's responsibilities are not' purely financial; must design a capital budgeting system for a creative environmen

(f) Q + NQ = D … mainly NQ!

(g) Computers very useful for CIA if based on valid assumptions.

(h) Only relevant cost and volumes should be included in CIA.

6/182b 10.8LEARNING POINTS

(i) Depreciation is still not a relevant cash flow.

(j) Assumptions of costs and prices may be wrong - verify underlying assumptions and seek alternatives.

(k) All valid CIA computations must include income tax.

(1) Return on investment must be DCF to be valid (SRI is not valid.)

6/182c 10.8LEARNING POINTS

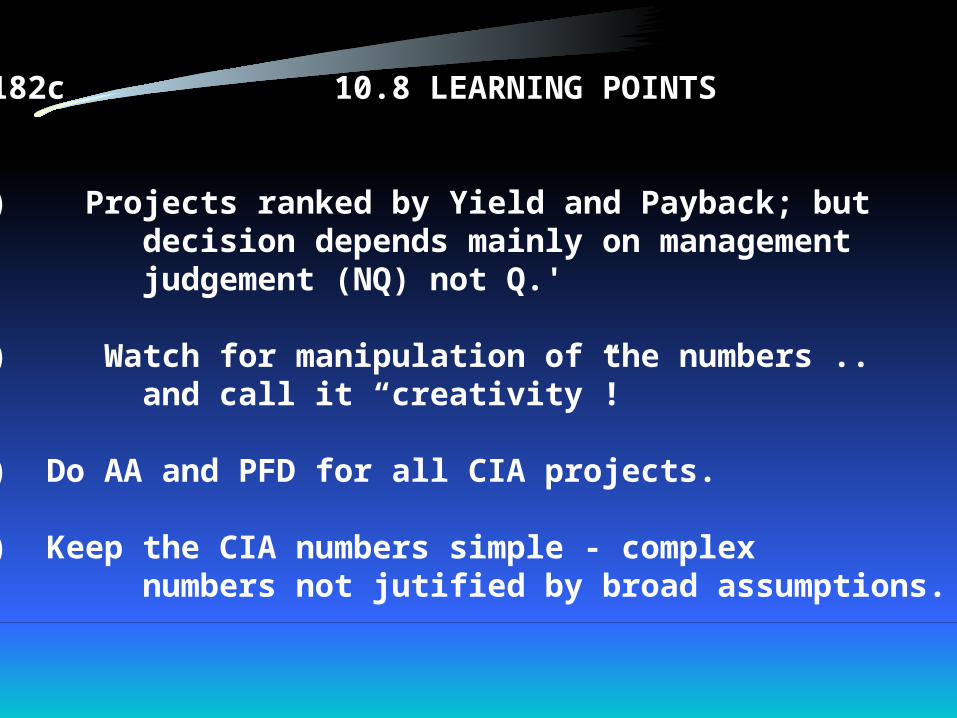

(m) Projects ranked by Yield and Payback; but decision depends mainly on management judgement (NQ) not Q.'

(n) Watch for manipulation of the numbers .. and call it “creativity”!

(o) Do AA and PFD for all CIA projects.

(p) Keep the CIA numbers simple - complex numbers not jutified by broad assumptions.

6/183 10.9 LEARNING PATTERNS

BUDGETING SYSTEMS

CIA not only for … Project Analysis …

But also for:

Long term planning

Short term capital budgets

Procedures for Search, Analysis, Ranking Decision, Audit and Disinvestment.

6/184 10.9 LEARNING PATTERNS

RANKING FOR SELECTION

RANK PROJECTS BY … PB, PI, YIELD …

BUT NOT BY … NPV OR SRI ...

6/185 10.9 LEARNING PATTERNS

CONTROLLER FUNCTIONS

Creative Cash FlowsCapital Future ProfitsSystem EVA & SVA

CREATIVE ENVIRONMENT

6/186 10.9 LEARNING PATTERNS

CIA & COMPUTERS

COMPUTERS CAN BE A LITTLE DANGEROUS IN CIA BECAUSE … THEY PROVIDE …

ALMOST UNLIMITED … CIA DATA AND CIA COMPLEX COMPUTATIONS ...

BUT THEY DO NOT (YET) MAKE THE KEY CIA DECISIONS

AND THEY DO DEPEND UPON GOOD ASSUMPTIONS …

BECAUSE ... Q + NQ still equal D

6/187 10.9 LEARNING PATTERNS

SETTING THE HURDLE RATE

E AVERAGE COST OF CAPITAL IS MINIMUM "HURDLE' RATE” DEPENDING UPON THE E:D RATIO ...

D SETTING THE COC … IS A KEY MANAGEMENT DECISION!

NOTE: COC cahnges over time ...!

6/188 10.9 LEARNING PATTERNS

ASSUMPTIONS

RELEVANT CASH FLOWS

VOLUMES COSTS CONTRIBUTIONS

6/189 10.9 LEARNING PATTERNS

CAPITAL INVESTMENT DECISIONS

THE CAPITAL BUDGETING SYSTEM

CIA, Q, NQ, DCF, AA, PFD

MANAGEMENT JUDGEMENT & INTUITION

DECISIONS

11.0 QUIZ -

JUST FOR FUN

12.0 SUMMARY LECTURE

FOR PART II

(WELL DONE!!!)

6/190 12.0 SUMMARY LECTURE FOR PART II

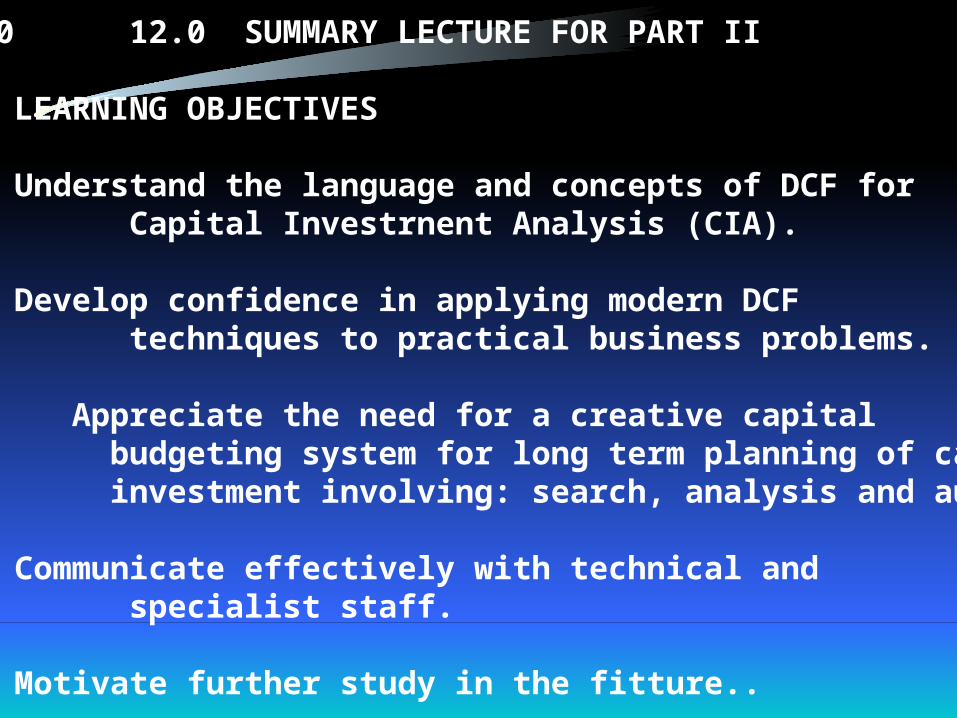

12.1 LEARNING OBJECTIVES

(a) Understand the language and concepts of DCF for Capital Investrnent Analysis (CIA).

(b) Develop confidence in applying modern DCF techniques to practical business problems.

© Appreciate the need for a creative capital budgeting system for long term planning of capital investment involving: search, analysis and audit.

(6) Communicate effectively with technical and specialist staff.

(e) Motivate further study in the fitture..

6/191 12.2 WORK COMPLETED

Language and concepts

Cases and eExercises

Program leanring

AA and PFD

Measures of investment - before tax and after tax.

Capital budgeting systems

6/192 12.3 CIA DECISIONS

Key decisions - large amounts - long time periods.Cornmitment of funds Year 0 for benefit years 1-20.Justification - law, policy and economics.

Importance:

(a) Future of company depends on sound CIA.

(b) Needs highest level of managernent judgement and complex skills.

(c} Magnitude, timing and wisdom of CIA ensures long-term survival of the firm.

6/193 12.4 CASH PROFILE

Reduce investment to cash Profile years 0-20.

Relevant costs and savings.

Ignore sunk and fixed costs1

Contribution (not net profit).

Depreciation for tax shield only.

Cash Proflie is the KEY!

6/194 12.5 SELECTING DISCOUNT RATES

Key management decision.

Need to research the "Average Cost of Capital" to determine the hurdle discount rate (DR). Policy decision.

Changes over time and possibly changes by project.

Company guidelines:

- General Motors 20% AT- Sears Roebuck 10-15% AT- US Steel 8% AT

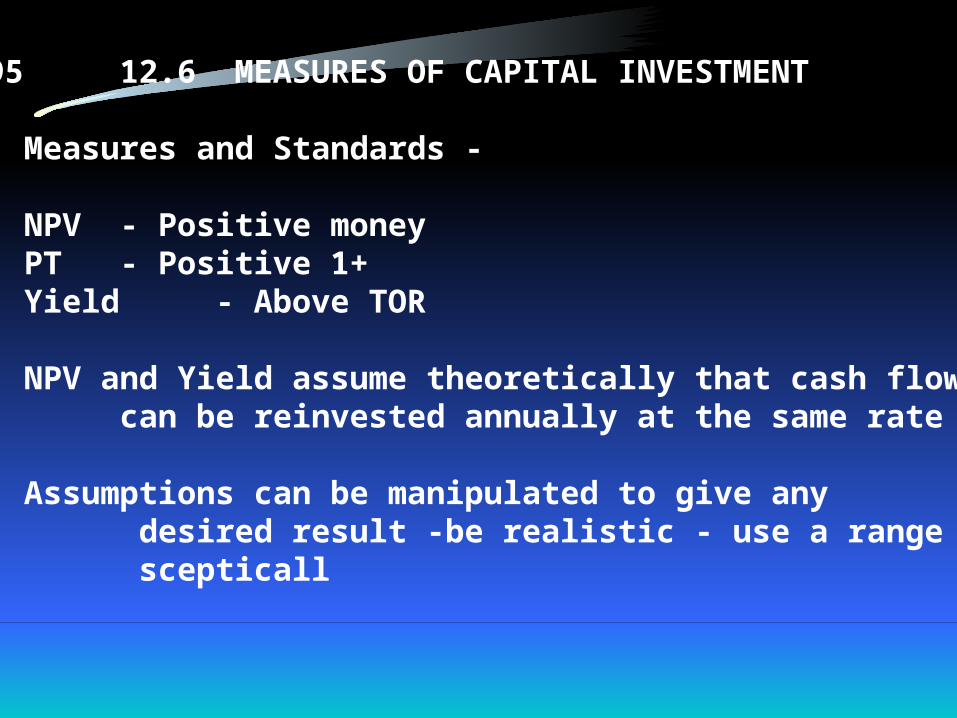

6/195 12.6 MEASURES OF CAPITAL INVESTMENT

(a) Measures and Standards -

NPV - Positive moneyPT - Positive 1+Yield - Above TOR

(b) NPV and Yield assume theoretically that cash flow can be reinvested annually at the same rate

(c) Assumptions can be manipulated to give any desired result -be realistic - use a range - be scepticall

6/196 12.7 PROVIDING FOR RISK

Conservative estimates of cash flovi.

High - low - expected values.

Higher IOR.

Shorter horizons.

Low TV'S.

6/197 12.8 SOPHISTICATED METHODS

Materiality - work in thousands.

Reality of assumptions.

Mathematical possibilities.

Multiple measures.

Graphical methods to show sensitivity of the resultsto changes in assumptions.

Hertz model using computers and probability andexpected value techniques.

6/198 12.9 DICH

D - Decision and CriteriaI - InvestmentC - Cash FlpwH - Horizon and Terminal Value

Foliowed by Cash Profile, Measures of Investment, NQFactors and Decisions.

NOTE: Don’t forget: Alternative Analysis, PFD, Emotional Investment, Coconuts and Peanuts.

6/199 12.10 DISINVESTMENT

(a) Existing projects may produce ketter earnings if sold (disinvested) rather than retained.

(b) Disinvestment is so often psychologically difficult because of EI. Outsourcing is now a key management skill.

(c) Criteria should be the same 10k.

(d) Specialised assets may have more value to others than the first owner.

(e) Accounting book values do not indicate Opportunity Cost of assets!

6/200 12.11 SYSTEMS

Search )Analysis ) Long term planningCriteria ) Short term capital budgetsDecision )Audit )

6/201 12.12 FORMS AND PROCEDURES

(a) Controls and procedures provide special forms for analysis. evaluation and approval.

(b) Training is essential for technical and human problems.

(c) Good capital budgeting; systems require control and enthusiasm based on the "spirit" rather than the “letter”of the rules - outgrowth of general environment of the firm.

(d) Need a creative approach to CIA.

6/202 12.13 BALANCED APPROACH TO CAPITAL BUDGEflNG

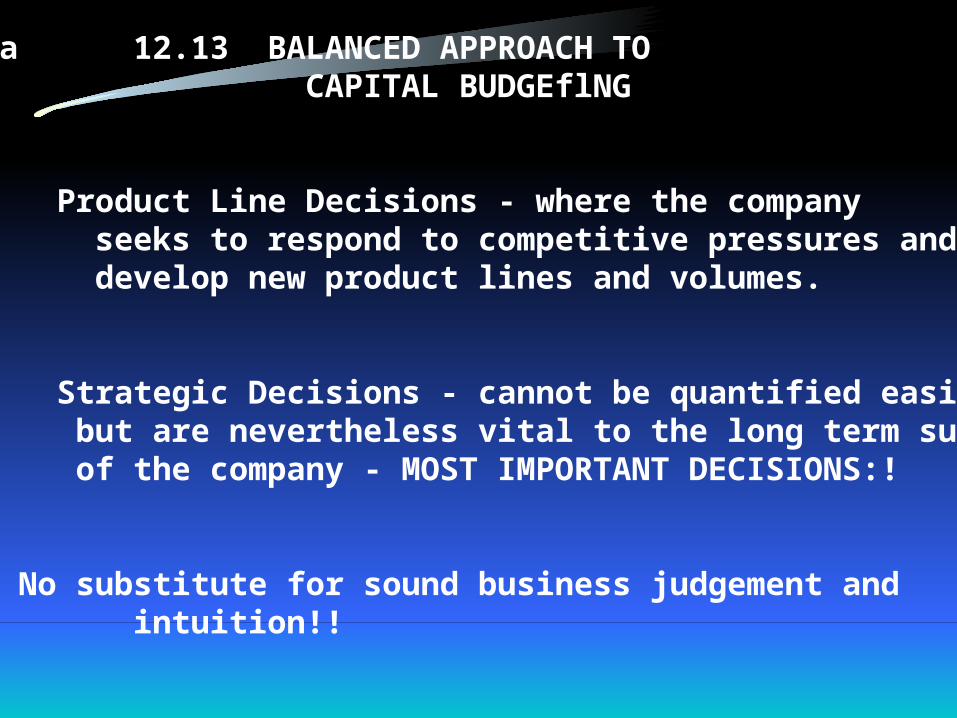

Promoting CIA projects neyer depends purely on the quantitative measures. Management must take abalanced approach:

(a) Replacement Decisions - where the company seeks cost savings and the data is fairly accurate.

(b) Expansion Decisions - where the company seeks to increase earnings from existing products.

6/202a 12.13 BALANCED APPROACH TO CAPITAL BUDGEflNG

(c) Product Line Decisions - where the company seeks to respond to competitive pressures and to develop new product lines and volumes.

(d) Strategic Decisions - cannot be quantified easily but are nevertheless vital to the long term success of the company - MOST IMPORTANT DECISIONS:!

NOTE: No substitute for sound business judgement and intuition!!

6/203 12.14 OVERALL

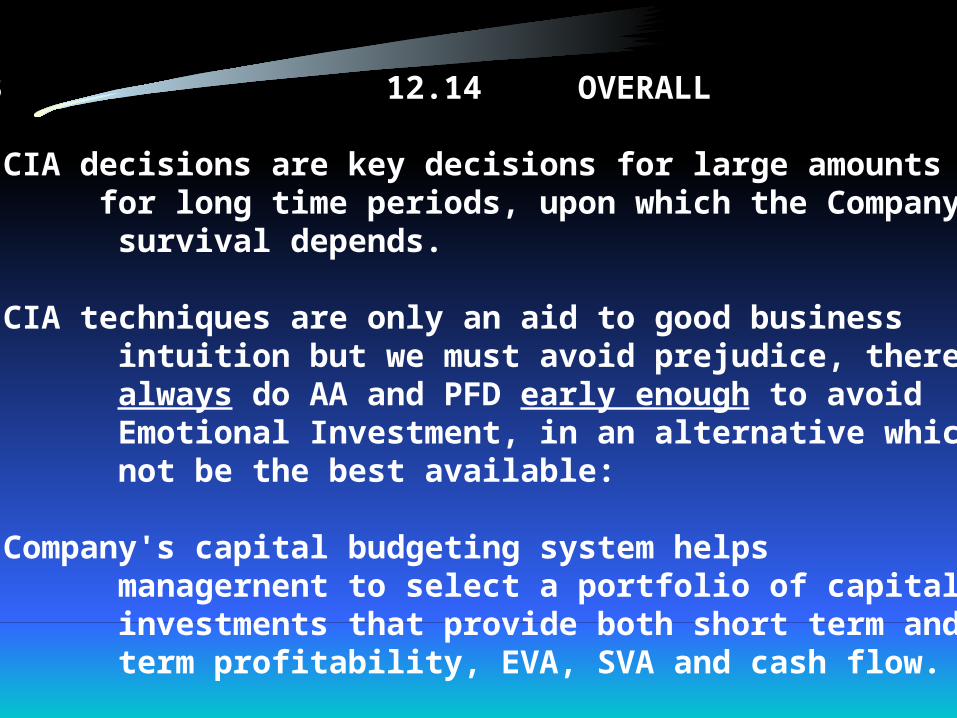

(a) CIA decisions are key decisions for large amounts for long time periods, upon which the Company's survival depends.

(b) CIA techniques are only an aid to good business intuition but we must avoid prejudice, therefore always do AA and PFD early enough to avoid Emotional Investment, in an alternative which may not be the best available:

(c) Company's capital budgeting system helps managernent to select a portfolio of capital investments that provide both short term and long term profitability, EVA, SVA and cash flow.

6/204 12.15 LEARNING PATTERNS

APPROACH TO RISK

Conservative estimatesShorter horizonsHigh DRLow TV’sLow expected cash flows

6/205 12.15 LEARNING PATTERNS

SYSTEMS

Search Analysis Criteria Decision Audit

… Search etc. etc .

6/206 12.15 LEARNING PATTERNS

DICH

DICH - CP - MOI

AA PFD EI

Q + NQ = D

6/207 12.15 LEARNING PATTERNSI

BALANCED APPROACH

Expansion Decisions

CIA - Replacement and Product Line Decisions

Strategic Decisions

SOUND BUSINESS JUDGEMENT

CONCLUSIONS

6/208 12.16 CONCLUSiONS

(a) CIA is useful for practical decision-making because it sharpens business intuition as to which major projects should be undertaken.

(b) CIA is a systematic analysis which explores the sensitivity of projects to different assumptions and seeks all alternatives.

6/208 12.16 CONCLUSiONS

(c) CIA must fit strategy; it must be part of long term planntng; choose not just individual projects, but a portfolio of investment opportunities.

(d) Capital Budgeting System should provide CIA with appropriate forms, procedures, and post decision audits.

6/208 12.16 CONCLUSiONS

(e) Sophisticated methods of CIA using probability, expected values, dispersion. Monte Carlo methods, decision trees, computers, etc. are only as good as the underlying assumptions.

(f) Approach:

- Examine.all alternatives. - Get major figures right. - Re-check assumptions.

Note: “Smell” the results - if they don't smell right, do them again (or get someone else to do them! )

6/208 12.16 CONCLUSiONS

(g) Don't be too conservative. If you keep that old machine too long you are probably paying for the new. one - without getting the benefit of it!'1

(h) Remember shareholders and management do not have the same goals; management is more concerned with cash flow.

(I) Payback does indicate when cash will be available again for new opportunities. However, quick payback alone may reject good long term investment opportunities.

6/208 12.16 CONCLUSiONS

(j) Provide for risk - political, economic, technical and business the Manager must feel responsible for his judgement of the experts: and the ASSUMPTIONS - even when ~ with the best of intentions - they turn out to be wrong!!

(k) Don't plan Qnly for the long term future - watch the effect on profits this year too.'

6/208 12.16 CONCLUSiONS

(l) DCF is to be used for large amounts over long time periods so don't "polish peanuts", however emotionally satisfying that may sometimes be.

(m) CIA is no substitute but only an aid to CREATIVE FINANCIAL MANAGEMENT, and GOOD BUSINESS JUDGEMENT in selecting a "Portfolio"~of projects for both short and long term profitability, cash flow, EVA and SVA.

6/208 12.16 CONCLUSiONS

REPEATING …. THE KEY MESSAGE...

(l) DCF is to be used for large amounts over long time periods so don't "polish peanuts", however emotionally satisfying that may sometimes be.

(m) CIA is no substitute but only an aid to CREATIVE FINANCIAL MANAGEMENT, and GOOD BUSINESS JUDGEMENT in selecting a "Portfolio"~of projects for both short and long term profitability, cash flow, EVA and SVA..

FINAL NOTES

FINAL NOTES

THIS ENDS OUR PROGRAM.

WE HOPE IT HAS INSPIRED YOU … TO DEVELOP YOUR SKILLS BY PRACTICAL APPLICATION.

THANK YOU FOR YOUR INtEREST AND HARD WORK.

FINAL NOTES

KEEP THE GLOSSARY HANDY AS A DAILY REFERENCEFOR CIA LANGUAGE AND CONTINUE YOUR STUDIES.

FOR ANY HELP NEEDED CONTACT US AT: : [email protected] WHICH PROVIDES A 24 HOUR SERVICE

WE HOPE YOU ENJOYED THE AGL LEARING EXPERIENCE AND WILL COME AGAIN FOR FURTHER TRAINING IN THE EXCITING FIELD OF FINANCE AND ACCOUNTING.