20

The Industrial Gas Industry A Wealth of Opportunities Dave Taylor Vice President, Equipment and Energy Citigroup Chemicals for the Non-Chemist Conference New York City December 3, 2007

| Date post: | 12-Nov-2014 |

| Category: |

Economy & Finance |

| Upload: | finance26 |

| View: | 533 times |

| Download: | 2 times |

The Industrial Gas IndustryA Wealth of Opportunities

Dave TaylorVice President, Equipment and Energy

Citigroup Chemicals for the Non-Chemist ConferenceNew York CityDecember 3, 2007

2

ForwardForward--Looking Statements Looking Statements NOTE: This presentation contains “forward-looking statements” within the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on management’s reasonable expectations and assumptions as of the date of this presentation regarding important risk factors. Actual performance and financial results may differ materially from projections and estimates expressed in the forward-looking statements because of many factors, including, without limitation, overall economic and business conditions different than those currently anticipated; future financial and operating performance of major customers and industries served by Air Products; the impact of competitive products and pricing; interruption in ordinary sources of supply of raw materials; the ability to recover unanticipated increased energy and raw material costs from customers; costs and outcomes of litigation or regulatory activities; consequences of acts of war or terrorism impacting the United States’ and other markets; the effects of a pandemic or epidemic or a natural disaster; charges related to portfolio management and cost reduction actions; the success of implementing cost reduction programs and achieving anticipated acquisition synergies; the timing, impact and other uncertainties of future acquisitions or divestitures or unanticipated contract terminations; significant fluctuations in interest rates and foreign currencies from that currently anticipated; the impact of new or changed tax and other legislation and regulations in jurisdictions in which Air Products and its affiliates operate; the impact of new or changed financial accounting standards; and the timing and rate at which tax credits can be utilized. The company disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained in this presentation to reflect any change in the company’s assumptions, beliefs or expectations or any change in events, conditions or circumstances upon which any such forward-looking statements are based.

3

Industrial Gas Industry: Size and Industrial Gas Industry: Size and Market ShareMarket Share

Total Industrial Gases Market: $51B in 2006

Electronics & Performance

Materials(22%)

ALPraxairAPNippon SansoLindeMGAirgasOther

2006, 100% basis (BOC added to Linde not adjusted for 2007 disposals)

4

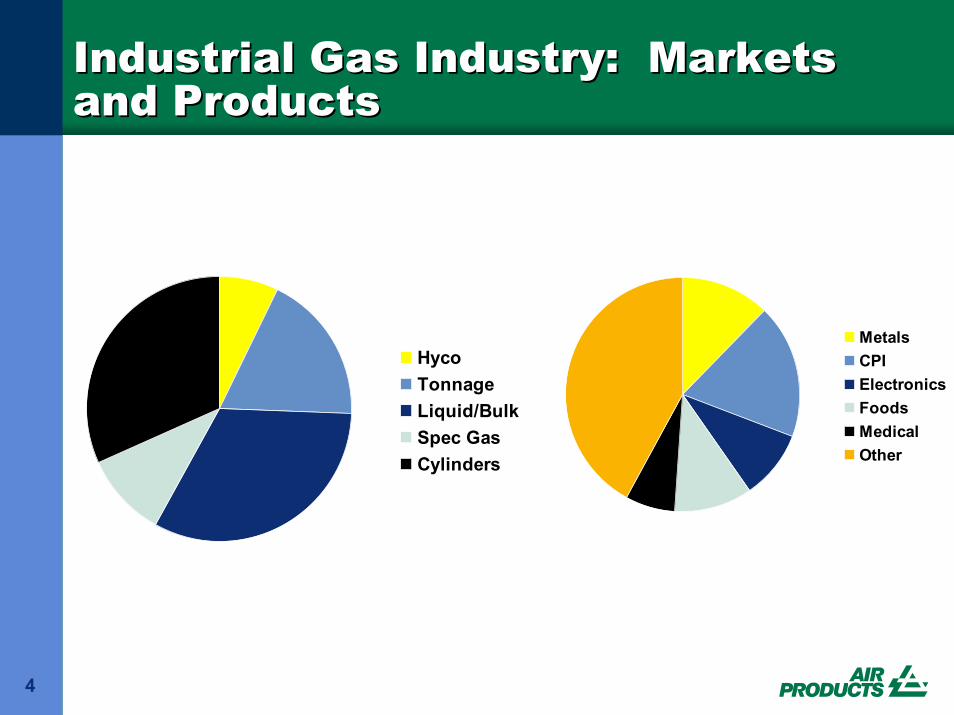

Industrial Gas Industry: Markets Industrial Gas Industry: Markets and Productsand Products

Electronics & Performance

Materials(22%)

HycoTonnageLiquid/BulkSpec GasCylinders

MetalsCPIElectronicsFoodsMedicalOther

5

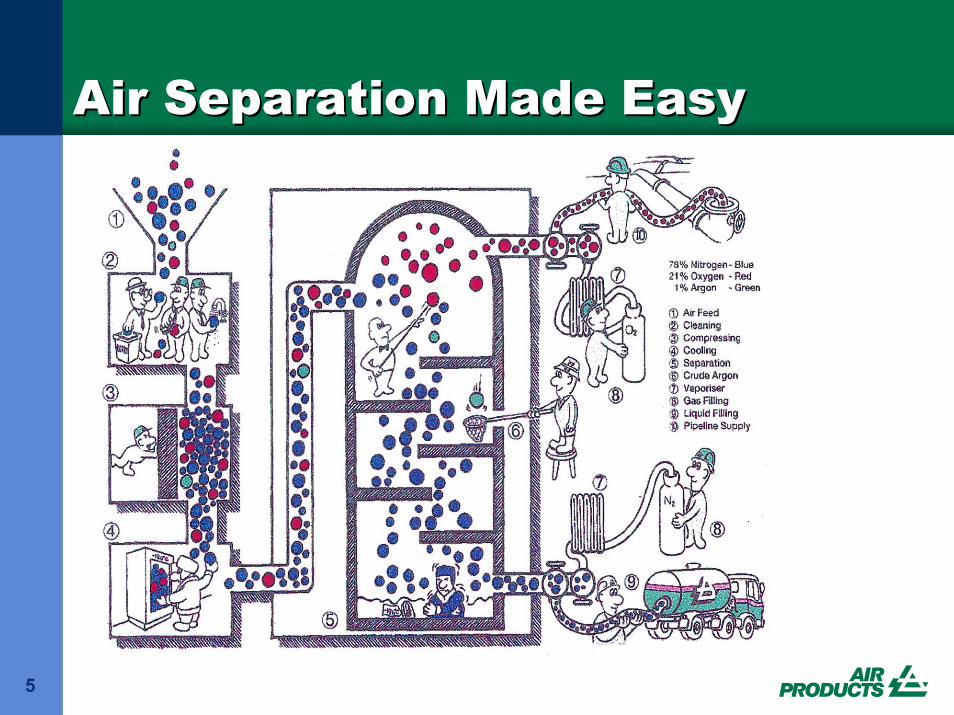

Air Separation Made EasyAir Separation Made Easy

6

What drives the use of What drives the use of industrial gases?industrial gases?

Provide energy efficiencyExpand capacityImprove end-product qualityImprove environmental performance

7

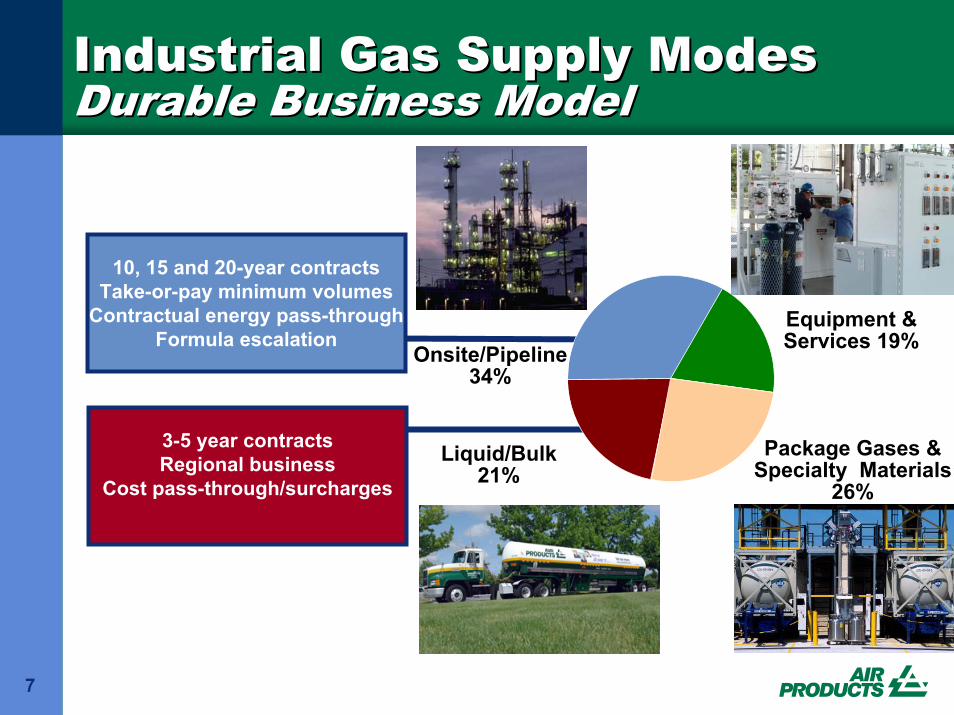

Industrial Gas Supply Modes Industrial Gas Supply Modes Durable Business ModelDurable Business Model

Package Gases & Specialty Materials

26%

Onsite/Pipeline34%

Liquid/Bulk21%

10, 15 and 20-year contractsTake-or-pay minimum volumes

Contractual energy pass-throughFormula escalation

3-5 year contractsRegional business

Cost pass-through/surcharges

Equipment & Services 19%

8

Merchant GasesMerchant Gases

Liquid/bulk, cylinder and small onsite gases to diverse industrial marketsGlobal business model– Marketing– Application development– Supply chain

Local execution– Logistics– Sales and pricing– Customer service

Opportunities for continued growth– Eastern Europe & Asia growth

Local Business

Regional Roles/Global Collaboration

Global Differentiators

Margin Improvement

& Growth

9

Merchant Gases ApplicationsMerchant Gases Applications

Nitrogen

Cryogenic CoolingCryogenic GrindingFood FreezingFood PackagingInertingMetals ProcessingMaterials Testing

Oxygen

Respiratory TherapyCombustionCutting and WeldingPulp BleachingWastewater TreatmentRocket Propellant

Argon

Heat TreatingMetal RefiningProtective AtmosphereWeldingPressure TestingBlanketingInerting

10

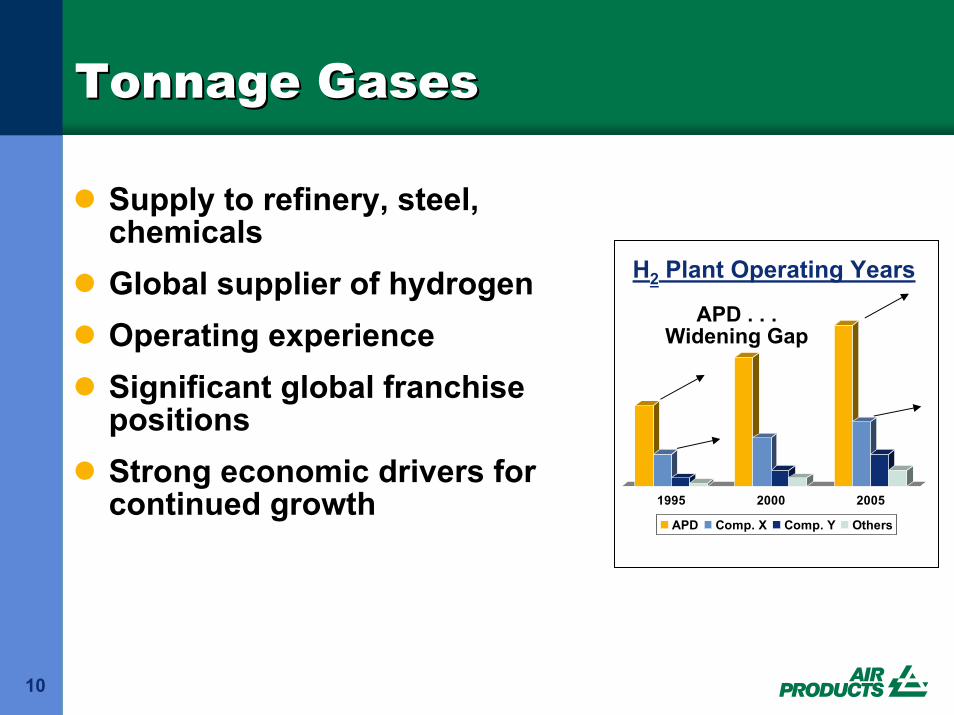

1995 2000 2005

APD Comp. X Comp. Y Others

H2 Plant Operating Years

APD . . .Widening Gap

Tonnage GasesTonnage Gases

Supply to refinery, steel, chemicalsGlobal supplier of hydrogenOperating experience Significant global franchise positionsStrong economic drivers for continued growth

11

How Hydrogen is ProducedHow Hydrogen is Produced

CO + H2O H2 + CO2CH4 + H2O 3H2 + CO

Conventional H2

H2 PRODUCTSHYDRO-DESULFURIZATION

HT / LTSHIFTS

CO2REMOVAL Methanation

N.G. FUEL

REFORMER

STEAMCO2

PRODUCTH2 Rec.

94-97%

Natural Gas and Light Hydrocarbons

12

Regulatory Growth DriversUS, W. Eur. Clean FuelsTransport FuelsUSGC Hvy, sour crudes

Economic Climate DriversMargins (Economics)Global incr. conversionReplacement SMR’sCrude capacity growthGlobal heavy sour crudesGlobal clean fuelsGeographically dispersed

Glo

bal R

efin

ing

Cap

acity

701995 2005 2016

MM BPD

~$5 B

80

100

90

of On purposeH2 Investments*

~$13 Bof on purpose

H2 investments*

Represents 10 Billion SCFDNew Capacity

*Note: Make plus Buy Market Opportunities

Significant Refinery HSignificant Refinery H22 GrowthGrowthForecasted 2006Forecasted 2006--20162016 Updated view

13

Plaquemine

Geismar

Lake Pontchartrain

Convent

Cosmar

Taft

Geismar10

NolaNew Orleans

Chalmette

LouisianaBaton Rouge

BPCarson

ShellWilmington

DominguezChannel

Conoco PhillipsWilmington

Conoco Phillips Carson

VAN NESSAVE.

SepulvedaBlvd

Anaheim Street

91

LongBeachArpt.

190th

St.

Carson H2

Wilmington H2

710

405

405

110

1

110

SouthernCalifornia

APD HyCO facilitiesH2 pipelineCO pipelineSyngas pipeline

1414630630

1414

1616

2121

CN RAIL Edmonton,Canada

SherwoodPark

Petro-CanadaImperial Oil

1616

Mont Belvieu

Port Arthur

Bayport

Battleground

Pasadena

City of Houston

Clear Lake

Baytown 2

LaPorte

Texas City

10

45

610

Lake CharlesBeaumont

225

73

6910

Zwijndrecht

To Moerdijk

Europoort

Pernis

Botlek

Rotterdam

40

40

Corunna

Suncor

Shell Refinery

40

ST.CLAIR RIVER

Air Products Canada

SarniaCanada

ValeroWilmington

Texas

Strong Hydrogen Pipeline PositionsStrong Hydrogen Pipeline Positions

TarragonaRefinery

14

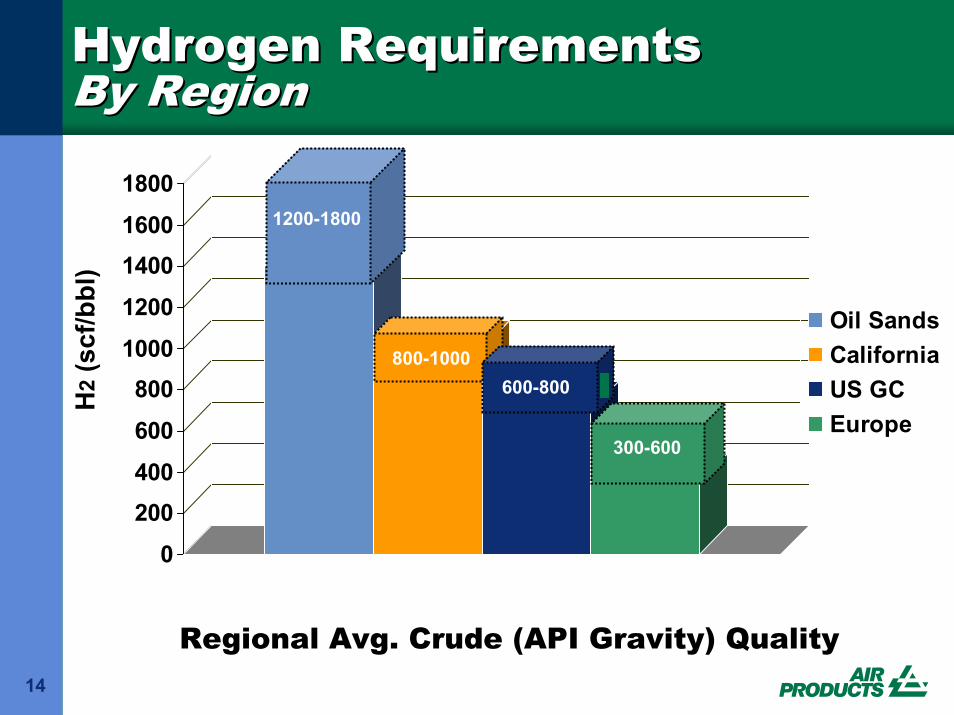

HydroHydrogen Requirements gen Requirements By RegionBy Region

18-20 22-25 26-30 30-35

H2

(scf

/bbl

)

0

200400

600

8001000

1200

14001600

1800

Oil SandsCaliforniaUS GCEurope

1200-1800

800-1000600-800

300-600

Regional Avg. Crude (API Gravity) Quality

15

APD is one of the largest suppliers of oxygen to gasification facilities around the world (>10 large units)Designed, built, own, and operate units in Texas for syngas, H2 and CO for pipeline systems:– NG based POX units (LaPorte)– Syngas cleanup / separation

facilities from heavy oil POX unit (Baytown)

Recently announced Tonnage relationship on O2 and H2:– Eastman Gasifier - Texas– Wison II in China – BP Clean Power in California

Gasification: Gasification: An Exciting Growth OpportunityAn Exciting Growth Opportunity

16

Equipment and EnergyEquipment and Energy

Broad customer base– Oil & gas, utilities, chemicals

and metalsProducts– LNG heat exchangers, large air

separation units, hydrocarbon separators, helium containers, hydrogen fueling systems…

Strategy– Leverage existing relationships– Develop energy projects– Leverage engineering

technology and products to grow gases businesses

17

X

CoalCoal--FiredFiredOxyfuel BoilerOxyfuel Boiler

Furnace

Coal~4,000 tpd

Stack

Turbines 500 MWe

Flue Gas Recycle

Oxygen~9000 tpd

AP CO2 Purification & Compression

~9,000+ tpd CO295-99+% purity

at 110 bar

65-75% CO2

Flexible AP CO2 system - 90-98% CO2 capture

X

AirAir

18

Extending Gas Expertise into Extending Gas Expertise into Other IndustriesOther Industries

Electronics and Performance Materials represent ~20% of our revenuesThe segment is underpinned by technology, innovationFranchise positions / global leadershipStrategic positions with leading customers Operationally excellent global supply chainLeading edge applied technology, new products

19

The Industrial Gas Industry The Industrial Gas Industry ProvidesProvides……

Great track record of growthSolid returnsStrong project backlog, good future insightLeadership in energy opportunitiesStrong applications growthMost importantly, fiscal stability in uncertain times

20

tell me morewww.airproducts.com

Thank you