22

ANNA RAPPAPORT CONSULTING After the Tsunami: The Departure of the Baby Boom Presented by Anna Rappaport University of Chicago Management Conference May 18, 2007

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | francine-knight |

| View: | 219 times |

| Download: | 1 times |

ANNA RAPPAPORT CONSULTING

STRATEGIES FOR A SECURE RETIREMENTSM

After the Tsunami:The Departure of the Baby Boom

Presented by Anna Rappaport

University of Chicago Management Conference

May 18, 2007

Presentation at GSB - Graduate School of Business May 18, 2007

2

Boomers in the Third Age:The Big Picture Today

Dec

line

of

DB

Pla

ns

Longer

Life Spans

LittleLonger TermThinking

Wha

t is

Long

evity

Ris

k?

Working in

Retirement

More People

at Retirem

ent

Ages

Premature

Retirement

Risk

Les

s R

etir

eeH

ealt

h B

enef

its

+

Hig

her

Co

sts

Presentation at GSB - Graduate School of Business May 18, 2007

3

Puzzles around longer work

More than 7 in 10 people say they want to work in retirement

About 4 in 10 people retire earlier than planned– Don’t plan for premature retirement risk

Higher age displaced workers take longer to get jobs Other research indicates that older applicants get fewer

call backs – Age discrimination? Will this change as population

ages? Future: unknown effect of longer work on retirement

patterns

Presentation at GSB - Graduate School of Business May 18, 2007

4

Our Goals Today

Think about future challenges with job content, job structure, and employees seeking phased retirement

Understand forces driving change and uncertainty Think about possible products/services

Presentation at GSB - Graduate School of Business May 18, 2007

5

Agenda

Context Practical Issues around Meeting Talent Needs Market Opportunities

Presentation at GSB - Graduate School of Business May 18, 2007

6

Context: Demographics

New ways to think about life cycle– Third age: period between full time work and total

retirement– During transition period

Some work and more leisure Supplement earnings with retirement resources Looks like traditional cyclical life plan

Key trends– Living longer– Healthy longer but not forever– Boomers: better education than groups before

Presentation at GSB - Graduate School of Business May 18, 2007

7

Context: Probability of Living to 80, 90, 100 Projected to 2025

Projection to 2025 – 1983 Mortality projected 40 years

Survival Age Female

65Male 65

Both Survive

Either Survive

survive to 80 0.84 0.69 0.58 0.95

survive to 90 0.52 0.30 0.16 0.67

survive to 100 0.14 0.04 0.01 0.18

Presentation at GSB - Graduate School of Business May 18, 2007

8

Context: The Boomers vs. the Prior Cohort

More Boomers—very large cohort Two distinct groups—early vs. late Boomers Boomers have higher expectations More Boomers are divorced

– 13% of men age 55-64 vs. 10% in 1994 and 6% in 1984– 18% of women vs. 13% and 9%

After many years of earlier retirement, later retirement Pension coverage has shifted to defined contribution More workers age 55-64 have health insurance (because

more women are covered) More people own long-term care insurance

Presentation at GSB - Graduate School of Business May 18, 2007

9

Context: Boomers—Greater Income & Wealth Dispersion vs. Prior Cohorts

Big gains in median income for top quartile, virtually flat for others Increase in median wealth for college graduates, decline for others

Median Wealth

1994 2004

College Graduates $305,000 $317,000

High School Graduates $145,000 $115,000

Net Worth

1994 2004

College Graduates $146,000 $128,000

High School Graduates $54,000 $30,000

Decline in net worth, excluding home equity, across all groups

Presentation at GSB - Graduate School of Business May 18, 2007

10

Context: New Ways to WorkWhat is Evolving: Phased Retirement

No accepted definition—may permit partial or full pension payments

Allows mature workers to work on reduced or modified basis before retirement (phasing pre-retirement)

Allows rehire of retirees (phasing post-retirement) Modified work may mean change of schedule, place or

duties Can be formal or informal arrangement Perspective of employer, policymaker and individual differ

Question: Is all “working in retirement” a form of phased retirement?

Presentation at GSB - Graduate School of Business May 18, 2007

11

Context: The work and retirement experience

People say they want to work longer Many work after “retirement”

– Often part-time or part-year Of those who are not in labor force at 50-61

– 67% of men are disabled– 40% of women are disabled

New job options and innovative practices are needed– Relationship alternatives– Restructuring of duties– Scheduling alternatives– Place alternatives

Presentation at GSB - Graduate School of Business May 18, 2007

12

Context:Pre-retirees expect to work longer

How old were you when you retired/began to retire from your primary occupation?/At what age do you expect to retire from your primary occupation? (Among retirees and employed pre-retirees)

Age CategoryRetirees (%) Pre-retirees (%)

2005 (n=302) 2005 (n=253)Under age 55 34 2

55 to 61 29 12

62 to 64 20 18

65 5 21

66 or older 8 20

Will not retire -- 13

Doesn’t apply 3 --

Don’t know 2 15

Source: Society of Actuaries, 2005 Risks and Process of Retirement Survey

Presentation at GSB - Graduate School of Business May 18, 2007

13

Utilizing Talent: Practical issues

Best option for phased retirement Phasing a little vs. phasing a lot Example: bank teller Example: research scientist Defining your talent needs Contracting issues

Presentation at GSB - Graduate School of Business May 18, 2007

14

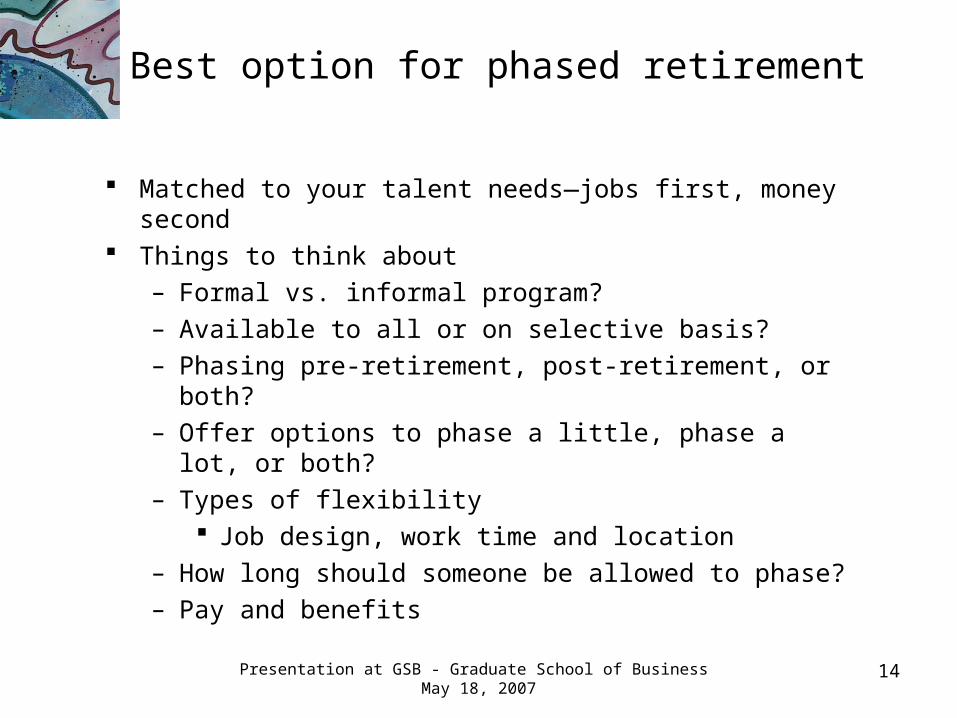

Best option for phased retirement

Matched to your talent needs—jobs first, money second Things to think about

– Formal vs. informal program?– Available to all or on selective basis?– Phasing pre-retirement, post-retirement, or both?– Offer options to phase a little, phase a lot, or both?– Types of flexibility

Job design, work time and location– How long should someone be allowed to phase?– Pay and benefits

Presentation at GSB - Graduate School of Business May 18, 2007

15

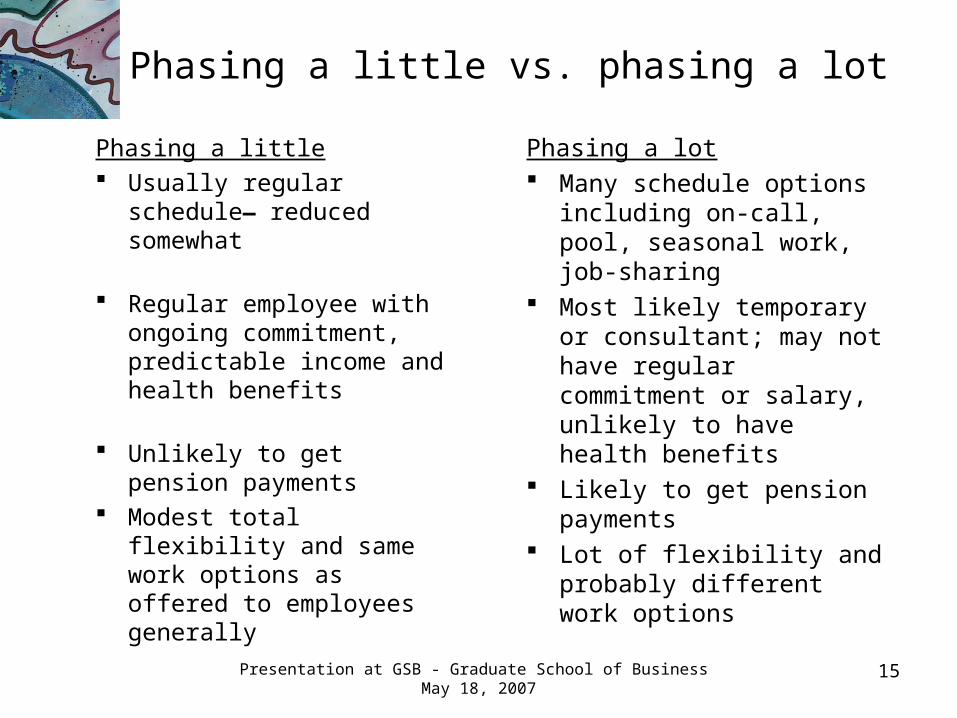

Phasing a little vs. phasing a lot

Phasing a little Usually regular schedule—

reduced somewhat

Regular employee with ongoing commitment, predictable income and health benefits

Unlikely to get pension payments

Modest total flexibility and same work options as offered to employees generally

Phasing a lot Many schedule options

including on-call, pool, seasonal work, job-sharing

Most likely temporary or consultant; may not have regular commitment or salary, unlikely to have health benefits

Likely to get pension payments

Lot of flexibility and probably different work options

Presentation at GSB - Graduate School of Business May 18, 2007

16

Bank teller

Phasing pre-retirement Works 3 or 4 days per week

on regular basis as regular employee

Works at regular work location

In future can be paid partial pension after age 62

Phasing post-retirement Work as fill-in during

vacations or on-call during the year

Work as temporary or through a retiree pool

In a bank with multiple branches, may work at different locations

Paid pension and appropriate compensation for work performed

Presentation at GSB - Graduate School of Business May 18, 2007

17

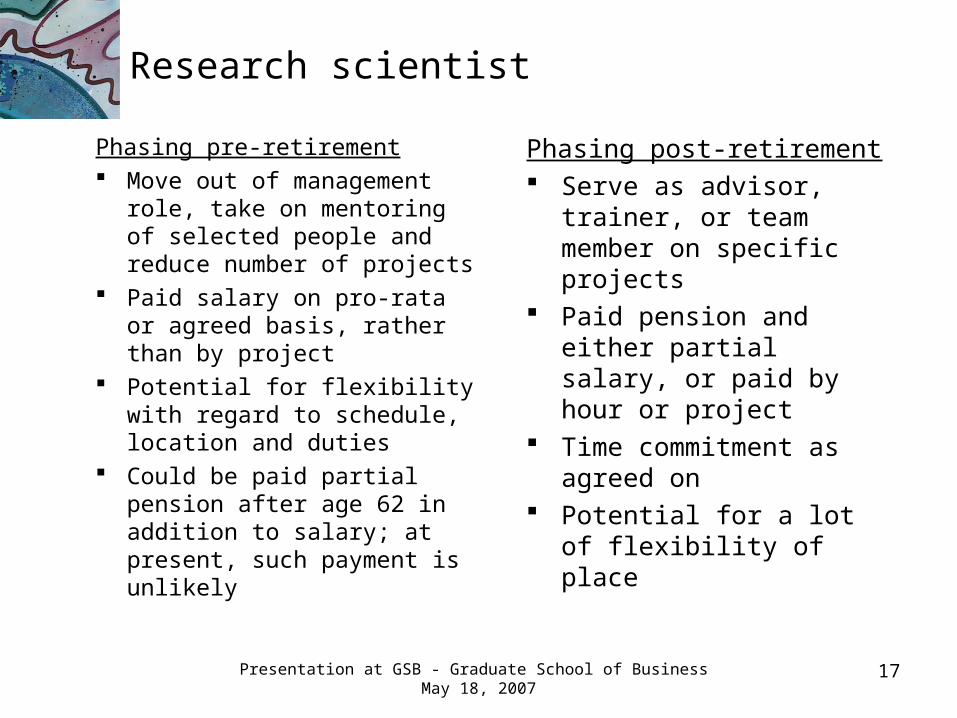

Research scientist

Phasing pre-retirement Move out of management

role, take on mentoring of selected people and reduce number of projects

Paid salary on pro-rata or agreed basis, rather than by project

Potential for flexibility with regard to schedule, location and duties

Could be paid partial pension after age 62 in addition to salary; at present, such payment is unlikely

Phasing post-retirement Serve as advisor, trainer,

or team member on specific projects

Paid pension and either partial salary, or paid by hour or project

Time commitment as agreed on

Potential for a lot of flexibility of place

Presentation at GSB - Graduate School of Business May 18, 2007

18

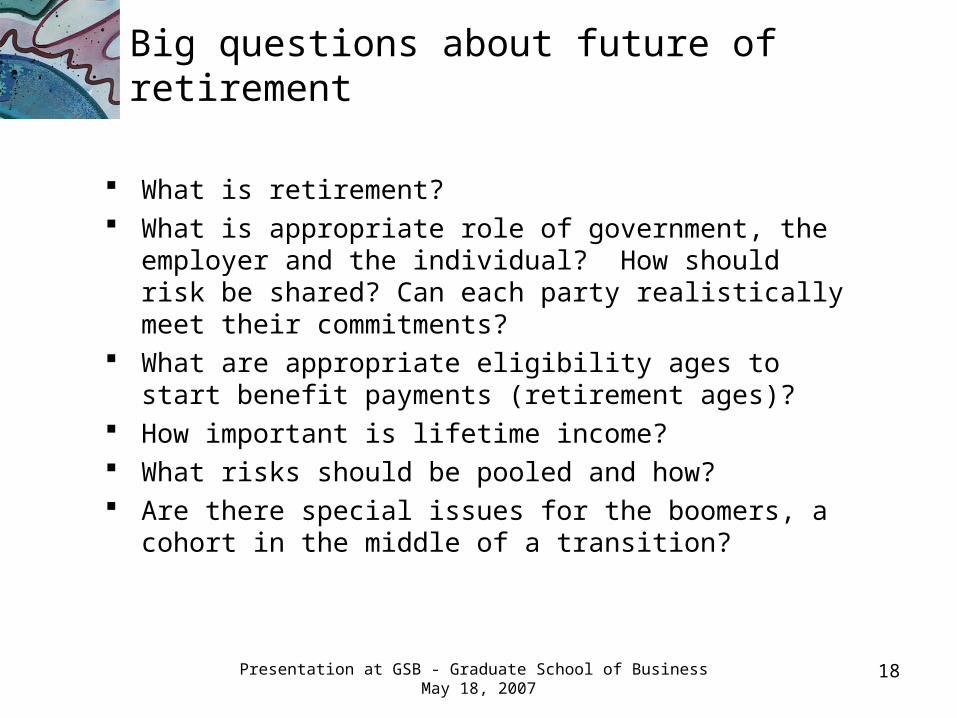

Big questions about future of retirement

What is retirement? What is appropriate role of government, the employer and

the individual? How should risk be shared? Can each party realistically meet their commitments?

What are appropriate eligibility ages to start benefit payments (retirement ages)?

How important is lifetime income? What risks should be pooled and how? Are there special issues for the boomers, a cohort in the

middle of a transition?

Presentation at GSB - Graduate School of Business May 18, 2007

19

Checklist for new approaches to using Boomer talent

Define new work options and think about phased retirement Build the program on solid needs analysis, identifying talent

issues and employee preferences Integrate with talent management strategy and align with

culture Integrate with knowledge transfer Communicate with business units Align health and pension benefits Give supervisors and division managers enough discretion Keep paperwork well defined and easy Start small, evaluate and refine

Presentation at GSB - Graduate School of Business May 18, 2007

20

Products for the Future:Think about Market Segments

High net worth – Asset management and estate conservation key– Nothing really changes—but there are more people

Middle group– Need to marry risk and asset management– For many of them, huge challenge to manage on their

own in retirement– Through employer is good way to reach them– Not enough money for much personal advice– New opportunities

Lower income group (40% of old age women alone have only Social Security)– Key is the social safety net

Presentation at GSB - Graduate School of Business May 18, 2007

21

Products for the Future:Opportunities that Address the Risks

Marry asset and risk management Distribution options and defaults—401(k) plans

– Risk protection linked to asset pool– Dream default option

Managing longevity risk in systematic way– Longevity insurance—deferred annuity to age 85 or a

similar age – Combination products = annuity+ long-term care

Think about dollar cost averaging without requiring multiple purchase decisions

Focus on how to get better risk pools Better planning tools and help for the middle market

22

Phone: 312-642-4720Fax: 312-642-4330

ANNA RAPPAPORT CONSULTING

STRATEGIES FOR A SECURE RETIREMENTSM

![Index [lyric.co.uk] · Nicholas Tennant Peter Brian Vernel Konstantin Cast Literal Translation by Helen Rappaport Associate Director Jude Christian Assistant Director Anna Crace ...](https://static.documents.pub/doc/80x56/60a89b24b80a092c4c569c66/index-lyriccouk-nicholas-tennant-peter-brian-vernel-konstantin-cast-literal.jpg)