61

ANNEX 14 Feasibility Study and GHG Mitigation & CDM Potential

ANNEX 14

Feasibility Study and GHG Mitigation & CDM Potential

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 1

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

EuropeAid/129506/L/ACT/TH Thailand-EC Cooperation Facility – Phase II (TEC II)

GRANT CONTRACT - EXTERNAL ACTIONS OF THE EUROPEAN UNION -

DCI-ASIE/2010/242-677

Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)

FEASIBILITY STUDY AND GHG MITIGATION & CDM POTENTIAL

Beneficiary/Applicant: World Alliance for Thai Decentralised Energy

(WADE THAI), Thailand

Partner : World Alliance for Decentralised Energy (WADE), UK

Associate: Full Advantage Co., Ltd. (FA), Thailand

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 2

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

TABLE OF CONTENTS 1. INTRODUCTION ................................................................................................................ 7

1.1 BACKGROUND OF SMART GRID TECHNOLOGY ................................................ 8 1.1.1 DEFINITION AND COVERAGE OF SMART GRID TECHNOLOGY .............. 8 1.1.2 POWER GRID’S EVOLUTION INTO SMART GRID ......................................... 8 1.1.3 TECHNOLOGICAL INNOVATIONS THAT ENABLED SMART GRID .......... 9

1.2 BACKGROUND ON SMART GRID DEPLOYMENT IN THAILAND ................... 12 1.2.1 SMART GRID DEPLOYMENT INITIATIVE IN THAILAND: PEA SMART GRID ROADMAP ........................................................................................................... 12 1.2.2 PATTAYA CITY: GENERAL INFORMATION ................................................. 15

2. TECHNICAL OVERVIEW AND ANALYSIS ................................................................. 18 2.1 ADVANCED METERING INFRASTRUCTURE (SMART METERS) .................... 18

2.1.1 SMART METER STANDARD FEATURES AND FUNCTIONALITIES ......... 21 2.1.2 TECHNICAL ANALYSIS OF SMART METER: METER ACCURACY .......... 23 2.1.3 TECHNICAL ANALYSIS OF SMART METER: APPLICABLE FEATURES AND FUNCTIONALITIES............................................................................................. 24 2.1.4 CONCLUSION: ON SMART METER................................................................. 24

2.2 IEC 61850 STANDARD IMPLEMENTATION.......................................................... 25 2.2.1 SUBSTATION AUTOMATION (SA) AND IEC 61850 (See Figure 11) ............ 25 2.2.2 SUBSTATION INTEGRATION AND AUTOMATION: TECHNICAL ISSUES.......................................................................................................................................... 26 2.2.3 TECHNICAL ANALYSIS ON IEC 61850 STANDARD .................................... 28 2.2.4 CONCLUSION: ON IEC 61850 STANDARD ..................................................... 29

2.3 DISTRIBUTION FEEDER AUTOMATION (FEEDER REMOTE TERMINAL UNIT) ................................................................................................................................... 29

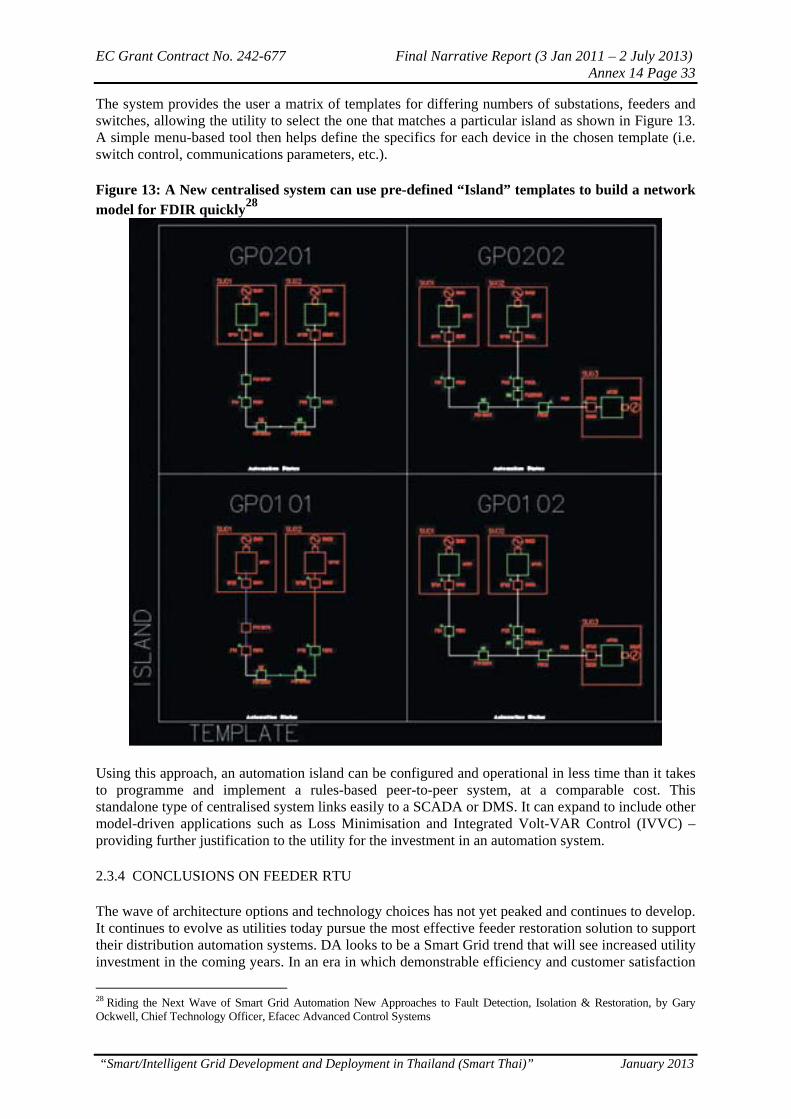

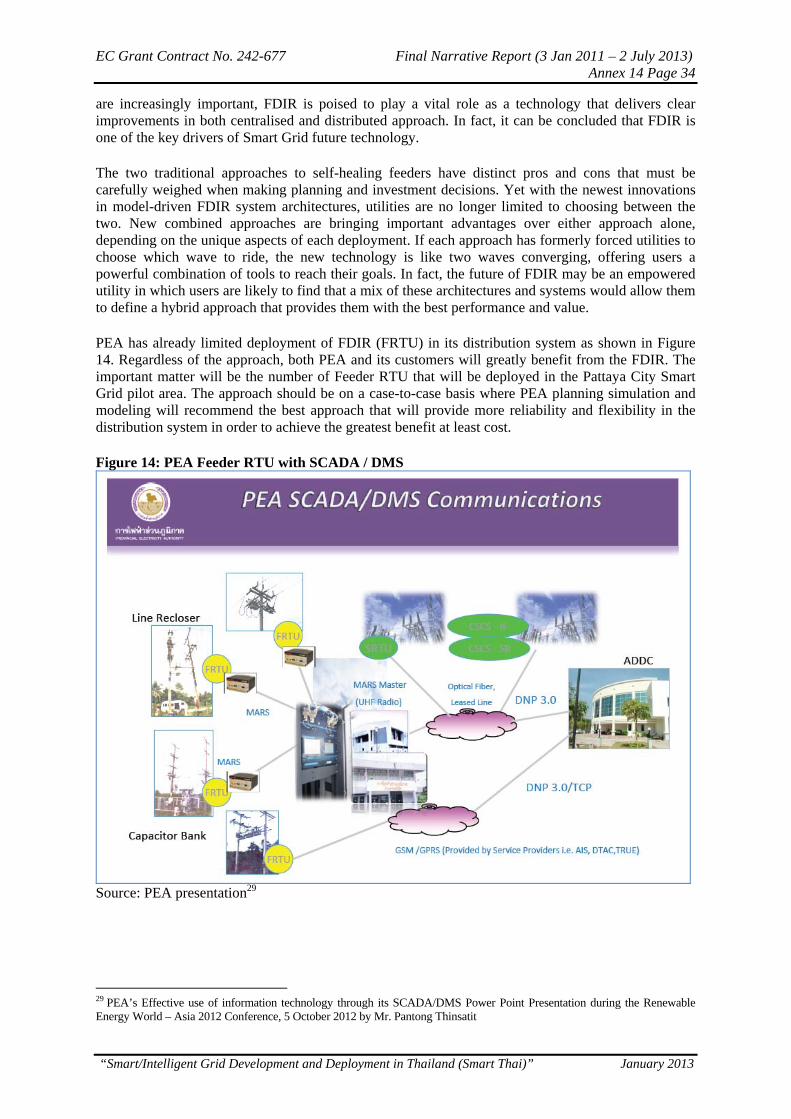

2.3.1 INTRODUCTION ON FEEDER AUTOMATION .............................................. 29 2.3.2 TECHNICAL ANALYSIS ON FEEDER RTU: DISTRIBUTED APPROACH.. 31 2.3.3 TECHNICAL ANALYSIS ON FEEDER RTU: CENTRALISED APPROACH 31 2.3.4 CONCLUSION: ON FEEDER RTU ..................................................................... 33

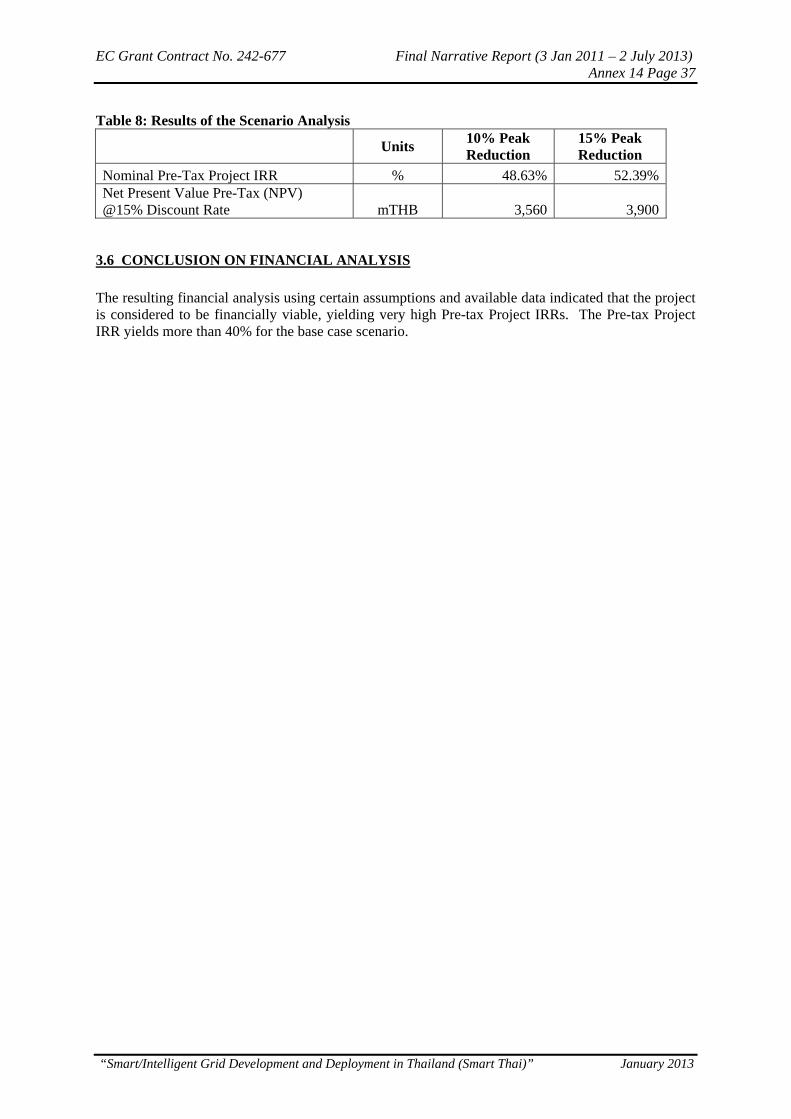

3. FINANCIAL ANALYSIS .................................................................................................. 35 3.1 INVESTMENT ............................................................................................................. 35 3.2 REVENUES .................................................................................................................. 35 3.3 EXPENSES ................................................................................................................... 36 3.4 RESULTS ..................................................................................................................... 36 3.5 SCENARIO ANALYSIS .............................................................................................. 36 3.6 CONCLUSION: ON FINANCIAL ANALYSIS.......................................................... 37

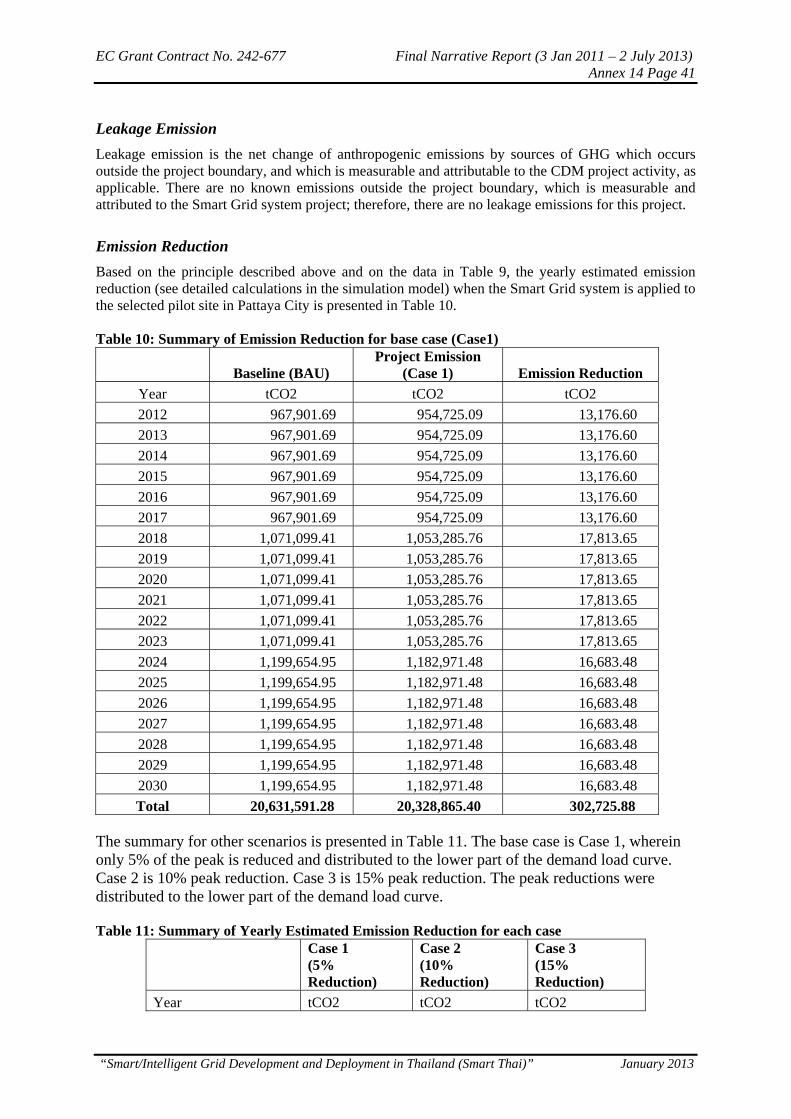

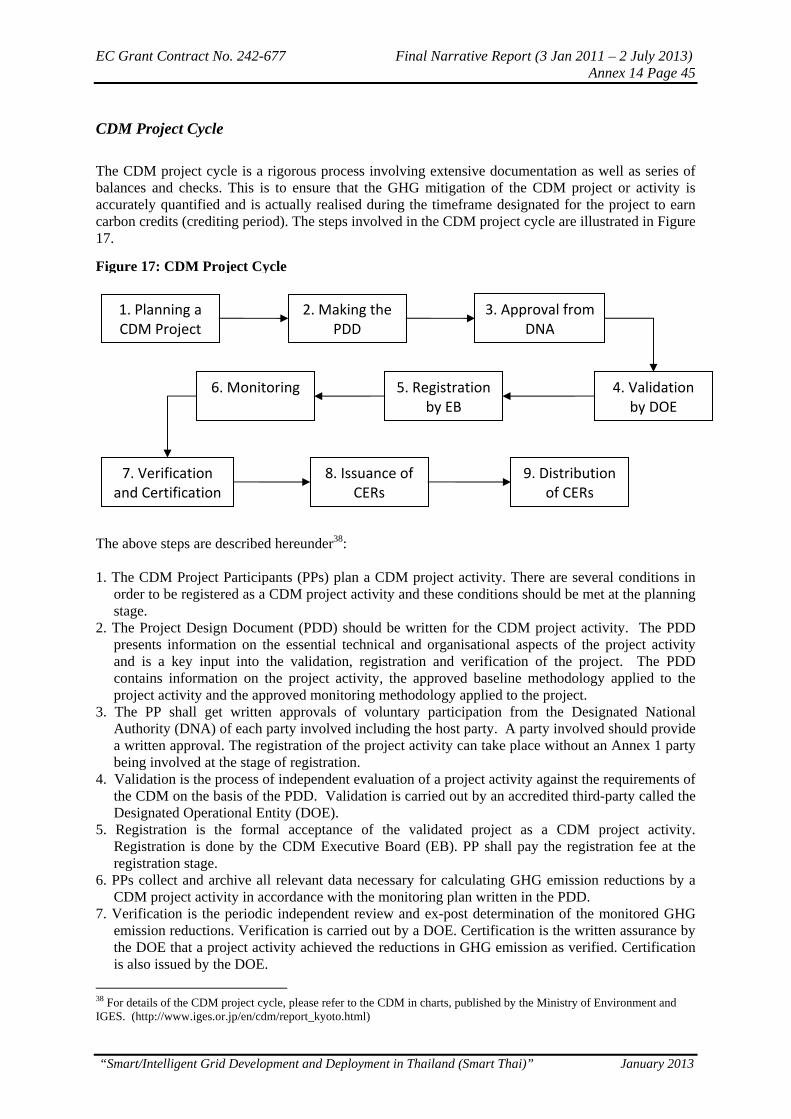

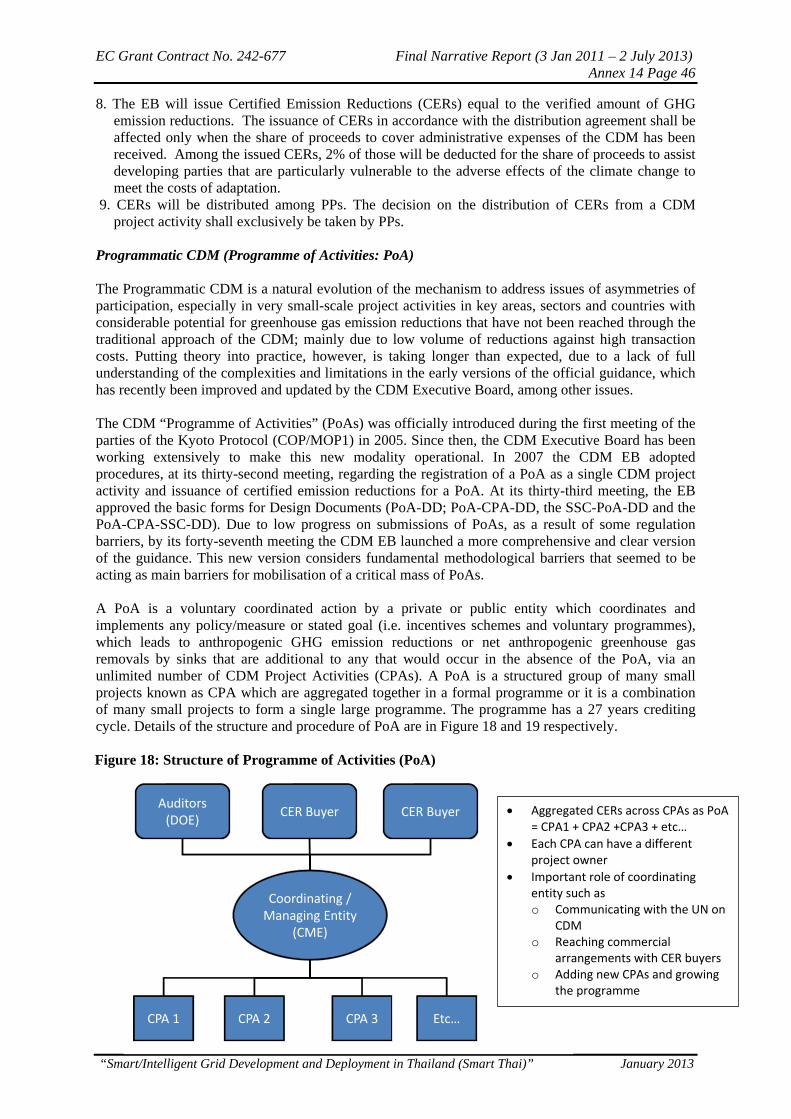

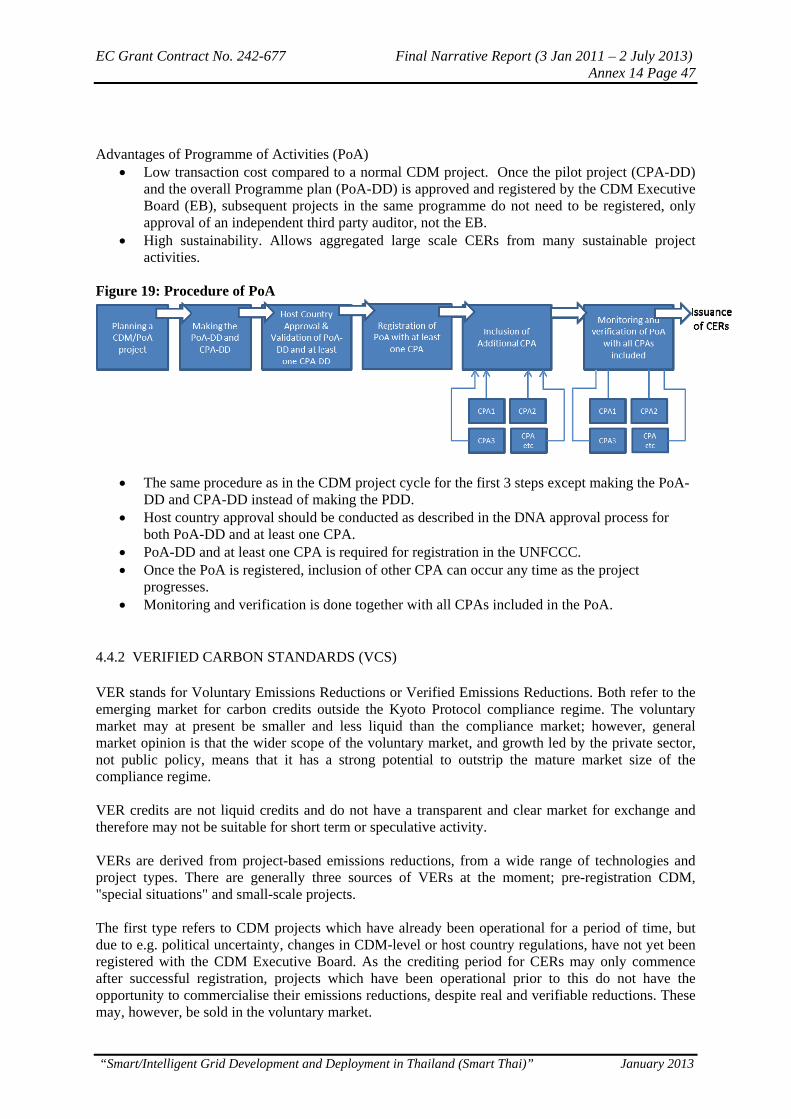

4. ENVIRONMENTAL ANALYSIS: GHG MITIGATION & CDM POTENTIAL ............. 38 4.1 BACKGROUND .......................................................................................................... 38 4.2 INTRODUCTION ........................................................................................................ 38 4.3 DETERMINATION OF EMISSION REDUCTION IN SMART GRID SYSTEMS .. 38

4.3.1 ESTIMATED EMISSION REDUCTION .............................................................. 40 4.4 CARBON EMISSIONS TRADING/MARKETS......................................................... 42

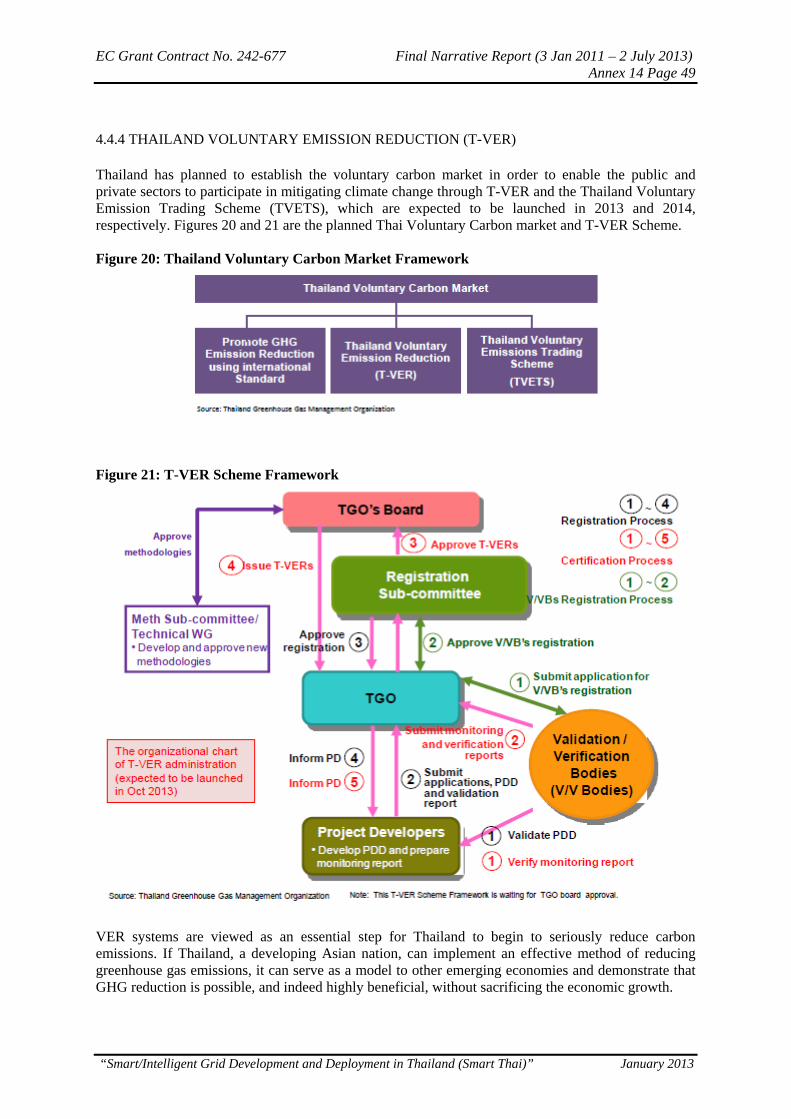

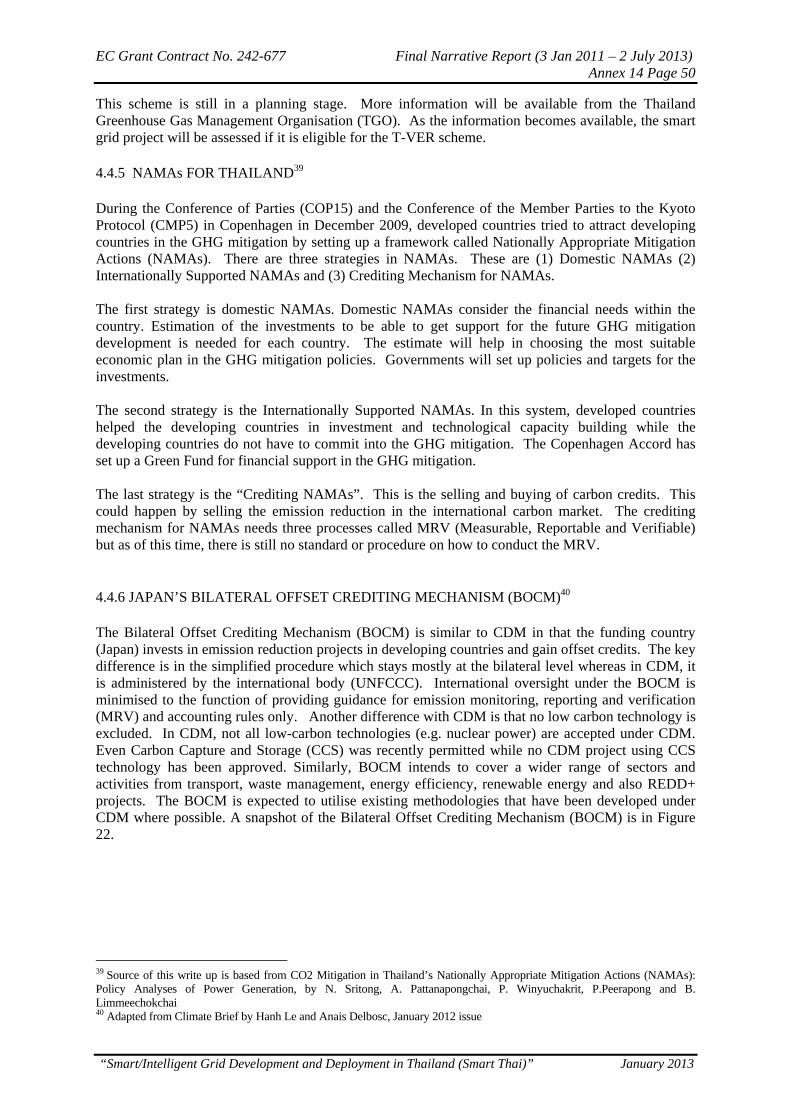

4.4.1 CLEAN DEVELOPMENT MECHANISM (CDM) ............................................. 43 4.4.2 VERIFIED CARBON STANDARDS (VCS) ....................................................... 47 4.4.3 GOLD STANDARD .............................................................................................. 48 4.4.4 THAILAND VOLUNTARY EMISSION REDUCTION (T-VER) ....................... 49

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 3

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

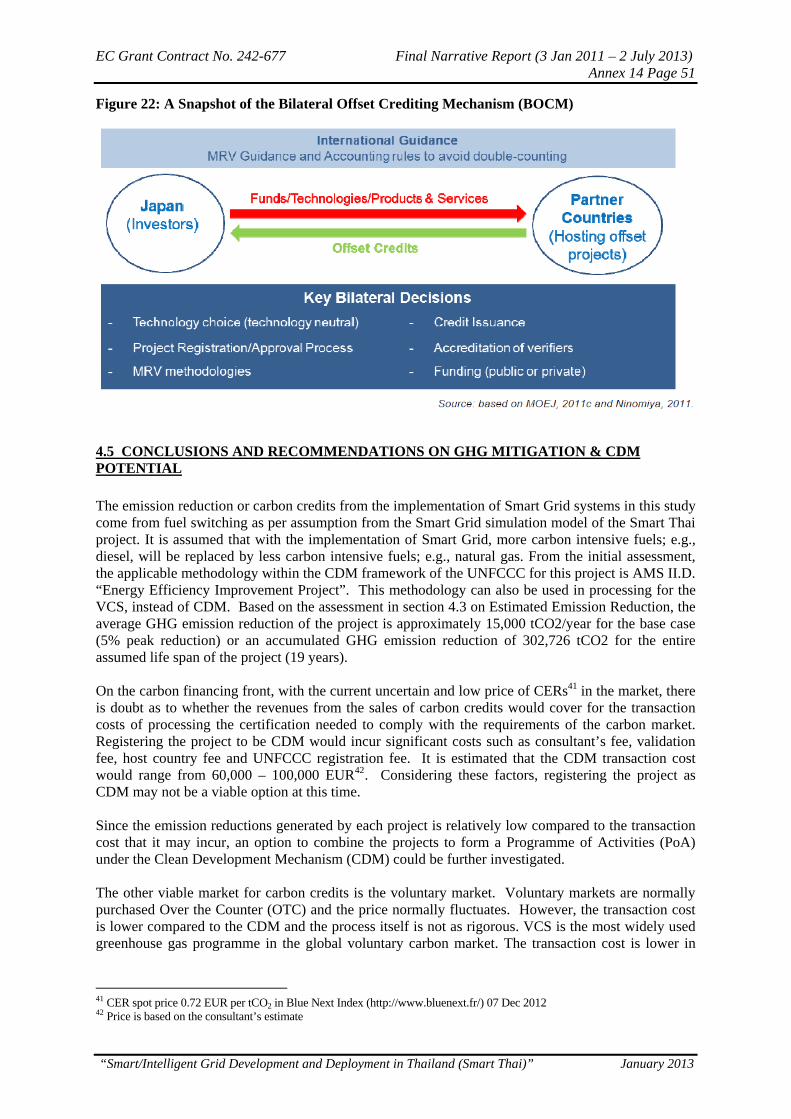

4.4.5 NAMAs FOR THAILAND ................................................................................... 50 4.4.6 JAPAN’S BILATERAL OFFSET CREDITING MECHANISM (BOCM) .......... 50

4.5 CONCLUSIONS AND RECOMMENDATIONS ON GHG MITIGATION & CDM POTENTIAL........................................................................................................................ 51

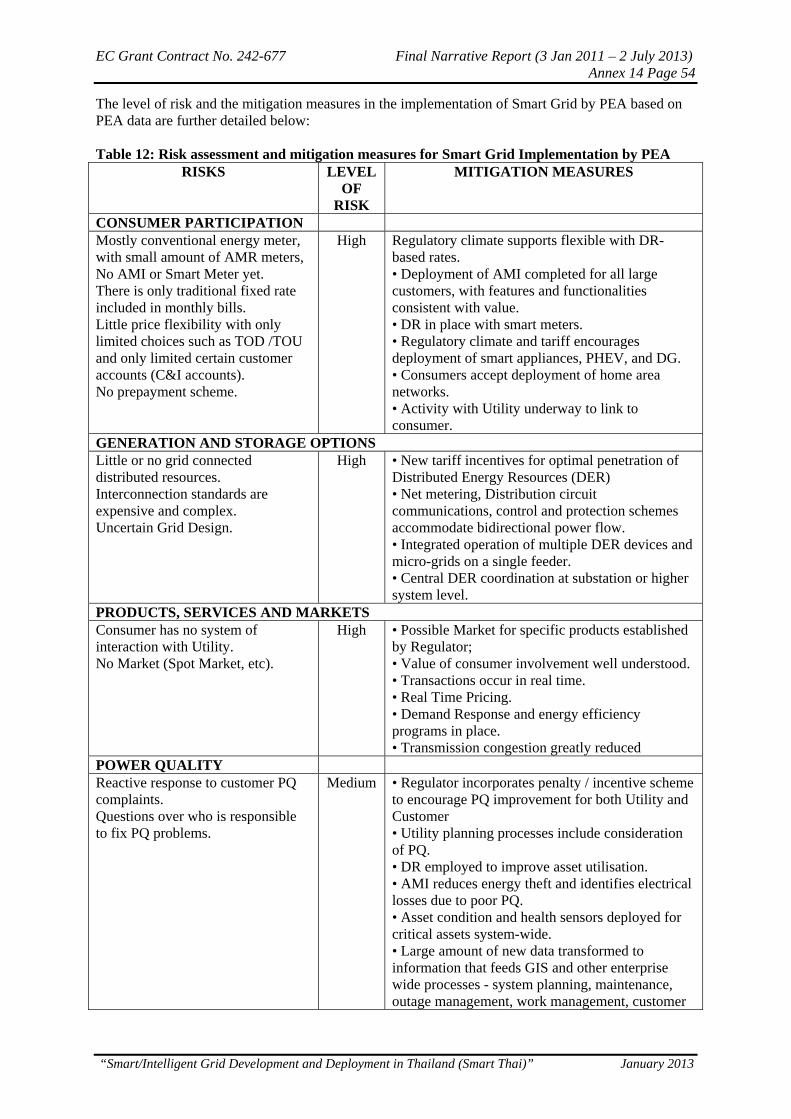

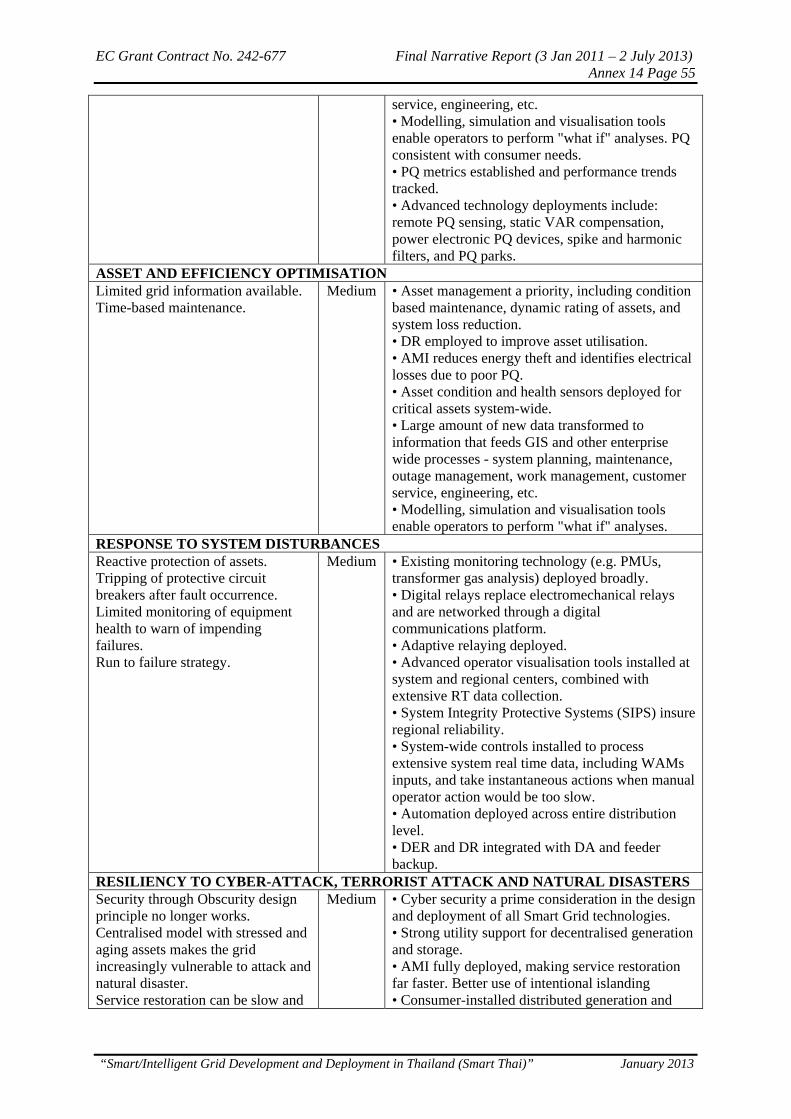

5. RISK ASSESSMENT ......................................................................................................... 53 5.1 FUTURE PROOFING .................................................................................................. 53 5.2 NEED FOR NEW SMART GRID PERSONNEL AND CAPACITY BUILDING FOR THE EXISTING PERSONNEL .......................................................................................... 53

6. RECOMMENDATIONS .................................................................................................... 57

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 4

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

LIST OF TABLES Table 1: Pattaya City Registered Population ........................................................................... 16 Table 2: Climate Data for Pattaya City .................................................................................... 17 Table 3: Comparison of Smart Meter and Electromechanical Meter ...................................... 23 Table 4: Investments (Millions of Baht) .................................................................................. 35 Table 5: Annual Savings from Investment and O&M Costs (Millions of Thai Baht) ............. 35 Table 6: Annual Operating Expenses of Smart Grid Systems ................................................. 36 Table 7: Results of the Financial Analysis .............................................................................. 36 Table 8: Results of the Scenario Analysis ............................................................................. 367 Table 9: Comparison for BAU and CASE1 on Peak Demand and Energy Supply of Year 2012.......................................................................................................................................... 39 Table 10: Summary of Emission Reduction for base case (Case1) ......................................... 41 Table 11: Summary of Yearly Estimated Emission Reduction for each case ......................... 41 Table 12: Risk assessment and mitigation measures for Smart Grid Implementation by PEA ………………………………………………………………………………………………..54

LIST OF FIGURES Figure 1: Conventional Grid Architecture ................................................................................. 9 Figure 2: Smart Grid within a Distribution System ................................................................. 10 Figure 3: Building Blocks of Smart Grid Deployment ............................................................ 12 Figure 4: PEA Smart Grid Roadmap ....................................................................................... 13 Figure 5: PEA Smart Grid Project Overview .......................................................................... 14 Figure 6: Location of Pattaya City ........................................................................................... 15 Figure 7: Location of Pattaya City in Chonburi Province ....................................................... 15 Figure 8: Pattaya City Map ...................................................................................................... 16 Figure 9: AMI showing Smart Meter in constant communication with Utility and Customer19 Figure 10: AMI Interface between Consumer and Utility ....................................................... 20 Figure 11: SMART Substation Automation – Process Bus ..................................................... 26 Figure 12: In a Semi-Distributed Approach, a FDIR Model is located at One Substation within the “Island.” .................................................................................................................. 32 Figure 13: A New centralised system can use pre-defined “Island” templates to build a network model for FDIR quickly ............................................................................................. 33 Figure 14: PEA Feeder RTU with SCADA / DMS ................................................................. 34 Figure 15: Peak Shifting .......................................................... Error! Bookmark not defined. Figure 16: How CERs are Claimed ......................................................................................... 44 Figure 17: CDM Project Cycle ................................................................................................ 45 Figure 18: Structure of Programme of Activities (PoA) .......................................................... 46 Figure 19: Procedure of PoA ................................................................................................... 47 Figure 20: Thailand Voluntary Carbon Market Framework .................................................... 49 Figure 21: T-VER Scheme Framework ................................................................................... 49 Figure 22: A Snapshot of the Bilateral Offset Crediting Mechanism (BOCM) ...................... 51

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 5

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

LIST OF ABBREVIATIONS AND ACRONYMS

AAM - Advanced Asset Management ADO - Advanced Distribution Operations AMI - Advanced Metering Infrastructure AMR - Automatic Meter Reading ATO - Advanced Transmission Operations BOCM - Bilateral Offset Crediting Mechanism BPL - Broadband over Power Lines C&I - Commercial and Industrial customers CDM - Clean Development Mechanism CEN - European Committee for Standardisation CENELEC - European Committee for Electrotechnical Standardisation CER - Certified Emission Reduction CFL - Compact Fluorescent Lamp CIM - Common Information Model CPA - CDM Programme Activity CPP - Critical Peak Pricing CVR - Conservation Voltage Reduction CT - Current Transformer DA - Distribution Automation DA/SA - Distribution and Substation Automation DCE - Data Circuit Terminating Equipment DE - Decentralised Energy DER - Distributed Energy Resources DMS - Distribution Management System DNA - Designated National Authority DNP - Distributed Network Protocol DOE - Designated Operating Entity DR - Demand Response EB - Executive Board of UNFCCC EBITDA - Earnings Before Interest, Tax, Depreciation and Amortisation EC - Energy Conservation EGAT - Electricity Generating Authority of Thailand EMS - Energy Management System EPM - Energy Planning Management EPRI - Electric Power Research Institute ET - Emissions Trading ETSI - The European Telecommunications Standards Institute EU - European Union FDIR - Fault Detection, Isolation and Restoration FLISR - Fault Location, Isolation and Service Restoration FRTU - Feeder Remote Terminal Unit FS - Feasibility Study GE - General Electric GHG - Green House Gas GOOSE - Generic Object Oriented Substation Event GPRS - General Packet Radio Service GSM - Global System for Mobile HAN - Home Area Networks HVAC - Heating, Ventilation and Air-Conditioning Systems ICT - Information and Communication Technology IEC - International Electrotechnical Commission IED - Intelligent Electronic Devices

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 6

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

IVR - Integrated Voice Response JI - Joint Implementation kV - Kilo Volt LAN - Local Area Network MDMS - Meter Data Management Systems MEA - Metropolitan Electricity Authority NAMA - Nationally Appropriate Mitigation Action NPV - Net Present Value O&M - Operation and Maintenance OMS - Outage Management Systems PDD - Project Design Document PEA - Provincial Electricity Authority PHEV - Plug-in Hybrid Electric Vehicles PLC - Power Line Carrier PLRC - Peak Load Reduction Credits PMU - Phasor Measurement Units PoA - Programme of Activities PoA-DD - Programme of Activities Design Document PP - Project Participant PQ - Power Quality PV - Photovoltaic RE - Renewable Energy RET - Renewable Energy Technologies RF - Radio Frequency RTP - Real Time Pricing RTU - Remote Terminal Units SA - Substation Automation SAS - Substation Automations Systems SCADA - Supervisory Control And Data Acquisition SCL - Substation Configuration Description Language SG - Strategic Group SIPS - System Integrity Protective Systems (SIPS) SMB - Standardisation Management Board T&D - Transmission and Distribution TBP - Time-Based Pricing TCP/IP - Transmission Control Protocol / Internet Protocol TOD - Time of Day TOU - Time of Use T-VER - Thailand Voluntary Emission Reduction UNFCCC - United Nations Framework Convention on Climate Change US DOE - United States Department of Energy USD - United States Dollar Currency VCS - Verified Carbon Standard VER - Voluntary Emission Reduction VSPP - Very Small Power Producer VT - Voltage (or Potential) Transformer WADE THAI - World Alliance for Thai Decentralised Energy Systems WAN - Wide Area Network XML - Extensible Markup Language

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 7

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

FEASIBILITY STUDY

1. INTRODUCTION

In 2010, WADE THAI received funding from the European Commission for the project on “Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” to develop policy options, action plans, and stakeholder participation to increase the availability and deployment of the Smart/Intelligent Grid in Thailand. This project aims to assist in capacity building and promotion of best practices happening in the European Union in the area of environment, climate change and energy security. The project intends to implement one of the mandates of WADE THAI1, which is to promote energy efficiency in the generation, transmission and distribution network of Thailand. The Overall Objective of the project is to "improve the sustainable economic and social development of Thailand through the efficient delivery of sustainable, economic and secure electricity using Smart/Intelligent Grid systems based on EU models and technologies". This action aims to achieve the Specific Objective, i.e. to "transform the generation, transmission and distribution network of Thailand through the enhancement of the capacity of Thai private and public sector organisations in introducing and promoting Smart/Intelligent Grid systems thereby contributing to the national development goals of Thailand in the area of environment, climate change and energy security". The performance of a "Technical and economic feasibility study for implementing Smart/Intelligent Grid systems on a pilot basis" is one of the key deliverables of the project. The pilot project that is the subject of this FS is located in Pattaya City, which is identified and included by the Provincial Electricity Authority (PEA) in their PEA Smart Grid Road Map. While PEA identified three (3) other sites as pilot areas, Pattaya City is their first priority.

1 WADE THAI is a short name for the “World Alliance for Thai Decentralised Energy Systems”, a non-profit organisation registered in Thailand as an output of the EU-funded project on “Enhancing institutional capacities for the market development of decentralised energy (DE) systems in Thailand”.

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 8

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

1.1 BACKGROUND OF SMART GRID TECHNOLOGY

1.1.1 DEFINITION AND COVERAGE OF SMART GRID TECHNOLOGY

“Smart Grid” is used as a promotional term, rather than a technical definition. It is also a new and evolving technologies. For these reasons there is no commonly accepted definition for what “smart” is. There are many smart grid definitions, some functional, some technological and some benefits-oriented. According to the European Smart Grids Task Force Expert Group 12, a Smart Grid is defined as an electricity network that can cost-efficiently integrate the behaviour and actions of all users connected to it – generators, consumers and those that do both – in order to ensure an economically efficient, sustainable power system with low losses and high levels of quality and security of supply and safety. A smart grid will also provide a framework for innovative services.

The Strategic Group 3 (SG3) on Smart Grid, set up by the International Electrotechnical Commission (IEC) Standardisation Management Board (SMB) defines Smart Grid simply as the concept of modernising the electric grid. Smart Grid is integrating the electrical and information technologies in between any point of generation and any point of consumption. The US Department of Energy website refers to Smart Grid as a class of technology people are using to bring utility electricity delivery systems into the 21st century, using computer-based remote control and automation. These systems are made possible by two-way communication technology and computer processing. A common element to most definitions is the application of digital processing and communications to the power grid, making data flow and information management central to Smart Grid. Various capabilities result from the deeply integrated use of digital technology with power grids. Integration of the new grid information flows into utility processes and systems is one of the key issues in the design of smart grids. Electric utilities now find themselves making three classes of transformations: (1) improvement of infrastructure; (2) addition of the digital layer, which is the essence of Smart Grid and (3) business process transformation, necessary to capitalise on the investments in smart technology. Much of the work that has been going on in electric grid modernisation, especially substation and distribution automation, is now included in the general concept of Smart Grid, but additional capabilities are evolving as well.

1.1.2 POWER GRID’S EVOLUTION INTO SMART GRID

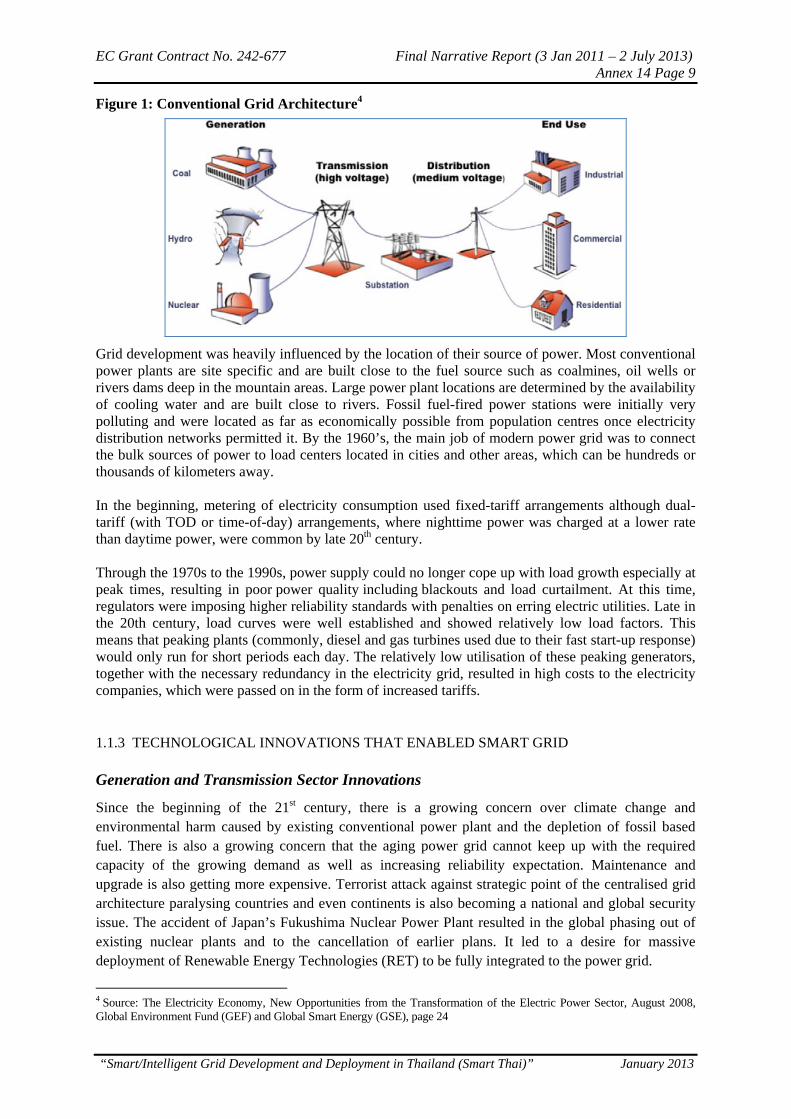

The first transmission line3 was installed in Oregon in the 1890s with a modest voltage of 4 kV and a length of around 14 miles. By the 20th century, power grids were operating as high as 800 kV and were eventually interconnected around the continents for economic and reliability reasons. By then, the developed world has delivered electric power using the same basic four-step approach: 1) generate power in large, centralised plants; 2) step up the power to high voltages and transmit it to regional utilities; 3) step down the power to medium voltages to distribute it locally; 4) step down the power a final time to deliver it to customer premises. This is illustrated in Figure 1.

2 Final report of CEN/CENELEC/ETSI Joint Working Group on Standards for Smart Grids, page 10 3 http://willamettefalls.org/Hist/Elec

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 9

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Figure 1: Conventional Grid Architecture4

Grid development was heavily influenced by the location of their source of power. Most conventional power plants are site specific and are built close to the fuel source such as coalmines, oil wells or rivers dams deep in the mountain areas. Large power plant locations are determined by the availability of cooling water and are built close to rivers. Fossil fuel-fired power stations were initially very polluting and were located as far as economically possible from population centres once electricity distribution networks permitted it. By the 1960’s, the main job of modern power grid was to connect the bulk sources of power to load centers located in cities and other areas, which can be hundreds or thousands of kilometers away. In the beginning, metering of electricity consumption used fixed-tariff arrangements although dual-tariff (with TOD or time-of-day) arrangements, where nighttime power was charged at a lower rate than daytime power, were common by late 20th century. Through the 1970s to the 1990s, power supply could no longer cope up with load growth especially at peak times, resulting in poor power quality including blackouts and load curtailment. At this time, regulators were imposing higher reliability standards with penalties on erring electric utilities. Late in the 20th century, load curves were well established and showed relatively low load factors. This means that peaking plants (commonly, diesel and gas turbines used due to their fast start-up response) would only run for short periods each day. The relatively low utilisation of these peaking generators, together with the necessary redundancy in the electricity grid, resulted in high costs to the electricity companies, which were passed on in the form of increased tariffs.

1.1.3 TECHNOLOGICAL INNOVATIONS THAT ENABLED SMART GRID

Generation and Transmission Sector Innovations

Since the beginning of the 21st century, there is a growing concern over climate change and environmental harm caused by existing conventional power plant and the depletion of fossil based fuel. There is also a growing concern that the aging power grid cannot keep up with the required capacity of the growing demand as well as increasing reliability expectation. Maintenance and upgrade is also getting more expensive. Terrorist attack against strategic point of the centralised grid architecture paralysing countries and even continents is also becoming a national and global security issue. The accident of Japan’s Fukushima Nuclear Power Plant resulted in the global phasing out of existing nuclear plants and to the cancellation of earlier plans. It led to a desire for massive deployment of Renewable Energy Technologies (RET) to be fully integrated to the power grid.

4 Source: The Electricity Economy, New Opportunities from the Transformation of the Electric Power Sector, August 2008, Global Environment Fund (GEF) and Global Smart Energy (GSE), page 24

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 10

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Distribution and Consumer Sector Innovations

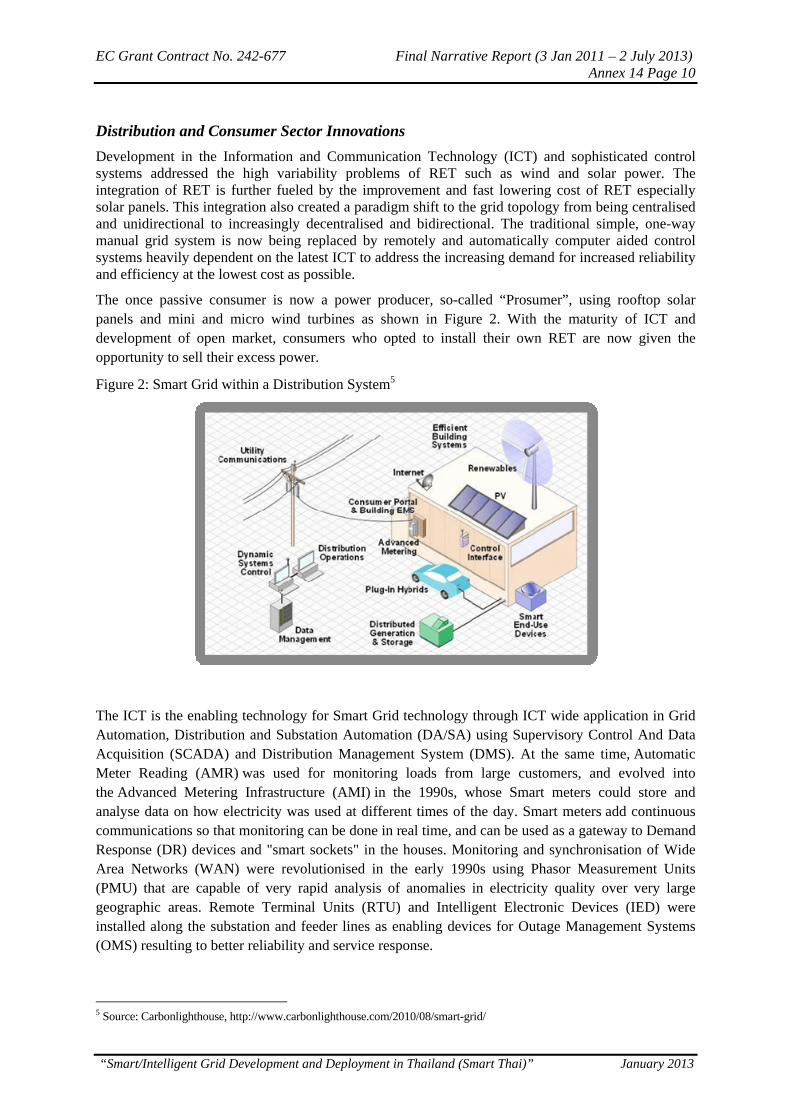

Development in the Information and Communication Technology (ICT) and sophisticated control systems addressed the high variability problems of RET such as wind and solar power. The integration of RET is further fueled by the improvement and fast lowering cost of RET especially solar panels. This integration also created a paradigm shift to the grid topology from being centralised and unidirectional to increasingly decentralised and bidirectional. The traditional simple, one-way manual grid system is now being replaced by remotely and automatically computer aided control systems heavily dependent on the latest ICT to address the increasing demand for increased reliability and efficiency at the lowest cost as possible.

The once passive consumer is now a power producer, so-called “Prosumer”, using rooftop solar panels and mini and micro wind turbines as shown in Figure 2. With the maturity of ICT and development of open market, consumers who opted to install their own RET are now given the opportunity to sell their excess power.

Figure 2: Smart Grid within a Distribution System5

The ICT is the enabling technology for Smart Grid technology through ICT wide application in Grid Automation, Distribution and Substation Automation (DA/SA) using Supervisory Control And Data Acquisition (SCADA) and Distribution Management System (DMS). At the same time, Automatic Meter Reading (AMR) was used for monitoring loads from large customers, and evolved into the Advanced Metering Infrastructure (AMI) in the 1990s, whose Smart meters could store and analyse data on how electricity was used at different times of the day. Smart meters add continuous communications so that monitoring can be done in real time, and can be used as a gateway to Demand Response (DR) devices and "smart sockets" in the houses. Monitoring and synchronisation of Wide Area Networks (WAN) were revolutionised in the early 1990s using Phasor Measurement Units (PMU) that are capable of very rapid analysis of anomalies in electricity quality over very large geographic areas. Remote Terminal Units (RTU) and Intelligent Electronic Devices (IED) were installed along the substation and feeder lines as enabling devices for Outage Management Systems (OMS) resulting to better reliability and service response.

5 Source: Carbonlighthouse, http://www.carbonlighthouse.com/2010/08/smart-grid/

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 11

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

The Distribution sector is at the forefront of the paradigm shift towards Smart Grid. The simple job of providing electrical service connection to customers within their franchise using flat rates are now being replaced with providing customers with the choice of retailers or preferred generators for purchasing their power and with the option of using power at a time most advantageous and beneficial to them using sophisticated ICT enabled Home Area Networks (HAN). Demand response also means that demand can respond to supply fluctuations in real time to prevent any power disturbance in the power grid. The traditional consumers are now the modern “prosumers” with several RET installed in their homes such as rooftop solar panels coupled with microwind turbines. The conventional unidirectional energy meter is now replaced with bidirectional net meter with TOU (Time of Use) register that allows “prosumers” to sell their excess energy during peak hours to the local distribution utility or grid operator.

Metering Innovations

Before the advent of smart meters, conventional meters were called energy meters because they only register energy consumption. They were made of electro-mechanical instruments that served as the utility cash registers. These conventional type of meters simply recorded the total energy consumed over a period of time and were read monthly. For substation metering and in some large industrial and commercial customers, additional demand and reactive energy functionality were also incorporated. With the development of computer and digital technology, Power Quality (PQ) meters were developed to record voltage sag and swell, harmonics, and TOU recording. Later, Automatic Meter Reading (AMR) technology was deployed which was the predecessor of the smart meter and the Advanced Metering Infrastructure (AMI). The technology automatically collects consumption, diagnostic, and status data from meters and transfers the data to a central database for billing, troubleshooting and analysing. This technology mainly saves utility providers the expense of traveling to each physical location to read a meter. Another advantage is that billing can be based on near real-time consumption rather than on estimates based on past or predicted consumption. This timely information coupled with analysis can help both utility providers and customers better control the use and production of electric energy consumption. AMR technologies include handheld, mobile and network technologies based on telephony platforms (wired and wireless), Radio Frequency (RF), or power line transmission6. In contrast, AMI also known as “Smart meter” is an electrical meter that records consumption of electric energy in intervals of an hour or less and sends information back to the utility for monitoring and billing purposes. Smart meters enable two-way communication between the meter and the central system. Unlike home energy monitors, smart meters can gather data for remote reporting. Such an AMI differs from the traditional AMR in that it enables two-way communications with the meter and allows for a customer option. Such devices can be shut down during times of peak demand7.

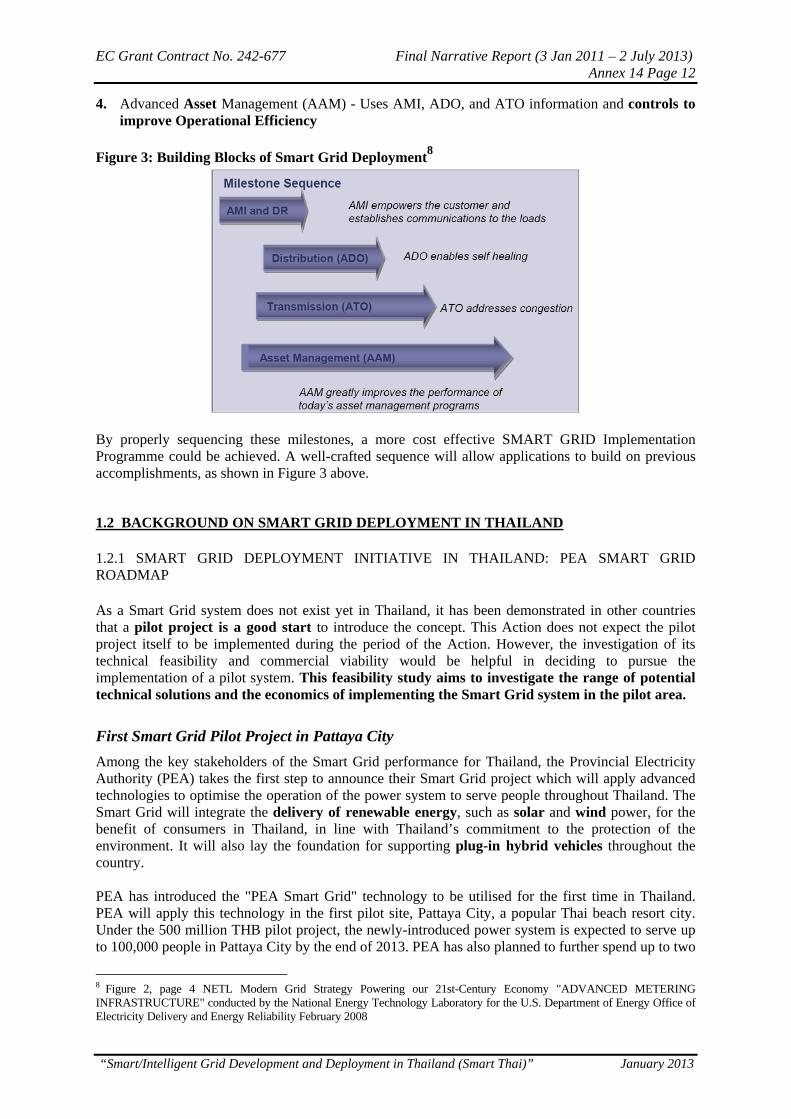

Building Blocks of Smart Grid Implementation

There are four major milestones on the road to a Smart Grid: 1. Advanced Metering Infrastructure (AMI) - Establishes communications with the consumer and

provides time stamped system information 2. Advanced Distribution Operations (ADO) - Uses AMI communications to collect distribution

information and uses AMI information to improve operations through Distribution Automation, Substation Automation and Distribution Management System

3. Advanced Transmission Operations (ATO) - Uses ADO information to improve operations and manage transmission congestion and voltage and uses AMI to give consumers access to markets

6 http://en.wikipedia.org/wiki/Automatic_meter_reading 7 http://en.wikipedia.org/wiki/Smart_meter

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 12

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

4. Advanced Asset Management (AAM) - Uses AMI, ADO, and ATO information and controls to improve Operational Efficiency

Figure 3: Building Blocks of Smart Grid Deployment8

By properly sequencing these milestones, a more cost effective SMART GRID Implementation Programme could be achieved. A well-crafted sequence will allow applications to build on previous accomplishments, as shown in Figure 3 above.

1.2 BACKGROUND ON SMART GRID DEPLOYMENT IN THAILAND

1.2.1 SMART GRID DEPLOYMENT INITIATIVE IN THAILAND: PEA SMART GRID ROADMAP

As a Smart Grid system does not exist yet in Thailand, it has been demonstrated in other countries that a pilot project is a good start to introduce the concept. This Action does not expect the pilot project itself to be implemented during the period of the Action. However, the investigation of its technical feasibility and commercial viability would be helpful in deciding to pursue the implementation of a pilot system. This feasibility study aims to investigate the range of potential technical solutions and the economics of implementing the Smart Grid system in the pilot area.

First Smart Grid Pilot Project in Pattaya City

Among the key stakeholders of the Smart Grid performance for Thailand, the Provincial Electricity Authority (PEA) takes the first step to announce their Smart Grid project which will apply advanced technologies to optimise the operation of the power system to serve people throughout Thailand. The Smart Grid will integrate the delivery of renewable energy, such as solar and wind power, for the benefit of consumers in Thailand, in line with Thailand’s commitment to the protection of the environment. It will also lay the foundation for supporting plug-in hybrid vehicles throughout the country. PEA has introduced the "PEA Smart Grid" technology to be utilised for the first time in Thailand. PEA will apply this technology in the first pilot site, Pattaya City, a popular Thai beach resort city. Under the 500 million THB pilot project, the newly-introduced power system is expected to serve up to 100,000 people in Pattaya City by the end of 2013. PEA has also planned to further spend up to two

8 Figure 2, page 4 NETL Modern Grid Strategy Powering our 21st-Century Economy "ADVANCED METERING INFRASTRUCTURE" conducted by the National Energy Technology Laboratory for the U.S. Department of Energy Office of Electricity Delivery and Energy Reliability February 2008

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 13

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

billion baht to expand the Smart Grid technology to some 400,000 people living in Thailand's northern Chiang Mai Province, southern Phuket Province and northeastern NakhonRatchasima Province in the foreseeable future9. Based of this development, this feasibility study under the Smart Thai project selected Pattaya City, Chonburi province as the study site in order to be in line with, and provide beneficial inputs to the PEA Smart Grid's first pilot project.

Initial PEA Smart Grid Definition10

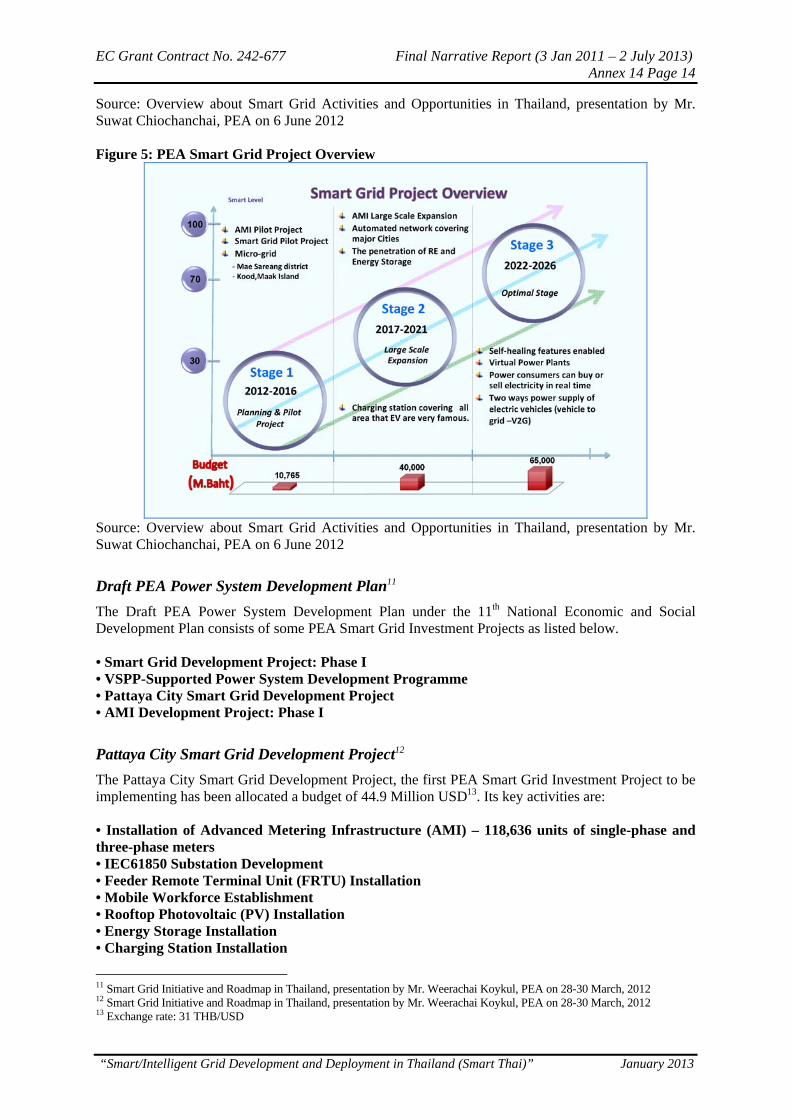

PEA has perceived Smart Grid as a holistic enterprise system encompassing technology processes and services to deliver electrical power efficiently, reliably, cost effectively and securely. It has perceived its Smart Grid initiative as an endeavour to create world-class electricity delivery systems that adopt best practices and the best technology not only to support the needs of its customers, but also to facilitate government policy with respect to renewable resources, fuel efficiency and CO2 emissions. PEA intends to be at the forefront of the transformation of the electrical delivery system in Thailand by enacting Smart Grid integration plans and subsequently make investments in the Smart Grid. In line with government policies, PEA will increase the ability of renewable resources to produce electrical energy and will engineer distribution system changes and adopt new modes of operation to incorporate these new resources. Hence, PEA defines Smart Grid as “Electricity networks that intelligently integrate generators and consumers to efficiently deliver electricity which is sufficient capacity and coverage area accessible, safe, economic, reliable, efficient, and sustainable.” Figure 4 shows PEA Smart Grid Roadmap consisting of 3 main phases and Figure 5 shows the overview of PEA Smart Grid Project. Figure 4: PEA Smart Grid Roadmap

9 Pattaya first city in Thailand to use 'PEA Smart Grid' technology 10 Principle and Concept of Smart Grid Development in Thailand, Presentation by Mr. Weerachai Koykul, PEA on March 26, 2011

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 14

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Source: Overview about Smart Grid Activities and Opportunities in Thailand, presentation by Mr. Suwat Chiochanchai, PEA on 6 June 2012 Figure 5: PEA Smart Grid Project Overview

Source: Overview about Smart Grid Activities and Opportunities in Thailand, presentation by Mr. Suwat Chiochanchai, PEA on 6 June 2012

Draft PEA Power System Development Plan11

The Draft PEA Power System Development Plan under the 11th National Economic and Social Development Plan consists of some PEA Smart Grid Investment Projects as listed below. • Smart Grid Development Project: Phase I • VSPP-Supported Power System Development Programme • Pattaya City Smart Grid Development Project • AMI Development Project: Phase I

Pattaya City Smart Grid Development Project12

The Pattaya City Smart Grid Development Project, the first PEA Smart Grid Investment Project to be implementing has been allocated a budget of 44.9 Million USD13. Its key activities are: • Installation of Advanced Metering Infrastructure (AMI) – 118,636 units of single-phase and three-phase meters • IEC61850 Substation Development • Feeder Remote Terminal Unit (FRTU) Installation • Mobile Workforce Establishment • Rooftop Photovoltaic (PV) Installation • Energy Storage Installation • Charging Station Installation

11 Smart Grid Initiative and Roadmap in Thailand, presentation by Mr. Weerachai Koykul, PEA on 28-30 March, 2012 12 Smart Grid Initiative and Roadmap in Thailand, presentation by Mr. Weerachai Koykul, PEA on 28-30 March, 2012 13 Exchange rate: 31 THB/USD

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 15

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

• Home Automation

1.2.2 PATTAYA CITY: GENERAL INFORMATION

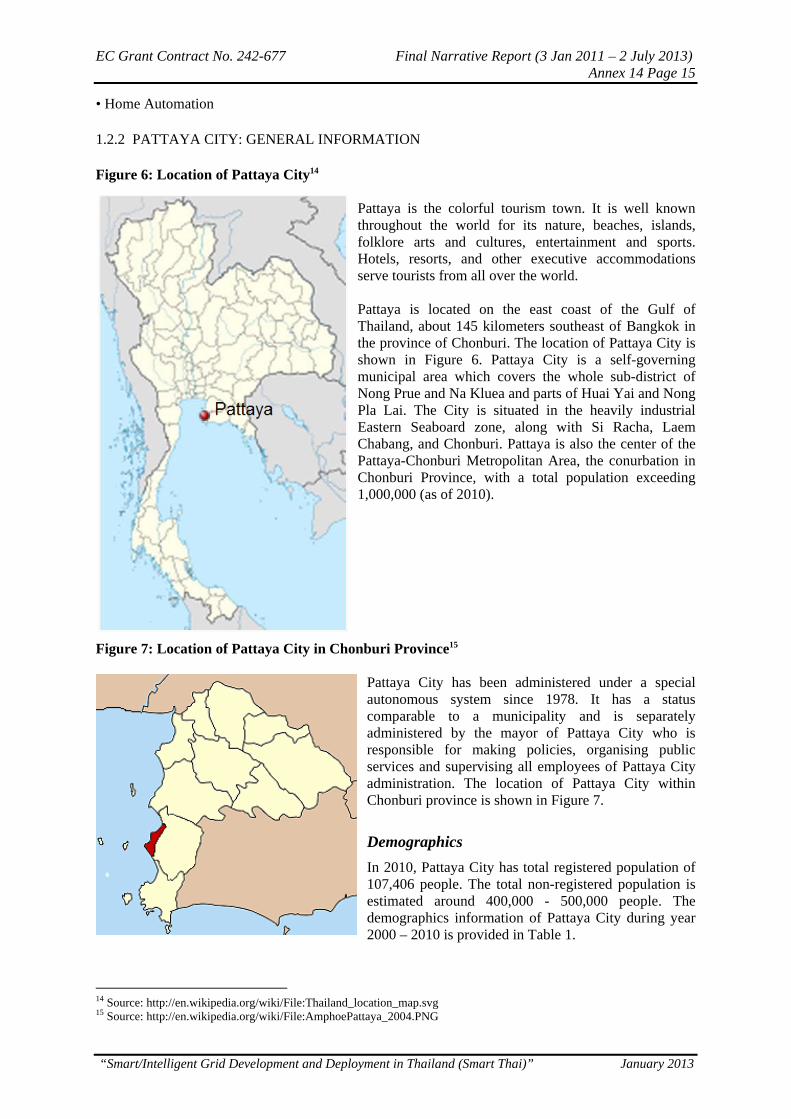

Figure 6: Location of Pattaya City14

Pattaya is the colorful tourism town. It is well known throughout the world for its nature, beaches, islands, folklore arts and cultures, entertainment and sports. Hotels, resorts, and other executive accommodations serve tourists from all over the world. Pattaya is located on the east coast of the Gulf of Thailand, about 145 kilometers southeast of Bangkok in the province of Chonburi. The location of Pattaya City is shown in Figure 6. Pattaya City is a self-governing municipal area which covers the whole sub-district of Nong Prue and Na Kluea and parts of Huai Yai and Nong Pla Lai. The City is situated in the heavily industrial Eastern Seaboard zone, along with Si Racha, Laem Chabang, and Chonburi. Pattaya is also the center of the Pattaya-Chonburi Metropolitan Area, the conurbation in Chonburi Province, with a total population exceeding 1,000,000 (as of 2010).

Figure 7: Location of Pattaya City in Chonburi Province15

Pattaya City has been administered under a special autonomous system since 1978. It has a status comparable to a municipality and is separately administered by the mayor of Pattaya City who is responsible for making policies, organising public services and supervising all employees of Pattaya City administration. The location of Pattaya City within Chonburi province is shown in Figure 7.

Demographics

In 2010, Pattaya City has total registered population of 107,406 people. The total non-registered population is estimated around 400,000 - 500,000 people. The demographics information of Pattaya City during year 2000 – 2010 is provided in Table 1.

14 Source: http://en.wikipedia.org/wiki/File:Thailand_location_map.svg 15 Source: http://en.wikipedia.org/wiki/File:AmphoePattaya_2004.PNG

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 16

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

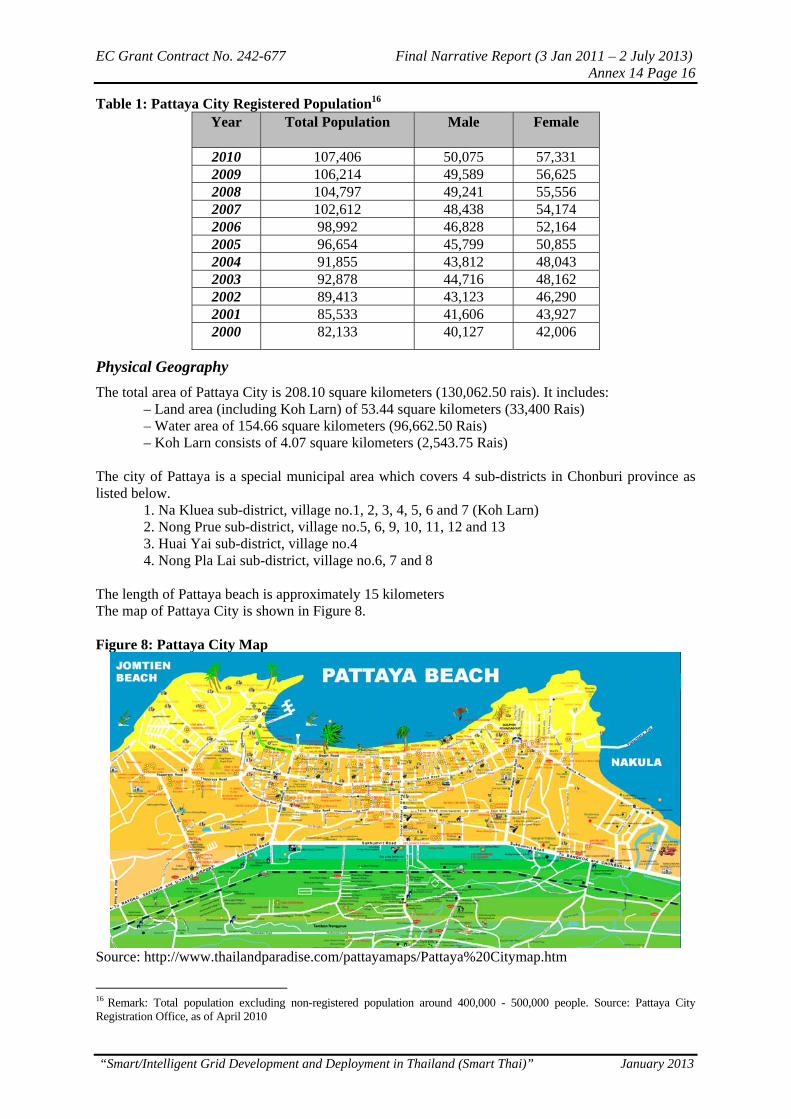

Table 1: Pattaya City Registered Population16 Year

Total Population Male Female

2010 107,406 50,075 57,331 2009 106,214 49,589 56,625 2008 104,797 49,241 55,556 2007 102,612 48,438 54,174 2006 98,992 46,828 52,164 2005 96,654 45,799 50,855 2004 91,855 43,812 48,043 2003 92,878 44,716 48,162 2002 89,413 43,123 46,290 2001 85,533 41,606 43,927 2000 82,133 40,127 42,006

Physical Geography

The total area of Pattaya City is 208.10 square kilometers (130,062.50 rais). It includes: – Land area (including Koh Larn) of 53.44 square kilometers (33,400 Rais) – Water area of 154.66 square kilometers (96,662.50 Rais) – Koh Larn consists of 4.07 square kilometers (2,543.75 Rais)

The city of Pattaya is a special municipal area which covers 4 sub-districts in Chonburi province as listed below.

1. Na Kluea sub-district, village no.1, 2, 3, 4, 5, 6 and 7 (Koh Larn) 2. Nong Prue sub-district, village no.5, 6, 9, 10, 11, 12 and 13 3. Huai Yai sub-district, village no.4 4. Nong Pla Lai sub-district, village no.6, 7 and 8

The length of Pattaya beach is approximately 15 kilometers The map of Pattaya City is shown in Figure 8. Figure 8: Pattaya City Map

Source: http://www.thailandparadise.com/pattayamaps/Pattaya%20Citymap.htm

16 Remark: Total population excluding non-registered population around 400,000 - 500,000 people. Source: Pattaya City Registration Office, as of April 2010

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 17

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

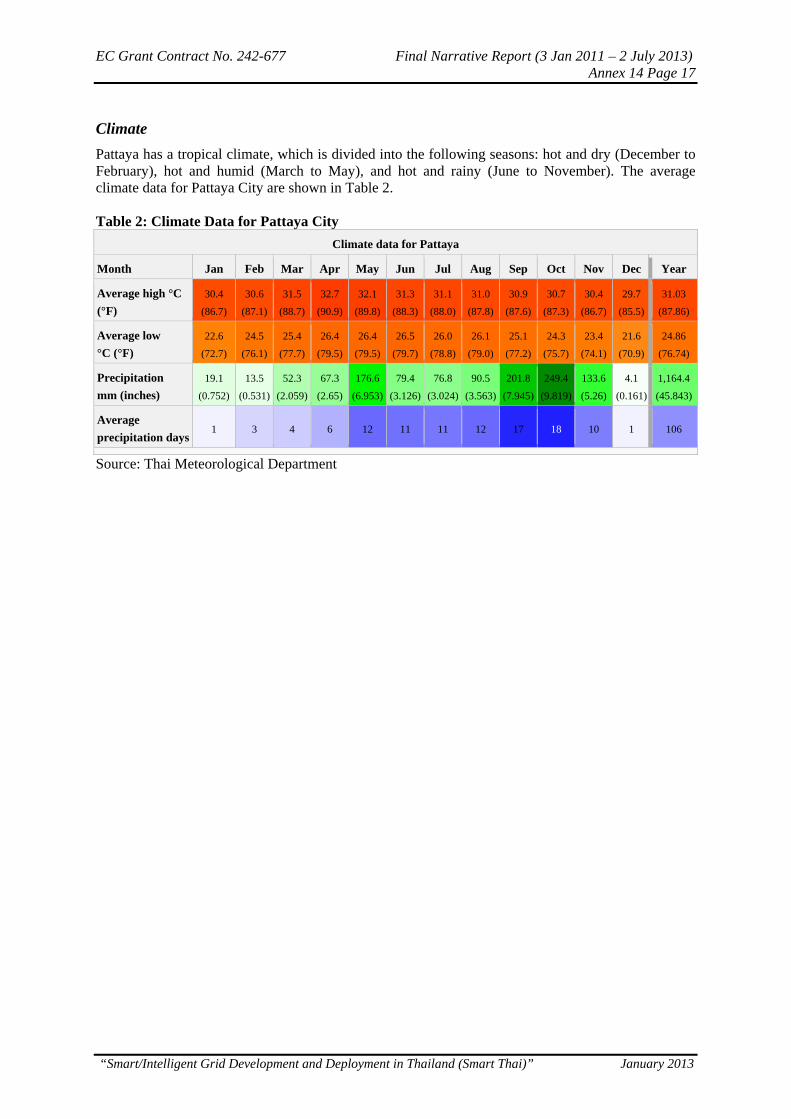

Climate

Pattaya has a tropical climate, which is divided into the following seasons: hot and dry (December to February), hot and humid (March to May), and hot and rainy (June to November). The average climate data for Pattaya City are shown in Table 2. Table 2: Climate Data for Pattaya City

Climate data for Pattaya

Month Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

Average high °C

(°F)

30.4

(86.7)

30.6

(87.1)

31.5

(88.7)

32.7

(90.9)

32.1

(89.8)

31.3

(88.3)

31.1

(88.0)

31.0

(87.8)

30.9

(87.6)

30.7

(87.3)

30.4

(86.7)

29.7

(85.5)

31.03

(87.86)

Average low

°C (°F)

22.6

(72.7)

24.5

(76.1)

25.4

(77.7)

26.4

(79.5)

26.4

(79.5)

26.5

(79.7)

26.0

(78.8)

26.1

(79.0)

25.1

(77.2)

24.3

(75.7)

23.4

(74.1)

21.6

(70.9)

24.86

(76.74)

Precipitation

mm (inches)

19.1

(0.752)

13.5

(0.531)

52.3

(2.059)

67.3

(2.65)

176.6

(6.953)

79.4

(3.126)

76.8

(3.024)

90.5

(3.563)

201.8

(7.945)

249.4

(9.819)

133.6

(5.26)

4.1

(0.161)

1,164.4

(45.843)

Average

precipitation days 1 3 4 6 12 11 11 12 17 18 10 1 106

Source: Thai Meteorological Department

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 18

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

2. TECHNICAL OVERVIEW AND ANALYSIS

One of the objectives of the feasibility study (FS) is to determine the technical feasibility of the Smart Grid system to be implemented on a pilot site. It aims at investigating the range of potential technical solutions and the economics of implementing the Smart Grid system in the pilot area. The assessment of the feasibility study is based on the output of the computer simulation model for Smart Grid system developed under the Smart Thai project. The test site of the computer simulation model and the study site used in conducting the technical and economic feasibility was selected in accordance with the PEA Smart Grid Roadmap. The fact that Smart Grid is very broad, the need for some limitation of the scope of the FS becomes apparent. The technical review is therefore based on the PEA proposed pilot project in Pattaya City. This Smart Grid technical review will consider three Smart Grid technology components that will be directly implemented by PEA through the upgrading of their distribution system and metering infrastructure. These are: a) Advanced Metering Infrastructure (AMI) focusing on Smart Meter; b) Substation Automation (SA) focusing on IEC 61850 Standards implementation; and c) Distribution Management System (DMS) focusing on Fault Detection, Isolation and Restoration (FDIR) using Remote Terminal Unit (RTU). The review will investigate the range of potential technical solutions, benefits, and challenges behind these activities.

2.1 ADVANCED METERING INFRASTRUCTURE (SMART METERS)

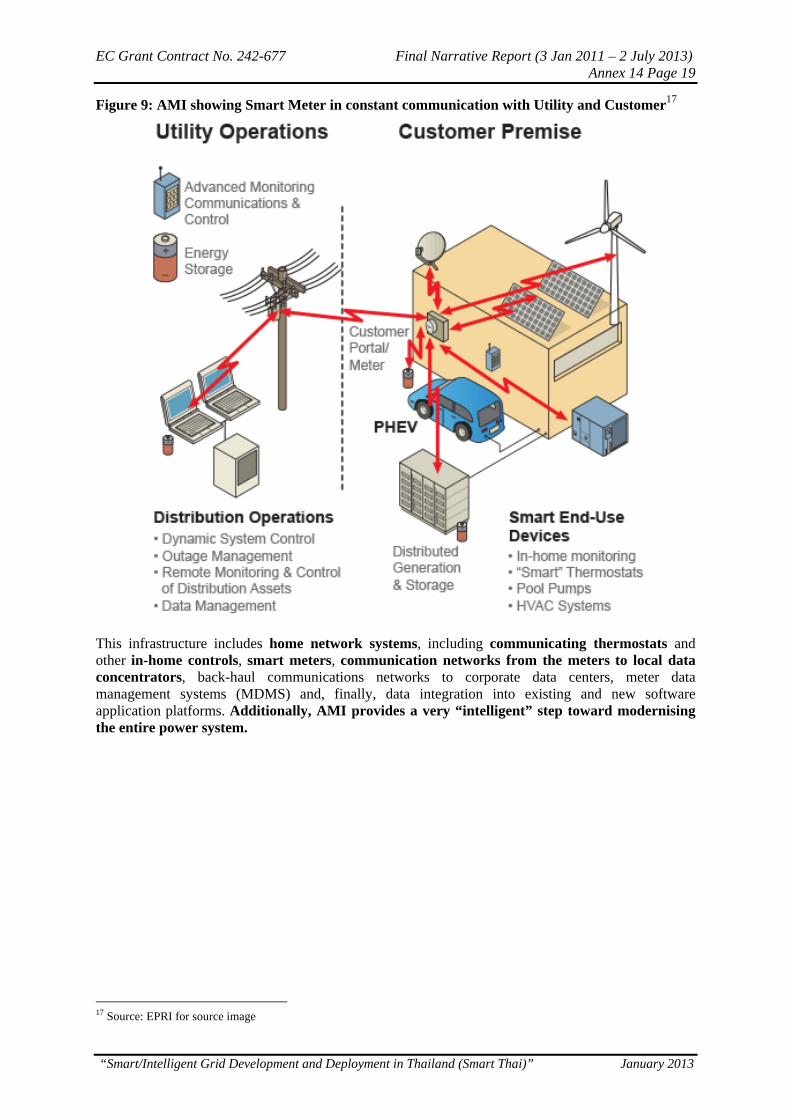

Deploying an Advanced Metering Infrastructure (AMI) is a fundamental step to grid modernisation. AMI provides the framework for meeting one of the Smart Grid’s principal characteristics, i.e. the consumer participation or Demand Response (DR). AMI is not a single technology implementation, but rather a complex infrastructure that must be integrated into existing and new utility processes and applications. Three features constitute the AMI system: “smart” meters, a two-way communications network and the information technology systems to support their interaction. AMI uses internal communications systems to convey real-time energy use and load information to both the utility and to the customer as shown in Figures 9 and 10.

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 19

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Figure 9: AMI showing Smart Meter in constant communication with Utility and Customer17

This infrastructure includes home network systems, including communicating thermostats and other in-home controls, smart meters, communication networks from the meters to local data concentrators, back-haul communications networks to corporate data centers, meter data management systems (MDMS) and, finally, data integration into existing and new software application platforms. Additionally, AMI provides a very “intelligent” step toward modernising the entire power system.

17 Source: EPRI for source image

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 20

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

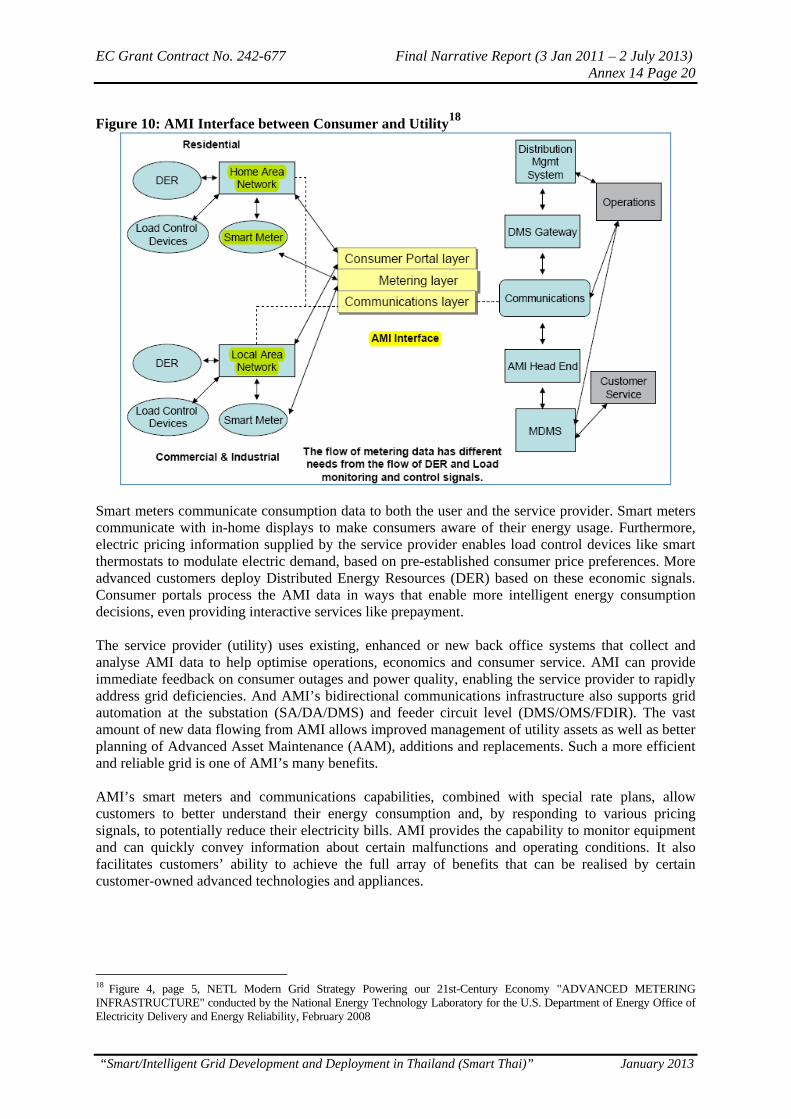

Figure 10: AMI Interface between Consumer and Utility18

Smart meters communicate consumption data to both the user and the service provider. Smart meters communicate with in-home displays to make consumers aware of their energy usage. Furthermore, electric pricing information supplied by the service provider enables load control devices like smart thermostats to modulate electric demand, based on pre-established consumer price preferences. More advanced customers deploy Distributed Energy Resources (DER) based on these economic signals. Consumer portals process the AMI data in ways that enable more intelligent energy consumption decisions, even providing interactive services like prepayment. The service provider (utility) uses existing, enhanced or new back office systems that collect and analyse AMI data to help optimise operations, economics and consumer service. AMI can provide immediate feedback on consumer outages and power quality, enabling the service provider to rapidly address grid deficiencies. And AMI’s bidirectional communications infrastructure also supports grid automation at the substation (SA/DA/DMS) and feeder circuit level (DMS/OMS/FDIR). The vast amount of new data flowing from AMI allows improved management of utility assets as well as better planning of Advanced Asset Maintenance (AAM), additions and replacements. Such a more efficient and reliable grid is one of AMI’s many benefits. AMI’s smart meters and communications capabilities, combined with special rate plans, allow customers to better understand their energy consumption and, by responding to various pricing signals, to potentially reduce their electricity bills. AMI provides the capability to monitor equipment and can quickly convey information about certain malfunctions and operating conditions. It also facilitates customers’ ability to achieve the full array of benefits that can be realised by certain customer-owned advanced technologies and appliances.

18 Figure 4, page 5, NETL Modern Grid Strategy Powering our 21st-Century Economy "ADVANCED METERING INFRASTRUCTURE" conducted by the National Energy Technology Laboratory for the U.S. Department of Energy Office of Electricity Delivery and Energy Reliability, February 2008

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 21

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

2.1.1 SMART METER STANDARD FEATURES AND FUNCTIONALITIES

Of special interest is the Smart Meter, which is the heart of AMI, since this will be the focus of PEA’s deployment in their Smart Grid Pilot Project in Pattaya City. Smart meters are solid-state programmable devices that perform many functions. Local and global standard19 of features and functionalities are being implemented which incorporate most or all of the following:

• Time-Based Pricing (TBP)

A smart meter is capable of recording consumption that incorporates Time of Day (TOD) and Time of Use (TOU) pricing mechanism to provide option for consumer to limit use of power during peak period (high price) and maximise use during off-peak (low price). More advance features on more advanced electricity market structure will include Critical Peak Pricing (CPP), Real-Time Pricing (RTP) also called dynamic pricing and Peak Load Reduction Credits (PLRC). Combined with a well-designed tariff scheme, this feature enables DR that will reduce peak load considerably.

• Consumption data storage for consumer and utility

A smart meter can record both Active (Watt-hour) and Reactive (VAR-hour) Energy. This enables regulators in implementing power factor incentive schemes and encourages user to implement a power factor programme that improves the overall system efficiency and reduces electricity cost. It can transmit and communicate information on the load and energy consumed in minutes (or seconds) to both utility and consumer. This feature enables and enhances TBP. It automatically resumes operational functionality after loss of power and retains all information held in its data storage prior to such power failure. This feature maintains data integrity and accuracy.

• Net metering

A smart meter is capable of recording exported and imported power (bi-directional flow) of consumers with embedded generator or integrated renewable energy supply like solar panels. Combined with other features, this transforms the passive consumer into an active “prosumer”. Aggregated prosumers can act in a similar way to a power plant by selling their self-generated power.

• Loss of power (and restoration) notification

A smart meter can detect, record and transmit loss and restoration of power notice to both utility and consumer. This feature enables Outage Management System (OMS) and improves the system reliability through real-time outage information. OMS reduces the impact of outages by reducing the time and resources used to deal with them, through automated call-taking, prediction and the integration of AMI and Integrated Voice Response (IVR). In simpler terms, it predicts the location of a failed fuse or breaker, prioritises restoration efforts, provides information on the extent of outages, calculates restoration times and manages repair crews. Some experts believed that the US could have recovered from Hurricane Sandy much better had they invested in this smart grid upgrade.

• Remote turn-on / turn-off operations (Load Switch)

A smart meter can be remotely turned on and turned off. This feature enables, among others, demand response mechanisms on voluntary load shedding during emergency and contingency plans. This enables Aggregated Energy Management services like the one provided by EnerNOC20 which manly provides demand response services that maintain real-time balance between electricity supply and demand. This energy management services provide solutions for energy conservation and efficiency.

19 Smart Metering Implementation Programme / Smart Metering Technical Equipment” prepared by Department of Energy and Climate Change. Draft provided to Parliament’s libraries dated September 2012. UK 20 http://en.wikipedia.org/wiki/EnerNOC#Notable_work

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 22

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

A smart meter can determine when power supply usage exceeds predetermined value such as contracted load, record and count the number of such occurrences, and send alert notice. Depending upon the existing contract, supply can be disabled. This protects the user from equipment overload. This provides distribution utility better Energy Planning Management (EPM) and improves operation.

• Energy prepayment

A smart meter can provide prepaid service options which allow users to better manage their energy consumption and optimise their budget allocation without the usual problem of accumulated unpaid bills. Utility in return can provide “pay-as-you-go” special rates since utility gains from advance payment for future consumption and simplified billing and collection operation. Utilities will also be insured of receiving payment from all customers, regardless of income levels.

• Power quality monitoring and control

A smart meter can detect, record and communicate notices on abnormal power quality beyond acceptable standards. Power quality monitored includes over and under voltages. Recent development in smart meter application includes Conservation Voltage Reduction (CVR) or Volt/VAR optimisation during peak periods that does not affect the performance of the equipment and appliances. This feature achieves not only the peak-shaving potential or the reduction of the peak load requirement of the grid but also lessens consumer energy consumption without sacrifice or involvement on his part.

• Tamper and energy theft detection

A smart meter has security features that can detect any attempt of unauthorised physical access through its secure perimeter casing. It can provide evidence of such an attempt through the use of tamper evident coatings or seals. When reasonably practical, it can generate entry in its Security log and can send an alert notice via its available interface and disable the supply. It has also security features that can detect and prevent, on all of its interfaces, unauthorised access that could compromise the confidentiality and/or data integrity of personal data, security credentials, firmware and other data essential for ensuring its integrity. Any such detection can generate entry in its Security log and can send an alert notice via its available interface. These features will deter power theft and drastically reduce non-technical system loss and consequently improve overall system efficiency.

• Communications with other intelligent devices in the home

A smart meter can establish open standard bi-directional communication links via each of its interfaces including consumer devices and microgeneration meters (e.g. rooftop solar panels and micro wind turbines) over the HAN interface and WAN interface. This feature enables real-time demand response and as a consequence more dynamic pricing schemes. It includes security features that authenticates the source, verifies the recipient and the command and validates its content and format. WAN interface can be in the form of any of the following technology depending on its availability as well as practical and technical considerations: • Power Line Carrier (PLC) • Broadband over Power Lines (BPL) • Copper or optical fiber • Wireless (Radio frequency), either centralised or a distributed mesh

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 23

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

• Internet • Public networks (landline, cellular, paging) • Combinations of the above

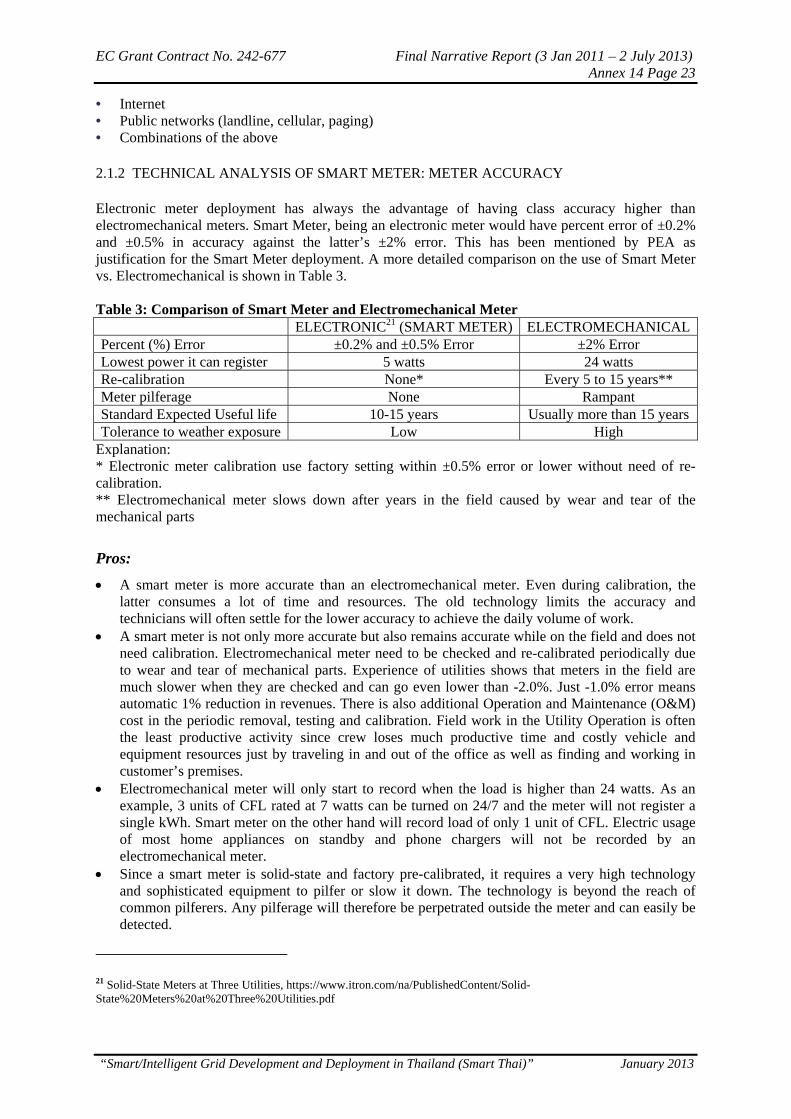

2.1.2 TECHNICAL ANALYSIS OF SMART METER: METER ACCURACY

Electronic meter deployment has always the advantage of having class accuracy higher than electromechanical meters. Smart Meter, being an electronic meter would have percent error of ±0.2% and ±0.5% in accuracy against the latter’s ±2% error. This has been mentioned by PEA as justification for the Smart Meter deployment. A more detailed comparison on the use of Smart Meter vs. Electromechanical is shown in Table 3. Table 3: Comparison of Smart Meter and Electromechanical Meter ELECTRONIC21 (SMART METER) ELECTROMECHANICALPercent (%) Error ±0.2% and ±0.5% Error ±2% Error Lowest power it can register 5 watts 24 watts Re-calibration None* Every 5 to 15 years** Meter pilferage None Rampant Standard Expected Useful life 10-15 years Usually more than 15 years Tolerance to weather exposure Low High

Explanation: * Electronic meter calibration use factory setting within ±0.5% error or lower without need of re-calibration. ** Electromechanical meter slows down after years in the field caused by wear and tear of the mechanical parts

Pros:

A smart meter is more accurate than an electromechanical meter. Even during calibration, the latter consumes a lot of time and resources. The old technology limits the accuracy and technicians will often settle for the lower accuracy to achieve the daily volume of work.

A smart meter is not only more accurate but also remains accurate while on the field and does not need calibration. Electromechanical meter need to be checked and re-calibrated periodically due to wear and tear of mechanical parts. Experience of utilities shows that meters in the field are much slower when they are checked and can go even lower than -2.0%. Just -1.0% error means automatic 1% reduction in revenues. There is also additional Operation and Maintenance (O&M) cost in the periodic removal, testing and calibration. Field work in the Utility Operation is often the least productive activity since crew loses much productive time and costly vehicle and equipment resources just by traveling in and out of the office as well as finding and working in customer’s premises.

Electromechanical meter will only start to record when the load is higher than 24 watts. As an example, 3 units of CFL rated at 7 watts can be turned on 24/7 and the meter will not register a single kWh. Smart meter on the other hand will record load of only 1 unit of CFL. Electric usage of most home appliances on standby and phone chargers will not be recorded by an electromechanical meter.

Since a smart meter is solid-state and factory pre-calibrated, it requires a very high technology and sophisticated equipment to pilfer or slow it down. The technology is beyond the reach of common pilferers. Any pilferage will therefore be perpetrated outside the meter and can easily be detected.

21 Solid-State Meters at Three Utilities, https://www.itron.com/na/PublishedContent/Solid-State%20Meters%20at%20Three%20Utilities.pdf

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 24

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Cons:

While a smart meter has an expected useful life of 15 years, an electromechanical meter is sturdy and will last more than 15 years. As an example, GE I-70 S22, which was manufactured in the 1970s is still a standard meter for most homes around the world. However, there are plenty of meter manufacturers in Asia that will not be that durable and will only be accurate for about 25 years. A smart meter can however easily compensate its shorter life with a better accuracy and other features it provides.

An electromechanical meter as already mentioned, is more durable, even when exposed to the weather. This can be mitigated by providing meter casing and by installing smart meter in secure area.

2.1.3 TECHNICAL ANALYSIS OF SMART METER: APPLICABLE FEATURES AND FUNCTIONALITIES

PEA mentioned that they are implementing two types of meters largely based on the type of customers, namely: (1) Residential and (2) Commercial and Industrial. During the pilot project, PEA will utilise limited smart meter features such as measurement of Active energy, Demand and TOU. In order for PEA to avail the whole range of benefits from Smart Grid implementation, it is important to specify that the smart meter deployed is upgradable. PEA can employ various types of meters and features depending on size and type of customer as well as preferences and programme participations. Customer profiling should also consider the following: Application of Net Metering features to customers with rooftop solar PV, micro wind turbines,

etc. Application of Power Quality features to customers with very low power factor Application of prepayment features to willing customers Participants to Smart Grid programmes such as CVR, extended TOU, prepayment, OMS, DR,

etc. Customer profiling can be done using information available in the utility database although some may need actual field survey. DR using complete AMI feature and DA may take some time.

2.1.4 CONCLUSIONS ON SMART METER

The installation of more than 100,000 smart meters in the pilot area; i.e., Pattaya area will immediately benefit PEA by the increase in accuracy and being less vulnerable from internal meter pilferage which is difficult to check. It is also normal at the start of smart meter deployment that not all benefits from the other features and functionalities can be realised. However, smart meter enables PEA to have more options in terms of improving its operation and quality of service, increasing its reliability and also its profitability. It also enables its customers to avail of DR programs, which will not only reduce customer electric bill but also benefit PEA.

22 GE model number uses the year it is manufactured. There are still GE I-30 meters working perfectly even after some 80 years

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 25

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

2.2 IEC 61850 STANDARD IMPLEMENTATION

2.2.1 SUBSTATION AUTOMATION (SA) AND IEC 61850 (See Figure 11)

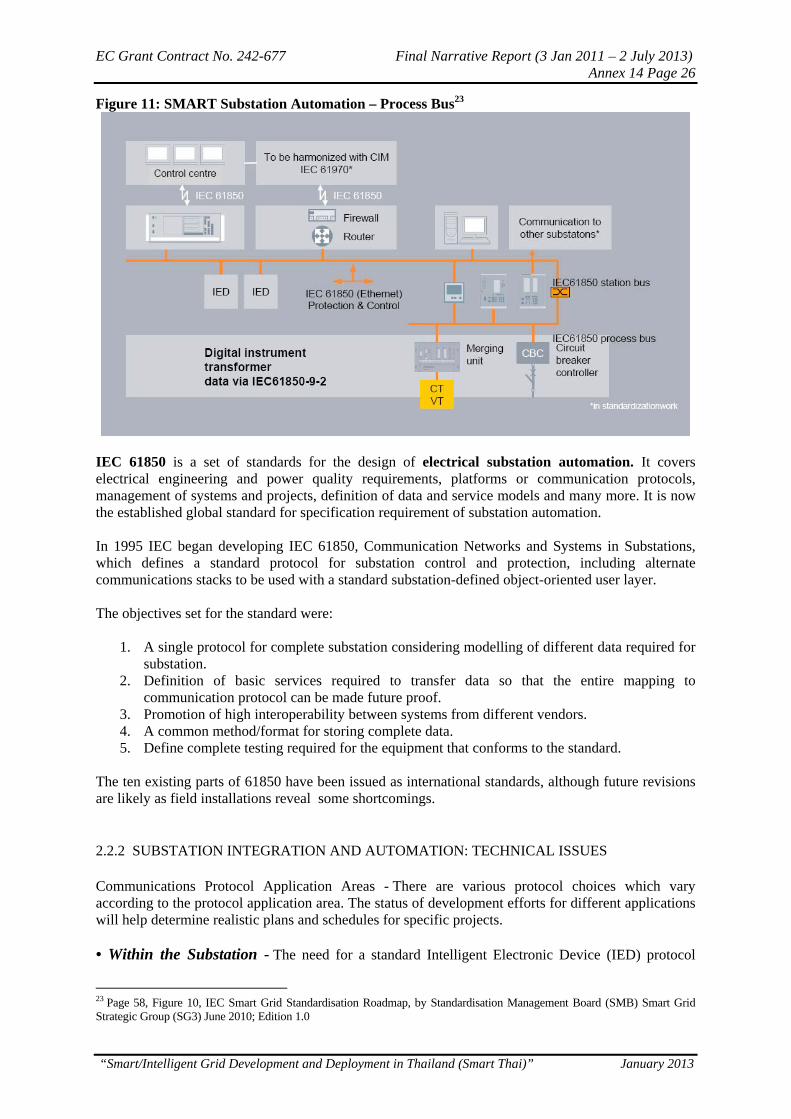

Legacy or traditional substation automation protocols and architectures typically provided basic functionality for power system automation and were designed to accommodate the technical limitations of the Information and Communications Technology (ICT) available for implementation. There has recently been a vast improvement in ICT that has dramatically changed what is now feasible for power system automation in the substation. Technologies such as switched Ethernet, TCP/IP, high-speed WAN, and high-performance low-cost computers are providing capabilities that could barely be imagined when most early substation automation protocols were designed. The possibility to build Substation Automations Systems (SAS) rests on the strong technological development of large-scale integrated circuits, leading to the present availability of advanced, fast, and powerful microprocessors. The result has been an evolution of substation secondary equipment, from electro-mechanical devices to digital devices. This in turn has provided the possibility of implementing Substation Automation (SA) using several Intelligent Electronic Devices (IEDs) to perform the required functions (protection, local and remote monitoring and control, etc.). SA is quite a mature application, which has been performed for many years. Its core functions are: • Protection • Local control and supervision • Remote control and supervision • Equipment supervision • Metering • Measuring • Online diagnosis The integration of substation automation functions into the Smart Grid architecture is accelerating its implementation to new distribution substations. Substation automation equipment, including communications, protective relays, Supervisory Control And Data Acquisition (SCADA) devices, and related sensors is now a significant and mature market and IEC 61850 is the enabling factor in the speedy transformation of substation automation design as shown in Figure 11.

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 26

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Figure 11: SMART Substation Automation – Process Bus23

IEC 61850 is a set of standards for the design of electrical substation automation. It covers electrical engineering and power quality requirements, platforms or communication protocols, management of systems and projects, definition of data and service models and many more. It is now the established global standard for specification requirement of substation automation. In 1995 IEC began developing IEC 61850, Communication Networks and Systems in Substations, which defines a standard protocol for substation control and protection, including alternate communications stacks to be used with a standard substation-defined object-oriented user layer. The objectives set for the standard were:

1. A single protocol for complete substation considering modelling of different data required for substation.

2. Definition of basic services required to transfer data so that the entire mapping to communication protocol can be made future proof.

3. Promotion of high interoperability between systems from different vendors. 4. A common method/format for storing complete data. 5. Define complete testing required for the equipment that conforms to the standard.

The ten existing parts of 61850 have been issued as international standards, although future revisions are likely as field installations reveal some shortcomings.

2.2.2 SUBSTATION INTEGRATION AND AUTOMATION: TECHNICAL ISSUES

Communications Protocol Application Areas - There are various protocol choices which vary according to the protocol application area. The status of development efforts for different applications will help determine realistic plans and schedules for specific projects. • Within the Substation - The need for a standard Intelligent Electronic Device (IED) protocol

23 Page 58, Figure 10, IEC Smart Grid Standardisation Roadmap, by Standardisation Management Board (SMB) Smart Grid Strategic Group (SG3) June 2010; Edition 1.0

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 27

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

dates back to the late 1980s. IED suppliers acknowledge that their expertise is in the IED itself – not in two-way communications capability, the communications protocol, or added IED functionality from a remote user. Though the industry made some effort to add communications capability to the IEDs, each IED supplier was concerned that any increased functionality would compromise performance and drive the IED cost so high that no utility would buy it. Therefore, the industry vowed to keep costs competitive and performance high as standardisation was incorporated into the IED. • Substation-to-Utility Enterprise - This is the area of traditional SCADA communication protocols. The Data Acquisition, Processing and Control Systems Subcommittee of the Institute of Electrical and Electronics Engineers Power & Energy Society (IEEE PES) Substations Committee began developing a recommended practice in the early 1980s in an attempt to standardise master/remote communications practices. At that time, each SCADA system supplier had developed a proprietary protocol based on technology available at the time. These proprietary protocols exhibited varied message structures, terminal-to-Data Circuit terminating Equipment (DCE) and DCE-to-channel interfaces, and error detection and recovery schemes. • Communications Interfaces - There are interfaces to substation IEDs to acquire data, determine the operating status of each IED, support all communication protocols used by the IEDs, and support standard protocols being developed. There may be an interface to the Energy Management System (EMS) that allows system operators to monitor and control each substation and the EMS to receive data from the substation integration and automation system at different times. There may be an interface to the distribution management system with the same capabilities as the EMS interface. • Protocol and IEC 61850- A communication protocol allows communication between two devices. The devices must have the same protocol (and version) implemented. There are two capabilities a utility considers for an IED. The primary capability of an IED is its standalone capabilities, such as protecting the power system for a relay IED. The secondary capability of an IED is its integration capabilities, such as its physical interface (e.g., RS-232, RS-485, Ethernet) and its communication protocol (e.g. DNP3, Modbus, IEC 61850 MMS). This is where IEC 61850 Standard protocol for substation control and protection and communication plays a crucial part in any Smart Grid deployment. • Utility Communication Architecture - The use of international protocol standards is now recognised throughout the electric utility industry as a key to successful integration of the various parts of the electric utility enterprise. One area addresses substation integration and automation protocol standardisation efforts. • IEC 61850 Standardisation - Since its publication in 2004, the IEC 61850 communication standard has became more and more relevant in the field of substation automation. It provides an effective response to the needs of the open, deregulated energy market, which requires both reliable networks and extremely flexible technology – flexible enough to adapt to the substation challenges of the next twenty years. IEC 61850 has not only taken over the drive of the communication technology of the office networking sector, but it has also adopted the best possible protocols and configurations for high functionality and reliable data transmission. Industrial Ethernet, which has been hardened for substation purposes and provides a speed of 100 Mbit/s, offers enough bandwidth to ensure reliable information exchange between IEDs, as well as reliable communication from an IED to a substation controller. The definition of an effective process bus offers a standardised way to digitally connect conventional as well as intelligent CTs and VTs to relays. More than just a protocol, IEC 61850 also provides benefits in the areas of engineering and maintenance, especially with respect to combining devices from different vendors.

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 28

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

Key features of IEC 6185024

As in an actual project, the standard includes parts describing the requirements needed in substation communication, as well as parts describing the specification itself. The specification is structured as follows: An object-oriented and application-specific data model focused on substation automation. This model includes features representing nearly all existing equipment and functions in a

substation – circuit breakers, protection functions, current and voltage transformers, waveform recordings, and many more.

Communication services providing multiple methods for information exchange. These services cover reporting and logging of events, control of switches and functions and polling of data model information.

Peer-to-peer communication for fast data exchange between the feeder level devices (protection devices and bay controller) is supported with Generic Object Oriented Substation Event (GOOSE).

Support of sampled value exchange. File transfer for disturbance recordings. Communication services to connect primary equipment such as instrument transducers to relays. Decoupling of data model and communication services from specific communication

technologies. This technology independence guarantees long-term stability for the data model and opens up the

possibility to switch over to feature communication technologies. Today, the standard uses Industrial Ethernet with the following significant features:

- 100 Mbit/s bandwidth - Non-blocking switching technology - Priority tagging for important messages - Time synchronisation

A common formal description code, which allows a standardised representation of a system’s data model and its links to communication services.

This code, called SCL (Substation Configuration Description Language), covers all communication aspects according to IEC 61850. Based on Extensible Markup Language (XML), this code is an ideal electronic interchange format for configuration data.

A standardised conformance test which ensures interoperability between devices. Devices must pass multiple test cases: positive tests for correctly responding to stimulation

telegrammes, plus several negative tests for ignoring incorrect information. IEC 61850 offers a complete set of specifications covering all communication issues inside a

substation.

2.2.3 TECHNICAL ANALYSIS ON IEC 61850 STANDARD

Choosing the Right Protocol – Vendor specific and dependent interfaces vs. IEC 61850 Standard Compliant interfaces Before the establishment of IEC 61850, substation controls use proprietary, vendor dependent software and hardware interfaces. Without IEC 61850, power utility protection, control and automation would have different vendor specific solutions using regional and preferred utility standards. This resulted to incompatibility and non-interoperability of equipment. Additional interfaces cost a lot of money, result in relatively poor performance, errors, conflicts, glitches and additional expenses on regular software updates or hardware upgrades.

24 IEC Smart Grid Standardisation Roadmap, by Standardisation Management Board (SMB) Smart Grid Strategic Group (SG3) June 2010; Edition 1.0

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 29

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

There are several factors to consider when choosing the right protocol for the application. First, determine the most concerning system area such as the protocol from a SCADA master station to the SCADA RTUs, a protocol from substation IEDs to an RTU or a PLC, or a LAN in the substation. Second, the timing of the installation shall be determined, e.g., 6 months, 18 to 24 months, or 3 to 5 years. In some application areas, technology is changing so fast that the timing of installation can have a great impact on the protocol choice. Using IEC 61850 compliant gadgets and equipment will provide smooth operation and interoperability for at least the next 20 years or more.

2.2.4 CONCLUSION ON IEC 61850 STANDARD

PEA will greatly benefit from the use of IEC 61850-compliant substation equipment. It is not only the complete SA that could be properly implemented but, there will also be assurance that interoperability to new equipment or gadget will not be a problem for a near future.

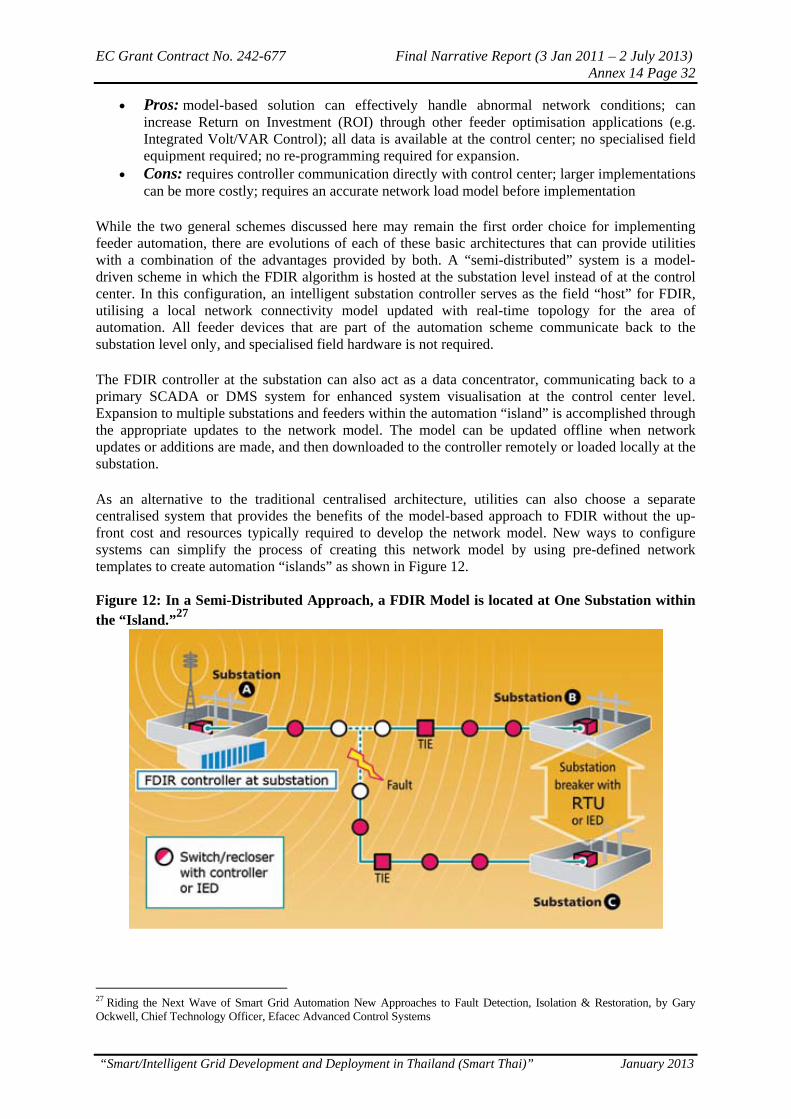

2.3 DISTRIBUTION FEEDER AUTOMATION (FEEDER REMOTE TERMINAL UNIT)

2.3.1 INTRODUCTION ON FEEDER AUTOMATION

When AMI and smart meter deployments begin, the next major focus area for Smart Grid projects is Distribution Automation (DA) and Distribution Management System (DMS). In particular, the automated isolation and restoration of distribution feeder faults is one application that can have significant impact on improving system reliability and quality of service. The value of new intelligent power meters and home area networks is largely dependent on a reliable and efficient distribution system that delivers quality power to the consumer. Fault management plays a greater role in the operation of distribution systems. It is imperative to localise faults in the distribution network (feeders) as precisely as possible in order to be able to restore power as quickly as possible to those sections of the network which have been de-energised although they are not faulty. For this purpose, there are applications and equipment designed for distribution system operation which narrows down the fault location as much as possible by analysing the fault messages and proposes ways of isolating the operational equipment which is suspected of being faulty. After that equipment has been isolated, switching proposals are then formulated whereby voltage can be restored to the fault-free but de-energised sections of the system without causing overload situations. Installing Feeder RTUs at strategic location along the distribution network enables such a process.

FEEDER Remote Terminal Unit (RTU)

An RTU (sometimes referred to as a Remote Telemetry Unit or Remote Terminal Unit) is a stand-alone data acquisition and control unit, generally microprocessor based, that monitors and controls equipment at a remote location. Its primary task is to control and acquire data from process equipment at a remote location and to transfer this data back to a central station. It generally has the facility of having its configuration and control programs dynamically downloaded from some central station. Although, traditionally, the RTU communicates back to some central station, it is also possible to communicate on a peer-to-peer basis with other RTUs. The RTU can also act as a relay station (sometimes referred to as a store and forward station) to another RTU that may not be accessible from the central station25.

25 Gordon R. Clarke, Deon Reynders, Edwin Wright, Practical modern SCADA protocols: DNP3, 60870.5 and related systems Newnes, 2004 ISBN 0-7506-5799-5 pages 19-21

EC Grant Contract No. 242-677 Final Narrative Report (3 Jan 2011 – 2 July 2013) Annex 14 Page 30

“Smart/Intelligent Grid Development and Deployment in Thailand (Smart Thai)” January 2013

An RTU monitors the field digital and analog parameters and transmits data to the Central Monitoring Station. An RTU can be interfaced with the Central Station with different communication media (usually serial (RS232, RS485, RS422) or Ethernet). RTU can support standard protocols (Modbus, IEC 60870-5-101/103/104, DNP3, IEC 60870-6-ICCP, IEC 61850, etc.) to interface any third party software26.