26

ANNUAL REPORT 2015 GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND ARSN 109 573 015

ANNUAL REPORT2015

GRESHAM PRIVATE EQUITYCO-INVESTMENT FUND

ARSN 109 573 015

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 1

INTRODUCTION 2 BARMINCO 3-5FINANCIAL REPORT 6DIRECTORY 24

CONTENTS

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 2

INTRODUCTION

We are pleased to enclose the Annual Report for the

Gresham Private Equity Co-Investment Fund (‘the

Fund’) for the financial year ended 30 June 2015.

The Fund has invested in seven portfolio companies,

of which six have now been realised, with Barminco

as the Fund’s remaining investment. While the

performance of currently realised investments in

the Fund is a significant disappointment to all, there

is full commitment to maximising the total value

of the Fund via it’s investment in Barminco. The

Fund’s focus continues to be on developing Barminco

for an exit in due course, and we have set out in the

following pages a summary of its performance and

key developments during FY2015.

SUNRISE DAM, WESTERN AUSTRALIA

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 3

Barminco is Australia’s leading underground

hard-rock miner, providing equipment, personnel

and technical expertise to conduct development

and production operations for mining companies.

Barminco also provides underground diamond

drilling services.

BARMINCO FY2015 YEAR IN REVIEW

The mining services industry continued to face

challenging conditions throughout FY2015. Prices

across most commodities have been at multi-year

lows, impacting the profitability of existing mines and

the pipeline of new projects.

In this environment, underground hard-rock

mining has been a relatively attractive part of the

mining services sector, as it also allows the client to

better manage ore grade and has higher barriers to

entry. Price performance in gold, Barminco’s key

commodity exposure, has also been positive relative

to other minerals (since the start of 2014, the A$ gold

price has increased by 13% compared to a 47% fall in

iron ore and 19% fall in thermal coal).

These factors, combined with Barminco’s strategy of

pursuing profitable growth opportunities, has put it in

a strong position to withstand the current downturn,

and ensures it is well placed to benefit as conditions

improve.

DIAMOND DRILLING AUMS JOINT VENTUREUNDERGROUND CONTRACT MINING

FINANCIAL PERFORMANCE AND POSITION

The Barminco Group (Barminco and its share of the

African Underground Mining Services joint venture

(‘AUMS’)) proportionate EBITDA in FY2015 was

$124.6m (FY2014: $129.3m). Barminco (excluding

AUMS) reported EBITDA of $95.1m for the period

(FY2014: $106.5m). The fall in earnings was primarily

driven by the full year impact of the Mount Lyell

mine closure and delayed commencement of

pipeline contracts. There were also operational

issues at certain sites including seismic events and

equipment availability, which the team has worked

hard to address. While the result was disappointing,

Barminco’s performance continues to compare

favourably to most ASX listed peers, which have

reported significant reductions in profitability over

the period, averaging more than 30%.

AUMS performed very well for the year driven by a

new management team and improved governance

and reporting processes. AUMS achieved EBITDA in

FY2015 of $59.1m (FY2014: $45.6m), outperforming

budget, and enabling the payment of a cash

distribution to the joint venture partners. AUMS is

accounted for on an equity accounting basis and

accordingly these earnings are not reflected in

Barminco’s reported EBITDA.

OTHER FINANCIAL HIGHLIGHTS DURING THE PERIOD

INCLUDE:

• maintenance of project margins and an improved

return on capital employed, reflecting a strong

focus on managing expenditure;

• a turnaround in performance of the diamond

drilling division, which increased revenue

materially; and

• completing an innovative capital management

transaction to repurchase nearly US$100m of

the company’s Senior Notes. The repurchase

was funded by utilising the value in the Notes’

cross-currency swap that had accrued as a result

of favourable exchange rate movements. This

transaction involved no cash outlay for Barminco

and will generate annual cash interest savings of

over $6m.

In 2013 Barminco refinanced its capital structure

with the issuance of US 5-year Senior Notes. The

Notes were designed to provide the Company with

stable and accommodating financing to execute its

strategy. At 30 June 2015, Barminco also had cash

of $105m (an increase of $9m on the previous year’s

closing balance) which can be used to fund growth

capex and other strategic opportunities.

BARMINCO STRUCTURE

ESTABLISHED 1989

HEADQUARTERS: HAZELMERE, WESTERN AUSTRALIA.

OVER 2000 EMPLOYEES ACROSS AUSTRALIA & AFRICA LARGEST SINGLE COMPANY OWNED FLEET OF UNDERGROUND MECHANISED EQUIPMENT IN THE WORLD

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 4

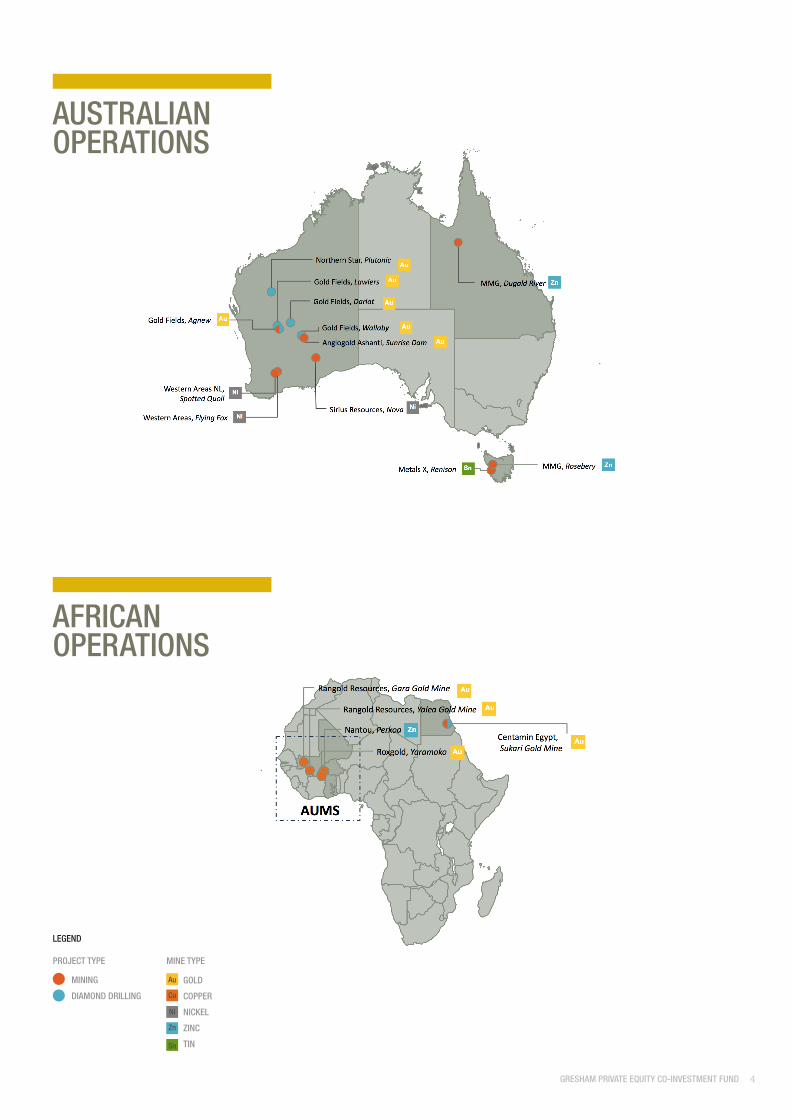

AUSTRALIAN OPERATIONS

AFRICANOPERATIONS

LEGEND

PROJECT TYPE MINE TYPE

MINING

DIAMOND DRILLING

GOLD

COPPER

NICKEL

ZINC

TIN

Au

Cu

Ni

Zn

Sn

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 5

OPERATIONAL HIGHLIGHTS

Barminco recorded a number of operational

achievements during FY2015, including:

• industry leading safety performance. Barminco

achieved a Lost Time Injury Frequency Rate

(‘LTIFR’) of zero for FY2015, an excellent outcome

in the industry and reflective of the commitment

to safety at every level of the company. New

safety initiatives significantly reduced critical

risk areas such as truck fires, light vehicle

collisions and explosives management breaches,

and a companywide hand safety campaign

materially reduced the incidence of hand

injuries. Barminco is also continuing to develop

innovations to improve safety performance

such as an in-vehicle management system for

measuring and changing driver behaviour, and

trialling truck driver fatigue monitoring.

• the award of $700m in new contracts and

contract extensions in Barminco’s core

Australian market. The company won new

underground mining contracts at Sirius’ Nova

nickel project ($130m), and MMG’s Rosebery

mine ($110m). Contract extensions were also

secured at Western Areas’ Flying Fox and Spotted

Quoll mines ($190m) and AngloGold Ashanti’s

Sunrise Dam ($270m).

• a range of initiatives designed to reduce costs and

improve productivity, such as the introduction of

Sandvik trucks, strategic procurement and rapid

sourcing.

THE YEAR AHEAD

The industry environment is expected to remain very

challenging, although the further depreciation of the

Australian dollar will help support the profitability of

local mines. There are also increasing opportunities

in lower cost international markets, which Barminco

is selectively pursuing.

The new contract awards during FY2015 have

provided Barminco with a solid base for FY2016.

Barminco will continue its focus on driving profitable

growth through additional operating efficiencies, and

utilising enhanced marketed capabilities to build its

workbook.

SUNRISE DAM, WESTERN AUSTRALIA

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 6

FINANCIALREPORT

DIRECTORS’ REPORTThe directors of Gresham Funds Management Limited (the “Company”), the Responsible Entity of the Gresham Private Equity Co-Investment Fund (the “Fund”), submit their report together with the financial report of the Fund for the financial year ended 30 June 2015.

DIRECTORSThe following persons held office as directors of the Company during the financial year and since the end of the financial year and up to the date of this report, unless noted otherwise:

James P Graham AM (Chairman) Roger S Casey (Deputy Chairman) Terence J BowenAntony G Breuer Tim J BultCharles J Graham

PRINCIPAL ACTIVITIES The Fund since inception has invested in seven entities in a wide range of sectors in Australia and New Zealand. Following the sale of six of these investments, the Fund’s remaining investment is in Barminco, which is predominately engaged in underground hard rock contract mining principally in Australia and Africa.

REVIEW OF OPERATIONSOn 19 August 2014, in order to optimise the value of the Funds’ investment in Barminco, unitholders of the institutional Gresham Private Equity Funds No. 2a and No. 2b approved the extension of the life of the those Funds from 30 June 2015 to 30 June 2018, which automatically resulted in an extension of the life of the Fund for the same period. In addition, the Fund’s investment in Silk Logistics Group was finalised during the year; and monies that were held in escrow pending completion arrangements regarding potential claims from the disposal of Tasmanian Walking Company were received.

As at 30 June 2015, Unitholders had invested 95.0 cents per unit in the Fund and have received cash distributions of 31.2 cents per unit, resulting in a net cash investment in the Fund of 63.8 cents per unit. As at 30 June 2015, the net assets of the Fund had an assessed carrying value of 18.8 cents per unit, however the ultimate financial outcome will reflect the underlying business and market conditions at the time of investment realisations.

For the financial year ended 30 June 2015, the net operating loss before financing costs attributable to Unitholders was $429,414 (2014: net operating profit before financing costs attributable to Unitholders $254,092), reflecting an overall net gain on the Fund’s investments offset by management and operating expenses of the Fund. The valuation method used by the Manager in determining this result is in accordance with Australian and international standards for Private Equity. This method reflects the fact that portfolio companies are long-term, illiquid investments. The Manager’s focus is on maximising the value of Barminco, the Fund’s remaining individual investment.

DISTRIBUTIONSNo cash distributions have been paid by the Fund for the year ended 30 June 2015 (2014: $2,489,288).

SIGNIFICANT CHANGESIn the opinion of the directors, there were no significant changes in the state of affairs of the Fund that occurred during the financial year under review not otherwise disclosed in this report and financial statements.

MATTERS SUBSEQUENT TO BALANCE DATEExcept as disclosed in the financial report, no matters or circumstances have arisen since 30 June 2015 that have significantly affected or may significantly affect: a) the operations of the Fund in future financial years; orb) the results of those operations in future financial years; orc) the state of affairs of the Fund in future financial years.

LIKELY DEVELOPMENTS AND EXPECTED RESULTS OF OPERATIONSThe Responsible Entity acknowledged that the extension to the life of the Fund noted above would have a direct cost in terms of the management fees and other expenses incurred over the period of extension. Accordingly, the Responsible Entity has agreed to reduce the basis of calculation of Management and Service fees from 1 July 2015 by 15%.

Other than the above, there are no material changes proposed for the operation of the Fund.

VALUE OF ASSETSThe carrying value of the Fund’s net assets attributable to Unitholders at 30 June 2015 was $19,214,739 (2014: $19,644,153 after cash distributions of $2,489,288) which is derived using the bases set out in Note 1 to the financial statements.

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 7

DIRECTORS’ REPORT (CONTINUED)

INDEMNIFICATION & INSURANCE OF OFFICERS AND AUDITORDuring the financial year, no insurance premiums were paid out of the Fund in respect of any insurance cover relating to the Responsible Entity or the auditor. So long as the officers of the Responsible Entity act in accordance with the Fund’s Constitution and the law, they will remain fully indemnified out of the assets of the Fund against any losses incurred whilst acting on behalf of the Fund. There is no indemnification of the auditor of the Fund out of the assets of the Fund.

FEES PAID TO AND INTERESTS HELD IN THE FUND BY THE RESPONSIBLE ENTITY OR ITS ASSOCIATESNote 11 sets out the fees paid to and interests held in the Fund by the Responsible Entity or its associates.

ENVIRONMENTAL REGULATIONThe activities of the Fund itself are not subject to any particular or significant environmental regulations under a Commonwealth, State or Territory law.

AUDITOR’S INDEPENDENCE DECLARATIONA copy of the Auditor’s Independence Declaration as required under Section 307 of the Corporations Act 2001 is set out on page 8.

This report is made out in accordance with a resolution of the directors.

James P Graham AM

Chairman

Sydney, 28 July 2015

FINANCIALREPORT(CONTINUED)

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 8

AUDITOR’S INDEPENDENCEDECLARATION

AUDITOR’S INDEPENDENCE DECLARATION As lead auditor for the audit of Gresham Private Equity Co-Investment Fund for the year ended 30 June 2015, I declare that to the best of my knowledge and belief, there have been:

a) no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and b) no contraventions of any applicable code of professional conduct in relation to the audit.

This declaration is in respect of Gresham Private Equity Co-Investment Fund during the period.

CJ Heath Partner PricewaterhouseCoopers

Sydney 28 July 2015

PricewaterhouseCoopers, ABN 52 780 433 757 Darling Park Tower 2, 201 Sussex Street, GPO BOX 2650, SYDNEY NSW 1171 DX 77 Sydney, Australia T +61 2 8266 0000, F +61 2 8266 9999, www.pwc.com.au Liability limited by a scheme approved under Professional Standards Legislation

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 9

note 2015 2014

$ $

INVESTMENT INCOME

Interest 41,384 47,143

Other income 4 226,207 343,630

Net gain on investments at fair value through profit or loss 289,844 1,005,938

TOTAL INVESTMENT INCOME 557,435 1,396,711

Expenditure

Administration and other expenses 39,009 38,814

Responsible Entity’s remuneration 11 947,840 1,103,805

TOTAL EXPENDITURE 986,849 1,142,619

Net operating profit/(loss) (429,414) 254,092

Financing costs/benefits attributable to Unitholders

(Increase)/decrease in net assets attributable to Unitholders 5(c) 429,414 (254,092)

TOTAL COMPREHENSIVE INCOME - -

The above statement of comprehensive income should be read in conjunction with the accompanying notes.

STATEMENT OFCOMPREHENSIVE INCOMEFOR THE YEAR ENDED 30 JUNE 2015

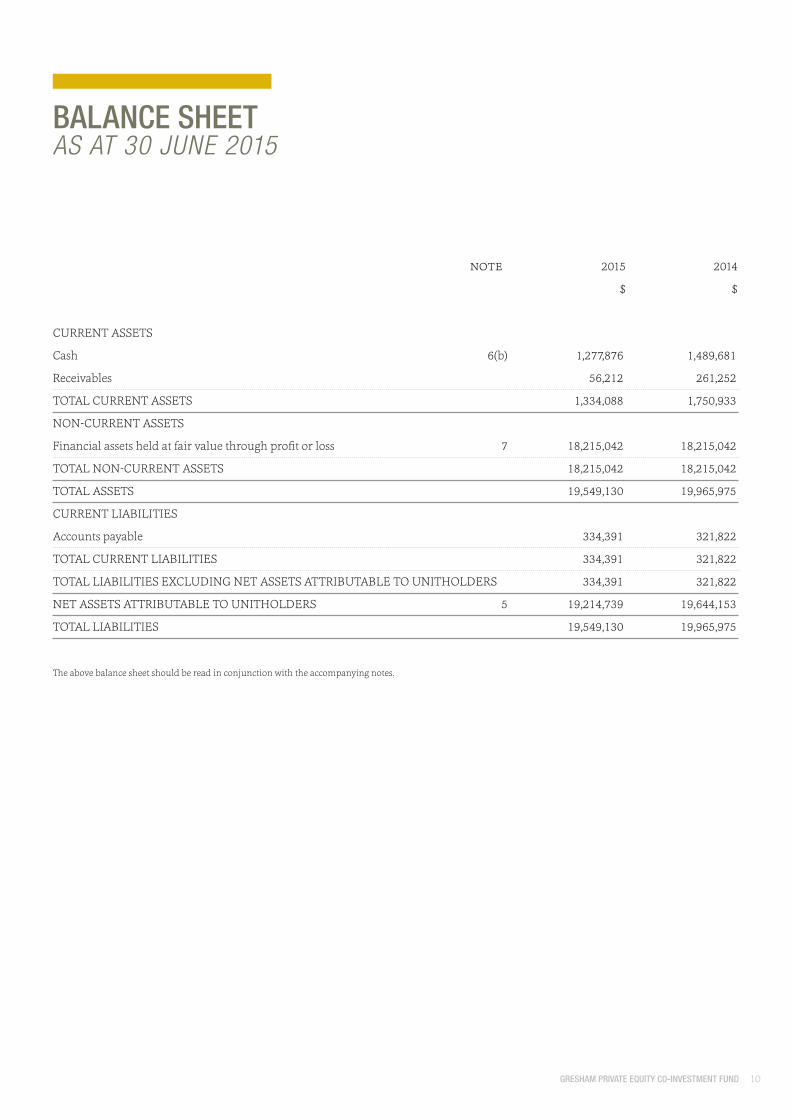

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 10

note 2015 2014

$ $

CURRENT ASSETS

Cash 6(b) 1,277,876 1,489,681

Receivables 56,212 261,252

TOTAL CURRENT ASSETS 1,334,088 1,750,933

NON-CURRENT ASSETS

Financial assets held at fair value through profit or loss 7 18,215,042 18,215,042

TOTAL NON-CURRENT ASSETS 18,215,042 18,215,042

TOTAL ASSETS 19,549,130 19,965,975

CURRENT LIABILITIES

Accounts payable 334,391 321,822

TOTAL CURRENT LIABILITIES 334,391 321,822

TOTAL LIABILITIES EXCLUDING NET ASSETS ATTRIBUTABLE TO UNITHOLDERS 334,391 321,822

NET ASSETS ATTRIBUTABLE TO UNITHOLDERS 5 19,214,739 19,644,153

TOTAL LIABILITIES 19,549,130 19,965,975

The above balance sheet should be read in conjunction with the accompanying notes.

BALANCE SHEETAS AT 30 JUNE 2015

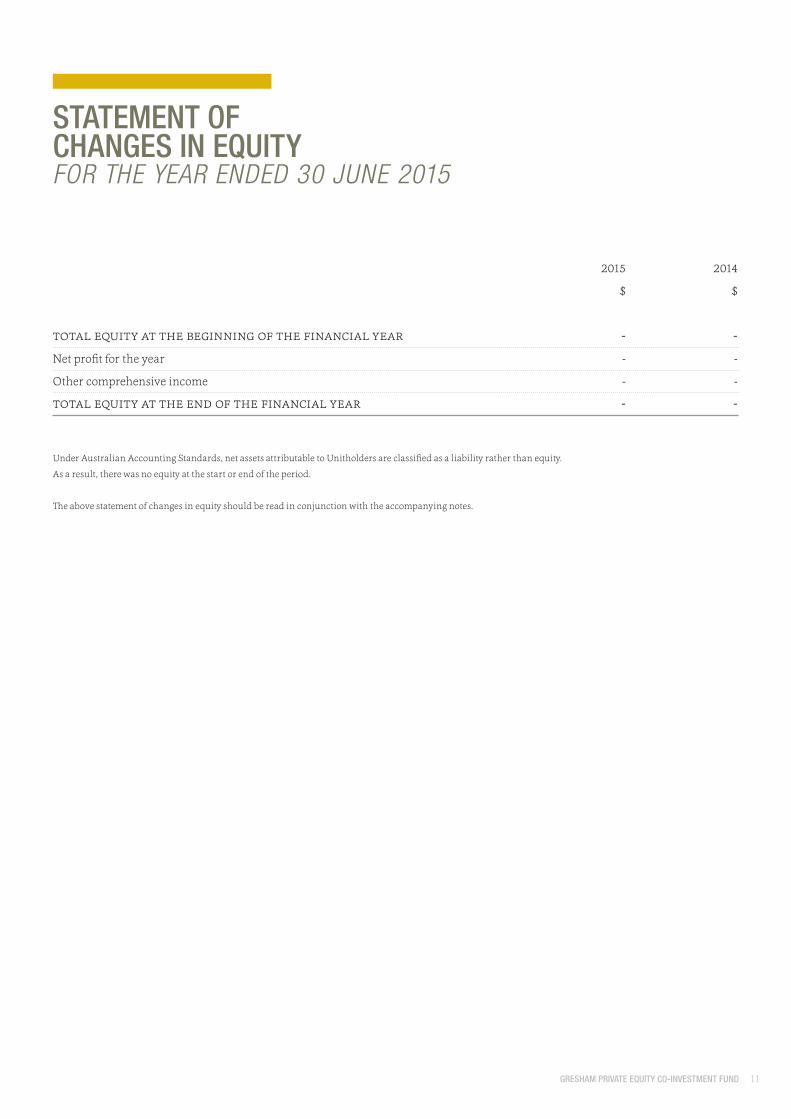

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 11

Under Australian Accounting Standards, net assets attributable to Unitholders are classified as a liability rather than equity.

As a result, there was no equity at the start or end of the period.

The above statement of changes in equity should be read in conjunction with the accompanying notes.

2015 2014

$ $

total equity at the beginning of the financial year - -Net profit for the year - -

Other comprehensive income - -

total equity at the end of the financial year - -

STATEMENT OFCHANGES IN EQUITYFOR THE YEAR ENDED 30 JUNE 2015

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 12

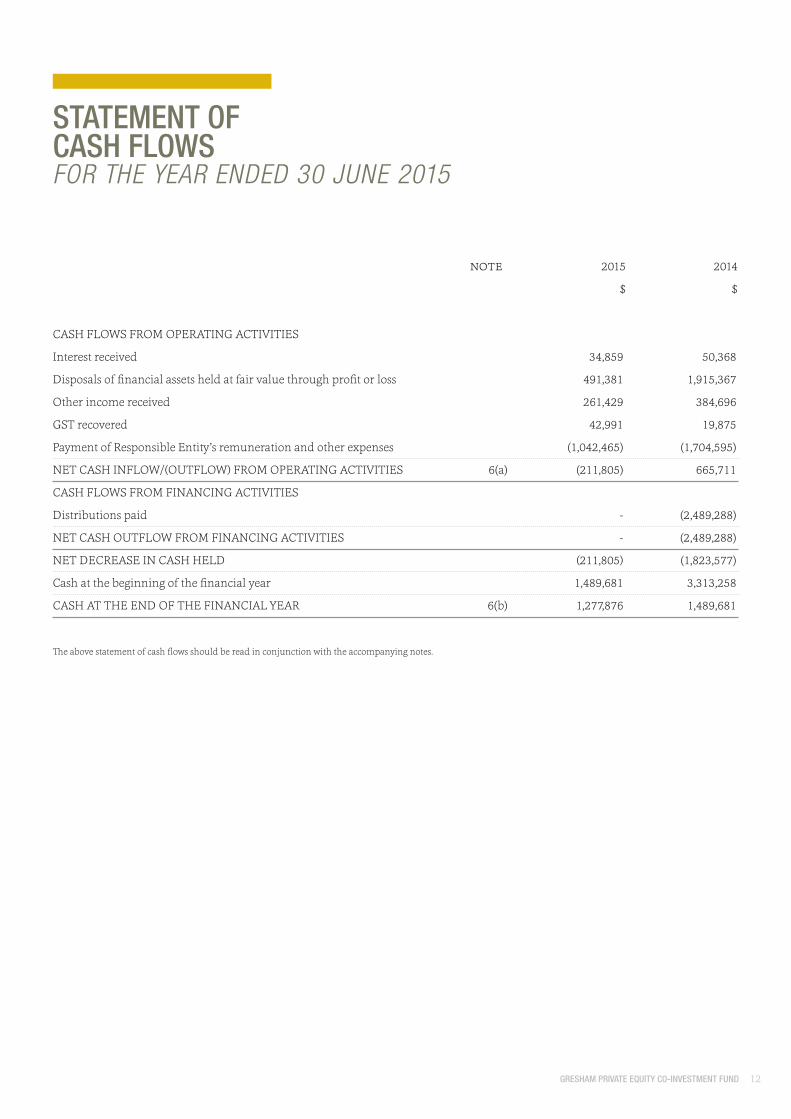

note 2015 2014

$ $

CASH FLOWS FROM OPERATING ACTIVITIES

Interest received 34,859 50,368

Disposals of financial assets held at fair value through profit or loss 491,381 1,915,367

Other income received 261,429 384,696

GST recovered 42,991 19,875

Payment of Responsible Entity’s remuneration and other expenses (1,042,465) (1,704,595)

NET CASH INFLOW/(OUTFLOW) FROM OPERATING ACTIVITIES 6(a) (211,805) 665,711

CASH FLOWS FROM FINANCING ACTIVITIES

Distributions paid - (2,489,288)

NET CASH OUTFLOW FROM FINANCING ACTIVITIES - (2,489,288)

NET DECREASE IN CASH HELD (211,805) (1,823,577)

Cash at the beginning of the financial year 1,489,681 3,313,258

CASH AT THE END OF THE FINANCIAL YEAR 6(b) 1,277,876 1,489,681

The above statement of cash flows should be read in conjunction with the accompanying notes.

STATEMENT OFCASH FLOWSFOR THE YEAR ENDED 30 JUNE 2015

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 13

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PREPARATIONThis general purpose financial report for the financial year ended 30 June 2015 for the Gresham Private Equity Co-Investment Fund as an individual entity, has been prepared in accordance with the Fund’s Constitution. The Constitution requires the financial report to be prepared in accordance with Australian Accounting Standards, other authoritative pronouncements of the Australian Accounting Standards Board, Urgent Issues Group (UIG) Consensus Views and the Corporations Act 2001. The financial statements of the Fund also comply with International Financial Reporting Standards as issued by the International Accounting Standards Board.

The financial statements have been prepared under the historical cost convention, as modified by the revaluation of investments held at fair value with changes in fair value recognised through the statement of comprehensive income.

The principal accounting policies applied in the preparation of these financial statements are set out below. The accounting policies adopted are consistent with the prior year unless otherwise stated.

USE OF ESTIMATES AND JUDGEMENTSThe preparation of financial statements in accordance with Australian Accounting Standards requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Critical accounting judgments made in applying the Fund’s accounting policies pertains to the determination of the fair value of financial instruments. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the year in which the estimate is revised and in any future years affected. It is possible that outcomes in future periods which are different from the assumptions used could require a material adjustment to the carrying amount of the financial instruments affected.

DETERMINATION OF FAIR VALUEThe Fund’s accounting policies and disclosures require the determination of fair value for all of the Fund’s financial assets held at fair value through profit and loss. The fair value for such assets has been determined for measurement and disclosure purposes based on the discounted cash flow method. The effect of changes to the key assumptions and inputs is discussed in Note 10 – Financial Instruments.

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 14

NOTE 1. SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (CONTINUED)

VALUATION OF FINANCIAL ASSETS AND LIABILITIES

HELD AT FAIR VALUE The Fund has designated all of its investments as at fair value through profit or loss. Individual investments may take the form of a combination of equities and loans and are managed as a single investment. These investments are initially recognised on the date the Fund becomes party to the contractual agreement at fair value, typically represented by cost. Investments are valued at their net fair value as at reporting date. Gains and losses arising from changes in the fair value of the financial assets at fair value through profit or loss category are included in the statement of comprehensive income in the period in which they arise. Investments are valued in line with industry practice using appropriate valuation techniques as reasonably determined by the Responsible Entity and which reflect market conditions as at the reporting date. However, given the financial markets’ volatility and economic conditions, future valuations may be volatile.

CASHCash includes cash in hand, deposits held at call with banks, and other short-term highly liquid investments with maturities of three months or less, net of bank overdrafts, if any.

Payments and receipts relating to the purchase and sale of investments are classified as cash flows from operating activities, as movements in the fair value of these investments represent the Fund’s main income generating activity.

INVESTMENT INCOME AND EXPENSESInterest income and expenses are recognised in the statement of comprehensive income for all debt instruments using the effective interest method. Dividends from companies are recorded as income when the Fund’s right to receive payment is established. Other investment income and expenses are brought to account on an accruals basis.

DISTRIBUTION EXPENSE AND CHANGES IN NET ASSET

VALUE ATTRIBUTABLE TO UNITHOLDERSThe Fund makes distributions in accordance with the Fund’s Constitution. The taxable and tax free component of distributions is recognised in the statement of comprehensive income as a distribution expense within financing costs. The difference between the distributions made and the taxable and tax free component of these distributions is recognised as a return of capital within net assets attributable to Unitholders. Income and expenses that are respectively not taxable or not deductible and do not form part of the taxable component of distributions are recognised in the statement of comprehensive income as changes in net assets attributable to Unitholders within financing costs.

RESPONSIBLE ENTITY’S REMUNERATIONResponsible Entity’s remuneration has been calculated in accordance with the Fund’s Constitution, noting that the Responsible Entity has voluntarily reduced the basis of calculation of Management Fees and Service Fees by 15% effective from 1 July 2015.

COMPARITIVE PERIODComparative information is reclassified where appropriate to enhance comparability.

RECEIVABLESReceivables may include amounts for dividends, interest and securities sold where settlement has not yet occurred. Amounts are generally received within 30 days of being recorded as receivables, with the exception of interest on certain non-current investments.

ACCOUNTS PAYABLEAccounts payable represent liabilities for amounts owing by the Fund that are unpaid at year end.

GOODS AND SERVICES TAX (GST)The Fund qualifies for Reduced Input Tax Credits. Investment management fees and other expenses have been recognised in the statement of comprehensive income inclusive of the amount of GST not recoverable from the Australian Taxation Office (ATO). The net amount of GST recoverable from the ATO is included in receivables in the balance sheet. Accounts payable are inclusive of GST. Cash flows relating to GST are included in the statement of cash flows on a gross basis.

NEW ACCOUNTING STANDARDS AND

INTERPRETATIONSCertain new accounting standards and interpretations have been published that are not mandatory for 30 June 2015 reporting periods. The directors’ assessment of the impact of these new standards (to the extent relevant to the Fund) and interpretations is set out below:

AASB 9 Financial Instruments addresses the classification, measurement and derecognition of financial assets and financial liabilities. The standard is not applicable until 1 January 2018 but is available for early adoption. When adopted, there will be no impact from the new classification, measurement and derecognition rules on the Fund’s financial assets and financial liabilities. The Fund has not yet decided when to adopt AASB 9.

AASB 15 Revenue from Contracts with Customers addresses the recognition of revenue from contracts and is effective from 1 January 2017. It replaces AASB 118 which covers contracts for goods and services and AASB 111 which covers construction contracts. The Fund does not expect changes from the way it currently recognises revenue from contracts.

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 15

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

NOTE 1. SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (CONTINUED)

NEW ACCOUNTING STANDARDS AND

INTERPRETATIONS (CONTINUED)

AASB 2015-2 Amendments to Australian

Accounting Standards - Disclosure Initiative:

Amendments to AASB 101 is effective from 1 January

2016. In January 2015, the AASB made various

amendments to AASB 101 as part of the Disclosure

Initiative which explores how financial statement

disclosures can be improved. The amendments

clarify guidance in AASB 101 on materiality and

aggregation, presentation of subtotals, structure of

financial statements and disclosure of accounting

policies. These amendments do not require

specific changes. However, they clarify a number

of presentation issues and highlight that preparers

are permitted to tailor the format and presentation

of the financial statements to their circumstances

and the needs of users. The Fund does not expect

major changes from the way it currently presents the

financial information.

FUNCTIONAL AND PRESENTATION CURRENCYItems included in the financial statements are measured using the currency of the primary economic environment in which the entity operates (“the functional currency”). The financial statements are presented in Australian dollars, which is the Fund’s functional and presentation currency.

ISSUE DATEThe financial statements were authorised for issue by the directors on 28 July 2015. The directors of the Responsible Entity have the power to amend and reissue the financial statements.

NOTE 2. TAXATIONUnder current legislation, the Fund would not be liable to income tax to the extent that the income of the Fund is distributed in full to Unitholders.

NOTE 3. LIFE OF FUND

The Fund was registered on 29 June 2004 under a

Constitution dated 28 June 2004 and was due to

terminate on 30 June 2015. As explained in the

Fund’s annual report for the year ended 30 June 2014,

the manager of the contractually linked institutional

Gresham Private Equity Funds No. 2a and No. 2b (“the

institutional funds”) recommended that in order to

optimise the value of the investment in Barminco,

the institutional funds’ unitholders extend the life of

these funds from 30 June 2015 to 30 June 2018, which

would automatically result in an extension of the life

of the Fund for the same period. On 19 August 2014,

the institutional unitholders approved the extension,

and hence the Fund’s life has also been extended to 30

June 2018.

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 16

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

NOTE 4. OTHER INCOME note 2015 2014

$ $

Transaction and advisory fees 201,386 241,542

Other income 24,821 102,088

226,207 343,630

NOTE 5. NET ASSETS ATTRIBUTABLE TO UNITHOLDERSNet assets attributable to Unitholders comprises:

Ordinary units 5(a) 67,790,563 67,790,563

Sponsor units 5(b) 500 500

Cumulative changes in net assets attributable to Unitholders transferred from the statement of comprehensive income 5(c) (48,576,324) (48,146,910)

19,214,739 19,644,153

Movements in the components of net assets attributable to Unitholders are as follows:

2015 2014 2015 2014

number number $ $

a) Ordinary units (refer below)

opening balance - 1 july 102,020,000 102,020,000 67,790,563 70,279,851

Nil (2014: 2.44) cents per unit return - - - (2,489,288)

closing balance - 30 june 102,020,000 102,020,000 67,790,563 67,790,563 As stipulated in the Fund’s Constitution, each ordinary unit represents a right to an individual share in the Fund and does not extend to a right to the underlying assets of the Fund. Calls are made in accordance with the Fund’s Constitution.

b) Sponsor units (refer below) 500,000 500,000 500 500

As stipulated in the Fund’s Constitution, sponsor units, which are held by the Manager of the Fund, Gresham Private Equity Limited, a related body corporate of the Responsible Entity, carry an entitlement to a share of any sponsor’s unit distributions of the Fund. The sponsor’s unit distributions are payable out of the proceeds of realised investments of the Fund. The distribution is calculated each time an investment is realised by the Fund. Ordinary Unitholders are entitled to a return equal to the Relevant Outflows of the Fund plus a preferred 8% per annum in respect of the Relevant Inflows and Relevant Outflows before any sponsor’s unit distribution becomes payable. Subject to this priority return for ordinary Unitholders, the sponsor’s unit distribution (if any) payable when investments are realised will generally be 20% of the profit, net of certain expenses, achieved. If the Fund’s assets were realised at their estimated fair value at reporting date, the resultant sponsor’s unit distribution entitlement would be $nil (2014: $nil).

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 17

NOTE 5. NET ASSETS ATTRIBUTABLE TO UNITHOLDERS (CONTINUED)

c) Cumulative changes in net assets attributable to Unitholders transferred from the statement of comprehensive income

2015 2014

$ $

opening balance - 1 july (48,146,910) (48,401,002)

Movement in net assets attributable to Unitholders transferred from the statement of comprehensive income (429,414) 254,092

closing balance - 30 june (48,576,324) (48,146,910)

NOTE 6. RECONCILIATION OF NET PROFIT/(LOSS) TO NET CASH INFLOW/(OUTFLOW) FROM OPERATING ACTIVITIES

a) Reconciliation of net profit/(loss) to net cash inflow/(outflow) from operating activities

Net profit for the year - -

Net operating profit/(loss) (429,414) 254,092

Change in operating assets and liabilities:

Decrease in investments - 1,110,966

(Increase)/decrease in receivables 205,040 (200,959)

Increase/(decrease) in accounts payable and provisions 12,569 (498,388)

net cash inflow/(outflow) from operating activities (211,805) 665,711

b) Components of cash

Cash as at the end of the financial year as shown in the statement of cash flows is equal to the cash position as shown on the

balance sheet.

NOTE 7. FINANCIAL ASSETS HELD AT FAIR VALUE THROUGH PROFIT OR LOSS

Investments 18,215,042 18,215,042

An overview of the risk exposures relating to financial assets at fair value through profit or loss is included in Note 10.

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 18

NOTE 8. BORROWING/FINANCING FACILITIESThe Fund did not have during the year and does not have any borrowing or financing facilities in place at the date of this report.

NOTE 9. REDEMPTION ARRANGEMENTThe Responsible Entity has no obligation in the Constitution to repurchase units or redeem units issued under the Fund’s Constitution.

NOTE 10. FINANCIAL INSTRUMENTSThe Fund’s activities expose it to a variety of financial risks: market risk (including price risk, foreign exchange risk and interest rate risk), credit risk and liquidity risk.

The Fund’s overall risk management programme which is carried out by the Manager focuses on ensuring compliance with the Constitution and seeks to maximise the returns derived for the level of risk to which the Fund is exposed.

PRICE RISKInvestments are valued in line with industry practice using appropriate valuation techniques as reasonably determined by the Manager. When applying a discounted cash flow technique, future earnings are discounted using the weighted average cost of capital (‘WACC’) and a terminal growth rate is applied. The determination of the values of the relevant inputs to be applied is a matter of professional judgement. The key inputs relate to earnings, weighted average cost of capital and terminal growth rate. The impact on the value of the Fund’s investments if these key inputs were 5% higher or 5% lower is as follows:

+5% -5% +5% -5% +5% -5%

30 june 2015 $2.7m $(2.7)m $(3.2)m $3.6m $0.3m $(0.3)m

30 june 2014 $3.1m $(3.1)m $(3.7)m $4.1m $0.4m $(0.4)m

earnings wacc terminal growth rate

The Manager mitigated price risk in the investment strategy by limiting the Fund’s exposure to an investment in a single entity to 20% of committed capital, such limit being able to be increased with the approval of the Policy Committee on a case by case basis, and by careful selection of prospective investment opportunities.

LIQUIDITY RISKLiquidity risk is the risk that the Fund may not be able to generate sufficient cash resources to settle its obligations in full as they fall due or can only do so on terms that are materially disadvantageous.

The Fund manages its net assets attributable to Unitholders as capital, notwithstanding net assets attributable to Unitholders are classified as a liability. Settlement of this liability is dependent on realisation of assets, with the net proceeds from such realisations being distributed to Unitholders as soon as practicable in accordance with the Constitution.

FOREIGN CURRENCY EXCHANGE RATE RISKForeign currency exchange rate risk is the risk that the Fund’s assets will fluctuate due to changes in exchange rates. The Fund does not have any significant exposure to foreign currency risk.

INTEREST RATE RISKInterest rate risk includes cash flow interest rate risk on financial instruments with variable interest rates as well as interest rate risk on the value of financial instruments with fixed interest rates that will fluctuate due to changes in market interest rates. The Fund does not have any significant exposure to interest rate risk.

CREDIT RISKCredit risk is the risk that a counter party will fail to perform obligations under a contract. The Fund does not have any significant exposure to credit risk.

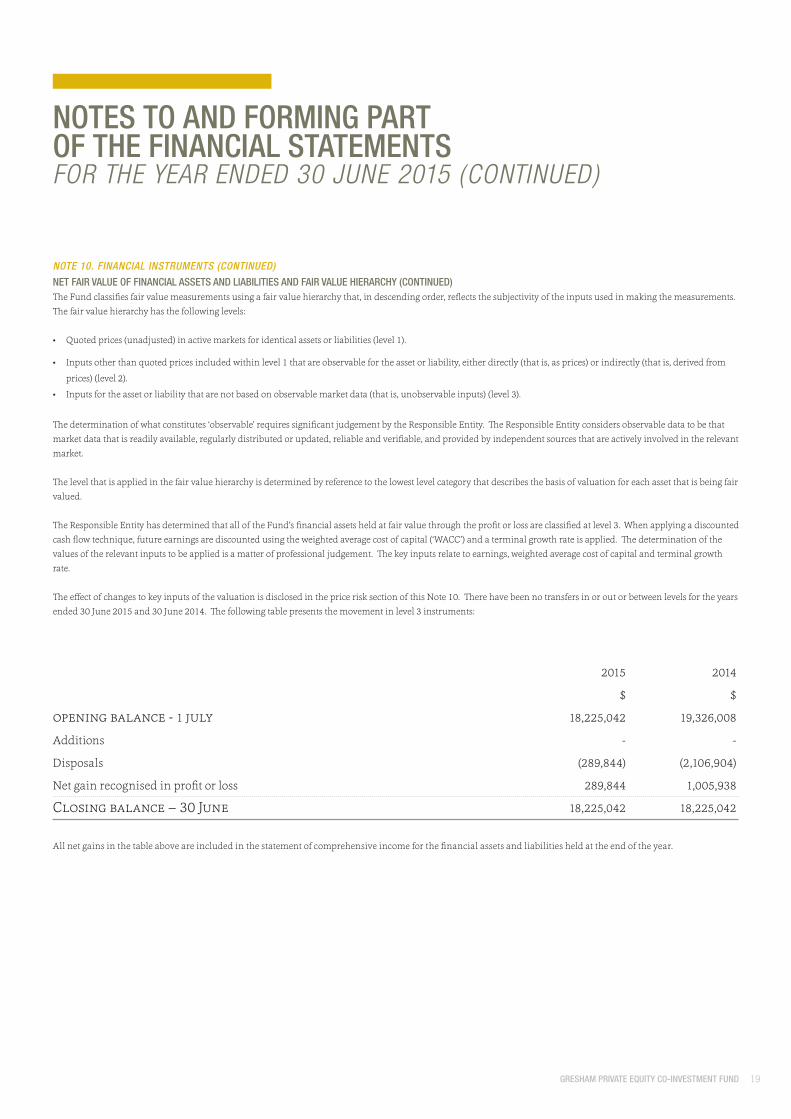

NET FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES AND FAIR VALUE HIERARCHYThe carrying value of the Fund’s financial assets and liabilities included in the balance sheet approximate their fair value.

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 19

NOTE 10. FINANCIAL INSTRUMENTS (CONTINUED)

NET FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES AND FAIR VALUE HIERARCHY (CONTINUED)The Fund classifies fair value measurements using a fair value hierarchy that, in descending order, reflects the subjectivity of the inputs used in making the measurements. The fair value hierarchy has the following levels:

• Quoted prices (unadjusted) in active markets for identical assets or liabilities (level 1).

• Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from

prices) (level 2).

• Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs) (level 3).

The determination of what constitutes ‘observable’ requires significant judgement by the Responsible Entity. The Responsible Entity considers observable data to be that market data that is readily available, regularly distributed or updated, reliable and verifiable, and provided by independent sources that are actively involved in the relevant market.

The level that is applied in the fair value hierarchy is determined by reference to the lowest level category that describes the basis of valuation for each asset that is being fair valued.

The Responsible Entity has determined that all of the Fund’s financial assets held at fair value through the profit or loss are classified at level 3. When applying a discounted cash flow technique, future earnings are discounted using the weighted average cost of capital (‘WACC’) and a terminal growth rate is applied. The determination of the values of the relevant inputs to be applied is a matter of professional judgement. The key inputs relate to earnings, weighted average cost of capital and terminal growth rate.

The effect of changes to key inputs of the valuation is disclosed in the price risk section of this Note 10. There have been no transfers in or out or between levels for the years ended 30 June 2015 and 30 June 2014. The following table presents the movement in level 3 instruments:

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

2015 2014

$ $

opening balance - 1 july 18,225,042 19,326,008

Additions - -

Disposals (289,844) (2,106,904)

Net gain recognised in profit or loss 289,844 1,005,938

Closing balance – 30 June 18,225,042 18,225,042

All net gains in the table above are included in the statement of comprehensive income for the financial assets and liabilities held at the end of the year.

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 20

NOTE 11. RELATED PARTIES

RESPONSIBLE ENTITYThe Responsible Entity of the Fund is Gresham Funds Management Limited, which is incorporated and domiciled in Australia. The registered office and principal place of business is:

Level 17,

167 Macquarie Street,

Sydney NSW 2000

KEY MANAGEMENT PERSONNELKey management personnel, who comprise the directors of the Responsible Entity during the financial year, were as follows:

James P Graham AM (Chairman) Roger S Casey (Deputy Chairman) Terence J BowenAntony G Breuer Tim J BultCharles J Graham

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

TRANSACTION WITH RELATED PARTIESResponsible Entity’s remuneration and non recoverable GST paid or payable in accordance with the Constitution:

2015 2014

$ $

Management fees 585,066 717,775

Service fees 262,081 265,259

Share of transaction and advisory fees 100,693 120,771

947,840 1,103,805

No payments are made by the Fund to key management personnel.

BALANCES WITH RELATED PARTIESThe aggregate amounts payable to related parties by the Fund at balance date comprise:

responsible entity 306,233 290,252

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 21

NOTES TO AND FORMING PARTOF THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 30 JUNE 2015 (CONTINUED)

NOTE 11. RELATED PARTIES (CONTINUED)

UNITS HELD BY RELATED PARTIES

The number of units held in the Fund by a related body corporate of the Responsible Entity as at the date of this report is as follows:

2015 2014

number numbersponsor units 500,000 500,000

NOTE 12. AUDITOR’S REMUNERATION 2015 2014

$ $

Auditing the financial statements 21,560 22,770

Taxation services 11,055 10,885

32,615 33,655

In addition, the auditor’s remuneration in relation to the Fund’s half-year audit review, Compliance Plan audit and other expenses totalling $40,600 (2014: $41,100) have been borne by the Responsible Entity.

NOTE 13. CAPITAL COMMITMENTSAs at 30 June 2015, the Fund had no capital commitments (30 June 2014: $nil).

NOTE 14. CONTINGENT ASSETS AND LIABILITIESAs at 30 June 2015, contingent assets of $34,000 (30 June 2014: $316,000) may be recoverable in relation to completion arrangements regarding potential claims under warranties, indemnities and other obligations arising from the Fund’s investments.

Other than the above, there are no other contingent assets or liabilities relating to the Fund as at 30 June 2015 (30 June 2014: $nil).

NOTE 15. EVENTS OCCURRING AFTER THE REPORTING DATENo significant events have occurred since balance date which could impact on the financial position of the Fund disclosed in the balance sheet as at 30 June 2015 or on the results and cash flows of the Fund for the year ended on that date.

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 22

DIRECTORS’DECLARATION

In the directors’ opinion:

(a) the financial statements and notes set out on pages 9 to 21 are in accordance with the Corporations Act 2001, including:

(i) complying with Australian Accounting Standards, the Corporations Regulations 2001 and other mandatory professional reporting requirements; and (ii) giving a true and fair view of the Fund’s financial position as at 30 June 2015 and of its performance for the financial year ended on that date; and

(b) there are reasonable grounds to believe that the Fund will be able to pay its debts as and when they become due and payable.

The summary of significant accounting policies confirms that the financial statements also comply with International Financial Reporting Standards as issued by the International Accounting Standards Board.

This declaration is made in accordance with a resolution of the directors.

James P Graham AM Director Sydney, 28 July 2015

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 23

INDEPENDENTAUDITOR’S REPORT

INDEPENDENT AUDITOR’S REPORT TO THE UNITHOLDERS OF GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND

REPORT ON THE FINANCIAL REPORT

We have audited the accompanying financial report

of Gresham Private Equity Co-Investment Fund (the

Fund), which comprises the balance sheet as at 30

June 2015, the statement of comprehensive income,

statement of changes in equity and statement of cash

flows for the year ended on that date, a summary of

significant accounting policies, other explanatory

notes and the directors’ declaration.

DIRECTORS’ RESPONSIBILITY FOR THE FINANCIAL

REPORT

The directors of Gresham Funds Management

Limited (the responsible entity) are responsible for

the preparation of the financial report that gives a

true and fair view in accordance with Australian

Accounting Standards and for such internal control

as the directors determine is necessary to enable the

preparation of the financial report that is free from

material misstatement, whether due to fraud or error.

In Note 1, the directors also state, in accordance with

Accounting Standard AASB 101 Presentation of

Financial Statements, that the financial statements

comply with International Financial Reporting

Standards.

AUDITOR’S RESPONSIBILITY

Our responsibility is to express an opinion on the

financial report based on our audit. We conducted

our audit in accordance with Australian Auditing

Standards. Those standards require that we comply

with relevant ethical requirements relating to audit

engagements and plan and perform the audit to

obtain reasonable assurance whether the financial

report is free from material misstatement.

An audit involves performing procedures to obtain

audit evidence about the amounts and disclosures

in the financial report. The procedures selected

depend on the auditor’s judgement, including the

assessment of the risks of material misstatement of

the financial report, whether due to fraud or error. In

making those risk assessments, the auditor considers

internal control relevant to the entity’s preparation

and fair presentation of the financial report in order

to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing

an opinion on the effectiveness of the entity’s

internal control. An audit also includes evaluating

the appropriateness of accounting policies used and

the reasonableness of accounting estimates made

by the directors, as well as evaluating the overall

presentation of the financial report.

We believe that the audit evidence we have obtained

is sufficient and appropriate to provide a basis for our

audit opinion.

AUDITOR’S OPINION

In our opinion:

(a) the financial report of Gresham Private Equity Co-

Investment Fund:

(i) gives a true and fair view of the Fund’s

financial position as at 30 June 2015 and

of its performance for the year ended on

that date; and

(ii) complies with Australian Accounting

Standards (including the Australian

Accounting Interpretations).

(b) the Fund’s financial report also complies with

International Financial Reporting Standards as

disclosed in Note 1.

PricewaterhouseCoopers

C J Heath, Partner

Sydney, 28 July 2015

PricewaterhouseCoopers, ABN 52 780 433 757 Darling Park Tower 2, 201 Sussex Street, GPO BOX 2650, SYDNEY NSW 1171 DX 77 Sydney, Australia T +61 2 8266 0000, F +61 2 8266 9999, www.pwc.com.au Liability limited by a scheme approved under Professional Standards Legislation

GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND 24

DIRECTORY

RESPONSIBLE ENTITY GRESHAM FUNDS MANAGEMENT LIMITED ABN 32 109 020 153 AFSL 276368

Registered Office: Level 17, 167 Macquarie Street Sydney NSW 2000 Australia Telephone: 61 2 9221 5133 Facsimile: 61 2 9223 9072

MANAGER GRESHAM PRIVATE EQUITY LIMITED ABN 86 084 509 946 AFSL 247102

Registered Office: Level 17, 167 Macquarie Street Sydney NSW 2000 Australia Telephone: 61 2 9221 5133 Facsimile: 61 2 9223 9072

DIRECTORS OF RESPONSIBLE ENTITY James P Graham AM (Chairman) Roger S Casey (Deputy Chairman) Terence J Bowen Antony G Breuer Timothy J Bult Charles J M Graham

REGISTRY COMPUTERSHARE INVESTOR SERVICES PTY LTD Level 3, 60 Carrington Street Sydney NSW 2000 Australia Within Australia: 1300 855 080 Outside Australia: 61 3 9415 4000 Facsimile: 61 2 8235 8150

SPONSORING BROKERS JBWERE Level 42, Governor Phillip Tower 1 Farrer Place Sydney NSW 2000 Australia

MORGANS Level 29, Riverside Centre 123 Eagle Street Brisbane QLD 4000 Australia

MACQUARIE EQUITIES

1 Martin Place Sydney NSW 2000 Australia

ORD MINNETT Level 8, NAB House 255 George Street Sydney NSW 2000 Australia

SOLICITORS HERBERT SMITH FREEHILLS ANZ Tower 161 Castlereagh Street Sydney NSW 2000 Australia

TAX ADVISOR PRICEWATERHOUSECOOPERS Darling Park Tower 2 201 Sussex Street Sydney NSW 2000 Australia

AUDITOR PRICEWATERHOUSECOOPERS Darling Park Tower 2 201 Sussex Street Sydney NSW 2000 Australia

CUSTODIAN PERPETUAL CORPORATE TRUST LIMITEDLevel 12, 123 Pitt Street Sydney NSW 2000 Australia

RESPONSIBLE ENTITYGRESHAM FUNDS

MANAGEMENT LIMTEDABN 32 109 020 153

AFSL 276368