Cross-section of expected returns typically analyzed gross of transactions costs

Questions regarding market efficiency should be net of transactions costs

• Are profits within trading costs?

Research Questions:

• How large are trading costs faced by large arbitrageurs?

• How robust are anomalies in the literature after realistic trading costs?

• At what size do trading costs start to constrain arbitrage capital?

• What happens if we take transactions costs into account ex ante?

– Tradeoff between expected returns and trading costs varies across anomalies

Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz 2

Objectives

Measure trading costs of an “arbitrageur”

Understand the cross-section of net returns on anomalies

Model of trading costs for descriptive and prescriptive purposes

Constructing optimized portfolios

Conclusion

3Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

What We Do

Take all (longer-term) equity orders and executions from AQR Capital• 1998 to 2013, $1.1 trillion worth of trades, traded using automated algorithms

• U.S. (NYSE and NASDAQ) and 18 international markets—

• *Exclude “high frequency” (intra-day) trades

Use actual trade sizes and prices to calculate • Price impact and implementation shortfall (e.g., Perold (1988))

More accurate picture of real-world transactions costs and tradeoffs• Get vastly different measures than the literature

• Actual costs are 1/10 the size of those estimated in the literature

• Why? 1) Average trading cost ≠ cost facing an arbitrageur 2) Design portfolios that endogenously respond to expected trading costs

4Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Measuring Trading Costs

Literature has used a variety of models and types of data to approximate trading costs:

• Daily spread and volume data[Roll (1984), Huang and Stoll (1996), Chordia, Roll, and Subrahmanyam (2000), Amihud (2002), Acharya and Pedersen (2005), Pastor and Stambaugh (2003), Watanabe and Watanabe (2006), Fujimoto (2003), Korajczyk and Sadka (2008), Hasbrouck (2009), and Bekaert, Harvey, and Lundblad (2007)]

• Transaction-level data (TAQ, Rule 605, broker)[Hasbrouck (1991a, 1991b), Huberman and Stanzl (2000), Breen, Hodrick, and Korajczyk (2002), Loeb (1983), Keim and Madhavan (1996), Knez and Ready (1996), Goyenko (2006), Sadka (2006), Holden (2009), Goyenko, Holden, and Trzcinka (2009), Lesmond, Ogden, and Trzcinka (1999), Lesmond (2005), Lehmann (2003), Werner (2003), Hasbrouck (2009), and Goyenko, Holden, and Trzcinka (2009)]

• Proprietary broker data [Keim (1995), Keim and Madhavan (1997), Engle, Ferstenberg, and Russell (2008)]

Several papers have applied trading cost models to anomalies, chiefly size, value, and momentum. Most find costs are significantly binding.

• Chen, Stanzl, and Watanabe (2002)

• Korajczyk and Sadka (2004)

• Lesmond, Schill, and Zhou (2003)

5Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Trading Execution Database

Trade execution database from AQR Capital Management• Institutional investor, around 118 billion USD in assets (October 2014)

• Data compiled by the execution desk and covers all trades executed algorithmically in any of the firm’s funds since inception (*excluding stat arb trades)

Information on orders, execution prices and quantities• Common stocks only: restrict to cash equity and equity swaps

• 19 Developed markets (drop emerging markets trades)

• Drop liqudity/statistical arbitrage trades

• Result: ~9,300 global stocks , 1.1 trillion USD worth of trades

Price, return and volume data• Union of the CRSP tapes and the XpressFeed Global database

6Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Trade Execution Database

This picture shows our trade execution database.• Last year’s data, the rest is in some nuclear-disaster-proof bunkers around the world

• Frazzini almost froze to death to take this photograph

7Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

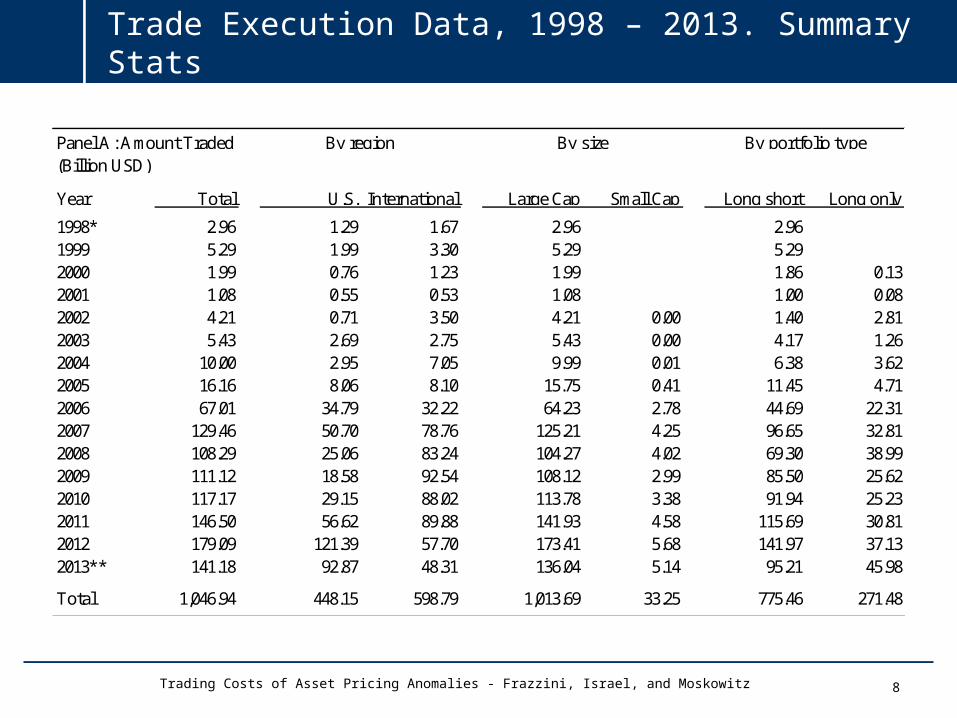

Trade Execution Data, 1998 – 2013. Summary Stats

8Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

(Billion USD)

Year Total U.S. International Large Cap Small Cap Long short Long only

Total 1,046.94 448.15 598.79 1,013.69 33.25 775.46 271.48

By region By size By portfolio typePanel A: Amount Traded

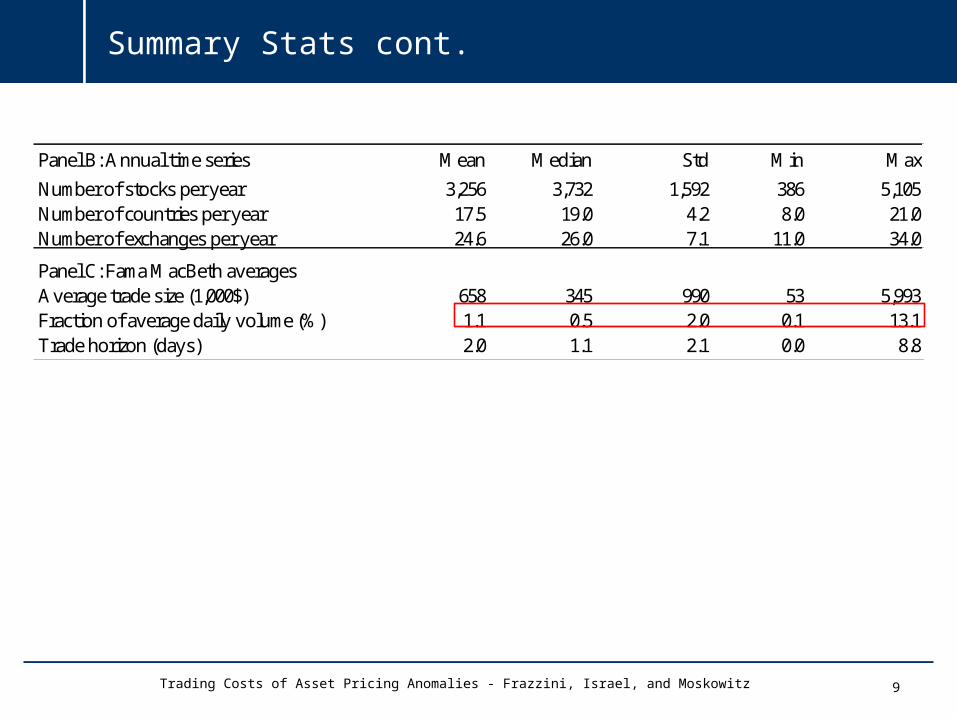

Summary Stats cont.

9Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Panel B: Annual time series Mean Median Std Min Max

Number of stocks per year 3,256 3,732 1,592 386 5,105Number of countries per year 17.5 19.0 4.2 8.0 21.0Number of exchanges per year 24.6 26.0 7.1 11.0 34.0

Panel C: Fama MacBeth averagesAverage trade size (1,000$) 658 345 990 53 5,993Fraction of average daily volume (%) 1.1 0.5 2.0 0.1 13.1Trade horizon (days) 2.0 1.1 2.1 0.0 8.8

Summary Stats cont.

10Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Trading Execution Algorithm

*The portfolio generation process is separate from the trading process - algorithms do not make any explicit aggregate buy or sell decisions• Merely determine duration of a trade (most within 1 day)

The trades are executed using proprietary, automated trading algorithms designed and built by the “manager” (aka Ronen)• Direct market access through electronic exchanges

• Provide rather than demand liquidity using a systematic approach that sets opportunistic, liquidity-providing limit orders

• Break up total orders into smaller orders and dynamically manage them

• Randomize size, time, orders, etc. to limit market impact

• Limit prices are set to buy stocks at bid or below and sell stocks at ask or above generally

We consider all of the above as part of the “trading cost” of a large arbitrageur

11Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

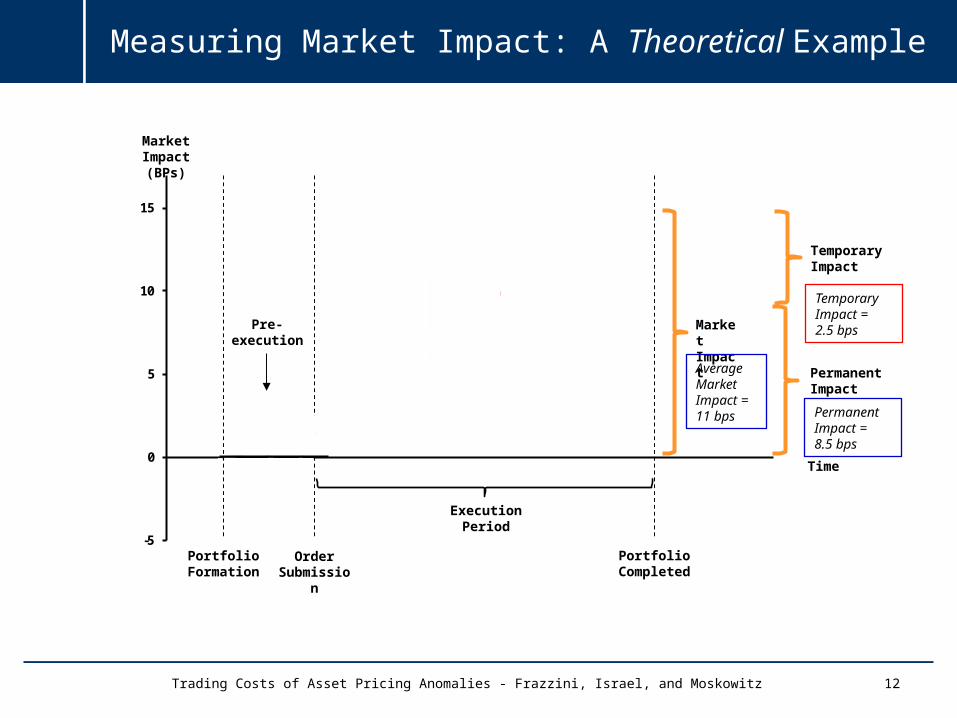

Click to edit Master title style-5

0

5

10

15

12

Market Impact(BPs)

Time

Portfolio Formation

Order Submission

PortfolioCompleted

ExecutionPeriod

Pre-execution

ExecutionPrices

Market Impact

PermanentImpact

TemporaryImpact

Measuring Market Impact: A Theoretical Example

Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

AverageMarket Impact = 11 bps

TemporaryImpact = 2.5 bps

PermanentImpact = 8.5 bps

Full sample: 1998 - 2013

All sample

US US Large Cap Small Cap Long short

Long onlyNyse-Amex

Nasdaq

MI mean 2.68 # 2.22 3.57 # 1.96 7.28 # 2.64 2.83MI median 2.29 # 2.29 2.29 # 1.88 5.63 # 2.15 2.94MI vw mean 3.13 # 2.15 3.18 # 2.74 6.78 # 3.16 0.95

Trading costs relative to theoretical prices = efficacy of strategy

Trading costs relative to VWAP = costs vs. best price available

Interpretation

How generalizable are the results?

How exogenous are trading costs to the portfolios being traded by our manager?

Trading costs we estimate are fairly independent from the portfolios being traded.

1. Only examine live trades of longer-term strategies, where portfolio formation process is separate from the trading process executing it.

2. Set of intended trades is primarily created from specific client mandates that often adhere to a benchmark subject to a tracking error constraint of a few percent.

3. Manager uses proprietary trading algorithms, but algorithms cannot make any buy or sell decisions. Only determine duration of trade (1-3 days).

4. Exclude all high frequency trading.

We also examine only the first trade from new inflows.

14Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Long-only trades, 1998 - 2013 Trade type Only inflows

All other trades

Difference t -statistics

MI mean All trades 16.95 15.54 1.40 0.20MI median All trades 12.51 10.23 2.28 0.35MI vw mean All trades 19.30 17.22 2.08 0.31

MI mean Large cap 14.76 13.83 0.93 0.11MI median Large cap 9.88 9.13 0.75 0.09MI vw mean Large cap 11.59 16.71 -5.12 -0.66

MI mean Small cap 20.94 20.56 0.37 0.07MI median Small cap 17.08 14.59 2.48 0.54MI vw mean Small cap 26.29 24.47 1.82 0.25

Exogenous Trades—Initial Trades from Inflows

15Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

0.0

5.0

10.0

15.0

20.0

25.0

All trades Large cap Small cap

Ave

rage

mar

ket

impa

ct (b

asis

poi

nts)

Inflows (long-only) All other long-only trades

Regression Results: Tcost Model

This table shows results from pooled regressions. The left-hand side is a trade’s Market Impact (MI), in basis points. The explanatory variables include the contemporaneous market returns, firm size, volatility and trade size (all measured at order submission).

16Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

*

*

• Use regression coefficients to compute predicted trading costs for all stocks1. Fix trade size (as a % of DTV) equal to the median size in our execution data2. Later, when running optimizations we’ll allow for variable (endogenous) trade size

Country Fixed Effects Yes Yes Yes Yes No No No No Yes Yes Yes Yes

All sample United States International

Market Impact by Fraction of Trading Volume, 1998 – 2011

This figure shows average Market Impact (MI). We sort all trades in our datasets into 30 bins based on their fraction of daily volume and compute average and median market impact for each bucket.

17Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Panel B: International trade execution sample, 1998 - 2013Panel A: U.S. trade execution sample, 1998 - 2013

Returns Results – Trade Execution Sample – U.S.

Actual dollar traded in each portfolio (past 6 month) to estimate trading costs at each rebalance

Trading costs and implied fund size are based on actual traded sizes

18Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Optimized Portfolios

So far, have ignored trading costs when building portfolios

How can portfolios take into account trading costs to reduce total costs substantially?• Can we change the portfolios to reduce trading costs without altering them significantly?

• Tradeoff between trading costs (market impact) and opportunity cost (tracking error)

Construct portfolios that minimize trading costs while being close to the “benchmark” paper portfolios (SMB, HML, UMD, …)

*Working on separating tracking error into style drift vs. idiosyncratic error (done)

19

min𝒘 𝑇𝑜𝑡𝑎𝑙 𝑇𝑟𝑎𝑑𝑖𝑛𝑔 𝐶𝑜𝑠𝑡 (𝒘)

Subject to:

Tracking Error Constraint: ඥሺ𝒘− 𝑩ሻ𝛀ሺ𝒘− 𝑩ሻ≤ 1%

$1 long and $1 short: 𝒘′𝒊 = 0 and ȁ�𝒘ȁ�′𝒊 = 2

Trading Constraint: Fraction of daily volume <=5%

Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Trading Cost vs. Tracking Error Frontier

20Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 50 75 100 125 150 200

Tot

al T

radi

ng

Cos

ts (

An

nu

al %

)

Ex-Ante Tracking (bps)

Total trading costs, U.S. tradable sample

SMB HML UMD Combo

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 50 75 100 125 150 200

Sh

arpe

Rat

io (

net

)

Ex-Ante Tracking (bps)

Sharpe Ratio (net), U.S. tradable sample

SMB HML UMD Combo

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0 50 75 100 125 150 200

Tot

al T

radi

ng

Cos

ts (

An

nu

al %

)

Ex-Ante Tracking (bps)

Total trading costs, International tradable sample

SMB HML UMD Combo

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0 50 75 100 125 150 200

Sh

arpe

Rat

io (

net

)

Ex-Ante Tracking (bps)

Sharpe Ratio (net), International tradable sample

SMB HML UMD Combo

Break-Even Sizes after Tcost Optimization

21Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

Conclusions

Unique dataset of live trades to approximate the real trading costs of a large institutional trader/arbitrageur

Our trading cost estimates are many times smaller (and break even capacities many times larger) than those previously claimed:

Size, Val, Mom all survive tcosts at high capacity, but STR does not

Fit a model from live traded data to compute expected trading costs based on observable firm and trade characteristics

• We plan to make the coefficients and the price impact breakpoints available to researchers to be used to evaluate trading costs

22Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

APPENDIX

23Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

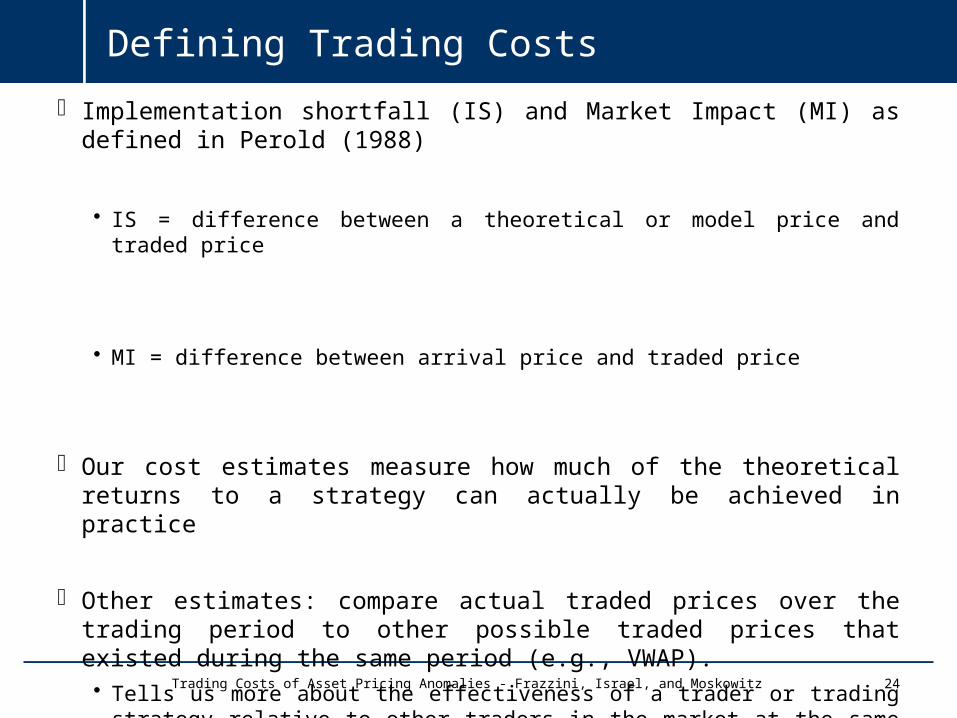

Defining Trading Costs

Implementation shortfall (IS) and Market Impact (MI) as defined in Perold (1988)

• IS = difference between a theoretical or model price and traded price

• MI = difference between arrival price and traded price

Our cost estimates measure how much of the theoretical returns to a strategy can actually be achieved in practice

Other estimates: compare actual traded prices over the trading period to other possible traded prices that existed during the same period (e.g., VWAP). • Tells us more about the effectiveness of a trader or trading strategy relative to other traders

in the market at the same time, not the efficacy of an investment strategy

24Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz

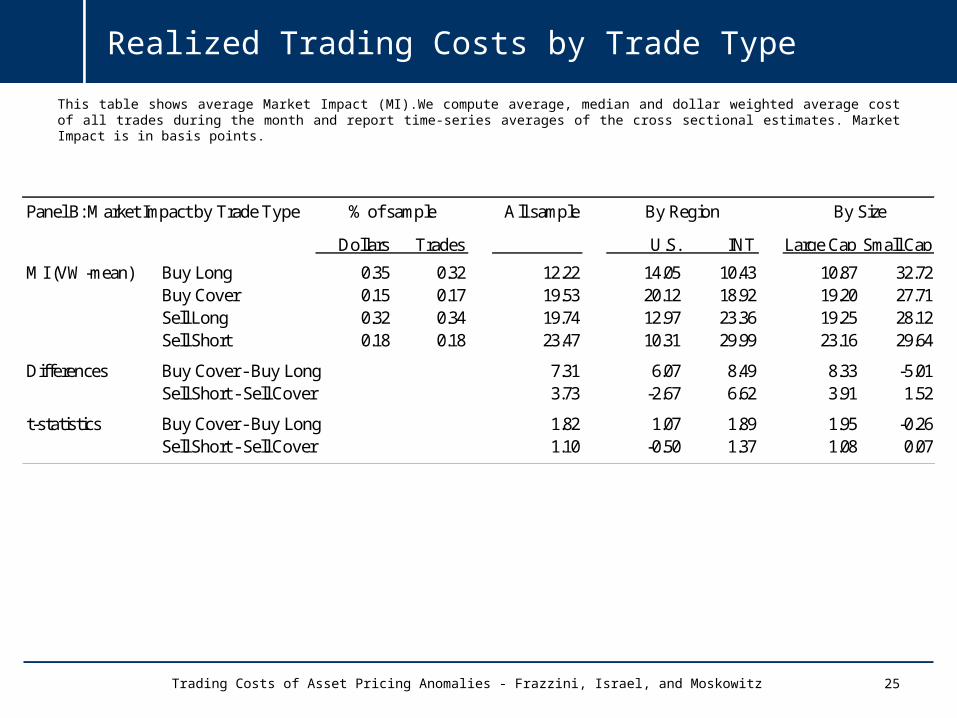

Realized Trading Costs by Trade Type

This table shows average Market Impact (MI).We compute average, median and dollar weighted average cost of all trades during the month and report time-series averages of the cross sectional estimates. Market Impact is in basis points.

25

All sample

Dollars Trades U.S. INT Large Cap Small Cap

MI (VW-mean) Buy Long 0.35 0.32 12.22 14.05 10.43 10.87 32.72Buy Cover 0.15 0.17 19.53 20.12 18.92 19.20 27.71Sell Long 0.32 0.34 19.74 12.97 23.36 19.25 28.12Sell Short 0.18 0.18 23.47 10.31 29.99 23.16 29.64

Differences Buy Cover - Buy Long 7.31 6.07 8.49 8.33 -5.01Sell Short - Sell Cover 3.73 -2.67 6.62 3.91 1.52

t-statistics Buy Cover - Buy Long 1.82 1.07 1.89 1.95 -0.26Sell Short - Sell Cover 1.10 -0.50 1.37 1.08 0.07

Panel B: Market Impact by Trade Type By Region By Size% of sample

Trading Costs of Asset Pricing Anomalies - Frazzini, Israel, and Moskowitz