42

1 ARM Holdings plc Q2 2013 Results ROADSHOW SLIDES v2

1

ARM Holdings plc

Q2 2013 Results

ROADSHOW SLIDES

v2

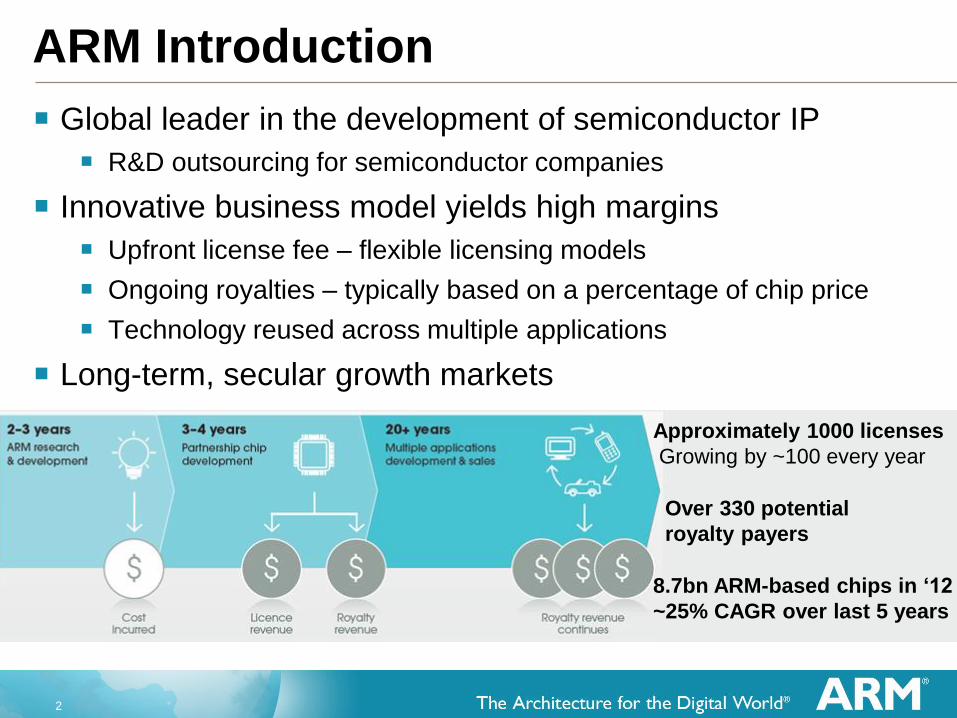

2

Approximately 1000 licenses

Growing by ~100 every year

Over 330 potential

royalty payers

8.7bn ARM-based chips in ‘12

~25% CAGR over last 5 years

ARM Introduction

Global leader in the development of semiconductor IP

R&D outsourcing for semiconductor companies

Innovative business model yields high margins

Upfront license fee – flexible licensing models

Ongoing royalties – typically based on a percentage of chip price

Technology reused across multiple applications

Long-term, secular growth markets

3

Key Growth Drivers

Increasing breadth

of ARM penetration

Growth in royalty

from smart products

Extending IP

Outsourcing

Growth into more markets

Increasing ARM penetration into broader

range of digital products

Growth in value per smart product

ARM’s processor content per chip increasing

More chips per product and higher priced chips

Growth into new technology outsourcing

Physical IP and graphics IP further increase

ARM’s value per chip

Growth

Opportunities

4

Licensing Drives Future Royalties

Licensing base grows by 25 in Q2 2013

ARM’s current royalty revenues are derived from licenses

signed many years ago

Growing base yields royalty revenues over long period

$0m

$50m

$100m

$150m

$200m

$250m

$300m

H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2009 to present

2004-2008

Pre 2004

Significant Royalty Potential

from Recent Licenses ~450

~1000

~450 most recent

licenses are

drivers of ARM’s

future royalty

Pre 2009 2010 2011 2012 YTD

2009 2013

Cu

mu

lati

ve

Lic

en

se

s

1000

500

0

~550

+87

+91

+122

+110

+47

~250 licenses

~300

5

Strong Growth in all Markets

Increasing penetration as semiconductor

companies deploy ARM technology into broad

range of end markets

Mobile devices is still our largest market with

embedded and enterprise the fastest growing

Licenses Royalty Units

2012 Licensing and Royalty

Mobile

Embedded

Enterprise

Home

4.6bn

2.3bn

1.4bn

0.4bn

25%

in 2012

3%

in 2012

10%

in 2012

40%

in 2012

6

Q2 2013 Revenues $m £m %revs

Licensing 102.6 60.6 39%

Royalty 135.3 91.1 51%

Other 15.1 18.6 10%

Total 264.3 171.2 100%

COGS 9.8

Gross Margin 94.3%

Operating Costs 78.2

Operating Margin 48.6%

Profit Before Tax 86.6

EPS 4.89

Cash Generation £95.0

Total Cash £613.1

From Revenue to Profits and Cash

95% of revenues earned in

US dollars

Cash generative, debt free

Royalty growth has driven higher

operating margins and earnings

Royalties more than 50% of

revenues

R&D expensed as incurred

Approximately 50% of costs in USD

10% move in $/£ impacts EPS

by ~15%

Note: Normalised numbers

7

Long-Term Growth Opportunity

ARM’s opportunity to increase revenue and profitability

2003-2012 Route from 2013 to 2020

PD Licensing CAGR 15% High single digits

PD Royalty CAGR* 22% ARM to outperform industry by 15-20%

Revenue CAGR 18%

Operating Margin 20% to 47% Operating leverage continues**

Earnings Per Share

CAGR

26% Revenue growth, margin expansion and

decreasing tax rate driving EPS growth***

* 7% semiconductor revenue CAGR 2003 to 2012. SIA data excluding memory and analog, January 2013

** Assuming Q4 2012 exchange rate of 1.58 and a <1% share dilution

8

Mo

bile

Markets for ARM in 2012

* Including tablets, netbooks and laptops * * Includes other applications not listed such as headsets, DVD, game consoles, etc

Devices Shipped

(Million of Units)

2012

Devices

Chips/

Device

TAM 2012

Chips

2012

ARM

2012

Share

Smart Phone 730 3-5 2,500 2,200 90%

Feature Phone 460 2-3 1,200 1,100 95%

Low End Voice 730 1-2 730 700 95%

Portable Media Players 130 1-3 250 220 90%

Mobile Computing* (apps only) 400 1 400 160 40%

Digital Camera 150 1-2 230 180 80%

Digital TV & Set-top-box 420 1-2 640 290 45%

Desktop PCs & Servers (apps) 200 1 200 - 0%

Networking 1,200 1-2 1,300 420 35%

Printers 120 1 120 85 70%

Hard Disk & Solid State Drives 700 1 700 620 90%

Automotive 2,600 1 2,600 210 8%

Smart Card 6,000 1 6,000 710 13%

Microcontrollers 8,700 1 8,700 1,500 18%

Others ** 2,000 1 2,000 300 15%

Total 25,500 27,000 8,700 32%

Ho

me

En

terp

ris

e

Em

bed

ded

Source:

Gartner, IDC, SIA, and

ARM estimates

Year Market

Share

2007 17%

2008 20%

2009 22%

2010 25%

2011 29%

2012 32%

9

Mo

bile

Markets for ARM in 2017

* Including tablets, netbooks and laptops * * Includes other applications not listed such as headsets, DVD, game consoles, etc

Devices Shipped

(Million of Units)

2017

Devices

Device

CAGR

Chips/

Device

2017

Chips

Chip

CAGR

Smart Phone 1,800 20% 3-5 6,800 20%

Feature Phone - - - - -

Low End Voice 710 -1% 1-2 1,400 15%

Portable Media Players 90 -10% 1-3 180 -5%

Mobile Computing* (apps only) 850 20% 1 850 20%

Digital Camera 130 -5% 1-2 200 -5%

Digital TV & Set-top-box 600 10% 1-4 2,000 25%

Desktop PCs & Servers (apps) 200 Flat 1 200 Flat

Networking 1,500 5% 1-2 1,700 5%

Printers 130 2% 1-3 130 2%

Hard Disk & Solid State Drives 1,100 10% 1 1,100 10%

Automotive 3,800 10% 1 3,800 10%

Smart Card 8,500 10% 1 8,500 10%

Microcontrollers 11,400 5% 1 11,400 5%

Others ** 3,000 10% 1-2 3,000 10%

Total 34,000 5% 41,000 10%

Ho

me

En

terp

ris

e

Em

bed

ded

Key Growth Areas for ARM

Source:

Gartner, IDC, SIA, and

ARM estimates

10

Average Selling Price of a Semiconductor Chip

ARM’s Opportunity at all Price Points

Opportunity

ARM Usage Today

>$25 $10-15 $3-6 $1-2

Vo

lum

e

11

Cortex

Mass market tablets, smartphones and

digital TVs

ARM’s Opportunity in Apps Processors

Devices Vol. (m) ARM (%) Chip ASP

Smartphones 730 >95% $5 to $20

Mobile Computing 400 40% $5 to $20

DTVs & STB 420 45% $5 to $10

Other 280 65% $5 to $20

Total 1,800 70%

2012 2017

Devices Vol. (m)

Smartphones 1,700

Mobile Computing 850

DTVs & STB 600

Other 850

Total 4,000

ARM Technology Penetration in Devices

Smartphones

ARM11Cortex-A >95%

Mali 15%

Physical IP 40%

Mobile Computing

Cortex-A 40%

Mali 10%

Physical IP 30%

DTVs & STB

ARM9Cortex-A 45%

Mali <10%

Physical IP <25%

ARM Technology

big.LITTLE

Mid-range and high end smartphones and tablets

64bit

Super smartphones and mobile

computers

Mali

Mali T6XX for super smartphones and tablets

Mali 4XX for smartphones, tablets and DTVs

Physical IP

POP IP available for all Cortex-A processors and

MaliT6xx

(laptops and tablets)

12

New Opportunities Driving Licensing

Cortex-A

Family

Cortex-R

Family

Cortex-M

Family

Mali

Graphics

179 (+9)

143 (+5)

37 (+3)

80 (+7)

Classic Processors: 532, Architecture: 15, Subscription: 11 (+1) *Note: Licensing numbers adjusted for licenses that are no longer expected to generate royalties.

Cumulative licenses (Q1 2013 licensing shown in parentheses*)

Estimated Royalty

Opportunity

for 2017

Real-time

Embedded

14bn units

per year

Micro-

controllers

23bn units

per year

Application

Processors

4bn units

per year Mobile computing, digital TVs Servers, networking and embedded computers

Networking equipment Mobile broadband (basestation and modem)

Internet of Things: personal GPS, medical Microcontrollers, automotive, storage

13

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 H12013

ARM Royalty Revenue

ARM Royalty Revenue (Q1-Q2)

Q2 royalty revenues nearly $119m

Up 24% YoY, industry up 2%

Helped by near trebling of Cortex-A and

5x increase in Mali shipments

2.4 billion units in Q2

Up 20% YoY, industry down 2%

Mobile: up 12% YoY, industry flat

Storage: up 5% YoY, industry down 7%

DTV: up 90% YoY, industry up 5%

MCU: up 20% YoY, industry down 5%

Processor Royalties

Non-mobile 48%

Q2 2013: ARM Outperforms Industry

Gro

wth

Rate

(%)

AR

M R

oyalt

y R

even

ue (

$M

)

Q2 2013 royalty revenue up 24% YoY

Industry up 2% over the relevant period

ARM $ Royalty CAGR (08-12) = 17% Industry $ Revenue CAGR (08-12) = 1%

Source: SIA May 2013, excludes memory and analog * Industry data offset one quarter to align with ARM’s royalty revenue

Q2 Market Analysis

Mobile, 51%

Embedded, 26%

Enterprise, 18%

Home, 5%

14

Licensing Increases Market Opportunity

Application Penetration of Key

Companies’ Products

2012

Share

Smartphone – Apps >95%

Mobile Computer – Apps* 40%

Mobile – Modems >95%

Mobile – BT & WiFi** 75%

Digital Camera*** 80%

Digital TV / Set-Top-Box 45%

Networking 25%

Printers*** 70%

Disk Drives (HDD & SSD) 90%

Automotive 8%

Smart Card 15%

Microcontrollers 18%

3D Graphics**** 13%

Public ARM design wins, but not yet shipping

Shipping mainly ARM-based chips

Shipping some ARM-based chips

No ARM design win or not yet public

* Includes handheld computers, tablets, and laptops

** Includes standalone WiFi and BT chips and BT-WiFI combo chips

***Based on OEM market share rather than semiconductor vendor

****Includes all smartphones, mobile computing and DTV devices, including those that don’t currently contain a GPU

ARM gains share by winning designs at leading semiconductor companies

Based on current market shares

and ARM’s view of how these

markets may develop.

ARM will update the chart on the left

only as design wins become public

Movement in H1 2013

4 companies reequipped

Movement from 2011 to 2012

1 company

1 company

1 company

5 companies

4 companies

15

Servers

AR

Mv

7 M

PC

ore

Relative TCO

Incu

mb

en

t

ARM Partner Chip Price: <$100

ARM technology suitable for

scale-out server workloads and energy constrained environments

Integration of hardware blocks

into SoCs reduces power and costs

Entry-level Smartphones & Tablets

Co

rtex-A

7

Relative

Performance

Co

rtex-A

7

Clo

vert

rail

+

Relative Power C

lov

ert

rail+

Relative Size

Clo

vert

rail

+

Co

rtex-A

7

ARM Partner Chip Price: ~$5

Mid-range Smartphones & Tablets

Co

rtex-A

9

Relative

Performance

Co

rtex-A

9

Clo

vert

rail

+

Relative Power

Clo

vert

rail

+

Relative Size

Co

rtex-A

9

Clo

vert

rail

+

ARM Partner Chip Price: ~$10

Low Power Leadership

Premium Smartphones & Tablets

AR

Mv

7 b

ig.L

ITT

LE

Relative

Performance

big

.LIT

TL

E

Clo

vert

rail+

Relative Power

Clo

vert

rail

+

Relative Size

Clo

vert

rail+

ARM Partner Chip Price: ~$15

big

.LIT

TL

E

Source: see appendix for details

16

2017 Royalty Opportunity in Mobile $

= U

nit o

f R

oya

lty R

eve

nu

e

Baseband - $

1 x $

Voice Only

Phones

Apps Processor .

& baseband - $

Connectivity - $

2 x $

Feature

Phones

Apps Processor .

& baseband - 8x$

Connectivity - $

Peripherals - $

10 x $

Mid-Range

Smartphone

4 x $

Entry-Level

Smartphones

Apps Processor .

& baseband - 3x$

Connectivity - $

Applications - 15$

3G/LTE BB - 3x$

Connectivity –$

Peripherals - $

20 x $

Premium

Smartphone

1.8 billion handset opportunity for Cortex-A processors and Mali graphics

550m devices in 2017

400m devices in 2017

850m devices in 2017

710m devices in 2017

0m devices in 2017

Assumptions in Smartphones

100% penetration of Cortex-A processors

100% penetration of big.LITTLE in mid-range and premium

30% to 50% penetration of Mali graphics

17

2017 Smartphone

Chip ASPs

2017 Royalty Opportunity in Mobile S

ourc

e: G

art

ner

and

AR

M

$15-$20

<$5

$5-$15

Sm

art

ph

on

e S

hip

me

nts

(m

, u

nit

s)

2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

2012 2017

ARMv8 big.LITTLE

Multi-core Cortex-A

Mali (GPU Compute)

Physical IP

20x$

10x$

4x$

2017 Smartphone

Technology 2017 ARM Royalty

per Device

(typical range)

big.LITTLE

Multi-core Cortex-A

Mali (GPU Compute)

Physical IP

Multi-core Cortex-A

Mali (3D-graphics)

Physical IP

$5-$10

$2-$3

$1-$2

Overall Smartphone

Device CAGR: 20% Overall Smartphone

Silicon Value CAGR: >10%

Overall Smartphone ARM

Royalty CAGR: 15-25%

Where 1x$ is a unit of

royalty equal to the royalty

that ARM receives from a

voice only phone

Premium smartphones Mid-range smartphones Entry-level smartphones

18

Billions of Internet-Connected Screens

With choice of suppliers, OEMs are

innovating with new types of products

ARM technology can be used for applications

processing, connectivity and storage

Standard software is available

today and enables all form factors to

connect to the internet and display all the web

pages, play videos, network with friends ...

ABI Research, IDC, Gartner and ARM forecasts

Form Factor TAM(m)

2017

Mobile Phones 1,700

Media players 90

Mobile Computers 850

Desktop PCs 150 Digital TV/STB 600

Automotive Infotainment 110

Other* 900

Total 4 billion

*Includes PND, photo-frames, etc

19

Toys

Billions of Microcontrollers

Microcontrollers make the world smarter

Motor control, smart metering, security, air

bags, toys, heating and air-conditioning

Government low-energy policy and

green initiatives

Innovation driving system cost of 32-bit

ARM microcontrollers toward levels of

traditional 8-bit solutions

End-Market TAM(m)

2017 Automotive 3,800

Smartcards 8,500 Microcontrollers 11,500

Total 23 billion

ABI Research, IDC, Gartner and ARM forecasts

Equipment Adopting

32-bit ARM Microcontrollers

Environmental

Control

Smartcards

Medical

Devices

Secure

Payment

Consumer

Goods

Smartmeter

In Vehicle Infotainment

Gadgets

20

Billions of Real-Time Devices

Consumer products becoming

increasingly connected

Mobile baseband, WiFi, Bluetooth & GPS

Local storage increasing for when we

are not connected

ARM provides efficient, reliable

processors for real-time communication

and control

Device TAM(m)

2017 Mobile baseband 3,500

Other mobile connectivity

2,000

Home & Computing 1,500

Networking & Printers 1,600 Industrial 2,000

Disk drives 1,100 Other* 2,000

Total 14 billion

*Includes medical, media players, etc

ABI Research, IDC, Gartner and ARM forecasts

21

Software Ecosystem

RedHat Fedora 19 demonstrated on ARM

64-bit

Oracle optimising Java for ARM on 64-bit

Linaro Enterprise Group continues to grow

ARM in Servers

Source: Gartner and ARM estimates

ARM-based Low Power Servers

Highly Integrated Server Chips

Calxeda

15x power/

performance

improvement

Calxeda

EnergyCore

5.3W

102W

Current

Incumbent

Source: Calxeda, 19 June 2012, Ubuntu Server v12.04;

Apache Server v2.4.2, ApacheBench v2.3 (16k request size)

2017 Server

Opportunity

Chip Tam (m) 50

Chip Value ($bn) 3.5

Target ARM

Penetration 10-15%

Multi-core ARM processors: Cortex-A and

ARMv8

Integrated server fabric and high speed

interfaces. Includes: PCIe, 10 GbE, SATA, USB

Recent Design Wins

15 licenses now signed for server

applications

ARM-based 32-bit and 64-bit servers now

shipping

Multiple design wins expected in 2013

22

ARM in Enterprise Networking

Source: Gartner and ARM estimates

3G/4G

Macro

Enterprise

Small Cell

Metro Cell

Home

Small Cell

Enterprise Small

Cell

WiFi

Distributed

Antenna

WiFi Hotspots

Technology Requires high performance, but constrained

power budget

Higher royalties as Cortex-A and ARMv8 and

more expensive chips

Connectivity Driving Infrastructure

50bn installed internet devices

by 2020

2x increase in mobile computers

& smartphones by 2017

18x

Data traffic

increase on

mobile

networks

2012-17

110% LTE Capex CAGR

2010-14

60-80% Energy consumption

attributed to base stations

Base Station Equipment

Enterprise Access

Points L2/L3 Switching

Routers

Enterprise Networking Opportunity

2017 Enterprise

Networking

Opportunity

Chip

TAM (m)

Chip

Value

($bn)

Target

Penetrat

-ion

Base station equipment 65 $3.5 60%

Carrier Infrastructure 75 $3.0 <5%

Enterprise Access Points 270 $2.0 50%

L2/L3 Switching 150 $3.0 20%

Routing 80 $2.5 20%

Other 100 $2.5 20%

Total 700 $16.5

23

ARM in Embedded

Source: Gartner and ARM estimates

A Smarter More Connected World

ARM 32-bit Growing Quickly

12bn Install base of

Internet embedded

devices by 2020

Connected Medical

Personal devices Connected Cities

Connected Home

0

2

4

6

8

10

12

14

16

2006 2007 2008 2009 2010 2011 2012

Indexed MCU Growth by Bit Width (2006=1)*

ARM 32-bit 4, 8 &16-bit Non-ARM 32-bit

Smarter Processors for a Smarter

World

65%ARM’s share of

the 32-bit MCU

market in 2012*

18% ARM’s share of

the total MCU

market in 2012*

200

100

150

50

Cu

mu

lati

ve L

icen

sin

g

Cortex-M Licensing and

Shipments

Cumulative Licenses

Co

rtex-M

Sh

ipm

en

ts

2bn

1bn

1.5bn

0.5bn

Shipping Licenses

24

Innovating for Mobile and Computing

big: Cortex-A15

2x performance of current smartphones in

same low-power envelope

8x performance for mobile computing

LITTLE: Cortex-A7

1/5th the size and 5x energy-efficiency of

current smartphones

Multi-core capable – delivering higher

performance

big.LITTLE

High-performance and low power

Automatically selects the right processor for

the right job

Increases power efficiency

Available for both Cortex-A7 and Cortex-A15,

and Cortex-A53 and Cortex-A57

big

“Demanding tasks”

LITTLE

“Always on, always

connected tasks”50% of the Power

Current

smartphone

big.LITTLECurrent

smartphone

big.LITTLE

>2x Performance

Redefining the efficiency/

performance trade-off

Relative Performance

Co

rtex

-15

Co

rtex

-A7

big

.LIT

TL

E

Cu

rren

t

sm

art

ph

on

e

Co

rtex

-57

Co

rtex

-53

big

.LIT

TL

E

Relative Power

Co

rtex

-15

Co

rtex

-A7

big

.LIT

TL

E

Cu

rren

t

sm

art

ph

on

e

Co

rtex

-57

Co

rtex

-53

big

.LIT

TL

E Number of Partners Enabled with big.LITTLE

ARMv7 big,LITTLE

(Cortex-A7 and Cortex-A15)

ARMv8 big,LITTLE

(Cortex-A53 and Cortex-A57)

15 7

25

ARMv8 Processors

Cortex-A57: 3x performance of 2012 smartphone

64-bit support for enterprise applications

Scalable beyond 16 cores

Common OS across

multiple devices

Greater scalability

Increased addressability

Memory-intensive

applications

Hi-resolution media,

rich applications

Energy-efficient processors for high-

end networking and server applications

big.LITTLE configuration allows high

performance at low power

First Cortex-A50 series chips available

from 2014

Chips containing ARM’s Cortex-A50

series processors will command higher

royalty rates

Memory intensive applications driving

adoption of 64-bit in mobile devices

Cortex-A53: Equivalent performance of Cortex-A9 but

40% smaller and 4x more efficient

64-bit support

26

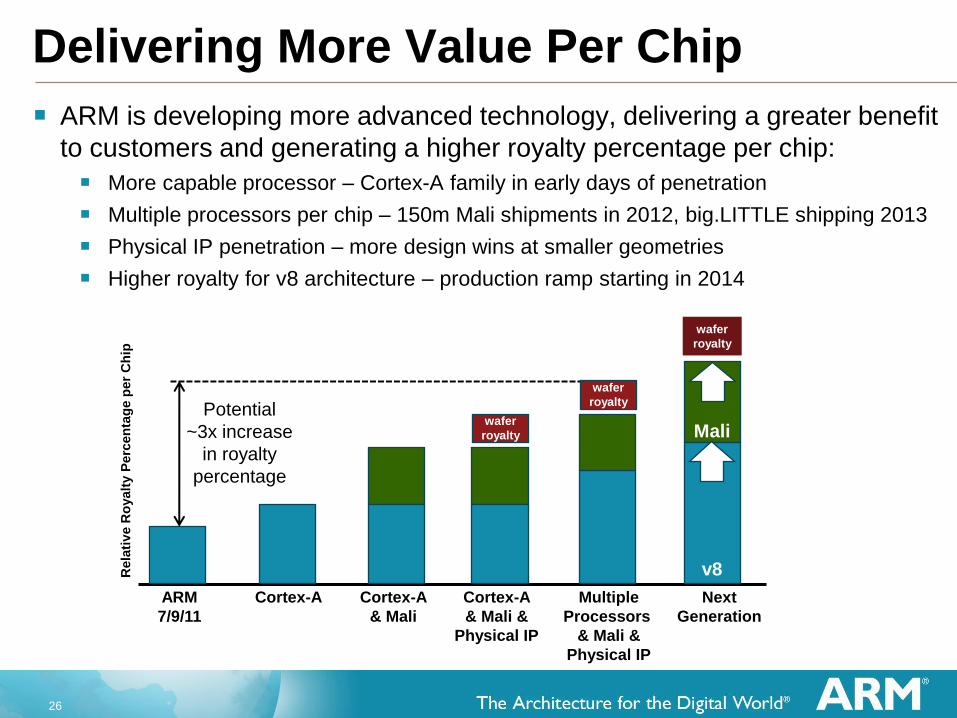

Delivering More Value Per Chip

ARM is developing more advanced technology, delivering a greater benefit

to customers and generating a higher royalty percentage per chip:

More capable processor – Cortex-A family in early days of penetration

Multiple processors per chip – 150m Mali shipments in 2012, big.LITTLE shipping 2013

Physical IP penetration – more design wins at smaller geometries

Higher royalty for v8 architecture – production ramp starting in 2014

Rela

tiv

e R

oyalt

y P

erc

en

tag

e p

er

Ch

ip

Cortex-A ARM

7/9/11

Potential

~3x increase

in royalty

percentage

Multiple

Processors

& Mali &

Physical IP

wafer

royalty

wafer

royalty

Next

Generation

Mali

v8

Cortex-A

& Mali

Cortex-A

& Mali &

Physical IP

wafer

royalty

27

Impact of Functional Integration

Integration of multiple functions into a single chip has limited overall

impact on ARM total royalty revenue

Chips containing multiple ARM processors yield higher royalties

Function X

$5

$2.50

Function Y

$6

Combination

Function X & Y

Integrated chip reduces cost for OEM and

increases profitability for the

semiconductor manufacturer

ARM royalty rate at

2% per chip ARM royalty rate at

2% for 1st processor

1% for 2nd processor

For this high volume application example:

ARM gets full royalty for first processor per chip;

discounted royalty for subsequent processors

15c

royalty 18c

royalty ($5@2%)+ ($2.50@2%)

Average of 7.5c

royalty per chip

$6@(2% + 1%)

Average of 18c

royalty per chip

OEM, semi and ARM all benefit from integration

Chips with multiple ARM-based processors

expected to increase

28

Physical IP Benefits Processors

POP IP

Optimised physical IP for improved

processor/graphics implementation

5 more POPs in Q2

1/. TSMC 28HPM, Typical Silicon 85C,

Overdrive 2/. TSMC 28HPM, Slow Silicon, 0C,

Worst case Vdd

3/. TSMC 28HPM Mali T600 Series

POP-Optimised

Mali

Graphics3

30% Higher

Frequency

25% Lower

Area

20% Lower

Power

Platform Licenses

Physical IP enables the optimized

implementation of SoC designs

99 royalty-bearing platform licenses

signed to date

First end user license for FinFET

Physical IP

Shipments from 32nm and below now

make up nearly 35% of royalties

PIPD royalty increased +20% YoY in

Q2 2013

Cumulative POPs

*Gartner 4Q12, Relevant shipment period

offset one quarter to align with ARM

POP Optimised1 ARM Cortex-A15 MP Core

Dual Core

POP Optimised2 ARM Cortex-A7 MP Core

Dual Core

Reach Higher

Frequency

up to 2.0 GHz Smaller Area Lower Power

15% 20%

Reach Higher

Frequency

850MHz Smaller Area Lower Power

10% 20%

Foundry32/28nm

Bulk CMOS

20nm

Bulk CMOS

16/14nm

FinFET

N/A N/A

0

10

20

30

40

50

60

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013

29

150m

Growing Mali Penetration

Mali is the most widely licensed graphics processor

80 licenses; 56 partners

Growth in adoption of GPU Compute

14 licensees for Mali T600 range of graphics processors

High performance, low power GPU compute enables new software applications

E.g. computational photography, multi-perspective views and real-time photo editing

Mali share gains continue as

multiple Partners ramp to volume

2012 market penetration

>70% of DTVs

>50% Android tablets

15% of smartphones

Mali YTD shipments already ahead

of 2012

Mali Processor

Licenses

+14

+11

+19

2009 2010 2011 2012 2013 YTD

80

+10

+17

<50m

Mali Royalty

Shipments (m, units)

2011 2012 2013 YTD

30

Scalable Mali GPU solutions

Performance

Mali-T604 First Midgard architecture product

OpenGL ES 3.0 support

Scalable to 4 cores

Mali-T628 50% performance uplift

OpenGL ES 3.0 support

Scalable to 8 cores

Mali-T678 High end solution

Max compute capability

Optimized for tablets

Performance

Mali-400 MP First OpenGL ES 2.0 multicore GPU

Scalable from 1 to 4 cores

Low cost solution with Mali-300

Mali-300 OpenGL® ES 2.0 compliant

Mali-450 MP 2x Mali-400 performance

Scalable up to 8 cores

Leading OpenGL ES 2.0

performance

Graphics Only Graphics and GPU Compute

Mali-T622 Smallest Full Profile GPU Compute

Enables mid-range smartphone

50% more energy efficient than

Mali-T604

Scalable to 2 cores

Mali-T624 50% performance uplift

OpenGL ES 3.0 support

Scalable to 4 cores

31

Effective Tax Rate Decreasing

ARM’s effective normalised tax rate is expected to decrease

UK Corporation Tax rate reducing to 21% from April 2014 and to

20% from April 2015

Patent box introducing 10% tax rate from April 2013

ARM’s normalised tax rate in 2013 expected to be just under 20%

Patent box applies to qualifying profits

Phased introduction: 60% of the benefit applying to qualifying profits

from April 1 2013, increasing in 10% increments per annum

Covers patents granted by UK IPO and European Patent Office

Applies to existing as well as new IP, and to acquired IP

2008 2009 2010 2011 2012

Tax rate could decline 1-2% per year

from 2013*

2013 2014 2015 2016

28% 27% 25% 25%

2017

* Before potential reclassification of R&D tax credits

26%

<20%

32

ARM Holdings plc

Q2 2013 Results

33

Major semiconductor companies

continue to invest in ARM

technology

ARM continues to outperform the

semiconductor industry

Licensing and royalty growth

driving 24% YoY revenue growth

ARM continues to invest whilst

delivering profits and record cash

Q2 2013 Highlights

37% YoY normalised EPS growth

25 PD Licenses

7 Mali licenses

24% YoY royalty growth

$264m Q2 Revenues

£96m Record cash generation

34

Outlook

ARM entered H2 2013 with:

Healthy opportunity pipeline and record order backlog

New product introductions and growing new markets

Q3 Outlook

Licensing revenue expected to be $80m +/-

ARM’s royalty revenues for Q3 based on shipments in Q2 2013

Small sequential increase in semiconductor industry revenues in Q2 2013

Normalised Opex expected to be £79-81 million

FY 2013

Building on our strong performance in the first half, we expect overall Group dollar revenues for full year 2013 to be at least in line with market expectations

35

Q2 2013 – Revenue Summary ($)

Q2 2013

$m

Q2 2012

$m

PD

Licensing 88.3 67.0 32%

Royalties 119.3 96.3 24%

PD Total 207.6 163.3 27%

PIPD

Licensing 14.3 11.6 23%

Royalties* 16.0 13.7 17%

PIPD Total 30.3 25.3 20%

Development Systems 13.4 13.3 1%

Services 13.0 11.1 17%

Total Revenue 264.3 213.0 24%

* Includes catch-up royalties in Q2 2013 of $1.4m and $1.5m in Q2 2012

36

Q2 2013 – Revenue Summary (£)

Q2 2013

£m

Q2 2012

£m

PD

Licensing 56.9 42.6 34%

Royalties 77.7 61.5 26%

PD Total 134.6 104.1 29%

PIPD

Licensing 9.2 7.3 26%

Royalties* 10.4 8.6 21%

PIPD Total 19.6 15.9 23%

Development Systems 8.7 8.5 3%

Services 8.3 7.0 19%

Total Revenue 171.2 135.5 26%

* Includes catch-up royalties in Q2 2013 of £0.9m and £1.0m Q2 2012

37

Backlog Analysis – End Q2 2013

Backlog by Maturity Profile Backlog Composition

76%

11%

13%

Processors

Physical IP

Support, Maintenance & Other

26%

18%

56%

Q313/Q413 Q114/Q214 Q314+

38

Backlog Underpins Licensing Revenue

*Some architecture licenses are recognised in a similar way to

subscription licenses

Group order backlog at record levels

Opportunity pipeline healthy for 2013

Backlog underpins future licensing

revenue

Over 2 years quarterly revenue from

backlog has doubled

Revenue from backlog consists of

Quarterly contribution from subscription

and architecture licenses*

Processors that are in development and

that have reached milestones

Backlog underpins future licensing

revenue

0

1

2

3

4

5

6

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2007 2008 2009 2010 2011 2012 2013

Indexed License Revenue vs. Backlog (H1 2007=1)

License Revenue

Backlog

$0m

$50m

$100m

$150m

$200m

$250m

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2007 2008 2009 2010 2011 2012 2013

Licensing: Backlog versus Turns

Turns Business

BacklogBusiness

5x

1.75x

39

Converting Profit into Cash

0

20

40

60

80

100

120

Q211 Q311 Q411 Q112 Q212 Q312 Q412 Q113 Q213

EBITDA Cash from operations

No

rma

lis

ed

(£

Ms)

(£m) Q211 Q311 Q411 Q112 Q212 Q312 Q412 Q113 Q213 Total

Normalised

EBITDA 55 56 69 61 66 69 81 90 88 635

Normalised

Cash from

Operations*

47 56 57 71 60 94 83 82 104 654

% Cash

Conversion 86% 99% 83% 116% 91% 136% 102% 91% 117% 103%

* Net cash inflow from operating activities (per IFRS cash flow), adding back tax and cash outflows from normalised items

40

Summary Balance Sheet

IFRS 30 Jun 13 31 Dec 12

£MM £MM

Assets

Cash (net of accrued interest) 613.1 520.2

Accounts receivable (including AROC) 136.5 124.5

Other assets, inventory and investments 139.0 151.7

Available-for-sale financial assets - current 66.3 -

Prepayment (advance contribution to consortium) - 103.7

Property and equipment 35.0 36.1

Goodwill 555.6 519.4

Other intangibles 69.5 11.2

Total assets 1,615.0 1,466.8

Liabilities & shareholders’ equity

Deferred revenue 179.0 150.6

Other creditors 131.8 110.1

Shareholders’ equity 1,304.2 1,206.1

Total liabilities & shareholders’ equity 1,615.0 1,466.8

41

Cash Flow Summary

£MM Q2 13 H1 13

Operating activities 101.2 167.7

Interest received, net 2.8 7.2

Tax (0.2) (9.2)

Capital and other intangible expenditure (9.7) (29.2)

Investments and acquisitions (net of disposals) (4.2) (7.6)

Dividends payable (39.5) (39.5)

Share options 0.3 2.7

Other (forex) - 0.8

Cash flow 50.7 92.9

Opening cash (net of accrued interest) 562.4 520.2

Closing cash (net of accrued interest) 613.1 613.1

Profit before tax (normalised) 86.6 176.0

Interest income, depreciation and amortisation 1.6 2.7

Cash flows from items excluded from normalised profits (2.3) (17.9)

Movements in working capital 15.3 6.9

Operating activities 101.2 167.7

42

Contact Information

Contact Title Contact

Ian

Thornton

Head of Investor

Relations

+44 1223 400796

Jonathan

Lawton

Director, Investor

Relations

+44 1223 400533

Philip

Sparks

Investor Relations

Manager

+44 1223 400566