22

ASCOM MISSION-CRITICAL WIRELESS COMMUNICATION

ASCOM

MISSION-CRITICAL WIRELESS

COMMUNICATION

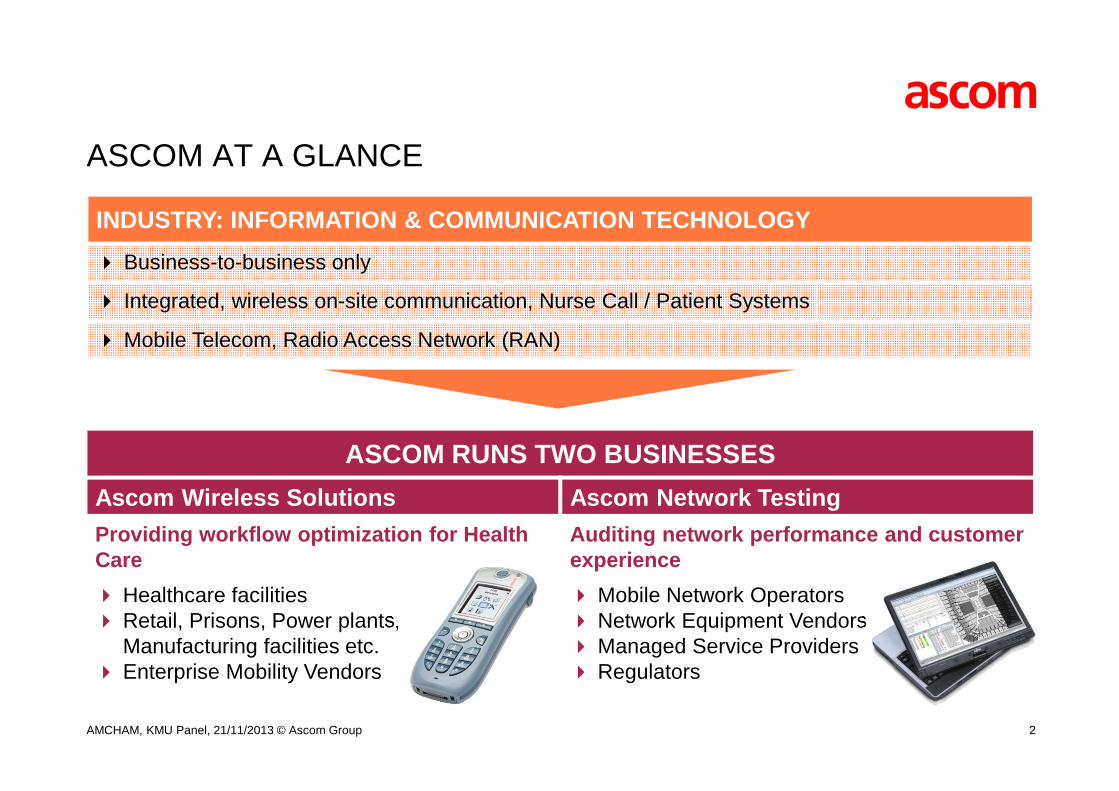

ASCOM AT A GLANCE

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

ASCOM RUNS TWO BUSINESSES

Ascom Wireless Solutions Ascom Network Testing

Providing workflow optimization for Health Care

Auditing network performance and customerexperience

� Healthcare facilities � Retail, Prisons, Power plants,

Manufacturing facilities etc.� Enterprise Mobility Vendors

� Mobile Network Operators� Network Equipment Vendors � Managed Service Providers� Regulators

INDUSTRY: INFORMATION & COMMUNICATION TECHNOLOGY

� Business-to-business only

� Integrated, wireless on-site communication, Nurse Call / Patient Systems

� Mobile Telecom, Radio Access Network (RAN)

2

Attractive value play after sucessful turnaround

ASCOM AT A GLANCE (FIGURES 2012)

RevenueCHF449.8m

Gross margin48.9%

EBITDACHF45.9m

Customer ROI at the core of our work

Clear strategic focus Total

AssetsCHF521.5mSolid balance sheet

Asset light strategy

Employee sFTE ~ 1600

International market leader

Global presence

in 17 Countries

R&D11% of Revenue

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 3

MARKET LEADER IN PATIENT SYSTEMS

MARKET LEADER IN CORDLESS ENTERPRISE TELEPHONY

MARKET LEADER IN ATTRACTIVE MARKET SEGMENTS

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 4

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

MARKET LEADER IN ATTRACTIVE MARKET SEGMENTS

TEST & MEASUREMENT

BENCHMARKING & MONITORING

REPORTING &ANALYSIS

Global market leader in drive-and walk-test tools for measuring mobile network performance

Industry‘s most versatile benchmarking software platform: handheld, automated, application services

Enterprise software for analyzing, optimizing device and network performance

5

Growth

� Increase penetration in established markets

� Leverage installed base to cross-sell

� Expand regionally

� Increase share of software and service business

Innovation

� Establish product platforms

� Increase level and speed of innovation

Operational Excellence

� Manage costs diligently

� Manage Group synergies

A ROBUST AND CLEAR STRATEGY BUILT ON 3 PILLARS

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 6

GLOBAL MARKET PRESENCE

7

North AmericaNorth America Western EuropeWestern Europe

Latin AmericaLatin America

CEECEE

APACAPAC

43249

3

45

6

417

Middle East/ Africa

Middle East/ Africa

15

10

ChinaChina

7

Corporate / division headquarterSubsidiary or branchNote: All figures based on FY 2012 revenues

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

ASCOM WIRELESS SOLUTIONS – OVERVIEW TODAY

• Ascom (US) Inc. incorporated on April 11, 2000

• North American Regional Sales Unit Headquartered in RTP Raleigh Durham, NC

• Patient Systems Product Line Headquartered in Bradenton, FL

• Distribution throughout North America, achieved largely through partner network

• R&D, channel, partner development dedicated to hospital communications since inception

• Leader in interoperability partnerships

• FDA registered and cleared medical device company

• 140+ employees

8

• Acquired Ericsson Personal Wireless Telephony (PWT) for $3.7M (4/2000)

• Introduced new 9p23 handset in the US (6/2002)

• Introduced Unite in US with Duty Assignment Client (5/2004)

• US Federal Communications Commission (FCC) changed Part 15 law which allowed for the sales DECT in US (4/2005)

• Introduced the i75 VoWiFi handset (4/2006)

• Introduced DECT Radio Exchange (RE) and 9d24 handset (2/2007)

• Introduced IP-DECT platform (1/2009)

• Introduced i62 VoWiFi handset (10/2010)

• Acquired GE Nurse Call System for $22M (6/2012)

• Introduced The Power of One (4/2013)

• Introduced Unite Axess for iPhones (10/2013)

ASCOM WIRELESS SOLUTIONS – MAJOR MILESTONES

9

ASCOM WIRELESS SOLUTIONS – PRODUCT MILESTONES

Freeset DCT1900(PWT)

Freeset DCT1900+(DECT)

4-2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

April 11, 2000 October 2013

i75

4-2006

9p23

7-2002

UNITE

4-2004

i62

10-2010d41/d62

1-2009

DECT w/9d24

2-2007

FreeNET VoWiFi(802.11)

IP-DECT(DECT)

IP-DECT

1-2009

PWT

Acquired

4-2000

Unite AM

10-2013

IP-DECT AP & TDM(DECT)

IP-DECT

2/2011 NCS

Acquired

6-2012

NURSE CALLSYSTEM

d81

4-2010

10AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

11

ASCOM WIRELESS SOLUTIONS - SALES REGIONS

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 11

1111

SAMPLE LIST OF HOSPITALS: 2,500+ AND COUNTING!

12AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

7.9 9.2 1011.9

17.521.4

19.4

26

31.1

44.8

60.0

0

10

20

30

40

50

60

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F

US

Dm 2003- 2012 CAGR = 20%

13

BUSINESS DEVELOPMENT IN WIRELESS SOLUTIONS USA

ASCOM NETWORK TESTING – OVERVIEW TODAY

• Ascom Network Testing Inc. incorporated on August 2009

• Division Headquartered in Reston, VA

• Americas Sales Region Headquartered in Reston, VA

• Global Product Unit Reporting&Analysis Headquarteted in Reston, VA

• R&D for the GPU Reporting&Analysis in Reston, VA and New Jersey

• Distribution throughout North America achieved largely through direct sales

• Market Leader in Network Testing

• Strong customer relationships with all leading Telco Operators: Verizon Wireless, AT&T Wireless, T-Mobile, Sprint

• 160+ employees

14

� ERICSSON

� 1994: Early entry to US market

� 1995: Implementing support for TDMA (2G standard in US competing with GSM)

� 1996: Established office with Ericsson in Dallas, TX - growing business from virtually zero to 12+ MUSD

� 1996: Supply agreement with largest competitor, LCC

� 1999: Acquisition of LCC's product businesses (tripling the US business and expanding direct channels)

� 2000: Worldwide headquarters moved to Reston, VA

ASCOM NETWORK TESTING – MAJOR MILESTONES

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 15

� ASCOM

� 2008: Acquired Argogroup giving access to US Tier-1 accounts

� 2009: Acquired Comarco Wireless Technologies expanding benchmarking business to the Americas and access to the world largest account (Verizon)

� 2009: Acquired TEMS business from Ericsson, gaining market share dominance in the US market through direct channels

So the US-business of network testing is really built on 4 (smart) acquisitions.

� 1. LCC products

� 2. Argogroup

� 3. Comarco Wireless Technologies

� 4. Ericsson TEMS

ASCOM NETWORK TESTING – MAJOR MILESTONES

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 16

Metro

Urban

Sub-urban

Rural85%90%

45%

85%

50%55%

5%

50%

0%

20%

40%

60%

80%

100%

2011 2017 2011 2017 2011 2017 2011 2017

LTE Population coverage still insignificant

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

Po

pu

lati

on

co

ve

rag

e in

%

Percentages represent portion of population that are within the deployed coverage area, not actual subscriber penetration.

GSM/EDGE WCDMA/HSPA CDMA LTE

Sou

rce:

Eric

sson

(20

12)

17

2012 2017

RegionsNumber of 4G connections

Percentage of Total Connections (%)

Number of 4G connections

Percentage of Total Connections (%)

Asia Pacific 24’143’897 0.7 425’094’836 8.0

Central & Eastern Europe 903’123 0.2 50’913’035 6.0

Latin America 326’212 0.0 51’772’961 6.0

Middle East & Africa 168’536 0.0 28’437’977 2.0

North America 31’329’522 6.8 264’618’277 31.0

Western Europe 3’544’454 0.6 171’013’933 18.0

Global 60’415’743 0.9 991’851’020 10.0

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

Source: Cisco VNI Mobile Forecast, 2013

18

LTE PENETRATION OFFERS ATTRACTIVE POTENTIAL

Only TEMS Investigation Tests with iPhone®

� Full support in TEMS Investigation for iPhone� iPhone generates more operator revenue and mobile data traffic

than any other phone

� Provides operators with an unprecedented level of visibility into network performance

� Enables efficient and detailed testing for key use cases� LTE Testing� Indoor Testing� Network Optimization

� Leverages operator investment � Seemlessly plugs into operator workflow

19

INTRODUCING: IPHONE® AND TEMS INVESTIGATION

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

� To build a market position in the US acquisitions are necessary but they then need to be enhanced with local organic business development

� Tech companies may have to develop / adapt their products for the US market but they can in return benefit from those developments in their other markets.

� Given the vastness of the territory, distribution is key, an indirect model may make sense

� The labor market in North America is very flexible which supports growth

� From a technology point-of-view, the US is often ahead of other markets (e.g. LTE)

� Local leadership makes the difference

� One market with over 300m people, one language (which we understand, speak and read), one currency is a huge advange and offers great potential

20

CONCLUSION

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group

LEGAL DISCLAIMER

This document contains specific forward-looking statements, e.g. statements including terms like“believe”, “expect” or similar expressions. Such forward-looking statements are subject to known andunknown risks, uncertainties and other factors which may result in a substantial divergence betweenthe actual results, financial situation, development or performance of Ascom and those explicitlypresumed in these statements.

Against the background of these uncertainties readers should not rely on forward-lookingstatements. Ascom assumes no responsibility to update forward-looking statements or adapt them tofuture events or developments.

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 21

[ ]

THANK YOU!

AMCHAM, KMU Panel, 21/11/2013 © Ascom Group 22

![IR Presentation@ASCOM 1 · PDF fileActix : 2 : Xceed : 3 : Qualitest : 4 ASCOM: 5 . Anite : IR Presentation@ASCOM 28 [ NETWORK TESTING ] VALUE CREATION NETWORK TESTING :](https://static.documents.pub/doc/80x56/5a7148a77f8b9aac538cb020/ir-presentationascom-1-nbsppdf-fileactix-2-xceed-3-qualitest.jpg)

![Ascom Investor Day Presentation 2014 · agenda 30th october 2014 [ ] § confirming the outlook § ascom myco - the game changer § ascom tems capacity manager – solving carriers’](https://static.documents.pub/doc/80x56/5e7499c69a3057609f23e3d0/ascom-investor-day-presentation-2014-agenda-30th-october-2014-confirming.jpg)