Page 1

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

31 March 2015

Asia Pacific

Equity Research

Strategy

Asian Investment Conference 2015

COMMENT

Key macro and company takeaways

Figure 1: Tone of corporate presentations at the AIC

Source: Credit Suisse research

■ We just concluded our week-long Asian Investment Conference (AIC) in

Hong Kong. With over 1,200 institutional investors attending the conference,

310 corporates providing their unique insight and with over 110 keynotes

and panel session speakers who shared their wisdom at the forum, this

18th AIC was amongst the biggest gathering of investors that Credit

Suisse has ever arranged in Asia. Our thanks to all the attendees who

made this event a success.

■ Our analysts were able to attend the presentations and group meetings for a

number of companies and in this note we provide the summary highlights from

these corporate meetings. The bullish mood of the investors noted during our

AIC sentiment survey (click here) also showed up at the company level where

62% of the companies (that our analysts attended the meetings for) sounded

positive against 38% that sounded negative or neutral in their outlook relative

to the prevailing views in the market (note that companies usually tend to

sound more positive than neutral about their business outlook). This is in

contrast to the mixed tone present at our last AIC, where only 52% were

positive, and 48% were negative or neutral.

■ This year we also had our largest and arguably the most impressive

repertoire of key note speakers. If you missed some of those, you could

watch them by clicking on this link AIC Keynotes.

61.8%

31.3%

6.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Positive Neutral Negative

Research Analysts

Manish Nigam

852 2101 7067

[email protected]

Mujtaba Rana

852 2102 6305

[email protected]

Page 2

31 March 2015

Asian Investment Conference 2015 2

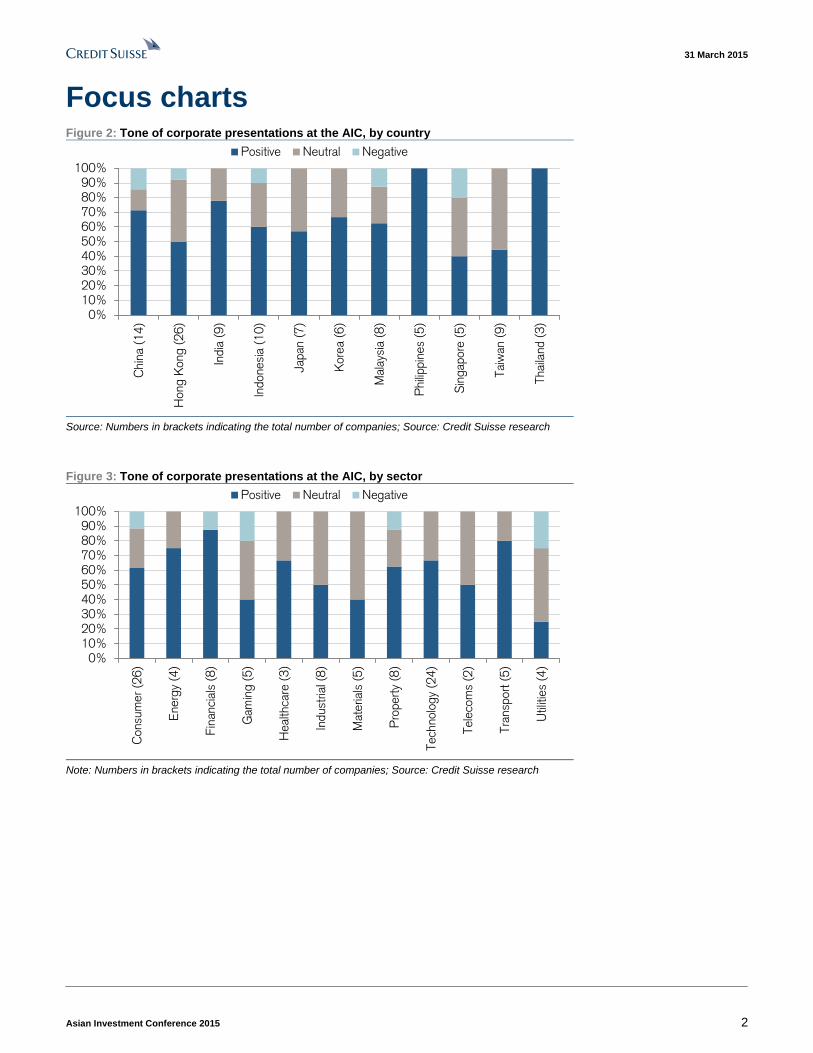

Focus charts Figure 2: Tone of corporate presentations at the AIC, by country

Source: Numbers in brackets indicating the total number of companies; Source: Credit Suisse research

Figure 3: Tone of corporate presentations at the AIC, by sector

Note: Numbers in brackets indicating the total number of companies; Source: Credit Suisse research

0%10%20%30%40%50%60%70%80%90%

100%

Chin

a (1

4)

Hong K

ong (

26

)

India

(9

)

Indonesi

a (1

0)

Japan

(7

)

Kore

a (6

)

Mal

ays

ia (

8)

Phili

ppin

es

(5)

Sin

gap

ore

(5)

Tai

wan

(9

)

Thai

land (

3)

Positive Neutral Negative

0%10%20%30%40%50%60%70%80%90%

100%

Consu

mer

(26)

Energ

y (4

)

Fin

anci

als

(8)

Gam

ing (

5)

Health

care

(3)

Indust

rial

(8

)

Mat

eria

ls (

5)

Pro

pert

y (8

)

Tech

nolo

gy

(24)

Tele

com

s (2

)

Tra

nsp

ort

(5)

Util

ities

(4)

Positive Neutral Negative

Page 3

31 March 2015

Asian Investment Conference 2015 3

Table of contents Focus Charts 2 Keynote & Analyst Presentations 6

Asia Technology Strategy 7 China Internet & New Media Expansion 7 Doing business in China, what is the reality? 8 Elephants can dance, and for very long 8 Geopolitical risks 10 Health check on global economy 11 Hong Kong: A Bright Future 12 Indonesian Challenges 12 Indonesia Central Bank 13 New governance in China – maintaining the rule of law 14 The new energy reality 15 The War on Graft 15 When will frontier markets prove rewarding to investors? 16 Will HK remain a compelling investment destination? 17

Company Presentations 18 AirAsia X (AIRX.KL) 19 Ajisen (0538.HK) 19 ASM Pacific (0522.HK) 20 Astra (ASII.JK) 21 AUO (2409.TW) 21 Ayala Land, Inc (ALI.PS) 22 Baidu (BIDU.OQ) 23 Bank Central Asia (BBCA.JK) 23 BASF (BASFn.DE) 24 Bharti Infratel (BHRI.BO) 25 BLOOM (BLOOM.PS) 25 Blue Bird (BIRD.JK) 25 BTS Group Holdings (BTS.SK) 26 Bumi Armada (BUAB.KL) 27 Cheung Kong Infrastructure (1038.HK) 28 China Animal Healthcare (0940.HK) 28 China Gas Holdings (0384.HK) 29 China Lodging (HTHT.OQ) 29 China Resources Cement (1313.HK) 30 China Resources Power (0836.HK) 30 China Shenhua (1088.HK) 31 Chow Tai Fook (1929.HK) 31 CIMB (CIMB.KL) 32 CTBC Holding (2891.TW) 32 Ctrip (CTRP.OQ) 33 Dawnrays Pharmaceutical (2348.HK) 33 Delta (2308.TW) 34 Dr. Reddy’s (REDY.BO) 34 DSN (DSNG.JK) 35 EDU (EDU.N) 36 Gajah Tunggal (GJTL.JK) 36 Genting Singapore (GENS.SI) 37 Globe Telecom (GLO.PS) 37 HCL Technologies (HCLT.NS) 38 HDFC Bank (HDBK.BO) 38 HDFC Ltd (HDFC.BO) 39

Page 4

31 March 2015

Asian Investment Conference 2015 4

Hollysys (HOLI.OQ) 39 Homeinns (HMIN.OQ) 40 Hong Kong Electric Investment (2638.HK) 41 HTC (2498.TW) 41 Huaneng Power International (0902.HK) 42 IDFC Ltd (IDFC.BO) 43 IJM Corporation (IJM MK) 43 Indofood Agri (IFAR.SI) 43 Indofood CBP (ICBP.JK) 44 Inotera (3474.TW) 45 JMEI (JMEI.N) 46 JSR (4185.T) 46 KEPCO (015760.KS) 47 Las Vegas Sands (LVS) / Sands China (1928.HK) 47 Lenovo (0992.HK) 48 LG Chem (051910.KS) 48 LG H&H (051900.KS) 49 Lifestyle (1212.HK) 50 Lippo Karawaci (LPKR.JK) 50 LT Group (LTG.PS) 52 Luk Fook (0590.HK) 52 Matahari Department Store (LPPF.JK) 53 Maxis (MXSC.KL) 54 Mediatek (2454.TW) 54 Melco Crown (MPEL.OQ) 55 Midea (000333.SZ) 55 Mitsubishi Chemical Holdings (4188.T) 56 MPPA (MPPA.JK) 56 NagaCorp (3918.HK) 57 Neptune Orient Lines (NEPS.SI) 58 NetEase (NTES.OQ) 58 Nine Dragon Paper (2689.HK) 59 NYK (9101.T) 59 Orient Overseas International (0316.HK) 60 OSIM International (OSIL.SI) 61 PTT (PTT.BK) 61 Qihoo (QIHU.N) 61 RHB Capital (RHBC.KL) 62 Robinsons Land Corp (RLC.PS) 62 Sa Sa (0178.HK) 63 Samsung C&T (000830.KS) 64 Sembcorp Industries (SCIL.SI) 64 Showa Denko (4004.T) 65 Shriram Transport Finance (SRTR.BO) 65 SK Hynix (000660.KS) 65 S-Oil (010950.KS) 66 SJM (0880.HK) 67 Skyworth Digital (0751.HK) 67 SMIC (0981.TW) 68 SPIL (2325.TW) 69 Stella (1836.HK) 69 Summarecon Agung (SMRA.JK) 70 TAL (TAL.N) 71 Tata Consultancy Services (TCS.BO) 71 TCL (000100.SZ) 72 Texhong Textile (2678.HK) 72

Page 5

31 March 2015

Asian Investment Conference 2015 5

Thai Beverage (TBEV.SI) 73 Tokuyama (4043.T) 73 Toshiba (6502.T) 74 Tosoh (4042.T) 74 TPK (3673.TW) 75 TSMC (2330.TW) 75 Tsui Wah (1314.HK) 76 TUF (TUF.BK) 77 Tune Insurance (TUNE.KL) 77 Ultratech / Grasim (ULTC.BO / GRAS.BO) 78 VGI Global Media (VGI.BK) 78 Visi Media Asia (VIVA.JK) 79 Waskita (WSKT.JK) 80 Weibo (WB.OQ) 80 Westports Bhd (WPRT.KL) 80 Wilmar (WLIL.SI) 81 Xiabu Xiabu (0520.HK) 82 YY (YY.OQ) 82 Zhaopin (ZPIN.N) 82 Zijin Mining (2899.HK) 83

Page 6

31 March 2015

Asian Investment Conference 2015 6

Keynote & Analyst Presentations

Page 7

31 March 2015

Asian Investment Conference 2015 7

Asia Technology Strategy

Speaker: Manish Nigam

New News: N/A

Tone: Bullish (on China Internet + Indian IT)

Summary: An extraordinary process of technological advancement has occurred in the

past decade – almost all of it being (in some way) manufactured out of Asia. The

consumer tech cycle has been the most apparent in this growth. We recommend a switch

from hardware and semis to software and Internet, specifically India and China.

CYCLE: Consumer tech cycle very different to others in that the very high end, very high

ASP product cycle has lasted eight years (consistent QoQ out performance since 3Q 11).

A significant base effect.

PCs: Have stabilised and grew positively in 1Q last year, but momentum in the last quarter

is beginning to roll over as replacement cycle now plateaus out.

SMARTPHONES: Vast majority who can afford a smartphone now own one, therefore unit

growth will fall rapidly.

The underpenetrated can largely only afford a low ASP product, so overall average prices

to come down

MARGINS / EARNINGS: Component manufacturing making the highest margins they've

ever made, with their customers (handset OEMs) making their lowest: not fundamentally

sustainable.

Korean semis, in particular, have gone from 40% EPS growth in 2014 to 0% in 2016, hard

to argue this sector will outperform.

CHINA: Still the fastest grower in 2015, with 25% top-line CAGR over next five years.

Death rate, however, will be high compared to Indian IT (top five companies now,

expected to be top five in a few years' time).

China Internet & New Media Expansion

Speaker: Dick Wei

New News: None

Tone: Bullish

Key points:

Increasing user growth seen consistently for 7 yr, with penetration just reaching world

average.

Mobile Internet counts for much of this: further growth here will unlock huge potential in e-

commerce.

Demographics tailwind to benefit online economy.

Top 15 mobile apps completely dominated by Tencent, Baba, Qihoo and Baidu

MOBILE:

64% of traffic comes from mobile, but revenue contribution only stands at 43%

We expect 60% YoY mobile game growth in 2015

Mobile ad revenue lowest in Asia-pac (around a sixth of US, for Facebook and twitter)

Tencent ad around $2.3 vs $8 for Facebook.

E-COMMERCE:

Page 8

31 March 2015

Asian Investment Conference 2015 8

Mobile shipping GMV to account for 16% of total online shopping by end 2016.

Conversion and payment are two biggest roadblocks.

F&B, health goods and medical services all underpenetrated in online.

LOCAL SERVICES:

User demographics shifting beyond gamers, and improved monetisation model in play.

Dianping strong in group buy sector.

O2O services should capture the next $100bn of growth.

There will likely be a battle between comprehensive and vertical start-ups in 2015.

Doing business in China, what is the reality?

Speaker: Bertrand-Marc(Marc), Allen, President, Boeing International, Robert

Buchbauer, Member,Executive Board, and CEO Consumer Goods,

Swarovski, Jörg Wuttke, President, European Union Chamber of

Commerce in China

New News: None

Tone: Positive

Growth pattern of China differentiated a lot from past years. China used to maintain a high

GDP growth across the country, but for now, economic growth patterns vary province by

province. Northeast region may suffer most, while the costal and southern areas can still

maintain a robust growth.

Although they admitted a slowdown in China's economic growth, Allen and Robert still

believe there is huge potential for them to expand market in China.

The regulatory enviornment of China is mixed and need to be judged sector by sector. For

aviation, Allen believed that government control exempted companies in this sector from

suffering overcapacity. And Robert gave a few examples to show that the impact of

government regulations on foreign companies depends on how enterprises react. But

overall, Jörg argues that the golden years for foreign capital to develop business in China

was during Zhu Rongji era, which is already past.

All the three welcomed competition with local players, and they believe competition is the

source of innovation and efficiency, the driver of better management and industry

consolidation.

Elephants can dance, and for very long

Speaker: Dr. Duvvuri Subbarao Distinguished Visiting Fellow, National

University of Singapore Business School; former Governor, RB

New News: None

Tone: Positive

What is the most important factor for growth?

India requires a phenomenal increase in investments, as was the case when the GDP was

growing at 9%-plus. The slowdown, at least as per the old series, has been led by the

slowdown in investment. On the surface the 38% of GDP investment rate may have fallen

to 34%, a relatively minor fall, but a lot of the investment is going into hard assets and gold.

So the slowdown in productive investment is large.

Page 9

31 March 2015

Asian Investment Conference 2015 9

What is the challenge in infrastructure investment?

There are two challenges:

Policy challenges: the optimism around PPP has melted away from both the

government (charges of crony capitalism) and the private sector (over-leverage,

delayed projects). This budget tried to address some of these issues.

Financing challenges: ~US$1tn is required to finance this infrastructure over the next

five years (almost double the current rate). But the government does not have the

money. The private sector also struggles because there is no long-term finance

market in India. The government and the RBI are trying to develop the bond market

but it has not grown at the expected pace. Banks had to step in, but they are not

geared to take these risks. The RBI has bent over backwards trying to accommodate

the challenge, but going any further is very risky.

Why is "Make in India" the central theme of Mr. Modi's policy?

India needs to create hundreds of millions of jobs. This cannot happen through agriculture

- in fact, with improving productivity, agriculture will throw out people. Services cannot

scale at that level. However, India cannot replicate the China model for two reasons:

China opened up in the 80s and 90s, when the rich world was growing (which is not

the case now). Global trade growth has slowed. India cannot rely on external demand.

Labor arbitrage doesn't work anymore. With automation, workers in developed

markets are willing to work for lower wages. There is also focus on keeping supply

closer to demand (near-shoring or re-shoring will pick up). So India cannot rely on

exports.

Inflation outlook for India.

Inflation is a repressive tax, and hurts the poor the most. There are two components of

inflation: the structural component, and the cyclical component. Rising wages of low

income people has meant food habits are changing, and that drives inflation. Longer-

term, RBI will be driven by three considerations:

Low and stable inflation is important for both internal and external investors.

As India's economy integrates with the rest of the world, inflation cannot be very

different from ROW

Interest of savers - important to keep a positive real savings rate.

Is India's BoP vulnerable?

No. In 2012 and 2013 India had 4.2% and 4.5% CAD which was much higher than the

sustainable CAD of 2.5%. But the self-adjusting characteristic of CAD did not play out

because of excess money supply globally. So, when the reversal happened, the rupee

made that adjustment very abruptly, and in a destabilising way. India became complacent,

and was taken by surprise. Now however, India is out of the Fragile Five, the CAD is lower,

reserves are higher, and India is much better prepared.

Why is fiscal consolidation so important?

In the past few years, India has seen all the classical problems of a high fiscal deficit: high

inflation, crowding out of the private sector and BoP imbalances as excess spending

spilled over into external balances. So, while for the rest of the world the debate is

"austerity vs. growth", in India the debate is "austerity FOR growth". There is a need to

give space to the private sector.

Way forward on ease of doing business.

Governance reforms are important. India ranks 142 on the ease of doing business

rankings. Governance hurdles have to be cleared at the central as well as the state

Page 10

31 March 2015

Asian Investment Conference 2015 10

government level. It is unfair to compare India to China. India is a tougher place to do

business in. However, there are things that can be done. As per the same study, if one

takes a hypothetical city called "Indiana" that adopts the best practices of all Indian states,

India could reach a rank of 69, and GDP growth could be 3 pp higher.

Changing Federalism.

One needs to look at changes at the state level. There are three changes happening:

Second generation reforms will require state involvement: issues like land, labour,

indirect taxes, are all state level issues. Almost by definition these reforms are not

amenable for big bang, and will be incremental.

Central government collects 60% of taxes and spends 40%. But now states collect

40% of taxes and spend 60%. With untied transfers to state governments going up,

they get more freedom.

Governance reforms: many projects are stalled because of some problems at the

state level.

Is the Indian growth story credible?

Yes. India has left fatalism behind. For the longest time, as the East Asian economies

were accelerating, Indians thought they were smaller, and India is too big. But once China

showed that large economies can grow, India started to think it could too. And then it

showed it could. That sense of belief is very important. The East Asian economies are

referred to as Tigers, China as a dragon, and India an elephant. An elephant keeps

lumbering away, but it can dance. And it has huge stamina - it can dance for very long! In

the past five years mistakes have been made in both fiscal and monetary policies, and

India need to learn and keep improving.

Geopolitical risks

Speaker: Anders Fogh Rasmussen, former Prime Minister of Denmark

New News: None

Tone: Optimistic

CONCLUSION: Believes in a peaceful rise of China in constructive co-operation with the

US

Rasmussen highlighted the following disruptive unknowns he is most concerned

about:

Possible Russian attack or intimidation of NATO member.

Risk that ISIS advances and controls Iraq/Syria/Libya and the infrastructure there

Closure of Suez canal and terrorism in Sinai/Yemen

Closure of Hormuz strait by Iran

Iranian nuclear weapon proliferation, leading to arms race in Middle East

North Korea missile attack against South Korea, Japan or the US.

Closure of Malacca strait.

China & US Relationship:

China is focused on continued growth generation

In their interest to keep trade channels open and a free trade system in place

Realises the world's strongest power, US, will remain the same for the next few decades.

Page 11

31 March 2015

Asian Investment Conference 2015 11

The US has certain advantages that can't be overcome easily or quickly: favourable

demographics, energy surplus, R&D, education, geographical positioning and military

capacity.

China should be included in future transpacific partnerships.

By helping each other, they increase the capacity of the world to keep the unknowns

above at bay.

Health check on global economy

Speakers: Jose Manuel Barroso: former President of European Commission,

Former President of Portugal. Richard W Fisher: Member US

Federal Open Market Committee. Michael Pettis: Professor

Guanghua School of Management - Peking University. Hideo

Hayakawa: Senior Executive Fellow: Economic Research Centre. Dr

Duvvuri Subbarao: Visiting Fellow, National University of Singapore.

New News: None

Tone: Cautious on China, Positive on EU and India

China - Growth will be much lower than we expect (Michael Pettis)

What China has done is nothing new...dozens of other countries have had "investment"

miracles and all of them have had to go through brutal adjustments.

Not that a lot of that has happened. There is a reasonable chance that China may be able

to adjust through this...and that is a very, very rare occurrence.

A great case scenario is that China can grow 3-4%, with 5-7% household income

growth...and this is not bearish, if they can pull it off that will be fantastic.

The only way you get out of a high level of debt historically is through debt forgiveness

programs...reforms don't work!!!

India - Will India do what is required? (Dr Duvvuri Subbarao)

On a number of issues, India is in a sweet spot

Indian economic cycle is the reverse of some other major economies in the world

First time in 30 years a government that is assured five years in office, and federal

government controls states with 50% of GDP.

But India is supply constrained. Especially, infrastructure. Need USD1tr in next 10 years.

That is 10% of GDP every year.

EU and reforms:

Reforms are slow but indeed happening. Retirement reform, employment reform.

This is going to be a good year for Europe (President Barroso)

Rise of extremism and what is happening in Russia is a risk, but will probably be handled.

US - where from here:

There is still no consensus on when to tighten inside the Fed.

This is the lowest rates in the US in the past 260 years history of the US.

Low oil puts pressure on the job market, especially in the Texas and the oil industry which

was the biggest contributor to job creation.

Page 12

31 March 2015

Asian Investment Conference 2015 12

There will be a natural reduction to raise rates as the lessons of 1937 are still worrying

policy makers. Then too we thought we were coming out of a recession and walked into

the depression.

So we are moving from Uber accommodative to just "accommodative".

Hong Kong: A Bright Future

Speaker: CY Leung

New News: None

Tone: Bullish

Hong Kong's past and future:

Displacement by Singapore and Shanghai not realised

Initial questions on two currencies and two systems: now realise China is big enough to

require Shanghai and HK

HK investments into mainland now cover all sectors and geographies, e.g., 70% of fees

earned by HK architects are from CN

Kowloon East and east Lantau now being developed into further business districts.

HK banks handle 70% of Foreign RMB payments.

Challenges:

Method of electing CEO by universal suffrage has to be passed by two thirds majority.

Wide range of GDP growth projections next year reflects volatility

Housing and land requirements

Filibustering by legislative members.

Tax and expenditure:

Service tax receipts should be at a record high soon

Old age living allowance has helped over 400k OAPs

Infrastructure development grown from $50 bn five years ago to $70 bn now.

Unemployment last year down to 3.2%, with minimum average earnings of lower taxile

group up 35% since minimum wage introductions four years ago.

Indonesian Challenges

Speaker: Dr B. Brodjonegoro, Minister of Finance Republic of Indonesia

New News: None

Tone: Positive

Managing the budget:

Loss of Rp1.3 tn due to lower oil price.

Tax ratio is a very low 11% of GDP, so we have to right away go about increasing this

Shows inability of collection rather than the capacity of the economy to pay taxes,

hopefully to 12%

Spending:

Last year only 95% of target spending, and Infrastructure only 80%.

Page 13

31 March 2015

Asian Investment Conference 2015 13

Some of the delays were regulation-related, some land acquisition-related. Trying to

resolve these problems now.

Budget deficit target at 2%.

Currency:

Impact on the budget for infrastructure?

Import equipment, steel, but commodities down as well so take off some of the impact

Helps the manufacturing sector, which is up 7% in exports last year

13,000 is a bit of a psychological level beyond which the people get worried

Balancing growth vs Currency: Growth focus from infra and SOE projects spending and

FDI.

CA deficit <3%

Increasing credit growth from 12% to 15%-17%.

Infrastructure:

Budget will cover the basic type of infra, like roads, irrigation, sanitation etc. Then will be

the fully private/SoE that will be run by companies either SOE or private companies.

Then there are the PPP projects. This is still in the early stage but already some projects

like mine-mouth IPPs, airport railway etc are going on in this area.

Rp5,000 tn over the next five years. 20% from Budget, 20% from SOEs, 20% from Private

and rest from PPP. For 2015 from the budget will be Rp300 tn, SOE Rp100 tn, PPP <

Rp100 tn.

Funding: Trying to readjust bilateral and multi-lateral loans to increase the duration of the

loans. Setting up Indonesia Infrastructure bank. Need to utilise funds from Social Security,

Hajj Fund, Endowment Education funds, etc. This bank can issue bonds and this "idle"

money can be invested in these bonds.

Are we becoming more interventionist:

Cigarettes still below Thailand (80-90%). In Indonesia, by law, it can only be 57% so we

will continue to be lower than the rest of the world.

Focus will be on bigger manufacturers rather than smaller ones.

Cement: Prices are probably higher than a free market would allow, so the government is

nudging companies towards a market-based price.

Banking Industry: No plans to intervene on banking and loan pricing, but need to improve

efficiencies in the banking sector that can bring pricing down.

Indonesia Central Bank

Speaker: M.Aditsyaswara, Senior Deputy Governor of Indonesia Central Bank

New News: None

Tone: Positive

The focus of BI remains to be

Inflation (target 15-17: 4%, plus and minus 1%, 18 onwards at 3.5%)

CAD should not go above 3% GDP, already include the acceleration of govt infrastructure

spending (estimating above US$1 bn)

Page 14

31 March 2015

Asian Investment Conference 2015 14

External debt, the reason of introduction of hedging last Dec 14 of 20-30% that is maturing

3-6 months period

The use of Rupiah in the domestic market transaction

LDR for banks already high at above 90%, encouraging banks to issue non-deposit

instruments

Payment system

Interest rate cut in Feb 15 because of the lower inflation, NOT because of the easing

monetary policy.

Depreciation of Rupiah is a bit too much already at this level. BI also concern because it

will impact the inflation. Stress test that up to Rp14,000 on the exchange rate, to the banks

and external debt are still fine. Survey on the corporates that did not hedge onshore, did

offshore hedge.

CAD for the next few years will still be 2.9-3%, but the structure is different now, it is more

for infrastructure rather than for consumption (fuel subsidy).

Debt service ratio is at 40-45%, partly because of Pertamina's short-term borrowing

resulting from the previous subsidy mechanism is waiting for the funds from the

government. However, with minimal subsidy now, the short-term borrowing of Pertamina is

going to be minimal as well.

Slowdown in economy because of commodity, particularly in Sumatra and Kalimantan.

Java houses the manufacturing and service industry, still growing at 5.5-6% (Jakarta at

6%, East Java 5.9%, West Java 5.6%, Sumatra 4.5-5%, Kalimantan 4-4.5%, Bali 6.5%)

Real effective exchange rate is being looked at as well, but not necessarily has to follow if

the other countries' exchange rate depreciates

In order to speed up the licenses for foreign investment in Indonesia, the Government has

given the authority to BKPM (Indonesia Coordinating Investment Board) instead of having

to go to different ministries

The government has announced a package to reduce the CAD: (1) insurance company,

(2) investment of profits, tax incentives given to corporates (need MoF decree), around

US$19 bn, (3) fee visa to 30 countries (target 25 mn tourists vs current 8-9 mn), (4) tax

incentives for corporates with 30% export.

NPL for the banking sector is about 2.3% currently, from 1.7% in 2012

Loan growth expected at 14-15%, including the govt infrastructure, currently at 11-12%.

New governance in China – maintaining the rule of

law

Speaker: Professor Liu Mingkang, Distinguished Fellow, Fung Global Institute

New News: None

Tone: Positive

Increase judicial system efficiency. China will allow lawyers previously working in

private sectors to play a role in the legislative system, thereby bringing in their expertise to

increase justice, transparency, and predictability of China's judicial system.

Local government debt replacement. In Prof Liu's view, whether the government's

switch from LGFV to a provincial government bond can reduce financial systemic risk

depends on how the government performs with the new borrowing tools. However, two

things are made clear: first, local government liabilities will be reduced; and second, bank

loans related to local government activities will decrease also.

Page 15

31 March 2015

Asian Investment Conference 2015 15

Rmb internationalisation. Capital account free cash flow is the destination of Rmb

internationalisation, but time is needed to gradually carry out the reform, as highlighted by

Prof. Liu. Although Shanghai–HK connect provided only a thin channel between China and

Hong Kong capital market, it is actually playing very important roles and will be used to

check whether China is on the right direction.

Other reforms. According to Prof. Liu, the government under Xi's leadership shows their

determination to implement reforms in other areas such as strengthening intellectual

property protection, increasing accounting system transparency, resolving pollution

problems, among others.

The new energy reality

Speaker: Dr. Fereidun Fesharaki, Dr Pierre Noël, Professor Ni Lexiong

New News: None

Tone: Neutral

Oil price expectations of around US$50 for 3Q, and US$55 for 4Q for most panellists.

What could change the current status quo?

OPEC and particularly Saudi want to see a SLOWDOWN in the US growth of production...

c. down to 100k-200k growth a year.

The market cannot expect them to act in the June meeting as nothing has happened in

that regard.

Higher oil prices will likely therefore only occur if Saudis can cut production substantially.

Shale effects?:

"YOU CAN NOT KILL THE EFFECTS OF SHALE OIL, ONLY POSTPONE IT"

Investors should expect these effects to last 10-15 years, as a best guess.

Naturally, these lower prices damage high cape projects.

Japan:

Still struggling with the restart of nuclear energy.

This is crucial to the 'three E's' : Energy Security, Environmental Effects, Economic

Efficiency.

China:

Strategic reserves of only 90 days. May use low prices as an opportunity to accumulate.

Energy demand is huge, of course. In the short term, they may stockpile or acquire foreign

fields and companies. In the long term, they need to focus on solar, hydro, nuclear and

wind.

Shale is in a mixed position in China. The technology is rapidly advancing but the

problems of a lack of water in the North, and population density in the south, persist.

Shale projects are being resisted economically and socially.

The War on Graft

Speaker: Professor Chang Li, Mr Michael Pettis

New News: None

Tone: N/A

Page 16

31 March 2015

Asian Investment Conference 2015 16

Below, we give an extract of the main points discussed during the keynote panel titled The

war on graft: What impact will it have on China's political and economic future?

Current situation:

Over a hundred minister-level politicians have now been arrested, making it the most

aggressive campaign to date.

Campaigns usually last 1 to 2 years, with the situation usually degrading further as soon

as it ends. This could be different.

We could expect this campaign to last until Feb '17.

China at a crossroads right now, more so than in the last 26 years... "A PARADOX OF

HOPE & FEAR"

- The HOPE is that after 2 or 3 years, we are over the peak of corruption.

- The FEAR is that this alienates people. Who or what is next?

Support for the anti-corruption measures:

Many still unsure whether this is just a facade for an internal power struggle and a party

purge.

The general population, military and low level public service employees are lending

support to this.

Party officials, military brass and liberal intellectuals are not.

Will this campaign aid reforms in China?:

Corruption is NOT incompatible with growth.

US had the same problems post the civil war, but on an even LARGER scale.

'Destabilising' corruption, which occurs in times of political instability (where corruption

gains are maximised in the short term), is something which we should worry about

however.

Liberalising reforms deny the elite the ability to extract rent, and have as such been

vehemently opposed in China.

Premier Xi has to implement these reforms, regardless of pushback, similar to the 1980s.

The pace, procedure and implementation of these reforms have been questioned. Not the

morality.

We should expect the Chinese government to steamroll these changes through. The

openness to reform that a free and independent judiciary affords will not be the case here.

Anti-corruption will be joined by a growth in discipline, stronger oversight bodies, etc, in the

coming years.

When will frontier markets prove rewarding to

investors?

Speaker: HE Sun Chanthol, Dr. Syed Samad, B. Bazargur, Serge Pun

New News: None

Tone: Mixed

Bangladesh:

FDI guaranteed by protected legislature

Democracy and accountability of government

Second easiest place in region to do business and start business according to World Bank

Page 17

31 March 2015

Asian Investment Conference 2015 17

Sector wise: Agribusiness, plastics, readymade garments, shipbuilding, furniture

Business financing largely direct, no real corporate bond market.

Private equity dominated by private investors

Large scale reform in process

Cambodia:

In the last 20 years, Cambodia has grown by 7% per annum: sixth fastest in the world.

1.2% inflation. Debt to GDP only 30%.

Political stability, pro business government

Investment law provides tax incentives, no capital controls + duty exemptions

EBA (everything but arms) means everything made in Cambodia can be shipped to

Europe without duties.

Myanmar:

Labour law came before economic reform

Political and social reforms are far reaching, but not immediate perhaps.

Inclusiveness, responsible business required.

Will HK remain a compelling investment destination?

Speaker: Regina lp Lau Suk Yee, Steve Vickers

New News: None

Tone: Bullish

Hong Kong Current Status:

Beijing's decision last summer has led to Youth pushback and anti-mainland sentiment.

One party Two Systems requires many factors to work efficiently.

Basic law draft in 1980s was to protect HK's liberal lifestyle and freedoms from

encroachment by socialist China.

Did not envision world today, with HK's position in the world today having changed so

substantially

Globalisation, China becoming a powerhouse, and HK's own economic changes, have all

played a part.

HK has failed to ride the digital wave:

Only accounts for 2.9% of China's economy.

Without a clear strategy, HK has stood still relying on classic system of no-interference.

Shenzhen has grown into a technological hub, whereas HK has not.

Challenges:

New role in China's evolving economic strategy. HK's own democratisation process. Over-

reliance on property and low-margin tourism driving growth. Bureaucratic civil service

Strengths:

Main channel for internationalisation of RMB. Business services and high value add

services such as logistics. R&D (especially education). China's most trusted partner.

Page 18

31 March 2015

Asian Investment Conference 2015 18

Company Presentations

Page 19

31 March 2015

Asian Investment Conference 2015 19

AirAsia X (AIRX.KL)

Speaker: Benyamin Ismail (CEO), Huei Shian Check, CFO

New News: None

Tone: Neutral

MH turnaround - focus on growing parts of the business that don't compete with Malaysia

Airlines (MH) such as Thai AAX and Indonesia AAX. Confident that new MH CEO

(Christophe Mueller) will execute the same "right-sizing" strategy as he did at Aer Lingus

and he is starting earlier than planned (now May). Will still face the issues of downsizing

pay-roll, which process seems to keep on being extended.

AirAsia X (D7) turnaround - systems had deteriorated since IPO and require a significant

overhaul, need to harmonise network better with short-haul, improve marketing. Looking to

lift yields, not give too much away to agents, regain ground lost to poor sentiment following

the AirAsia Indonesia crash. Also cutting headcount and renegotiating airport and supplier

agreements in return for extended contract tenor. Cutting routes will also save money:

ADL cost RM100 mn a year, double-daily MEL-SYD was RM50 mn a year and NGO was

RM70 mn a year in losses in 2014, so reducing exposure here alone would cut losses

incurred in 2014

Macro-drivers - 54% hedged at US$88/bbl, costs 60% USD-denominated. Leasing

income just temporary. Working on an ACMI basis (aircraft, crew, maintenance, insurance)

with three aircraft right now and another two later in the year. Generally on two-to-six-

month terms, but want to reduce exposure to this to only two planes in 2016.

Cash flow - need the rights issue to generate adequate cash flow to change balance

sheet shape and service creditors aside from bank loans. RM400 mn rights issue should

allow the company to restructure balance sheet within six months. Haven't been able to

market adequately as budget has been cut to conserve cash. Need to generate more

sales so focusing on launching Sapporo ahead of Golden Week, looking at Hawaii,

Auckland and London, but will need an A330-HGW that has the "legs" to get there.

Ajisen (0538.HK)

Speaker: Robert Lau (CFO), Richard Liu (Vice President)

New News: Yes

Tone: 1Q15 negative, overall positive

1Q15 update: China is challenging, Hong Kong is better because of poor traffic in malls.

Strategy focus: (1) smaller stores – 30-40% higher sales per sqm; 1% higher OP margin;

15% save of capex; (2) delivery –15 stores in Beijing on trial; third-party delivery partners

include Meituan, Eleme, Daojia, and Baidu Waimai; now only accounts for 6% per-store

sales; target is to reach 10%; incremental net profits margin from delivery is 30-40%; (3)

store in malls – Ajisen will still have >90% stores in malls because management expects

malls would draw better traffic when increasing F&B area.

Management is committed to improving efficiency and business diversity. However, less

focus on product and service quality, which is the reason for Ajisen's losing customer

traffic.

Timothy Ross

+ 65 6212 3337

timothy.ross@credit-

suisse.com

Sophie Chiu

+852 2101 7657

sophie.chiu@credit-

suisse.com

Page 20

31 March 2015

Asian Investment Conference 2015 20

ASM Pacific (0522.HK)

Speaker: Leonard Lee, Strategy and Corporate Communications Manager

New News: None

Tone: Positive

Similar broader end market drivers for the business. In 2014, top drivers were

automotive orders, industrial, and strong orders for a high-end smartphone (normally

orders for a two-year cycle so may slow in 2015) and emerging market smartphone. For

2015, the company is looking at a similar set of growth drivers as auto/industrial has long

product cycles and mobile investment continues.

Sales and share gains targeted to continue in SMT. The company believes the SMT

market will grow from US$3.5 bn to $3.8 bn and targets modest share gains. ASM Pacific

has crossed 20%, up from an 11% share when it entered the business, with $600-700 mn

annual sales. It expects to pass Panasonic’s 24% share by 2016. The company has #1

share in Europe, #2 in the US and #3 in China/#4 in SE Asia, so targets more share in

mobile/IT and emerging markets. This year, the company is launching a mid-speed SMT

tool (Eby SiPlace) targeting the mainstream market at lower cost to gain share and has

gained in the US/Mexico small manufacturers. The company is also launching an

integrated close loop for yield improvement/cost savings for customer with screen printer

acquired from DEK (applying solder paste to PCB), solder paste inspection (being

developed by the back-end) followed by SMT pick and place. The TAM of SMT is US$3-

4bn (screen printer added US$500mn with DEK at about US$40-50mn run rate).

Back-end has tougher compares after a strong 2014. The back-end market is about

US$4-5 bn although the company cites Gartner data forecasting flat in 2015 and -10% in

2016 although its own market feedback is for some YoY improvement in 1H15, but 2H15

YoY faces tougher compares. Last year saw strong lift from smartphones,

automotive/industrial, LED and moderate expansion in CMOS sensors.

Advanced packaging growing. The company now has 60% from traditional die and

wirebonders and 40% from advanced packaging (TCB bonders, flip chip bonders, and

encapsulation, molding, test handlers, clip bonders for power management and CMOS

sensors). Advanced packaging has grown from 20% to 40% since 2011, with newer

products having better margins. The company has TCB bonder for CPU and is working on

a faster solution for mobile (3-4bn unit module addressable market), as pricing /

throughput is less competitive with flip chip bonders. In flip chip bonders, the company is

#2 and doing well in low pin count for RF with a die bonder with flip chip capability.

Margin impact. ASM is guiding a few points GM increase in SMT to high 30% for the full

2015 by insourcing more production in Asia to counteract ASP pressure from the Yen. It

has shifted feeders to Malaysia to lower costs and some modules to China. The back-end

target GM is 40%, targeting outsourcing at 30% of its production. It targets opex at 20% of

sales.

Currency impact favorable. The company believes currency is favourable netting

everything out. While the Yen puts strong pricing pressure on SMT, it has less on back-

end as Towa/Shinkawa are smaller players there and ASM Pacific is gaining share with

insourcing and new lower cost tool. The company has a good portion of costs in Germany

in SMT so Euro is favourable.

ASMI selling pressure is now lower. ASMI reduced holdings from 52% to 40% of ASM

Pacific two years ago to unlock some value. ASMI has now done much better and lifted its

own share price, so the company believes pressure for ASMI to divest shares of ASM

Pacific is lower.

Randy Abrams

+ 886 2 2715 6366

randy.abrams@credit-

suisse.com

Page 21

31 March 2015

Asian Investment Conference 2015 21

Astra (ASII.JK)

Speaker: Iwan Hadiantoro - Chief of group treasury, Tira Ardianti - Head of IR

New News: None

Tone: Neutral

Last year, domestic 4W auto sales volume were 1.2mn; fell slightly YoY.

Jan/Feb sales were weak due to (1) flood affecting logistics, (2) adjustments to inventory

and (3) the introduction of new models by competitors.

Starting two years ago, auto players in the market began increasing production capacity;

currently around 2 mn units, but domestic demand is only 1.2 mn units and exports 200k

units, which leads to high discounts in the market.

Mitsubishi intends to build a plant in Indonesia with production capacity of 160,000 units.

Management thinks that this is temporary, not structural.

Current average discount for Astra's cars is 6-8%; management expects similar level for

the next 12M.

Can improve market share via new launchings? Astra has several products in pipeline but

the timing of its launching remains undisclosed.

Management intends to do major facelifts for low MPV models (exterior and engine) for

this year.

Complete model change for Toyota Innova and Fortuner for this year.

With Astra's comfortable market share level at least 50%, the company is optimistic that

with strong value chain and after sales services, supporting financing and insurance

businesses, market share can be maintained.

In the heavy machinery division, clients delay replacements and extend lifecycle.

Management expects replacements to occur this year as the average life cycle is around 7

years, which is the max before productivity declines.

Management is comfortable with overall revenue mix of 55% autos and 45% non-autos.

Dollar debt is fully-hedged with currency swap.

AUO (2409.TW)

Speaker: Pearl Lin, Senior IR Manager

New News: None

Tone: Cautiously optimistic

1Q15 tracking in-line with guidance. AUO guided 1Q15 large size panel shipment to

decline high-single digit to low-teens QoQ and maintains its unchanged guidance

(Jan+Feb large size shipment is 67% of mid-point of guidance). Loading rate is expected

to stay at low-90% level due to annual maintenance for some fabs. It noted the sequential

decline for TV shipments in 1Q is mainly due to annual maintenance, while the IT

shipment decline is due to weaker end demand.

TV inventory level healthy for most regions, IT inventory still slightly higher. AUO

thinks TV inventory level post CNY returned to a healthy level of six to eight weeks, but

inventory level in Eastern Europe is one to two weeks higher due to weaker currency. For

IT (NB, monitor), it thinks inventory is one week higher than normal and believes the

supply chain will still need to work down the inventory after strong 2H14 shipment.

2Q15 outlook depends on sell through. AUO noted TV panel demand for 2Q will

depend on China May holiday sell through, especially there is no major sports event this

Jahanzeb Naseer

+62 21 255 37977

jahanzeb.naseer@credit-

suisse.com

Bernard Kie

+ 62 21 255 37902

bernard.kie@credit-

suisse.com

Jerry Su

+886 2 2715 6361

[email protected]

Page 22

31 March 2015

Asian Investment Conference 2015 22

year (last year had World Cup), and it hopes leading TV brands to start pull-in by end-2Q

to prepare 2H demand. For NB panels, it sees pent-up demand in 1H prior to Win 10

launch. NB makers might need to modify their design to meet the new MSFT

requirement/subsidy. Overall, it thinks 2Q demand will be weaker than last year's, due to

no sports event, but still in-line with normal seasonality.

New products/technologies to differentiate. AUO has been developing new

technologies for TV panels, such as 4K, curved TV, HDR (high dynamic range), Quantum

Dot, etc., in order to differentiate itself with Chinese peers. It expects 2015 4K TV sell-

through of 23-24 mn units (10% penetration), vs 9 mn last year (4% penetration), and

believes panel demand will be higher than this. It is also working on NB OTP (on-cell

touch) and in-cell smartphone panels for 2Q (OTP NB) and 2H (in-cell) mass production.

Balancing customer portfolio. AUO aims to further balance its customer portfolio to

offset demand slowdown, if any. Currently, China TV customers account for one-third of its

TV business, one-third for Korean brands, and one-third for others (US/European brands,

ODMs). Also, its smartphone is more exposed to mid-to-high end (HD720/FHD) with

Chinese customers accounting for 50% of smartphone business.

Ayala Land, Inc (ALI.PS)

Speaker: Jaime Ysmael (CFO), Ricky Celis (President - Amaia)

New News: None

Tone: Positive

Achieved 5-10-15 plan: Initially targeted to reach P10 bn NIAT and 15% ROE in five

years from 2009, they were able to reach NIAT target one year ahead in 2013 with FY14

NIAT reaching P14.8 bn. Nevertheless, ROE only reached 14.4% by FY14 because of

capital raising activities, i.e., FTI acquisition and opportunistic land banking in 2012 and

2013. Recently, had a private placement in January 2015; the company doesn't see any

additional equity raising this year, FY16 funding will be reviewed given internal net debt

threshold of 1.0x (currently 0.74x).

Sets new "2020-40 Vision" plan: The company has guided for a NIAT of P40 bn by 2020,

or 20% annual growth from its 2013 level. It is well positioned to take advantage of the

property cycles given expansive land bank of 8,639 hectares (gross) across 31 growth

centers in the Philippines (90/10 land bank split Metro Manila/Provincial). Focus is on

developing new large scale/mixed-use/integrated property estates, which has been a

successful model for them in Makati CBD, Bonifacio Global City, Cebu Park District, and

Nuvali. They look to triple their Office and Malls GLA and Hotel rooms by 2020 - bring

residential revenue contribution to 50% of total revenues (currently at 2/3).

2015 guidance: FY15 capex budget of P100 bn from P83 bn last year - 37% residential,

31% land banking, 15% malls, 5% offices, 3% hotels and resorts, 9% general use. Mixed

tone on residential project launches, they reduced it to P87 bn worth of residential sales in

FY14 from P108 bn in FY13 due to supply glut concerns, but look to offer P100-120 bn of

new residential projects this year. Demand for office and malls leasing is stable, and they

will continue to grow office GLA primarily because of BPO demand.

Comments on regulatory risks and recent market developments: Management is well

aware of stringent regulatory measures, in fact they are in constant discussion with the

central bank to discuss the situation of the property market. They believe that there is no

price bubble given that the property developers behaved rationally in their yearly ASP

adjustments; they also think the high land bidding in Bonifacio back in Oct'14 was a one-

off. Supply-demand imbalance in Metro Manila because of aggressive launching of small-

cut low-end residential units. Banks will continue to lend given high liquidity and property

developers will continue to moderately grow their residential business given an

addressable housing demand especially in the low-end segment.

Danielo Picache

+ 63 2 858 7758

danielo.picache@credit-

suisse.com

Page 23

31 March 2015

Asian Investment Conference 2015 23

Baidu (BIDU.OQ)

Speaker: Sharon Ng, IRD

New News: None

Tone: Positive

Mobile monetisation is behind PC, but trending up supported by more data points from

users on mobile. Click-to-call/click-to-action on mobile shows clear conversion to

advertisers. In 4Q14, mobile revenue accounted for 42% of the total revenue.

LBS is a broad strategy for Baidu. The company will increase spending on the O2O

initiatives in 2015. Baidu Connect had aggregated 600K customer accounts spanning 13

verticals. Number of O2O transactions completed on Baidu has grown 4x YoY. 15% of

movie tickets were sold through Baidu on Girls Day. Baidu is planning to tap into the take

rate model and form a closed transaction loop by leveraging the large traffic on the

platform.

On the cost side, 1Q will be at an elevated level (does not mean peak spending of the

year), with different festivals. PC is still the major part of TAC, such as contextual ad,

which as a percentage of total revenue went up in the past few quarters. TAC as a

percentage of revenue will step up with pace similar to last year. Content cost will be more

than doubled this year mainly from iQiyi. Sales and marketing will also increase due to the

spending on new O2O initiatives.

Bank Central Asia (BBCA.JK)

Speaker: BCA management: Eugene Galbraith, Dy.CEO

New News: None

Tone: Neutral to cautious

Economic Outlook: Not much fiscal stimulus this year but it should pick up next year.

Infrastructure spending unlikely to start this year either. IDR currency depreciation adds to

the nervousness among people.

Even though the overall banking market may not grow as much as it used to, the

interesting action will be at the firm level - winners and losers. Foreign-owned mid-tier

banks having trouble at home (STAN, HSBC, CIMB, etc), so larger banks have

opportunities to pick up market share. Also a couple of state-owned banks have new

management, hence some disruption possible.

Infra Spending: Government is targeting a 40% increase in tax revenues, never seen so

much focus, but money not really available yet. Corporates are spooked, our loans are

below Dec year-end level and unlikely to come up until April.

FDI: For Japanese businesses, Indonesia is strategic and they are active. Koreans have

plans but they have a problem with the labour laws.

Luxury Tax: Not good for the mortgage market, but ok for us. Our origination average is

US$100k and LTV is 65-67%. We launched a new product on Chinese New Year at fixed

8.88% and capped at 9.99%, applications went up 25% in past six weeks. So mortgage

balances should rise, and our market share of 18% may rise.

SME: Our mid-market is not affected by lack of infra lending. Our budget is to grow mid-

market book by 18%, looks ambitious.

Loan Growth: In 2012 we did Rp52 tn in net new lending, 2013 Rp56 tn, 2014 budget was

Rp40 tn, we did only Rp35 tn. 2015 out budget is 45 tn. Highest delta is mid market at

18%, it is going be difficult. Corporate lending target is 15-16%, but so far pipeline is dry.

Mortgage should grow around 5-6% on budget, we turn away more than half of the

applications. We're announcing four wheeler packages, should start growing.

Dick Wei

+ 852 2101 7339

[email protected]

Sanjay Jain

+ 65 6306 0668

sanjay.jain@credit-

suisse.com

Page 24

31 March 2015

Asian Investment Conference 2015 24

Net Interest Margins: No pressure on liquidity as of now. We have cut time dep rate by 25

bp and we are on 7.25% TD mostly. Roughly 25% of our funds are TD, around 75% are

Rp2 bn or less. On lending side, we have cut PLR by 25 bp but eliminated branch

manager's discretion of 25 bp. Also we have cut saving dep rate by 10 bp, so overall

margins should be ok. But can only cut so much - BCA is the bank that loses the most in

falling interest rate environment.

Deposits: Dep/GDP is around 35%, lowest in Asia. C/A deficit is 3% of GDP and solution

lies there. Our LDR target remains 80% (vs 76% actual), we should move to LCR.

Consolidation: Regulators want to go from 118 to 80 bank licences, want BCA to acquire

hence we've budgeted for one. But we want to fire people, not allowed.

Asset Quality: Has not deteriorated. We are not immune to commodity pressures, our

credit risk guy had expected NPLs to rise to 80 bp. What worries us is dollar borrowings,

many of which are undisclosed. The system as a whole also had a good 2014 but there

should be some cracks there.

BASF (BASFn.DE)

Speaker: Magdalena Moll, Head of IR, Amber Usman, Director IR Asia

New News: Yes

Tone: Neutral

2014 review (chemical segment): Performance was slightly lower in 2014 as compared

to previous years. North America had witnessed good cracker margins and cracker

maximisation, Europe had seen stability and Asia was slightly down due to pricing

pressures on caprolactam and isocyanates amid new capacity additions in the region.

2015 outlook: 2015 had seen a good start already with double-digit volume growth from

the agribusiness. Management is cautiously optimistic for BASF’s 2015 outlook, expecting

positive and healthy momentum to continue for US and stable growth from Europe. EBIT

level for all segments will be keeping at similar levels as last year, except for slight

decrease within oil & gas segment (higher volume to offset the drop in oil price) and

chemical segment (due to considerable start-up costs and additional depreciation charges

from the new plants). Management also guided to better cash flow in 2015 due to lower

capex and lower inventory build-up.

Long-term strategy: Management is committed to focus more on the downstream

segment (where they can charge higher margins from customers due to innovations and

tailor-made services) in the long run, and moving away from the cyclical upstream

segments (petrochemicals, i.e., only for supporting the downstream development).

Capex plan: According to management, near-term capex (~US$4 bn in 2015) will be

focused mainly on upstream projects in emerging markets, e.g., MDI plant in Chongqing.

Notable projects in North America include: (1) Refurbishment of existing crackers to use

ethane, propane and butane as feedstock (currently relying on naphtha only); (2) Minority

stake in an ammonia plant (750,000 MT/year) and (3) MMTP plant (still under feasibility

studies) to convert methane into propylene (20% cost advantage).

Kenneth Whee

+852 2101 73196

kenneth.whee@credit-

suisse.com

Page 25

31 March 2015

Asian Investment Conference 2015 25

Bharti Infratel (BHRI.BO)

Speaker: Mr Devender Singh Rawat, CEO

New News: None

Tone: Positive

Expect tenancy to continue to rise as data consumption volumes grow and smaller

operators play catch up on coverage. RJio could be another catalyst for accelerated data

networks rollout

Have initiated talks with regulators in Sri Lanka and Bangladesh for the purchase of tower

assets of Bharti Airtel, but these will be small in size. Overall, management is committed to

increasing leverage levels

Competition in tower industry remains stable and pricing is intact. Capex requirement is

low in the near term due to sufficient capacity installed

The company is exploring opportunities in fibre sharing in future, as well as in building

coverage/ wifi hotspots

BLOOM (BLOOM.PS)

Speaker: Leo Venezuela, Director for Investor Relations

New News: No

Tone: Positive

Operating trend remains robust, specifically in the VIP segment. Bloomberry achieved its

highest quarterly VIP turnover in 4Q14 at P162 bn (HK$2 bn). Management expects this

trend to continue as more junkets sign up. In fact, Sun City, Macau's biggest junket, is

already in the hiring process and will likely begin operations in Solaire as early as April.

The VIP segment, which accounts for 50% of total GGR, is composed of 75% junket VIP

and 25% direct VIP. Management estimates that mainland China, HK/Macau, Korea and

other SEA account for 50%, 10%, 20%, 20% of foreign VIP revenues, respectively.

Solaire has acquired three Korean properties: (1) 12.2 hectares in Muui, (2) the 20.96-

hectare Silmi Island and (3) up to 92% stake in G&L, which operates T.H.E. Hotel and

Vegas Casino in Jeju. These Korean acquisitions have raised concerns regarding funding.

According to management, they are not raising capital for these acquisitions. It is worth

noting that the company has already raised US$125 mn in November 2014 and the US$50

mn in escrow as a requirement of the provisional license will now be released.

Only the VIP junket tables were opened in November 2014 but Phase 1A will also include

an array of non-gaming facilities. A karaoke bar will be opening within the next two weeks.

The 10,000-sqm retail area is expected to open in 2H15. The expansion will also include a

1,400-sqm night club and a 2,800-sqm spa/gym/salon. Lastly, the 6.2 hectares of land

beside the current property will be developed as Phase 2.

Blue Bird (BIRD.JK)

Speaker: Andre Djokosetono (Director), Robert Reimmsei (CFO)

New News: Margins expanding on lower fuel and higher tariff, sharing part of the

margin increase with drivers for better retention, new licenses likely by

the end of this year

Tone: Positive

Fleet size update – 26K BB taxis, 80% in Jakarta. Roughly 50% market share in Jakarta.

Sunil Tirumalai

+ 91 22 6777 3714

sunil.tirumalai@credit-

suisse.com

Patricia Palanca

+63 2 858 7752

patricia.palanca@credit-

suisse.com

Jahanzeb Naseer

+62 21 255 37977

jahanzeb.naseer@credit-

suisse.com

Page 26

31 March 2015

Asian Investment Conference 2015 26

Licenses – 6,200 new licenses still unused. Expected another auction later this year,

which should put to rest worries of future expansion plans.

Drivers – Recruitment is going on aggressively but quality drivers is a challenge. Accept

only 43% of the candidates that apply and about 50% of them are let go in six months

Online booking – There is rising preference, 8,500 bookings per day, 600k downloads.

25% of total bookings. Nearly 45K bookings per day

New tariff – Using the lower band of tariff now. Does that affect the brand? The main

reason is we just had a tariff hike in 2013 so did not want a strong up to 35% increase

again. And usually BB waits a few months before moving to the higher band.

Margins – Effectively an 11% increase in average revenue per can and fuel cost increased

by 7% so have a 5% advantage but passed some of this to the drivers. About half has

been passed on to the drivers. The next tariff level is about 15% higher than the current

tariff. If Blue Bird moves to that level most of that incremental gain will be retained by the

company rather than shared with the drivers (the current tariff increase shared half-half

with drivers).

Growth – Last year saw a squeeze in margin due to the fuel price increase, and the tariff

came in with a lag. 20% expansion in fleet size in the regular taxis, and a 10% increase in

revenue per car. Focused on more second half. While BB raised the payment to the

drivers to keep them incentivized, in 2015 it expects to get 4% increase in net margin.

EBIT margin is also expected to increase 2%.

Concerns – Fuel price and rupiah depreciation. Now the oil price is no longer subsidised

so depends on both the oil price and the rupiah value as it affects the local price.

Are there plans to be an aggregator as we have seen in India? This is an option worth

thinking about, but at this point BB wants to keep the app-driven traffic to themselves.

BTS Group Holdings (BTS.SK)

Speaker: Mr. Surapong Laoha-Unya, Executive Director, Mr. Daniel Ross,

Financial Director, Ms. Sinatta Kiewkhong, Investor Relations Manager

New News: Yes

Tone: Positive

Dividend to remain healthy after FY17: BTS is committed to pay Bt3.5 bn for the FY15

(end Mar 15) and Bt8 bn for FY16 (end-Mar 16), implying a yield of around 7%. 50% of

this payment is coming from recurring income and the rest from existing cash on hand.

Management expects to see at least a healthy dividend yield level of 3.5% from FY17 and

could be higher depending on the potential new mass transit contracts.

Mass transit update: Green line south is now 50% done for construction. O&M contract is

expected to be awarded in 4Q. E&M could start in 3Q. First station could be open by 2016.

The contract awarding will be through a direct negotiation. For green line in the north,

contract awarding is expected in early 2016 with operations from 2019 onward. Light Rail

Transit (LRT) line is waiting the central government's approval. The internal process from

the city government part is done and the bidding will happen within 2015. Management

expects a direct negotiation for this route. Grey line bidding is expected in early 2016. Pink

is likely to be tendering for civil and O&M contracts in 3Q15.

Warayut (Yuth)

Luangmettakul

+ 66 2 614 6214

warayut.luangmettakul@cre

dit-suisse.com

Page 27

31 March 2015

Asian Investment Conference 2015 27

Target six lines: BTS particularly targets three green line extensions; pink, LRT and grey

given some advantage on these routes. These are an MOU on BTS's land plot for depot

construction for the LRT line; some connections and linkages with stations of existing

green line BTS are operating. BTS is expected to bid O&M (long term operations)

contracts of these routes, which could generate 40% EBITDA margin based on the

existing O&M contracts. IRR would be 11-12% and equity IRR should be higher depending

on the leverage level. Warrants and existing cash on hands will be used to finance the

investment.

Increase its media stake: Recently, BTS raised its stake in VGI to 70% last week from

previously 65%. VGI had a tough year but management has full confidence in the long

term business outlook and expects to see double digit growth next year.

Eligible for fare adjustment this year: A bit of fare adjustment is possible given the gap

between the authorised fare and the effective fare. There remains room for the increase

despite the benign inflation situation.

Asset injection to infra fund not in the near term: Some assets could be injected into

the fund but this depends upon the funding requirement from the company and it is

pressed to do that for the time being. BTS may need to do it if there's a lot of mass transit

investments in the future.

Bumi Armada (BUAB.KL)

Speaker: Kenneth Murdoch, CFO; Jonathan Duckett, SVP Corp Affairs

New News: Yes

Tone: Neutral

Despite the significant downturn in O&G, BAB is still seeing some prospects: From ten

FPSO awards last year, they expect five-to-six this year, in West Africa, Mexico and even

one in the North Sea. With plenty of work secured (3 ongoing conversions, more than

competitors), they are not pressured to win contracts at this point; more concerned about

maintaining an attractive risk/reward profile in their project bids, and avoiding

overextending themselves.

Resilience of their FPSO projects due to proximity to production (i.e., cash inflow) and

project economics. Value-add is beyond providing off-balance sheet financing and lower

cost of capital: engineering solutions, project management to complete conversions on

budget and on time.

CFO stressed their (1) conservative approach and focus on steadily improving the risk

reward profile of their individual projects via contractual protection; and (2) intention to

continue focusing on improving shareholder returns rather than planting flags - part of this

will involve reviewing capital allocation in their T&I and OSV segments. OSV segment is

very tough and commoditised but there are also niches there.

A bit more detail was given about the gas project in Europe (FSU in Malta, less than

US$100 mn capex, long-term contract).

Muzhafar Mukhtar

+ 603 2723 2084

muzhafar.mukhtar@credit-

suisse.com

Page 28

31 March 2015

Asian Investment Conference 2015 28

Cheung Kong Infrastructure (1038.HK)

Speaker: Ivan Chan, CIO, and Chris Chan, IR

New News: None

Tone: Positive

The railway leasing business (Eversholt) has recently achieved a good IRR (12.5 percent)

as the industry is highly concentrated. Eversholt has a 28% mkt share. Transaction likely

to be completed by April.

CKI can leverage up with a low gearing ratio, which is a powerful pool for project bidding.

But CKI is also keeping its credit rating in mind as credit agencies tend to look at see-

through gearing, which incorporates the associate debt, but there is no covenant that CKI

cannot go below A-.

Overall CKI remains well positioned with strong balance sheet and wide investment

groups (3 deals done in past 12 months).

Dividend is targeted to increase on an absolute basis, following a strong track record. But

this needs to be balanced with keeping cash for potential acquisitions. This is unlike Power

Assets (6 HK), which has net cash, and the ability to turn cash into growth could fall if

there are no deals in the near term.

China Animal Healthcare (0940.HK)

Speaker: Jinguo Sun, Deputy CEO/Ching Chien Toh, CFO

New News: None

Tone: Positive

Top-line guidance of CAH core business

Management gave a long-term outlook of the animal healthcare pharmaceutical industry.

According to management, the industry growth rate of animal chemical drug will slow

down to 5% YoY, while the animal vaccine segment will maintain strong growth

momentum with expected growth rate at ~15% YoY.

In terms of company’s own business, the future growth driver will be focused on direct

sales of mandatory vaccine, with estimated growth over 100% YoY on top of gross margin

as high as 90%. The in-house innovation of CAH also started to bear fruit this year. As

expected by management, a new vaccine targeting foot and mouth disease will be

approved by SFDA within this year On average, the company’s vaccine business will

deliver sales growth of 30~40% YoY.

Co-operation with Lilly add values

The company has entered into a five-year agreement with Elanco (Eli Lilly's animal

healthcare business division) to co-operate on the following items: (1) Promote registration

and market launch of Lilly’s products in China, (2) Seek technical consultancy from Lilly to

improve product standards, and thus to enhance leading position on certain products, (3)

Utilise Lilly’s distribution network to promote vaccine export business

Further acquisition on Liaoning Yikang

Post the announcement of the acquisition of a 17% equity interest in Yikang, a bird flu

vaccine manufacturer, CAH has striven to further increase its shareholding and aims to

become a controlling shareholder in the future. Management expects to increase its

interest in Yikang to ~25% within 2015 through injection of its advanced suspension

culture technology.

Dave Dai

+852 2101 7358

[email protected]

Iris Wang

+852 2101 7646

iris.wang@credit-

suisse.com

Page 29

31 March 2015

Asian Investment Conference 2015 29

China Gas Holdings (0384.HK)

Speaker: Frank Li, CEO Assistant and Kevin Zhu, CFO

New News: None

Tone: Positive

After the recent city-gate gas price cut, management believes that the next gas price cut

should come within six months, given that oil prices remain weak and the city-gate gas

pricing mechanism is linked to prices of oil products.

The gas dollar margin has been stable for the company over the past few years, currently

at Rmb0.68 per cubic meter.

The company is confident about the gas demand growth in their project cities, given ~40%

of their city projects are pre-mature (Out of its 250 city gas projects, 78 are still under

construction and 23 are in their first-year of operation). Gas price cuts should also

stimulate demand.

For vehicle gas sales, the company will continue to focus on CNG instead of LNG. They

believe CNG is a more mature and profitable market with abundant demand.

The company believes the risk of connection fee being cancelled for their projects is low in

the next few years, given the low penetration rate. The company expects to beat their new

connection target in 2015.

China Lodging (HTHT.OQ)

Speaker: Baonnie Bao, Director of Strategy; Jenny Zhang, CFO; Ida Yu, IR

New News: Yes

Tone: Negative

Accor deal: Anti-trust review is passed. Move on to next stage. Still expect to close the

deal by end FY15.

1Q15: 2M15 same-hotel RevPAR down 5%. March sees the decline shrink.

Strategy focus:

More efficient franchise model - launch of Élan brand to convert existing independent hotel

more efficiently to China Lodging's format. Elan will account for 1/7 of new stores in 2015.

Direct channel - China Lodging continue to offer better price on their own channels (APP,

website)

Mid-scale hotel - Management expects branded hotel to gain market shares from

independent hotels. Will continue to build up mid-scale products and alliance with Accor to

target this segment.

CS view:

Budget hotel is facing fierce competition and soft macro. No signals suggest immediate

recovery.

China Lodging has much higher pipeline of contract hotel (>600) compared to Homeinns

(200) and Jinjiang (230), suggesting a stronger brand value and attractiveness.

China Lodging now has 8-10% of portfolio being mid-scale, higher than Homeinns. With

successful alliance with Accor, China Lodging still has decent potential to dominate in mid-

scale segment in the long run.

Dave Dai

+852 2101 7358

[email protected]

Sophie Chiu

+852 2101 7657

sophie.chiu@credit-

suisse.com

Page 30

31 March 2015

Asian Investment Conference 2015 30

China Resources Cement (1313.HK)

Speaker: Robert Lau, CFO; Elaine Lam, IR director

New News: None

Tone: Neutral

Demand: In 2015, overall China cement demand will likely be flat versus 2014, while

demand in the southern area is expected to increase by 1-3%. The company believes the

infrastructure in GD/GX is still behind eastern China, so there must be some catch-ups.

Supply: The company estimates the effective new supply in 2015 would be 10mnt, or 3-

4%, in GD/GX region. The average utilisation of CRC is 99%, versus peers 84-88%.

Pricing: 1Q15 ASP is hk$50/t lower YoY. The company estimates the price will be flat in

2-3Q and rebound in the 4Q15. The results in 1Q15 will be lower significantly YoY in 1Q15.

But the gap will be narrowed in 2Q and 3Q, and expects higher YoY in 4Q15.

M&A: The lower acquisitions in the past years were mainly due to the internal compliance

issues of the M&A target and the limited limestone resources.

China Resources Power (0836.HK)

Speaker: X. Wang (CFO), Karl Ho (IR), Shenwen Zhang (GM of New Energy)

New News: Yes

Tone: Neutral

About the power reform (guidelines were circulated within the industry over the weekend),

guidelines include opening up the retail business. CRP sees limited impact for their

business in the long term. Compared with Big 5 power groups, CRP is located in

developed regions and the company is interested in participating in the new business with

existing track record in co-generation (power and heat).

More detailed steps should be announced in the future but could take some time to

implement.

Will focus more on renewable energy and cherry-pick coal-fired investments where there

is favourable long-term demand-supply.

CRP is aware of an on-going study of a tariff cut but looking at past, EBITDA margin has

been stable with past tariff cuts offset by weak coal prices.

CRP expects unit fuel cost to drop 1% within 2015 and the drop reflects improving coal

consumption rate.

Utilisation hours are expected to drop to 5,050 hours in 2015 (5,325 in 2014).

18 units (8.59GW) will go through thermal unit upgrade to remain competitive with less

than seven years of payback period but the power plants may get some local government

incentives.

Gary Xu

+86 21 3856 0335

[email protected]

Dave Dai

+852 2101 7358

[email protected]

Page 31

31 March 2015

Asian Investment Conference 2015 31

China Shenhua (1088.HK)

Speaker: Xiaolin Wang (Executive Director and SVP)

New News: None

Tone: Neutral

Shenhua continues to strive in a challenging operating environment, including optimising

production and sales structure, and decelerating capex. Specifically, Shenhua targets to