This report addresses why investors should try to understand the inherent value andpotential GBM Resources Limited (“GBM” or “the Company”) represents.

GBM’s 100% owned Milo Prospect near Cloncurry in far north Queensland is fastbecoming a company making project as the Company moves towards completing aScoping Study in mid CY 2013 and a Preliminary Feasibility Study (PFS) in mid 2013. Asexploration progresses, it is clear that the project is more than a multi commodity IOCG(iron-oxide/copper/gold) deposit. Exploration has delineated sulphide mineralisationcontaining copper (Cu), gold (Au), molybdenum (Mo) and uranium (U) that has beenoverprinted and enveloped by widespread value adding rare earth elements (REE) andyttrium (Y).

Additional shareholder value will soon become apparent once GBM vends the phosphaterights held by its 100% owned Bungalien Phosphate Pty Ltd to joint venture partnerSwift Resources Ltd (“Swift”) (GBM ASX announcement, 16 February 2012). GBM willreceive A$3.3 million for 30% of its phosphate rights in the form of equity in Swift and willundertake an in-specie distribution of the shares to shareholders.

Based on an EV/Cu tonne of approximately A$450 for ASX listed copperexplorers/developers, we anticipate that Cu-REE or IOCG-REE companies should tradeat perhaps a 70-80% discount to reflect the lower recoveries (perhaps 30-40%), highercapital costs (+20-30%) and more limited market for concentrates (ie dominated byChinese smelters). Based on this methodology would translate to a six month share pricetarget of say A$0.35 per Share for GBZ whose Milo Project is essentially likely tocomprise around 30-40% Cu and 60-70% REE by contained value. Speculative Buy.

INVESTMENT CASE Milo IOCG/REE: A Scoping Study and maiden JORC complaint resource statement

due by mid CY 2012 is an upcoming highlight. The initial conceptual explorationtarget of between 30-80 million tonnes of poly-metallic mineralization and REEsgrading 0.8%-1.2% Cu-equivalent has been well and truly exceeded as the maidenInferred JORC resource for the REE mineralization is already 103 million tonnes @760ppm for around 82,500 tonnes of REEYO.

The Milo Project resource has over 1 kilometre of continuous Cu & REEmineralization and is still open-ended to the north and south and at depth. Planneddrilling will be a highlight over the next quarter.

Swift will acquire 100% of the Bungalien Phosphate Project for the phosphate rightsand intends to list on the ASX. GBM shareholders will receive free shares in Swift.

GBM acquired a new tenement from Newcrest Mining (ASX: NCM) that surroundsIvanhoe Australia’s (ASX: IVA) Trekelano Cu-Au mine which extends over 1.2kilometres southwards to the Tick Hill gold mine. The potential will be determinedonce all previous data is assimilated, assessed and targets are generated.

The Bungalien IOCG JV Project’s maiden drilling program at the Bronzewing Boreprospect intersected significant widths of anomalous IOCG style coppermineralization.

At the Mt Morgan Project, a large porphyry Cu/Au system was discovered at theSandy Creek Prospect. This will now be a priority drill target for 2012.

Capital Structure

Sector Materials

Share Price (A$) 0.082

Fully Paid Ordinary Shares (m) 221.6

Opt (ex 20c, exp 30/06/13) (m) 129.5

Market Cap (undil) (A$m) 18.2

Share Price Year H-L (A$) 0.135-0.051

Approx Cash (A$m) 1.5

Directors & Management

Peter Thompson Chairman & MD

Neil Norris Exploration Director

Cameron Switzer Non-Exec Director

Guan Huat Sunny Loh Non-Exec Director

Kevin Hart Company Secretary

Major Shareholders

UOB Kay Hian Private Ltd 16.1%Swift Venture Holdings Ltd 5.0%

Superfine Nominees Pty Ltd 2.8%

Carpentaria Corporation P/L 2.1%

Australian Global Capital 2.0%

Analyst

Andy Comas +61 8 9488 0800

12 Month Share Price Performance

GBM Resources LimitedMaiden Resource due June Quarter at Milo...Phosphate Spinout...Mt Morgans exploration kicks into gear

COMPANY OVERVIEWGBM Resources is a Perth based exploration company with IOCG-type copper and goldprojects with REEs and phosphate in the Mt Isa/Cloncurry district of Queensland, porphyrycopper and gold projects near Rockhampton, Queensland, and copper and gold projects inVictoria.

GBM has a joint venture with Japanese firms Pan Pacific Copper (“PPC”) and MitsuiCorporation (Pan Pacific/Mitsui JV discussed below) via the company Cloncurry Explorationand Development Pty Ltd (“CED”) with a A$55 million farm-in agreement on the BronzewingBore, Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects.

The Bungalien Phosphate JV with Singapore based Swift Venture Holdings Corporation forthe phosphate rights on the Bungalien tenements has proven successful. Swift will nowproceed with acquiring 100% of the rights once certain conditions have been met and isproposing to list on ASX.

EXPLORATION OVERVIEWMilo ProjectThe Milo Project (Figure 1, Figure 2) is the Company’s most advanced exploration project andis located due east of major regional town Mount Isa and just 20 kilometres west of Cloncurryin far northwest Queensland.

The mineralization is hosted in a highly brecciated and altered rock that is generally strikingnorthwest-south and is coincident with magnetic highs within a broader magnetic low anomalythat has been interpreted as a possible buried granite that gave rise to the IOCG & REEmineralization. The REE and yttrium mineralisation (REEY) appears to overprint and envelopethe IOCG style Cu‐Au‐Ag‐Mo‐U‐Co mineralisation. Drilling shows that the mineralization dipsto the east, is possibly fault related, and that higher grade copper mineralization plunges tothe north.

COMPANY OVERVIEWGBM Resources is a Perth based exploration company with IOCG-type copper and goldprojects with REEs and phosphate in the Mt Isa/Cloncurry district of Queensland, porphyrycopper and gold projects near Rockhampton, Queensland, and copper and gold projects inVictoria.

GBM has a joint venture with Japanese firms Pan Pacific Copper (“PPC”) and MitsuiCorporation (Pan Pacific/Mitsui JV discussed below) via the company Cloncurry Explorationand Development Pty Ltd (“CED”) with a A$55 million farm-in agreement on the BronzewingBore, Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects.

The Bungalien Phosphate JV with Singapore based Swift Venture Holdings Corporation forthe phosphate rights on the Bungalien tenements has proven successful. Swift will nowproceed with acquiring 100% of the rights once certain conditions have been met and isproposing to list on ASX.

EXPLORATION OVERVIEWMilo ProjectThe Milo Project (Figure 1, Figure 2) is the Company’s most advanced exploration project andis located due east of major regional town Mount Isa and just 20 kilometres west of Cloncurryin far northwest Queensland.

The mineralization is hosted in a highly brecciated and altered rock that is generally strikingnorthwest-south and is coincident with magnetic highs within a broader magnetic low anomalythat has been interpreted as a possible buried granite that gave rise to the IOCG & REEmineralization. The REE and yttrium mineralisation (REEY) appears to overprint and envelopethe IOCG style Cu‐Au‐Ag‐Mo‐U‐Co mineralisation. Drilling shows that the mineralization dipsto the east, is possibly fault related, and that higher grade copper mineralization plunges tothe north.

COMPANY OVERVIEWGBM Resources is a Perth based exploration company with IOCG-type copper and goldprojects with REEs and phosphate in the Mt Isa/Cloncurry district of Queensland, porphyrycopper and gold projects near Rockhampton, Queensland, and copper and gold projects inVictoria.

GBM has a joint venture with Japanese firms Pan Pacific Copper (“PPC”) and MitsuiCorporation (Pan Pacific/Mitsui JV discussed below) via the company Cloncurry Explorationand Development Pty Ltd (“CED”) with a A$55 million farm-in agreement on the BronzewingBore, Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects.

The Bungalien Phosphate JV with Singapore based Swift Venture Holdings Corporation forthe phosphate rights on the Bungalien tenements has proven successful. Swift will nowproceed with acquiring 100% of the rights once certain conditions have been met and isproposing to list on ASX.

EXPLORATION OVERVIEWMilo ProjectThe Milo Project (Figure 1, Figure 2) is the Company’s most advanced exploration project andis located due east of major regional town Mount Isa and just 20 kilometres west of Cloncurryin far northwest Queensland.

The mineralization is hosted in a highly brecciated and altered rock that is generally strikingnorthwest-south and is coincident with magnetic highs within a broader magnetic low anomalythat has been interpreted as a possible buried granite that gave rise to the IOCG & REEmineralization. The REE and yttrium mineralisation (REEY) appears to overprint and envelopethe IOCG style Cu‐Au‐Ag‐Mo‐U‐Co mineralisation. Drilling shows that the mineralization dipsto the east, is possibly fault related, and that higher grade copper mineralization plunges tothe north.

In December 2011, a six hole diamond drilling program commenced in order to test formineralisation at depth and along strike to the north. These targets were outlined fromprevious geological mapping and anomalous assays returned from the soil sampling program.At the time of writing, only three drill holes have been completed (MIL011, MIL012 andMIL013) (Figure 3).

The good news is that the geology observed in the drill core from these three holes confirmsthat the copper and REEY mineralisation extends over 400 metres further to the north andpositively correlates with the geochemical anomaly (Figure 3). Assay results have only beenreceived to date for MIL011 which returned 124 metres @ 0.5% Cu-equivalent from 82 metreincluding 21 metres @ 1.0% Cu-equivalent together with several zones of REEYmineralisation. As a stand-alone copper resource, the copper grades are on the low side foran economic single commodity mining operation. However, the associated IOCGU mineralogyand REE composition add significant economic value and hence a large tonnage Cu-equivalent grade >0.5% is looking quite robust.

In regard to the REE mineralisation at Milo, assay results suggest that REEs of significanceare light rare earth elements (LREE) Cerium (Ce), Lanthanum (La), Neodymium (Nd) andheavy rare earth elements (HREE) Yttrium (Y), Dysprosium (Dy), and Europium (Eu). I willtouch on the REE significance in the Resource Statement section below.

Drilling to date has delineated over 1 kilometre of continuous Cu and REE mineralizationwhich is interpreted to be up to 200 meters wide. The geochemical anomaly generated fromthe previously reported soil sampling continues north-westerly past drill hole MIL013 for atleast another 500 meters (Figure 3). There are also a number of parallel geochemicalanomalies to the north-west which may be structurally related but have yet to be drill tested.

Given the positive correlation between the geochemical signature in the soil and copper andREEY mineralisation delineated by exploratory drilling, the total strike length of mineralisationcould conceivably extend for up to two kilometres. Future drilling programs should determine ifthis is the case.

In December 2011, a six hole diamond drilling program commenced in order to test formineralisation at depth and along strike to the north. These targets were outlined fromprevious geological mapping and anomalous assays returned from the soil sampling program.At the time of writing, only three drill holes have been completed (MIL011, MIL012 andMIL013) (Figure 3).

The good news is that the geology observed in the drill core from these three holes confirmsthat the copper and REEY mineralisation extends over 400 metres further to the north andpositively correlates with the geochemical anomaly (Figure 3). Assay results have only beenreceived to date for MIL011 which returned 124 metres @ 0.5% Cu-equivalent from 82 metreincluding 21 metres @ 1.0% Cu-equivalent together with several zones of REEYmineralisation. As a stand-alone copper resource, the copper grades are on the low side foran economic single commodity mining operation. However, the associated IOCGU mineralogyand REE composition add significant economic value and hence a large tonnage Cu-equivalent grade >0.5% is looking quite robust.

In regard to the REE mineralisation at Milo, assay results suggest that REEs of significanceare light rare earth elements (LREE) Cerium (Ce), Lanthanum (La), Neodymium (Nd) andheavy rare earth elements (HREE) Yttrium (Y), Dysprosium (Dy), and Europium (Eu). I willtouch on the REE significance in the Resource Statement section below.

Drilling to date has delineated over 1 kilometre of continuous Cu and REE mineralizationwhich is interpreted to be up to 200 meters wide. The geochemical anomaly generated fromthe previously reported soil sampling continues north-westerly past drill hole MIL013 for atleast another 500 meters (Figure 3). There are also a number of parallel geochemicalanomalies to the north-west which may be structurally related but have yet to be drill tested.

Given the positive correlation between the geochemical signature in the soil and copper andREEY mineralisation delineated by exploratory drilling, the total strike length of mineralisationcould conceivably extend for up to two kilometres. Future drilling programs should determine ifthis is the case.

In December 2011, a six hole diamond drilling program commenced in order to test formineralisation at depth and along strike to the north. These targets were outlined fromprevious geological mapping and anomalous assays returned from the soil sampling program.At the time of writing, only three drill holes have been completed (MIL011, MIL012 andMIL013) (Figure 3).

The good news is that the geology observed in the drill core from these three holes confirmsthat the copper and REEY mineralisation extends over 400 metres further to the north andpositively correlates with the geochemical anomaly (Figure 3). Assay results have only beenreceived to date for MIL011 which returned 124 metres @ 0.5% Cu-equivalent from 82 metreincluding 21 metres @ 1.0% Cu-equivalent together with several zones of REEYmineralisation. As a stand-alone copper resource, the copper grades are on the low side foran economic single commodity mining operation. However, the associated IOCGU mineralogyand REE composition add significant economic value and hence a large tonnage Cu-equivalent grade >0.5% is looking quite robust.

In regard to the REE mineralisation at Milo, assay results suggest that REEs of significanceare light rare earth elements (LREE) Cerium (Ce), Lanthanum (La), Neodymium (Nd) andheavy rare earth elements (HREE) Yttrium (Y), Dysprosium (Dy), and Europium (Eu). I willtouch on the REE significance in the Resource Statement section below.

Drilling to date has delineated over 1 kilometre of continuous Cu and REE mineralizationwhich is interpreted to be up to 200 meters wide. The geochemical anomaly generated fromthe previously reported soil sampling continues north-westerly past drill hole MIL013 for atleast another 500 meters (Figure 3). There are also a number of parallel geochemicalanomalies to the north-west which may be structurally related but have yet to be drill tested.

Given the positive correlation between the geochemical signature in the soil and copper andREEY mineralisation delineated by exploratory drilling, the total strike length of mineralisationcould conceivably extend for up to two kilometres. Future drilling programs should determine ifthis is the case.

Essentially, the Milo mineralisation is still open-ended and further drilling will be required todetermine the extent of mineralisation both along strike and at depth. In-fill drilling will also berequired in the future as the project develops in order to upgrade the classification of theresource under the JORC reporting standards.

FIGURE 3: Milo Projectdrill location mapoverlying the soilanomaly and magneticimage (source: GBMResources ASXAnnouncement 29th

February 2012).

The strike length of themineralisation couldextend for up to twokilometres.

Essentially, the Milo mineralisation is still open-ended and further drilling will be required todetermine the extent of mineralisation both along strike and at depth. In-fill drilling will also berequired in the future as the project develops in order to upgrade the classification of theresource under the JORC reporting standards.

FIGURE 3: Milo Projectdrill location mapoverlying the soilanomaly and magneticimage (source: GBMResources ASXAnnouncement 29th

February 2012).

The strike length of themineralisation couldextend for up to twokilometres.

Essentially, the Milo mineralisation is still open-ended and further drilling will be required todetermine the extent of mineralisation both along strike and at depth. In-fill drilling will also berequired in the future as the project develops in order to upgrade the classification of theresource under the JORC reporting standards.

FIGURE 3: Milo Projectdrill location mapoverlying the soilanomaly and magneticimage (source: GBMResources ASXAnnouncement 29th

February 2012).

The strike length of themineralisation couldextend for up to twokilometres.

During the last quarter, GBM announced a maiden Inferred JORC resource (NI43-101equivalent) for the REEY component of the Milo Project of 103 million tonnes at 760ppm forapproximately 82,500 tonnes of TREEYO based on a 400ppm cut‐off grade of the data used(Table 1). A maiden JORC resource for the IOCG polymetallic copper mineralisation and thephosphate and magnetite content is pending. The total potential economic value of theresource will then become apparent and may well revalue the share price as a result.

The traditional classification of REEs into predominately light rare earth elements (LREE)and/or heavy rare earth elements (HREE) is not necessarily important, but the presence ofHREEs and a recent category known as the critical rare earth oxides (CREO) are important asthey are considered to be the more valuable REEs in the foreseeable future.

In 2010, the inaugural Critical Materials Strategy report prepared by the U.S. Department ofEnergy (DOE) defined which REEs were in critical supply based on the supply and demandrisk to clean energy applications. The annual update was released in December 2011 and theDOE declared that the supply of dysprosium, terbium, europium, neodymium and yttrium willbe the CREOs essential to clean energy applications over the next 15 years (Figure 4).

Using the published inferred tonnages of REE oxides (REEO) in the JORC resourcestatement (Table 1), the contained REEs are predominately Ce-La-Nd with additional Y-Pr-Sm-Dy mineralogy. On this basis, the Milo TREEYO resource has a hybrid mostly LREEcomposition with a significant proportion of the CREOs. The assay results to date show thataround 21% of the total REE mineralisation consists of the CREOs neodymium, europium,yttrium and dysprosium. That may be so, but what will the recovery rates be?

During the last quarter, GBM announced a maiden Inferred JORC resource (NI43-101equivalent) for the REEY component of the Milo Project of 103 million tonnes at 760ppm forapproximately 82,500 tonnes of TREEYO based on a 400ppm cut‐off grade of the data used(Table 1). A maiden JORC resource for the IOCG polymetallic copper mineralisation and thephosphate and magnetite content is pending. The total potential economic value of theresource will then become apparent and may well revalue the share price as a result.

The traditional classification of REEs into predominately light rare earth elements (LREE)and/or heavy rare earth elements (HREE) is not necessarily important, but the presence ofHREEs and a recent category known as the critical rare earth oxides (CREO) are important asthey are considered to be the more valuable REEs in the foreseeable future.

In 2010, the inaugural Critical Materials Strategy report prepared by the U.S. Department ofEnergy (DOE) defined which REEs were in critical supply based on the supply and demandrisk to clean energy applications. The annual update was released in December 2011 and theDOE declared that the supply of dysprosium, terbium, europium, neodymium and yttrium willbe the CREOs essential to clean energy applications over the next 15 years (Figure 4).

Using the published inferred tonnages of REE oxides (REEO) in the JORC resourcestatement (Table 1), the contained REEs are predominately Ce-La-Nd with additional Y-Pr-Sm-Dy mineralogy. On this basis, the Milo TREEYO resource has a hybrid mostly LREEcomposition with a significant proportion of the CREOs. The assay results to date show thataround 21% of the total REE mineralisation consists of the CREOs neodymium, europium,yttrium and dysprosium. That may be so, but what will the recovery rates be?

During the last quarter, GBM announced a maiden Inferred JORC resource (NI43-101equivalent) for the REEY component of the Milo Project of 103 million tonnes at 760ppm forapproximately 82,500 tonnes of TREEYO based on a 400ppm cut‐off grade of the data used(Table 1). A maiden JORC resource for the IOCG polymetallic copper mineralisation and thephosphate and magnetite content is pending. The total potential economic value of theresource will then become apparent and may well revalue the share price as a result.

The traditional classification of REEs into predominately light rare earth elements (LREE)and/or heavy rare earth elements (HREE) is not necessarily important, but the presence ofHREEs and a recent category known as the critical rare earth oxides (CREO) are important asthey are considered to be the more valuable REEs in the foreseeable future.

In 2010, the inaugural Critical Materials Strategy report prepared by the U.S. Department ofEnergy (DOE) defined which REEs were in critical supply based on the supply and demandrisk to clean energy applications. The annual update was released in December 2011 and theDOE declared that the supply of dysprosium, terbium, europium, neodymium and yttrium willbe the CREOs essential to clean energy applications over the next 15 years (Figure 4).

Using the published inferred tonnages of REE oxides (REEO) in the JORC resourcestatement (Table 1), the contained REEs are predominately Ce-La-Nd with additional Y-Pr-Sm-Dy mineralogy. On this basis, the Milo TREEYO resource has a hybrid mostly LREEcomposition with a significant proportion of the CREOs. The assay results to date show thataround 21% of the total REE mineralisation consists of the CREOs neodymium, europium,yttrium and dysprosium. That may be so, but what will the recovery rates be?

The mineralogical composition, metallurgical, processing and recovery tests have yet to becompleted, however the results of initial test work suggests that between 30% and 70% ofindividual REEs may be recoverable. Ongoing testing and the upcoming scoping study willclarify the recovery issue.

As exploratory and infill drilling of the resource is incomplete both along strike and at depth itis conceivable that the total tonnage and grade may increase, particularly to the north.Geological modelling of all the current data suggests that the cut-off grade will be an importantvariable in the economics of the resource. Naturally, by using a lower cut‐off grade the totaltonnage generally increases and conversely, by using a higher cut-off grade, the tonnage willdecrease. The Scoping Study will however provide a clearer understanding of what grade andtonnage will support a viable mining operation.

Metallurgical Test Work

Metallurgical test work was initiated in April 2011 on the poly-metallic mineralisation prior tothe discovery of the REE mineralisation in 2H 2011. Since that time, it has been demonstratedthat a copper/gold/molybdenite concentrate, a low grade gold concentrate for cyanidation, andtailings for uranium leaching can be economically extracted. Recoveries of up to 80% werereported for Cu, Au, Ag, Mo, and over 90% of the uranium. The Co, magnetite and phosphaterecoveries will be reported as part of the scoping study by mid CY 2012.

Identification of the minerals hosting the REEs is underway and initial test-work indicates thatmineralisation is hosted by apatite and a range of carbonate minerals. Apatite is a phosphategroup mineral that yttrium can be found in and initial flotation test work has indicated thataround 30% of the TREEYOs can be recovered as an apatite concentrate using traditionalflotation techniques. The relationship of the REEs to the poly-metallic mineralization stillwarrants further investigation.

SCOPING STUDYA Scoping study has been in progress since mid-2011 and is expected to be completed bymid-2012. Mining One Pty Ltd will manage the study that will address the parameters that willdetermine whether the Milo Project has the economic viability to proceed to a mining scenario.

The technical hurdles to be addressed are summarized as follows:

Maiden JORC resource statement

Metallurgical test results on the recovery of cobalt, magnetite & phosphate

Metallurgical test work on the rare earths to produce a saleable concentrate

Metallurgical test work on the recovery of IOCG metals

Potential pilot plant design

Potential pit design

Resource modeling e.g. optimal cut-off grades and tonnage

Project economics modeling to demonstrate commercial viability

In tandem with the Scoping Study, the following exploration still needs to be completed:

Geological mapping and extension of the soil sampling to test for extensions of Cuand REE soil anomalies.

Infill resource drilling to increase the level of confidence in the data to a JORCcompliant category above inferred status.

Further exploration drilling to define the northern, western and depth extremities ofthe mineralisation.

On the completion of the scoping study, and assuming a sucessful outcome, a PreliminaryFeasibility Study (PFS) will be the next step in advancing the Milo Project.

Around 30% of theTREEYOs can be recoveredas an apatite concentrate.

GBM entered into a farm-in agreement with Pan Pacific Copper (“PPC”) and MitsuiCorporation (“MC”) via their co‐established Australian company Cloncurry Exploration andDevelopment Pty Ltd (“CED”) in April 2011. The farm-in agreement is on the Bungalien,Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects (Figure 5).

CED can earn up to a 90% interest by spending A$55 million on the exploration anddevelopment of the IOCG style projects over a minimum six year period. GBM will retain afree carried interest of 10% through to the completion of a Bankable Feasibility Study.

Bungalien IOCG Project

The PPC/MC JV covers exploration of basement lithologies for IOCG style mineralization andtargets strong magnetic anomalies at the Bronzewing Bore, Malbon2 and Horse CreekProspects. Geophysics is an important exploration tool to generate targets as the project areais covered by 100-500 meters of sediments. Three diamond drill holes have been completedat the Bronzewing Bore Prospect and all holes have intersected broad widths (>100 meters) ofanomalous albeit low grade copper. The chalcopyrite is associated with magnetite +/- chloriteand carbonate alteration.

Limited deep drilling to date at the Bungalien projects has intersected significant widths ofanomalous IOCG style mineralization which is noteworthy given the dearth of any priorexploration. It is obvious that there has been a widespread mineralizing event but narrowingthe search down to a higher grade core is the result I’d like to see. Future drilling will defineeach project’s potential.

Talawanta-Grassy Bore

Coincident gravity and magnetic highs are the conceptual targets at this typical IOCG project.Diamond drill hole TGD003 was completed at Talawanta however only low grade copper wasintersected. Further drilling has been deferred until landholder negotiations have beenfinalised.

GBM entered into a farm-in agreement with Pan Pacific Copper (“PPC”) and MitsuiCorporation (“MC”) via their co‐established Australian company Cloncurry Exploration andDevelopment Pty Ltd (“CED”) in April 2011. The farm-in agreement is on the Bungalien,Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects (Figure 5).

CED can earn up to a 90% interest by spending A$55 million on the exploration anddevelopment of the IOCG style projects over a minimum six year period. GBM will retain afree carried interest of 10% through to the completion of a Bankable Feasibility Study.

Bungalien IOCG Project

The PPC/MC JV covers exploration of basement lithologies for IOCG style mineralization andtargets strong magnetic anomalies at the Bronzewing Bore, Malbon2 and Horse CreekProspects. Geophysics is an important exploration tool to generate targets as the project areais covered by 100-500 meters of sediments. Three diamond drill holes have been completedat the Bronzewing Bore Prospect and all holes have intersected broad widths (>100 meters) ofanomalous albeit low grade copper. The chalcopyrite is associated with magnetite +/- chloriteand carbonate alteration.

Limited deep drilling to date at the Bungalien projects has intersected significant widths ofanomalous IOCG style mineralization which is noteworthy given the dearth of any priorexploration. It is obvious that there has been a widespread mineralizing event but narrowingthe search down to a higher grade core is the result I’d like to see. Future drilling will defineeach project’s potential.

Talawanta-Grassy Bore

Coincident gravity and magnetic highs are the conceptual targets at this typical IOCG project.Diamond drill hole TGD003 was completed at Talawanta however only low grade copper wasintersected. Further drilling has been deferred until landholder negotiations have beenfinalised.

GBM entered into a farm-in agreement with Pan Pacific Copper (“PPC”) and MitsuiCorporation (“MC”) via their co‐established Australian company Cloncurry Exploration andDevelopment Pty Ltd (“CED”) in April 2011. The farm-in agreement is on the Bungalien,Talawanta-Grassy Bore, Chumvale Breccia and Mount Margaret Projects (Figure 5).

CED can earn up to a 90% interest by spending A$55 million on the exploration anddevelopment of the IOCG style projects over a minimum six year period. GBM will retain afree carried interest of 10% through to the completion of a Bankable Feasibility Study.

Bungalien IOCG Project

The PPC/MC JV covers exploration of basement lithologies for IOCG style mineralization andtargets strong magnetic anomalies at the Bronzewing Bore, Malbon2 and Horse CreekProspects. Geophysics is an important exploration tool to generate targets as the project areais covered by 100-500 meters of sediments. Three diamond drill holes have been completedat the Bronzewing Bore Prospect and all holes have intersected broad widths (>100 meters) ofanomalous albeit low grade copper. The chalcopyrite is associated with magnetite +/- chloriteand carbonate alteration.

Limited deep drilling to date at the Bungalien projects has intersected significant widths ofanomalous IOCG style mineralization which is noteworthy given the dearth of any priorexploration. It is obvious that there has been a widespread mineralizing event but narrowingthe search down to a higher grade core is the result I’d like to see. Future drilling will defineeach project’s potential.

Talawanta-Grassy Bore

Coincident gravity and magnetic highs are the conceptual targets at this typical IOCG project.Diamond drill hole TGD003 was completed at Talawanta however only low grade copper wasintersected. Further drilling has been deferred until landholder negotiations have beenfinalised.

The Chumvale Breccia is a five kilometer by one kilometer target. Two drill holes have beencompleted and assay results are pending.

Mount Margaret Projects

These tenements are prospective for deep basement lithology IOCG style mineralizationsimilar to the nearby Ernest Henry Mine. Very little work has been carried out on thetenements by GBM however a Squitem geophysical survey was conducted over the projectarea during the December Quarter 2011. The data is still being interpreted in order togenerate prospective drilling targets in 2012.

Bungalien Phosphate Project

The initial public offer (IPO) by Swift is expected to be for up to 25 million fully paid ordinaryshares at an issue price of 20 cents each to raise up to A$5 million. Swift is seeking to belisted on ASX by mid-2012 however if it is not admitted to the official list then SVHC andGBM’s interests in the phosphate rights will revert to an unincorporated joint venture in whichSVHC’s interest will be 70% and GBM’s interest 30%.

Mayfield Project

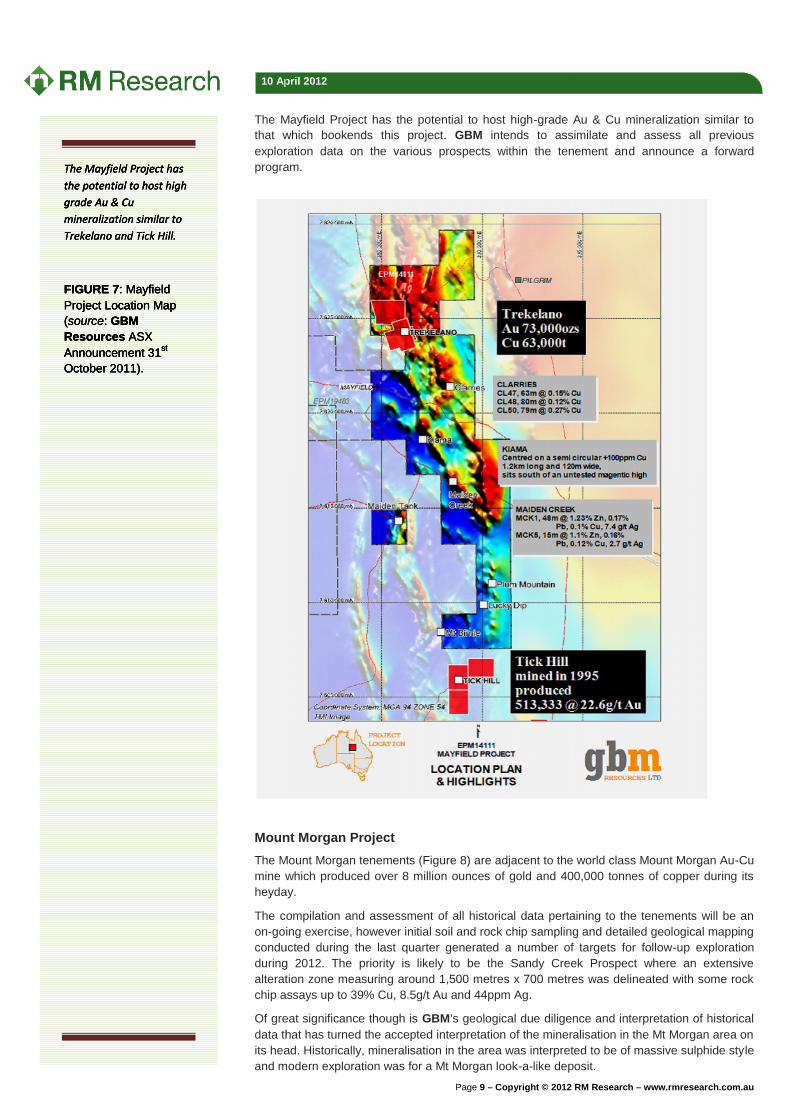

Just as GBM divests itself of the Bungalien Phosphate Project, it has reached agreement withNewcrest Operations Limited (ASX: NCM) to acquire a highly prospective ExplorationPermit (EPM1411) that is just west of the Bungalien tenements (Figure 5). The MayfieldProject (Figure 7)as it will be known, completely surrounds the Trekelano copper mine whichis owned by Ivanhoe Australia (ASX: IVA) and extends around 24 kilometres southwards tojust north of the Tick Hill gold mine (Figure 7).

The significance of this acquisition is that the Trekelano copper mine is a high grade copperand gold deposit that IVA is drilling and reporting exceptional high grade copper intersections.

The Tick Hill gold mine (currently owned by Xstrata) was a high-grade gold producer that from1991-1995 produced 513,333 ounces of gold at a head grade of 22.6 g/t gold from both openpit and underground operations (DRX ASX announcement 4 Sept 2009).

The Bungalien Phosphate Project(Figure 6) is a JV with Singaporebased Swift Venture HoldingsCorporation (“SVHC”). SVHC’swholly owned subsidiary SwiftResources Limited (“Swift”) hasconditionally agreed to acquire100% of the JV’s phosphate rightson the successful listing of Swift onthe Australian Stock Exchange(ASX).

Assuming all the conditionsprecedent are fulfilled, GBM willreceive 16.5 million fully paid Swiftshares @ 20 cents each for a totalof A$3.30 million and, subject toShareholder Approval, willdistribute the Shares in specie toGBM shareholders. It is envisagedthat GBM shareholders will receiveone Swift share for every 15 GBMShares held on the record date

The Chumvale Breccia is a five kilometer by one kilometer target. Two drill holes have beencompleted and assay results are pending.

Mount Margaret Projects

These tenements are prospective for deep basement lithology IOCG style mineralizationsimilar to the nearby Ernest Henry Mine. Very little work has been carried out on thetenements by GBM however a Squitem geophysical survey was conducted over the projectarea during the December Quarter 2011. The data is still being interpreted in order togenerate prospective drilling targets in 2012.

Bungalien Phosphate Project

The initial public offer (IPO) by Swift is expected to be for up to 25 million fully paid ordinaryshares at an issue price of 20 cents each to raise up to A$5 million. Swift is seeking to belisted on ASX by mid-2012 however if it is not admitted to the official list then SVHC andGBM’s interests in the phosphate rights will revert to an unincorporated joint venture in whichSVHC’s interest will be 70% and GBM’s interest 30%.

Mayfield Project

Just as GBM divests itself of the Bungalien Phosphate Project, it has reached agreement withNewcrest Operations Limited (ASX: NCM) to acquire a highly prospective ExplorationPermit (EPM1411) that is just west of the Bungalien tenements (Figure 5). The MayfieldProject (Figure 7)as it will be known, completely surrounds the Trekelano copper mine whichis owned by Ivanhoe Australia (ASX: IVA) and extends around 24 kilometres southwards tojust north of the Tick Hill gold mine (Figure 7).

The significance of this acquisition is that the Trekelano copper mine is a high grade copperand gold deposit that IVA is drilling and reporting exceptional high grade copper intersections.

The Tick Hill gold mine (currently owned by Xstrata) was a high-grade gold producer that from1991-1995 produced 513,333 ounces of gold at a head grade of 22.6 g/t gold from both openpit and underground operations (DRX ASX announcement 4 Sept 2009).

The Bungalien Phosphate Project(Figure 6) is a JV with Singaporebased Swift Venture HoldingsCorporation (“SVHC”). SVHC’swholly owned subsidiary SwiftResources Limited (“Swift”) hasconditionally agreed to acquire100% of the JV’s phosphate rightson the successful listing of Swift onthe Australian Stock Exchange(ASX).

Assuming all the conditionsprecedent are fulfilled, GBM willreceive 16.5 million fully paid Swiftshares @ 20 cents each for a totalof A$3.30 million and, subject toShareholder Approval, willdistribute the Shares in specie toGBM shareholders. It is envisagedthat GBM shareholders will receiveone Swift share for every 15 GBMShares held on the record date

The Chumvale Breccia is a five kilometer by one kilometer target. Two drill holes have beencompleted and assay results are pending.

Mount Margaret Projects

These tenements are prospective for deep basement lithology IOCG style mineralizationsimilar to the nearby Ernest Henry Mine. Very little work has been carried out on thetenements by GBM however a Squitem geophysical survey was conducted over the projectarea during the December Quarter 2011. The data is still being interpreted in order togenerate prospective drilling targets in 2012.

Bungalien Phosphate Project

The initial public offer (IPO) by Swift is expected to be for up to 25 million fully paid ordinaryshares at an issue price of 20 cents each to raise up to A$5 million. Swift is seeking to belisted on ASX by mid-2012 however if it is not admitted to the official list then SVHC andGBM’s interests in the phosphate rights will revert to an unincorporated joint venture in whichSVHC’s interest will be 70% and GBM’s interest 30%.

Mayfield Project

Just as GBM divests itself of the Bungalien Phosphate Project, it has reached agreement withNewcrest Operations Limited (ASX: NCM) to acquire a highly prospective ExplorationPermit (EPM1411) that is just west of the Bungalien tenements (Figure 5). The MayfieldProject (Figure 7)as it will be known, completely surrounds the Trekelano copper mine whichis owned by Ivanhoe Australia (ASX: IVA) and extends around 24 kilometres southwards tojust north of the Tick Hill gold mine (Figure 7).

The significance of this acquisition is that the Trekelano copper mine is a high grade copperand gold deposit that IVA is drilling and reporting exceptional high grade copper intersections.

The Tick Hill gold mine (currently owned by Xstrata) was a high-grade gold producer that from1991-1995 produced 513,333 ounces of gold at a head grade of 22.6 g/t gold from both openpit and underground operations (DRX ASX announcement 4 Sept 2009).

The Bungalien Phosphate Project(Figure 6) is a JV with Singaporebased Swift Venture HoldingsCorporation (“SVHC”). SVHC’swholly owned subsidiary SwiftResources Limited (“Swift”) hasconditionally agreed to acquire100% of the JV’s phosphate rightson the successful listing of Swift onthe Australian Stock Exchange(ASX).

Assuming all the conditionsprecedent are fulfilled, GBM willreceive 16.5 million fully paid Swiftshares @ 20 cents each for a totalof A$3.30 million and, subject toShareholder Approval, willdistribute the Shares in specie toGBM shareholders. It is envisagedthat GBM shareholders will receiveone Swift share for every 15 GBMShares held on the record date

The Mayfield Project has the potential to host high-grade Au & Cu mineralization similar tothat which bookends this project. GBM intends to assimilate and assess all previousexploration data on the various prospects within the tenement and announce a forwardprogram.

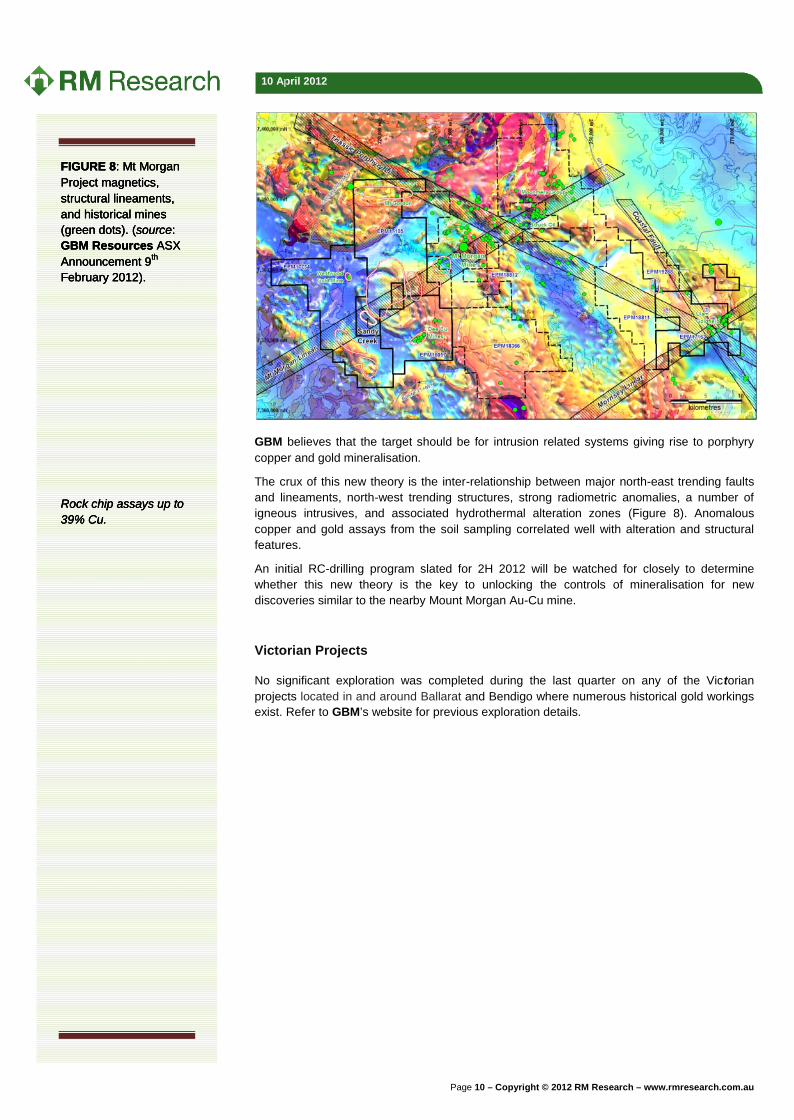

Mount Morgan ProjectThe Mount Morgan tenements (Figure 8) are adjacent to the world class Mount Morgan Au-Cumine which produced over 8 million ounces of gold and 400,000 tonnes of copper during itsheyday.

The compilation and assessment of all historical data pertaining to the tenements will be anon-going exercise, however initial soil and rock chip sampling and detailed geological mappingconducted during the last quarter generated a number of targets for follow-up explorationduring 2012. The priority is likely to be the Sandy Creek Prospect where an extensivealteration zone measuring around 1,500 metres x 700 metres was delineated with some rockchip assays up to 39% Cu, 8.5g/t Au and 44ppm Ag.

Of great significance though is GBM’s geological due diligence and interpretation of historicaldata that has turned the accepted interpretation of the mineralisation in the Mt Morgan area onits head. Historically, mineralisation in the area was interpreted to be of massive sulphide styleand modern exploration was for a Mt Morgan look-a-like deposit.

The Mayfield Project hasthe potential to host highgrade Au & Cumineralization similar toTrekelano and Tick Hill.

The Mayfield Project has the potential to host high-grade Au & Cu mineralization similar tothat which bookends this project. GBM intends to assimilate and assess all previousexploration data on the various prospects within the tenement and announce a forwardprogram.

Mount Morgan ProjectThe Mount Morgan tenements (Figure 8) are adjacent to the world class Mount Morgan Au-Cumine which produced over 8 million ounces of gold and 400,000 tonnes of copper during itsheyday.

The compilation and assessment of all historical data pertaining to the tenements will be anon-going exercise, however initial soil and rock chip sampling and detailed geological mappingconducted during the last quarter generated a number of targets for follow-up explorationduring 2012. The priority is likely to be the Sandy Creek Prospect where an extensivealteration zone measuring around 1,500 metres x 700 metres was delineated with some rockchip assays up to 39% Cu, 8.5g/t Au and 44ppm Ag.

Of great significance though is GBM’s geological due diligence and interpretation of historicaldata that has turned the accepted interpretation of the mineralisation in the Mt Morgan area onits head. Historically, mineralisation in the area was interpreted to be of massive sulphide styleand modern exploration was for a Mt Morgan look-a-like deposit.

The Mayfield Project hasthe potential to host highgrade Au & Cumineralization similar toTrekelano and Tick Hill.

The Mayfield Project has the potential to host high-grade Au & Cu mineralization similar tothat which bookends this project. GBM intends to assimilate and assess all previousexploration data on the various prospects within the tenement and announce a forwardprogram.

Mount Morgan ProjectThe Mount Morgan tenements (Figure 8) are adjacent to the world class Mount Morgan Au-Cumine which produced over 8 million ounces of gold and 400,000 tonnes of copper during itsheyday.

The compilation and assessment of all historical data pertaining to the tenements will be anon-going exercise, however initial soil and rock chip sampling and detailed geological mappingconducted during the last quarter generated a number of targets for follow-up explorationduring 2012. The priority is likely to be the Sandy Creek Prospect where an extensivealteration zone measuring around 1,500 metres x 700 metres was delineated with some rockchip assays up to 39% Cu, 8.5g/t Au and 44ppm Ag.

Of great significance though is GBM’s geological due diligence and interpretation of historicaldata that has turned the accepted interpretation of the mineralisation in the Mt Morgan area onits head. Historically, mineralisation in the area was interpreted to be of massive sulphide styleand modern exploration was for a Mt Morgan look-a-like deposit.

The Mayfield Project hasthe potential to host highgrade Au & Cumineralization similar toTrekelano and Tick Hill.

GBM believes that the target should be for intrusion related systems giving rise to porphyrycopper and gold mineralisation.

The crux of this new theory is the inter-relationship between major north-east trending faultsand lineaments, north-west trending structures, strong radiometric anomalies, a number ofigneous intrusives, and associated hydrothermal alteration zones (Figure 8). Anomalouscopper and gold assays from the soil sampling correlated well with alteration and structuralfeatures.

An initial RC-drilling program slated for 2H 2012 will be watched for closely to determinewhether this new theory is the key to unlocking the controls of mineralisation for newdiscoveries similar to the nearby Mount Morgan Au-Cu mine.

Victorian Projects

No significant exploration was completed during the last quarter on any of the Victorianprojects located in and around Ballarat and Bendigo where numerous historical gold workingsexist. Refer to GBM’s website for previous exploration details.

GBM believes that the target should be for intrusion related systems giving rise to porphyrycopper and gold mineralisation.

The crux of this new theory is the inter-relationship between major north-east trending faultsand lineaments, north-west trending structures, strong radiometric anomalies, a number ofigneous intrusives, and associated hydrothermal alteration zones (Figure 8). Anomalouscopper and gold assays from the soil sampling correlated well with alteration and structuralfeatures.

An initial RC-drilling program slated for 2H 2012 will be watched for closely to determinewhether this new theory is the key to unlocking the controls of mineralisation for newdiscoveries similar to the nearby Mount Morgan Au-Cu mine.

Victorian Projects

No significant exploration was completed during the last quarter on any of the Victorianprojects located in and around Ballarat and Bendigo where numerous historical gold workingsexist. Refer to GBM’s website for previous exploration details.

GBM believes that the target should be for intrusion related systems giving rise to porphyrycopper and gold mineralisation.

The crux of this new theory is the inter-relationship between major north-east trending faultsand lineaments, north-west trending structures, strong radiometric anomalies, a number ofigneous intrusives, and associated hydrothermal alteration zones (Figure 8). Anomalouscopper and gold assays from the soil sampling correlated well with alteration and structuralfeatures.

An initial RC-drilling program slated for 2H 2012 will be watched for closely to determinewhether this new theory is the key to unlocking the controls of mineralisation for newdiscoveries similar to the nearby Mount Morgan Au-Cu mine.

Victorian Projects

No significant exploration was completed during the last quarter on any of the Victorianprojects located in and around Ballarat and Bendigo where numerous historical gold workingsexist. Refer to GBM’s website for previous exploration details.

PEER COMPARISON AND ESTIMATE OF VALUEIn an attempt to peg the performance of GBM against some of its peers and determine therelative value it soon became obvious that any comparison would be a challenge. Do Icompare GBM with peers in the Cloncurry district exploring for IOCG-type copper deposits orwider afield with REE explorers? Not only that, GBM is more than just the Milo Project and anenterprise valuation (EV) based on the Milo resource alone would not be representative of theadditional inherent value that extends to GBM’s other projects.

Directly comparable small market capitalisation (market cap) peers were not readily apparentso instead I have distilled a blend of predominately REE explorers together with some of theCloncurry district’s IOCG/REE explorers. As a REE explorer, GBM‘s peers with a market capof less than A$100 million would include Northern Minerals (ASX: NTU), TUC Resources(ASX: TUC), Hastings Rare Metals (ASX: HAS) (see RM Research, Hastings Rare MetalsLimited, 6 February 2012), Kimberley Rare Earths (ASX: KRE), and Krucible Resources(ASX: KRB). Junior Cu-Au explorers in the Cloncurry district would include Exco Resources(ASX: EXS), Chinalco Yunnan Copper Resources (ASX: CYU), Queensland Mining Corp(ASX: QMN), Goldsearch (ASX: GSE), and Paradigm Metals (ASX: PDM). The currentmarket caps of these companies are shown in Figure 9.

Obviously, the larger explorers and miners in the district such as Cudeco (ASX: CDU) havemuch larger market caps and EVs than GBM (Figure 9).

CYU’s Cloncurry district projects are similar in style to GBM’s Milo project in so far as the Cu-Co-Au mineralization has been overprinted in places by late stage uranium +/- REEmineralization. The light rare earth elements (LREE) cerium, lanthanum and neodymium makeup around 95% of the TREEYO mineralisation with a general dearth of the higher valueHREEs and CREOs. The CREO content of the Milo project is currently around 21%.

QMN has similar style Cu mineralisation to GBM’s Milo Project and the JORC resource for itsprojects in the district currently tallies to a much smaller total resource of around 36 Mt hencethe lower EV (Figure 10).

84.6

64.1

28.623.6

18.8 18.915.7

10.5 9.8 7.31.3

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

NTU EXS CYU TUC GBZ QMN HAS KRE GSE KRB PDM

ASX ASX ASX ASX ASX ASX ASX ASX ASX ASX ASX

A$ M

illio

n

Explorer'sMarket Capitalisation

REE ExplorerIOCG/REE Explorer

Our peer analysis includesboth REE and IOCG/REEExplorers

EXS’s Cloncurry/Mt. Isa district projects cover over 2,900 km2, a vast areal extent of highlyprospective ground with the majority of the projects being Cu/Au exploration projects. Theyalso have a 50/50 JV with PDM on the Toolebuc REE Project (similar in style to GBM’s MiloProject) together with a number of other JV projects with Xstrata, BHP, QMN and IVA and anoperating gold mine in South Australia. Their EV (Figure 10) is double that of GBM’ssuggesting that the EV ascribed to GBM undervalues the Milo resource and does not assignany value to their portfolio of projects. If that were the case and GBM had a similar EV, thenthat would equate to a share price of at least 15c per GBM share.

Based on an EV/Cu tonne of approximately A$450 for ASX listed copperexplorers/developers, we would anticipate that Cu-REE or IOCG-REE companies shouldtrade at perhaps a 70-80% discount to reflect the lower recoveries (perhaps 30-40%), highercapital costs (+20-30%) and more limited market for concentrates (ie dominated by Chinesesmelters). This would translate to a six month share price target of say A$0.35 per Share forGBZ. In addition to the REE, we believe that the Cu and Cu-equivalent values of thecontained metals Au, Ag, Co, Mo etc are also likely to add significant additional value to theMilo Project.

Of the predominately REE companies, NTU and TUC have yet to publish maiden JORCcompliant resource statements and until they do, it is difficult to calculate comparablevaluation numbers. NTU’s and TUC’s projects differ from GBM’s Milo project in that theyhave a high HREO to TREEYO ratio and the mineralisation is richer in the higher valueCREOs yttrium and dysprosium. However, GBM and NTU are making progress towards themetallurgical testing and Scoping Study stages whereas TUC’s Stromberg HREE project iswell behind GBM in the various stages or hurdles to conquer in order to progress to thepenultimate production stage.

Keep in mind though that GBM’s inherent value should be based on more than just the Cuand REE content of their Milo Project especially since their Bungalien IOCG JV Project, theMt Morgan Project and the newly acquired Mayfield Project are all in the early stages ofexploration and their respective values will be better realised as exploration progresses.

RM Research is therefore of the opinion that the overall intrinsic value of GBM has yet to berecognised and that the release of the pending scoping study will confirm this. Theexpectation is that GBM should then be better acknowledged by the investment community.

$2 $14 $20 $22$68 $76

$173

$297

$451

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

$500.00

QMN GBZ EXS AVG RXM DML VRX HGO CDU

EV/T Cu Equiv selected ASX Explorers/DevelopersFIGURE 10 EnterpriseValue per tonne of Cuequivalent for selectedcopper REE andIOCG/REEExplorers/Developers.(source: RM Researchinternal modelling, April2012).

M Research believes thatthe Cu and Cu-equivalentvalues of the containedmetals Au, Ag, Co, Mo etcwill add significantadditional value to theMilo Project valuation.

SUMMARYFrom the discussion above, it is apparent that GBM’s market cap and EV (Figure 10) are onthe low side compared to many of its peers. It is difficult to truly evaluate GBM in total giventhat of all its projects, the Milo Project is the most advanced and it is too early to quantify theinherent value of all its other projects until such time as GBM reports JORC compliantresource statements for each project.

I believe that any company with REE mineralisation needs to be considered on its own merits,how far it has progressed on the REE industry’s widely understood steps to production, andultimately the composition of its mineralogy. I would assign a higher valuation on a resource ifthe HREE and CREO contents are relatively high compared to its peers as they are of highervalue and in shorter supply. A predominately LREE deposit may not necessarily beeconomically viable given that the Chinese dominate the global supply at much lower costsand can ramp up production of LREE as they see fit.

The REE industry is capital intensive at each stage of a project’s development and a goodsource of funding is required together with joint ventures and commercial relationships. Thefuture pricing and market supply and demand equation will ultimately determine thecommercial viability of any given project depending on the ratio of individual REEs containedin the mineralisation. There is no guarantee that prices for REEs contained in a particularresource will render the project as economic in the future.

It is well documented that China will continue to dominate the global supply and demand ofREEs and other strategic metals and commodities and the refining and production of metalalloys for the foreseeable future. I expect to see Chinese dominance to continue to movebeyond its borders as they farm-in, joint venture or takeover promising resource projects andtake-up ground to explore in their own right as they have in the Cloncurry district (as ASX-listed companies) and elsewhere in the world.

PENDING MILESTONESRM Research forecast news releases to the ASX are as follows:

April 2012

Milo North drilling assay results due (MIL012, MIL013)

Mt. Morgan field exploration results due

Pan Pacific/ Mitsui IOCG JV 2012 month budget approval

May-July 2012

Successful IPO of the Bungalien phosphate JV project as Swift Resources Ltd

June 2012

Expected release of the JORC compliant inferred resource for the Milo Project.

Milo Project Scoping Study results

July 2012

Preliminary Feasibility Study for the Milo prospect starts

Elevated contents ofHREE and CREO willlikely lead to higherproject values

The Phosphate spinoutis scheduled for mid CY2012

The maiden JORCResource for MILO is amajor milestone forGBM

RISK ANALYSIS Further exploration may not define an economic JORC compliant resource at any of the

Company’s projects as to date the level of drill exploration is not close-spaced enough todefine a sufficient level of confidence in the continuity of the data. This may have anegative impact on the securities of the Company.

GBM has just over A$1.5 million cash left for exploration and other activities. A capitalraising will be required to increase cash reserves to continue exploration and to completethe scoping study and pre-feasibility study in 2012. This could be dilutionary to existingshareholders.

Further declines in equity markets may continue to put pressure on junior resourcecompanies as investors switch out of “risk” into perceived safe haven investments suchas cash, gold and counter cyclical equities. Our medium term view is that the riskpremium has been eroded for many junior resource companies and we see near termupside as risk adverse shareholders would have exited these stock by now.

It is currently unknown as to whether all or any of the REEs will be able to be extractedeconomically. The upcoming scoping study will clarify this issue.

Metallurgical test work has yet to determine the optimal extraction and concentratemethodology for the Milo mineralogy.

Positive ongoing exploration results, a maiden JORC compliant resource statement and apositive scoping study should have positive impacts on the company’s share price.

Further drilling at Milo North is expected to discover further Cu and REE mineralisationthat will extend the strike length of the resource beyond one kilometer in length.Additional tonnes and higher grades will have a positive effect on the project’scommercial viability.

The Company wouldneed to raise additionalfunds to completefurther mining studies

Mr Peter Thompson is a senior resources industry figure with over 30 years experience acrossAustralia, the UK, and South America including stints at MIM Holdings, Xstrata Plc, and MtEdon Gold Mines. He has held directorships at Queensland mining and civil contractor JJMcDonald & Sons Group and ASX listed Golden West Resources. He is a CPA qualifiedaccountant and a Fellow of Chartered Secretaries Australia.

Neil Norris EXECUTIVE DIRECTOR

Mr Neil Norris has some 25 years experience in mining and exploration as a geologist withinvolvement in the discovery of Newcrest’s Cadia and Ridgeway mines in New South Walesto his credit and the Phoenix gold deposit at Fosterville in Victoria. Before joining GBM, MrNorris held senior roles with Newmont Australia Ltd and was Group Exploration Manager forPerseverance Corporation Ltd. He is the main driver of GBM’s technical and strategicdirection.

Cameron Switzer NON-EXECUTIVE DIRECTOR

Mr Cameron Switzer is a Queensland based geological consultant with over 20 yearsexperience as a geologist across the globe and importantly for GBM he was PrincipalGeologist with MIM Exploration Ltd the diverse experience he gained across a range ofgeological deposits and environments benefits the company in its exploration activities.Additionally, he has held senior roles including Senior Project Geologist at Newcrest MiningLtd’s Telfer gold mine in Western Australia and Geology Manager at Acacia ResourcesLtd’s Union Reef gold mine in the Pine Creek goldfields.

Guan Huat Sunny Loh NON-EXECUTIVE DIRECTOR

Mr Sunny Loh brings corporate and investment banking expertise in the Asian region to GBMand represents major shareholder Swift Venture Holdings Corporation of which he is theManaging Director. Mr Loh is also the Vice Chairman of Shanghai Fortune Capital, aninvestment banking and corporate advisory firm. Mr Loh holds a BBA from National Universityof Singapore, an MBA of Strategic Marketing from the University of Hull, and is an associateof the Institute of Chartered Secretaries and Administrators.

CONCLUSIONThe Milo Project is GBM’s priority exploration project that is rapidly progressing towards thecompletion of a scoping study by mid-2012. A successful outcome that reports aneconomically viable extraction process and saleable concentrate will ensure that the projectproceeds to the next stage of a feasibility study. The Holy Grail is for a commercial miningscenario dare I say as early as 2015?

To answer the question as to whether the Milo Project will be a copper or REE story, RMResearch considers that given the IOCG mineralisation is overprinted and enveloped byREEYOs, the resource is likely to be a hybrid deposit whereby the IOCG metals and the REEsmay all be commercially extractable but with variable recovery rates. The maiden JORCcompliant resource statement will go a long way to better value the project and the company.

GBM’s value lies in more than just the Milo Project and it will be positively correlated withexploration success at the Bungalien IOCG JV Project, the Mt Morgan Project and theMayfield Project which are all in the early stages of exploration and hence their respectivevalues have yet to be realised.

RM Research considers that the potential of GBM is de-risking as exploration successprogresses and have placed an initial share price target of 35c within the next six months.Speculative Buy.

RM Research Recommendation CategoriesCare has been taken to define the level of risk to return associated with a particular company.Our recommendation ranking system is as follows:

Buy Companies with ‘Buy’ recommendations have been cash flow positive for some time and have a moderate tolow risk profile. We expect these to outperform the broader market.

Speculative Buy We forecast strong earnings growth or value creation that may achieve a return well above that of thebroader market. These companies also carry a higher than normal level of risk.

Hold A sound well managed company that may achieve market performance or less, perhaps due to anovervalued share price, broader sector issues, or internal challenges.

Sell Risk is high and upside low or very difficult to determine. We expect a strong underperformance relative tothe market and see better opportunities elsewhere.

Disclaimer / DisclosureThis report was produced by RM Research Pty Ltd, which is a Corporate Authorised Representative of RM Capital Pty Ltd (Licence no. 221938). RM Research will receivepayment of A$35,000 for the compilation and distribution of four research reports. RM Research Pty Ltd has made every effort to ensure that the information and materialcontained in this report is accurate and correct and has been obtained from reliable sources. However, no representation is made about the accuracy or completeness of theinformation and material and it should not be relied upon as a substitute for the exercise of independent judgment. Except to the extent required by law, RM Research Pty Ltddoes not accept any liability, including negligence, for any loss or damage arising from the use of, or reliance on, the material contained in this report. This report is forinformation purposes only and is not intended as an offer or solicitation with respect to the sale or purchase of any securities. The securities recommended by RM Researchcarry no guarantee with respect to return of capital or the market value of those securities. There are general risks associated with any investment in securities. Investorsshould be aware that these risks might result in loss of income and capital invested. Neither RM Research nor any of its associates guarantees the repayment of capital.WARNING: This report is intended to provide general financial product advice only. It has been prepared without having regarded to or taking into account any particularinvestor’s objectives, financial situation and/or needs. Accordingly, no recipients should rely on any recommendation (whether express or implied) contained in this documentwithout obtaining specific advice from their advisers. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financialsituation and/or needs, before acting on the advice. Where applicable, investors should obtain a copy of and consider the product disclosure statement for that product (if any)before making any decision.DISCLOSURE: RM Research Pty Ltd and/or its directors, associates, employees or representatives may not effect a transaction upon its or their own account in theinvestments referred to in this report or any related investment until the expiry of 24 hours after the report has been published. Additionally, RM Research Pty Ltd may have,within the previous twelve months, provided advice or financial services to the companies mentioned in this report. As at the date of this report, the directors, associates,employees, representatives or Authorised Representatives of RM Research Pty Ltd and RM Capital Pty Ltd may hold shares in GBM Resources Limited.

![Gbz catalogue en lowres 72 hi[1]](https://static.documents.pub/doc/80x56/568ca6041a28ab186d8f7830/gbz-catalogue-en-lowres-72-hi1.jpg)