24

| Date post: | 22-Mar-2016 |

| Category: |

Documents |

| Upload: | kayla-longbrake |

| View: | 215 times |

| Download: | 3 times |

2

3

EDUCATE – to prevent E&O claimsARE you interested in reducing your premium costs,

enhancing customer relationships and improving youremployees’ professional development?

INVEST time in continuing education – It is important forprincipals and managers to make a commitment to providecontinuing education opportunities for your staff. Lead the wayby taking advantage of the continuing education opportunitiesoffered by your association and encourage your employees to dothe same. If you hire newly licensed employees, continuingeducation curriculum benefits will provide:

1. a faster learning curve to bring your new-hire up to speed;

2. an atmosphere of professionalism fostered by a learning culture and

3. the development of good habits as your new employee gains experience and confidence in your office.

Educating your employees can also improve employeeretention and morale by assisting them to further their careers.Experienced employees sometimes fall into the comfort zone ofpast habits – basic fundamentals of risk management may beneglected. Or, veterans may develop bad habits over time –relying on handshakes to bind coverage and cutting corners tofacilitate securing the next new client. Even with the best workhabits, changes in the industry, new regulations or technology,can lead to increased exposures for your agency. Continuingeducation cam help your staff stay abreast of changes in yourprofession while encouraging consistency within your agency.Both of these benefits help manage exposure and reduce thepotential for claims. To ensure a true focus on education,include the objective in each employees annual goals to enhancetheir technical competence. Work together with the employee tochoose the appropriate coursework so they have some “skin inthe game”.

Uncover the education needs of your employees

Training in technology including your agency software andsystems, procedures needed to protect the personal data thatyour agency handles, use of disclaimers, etc. is extremelyimportant, yet often overlooked. While strengthening technicalskills is essential, backing that training up with sales skills willallow your employees to reach their full potential and ultimatelyincrease your profit line.

Use IIASD Member Resources

Your Association is here to provide you with the resourcesyou need to educate your agency personnel to operateproductively and professionally and at the same time, limitingyour agency exposure to E&O claims. Our education agendaincludes Property/Casualty, Life & Health, specialty lines suchas Flood and Crop Insurance as well as our annual E&O LossControl seminars. We welcome your input on educational needsof your agency and staff.

E&O EDGECarolyn Hofer, E&O Administrator

Annual Convention Education Opportunities:

Cyber Liability – 3 hours Gen. CEC

Ethics – 2 hours Gen. CEC

Health Care Reform – 3 hours CEC

Flood – 3 hours CEC

Don’t miss the opportunity to provide education training toyour employees while allowing them to meet industryprofessionals and socialize with fellow insurance producers.Convention is a great time to share ideas, develop relationshipswith carriers and industry wholesalers , strengthen technicalknowledge and just relax and have a good time.

ANNUAL CONVENTIONJoin us in Sioux FallsSeptemeber 18th – 20th

Ramkota Hotel & Convention Center – Sioux Falls, SDRegister online at www.iiasd.org or contact us [email protected] or [email protected]; Banquet Entertainment – JASON HEWLETT

Comedian and Impressionist Don’t miss this amazing show!

4

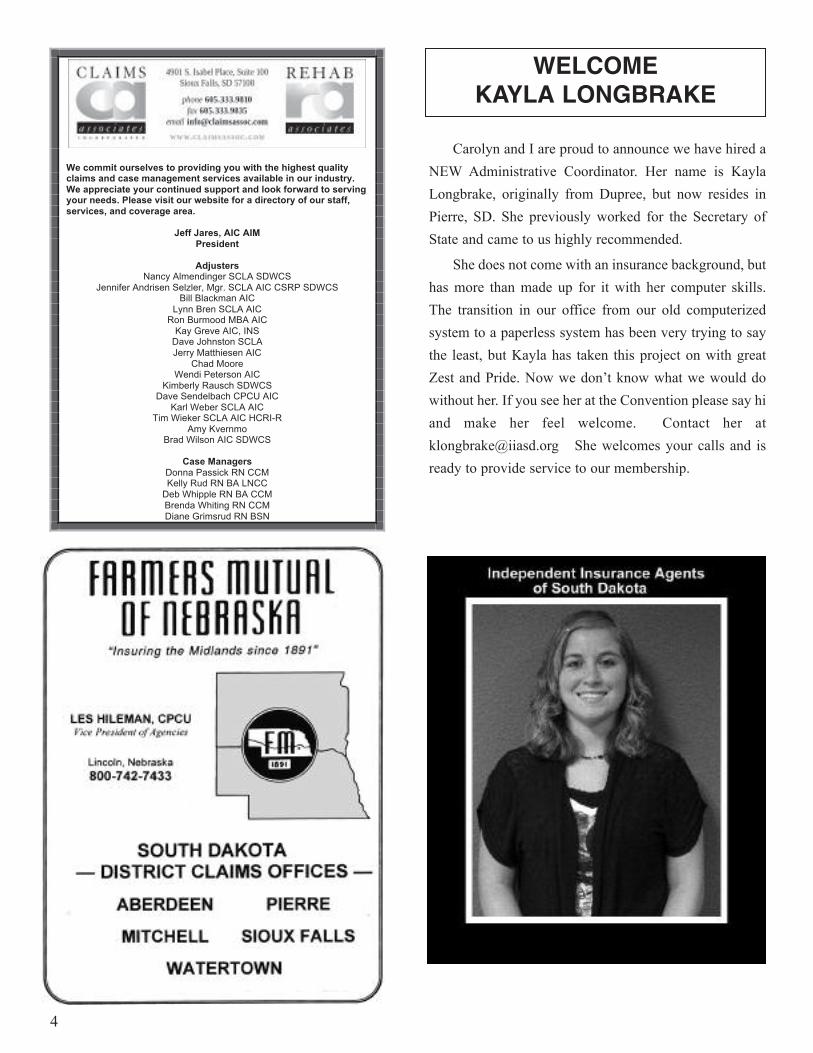

Carolyn and I are proud to announce we have hired a

NEW Administrative Coordinator. Her name is Kayla

Longbrake, originally from Dupree, but now resides in

Pierre, SD. She previously worked for the Secretary of

State and came to us highly recommended.

She does not come with an insurance background, but

has more than made up for it with her computer skills.

The transition in our office from our old computerized

system to a paperless system has been very trying to say

the least, but Kayla has taken this project on with great

Zest and Pride. Now we don’t know what we would do

without her. If you see her at the Convention please say hi

and make her feel welcome. Contact her at

[email protected] She welcomes your calls and is

ready to provide service to our membership.

We commit ourselves to providing you with the highest quality claims and case management services available in our industry. We appreciate your continued support and look forward to serving your needs. Please visit our website for a directory of our staff, services, and coverage area.

Jeff Jares, AIC AIM President

Adjusters

Nancy Almendinger SCLA SDWCS Jennifer Andrisen Selzler, Mgr. SCLA AIC CSRP SDWCS

Bill Blackman AIC Lynn Bren SCLA AIC

Ron Burmood MBA AIC Kay Greve AIC, INS

Dave Johnston SCLA Jerry Matthiesen AIC

Chad Moore Wendi Peterson AIC

Kimberly Rausch SDWCS Dave Sendelbach CPCU AIC

Karl Weber SCLA AIC Tim Wieker SCLA AIC HCRI-R

Amy Kvernmo Brad Wilson AIC SDWCS

Case Managers

Donna Passick RN CCM Kelly Rud RN BA LNCC

Deb Whipple RN BA CCM Brenda Whiting RN CCM Diane Grimsrud RN BSN

WELCOMEKAYLA LONGBRAKE

5

6

In talking with an agent recently the agent thought that

they needed CE cedits every two years to meet state

requirements to sell long-term care policies, however in

checking with Jeff Smith with the Division of Insurance, an

agent is not required to take CE for long-term policies.

The federal government, however requires that an

agent take continuing educational courses every two years to

meet the federal government requirements. This has nothing

to do with CE. Jeff did state that it might be a good idea when

taking a long-term care course that you check with your

provider of the course to see if it qualifies for CE. In other

words, if you are taking any course you should try to get CE

credits.

DID YOU KNOW?Long Term Care CEC Requirements

ASSOCIATION EMAIL CHANGE

Jerry Diamond:[email protected]

Carolyn Hofer: [email protected]

Kayla Longbrake:[email protected]

Make this important change in your email contact list.

7

TRUSTED CHOICE AWARDSCHOLARSHIPS

Trusted Choice is conjunction with IIASD has

awarded two $1,000 scholarships to two South Dakotans.

The winners are Talia Peters of Wagner South Dakota.

She is the daughter of Chad and Lisa Peters, she will be

attending DWU in the Fall.

The second scholarship went to Jenna Winckler of

Lake Andes South Dakota. She is the daughter of Randy

and Carla Winckler, she also will be attending DWU in

the Fall.

These scholarships were based on grade point

average, school activities, and community involvement.

Congratulations Talia and Jenna on a job well done.

NAIC SUPPORTS EXCLUDINGAGENT COMMISSIONS FROM MLR

Efforts toward a producer carve-out from the

calculation of Medical Loss Ratios (MLR) got a much-

needed boost recently. The National Association of

Insurance Commissioners (NAIC), after weeks of

deliberation, came out in support of H.R. 1206 which

would exclude producer compensation from MLR

calculations.

A ruling from the Department of Health and Human

Services (HHS) states that health insurance companies

must spend between 80 to 85 percent on direct care,

leaving only 15 to 20 percent for administrative costs.

Currently, agent commissions are included in HHS’s

definition of administrative costs.

The bill has 97 bipartisan co-sponsors, but has not

yet been discussed in committee. The Big “I” is working

with its national affiliates to maintain momentum.

8

VIRTUAL RISK CONSULTANTThe Big “I’s” Virtual Risk Consultant can help you present yourself to clients as a risk manager, distinguishing you from

all the other agents who are focused on selling price. This approach can even apply to BOP risks. Take, for example, a typical

prospect that would be eligible for a BOP product. You can get a list of the types of exposures and can truly act as their risk

consultant.

Step 1: Understanding the Risk- This section provides a summary of operations and an explanation of exposures to evaluate

for the risk to be insured. Also included are minimum coverage’s to offer and additional coverage’s to consider.

Step 2: Exposure Identification Survey- You can build a questionnaire designed to assist in revealing client exposures and

uncover potential coverage gaps. The information serves as a guide in developing an insurance program to meet the client’s

needs. The questionnaire is a supplement to the ACORD forms, not a replacement for them, so the ACORD form must also be

completed and used.

Step 3: Proposal Assistant- The proposal assistant provides concise definitions for all coverages included in your customer

proposal. It offers a comprehensive list of Commercial Lines coverages with succinct definitions to enhance customer

understanding at the point of sale. It also offers links directly to the appropriate ACORD forms.

Step 4: Customer Coverage Checklist/File Documentation- Get a printable coverage checklist complete with a client/agent

signature block to document coverages recommended and rejected by the customer.

9

Meet our Speakers:Inga Goddijn is a Managing Director for Markel Corporation inDeerfield, IL. She has a broad spectrum of insurance knowledgeand will be presenting – “Cyberliability”

Holly Hoffman is a local South Dakotan and has a lot of lifeexperiences to share with us. She will be sharing “Life in anEthical World”.

Randy Moses – as you can tell by his last name, he has beenaround a long time, with many years experience at the SDDivision of Insurance.

Sandy Kost is the owner/managing director of A.D. Banker ofSD and provides continuing education and exam preparationcourses.

Deb Muller is an executive for Avera McKennan in the healthcare field with years of experience.

Randy Moses, Sandy Kost & Deb Muller make up the “HealthCare Reform Dream Team”

Meet our Entertainment:Jason Hewlett is the consummate comedian/impressionist andwill keep us all in side-splitting stitches.

CONVENTION HIGHLIGHTSRegister online at ww.iiasd.org

1752 Club ScholarshipThe 1752 Club will be giving out scholarships again at the convention in conjunction with theIIASD. Agents and staff who are members of SDIIA are eligible to submit their children who areattending a secondary educational institute, for consideration.

Agent:

Agency Name:

Student’s Name:

College/Vo-tech:

Please submit to Jeff Jones at 1004 S. 7th St., Milbank, SD 57252 or by e-mail [email protected].

10

Who else but United Fire?

TOM DIEFENDORF605-763-8077 tdiefendorf@

unitedfi regroup.com

Ask Tom, United Fire Group South Dakota Representative, about our automated cancella-tion notifi cation system, available on qualifying accounts.

• No reduced number of days notice for non-payment. The number of days for cancellation notifi cation to parties of interest is the same, regardless of the cancellation reason.

• We provide notice to parties of interest for insured-initiated cancellation as well as company-initiated cancellation.

• For all requested lines of business, we will provide notice to parties of interest — this service is not limited to select lines of business only.

• UW1730, Notifi cation Endorsement for Cancellation, Non-Renewal or Material Change in Coverage is available to support your notifi cation request.

United Fire GroupCedar Rapids, Iowa www.ufgAgent.com

• Ranked among the “Most Trustworthy Companies in America” by Audit Integrity and Forbes

• Named a “Top 10 Ease of Doing Business Performer” by Deep Customer Connections Inc. (DCC)

• Named a “Super Regional Property/Casualty Insurer” by Insurance Journal and Demotech Inc.

• Rated “A” by A.M. Best

11

Can Insurance Save Us from ClimateChange?By Brian Thomas

People judge risk badly. We worry too much aboutminor hazards and are nonchalant about more seriousones. We’re especially inept at judging chronic long-term risks – like climate change.

Insurance is a major part of how we deal with risk– can it lead us to more viable ways to address climateissues? The picture is mixed.

When we manage risk by buying insurance, weendure the slow, small pain of insurance premiums inexchange for a big compensation should somethingugly happen. The insurers profit from our lack ofknowledge about risk. Buying insurance goes againstthe grain, but paying our premiums gives us a littlemore security against fires, earthquakes, businessinterruption, and the numerous other events againstwhich we can buy an insurance product.

Insurers review their policies annually and changetheir terms if they see a change in the probabilities.When no major losses occur, the industry pats itselfon the back for judging their risks correctly for thatyear. They’re happy and profitable. If the risklandscape changes, they absorb the payouts and adjustthe terms accordingly.

The optimistic point of view is that insurance canplay a major role in guiding businesses andindividuals toward more climate-friendly decisions. Intheory, insurers study the real probabilities of knownhazards, figure out a viable premium that givesthemselves a profit and the policyholders the agreedupon protection against the risk. When climate changeraises the risks of flooding, business interruption, andother insurance hazards, the premiums go up, whichcan lead their policyholders to change their behavior.Financing for a new factory can be prohibitive or evenimpossible to get, if insurers won’t cover it.

In practice, though, this theory is faulty for several

12

reasons. Climate change poses special challengesto insurers, not merely because they are on thehook for many weather risks such as hurricanes.

First, to single out one kind of insurance,many factors combine in extreme weather events.A hurricane has many causes, and global warmingmight only be two percent part of the overall risk.If that part grows from two percent to fivepercent, it seems negligible, but in fact it’s quitesignificant. As one insurance executive said,“Even a minor increase in a risk like that canmean billions of dollars in additional losses toinsurers.” If the winds are a few miles per hourstronger, and the storm takes a path through aheavily insured area, insurers can beoverwhelmed.

The same is true for other climate impacts.There have always been floods, extreme weather,and times when the water cycle intensifies. But ifclimate change is turning up the dial, thesefamiliar events may break out of their boundariesand become more frequent, more intense, orchanged in unexpected ways.

Second, insurers are people too, and thecognitive blind spots that afflict individuals alsoaffect the risk business. In practice, the insuranceindustry’s grip on certain probabilities often relieson seat-of-the-pants methods that are subjective,and whose over-optimistic assumptions aresometimes rudely corrected by ugly surprises,especially when risks are constantly changing, asthey are with climate change.

Like all of us, insurers want certainty, evenwhen they know that certainty cannot be attained.At a 2007 conference about hurricane science foran insurance audience, the world’s topclimatologists discussed various topics inmodeling and hurricanes. The head ofunderwriting at a major North American insurersnorted at the hedged, qualified way the scientistsstate their conclusions. The underwriter thencomplained, “Why don’t the scientists give us

13

We have been solving specialty insurance puzzles with excellence since 1980.

Call us for the right !t.

THE RIGHTPIECE.

Excellence & Leadership

Log on to SPOT, our online rating tool at:www.ericksonlarseninc.com

14

numbers we can use! These probabilities are toonebulous for us to write business with them!” Hisimpatience is widely shared, but the answer is no.

Third, insurance functions well when the risksof various hazards are truly independent of eachother, and truly random. One trouble with climatechange is that climate instability tends to makefloods, windstorms, and other extreme weathermore interrelated.

One force binding all these factors togethermore tightly is land use, which in the US is oftenpart of a highly entrenched political juggernautpromoting the worst possible policies, such asbuilding heavily in flood plains, or on beaches veryprone to hurricane damage.

Consider Florida, where the laws, businesspractices and general culture are geared todeveloping every square inch of land near water –oceans, certainly, but also lakes, streams, wetlands.Even in the absence of climate change, this is anobviously dangerous policy. It’s also very popular.John Coomber, former CEO of Swiss Re, oncegrumbled that every American wants to live on themost vulnerable beaches they can find in Florida.

Governments occasionally try to buck the pro-development tide, but the political pressure againstthe anti-development forces is swift and merciless.

1515

Certainly no politician can withstand it. Rather than resisting, many property and casualty insurers havepulled away from vulnerable coastal property in Florida.

In response, Florida created its own public insurance pool. Result? Development continues, and the statefund is actuarially unsound – a major storm hitting a developed area would bankrupt the fund in short order.A few more storms would bankrupt the state of Florida, which would then call on the Federal government --as the stand-in for taxpayers in all other states -- to bail them out.

These three factors mean that the insurance industry is weaker than it appears when in matters ofchanging social and economic policies. The only way to change these entrenched policies would be for othersocial forces to align with the insurance point of view. That will require energetic political leadership andvigorous regulation. The market alone cannot save us.

Brian Thomas left Swiss Re in 2006 and became a sustainability consultant with a focus oncommunications. He has developed green-themed projects for clients including Merill Lynch Global Marketsand Investment Banking, Cofra Holding, Good Energies, Zurich Financial, Edelman, the City of Chicago, theCity of New York, and others. He is currently a member of the New York City Panel on Climate Change,EnviroComm, and the Association of Green Technology Auditors, to name a few. Thomas started his blog,Carbon Based, in 2007, after requests from contributors to the Intergovernmental Panel on Climate Change(IPCC). He is the author of Climate Change Adaptation in 2010 and currently resides in West Cornwall, CT.,where he is an activist member of the Conservation Commission. For more information, please visitwww.carbon-based-ghg.com, and his blog, http://carbon-based-ghg.blogspot.com.

16

trust.

acuity.com

17

QUOTABLES“Happiness is good health and a bad memory.” -

Ingrid Bergman (1917-1982)

“Friends may come and go, but enemies

accumulate.”-Thomas Jones

“It is time I stepped aside for a less experienced and

less able man.”- Professor Scott Elledge on his

retirement from Cornell

“While we are postponing, life speeds by.” -Seneca

(3BC-65AD)

“An idea can turn to dust or magic, depending on the

talent that rubs against it.” - William Bernbach

“Men are not disturbed by things, but the view they

of things.”- Epictetus (55-135 AD)

“Men have become the tools of their trade.”-Henry

David Thoreau (1817-1862)

“I have never let my schooling interfere with my

education.”- Mark Twain (1835-1910)

“To sit alone with my conscience will be judgement

enough for me.”- Charles William Stubbs

“Men and actions behave wisely once they have

exhausted all other alternatives.”- Abba Eban (1915-

2002)

Maple Grove, MN 55369

Protection you can count on.

Austin’s got you covered.

18

WEEKLY FRAUD NEWS & REVIEW

FRAUD CONVICTIONSA career criminal shot five people, including a toddler, in an apparent revenge for an insurance-fraud deal thatwent sour. Details are still emerging, but cash-strapped New York City plumber Paul Shay allegedly hired MarkRichard Geisenheyner to burn down Shay’s rural vacation home in Douglass, PA for a large insurance payout.The claim included expensive artwork Shay had removed before the fire. Shay supposedly promisedGeisenheyner $300,000 of the insurance loot but after burning the house, Geisenheyner claimed he received only$70,000 and took the rap with jail sentence. Geisenheyner was convicted after police found one of thesupposedly stolen paintings in his home. He stewed in jail. A lot. When he finally got out, he told many peoplethat he was hellbent on revenge. Geisenheyner showed up at Shay’s vacation home and opened fire on a partySaturday night shooting Shay execution-style in the head. Then he shot four other people in the head, includingtwo-year-old Gregory Erdmann. Gregory and two other guests died. Shay and another guest remain criticallywounded. A SWAT team later killed Geisenheyner after a six-hour standoff at the home of a crony in Trainer,PA.

Doc-hopping to keep receiving workers’ comp money has earned Los Angeles cop Robert Yanez a fraudconviction. He was injured on the job. His first doc ordered him back to work, so he kept going from one docto the next after each ordered him back to work. Yanez then submitted forged or altered doctor notes that allowedhim to receive comp money and stay off work for about four months. He received two years of probation andmust repay $6,200.

Thanks to a sharp-eyed investigator, James Flack has a fraud rap sheet. The Philadelphia-area man told hisinsurer that someone burglarized his home, stealing $17,500 worth of possessions. An investigator reviewing the

19

file noticed that Flack had made a $27,000 burglary claim in 1999. Many items Flack had said were stolen endedup on his 2010 claim. He withdrew the latest claim when confronted, but it was too late. The insurer referredthe case for prosecution. Flack received two years of probation Thursday.

Bad day in court for Jose Cruz. The Salinas, CA, man was out on disability money after being hurt whileworking as a chef at a Hyatt Regency Hotel. All the while, he secretly worked as a contractor while collectingdisability money. He told a claims adjuster that he received $305 “in gratitude” for installing a homeowner’sconcrete driveway. Cruz also did not have a contractor’s license, and did not buy state-required workers’ compcoverage for his employees. Cruz pleaded guilty and will be sentenced August 31.

Psychiatrist Alan Gumer could use a little couch time himself. The South Florida psychiatrist was a keyplayer in a massive $200-million con job involving fake group-therapy billings against Medicare. The Miami-based American Therapeutic Corp. chain of clinics billed Medicare for needless psychotherapy for thousands ofpatients who were paid to fake depression, schizophrenia, or bipolar illness. Other patients suffered fromAlzheimer’s and dementia and did not even need psychotherapy. Gumer alone billed Medicare $19.3 million,signing bogus medical evaluations that authorized patients for expensive group-therapy sessions. Recruitersreceived millions of dollars for bringing in patients from assisted-living facilities and halfway houses. Gumerpleaded guilty Thursday, and faces up to seven years in federal prison when sentenced next January.

CRIMINAL CHARGESA woman’s bills for prescription pain meds were so high that her insurer hiked her premiums. The surprised woman had no

idea how the claims ended up on her policy. That triggered an investigation that led to the bust of an Orlando-area doc for

allegedly using her insurance info to illegally obtain prescription pain meds. Dinash Yanamadula runs Central Florida Pain and

20

21

Spine Institute. He obtained the unnamed woman’s info and

charged meds to her policy, prosecutors allege. He billed for

at least five phantom visits to his clinic and at least 10

prescriptions using her name, officials say. Yanamadula’s case

also reveals a big loophole in a new Florida law requiring

licensing and state inspections of doc-owned pain clinics: He

is exempt from the law. As a pain-management specialist, the

law exempts certain specialist categories from licensing. The

number of licensed pain clinics in Florida also will drop to

roughly half of the current 800 clinics because surgeons,

anesthesiologists, and pain docs do not have to register their

clinics, the head of the association of Florida pain-

management specialists predicts.

RELATED NEWSProsecutors are the critical final step in nailing fraud

convictions. Let us honor their hard work by nominating a

deserving courtroom wizard for the Coalition’s Prosecutor of

the Year Award. The award recognizes skilled prosecutors

who go that extra mile. Maybe the prosecutor won an

extraordinary conviction, or series of convictions, or

developed a brilliant legal strategy, or showed unusual

leadership in fraud fighting outside the courtroom. No other

national award honors fraud prosecutors. Deadline for

nominations is September 26. Questions? Contact Jim Quiggle

at 202-393-7331.

Massachusetts insurers have immunity from defamation

suits for reporting suspected insurance fraud to the state’s

insurance fraud bureau, but that immunity ends if an insurer

inserts itself too deeply into the prosecution, the state’s highest

court has ruled in allowing a comp claimant to sue AIG for

malicious prosecution and other grounds. Here is the

backstory: Struggling with mental illness, Jesse Maxwell

ended up homeless when AIG denied his workers’ comp claim

after he said he injured himself while picking up a 100-pound

drain gate for his Boston employer. AIG videotaped him

allegedly working as a janitor, and Maxwell was convicted of

workers’ comp fraud. He is trying to overturn his conviction,

and is suing AIG. He contends the insurer went too far by

getting too involved in his prosecution after referring the case.

The state’s highest court gave AIG qualified immunity from

Maxwell’s lawsuit. The Massachusetts immunity law grants

clear protection from such lawsuits when an insurer simply

refers a case for prosecution, the court reaffirmed. But some

of AIG’s conduct went beyond the scope the immunity law and

thus is not protected from lawsuits. The insurer’s motion for

summary judgment based on the state immunity law was

denied, the court ruled. [Maxwell v. AIG Domestic Claims,

Inc, (SJC - 10757)]

An Indiana contractor has won a $14.5-million lawsuit

alleging that State Farm had defamed him after denying his

restoration claims when hailstorms hit the Indianapolis area in

2006. The insurer had denied Joseph Radcliff’s hail-damage

22

Need A Ride?

800-708-7448 • Fax 402-916-3333 • www.ringwalt.com

Email submissions to us at [email protected]

Ringwalt Liesche Co.&®

Ringwalt & Liesche Co. Provides a

front row seat to placing public livery risks.

You can rely on coverage from an A++ carrier that has been writingcommercial auto risks for over 65 years.

We are able assist you and your customer with the following

• Luxury, SUV & Super Stretched Limousines

• Liability limits up to $5 million (surplus lines may apply in some states)

• Federal and/or State filings

• Coverage for Audio Visual Equipment (up to $10,000 per vehicle)

• Medical Payments (up to $5,000 per passenger)

:

claims due to suspected fraud. He said the denials resulted in considerable negative news coverage. Criminal charges were

dismissed but he said the news coverage ruined his business. [State Farm Fire & Casualty Company v. Joseph Martin Radcliff,

et al., Cause No. 29D01-0810-CT-1281 – Hamilton Co. Superior Court No. 1]

Comp claims by employees of the Los Angeles County Probation Department strangely spiked 21 percent last year, and

officials are investigating how many claims are fraudulent. The total payouts were $24 million in FY 2009-10. A large number

of the claims involved employees who said they were hurt when they fell onto the floors or in parking lots of probation facilities.

Risk-management staff say they found no significant uplift, cracks, or other reasons for the spike in falls.

Sacramento-area DAs have been awarded more than $1.4 million in state grants to investigate and prosecute workers’ comp

fraud next year. The grants are part of $32 million awarded to DAs around California. Overall, 36 of California’s 58 counties

have received funding. The state still must approve the funding, which comes from annual state-required assessments paid by

California employers.

Medicare can reduce fraud by adopting practices that private insurers already use. That will likely be one discussion theme

of a hearing that a U.S. Senate subcommittee will hold at 2:30 p.m. this Tuesday, July 12, to review technology and business

practices for reducing fraud in the federal health-insurance program for seniors. The Coalition has been pushing for more

adoption of private-sector business practices and speakers are expected to show effective ways in which private-sector insurers

are dealing with fraud.

HHS’s excluding individual employees of shady medical providers from Medicare and Medicaid is unconstitutional, the U.S.

Chamber of Commerce says. HHS now can exclude individuals solely because they are employed by an entity that has defrauded

a federal health-care program. This power can wreck the careers of employees and deprives them of their right to due process,

the Chamber contends. The exclusionary rule was drafted partly because health care executives were avoiding prosecution by

23

PO Box 89846 Sioux Falls, SD 57109-9846

P. 605.361.5705 or 866.440.1840E. [email protected]

WHOLESALE ACCESS toFirst Dakota Indemnity and Dakota Truck Underwriters,known as the Dakota Group. The DakotaGroup is the largest writers of workers’compena�on business in South Dakotaand a leading writer in the Midwest.

Contractors

Healthcare

Hospitality

Manufacturing

Retail

providing workers’ compensa�on solu�ons

purposely shielding themselves from their company's

fraudulent activities.

Auto insurers in the UK are selling info about policyholders

involved in crashes to lawyers who then lodge inflated injury

claims against the same insurers, a member of parliament

charges. Jack Straw says two large insurers have admitted

selling the customer data for up to 1,000 per policyholder to

law firms that advertise on daytime TV, promising large

payouts for accident victims. Motorists then are bombarded

with text messages and phone calls offering to pursue claims

for often-fabricated injuries, Straw says. The allegations

have sparked a firestorm of controversy over whether

parliament should ban such “referral fees.”

LEGISLATIONThe Minnesota commerce department has laid off several

insurance investigators during a budget impasse that has

virtually shut down the state government. Law enforcement

was exempt from the shutdown but fraud investigators were

not considered an “essential service.” All the while, the state

legislature also is looking to cut the fraud bureau’s budget in

half.

From New York, first the good news: Two auto-fraud bills

have cleared the New York Senate. Now the bad news: The

bills passed just before the statehouse closed for the year.

With Albany largely shuttered, yet another year likely will

speed by without no-fault fraud reforms that nearly everyone

agrees are needed to put more heat on widespread auto-crash

rings.

• Anti-runner: SB 2004A makes it a misdemeanor to

recruit crash victims for bogus injury claims once in a 12-

month time period. That is a virtual free pass for often-

large frauds. It is a low-level felony if the suspect

commits five or more acts as a runner, or the fraud

scheme exceeds $5,000. It is a higher-level felony for 10

or more acts if the fraud exceeds $20,000. The bill is

scaled back from the original, which made being a runner

a flat-out felony. The Assembly will consider the bill

next year.

• Policy rescissions: Insurers can rescind auto policies if

the payments came from a bank account with insufficient

funds or from a non-existent account. This gets at crash

rings that buy policies to cover cars used in set-up

wrecks. The ring quickly makes bogus injury claims

while the policies are still in effect and before the insurer

discovers the check bounced. SB 4507B also protects the

coverage of staged-crash victims. The Coalition testified

in April before the Senate Insurance Committee in

support of SB 2004 and SB 4507. Both bills were

watered down after the hearing.

I I A S D

2011 IIASD OFFICERS President Amy Olson-Miller

President-Elect Dale Heesch

Vice-President Kathy Johnson

Past President Darrin Erickson

Secretary-Treasurer Roger Larson

State National Director Gary Joyce

2011 BOARD DIRECTORS District 1 Roger Larson

District 2 Rich Puthoff

District 3 Steve Walker

District 4 Chad Dubisar

District 5 Gerrit Juffer

District 6 Pat Tollefson

District 7 Ed Starr

District 8

Kathy Johnson

EXECUTIVE VICE PRESIDENT Jerry Diamond

COMING EVENTS

Register at www.iiasd.org

August 30th – Fall Crop Seminar - Pierre

Sept. 18th – 20th –Convention – Sioux Falls

_________________________________________________________________

AT YOUR SERVICE

IIASD – Pierre Office…………………….….…..………..…..…224-6234 IIABA National……………….……..….………..………….800-221-7917 Division of Insurance………….……..….…………….…………773-3563

Jerry Diamond’s e-mail [email protected]

Carolyn Hofer’s e-mail [email protected] Kayla Longbrake’s e-mail [email protected]

ERRORS & OMISSIONS PROGRAM

Carolyn Hofer, E&O State Administrator [email protected] 605-224-6234

INDEPENDENT INSURANCE AGENTS OF SD (IIASD) PO BOX 327 PIERRE SD 57501

PRSRT STD U.S. Postage

PAID Pierre, S.D.

Permit No. 186

Independent Insurance Agent