36

Australia’s Energy Sector: The State of the Market Steve Edwell, AER Chairman CEDA, 29 August 2007

Australia’s Energy Sector: The State of the Market

Steve Edwell, AER ChairmanCEDA, 29 August 2007

Overview

• New AER functions

• Electricity and gas prices

• Industry consolidation

AER roleNow:

electricity transmissionNational Electricity Market monitoringNational Electricity Law enforcement

Early 2008: addgas transmissionelectricity and gas distribution

Late 2008: add retailconsumer protection, retailer of last resort etcretail price regulation at discretion of each jurisdiction

Regulatory structure post reform

(including NEM and Gas Code regulation)

ERAUCAustralian Energy Regulator (AER)

Australian Competition and Consumer Commission (ACCC)Competition Regulation

WANTTasACTQLDSAVicNSW

ERAUCOTTER/ GPOCICRCOffice of EnergyESCESCIPARTRetail Pricing

Wholesale

Transmission

Distribution

Retail

AEMCAEMCAustralian Energy Market Commission (AEMC)

Rule Changes

Energy prices

Electricity price update

• Price shocks in 2007

• Impacts– Forward market– Retail sector– Investment

• AER monitoring

Weekly electricity prices

NEM prices March 2006 – August 2007 (weekly volume weighted averages)

0

50

100

150

200

250

300

350

400

450

Mar

–06

Apr

–06

May

–06

Jun–

06

Jul–

06

Aug

–06

Sep

–06

Oct

–06

Nov

–06

Dec

–06

Jan–

07

Feb–

07

Mar

–07

Apr

–07

May

–07

Jun–

07

Jul–

07

Aug

–07

$/M

Wh

NSW Qld SA Tas Vic

Drought

Water shortages:• Snowy dams• Tasmanian and Vic hydro• Queensland coal plant

Impact: tighter supply conditions, higher prices

Market under stress in June 2007

• Record prices: 42 price events above $5000 • Retailers under pressure

– High prices squeezing margins– Energy One withdrew from the market– Momentum sold 15,000 customer accounts

• Some major users under pressure

Why the high June prices?

• Continuing drought conditions

• Flood impacts on Hunter Valley coal supplies

• High demand

• Macquarie Generation bidding

Forward prices

0

25

50

75

100

125

150

Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

$/M

Wh

NSW June 07 NSW Feb 07 NSW Aug 07

Higher forward prices — why?

• Uncertainty about future supply– risk of persistent drought?– timing of investment response?– uncertain effects of carbon trading on

investment and prices?

Reliability outlook to 2012

30 000

35 000

40 000

45 000

50 000

55 000

2006–07 2007–08 2008–09 2009–10 2010–11 2011–12

Meg

awat

ts

Proposed scheduled capacity

Non-scheduled generationprojections (summer)

Aggregate scheduled generationcapacity (summer)

Capacity for reliability

Maximun demand

Electricity networks – real investment

0

500

1000

1500

2000

2500

3000

3500

4000

2003-04 2004-05 2005-06 2006-07 2007-08

$m (2

006)

DistributionTransmission

Reliability – distribution

0

50

100

150

200

250

300

350

400

450

1995–96 1997–98 1999–00 2001–02 2003–04 2005–06

Min

utes

Victoria NSW & ACT Queensland South Australia NEM Ave.

Gas prices

Natural gas prices

Historical prices around $2.25–$4.00/Gj

WA prices rising sharply since 2006

Victorian spot prices creeping higher

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

EastQld

Vic NSW EastCoast

Qld-SA

WA NT

2005 2006

$/G

J

2007

2007

Western Australia

• Prices up from $2.50 to $7.50/Gj since 2006

• Tight supply• Competition from LNG exports• High prices attracting new entry, but tight

supply may persist for some time

East Coast gasDownward pressure on prices

– Coal seam methane increases supply

Upward pressure on prices– Increasing demand – electricity generation– Santos LNG proposal for export capability ?

Net impact?– Price rises contained for now – $3.00 to $4.00 range– Victoria prices reached $5 this winter– Longer term risks

Coal seam methane production

0102030405060708090

1996 1998 2000 2002 2004 2006

NSW

Qld

PJ

Ownership consolidation

Energy sector mergers

• Networks

• Retailers

• Vertical integration

Recent merger activity

• AGL and TRUenergy swap generation assets in SA — AGL acquires Torrens Island (1260MW)

• Sale of Origin Energy’s gas assets to APA group

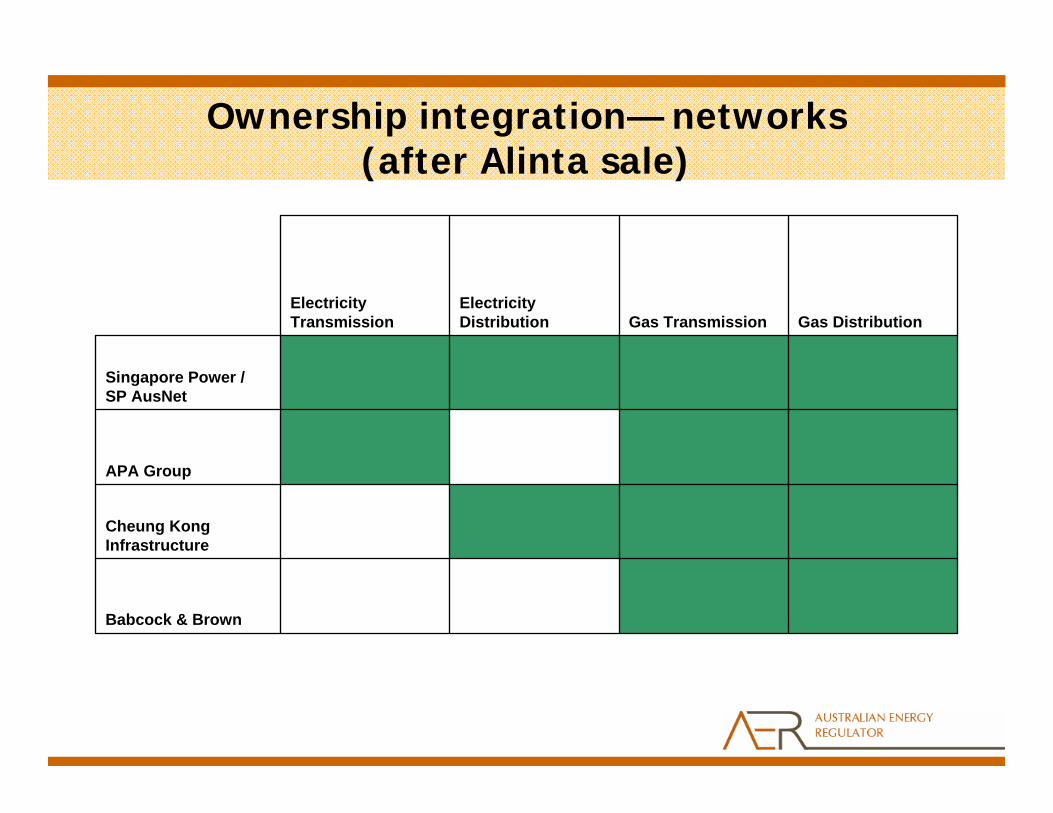

• Sale of Alinta to Babcock & Brown / Singapore Power

• International Power to buy EnergyAustralia–IP retail partnership

• Basslink sale

Ownership integration— networks (after Alinta sale)

Cheung Kong Infrastructure

Babcock & Brown

APA Group

Singapore Power / SP AusNet

Gas DistributionGas TransmissionElectricityDistribution

ElectricityTransmission

Retail market share – Vic/SA

AGL AGL

AGL

AGL

Origin Origin

Origin

Origin

TRUenergyTRUenergy

TRUenergy

OtherOther

TRUenergyEnergy Australia Energy Australia

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Electricity Gas Electricity Gas

Victoria South Australia

% o

f sm

all b

usin

ess

& d

omes

tic c

usto

mer

s

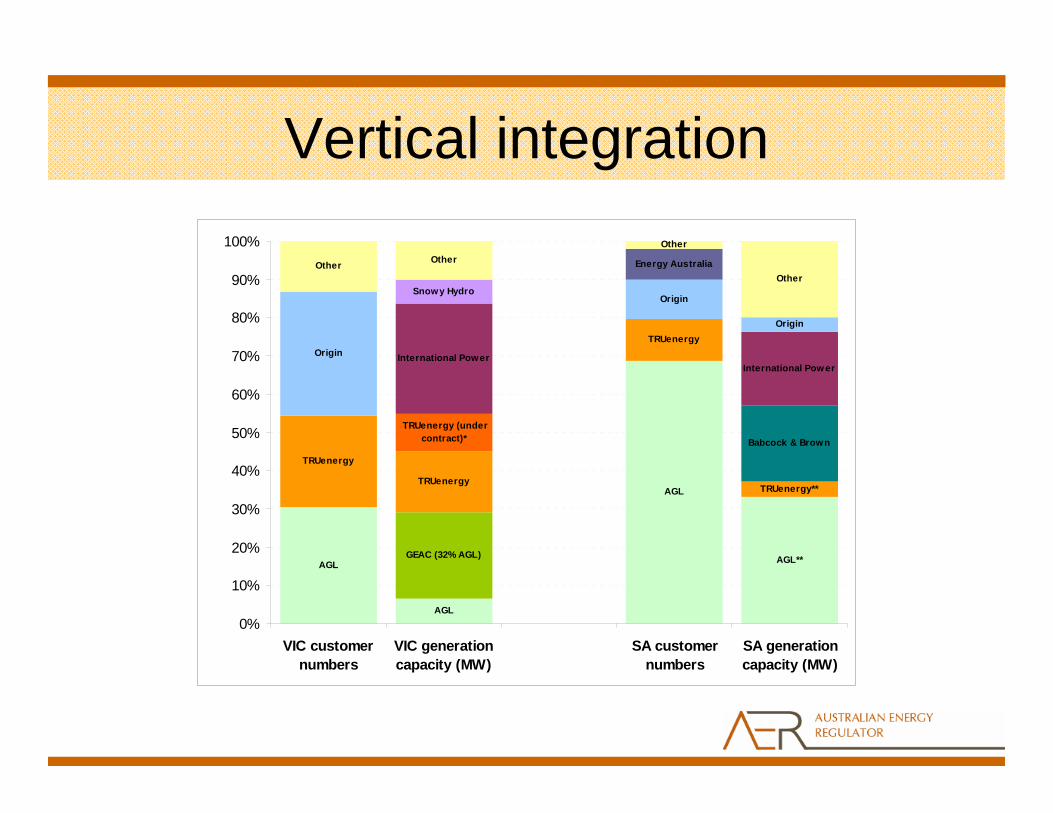

Vertical integration

AGL

AGL

AGL

GEAC (32% AGL)

TRUenergy

TRUenergy

TRUenergy

Babcock & Brown

International PowerInternational Power

Snowy Hydro

Origin

Origin

Origin

Energy AustraliaOther OtherOther

Other

AGL**

TRUenergy**

TRUenergy (under contract)*

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

VIC customernumbers

VIC generationcapacity (MW)

SA customernumbers

SA generationcapacity (MW)

State of the Energy Market

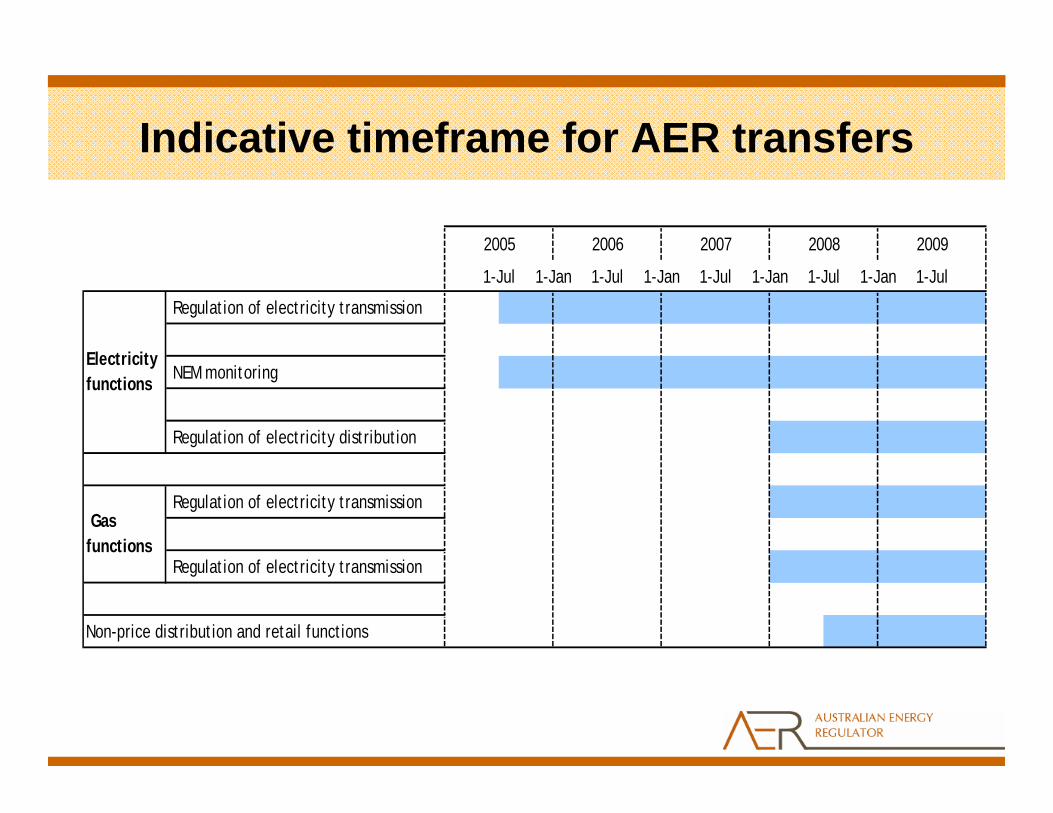

AER’s new functions

Indicative timeframe for AER transfers

Regulation of electricity transmission

NEM monitoring

Regulation of electricity distribution

Regulation of electricity transmission

Regulation of electricity transmission

Non-price distribution and retail functions

Electricity functions

Gas functions

1-Jan 1-Jul

2007 2008 2009

1-Jan 1-Jul 1-Jan 1-Jul

2005

1-Jul 1-Jan

2006

1-Jul

ElectraNet, SA, ET

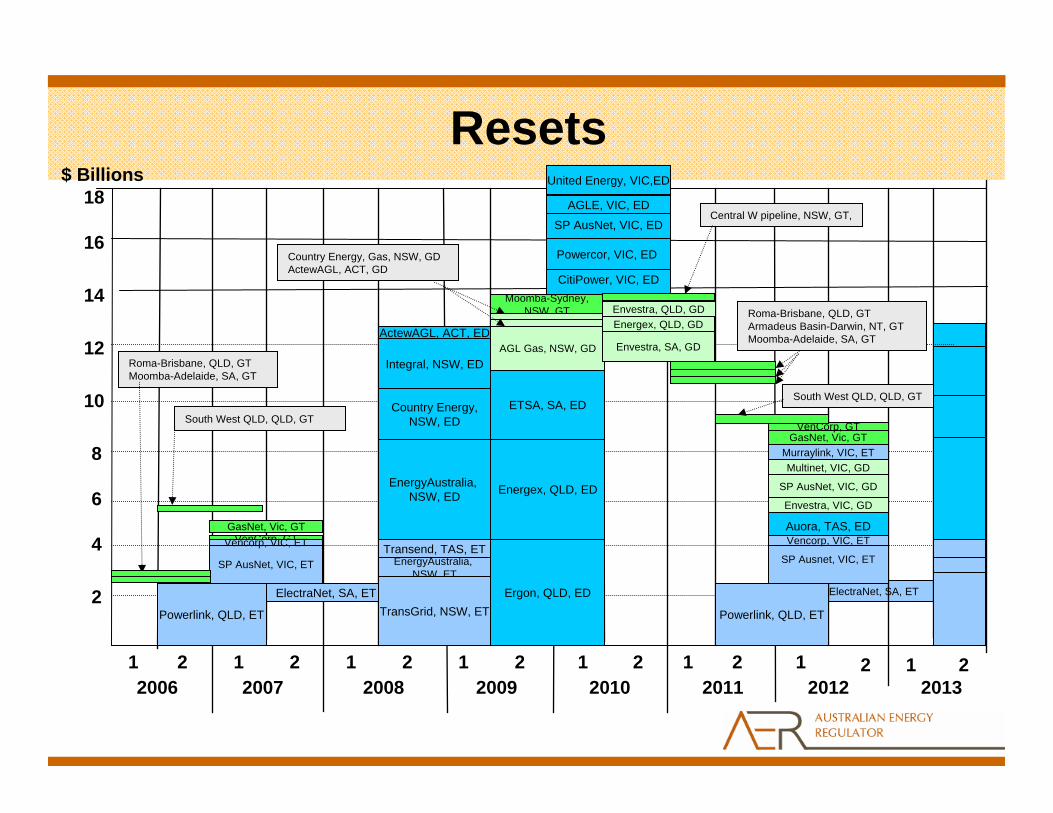

Resets

2010 201120082007 20092006 2012

2

6

4

8

10

12

14

16

18

20131 2 121 2 1 2 1 2 1

SP AusNet, VIC, ET

Powerlink, QLD, ET

Roma-Brisbane, QLD, GTMoomba-Adelaide, SA, GT

GasNet, Vic, GT

ElectraNet, SA, ET

Moomba-Sydney,NSW, GT

ActewAGL, ACT, ED

Country Energy,NSW, ED

Integral, NSW, ED

EnergyAustralia, NSW, ED

EnergyAustralia, NSW, ET

TransGrid, NSW, ET

Transend, TAS, ET

ETSA, SA, ED

Country Energy, Gas, NSW, GDActewAGL, ACT, GD

AGL Gas, NSW, GD

Energex, QLD, ED

SP AusNet, VIC, ED

AGLE, VIC, ED

CitiPower, VIC, ED

Powercor, VIC, ED

Central W pipeline, NSW, GT,

Roma-Brisbane, QLD, GTArmadeus Basin-Darwin, NT, GTMoomba-Adelaide, SA, GT

VenCorp, GT

Ergon, QLD, ED

2 21 1 2

Auora, TAS, ED

Powerlink, QLD, ET

SP Ausnet, VIC, ET

Vencorp, VIC, ET

Envestra, VIC, GD

SP AusNet, VIC, GD

Multinet, VIC, GDMurraylink, VIC, ET

Vencorp, VIC, ET

Envestra, QLD, GD

United Energy, VIC,ED

South West QLD, QLD, GT

GasNet, Vic, GTVenCorp, GT

South West QLD, QLD, GT

Energex, QLD, GD

Envestra, SA, GD

$ Billions

AER regulatory portfolio

Sector Number of regulated businesses / pipleines

Combined regulated asset base

Electricity transmission 9 $11 billion

Electricity distribution 13 $28 billion

Gas transmission 14 $3 billion

Gas distribution 11 $6 billion

47 $48 billion

New regulatory framework

• More prescriptive framework – certainty • Electricity & gas more aligned• Merit review extended to electricity• Light regulation option in gas• Tighter timeframes• Information powers stronger – and more

accountable

Preparation for new functions

• Internal capacity– Budget secured– Increase in staff numbers– Transfer of staff from the state regulators

• Regulatory guidelines – transmission and distribution

• Preparation for NSW resets

• Industry consultation

Objectives

• Committed to smooth transition to national framework

• Keen to pursue ways to improve the quality of regulation. Looking at:– consistent and timely processes established well up

front– streamlining implementation requirements through

standard information templates– ways to make regulation less intrusive but still robust– ways to effectively engage stakeholders

Conclusions

• AER is well prepared for transition to national regulation

• Electricity price shocks in 2007, but market has eased since July

• Gas prices rising in WA; price pressure in the east cushioned by CSM

• Extensive ownership consolidation• Strong investment and steady reliability in

regulated networks

Questions?