Keywords: Auctions, auction theory, matching theory, FCC auctions, package bidding, combinatorial bidding, Vickrey auction, activity rule, e-commerce, electronic commerce Ascending Auctions with Package Bidding By Lawrence M. Ausubel, University of Maryland and Paul Milgrom, Stanford University * This draft: June 7, 2001 Comments welcome! Abstract . A benchmark “package auction” is introduced in which bidders may determine their own packages on which to bid. If all bidders bid straightforwardly, then the outcome is a point in the core of the exchange economy that minimizes the seller’s revenue. When goods are substitutes, straightforward bidding strategies comprise an ex post Nash equilibrium. Compared to the Vickrey auction, the benchmark ascending package auction has cheaper information processing, better handling of budget constraints, and less vulnerability to joint bidding strategies among bidders who would otherwise be losers. Improvements are suggested that speed the auction and limit opportunities for collusion. 1. Introduction Asset sales often begin with an evaluation by the seller about how to divide an asset into suitable marketable pieces. A farm can be sold either as a single entity or in pieces comprising the house and barn, the arable land, other land, and perhaps water rights; radio spectrum licenses can cover an entire nation or be split among smaller geographic areas and the available set of frequencies in each area sold as a single unit or in smaller pieces; a large company can be sold intact to new owners or broken up into individual product divisions. The regulators, brokers, investment bankers and auctioneers who conduct these sales commonly consult potential bidders in an effort to identify which packages they find most attractive and which best advance the seller’s efficiency or revenue goals. 1 Some auction designs are flexible, allowing bidders a choice of packages on which to bid. For example, Cassady (1967) describes a sale of five buildings of a bankrupt real estate firm in which three buildings were defined to constitute a “complex.” An ascending auction was used for the sale, with bids accepted for either the individual buildings or for the complex. 2 * This paper builds upon and supercedes Ausubel (1997b) and Milgrom (2000c). We thank Evan Kwerel for inspiring this research, John Asker for his research assistance, particularly in evaluating the Cybernomics experiment, Eva Meyersson-Milgrom for surgical jargon-removal, and Peter Cramton, Ilya Segal, Valter Sorana, Lixin Ye and the referees for comments on previous drafts. 1 The revenue and efficiency criteria can lead to quite different choices; see Palfrey (1983). Milgrom (2000a) reports examples in which the sum of total value and auction revenue is constant across packaging decisions, so that there is a dollar for dollar trade-off between creating value and raising revenue. 2 Sometimes, bidders for large packages are required to bid on certain smaller packages as well. An example is an auction one author designed for selling the power portfolio of the Portland General Electric Company (PGE), which was adopted by the company and the Oregon Public Utility Commission. The auction design requires that bidders for the whole package of plants and contracts must also name “decrements” for individual power supply contracts on which there are competing individual bids.

Ascending Auctions with Package Bidding By Lawrence M. Ausubel, University of Maryland and Paul Milgrom, Stanford University* This draft: June 7, 2001 Comments welcome!

Abstract. A benchmark “package auction” is introduced in which bidders may determine their own packages on which to bid. If all bidders bid straightforwardly, then the outcome is a point in the core of the exchange economy that minimizes the seller’s revenue. When goods are substitutes, straightforward bidding strategies comprise an ex post Nash equilibrium. Compared to the Vickrey auction, the benchmark ascending package auction has cheaper information processing, better handling of budget constraints, and less vulnerability to joint bidding strategies among bidders who would otherwise be losers. Improvements are suggested that speed the auction and limit opportunities for collusion.

1. Introduction Asset sales often begin with an evaluation by the seller about how to divide an asset

into suitable marketable pieces. A farm can be sold either as a single entity or in pieces comprising the house and barn, the arable land, other land, and perhaps water rights; radio spectrum licenses can cover an entire nation or be split among smaller geographic areas and the available set of frequencies in each area sold as a single unit or in smaller pieces; a large company can be sold intact to new owners or broken up into individual product divisions. The regulators, brokers, investment bankers and auctioneers who conduct these sales commonly consult potential bidders in an effort to identify which packages they find most attractive and which best advance the seller’s efficiency or revenue goals.1

Some auction designs are flexible, allowing bidders a choice of packages on which to bid. For example, Cassady (1967) describes a sale of five buildings of a bankrupt real estate firm in which three buildings were defined to constitute a “complex.” An ascending auction was used for the sale, with bids accepted for either the individual buildings or for the complex. 2

* This paper builds upon and supercedes Ausubel (1997b) and Milgrom (2000c). We thank Evan Kwerel for inspiring this research, John Asker for his research assistance, particularly in evaluating the Cybernomics experiment, Eva Meyersson-Milgrom for surgical jargon-removal, and Peter Cramton, Ilya Segal, Valter Sorana, Lixin Ye and the referees for comments on previous drafts. 1 The revenue and efficiency criteria can lead to quite different choices; see Palfrey (1983). Milgrom (2000a) reports examples in which the sum of total value and auction revenue is constant across packaging decisions, so that there is a dollar for dollar trade-off between creating value and raising revenue. 2 Sometimes, bidders for large packages are required to bid on certain smaller packages as well. An example is an auction one author designed for selling the power portfolio of the Portland General Electric Company (PGE), which was adopted by the company and the Oregon Public Utility Commission. The auction design requires that bidders for the whole package of plants and contracts must also name “decrements” for individual power supply contracts on which there are competing individual bids.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 2

In the last few years, there has been growing interest in allowing bidders much greater freedom to name the packages they bid on during the auction. The plan for FCC spectrum auction #31, which will sell licenses in the 700 MHz band, permits bids for any combinations of the twelve licenses on offer. Other examples include proposed auctions for industrial procurement on the Internet in which individual sellers may offer all or part of a bill of materials and services sought by buyers (Milgrom, 2000b).

Package auctions can take the form of sealed bid auctions, such as the Vickrey (1961) package auction or the Bernheim-Whinston (1986) menu auction. The present study is the first theoretical exploration of ascending package auctions. These are auctions in which bidders may bid on any packages they choose and may add new packages and increase bids during the course of the auction. The eventual winning bids are the ones that maximize the total selling price of the goods.

Ascending package auctions have attracted increasing interest for a variety of reasons reviewed in section 2. Subsections discuss advances in technology, changes in spectrum regulation, limitations of the generalized Vickrey auction, theory and experience with the FCC’s simultaneous ascending auction (SAA), and evidence from economics laboratories regarding the performance of an ascending package auction design.

The formal analysis begins in Section 3 with descriptions of the package exchange problem and the benchmark ascending package auction. That section also introduces a particular myopic strategy, which we call “straightforward bidding,” which may account for the performance of bidders in certain laboratory settings.

Section 4 is devoted to an exploration of package auctions with straightforward bidding as a new kind of “deferred acceptance algorithm,” similar in key respects to the ones studied in two-sided matching theory. For this purpose, we introduce the coalitional game that corresponds to the package economy. Just as deferred acceptance algorithms terminate at points in the core in two-sided matching models, the benchmark auction “algorithm” terminates at a point in the core of the package exchange economy. Just as the deferred acceptance algorithms select points in the core in two-sided matching models that are least preferred by the side receiving offers, the ascending package auction with straightforward bidding selects a core point at which the seller’s revenue is minimized. When bidders regard the items for sale as mutual substitutes and when there are no budget constraints, the benchmark auction also duplicates the property of deferred acceptance algorithms in some two-sided matching models that truthful reporting of preferences by the offering side—the buyers in our case, is a dominant strategy. In the present context, that conclusion takes the form that each bidder’s payoff in the benchmark auction is equal to its equilibrium payoff in the generalized Vickrey auction.

In section 5, we explore these results further. We show that the condition that bidders are mutual substitutes in the coalitional game is very closely related to the condition that the goods are mutual substitutes for the bidders. In addition, we show that some of the main results apply as well when bidders are budget-constrained.

The incentive analysis in section 4 is limited to consideration of the revelation game associated with the straightforward bidding, but the actual ascending auction admits many strategies that are far from straight forward. So, in section 6, we study whether straightforward bidding is an ex post Nash equilibrium of the ascending auction. We find

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 3

that it is not so in general. Straightforward strategies do comprise a Nash equilibrium when goods are mutual substitutes or when there are just two bidders or when the winning bidder wants the package of the whole. In general, if competitors bid straightforwardly, a strategy that is a best reply whether goods are substitutes or not is to bid as slowly as possible.

We compare the characteristics of the benchmark auction to those of the Vickrey auction in section 7. Although the Vickrey auction has well-known advantages, the benchmark auction has potentially important advantages over the Vickrey auction as well. These include less vulnerability to certain kinds of collusion (important when the items for sale can be complements), lower package evaluation costs (important when there are many items to be packaged), and greater flexibility in specifying preferences (important when budget constraints are tight).

Section 8 includes suggestions that would ensure quicker completion of the ascending auction and that eliminate retaliatory strategies that might be used to enforce a low-price outcome. Section 9 concludes.

2. Background A variety of developments have contributed to the present drive to develop and

implement package auctions. These can be grouped into three general categories: rapid advances in technology, favorable developments in regulated spectrum markets and unregulated Internet exchange markets, and research that highlights the potential benefits of package auctions.

2.1 Changing Technology and Markets The most important group factors contributing to the new package bidding designs is

associated with the rapid advance of technology, which enables certain new auction designs. To understand the technical challenge, suppose that bidders submit bids for overlapping packages. Given these bids, the first step of finding the sets of “consistent” bids in which each individual item is included in just one package (“sold just once”) is a hard computational problem. Then, the total bid associated with each such package must be computed and the revenue-maximizing set of “consistent” bids must be found. All this must be done quickly, while bidders sit in front of their individual computer terminals.

To get an idea of the size of the problem, consider the proposed FCC auction 31 of licenses in the 700 Mhz range in the US for use in commercial wireless communications. The twelve licenses on offer allow for 4095 distinct combinations involving between one and twelve licenses. A decade ago, this number of combinations might have overwhelmed users and posed serious computational problems. Now, however, there are processors, interfaces, algorithms, and communications systems that make it practical for users to identify and bid for many combinations, for auctioneers to compute optimal bid combinations, and for all to verify and track the progress of the auction, even from remote locations.3

3 The computational aspect of package bidding is surveyed by deVries and Vohra (2001).

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 4

Even as technology was advancing, markets were changing in ways that facilitate the adoption of sophisticated auction designs. The adoption of US legislation authorizing spectrum auctions in 1993 and the bold decision by the Federal Communications Commission (FCC) the following year to adopt the computerized simultaneous ascending auction (SAA) gave an important boost to advocates of more sophisticated auction designs. The perceived successes of spectrum auctions have led some to propose even more ambitious designs.

In Australia, spectrum regulators eager to “let the market decide” all details of the allocation initiated a serious discussion about the sale of “postage stamp” sized licenses. These would entail very small geographic areas and narrow slivers of bandwidth to be licensed and ultimately recombined as desired by spectrum buyers. Those proposals were shelved because of concerns that the complementarity among the licenses might make the auction and subsequent resale markets perform poorly.

Shortly afterward, another area of high- tech applications began to develop as Internet-based businesses raced to develop electronic markets that could serve the needs of business customers. Often, industrial buyers seek to purchase not just single components but all the materials and services for a large project, such as a construction project. Multiple suppliers may each supply part of the buyer’s needs on terms that may involve quantity discounts, which make the buyer’s procurement optimization problem a non-convex one. If such procurements are to be managed by competitive bidding, then some form of package auction will be needed, and supporting software for these auctions has recently become available.

These developments and others have inspired new research by economists, operations researchers and computer scientists into the theory and practice of package bidding.

2.2 Vickrey Auctions: Advantages and Disadvantages The theory of package bidding, like so much of auction theory, began with the

seminal paper by William Vickrey (1961), which focused on sales involving a single type of good. Vickrey’s mechanism can be described as follows. Each bidder is asked to report to the auctioneer its entire demand schedule for all possible quantities. The auctioneer uses that information to select the allocation that maximizes the total value. It then requires each buyer to pay an amount equal to the lowest total bid the buyer could have made to win its part of the final allocation, given the other bids. Vickrey showed that, with this payment rule, it is in each bidder’s interest to make its “bid” correspond to its actual demand schedule, regardless of the bids made by others. Subsequent work by Clarke (1971) and Groves (1973) demonstrated that a generalization of the Vickrey mechanism leads to the same “dominant strategy property” in a much wider range of applications. In particular, Vickrey’s conclusion holds even when there are many types of goods, provided the original requirement to make bids for “all possible quantities” is replaced by the requirement to make bids on “all possible packages.” This extension has come to be known as the “generalized Vickrey auction” or as the “Vickrey-Clarke-Groves (VCG) mechanism.”

These discoveries had profound ramifications. For some operations researchers, they seemed to reduce the economic problem of auction design to a computational problem. If

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 5

only one could describe and compute values and allocations quickly, it seemed, then the generalized Vickrey auction would become a practical solution to a wide range of resource allocation problems.

For economists, Vickrey’s findings raised expectations about the possibility of designing effective auctions using economic analysis. Vickrey’s analysis, however, was based on particular assumptions and a particular framing of the auction problem, making it natural to ask: How well would the generalized Vickrey auction perform if Vickrey’s simplifying assumptions were relaxed and the frame of analysis widened?4 As it has turned out, investigating that question has revealed defects that limit the practical usefulness of the Vickrey design.5

One assumption of the Vickrey analysis is that the bidder knows all its values or can compute them costlessly, but the sheer number of combinations that a bidder must evaluate to bid in the auction calls that assumption into question. Compared to many of the costs involved in conducting combinatorial auctions, bidder valuation costs are relatively less affected by advancing technologies, because the valuation of large assets requires substantial human inputs.6 Potential buyers who find it too expensive to investigate every packaging alternative will instead choose a few packages to evaluate fully. Good auction design requires accounting for the way those choices are made as well as the evaluation costs that bidders incur.

Compounding the problem is that when package evaluation is costly, the choice of which packages to evaluate is itself a strategic problem, because the profitability of a bidder’s choices depends on other bidders’ choices. For example, suppose the items offered in an auction are {ABCD}. It does little good for a bidder to bid for package AB unless someone else is bidding either on CD or on C and D separately. In a Vickrey auction, if it is too costly to eva luate all the packages, then bidders must guess about which packages are most relevant and how to allocate their limited evaluation resources.

4 Vickrey’s own work expresses doubt about the usefulness of his invention, based on the idea that it would be too costly, but that doubt appears to be misplaced. Williams (1999) finds that all Bayesian mechanisms that yield efficient equilibrium outcomes lead to the same expected equilibrium payments as the generalized Vickrey auctions. This establishes that any tradeoff between payments and efficiency is inherent in the problem and not a special consequence of Vickrey’s design. 5 The following discussion of disadvantages of the Vickrey auction draws heavily from a report to the FCC by Charles River Associates and Market Design Inc (1997). The reports to the FCC and related papers were presented at a conference sponsored by the FCC, the National Science Foundation, and the Stanford Institute for Economic Policy Research. See http://www.fcc.gov/wtb/auctions/combin/papers.html. 6 Valuing significant business assets involves both investigating the asset itself and creating business plans showing how the assets will be used. For example, a bidder hoping to purchase parts of an electrical generating portfolio might investigate the physical condition of each plant, the availability of land and water for cooling to allow plant expansion, actual and potential transmission capacity, and other physical variables. In addition, it will consider labor and contractual constraints, zoning and other regulatory constraints, the condition of markets in which power might be sold, partnerships that might enhance the asset value, and so on. The final valuation is the result of an optimization over business plans using all this information, and tempered by human judgment. When the assets in the collection interact in complex ways that affect the optimal business plan, then significant extra costs must be incurred to evaluate each package.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 6

In comparison, a multi- round ascending auction economizes on the need to guess because bidders can adapt their plans based on observations made during the auction. 7

The Vickrey design is unusually vulnerable to coordinated deviations that bidders might make to another Nash equilibrium, in which bidders’ profits are higher but the seller’s revenue and the value-created are less. Most strikingly, there can be profitable joint deviations among losing bidders in the Vickrey auction, in which each bidder raises its bid at no cost to itself in a way that reduces its partners’ winning prices.8

Another characteristic of the Vickrey auction that is sometimes considered a drawback is its use of explicit price discrimination: two bidders may pay different prices for identical allocations, even when both have made the same bids for those allocations.9 Such discriminatory prices are sometimes illegal and often regarded as “unfair.”

Compared to standard auction designs in which winning bidders pay what they bid, the performance of the Vickrey auction is uniquely sensitive to certain assumptions of the standard models. Various analyses find that these “pay-as-bid” auctions perform better than Vickrey auctions in models with effective limits on bidder budgets,10 “common value” and “almost common value” uncertainty (Milgrom (1981), Klemperer (1998)), or endogenous entry decisions (Bulow, Huang and Klemperer (1999)).

Finally, the revelation of bidders’ maximum willingness to pay during the auction can be problematic (Rothkopf, Teisberg and Kahn (1990)), at least for non-computerized auctions in which secure encryption technologies are not available. Winning bidders may

7 See also the discussion of advantages of ascending auctions over sealed-bid auctions in the Introduction of Ausubel (1997a). 8 Here is such an example, suggested by Jeremy Bulow. Suppose that A’s values are (5,5,5), B’s are (5,5,5) and C’s are (0,0,20). In a Vickrey auction, if the bidders play their weakly dominant strategies, C will win the pair and pay a price of 5+5=10, while A and B win nothing and pay nothing. If, however, A and B discuss the matter beforehand without C’s knowledge, they could agree to play the (weakly dominated) Nash equilibrium in which A and B each bid 100. With those strategies, each wins one item at a price of zero! The same deviation is profitable when C’s valuation is (0,0,8), but in that case the profitable joint deviation is among winning bidders rather than among losers. 9 To illustrate the price discrimination problem, suppose there are two bidders—A and B—and two items —X and Y. A valuation for a bidder is a triple (x,y,z), specifying how much the bidder would be willing to pay for item X alone, item Y alone, and the package XY. Suppose the parties report valuations of (12,12,13) and (12,12,20). The result is that A and B will each be awarded an item (at an efficient allocation, either bidder may get either item) at prices of 8 and 1 respectively, even though the items are perfect substitutes and bidders A and B made identical bids for the individual items.

When the items are not identical, the price discrimination is not so obvious, but the auction outcome is not generally “envy free”: a bidder may prefer the price and allocation assigned to another bidder and may complain on that basis. 10 Che and Gale (1998) compare first-price and second-price auctions in the face of budget constraints, but the main point here is somewhat different. To illustrate, suppose there are two identical items. A bidder X has value of 5 for one item and 10 for the pair, but has a budget of just 6, which limits its bids. If X has a single competitor with values of 3 for one item and 7 for a pair and bids accordingly, then X must bid at least 4 in a Vickrey auction to acquire a single item. If, however, X’s competitor has a value of 3 for one item and 5 for the pair, then the same bid would cause X to lose one item. In that case, X should instead bid no more than 2 for one item and 6 for the pair in order to acquire both. Notice that in each case the Vickrey price is less than X’s budget, but sincere bidding is nevertheless not optimal for X and indeed X has no dominant strategy.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 7

fear that information revealed by their bids will be used by auctioneers to cheat them or by third parties to disadvantage them in some negotiation. Similarly, the public has sometimes been outraged when bidders for government assets are permitted to pay significantly less than their announced maximum prices in a Vickrey auction (McMillan (1994)). A bidder’s motive to conceal its information can destroy the dominant strategy property that accounts for much of the appeal of the Vickrey auction. 11,12.

These drawbacks of the Vickrey auction have created interest in exploring multiple round designs in which bidders must pay the amounts of their own winning bids. The multiple rounds feature provides feedback to bidders about relevant packages, economizes on bidder evaluation efforts, conceals the winning bidder’s maximum willingness to pay, and may lead to better performance in settings with “almost common values.” The pay-as-bid feature may discourage the type of “collusive” strategies sometimes possible in a Vickrey auction, in which a bidder increases its own bid solely to reduce a collaborator’s price. The two features combined may alleviate problems associated with budget constraints and The next sections consider two such designs: the simultaneous ascending auction (SAA), which entails no package bidding, and the simultaneous ascending auction with package bidding (SAAPB).

2.3 Simultaneous Ascending Auctions The simultaneous ascending auction, which has been employed by the FCC in the US

for most of its radio spectrum auctions, differs from the Vickrey auction in two ways that have made it an attractive practical alternative to the Vickrey auction: it is a pay-as-bid, multiple round auction design.

The auction design has an iterative structure, with the “state of the auction” after each round described by the identities of the standing high bidders and the amounts of the standing high bids for each item. Initially, the standing high bid for each item is zero13 and the standing high bidder is the seller. During each round, bidders may raise the bid by an integer number of increments on any items that they wish, which determines new bidders and standing high bids. The process repeats itself until there is a round with no new bids on any item. At that point, bidding on all items is closed and the standing high bids determine the prices. As described earlier, there is also an activity rule designed to ensure that bidding activity starts out high and declines during the auction as prices rise far enough to discourage some bidders from continuing.

Although early experimental testing of the SAA demonstrated that it performed well in some environments possibly resembling the FCC environment (Plott (1997)), it has a 11 Notice that a similar case can be made against ordinary first-price auctions, since the theoretical bid functions are invertible to reveal bidders’ values. In this respect, ascending auctions are theoretically superior to both kinds of sealed bid auctions because they better conceal the winning bidder’s valuation. 12 Another disadvantage of the Vickrey auction that, relative to uniform pricing rules, it tends to promote inefficient pre-auction mergers or joint bidding when the items for sale are substitutes. The reason is that such mergers result in lower Vickrey auction prices for the merged firm or joint bidders without affecting the prices paid by others. This contrasts sharply with incentives in markets where the same price is paid for each unit sold. In such markets, it is the non-participants who benefit most from any non-efficiency-enhancing merger, which can make such mergers hard to arrange. 13 A reserve price may also be used.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 8

variety of theoretical limitations. The two most important of these are the incentives it provides for inefficient withholding of demand in the case goods are substitutes and its degraded performance in laboratory experiments in which the substitutes condition fails (Ledyard, Porter and Rangel (1997)), a condition that may have applied to the radio spectrum auctions (Ausubel, Cramton, McAfee and McMillan (1997)). To explain the role of the substitutes condition in theoretical terms, we compare two different situations.

In the first situation, the items for sale are mutual substitutes14 for all the bidders. In addition, the bid increment is “small” and the initial prices are low enough to attract at least one bid during the auction for every item. In such cases, suppose bidders bid “straightforwardly” at each round for the items in a package they most prefer at the current prices. Then, the final allocation is efficient and the final prices are competitive equilibrium prices for an economy with “almost” the same values as the actua l economy, differing by at most the relevant bid increment (Milgrom, 2000a).

The preceding result demonstrates several interesting conclusions for the case when goods are substitutes. First, market-clearing prices do exist, despite the indivisibility of the items offered for sale. Second, the information communicated during the course of the SAA is rich enough to allow the auction algorithm to discover equilibrium prices and allocations. Third, the auction algorithm can recover from some kinds of anomalous bidding behavior early in the auction. Starting from any prices that are sufficiently low, the sequence of prices and allocations under straightforward bidding from that point onward still converges to equilibrium prices and an efficient allocation.

In the second situation, some items are sometimes complements.15 In that case, all the conclusions change drastically. Indeed, let S denote the set of valuations in which bidders regard the items as substitutes. If T is any strict superset of S and provided that there are at least two bidders, there exists a profile of valuations drawn from T such that no competitive equilibrium exists (Milgrom, 2000a).

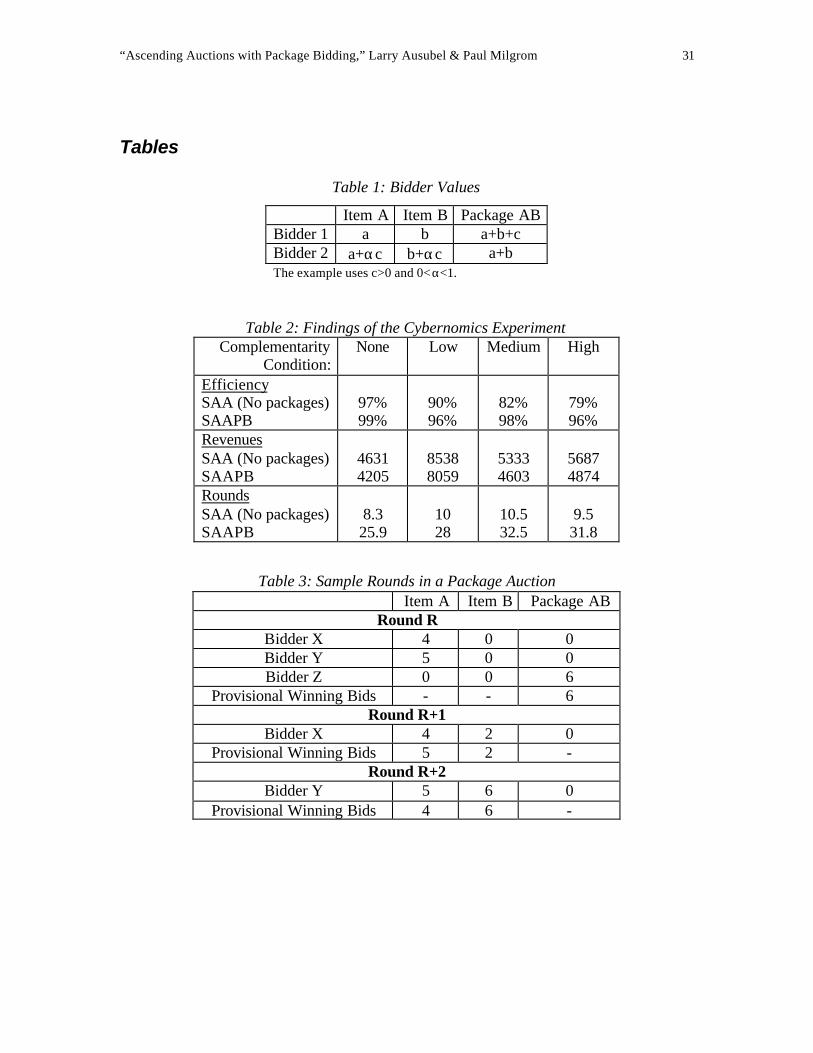

Intuition for this result is provided by Table 1, which tabulates bidder values. In the table, bidder 1’s va lues are an arbitrary set of values in which the two licenses are complements. Bidder 2’s values are then constructed so that (1) the items are substitutes for bidder 2 and (2) the unique efficient outcome is for bidder 1 to win both licenses. By the first welfare theorem, if a competitive equilibrium exists, then the outcome is efficient. Suppose it is so and let pA and pB be the equilibrium prices. Since 2 doesn’t demand either good at equilibrium, it must be true that α+ ≤ Aa c p and α+ ≤ Bb c p . On

14 The common terms, “net substitutes” and “gross substitutes,” emphasize the distinction between compensated and uncompensated demand. Since models of corporate bidders in the FCC auctions invariably abstract from wealth effects, compensation is irrelevant for them. The important point here is “mutuality”—each good is a substitute for each other good. This mutual substitutes property may be defined by supermodularity of the expenditure function, as in Milgrom and Roberts (1991). For an alternative formulation that treats preferences as primitives, see Gul and Stacchetti (1999). 15 The idea that price formation processes behave drastically differently in the cases of substitutes and complements has a long history in economics. Arrow, Bloch and Hurwicz (1959) first established the stability of tatonnement in the case of gross substitutes. Milgrom and Roberts (1991) showed that the same sort of stability holds over a vast set of discrete and continuous time, synchronous and asynchronous, backward- and forward-looking price-setting processes. Scarf (1960) provided examples of global instability in the case when the goods are complements, sharply contrasting with the case for substitutes.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 9

the other hand, since 1’s purchases both goods at equilibrium, we may infer that + + ≥ +A Ba b c p p . For α>½, these inequalities are inconsistent: the contradiction

establishes that no market clearing prices exist.

In the example just described, if bidder 1 does not know whether α>½, then it may face a difficult bidding problem. Suppose that its competitor, bidder 2, bids straightforwardly. To win both items, bidder 1 will have to bid more than a for item A and more than b for item B. Consider the situation at any time after the prices exceed a and b and bidder 2 places a bid on, say, item A. If bidder 1 stops now, it will wind up acquiring only item B for a price greater than its value b to the bidder. If α>½ and if it continues to bid, it will eventually find that the total price exceeds a+b+c. At that point, it has no hope of avoiding a loss. For an efficient outcome always to emerge, bidder 1 must always take this risk and always decide in this situation to stop bidding and accept the loss from acquiring a single item, but this is rarely the optimal strategy. Thus, one might expect to find inefficient outcomes and bidder losses as common occurrences in circumstances like this one.

The problem facing a bidder for whom goods are sometimes complements has come to be called the “exposure problem.” In 1994, the FCC adopted a rule permitting bid withdrawals under some circumstances to mitigate it. Experimental evidence (Porter, 1997) suggests that withdrawal do mitigate the problem, but they do not solve it completely.

2.4 Experimental Evaluation of Ascending Auction Designs Besides theoretical considerations, contributions by economic experimenters played a

crucial role. Particularly influential was a study sponsored by the FCC and conducted by Cybernomics (2000) comparing the experimental performance of the SAA to that of a particular combinatorial auction called the simultaneous ascending auction with package bidding (SAAPB). The major findings of that study are summarized in Table 2 below.

The study was conducted under four experimental conditions. In the first, a bidder’s value for any package was equal to the sum of its values for the individual items in the package. This condition involves no complementarities. The remaining three conditions involved increasing amounts of complementarity, labeled low, medium and high. Bidder values were drawn at random for each experimental condition and were used twice, once for a group of subjects participating in the non-package auction—the SAA—and once for a group participating in the package auction—the SAAPB. Efficiency in the study was measured by the ratio of the total value of the allocation resulting from the auction to the maximum of that total over all possible allocations.

The experimental results show several prominent features. First, the measured efficiency of the SAA falls off markedly as complementarities increase, but the efficiency of the package auction is largely unaffected by complementarity. 16 Second, the SAAPB

16 In the experiments, the ascending package auction generates higher efficiency than the SAA even when there are no complementarities, although the reported difference is small. The theoretical analysis for the case of substitutes provides a possible explanation: the straightforward bidding that supports efficient allocations is incentive-compatible in the package auction, but not in the SAA.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 10

took roughly three times as many rounds to reach completion, compared to the SAA. In addition, revenues are higher in all conditions for the SAA compared to the SAAPB.

All experiments require making implementation choices that may affect the experimental outcome. For that reason, experimental results are most convincing when similar results are obtained under a variety of relevant conditions. In the present case, the Cybernomics experiment was constructed to involve a simple kind of complementarities that make it relatively easy to compute optimal allocations. This is problematic for two reasons: the selected complementarities appear unlikely to reflect those in the structure of the actual FCC auction and, viewing the package auction as an optimization algorithm, the relative simplicity of the package optimization problem might have influenced the experimental outcome.

The Cybernomics experimental setting may also have offered less scope for strategic manipulation of the rules than the FCC auction setting. There are several reasons to suspect this. First, the experimental subjects’ lack of information about other bidders’ values is not typical of FCC spectrum auctions and make it harder for them to exploit the strategic opportunities that the auction affords. Compounding this is the fact that rounds were relatively short, affording subjects little opportunity to evaluate others’ bids and assess the strategic opportunities. Third, the relatively long training sessions that subjects required seemed to highlight their difficulty in understanding the rules, further limiting their ability to exploit gaps in the rules. Long as these sessions were, they fall far short of the preparation undertaken by bidders in the FCC auctions, where the stakes are also very much higher. Finally, unlike bidders in the FCC auction, subjects in the experiments had no access to expert assistance or to analyses that could pinpoint opportunities for strategic bidding.

Despite these limitations, the history of successes of various “combinatorial auctions” in laboratory settings, beginning with the experiments by Rassenti, Smith and Bulfin (1982), makes it important to review the Cybernomics results seriously. In the next two sections, we provide a theoretical analysis that seeks to account for the results of the Cybernomics experiments and to explore more generally the strategic opportunities that such auctions create.

3. The Benchmark Package Auction Let there be finite number N of types of items to be sold and let 1( , . . . , )NM M M=

denote the number of items of each type. A “package” A=(A1,…,AN) is a vector of integers whose components indicate the number of units of each type in the package. The relevant packages in the auction are those for which 0 ≤ A ≤ M; let [0,M] denote this set.

An important special case arises when M is a vectors of 1’s, meaning that the auction treats each item as unique. This condition is common in the FCC auctions, including the planned package auction #31. Although there is no loss of generality in limiting attention to this case, as a practical matter is can be advantageous to identify groups of similar items as identical. Setting Mk >1 reduces the number of possible bids—sometimes drastically so—and ensures that equivalent packages receive equal bids.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 11

The set of auction participants L consists of the seller, designated by l = 0, and the buyers, designated by 1, . . . , | | 1l L= − . Each individual l has a valuation vector

( : [0, ])l lAv v A M= ∈ . Component lAv specifies the maximum amount that l is willing to pay to acquire package A. We limit and simplify our analysis by the following assumptions:

(i) Private values: each bidder l knows its own value vector vl; it does not change its value when it learns about what others are willing to pay.

(ii) Quasilinear utility without externalities: a. A bidder l that acquires package A and pays price lAb earns a net payoff of

−lA lAv b , which does not depend on what l’s competitors acquire. b. A bidder l that acquires nothing and pays nothing earns a net payoff of

zero: 0 0lv = .

(iii) Monotonicity (Free Disposal): For all l and A B≤ , lA lBv v≤ .

(iv) Zero seller values: 0 0≡Av .

Assumption (i) rules out the possibility of “common value” elements (Milgrom and Weber, 1982), in which the factors that affect value are the same for various bidders but in which bidders have different estimates of those values. In the spectrum auctions, the relevant factors include technology and demand forecasts. Rational bidders should often respect common value estimates made by a competitors’ analysts as much as or more than the estimates made by their own analysts—a fact that can have a profound impact on bidding strategy. Our conjecture is that dynamic auctions have an advantage in mitigating inefficiencies that result from common values, but we do not analyze that here.

Assumption (ii) rules out a class of issues that were first emphasized by Jehiel and Moldovanu (1996). Particularly, in spectrum auctions, buyers do interact after the auction and these can influence bidding behavior.17 Nevertheless, we abstract from this issue to make progress on other important aspects of the auction design.

The last two assumptions are relatively innocuous.

The next modeling/design issue is the form that package bidding may take. The most flexible sort of package bidding is the kind used in the generalized Vickrey auction, in which bidders are free to make mutually exclusive bids on as many packages as they may wish. Such a rule imposes no restrictions on what packages the bidder may name and no restrictions on what amounts it may bid for different packages.

For practical purposes, other rules governing packages have sometimes been adopted in which different bids from a single bidder are not mutually exclusive. Allowing such bids in addition to mutually exclusive bids would have no consequences for our

17 See also Jehiel and Moldovanu (2001) and the references therein, as well as Das Varma (2000a&b).

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 12

theoretical analysis, for allowing such bids merely enriches the language in which the complete bid vector can be expressed.18

Auctions that permit only bids that are not mutually exclusive restrict the bidder’s options. A bidder who wishes to buy package A or B but not both finds its options limited.

The plans for FCC auction 31 include a combination of exclusive and non-exclusive bids. Bids made in different rounds are treated as mutually exclusive, but bids made in the same round are not. A bidder who prefers its bids made in different rounds to be treated as non-exclusive can accomplish that by “renewing” old bids in the current round. By making bids for substitute packages in different rounds, bidders in the FCC auction will enjoy much of the same flexibility as in the benchmark auction design.

Many more details, including ones that are left unspecified in standard game theoretic analyses,19 are needed to complete the rules of a practical auction design. The rules that figure into our analysis are the following ones.20

First, all bids are firm offers. A bidder can never reduce or withdraw a bid it has made on any package. Any new bid a bidder makes on any package A must be positive and must exceed the bidder’s best previous bid on A by some integer number of bid increments.

Second, after each round in the benchmark model, the auctioneer identifies a set of “provisionally winning bids.” This is the set of bids that maximizes the total price, subject to two kinds of constraints: each bidder may own only one provisionally winning bid and at most Mn items of type n may be sold. We suppose that, as in the FCC design, the auctioneer announces the full history of winning and losing bids after each round (although straightforward bidders will not utilize all that information).

Third, the auction continues round by round until there are two consecutive rounds with no new bids. The auction then ends and the provisionally winning bids at that time become the winning bids in the auction.

In contrast to the SAA, no “activity rules” are included in the benchmark auction. Excluding such rules from the benchmark auction prepares us to analyze their significance later in this paper.

Several other differences between the benchmark auction and the SAA merit special emphasis. First, the minimum bids can differ among bidders on any item or package. This feature is important in accelerating the auction without preventing it from supporting efficient outcomes. Second, a bid that was a losing bid at round t can become a provisional winner at later round, such as round t+1. This is illustrated in Table 3 by the bid of 5 by bidder Y, which becomes a provisional winner in round R+1 even though it 18 Nissan (1999) investigates the expressive power of various “languages” for package bidding, supposing that the objective of a bidding language is to express the richest possible set of plausible preferences as succinctly as possible. 19 The details omitted in conventional game theoretic analyses include how long each bidder has to submit its bid, the design of the user interface, how much discretion the auctioneer has to make exceptions, and many more. 20 A version of the benchmark auction is described in detail in Ausubel (2000).

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 13

was not one in round R. Third, the price of an item or package can decrease from round to round. This is illustrated in the table by the fall in the price of Item A from 5 in round R+1 to 4 in round R+2. In the SAA, prices for individual items can never fall. The fact that bids may change from losing to winning explains why, in the SAAPB, it is necessary to specify whether bids from previous rounds remain binding on bidders.

These are complicating features that make the auction less transparent for onlookers and that create certain new strategic bidding issues. Nevertheless, without these features, straightforward bidding would not generally lead to such nearly efficient outcomes, as described in the next sub-section.

3.1 Bidding Strategies Let Ht denote the list, or “history” of bids made by all bidders up to and including

round t. Let ( , )=tlA l tB B H A denote the highest bid made by bidder l for package A up to

time t and let 0 0≡lAB . We assume for simplicity that the seller sets reserves of zero for all packages.

A bidding strategy bl for any bidder l is a map from histories to new bids that satisfies the minimum bid restriction that, for every package A, 1−> ⇒t t

lA lAb B 1 1t t tlA lA lAb B I− −≥ + ,

where 11( , )−

−≡tlA l tI I H A is the bid increment applicable to bidder l for package A at round

t. One may equivalently describe l’s strategy in terms of the function Bl, requiring that 1t t

lA lAB B −≥ and that 1t tlA lAB B −> ⇒ 1 1t t t

lA lA lAB B I− −≥ + .

3.2 Round by Round Optimization

The doubly indexed vector ( ; , [0, ])lAx x l L A M= ∈ ∈ designates a “package assignment” or “allocation,” with xlA=1 indicating that bidder l is assigned package A. The allocation is “feasible” if:

[0, ]

[0, ]1

{0,1} ,

lAl L A M

lAA M

lA

x A M

x l L

x l L A

∈ ∈

∈

≤

= ∈

∈ ∈

∑ ∑∑ (1)

The first constraint is a vector constraint. It says that the total number of each type of item assigned to all buyers cannot exceed the number available. The second constraint says that each bidder is allocated precisely one package (which may be the null package). The last requires that x be a vector of zeros and ones. When these feasibility conditions are satisfied for the available package M, we write ( )x F M∈ .

The provisional winning allocation for round t, x*t maximizes the sum of the provisionally accepted bids. This sum can be written explicitly or, equivalently, using dot-product notation:

*

[0, ]( ) ( )

argmax argmaxt t t t tlA lAl L A M

x F M x F M

x B x B x∈ ∈

∈ ∈∈ =∑ ∑ i . (2)

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 14

Let us assume that in case there are multiple optima in (2), there is some fixed tie-breaking rule that depends only on the vector of best bids ( ); , [0, ]t t

lAB B l L A M= ∈ ∈ .

3.3 Straightforward Bidding We now investigate a strategy in which bidders bid “straightforwardly” at each round

on the package that has the highest profit potential. Professor Charles Plott has called this strategy “bidding the gradient” and observed that it is consistent with the behavior of some bidders in his package auction experiments.

The lowest price that l can bid for any package A at round t is l’s highest bid from the previous round if l was the provisional winner, or otherwise that bid plus one increment:

1 * 1

1 1

if 1

otherwise

− −

− −

== +

t tlA lAt

lA t tlA lA

B xB

B I (3)

Let π = −t tlA lA lAv B be called l’s “potential profit” from a bid on A at round t; let

max(0,max )t tl A lAπ π= ; and let ( )t

l lA v be the set of packages that achieve the maximum potential profit and for which that profit is strictly positive. Then, the straightforward bidding strategy ˆ( )lb v is the strategy in which l makes new bids only on the packages in

( )tl lA v and makes the minimum bid t

lAB on each of those. The strategy can be described mathematically by:

1

if ( )ˆ ( ) otherwise−

∈=

t tlA l lt

lA l tlA

B A A vB v

B (4)

Theorem 1. Let ε > 0 be an upper bound on the bid increments used during the auction. If l plays the straightforward strategy throughout the benchmark auction, then

(i) for all rounds t and packages A, | max(0, ) |π ε− − ≤t tlA lA lB v and

(ii) at the final round T, either l is a provisionally winning bidder or 0 Tlπ ε≤ ≤ .

Properties (i) and (ii) of Theorem 1 are useful both for empirical and engineering design analyses of package bidding. Empirically, one may measure the distance between the strategies actually played and straightforward strategies by finding the smallest ε for which statements (i) and (ii) are true. For purposes of design, one can identify bounds based on ε that establish how close the approximations developed in this paper are to the actual auction situation.

To simplify the analysis and develop its relationship to others, we focus attention in this paper on a limiting version of the model that we call the “benchmark limit auction.” For that auction, theorem 1 applies for every 0ε > . Hence, the conclusion holds for

0ε = .

The benchmark limit auction is the limit of a class of auctions in which each buyer periodically instructs a “proxy agent.” The agent for bidder l accepts as input a valuation profile lv% and bids straightforwardly according to that profile until it is interrupted and

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 15

given new instructions. If bidders were able to interrupt the agent at every round, then this description would entail no restrictions on how a bidder might bid. Suppose, however, that bidders may change their instructions only when the sum total of all bids has increased by at least a threshold amount since the last change.

Formally, let us assume that there is a fixed number ˆ 0ε > and a series of times { }kt ,

satisfying t0 = 0 and 1kt + = { }, ,ˆinf : ktt

lA lAl A l At B B ε> +∑ ∑ , at which bidders may instruct

their agents. Further assume that the bidders are informed only of the bid amounts at the times {tk}, so their instructions may depend only on that information, and the instructions at time tk are assumed to depend continuously on the information vector. Finally, let us impose a large finite upper bound on the bids, so that the auction is assured to terminate in finite time. With this specification, for any fixed strategies, the maximum bids converge to some limit value. Adapting a device suggested by Simon and Zame (1990), if there are multiple allocations that maximize the total bid in the limit, then we select the single allocation that has the highest total value as the allocation in the limit game. The strategies, outcomes and payoffs described above define the benchmark limit auction.

The remainder of our analysis in this paper applies to the benchmark limit auction. To keep track of our reliance on the assumed small size of the increment, we sometimes write x y≈ in place of x y= where the limiting condition 0ε ≈ is used.

4. Package Auctions and Matching Theory Our approach in this section is to analyze the benchmark auction with package

bidding as a kind of deferred acceptance algorithm in the sense that term is understood in the theory of two-sided matching.

All deferred acceptance algorithms entail a series of rounds. At each round players on one side of a market make offers to players on the other side and the receiving players reject all but their most preferred offers at each round. The process iterates as long as the offering players have unfilled openings that they prefer to the no trade outcome. At that time, any offers that were never rejected become finally accepted. This class of algorithms acquires its name from the fact that even the best offers are not finally accepted until the last round.

Deferred acceptance algorithms arise in models where there is no exchange of money—the so-called “marriage problem” and “college admissions problem” are examples—as well as in problems where money is exchanged. The ordinary ascending “English” auction is an example of the second kind, with buyers shouting offers and the seller holding onto the best offer until a better offer is made. Most closely related to our analysis is one by Kelso and Crawford (1982), who analyzed a simultaneous ascending auction in which the bidders are firms and the sellers are workers who have preferences over both the employer’s identity and income.

In view of our present application, let us call the players on the offering side of the deferred acceptance algorithm “buyers” and the players on the accepting side “sellers.”

A recurring result in matching models with and without money is that the outcome of the deferred acceptance algorithm is a “stable match” or core allocation of the matching

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 16

game. That is, the outcome has the property that there is no coalition of players that can match or trade among themselves in a way that coalition members all prefer to the outcome proposed by the algorithm. In particular, this result implies that the core of the matching game is non-empty.

A second recurring result in matching models is that the core allocation to which the deferred acceptance algorithm converges is the most preferred point in the core for each buyer and the least preferred point in the core for each seller. In particular, this implies that such a core point exists.

A third common result in matching models is that it is a dominant strategy for each buyer to report its preferences truthfully. That is, for any specification of the preferences of the others, the result of the algorithm when a buyer reports truthfully is at least as favorable when it reports truthfully as when it reports untruthfully, and any given untruthful strategy leads to strictly worse outcomes for some profile of preferences of the other players. However, it is not generally a dominant strategy for the sellers to report their preferences truthfully.

Each of these results relies on assumptions about preferences that can typically be interpreted as meaning that, from each player’s point of view, the parties on the other side of the market are “substitutes.” Here, the statement that “buyers are substitutes” means roughly that each seller finds that trading with some buyers makes trading with others (at any given terms) either impossible or less valuable. A symmetric definition applies to the statement that “sellers are substitutes.”

In this section, we explore the benchmark package auction with straightforward bidding as a kind of deferred acceptance algorithm. Straightforward bidding plays an essential role in our analysis: it enforces the condition found in all defe rred acceptance algorithms that the buyers first make the offers they prefer most and proceed monotonically to the offers they prefer least, stopping at last when no unmade offer is preferred to the no-trade outcome. As part of the development, we find ana logues for the results described above and other typical results of matching theory.

4.1 The Auction Outcome and the Core To make formal sense of these claims, we begin by defining a coalitional form game

(L,w) that is associated with the package economy. The coalitional value function w is defined by w(S) = 0 if the seller is not a member of the coalition (0∉S) and otherwise by the following expression:

[0, ]( )

( ) max lA lAl S A Mx F Mw S x v

∈ ∈∈= ∑ ∑ (5)

Thus, the value of a coalition including the seller is the maximum total value the players can create by trading among themselves. Also,

{ }( , ) : ( ) , ( ) for all l ll L l SCore L w w L w S S Lπ π π

∈ ∈= = ≤ ⊂∑ ∑ . (6)

The core is the set of profit allocations that are feasible for the coalition of the whole and unblocked by any coalition S.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 17

If all bidders bid straightforwardly, then the seller’s revenue at any round t of the auction is given by

{ }

0( )

\0 [0, ]( )

\0 [0, ]( )

\0

ˆmax

max max(0, )

max max ( )

max ( )

t t

x F M

tlA lA ll L A Mx F M

tlA lA ll S A MS L x F M

tll SS L

B x

x v

x v

w S

π

π

π

π

∈

∈ ∈∈

∈ ∈⊂ ∈

∈⊂

= ⋅

≈ −

= −

= −

∑ ∑∑ ∑

∑

(7)

The four steps in (7) follow from (i) the assumption that bidding is straightforward and the definition of 0

tπ , (ii) the characterization of straightforward bids in Theorem 1, (iii) choosing S to be the winning coalition at round t, and (iv) the definition of w.

According to (7), when all bidding is straightforward, the effect is as if each bidder makes a profit demand 0t

lπ ≥ and each coalition S offers to the seller the value of the coalition minus the profit demands.21 An immediate consequence of (7) is that for all coalitions S that include l = 0 (the seller), ( ) t

ll Sw S π

∈≤ ∑ , and the same result holds

trivially for coalitions excluding the seller. Hence, for all t, the vector of payoffs tπ satisfies all the inequalities defining the core.

Let S* be the final winning coalition. Then,

*

( ) ( *) ( )T Tl ll L l S

w L w S w Lπ π∈ ∈

≤ ≈ = ≤∑ ∑ (8)

The four steps in (8) follow from (i) a core inequality which we have already established, (ii) the Theorem 1 approximation that 0T

lπ ≈ for bidders not in S*; (iii) the fact that S* is the winning coalition, and (iv) the observation that w(S) increases (weakly) as S becomes more inclusive. It follows from (8) that when the auction concludes, the payoff vector Tπ satisfies the feasibility condition: ( ) T

ll Lw L π

∈= ∑ .

Combining the last two observations, we have the following.

Theorem 2. If all bidders play their straightforward strategies, then the resulting profit allocation from the benchmark limit auction satisfies ( , )T Core L wπ ∈ .

Theorem 2 corresponds to an expected result for a deferred acceptance algorithm, but the next result differs somewhat from the usual pattern for matching models. It does establish that the benchmark limit auction is the least preferred core result for the seller’s side, but not that there is a single core point that is most preferred by every buyer.

21 This is the key step in the argument. In general matching models, attention is typically focused on offers of matches or positions or money. What unifies the theory and makes this application possible is a change in perspective in which the offering side offers a reservation utility. In utility space, the same basic analysis applies regardless of the form of the offer. At each round of a deferred acceptance algorithm, the vector of buyer utility offers and seller acceptance is unblocked by any coalition. At the final round, the vector becomes feasible and a core point is identified.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 18

Theorem 3. Suppose that all bidders play their straightforward strategies and that the resulting profit allocation from the benchmark limit auction is Tπ . There exists no point ˆ ( , )Core L wπ ∈ such that 0 0ˆ Tπ π< .

Proof. Suppose that the winning coalition last changed from, say, S to S* at time τ. Then,

\0 \0

0 0*\0 *\0

( ) ( )

ˆ( *) ( *) ,

Tl ll S l S

T T Tl ll S l S

w S w S

w S w S

τ

τ

π π

π π π π∈ ∈

∈ ∈

− ≈ −

≈ − = − = >∑ ∑

∑ ∑ (9)

which implies that 0\0ˆ( ) T T

ll Sw S π π

∈> +∑ . Hence, the outcome is blocked by the

penultimate winning coalition S. ■

Bernheim and Whinston (1986) have shown that the set of payoffs consistent with coalition-proof equilibrium in their “menu auctions” is precisely the set of points

( , )Core L wπ ∈ that minimize the seller’s revenue. According to Theorem 3, the payoff outcome of the benchmark limit auction with straightforward bidding is also a coalition-proof equilibrium payoff of the menu auction.

4.2 When Buyers are Mutual Substitutes We turn next to the question of when the structure of the core leads to a coincidence

of interests among the bidders, in the sense that there is a single point that is unanimously preferred by all. As reviewed earlier, this characterization does hold in many matching models. Those models typically assume that players on each side of the market are “substitutes.”

Definition. Buyers are mutual substitutes if for all l≠0 and all coalitions S S′⊂ , ( {}) ( ) ( { }) ( )w S l w S w S l w S′ ′∪ − ≥ ∪ − .22

Definition. Goods are mutual substitutes if for all packages A and B ≤ B′, ( ) ( ) ( ) ( )l l l lv A B v B v A B v B′ ′+ − ≥ + − .23

The first definition holds that buyers are mutual substitutes when any buyer l adds less value to “larger” (more inclusive) coalitions. In the same way, goods are mutual substitutes when any package A adds less value to larger packages.

22 The “buyers are mutual substitutes” condition and a version of theorem 5 first appeared in Ausubel (1997b), which this paper supercedes. That predecessor also included the following necessary condition for

the conclusion of theorem 5: ( )\0

( ) ( ) ( ) ( ) ,l S

w L w L S w L w L l∈

− ≥ −∑\ \ for all coalitions S

(0 )S L∈ ⊂ . Bikhchandani and Ostroy (1999) subsequently developed the implications of these

conditions for dual problems to the package assignment problem. 23 Since payoffs are linear in money, there is no difference between compensated and uncompensated demand and hence no difference between “net substitutes” and “gross substitutes.” We use “mutual substitutes” to emphasize that the condition is one that applies among all goods and not just between some particular pairs of goods.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 19

Consider first the case in which buyers are mutual substitutes. Let π denote the profit and revenue outcome of a generalized Vickrey auction. That is, let ( ) ( \ )l w L w L lπ = −

for l ≠ 0 and let 0 \0( ) ll L

w Lπ π∈

= −∑ . With this notation, we introduce four more results.

Theorem 4. No bidder gets more than its Vickrey payoff at any point in the core. Formally, for any ( , )Core L wπ ∈ , l lπ π≤ for all l ≠ 0.

Theorem 5. If buyers are mutual substitutes, then the core is the set of feasible payoffs in which no buyer gets more than its generalized Vickrey payoff. Formally,

( , ) { : ( ),0 for all 0}l l ll LCore L w w L lπ π π π

∈= = ≤ ≤ ≠∑ . (10)

Theorem 6. If buyers are mutual substitutes, then the outcome of straightforward bidding in the benchmark limit auction is the generalized Vickrey outcome: Tπ π= .

For theorem 7, we restrict the set of feasible valuations for each bidder l to some satisfy vl ∈ Vl and we write v ∈ V to denote vl ∈ Vl for all l.

Theorem 7. Suppose that for all v ∈ V, buyers are mutual substitutes. Consider the game in which each buyer l is permitted to announce any preferences satisfying vl ∈ Vl, and the outcome is determined by proxy bidding in the benchmark limit auction. Then it is a dominant strategy for each buyer to report its strategy truthfully.

Proofs. For theorem 4, suppose π is a feasible profit allocation with l lπ π> for some

l ≠ 0. Then \

( ) ( \ )k lk L lw L w L lπ π

∈= − <∑ , so L \ l blocks the allocation. Hence,

( , )Core L wπ ∉ .

For theorem 5, we begin with the inference from theorem 4 that ( , )Core L w ⊂ Π ≡

{ : ( ),0 for all 0}l l ll Lw L lπ π π π

∈= ≤ ≤ ≠∑ . For the reverse inclusion, suppose π ∈Π .

Let S be a coalition including the seller, say, {0,..., }S k= . We must show that S does not block π . This follows because:

| |

1

| |

1

| |

1

| |

1

( )

( )

( ) ( ) ( \ )

( ) ({0,..., }) ({0,..., 1})

( ) [ ( ) ( )]

( )

L

l ll S l k

L

ll k

L

l k

L

l k

w L

w L

w L w L w L l

w L w l w l

w L w L w S

w S

π π

π∈ = +

= +

= +

= +

= −

≥ −

= − −

≥ − − −

= − −=

∑ ∑∑∑∑

(11)

The first step in (11) follows from feasibility of π , the second from π ∈Π , the third from the definition of π , and the fourth from the condition that bidders are substitutes.

For theorem 6, it suffices to show that once a buyer l ≠ 0 reduces its profit demand to less than lπ , it never makes another bid, because it is always part of the winning

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 20

coalition. For suppose tl lπ π< . We show that if l S∉ , then S is not the winning coalition

at time t.

{ }

{ }

{ }

( ) ( )

( ) ( ) ( \ )

( ) ( ) ( )

( {})

t t tk k l lk S k S

tkk S l

tkk S l

tkk S l

w S w S

w S w L w L l

w S w S l w S

w S l

π π π π

π

π

π

∈ ∈

∈ ∪

∈ ∪

∈ ∪

− < − + − = − + −

≤ − + ∪ −

= ∪ −

∑ ∑∑∑

∑

(12)

This establishes that the total bid made by coalition S is less than that made by { }S l∪ . Hence, a straightforward bidder l’s profit is never less than lπ ε− . For the

benchmark limit auction, we use the approximation that 0ε ≈ .

Theorem 7 is a direct corollary of theorem 6. ■

5. Two Special Cases There are two special cases that are important for our analysis. The first is the case in

which buyers are mutual substitutes. Its importance is already established by Theorems 5-7. The second is the case in which there are budget constraints, which have been important in some actual spectrum auctions.

5.1 When Goods are Mutual Substitutes In models for which the coalitional game (L,w) is the primitive, the assumption that

bidders are substitutes is not subject to further analysis. In the present model, however, coalition values are not primitive—they are derived from individual package values. It is natural to ask: what conditions on bidder valuations imply that bidders are substitutes in the coalition game? In answering that question, the condition that goods are substitutes emerges as a best sufficient condition. This is established in two theorems. Theorem 9 holds that if the goods are mutual substitutes for all bidders, then the bidders are mutual substitutes. Moreover, according to theorem 10, if the set of individual valuations is any strictly superset of the set of all substitute valuations, then there are cases consistent with the valuation assumptions in which bidders are not substitutes and the conclusions of Theorems 5-7 all fail to hold.

We conduct our analysis of the case of substitutes by treating each item as if it were unique. This relabeling of items clearly does not alter the feasible payoffs for any coalition, so it does not alter the core of the game. It does, however, simplify certain arguments made below.

Let p be a vector of prices for the individual items and define bidder l’s expenditure function by ( , ) minl A lAe p u u p A v= + ⋅ − .

Theorem 8. Goods are “mutual substitutes” for bidder l if and only if the expenditure function ( , )le ⋅ ⋅ is supermodular.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 21

Proof. By an envelope theorem of Milgrom and Segal (2000), the expenditure function is absolutely continuous and hence partially differentiable almost everywhere in the price pm. Moreover, wherever the partial derivative exists, it is equal to the unique utility-maximizing quantity xm of good m at that price. By definition, the substitutes condition is satisfied if and only if ( )mx p is nondecreasing in each pj for j ≠ m. Thus,

goods are mutual substitutes if and only if /l me p∂ ∂ is nondecreasing in each pj for j ≠ m,

that is, if and only if el is supermodular. ■

Theorem 9. If goods are mutual substitutes for all bidders, then bidders are mutual substitutes.

Proof. The only relevant coalitions S are ones that include the seller, so we limit attention to those.

Define coalition value functions by ( )maxSA x F A lB lBl S B Av x v∈ ∈ ≤

= ∑ ∑ . The

corresponding coalition expenditure function ( , )Se p u describes the minimum expenditure needed to achieve total payoff u for the members of coalition S at price vector p. It is given as follows:

,

( , ) min

min

( ,0)l l

S A SA

A l S l lAl S

ll S

e p u u p A v

u p A v

u e p

∈ ∈

∈

= + ⋅ −

= + ⋅ −

= +∑

∑ (13)

By theorem 8 and inspection of (13), the function ( , )Se p u parameterized by S is supermodular (because it is the sum of supermodular functions) and has nondecreasing (“isotone”) differences (because for each l, ( ,0)le p is nondecreasing in p).

One may recover the valuation function from the expenditure function in the usual way: { }:0 for all min ( ,0)

m LMSA Sp p v mv p A e p≤ ≤= ⋅ − . The objective function is continuous and

submodular and has isotone differences in the prices and the parameter S, and the feasible set is a complete lattice. Hence, by a theorem of Topkis, the set of maximizers is a complete sublattice with a maximum element ( )Ap S , that is isotone in S. The maximum price is ( )mA LMp S v= for each m A∉ . For each m A∈ , raising the price of item m

slightly above ( )mAp S causes m not to be demanded but, by mutual substitutes does not

reduce demand for the other goods. Hence, ( )mAp S = , \SA S A mv v− .

For any package A consisting of m items, let 1...m m nA A A A M+= ⊂ ⊂ = be an increasing sequence of packages such that each element differs from its predecessor by the inclusion of a single additional element. Then,

11 1

( ) ( )j j j

n n

SM SA SA SA jAj m j mv v v v p S

−= + = +− = − =∑ ∑ (14)

which is nondecreasing in S since each term is.

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 22

Finally, observe that for each bidder l, ( {}) ( )w S l w S∪ − = ,max A SA l M A SMv v v−+ − is a

maximum of non- increasing functions of S and hence is itself non- increasing in S. ■

For the next result, define S to be the set of bidder valuations.

Theorem 10. Suppose that the set of possible buyer valuations strictly includes all those for which goods are mutual substitutes. Then there is a profile of valuations drawn from the set of possible valuations such that bidders are not substitutes and the conclusions of theorems 5, 6 and 7 all fail to hold.

Proof. Consider first the case in which there are just two goods for sale. Suppose some buyer’s values do not satisfy the substitute goods condition. Say that buyer’s values are a1 >0 for good 1, a2 >0 for good 2, and a12 = a1 + a2 +ε for the pair, where ε > 0. Introduce two more bidders who each has positive value for just one good—the first with value a1+ε for good 1 and the second with value a2+ε for good 2. These two bidders’ values satisfy the condition that goods are mutual substitutes.

By inspection, (12) (1) 0 (123) (13)w w w wε− = < = − , so bidders are not substitutes.

Moreover, the 2 3 2 3 2 3( , ) {(0, , ) : , 0, }Core L w π π π π π π ε= ≥ + = , so the conclusion of theorem 5 fails. Finally, the Vickrey profits of bidders 2 and 3 are each ε and are not both realized at any point in the core. Hence, by theorem 2, the conclusion of theorem 6 fails to hold.

Since the benchmark revelation game with honest reporting achieves an efficient outcome and entails zero transfers to or from losing bidders, and since the Vickrey auction is the unique dominant strategy auction with these properties, for this class of environments (Holmstrom (1979)), the conclusion of theorem 7 must fail as well.

The same construction can be adapted to the case with more than two goods. Indeed, the failure of the substitutes condition for a value function v implies that there is a package A and goods, call them 1 and 2, such that the previous example characterizes marginal values for increments to A, that is, 1( {1}) ( )l lv A v A a∪ − = ,

2( {2}) ( )l lv A v A a∪ − = , and 1 2( {1,2}) ( )l lv A v A a a ε∪ − = + + . Introduce three additional bidders for whom values are substitutes. The first values each good in ( {1,2})M A− ∪ very highly and has values of zero for all other goods. The other two are as described above, with values only for goods 1 and 2. ■

5.2 The Benchmark Auction with Budget Constraints Binding budget constraints introduce enormous complexity into auction strategy, but

they are also an important feature of many real auctions for valuable assets. Because some analyses of matching problems—such as the marriage problem and the college admissions problem—are conducted in non-transferable utility games, it is natural to inquire whether the results obtained above can be extended to the case in which binding budget constraints prevent the outcome from lying in the transferable utility core.

For this analysis, we need to redefine several terms. First, the coalitional game (L,w) becomes a non-transferable utility (“NTU”) game in which w(S) is the set of achievable

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 23

utility vectors for coalition S, trading just among its own members. For coalitions S not including the seller, w(S) = {0S} is a singleton vector of zeroes, one corresponding to each member of coalition S. For coalitions including the seller (player 0):

( ) ( ) ( ){ }0 \0\0( ) : ( ),0 , ,S l l lA lA l ll S A l Sl S

w S x F M b B x v b bπ π π π∈ ∈∈

= = ∃ ∈ ≤ ≤ = − =∑ ∑ (15)

In equation (15), b is a non-negative vector of payments respecting the player’s budget limits. A profit vector π is blocked by a coalition S in the NTU game if there is some vector in w(S) that entails strictly higher profits for all members of coalition S. A feasible profit vector π ∈ w(L) is in the core of the game if it is unblocked, that is:

[ ]( ){ }( , ) ( ) : , ( ) S SCore L w w L S L w Sπ π π π′ ′= ∈ ¬∃ ⊂ ∈ >> (16)

Straightforward bidding also needs to be redefined to respect the budget constraints. Given the budget constraint, the bidder’s maximum potential profit from a winning bid made at round t is:

{ } { }( )max 0 : , [0, ]t t tl lA lA lA lv B B B A Mπ = ∪ − ≤ ∈ (17)

and, corresponding to theorem 1, its bids at round t satisfy:

( )max 0,min( , )t tlA l lA lB B v π= − (18)

At round t, the highest total bid by any coalition of buyers S is:

{ }0 0max : ( {0}), for all t tS l lw S l Sπ π π π π= ∈ ∪ ≥ ∈ (19)

and the seller’s maximum total price is { }0 0max : \ 0t tS S Lπ π= ⊂ . By inspection, the

vector tπ is unblocked at every round. Also, at the final round, each non-winning bidder l has 0t

lπ = , so the outcome is feasible: ( )T w Lπ ∈ . We have the following:

Theorem 11. If all bidders play their straightforward strategies, then the resulting profit allocation from the benchmark limit auction with budget constraints satisfies

( , )T Core L wπ ∈ .

Theorem 11 corresponds closely to theorem 2, which was derived for the case of transferable utility games (that is, no budget constraints). Note that the argument proving theorem 11 relies on the definitions of 0

tπ and Core(L,w), but not on the structure of w given in (15). The logical structure of the argument is thus easily extended to many variations of the basic model, including for example ones in which the each bidder’s utility ( , )l lA bπ is a general increasing function of the package A and a continuous, decreasing function of the amount bl that the bidder pays.

Theorem 12. Suppose that all bidders play their straightforward strategies and that the resulting profit allocation from the benchmark limit auction is Tπ . There exists no point ˆ ( , )Core L wπ ∈ such that for all members l of the winning coalition S*, ˆ T

l lπ π> .

“Ascending Auctions with Package Bidding,” Lawrence Ausubel & Paul Milgrom 24