54

03/20/22 1 Equivalence and Compound Interest Minggu 3

| Date post: | 24-Oct-2015 |

| Category: |

Documents |

| Upload: | saravanan-mathi |

| View: | 4 times |

| Download: | 0 times |

04/17/23 1

Equivalence and Compound Interest

Minggu 3

04/17/23 2

Time Value of Money

The value of money today is worth more than its value in the next several years. So, the interest of money is needed to compensate its value changed.

04/17/23 3

Interest (1)

Simple InterestThe total interest earned/charged is linearly proportional to the initial amount of the loan (principle), the interest rate and the number of inteest value. The formula of simple interest for several periods (N) is :

F = Future value of moneyP = Present value of money (principle loan) N = Number of periods (e.g, years)i = Interest rate

(1 . )F P i N

04/17/23 4

Interest (2) Compound Interest

The interest charge of any interest value is based on the remaining principle amount plus any accumulated interest charge up to the beginning of the period. The formula of compound interest for several periods is :

F = Future value of moneyP = Present value of money (principle loan) N = Number of periods (e.g, years)i = Interest rate

NP ( 1 + i )F

04/17/23 5

Equivalence (1)

Economic equivalence is established, in general, when we are indifferent between a future payment, or series of future payments, and a present sum of money.

Its can affect the difference in repayment plans although the value of money actually similar. It can be explained by this example :

04/17/23 6

Equivalence (2) Example : Four plans for repayment of $5000 in

five years at 8% interest :- Plan 1 : At end of each year pay $1000 principle

plus interest due.

(1) (2) (3) (4) (5) (6)

YearAmount owed

at beginning of year

Interest owed for that year

Total owed at end of year

Principlepayment

Total end of year payment

[8% x (2)] [(2) + (3)}

1 5000 400 5400 1000 1400

2 4000 320 4320 1000 1320

3 3000 240 3240 1000 1240

4 2000 160 2160 1000 1160

5 1000 80 1080 1000 1080

Total 1200 5000 6200

04/17/23 7

Equivalence (3)

- Plan 2: Pay Interest due at end of each year and principal at end of five years

(1) (2) (3) (4) (5) (6)

Year

Amount owed at

beginning of year

Interest owed for that year

Total owed at end of

year

Principle

payment

Total end of year

payment

[8% x (2)] [(2) + (3)}

1 5000 400 5400 0 400

2 5000 400 5400 0 400

3 5000 400 5400 0 400

4 5000 400 5400 0 400

5 5000 400 5400 5000 5400

Total 2000 5000 7000

04/17/23 8

Equivalence (4)

- Plan 3 : Pay in five equal end-of-year payments.

(1) (2) (3) (4) (5) (6)

YearAmount owed at beginning

of year

Interest owed for that year

Total owed at end of

year

Principle

payment

Total end of year

payment

[8% x (2)] [(2) + (3)}

1 5000 400 5400 852 1252

2 4148 331 4479 921 1252

3 3227 258 3485 994 1252

4 2233 178 2411 1074 1252

5 1159 93 1252 1159 1252

Total 1260 5000 6260

04/17/23 9

Equivalence (5)

- Plan 4 : Pay interest and principal at the end of periods.

(1) (2) (3) (4) (5) (6)

YearAmount owed at beginning

of year

Interest owed for that year

Total owed at end of

year

Principle

payment

Total end of year

payment

[8% x (2)] [(2) + (3)}

1 5000 400 5400 0 0

2 5400 432 5832 0 0

3 5832 467 6299 0 0

4 6299 504 6803 0 0

5 6803 544 7347 5000 7347

Total 2347 5000 7347

04/17/23 10

Equivalence (6)

ratio = total interest paid /total amount owed at the beginning of year.

PlanTotal Interest

paid

Total amount owed at the

beginning of yearratio

1 $ 1200 $ 15000 0,08

2 2000 25000 0,08

3 1260 15767 0,08

4 2347 29334 0,08

From our calculations, we more easily see why the repayment plans require the payment of different total sums of money, yet are actually equivalent to each other.

04/17/23 11

Compound Interest

To facilitate equivalence computations, a series of interest formulas will be derived. To simplify the presentation, we’ll use the following notation :

i = Interest rate per interest period (%)

n = Number of interest periods

P = A present sum of money

F = A future sum of money

A = An end-of-period cash receipt or disbursement in a uniform series

04/17/23 12

Single Payment Formulas (1)Single payment formulas, consist of :1. Future Equivalent Values

In other words a present sum P increase in n periods to P(1+i)n

Therefore have a relationship between a present sum P and its equivalent future sum F F = P (1+i)n

Year

Amount at beginning of

interest period +Interest for

period =

Amount at end of interest

period

1'st year P + iP = P (1+i)

2'nd year P(1+i) + iP(1+i) = P(1+i)2

3'rd year P(1+i)2 + iP(1+i)2 = P(1+i)3

n'th year P(1+i)n-1 + iP(1+i)n-1 = P(1+i)n

04/17/23 13

Single Payment Formulas (2)

The single payment compoud amount formula function notation is

F = P(F/P,i,n) example :If $500 were deposited in a bank savings account, how much would be in the account 3 years hence if the bank paid 6% interest compounded annualy?

F = 500 (F/P,6%,3) = 500 (1,191) = $ 595,5

P = 500

F = ?

n = 3i = 0,06

1 2 3

04/17/23 14

Single Payment Formulas (3)

2. Present Equivalent Values

If we take F = P(1+i)n and solve for P

This is the single payment present worth formula.

The equation :

In our notation becomes

P = F(P/F,i,n)

11

1

n

nP F F ii

1n

P F i

04/17/23 15

Single Payment Formulas (4)

example : An investor (owner) has an option to purchase a tract of

land that will be worth $ 10.000 in six years. If the value of the land increases at 8% each year, how much sould the investor be willing to pay now for this property ?

P = 10.000 (P/F,8%,6) = 10.000 (0,6302)

= $6.302

P = ?

F = 10.000

n = 6i = 0,08

1 2 3 4 5 6

04/17/23 16

Uniform Series Formula (1)

According to the equation F=P(1+i)n, we’ll use this relationship in uniform series derivation

= + + +

In the general case for n years,

F = A(1+i)n-1 + …. + A(1+i)3 + A(1+i)2 + A(1+i) + A

Multiplying equation above by (1+i),

(1+i)F = A(1+i)n + …. + A(1+i)4 + A(1+i)3 + A(1+i)2 + A(1+i)

A A A A

F =

A

A(1+i)3 +

A

A(1+i)2 +

A

A(1+i) +

A

A

04/17/23 17

Factoring out A from two equation above and subtracting them,

(1+i)F = A[(1+i)n + …. + (1+i)4 + (1+i)3 + (1+i)2 + (1+i)]

F = A[(1+i)n-1 + …. + (1+i)3 + (1+i)2 + (1+i) + 1]

iF = A[(1+i)n – 1]

Solving equation for F,

The term within the bracket

is called uniform series compound amount factor and the notation is (F/A,i,n)

F = A (F/A,i,n)

i

iAF

n 1)1(

i

i n 1)1(

Uniform Series Formula (2)

04/17/23 18

Uniform Series Formula (3)

If the equation is solved for A, we have

Where

is called the uniform series sinking fund factor and is written as (A/F,i,n)

A = F (A/F,i,n)

(1 ) 1n

iA F

i

(1 ) 1n

i

i

04/17/23 19

Uniform Series Formula (4)

We know that F = P (1+i)n, then

Solving equation for P,

Where

is called the uniform series present worth factor and is written as (P/A,i,n)

P = A (P/A,i,n)

(1 ) 1(1 )

nn i

P i Ai

(1 ) 1

(1 )

n

n

iP A

i i

(1 ) 1

(1 )

n

n

i

i i

04/17/23 20

Uniform Series Formula (5)

If the equation is solved for A from P, we have

Where

is called the uniform series capital recovery factor and is written as (A/P,i,n)

A = P (A/P,i,n)

(1 )

(1 ) 1

n

n

i iA P

i

(1 )

(1 ) 1

n

n

i i

i

04/17/23 21

Uniform Series Formula (6)

Example 1 :Using a 15% interest rate, compute the value

of F in the following cash flow :

Solution :we see that the cash flow diagram is not the same as the sinking fund factor diagram

A =100

F = ?

0

year cash flow

1 +100

2 +100

3 +100

4 0

5 -F

04/17/23 22

Uniform Series Formula (7)

F1 = 100(F/A,15%,3)

= 100(3,472)

= 347,2

F = F1(F/P,15%,2)

= 347,2(1,322)

= $ 459

A =100

F = ?

0A =100

F = ?

0

F1

P = F1

F = ?

04/17/23 23

Uniform Series Formula (8) Example 2 :

Using a 15% interest rate, compute the value of P in the following cash flow

P = ?

20 20

30

0

year cash

flow

0 -P

1 0

2 20

3 30

4 20

04/17/23 24

Uniform Series Formula (9) Solution :

P=P1(P/F,15%,1) P1= A(P/A,15%,3) + F(P/F,15%,2)

P1= 20(P/A,15%,3) + 10(P/F,15%,2)

P1= 20(2.283) + 10(0.7561)

P1= 45.66 + 7.561 = 53.221

P = 53.221(0.8696)

P = 46.28

P

20 2030

20 2010

20

P1

20 2030

P1P1

P1

00

04/17/23 25

Relationship Between Compound Interest Factor(1)

Single Payment

Compound amount factor = 1 / Present worth factor

Uniform Series

Capital recovery factor = 1 / Present worth factor

Compound amount factor = 1 / Sinking fund factor

),,/(

1),,/(

niFPniPF

),,/(

1),,/(

niAPniPA

),,/(

1),,/(

niFAniAF

04/17/23 26

Relationship Between Compound Interest Factor(2)

Uniform series present worth factor is simply the sum of the n

terms of the single payment present worth factor

Uniform series compound amount factor equals 1 plus the sum

of (n-1) terms of the single payment compound amount factor.

Uniform series capital recovery factor equals the uniform series

sinking fund factor puls i

n

J

JiFPniAP1

),,/(),,/(

1

1

),,/(1),,/(n

J

JiPFniAF

iniFAniPA ),,/(),,/(

04/17/23 27

Arithmetic Gradient(1)

Arithmetic Gradient is a series of increasing cash flows.

Derivation of arithmetic gradient factor :

= + ….. + +

F = G(1+i)n-2 + 2G(1+i)n-3 + … + (n-2)G(1+i)1 + (n-1)GorF = G[(1+i)n-2 + 2(1+i)n-3 + … + (n-2)(1+i)1 + (n-1)]

F

0G

2G(n-2)G

(n-1)G

FI

G

FII

(n-2)G

FIII

G2G

(n-2)G

04/17/23 28

Arithmetic Gradient(2)

Multiply equation above by (1+i) and factor out G,

(1+i)F = G[(1+i)n-1 + 2(1+i)n-2 + … + (n-2)(1+i)2 + (n-1)(1+i)]

Subtracting two equation above,

F + iF – F = G[(1+i)n-1 + (1+i)n-2 + … + (1+i)2 + (1+i) +1] – nG

The term in the bracket were shown to equal the series compound

amount factor :

Thus the equation becomes

1 2 2 1 (1 ) 1[(1 ) (1 ) ... (1 ) (1 ) 1]

nn n i

i i i ii

(1 ) 1niiF G nG

i

04/17/23 29

Arithmetic Gradient(3)

Rearranging and Solving for F,

Using F = P (1+i)n ,

The term in the bracket

is called arithmetic gradient present worth factor and denote by (P/G,i,n)

(1 ) 1nG iF n

i i

(1 ) 1 1

(1 )

n

n

G iP n

i i i

2

(1 ) 1

(1 )

n

n

i inG

i i

2

(1 ) 1

(1 )

n

n

i in

i i

04/17/23 30

Arithmetic Gradient(4)

Using then,

The term in the bracket

is called arithmetic gradient uniform series factor and denote by (A/G,i,n)

i

iAF

n 1)1(

(1 ) 1

(1 ) 1

n

n

G i iA n

i i i

iii

iniG

n

n

)1(

1)1(

iii

inin

n

)1(

1)1(

04/17/23 31

Arithmetic Gradient(5)

Example :

One a certain piece of machinery it is estimated that the maintenance expense will be as follows :

what is the equivalent uniform annual maintenance cost for the machinery if 6% interest is used

100

400200 300 year

cash flow

1 $ 100

2 200

2 300

4 400A A A A

04/17/23 32

Arithmetic Gradient(6)

A = 100 + G (A/G,i,n)

= 100 + 100(A/G,6%,4)

= 100 + 100(1,427)

= $ 242,7

100

400200 300

0300

100 200100 100 100 100

04/17/23 33

Geometric Gradient (1)

Year Cash Flow

1 100.00 = 100.00

2 100.00 + 10%(100.00) = 100(1 + 0.10)1 = 110.00

3 110.00 + 10%(110.00) = 100(1 + 0.10)2 = 121.00

4 121.00 + 10%(121.00) = 100(1 + 0.10)3 = 133.10

5 133.10 + 10%(133.10) = 100(1 + 0.10)4 = 146.41

04/17/23 34

Geometric Gradient (2)

100.00110.00

121.00

133.10

146.41

04/17/23 35

Geometric Gradient (3)

From the table, we get : $100.00(1 + g)n-1

General Form : An= A1(1 + g)n-1

where : g = Uniform rate of cash flow

A1= Value of A at Year 1

An= Value of A at any Year n

Present worth Pn of any cash flow An :

Pn = An(1 + i)-n

04/17/23 36

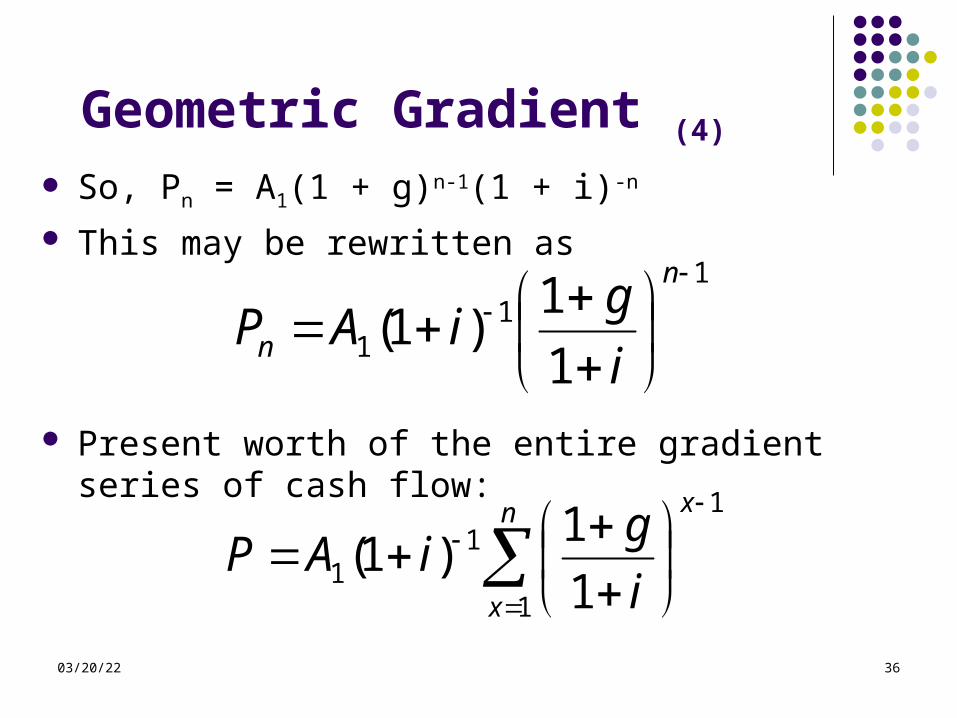

Geometric Gradient (4)

So, Pn = A1(1 + g)n-1(1 + i)-n

This may be rewritten as

Present worth of the entire gradient series of cash flow:

11

1 1

1)1(

n

n i

giAP

n

x

x

i

giAP

1

11

1 1

1)1(

04/17/23 37

Geometric Gradient (5)

A1

A2

A3

An-1

An

P

04/17/23 38

Geometric Gradient (6) In general case where i ≠ g ;

Let a = A1(1 + i)-1 and b = {(1+g) / (1+i)}then the equation becomes :

21

11

11

1 1

1)1(

1

1)1()1(

i

giA

i

giAiAP

11

1 1

1)1(...

n

i

giA

04/17/23 39

Geometric Gradient (7)

P = a + ab + ab2 + …. + abn-1

multiply the equation above by b :

bP = ab + ab2 + ab3 + …. + abn-1 + abn

subtract two equation above :

P – bP = a – abn

P(1 – b) = a(1 – bn)

P = a(1 – bn) / (1 – b)

04/17/23 40

Geometric Gradient (8)

Replacing original value for a and b then :

igig

iAP

n

11

1

11

1)1( 1

1

gi

igAP

nn )1()1(11

where i ≠ g

04/17/23 41

Geometric Gradient (9)

Cash flow that applicable where the period-by-period change is a uniform rate

Using the formula : :

· Geometric series present worth factor where i = g,

· Where i = g :

gi

ignigAP

nn )1()1(1),,,/(

1)1(),,,/( innigAP

04/17/23 42

Geometric Gradient (10)

Example :The first year mintenance cost for a new automobile is estimated to be $100 , and it increases at a uniform rate of 10% per year. What is the present worth of cost of the first five years of maintenance in this situation, using an 8% interest rate?

Year maintenance cost PWn (P/F,8%,n) 1 100 = 100 x 0,9259 $92,59

2 100 + 10%(100) = 110 x 0,8573 94,3 3 110 + 10%(110) = 121 x 0,7938 96,05 4 121 + 10%(121) = 133,1 x 0,735 97,83

5 133,1 + 10%(133,1)= 146,41 x 0,6806 99,65 $480,42

04/17/23 43

Geometric Gradient (11)

P = A1 1 – (1 + g)n(1+i)-n

i – g

= 100 1 – (1,1)5(1,08)-5 = $480,42

0,02

04/17/23 44

Nominal and Effective Interest(1) Nominal interest rate per year, r , is the annual interest

rate without considering the effect of any compounding example : the bank pays 2.5 % interest every six

months. The nominal interest rate per year , r , therefor, is 2 x 2.5 % = 5%

Effective interest rate per year, ieff , is the annual interest rate taking into account the effect of any compounding during the year.

Example : we saw $100 left in the savings account for one year increased to $105.06, so the interest paid was $5.06. the effective interest rate per year, ieff is $5.06/$100 = 5.06%

04/17/23 45

Nominal and Effective Interest(2) If : r = Nominal interest rate per year

i = effective interest rate per compounding subperiod

m= Number of compounding subperiods per year.

ieff = (1 + r/m)m – 1 atau ieff = (1 + i)m – 1.

For continuous compounding, maka ieff = er - 1

04/17/23 46

Nominal and Effective Interest(3)

If a savings bank pays 1.5% interest every three months, what are the nominal and effective interest rate per year ?

r = 4 x 1,5% = 6 %

ieff = (1+r/m)m – 1 atau ieff = (1+i)m – 1 = (1+0,06/4)4 – 1 = (1+0,015)4 - 1 = 0,061 = 0,061 = 6,1 % = 6,1 %

04/17/23 47

Continuous Compounding(1) Since The interest period is normally one year, we’ll use

the following notation :

- r = Nominal interest rate per year

- m = Number of compounding subperiods per year

- r/m = Interest rate per interest period

- mn = Number of interest periods in n years

F = P(1+i)n may be rewritten as F = P(1+r/m)mn

if we increase m without limit, m becomes very large approaches infinity, and r/m becomes very small approaches zero

04/17/23 48

Single Payment Interest Factors Continuous Compounding(1)

lim 1mn

x

rF P

m

1/lim 1

rnx

xF P x

If we set x = r/m, then mn may be written as (1/x)(rn)

Because

F = P(1+i)n becomes F = Pern = P(F/P,r,n) and P = F(1+i)-n becomes P = Pe-rn = F(P/F,r,n)

1/lim 1 2.71828

x

xx e

04/17/23 49

Single Payment Interest Factors Continuous Compounding(2)

Example :

If you were to deposit $2000 in a bank that pays 5% nominal interest, compounded continuously, how much would be in the account at the end of two years?

r = 0,05 ; n = 2

F = P(er n)

F = 2000(e0,05x2)

= $ 2210,4

04/17/23 50

Uniform Payment Series Continuous Compounding If we subsitute the equation i = er – 1 into the equations

for periodic compounding, we get :a. Continuous Compounding Sinking Fund :

(A/F,r,n) = er – 1 er n – 1

b. Continuous Compounding Capital Recovery :(A/P,r,n) = er n (er – 1)

er n – 1c. Continuous Compounding Series Compound

Amount (F/A,r,n) = er n – 1

er – 1

04/17/23 51

Uniform Payment Series Continuous Compounding(2)

• A man deposited $500 per year into a credit union that paid 5% interest, compounded annualy. At the end of five years, he had $2763 in the credit union. How much would he have if the paid 5% nominal interest, compounded continuously ?A = $500 ; r = 0,05 ; n = 5F = A(F/A,r,n) = er n – 1

er – 1 = 500 e0,05(5) – 1 e0,05 – 1 = $ 2769,84

04/17/23 52

Continuous, Uniform Cash Flow (1 period) with continuous compounding at nominal interest rate (r)(1)

Uniform cash flow P be distributed over m subperiods within one period (n = 1)

• Compound Amount :

• Present Worth :

1 2 3 … n

F

1 2 3 … n

P

r

rnr

re

eenrPF

))(1(),,/(

rn

r

re

enrFP

)1(),,/(

P

F

04/17/23 53

Continuous, Uniform Cash Flow (1 period) with continuous compounding at nominal interest rate (r)(2)

Example :

A self-service gasoline station has been equipped with an automatic teller machine (ATM). Customer may obtains gasoline simply by inserting their ATM bank card into the machine and filling their car with gasoline, the ATM unit automatically deducts the gasoline purchase from the customer’s bank account and credits it to the gas station’s bank account. The gas station received $40.000 / month in this manner with the cash flowing uniformly troughout the month. If the bank pays 9% nominal interest, compounded continuously, how much will be in the gasoline station bank account at the end of the month?

04/17/23 54

Continuous, Uniform Cash Flow (1 period) with continuous compounding at nominal interest rate (r)(3)

r = nominal interest rate per month

= 0,09 / 12 = 0,0075

F = P (er – 1)(er n) = 40.000 (e0,0075 –1)(e0,0075(1))

rer 0,0075e0,0075

F = $40150,4