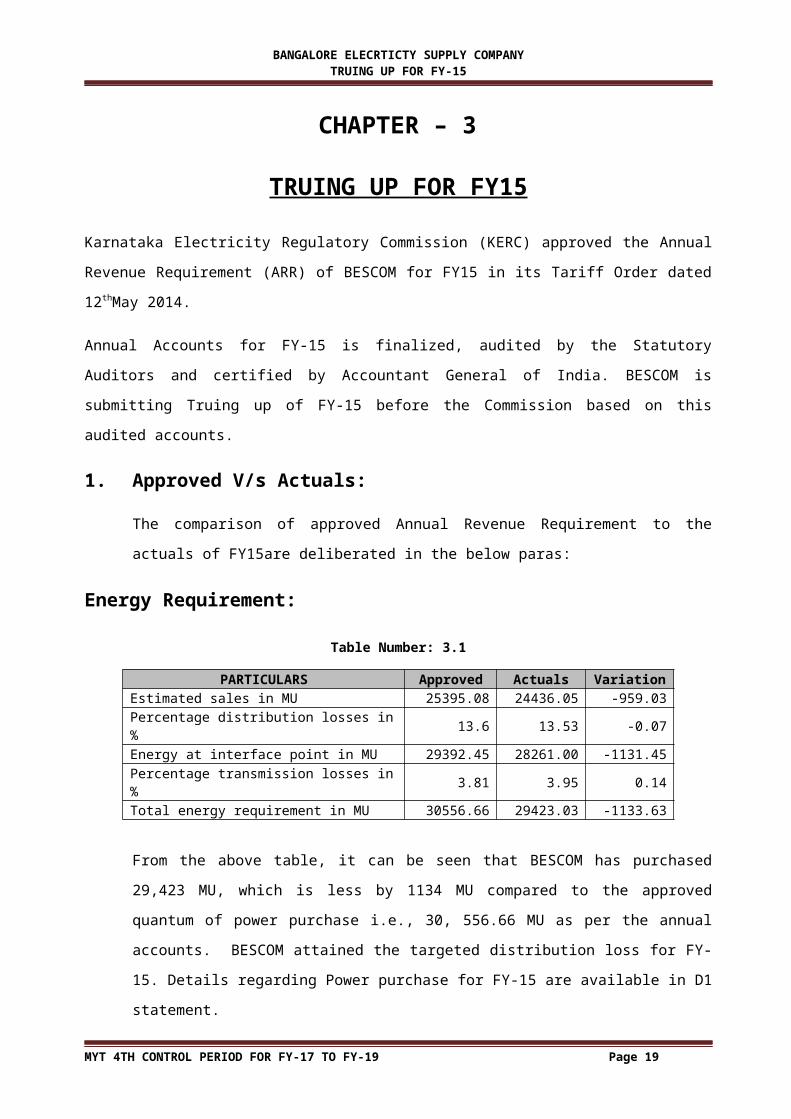

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15 CHAPTER – 3 TRUING UP FOR FY15 Karnataka Electricity Regulatory Commission (KERC) approved the Annual Revenue Requirement (ARR) of BESCOM for FY15 in its Tariff Order dated 12 th May 2014. Annual Accounts for FY-15 is finalized, audited by the Statutory Auditors and certified by Accountant General of India. BESCOM is submitting Truing up of FY-15 before the Commission based on this audited accounts. 1. Approved V/s Actuals: The comparison of approved Annual Revenue Requirement to the actuals of FY15are deliberated in the below paras: Energy Requirement: Table Number: 3.1 PARTICULARS Approved Actuals Variation Estimated sales in MU 25395.08 24436.05 -959.03 Percentage distribution losses in % 13.6 13.53 -0.07 Energy at interface point in MU 29392.45 28261.00 -1131.45 Percentage transmission losses in % 3.81 3.95 0.14 Total energy requirement in MU 30556.66 29423.03 -1133.63 From the above table, it can be seen that BESCOM has purchased 29,423 MU, which is less by 1134 MU compared to the approved quantum of power purchase i.e., 30, 556.66 MU as per the annual accounts. BESCOM attained the targeted distribution loss for FY- 15. Details regarding Power purchase for FY-15 are available in D1 statement. MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19 Page 19

Transcript

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

CHAPTER – 3

TRUING UP FOR FY15

Karnataka Electricity Regulatory Commission (KERC) approved the Annual Revenue Requirement

(ARR) of BESCOM for FY15 in its Tariff Order dated 12thMay 2014.

Annual Accounts for FY-15 is finalized, audited by the Statutory Auditors and certified by

Accountant General of India. BESCOM is submitting Truing up of FY-15 before the Commission based

on this audited accounts.

1. Approved V/s Actuals:

The comparison of approved Annual Revenue Requirement to the actuals of FY15are

deliberated in the below paras:

Energy Requirement:

Table Number: 3.1

PARTICULARS Approved Actuals VariationEstimated sales in MU 25395.08 24436.05 -959.03Percentage distribution losses in % 13.6 13.53 -0.07Energy at interface point in MU 29392.45 28261.00 -1131.45Percentage transmission losses in % 3.81 3.95 0.14Total energy requirement in MU 30556.66 29423.03 -1133.63

From the above table, it can be seen that BESCOM has purchased 29,423 MU, which is less by

1134 MU compared to the approved quantum of power purchase i.e., 30, 556.66 MU as per

the annual accounts. BESCOM attained the targeted distribution loss for FY-15. Details

regarding Power purchase for FY-15 are available in D1 statement.

Power Purchase Cost:

Comparison of actual Power purchase with respect to Commission approved in the Tariff

Order dated 12.05.2014 is shown below:

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 19

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Short Term/Medium Term 6.36% 11.48% 5.12% 9.50% 16.48% 6.98%

TOTAL 100.00% 100.00% 100.00% 100.00%

From the above table it can be seen that there is an energy shortage of -0.13%, -0.69%, -

0.81%, -2.94% and -0.81% in Juralahydel, KPCL thermal, CGS supply, IPPs and NCE

respectively. This energy shortage is made good by 5.12% through short term. Likewise, the

power purchase cost has reduced by -0.06%, -0.34%, -2.11%, -3.65%, and -0.85% in

Juralahydel, KPCL thermal, CGS supply, IPPs and NCE respectively. Power purchase

increased by 6.98% in short term.

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 20

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

The Commission approved the power procurement of 30,556.66 MU which includes

3,323.87 MU of energy from NCE sources for FY 15 to BESCOM. The actual percentage of

NCE to the total purchase is 11.45 % and solar energy is 362.33 MU which works out to

1.23% of the actual l power purchase. Details are as under.

Table Number: 3.4

Particulars UoM Reference QuantumEnergy Sales from Apr-14 to Mar-15 MU A 29423.03Solar RPO as per RPO Regulations % B 0.25Energy to be purchased through solar during FY 15 MU C=AXB 73.56RE RPO as per RPO Regulations % D 10Total RE to be purchased during FY 15 MU E=AXD 2942.3Purchased through Solar MU F 362.33Actual total RE purchase MU G 3369.60Shortfall/Excess – Solar MU H=C-F -288.77Shortfall/Excess – RE MU I=E-G -427.3

Power purchase cost has increased by7paise above the approved cost. Commission is

requested to true up actual power purchase cost of Rs.11, 689.55Cr.

Transmission Charge:

As shown in table 1.2, State Transmission charges was increased by Rs.10.05 Cr., SLDC

charges by Rs. 5.27 Crs and Central transmission charges was increase by Rs. 14.03 Cr. Thus

total transmission charges increased by Rs.29.35Cr. Commission is requested to true up the

net increase in transmission charge of Rs. 29.35Crs. above the approved cost.

Capital Expenditure for FY-15:

The capital expenditure for FY15 is depicted in the table below:

Table Number: 3.5

Sl. No. Nomenclature of work

FY 2014-15 (Rs. In Lakhs)Sanctioned

BudgetExpenditure

Incurred1 E & I Works(11kV link lines) 5000 5458.0332 E & I Works(Additional DTC's) 4000 5412.64

3Expenditure incurred under E& I Works(HT and LT reconductoring, Providing AB cable, Spill over, Urgent works, Emergency and T&P etc.,)

15300 19575.31

4 Local Planning 2000 3130.065 Ganga Kalyana

45003475.97

6 Service Connection & Drinking water supply 8534.777 Meter Programming 9500 19316.068 Replacement of Faulty transformers by new Transformers 1500 10154.489 Providing infrastructure to Unauthorized IP sets 6000 16677.58

10 RGGVY 12th plan 0 14.993

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 21

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

13 DAS 5052.5514 R-APDRP Part-B 3418.2515 HVDS 12000 24896.0916 Civil Eng works and DSM 2500 2936.20

Total 76300 147458

Operation and Maintenance Expenses:

Operation and Maintenance Expenses (O&M Expenses) includes, Repair and Maintenance

expenses, Employee cost and Administrative and General Expenditure. Commission is

approving O&M Expenses through formula on normative basis. Factors contributing for

increase in O&M expenses are Inflation index and consumer growth rate. Increases in cost

by these indices are reduced to an extent of predetermined BESCOM’s efficiency factor of

1%.

For-15, to arrive at normative O&M expenses, Commission considered previous 12 years

Consumer Price Index (CPI-IW) and Whole sale Price Index (WPI) (i.e., 2002 to 2013) at the

ratio of 80:20 and weighted inflation index was arrived through statistical formula.

Computed weighted inflation index was6.89%. Consumer growth rate at 5.37% was

considered by taking 3 years CAGR upto FY-13. Approved O&M expenses is compared with

the actual as under.

Approved O&M expenses for FY-15 is per Tariff Order dated 12.05.2014 is shown below:

Table Number: 3.6

Particulars FY15No. of Installations 9260781Weighted Inflation Index (WII) 6.89%Consumer Growth Index (CGI) based on 3 Year CAGR 5.37%Actual O & M expenses for FY13 in Rs. Crs 901.15O&M expenses in Rs. Crs 1110.95

As per accounts of FY-15, O&M expenses are as follows:

1. BESCOM has filed an appeal petition before Hon’ble Appellate Tribunal for Electricity regarding true

up of expenses for FY- 14 including O&M expenses. However, for the purpose of computation

Commission approved O&M cost for FY-14 is considered.

2. Tabulation of approved O&M cost for FY-15 vide table5.10 of T.O 2014, dated 12.05.2014 needs to be

relooked as computation of O&M cost as per the formula works out Rs.1002.62Crs.as against

1110.95Crs.

3. Commission in its Tariff Order -2013, for computation of FY-15 O&M expenses, FY-13 figures were

considered instead of FY-14.

Comparison of approved, actual and proposed for truing up for FY15 is depicted below:

Table Number: 3.16

Sl.No. PARTICULARS Approved by the Commission for FY-15

Actuals as per Accounts

Proposed for Truing up on normative basis

1 O&M Expenses 1110.95 1054.60 1084.80

Commission is requested to true up the O&M expenses of Rs.1084.80 Cr. on normative basis.

Depreciation:

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 28

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Depreciation amount of Rs. 310.28Crs is worked out as per annual accounts for FY-15. After

deducting an amount of Rs. 110.50 Crs. as per Accounting Standard (AS) – 12, the net

depreciation works out to Rs. 199.78Crs.

Computation of Depreciation as per audited accounts for FY-15 is shown below:

Table Number: 3.17

PARTICULARS Amount in Rs. Crs.Gross fixed asset at the beginning of the year 5605.28Additions 1645.01Deductions 175.93Gross fixed asset at the end of the year 7074.36Depreciation provided 310.28Average rate of Depreciation ( on 90% gross fixed asset) 4.87%Assets created on Contributions, subsides and grant at the beginning of the year 1426.28Additions 396.12Deductions 110.49Gross fixed asset created on contributions, subsidies and grants at the end of the year 1711.89Depreciation with drawn as per AS-12 110.49Average rate of depreciation with drawn as per AS-12 6.45%

The average rate of depreciation works out to 4.87%, which is comparable with the KERC

prescribed rate of depreciation at 5.04%. Depreciation rate for the assets created under

contribution, subsidy and grants is at the rate of 6.45%.

It is ascertained that the average depreciation rate of depreciation for the assets held works

out to 4.87% and average depreciation withdrawn as per AS-12 works out 6.45%. The

difference is only by 1.58%. The error occurred in the previous years is rectified duly

considering the average life of all the assets.

Commission is requested to true up the depreciation of Rs.199.78 Cr. as per actual.

Interest and Finance Charges:

As per MYT regulations, Commission is allowing actual interest incurred on the loans

borrowed towards creation of Capital Assets, interest paid towards consumer deposit and

interest on working capital on normative basis.

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 29

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Breakups of interest and finance charges are as under:

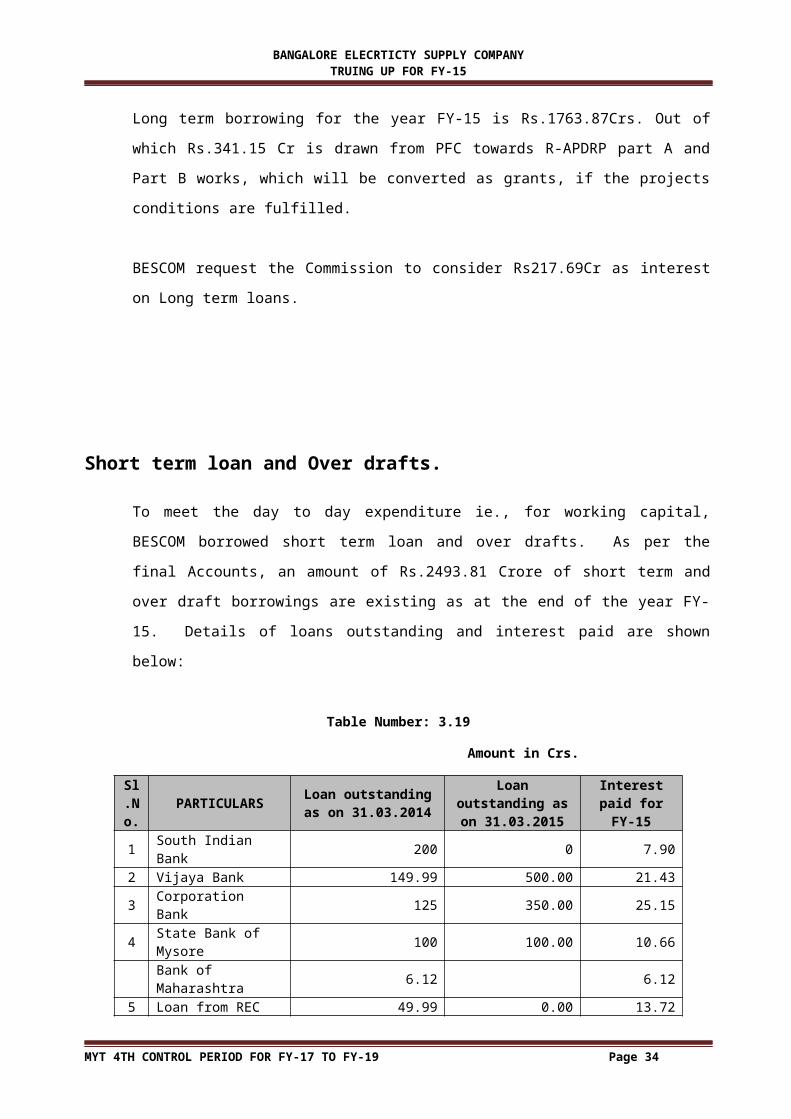

Long term loan

As per the final Accounts, an amount of Rs.1763.87 Crore of long term borrowings are

existing as at the end of FY-15. Details of loans outstanding and interest paid are shown

Benchmark Prime Lending Rate (BPLR) reduced from 14.60% p.a. to 14.45% p.a.

w.e.f.08.06.2015.

Base Rate reduced from 09.85% p.a. to 9.70% p.a. w.e.f. 08.06.2015.

Hon’ble Commission in its earlier Tariff Orders considered only 11.75% as rate of interest on

working capital.

Commission continued the same in Tariff Order dated 02.03.2015, had considered 11.75% as the

rate of interest for the computation of working capital without looking into the short-term prime

lending Rate of State Bank of India as on 1st April of the year.

As per the notified MYT regulations, Interest and finance charges are termed as controllable

expenditure. Commission approves the expenditure based on the normative basis. Expenditure

over and above the normative level shall be charged to the Licensee and any gain on this count shall

be allowed to be retained by the Licensee.

Commission by amending the regulation 3.11.2 opted to charge the Licensee for over and above the

cost on normative basis but chose to limit the gains on this count by 50%.

This amendment will not encourage competition and will not support the improvement in the

efficiency of the Licensee which is against the core objective of the Electricity Act-2003. Electricity

Act 2003 is enacted with an ambition to encourage competition and for improvement in the

efficiency of the electrical industry.

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 34

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

It is submitted to the Commission that any regulations which are not in line with the Electricity Act-

2003 will become null and void.

Hon’ble Appellate Tribunal for Electricity in its judgment dated 2nd January 2013, vide appeal

No.108/2010, FKCCI V/s KERC and other ruled vide para 39 that :“The Commission has no power to

deviate from its own MYT Regulations and ………without amending the MYT Regulations”

Hon’ble Commission is requested to adhere to the regulations prevailing for the computation of

working capital.

Rate of interest on working capital existed as on 1st of April 2014 is 14.60% as per SBI web site.

Computed interest on working capital on normative basis is as under:

Table Number: 3.24

Sl.No Particulars Amount Amount1 2 months Receivables (Rs.13479.60/6M) 13479.60 2246.602 One month O&M expenses (Rs.1054.60/12 M) 1084.80 90.403 1% of Gross fixed Assets as on 01.04.2014 (Rs.5605.27) 5605.27 56.05

Total 2393.054 Allowable Interest on working capital at 14.60% 349.38

5 Actual interest incurred for working capital 247.73

6 Savings to the Normative cost 101.65

7Allowable interest on working capital (50% of savings+ actual cost) ( As per amended version)

298.35

It is submitted before the Commission that, Hon’ble Appellate Tribunal in OP 01/2011 has ruled

that, interest on working capital cannot be comparable with the actual cost or normative

expenditure cannot be shared to the consumers. It should be fully passed to the Licensee. The

extract of the judgment of the Hon’ble ATE of OP01/2011 dated 5th January 2012 is reiterated for

kind reference:

4.6.5.2 Rate of interest on working capital so assessed on normative basis, shall be equal to the

short-term prime lending rate of State Bank of India as on the 1st April of the year preceding the

year for which tariff is proposed to be determined or at the actual rate of borrowing whichever is

less”.

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 35

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

The Regulations provide that the working capital will be assessed on normative basis but the

interest rate on working capital shall be the short term prime lending rate of SBI as on 1stApril of

the preceding year or the actual rate of borrowing, whichever is less.

8.4. This issue has already been decided by this Tribunal in the case of Reliance Infrastructure Ltd.

vs. Maharashtra Electricity Regulatory Commission &Ors. Reported as 2009 ELR (APTEL) 0672.

The relevant extracts of the judgment are reproduced below:

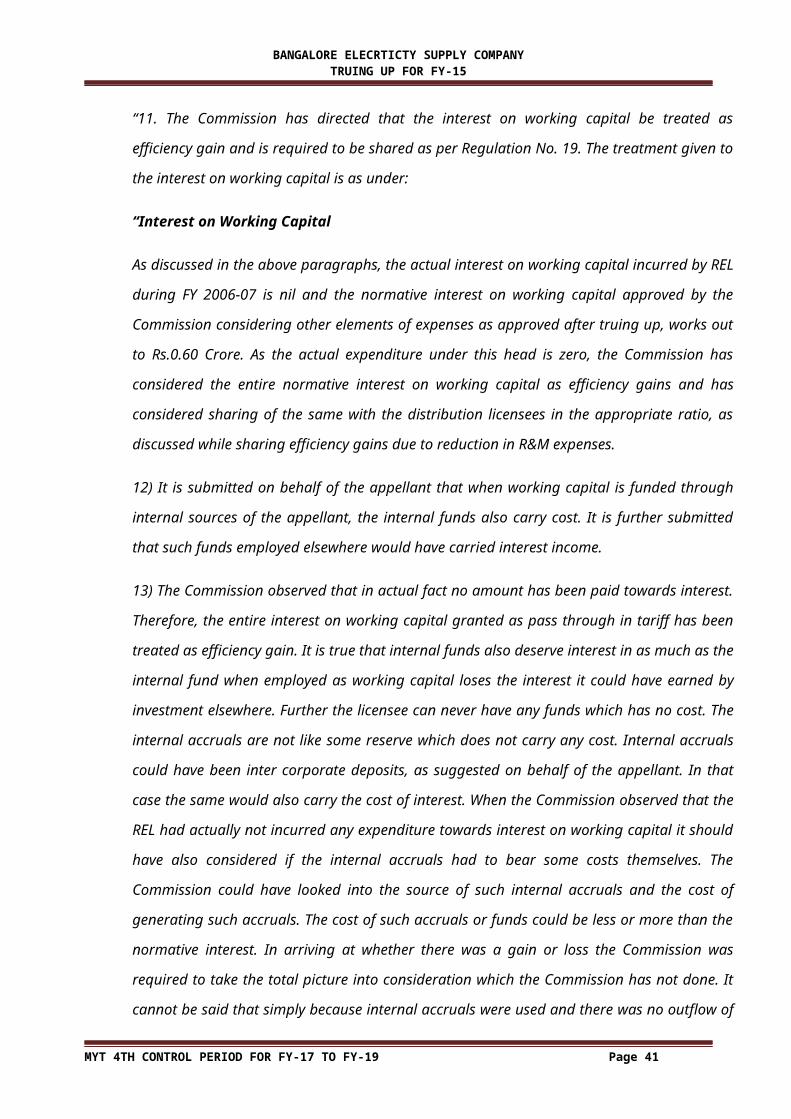

“11. The Commission has directed that the interest on working capital be treated as efficiency gain

and is required to be shared as per Regulation No. 19. The treatment given to the interest on

working capital is as under:

“Interest on Working Capital

As discussed in the above paragraphs, the actual interest on working capital incurred by REL

during FY 2006-07 is nil and the normative interest on working capital approved by the

Commission considering other elements of expenses as approved after truing up, works out to

Rs.0.60 Crore. As the actual expenditure under this head is zero, the Commission has considered the

entire normative interest on working capital as efficiency gains and has considered sharing of the

same with the distribution licensees in the appropriate ratio, as discussed while sharing efficiency

gains due to reduction in R&M expenses.

12) It is submitted on behalf of the appellant that when working capital is funded through internal

sources of the appellant, the internal funds also carry cost. It is further submitted that such funds

employed elsewhere would have carried interest income.

13) The Commission observed that in actual fact no amount has been paid towards interest.

Therefore, the entire interest on working capital granted as pass through in tariff has been treated

as efficiency gain. It is true that internal funds also deserve interest in as much as the internal fund

when employed as working capital loses the interest it could have earned by investment elsewhere.

Further the licensee can never have any funds which has no cost. The internal accruals are not like

some reserve which does not carry any cost. Internal accruals could have been inter corporate

deposits, as suggested on behalf of the appellant. In that case the same would also carry the cost of

interest. When the Commission observed that the REL had actually not incurred any expenditure

towards interest on working capital it should have also considered if the internal accruals had to

bear some costs themselves. The Commission could have looked into the source of such internal

accruals and the cost of generating such accruals. The cost of such accruals or funds could be less

or more than the normative interest. In arriving at whether there was a gain or loss the

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 36

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Commission was required to take the total picture into consideration which the Commission has

not done. It cannot be said that simply because internal accruals were used and there was no

outflow of funds by way of interest on working capital and hence the entire interest on working

capital was gain which could be shared as per Regulation No. 19. Accordingly, the claim of the

appellant that it has wrongly been made to share the interest on working capital as per Regulation

19 has merit”.

In the above judgment the Tribunal has held that the working capital funded through internal

sources also carry cost. Such funds employed elsewhere would have carried interest income.

8.5. The above issue has also been dealt with in this Tribunal’s judgment dated 28.8.2009 in Appeal

No. 117 of 2008 in the matter of Reliance Infrastructure Ltd. vs. Maharashtra Electricity

Regulatory Commission &Ors. The relevant extract is reproduced below:

“15. In Appeal No.111/08, in the matter of Reliance Infrastructure v/s MERC and Ors., this Tribunal

has dealt the same issue of full admissibility of the normative interest on Working Capital when the

Working Capital has been deployed from the internal accruals. Our decision is set out in the

following paras of our judgment dated May 28, 2008 in Appeal No. 111 of 2008.

“7) The Commission observed that in actual fact no amount has been paid towards interest.

Therefore, the entire interest on Working Capital granted as pass through in tariff has been treated

as efficiency gain. It is true that internal funds also deserve interest in as much as the internal fund

when employed as Working Capital loses the interest it could have earned by investment elsewhere.

Further the licensee can never have any funds which has no cost. The internal accruals are not like

some reserve which does not carry any cost. Internal accruals could have been inter corporate

deposits, as suggested on behalf of the appellant. In that case the same would also carry the cost of

interest. When the Commission observed that the REL had actually not incurred any expenditure

towards interest on Working Capital it should have also considered if the internal accruals had to

bear some costs themselves. The Commission could have looked into the source of such internal

accruals or funds could be less or more than the normative interest. In arriving at whether there

was a gain or loss the Commission was required to take the total picture into consideration which

the Commission has not done. It cannot be said that simply because internal accruals were used

and there was no outflow of funds by way of interest on Working Capital and hence the entire

interest on working capital was gain which could be shared as per Regulation No. 19. Accordingly,

the claim of the appellant that it has wrongly been made to share the interest on Working Capital

as per Regulation 19 has merit.

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 37

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

15. b): The interest on Working Capital, for the year in question, shall not be treated as efficiency

gain.

16. In view of our earlier decision on the same issue we allow the appeal in this view of the matter and hold that the entire interest on normative interest rate basis is payable to the appellant”.

From the above judgment, interest on working capital is to be allowed on normative basis and it

cannot be considered as efficiency gain and entire interest on normative interest rate basis is

payable to the Licensee. Hence it is requested to allow interest on working capital on normative

basis which works out to Rs.348.98 Crs.

Interest on consumer Security Deposit:

As per Section 47(4) of the Electricity Act 2003 and KERC Regulations on interest on

security deposits, the ESCOMs have to pay interest on consumer deposits at prevailing bank

rate.

Reserve Bank of India vide letter No. RPCD.CO.RRB.RCB.BC. No. 82 /03.05.33/2013-14

January 29, 2014, revised the Bank rate from 8.75 to 9 percent from 28 January 2014.

Hence, 9 percent Bank rate is paid to the consumer deposit.

As per the final accounts, Consumer deposit held as on 31.03.2015 is Rs.

2831.86Crs.Applying bank rate of interest at 9% on consumer deposit, interest component

works out to Rs.254.86Crs.

As per accounts, BESCOM has incurred Rs.210.37 Crores towards payment of interest on

consumer security deposit for the year FY-15. Interest incurred is within the Bank rate of

RBI. Calculations are as follows:

Interest on consumer deposits for FY15

Table Number: 3.25

Rs. in CroreParticulars FY15

Opening balance of consumer deposit 2453.79

Outstanding balance of consumer deposits. 2831.86

Interest on consumer deposits 210.37

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 38

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Weighted average Rate of Interest 7.96%

BESCOM requests the Commission to allow the amount of Rs. 210.37Crs for FY-15 towards

interest on security deposit which is within the Bank rate of 9%.

Other finance charges: As per accounts of BESCOM, Rs. 10.19 Cr. is incurred towards other

finance charges.

Table Number: 3.26

Finance chargesBank charges 10.19

Interest and Finance Charges approved actual and proposed for truing up

for FY-15 is tabulated as under:

Table Number: 3.27

Sl.No PARTICULARS

Approved by the Commission for

FY-15

Actuals as per Accounts

Proposed for Truing up on

normative basis1 Interest on Loan Capital 160.92 217.69 217.692 Interest on Working Capital 265.15 247.73 348.983 Interest on Consumers Deposit 214.74 210.37 210.374 Other Interest & Finance Charges 7.63 10.19 10.19

Total 648.44 685.98 787.23

The Commission is requested to approve the interest and finance charges of Rs.787.23Crs.

For FY-15

Expenses capitalized.

As per the audited accounts following are the expenses capitalized.

Table Number: 3.28

SL. NO PARTICULARS Current Year 2014-151 Interest and finance charges 67.75

2 Employee cost 4.75

3 Administrative and General expenses 6.37

Total 78.87

Commission requested to allow 78.87 Cr to capitalize for FY-15

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 39

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Other Debits:

Commission is approving the other debits based on actuals. As per accounts other debits are as

under:

Table Number: 3.29

SL. NO PARTICULARS Current Year 2014-15OTHER DEBITS

1 Small & Low value items Written off 0.272 Asset decommissioning cost -0.043 Material cost variance -15.094 Miscellaneous losses and Write offs including provisions 5.035 Bad Debts written off 0.016 Loss of materials by pilferage, etc.,7 Provision for Loss on obsolescence of stores, etc. in stock -10.988 Losses/gain relating to Fixed Assets 14.10

Total -6.70

Commission is not considering the provisions for bad debts provided in the accounts.

Hence, Rs.8.75Crs. provided as Provision for Bad & doubtful debts is not proposed for truing

up. Commission is requested to consider Rs. (-) 6.70Crs. As other debits for FY-15

Prior period charges/credits:

Commission is approving the prior period charges/credits based on actuals. As per accounts

prior period charges/credits are as under.

Table Number: 3.30

SL. NO PARTICULARS Current Year 2014-15Other Debits

1 Short provision prior period – Depreciation 9.662 Short provision -Other expenses 4.93

Total 14.59Less:

3 Excess provision prior period- Int. finance charges 8.664 Excess provisions related prior periods 19.97

Total 28.635 Net prior period credit 14.04

Commission is requested to consider Rs.14.04Crs. Of prior period credit for FY-15.

Return on Equity:

RoE computed as per norms is shown in the table below:

Table Number: 3.31

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 40

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Rs. in Crs

Particulars FY14

Paid Up Share Capital 546.91

Add: Net profit for FY-15 113.44

Total Share capital 660.35

Reserves & Surplus -589.20

Equity for FY15 71.15

BESCOM carried accumulated loss to an extent of Rs.589.20Cr as against the share capital of

Rs.660.35Cr. Thus resulting in net share capital of Rs.71.15Crs.

As per MYT regulations Return on equity means:

“Return on equity shall be computed on the equity base determined in accordance with

clause 3.7 above and shall be @ 14% per annum.

For the purpose of return on equity, any cash resources available to the licensee from its share

premium account or from its internal resources that are used to fund the equity commitments

of the project under consideration shall be treated as equity subject to limitation contained in

clause 3.6 above. “

As per the MYT regulations, for the purpose of computation of return on equity any cash

resources available to the licensee from its share premium amount and from internal

resources that are used to fund the equity commitments of the project under consideration

shall be treated as equity.

Now, Electricity Distribution business is regulated business. Income and Expenditure of

Distribution Company is approved by KERC and latter it will be trued up based on the

actuals. Hence, the difference in the expenditure and the receipts will be validated in truing

up exercise and any excess or shortage will be carried to the next tariff revision along with

the carrying cost. Hence, any loss in the distribution business will be compensated in the

future years which restore the equity.

For an investor, Return on Equity is computed based on the amount of Capital; he has

invested into the Business. Total investment is considered as Capital (either as equity or as

debt). Investment by way of debt will reduce only when the repayment is done towards the

principal amount of debt. Likewise, reduction in equity happens only when Capital is

withdrawn from the business by the investor. Loss in business never results in withdrawal

of Capital. However, profit or surplus belongs to the investor and investor re-invests the

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 41

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

surplus in business until it is withdrawn as dividend/reduction in Capital. That is the reason,

surplus should be added while computing the Return on Equity and loss “should not be”

deducted, while computing the Return on Equity. Share Capital is distinctly shown in

Balance Sheet to identify the amount of direct investment by the investor.

It can be understood easily as per below example:

Table Number: 3.32

Particulars Sitation-1 Situation-2Capital A 100 100Surplus/Loss B 200 -200Total A+B=C 300 -100RoE D 15% 15%

Tariff ComputationOther Costs E 1000 1000RoE F=D*C 45 -15Total Cost G=E+F 1045 985Total units H 1000 1000Per unit cost I=G/H 1.05 0.99

From the above table it can be seen that the other cost is Rs.1000 and the total number of units

is 1000, the minimum tariff in all circumstances should be Rs.1. However, if RoE is computed

by reducing loss from the Capital, in the above situation-2 the tariff falls below the minimum

mark of Rs.1 and leads to increase in losses. In situation -2, the RoE must be taken as Rs. 15 by

which the total cost works out to 1015. The tariff will then be 1.015 ideally.

Further, Commission is allowing ROE on the equity held at the beginning of the year. Equity

induced in the middle of the year or Incremental internal resources accrued in the months and

invested during the year should also earn the returns. If the RoE allowed for the equity held at

the beginning of the year, it will not give any returns on the equity induced during the year.

Consumers pay additional security deposit (2MMD) in the middle of the year for which interest

for that portion of the year is paid. The same analogy is also applicable to the equity

investments which are induced during the year. Hence it is requested to allow the Return on

equity for the share capital held by BESCOM at the end of year ie., 31.03.2015.

Table Number: 3.33

Rs. in Crs

Particulars Amount

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 42

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Equity held as on 31.03.2015 546.91

Return on Equity 15.5 %

Total 84.77

The Commission is requested to allow Rs 84.77Crs. as RoE.

1.13 Income Tax

As per the Annual Accounts, an amount of Rs.25.75 Crores is paid towards Income tax. The

Commission is requested to allow the same.

1.14 Other income:

Commission had approved other income to an extent of Rs. 225 Crs. As per the final

accounts for FY-15 other income is tabulated as under:

Table Number: 3.34

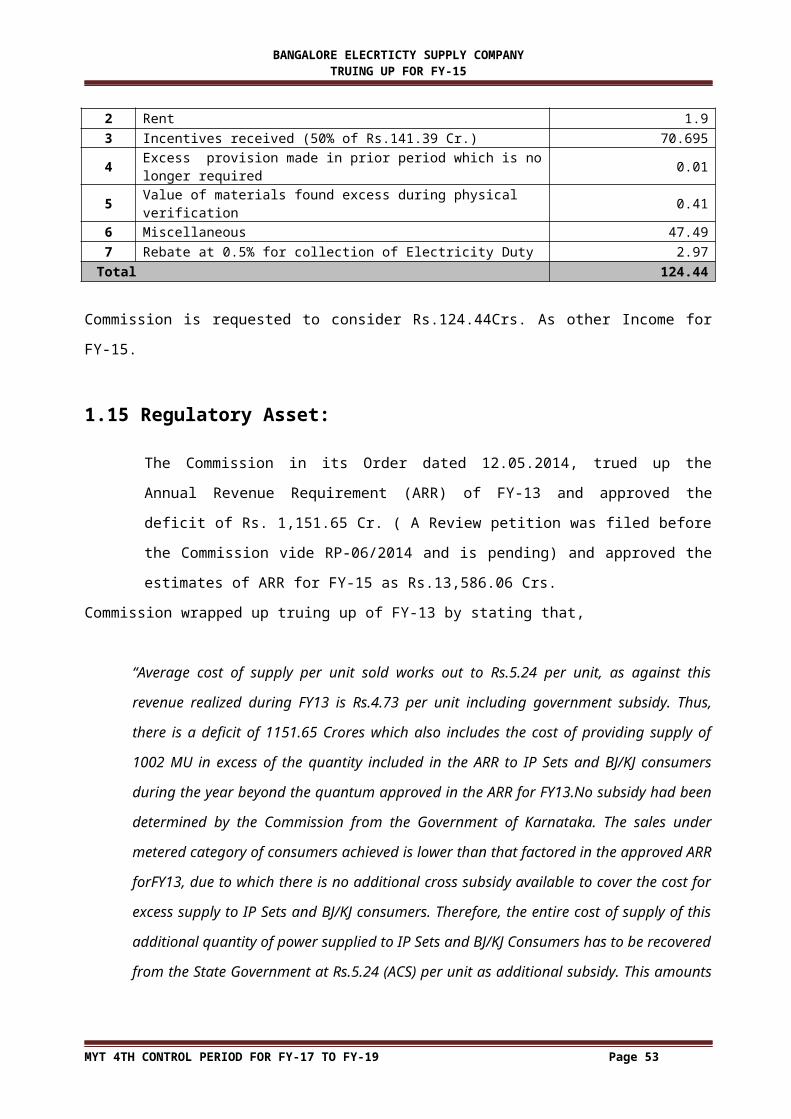

SL. NO PARTICULARS Current Year 2014-15

1 Interest on Bank Fixed Deposits 10.722 Profit on sale of stores 0.983 Rent 1.904 Incentives received 141.395 Excess provision made in prior period which is no longer required 0.016 Value of materials found excess during physical verification 0.037 Miscellaneous 47.138 Rebate at 0.5% for collection of Electricity Duty 2.97

Total 205.13

Major portion of other income is from incentives received ie., Rs.141.39 Crs.

Commission in its tariff Order -2014 issued on 12th May 2014 notes that:

‘The Commission notes that timely payment to Generators is as agreed in the power purchase

agreements. The incentive earned for such timely payments is further translated as savings in the

cost of power purchase. However, providing incentives on such financial prudence is required, to

encourage ESCOMs to be disciplined in payments to generators without incurring costs of interest

on belated payment as being reported in their accounts.

It is pertinent to focus on the Tariff Policy wherein it states that,

“…….Making the distribution segment of the industry efficient and solvent is the key to success

of power sector reforms and provision of services of specified standards. Therefore, the

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 43

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Regulatory Commissions need to strike the right balance between the requirements of the

commercial viability of distribution licensees and consumer interests. Loss making utilities need

to be transformed into profitable ventures which can raise necessary resources from the capital

markets to provide services of international standards to enable India to achieve its full growth

potential. Efficiency in operations should be encouraged. Gains of efficient operations with

reference to normative parameters should be appropriately shared between consumers and

licensees…………….”

The Commission is therefore of the view that BESCOM’s efforts in making timely payments to

generators and earning incentives in the form of rebate under the terms of PPA need to be

encouraged even though BESCOM is bound to endeavor to make prompt payments as a normal

prudence in financial management. Hence, the Commission decides to allow10% of the total

incentive“

It is brought to the kind notice of the Commission that as per the MYT regulations gains of efficient

operations with reference to normative parameters should be appropriately shared between

consumers and licensees. Hence, Commission is requested to share the efficiency gain by at least

50%.

It is submitted before the Commission, that as per the corporate cash book, closing balance on each

day is negative. This means to say always there is an overdraft. Maximum overdraft stood at 2100 Cr.

and minimum overdraft is at Rs. 700 Crs. Such being the case, earning of interest on security deposit

does not arise. It is learnt that the amount received from the Central Government towards R-APDRP

is kept as deposit in the banks for disbursement as per Schedule. Interest earned on this deposit is

considered as receipts as per final accounts.

For the purpose of truing up, this cannot be termed as Revenue receipts. If the amount released by

the Central Govt. is converted into grants, then the interest earned on this amount is also termed as

grant by the Central Govt. If it is termed as loan, then the loan amount will be reduced to the extent

of interest. On both the counts, interest earned will be a capital receipt and not the revenue receipt.

Hence, this cannot be considered as income for the purpose of truing up exercise.

As per the judgment of Hon’ble Appellate Tribunal for Electricity vide Appeal No.46/2014 dated

17.09.2014,

“The State Commission is not bound to follow the audited accounts and the State Commission can

scrutinize the same and allow the expenditure only after prudence check”

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 44

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Hence, for the purpose of truing up, interest earned on bank fixed deposits may not be considered.

Revised other income is tabulated as under:

Table Number: 3.35

SL. NO PARTICULARS Current Year 2014-151 Profit on sale of stores 0.98

2 Rent 1.9

3 Incentives received (50% of Rs.141.39 Cr.) 70.695

4 Excess provision made in prior period which is no longer required 0.01

5 Value of materials found excess during physical verification 0.41

6 Miscellaneous 47.49

7 Rebate at 0.5% for collection of Electricity Duty 2.97

Total 124.44

Commission is requested to consider Rs.124.44Crs. As other Income for FY-15.

1.15 Regulatory Asset:

The Commission in its Order dated 12.05.2014, trued up the Annual Revenue Requirement

(ARR) of FY-13 and approved the deficit of Rs. 1,151.65 Cr. ( A Review petition was filed

before the Commission vide RP-06/2014 and is pending) and approved the estimates of

ARR for FY-15 as Rs.13,586.06 Crs.

Commission wrapped up truing up of FY-13 by stating that,

“Average cost of supply per unit sold works out to Rs.5.24 per unit, as against this revenue

realized during FY13 is Rs.4.73 per unit including government subsidy. Thus, there is a deficit of

1151.65 Crores which also includes the cost of providing supply of 1002 MU in excess of the

quantity included in the ARR to IP Sets and BJ/KJ consumers during the year beyond the

quantum approved in the ARR for FY13.No subsidy had been determined by the Commission

from the Government of Karnataka. The sales under metered category of consumers achieved is

lower than that factored in the approved ARR forFY13, due to which there is no additional cross

subsidy available to cover the cost for excess supply to IP Sets and BJ/KJ consumers. Therefore,

the entire cost of supply of this additional quantity of power supplied to IP Sets and BJ/KJ

Consumers has to be recovered from the State Government at Rs.5.24 (ACS) per unit as

additional subsidy. This amounts to Rs.524.53 Crores. With this additional subsidy from the

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 45

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

Government of Karnataka, the unfilled gap for FY13 will be reduced from Rs.1151.65 Crores to

Rs.627.13 Crores”.

Commission had carried Rs.627.13 Crs. of deficit of FY-13, for determination of Tariff for FY-15.

The calculated table of the Commission is as follows.

Revenue gap for FY15

Table Number: 3.36

Particulars FY15

Net ARR including carry forward gap of FY13 (in Rs. Crores) 14213.19

Approved sales (in MU) 25395.07

Average cost of supply for FY15 (in Rs./unit) 5.60

Revenue at existing tariff (in Rs. Crores) 12653.88

Gap in revenue for FY15 (in Rs. Crores) 1559.31

Regulatory asset to be recovered over next two years (in Rs.Crores) 611.00

Balance revenue gap to be collected by revision of tariff forFY15 (in Rs. Crores) 948.31

In the above table, Commission carried the deficit of Rs.627.13 Cr. trued up gap of FY-13 to FY15.

The Commission approved annual revenue requirement of FY-15 at Rs.13, 586.06 Cr. to sum up net

ARR of Rs.14, 213.19 Cr.(13,586.06+627.13). Of which Rs.611.00 Cr. was set aside as regulatory

asset. Thus absorbing Rs. 16.13 Cr of trued up deficit of FY-13 in the ARR of FY-15. (Rs.627.13-

Rs.611 =Rs.16.13) Hence, Commission is requested to consider Rs.16.13 Crs for the purpose of

truing up of FY-15.

Carrying cost of regulatory asset:

Commission apportioned the trued up gap of FY-13, Rs.1151.65 into two parts.

Rs. 524.53 Cr. payable by Government of Karnataka and

Rs. 627.13 Cr. recoverable from tariff in the next two years. Ie., FY-16 and FY-17.

A claim for payment of Rs.524.53 Crs. was made to the Government and the said amount is not yet

considered by the government for payment. Rs.627.13 Cr apportioned to be recoverable from tariff

is deferred for the next two years ie., FY-16 and FY-17. Hence, BESCOM is eligible for carrying cost

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 46

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

at the rate of 12% p.a. on Rs.1151.65 Crs. Hence, Commission is requested to allow Rs.138.198 Cr as

carrying cost on Rs.1151.65 Crs.at 12% p.a.

Table Number: 3.37

SL. NO PARTICULARS Current Year 2014-151 Regulatory asset ( trued up gap of FY-13) absorbed in FY-15 ARR 16.1302 Carrying cost at 12% on Rs.1151.65 Crs. 138.198

1.16 Revenue from sale of power:

Revenue from sale of power is one of the topics which is not dealt by the Commission for the

purpose of truing up exercise in the previous years.

Of late, it is noticed over the years, that the expenditure is not the main cause for increase in

the deficit year on year, but it is the receipts. Hence, it is submitted before the Commission to

consider the revenue receipts from sale of power for the purpose of truing up of respective

years. This may show the path for corrective measures.

Demand, Collection and Balance (DCB) for FY-15 as per accounts are as follows:

10 Interest on Loans 160.92 217.6811 Interest on Working capital 265.15 348.9812 Interest on consumer deposits 214.74 210.3813 Other Interest & Finance charges 7.63 10.1914 Less interest & other expenses capitalized 39.99 78.87

15 Funds towards Consumer Relations/Consumer

1

15 Other debits (6.70)16 Prior period credits (14.04)17 ROE 84.7718 Income tax 25.7516 Other Income 225 124.4417 Regulatory asset 16.12 16.1318 Carrying cost 138.19

ARR 13602.19 13797.65GAP 0 722.47

19 Sales 25395.07 24436.08

MYT 4TH CONTROL PERIOD FOR FY-17 TO FY-19Page 54

BANGALORE ELECRTICTY SUPPLY COMPANY TRUING UP FOR FY-15

20 Average cost of supply 5.36 5.65

As per proposed trued up figures, average cost of supply shoots up to Rs. 5.65 per unit as against

approved average cost of Supply of Rs. 5.36 per unit. Commission is requested to approve the above