Peaks And Valleys in the World of Lentils Thomas W. Higginson (author, aboli- tionist and leader of men) once said, "Great men are rarely isolated mountain peaks, they are the summits of ranges". I have always thought of green lentil growers as "great men and women" who do not mind being seen as contrarians, or as mountain peaks. Unfortunately in these last several years, there was no room to be anything other than in the valley of oversupply, as lentils were the best game in town and everyone joined in. Upshot: we oversupplied and prices plunged. Now we have a more orderly supply and a better return to the values growers deserve. The challenge before us is maintaining current levels and helping preserve market integrity, especially for those who have stepped up to the new crop plate and paid the 23 and 25 cent prices for lairds. At Pulse Days in Saskatoon, the consensus seems to be that growers will increase lentil acres by over 20 per cent to 1.75 million. That is not so bad if most of the increase comes from red lentils (currently priced at 22 - 24 for new crop), but that seems unlikely. If we increase green lentil plantings too far, we run the danger of oversupply, but not necessarily imploded values. The most inelastic of green lentils are Eston type. If you see a bid that starts with a ‘2'...sell! Our buyers are well covered. With medium green lentils, I am tempted to say "if you see any bid, then sell," but that would be a little facetious. They are simply not very popular. Canada's game is in large green lentils. We rule. But demand at today's prices is finite. With all the excitement for oilseeds, grains and the mighty yellow pea, lentils have been a bit in the shadows. Expect demand to stay steady with most emphasis on No.2's. Try to meet demand when it is there. Prices are close to 27-28 cents, which I believe is very good. Meanwhile the flow of the market is not as orderly as we would like. On the other hand, "don’t be short the grower", is a maxim most are starting to live by. (“Don't be short the freight “ is another maxim we are embracing). With oil prices escalating and with vessel space around the world at a premium, gazing off into new crop values in January for next fall is not such a joyful prospect. As exporters, another dilemma is determining how much to expect freight rates to increase in next nine months and how that will factor into the price. Conceivably, there is 1-2 cents per pound we have to find from now until then. Will growers be asked to give that up or will the buyer pay it? Martin Chidwick is Senior Vice President Canada and International Operations with Bissma Pacific in Winnipeg, MB. ([email protected]) February 2008 Saskatchewan Pulse Growers / Green Lentil Market Report Bears&Bulls OPINION The Green Lentil Market Report is a monthly newsletter designed to provide technical data and market commentary to Saskatchewan lentil producers to assist with green lentil production and marketing decisions. Each month different contributors from the industry will provide their opinions in our Bears and Bulls column. Brian Clancey of STAT Publishing will be a regular contributor in our On the Market column. Martin Chidwick Bissma Pacific Inc.

Transcript

Peaks And Valleys in theWorld of Lentils

Thomas W.Higginson(author, aboli-tionist and leaderof men) oncesaid, "Great menare rarely isolatedmountain peaks,they are the

summits of ranges". I have alwaysthought of green lentil growers as"great men and women" who do notmind being seen as contrarians, or asmountain peaks. Unfortunately inthese last several years, there was noroom to be anything other than in thevalley of oversupply, as lentils were thebest game in town and everyonejoined in. Upshot: we oversuppliedand prices plunged.

Now we have a more orderly supply anda better return to the values growersdeserve. The challenge before us ismaintaining current levels and helpingpreserve market integrity, especially for

those who have stepped up to the newcrop plate and paid the 23 and 25 centprices for lairds.

At Pulse Days in Saskatoon, theconsensus seems to be that growerswill increase lentil acres by over 20per cent to 1.75 million. That is not sobad if most of the increase comes fromred lentils (currently priced at 22 - 24for new crop), but that seems unlikely.If we increase green lentil plantings toofar, we run the danger of oversupply,but not necessarily imploded values.

The most inelastic of green lentils areEston type. If you see a bid that starts witha ‘2'...sell! Our buyers are well covered.With medium green lentils, I am temptedto say "if you see any bid, then sell,"but that would be a little facetious.They are simply not very popular.

Canada's game is in large green lentils.We rule. But demand at today's pricesis finite. With all the excitement foroilseeds, grains and the mighty yellowpea, lentils have been a bit in theshadows. Expect demand to stay

steady with most emphasis on No.2's.Try to meet demand when it is there.Prices are close to 27-28 cents, which Ibelieve is very good.

Meanwhile the flow of the market isnot as orderly as we would like. On theother hand, "don’t be short thegrower", is a maxim most are startingto live by. (“Don't be short the freight “is another maxim we are embracing).With oil prices escalating and withvessel space around the world at apremium, gazing off into new cropvalues in January for next fall is notsuch a joyful prospect. As exporters,another dilemma is determining howmuch to expect freight rates to increasein next nine months and how that willfactor into the price. Conceivably, there is1-2 cents per pound we have to find fromnow until then. Will growers be askedto give that up or will the buyer pay it?

Martin Chidwick is Senior Vice PresidentCanada and International Operationswith Bissma Pacific in Winnipeg, MB.([email protected])

February 2008

Saskatchewan Pulse Growers / Green Lentil Market Report

Bears&BullsOPINION

The Green Lentil Market Report is a monthly newsletter designed to provide technical data and market commentary toSaskatchewan lentil producers to assist with green lentil production and marketing decisions. Each month different contributorsfrom the industry will provide their opinions in our Bears and Bulls column. Brian Clancey of STAT Publishing will be a regular

contributor in our On the Market column.

Martin ChidwickBissma Pacific Inc.

Can you really ration demandfor lentils when your customeris hungry?

Economic theory:raise the priceand decreasedemand. Theendless discussionin the grain/foodmarkets equatesto raise theprice and the

customers will… what… will eat less?

At the beginning of the marketing yearthere was an estimated 817,000 MTof lentils to market. From Aug – Oct2007, 267,000 MT were exported.Market demand continued to be stronginto November and December and it issafe to assume that exports kept thepace of 90,000 MT per month. Addingin 117,000 MT for seed and domesticneeds, leaves 253,000 MT in the market.

The last bin will never be purchased, sothat carry out at July 31 is going to50,000 MT. The carry this year is notgoing to be a lack of demand; it will bethe farmer choosing not to sell. All ofthe above leaves us with 203,000 MTas of January 2008 to market for thenext seven months (29,000 MT permonth for the next seven months).Trying to ration demand to a hungrycustomer by decreasing exports from90,000 MT to 29,000 MT per month isgoing to be met with price increases atthe farm gate, as the market attemptsto ration out demand. To explain thisin more simplistic terms, we do nothave the product in Canada tocontinue exporting it at the current rate.Consumers worldwide won’t be dialingJenny Craig’s 1-800 line anytime soon.Add to that the dryness in our best

lentil area this fall and winter, and youwill be prying lentils from farmer’s bins.

It brings back the economics of themarket. Raise prices and demand goesdown – or does it?

Large Green,Lentils: Strongdemand for allgrades continueswith the marketlikely to remainfirm throughspring seedingand into the

summer months. Carryover stocks willbe low so we can expect strong exportsin Sept-Oct 2008. New crop acreageshould be similar to the 2007 crop orperhaps an increase of 10 -15 per cent.

Small Green: Recently, demand hasweakened as most buyers took coveragein Nov and Dec for Jan-Feb consumptionin their local markets. The 2007 crop ismainly No.1 so buyers of No.2 andlower grades have had to cover withhigher quality. Ending stocks will besignificant, but this will not necessarilypull the market lower as we can expecta slightly lower acreage of small greentypes in 2008. We expect good demandthrough the late spring and into thesummer months, due to buyers’reluctance to absorb all of the risk ofpotentially higher prices for the newcrop when both inland and oceanfreight rates may increase—again!

Medium Green: Demand is steady,but stocks are minimal. We can expectthis trend of reduced plantings due toprice considerations. We anticipateminimal ending stocks and a lowerproduction in 2008.

Market Outlook: Prices for all typesof lentils will unlikely fall from currentlevels. The Canadian dollar has had asignificant impact this year on ourexport [USD-CIF (Cargo InsuranceFreight)] values, but this has not beenreflected at the producer price levelswhere prices have been tending highersince harvest. We have seen exportersabsorb most of the currency losses, notthe producer, and this is likely to continue.

We suggest producers consider all ofthe crops they hold in their bins whenmaking their marketing decisions in thecoming months. For example, greenlentils do not necessarily hold their coloras well as red or dark speckled lentils.Canaryseed, flaxseed and yellow peascan be held for much longer periods instorage without impacting quality.

New crop: We estimate green lentilplantings will increase by 10-15 percent in 2008. In our view, this is notsignificant and should not impactheavily on supply nor price. The mainpoints are: carryover of green lentils willnot be large; old and new crop pricesare firm and Canada is the world’slargest producer. In other words, weshould be a price-setter, not a pricetaker in green lentils.

Tyler Thorpe has been trading pulsesfor 25 years and is the founder andPresident of Agricom International Inc.based in Vancouver, B.C.(http://www.agricom.com/)

Saskatchewan Pulse Growers / Green Lentil Market Report

Bears&BullsOPINION

Heidi Dutton-WeberWestern Grain Trade Ltd.

Tyler ThorpeAgricom International Inc.

February 2008 2

On the MarketBRIAN CLANCEY

Saskatchewan Pulse Growers / Green Lentil Market Report

Limited productionof Extra 3 and No.3 grade lentils inSaskatchewan lastyear has changedthe grades someimporters arefocusing on.

Importers in Chile, for instance, like tobuy natural Extra 3 Laird lentils. They donot consider those that are cleaned outof No. 1 and No. 2 grade product asbeing natural and prefer not to buy them.As a result, they expect to focus on No.2 grade lentils when they re-entermarkets. By contrast, buyers in Colombiaand Venezuela will likely try to buy anyremaining Extra 3 grade lentils, beforemoving up to No. 2 grade product.

Many Latin American importers initiallyresisted last fall's steady increases inexport asking prices. Knowing theproblems they were having getting theirown farmers to grow dry edible beansand other pulses instead of corn andsoybeans, they realized fighting marketswas foolish and covered most of theirneeds through the end of April. Thissuggests we will begin to see fresh buyingin February and March and reflectsSouth America's recent import pattern.Looking at average monthly exports forthe previous three years, Canadian

shipments to all South Americandestinations bulged in November andDecember, again in March and April,and lastly in June and July. In fact, halfof the lentils normally shipped to SouthAmerica each season move during thelast five months of the marketing year:between February and July.

This season started with a hiccup.Colombia took almost 12,000 tons inAugust and over 9,700 in September.Other buyers in the region seem to besticking to their normal patterns, makingit clear there will be good demand foroff-grade product in the last half ofFebruary and into March. Moreimportantly, recent increases in regionaldry edible bean and chickpea priceshave made lentils relatively cheap inthe eyes of Latin American packagers.This will encourage demand, but stocksare tightening quickly in Western Canada,which suggests it will get harder tocover needs as we go through springinto the summer shipping period.

Technical analysis used in futures or stockmarkets can be applied to specialtycrops. Looking at prices for No. 2 greenlentils between December 14 andJanuary 14, it is possible to calculatecurrent resistance and support levels.When we talk about resistance andsupport levels we are not talking aboutprices at which markets would be stopped

from rising or falling, they are pricepoints which help us judge whether theunderlying market is bullish or bearish. Itis a good sign if prices break through thefirst resistance level and keep headingup, it is not good when they fall throughtheir support levels, unless you are shortagainst a fixed price contract and needto buy lentils to cover the shortfall.

No. 2 Grade Large Green Lentil Monthly Price Summary (cdn cent/lb)

Large Medium Small French Red

Jan 14 Close 25.50 23.50 19.75 18.00 24.50

Monthly High 25.50 23.75 20.00 18.00 24.50

Monthly Low 22.00 18.00 17.00 17.10 18.00

Resistance 1 26.67 25.50 20.83 18.30 26.67

Resistance 2 27.83 27.50 21.92 18.60 28.83

Support 1 23.17 19.75 17.83 17.40 20.17

Support 2 20.83 16.00 15.92 16.80 15.83

Marketing Your Grade

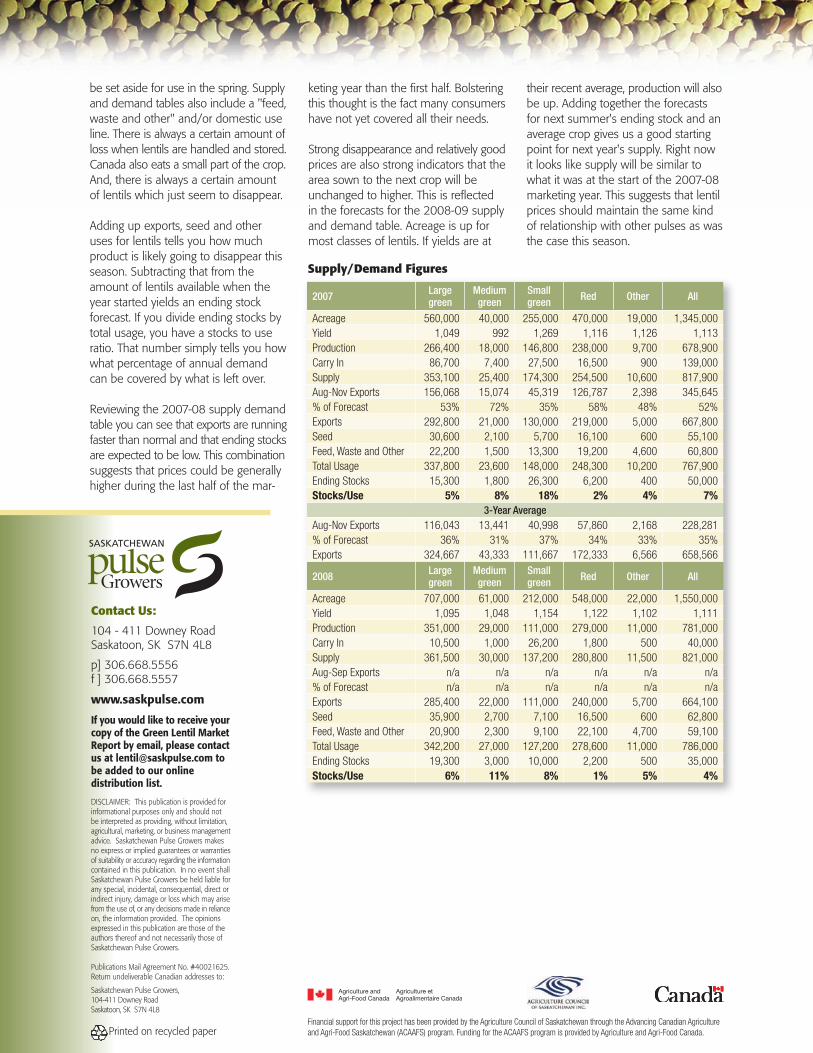

Feb 2008 Supply/Demand Explained

Supply-demand tables combine hardinformation with predictions about whatmight happen in the future. This is whydifferent sources can have different ideasabout ending stocks and predictionsabout seeded area and exports.

Right now, we know how many lentilswere planted and harvested in 2007.We also know how many lentils wereexported through the end of November.Lentils are being exported at a fasterpace than normal this season. Thisbecomes clear when looking at exportsas a percentage forecast for the marketingyear. By end of November, we hadexported 52 per cent of all the lentilswe expect to in 2007-08. Normally, weship 35 per cent.

This suggests exports might be higherthan people think. But, you can onlyship as much product as you have.That includes the lentils which weregrown and any lentils carried over fromthe previous marketing year. Thosenumbers form the supply part of thesupply and demand table.Since exports are going at a fast paceand since prices have been pretty goodall season, there is a good chance lentilarea will stay the same or rise this spring.That defines how much seed needs to

February 2008 3

Contact Us:

104 - 411 Downey RoadSaskatoon, SK S7N 4L8

p] 306.668.5556f ] 306.668.5557

www.saskpulse.com

If you would like to receive yourcopy of the Green Lentil MarketReport by email, please contactus at [email protected] tobe added to our onlinedistribution list.

DISCLAIMER: This publication is provided forinformational purposes only and should notbe interpreted as providing, without limitation,agricultural, marketing, or business managementadvice. Saskatchewan Pulse Growers makesno express or implied guarantees or warrantiesof suitability or accuracy regarding the informationcontained in this publication. In no event shallSaskatchewan Pulse Growers be held liable forany special, incidental, consequential, direct orindirect injury, damage or loss which may arisefrom the use of, or any decisions made in relianceon, the information provided. The opinionsexpressed in this publication are those of theauthors thereof and not necessarily those ofSaskatchewan Pulse Growers.

Publications Mail Agreement No. #40021625.Return undeliverable Canadian addresses to:

Saskatchewan Pulse Growers,104-411 Downey RoadSaskatoon, SK S7N 4L8

Printed on recycled paper

be set aside for use in the spring. Supplyand demand tables also include a "feed,waste and other" and/or domestic useline. There is always a certain amount ofloss when lentils are handled and stored.Canada also eats a small part of the crop.And, there is always a certain amountof lentils which just seem to disappear.

Adding up exports, seed and otheruses for lentils tells you how muchproduct is likely going to disappear thisseason. Subtracting that from theamount of lentils available when theyear started yields an ending stockforecast. If you divide ending stocks bytotal usage, you have a stocks to useratio. That number simply tells you howwhat percentage of annual demandcan be covered by what is left over.

Reviewing the 2007-08 supply demandtable you can see that exports are runningfaster than normal and that ending stocksare expected to be low. This combinationsuggests that prices could be generallyhigher during the last half of the mar-

keting year than the first half. Bolsteringthis thought is the fact many consumershave not yet covered all their needs.

Strong disappearance and relatively goodprices are also strong indicators that thearea sown to the next crop will beunchanged to higher. This is reflectedin the forecasts for the 2008-09 supplyand demand table. Acreage is up formost classes of lentils. If yields are at

their recent average, production will alsobe up. Adding together the forecastsfor next summer's ending stock and anaverage crop gives us a good startingpoint for next year's supply. Right nowit looks like supply will be similar towhat it was at the start of the 2007-08marketing year. This suggests that lentilprices should maintain the same kindof relationship with other pulses as wasthe case this season.

Financial support for this project has been provided by the Agriculture Council of Saskatchewan through the Advancing Canadian Agricultureand Agri-Food Saskatchewan (ACAAFS) program. Funding for the ACAAFS program is provided by Agriculture and Agri-Food Canada.