Reforms and difficulties in fiscal relations in a context of multilevel governance reforms Federal Public Service Finance – Belgium OECD Network on Fiscal Relations Across Levels of Government Paris, 23-24 November 2017

Transcript

Reforms and difficulties in fiscal relations in a context of multilevel governance reforms

Federal Public Service Finance – Belgium

OECD Network on Fiscal Relations Across Levels of Government

Paris, 23-24 November 2017

Structure of the presentation

Background information: institutional context

Personal income tax after the sixth State Reform (reform of the Special Finance Act) : impact on fiscal relations of the increased tax autonomy for SNG’s

Evolution in tax collection

Challenges ahead in fiscal relations

Impact on the High Council of Finance of the increased multilevel governance context

Background information: institutional context

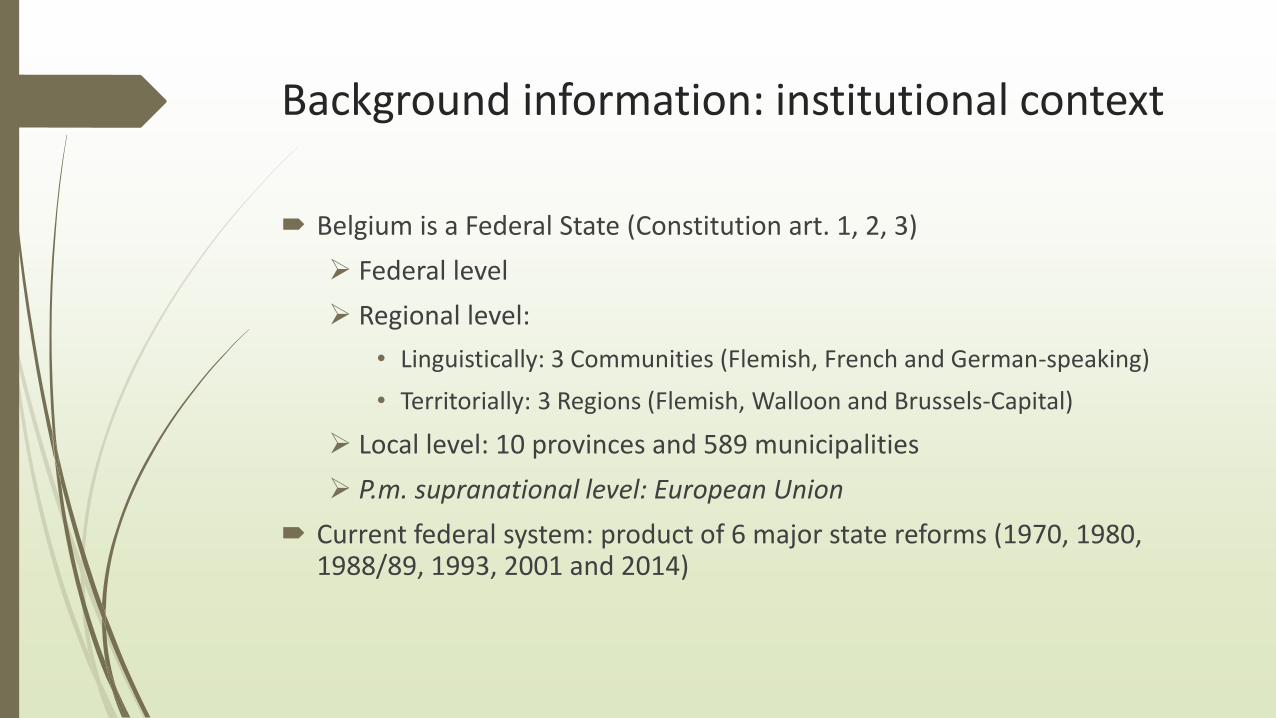

Belgium is a Federal State (Constitution art. 1, 2, 3)

Federal level

Regional level:

• Linguistically: 3 Communities (Flemish, French and German-speaking)

• Territorially: 3 Regions (Flemish, Walloon and Brussels-Capital)

Local level: 10 provinces and 589 municipalities

P.m. supranational level: European Union

Current federal system: product of 6 major state reforms (1970, 1980, 1988/89, 1993, 2001 and 2014)

PIT after the Sixth State Reform (July 2014, applicable as of assessment year 2015 for tax component of the reform of Special Finance Act*)

Complex fiscal relations in PIT due to recent reforms

Since the Sixth State Reform : federal PIT & regional PIT (extended tax autonomy)

No prejudice to the local additional surtaxes on PIT

But…

PIT tax collector / tax servicing remains exclusive competence of federal authority

(*) Special Finance Act of 16 January 1989, as modified by the Special Act of 6 January 2014 reforming the financing of Communities and Regions, increasing tax autonomy for the Regions and financing the new competences

PIT after the Sixth State Reform

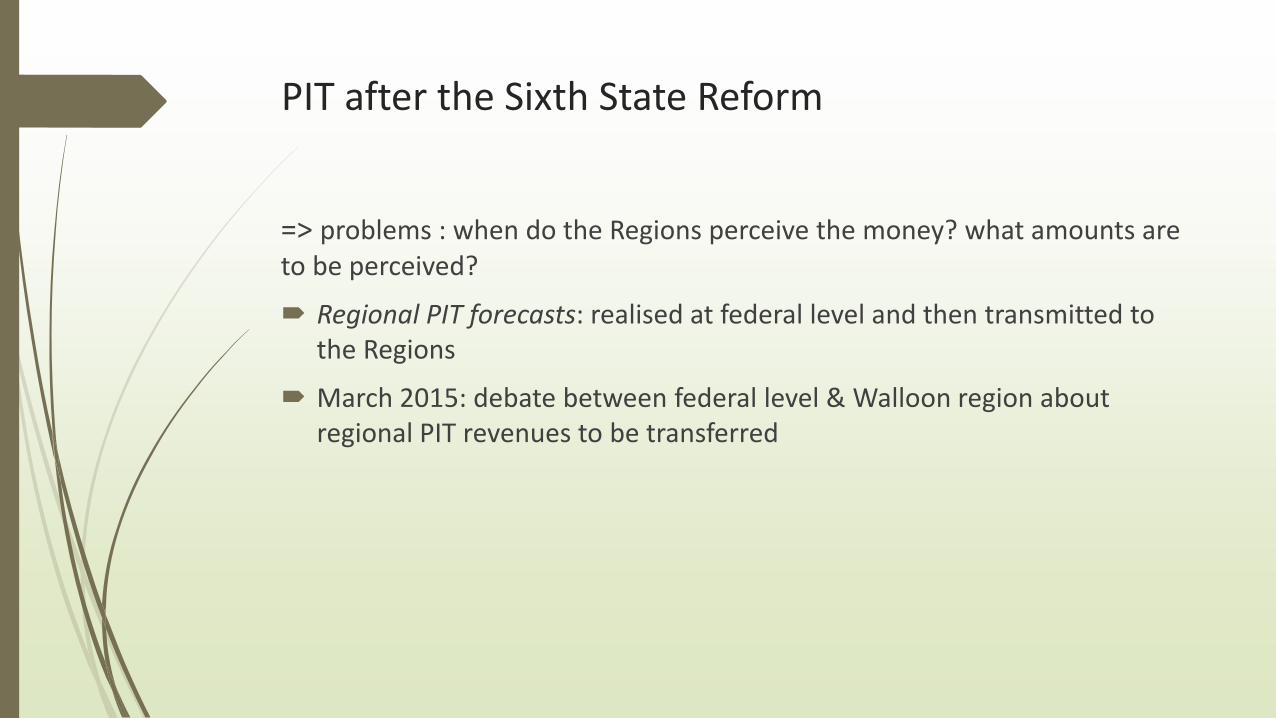

=> problems : when do the Regions perceive the money? what amounts are to be perceived?

Regional PIT forecasts: realised at federal level and then transmitted to the Regions

March 2015: debate between federal level & Walloon region about regional PIT revenues to be transferred

PIT after the Sixth State Reform

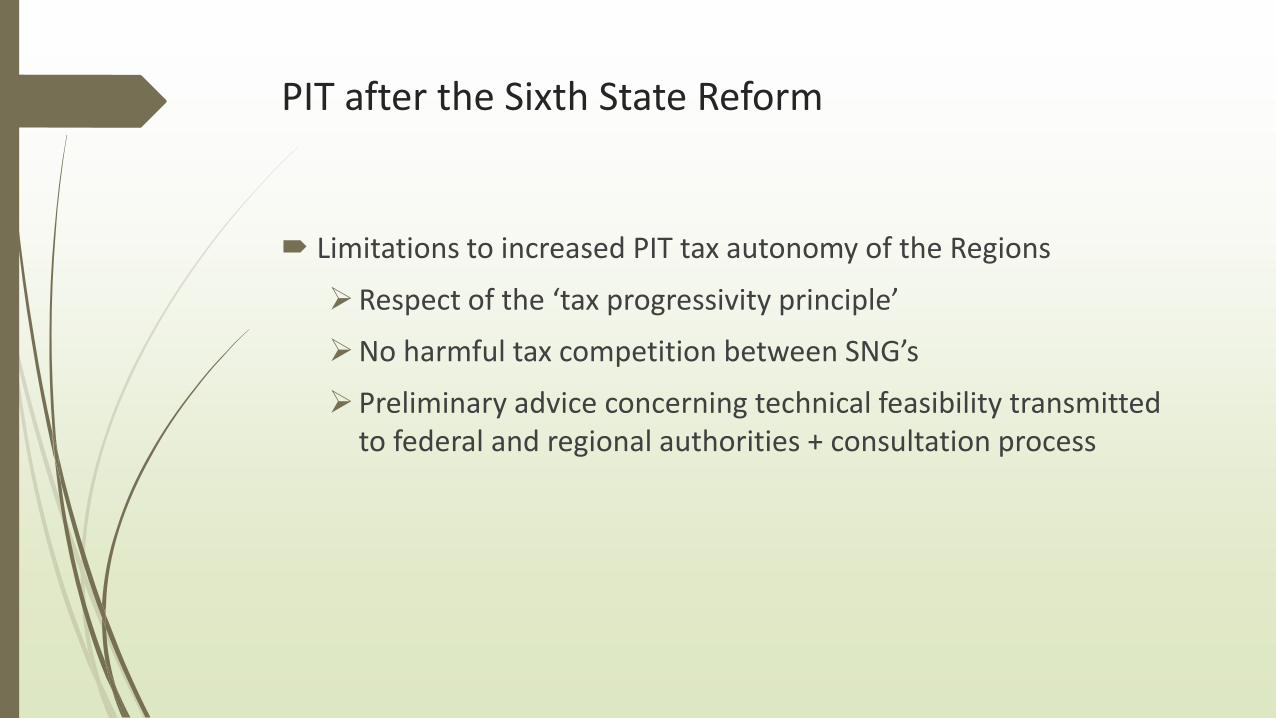

Limitations to increased PIT tax autonomy of the Regions

Respect of the ‘tax progressivity principle’

No harmful tax competition between SNG’s

Preliminary advice concerning technical feasibility transmitted to federal and regional authorities + consultation process

Regional taxes : reforms at tax collection level

Historically: collected at federal level --> evolution: by regional tax administrations

Sometimes postponed: due to necessary transfer of civil servants

Transfer has to be carried out per group of regional taxes (4 groups defined)

Timing of transition differs strongly from one SNG to another => asymmetric arrangements

Region can choose whether to take over the federal staff (then: dotation), or not (no dotation in this case)

Example 1 : the property tax(withholding tax on immovable property)

Tax collection

Historically: collected at federal level for the three Regions

Flemish Region responsible for tax collection since 1999

Further transfers:

Brussels-Capital Region intends to collect the tax as from 2018

Walloon Region : by 2020 or 2021?

Regions may not change the federal taxable basis (i.e. the cadastral income) but are free to choose another taxable basis (not – yet? -applicable)

Example 2 : taxes assimilated to income taxes –recent changes in tax collection

Group of regional taxes Beneficiary of tax revenues Tax collector

Circulation tax& tax of entry into service(vehicle taxation)

Regional and local authorities Federal level (Ministry of Finance) for Brussels-Capital RegionFlemish Region since 2011Walloon Region since 2014 (but problems during transfer)

Betting and gambling taxes& Gaming machine licence duty

Regional authorities Federal level for FlemishRegion and Brussels-Capital RegionWalloon Region since 2010Flemish Region as of 2019 (?)

Fiscal relations in a changing environment (tax servicing to SNGs, SNGs enhanced tax autonomy) – Challenges Increased SNGs tax autonomy:

To close information gaps occurring with decentralisation mainly between federal and state level

Tax servicing transferred from federal to state level (Regions)- how to smooth the transition? Best practices?

Transfer of federal civil servants to the SNG’s administrations : always first on voluntary basis

Not underestimate sufficient human resources to be transferred

Taking into account past experiences (vehicle taxation, 2014, Walloon Region)

Preparation of transfer is crucial (in theory 2 years in advance / actually about 1 year in advance)

High Council of Finance (HCF) – Section ‘Public Sector Borrowing Requirements’ (PB Section)

HCF established in 1937 as an advisory council for the Ministry of Finance

Several reforms over the years

1989 reform: against the background of a transition to a federal state

Creation of a Section ‘Public Sector Borrowing Requirements’

Specific competences for fiscal coordination between federal government and regions and communities

Since 2014: role of fiscal council with extended tasks

Cooperation Agreement of 13 December 2013 between the Federal Government, the Communities, the Regions and the Community committees

High Council of Finance – PB Section

Extension of the tasks

Determination of yearly budgetary targets for general government and by government sub-entity → needs to be approved by the intergovernment Concertation Committee

Fiscal surveillance

Problem:

No agreement reached in Concertation Committee

Regions and Communities only ‘take note’ of Stability Programme submitted by federal government

So far HCF-PB Section has not been able to perform its monitoring task

Evolution of secretariat of the HCF-PB Section in a context of multilevel governance

Extension to delegates of the SNG’s : in process

Strengthening of multilevel coordination in the management of budgetary policy and borrowing requirements