43

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV © COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV Benchmarking KPIs for Financial Success

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Benchmarking KPIs forFinancial Success

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Speakers

Keith Rushing

Director, Applied Research

Institute of Child Nutrition

Olga Botero

Executive Director

Department of Food & Nutrition

Miami-Dade County Public Schools

Sandy Curwood

Director, Office of SNPs

Virginia DOE

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Keith Rushing⎻ Institute of Child Nutrition

⎻ No Financial Disclosure

• Olga Botero⎻ Miami-Dade Count Public Schools

⎻ No Financial Disclosure

• Sandy Curwood⎻ Virginia Department of Education

⎻ No Financial Disclosure

Affiliation or Financial Disclosure

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Completed in 2017

• Assistance of 25 SN Professionals

• Straight-forward

• Easy-to-use reference

• Applying KPIs

Essential KPIs for SN Success

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

WHAT ARE KPIs?

• Measures of performance

• Rigorous / Numbers-oriented / Objective

• Provide standards

• Identify where to invest resources

• Track major initiatives

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

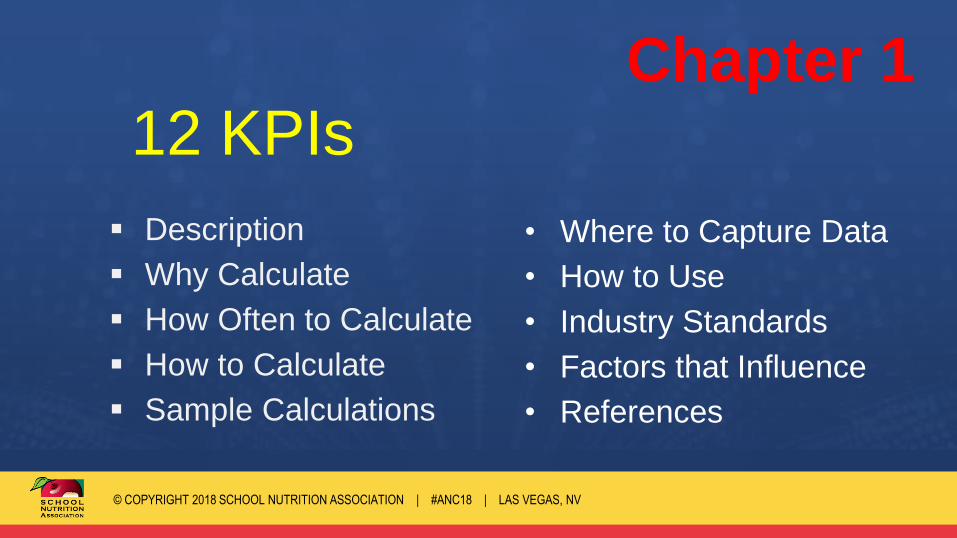

Chapter 1

12 KPIs

▪ Description

▪ Why Calculate

▪ How Often to Calculate

▪ How to Calculate

▪ Sample Calculations

• Where to Capture Data

• How to Use

• Industry Standards

• Factors that Influence

• References

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Chapter 2

Case Study

• Cover all KPIs

• Shared background

How to Utilize KPIs

• Benchmarking

• Trend Analysis

• Action Plans

• Communicating KPIs

Chapter 3

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

•comparing performance with an established standard

• Internal

• Industry

Benchmarking

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Determine which KPIs to benchmark

• Collect, calculate and analyze KPI data over time

• Compare results to the benchmark

• Take actions

Benchmarking Steps

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

•comparing results over time

Trend Analysis

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Communicating KPI Data

with Key Stakeholdersto

Facilitate Change

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

3.2

3.21

3.22

3.23

3.24

3.25

3.26

3.27

3.28

3.29

3.3

August September October November December January February March April

District Total Revenue

Per MEQ

Compared to

Federal Lunch Reimbursement

Rate

What might this suggest?

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

District Total Revenue

Per MEQ

Compared to

District Total Cost per MEQ

What might this suggest?

3.12

3.14

3.16

3.18

3.2

3.22

3.24

3.26

August September October November December January February March April

Chart Title

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Sandy Curwood, PhD, RDN

Director, Office of SNP

Virginia Dept. of Education

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Break-Even Point (BEP) Analysis:

Case Study

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• School Nutrition Programs (SNPs) are expected to be

self-sustaining

• SNPs evaluate expenditures and revenues impact on their operation

• To accomplish this, need to calculate their

break-even point

BEP Purpose

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Point at which expenditures and revenues are equal

• Amount of revenue (sales or income) needed to cover

fixed and variable costs

⎻ Contribution margin: Percent of revenue that can be

attributed to cover fixed costs

BEP Definition

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Break-Even Point (BEP)

BEP =Fixed Costs

Contribution Margin

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

•Analysis shows your revenue is higher than your BEP⎻ SN program has adequate revenue to cover expenditures

⎻ Opportunity to explore new initiatives

⎻ Analysis shows your revenue is lower than your BEP

⎻ SN program expenditures exceed the revenue and the program is not self-sustaining

⎻ Where should you focus?

Applying Break-Even Point to Your Program

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Lynchburg City Schools has 20 schools, 8,546 students, 68% eligible to receive free and reduced-price meals.

This is their data for the 2016-2017 SY:

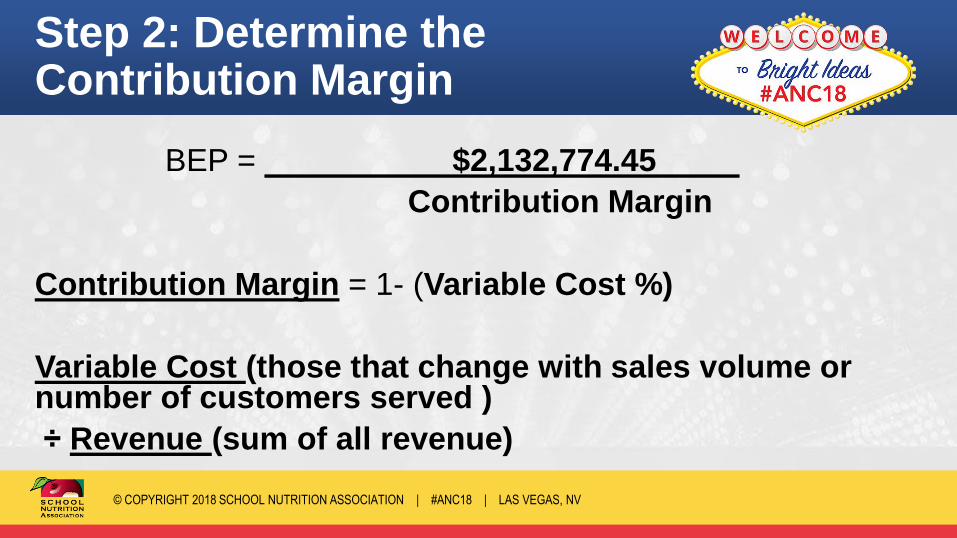

•Fixed costs: $2,132,774.45 ⎻ Includes: Personal services, employee benefits, utilities, etc.

•Variable Costs: $2,334,873.14⎻ Includes: Food and Supplies

•Revenue: $4,759,939.18⎻ Includes: School meals purchased (paid meals), state and federal reimbursement,

catering, and ala carte

➢Is the school nutrition program covering its costs?

Case Study

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Let’s Look at an Example in Practice

➢Is the school nutrition program covering its costs?

YES!

Let’s see how we got this answer.

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Step 1: Determine the Fixed Costs

BEP =

Fixed Costs: Sum of all expenditures that do not vary with sales volume or number of customers served

➢In the example, fixed costs, those that generally don’t vary: salary and benefits, utilities, etc.

Fixed costs in the example = $2,132,774.45

Fixed CostsContribution Margin

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

BEP = $2,132,774.45

Contribution Margin

Contribution Margin = 1- (Variable Cost %)

Variable Cost (those that change with sales volume or number of customers served )

÷ Revenue (sum of all revenue)

Step 2: Determine the Contribution Margin

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Step 3: Determine the Variable Cost %

From the example:

Variable Cost % = Variable cost $2,334,873.14 ÷Revenue $4,759,939.18

Variable Cost % = 49.05% = .4905

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Step 4: Calculate BEP

Fixed Costs

Contribution Margin (1- (Variable Cost %)BEP =

$2,132,774.451- 0.49050 = 0.5095

50.95% of the revenue from the SN program is needed to cover the program’s fixed costs.

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Step 5: Determine theBreak-Even Point

BEP = $4,186,014.62

$2,132,774.45 =0.5095

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Revenue = $4,759,939.18

Break-even point= $4,186,014.62

Revenue > BEP Flexibility in budget for new initiatives!

Step 5: Comparison of Revenue and Break-Even Point

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

•Monthly analysis⎻ Set annual goals for your program

⎻ Benchmark- Is your program on track?

•Annual analysis⎻ How sufficient was your program throughout the school-year and

year-to-year?

•Next Steps⎻ What adjustments will you make to your program?

Using Break-Even Point In Your Program

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Olga Botero, RD

Executive Director

Department of Food and Nutrition

Miami-Dade County Public Schools

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

2016/17 2017/18

Enrollment 294,881 289,085

Free/Reduced 228,431 230,731

Employees 3,264 3,530

Annual Budget $198,240,000 $203,250,000

Schools/Sites 356 358

Demographics

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

2016/17 2017/18

79,700 76,750

179,200 171,500

28,750 29,000

Breakfast

Lunch

After school

Average Daily Participation

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Goals

Increase Meal

Participation

Cutting Costs Promote lean

and green

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Create your Brand

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Employees must understand the importance of serving one

more breakfast, one more lunch, one more after school

meal.

• How does serving that additional meals impacts their life

• And then……..of course it is not only about serving, BUT

• Recording it so that it gets into the CLAIM

“Every Meal Counts”

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Who is Miami-Dade County Public SchoolsDepartment of Food and Nutrition?

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Cost per Meal Equivalent

(MEQ)

Total Costs ÷ MEQ = Costs/MEQ

• Revenue per Meal

Equivalent (MEQ)

Total Revenue ÷ MEQ = Revenue/MEQ

Benchmarking – know your numbers

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

Revenue/MEQ - Cost/MEQ = KPI

Goal – Cost/MEQ should be lower than Revenue/MEQ

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

0.0000

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

3.5000

4.0000

4.5000

5.0000

November December January February March April

Revenue Per Meal Equivalent

2016-2017 2017-2018

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

0.0000

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

3.5000

4.0000

4.5000

5.0000

November December January February March April

Expenses Per Meal Equivalent

2016-2017 2017-2018

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

-1.0000

-0.8000

-0.6000

-0.4000

-0.2000

0.0000

0.2000

0.4000

0.6000

0.8000

1.0000

November December January February March April

Difference Between Revenue Per Meal Equivalent and Cost Per Meal Equivalent

2016-2017 2017-2018

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• Know your numbers

• Stay in touch with your employees

• Food and Nutrition team player in the school

• Students – the REASON for school meals

Summarizing

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

It does not matter if you are a large District or a small

one, deal with daily issues as if you were a very small

District and maintain personal attention with cafeteria,

school or other department’s staff. Always remember

that you cannot reach your GOALS unless the entire

team is working toward it.

Reflection

© COPYRIGHT 2018 SCHOOL NUTRITION ASSOCIATION | #ANC18 | LAS VEGAS, NV

• This session provides one (1) CEU

⎻ Key Area: Administration-3000

⎻ Key Topic: Benchmarking KPIs

Professional Standards Code

EARN

CONTINUING

EDUCATION

CREDITS