Hypothesis 1 / 1 Best Value Review of ICT Hypothesis 1 Report Summary sheet Hypothesis To test whether total outsourcing of our ICT function, selective outsourcing of various elements / processes, or total insourcing of ICT provides the best way forward for HCC in terms of efficiency / effectiveness / meeting the needs of services and delivering the corporate agenda. Summary of recommendations To pursue outsourcing of ICT services within service areas identified within this report using a “best of breed” approach rather than employing a total outsourcing model. To target identified improvements over current arrangements when re-tendering those services and look to move towards output based service contracts. To establish a single help desk for ICT services that addresses the failings identified by this best value review which is either located in-house or with a separate contractor to other ICT contracts dependent on further analysis of costs / benefits of each option. (See linked hypothesis on support issues.) Service Benefits Establishment of contracts that better meet the needs of current HCC services and staff. To address the contract failings identified from best value review benchmark exercise. Estimated future costs / efficiencies This is dependent of future negotiations with contractors. Benchmarking has shown that we are not currently paying over the odds for our services but that there are areas such as client management where we could better utilise resource. 25-50% could theoretically be realised from project based work through including this in up-front negotiations (currently running at circa £570k). Possible efficiencies from amalgamating and reducing total number of staff involved in help desk operations. Currently around 10FTEs across ITNet and services. This number could be reduced by professional, centralised help desk services.

Transcript

Hypothesis 1 / 1

Best Value Review of ICT

Hypothesis 1 Report

Summary sheet

Hypothesis

To test whether total outsourcing of our ICT function, selective outsourcing of variouselements / processes, or total insourcing of ICT provides the best way forward for HCCin terms of efficiency / effectiveness / meeting the needs of services and delivering thecorporate agenda.

Summary of recommendations

q To pursue outsourcing of ICT services within service areas identified within thisreport using a “best of breed” approach rather than employing a total outsourcingmodel.

q To target identified improvements over current arrangements when re-tenderingthose services and look to move towards output based service contracts.

q To establish a single help desk for ICT services that addresses the failings identifiedby this best value review which is either located in-house or with a separatecontractor to other ICT contracts dependent on further analysis of costs / benefits ofeach option. (See linked hypothesis on support issues.)

Service Benefits Establishment of contracts that better meetthe needs of current HCC services and staff.To address the contract failings identifiedfrom best value review benchmark exercise.

Estimated future costs / efficiencies This is dependent of future negotiations withcontractors. Benchmarking has shown thatwe are not currently paying over the odds forour services but that there are areas such asclient management where we could betterutilise resource.

25-50% could theoretically be realised fromproject based work through including this inup-front negotiations (currently running atcirca £570k).

Possible efficiencies from amalgamating andreducing total number of staff involved inhelp desk operations. Currently around10FTEs across ITNet and services. Thisnumber could be reduced by professional,centralised help desk services.

Hypothesis 1 / 2

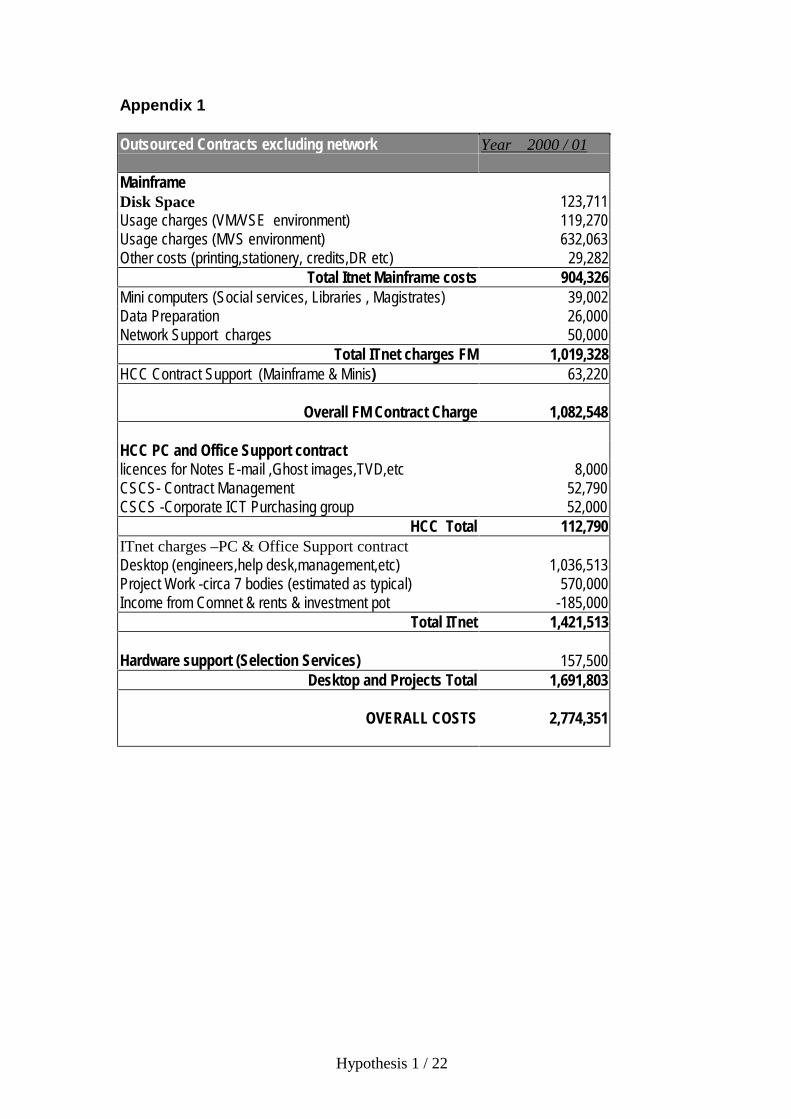

Current costs Please see attached appendix 1.

Risksq Contract failure – failure of third party to

deliver service.q Inflexible approach by contractors to fast

moving area.q Fail to get mix of contractors that are

signed up to best of breed approach.q Underestimate contract management task

– fail to get best people on this.

Volumes See attached figure 1.

Ease of Implementation These changes require a major project to retender services and deliver improvedcontracts and client management practices.This should be undertaken by a team thatincludes representatives from legal, contractand ICT services as well as businessrepresentatives to quality assure theprogramme.

Further information / work required See above under ease of implementation. Inorder to tender contracts from April 2001team needs to commence work uponcompletion / acceptance of Best Value report.Unlikely to be achieved prior to June 2001.

Report Author…Stuart Campbell

Hypothesis 1 / 3

Report Summary of Hypothesis The purpose of this hypothesis is to test whether total outsourcing of our ICT function,selective outsourcing of various elements / processes, or total insourcing of ICTprovides the best way forward for HCC in terms of efficiency / effectiveness / meetingthe needs of services and delivering the corporate agenda.

Approach Taken The approach taken to test this hypothesis was as follows: -

q Outline current costs / extent of outsourcing at HCC.

q Understand what the market place is doing – where are other organisationsusing outsourcing, what are the issues encountered? Are there any areasthat organisations are avoiding when outsourcing and why? What are therange of outsourcing delivery mechanisms open to any organisation?

q Examine the total outsourcing option. What are the benefits / costs / risksassociated with such a move? Who else is doing it? How developed is themarketplace?

q Examine various scenarios based on selective outsourcing of elements ofour ICT service / selective use of the range of delivery mechanisms. Whatare the benefits / costs / risks associated with each? What does themarketplace have to offer?

q Total insourcing. Again, what are the benefits / costs / risks associated withinsourcing operations that are currently externalised? What advantages /disadvantages would such an approach would present?

In order to address each of the areas outlined above the following sources were used: -

1) Experience of HCC staff and statistics gathered in relation to currentexperience / contracts.

2) Hedra Best Value Review report July 2000.3) Interviews with provider companies – Hyder, Capita, ITNet. (We also

sought an audience with EDS but to date have been unsuccessful in settingup that exchange.)

4) Interviews with other authorities – Kent, Surrey, Warwickshire, Newcastle.5) Various articles / books covering this field (e.g. Outsourcing Information

Technology, Systems and Services – Robert Klepper, Wendell O Jones -1998) references to source material are included in the text.

Hypothesis 1 / 4

Extent of IT outsourcing at HCC / associated costs

There are two main ICT based contracts in use at HCC both currently with ITNet.These are as follows: -

1) Facilities Management (FM) – Covers running of mainframe service fromBirmingham and several mini computers at an operational level. Management of theapplications running on these boxes still largely resides with HCC. This contractcurrently costs circa £900k Per annum. With removal of applications from themainframe over the next three years there should be no further use for this contractonce it reaches the end of the current contract period in 2003.

2) PC Desktop support contract – Currently running at £1m per annum. Thiscontract provides engineers to fix and advise on desktop computing issues / software.In addition to the £1m contracted for we also undertake around £570k worth of projectbased business with external suppliers that could possibly be provided at better rates ifwe negotiated it into any future contract up-front.

(For detailed breakdown of these contract costs please see Appendix 1.)

Potential Changes /Proposals

In summary the changes proposed are as follows: -

q Tender of desktop support contract in spring / summer 2001. Thespecification of this tender to be targeted at addressing concerns raised bythis review as detailed in Hedra findings and exclude help desk element.

q New contract to be based on definition of outputs and managed /monitored / rewarded accordingly.

q Help Desk to be tendered in separate contract to manage multiple supplierscenario and provide management information for those contracts. Thesuccessful contractor to act as “management contractor” to other contracts.

q Rationalisation of help desk and support areas to look to free up resourcecurrently tied up in duplication of activity and client management of theexisting contracts.

q HCC to move away from in-house development activity over next threeyears by project based introduction of new systems with partner suppliers –e.g. Children Schools and Families system. This model to also be adoptedfor other major projects such as financial systems replacement.

q Corresponding development of IS management role in departments (seeseparate hypothesis).

Hypothesis 1 / 5

q Examine possibility of introducing partnership contract with independentadvisor who does not have an interest in implementation / business ofdelivery contracts. Use such a contract to benchmark / advise on futuredirection and performance of delivery contractors. Need to agree approach/ relationship with delivery contractors before appointing.

Service Benefits The service benefits realised from the above should be as follows: -

q Establishment of contracts that better meet the needs of the servicemanagers and ultimately the service clients. Addressing failings of currentcontracts.

q Release of resource from current duplication and client management of thefunction to better concentrate HCC activity on exploitation of technologyand investment in future service improvements.

q Improved flexibility of future arrangements and development of problem“ownership” role with help desk to ensure all client issues are managed tosuccessful conclusion.

Current Costs Current costs of ITNet contracts are outlined in Appendix 1. Figure 1 also outlineswhere current costs fall across all functional areas whether in-house or externalised.

Estimated Future Efficiencies

As outlined in the summary page this is dependent on future negotiations withcontractors. Benchmarking has shown that we are not currently paying over the oddsfor ITnet services but that there are areas such as client management where we couldbetter utilise resource. Any efficiencies realised here need to be balanced againstpotential additional costs to meet failings of current contracts and the need to developIMS skills in departments (see sections below).

q 25-50% could theoretically be realised from project based work to address qualityissues raised through including this in up-front negotiations (currently running atcirca £570k). Rather than paying this on an as required basis at market rates.

q Possible efficiencies from amalgamating and reducing total number of staffinvolved in help desk operations. Currently around 10FTEs across ITNet andservices. This number could be reduced by professional, centralised helpdeskservices.

Hypothesis 1 / 6

q Need to address levels of client management of contracts. By rationalising thisarea and managing centrally under infrastructure resource could be freed up at ICTmanagement level.

Implementation Issues The project to implement new contracts would take significant resource in order tospecify and negotiate through successfully. However, this level of resource would berequired whatever approach is taken regarding the way forward. It is likely that aninsourcing operation would be significantly more costly in terms of set-up costs giventhat it would require both successful negotiation of end of contract and hand over to /development of in-house team. We have suggested that in order to specify and negotiate proposed contracts tosuccessful conclusion we would need an implementation team approach as follows: -

q Contracts Officer 3-4 days input.

q Small team of senior officers to specify and negotiate the contract over saya three month period. Estimate around 25 days input each. Important toget best people assigned to this role.

q Evaluation team of around 5 persons over say 5 day period. Any change of contract would take careful negotiation with current suppliers for handover and continuity of service during implementation phase.

Potential Risks q Contract failure – failure of third party to deliver service as intended. Penalties

might be realised but delivery of contract is target rather than recovery of losses.q Inflexible approach by contractors to fast moving area. Inability to find

appropriate mechanisms to drive contractor interest/investment in this area.q Fail to get mix of contractors that are signed up to best of breed approach.

Appointed contractors do not work well together.q Underestimate contract management task – fail to get best people in this role /

negotiation of contractq Failure to realise efficiencies. Make changes but fail to reassign resources

appropriately. Need to assign accountability to this roleq Stability of supplier companies. Supplier direction changing in fast moving

market.

Volume Information Used See appendix 1 and figure 1 for both costs and staff numbers involved

Hypothesis 1 / 7

Extra skills / training required q Development of IS role in departments. Refocusing of current resources / skills. q Help Desk expertise in introducing separate contract or managing in-house if

appropriate contract cannot be established.

IT Development/Investment

q Main investment will be in officer time to negotiate and implement newcontracts. Based on the above estimates this would cost approximately£25k – see appendix B for breakdown of assumptions / calculation.

q Although potential efficiencies have been identified within this hypothesisthere is also the need to look to improve services to address failings ofcurrent arrangements. Potential additional cost of such arrangements willnot be known until we commence detailed negotiation with suppliers.

Further Information / Work Required

q Establishment of project team and implementation as outlined above.

q Further investigation of possible contract improvements / methods ofdelivery in the telecommunications arena. Should be aiming to realiseefficiencies in this field as delivery mechanisms / services become cheaperover the next 5 years. Should also be planning to meet increasing demandsof network traffic as more services are provided by electronic means.

q Further analysis of areas not addressed in detail in this report. We ofnecessity concentrated work on those services identified as issues for us bythe benchmarking exercise and on contract areas that are about to expire.

Recommendations These can be summarised as follows: -

q Do not favour total outsourcing model based on assessment of currentmarket and Hertfordshire’s stage of development in relation to others whoare adopting this model. High risk, low flexibility option. If HCC shouldchoose to investigate further then this needs to be undertaken on a widerbasis than just ICT in order to realise full benefits and as such is outsidethe scope of this review.

q Reject insourcing of activity in areas that are best delivered by ICTsuppliers. HCC would struggle to develop /recruit the appropriate skills

Hypothesis 1 / 8

and we could risk taking our eye off the strategic ball.

q Move forward with best of breed approach to outsourcing / insourcingbased on the potential changes / proposals section above. See also figure 2in the attached report for discussion on each functional area and it’srelationship to future contracts.

Hypothesis 1 / 9

The marketplace An analysis of what other organisations are doing provides us with an indication ofthe areas in which outsourcing is more developed and of where it is perceived to offerless risk / greatest benefits. One of the latest studies (Mary C. Lacity & Leslie P.Willcocks – Inside Information Technology Outsourcing: A State-of-the-Art ReportTempleton Research - January 2000.) indicates that: - “The least commonly outsourced IT activities involve IT management andapplications. Only 5% of respondents outsource IT Strategy, 10% outsourceprocurement, and 28% outsource systems architecture. These activities are oftenconsidered strategic in nature... In general infrastructure operations are the mostcommonly outsourced activities, including disaster recovery (68%), client/servers andpersonal computer operations (67%), mainframe operations (61%), networks (57%),and midrange computing (54%).” The same study also examined what the marketplace is doing in relation to single /multiple suppliers. It can be argued that although a single supplier approach removessome of the benefits of competition / use of best of breed solutions this is a priceworth paying given the issues that arise regarding demarcation and effectivemanagement of a multiple supplier environment. However, in practice 82% ofrespondents in the study do use multiple supplier contracts. The tendency towards multiple supplier relationships and retention of key functionsin-house is expressed by PA Consulting in “IT Outsourcing Getting The BalanceRight: - PA Consulting -(www.firmbuilder.com/function/it – as of August 2000)”.They note: - “Wholesale outsourcing of IT is being abandoned and many organisations are nowtaking a much smarter approach to their outsourcing. Companies are realising that itmakes sense to retain in-house responsibility for those IT capabilities that are criticalto their businesses as opposed to delegating such core competencies to a third party...” Delivery Mechanisms There is no one simple model for delivery of outsourced solutions. The following listdescribes a range of options available to us within the marketplace. In any proposalsas to how best to manage our IT portfolio we should consider which of the solutionsbelow best meets the needs of any particular area/service: -

q Facilities management – (operational management of hardware/softwareusually associated with mainframe contracts).

q Managed Service (ICT solution delivered as part of an overall servicedelivery package – e.g. ITNet Payroll).

q Contracts targeted at specific ICT areas (e.g. Desktop).q Consulting.q Application Service Provision (applications paid for on rental basis).

Hypothesis 1 / 10

q Third party development contracts.q Use of IT specialist contractors.q Software Packages.

Hypothesis 1 / 11

Total Outsourcing As one might expect from the statistics outlined in the previous section the “TotalOutsourcing” model to a single contractor of all functions is less favoured (in termsof numbers of contracts) at present than the multiple supplier / split functionapproach. During our initial data gathering exercise we did explore this approachwith one Local Authority that has taken the Total Outsourcing approach –Lincolnshire County Council. In order to explore this option further we subsequentlymet with their outsourcing partner Hyder. Capita were also keen to explore thisoption with us in our conversation with them. The advantages of the Total outsourcing model derived from the above contacts are asfollows: -

q Economies of scale / ability to re-engineer processes across the wholebusiness.

q Given the above possibilities of realising 15-20% efficiencies across therange of services outsourced (requires range of services over and above ITto be put out. 20% quoted by Hydra in relation to Lincolnshire typecontract, 15% mentioned by Capita).

q For those who enter into the arrangement early for their region thepossibility of setting up regional centre for delivery of such services toprotect staff / create future employment.

q Realisation of up-front investment by incoming organisation given thelonger term income for them from such a contract.

Set against these benefits the following risks / dis-benefits were identified.

q All eggs in one basket. Wholly reliant upon the performance of a singlecontractor. If they fail to perform then the authority fails across a widerange of services.

q Contracts are established for 10 years or more. Ties into single companyfor that time. Reduces flexibility. Can potentially leave the authoritywithout the critical mass of competent staff to pick up pieces followingtermination or failure of the contract. Investment tends to be concentratedin early years – could lead to difficulty if demands rise /direction changesin subsequent years.

q Potential for the company to whom the contract was awarded to changefocus / be taken over during the contract period. As these contracts areoften reliant on high degree of trust and compatible culture between theorganisations involved this has the potential to seriously affect the qualityof the delivered services. Note recent change of ownership of Hyder.

q Inability to focus particular areas at “best of breed providers”. May be lackof synergy between various aspects of the contract – e.g. Catering and IT.

q This is a very new market. By the end of this year there will be only 10 orso such contracts in the country. They are to that extent untested and giventhe range of services involved thus carry high risk until it becomes clearthat they can deliver the benefits promised.

Hypothesis 1 / 12

In addition to the issues highlighted above the following should be taken into accountfrom the Hertfordshire perspective: -

q Hertfordshire has already outsourced in a number of the areas that aretypical of such total outsourcing arrangements. I.E. Finance, IT, Property.To bring all of these contracts together under one supplier at the same timewould not be a simple task given the terms of the current contracts.Furthermore it is likely that a number of efficiencies (in terms of businessprocess re-engineering) have already been realised within the existingcontracts thus leaving it difficult to find the 15-20% efficiencies referred toabove. These savings can be further exemplified by contract management.

q Hertfordshire is not the first authority in this region to pursue this type ofcontract. Lincolnshire is not too far away, but Norfolk have established acontract with Capita for around 1 year now and Bedfordshire are about toaward a similar contract. We would thus find it hard to establish a regionalcentre and our people / personnel could be at risk if we were to pursuesuch a route.

q The Lincolnshire contract appears to have been awarded with the particularfocus of:-

1) Cost reductions / efficiencies.2) Investment in back office systems (e.g. Finance and HR, Property).

Although Hertfordshire would also like to realise the above they arenot the only drivers behind our thinking on ICT. HCC as anorganisation has started to realise the potential of ICT to drive forwardservice quality improvements, meet the Modernising Governmentagenda, and enable a much more client focussed approach to ourservice delivery. Herts Connect is one example of such thinking /development. A partner organisation/contract that has a focus solelyon the drivers outlined above could stifle such innovation anddirection.

q Hertfordshire has taken a range of approaches towards outsourcing already.As well as the range of the contracts across services noted above we havealso adopted many of the various mechanisms – e.g. Managed Service inPayroll, Pensions, - consulting – managed package implementations etc.

Taking into account the overall balance of benefits / risks outlined above it issuggested that a total outsourced model would be inappropriate for Hertfordshire ICTat this time. Such a model should not be completely ruled out for the future but onlyif the model can be shown to work with suppliers that are now entering into themarket to an extent that such success outweighs the other potential risks / dis-benefits.Both Hyder and Capita were of the view that services other than ICT should beconsidered as an overall part of such a deal in order to realise the full potential of suchan approach and this will need to be considered in any future examination of thisapproach and as such is outside the scope of this review. We recommend that anyfurther investigation should be considered by the “procurement board” established

Hypothesis 1 / 13

under best value review of contract management and procurement.

Hypothesis 1 / 14

Selective Outsourcing As noted above, it is more common for companies to enter into contracts withmultiple suppliers than with a single provider. Such an approach is favoured becauseit enables: -

q The organisation to maintain influence / decision making over businesscritical areas and direction.

q Buy in to areas in which specialist skills might be missing in theorganisation or where areas such as recruitment/retention of appropriateskills are an issue.

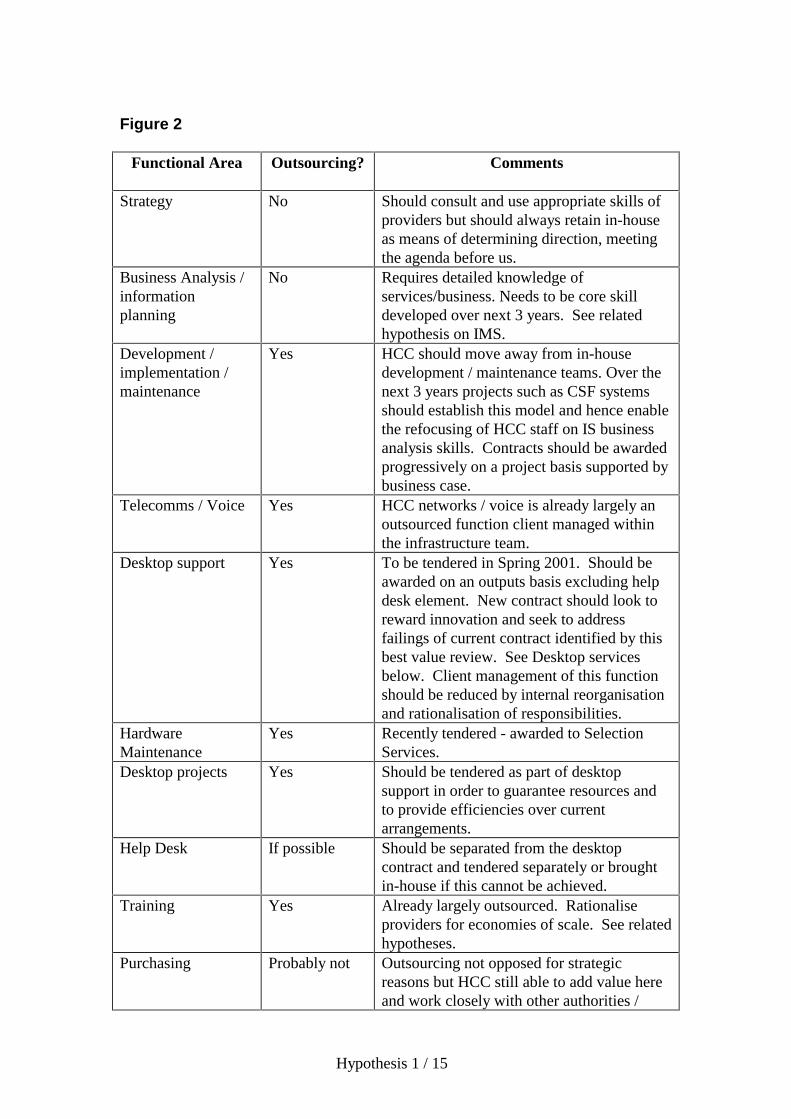

This raises the question of what areas might be appropriate for an organisation toretain in-house and which areas might be better performed by an outsourcingarrangement? Some pointers as to what organisations are currently thinking aroundthe right level of portfolio mix can be taken from the analysis of what is happening inthe market place – as discussed earlier (e.g. not many organisations are outsourcingtheir ICT strategy). However, drivers differ between organisations and we havetherefore sought to analyse the best fit for Hertfordshire County Council based on therange of ICT activities undertaken. We have also taken note of the views expressedby the companies whom we interviewed. The approach that we have adopted to help determine where outsourcing solutionsmight be appropriate is to take a measured look at the relationship between thebusiness and IT. This has been outlined in the matrix in figure (1) where eachcompetency is described, grouped in terms of functions and it’s strategic importanceto HCC business is logged. Any particular issues concerning maintenance of thatparticular activity in-house is also noted within the matrix. Where possible we haveindicated available costs for the function along with the numbers of staff associatedwith each activity as assigned through the Hedra analysis. Our headline conclusions are detailed below grouped into functional areas. Theyreflect the views of the authors as to the relative strategic importance of each of theareas discussed and the particular issues with each of the elements of the service.They also reflect the general views of our wider reading on the subject / experience ofothers. As such the recommendations workshop may wish to discuss / reprioritisebased on the consensus of opinion across representatives of services: -

Hypothesis 1 / 15

Figure 2

Functional Area Outsourcing?

Comments

Strategy No Should consult and use appropriate skills ofproviders but should always retain in-houseas means of determining direction, meetingthe agenda before us.

Business Analysis /informationplanning

No Requires detailed knowledge ofservices/business. Needs to be core skilldeveloped over next 3 years. See relatedhypothesis on IMS.

Development /implementation /maintenance

Yes HCC should move away from in-housedevelopment / maintenance teams. Over thenext 3 years projects such as CSF systemsshould establish this model and hence enablethe refocusing of HCC staff on IS businessanalysis skills. Contracts should be awardedprogressively on a project basis supported bybusiness case.

Telecomms / Voice Yes HCC networks / voice is already largely anoutsourced function client managed withinthe infrastructure team.

Desktop support Yes To be tendered in Spring 2001. Should beawarded on an outputs basis excluding helpdesk element. New contract should look toreward innovation and seek to addressfailings of current contract identified by thisbest value review. See Desktop servicesbelow. Client management of this functionshould be reduced by internal reorganisationand rationalisation of responsibilities.

HardwareMaintenance

Yes Recently tendered - awarded to SelectionServices.

Desktop projects Yes Should be tendered as part of desktopsupport in order to guarantee resources andto provide efficiencies over currentarrangements.

Help Desk If possible Should be separated from the desktopcontract and tendered separately or broughtin-house if this cannot be achieved.

Training Yes Already largely outsourced. Rationaliseproviders for economies of scale. See relatedhypotheses.

Purchasing Probably not Outsourcing not opposed for strategicreasons but HCC still able to add value hereand work closely with other authorities /

Hypothesis 1 / 16

providers to establish best possible prices(see Hedra confirmation). Attemptedoutsourcing of desktop PC purchasing inearly 90s was a failure as supplier did nothave the same interest in speed of deliveryetc.

R&D Retain some Need to embed R&D in the above contractsbut retain some R&D potential to addressHCC specific challenges and keep in-houseanalysis function up to speed.

Standards/awareness/ security

No Should be retained to realise control overframework and secure environment in whichwe expect our contractors to operate.

New Technologies Retain some Development has already been addressedabove where recommendation has been tooutsource. It is suggested that the onlyexception might be in new technology areaswhere in-house work can provide HCC witha leading edge in terms of developing newmethods of service delivery etc. e.g. HertsConnect – joint delivery with contractors.

q ICT strategy should remain the preserve of HCC. That is not to sayproviders cannot assist / provide valuable guidance around this particulararea but strategic direction setting for a service that affects / impacts muchof what we deliver as an authority is key to achieving the authority’sagenda. Both Capita and ITNet were supportive of this position.

q Business analysis / skills to exploit emerging ICT should remain withinHCC. i.e what we are commonly referring to as IMS throughout in otherareas of this best value review. Again, Capita offered this up as an areathat they thought should be the preserve of the authority. We support thisas an in-house activity because it is the essential link between the servicerequirements and the ICT that is finally delivered to support them. Assuch it requires an intimate knowledge of the business / service and istherefore a prime candidate for the dividing line between client andprovider. We have not yet come across proven alternative models in ourdiscussions / experience that places this activity wholly with the providerorganisation. This should be the future base for client management(currently the domain of IT managers).

q Project based desktop work. Currently this is theoretically capable ofbeing undertaken by a range of different suppliers. In practice it is oftenonly practically undertaken by the same company that provides ICTsupport because of the requirement to have knowledge of HCC standards /set up and to work in a way that is acceptable / supportable by the supportteam. This activity is therefore best met by the same outsourced supplieras the support contract and should therefore be contracted for at the same

Hypothesis 1 / 17

time using an estimate of ongoing project work (in this case circa £570kper annum – see appendix 1). In so doing we should be able to negotiatedown current costs. This could theoretically lead to efficiencies in theregion of 25-50% on project based activity given the relative cost ofproject versus support based staff – this would offset the additional cost ofservice improvements.

q Development / implementation/maintenance. It is proposed that HCC lookto move away from in-house delivery of such activities over the next 3years by the introduction of project based, packaged systems solutions thatare provided and implemented by external suppliers. The ChildrenSchools and Families Adult Care Services system is already beingdelivered via this route and the Financial / HR systems replacement shouldfollow the same model. This would permit the organisation to concentrateon service / business analysis rather than technical delivery. It would havethe added advantage of supported upgrades being available as part of ourlicence agreements. Finally, by ensuring that such systems are developedon package basis to agreed standards we can look to eradicate issues ofdual entry and systems incompatibility. Needs to go hand in hand withdevelopment of IS role in departments (separate hypothesis).

• Helpdesk. We are proposing that this be tendered as a separate contractand if that cannot be achieved that we should consider establishment of in-house solution.

Reasoning behind establishment of separate contract is as follows: -

a) One of our key issues around management of problem resolution in theICT arena is around question of “ownership”. New help deskarrangements should look to establish management contractor concept athelp desk level with that contractor being responsible for chasing, closingdown calls, ensuring client satisfaction.

b) Help Desk provides key management information on contract delivery.It does not therefore seem good practice to imbed this in one of thesupplier contracts. Need to have independent information on howcontracts are performing.

c) Users of help desk want single point of contact for multiple ICT issues.The operation therefore needs to be independent of all of the contracts towhom it then directs activity.

d) We favour outsourcing because it would bring professional skills to anarea that requires specialist knowledge / management. We could alsobenefit from efficiencies of scale both in terms of range of staff availableto pool activity from and in overall costs of technology to provide theservice. Outsourcing would also provide us with greater flexibility inrealising efficiencies in this area.

Hypothesis 1 / 18

q Telecommunications. We have not had time to fully evaluate the optionsavailable to us in the telecommunications arena. Further development ofcontracts in this area should be based on addressing concerns raised in theVital Networks report and in meeting projected increased demand over thenext 5 years. Efficiencies should be realised through exploration ofalternative service delivery mechanisms and reducing costs of telecommsover that period. A programme to achieve this should be required to bedelivered.

q New Technology. Although suggesting we retain some of these skills in-house we should also explore the option of engaging a partner consultancythat can advise us on an ongoing basis re benchmarks / performance of ourcontractors / future market trends etc.

Hypothesis 1 / 19

Insourcing The discussions outlining best possible portfolio of outsourcing arrangements abovehave covered some of this area. However, we were keen to give equal weight to thisstudy in a section of its own that outlines the benefits and potential dis-benefits of aninsourced approach. In particular the work undertaken for us by the Hedraconsultancy in the first phase of this Best Value Review did lay down some challengesin this area in terms of possible efficiencies that could be made by adopting aninsourcing. In brief the benefits outlined by Hedra of considering insourcing of ICT services wereas follows: -

q “HCC has a higher cost per supported PC at £943 per annum. This iscompared to £833 in the benchmark.” One of the reasons for this highercost was put down to outsourcing of PC support to ITNet. Hedraacknowledges that costs of the ITNet contract are not high in relation toother typical contracts of this type.

q Hedra therefore suggested that we might consider insourcing of thissupport activity in order to bring costs in line with the benchmark figure.

q Hedra also outlined a number of areas where the ITNet contract was notmeeting user expectations and therefore argued that the additional cost ofthe outsource contract was not providing us with any better service than wecould address ourselves through cheaper in-house activity.

NB: Not all of the additional costs were down to ITNet. Hedra outlined that HCCappeared to have excessive client management of the contract through the devolvedmanagement of ICT infrastructure. The risks / dis-benefits of pursuing insourcing of our IT services in the areas identifiedabove are as follows: -

q Outsourcing is undertaken for a range of reasons other than cost savings.Unit costs of specific personnel / engineers etc may well be higher than acomparative insourced operation but this has to be weighed against otherpotential advantages of the outsourced model. A comprehensive list ofreasons behind outsourcing are given in R Keppler W O Jones“Outsourcing Information Technology, Systems & Services pp 47-53” butthe following points highlight just some of the reasons why HCC wouldbenefit from continued outsourcing rather than opt for insourcing of IToperations.

q Flexibility of addressing variable project based activity may be lostthrough insourcing of activity. As can be seen from Appendix 1 HCCundertakes around £570k worth of project based activity with our currentsupplier in a typical year. It is proposed that such activity be built intofuture contracts to seek to reduce overall cost of the activity. Anoutsourced supplier should also bring the benefit of additional staff/skill to

Hypothesis 1 / 20

address these areas at times of peak requirement. Insourced activity islimited to the numbers of staff employed at any one time and is difficult tosupplement at times of additional need.

q Through our visits to other sites that have been shown to have better“insourced” benchmarks in the support / help desk arena we were able togain a wider view of performance against service agendas etc. From thiswe formed the view that there is very often a trade off between energiesput in to manage such activities in-house and achievements in other areas.For example, Warwickshire have a well run in-house help desk supportarrangement but it could be argued that this is at the expense ofachievement in other areas such as compatibility across departments, lackof annual technology refresh, little corporate ICT visioning / strategy, andlittle undertaken yet in terms of Herts Connect / Modernising Governmenttype projects. Hertfordshire is recognised as being successful in movingthis agenda forward and one would have to question if this would be thecase if resource was tied up in managing detailed ICT support operations?

Interestingly both Warwickshire and Newcastle are currently looking atoutsourcing as an option for the future.

q Some of the challenges of the Hedra findings themselves are best metthrough a continued outsourced arrangement. For example, in an area suchas help desk / support where we ought to look to manage quality up andnumbers of staff down an outsourced supplier could provide the flexibilityto move staff onto other accounts to achieve our targets. In an insourcedoperation such rationalisation is not easy and could potentially result inredundancy for some staff together with the costs and managementproblems that this can bring.

q Another area that we need to address in taking forward ICT support atHertfordshire is introduction of new technologies such as Windows 2000,and remote control / updating via appropriate software (in itself designedto reduce costs). Although we have not been entirely successful inrealising the benefits that an outsourced company can bring in this areafuture contracts should be negotiated to ensure / guarantee access to thewider expertise that should come from an IT focused company.

q Recruitment of ICT staff in this part of the world is not easy. Although wehave not had time to provide relevant statistics it is known that ITNetthemselves have had difficulty in recruiting to the operation and thatcertain HCC posts have been hard to fill. In such a scenario an IT basedcompany will always have an edge over a local authority in being able torecruit and retain staff given the wider opportunities and career paths theyare able to offer them.

In short, taking into account the overall balance of arguments for / against insourcing /outsourcing of activity it is felt that outsourcing provides us with opportunities tomore readily address the range of ICT issues before us in the areas of desktop support

Hypothesis 1 / 21

and helpdesk. Insourcing, although initially attractive from a unit cost perspectivewould be both difficult to achieve and may have a negative impact in terms ofachieving strategic direction, and authority agenda. The levels of efficiencies thatcould be achieved by insourcing the operation, are no higher than should be realisablethrough better negotiated/managed contract.

There appears to be no reason why the weaknesses of our current set-up could not beaddressed though improved outsourcing arrangements / contracts.

The decisions regarding insourcing / outsourcing of other should be judged on theirrelative merit – see discussions around fig2 above.

Hypothesis 1 / 22

Appendix 1

Outsourced Contracts excluding network Year 2000 / 01

Total Itnet Mainframe costs 904,326Mini computers (Social services, Libraries , Magistrates) 39,002Data Preparation 26,000Network Support charges 50,000

Total ITnet charges FM 1,019,328HCC Contract Support (Mainframe & Minis) 63,220

Overall FM Contract Charge 1,082,548

HCC PC and Office Support contractlicences for Notes E-mail ,Ghost images,TVD,etc 8,000CSCS- Contract Management 52,790CSCS -Corporate ICT Purchasing group 52,000

HCC Total 112,790ITnet charges –PC & Office Support contractDesktop (engineers,help desk,management,etc) 1,036,513Project Work -circa 7 bodies (estimated as typical) 570,000Income from Comnet & rents & investment pot -185,000

Total ITnet 1,421,513

Hardware support (Selection Services) 157,500Desktop and Projects Total 1,691,803

OVERALL COSTS 2,774,351

Hypothesis 1 / 23

Appendix 2. Estimated Cost - negotiations

Costings

Contract Management Input Total: £6,000.00

Small Team (3 people for 25 days) – Consisting of say 2 people on Grade PM2 localpoint 05 and 1 person on Grade MS scp 55 with superannuation

HourlyRate

DailyRate

Total for 25days

PM2 local point 05 (inc. on costs) withsuperannuation

£26.50 £196.10 £4,902.50

PM2 local point 05 (inc. on costs) withsuperannuation

£26.50 £196.10 £4,902.50

M5 scp 55 (inc. on costs) withsuperannuation

£23.41 £173.23 £4,330.85

Total for the team over 25 days: £14,135.85

Evaluation Team (5 people for 5 days) – Consisting of 3 people on Grade M5 scp 55and 2 people on Grade PM2 local point 05 with superannuation

HourlyRate

DailyRate

Total for 5days

M5 scp 55 (inc. on costs) withsuperannuation

£23.41 £173.23 £866.17

M5 scp 55 (inc. on costs) withsuperannuation

£23.41 £173.23 £866.17

M5 scp 55 (inc. on costs) withsuperannuation

£23.41 £173.23 £866.17

PM2 local point 05 (inc. on costs) withsuperannuation

£26.50 £196.10 £980.50

PM2 local point 05 (inc. on costs) withsuperannuation

£26.50 £196.10 £980.50

Total for the team over 5 days: £4,559.51TOTAL COST: £24,695.36