53

How to Value Companies Using Trading Multiples

| Date post: | 17-Aug-2015 |

| Category: |

Economy & Finance |

| Upload: | bluebookacademy |

| View: | 79 times |

| Download: | 0 times |

How to Value Companies Using Trading Multiples

•Relative Valuation Approach

•Enterprise Value vs Equity Value

•Valuation Ratios

•Benefits and Limitations in Relative Valuation

INTRODUCTION

Asset based valuation Using a business’ assets to determine value

COMMON VALUATION METHODS: ASSET BASED

Discounted Cash Flow Valuation A business’ cash-generating potential and capitalise its

value

COMMON VALUATION METHODS: CASH FLOW

Relative Valuation What comparable companies are worth to

benchmark a value

COMMON VALUATION METHODS: RELATIVE

RELATIVE VALUATION: INTRODUCTION

In relative valuation, the value of an asset is compared to the values assessed by the market for similar or comparable assets.

RELATIVE VALUATION: INTRODUCTION

4 STEPS TO PERFORM A RELATIVE VALUATION

RELATIVE VALUATION: INTRODUCTION

Identify comparable assets and obtain market values for them

1

RELATIVE VALUATION: INTRODUCTION

Translate these market values into comparable metrics - price multiples

(because absolute figures cannot be compared)

2

RELATIVE VALUATION: INTRODUCTION

Compare price multiples for the asset being analysed to the multiples of its peers

3

RELATIVE VALUATION: INTRODUCTION

Determine whether the asset is under or over valued

4

MULTIPLE APPROACHES

There are two types of multiples in company valuation:

1. Enterprise Value (Firm Value) multiples

2.Equity Value multiples

ENTERPRISE VALUATION

Enterprise Value is the market value of a company’s:

• Net operational assets +

• Value of its future growth opportunities +

• Intangible assets

FIRM VALUE USING THE BALANCE SHEET

Debt

Equity

Cash

Operating Assets

ENTERPRISE VALUE

=

Debt

Equity

Cash

Operating AssetsEnterprise

Value is the market value of

the Balance Sheet

+

+

CALCULATING ENTERPRISE VALUE

Enterprise Value = Equity Value + Total Debt - Cash

Net DebtShare price * No. shares outstanding

CALCULATING ENTERPRISE VALUE

Enterprise Value = Equity Value + Net Debt

EQUITY VALUATION

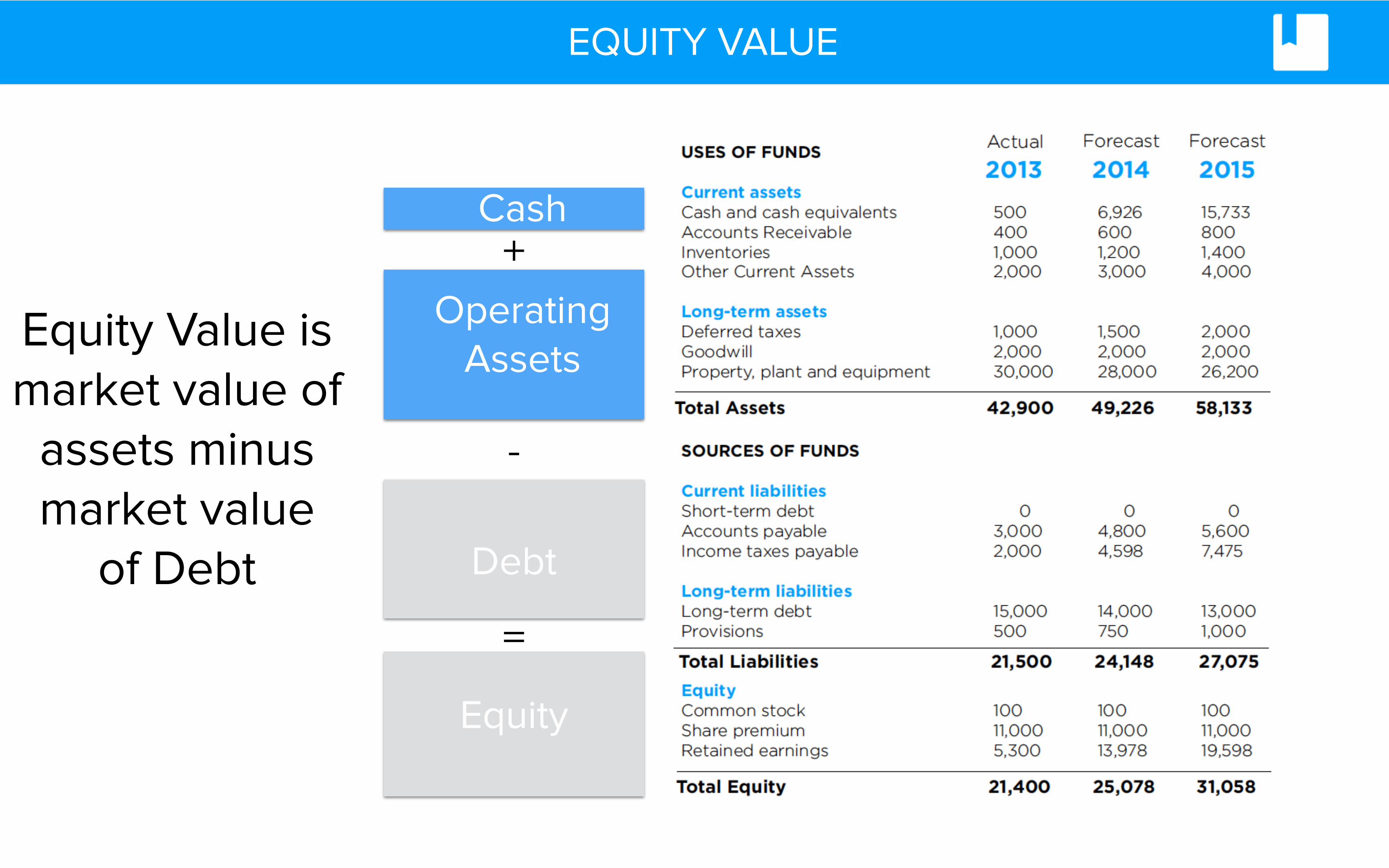

Equity value is the market value of a company’s shares to

its owners or shareholders

EQUITY VALUE

-

Debt

Equity

Cash

Operating Assets

Equity Value is market value of

assets minus market value

of Debt

+

=

CALCULATING EQUITY VALUE

Equity Value = Enterprise Value - Net Debt

EQUITY & ENTERPRISE VALUE

Sales

-COGS

Gross Profit

-Operating Expenses

Operating Income (EBIT)

-Interest Expense / Income

Profit before Tax

-Tax

Profit after Tax (Net Income)

Enterprise Value

Net Debt / Cash

Equity Value

MULTIPLES OVERVIEW

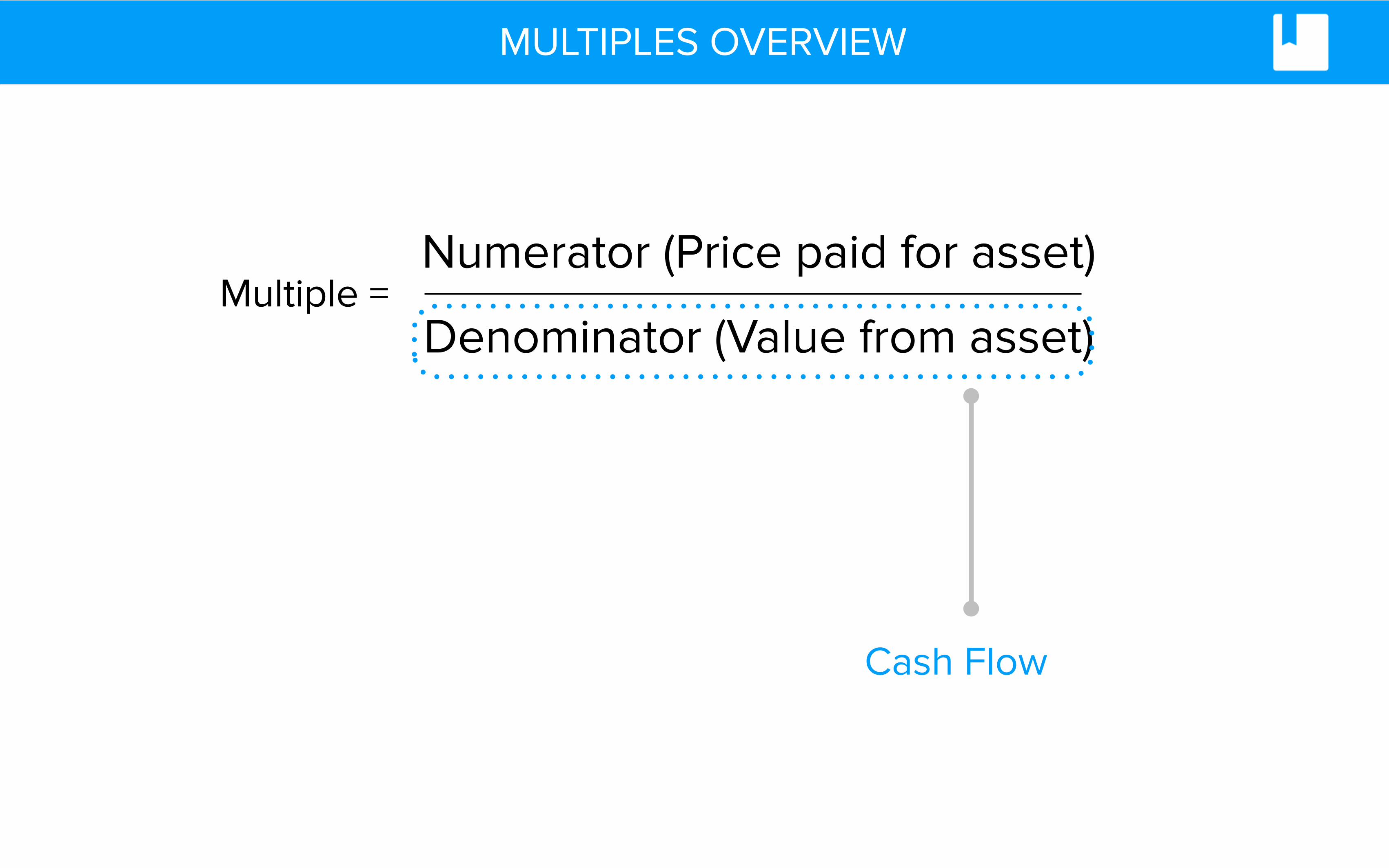

Multiple =Numerator (Price paid for asset)

Denominator (Value from asset)

MULTIPLES OVERVIEW

Multiple =Numerator (Price paid for asset)

Denominator (Value from asset)

Equity Value Enterprise Value

MULTIPLES OVERVIEW

Multiple =Numerator (Price paid for asset)

Denominator (Value from asset)

Sales

Multiple =Numerator (Price paid for asset)

Denominator (Value from asset)

Earnings

MULTIPLES OVERVIEW

Multiple =Numerator (Price paid for asset)

Denominator (Value from asset)

Cash Flow

MULTIPLES OVERVIEW

VALUATION MULTIPLES

Most multiples are based on a type of earnings on a company’s income statement.

Enterprise multiples are calculated using earnings from above the interest line. • Eg. EV/Sales, EV/EBIT, EV/EBITDA

Equity multiples uses earnings figures from below the interest line. • Eg. P/E

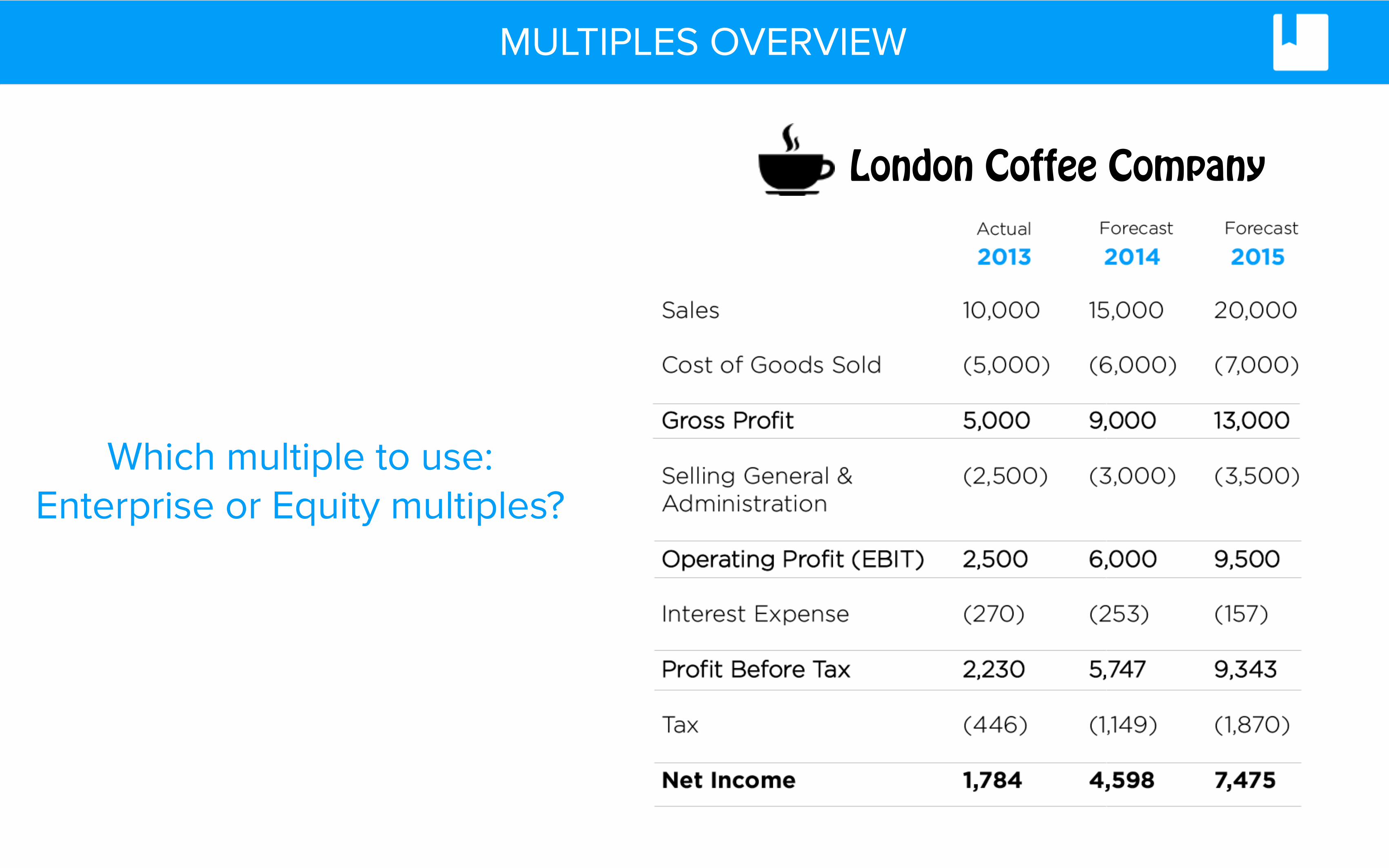

London Coffee Company

Which multiple to use: Enterprise or Equity multiples?

MULTIPLES OVERVIEW

ENTERPRISE VALUE MULTIPLES: EV/SALES

Market Cap + Total Debt - Cash Sales

EV/Sales =

Revenue multiples are used to value companies where earnings are not expected in the near term.

For example:

• High-growth firms or • Distressed companies

ENTERPRISE VALUE MULTIPLES: EV/SALES

QUESTION

Which of the following is the best description for equity value?

A. The total value of the business to all providers of capital

B. The total value of the business to all shareholders

C. The total value of the business to all providers of debt

QUESTION

Which of the following is the best description for enterprise value?

A. The total value of the business to all providers of capital

B. The total value of the business to all shareholders

C. The total value of the business to all providers of debt

ENTERPRISE VALUE MULTIPLES: EV/EBITDA

Market Cap + Total Debt - Cash EBIT + Depreciation + Amortisation

EV/EBITDA =

By applying EBITDA multiples to value a target company, this yields an enterprise value.

As an enterprise value multiple, it can be used to compare companies with differing amounts of debt (gearing)

It is also not affected by differences in depreciation and amortisation

ENTERPRISE VALUE MULTIPLES: EV/EBITDA

EQUITY MULTIPLES: PRICE-EARNINGS RATIO (P/E)

P/E = Market Price per Share Earnings per Share

EQUITY MULTIPLES: P/E

•P/E ratios can only be judged against ratios of other companies in the same industry.

•P/E ratios can be distorted as Earnings per Share (EPS) is an accounting term.

•A high P/E can be achieved by retaining a great proportion of earnings and paying low dividends to reinvest for growth.

HOW TO INTERPRET A MULTIPLE?

The P/E ratio is the price an investor would pay for $1 of a company's earnings or net profit.

If a company is reporting earnings per share of $4 and the stock is selling for $40 per share, the P/E ratio is 10x

HOW TO INTERPRET A MULTIPLE?

Two similar companies are both trading for $40 per share

Company A has reported earnings of $10 per share.

Company B has reported earnings of $20 per share.

How do we interpret both companies P/E ratios?

HOW TO INTERPRET A MULTIPLE?

Company A has a price-to-earnings ratio of 4x. Company B has a P/E ratio of 2x.

This means company B is much cheaper on a relative basis.

If a company has a higher EBITDA multiple compared to other companies in its sector, this indicates all of the following except:

A. The company is over valued

B. The company demonstrates high growth prospects

C. The company is highly geared

QUESTION

THE ART OF SELECTING MULTIPLES

Investors in different sectors calculate different equity and enterprise value multiples depending on their focus:

In retailing: The focus is usually on like for like sales (turnover) and profit margins.

In real estate and financial services: The emphasis is usually on return on equity.

In technology: the emphasis is on growth theme

DIFFERENT MULTIPLES FOR DIFFERENT INDUSTRIES

Industry Multiple Reason

Manufacturing P/E Normalised with business cycle

Early stage growth Cos. Revenue Limited figures available

Financial Services Price / Book equity Marked to market

Infrastructure EV/EBITDA Large D&A

Which of the following is true?

A. Price to earnings ratio multiplied by earnings per share equals price per share

B. Price to earnings ratio divided by earnings per share equals price per share

C. Price per share multiplied by earnings per share equals price to earnings ratio

QUESTION

SOURCING FINANCIAL INFORMATION

Where can you find the relevant information to calculate valuation multiples?

SOURCING FINANCIAL INFORMATION

• Company accounts (10-K, 10-Q, Annual Report) - (Historical Financials)

• Bloomberg, Google Finance - (Market Values)

• Banks Research Reports - (Forecasts)

• Industry Classification Groups (SIC, Bloomberg, Factset)

• Independent Sector Reports

• Banks Industry & Company Research Notes

• Peer competitors

Where to find comparable companies

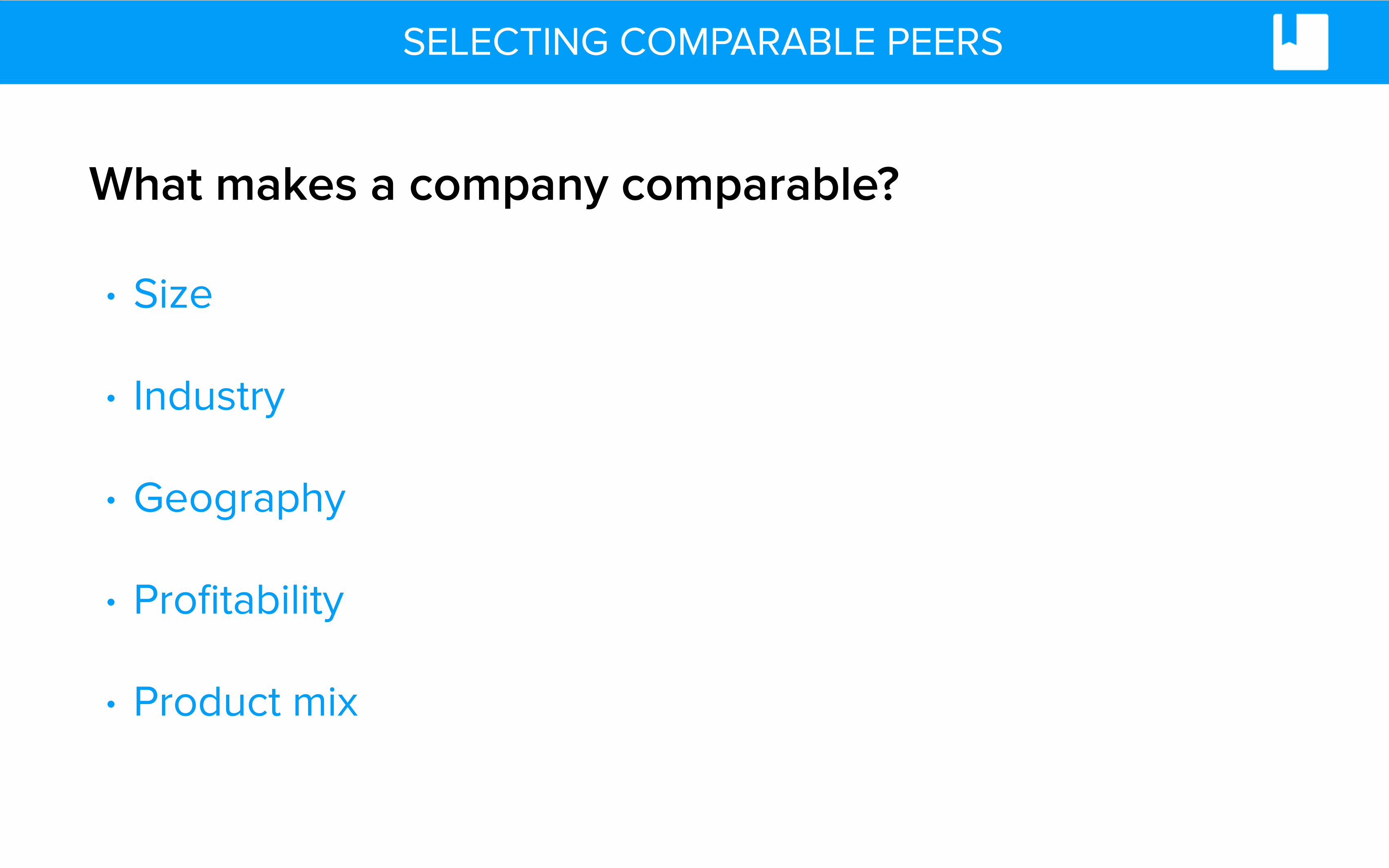

SELECTING COMPARABLE PEERS

• Size

• Industry

• Geography

• Profitability

• Product mix

What makes a company comparable?

SELECTING COMPARABLE PEERS

BENEFITS OF TRADING MULTIPLES

Q. What are some of the benefits of using trading multiples for valuation?

BENEFITS OF TRADING MULTIPLES

• Easy to calculate

• Widely used by investing community

• Provides useful information for value judgements

ISSUES WITH TRADING MULTIPLES

Q. What might be some of the issues with using trading multiples for valuation?

•Overly Simplistic

•Difficult to make true comparisons

•Must accurately value multiples of peers

•Not a dynamic view of long-term prospects

ISSUES WITH TRADING MULTIPLES

TRAILING VS FORWARD LOOKING MULTIPLES

• Multiples based on Last 12 month (LTM) earnings are called Trailing multiples

• Share price divided by EPS forecasts for the next 12 months gives us a forward multiple

• Forward multiples are applied to the forecast earnings of the target company

• Incorporate expectations about future company performance

Recap

• The Relative Valuation Approach

• Enterprise Value vs Equity Value

• Common EV and Equity-based Multiples

• How to Interpret a Multiple

• Benefits and Limitations of Using Trading Multiples