30

Gordon MacAulay BRI Australia What the World Wants from Australian Wheat

Gordon MacAulayBRI Australia

What the World Wants from Australian Wheat

OutlineOutline

2

• Scale of the World Wheat Industry• Competition is tough—Black Sea Ports

– Price is important• Wheat markets are risky—why?

– The nature of supply and demand– Risk management is essential

• Our biggest customer—Indonesia– This market wants our wheat—’look after it’

• Baked goods sector most important– Baking type wheat is wanted

• Quality versus yield—consistency– Product differentiation and market servicing costs– Consistency a major issue

• Internationalisation– Economies of scale and scope and the competitive fringe

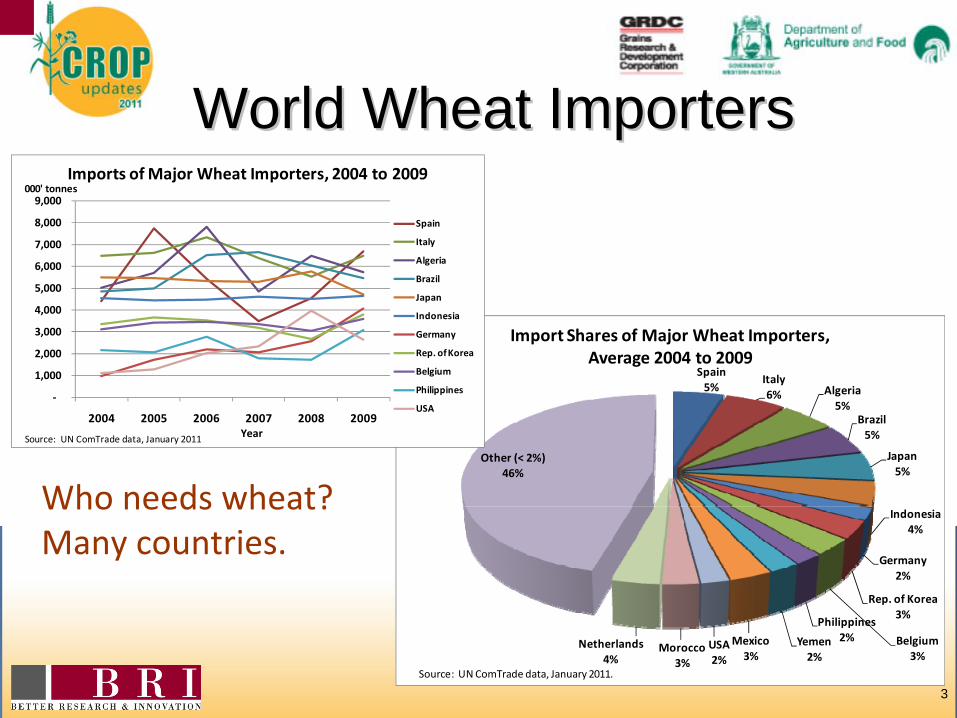

World Wheat ImportersWorld Wheat Importers

3

Who needs wheat?Many countries.

Spain5%

Italy6% Algeria

5%Brazil5%

Japan5%

Indonesia4%

Germany2%

Rep. of Korea3%

Belgium3%

Philippines2%Yemen

2%Mexico3%

USA2%

Morocco3%

Netherlands4%

Other (< 2%)46%

Import Shares of Major Wheat Importers, Average 2004 to 2009

Source: UN ComTrade data, January 2011.

‐

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2004 2005 2006 2007 2008 2009

Imports of Major Wheat Importers, 2004 to 2009

Spain

Italy

Algeria

Brazil

Japan

Indonesia

Germany

Rep. of Korea

Belgium

Philippines

USA

Source: UN ComTrade data, January 2011 Year

000' tonnes

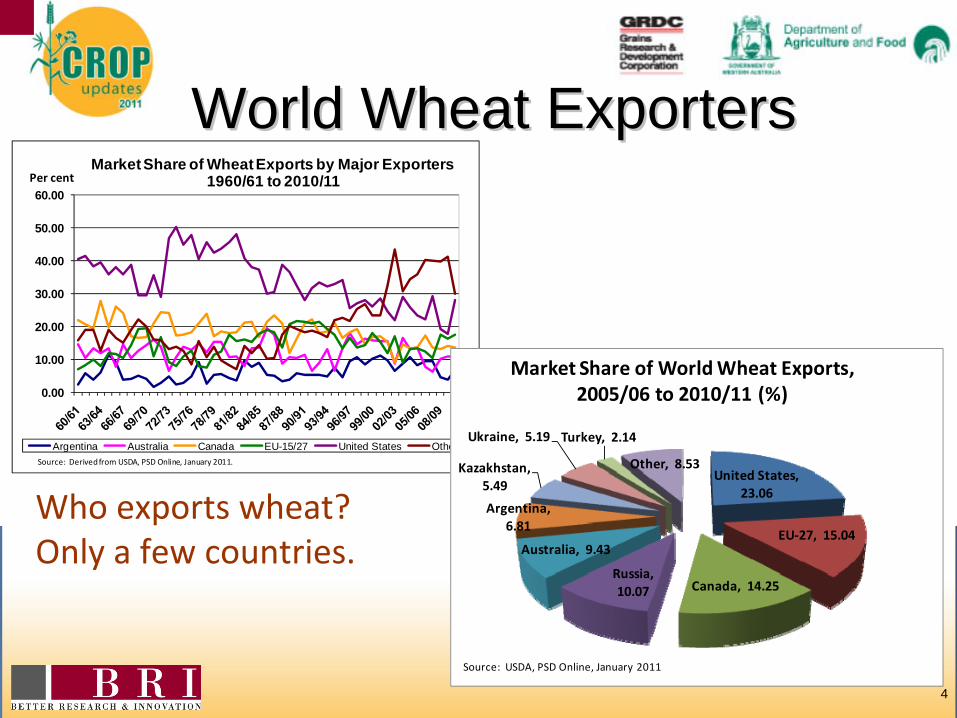

World Wheat ExportersWorld Wheat Exporters

4

Who exports wheat?Only a few countries.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Market Share of Wheat Exports by Major Exporters 1960/61 to 2010/11

Argentina Australia Canada EU-15/27 United States OtherSource: Derived from USDA, PSD Online, January 2011.

Per cent

United States, 23.06

EU‐27, 15.04

Canada, 14.25 Russia, 10.07

Australia, 9.43

Argentina, 6.81

Kazakhstan, 5.49

Ukraine, 5.19 Turkey, 2.14

Other, 8.53

Market Share of World Wheat Exports,2005/06 to 2010/11 (%)

Source: USDA, PSD Online, January 2011

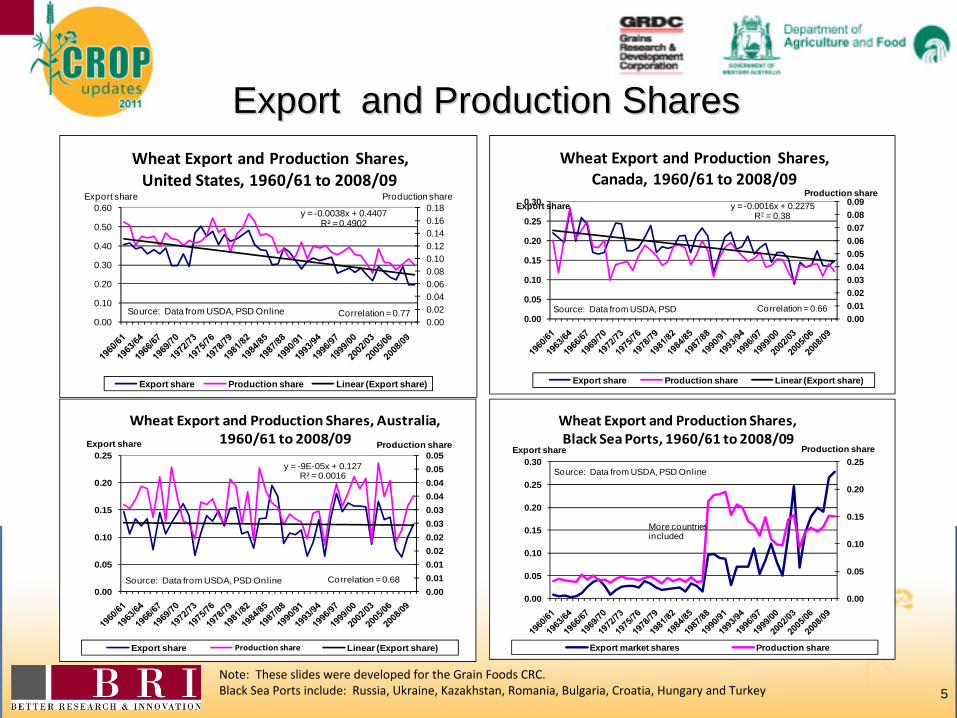

Export and Production SharesExport and Production Shares

5Note: These slides were developed for the Grain Foods CRC.Black Sea Ports include: Russia, Ukraine, Kazakhstan, Romania, Bulgaria, Croatia, Hungary and Turkey

y = -0.0038x + 0.4407R² = 0.4902

0.000.020.040.060.080.100.120.140.160.18

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Wheat Export and Production Shares, United States, 1960/61 to 2008/09

Export share Production share Linear (Export share)

Export share Production share

Source: Data from USDA, PSD Online Correlation = 0.77

y = -0.0016x + 0.2275R2 = 0.38

0.000.010.020.030.040.050.060.070.080.09

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Wheat Export and Production Shares, Canada, 1960/61 to 2008/09

Export share Production share Linear (Export share)

Export shareProduction share

Source: Data from USDA, PSD Correlation = 0.66

y = -9E-05x + 0.127R² = 0.0016

0.000.010.010.020.020.030.030.040.040.050.05

0.00

0.05

0.10

0.15

0.20

0.25

Wheat Export and Production Shares, Australia, 1960/61 to 2008/09

Export share Production share Linear (Export share)

Export share Production share

Source: Data from USDA, PSD Online Correlation = 0.68

0.00

0.05

0.10

0.15

0.20

0.25

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Wheat Export and Production Shares, Black Sea Ports, 1960/61 to 2008/09

Export market shares Production share

Export share Production share

Source: Data from USDA, PSD Online

More countries included

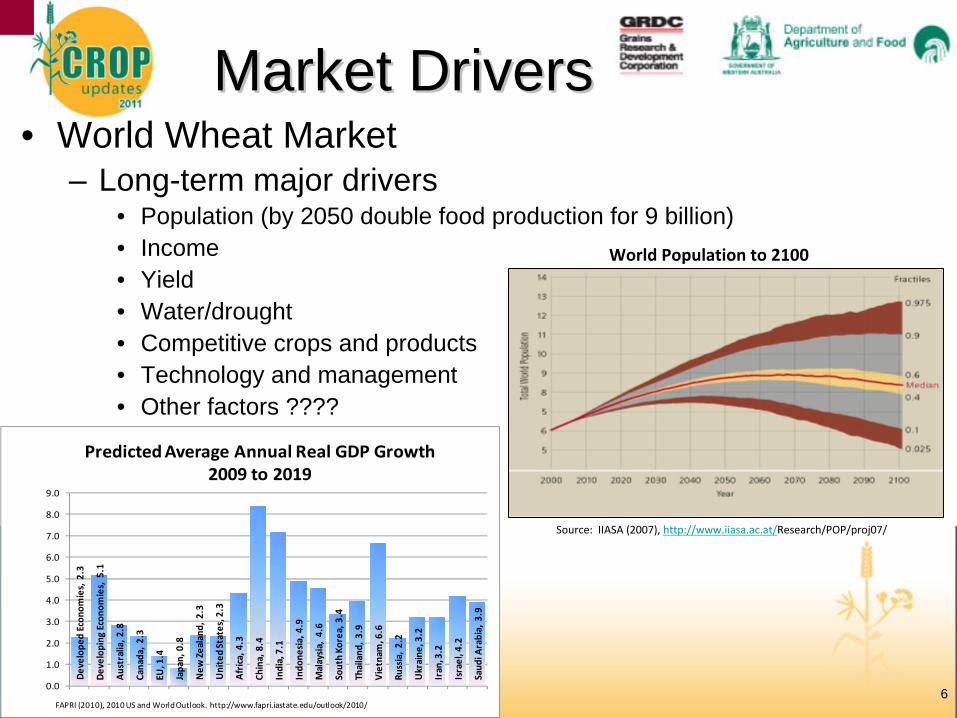

Market DriversMarket Drivers

6

• World Wheat Market– Long-term major drivers

• Population (by 2050 double food production for 9 billion)• Income• Yield• Water/drought• Competitive crops and products• Technology and management• Other factors ????

World Population to 2100

Source: IIASA (2007), http://www.iiasa.ac.at/Research/POP/proj07/

Develop

ed Econo

mies, 2.3

Develop

ing Econ

omies, 5.1

Australia, 2

.8

Canada, 2.3

EU, 1.4

Japan, 0.8

New

Zealand

, 2.3

United States, 2.3

Africa, 4.3

China, 8.4

India, 7.1

Indo

nesia, 4.9

Malaysia, 4.6

South Ko

rea, 3.4

Thailand

, 3.9

Vietnam

, 6.6

Russia, 2.2

Ukraine

, 3.2

Iran, 3.2

Israel, 4.2

Saud

i Arabia, 3.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Predicted Average Annual Real GDP Growth 2009 to 2019

FAPRI (2010), 2010 US and World Outlook. http://www.fapri.iastate.edu/outlook/2010/

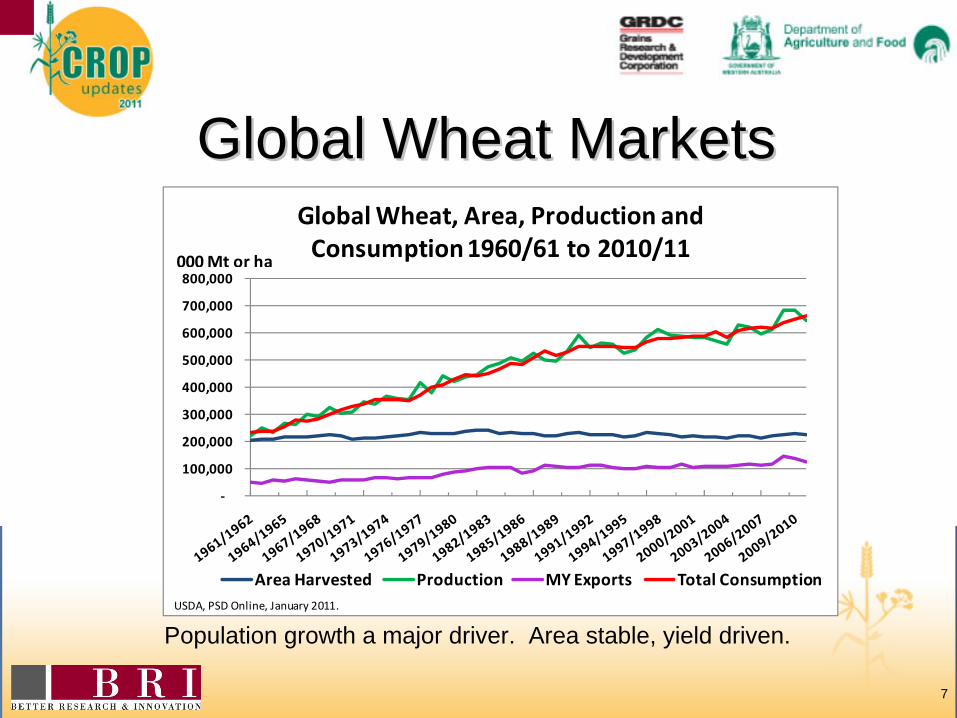

Global Wheat MarketsGlobal Wheat Markets

7

Population growth a major driver. Area stable, yield driven.

‐

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Global Wheat, Area, Production and Consumption 1960/61 to 2010/11

Area Harvested Production MY Exports Total ConsumptionUSDA, PSD Online, January 2011.

000Mt or ha

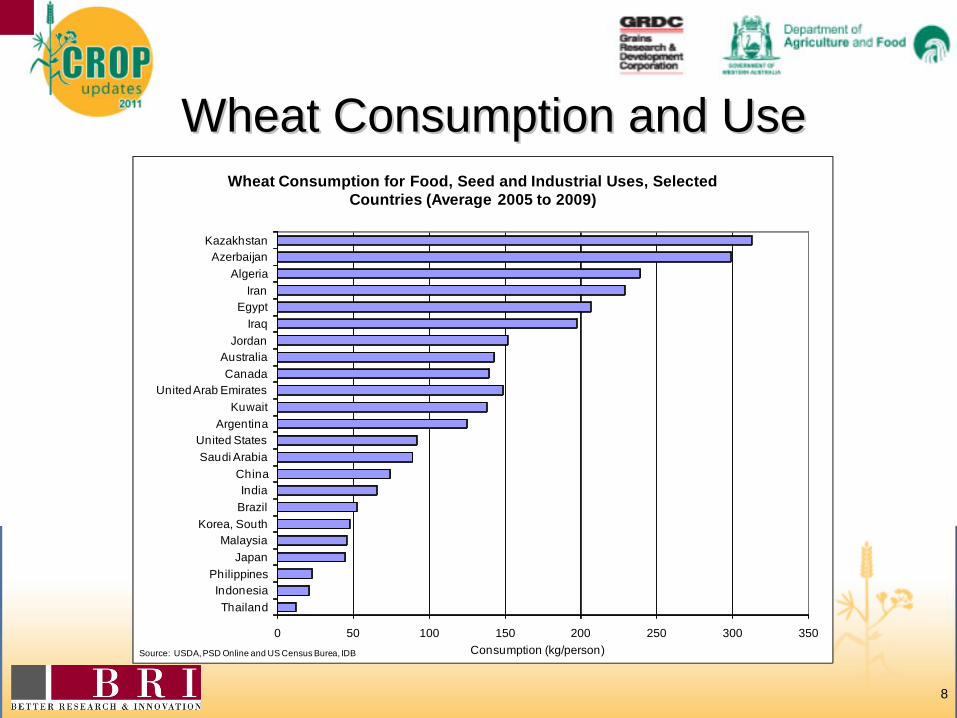

Wheat Consumption and UseWheat Consumption and Use

8

0 50 100 150 200 250 300 350

KazakhstanAzerbaijan

AlgeriaIran

EgyptIraq

JordanAustraliaCanada

United Arab EmiratesKuwait

ArgentinaUnited StatesSaudi Arabia

ChinaIndia

BrazilKorea, South

MalaysiaJapan

PhilippinesIndonesiaThailand

Consumption (kg/person)

Wheat Consumption for Food, Seed and Industrial Uses, Selected Countries (Average 2005 to 2009)

Source: USDA, PSD Online and US Census Burea, IDB

Market DriversMarket Drivers

9

• What do you think determines the market price for wheat (milling wheat)? (Rank your answers)– Exchange rate– Weather– Income– Futures traders– Supply and demand– Energy prices– Population growth– Other …..

Changing World MarketsChanging World Markets

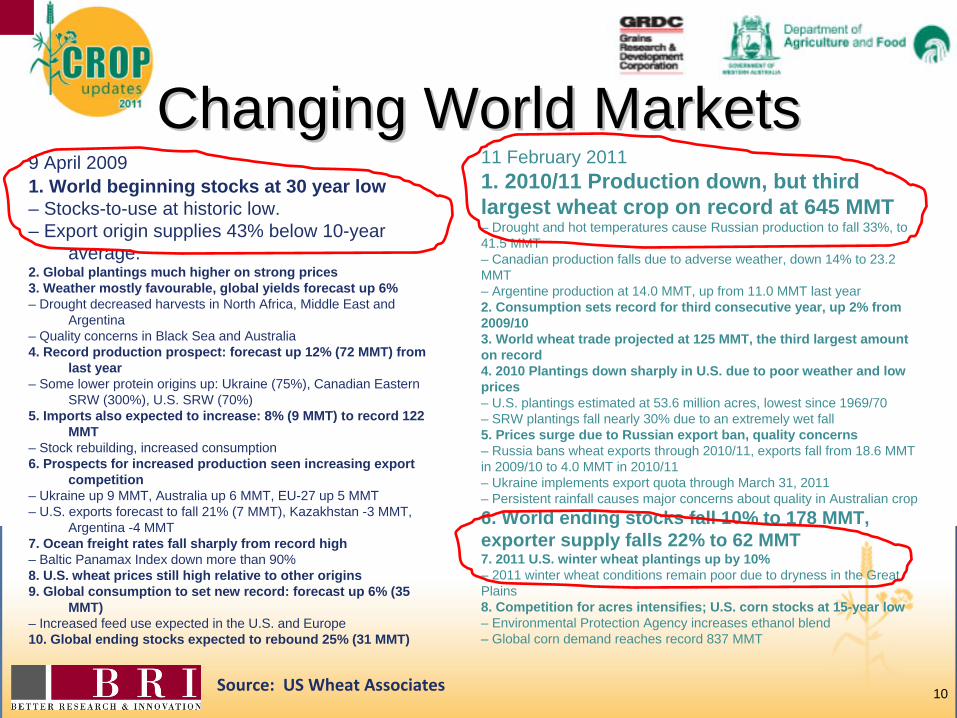

10

9 April 20091. World beginning stocks at 30 year low– Stocks-to-use at historic low.– Export origin supplies 43% below 10-year

average.2. Global plantings much higher on strong prices3. Weather mostly favourable, global yields forecast up 6%– Drought decreased harvests in North Africa, Middle East and

Argentina– Quality concerns in Black Sea and Australia4. Record production prospect: forecast up 12% (72 MMT) from

last year– Some lower protein origins up: Ukraine (75%), Canadian Eastern

SRW (300%), U.S. SRW (70%)5. Imports also expected to increase: 8% (9 MMT) to record 122

MMT– Stock rebuilding, increased consumption6. Prospects for increased production seen increasing export

competition– Ukraine up 9 MMT, Australia up 6 MMT, EU-27 up 5 MMT– U.S. exports forecast to fall 21% (7 MMT), Kazakhstan -3 MMT,

Argentina -4 MMT7. Ocean freight rates fall sharply from record high– Baltic Panamax Index down more than 90%8. U.S. wheat prices still high relative to other origins9. Global consumption to set new record: forecast up 6% (35

MMT)– Increased feed use expected in the U.S. and Europe10. Global ending stocks expected to rebound 25% (31 MMT)

11 February 20111. 2010/11 Production down, but third largest wheat crop on record at 645 MMT– Drought and hot temperatures cause Russian production to fall 33%, to 41.5 MMT– Canadian production falls due to adverse weather, down 14% to 23.2 MMT– Argentine production at 14.0 MMT, up from 11.0 MMT last year2. Consumption sets record for third consecutive year, up 2% from 2009/103. World wheat trade projected at 125 MMT, the third largest amount on record4. 2010 Plantings down sharply in U.S. due to poor weather and low prices– U.S. plantings estimated at 53.6 million acres, lowest since 1969/70– SRW plantings fall nearly 30% due to an extremely wet fall5. Prices surge due to Russian export ban, quality concerns– Russia bans wheat exports through 2010/11, exports fall from 18.6 MMT in 2009/10 to 4.0 MMT in 2010/11– Ukraine implements export quota through March 31, 2011– Persistent rainfall causes major concerns about quality in Australian crop6. World ending stocks fall 10% to 178 MMT, exporter supply falls 22% to 62 MMT7. 2011 U.S. winter wheat plantings up by 10%– 2011 winter wheat conditions remain poor due to dryness in the Great Plains8. Competition for acres intensifies; U.S. corn stocks at 15-year low– Environmental Protection Agency increases ethanol blend– Global corn demand reaches record 837 MMT

Source: US Wheat Associates

50

100

150

200

250

300

350

400

15%

20%

25%

30%

35%

40%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

USD

per

Ton

ne

Stoc

ks to

Use

Rat

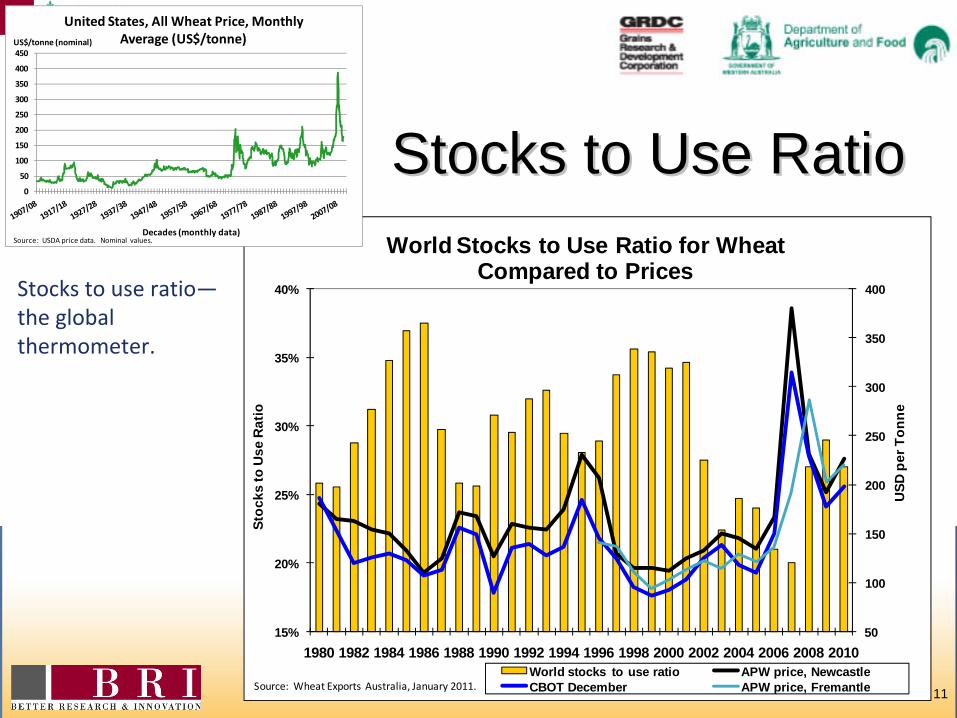

ioWorld Stocks to Use Ratio for Wheat

Compared to Prices

World stocks to use ratio APW price, NewcastleCBOT December APW price, FremantleSource: Wheat Exports Australia, January 2011.

Stocks to Use RatioStocks to Use Ratio

11

Stocks to use ratio—

the global

thermometer.

0

50

100

150

200

250

300

350

400

450

Decades (monthly data)

United States, All Wheat Price, Monthly Average (US$/tonne)US$/tonne (nominal)

Source: USDA price data. Nominal values.

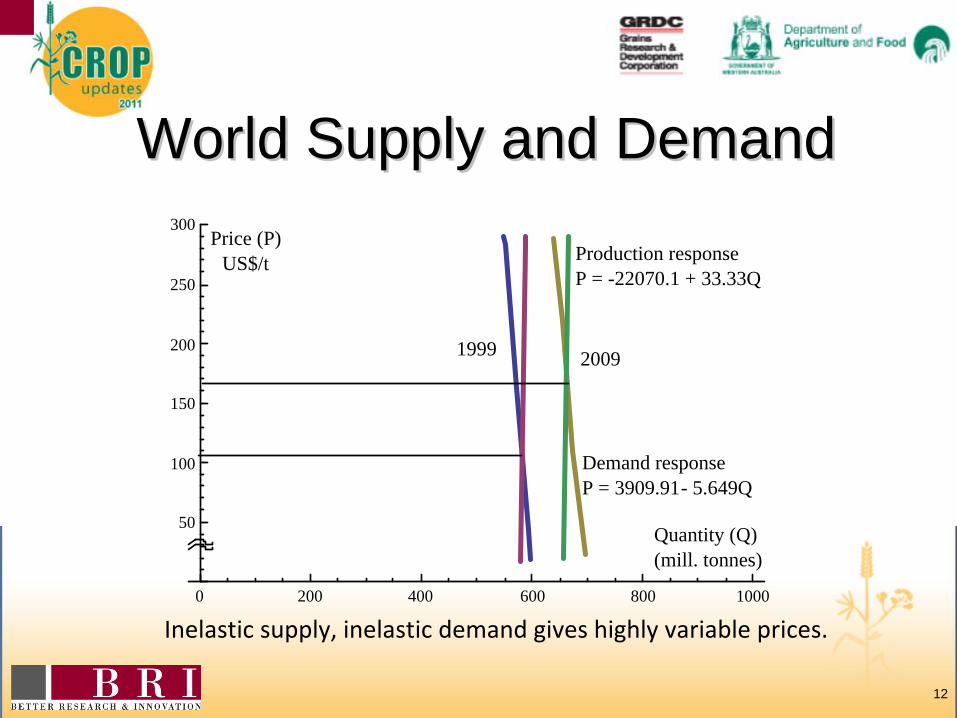

World Supply and DemandWorld Supply and Demand

12

Inelastic supply, inelastic demand gives highly variable prices.

Demand responseP = 3909.91- 5.649Q

Production responseP = -22070.1 + 33.33Q

1999 2009

Price (P) US$/t

Quantity (Q)(mill. tonnes)

0 200 400 600 800 1000

50

100

150

200

250

300

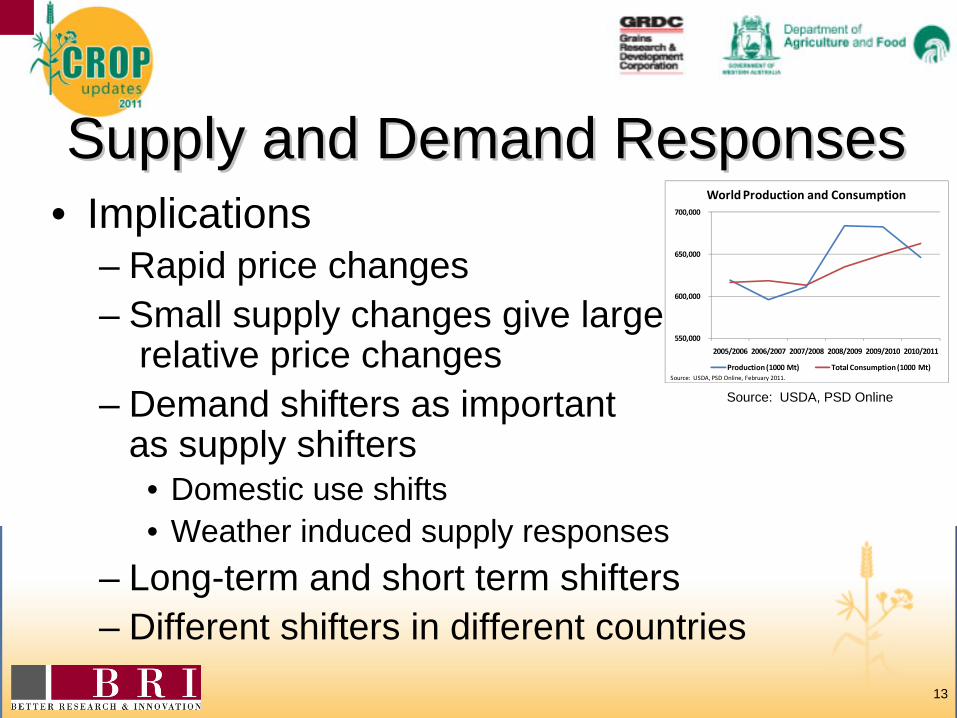

Supply and Demand ResponsesSupply and Demand Responses

13

• Implications– Rapid price changes– Small supply changes give large

relative price changes– Demand shifters as important

as supply shifters• Domestic use shifts• Weather induced supply responses

– Long-term and short term shifters– Different shifters in different countries

Source: USDA, PSD Online

550,000

600,000

650,000

700,000

2005/2006 2006/2007 2007/2008 2008/2009 2009/2010 2010/2011

World Production and Consumption

Production (1000 Mt) Total Consumption (1000 Mt)Source: USDA, PSD Online, February 2011.

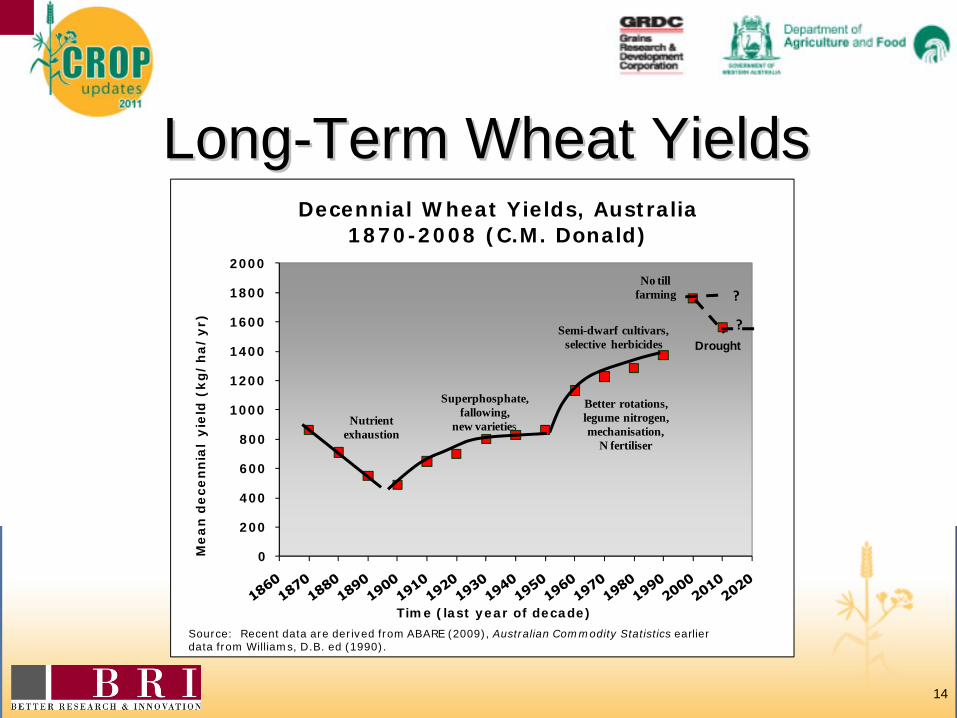

LongLong--Term Wheat YieldsTerm Wheat Yields

14

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Me

an

de

ce

nn

ial

yie

ld (

kg

/h

a/

yr)

Time (last year of decade)

Decennial Wheat Yields, Australia 1870-2008 (C.M. Donald)

Nutrient exhaustion

Superphosphate,fallowing,

new varieties

Better rotations, legume nitrogen, mechanisation,

N fertiliser

No tillfarming

Semi-dwarf cultivars, selective herbicides Drought

Source: Recent data are derived from ABARE (2009), Australian Commodity Statistics earlier data from Williams, D.B. ed (1990).

?

?

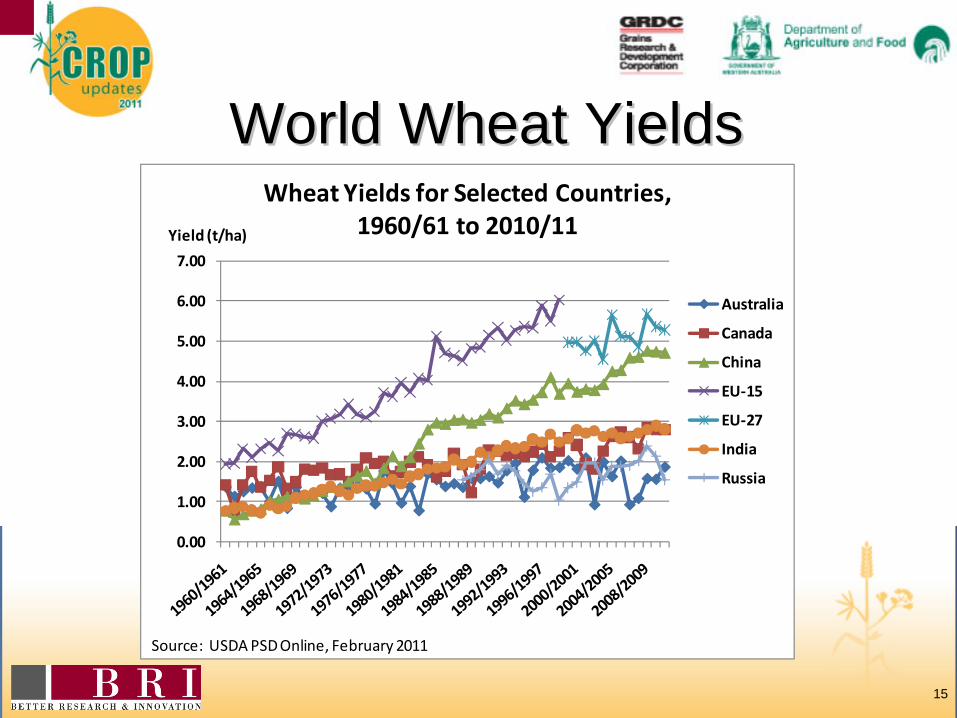

World Wheat YieldsWorld Wheat Yields

15

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Wheat Yields for Selected Countries, 1960/61 to 2010/11

Australia

Canada

China

EU‐15

EU‐27

India

Russia

Source: USDA PSD Online, February 2011

Yield (t/ha)

0

5,000

10,000

15,000

20,000

25,000

30,000

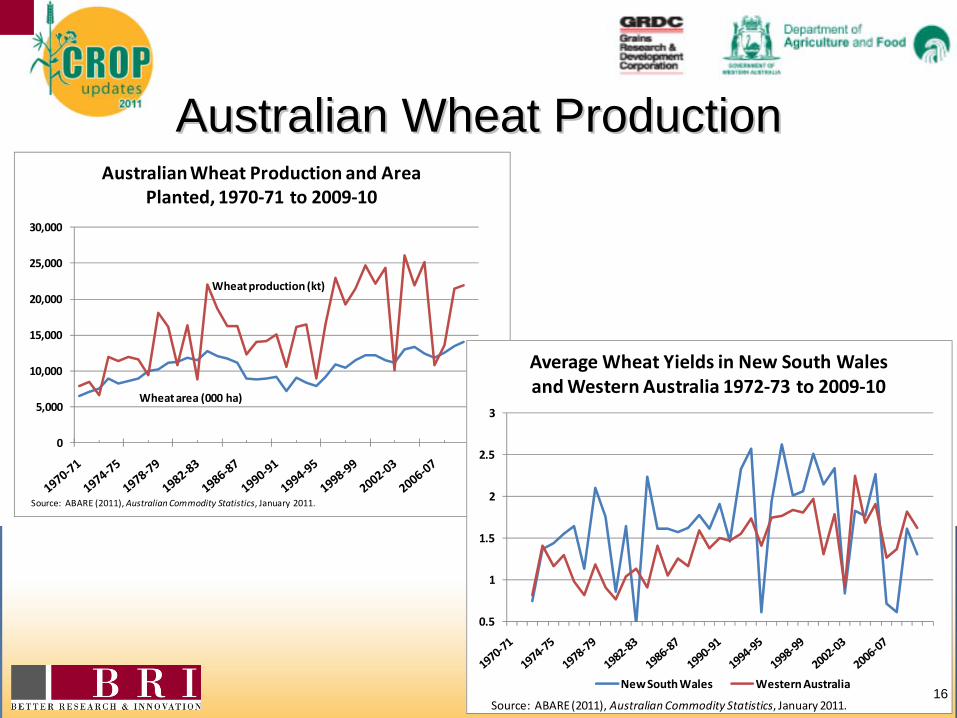

Australian Wheat Production and Area Planted, 1970‐71 to 2009‐10

Wheat production (kt)

Wheat area (000 ha)

Source: ABARE (2011), Australian Commodity Statistics, January 2011.

0.5

1

1.5

2

2.5

3

Average Wheat Yields in New South Wales and Western Australia 1972‐73 to 2009‐10

New South Wales Western Australia

Source: ABARE (2011), Australian Commodity Statistics, January 2011.

Australian Wheat ProductionAustralian Wheat Production

16

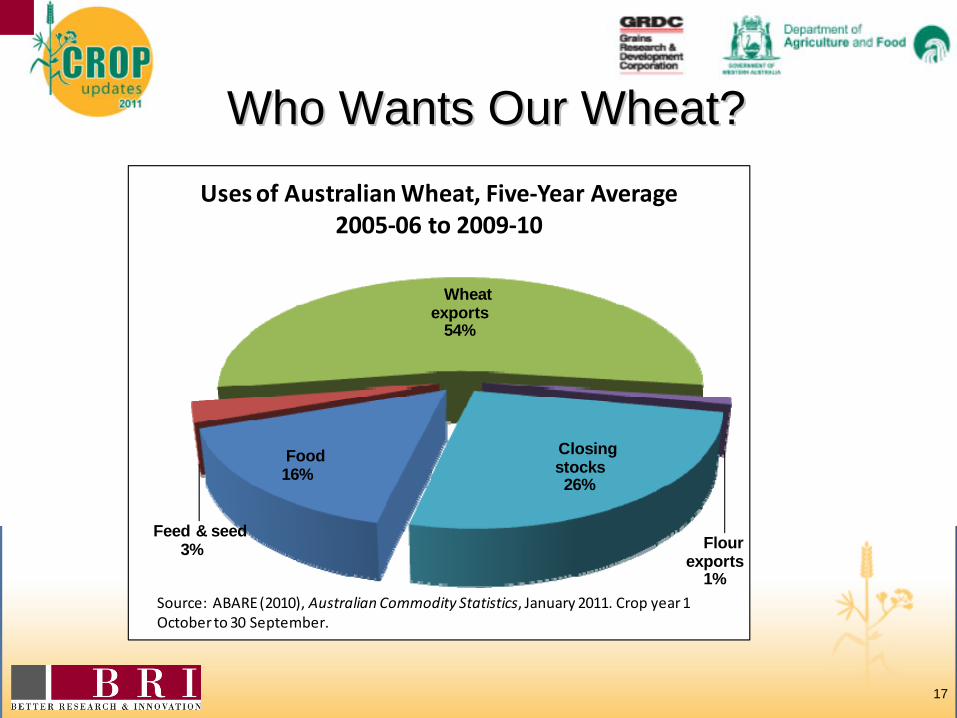

Who Wants Our Wheat?Who Wants Our Wheat?

17

Food16%

Feed & seed3%

Wheat exports

54%

Flour exports

1%

Closing stocks26%

Uses of Australian Wheat, Five‐Year Average 2005‐06 to 2009‐10

Source: ABARE (2010), Australian Commodity Statistics, January 2011. Crop year 1 October to 30 September.

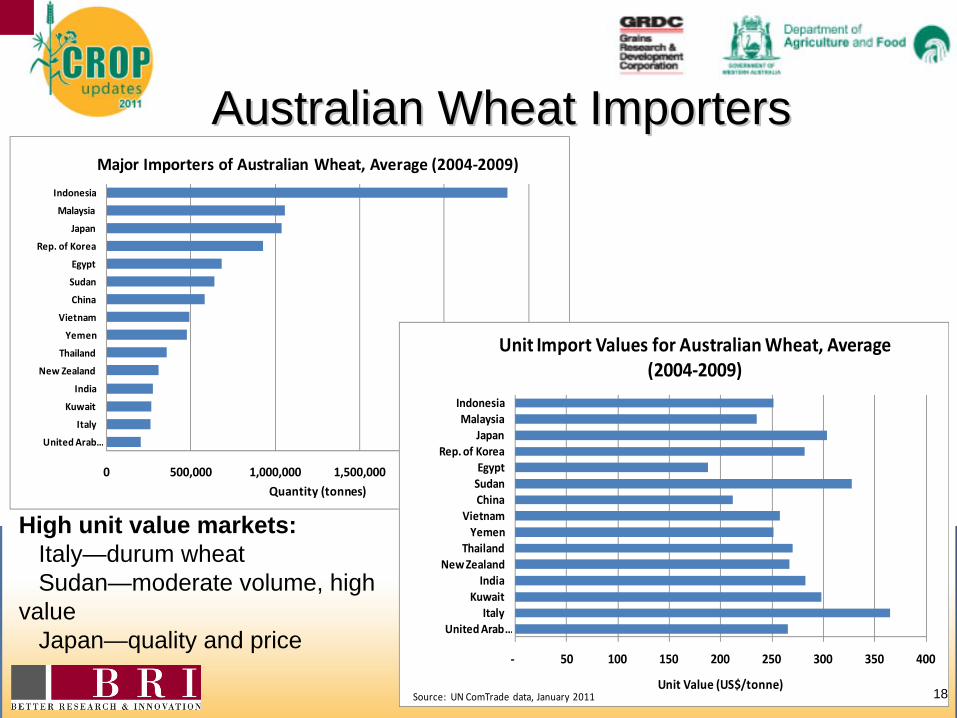

0 500,000 1,000,000 1,500,000 2,000,000 2,500,000

Indonesia

Malaysia

Japan

Rep. of Korea

Egypt

Sudan

China

Vietnam

Yemen

Thailand

New Zealand

India

Kuwait

Italy

United Arab …

Quantity (tonnes)

Major Importers of Australian Wheat, Average (2004‐2009)

‐ 50 100 150 200 250 300 350 400

IndonesiaMalaysia

JapanRep. of Korea

EgyptSudanChina

VietnamYemen

ThailandNew Zealand

IndiaKuwait

ItalyUnited Arab …

Unit Value (US$/tonne)

Unit Import Values for Australian Wheat, Average (2004‐2009)

Source: UN ComTrade data, January 2011

Australian Wheat ImportersAustralian Wheat Importers

18

High unit value markets:Italy—durum wheatSudan—moderate volume, high

valueJapan—quality and price

0

50

100

150

200

250

300

350

400

'000

tonn

es

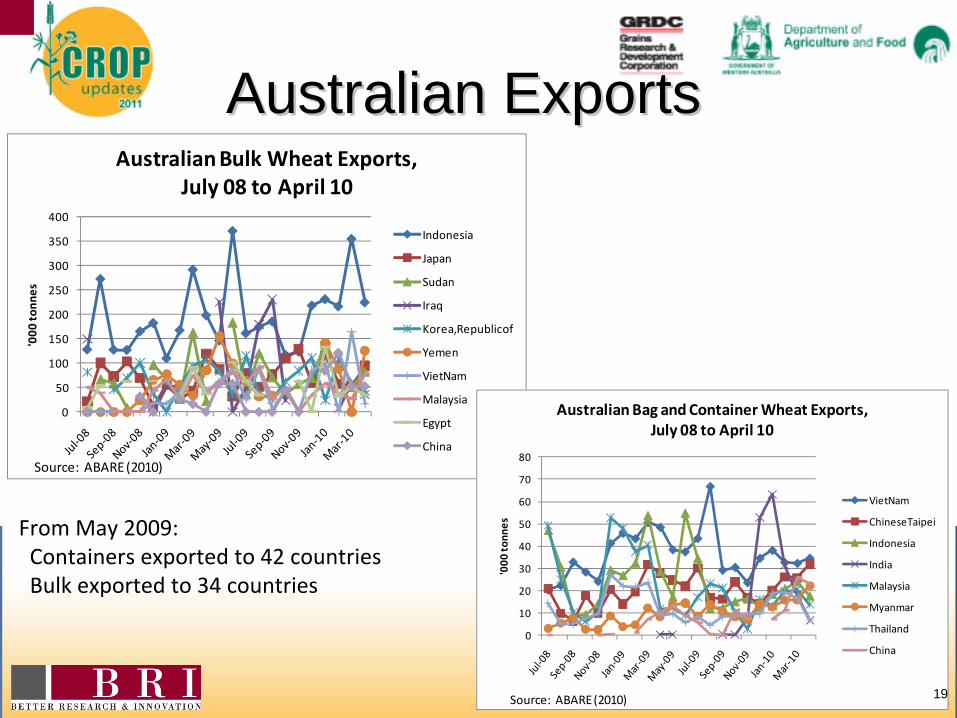

Australian Bulk Wheat Exports, July 08 to April 10

Indonesia

Japan

Sudan

Iraq

Korea,Republicof

Yemen

VietNam

Malaysia

Egypt

China

Source: ABARE (2010)

0

10

20

30

40

50

60

70

80

'000

tonn

es

Australian Bag and Container Wheat Exports, July 08 to April 10

VietNam

ChineseTaipei

Indonesia

India

Malaysia

Myanmar

Thailand

China

Source: ABARE (2010)

Australian ExportsAustralian Exports

19

From May 2009:Containers exported to 42 countriesBulk exported to 34 countries

Australian Bulk Exports by GradeAustralian Bulk Exports by Grade

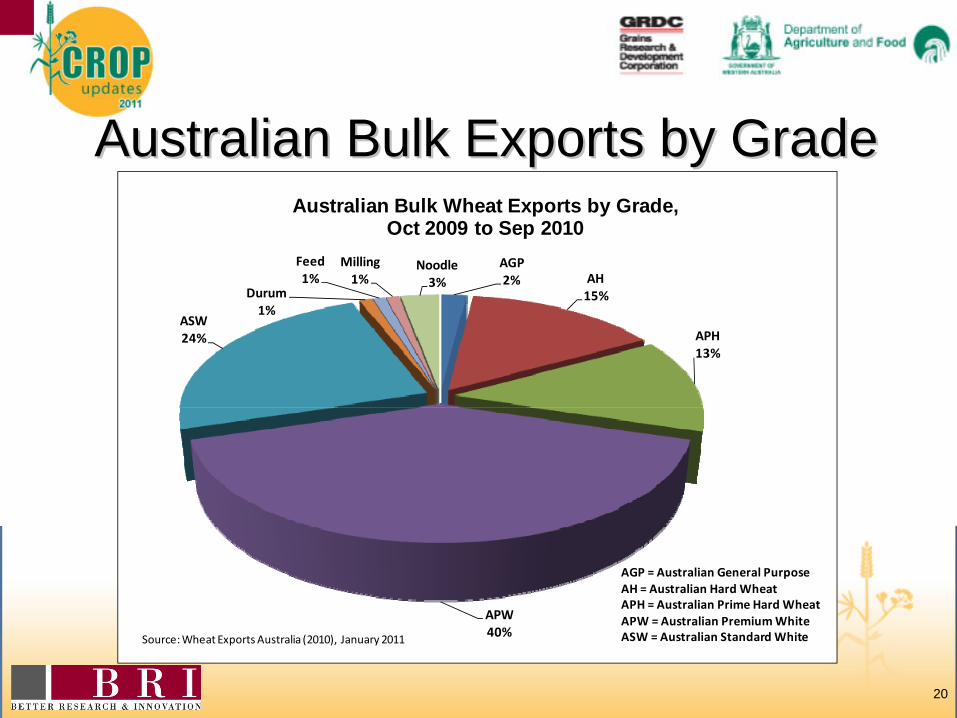

20

AGP2% AH

15%

APH13%

APW40%

ASW24%

Durum1%

Feed1%

Milling1%

Noodle3%

Australian Bulk Wheat Exports by Grade, Oct 2009 to Sep 2010

Source:Wheat Exports Australia (2010), January 2011

AGP = Australian General PurposeAH = Australian Hard WheatAPH = Australian Prime Hard WheatAPW = Australian Premium WhiteASW = Australian Standard White

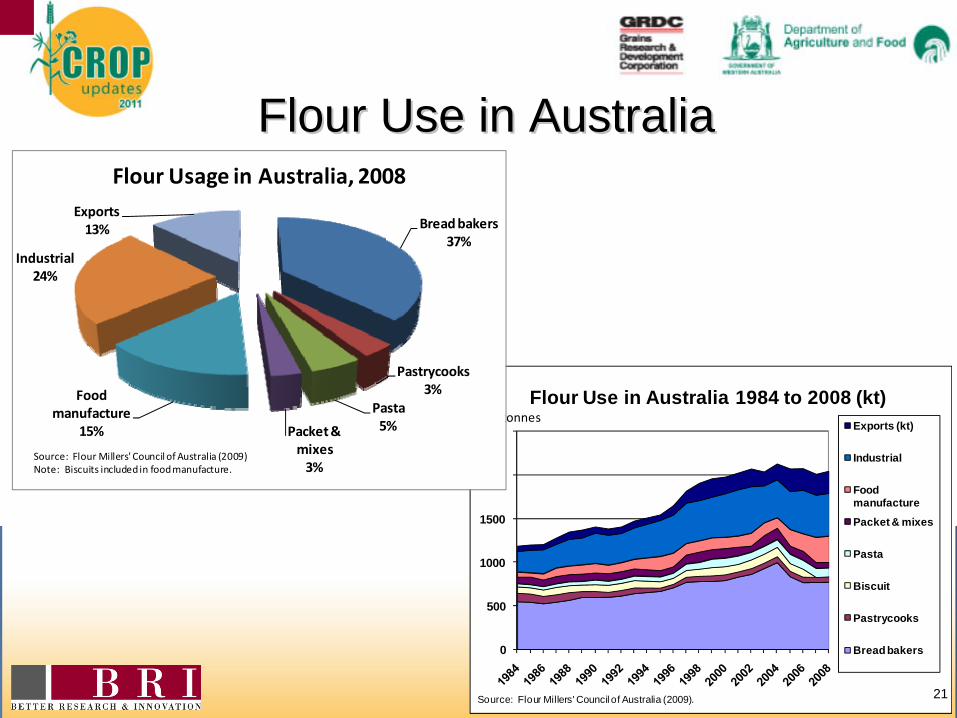

0

500

1000

1500

2000

2500

Flour Use in Australia 1984 to 2008 (kt)Exports (kt)

Industrial

Food manufacture

Packet & mixes

Pasta

Biscuit

Pastrycooks

Bread bakers

Source: Flour Millers' Council of Australia (2009).

000 tonnes

Flour Use in AustraliaFlour Use in Australia

21

Bread bakers37%

Pastrycooks3%

Pasta 5%Packet &

mixes3%

Food manufacture

15%

Industrial24%

Exports13%

Flour Usage in Australia, 2008

Source: Flour Millers' Council of Australia (2009)Note: Biscuits included in food manufacture.

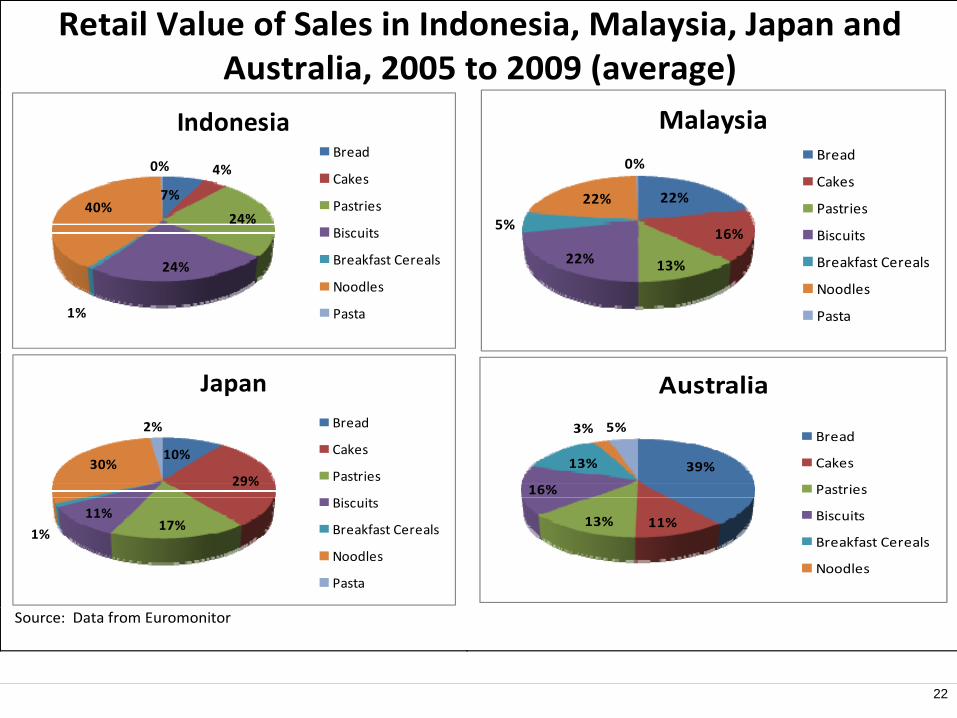

Retail Value of Sales in Indonesia, Malaysia, Japan and Australia, 2005 to 2009 (average)

7%

4%

24%

24%

1%

40%

0%

IndonesiaBread

Cakes

Pastries

Biscuits

Breakfast Cereals

Noodles

Pasta

22%

16%

13%22%

5%

22%

0%

MalaysiaBread

Cakes

Pastries

Biscuits

Breakfast Cereals

Noodles

Pasta

10%

29%

17%11%

1%

30%

2%

JapanBread

Cakes

Pastries

Biscuits

Breakfast Cereals

Noodles

Pasta

39%

11%13%

16%

13%

3% 5%

Australia

Bread

Cakes

Pastries

Biscuits

Breakfast Cereals

Noodles

Source: Data from Euromonitor

22

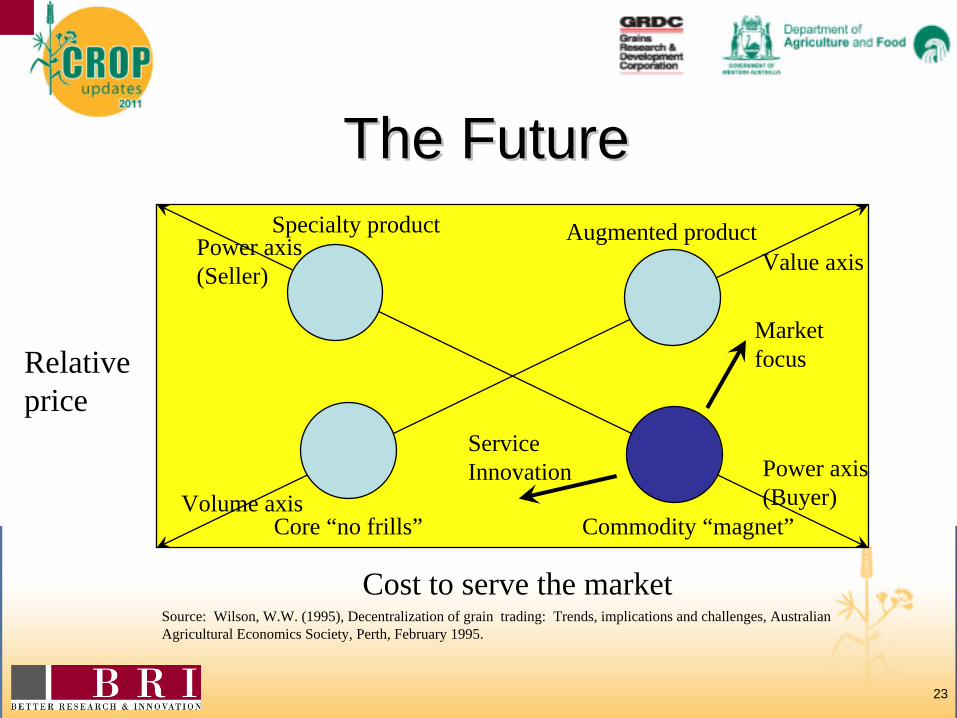

The FutureThe Future

23

Relative price

Source: Wilson, W.W. (1995), Decentralization of grain trading: Trends, implications and challenges, Australian Agricultural Economics Society, Perth, February 1995.

Cost to serve the market

Specialty product Augmented product

Core “no frills” Commodity “magnet”

Marketfocus

ServiceInnovation

Power axis(Seller)

Volume axisPower axis(Buyer)

Value axis

Market TypesMarket Types

24

• Market types– Specialty—high price, low cost to serve– Commodity—low price, high cost to serve

• Give away services to maintain market share

• Market Dynamics– Commodity ‘magnet’ pull

• Market focus—move toward the value axis– Seller power through differentiation

• Segment customers willing to pay for product characteristics– Service innovation strategy

• Products and services unbundled—reduce customer costs

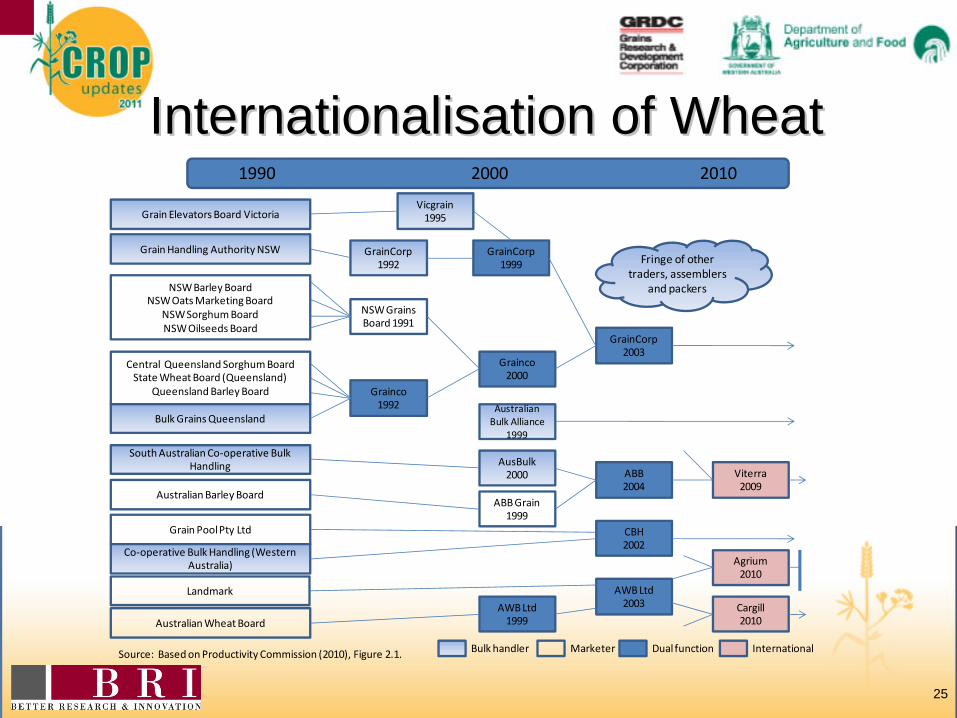

Internationalisation of WheatInternationalisation of Wheat

25

1990 2000 2010

Grain Elevators Board Victoria

Grain Handling Authority NSW

NSW Barley BoardNSW Oats Marketing Board

NSW Sorghum BoardNSW Oilseeds Board

Central Queensland Sorghum BoardState Wheat Board (Queensland)

Queensland Barley Board

Bulk Grains Queensland

South Australian Co‐operative Bulk Handling

Australian Barley Board

Grain Pool Pty Ltd

Co‐operative Bulk Handling (Western Australia)

Australian Wheat Board

GrainCorp1992

GrainCorp1999

GrainCorp2003

Grainco2000

NSW Grains Board 1991

Grainco1992

Vicgrain1995

Australian Bulk Alliance

1999

AusBulk2000

ABB Grain 1999

ABB2004

Viterra2009

CBH 2002

AWB Ltd1999

Cargill2010

Fringe of other traders, assemblers

and packers

Source: Based on Productivity Commission (2010), Figure 2.1. Bulk handler Marketer Dual function

AWB Ltd2003

Landmark

Agrium2010

International

Internationalisation of WheatInternationalisation of Wheat

26

• From export monopoly to oligopoly (few firms)– Economies of scale and scope– International scale firms– Extraction of oligopoly rents (market power)

• Role of the competitive fringe– Frequent entry and exit – Innovative and product differentiate– Keep pressure on oligopoly rents

SummarySummary

27

• World wheat industry is large, complex and risky

• Black Sea Ports are serious competition• Supply and demand are inelastic—price

‘spikes’• Indonesia our largest market• Baking sector is the largest end-use sector• Quality versus yield—consistency required• Production differentiation

– helps both customers and producers

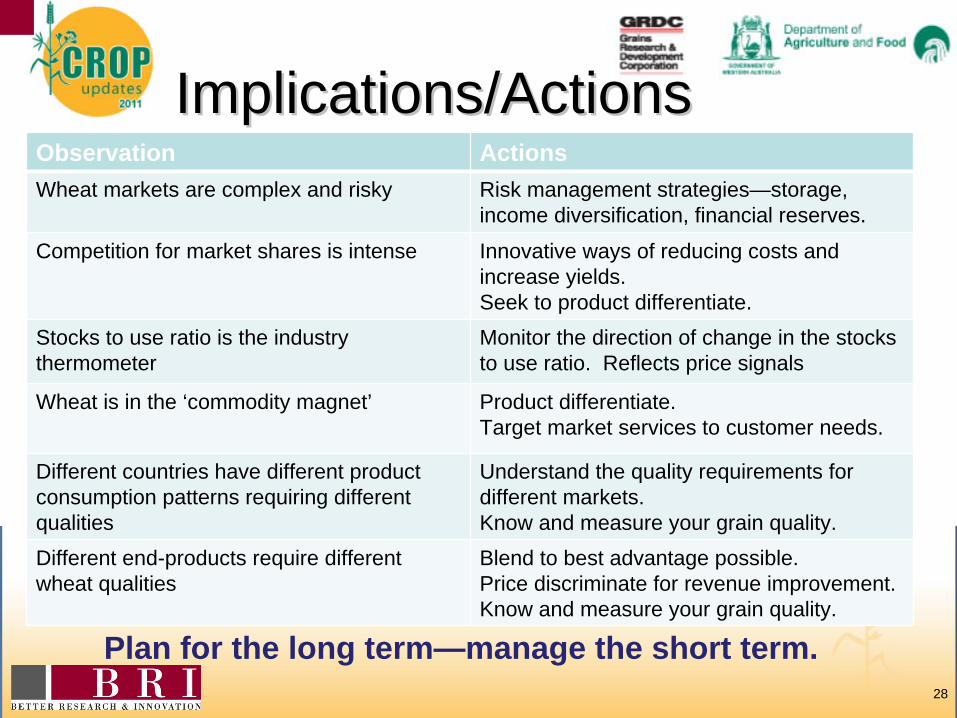

Implications/ActionsImplications/Actions

28

Observation ActionsWheat markets are complex and risky Risk management strategies—storage,

income diversification, financial reserves.

Competition for market shares is intense Innovative ways of reducing costs and increase yields.Seek to product differentiate.

Stocks to use ratio is the industry thermometer

Monitor the direction of change in the stocks to use ratio. Reflects price signals

Wheat is in the ‘commodity magnet’ Product differentiate.Target market services to customer needs.

Different countries have different product consumption patterns requiring different qualities

Understand the quality requirements for different markets.Know and measure your grain quality.

Different end-products require different wheat qualities

Blend to best advantage possible.Price discriminate for revenue improvement.Know and measure your grain quality.

Plan for the long term—manage the short term.

Work on “What the World Wants from Australian Wheat” is a jointly funded project of the

Grain Growers Association and the Department of Agriculture, Fisheries and Forestry.

29

Thank YouThank You

More information can be found at http://www.graingrowers.com.au/

by downloading “What the World Wants from Australian Wheat: Update 2010.”

Thank YouThank You