18

Building Profitable Relationships with Multichannel Consumers February 2011

| Date post: | 14-Jul-2015 |

| Category: |

Economy & Finance |

| Upload: | paul-mcadam |

| View: | 376 times |

| Download: | 1 times |

Building Profitable Relationships with Multichannel Consumers February 2011

The days of barbell profitability in retail banking are ending

Fee Income Spread Income

- 1 2 3 4 5 6 7 8 9 10

The forgotten 80%

The small pool of high-end customers and extreme NSF-paying customers

will no longer subsidize the mass market Fee Income Spread Income

Illustrative Customer Profitability Deciles

Channel Rationalization

Fee Income Generation

Wallet Consolidation

Reduce branch network operating expense while increasing investments in self-service delivery channels

Make up for lost NSF and debit card interchange revenues by increasing fee pricing

Encourage consumers to consolidate deposit, payment and credit relationships

2

Channel Rationalization Online banking, bank-owned ATMs and branches are used most frequently

3 n = 1,808 Source: FIS Enterprise Strategy, September 2010

Percent of consumers reporting use of each channel in the past 30 days

3

30%

33%

35%

47%

65%

67%

75%

Automated phone/IVR

Live phone rep

Foreign ATM

Debit card cash back at POS

Branch lobby transaction

Bank owned ATM

Online Banking

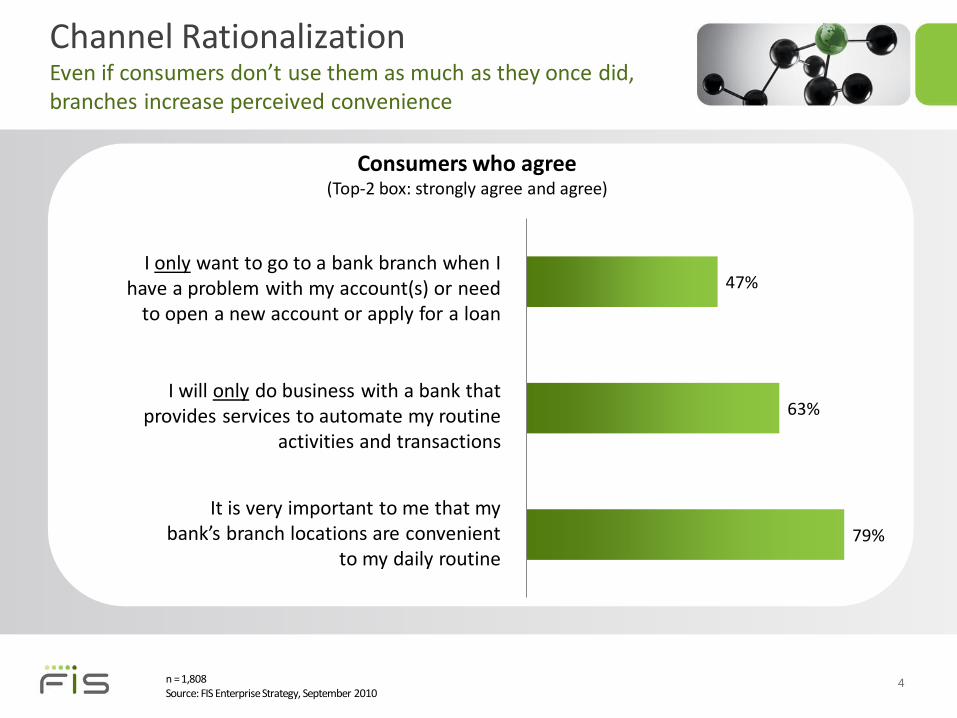

Channel Rationalization Even if consumers don’t use them as much as they once did, branches increase perceived convenience

Consumers who agree (Top-2 box: strongly agree and agree)

n = 1,808 Source: FIS Enterprise Strategy, September 2010

47%

63%

79%

It is very important to me that my bank’s branch locations are convenient

to my daily routine

I will only do business with a bank that provides services to automate my routine

activities and transactions

I only want to go to a bank branch when I have a problem with my account(s) or need

to open a new account or apply for a loan

4

In-person 23%

Mixed

Channel 57%

Self-service 20%

Channel Rationalization The majority of consumers are multi-channel and use a mix of in-person and self-service banking channels

n = 1,808 Source: FIS Enterprise Strategy, September 2010

Heavily In-person customers

• Conducted primarily in-person branch or telephone transactions

• Conducted no online or mobile interactions in past 30 days

• May use the ATM

Heavily Self-service customers

• Used only online, mobile and remote channel transactions

• Conducted no in-person branch transactions or phone calls to live service reps in past 30 days

• Used the ATM

Multi-channel customers

• Have used both in-person and online/self-service channels within the past 30 days

• Used ATM

5

Channel Rationalization The majority of consumers use 2 – 4 banking channels

n = 1,808 Source: FIS Enterprise Strategy, September 2010

4%

13%

22% 22%

17%

10%

4% 3%

7%

0 1 2 3 4 5 6 7 8

Number of channels used in past 30 days The eight channels included in this analysis

• Branch

• Bank-owned ATM

• Foreign ATM

• Call to live phone rep

• Call to automated phone/IVR

• Online banking

• Mobile banking

• Remote deposit of check with mobile phone

6

0%

5%

10%

15%

20%

25%

30%

0 1 2 3 4 5 6 7 8

Gen Y

Gen X

Baby Boomers

Mature

n = 1,808 Source: FIS Enterprise Strategy, September 2010

Number of channels used in past 30 days by generation

More than five channels used in the past 30 days

41%

28%

15%

9%

More than five channels

7

Channel Rationalization Younger generations (especially Gen Y) are driving the increase in number of channels used

n = 1,808 Source: FIS Enterprise Strategy, September 2010

3.8

3.1

2.4

2.5

18.1 *

15.5

9.6

7.6

Gen Y

Gen X

Baby Boomers

Mature

Average number of transactions/interactions in past 30 days

In Person

Self Service

Percent of transactions/

interactions that are in-person

17%

17%

20%

25%

8

Channel Rationalization Younger generations fuel the growth of self-service channels, but still heavily use in-person channels

Fee Income Generation Consumers have been trained not to expect to pay monthly fees

n = 1,808 Source: FIS Enterprise Strategy, September 2010

20%

82%

Consumers who agree (top-2 box: strongly agree/agree)

I believe the fees that banks charge for their services are fair

I do not expect to pay any fees for my checking account

Large National

Bank Customers

Regional Bank

Customers

Community Bank

Customers Credit Union

Members

I do not expect to pay any fees for my checking account 80% 88% 81% 83%

I believe that the fees banks charge for their services are fair 19% 19% 27% 19%

9

n = 1,808 Source: FIS Enterprise Strategy, September 2010

3%

3%

3%

9%

35%

42%

$30.00 or more

$20.00 - $29.99

$10.00 - $19.99

$5.00 - $9.99

Less than $5.00

I don’t pay any fees

Amount of fees for primary checking account in typical month

18%

Fees paid include:

• Monthly maintenance

• ATM

• Transaction or per-item fees

• NSF/OD

• Other

10

Fee Income Generation Most consumers pay minimal (if any) fees for their primary checking account

n = 1,808 Source: FIS Enterprise Strategy, September 2010

17%

23%

27%

33%

$10.00 or more

$5.00 - $9.99

$1.00 to $4.99

Less than $1.00

Amount of monthly fee increase that could motivate switching consideration

40%

60%

11

Fee Income Generation Even a modest monthly fee increase could motivate switching consideration among a majority of consumers

Wallet Consolidation Consumers are willing to consolidate their bank products and services to benefit from one-stop shopping

n = 1,808 Source: FIS Enterprise Strategy, September 2010

54%

56%

60%

71%

Strongly Agree/Agree (Top-2 Box)

I am willing to consolidate all of my money with one financial institution as long as it can provide all the

products and services I need

I would trust my bank for all my financial needs

I would be very interested in having all of my bank accounts, from checking accounts to loans to

investment products, all from one financial institution

I would consider moving all or most of my bank accounts to a financial institution that rewards me

for the amount of business I conduct with them

12

Source: FIS Enterprise Strategy, September 2010

14% Neither Likely

or Unlikely

2% Not too likely

2% Not at all likely

Likelihood of Bringing More Business to Current Provider to Avoid Fees

35%

Very Likely

48%

Somewhat

Likely

7%

11%

13%

28%

41%

$25,000 or more

$10,000 to $24,999

$5,000 to $9,999

$1,000 to $4,999

Less than $1,000

Deposit Balances Could Consolidate to Avoid Fees

(among those very/somewhat likely)

18%

n = 1,808 n = 1,396

13

Wallet Consolidation Although consumers are motivated to consolidate, only a small portion can bring meaningful deposit balances

Wallet Consolidation There is substantial opportunity for the primary checking account provider to gain wallet share

Where product relationships reside (for those consumers who own the product)

68%

51% 51%

35% 26%

51%

35% 33% 28%

23%

18%

14% 11%

4%

5%

3%

21%

2% 3%

2%

14%

35% 39%

60% 69%

46% 44%

65% 69% 75%

Savings CD MoneyMarketAccount

MoneyMarket

Mutual Fund

IRA HomeEquityLoan

CreditCard

Mortgage AutoLoan

StudentLoan

Own product withanother financialinstitution

Own product withprimary checkingaccount providerand another FI

Own product withprimary checkingaccount provider

n = 1,808 Source: FIS Enterprise Strategy, September 2010 14

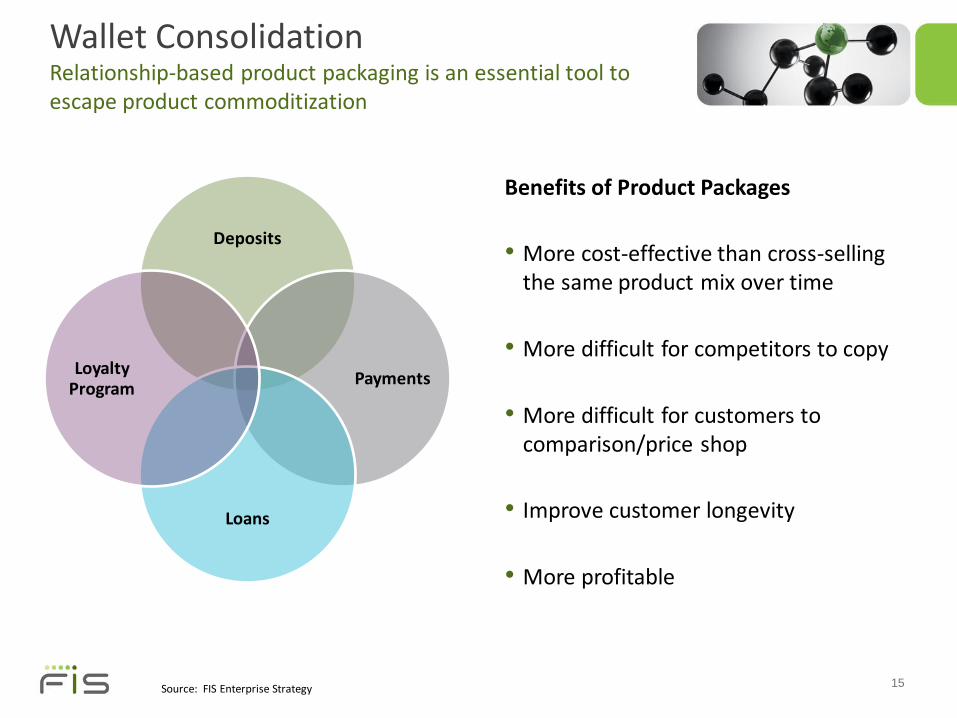

Wallet Consolidation Relationship-based product packaging is an essential tool to escape product commoditization

Deposits

Payments

Loans

Loyalty Program

Source: FIS Enterprise Strategy

Benefits of Product Packages

• More cost-effective than cross-selling the same product mix over time

• More difficult for competitors to copy

• More difficult for customers to comparison/price shop

• Improve customer longevity

• More profitable

15

Wallet Consolidation Several variables can be configured to optimize a package’s profitability and customer appeal

Source: FIS Enterprise Strategy 16

Monthly maintenance fees

Minimum balance threshold

Consumer credit included in package

Consumer assets included in package

“Free” channel access included in package

Loyalty program benefits

High

Low

Short-term credit (e.g., credit card)

Short term assets (e.g., deposits)

Self service only

None or modest

Low or none

High

Long-term credit (e.g., mortgages)

Long-term assets (e.g., investments)

All channels

Significant & relationship based

Mass-market Package Relationship Package

Wallet Consolidation Matching logical consumer segments with packaged opportunities will optimize revenue

Source: FIS Enterprise Strategy 17

Age

Saving Families

Borrowing

Families Students &

Gen Y

Upwardly

Mobile

Gen X &Y Mature Bank Loyalists

Inc

om

e /

We

alt

h

Self-directed Mass Affluent

Survivors

Young, Tech Savvy

Account

~ 25% of population

Prepaid Debit

Account

~ 10% of population

Mass Market,

Loyalty Account

~ 40% of population

Retirement Income

Account

~ 10% of population

Tech Savvy, Emerging

Affluent Account

~ 15% of population

Contact information

FIS delivers banking and payments technologies to more than 14,000 financial institutions and businesses in over 100 countries worldwide. FIS provides financial institution core processing, and card issuer and transaction processing services, including the NYCE® Network. FIS maintains processing and technology relationships with 40 of the top 50 global banks, including 9 of the top 10. FIS is a member of Standard and Poor's (S&P) 500® Index and consistently holds a leading ranking in the annual FinTech 100 rankings. Headquartered in Jacksonville, Florida, FIS employs more than 30,000 on a global basis. FIS is listed on the New York Stock Exchange under the “FIS” ticker symbol. For more information about FIS see www.fisglobal.com.

This research was conducted by FIS Research and Thought Leadership, a key function of FIS’ Enterprise Strategy department. The FIS Research & Thought Leadership team proactively manages market and client perceptions of FIS as a thought-leader and thought-partner by conducting high-quality primary research on critical industry issues and delivering interpretation and recommendations to client organizations.

The research team for this project include:

Paul McAdam Mandy Putnam Senior Vice President Director Ph: 708-449-7742 Ph: 614-414-4207 [email protected] [email protected] James Gamble Chris Nay Director Senior Strategic Researcher Ph: 614-414-4213 Ph: 614-414-4218 [email protected] [email protected]

18