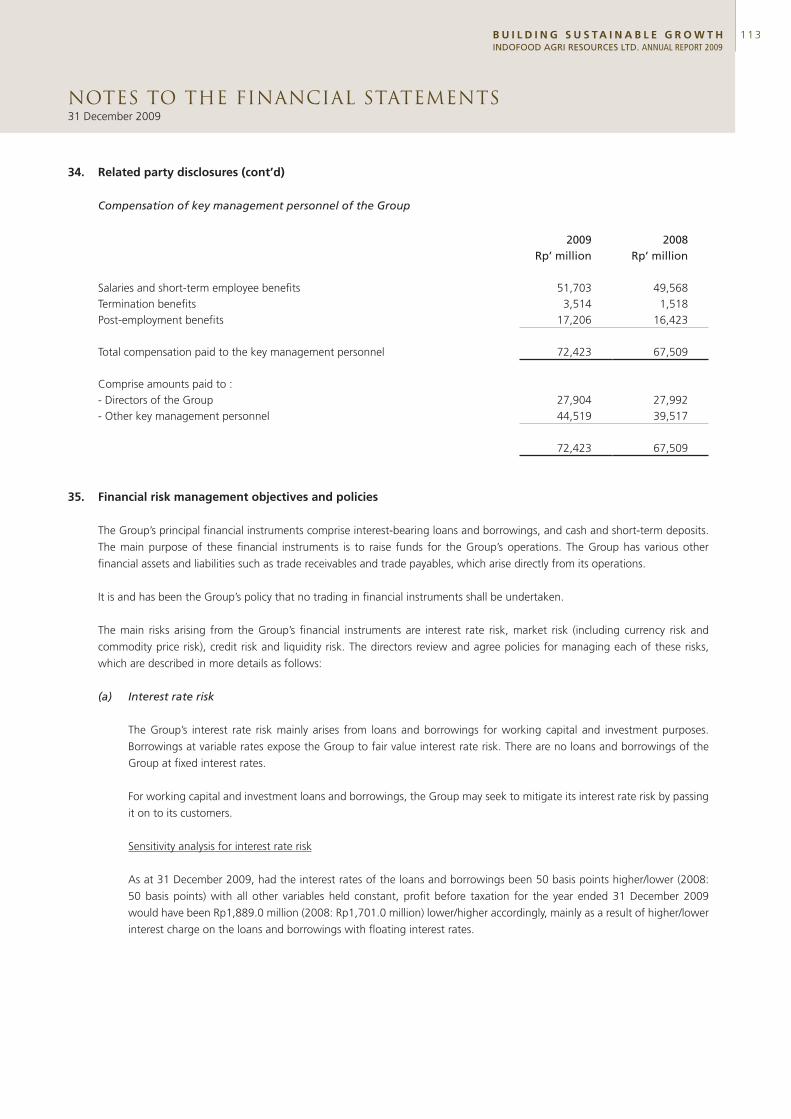

144

INDOFOOD AGRI RESOURCES LTD. | Annual Report 2009 Building Sustainable Growth

INDOFOOD AGRI RESOURCES LTD. | Annual Report 2009

BuildingSustainableGrowth

Mission

1. To be a low-cost producer, through high yields and

cost-effective and effi cient operations

2 To continuously improve our people, processes

and technology

3. Exceed our customers’ expectations, whilst

ensuring the highest standards of quality

4. Recognise our role as responsible and

engaged corporate citizens in all our

business operations, including sustainable

environmental and social practices

5. To continuously increase stakeholders’ value

Values

1. CONSISTENT

2. Our Success Rests On Satisfying CUSTOMERS’ Needs

3. INNOVATION Is Our Key To Future Growth

4. Reliable STAFF Is Our Biggest Asset

5. EXCELLENCE Is Our Way Of Life

6. TEAMWORK Makes A Winning Team

Vision

To Become a Leading Integrated

Agribusiness, and one of the world-

class agricultural research and seed

breeding Companies.

At a Glance Indofood Agri Resources Ltd (“IndoAgri”) is a vertically

integrated agribusiness group with activities spanning the entire

supply chain from research and development, seed breeding,

oil palm cultivation and milling; as well as the production

and marketing of cooking oil and margarine. Headquartered

in Jakarta, we are among the largest palm oil producers in

Indonesia. Our branded cooking oil, shortening and margarine

products garner a leading share in the domestic market. As a

diversified agribusiness group, IndoAgri also engages in the

cultivation of sugar cane, rubber and other crops.

Staff force of more than 29,000 people

Over 500,000 hectares of land bank with over 220,000 hectares planted

Leading market position in Indonesia, with renowned brands of cooking oil and margarine

01 At A Glance

02 Milestones

04 Key Events in 2009

05 Corporate Structure

06 Location Map

10 Chairman’s Statement

11 CEO’s Statement

14 Business Overview

16 Financial Highlights

17 Operational Highlights

20 Operations Review

31 Manufacturing Process

32 Environment & Corporate Social Responsibility

36 Board of Directors

40 Corporate Information

41 Corporate Governance

50 Financial Statements

126 Interested Person Transactions

127 Estates Location

129 Statistics of Shareholdings

131 Notice of Annual General Meeting

CONTENTS

0 1B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

Diversifi ed into sugar business via the

subscription of 60%-stake in PT Laju

Perdana Indah.

Entered into a joint venture with

Ghanian Council for Scientifi c and

Industrial Research to develop and

realize the genetic potential of oil palm

for commercial production.

Achieved the world’s fi rst patent to

produce F1 oil palm hybrid seeds.

Acquired plantation land bank of 82,300

hectares in South Sumatra and Central

Kalimantan, Indonesia.

Acquired a bulking facility at the Dumai

port, Indonesia.

2007

2008

Completed a reverse takeover

of CityAxis Holdings Limited in

January and changed name to

Indofood Agri Resources Ltd.

Listed on the main board of the SGX-ST

on 14 February and raised S$420 million

proceeds from the placement of 338 million

new shares.

Acquired plantation land bank of 98,491

hectares in South Sumatra

and Kalimantan.

Acquired a 58.8% effective interest in

Lonsum, becoming one of the largest

plantation companies in Indonesia with land

bank doubling to over 400,000 hectares.

n

ooo

2007

0 2

MILESTONESSINCE LISTING IN FEBRUARY 2007, INDOAGRI

ACHIEVED RESPECTABLE GROWTH IN ITS PLANTED

AREA AND PRODUCTION VOLUME. ITS NORTH

SUMATRA OIl PALM ESTATES AND MILLS ARE NOW

CERTIFIED AS SUSTAINABLE UNDER RSPO.

2009

Achieved the Roundtable on Sustainable

Palm Oil (RSPO) certifi cation for its North

Sumatra estates and factories.

Raised Rp730 billion or approximately

US$78 million from 5-year Indonesian

Rupiah Bonds and Islamic

Lease-based Bonds.

Acquired plantation land bank of 10,000 hectares

in South Sumatra, Indonesia.

Incorporated a new subsidiary to own barges,

tugboats and operation of shipping logistics

business.

B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

0 3

KEY EVENTS IN 2009

ACHIEVED RSPO CERTIFICATION, EXPANSION OF LAND BANK AND PLANTED AREA, STRENGTHENED CAPITAL STRUCTURE.

2009

17 February PT SIMP increased its shareholding interest in PT Sarana Inti Pratama (PT SAIN) and PT Mitra Inti Sejati Plantation (PT MISP) from 70.02% and 70% respectively to 100%.

The acquisition of minority interest in PT MISP is in line with the Group’s strategy to enhance its integrated agribusiness model and to improve operating effi ciency and execution effectiveness.

The acquisition of the minority stake in PT SAIN is in line with IndoAgri’s strategy to merge the seeds business and breeding expertise of PT SIMP and Lonsum to achieve greater value and higher yields through seed breeding, best-practice agronomy and crop protection.

12 June PT SIMP, our 90%-owned subsidiary, incorporated a wholly-owned subsidiary – PT Samudera Sejahtera Pratama (PT SSP) in Jakarta. The principle activity of the new subsidiary is to own barges, tugboats and operation of shipping logistics business.

The incorporation of PT SSP is in line with IndoAgri’s strategy to have an integrated supply chain and reducing our reliance on external parties for the shipment of CPO from the tank farms located at the port of Dumai and Rengat in the province of Riau, Indonesia to our refi neries at Jakarta and Surabaya.

18 June PT PP London Sumatra Indonesia Tbk (“Lonsum”) attained the Roundtable on Sustainable Palm Oil (RSPO) certifi cation for sustainable palm oil for its North Sumatra estates and factories. The RSPO certifi cation covers approximately 20% of the Group’s annual palm oil production.

13 July As part of the Group’s effort to optimise its capital structure and enhance its fi nancial position, PT SIMP announced its intention to consider the issuance of 5-year Indonesian Rupiah Bonds up to Rp1.0 trillion to refi nance its existing borrowings.

14 August IndoAgri’s subsidiaries, PT Serikat Putra and PT Indoagri Inti Plantation acquired 100% interest of PT Intimegah Bestari Pertiwi (“PT IBP”), adding a total of land bank of 10,000 hectares in South Sumatra, Indonesia. This acquisition was completed on 12 October 2009.

20 November PT SIMP raised Rp452 billion and Rp278 billion (total aggregate of Rp730 billion or approximately US$78 million) from 5-year Indonesian Rupiah Bonds and Islamic Lease-based Bonds respectively, with a coupon rate of 11.65%. The bonds were listed in the Indonesia Stock Exchange on 2 Dec 2009.

0 4

CORPORATE STRUCTURE

0 5B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

83.8%

69.4%

100.0%

90.0%

56.4%

8.4%

8.0%

INDOFOOD SINGAPOREHOLDINGS PTE LTD

INDOFOOD OIL & FATS PTE LTD

PT SALIM IVOMAS PRATAMA

5656.4.4%%

30.6%

PUBLIC

LOCATION MAP

OUR PLANTATIONS AND REFINERIESIndoAgri owns strategically located plantations and production facilities across the

Indonesia archipelago. We have over 500,000 hectares of land bank, largely located in

Sumatra and Kalimantan, of which over 220,000 hectares are planted. Oil palm is our

dominant crop, followed by rubber, sugar cane, cocoa and tea. On the downstream,

our refineries are strategically located at major cities in Jakarta, Surabaya, Medan

and Bitung.

S U M A T R AS I N G A P O R E

M A L A Y S I A

J A V A

Medan

Palembang

Jakarta

Pekanbaru Pontianak

0 6

Our workers gather for routine briefi ngs at the start of each day.

K A L I M A N T A N

S U L A W E S I

N O R T HM A L U K U

Surabaya

Samarinda

TOBELO

Makassar

Muotong

Bitung

Town / City

Oil Palm

Sugar Cane

Rubber

Cocoa

Tea

Refinery

Copra Mill

LEGEND

0 7B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

8

WE CONTINUE TO EXPAND OUR OIL PALM ACREAGE

CHAIRMAN’S STATEMENT

Dear Shareholders,

In the short time since IndoAgri’s listing on the Singapore Exchange in 2007, we have made signifi cant progress in realising our vision to become a leading Integrated Agribusiness Group. Our key achievements such as the acquisition of Lonsum, our expansion into sugar cane plantations and continued investments to boost R&D and production capacities have placed us on a faster but sustainable track for growth.

With rising global consumption and a projected world population of 9.2 billion people by 2050 (50% of the population growth will be in Asia), we will continue to strengthen our business model and identify new business opportunities in Indonesia, to position ourselves for escalating market growth.

TAPPING INTO A RESILIENT HOME BASEWhile most economies are only just beginning to recover from the global fi nancial crisis, Indonesia has been up on its feet as early as the start of 2009. This is attributable to a strong domestic market that was less dependent on exports. Its population of 240 million makes it Southeast Asia’s biggest economy with domestic consumption accounting for 70% of its estimated GDP of over US$500 billion.

The Rupiah’s strength against the US dollar has enabled local businesses, including plantation owners, to weather the economic turbulence relatively well. In January 2010, Fitch Ratings upgraded the country’s sovereign debt from ‘BB’ to ‘BB+’ with a “stable outlook”, citing Indonesia’s resilience amidst the global fi nancial crisis and a well-managed state budget.

The upbeat economic outlook, coupled with political stability, has increased investor confi dence in Indonesia. Together with its strong population growth, we expect demand for palm oil products to improve and domestic

consumption in Indonesia to remain robust in the short to medium term.

Additionally, the World Bank has estimated a GDP growth rate of 5.6% in 2010 compared to 4.5% in 2009 supported by strong domestic consumption and government infrastructure-related projects. We are confi dent that IndoAgri will be able to ride the turbulent times and emerge from the economic crisis with confi dence and strength.

UNLOCKING OUR FULL POTENTIALChanneling our expertise and resources to become one of the largest plantation owners in Indonesia has been the right strategy for our business. Indonesia remains one of the world’s cheapest places to grow palm oil, and is ideally placed to service the increasing import demands of India and China and other emerging Asian economies.

Expanding the scope of our agribusiness to include sugar production has resonated well with the Group’s objective in harnessing greater economies of scale and tapping into synergies from our expertise in large-scale plantation management.

Besides the good synergistic fi t, we believe this will enhance our competitive edge in the commodities market. The completion of our cutting-edge sugar refi nery in 3Q2010 will give us the capacity to grow this business and to realise our potential. Indonesia currently has a domestic shortfall of approximately 2 million tonnes of sugar, which equates to 40% of consumption, allowing further scope for us to expand our sugar footprint.

Our commitment to sustainable agriculture was further enhanced with our North Sumatra estates gaining Roundtable on Sustainable Palm Oil (RSPO) Certifi cation for sustainable palm oil.

GEARING FOR GROWTHLooking ahead, we will continue to pursue strategic opportunities, including the identifi cation of new and suitable land banks in Indonesia and beyond, in order to expand our planted area and improve our production yields. We will balance this with a fi rm commitment to manage our business operations in a sustainable manner, supported by a strong R&D emphasis and a prudent approach to managing resources, underscored by the highest standards of corporate governance.

APPRECIATIONI would like to thank the Board of Directors, management and staff for their hard work and dedication; and our shareholders for their continued confi dence and support in a challenging year. We are well placed to reap the harvest in the coming years.

Mr Edward LeeCHAIRMAN

1 0

THE TURBULENT ECONOMY HAS NOT DETERRED INDOAGRI FROM ACHIEVING A NUMBER OF SUCCESSES THIS FINANCIAL YEAR. WE CONTINUED TO DRIVE RESULTS THROUGH EFFICIENT AND COST-EFFECTIVE MEASURES THAT HONE OUR OPERATIONS. WE ALSO STEPPED-UP ON R&D EFFORTS AND STREAMLINED OUR VERTICALLY INTEGRATED AGRIBUSINESS MODEL IN ORDER TO BUILD SUSTAINABLE GROWTH.

CEO’S STATEMENT

Dear Shareholders,

A leading integrated Agribusiness group with strong R&D and seed breeding operations.

Despite a diffi cult year for all sectors, commodity prices were surprisingly buoyant in 2009. We expect the trend to remain well supported in 2010 as stability and world consumption increases after the global crisis, coupled with stronger demand for biodiesel driven by government mandates in Europe, Brazil and Argentina.

In 2009, adverse weather triggered most of the volatility in commodity prices. Severe droughts in Argentina affected the production of soybean, a close palm oil substitute, resulting in 14 million tonnes decline in actual crops harvested. Additionally wet weather in India caused a reduction in their oilseed crops, driving the increase in India’s import of palm oil from 5.8 million tonnes in 2008 to 6.8 million tonnes in 2009.

Resultantly, CPO prices staged a strong recovery from the second quarter of 2009 with a range of US$640 (CIF Rotterdam) to US$801 per tonne before ending the year at US$792 per tonne. Prices averaged US$683 per tonne in 2009 against US$949 per tonne in 2008. Palm oil remains a low-cost vegetable oil to produce given its high yield per hectare as compared to other crops; capturing strong growth from major economies like China and India, where demand is likely to remain vibrant despite challenging economic conditions.

On the other hand, rubber prices, which were severely affected in late 2008 by a signifi cant drop in demand, ranged from a low of US$1,420 to a high of US$2,885 per tonne by the end of 2009. As signs of recovery return, we expect to see improved demand as we enter 2010.

PRUDENT RESPONSES TO THE GLOBAL CRISISAlthough the effects from the severe economic crisis will be felt for some time to come and recovery in the fi nancial sector is underway, 2009 proved to be far less volatile in our markets than 2008. What became very apparent in 2009 is that US consumer spending, which supported most of the previous decade’s global growth, will diminish in prominence as new markets provide the impetus for stronger demands in the medium term.

As a Group, our response to the global crisis was quick and prudent. Our immediate reaction was to protect our cash fl ow and increase the focus on our balance sheet. We acted swiftly to reduce capital expenditure by slowing down our new plantings and focusing on our core capital programme to deliver our expansion plans while ensuring tighter cost control. We also took a much closer scrutiny on counterparty risks, and an increased focus on receivables to protect our cash fl ow.

1 1B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

CEO’S STATEMENT

In November 2009, we strengthened the Group’s capital structure by issuing 5-year Indonesia Rupiah Bonds amounting to Rp730 billion, refi nancing our short-term borrowings to accommodate the cash fl ow patterns of our continued business expansion plans.

Looking ahead, emerging markets like Brazil, India and China will drive global economic growth. Our priority is to ensure that IndoAgri is well positioned to benefi t from the opportunities, as our agribusiness model caters to consumption growth particularly in the Indonesian and Asian economies.

DELIVERING STEADY PERFORMANCE AMIDST CHALLENGING TIMESGiven the unprecedented high in CPO prices in the fi rst half of 2008, the Group’s revenue of Rp9.0 trillion (S$1.3 billion) in 2009, which was 24% lower than a year ago, was attributed mainly to lower average selling prices of commodities during the year in review. This was partially offset by stronger sales volume growth in CPO, palm kernel (PK) and margarine of 4%, 11% and 8% respectively in 2009 compared to the same period last year.

Nonetheless, EBITDA margins expanded to 33.0% from 26.1% in 2008 as a result of foreign currency gains, lower operating expenses and tighter cost control. We also achieved a strong net profi t attributable to equity holders of Rp1.5 trillion (S$213 million), up 92% compared to 2008.

Notwithstanding economic challenges, the Group is committed to continued growth and expansion in 2010.

HARNESSING SYNERGIES The acquisition of Lonsum has enabled the Group to realise a number of operational synergies beyond scale. It has boosted internal CPO from 274,000 tonnes in 2007 to 457,000 tonnes in 2009, giving us greater assurance over the quality of raw material used for downstream refi nement.

Our research centres pool R&D technology, information from fi eld trials and plantation production data to accelerate our breeding and seed cultivation programmes and to achieve better quality and higher-yielding seed material. Our combined purchases have given us greater economies of scale and improved bargaining power with our suppliers.

Harnessing internal resources, fresh fruit bunches (FFB) production from our Kalimantan estates are now fully processed at Lonsum’s new 45 tonne/hour palm oil mill in East Kalimantan, thereby preserving the freshness of our fruit quality and reducing the costs of transporting our FFB to third party mills located 400 km away.

As a result, we have added more trucks to our fl eet at Lonsum, as increased in-house transportation allows us greater logistical control and a more economical alternative to outsourcing. We intend to achieve 100% in-house FFB transportation by end-2010.

In the longer term, we expect the synergies from the Lonsum acquisition to contribute more signifi cantly to the Group through sustainable cost reductions and improved productivity that will help us to realise higher profi tability and increased returns for our shareholders.

STRENGTHENING OUR CORPORATE GOVERNANCE FRAMEWORKA well integrated and coordinated approach to Enterprise Risk Management or ERM is critically essential to an effi cient risk management framework, and to ensure the day to day tracking, monitoring and control of risks.

In 2009, we established a central ERM unit with the primary objective of promoting a more systematic, integrated and well-coordinated approach to risk management strategies across all our operating and functional units. Adopting a prudent approach to risk management as we navigate through volatile commodity markets underpins our ability to execute on our growth strategy in creating shareholder value.

The ERM unit immediately consolidated all existing risk management activities under its ambit in order to monitor and assess the Group’s overall risk profi le. It has embarked on a comprehensive risk management awareness and integration programme to develop and enhance our formal risk policies and procedures; develop and update our risk management methodologies, guides and tools; and work closer with operating units and functional departments on critical matters relating to risk management.

We will sustain our priorities in risk management by promoting awareness through staff communication and ERM training to key employees. The development of a comprehensive Risk Management Manual that details the roles and responsibilities of management and respective employees, will further aid the effective implementation of ERM, and is core to our ongoing business process improvements.

LEVERAGING IT FOR BETTER DECISION MAKING In 2008, we decided to increase our investment in Information Technology as a strategic business support tool that would enable us to leverage on scalability as we grow our business.

1 2

As such, the Group upgraded its IT platform in 2009 by adopting SAP as the enterprise resource planning system for its refi nery operations. SAP has enabled an integrated platform for quicker and more effi cient decision making, as well as more effective business planning and execution. In the year ahead, we expect to move into the next phase of design as well as testing and implementing the SAP system across our plantation operations.

NURTURING OUR HUMAN CAPITAL The Group’s single most important competitive advantage lies in its people. We value the importance of teamwork, cohesiveness and a productive work environment in achieving our full potential. As such, we will continue to engage and motivate our employees through regular communication, as well as training and development opportunities.

As part of ongoing improvements across the Group, we have engaged in a new phase of our human capital management that will help us to align our HR strategies to organisational goals. We are undertaking a wide-ranging review of our HR practices, with a strong focus on leadership renewal. To expedite results, we have recruited a senior HR executive to spearhead these efforts Group-wide.

We have also embarked on leadership training programmes as well as formal processes for succession planning, so that talented employees may be identifi ed and developed for higher roles and responsibilities under a planned development programme.

These, together with our other HR initiatives, will enable us to build the right competencies and capability to deliver on our expansion plans.

GEARING TOWARDS SUSTAINABLE PRODUCTIONThe Group continues to advocate responsible farming and agribusiness practices, and has a long-term commitment to the sustainable production of our products.

This year, we are very proud to have achieved the Roundtable on Sustainable Palm Oil (RSPO) certifi cate, the highest global recognition for sustainable production, for our North Sumatra oil palm estates and mills. The RSPO sustainable certifi cate covers 8 principles and 39 criteria, which are in turn measured by external RSPO-certifi ed auditors across 139 indicators. This certifi cation is both comprehensive and relevant in today’s business environment, while accounting for 170,000 tonnes of sustainable palm oil produced each year by the Group.

We are already well under way to expanding this certifi cation within our plantations in Sumatra, and aim to extend our production of certifi ed sustainable palm oil in the future.

ACCELERATING INNOVATION THROUGH R&DR&D remains a key pillar in our efforts to build sustainable growth. Working through Sumatra Bioscience and PT SAIN, the Group’s in-house research centres, we will continue to focus on improving plantation yields and cultivation practices in 4 key areas: plant breeding, agronomy, crop protection and data analysis.

As pioneers of the world’s fi rst patented process for the production of F1 oil palm hybrids, we are confi dent that we will be able to signifi cantly improve conventional oil palm yields. Capitalising on our fi rst-mover advantage, we have embarked on our 10-year roadmap to commercialise the production of our F1 oil palm hybrids.

More importantly, we believe these efforts will contribute signifi cantly to environmental sustainability with less land being required for crop cultivation.

IN APPRECIATIONI would like to take this opportunity to extend my appreciation to the Board of Directors for their dedication, support and valuable inputs in charting the Group’s strategy.

I would also like to thank our suppliers and business partners for their commitment and unfailing support.

To the management and staff at IndoAgri, I would like to express my special thanks for the loyalty and hard work, and for going the extra mile during an extremely challenging year.

Last but not least, my heartfelt appreciation goes to you, our shareholders, for your unwavering trust during a turbulent year. Your confidence in the Group has contributed to our success.

Mr Mark WakefordCHIEF EXECUTIVE OFFICER

1 3B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

BUSINESS OVERVIEW

INDOFOOD AGRI RESOURCES LTD (“INDOAGRI” OR “THE GROUP”) IS A VERTICALLY INTEGRATED AGRIBUSINESS GROUP WITH ACTIVITIES SPANNING THE ENTIRE SUPPLY CHAIN FROM RESEARCH AND DEVELOPMENT, SEED BREEDING AND OIL PALM CULTIVATION; TO PLANTATION AND MILLING OF PALM OIL AND COPRA; AND THE PRODUCTION AND MARKETING OF BRANDED COOKING OIL AND MARGARINE. AS A DIVERSIFIED AGRIBUSINESS, WE ARE ALSO ENGAGED IN THE CULTIVATION OF SUGAR CANE, RUBBER AND OTHER CROPS.

Headquartered in Jakarta, the Group is among the largest palm oil producers in Indonesia. Our branded cooking oil, shortening and margarine products garner a leading share in the domestic consumer market. IndoAgri is listed on the Singapore Exchange, and is organised into three business divisions: Plantation, Cooking Oil & Fats, and Commodity.

FINANCIAL HIGHLIGHTSAmidst the challenges of 2009, IndoAgri recorded revenue of Rp9.0 trillion (S$1.3 billion), a 24% decline compared to a year ago given the lower average prices of CPO, palm kernel (PK), rubber, edible oil products and reduced volume in the sales of cooking oil. This was partially offset by stronger sales volume growth in CPO, PK and margarine of 4%, 11% and 8% respectively in 2009 compared to the same period last year.

Despite the weaker revenue, EBITDA margins grew from 26.1% to 33.0% this year due to reduced selling and distribution costs on lower export taxes, tighter cost controls and net gains on foreign currency.

The Group’s 2009 net profi t attributable to equity holders grew 92% to Rp1.5 trillion (S$213 million) compared to the previous year, driven mainly by gains on biological assets, lower operating costs and net gains on foreign currency.

CHARTING STRATEGIES FOR SUSTAINABLE GROWTHThe Group remains one of Indonesia’s largest plantation owners with an aggregate land bank of 549,287 hectares and a planted area of 227,721 hectares. Nonetheless, due to economic uncertainties arising from the fi nancial crisis, we reduced new plantings of oil palm to 11,773 hectares in 2009, compared to the 22,014 hectares achieved in the previous year.

OIL PALMS – CONTINUED EXPANSION• As our dominant crop, oil palm constitutes 193,613

hectares or 85% of our total planted area as at end December 2009. This includes 61,053 hectares of immature plantings (roughly the size of Singapore), which will come into maturity over the next 24 months ensuring continued growth in our CPO production.

REVENUE

0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

05 06 07 08 09

R p t r i l l i o n

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

3.64.1

6.5

11.8

9.0

PROFIT FROM OPERATIONS

0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

05 06 07 08 09

R p t r i l l i o n

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

0.91.2

1.61.9

3.3

1 4

• Bolstered by maturing new estates, the Group achieved an FFB output of 2,613,345 tonnes, a 5% increase over the previous year.

• CPO production grew 7% to 762,570 tonnes on the back of higher FFB output and higher purchases from plasma and third party farmers. Additional capacities from two 45 tonne/hour palm oil mills in Kalimantan completed in 2009 will improve our CPO production in the years ahead.

• We will continue to increase our oil palm acreage, and look forward to the completion of two new palm oil mills in 2011.

SUGAR – COMING ON STREAM• In 2009, the Group’s investment in the sugar business

produced 295,948 tonnes of sugar cane from its South Sumatra estates, while its sugar mill in Central Java produced 8,751 tonnes of sugar and 6,188 tonnes of molasses.

• As at the end of December 2009, our planted acreage of 8,672 hectares of sugar cane is well on the way to achieving our targeted planted area by 2011.

• Completion of our 8,000 TCD sugar mill in South Sumatra in 3Q2010 will enable us to achieve the vertical integration we require for full-scale operations and growth.

COOKING OIL & FATS – EXPANDING REFINING CAPACITY• The Medan refi nery expansion programme, which was

completed in 1Q2009, has enabled us to expand our refi ning capacity to 1 million tonnes per annum.

• The new 420,000-tonne per year refi nery in Jakarta, which is scheduled to complete in 4Q2010, will further enhance our speciality fats capability and output levels whilst reducing operating costs.

The Group advocates responsible farming and agribusiness practices, achieving the highest global recognition – the Roundtable on Sustainable Palm Oil (RSPO) certifi cate – for our North Sumatra oil palm estates and mills in 2009. The certifi cation accounts for 170,000 tonnes of sustainable palm oil produced each year.

Strengthening our capital structure, the Group issued 5-year Indonesian Rupiah Bonds amounting to Rp730 billion to refi nance our short-term borrowings and accommodate the cash fl ow patterns of our business expansion plans.

R&D remains a key pillar in our efforts to build sustainable growth, as we continue to seek greater economies of scale as a competitive and vertically integrated agribusiness group.

NET PROFIT TO EQUITY HOLDERS

0

1.8

1.6

1.4

1.2

0.8

1.0

0.6

0.4

0.2

05 06 07 08 09

R p t r i l l i o n

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

0.5

0.7

0.90.8

1.5

NAV PER SHARE

0

7,000

6,000

5,000

4,000

3,000

2,000

1,000

05 06 07 08 09

R p

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

2,0962,762

4,9435,506

6,567

1 5B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

FINANCIAL HIGHLIGHTS

1 Profi t from operations divided by total assets

2 Net profi t to equity holders divided by shareholders’ equity

3 Net debt divided by total equity

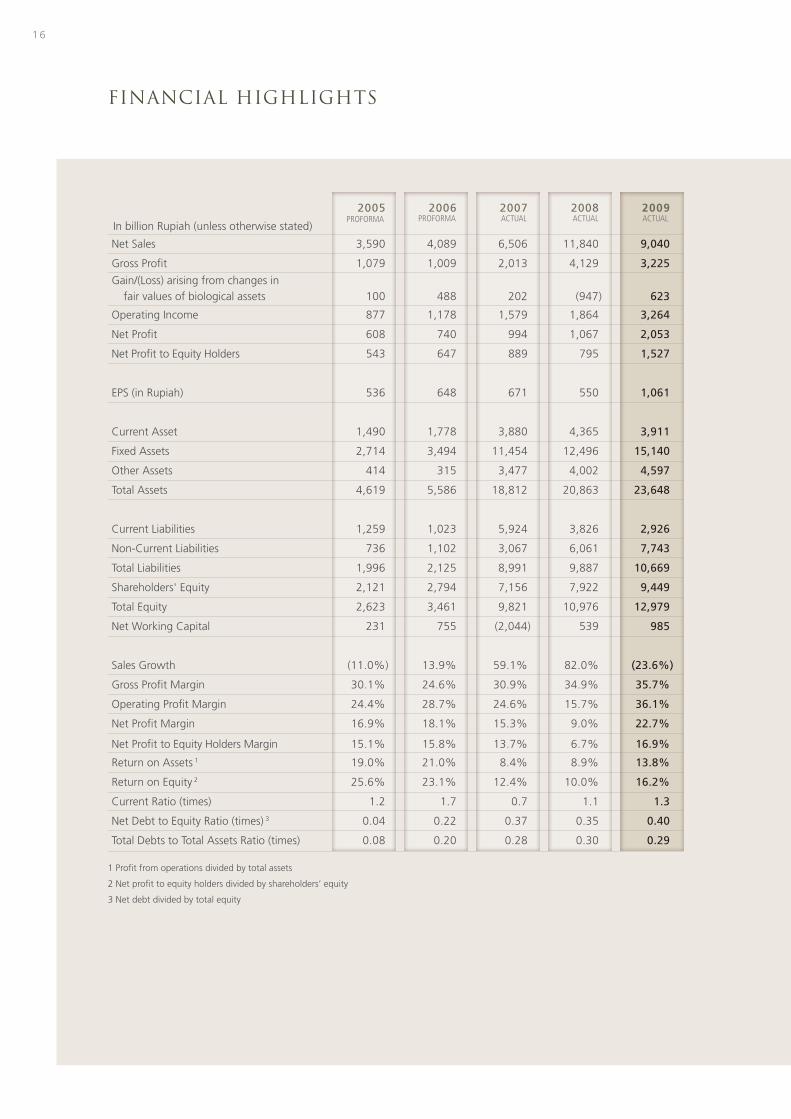

2005 2006 2007 2008 2009

In billion Rupiah (unless otherwise stated)

Net Sales 3,590 4,089 6,506 11,840 9,040

Gross Profi t 1,079 1,009 2,013 4,129 3,225

Gain/(Loss) arising from changes in fair values of biological assets 100 488 202 (947) 623

Operating Income 877 1,178 1,579 1,864 3,264

Net Profi t 608 740 994 1,067 2,053

Net Profi t to Equity Holders 543 647 889 795 1,527

EPS (in Rupiah) 536 648 671 550 1,061

Current Asset 1,490 1,778 3,880 4,365 3,911

Fixed Assets 2,714 3,494 11,454 12,496 15,140

Other Assets 414 315 3,477 4,002 4,597

Total Assets 4,619 5,586 18,812 20,863 23,648

Current Liabilities 1,259 1,023 5,924 3,826 2,926

Non-Current Liabilities 736 1,102 3,067 6,061 7,743

Total Liabilities 1,996 2,125 8,991 9,887 10,669

Shareholders' Equity 2,121 2,794 7,156 7,922 9,449

Total Equity 2,623 3,461 9,821 10,976 12,979

Net Working Capital 231 755 (2,044) 539 985

Sales Growth (11.0%) 13.9% 59.1% 82.0% (23.6%)

Gross Profi t Margin 30.1% 24.6% 30.9% 34.9% 35.7%

Operating Profi t Margin 24.4% 28.7% 24.6% 15.7% 36.1%

Net Profi t Margin 16.9% 18.1% 15.3% 9.0% 22.7%

Net Profi t to Equity Holders Margin 15.1% 15.8% 13.7% 6.7% 16.9%

Return on Assets 1 19.0% 21.0% 8.4% 8.9% 13.8%

Return on Equity 2 25.6% 23.1% 12.4% 10.0% 16.2%

Current Ratio (times) 1.2 1.7 0.7 1.1 1.3

Net Debt to Equity Ratio (times) 3 0.04 0.22 0.37 0.35 0.40

Total Debts to Total Assets Ratio (times) 0.08 0.20 0.28 0.30 0.29

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

1 6

OPERATIONAL HIGHLIGHTS

2005 2006 2007 2008 2009In Hectares (unless otherwise stated)Planted Area - NucleusOil Palm 61,408 66,900 161,457 183,113 193,613

Mature 56,939 60,817 118,030 124,169 132,560

Immature 4,469 6,083 43,427 58,944 61,053

Rubber 5,015 5,015 22,003 22,410 21,738Mature 5,015 5,015 18,956 17,873 17,263Immature - - 3,048 4,537 4,475

Sugar - - - 4,174 8,672Mature - - - 4,174 8,672

Others - - 3,522 3,631 3,698Mature - - 2,800 2,870 2,971Immature - - 722 761 727

Plasma 25,000 25,000 61,000 76,472 76,851

Age Maturity of Oil Palm TreesImmature 3,344 5,604 43,427 58,944 61,0534 - 6 years 6,231 5,365 9,331 12,332 19,5597 - 20 years 51,734 47,072 90,628 82,008 73,262Above 20 years 99 8,859 18,070 29,829 39,739Total 61,408 66,900 161,457 183,113 193,613

Distribution of Planted Areas-Nucleus

Riau 56,009 56,610 57,003 57,003 56,782North Sumatra - - 40,535 40,506 40,463South Sumatra - - 43,692 61,254 71,385West Kalimantan 5,399 10,290 18,632 21,758 21,878East Kalimantan 5,015 5,015 19,030 24,478 28,120Central Kalimantan - - - - 725Java - - 2,555 2,795 2,860Sulawesi - - 5,535 5,534 5,508Total 66,423 71,915 186,982 213,328 227,721

Production Volume (‘000 Tonnes)Nucleus Fresh Fruit Bunch (FFB) 1,295 1,324 1,506 2,496 2,613Processed FFB 1,294 1,320 1,708 3,160 3,346Crude Palm Oil (CPO) 299 300 384 714 763Palm Kernel (PK) 61 63 85 166 181Oil Palm Seed ('000) - 800 5,550 24,839 18,713Rubber - 4 8 28 28

Sales Volume (‘000 Tonnes)Crude Palm Oil (CPO) 297 305 361 730 759Palm Kernel (PK) 59 64 82 161 179Rubber 1 3 7 26 25Cooking Oil 322 371 371 424 387

Magarine 177 178 183 161 173

Coconut Oil 84 87 109 108 82

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

1 7B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

OIL PALM SEED BREEDING

P L A N T A T I O N S

PALM OIL MILLSSS

R E F I N E R I E S

OO

R E S E A R C H & D E V E L O P M E N T

P L A N T A T I O N SP

D I S T R I B U T I O NN

F I N I S H E D P R O D U C T S

OURINTEGRATEDAGRIBUSINESS MODEL

OPERATIONS REVIEW

PLANTATION | Palm Oil

OVERVIEWThe Plantation Division manages IndoAgri’s strategically located estates across Indonesia. The Group’s land bank of 549,287 hectares, including 227,721 hectares of planted area, makes us one of the largest plantation owners in the archipelago.

Oil palm, our dominant crop, occupies 193,613 hectares or 85% of total planted area, followed by rubber and sugar plantations at 10% and 4% respectively. With 61,053 hectares or 32% of our oil palm estates demarcated by young or immature trees, the Group is poised for stronger FFB output as these trees approach their productive ages.

Leveraging the combined heritage of our subsidiaries, PT SIMP and Lonsum, the Group brings together nearly 130 years of plantation management experience and expertise, scaling new heights in seed breeding and cultivation programmes that have made us one of the most productive plantation companies in Indonesia. Our focus on cutting-edge R&D has also rewarded us with a patented process that produces seed material with improved quality and yields.

Through the division, the Group operates 20 palm oil mills across Sumatra and Kalimantan, with a total processing capacity of 4.5 million tonnes of FFB per year. We also operate four crumb rubber factories, three sheet rubber factories, a cocoa factory, a tea factory and a sugar factory.

Our mills and estates in North Sumatra are certifi ed to the rigorous standards of the Roundtable on Sustainable Palm Oil (RSPO), producing 170,000 tonnes of sustainable crude palm oil per annum.

With Lonsum in its second year of operation under our wings, the Group is reaping signifi cant progress from acquisition synergies.

Our diversifi cation into the sugar business has also yielded encouraging results, with construction of new facilities proceeding on schedule for full-scale operations in 2010.

2009 REVIEWSigns of stabilisation in the global economy, coupled with increased imports and consumption in emerging markets like China and India, have helped commodity prices to rebound from their recent low in Q42008. Higher demand, fuelled by tighter supplies and a severe drought in Argentina, which reduced soybean output from 46 to 32 million tonnes, drove the recovery of CPO prices (CIF Rotterdam) in 2009 to US$683 per tonne, from US$503 per tonne in December 2008. Rubber prices refl ected a similar rebound; prompted by lower global production, recovery in global demand and higher mineral oil prices.

INDOAGRI REMAINS ONE OF THE

INDONESIA’S LARGEST PLANTATION

OWNERS WITH A PLANTED OIL PALM

ACREAGE OVER 193,000 HECTARES.

2 0

Rows of seedlings cultivated in our oil palm plantations.

0.00

3.50

3.00

2.00

2.50

1.50

1.00

0.50

U S $ / k g

Rubber Price (RSS 3 SICOM)

Jun

-05

Dec

-05

Jun

-06

Dec

-06

Jun

-07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

Dec

-09

2 1B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

0

1400

1200

800

1000

600

400

200

U S $ / t o n n e

CPO Price (CIF N.W.Europe)

Jun

-05

Dec

-05

Jun

-06

Dec

-06

Jun

-07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

Dec

-09

For the year in review, the plantation division recorded total sales of Rp6,046 billion (S$842million), a 11% decrease against 2008 due to lower average selling prices of CPO, PK and rubber. The decline was partially mitigated by higher CPO and PK sales volume of 4% and 11% respectively, as well as sales of sugar cane and sugar products.

Operating profi t margin, excluding biological asset gains, was lower at 37% compared to 42% in 2008. This was attributed to lower selling prices of plantation crops.

Through the division, the Group harvested 2,613,345 tonnes of nucleus FFB in 2009, a 5% increase over the previous year. The stronger production was driven by higher output in our North Sumatra estates as the trees recover from biological stress in 2008, and higher production in South Sumatra and Kalimantan due to increased mature area and yield improvements.

CPO production increased 7% to 762,570 tonnes on the back of higher FFB processed. Oil extraction rate (OER) remained relatively stable at 22.8%, compared to 22.6% in 2008.

Rubber production improved marginally by 1% from 28,100 tonnes in 2008 to 28,329 tonnes in 2009. The Group also harvested 295,948 tonnes of sugar cane in 2009, as our sugar plantations complete their fi rst year in operation.

As at 31 December 2009, the Group’s oil palm planted area stood at 193,613 hectares, a 10,500-hectare increase over the previous year. Mature oil palm estates span 132,560 hectares, an 8,391-hectare increase over 2008, as young trees begin to bear fruit.

SYNERGIES THROUGH LONSUM The acquisition of Lonsum has enabled the Group to realise a number of operational synergies beyond scale. It has boosted internal CPO supply to our refi neries from 274,000 tonnes in 2007 to 457,000 tonnes in 2009, giving us greater assurance over the quality of raw material used for downstream refi nement. Our research centres pool R&D technology, information from fi eld trials and plantation production data to accelerate our breeding and seed cultivation programmes and to achieve better quality and higher-yielding seed material. Our combined purchases have given us greater economies of scale and higher bargaining power.

FFB production from Lonsum’s Kalimantan estates are now fully processed at our new 45 tonne/hour palm oil mill in East Kalimantan, thereby preserving the freshness of our fruit quality and reducing the costs of transporting our FFB to third party mills located 400 km away. We have added more trucks to our fl eet at Lonsum, as increased in-house transportation allows us greater logistics control and a more economical alternative to outsourcing. We intend to achieve 100% in-house FFB transportation by end-2010.

OPERATIONS REVIEW

0

3000

2000

2500

1500

1000

500

05 06 07 08 09

‘ 0 0 0 m t

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

1,295 1,3241,506

2,4962,613

FFB production (nucleus)

0

1000

800

600

400

200

05 06 07 08 09

‘ 0 0 0 m t

PROFORMA PROFORMA ACTUAL ACTUAL ACTUAL

CPO production

299 300384

714 763

2 2

Above 20 Years20%

7-20 Years38%

4-6 Years10%

Immature32%

Oil palm plantation age profi le

We are improving the road infrastructure in our South Sumatra estates, which will signifi cantly enhance the transportation of crops and fertilizer, especially during the rainy season. We are also building new houses in our South Sumatra estates to reduce reliance on contract workers, improve the productivity of our operational staff, and enable them to live together with their families on the plantations.

THE ACQUISITION OF LONSUM HAS

ENABLED INDOAGRI TO ACHIEVE

OPERATIONAL SYNERGIES INCLUDING

INCREASED INTERNAL CPO SUPPLY TO

REFINERIES, R&D, GREATER ECONOMIES

OF SCALE AND HIGHER

BARGAINING POWER.

2010 OUTLOOK Looking ahead, we expect CPO prices to remain volatile in 2010 as they hinge on multiple factors that include global production and consumption rates for vegetable oil, mineral oil prices, robustness of the economy and stability of the US Dollar.

Long-term prospects for the palm oil industry remain positive. The lower cost of producing palm oil will continue to drive its demand as the most widely consumed vegetable oil at 27% compared to soybean at 22% and rapeseed oil at 13%. CPO demand will also be supported by the introduction of government mandates to increase the percentage of biofuel content in conventional transportation fuels, particularly in Europe and South America.

Despite the challenging economic climate, we expect demand for palm oil to remain resilient in 2010. We will continue our strategy to increase our oil palm acreage, and look forward to the targeted completion of two new palm oil mills in 2011. We will also continue to invest in R&D to capture additional value and improve our competitive advantage.

ABOVE: Oil palm seedlings contributing to the lush greenery.

RIGHT: A harvester transporting FFB in a wheelbarrow.

2 3B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

OPERATIONS REVIEW

PLANTATION | Sugar

THE DIVERSIFICATION INTO SUGAR HAS

OFFERED STRATEGIC FIT AND NUMEROUS

COMPETITIVE ADVANTAGES FOR

INDOAGRI.

OVERVIEWIn 2008, IndoAgri diversifi ed into the lucrative industry of sugar cultivation, plantation and production – a decision backed by shortfalls in domestic supply, increasing population growth and the development of processed F&B industries in Indonesia. As net importers of sugar, the government imposes various policies ranging from price regulation to import quotas to protect and promote the domestic sugar industry in Indonesia. In 2009, about 40% of the estimated domestic consumption of 4.9 million tonnes of sugar was imported.

We believe the sugar industry offers both strategic fi t and numerous competitive advantages for the Group. Upstream, we believe we are able to achieve better yields and lower cost through economies of scale and our vast experience in large-scale plantation management. The completion of our modern sugar mill in 3Q2010 will enable us to operate at higher effi ciency levels, with higher extraction, lower wastage and lower processing cost per unit. Additionally, signifi cant savings will be achieved from leveraging Indofood’s distribution network for our end products.

During the year in review, the market witnessed a huge rallying in global sugar prices on the New York Board of Trade, with the price of CSCE No. 11 rising 84% from US$13.59 cent/lb in January to its 28-year high of US$27.45 cent/lb in December. This was triggered by adverse weather and poor harvest conditions in Brazil and India, two of the world’s largest sugar producers, which saw global sugar supply defi cits of approximately 9 million tonnes in 2009.

2 4

0.00

30.00

20.00

25.00

15.00

10.00

5.00

U S c e n t / l b

Sugar Price (CSCE No.11)

Jun

-05

Dec

-05

Jun

-06

Dec

-06

Jun

-07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

Dec

-09

2009 REVIEWThe sugar business made headways in its second year of operation with new plantings and the construction of new milling facilities. While revenue contributions for 2009 were relatively subdued at Rp146 billion, we expect this to increase in 2010 as our increased sugar cane plantings mature and when our new 8,000 tonnes of cane per day (TCD) sugar processing mill in South Sumatra is commissioned in 3Q2010.

The Group achieved a sugar cane planted area of 8,672 hectares as at end-December 2009, an increase of 4,498 hectares from 4,174 hectares as at end-December 2008. Our harvested area of 3,693 hectares yielded 80 tonnes of sugar cane per hectare, producing 295,948 tonnes of sugar cane in 2009.

2010 OUTLOOKMoving forward, we will continue with our sugar planting and expansion plans over the next two years in order to achieve the targeted planted area by end-2011. Our South Sumatra sugar mill construction is on schedule for completion in 3Q2010 and we expect the division to make notable contributions to Group revenue in 2011.

Sugar cane plantation in South Sumatra.

2 5B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

PLANTATION | R&D

OPERATIONS REVIEW

A STRONG RESEARCH FOUNDATION

IS THE FIRST STEP TO IMPROVING

PLANTATION YIELDS.

OVERVIEWUnderlying IndoAgri’s business strategy is a fi rm commitment to research practices that are focused on improving plantation yields and cultivation practices. Through Sumatra Bioscience (SumBio, formerly known as Bah Lias Research Station), an advanced agriculture research centre founded in 1983, and PT SAIN located in Pekanbaru, the Group owns in-house capabilities and a strong R&D heritage in the analysis of soil, plant tissue, oil palm and latex. Our laboratories and comprehensive facilities equip us for cutting-edge research in tissue culture, biotechnology, pathology and entomology.

Through SumBio’s advanced programmes in palm oil seed breeding, it produces up to 25 million superior oil palm seeds per annum. We also operate a research and seed breeding facility in Riau that produces up to 8 million seeds per annum.

The Group’s R&D activities are focused in four key areas:

• Plant breeding: The development of top quality seed and planting material through traditional breeding methods, a diverse germ-plasm base and biotechnology, supported by fi eld trials that test progenies across a range of breeding environments.

• Agronomy: Detailed analyses that provide our estates with optimal recommendations on crop management and planting densities, fertilizer and herbicide usage, as well as predictions on yields and oil extraction rates.

• Crop protection: The development of integrated pest management systems to minimise crop losses and to monitor potential pest and disease outbreaks.

• Data analysis: The analyses of data collected from fi eld trials, as well as information pertaining to crop genetics and estate for future reference.

With innovative plant breeding, agronomy and crop protection, the Group aims to improve yields per hectare while reducing labour costs. We also leverage R&D and seed-breeding programmes to improve production costs, improve environmental sustainability and maximise profi tability in the long run.

2009 REVIEWThe Group reported a decline in the sales volume of oil palm seeds from 18 million seeds in 2008 to 5 million seeds in 2009 due largely to lower demand and a recession-induced reduction in new plantings across the industry. Despite the challenging year, the market for oil palm seedlings showed signs of recovery as orders gained momentum during 4Q2009.

Through SumBio, the Group owns the world’s fi rst patented process for the production of F1 oil palm hybrids. These hybrids, which are produced without any genetic modifi cation, have been patented in selected countries around the world.

2 6

A researcher examining an oil palm specimen.

Our pioneering efforts have enabled us to signifi cantly improve conventional oil palms yields, which will result in less land being required for crop cultivation in the long run. Aside from these benefi ts, the production of F1 oil palm hybrids will also bring about greater economic viability and environmental sustainability.

The Group expects to commercialise the production of F1 oil palm hybrids over a 10-year period. In line with our commercialisation plans, SumBio is evaluating the feasibility of establishing a new Genetics Research & Development Centre at Bah Lias in North Sumatra. This state-of-the-art facility will enable us to further our capabilities in the fields of genomics and biotechnology.

2010 OUTLOOKWe expect demand for oil palm seeds to recover, following the revival in commodity prices and improved global economic conditions. Major oil palm plantation companies have resumed their expansion programmes during the second half of 2009.

The Group will continue to invest in applied bioscience, and collaborate with the world’s leading plant scientists in order to increase our yield potential and sustain our commercial, environmental and societal competitive advantages. We will also step up on efforts to brand our seeds as the culmination of the highest possible genetic quality.

We will also further our efforts in agronomy and crop protection in order to develop comprehensive and robust management systems that can realise the genetic potential of our seeds in different breeding environments.

The Group is a fi rm advocate in the usage of information technology to store, manage and maximise the utilisation of the information generated from our fi eld trials and biotechnology processes.

We recognise the importance of R&D and its substantial long-term benefi ts not only for the Group, but also for the industry and the world at large. Increasing crop yields will lower unit costs, alleviate global food shortage and reduce the pressure to clear land for new plantings. As a Group, our advancements in R&D can make a signifi cant and vital contribution towards the sustainability of Indonesia’s forests, peat-swamps and natural biodiversity.

R&D WILL HELP

INDOAGRI TO SUSTAIN

ITS COMMERCIAL,

ENVIRONMENTAL AND

SOCIETAL COMPETITIVE

ADVANTAGES IN THE

LONG RUN.

2 7B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

COOKING OIL & FATS

OPERATIONS REVIEW

INDOAGRI COMMANDS A LEADING

MARKET SHARE IN INDONESIA FOR

BRANDED COOKING OIL, MARGARINE

AND SHORTENING PRODUCTS.

OVERVIEWThe Cooking Oil and Fats Division manufactures and markets IndoAgri’s downstream products, which include leading brands of cooking oil, margarine and shortening for both exports and domestic consumption. Bimoli, along with its other brands, Happy Salad Oil and Delima, the Group continues to command a leading share in the Indonesian market for branded cooking oils.

Our margarine & shortening products, branded under Simas Palmia, Palmia and Amanda, are also market leaders in the domestic margarine & shortening market. Approximately 75% of our margarine and shortening sales were derived from the domestic market, with the bulk of sales coming from industrial pack margarine and shortening which are supplied to bakeries, snack and biscuit manufacturers.

Supporting our marketing strategy is a comprehensive network of 120 distributors, who deliver our end products to 255,000 retail outlets across the Indonesian archipelago. We also leverage our parent company’s distribution network to supplement our market penetration efforts in Indonesia.

The division operates four refi neries located strategically in major cities across Indonesia: Jakarta, Surabaya, Medan and Bitung. With the target completion of our 420,000 tonnes per year refi nery in Jakarta by end-2010, our total refi ning capacity will achieve 1.4 million tonnes per year.

The Group refi ned 595,000 tonnes of CPO in 2009, of which 457,000 tonnes were supplied by our own plantations. To ensure consistent supplies of high quality CPO and enhance logistics management, we intend to increase internal CPO supplies in 2010.

2009 REVIEWThe division recorded mixed results for its edible oil products in 2009. Strong industrial demand delivered a sales volume of 172,970 tonnes of margarine and shortening products, or an 8% improvement over the previous year. Sales volume of cooking oil declined by 9% to 387,391 tonnes due to:

• A 10% VAT on branded cooking oil products in January 2009, which widened the price gap between branded and unbranded products; and

• An overall shrinkage in the domestic market for branded cooking oil as some consumers switched to unbranded products.

Despite the overall shrinkage in the branded cooking oil market in Indonesia, we retained our market leadership in this segment and strengthened our leading Bimoli brand though TV commercials, which promoted the product as “cooking oil perfection”.

2 8

ABOVE: Margarine being packaged for consumption.

RIGHT: Bimoli Spesial on the conveyor belt.

Margarine sales volume improved on stronger demand for industrial margarine. We also participated in a culinary program with a national TV channel to promote Simas Palmia as a multipurpose margarine. Other activities included the Palmia Baker’s Forum, a baking demonstration conducted in 29 cities across Indonesia, and participation in the Interfood Exhibition, a food and beverage showcase.

The division won a number of awards during the year. Bimoli won the Top Brand award in the cooking oil category from SWA Frontier for the fourth consecutive year, and the Platinum Brand IBBA - SWA MARS award for the sixth consecutive year.

The division reported total sales of Rp5,181 billion in 2009, a 21% decline against 2008 due to lower average selling prices and lower sales volume of cooking oil. Operating profi ts fell 50% to Rp119 billion due to lower gross profi t and higher distribution costs. The division’s profi t margin declined from 3.7% in 2008 to 2.3% in 2009.

2010 OUTLOOK Despite the challenging business conditions, we will continue to review our pricing strategy from time-to-time to maintain our competitiveness in the market. Given the Group’s market leadership, established brands, comprehensive distribution network, strong sales and marketing efforts and expertise, we believe we are well positioned for the challenges ahead.

In the year ahead, our key strategies will be centred on:

• Strengthening of brand identity and brand loyalty through enhanced product packaging and quality

• Rebranding and re-launch of our core brands: Bimoli and Bimoil Spesial

• Focused advertising and promotional activities to raise awareness and brand image

• Deeper penetration of distribution to increase product visibility as well as improved after sales services; and

• Focus on High Class Outlets (HCO) in line with their rapid growth in Indonesia

2 9B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

COMMODITIES

OPERATIONS REVIEW

INDOAGRI OPERATES THREE

COPRA-CRUSHING PLANTS WITH A

COMBINED CAPACITY OF 270,000

TONNES PER ANNUM.

OVERVIEWThe Commodities Division manufactures crude coconut oil (CNO) and other by-products from crushed copra for export to the United States, Europe and Asia. Most of our CNO and derivative products are bought by manufacturing plants producing oleochemicals such as fatty acids and glycerine used in the production of detergents, personal care products, lubricants, solvents and bioplastics, while by-products such as copra pellets are sold as animal feeds in overseas markets.

The division operates three copra-crushing plants located at Bitung in North Sulawesi, Moutong in Central Sulawesi and Tobelo on Halmahera Island, with a combined production capacity of 270,000 tonnes per annum.

2009 REVIEWCommodity traders continued to battle price instabilities in 2009, with CNO prices (CIF Rotterdam) averaging US$726 per tonne or 41% lower than its transacted rate of US$1,224 per tonne in 2008. The division recorded a 49% decline in revenue over the same period last year, due mainly to lower selling prices and lower sales volume of copra-based and palm oil-based products.

Operating losses for the division totalled Rp47 billion in 2009, largely attributable to lower revenue and negative effects emerging from a stronger Rupiah against US Dollars, given that the Group does not hedge the foreign exchange fl uctuations arising from its sales, which are conducted in US currency, and its raw material purchases, which are transacted in Rupiah.

2010 OUTLOOKBracing for further uncertainties, we will continue to secure back-to-back contracts from both our suppliers and customers to lower the impact of price volatility. We will also step up on management strategies for currency risks by exploring various options to cushion our currency exposure.

Other key initiatives for the division include increasing the utilisation of our copra crushing facilities, exploring new export opportunities through closer analysis of potential markets and increasing the level of marketing in those markets.

3 0

MANUFACTURING PROCESS

Fresh Palm Fruit Bunches

3 1B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

Milling

Crude Palm Oil

Refining

RBD Palm Oil

Fractionating & Filtration

RBD Palm Stearin Lauric Oil

Margarine Plant

Blending

Mixing Tank

Chilling Chilling

Packaging Packaging

Mixing Tank

Blending

RBD Palm Olein

Shortening Margarine

Palm Fatty Acid Distillate Crude Palm Kernel Oil

Palm Kernel Meal Crushing

Palm Kernel

Empty Fruit Bunches and By Products

Nitrogen gas

Water & Salt

Flavouring &Vitamins

Fresh Palm Fruit Bunches

Shorteningg

Cooking OilCooking Oil

Margarine

Packaging

ENVIRONMENT & CORPORATE SOCIAL RESPONSIBILITY

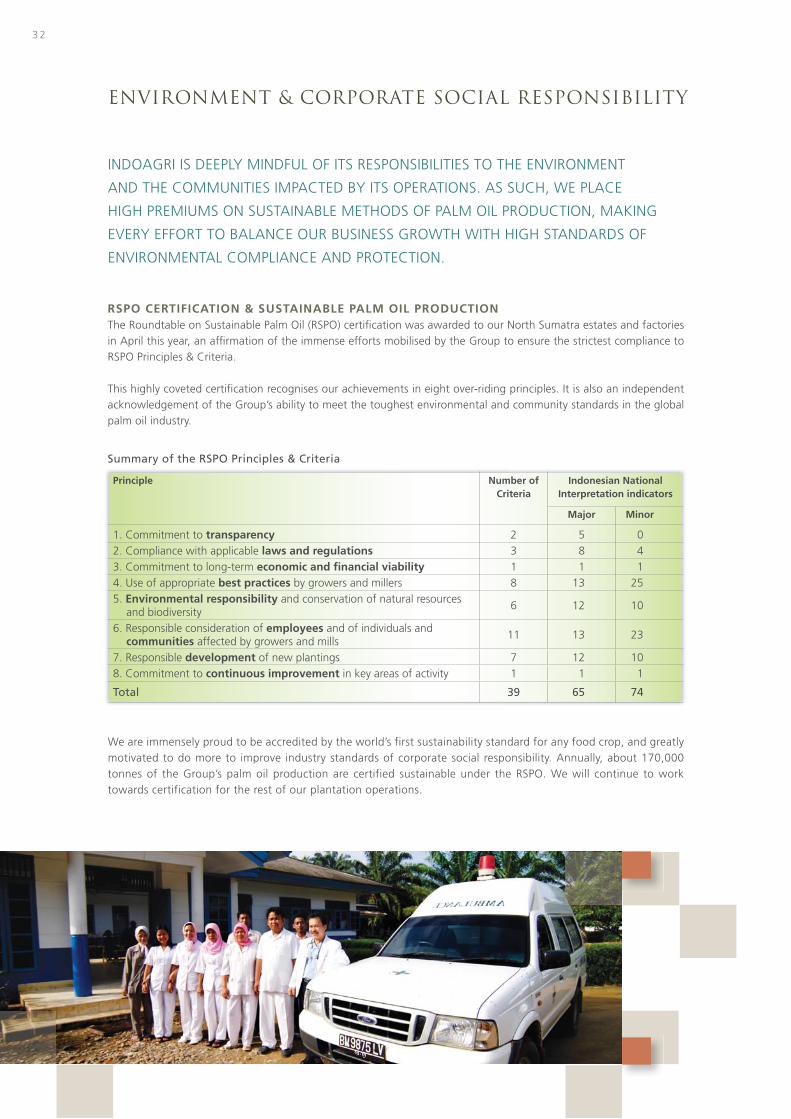

RSPO CERTIFICATION & SUSTAINABLE PALM OIL PRODUCTIONThe Roundtable on Sustainable Palm Oil (RSPO) certifi cation was awarded to our North Sumatra estates and factories in April this year, an affi rmation of the immense efforts mobilised by the Group to ensure the strictest compliance to RSPO Principles & Criteria.

This highly coveted certifi cation recognises our achievements in eight over-riding principles. It is also an independent acknowledgement of the Group’s ability to meet the toughest environmental and community standards in the global palm oil industry.

INDOAGRI IS DEEPLY MINDFUL OF ITS RESPONSIBILITIES TO THE ENVIRONMENT

AND THE COMMUNITIES IMPACTED BY ITS OPERATIONS. AS SUCH, WE PLACE

HIGH PREMIUMS ON SUSTAINABLE METHODS OF PALM OIL PRODUCTION, MAKING

EVERY EFFORT TO BALANCE OUR BUSINESS GROWTH WITH HIGH STANDARDS OF

ENVIRONMENTAL COMPLIANCE AND PROTECTION.

Summary of the RSPO Principles & Criteria

We are immensely proud to be accredited by the world’s first sustainability standard for any food crop, and greatly motivated to do more to improve industry standards of corporate social responsibility. Annually, about 170,000 tonnes of the Group’s palm oil production are certified sustainable under the RSPO. We will continue to work towards certification for the rest of our plantation operations.

3 2

Principle Number of Criteria

Indonesian National Interpretation indicators

Major Minor

1. Commitment to transparency 2 5 02. Compliance with applicable laws and regulations 3 8 43. Commitment to long-term economic and fi nancial viability 1 1 14. Use of appropriate best practices by growers and millers 8 13 255. Environmental responsibility and conservation of natural resources

and biodiversity6 12 10

6. Responsible consideration of employees and of individuals and communities affected by growers and mills

11 13 23

7. Responsible development of new plantings 7 12 108. Commitment to continuous improvement in key areas of activity 1 1 1

Total 39 65 74

As part of efforts to further our cause, the Group’s main operating subsidiaries, PT SIMP and Lonsum, continue to serve as members of the RSPO, helping the RSPO to promote the growth and use of sustainable oil palm products through credible global standards and dialogue with stakeholders in the supply chain.

The Group is also a founding member of the Indonesian National Interpretation Working Group (INA-NIWG), which formulates the interpretation of RSPO Principles & Criteria within the context of the laws and regulations of Indonesia.

ENVIRONMENTALLY FRIENDLY AGRICULTURAL PRACTICESThe Group believes that every conscientious effort can make a positive difference to long-term sustainability. During the year in review, we continued to implement various sustainable agricultural practices across our plantation estates and processing plants.

We adopt a zero burning policy for the clearing of plantation land. Across our plantation operations, fully mechanical methods are deployed for land clearing and replanting – whether to fell trees or to stack them into planting rows. Wherever possible, we encourage the

practice of non-polluting techniques that minimise global warming and preserve the physical properties of soil.

During plantation expansion, we emphasise the management and monitoring of High Conservation Value (HCV) forests in order to protect these areas. Our efforts include the careful mapping of designated HCV zones, monitoring for signs of erosion and training programmes to educate our staff in the identifi cation of various fl ora and fauna.

We have a scheme to recycle all solid and liquid by-products (empty fruit bunch, decanter solid, mill effl uent) at our palm oil mills, reusing them in the fi eld as mulch/irrigation water and fertilizer substitutes. As a result, the use of inorganic fertilizers is greatly reduced.

Since 1997, the innovative use of barn owls has helped to combat the prevalence of rats in our plantations. While traditional pest control methods involving anti-coagulant rodenticides, herbicides and insecticides are effective, creating a natural habitat that favours the rat-hunting instincts of barn owls has enabled us to minimise the release of harmful chemicals into our ecosystem.

A FFB harvestor.

3 3B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

ENVIRONMENT & CORPORATE SOCIAL RESPONSIBILITY

LEVERAGING TECHNOLOGICAL ADVANCEMENTSConcurrently, the Group leverages its strengths in R&D to push the frontiers of environmental sustainability. In particular, we have paid special attention to the study of genomics, tissue culture research and seed breeding to maximise plantation yields in order to increase the productivity of our land bank and resources.

As a result of these technological achievements, the Group successfully registered a patented process for the production of high-yielding F1 oil palm hybrids. The hybrids will alleviate the pressure on usage and expansion of land for palm oil cultivation to satisfy growing global demands.

The Group is currently embarking on plans to commercialise the production of its patented F1 oil palm hybrids. We expect these efforts to bring positive impact to the environment in the next few years.

REACHING OUT TO OUR COMMUNITIESAs one of Indonesia’s largest plantation owners, communities are important stakeholders in our business. In line with the Group’s CSR efforts, we strive to establish mutually benefi cial relationships with these stakeholders through a diversity of community development initiatives.

• Employment: The Group creates jobs for residents in the local and plasma community through a range of direct and indirect employment opportunities. As at 31 December 2009, the Group employs a direct workforce of 29,401 in various capacities.

However, our footprint extends much further than our

29,401 employees, as their families, local communities, plasma farmers, contractors and suppliers all share in the economic benefi t of our operations.

• Education: We continue to promote literacy and a secure future for the next generation by making education accessible through the establishment of schools and scholarships. As at 31 December 2009, the Group sponsors a total of 18 schools, providing free education at elementary and junior high level, and highly subsidised fees at the senior high levels. These efforts have benefi ted close to 8,000 of our employee’s children.

We also contribute learning aids and teaching tools such as textbooks, furniture, science labs and computers for the schools, as well as salaries paid to their teachers and administrative staff.

In 2009, we were extremely heartened when one of our elementary schools was voted the best elementary school, while one of our junior high schools emerged among the top-10 schools in their respective regencies.

3 4

• Health: The health of our employees and their families is a responsibility we take very seriously. Local health clinics and hospitals are often too far away from our plantations for effective medical care. Therefore, we provide public health infrastructure by building medical clinics and emergency care units that extend their services to surrounding communities.

We also organise blood donation drives, promote immunisation programmes and carry out regular fogging to destroy mosquito-breeding areas.

• Infrastructure/Public Facilities: We build and repair roads/bridges to improve transportation access. We also facilitate the construction of public installations for telephone networks, power and water supply.

• Religious: We participate in local customs and contribute to the building and repair of religious infrastructures such as mosques and churches. We also provide religious teachers and distribute Lebaran and Christmas packages to less advantaged families.

• Sports & Youth, Arts & Culture: We contribute facilities for sports and recreation, and organise and/or sponsor local tournaments, musical concerts, cultural activities and religious events to encourage community bonding and team spirit.

• Local Business Development: We support the development of small businesses and offer incentive programmes for local trades such as goat breeding and pallet production.

The Group fully appreciates its symbiotic relationship with its communities and the environment. We remain fi rmly committed to responsible agribusiness practices and sustainable operations, and believe this can be achieved only if our communities grow and develop in tandem with us. As we chart sustainable growth, we will continue to engage and bring value to our community stakeholders.

Our educational programmes promote literacy and a secure future for the next generation.

3 5B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

BOARD OF DIRECTORS

Mr Lee Kwong Foo Edward Chairman and Lead Independent Director

Mr Lee spent 36 years in the Singapore Administrative Service (Foreign Service Branch), during which time he has served as Singapore’s High Commissioner in Brunei Darussalem (1984 to 1990), Ambassador to the Philippines (1990 to 1993) and Ambassador to Indonesia (1994 to June 2006).

Mr Lee was awarded the Public Administration Medal (Silver) in 1996, the Long Service Medal in 1997, the Public Administration Medal (Gold) in 1998 and the Meritorious Service Medal in 2006 by the Singapore Government. He was also awarded the Order of Sikatuna, Rank of Datu (Grand Cross) by the Philippine government in 1993. In 2007, the Indonesian Government awarded him the highest civilian honour, the Bintang Jasa Utama (First Class Order of Services).

Mr Lee holds a Masters of Arts from Cornell University and is the Chief Executive of PT Ekalumintas, an investment consultancy fi rm in Jakarta.

Mr Mark WakefordChief Executive Offi cer and Executive Director

Mr Wakeford is currently the President Director of PT Salim Ivomas Pratama and a director of PT Perusahaan Perkebunan London Sumatra Indonesia Tbk (Lonsum). He started his career with Kingston Smith & Co, a fi rm of Chartered Accountants in London, England. Mr. Wakeford has been in the plantation industry since 1993, working with plantation companies in Indonesia, Papua New Guinea, Soloman Islands and Thailand. He started his plantation career as the Finance Director of Lonsum in 1993, based in Indonesia, before moving to Pacifi c Rim Plantations Limited (PROPL) as the CFO from 1995 to 1999, based in Papua New Guinea. In 1999, Mr. Wakeford became CEO and Executive Director of PROPL. PROPL was sold to Cargill in 2005, and Mr. Wakeford spent one year with Cargill, prior to joining the Company in January 2007.

Mr. Wakeford trained and qualifi ed as a Chartered Accountant in London, England. He also attended the Senior Executive Program at the London Business School.

3 6

Mr Moleonoto Tjang Executive Director and Head of Finance and Corporate Services

Mr Tjang is currently a Vice President Director of PT Salim Ivomas Pratama and a director of PT Perusahaan Perkebunan London Sumatra Indonesia Tbk. He started his career in 1984 with Drs Hans Kartikahadi & Co., a public accounting fi rm in Jakarta. In 1990, he joined the Salim Plantations Group as Manager and became Assistant Vice President (Commercial and Accounting) in 1993. In 1996, he was appointed as Vice President (Finance) of the Salim Plantations Group. He was made CFO of the PT ISM Group’s Plantations Division in 2001 and subsequently the Deputy Head of Corporate Treasury of the PT ISM Group in 2003.

He has a Bachelor of Accountancy degree from the University of Tarumanagara, a degree in Bachelor of Management and a Master of Science in Administration & Business Policy from

the University of Indonesia. Mr Tjang is also a registered accountant in Indonesia.

Mr Gunadi Executive Director and Head of Plantation Operations

Mr Gunadi is currently a director PT Salim Ivomas Pratama. Mr Gunadi started his career in 1977 with Drs Hans Kartikahadi & Co. , a public accounting fi rm in Jakarta. He was with PT Besuki Indah Electric Industry (Luxor), Jakarta in 1979 as Finance Manager before joining PT Lippo Mulia Jakarta in 1980 as Finance and Administration Manager.

From 1981 to 1991, Mr Gunadi was with PT Broco, Jakarta, as Group Finance Director. In 1991, Mr Gunadi joined the Salim Plantations Group (which was subsequently acquired by PT ISM) as Senior Vice President (Finance). In 2004, he was appointed to the position of Chief Operating Offi cer of PT SIMP.

Mr Gunadi has a Bachelor of Accountancy degree from University of Indonesia.

Mr Suaimi SuriadyExecutive Director and Head of Refi nery and Commodity Division

Mr Suriady started his career with an automotive battery distributor, PT Menara Alam Teknik of Astra group and moved on to consumer goods manufacturer, Konica Film and Paper, in 1991. He joined PT Indofood Fritolay Makmur, a JV between Indofood group and Pepsi International, as National Sales Manager in 1994 and was promoted to Sales and Marketing Manager in 1997. Before his appointment as President Director in PT Indofood Fritolay Makmur in 2002, he worked as the Branch Manager of the Noodle Division of PT Indofood Sukses Makmur Tbk from Jan 2000 to April 2002.

Mr Suaimi has a MBA degree from De Montfort University, United Kingdom.

3 7B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

BOARD OF DIRECTORS

Mr Tjhie Tje Fie Non-executive Director

Mr Tjhie is currently the director of PT Indofood Sukses Makmur Tbk and PT Indofood CBP Sukses Makmur, as well as the Head of Treasury Division of these companies. In addition, he is currently vice President Director of PT Salim Ivomas Pratama and a director of PT Perusahaan Perkebunan London Sumatra Indonesia Tbk. Previously, he was director of PT Indomiwon Citra Inti and senior executive of PT Kitadin Coal Mining.

Mr Tjhie was awarded a Bachelor’s degree in Accountancy from the Perbanas School of Economics.

Mr Axton SalimNon-Executive Director

Mr Axton is currently the director of PT IndoFood Sukses Makmur Tbk and PT Indofood CBP Sukses Makmur. In addition, he is currently a commissioner of PT Perusahaan Perkebunan London Sumatra Indonesia Tbk.

Mr Axton has a Degree in Bachelor of Science, Business Administration from University of Colorado.

Mr Lim Hock San Independent Director

Mr Lim is presently the President and CEO of United Industrial Corporation Limited and Singapore Land Limited. He is also the Non-executive Chairman and Independent Director of Gallant Venture Ltd. Mr Lim started his career in 1966 with the then Inland Revenue Department of Singapore. He became an Accountant at Mobil Oil Malaya Sdn Bhd in 1967 before joining the Port of Singapore Authority in 1968, where he served in various management positions. From 1975 to 1992, he was with the Civil Aviation Authority of Singapore and fi nally promoted to the position of the Director-General. He has a Bachelor of Accountancy degree from the then University of Singapore, a Master of Science (Management) degree from the Massachusetts Institute of Technology and attended the Advanced Management Program at Harvard Business School. He is a Fellow of The Chartered Institute of Management Accountants (UK) and a Fellow and past President of the Institute of Certifi ed Public Accountants of Singapore. He is also a recipient of the Singapore Government Meritorious Service Medal, the Public Administration Medal (Gold) and the Public Service Medal.

3 8

Mr Hendra Susanto Independent Director

Mr Susanto began his career with the Standard Chartered Bank as an Account Relationship Manager of the Corporate Banking division in 1990. He joined PT BNP Lippo Leasing in 1993 as the Head of the Corporate Marketing division. In 1996, he joined PT ING Indonesia Bank as Vice President in the Project and Structured Finance division and was subsequently promoted to Director in the Wholesale Banking division of the bank. Mr Susanto also acted as the Chief Representative of ING Bank N.V. in Indonesia until 2005.

Mr Susanto has a Bachelor of Computer Science degree and a Master of Commerce degree from the University of New South Wales, Australia.

Mr Goh Kian Chee Independent Director

Mr Goh is presently the CFO of National University of Singapore, Centre For The Arts (NUS). He is also an independent director of AsiaMedic Limited, in which the Salim Group has a shareholding interest. Mr Goh started his career in 1979 as an audit trainee with Goldblatt & Co (UK). He joined American International Assurance Pte Ltd in 1981 as an Accounting Supervisor. In 1982, he became a Regional Internal Auditor in Mobil Oil Singapore Pte Ltd and rose to the position of Regional Credit and Insurance Manager in 1987. In 1990, he joined Mobil Petrochemicals International Ltd where he served as Regional Accounting Manager and later, as the Financial Controller of the Asia Pacifi c region. Before his present position in NUS, Mr Goh was the Regional Vice President & Controller as well as an Executive Director of John Hancock International Pte Ltd.

Mr Goh has a Bachelor of Arts (Hons) degree in Accounting and Economics from Middlesex University (London, United Kingdom).

3 9B U I L D I N G S U S T A I N A B L E G R O W T HINDOFOOD AGRI RESOURCES LTD. ANNUAL REPORT 2009

CORPORATE INFORMATION

EXECUTIVE COMMITTEEMark Wakeford (Chairman)

Tjhie Tje Fie

Moleonoto Tjang

Gunadi

Suaimi Suriady

AUDIT COMMITTEEGoh Kian Chee (Chairman)

Lim Hock San

Hendra Susanto

NOMINATING COMMITTEELee Kwong Foo Edward (Chairman)

Tjhie Tje Fie

Lim Hock San

Hendra Susanto

REMUNERATION COMMITTEELim Hock San (Chairman)

Tjhie Tje Fie

Goh Kian Chee

REGISTRARBoardroom Corporate &

Advisory Services Pte. Ltd.

50 Raffl es Place

Singapore Land Tower #32-01,

Singapore 048623

REGISTERED OFFICE8 Eu Tong Sen Street

#16-96/97 The Central

Singapore 059818

Chairman and Lead Independent Director Lee Kwong Foo Edward

Chief Executive Offi cer and Executive Director Mark Wakeford

Executive Director and Head of Finance and Corporate Services

Moleonoto Tjang

Executive Director and Head of Plantation Operations

Gunadi

Executive Director and Head of Refi nery and Commodity

Suaimi Suriady

Non-Executive Director Tjhie Tje Fie

Non-Executive Director Axton Salim

Independent Director Lim Hock San

Independent Director Goh Kian Chee

Independent Director Hendra Susanto

DIRECTORS

COMPANY SECRETARIESLee Siew Jee, Jennifer

Mak Mei Yook

AUDITORSErnst & Young LLP

One Raffl es Quay

North Tower, Level 18

Singapore 048583

AUDIT PARTNERVincent Toong Weng Sum (appointed 20 April 2007)

4 0

CORPORATE GOVERNANCE