24

Financial Projections for Presentations September 19, 2013

| Date post: | 12-Jul-2015 |

| Category: |

Business |

| Upload: | the-capital-network |

| View: | 696 times |

| Download: | 1 times |

Financial Projections for Presentations September 19, 2013

Heather Onsto,

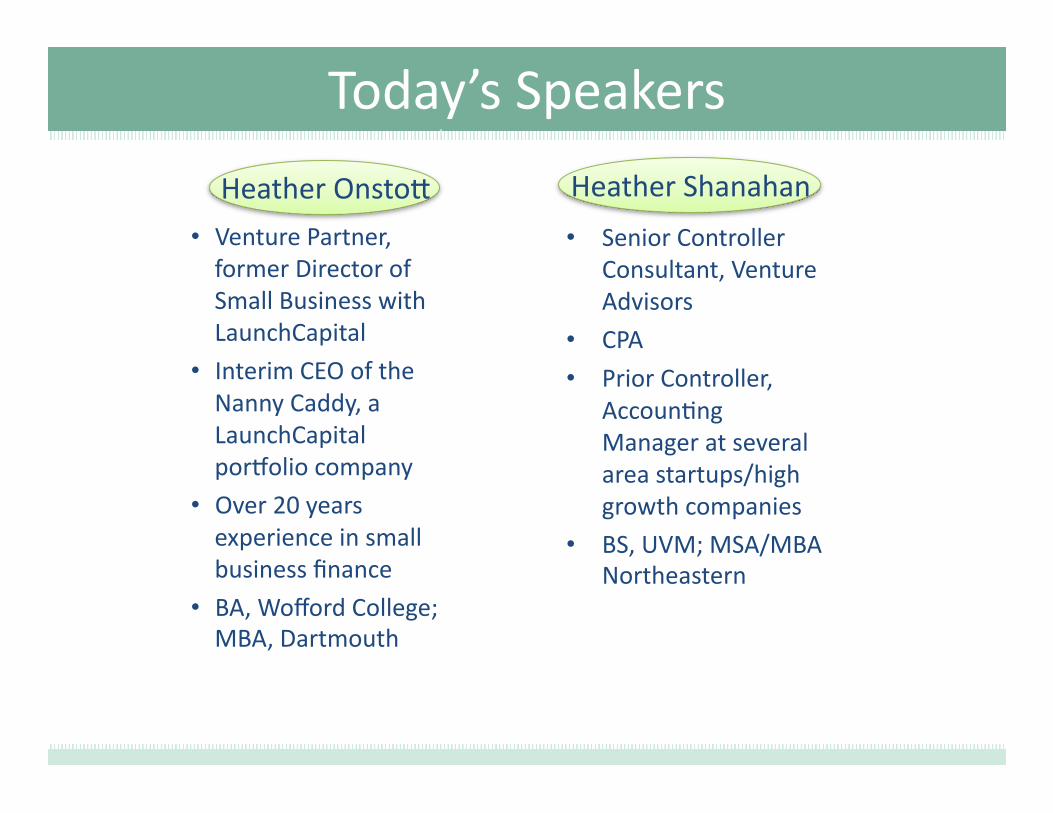

Today’s Speakers

• Senior Controller Consultant, Venture Advisors

• CPA

• Prior Controller, Accoun>ng Manager at several area startups/high growth companies

• BS, UVM; MSA/MBA Northeastern

• Venture Partner, former Director of Small Business with LaunchCapital

• Interim CEO of the Nanny Caddy, a LaunchCapital porMolio company

• Over 20 years experience in small business finance

• BA, Wofford College; MBA, Dartmouth

Heather Shanahan

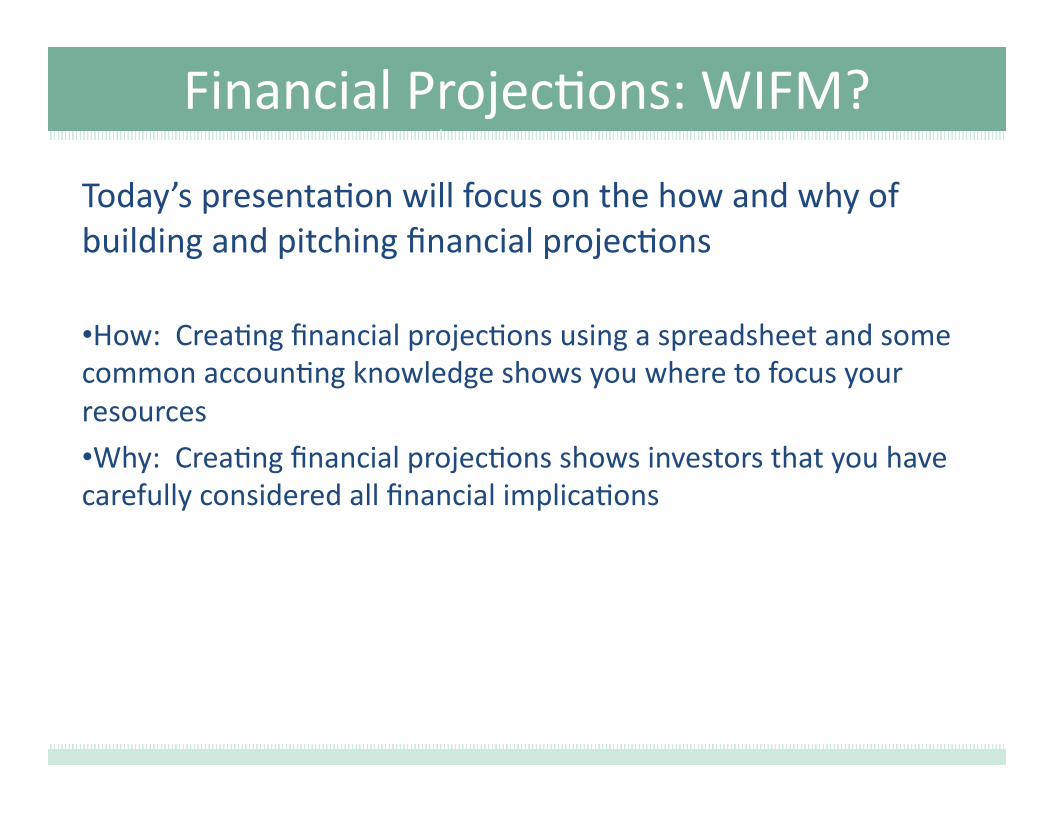

Financial Projec>ons: WIFM?

Today’s presenta>on will focus on the how and why of building and pitching financial projec>ons

• How: Crea>ng financial projec>ons using a spreadsheet and some common accoun>ng knowledge shows you where to focus your resources

• Why: Crea>ng financial projec>ons shows investors that you have carefully considered all financial implica>ons

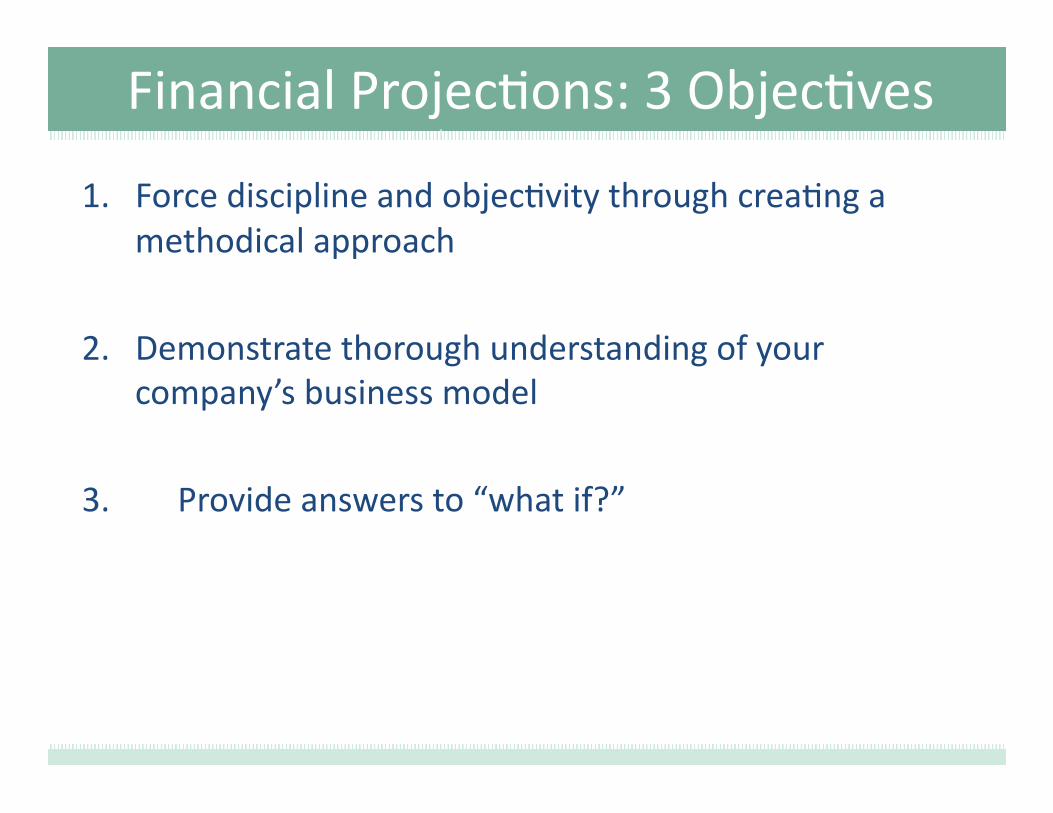

Financial Projec>ons: 3 Objec>ves

1. Force discipline and objec>vity through crea>ng a methodical approach

2. Demonstrate thorough understanding of your company’s business model

3. Provide answers to “what if?”

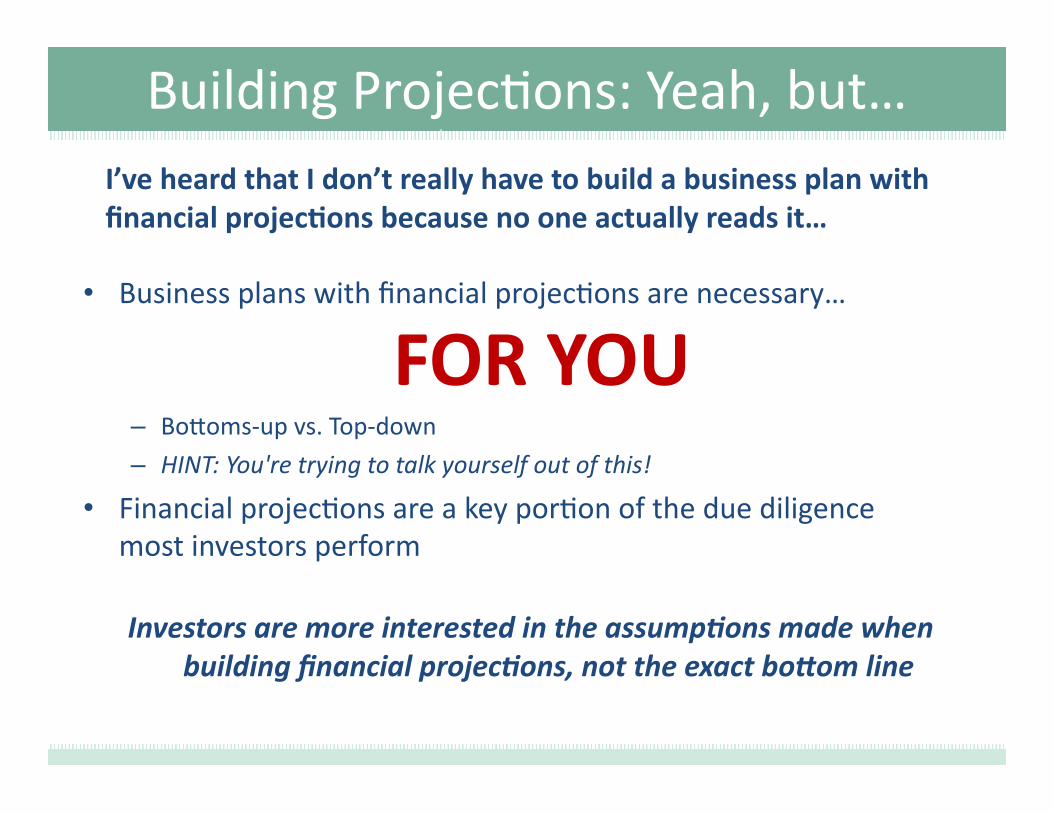

Building Projec>ons: Yeah, but… I’ve heard that I don’t really have to build a business plan with financial projec8ons because no one actually reads it…

• Business plans with financial projec>ons are necessary…

– Bo,oms-‐up vs. Top-‐down

– HINT: You're trying to talk yourself out of this! • Financial projec>ons are a key por>on of the due diligence

most investors perform

FOR YOU

Investors are more interested in the assump1ons made when building financial projec1ons, not the exact bo;om line

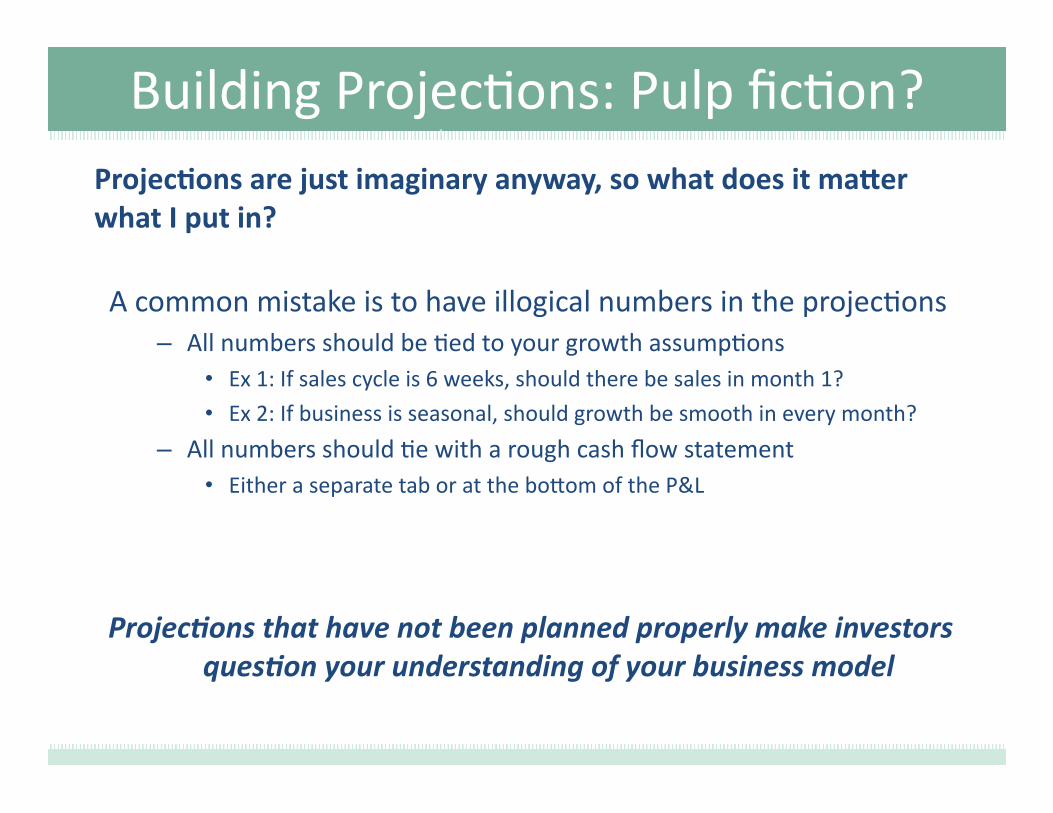

Building Projec>ons: Pulp fic>on? Projec8ons are just imaginary anyway, so what does it maCer what I put in?

A common mistake is to have illogical numbers in the projec>ons – All numbers should be >ed to your growth assump>ons

• Ex 1: If sales cycle is 6 weeks, should there be sales in month 1?

• Ex 2: If business is seasonal, should growth be smooth in every month?

– All numbers should >e with a rough cash flow statement • Either a separate tab or at the bo,om of the P&L

Projec1ons that have not been planned properly make investors ques1on your understanding of your business model

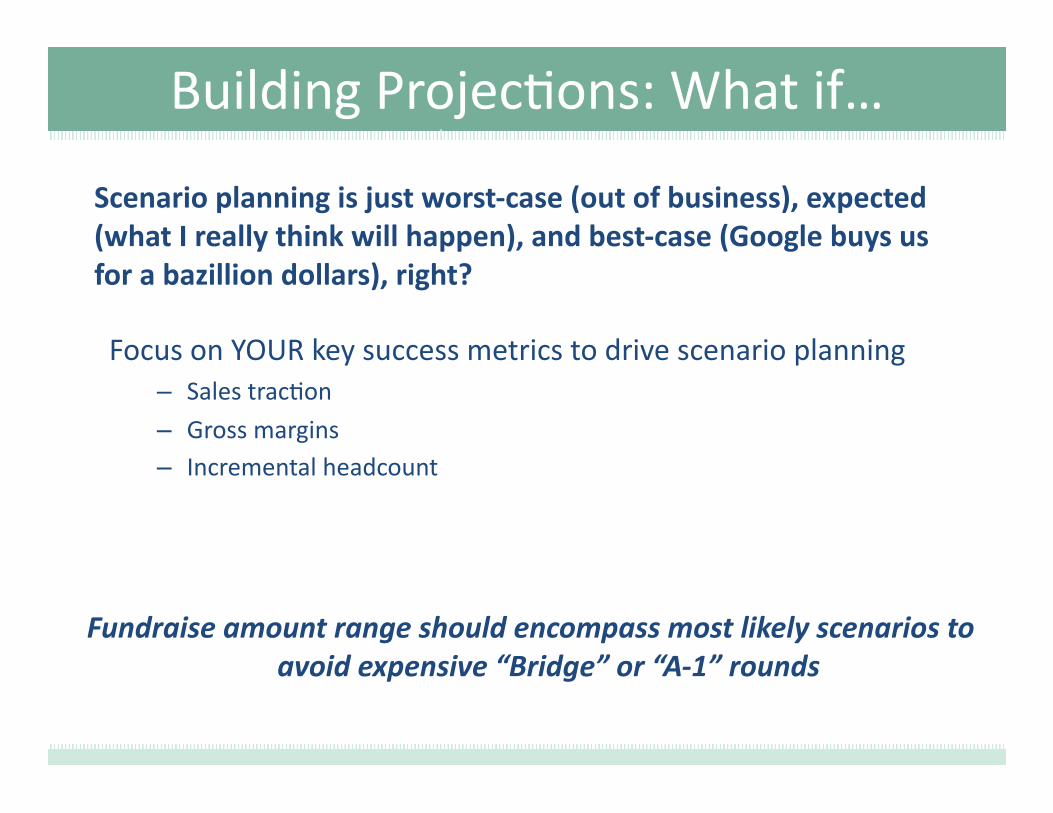

Building Projec>ons: What if…

Scenario planning is just worst-‐case (out of business), expected (what I really think will happen), and best-‐case (Google buys us for a bazillion dollars), right?

Focus on YOUR key success metrics to drive scenario planning – Sales trac>on – Gross margins – Incremental headcount

Fundraise amount range should encompass most likely scenarios to avoid expensive “Bridge” or “A-‐1” rounds

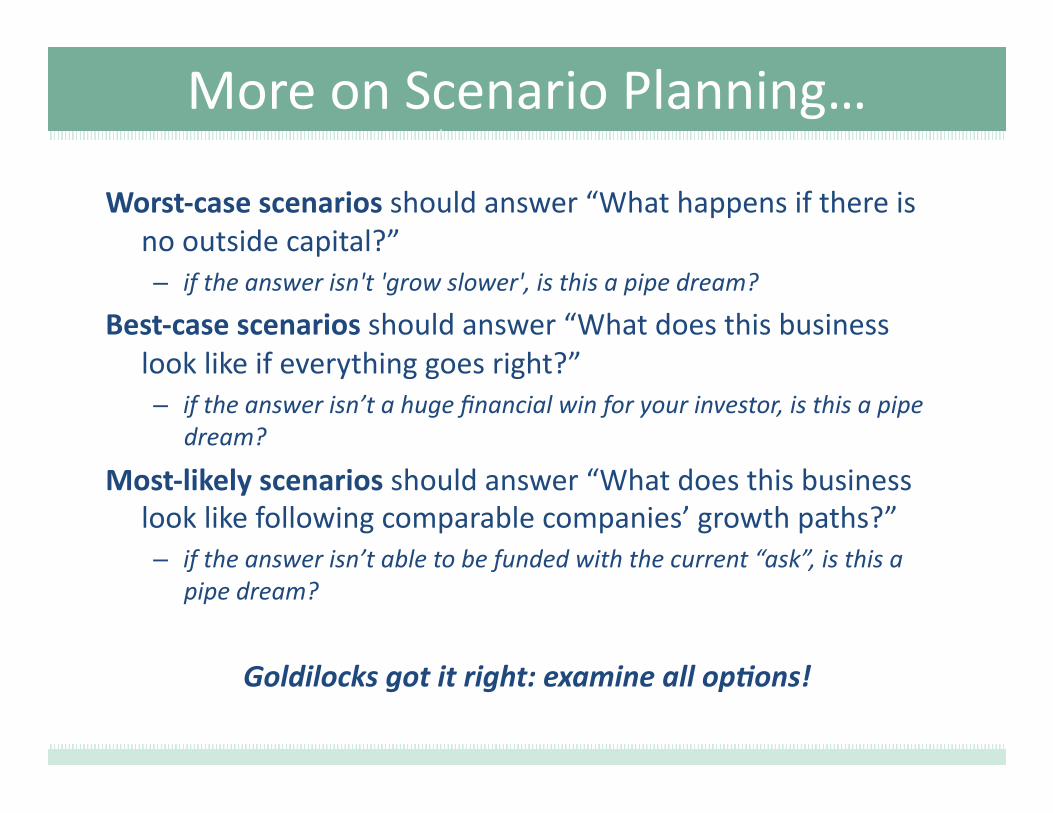

More on Scenario Planning…

Worst-‐case scenarios should answer “What happens if there is no outside capital?” – if the answer isn't 'grow slower', is this a pipe dream?

Best-‐case scenarios should answer “What does this business look like if everything goes right?” – if the answer isn’t a huge financial win for your investor, is this a pipe

dream?

Most-‐likely scenarios should answer “What does this business look like following comparable companies’ growth paths?” – if the answer isn’t able to be funded with the current “ask”, is this a

pipe dream?

Goldilocks got it right: examine all op1ons!

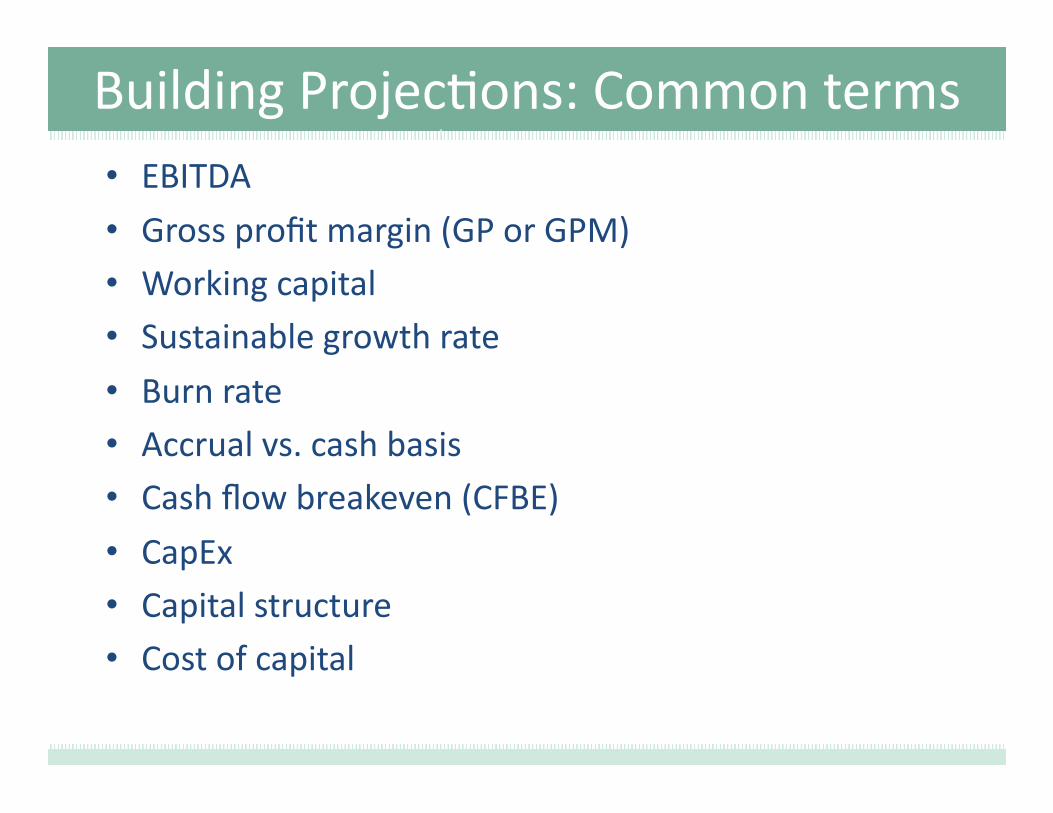

Building Projec>ons: Common terms • EBITDA • Gross profit margin (GP or GPM) • Working capital • Sustainable growth rate • Burn rate • Accrual vs. cash basis • Cash flow breakeven (CFBE) • CapEx • Capital structure • Cost of capital

Building Projec>ons: How it works

• Have an assump8ons page and reference cells for your P&L (don’t hard code anything)

• A separate assump>ons page allows flexibility – change them for different growth scenarios

• Assump>ons are the backbone of your projec>ons, so you should know them COLD

Excel is your friend, but be careful with cell references – it’s easy to make a mistake!

Building Projec>ons: Proper start…?

Es>mate 1% of $100 bazillion market

share

Building Projec>ons: Proper start…?

Es>mate 1% of $100 bazillion market

share JUST

KIDDING!

Projec>ons: Start with Revenue

Take a “Bo,oms Up” approach

• Ex: We have tracked X unique visitors to our website and with an industry averages 2% conversion rate, sales will be Y.

• Ex: Survey revealed customers are willing to pay $X for a product with Y features.

• Ex: Q4 sales were $X. With a customer acquisi>on cost of $Y, we expect a 20% growth rate as a result of marke>ng efforts

Econ 101: revenue = price * volume. Knowing which element is driving your company’s revenue is a key metric.

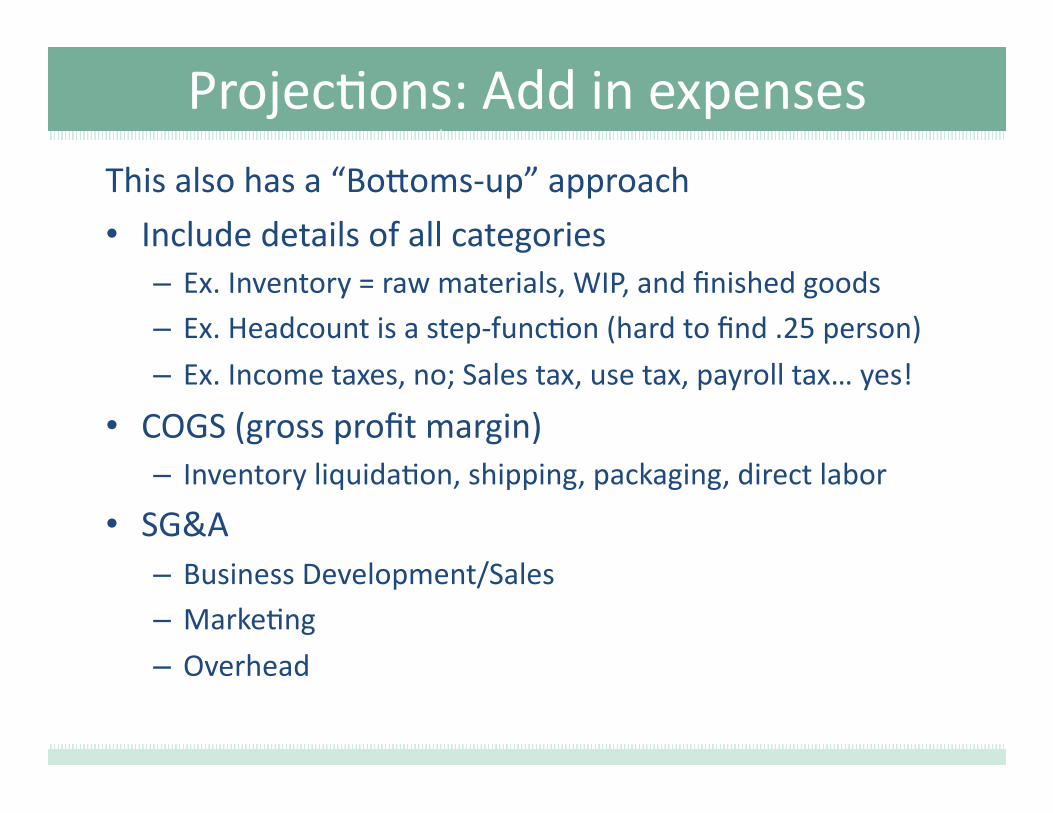

Projec>ons: Add in expenses This also has a “Bo,oms-‐up” approach

• Include details of all categories – Ex. Inventory = raw materials, WIP, and finished goods – Ex. Headcount is a step-‐func>on (hard to find .25 person) – Ex. Income taxes, no; Sales tax, use tax, payroll tax… yes!

• COGS (gross profit margin) – Inventory liquida>on, shipping, packaging, direct labor

• SG&A – Business Development/Sales – Marke>ng

– Overhead

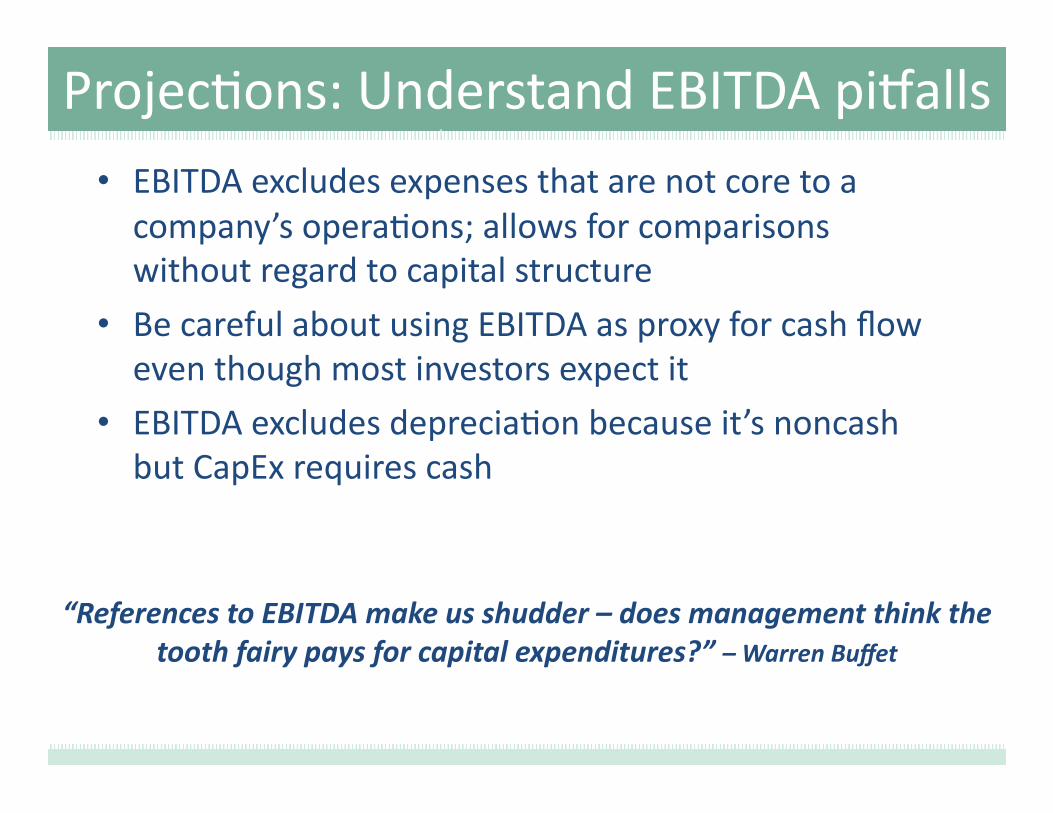

Projec>ons: Understand EBITDA piMalls

• EBITDA excludes expenses that are not core to a company’s opera>ons; allows for comparisons without regard to capital structure

• Be careful about using EBITDA as proxy for cash flow even though most investors expect it

• EBITDA excludes deprecia>on because it’s noncash but CapEx requires cash

“References to EBITDA make us shudder – does management think the tooth fairy pays for capital expenditures?” – Warren Buffet

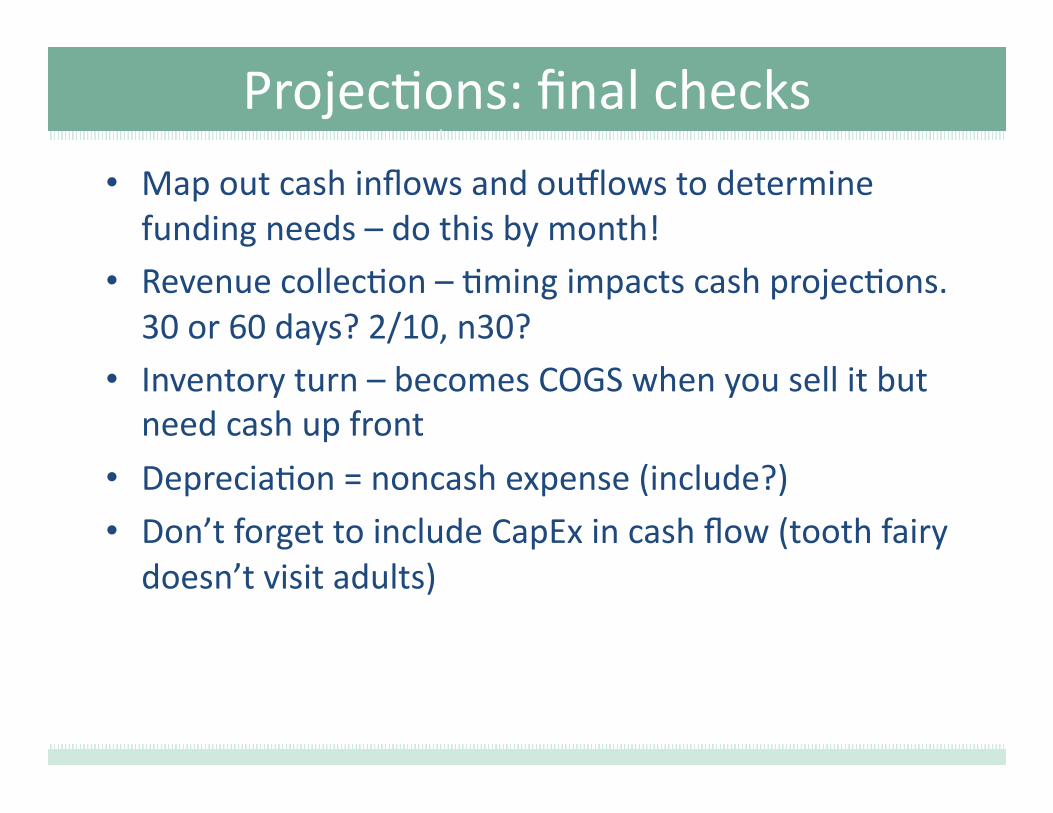

Projec>ons: final checks

• Map out cash inflows and ouMlows to determine funding needs – do this by month!

• Revenue collec>on – >ming impacts cash projec>ons. 30 or 60 days? 2/10, n30?

• Inventory turn – becomes COGS when you sell it but need cash up front

• Deprecia>on = noncash expense (include?) • Don’t forget to include CapEx in cash flow (tooth fairy doesn’t visit adults)

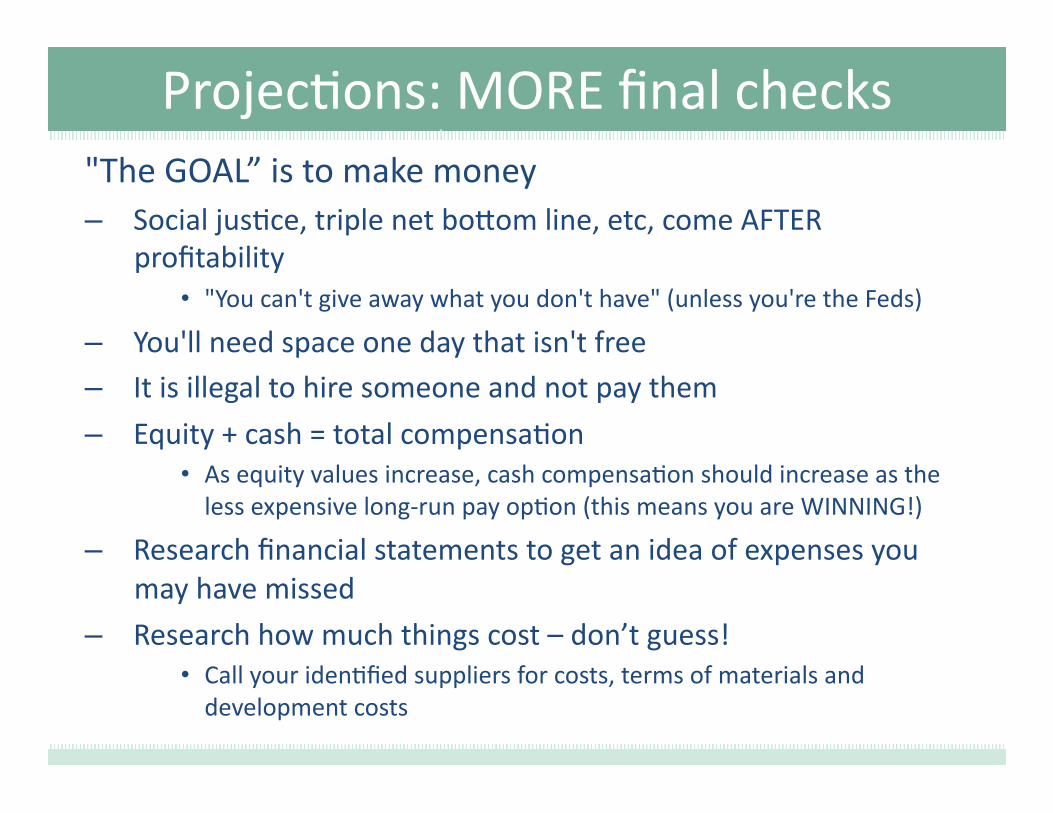

"The GOAL” is to make money – Social jus>ce, triple net bo,om line, etc, come AFTER

profitability • "You can't give away what you don't have" (unless you're the Feds)

– You'll need space one day that isn't free – It is illegal to hire someone and not pay them

– Equity + cash = total compensa>on • As equity values increase, cash compensa>on should increase as the less expensive long-‐run pay op>on (this means you are WINNING!)

– Research financial statements to get an idea of expenses you may have missed

– Research how much things cost – don’t guess! • Call your iden>fied suppliers for costs, terms of materials and development costs

Projec>ons: MORE final checks

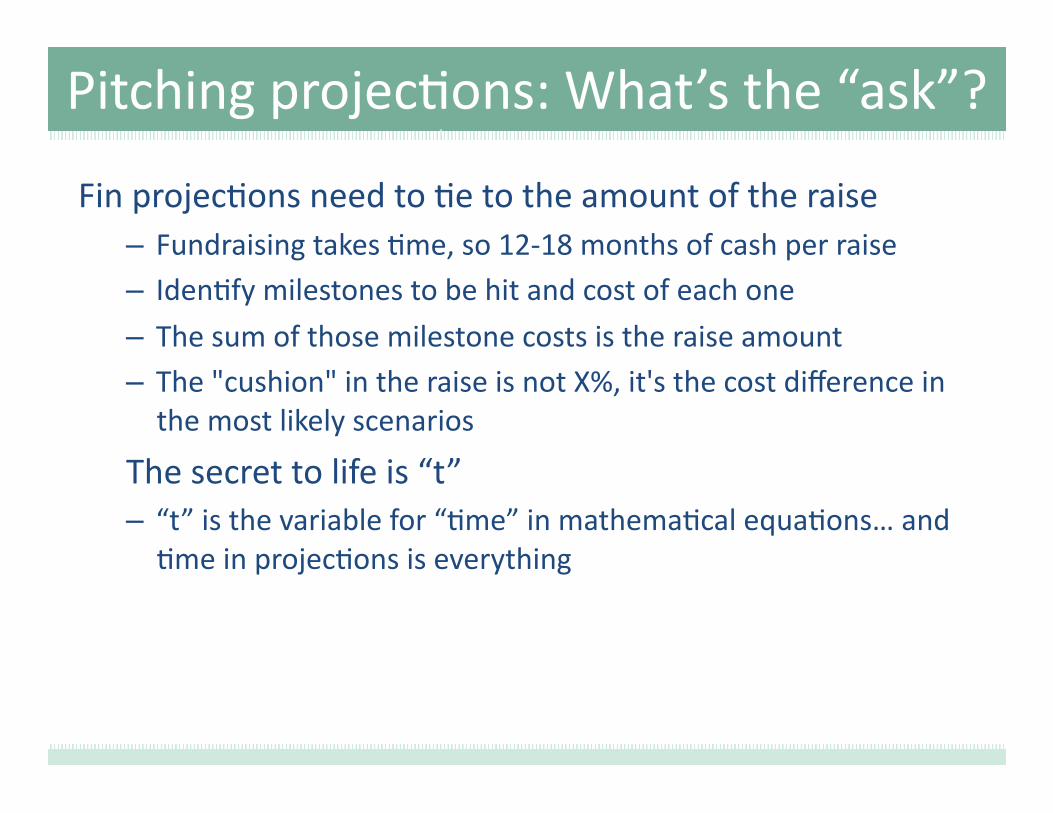

Pitching projec>ons: What’s the “ask”?

Fin projec>ons need to >e to the amount of the raise – Fundraising takes >me, so 12-‐18 months of cash per raise – Iden>fy milestones to be hit and cost of each one

– The sum of those milestone costs is the raise amount – The "cushion" in the raise is not X%, it's the cost difference in the most likely scenarios

The secret to life is “t” – “t” is the variable for “>me” in mathema>cal equa>ons… and >me in projec>ons is everything

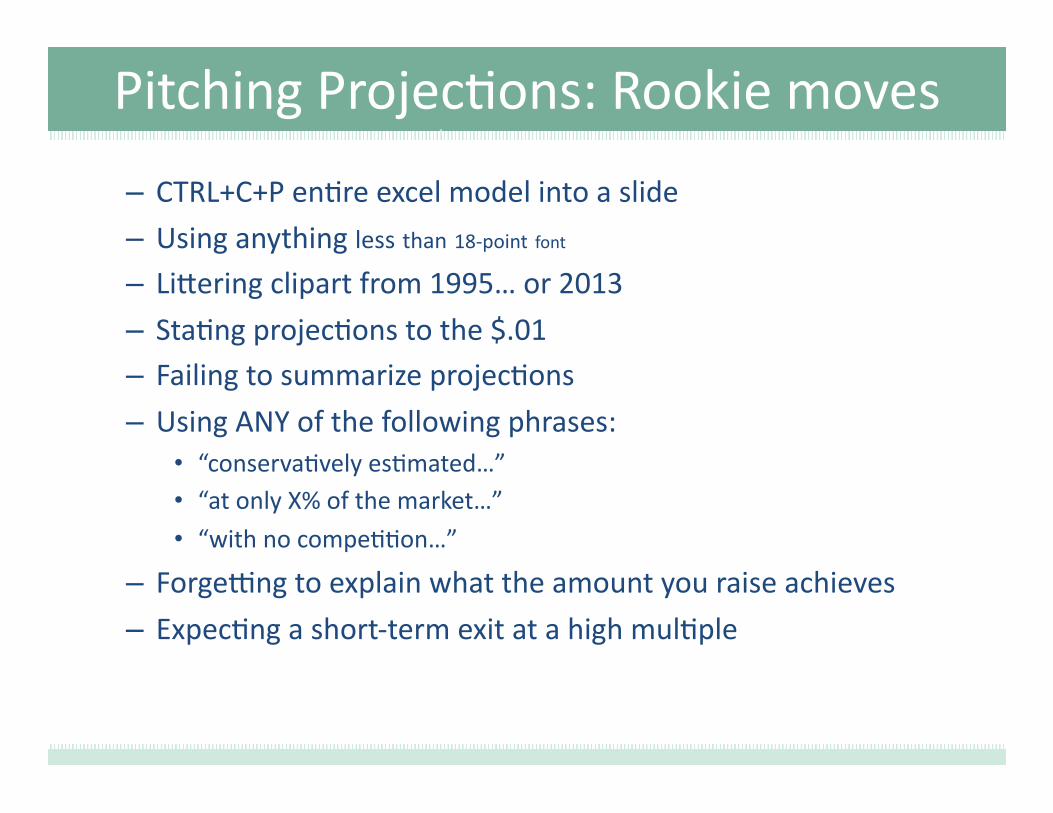

Pitching Projec>ons: Rookie moves

– CTRL+C+P en>re excel model into a slide

– Using anything less than 18-‐point font – Li,ering clipart from 1995… or 2013

– Sta>ng projec>ons to the $.01 – Failing to summarize projec>ons

– Using ANY of the following phrases: • “conserva>vely es>mated…” • “at only X% of the market…”

• “with no compe>>on…”

– Forgexng to explain what the amount you raise achieves

– Expec>ng a short-‐term exit at a high mul>ple

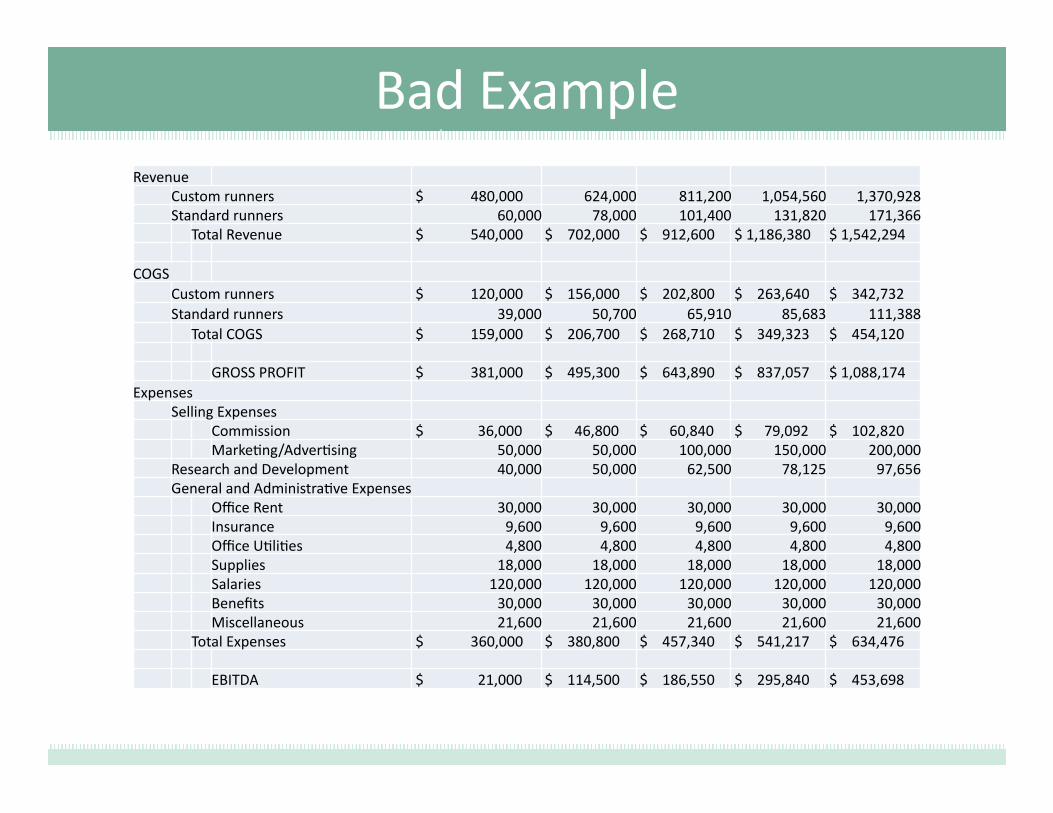

Bad Example Revenue

Custom runners $ 480,000 624,000 811,200 1,054,560 1,370,928 Standard runners 60,000 78,000 101,400 131,820 171,366

Total Revenue $ 540,000 $ 702,000 $ 912,600 $ 1,186,380 $ 1,542,294

COGS Custom runners $ 120,000 $ 156,000 $ 202,800 $ 263,640 $ 342,732 Standard runners 39,000 50,700 65,910 85,683 111,388

Total COGS $ 159,000 $ 206,700 $ 268,710 $ 349,323 $ 454,120

GROSS PROFIT $ 381,000 $ 495,300 $ 643,890 $ 837,057 $ 1,088,174 Expenses

Selling Expenses Commission $ 36,000 $ 46,800 $ 60,840 $ 79,092 $ 102,820 Marke>ng/Adver>sing 50,000 50,000 100,000 150,000 200,000

Research and Development 40,000 50,000 62,500 78,125 97,656 General and Administra>ve Expenses

Office Rent 30,000 30,000 30,000 30,000 30,000 Insurance 9,600 9,600 9,600 9,600 9,600 Office U>li>es 4,800 4,800 4,800 4,800 4,800 Supplies 18,000 18,000 18,000 18,000 18,000 Salaries 120,000 120,000 120,000 120,000 120,000 Benefits 30,000 30,000 30,000 30,000 30,000 Miscellaneous 21,600 21,600 21,600 21,600 21,600

Total Expenses $ 360,000 $ 380,800 $ 457,340 $ 541,217 $ 634,476

EBITDA $ 21,000 $ 114,500 $ 186,550 $ 295,840 $ 453,698

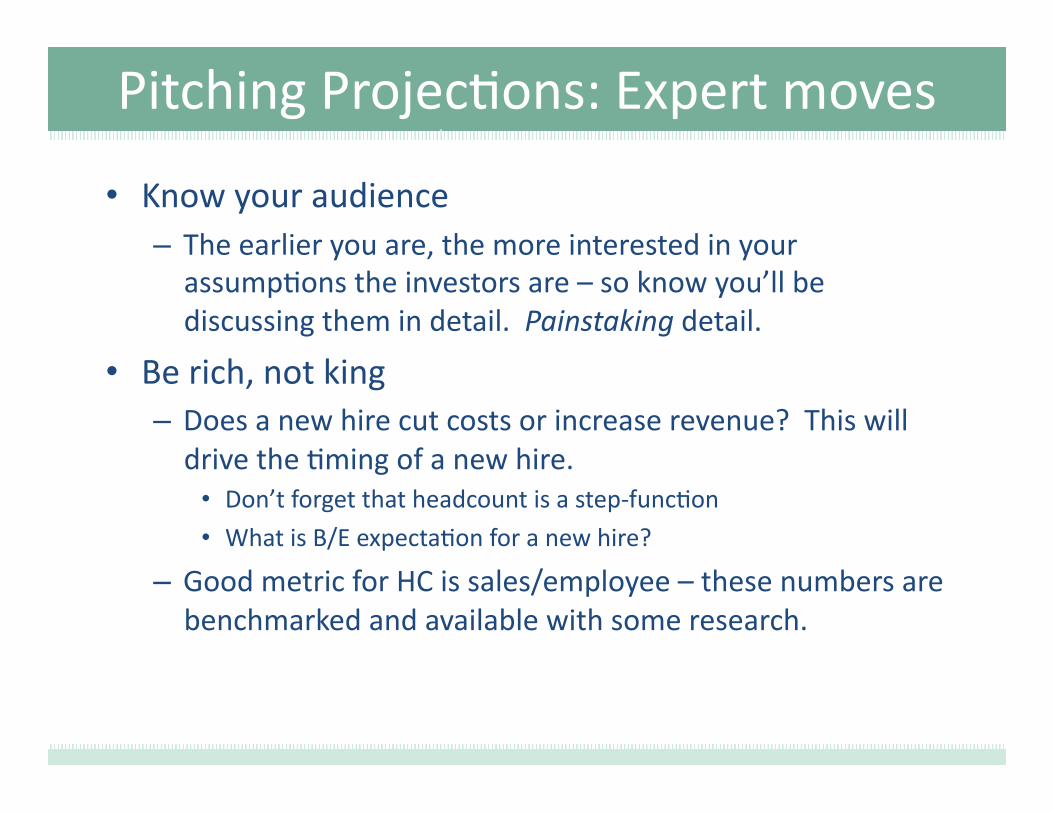

Pitching Projec>ons: Expert moves

• Know your audience – The earlier you are, the more interested in your assump>ons the investors are – so know you’ll be discussing them in detail. Painstaking detail.

• Be rich, not king – Does a new hire cut costs or increase revenue? This will drive the >ming of a new hire.

• Don’t forget that headcount is a step-‐func>on • What is B/E expecta>on for a new hire?

– Good metric for HC is sales/employee – these numbers are benchmarked and available with some research.

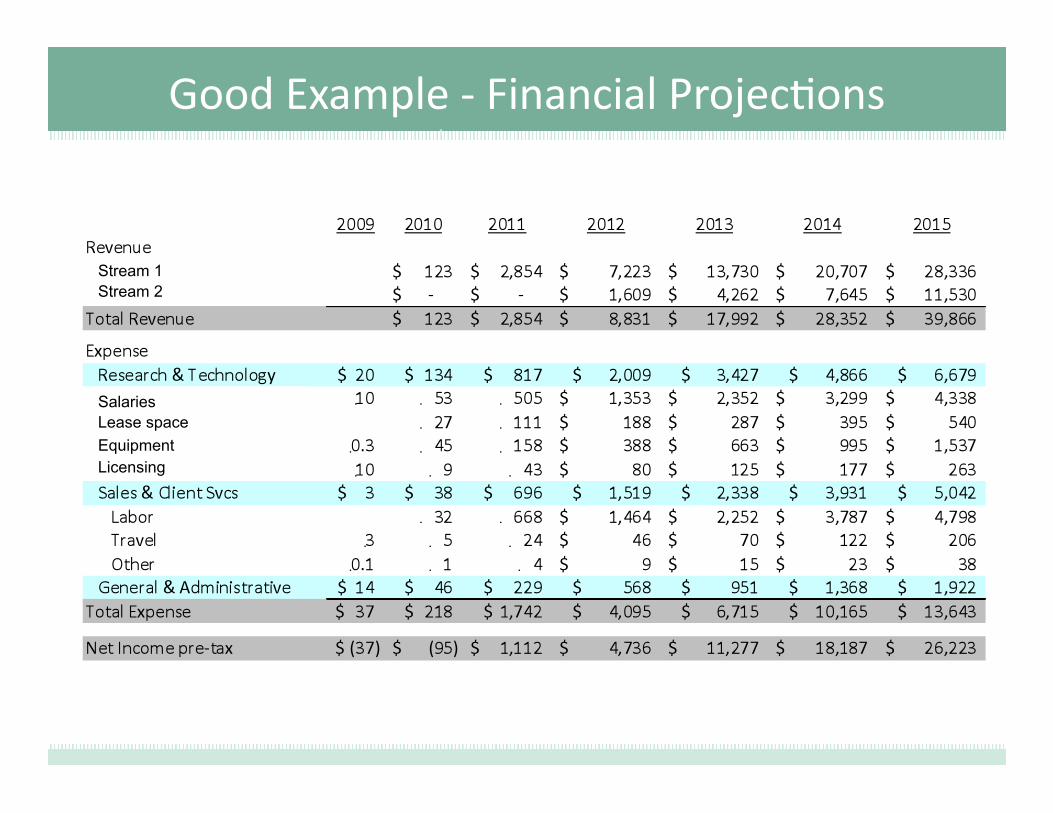

Good Example -‐ Financial Projec>ons

Stream 2

Licensing

Stream 1

Equipment Lease space Salaries

23

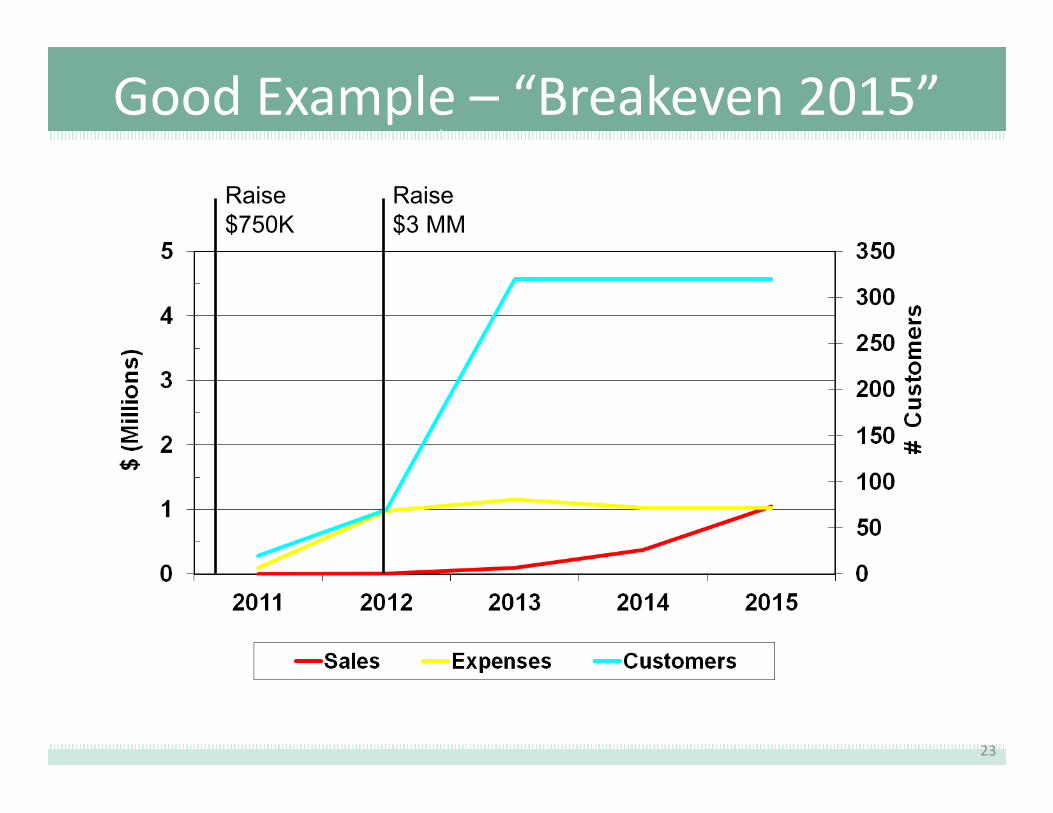

Good Example – “Breakeven 2015”

Raise $750K

Raise $3 MM