34

Canadian Institute of Actuaries L’Institut canadien des actuaires 2009 General Meeting ● Assemblée générale 2009 Ottawa, Ontario ● Ottawa (Ontario)

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires

2009 General Meeting ● Assemblée générale 2009Ottawa, Ontario ● Ottawa (Ontario)

2009 General Meeting ● Assemblée générale 2009Ottawa, Ontario ● Ottawa (Ontario)

Agenda• Insurance contracts measurement –

IFRS Phase II update• IAS 39 (Financial Instruments)

revisions• Appendix I - Field Testing • Appendix II - Comparison of

Management Candidates• Appendix III - Summary of tentative

decisions – November 2009

2

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

IFRS – Insurance Contracts Project

• IASB developing IFRS for insurance contracts as accounting for insurance contracts differs from practices in other sectors

• Project split into two phases:• Phase I: IASB issued IFRS 4 – Insurance Contracts,

interim standard that permits a wide variety of accounting practices for insurance contracts

• Phase II (Current Phase): Development of a standard that replaces interim standard and will provide a basis for consistent accounting for insurance contracts

• IASB and Financial Accounting Standards Board (FASB) taking building block approach to develop accounting

3

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

IASB — discussion paper issued

Insurance Contracts Project - Timelines

FASB — invitation

to comment

2005 2006 2007 2008 2009 2010 2011 2012 2013

April JuneMay November

August

End of comment periods (IASB and FASB)

Exposure draft Final standard

Implementation date

ImplementationPhase 2Phase 1

FASB — Joined the project

October

IFRS 4 Insurance Contracts devised

JanuaryJanuary Jan. thru Dec.

IASB and FASB meetings to develop accounting standards

4

Insurance Contracts Project – Contract Measurement

The boards discussed two measurement approaches for insurance contracts: Measurement approach based on approach being

developed in the IASB’s project to amend IAS 37 Provisions, Contingent Liabilities and Contingent Assets IASB tentatively selected updated model being

developed in the project to amend IAS 37, modified to exclude day one gains.

Current fulfillment value with a composite margin FASB affirmed tentatively that the objective of

liability measurement is to report a value based on the insurer’s fulfillment of its contractual obligations to its policyholders over time

January 2010 exposure draft will explain both of the above measurement approaches

IASB tentatively decided on unearned premium approach for short-duration contracts

5

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Current Candidates for Measurement Model

The amount the entity would rationally pay to be relieved of an obligation (a transfer notion).

A “residual” margin”, based on the day one difference, is added.

The expected present value of the cost of fulfilling the obligation to the policyholder over time (a settlement notion, excluding the cost of bearing risk).

A “composite margin”, based on the day one difference, is added.

May include a risk margin.

Discounted current estimate of future cash flows

Risk margin

Service margin

Residual margin

Insurance liability

Discounted current estimate of future cash flows

CompositeMargin

The part of the premiums for the unexpired part of the insurer’s contractual obligation, subject to a liability adequacy test.

This model would probably only apply to the pre-claims period.

An unearned premium model may be favoured for certain short duration contracts.

Updated IAS 37 model Current fulfilment value with composite margin

Unearned premium

6

Insurance Contracts Project – Risk Margin

The IASB tentatively decided that that a risk margin should be shown separately from the rest of the margin and remeasured at each reporting period.

FASB tentatively decided that no risk margin should be included in the measurement of an insurance contract. The FASB believed that a risk margin conflicted with

the basic principles in CON 7 The FASB has received additional information

regarding risk margin and now are considering a risk margin.

The FASB is troubled by the wording of the proposed IAS 37 model as the definition implies a transfer notion.

The FASB to review updated IAS 37 definition and provide the IASB with suggested changes.

7

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Key issues that need to be resolved before an Exposure Draft

Measurement, including Measurement objective Margins Embedded derivatives

Unbundling Presentation, including the use of other comprehensive income Policyholder participation Margins Participating, unit-linked and index-linked insurance contracts and

investment contracts and universal life contracts Business Combinations Definition and scope (including consideration of whether to deal

with policyholder accounting) Disclosures Reinsurance Transition Sweep issues 8

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• IAS 37 model• Price you would rationally pay to be relieved of the

obligations• Fulfilment value

• How much it would cost you to fulfil the obligations • In the absence of evidence to the contrary (e.g., could

transfer to a third party at a lower amount), IAS 37 model would default to fulfilment value

9

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Approaches have the same building blocks• Current estimate of expected present value of future cash

flows• Time value of money• An explicit margin

• Both are from the perspective of the insurer, so both include entity-specific cash flows (one problem with exit value)

• Both look like PPM

10

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Current estimate of expected present value of future cash flows:

• Current estimates means use all information available and update for new information

• Use market information where relevant• “Expected present value” means probability-weighted (vs.

present value of the best estimate of cash flows)• Changes in estimates flow through profit or loss

• Canadian methods already do this

11

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Future premiums – which can be included? • IASB leaning towards including future renewal premiums

as part of the current contract (vs. customer intangible asset)

• Renewal/cancellation is an option the insurer is providing to policyholders

• Renewal premiums would be included up to the point where entity has an unconditional right to re-underwrite or re-price or cancel the contract

• Similar to our ‘term of the liability’ concept• Whether excess premiums (e..g, UL) could be included or

not is still up in the air

12

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• No front-ending of profits will be allowed in any case• Consistent with IASB’s position on revenue recognition

(not until contract is delivered)• Margin to be calibrated to initial premium

13

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Will be strain at issue• Acquisition expenses are expensed when incurred (i.e., no

DAC asset)• FASB has decided to allow no recognition of revenue to

offset acquisition expenses• IASB originally decided to allow recognition of revenue to

offset direct incremental acquisition expenses, but recently changed to agree with FASB

• Any allowance would be viewed as an exception for the insurance industry

14

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Margins - separate or composite?• IAS 37 model includes separate margins for risk, service

(if any), and ‘residual’ for elimination of day one gains• Runoff pattern of residual margin undecided

• Fulfilment value includes a composite margin only• Runoff pattern of composite margin undecided• FASB is reconsidering whether ‘risk’ (uncertainty)

margin should be separate

15

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Risk margin in IAS 37 model• Value to the entity of not having to bear the risk in the

expected cash flows• Remeasured at each reporting date• Should not be adjusted for changes to estimates• Further guidance expected from IAA

• Cost of capital appears to be the favourite• Quantile approaches• Margins for adverse deviations on assumptions

16

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Discount rate• “Consistent with observable current market prices,

capturing the characteristics of the liability” • Not connected to supporting assets

• Whether or not to take account of credit risk is topic of a separate IASB paper

• IASB decided not to provide more detailed guidance• Expect the IAA to provide guidance

17

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Insurance ContractsIFRS Phase 2 Update

• Other recent decisions• No deposit floor • Unbundling might be required if components not

interdependent

18

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Financial InstrumentsIAS 39 Revisions

• Objective is to simplify accounting and reporting of financial instruments

• Three main phases:• Classification and measurement

• Exposure draft July 2009; comments Sept 14• Adoption before Jan 1, 2012

• Impairment of financial assets• Exposure draft Oct 2009• ‘expected loss model’ comments requested June 2009

• Hedge accounting• Exposure draft Dec 2009

19

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Financial InstrumentsIAS 39 Revisions

• Classification and measurement• Amortized cost for contracts with basic loan

features and managed on a contractual yield basis

• No “tainting” provisions• Subject to impairment test• No need to separately report embedded

derivatives• Otherwise at fair value through profit and loss• Fair value option is available for amortized cost

assets if it eliminates or significantly reduces mismatch

20

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Financial InstrumentsIAS 39 Revisions

• Classification and measurement (continued)• Optional classification of some equities (not held for

trading) as fair value but with changes through OCI• Gains/losses/dividends would never hit earnings• No impairment test

• Classification at initial recognition; no subsequent reclassifications permitted

21

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Financial InstrumentsIAS 39 Revisions

• Transitional issues• Adds a step to the IFRS conversion process• Early adoption of IAS 39 changes in time for Phase 1

conversion is simply not feasible• Would need to classify all assets by end Q1 2010 to

meet requirements of conversion• Would increase the number of changes to actuarial

liabilities• Unlikely OSFI would allow different companies to use

a different basis

22

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

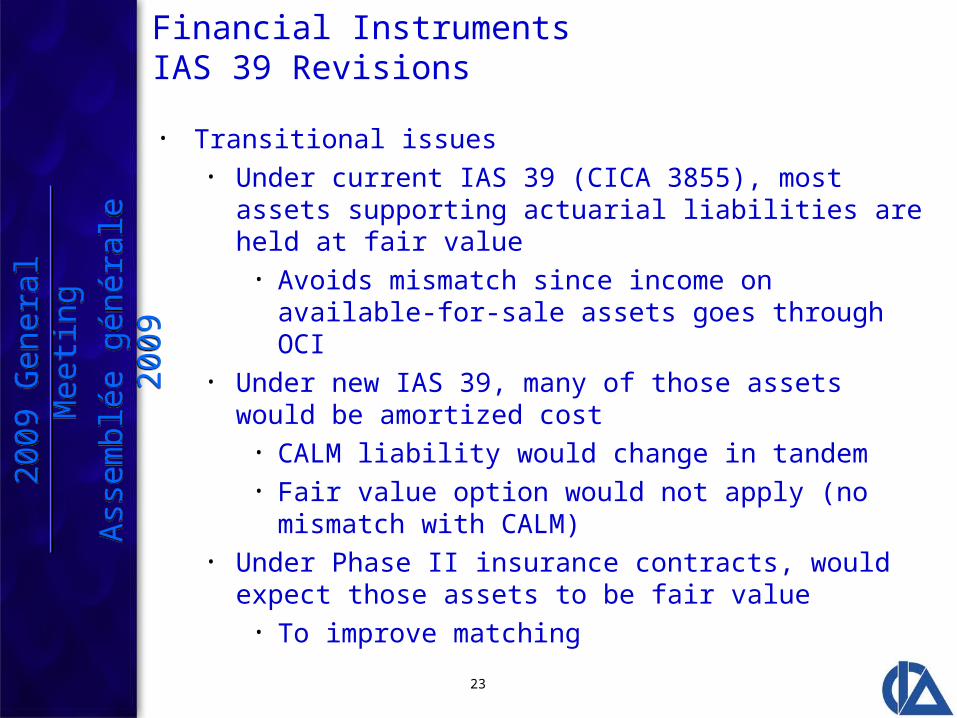

Financial InstrumentsIAS 39 Revisions

• Transitional issues• Under current IAS 39 (CICA 3855), most assets

supporting actuarial liabilities are held at fair value• Avoids mismatch since income on available-for-sale

assets goes through OCI• Under new IAS 39, many of those assets would be

amortized cost• CALM liability would change in tandem• Fair value option would not apply (no mismatch with

CALM)• Under Phase II insurance contracts, would expect those

assets to be fair value• To improve matching

23

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Financial InstrumentsIAS 39 Revisions

• Other issues• Volatility of surplus assets• Increased flexibility to trade assets between liabilities and

surplus• Need to redesignate assets when Phase II insurance

contracts is adopted• IASB staff has indicated this is likely

• Tax implications? • Capital implications?

24

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Appendix I - Field Testing

• The main objectives of field testing the Insurance Contracts project proposals are:– (a) to test proposals and get input from our constituents on whether they:

• (i) result in a faithful representation of insurers’ financial position and performance

• (ii) can be applied rigorously and consistently in practice• (iii) provide workable and auditable solutions

– (b) to collect observable and measurable evidence that supports conclusions– (c) to consult interested parties prior to the issue of an ED and final standard.

• Staff recommend a targeted field test approach which, being flexible and focused, will enable proposals to be tested as they evolve and the results fed back promptly. This approach also minimizes the risk of delay to the project timetable.

• Staff aim to understand:– (a) the current basis of accounting– (b) incremental costs and benefits of moving to the new approach– (c) obstacles affecting application of the proposed approach– (d) whether the proposed approach is operational for an entity with a reasonable level

of knowledge and sophistication, using information that is currently available or that can be created.

• Staff propose a test group of 15 insurers, which is a manageable number that still allows for

some diversity. Staff suggest the following selection criteria for participants:– (a) geographic spread (which determines the regulatory and financial reporting

environment)– (b) diversity of line of business (life, general, health and reinsurance)– (c) some mutual companies– (d) size, so that smaller and medium sized insurers are represented– (e) willingness and ability to participate (e.g., sufficient resources).

25

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

Appendix I - Field Testing

• Participants will be asked to make an assessment of both one-time costs and ongoing costs associated with the proposals. Such costs may include:

– (a) costs to understand the new requirements (e.g., training)– (b) costs to collect, process and analyze new information (e.g., systems changes)– (c) costs associated with disclosure of proprietary information (competitive

advantages/disadvantages).• Benefits associated with a new standard may include:

– (a) increased credibility and representational faithfulness of financial reporting– (b) improved financial processes resulting in better pricing, risk and capital

management.• Participants will be asked to answer questions on specific topics and, if possible, to design their own tests to support their conclusions using internal modeling techniques and financial data. The following topics may be suitable candidates for

field testing:– (a) estimation of cash flows– (b) determination of discount rates– (c) determination of risk margins– (d) other application issues of the measurement approach– (e) treatment of acquisition costs– (f) features of participating contracts– (g) investment contracts– (h) the effects of policyholder behaviour, including boundaries of

existing contracts.

26

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

2009

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2009

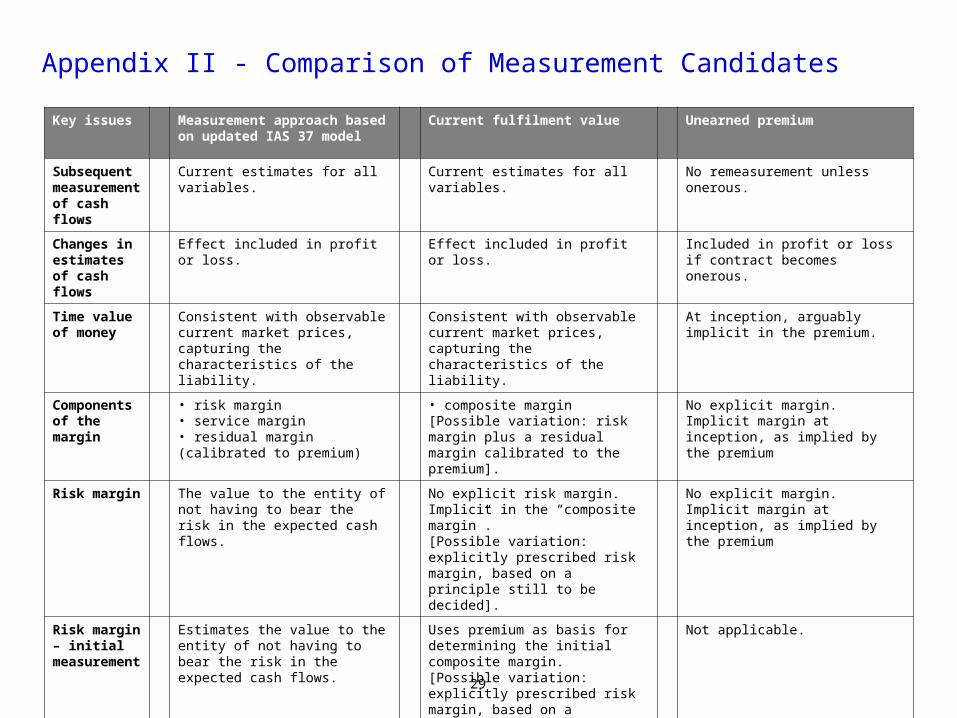

Appendix II - Comparison of Measurement Candidates

Key issues

Measurement approach based on updated IAS 37 model

Current fulfilment value Unearned premium

Definition The amount the entity would rationally pay at the end of the reporting period to be relieved of the present obligation.

Plus a “residual margin, based on the day one difference.

The amount the entity would rationally pay is the lowest of:a) the value to the entity of not having to fulfil the liability (an entity-specific measure);b) the price that the market would demand to assume the liability; andc) the price that the counterparty would demand to cancel the liability, if cancellation is possible.

The expected present value of the cost of fulfilling the obligation to the policy holder over time.

Plus a “composite margin”, based on the day one difference.

[Possible variation: including an explicitly prescribed risk margin of some form, plus a “residual margin, based on the day one difference.]

The part of the premiums for the unexpired part of the insurer’s contractual obligation, subject to a liability adequacy test.

Scope All insurance liabilities. All insurance liabilities. Only pre-claim short duration insurance liabilities.

Building blocks for the measurement approach*

• current estimate of the expected (i.e., probability weighted) present value of future cash flows•time value of money•an explicit margin

If there is no evidence that the entity could cancel or transfer it to a third party for a lower amount, the entity measures the liability at the value it would gain if it did not have to fulfil the obligation.

• current estimate of the expected (ie probability weighted) present value of future cash flows•time value of money•an explicit margin

An implicit building block approach that includes (1) expected cash flows (2) time value of money (3) a margin; all locked-in at inception.

27

Appendix II - Comparison of Measurement Candidates

Key issues Measurement approach based on updated IAS 37 model

Current fulfilment value Unearned premium

Inputs for estimates of cash flows

Inputs for which observable market information is available (financial market variables)

Consistent with observed market prices

Consistent with observed market prices.

Not applicable unless onerous.

Other inputs The entity’s estimate of the cash flows it would incur in fulfilling the liability.

In some cases the amount required by a subcontractor for other services [often to be estimated by the amount the insurer requires for other services].

The entity’s estimate of the cash flows it would incur in fulfilling the liability.

Not applicable unless onerous.

Characteristics of cash flows

Cash flows that arise from the characteristics of the portfolio (portfolio-specific)

Included. Included. Not applicable unless onerous.

Cash flows that arise from the characteristics of the entity (entity-specific)

Included. Included. Not applicable unless onerous.28

Appendix II - Comparison of Measurement Candidates

Key issues Measurement approach based on updated IAS 37 model

Current fulfilment value Unearned premium

Subsequent measurement of cash flows

Current estimates for all variables.

Current estimates for all variables.

No remeasurement unless onerous.

Changes in estimates of cash flows

Effect included in profit or loss. Effect included in profit or loss. Included in profit or loss if contract becomes onerous.

Time value of money

Consistent with observable current market prices, capturing the characteristics of the liability.

Consistent with observable current market prices, capturing the characteristics of the liability.

At inception, arguably implicit in the premium.

Components of the margin

• risk margin • service margin• residual margin (calibrated to premium)

• composite margin[Possible variation: risk margin plus a residual margin calibrated to the premium].

No explicit margin. Implicit margin at inception, as implied by the premium

Risk margin The value to the entity of not having to bear the risk in the expected cash flows.

No explicit risk margin. Implicit in the “composite margin”.[Possible variation: explicitly prescribed risk margin, based on a principle still to be decided].

No explicit margin. Implicit margin at inception, as implied by the premium

Risk margin – initial measurement

Estimates the value to the entity of not having to bear the risk in the expected cash flows.

Uses premium as basis for determining the initial composite margin.[Possible variation: explicitly prescribed risk margin, based on a principle to be decided yet].

Not applicable.

Risk margin – subsequent measurement

Remeasured at each reporting date.

Not applicable. (Implicit release as the composite margin runs off)[Possible variation: risk margin remeasured at each reporting date].

Not applicable. (Implicit release as the premium becomes earned)29

Appendix II - Comparison of Measurement Candidates

Key issues Measurement approach based on updated IAS 37 model

Current fulfilment value Unearned premium

Service margin

The profit the insurer requires for undertaking services. [Sometimes already included in the amount a subcontractor would charge for undertaking a service].

No explicit service margin. Implicit in the “composite margin”.

No explicit margin. Implicit margin at inception, as implied by the premium

Service margin – subsequent measurement

Remeasured at each reporting date.

Not applicable. (Implicit release as the composite margin runs off)

Not applicable. (Implicit release as the premium becomes earned)

Day one difference (the difference between the actual margin and the required margin)

No profit at inception; “residual margin” recognised as a separate item (presumably within the insurance liabilities).

No profit at inception; “composite margin” recognised as a separate item (presumably within the insurance liabilities).

No profit at inception. Loss at inception if onerous.

Liability adequacy test

Not applicable. Not applicable. Required at inception and each subsequent reporting date.

Acquisition costs

Expensed when incurred. Expensed when incurred. Expensed when incurred.

Part of the premium expected to recover incremental acquisition costs

Included in the residual margin. Included in the composite margin.

IASB: Recognised as revenue on day one. FASB: Included in unearned premium.

Own credit risk

To be discussed (arguably implicit in residual margin at inception).

To be discussed (arguably implicit in composite margin at inception).

Not applicable (arguably implicit at inception).

30

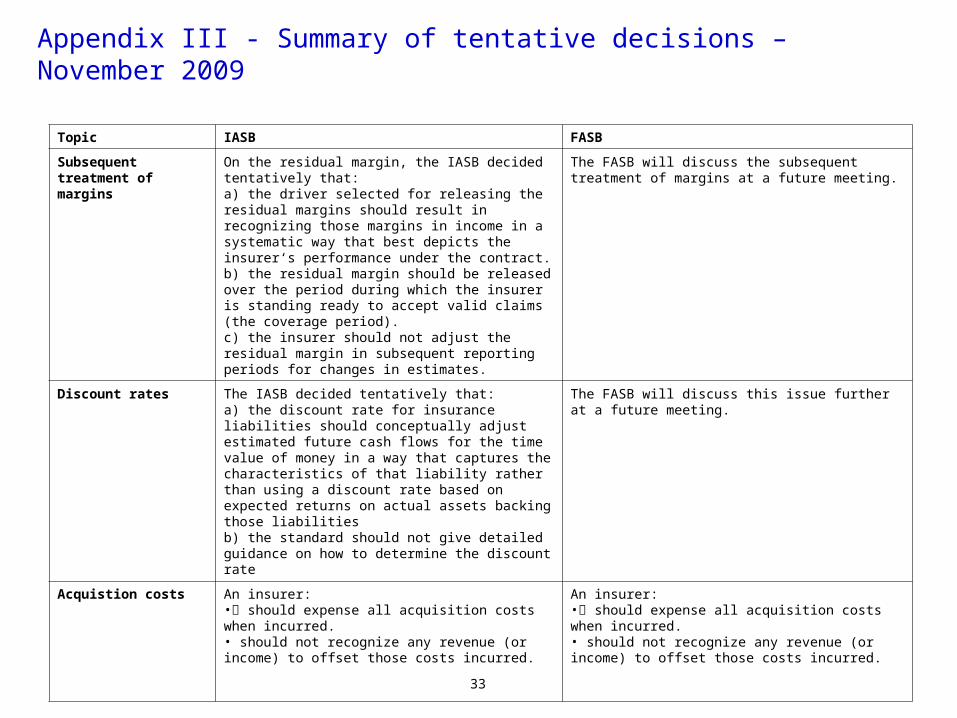

Appendix III - Summary of tentative decisions – November 2009

Topic IASB FASB

Building Blocks

The IASB tentatively decided that the measurement for insurance contracts should include three building blocks:• current estimates of expected (that is, probability weighted) future cash flows,• incorporation of time value of money, and• an explicit margin.

The FASB tentatively decided that the measurement for insurance contracts should include three building blocks:• current estimates of expected (that is, probability weighted) future cash flows,• incorporation of time value of money, and• an explicit margin.

Candidate measurement approaches

The IASB tentatively selected the approach being developed in the project to amend IAS 37, modified to exclude day-one gains.

Nevertheless, a significant minority of Board members supported the approach based on current fulfilment value. Therefore, the exposure draft will explain both approaches.

The FASB tentatively selected a current fulfilment approach with a composite. Margin

Excludediscountingand marginsin someinstances?

The IASB noted the arguments for and against an approach that uses an estimate of future cash flows with no margins and no discounting. The IASBconsidered whether to use such an approach for non-life claims liabilities and tentatively decided not to add it to the list of candidates.

The FASB will consider at a future meeting whether, in certain instances, a measurement of insurance contracts would use future cash flows with no margins and no discounting.

31

Appendix III - Summary of tentative decisions – November 2009

Topic IASB FASB

Use of inputs A measurement approach for insurance contracts conceptually should use current estimates of financial market variables that are as consistent as possible withobservable market prices.

The measurement of cash flows should be discounted and the discount rate should be updated each reporting period.

The measurement of cash flows should consider all available information that represents the fulfilment of the insurance contract. All available information includes, but is not limited to, industry data, historical data of an entity’s costs, and market inputs when those inputs are relevant to the fulfilment of the contract.

The measurement of cash flows should be discounted and the discount rate should be updated each reporting period.

Unearned Premium

The IASB decided tentatively that:a)an unearned premium approach would provide decision-useful information about pre-claims liabilities of short-duration insurance contracts.b)to require rather than permit the use of an unearned premium approach for those liabilities.

The FASB will discuss an unearned premium approach at a future meeting.

Measurement of the margin at inception

The margin at inception should be measured by reference to the premium. Therefore, no day one gains should be recognised in profit or loss.

If the initial measurement of an insurance contract results in a day-one loss, the insurer should recognise that day-one loss in profit or loss.

In principle the initial recognition of an insurance contract should not result in the recognition of an accounting profit.

The FASB will discuss this issue (day-one loss) at a future meeting.

32

Appendix III - Summary of tentative decisions – November 2009

Topic IASB FASB

Subsequent treatment of margins

On the residual margin, the IASB decided tentatively that:a) the driver selected for releasing the residual margins should result in recognizing those margins in income in a systematic way that best depicts the insurer‘s performance under the contract.b) the residual margin should be released over the period during which the insurer is standing ready to accept valid claims (the coverage period).c) the insurer should not adjust the residual margin in subsequent reporting periods for changes in estimates.

The FASB will discuss the subsequent treatment of margins at a future meeting.

Discount rates The IASB decided tentatively that:a) the discount rate for insurance liabilities should conceptually adjust estimated future cash flows for the time value of money in a way that captures the characteristics of that liability rather than using a discount rate based on expected returns on actual assets backing those liabilitiesb) the standard should not give detailed guidance on how to determine the discount rate

The FASB will discuss this issue further at a future meeting.

Acquistion costs An insurer:• should expense all acquisition costs when incurred.• should not recognize any revenue (or income) to offset those costs incurred.

An insurer:• should expense all acquisition costs when incurred.• should not recognize any revenue (or income) to offset those costs incurred.

33

Appendix III - Summary of tentative decisions – November 2009

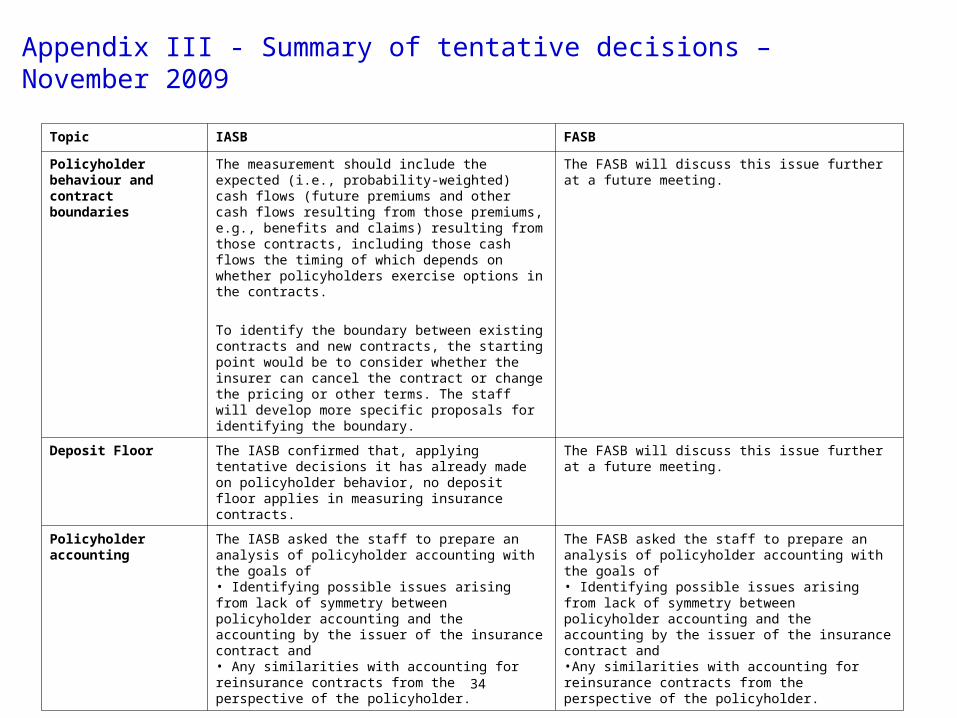

Topic IASB FASB

Policyholder behaviour and contract boundaries

The measurement should include the expected (i.e., probability-weighted) cash flows (future premiums and other cash flows resulting from those premiums, e.g., benefits and claims) resulting from those contracts, including those cash flows the timing of which depends on whether policyholders exercise options in the contracts.

To identify the boundary between existing contracts and new contracts, the starting point would be to consider whether the insurer can cancel the contract or change the pricing or other terms. The staff will develop more specific proposals for identifying the boundary.

The FASB will discuss this issue further at a future meeting.

Deposit Floor The IASB confirmed that, applying tentative decisions it has already made on policyholder behavior, no deposit floor applies in measuring insurance contracts.

The FASB will discuss this issue further at a future meeting.

Policyholder accounting

The IASB asked the staff to prepare an analysis of policyholder accounting with the goals of• Identifying possible issues arising from lack of symmetry between policyholder accounting and the accounting by the issuer of the insurance contract and• Any similarities with accounting for reinsurance contracts from the perspective of the policyholder.

The FASB asked the staff to prepare an analysis of policyholder accounting with the goals of • Identifying possible issues arising from lack of symmetry between policyholder accounting and the accounting by the issuer of the insurance contract and•Any similarities with accounting for reinsurance contracts from the perspective of the policyholder.

34