Issues on Brazil Agricultural Policy ISSN 1413-4969 200 Year XIV October 5 Revista de OECD Exclusive Review of agricultural policies in Brazil Journal of Agricultural Policy published by the Secretariat of Agricultural Policy - Ministry of Agriculture, Livestock and Food Supply Edition Special Ministry of Agriculture, Livestock and Food Supply Building bridges between the agribusiness and the financial market

Review of agricultural policies in Brazil1 ......................... 5Highlights and policy recommendationsOECD

Issues on Brazil agricultural policy ................................ 17Ivan Wedekin

Editorial councilEliseu Alves (President)

Elísio ContiniHélio Tollini

Antônio Jorge de OliveiraRegis Alimandro

Biramar Nunes LimaPaulo Magno Rabelo

General secretaryRegina Vaz

Editorial coordinationVicente G. F. Guedes

CadastreCristiana D. Silva

Editorial supervisionLillian Alvares

Lucilene Maria de Andrade

ProofreaderFrancimary de M. e Silva

TranslationJosé Sette

Marcelo Fernandes Guimarães

Design and coverCarlos Eduardo Felice Barbeiro

Photo coverMAPA’s archive

Print and finishingEmbrapa Publishing House

1 The opinions expressed and arguments employed herein do not necessarily reflect the official views of the OECD orthe governments member countries. This document has been produced with the financial assistance of the EuropeanUnion. The views expressed herein can in no way to reflect the official opinion of the European Union.

Year XIV - Special edition - October 2005 2

The Revista de Política Agrícola is a quarterly publication ofthe Secretariat of Agricultural Policy of the Ministry of Agri-culture, Livestock and Food Supply, aimed at technicians,entrepreneurs, agribusiness researchers and those interestedon agricultural policy.

Subscription service

Ministry of Agriculture, Livestock and Food SupplySecretariat of Agricultural PolicyEsplanada dos Ministérios, Bloco D, 5º andarCEP 70043-900 Brasília, DFPhone: 55-061-3218-2505Fax: 55-061-3224-8414www.agricultura.gov.brreginavaz@agricultura.gov.br

Articles and data may be quoted if their sources arementioned. Signed articles do not necessarily reflect theofficial view of the Ministry of Agriculture, Livestock and FoodSupply.

Edition5,000 copies

All rights reserved.Non authorized reproductions of this publication, either partial

or total, is a violation to the author's right (Law Nº 9610).

International Data Publishing Classification (CIP).Embrapa Publishing House

Revista de política agrícola. – Ano 1, n. 1 (fev. 1992) - . – Brasília: Secretaria Nacional de Política Agrícola, Companhia Nacionalde Abastecimento, 1992-

v. ; 27 cm.

Trimestral. Bimestral: 1992-1993.Editores: Secretaria de Política Agrícola do Ministério da Agricultura,

Pecuária e Abastecimento, 2004- .Disponível também em World Wide Web: <www.agricultura.gov.br>

<www.conab.gov.br> <www.bb.gov.br>ISSN 1413-4969

1. Política agrícola. I. Brasil. Ministério da Agricultura, Pecuária eAbastecimento. Secretaria de Política Agrícola. II. Ministério daAgricultura, Pecuária e Abastecimento. Assessoria de GestãoEstratégica. III. Empresa Brasileira de Pesquisa Agropecuária.Secretaria de Gestão e Estratégia. IV. Companhia Nacional deAbastecimento.

CDD 338.18 (21 ed.)

Federal Republic of Brazil

Luiz Inácio Lula da SilvaPresident

Ministry of Agriculture,Livestock and Food Supply

Roberto RodriguesMinister

Secretariat of Agricultural Policy

Ivan WedekinSecretary

Department of Marketing,and Agricultural and Livestock Supply

José Maria dos AnjosDirector

Agricultural Economic Department

Edilson GuimarãesDirector

Department of Rural Risk Management

Welington Soares de AlmeidaDirector

Year XIV - Special edition - October 20053

Over the last fifteen years, internationalagriculture has been marked by significantchanges in agricultural and macro economicpolicies in Brazil and other emerging nations,a phenomenon that has been repeated withlesser intensity in the OECD countries.

These transformations, which are stronglymarket-oriented, resulted in greaterefficiency, increased production and incomegrowth in emerging economies, bringingimportant changes to world agricultural trade.

The dynamism, size and high competitivenessof the Brazilian agriculture have beenresponsible for its impressive growth andparticipation in the international market,strengthening its position as an agriculturalpowerhouse.

In order to enlarge knowledge about thisreality, OECD conducted a study called“Review of agricultural policies in Brazil”,identifying the main changes in agriculturalpolicy and the productive and commercialperformance of the agriculture sector, payingspecial attention to social and environmentalaspects. One of the study's main conclusionsis that Brazil is one of the countries that leastsubsidizes agriculture. In other words, thegrowth of Brazilian agribusiness in the worldmarket is solely the result of itscompetitiveness.

The publication of the study was preceded byan ample debate between the OECD teamand specialists from the Secretariat for

The world viewof the brazilianagriculture

Agr

icul

tura

l Le

tter

Agricultural Policy (SPA/MAPA), from otherareas of the government and from researchand teaching institutions. This initiative wascomplemented by the text “BrazilianAgricultural Policy in Perspective” made bySPA, which lays emphasis on agriculturalpolicy transition and the launching of newfinancial instruments designed to fosteragribusiness competitiveness.

Considering the importance of these initiativesfor a more ample knowledge of the Brazilianagricultural policy, this special bilingualedition of the Revista de Política Agrícolapresents a summary and the conclusions ofthe study conducted by the OECD and the fullcontent of SPA study.

The innovative feature of recently-approvedagricultural policy instruments works asbridges which will link the interests of ruralproducers, cooperatives and agribusinessfirms, to those related to financial and capitalmarkets. This union of interests between fieldand city will strengthen Brazil’s agricultureand agribusiness, which reveals the strengthand entrepreneurship of our agribusinessproducers.

With the publication of these two studies, thebrazilian government expresses its gratitudeto the OECD and to all involved persons, fortheir contribuition to world agriculture and toBrazil.

Roberto Rodrigues1

1 Minister of Agriculture, Livestock and Food Supply.

Year XIV - Special edition - October 2005 4

This Special Edition presents the highlights of theOECD Review of Agricultural Policies: Brazil.The Review was undertaken as part of aninitiative to provide analyses of agriculturalpolicies for four major agricultural economiesoutside the OECD area, the others being China,India and South Africa. The study measures theextent of support provided to agriculture usingthe same method that OECD employs to monitoragricultural policies in OECD countries. Inaddition, it focuses on key interactions betweenBrazil and OECD countries, including theimpacts of trade and agricultural policy reforms.The aims of the country study is to strengthenthe policy dialogue with OECD members on thebasis of consistent measurement and analysis,and to provide an objective assessment of theopportunities, constraints and trade-offs thatconfront Brazil's policy makers.

The study was carried out by the OECDDirectorate for Food, Agriculture and Fisheries.The principal authors were Jonathan Brooks andOlga Melyukhina, who received valuablecontributions from Darryl Jones, AndreaCattaneo, Hsin Huang, and Garry Smith.Research and statistical support were providedby Florence Mauclert and Adriana Verdier, andtechnical and secretarial assistance by StefanieMilowski and Anita Lari.

The study benefited from the substantive input ofa range of Brazilian experts. Information ondomestic policies was provided by GuillermeLeite da Silva Dias from the University of SãoPaolo (USP); Gervasio Castro de Rezende andJosé Garcia Gasques from the Institute ofApplied Economic Research (IPEA); AntônioSalazar Brandão from the Federation ofIndustries of the State of Rio de Janeiro; andVicente Marques from the Centre for AgrarianStudies and Rural Development of the Ministry

Foreword

of Agrarian Development (NEAD). Informationon trade policies was provided by researchers atthe Institute for International Trade Negotiations(ICONE), including Mário Jales, Antônio Neto,Joaquim da Cunha Filho and Marcos SawayaJank. The analysis of changes in incomes,poverty and inequality was provided by StevenHelfand and Edward Levine from the Universityof California, Riverside (USA). A database andframework for assessing the prospective impactsof global trade and agricultural policy reforms inBrazil was provided by a research team at theFIPE / USP, including Carlos Azzoni, FernandoGaiger, Joaquim Guilhoto, Eduardo AmaralHaddad, and Tatiane de Menezes. This wascomplemented by modeling work undertakenby Scott McDonald (University of Sheffield, UK).

The study benefited greatly from the support ofthe Brazilian Ministry of Agriculture and Food,the Ministry of Agrarian Development, and theNational Treasury, whose experts providedessential information on the functioning ofagricultural programmes in Brazil as well ascomments on the draft report.

The study was made possible through financialassistance from Germany, the Netherlands,New Zealand, Spain, Switzerland, the UnitedStates, and the European Union.

The study was reviewed in a roundtable withBrazilian officials and experts in Brasilia inMarch 2005. Subsequently, Brazilianagricultural policies were examined by theOECD's Committee for Agriculture in its 141stsession in June 2005, bringing together policy-makers from Brazil, OECD Member countriesand some non-OECD countries. The report ispublished under the authority of the Secretary-General of the OECD.

1 OECD: Director of the Directorate for Food, Agriculture and Fisheries.

Stefan Tangermann1

Year XIV - Special edition - October 20055

Brazil provides relatively little support to itsfarmers. Producer support, as measured by thePSE, accounted for 3% of the gross value offarm receipts in 2002-04 – a rate comparablewith that of New Zealand (2%) and Australia(4%), and far below the OECD average (30%).The highest support levels are for import-competing staples (wheat, maize and rice)and cotton, ranging between 6% and 17% forthese products.

Support to farmers accounts for about three-quarters of all support to agriculture, with theremaining quarter delivered as generalservices to the sector, such as research andextension, training, and the development ofrural infrastructure. These general servicesinclude important long term investments, buthave been declining in relative terms at theexpense of credit subsidies, about half ofwhich stem from the restructuring of farm debtaccumulated over the period ofmacroeconomic instability in the late-1980s tomid-1990s.

The low level of producer support reflects theradical transformation of the Brazilianeconomy that has occurred over the last 15years. The abandonment of import substitutionpolicies has enabled agriculture to growrapidly. Livestock output rose particularlyquickly in the 1990s, while more recentlythere has been a boom in the production ofsoybeans, driven by high prices and a lowexchange rate. These effects have sincedissipated, so it is unrealistic to extrapolate

Review of agriculturalpolicies in Brazil1

Highlights and Policy Recommendations

current growth rates. Agricultural growth hasbeen mostly attributable to improvedproductivity and lower prices for importedinputs, with increases in agricultural area amore recent factor.

The recent boom in Brazil's agriculturalexports has been associated with a change inthe composition and direction of trade. Therehas been a shift away from traditional tropicalproducts, such as coffee and orange juice,towards soybeans, sugar, and meats, notablypoultry and pigmeat. Although OECD countrymarkets are still very important, with morethan 40% of agricultural exports destined forthe European Union, the fastest export growthis with countries outside the OECD area,notably China and Russia. Even so, themajority of agricultural production in Brazilserves the domestic market. The share ofagricultural production exported has typicallyaveraged around 25%, although that shareclimbed to 30% in 2004.

Having substantially liberalised its ownagricultural policies, the main source of futurebenefits to Brazil is reforms in other countries,where access to OECD country markets is themost important issue. Brazilian exporters areimpeded by high tariffs in key markets, tariffescalation according to the degree ofprocessing for several important commodities,unfavourable treatment under tradepreference schemes and tariff-rate quotasystems, and significant non-tariff measures(notably for livestock products).1 Extract from the study “Review of Agricultural Policies in Brazil”, OECD 2005.

Year XIV - Special edition - October 2005 6

At the domestic level, sectoral growth couldbe further supported through improvements ininfrastructure, changes in the credit system(notably on the treatment of outstanding debt),and a simplification of tax policies.

At the same time, there is a strong need foreffective social policies. Although rural povertyhas fallen significantly in Brazil, the situation forthe poorest of the rural poor has actuallydeteriorated, and poverty has becomeincreasingly concentrated in the North andNorth East regions. This calls for targetedmeasures to upgrade the farming skills ofsmallholders, and to facilitate incomediversification and the exploitation of non-farmopportunities. Investments at the individuallevel, for example through education and healthexpenditures, are important, as are policies thatfoster rural development, such as infrastructuredevelopment.

Reforms and their impacts

Brazil's economy has undergoneradical reforms that have provideda more stable investment climateand stimulated agricultural growth.

Brazil is a major player in the globaleconomy, with a population of 180 millionand a GDP of USD 1,300 billion (in PPPterms) that places it among the ten largesteconomies in the world. The country isendowed with vast natural resources, and hasan agricultural area that is exceeded only byChina, Australia and the United States.Primary agriculture accounts for 8% of GDP,while agricultural products account for about30% of exports. Agriculture thus plays animportant role in the overall functioning of thenation's economy.

Over the past 15 years, the Brazilianeconomy has undergone a radicaltransformation. Following the abandonment of

import substitution policies in the late 1980s,the government embarked upon a wide rangeof reforms. These included macroeconomicstabilisation, structural reforms and tradeliberalisation. Macroeconomic stability wasachieved in the mid-1990s when, followingseveral unsuccessful stabilisation plans, theReal Plan invoked the budgetary restraintnecessary to bring inflation under control.Structural reforms included the privatisation ofstate-owned enterprises, the deregulation ofdomestic markets, and the establishment of acustoms union, Mercosur, with other SouthAmerican countries. Policy changes includeddeep tariff cuts and the elimination of non-tariff barriers to trade.

Agriculture both contributed to these reformsand benefited from them. Through the 1990s,there was a scaling down of expenditures onprice support and subsidised credit; themarkets for wheat, sugar cane and coffeewere deregulated; and trade was liberalisednot just on the import side, but also forexports, notably with the elimination of exportlicenses, quotas and taxes. Agriculturebenefited in overall terms from the change indevelopment paradigm, as it removed thediscrimination against the sector that wasimplicit in the support for manufacturingindustry, and helped establish a more stableinvestment climate.

The Brazilian economy is now much morerobust than it was ten years ago, but itremains vulnerable to outside shocks, asevidenced by contagion from the Asian crisisin 2001, and the effects of weak marketsentiment in the run-up to the presidentialelection of 2002.

Macroeconomic stabilisation, by removingthe regressive effects of inflation, led to asubstantial reduction in the level of poverty,which fell by 10 million in just two years(1994-95). But reforms also inducedadjustment stresses, including within theagricultural sector, where producers ofimportable commodities (such as wheat) were

Year XIV - Special edition - October 20057

suddenly forced to compete. Moreover,reforms have not resolved Brazil's socialproblems. The incidence of poverty remainshigh, at more than 30% of the population,while the distribution of income is among themost unequal in the world.

Agriculture has grown rapidly since theabandonment of import substitution policies,and this growth has accelerated in the lastfew years (Figure 1). A large share of thisexpansion has occurred in the Centre West ofthe country, where, through the 1990s,livestock output rose particularly rapidly.More recently there has been a boom in theproduction of soybeans and complementarycrops (e.g. second crop maize). Much of therecent boom is attributable to the combinationof a short term strengthening of world pricesand a low exchange rate. These effects havesince dissipated, so it is unrealistic toextrapolate current growth rates.

access to imported inputs (notablymachinery). Allied to this, productivityimproved substantially, with a 40%improvement in total factor productivitybetween 1990 and 2004. The productivity ofimportables (wheat, dairy) improved morethan that of exportables, as the former wereexposed to foreign competition while thelatter were competitive anyway. In fact, somecrops that were formerly imported haverecently become net exports (e.g. maize andcotton). Yields have improved substantially,thanks largely to agricultural research tailoredto climatic conditions in the Centre West,while big improvements in labour productivity(77% between 1990 and 2004) reflect therelease of farm labour from the sector.However, with high real interest rates, accessto capital remains a problem for manyfarmers, and continues to dampen overallproductivity growth.

Until recently, it was productivity growthrather than the mobilisation of new factorresources that underpinned agriculturalgrowth. Total agricultural area remained moreor less constant through the 1990s, asincreases in the Centre West were offset byreductions in the South and South East.However, between 2000-01 and 2003-04 thearea planted to crops increased from 52 to 61million ha, with soybean area aloneincreasing by 50%. The rapid expansion ofsoybean acreage in the Centre West can beseen as a precursor to more balancedagricultural development in this region, asinfrastructure development catches up andproducers stand to benefit from externaleconomies of scale. The shift in the locus ofagricultural production has also led to anincrease in the average size of farmoperations, as land in the Centre West offersgreater economies of scale.

The growth in soybean area and risingdemand for pasture from livestock farmersthreatens the Amazon rainforest. In additionthere are concerns about the environmentalimpacts of agricultural development in the

Figure 1. Output indices for crops and livestockproducts, 1990-2004.1990=100Source: IBGE / SIDRA.

Agricultural growth has been mostly attributableto improved productivity and lower prices forimported inputs, with increases in agriculturalarea a more recent factor.

The growth in output has occurred despitefalling long term prices for most commodities.One reason is that output prices fell moreslowly than input prices through most of the1990s, as the opening up of trade allowed

Year XIV - Special edition - October 2005 8

Cerrado grasslands. Since 1990, Brazil haslost an area of forest equal to the size of theUnited Kingdom. Large scale commercialranchers are responsible for the majority ofthis deforestation, ahead of logging and themigratory slash and burn practises of manysubsistence farmers. Some argue that soybeanfarming has contributed indirectly, by causingthe migration to the forest frontier of displacedcattle ranchers and subsistence farmers. Thetrade-off between the economic benefits ofagricultural expansion and the environmentalbenefits of forest preservation is a difficultdomestic policy decision facing Brazil, whilethe choice of instrument to achieve thedesired balance needs to take account of thedifficulties of policing such a vast area.Deforestation would be more limited if moreintegrated farming practises with higherlivestock stocking rates were adopted in theCerrado. Current research in Brazil is orientedtowards this objective.

The recent boom in Brazil's agriculturalexports has been associated with a change inthe composition and direction of trade.

Despite rapid export growth, the majority ofagricultural production in Brazil serves thedomestic market. The share of agriculturalproduction exported has typically averagedaround 25%, although that share climbed to30% in 2004. This share is similar to that ofthe United States (which also has a largedomestic market), but lower than that of otheragricultural exporters such as Canada, where40% of production is exported, and Australia,where the exported proportion averagesabout two-thirds. The domestic market islikely to continue to be the main outlet forproduction. On the supply side, the recentproduction boom is likely to fade with weakerprices, a higher exchange rate, and theexposure of infrastructure bottlenecks. On thedemand side, there is considerable scope forpoorer Brazilians to consume more productswith relatively high income elasticities (suchas meat and fruit and vegetables).

The recent export boom has been drivenprimarily by soybeans and soybean products,but supported by other products, such assugar, poultry and pigmeat. In the last fewyears, Brazil has become an exporter ofmaize and cotton (both of which can berotated with soybean production). Moregenerally, there has been a shift in thecomposition of exports, away from traditionaltropical products, such as coffee and orangejuice, towards soybeans, sugar, and meats,notably poultry and pigmeat.

The direction of agricultural trade has alsochanged. Although OECD country marketsare still very important, with more than 40%of agricultural exports destined for theEuropean Union (Figure 2), and exports tomost OECD countries are increasing inabsolute terms, the fastest export growth iswith countries outside the OECD area,notably China and Russia (Figure 3).

Shifts in the scale, composition and location ofproduction have been associated with profoundstructural changes within the agricultural sector.These changes have had important implicationsfor the level and distribution of incomes, and theincidence of poverty.

Figure 2. Brazilian agro-food exports by destinationregion, 2000-03 average.(1) EU/15; (2) Other countries include Cyprus, Iceland, Liechtenstein, Malta,Norway and Switzerland.

Source: MDIC ALICE.

Year XIV - Special edition - October 20059

Although rural poverty has fallen significantly inBrazil, the situation for the poorest of the ruralpoor has actually deteriorated, and poverty hasbecome increasingly concentrated in the Northand North East regions.

In general terms, per capita income growthhas led to a substantial fall in the incidence ofpoverty and extreme poverty. For Brazil as awhole, real per capita incomes rose by 29%between 1991 and 2000, reducing theproportion of the population living in povertyfrom 40% to 32% (Figure 4), and the shareliving in extreme poverty from 20% to 15%2.

2 The poverty and extreme poverty lines are set at ½ and ¼ respectively of theAugust 2000 minimum monthly wage per person (BR 151). At thecontemporaneous nominal exchange rate, this translated into a poverty lineof approximately USD 1.33 per person per day and an extreme poverty lineof USD 0.67 per person per day.

The incidence of poverty is higher in ruralareas, but because 80% of the population livein urban areas the number of urban poorexceeds the number of rural poor. In the1990s, rural incomes rose more rapidly thanurban incomes (32% versus 23% between 1991and 2000). This enabled rural poverty to fallfrom 72% of households in 1991 to 61% in 2000,and extreme rural poverty to decline from 45%to 36% over the same period.

However, the improvement in rural incomes hasnot been principally attributable to agriculturalincomes, which grew by just 2% between 1991and 2000, compared with non-agriculturalincome growth of 38%. Moreover, agriculturalincome became more concentrated amongricher households (although it remains lessconcentrated than non-agricultural income), andso made little contribution to poverty reduction.

The situation for the bottom 20% of ruralhouseholds, who are well below the extremepoverty line (more than a third of ruralhouseholds), has actually deteriorated.A trebling of government transfers between1991 and 2000 helped poor households ingeneral, but many of the poorest missed outbecause they fell outside the remit of the formaleconomy and the coverage of pensions andother programmes.

Figure 3. Changes in export shares of Brazil's major export destinations between 2000 and 2003(1) Includes Mainland China, Hong Kong, and Macao.Source: MDIC/ALICE.

Figure 4. Poverty in Brazil, 1991 and 2000 – Percent of population below the poverty line.

Source: Helfand and Levine (2004) based on the Demographic Census.

Year XIV - Special edition - October 2005 10

These national averages mask importantregional variations. Income growth in the CentreWest has been strong enough to reduce ruralpoverty, even though inequality has increased.Rural poverty has fallen more slowly in theNorth East and actually risen in the North(where the rural population has actually grown),meaning that rural poverty is increasinglylocated in these regions.

Structural changes at the farm level have beenreinforced by wider developments along thefood chain. In particular, the increasing share ofretail sales accounted for by supermarketscarries important implications for farmstructures. The associated growth of contractingoffers opportunities for some producers, whomay, for example, see their credit constraintseased through the forward supply of seed.However, it poses a threat to many smallholderswho may not be able to meet the standards setby downstream purchasers, yet find itincreasingly difficult to find local outlets.

The opportunities for smallholders also dependon the success of land reform initiatives andassociated credit programmes. So far, the scaleof land reform has not been sufficient to make asignificant dent in the overall poverty figures,and it is likely that its ultimate potential willdepend on how well it is complemented bybroader investments (e.g. in education) thatimprove households’ income earning potentialboth within and outside agriculture.

Current agricultural policies

Brazil provides a relatively low level ofsupport to its agricultural sector. Most of thatsupport goes to producers in the form ofpreferential credit.

Brazilian agricultural policies have beenbroadly liberalised, although there continues tobe an array of policy interventions. Total supportto the sector, as measured by the Total SupportEstimate (TSE), averaged BRL 8.2 billion (USD

2.7 billion) per year in 2002-04, or 0.5% of GDP.The cost of support to the overall economy islow relative to most OECD countries, and isroughly comparable to that in Australia (0.3%)and New Zealand (0.4%).

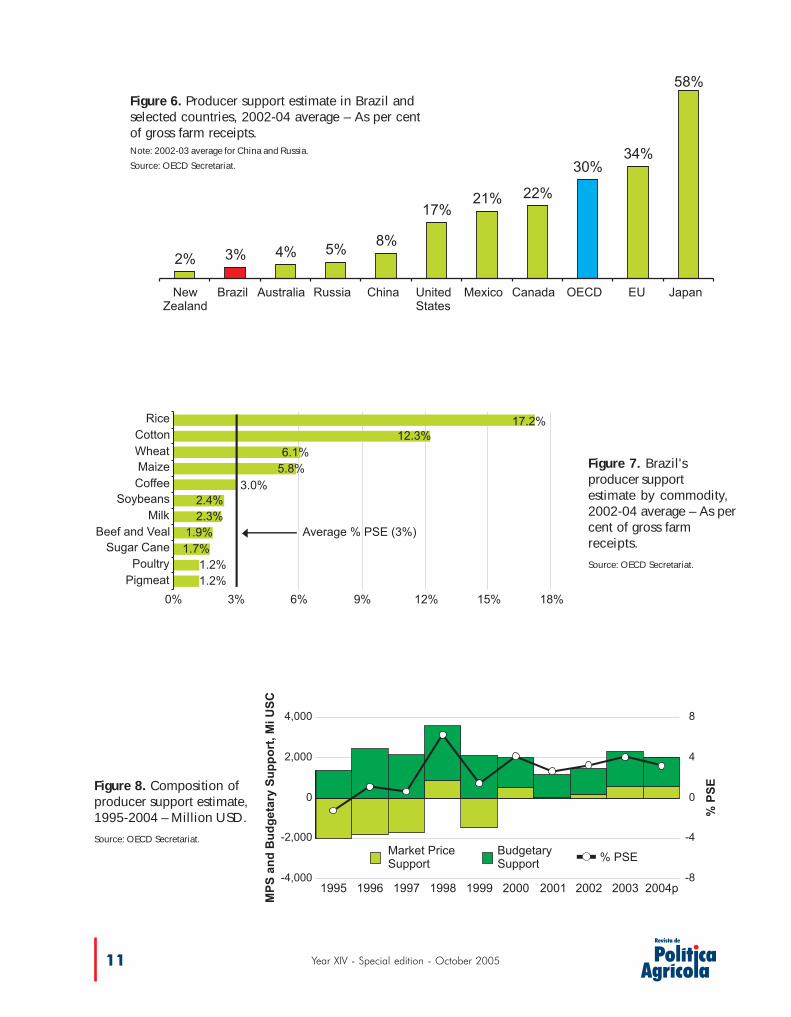

Most of this support is delivered to producers, asopposed to general services to the sector.Indeed, producers received about three-quartersof total support to agriculture in 2002-04(Figure 5). Producer support in Brazil, asmeasured by the percentage PSE, accounted foran average of 3% of the value of gross farmreceipts between 2002 and 2004 – a rate ofsupport that is comparable with that of NewZealand (2%) and Australia (4%), and far belowthe OECD average of 30% (Figure 6).

The highest support levels are for import-competing staple crops (wheat, maize and rice)and cotton (Figure 7). These commoditiesreceive minimal border protection, butproducers are effectively compensated forhaving to compete with other Mercosurpartners, as the value of domestic assistance isapproximately equivalent to Brazil's currentextra-Mercosur tariff.

Producer support is provided mostly throughtaxpayer transfers associated with preferentialcredit to the sector (Figure 8). Brazil's officialcredit system, which accounts for about 28% ofagricultural borrowings, confers specialtreatment on the agricultural sector, through theadministered allocation of credit resources andcontrolled interest rates. This system has beenjustified on the grounds that it offsets high market

Figure 5. Composition of the total support estimatein Brazil – Per cent.Source: OECD Secretariat.

Year XIV - Special edition - October 200511

Figure 7. Brazil'sproducer supportestimate by commodity,2002-04 average – As percent of gross farmreceipts.

Source: OECD Secretariat.

Figure 6. Producer support estimate in Brazil andselected countries, 2002-04 average – As per centof gross farm receipts.Note: 2002-03 average for China and Russia.

Source: OECD Secretariat.

Figure 8. Composition ofproducer support estimate,1995-2004 – Million USD.

Source: OECD Secretariat.

Year XIV - Special edition - October 2005 12

interest rates that are a legacy ofmacroeconomic instability (from whichagriculture suffered disproportionately). A furtherrationale for special treatment of the sectoremanates from social goals, where affordabilityof production credit is seen as a crucial elementof supporting income generation among therural poor. The preferences are to some extenteroded by the practice of banks imposingadditional requirements on rural borrowers (suchas the purchase of insurance) as a condition forreceiving reduced interest credit.

Approximately one half of the overall benefitfrom credit support stems from therestructuring of large debt accumulated overthe period of macroeconomic instability in thelate 1980s to mid-1990s. Debt reschedulingwas unavoidable, given the need to renewthe flow of liquidity into the sector. However,successive rescheduling has created “moralhazard” and led to defaults that are likely tocontinue in anticipation of furtherconcessions. This may impede fresh lending.Also, to the extent that debt reschedulinginvolves budgetary support, it may crowd outmore productive public spending (e.g. forinfrastructure development).

Aside from preferential credit, Brazil employsseveral mechanisms to support producer prices,such as intervention purchases and commodityloans. However, these do not result in broad,sector-wide price distortions. Indeed marketprice support has tended to be close to zero inrecent years.

The purported aim of price support policies is toreduce price instability, as well as to provide alimited subsidy to producers who are consideredto be at a disadvantage, either because theircosts are raised by underdevelopment ofinfrastructure, or because of locally depressedincomes. Insofar as these policies are locallytargeted to keep potentially viable farmers afloatuntil they become profitable - either asinfrastructural development catches up, or asinvestments to improve semi-subsistencefarmers' competitiveness take hold - they have

the potential to correct market failures. On theother hand, they also have the potential to retardadjustment among farmers whose best prospectslie ultimately outside agriculture.

To summarise, Brazil provides little support to itsagricultural sector, yet it has become moredistorting and less oriented towards long-termdevelopment. The share of support provided toproducers, mostly in the form of credit subsidies,is increasing, while expenditures on generalservices are becoming less important. However,the latter category includes important long-terminvestments for Brazil, in areas such as researchand extension, training, and the development ofrural infrastructure.

The future benefitsof policy reforms

The benefits to Brazil from multilateral reformwill come mainly from reforms in agriculturalpolicies, where access to OECD countrymarkets is the most important issue.

Given that Brazil has broadly liberalised itsown agricultural policies, most of the futurebenefits to the country from multilateralagricultural policy reforms are expected tocome from the removal of protectionistmeasures in other countries. Indeed, Brazil isexpected to be one of the biggest externalbeneficiaries from reforms in OECD countriesand elsewhere.

For Brazil, agricultural reforms matter morethan reforms to any other sector, and themajority of the potential gains derive fromreforms in OECD countries (Figure 9). It isestimated that a 50% cut in tariffs and exportsubsidies globally and for all sectors, togetherwith a 50% reduction of domestic support toagriculture in OECD countries, would providea welfare gain to Brazil of USD 1.7 billionequating to about 0.3% of GDP. Of thesegains, 59% would come from tariff reductions

Year XIV - Special edition - October 200513

on agricultural products by OECD members.The gains to Brazil from agricultural policyreforms in OECD countries account for morethan half of all the gains to developingcountries.

There are two reasons why OECD reformsmatter most: first, a large share of Brazil'sagricultural exports go to OECD countries(notably the European Union), and protection inthese markets is relatively high; second, OECDcountries account for the majority of support thatundermines Brazil's competitiveness in thirdcountry markets. That said, a rising proportion ofBrazil's exports is going to non-OECD countrydestinations, notably China and Russia, whichmakes policies in these countries of increasingimportance.

Among the areas in which an agreement onreforms is being pursued, market access isparamount for Brazil, as for world marketsoverall. Brazil faces a range of difficulties ingaining access to foreign agricultural markets,especially among OECD countries. Theseinclude:

High tariffs in key markets (notably sugar,poultry, orange juice, beef and pigmeat, andtobacco).

Tariff escalation according to the degree ofprocessing (notably in the soybean sector, andfor processed food products and coffee).

Discriminatory import regimes, such ascountry-specific TRQ allocations, andpreference schemes, which typically do not

favour Brazil. These mechanisms for controllingimports tend to be relatively important in thesugar, beef and cotton sectors and are appliedmost by those countries which represent Brazil'sbiggest overall markets, i.e. the EuropeanUnion, the United States, China and Russia.

Non-tariff measures, such as sanitary andphyto-sanitary regulations, which, irrespectiveof their legitimacy, impede market access.These are a particular problem for meatproducts, where several countries do not acceptBrazil's contention that specific regions shouldbe considered as free from foot-and-mouthdisease, even if this is not the case for thecountry as a whole.

Reforms in these areas, and accompanyingreductions in domestic support promise gains toBrazil that are expected to be widespreadamong different groups of households:

Commercial agricultural producers with linksto foreign markets are expected to reap most ofthe benefits that derive from higher internationalprices. Potential losses to import-competingsectors are less of a threat, since these sectorshave already been opened up to imports fromlow-cost Mercosur members (e.g. Argentinewheat).

Non-commercial “family” farms are alsoexpected to benefit, to the extent that they areintegrated with markets. This does not rule outthe possibility that some households will lose,for example because they are net consumersof agricultural products, or because landrental payments are forced up by more thanany increase in farm receipts. But on balancethis is not expected to be the case - even forthe poorest farm households.

Non-agricultural households are alsoexpected to gain from multilateral reforms,with the benefits from higher profits and wagepayments in the agro-food sector andelsewhere exceeding the losses to consumersfrom higher food prices.

Wage-earning agricultural employees shouldbe a major beneficiary from the expansion in

Figure 9. Welfare gains to Brazil from multilateralreform.Source: OECD Secretariat.

Year XIV - Special edition - October 2005 14

commercial production and exports; most likelyfrom an increase in employment (i.e. a brake onthe structural decline) rather than higher wages,given the high rate of unemployment (andunderemployment) in Brazil.

In the case of the reform scenario describedabove, real incomes are expected to increasebetween 2% and 4% for agriculturalproducers, by around 3% for agriculturalemployees and by about 1% for urbanhouseholds. These income gains lead to amodest decline in the incidence of poverty.Because commercial farmers gain more thansmallholders, inequality among producers isexpected to increase. But the wider gains toagricultural employees and urban households(who account for about 80% of the population)imply that the overall effect on incomeinequality is likely to be broadly neutral.

In any event, these impacts are much milderthan those induced by market changes,including global demand growth anddeclining real agricultural prices. Indeed, it isimportant not to confuse all the enhancedopportunities for exporters, or the adjustmentstresses facing farmers (often operating on asmall scale) whose productivity cannot keeppace with price declines, with the morelimited impacts of multilateral reforms.

Policy challenges

Brazil's agricultural policies seek to reconcilethe pursuit of agricultural growth with socialand environmental objectives. Sectoralgrowth can be supported domesticallythrough improvements in infrastructure andthe country's credit and tax systems; whileinternationally the biggest need is forimproved access to key markets.

Agricultural policy design in Brazil involvesreconciling multiple objectives. Theseobjectives include the promotion ofagricultural growth and competitiveness

within the constraints of environmentalobjectives, and the design of specific policiesthat are tailored to the needs of poor farm andrural households.

Weak infrastructure is emerging as asignificant bottleneck to agriculturaldevelopment. Producers in Brazil aretypically a long distance from their principalmarkets, and face internal logistics systemsthat are relatively underdeveloped. Forexample, only 10% of all highways in Brazilare paved, compared with 29% inneighbouring Argentina. Moreover, transportcosts are relatively important for Brazilianexporters, as a relatively large share of thecountry's agro-food exports tends to be in theform of bulk commodities.

The upgrading of rural infrastructure need notbe detrimental to the environment, but nor is itlikely that an unregulated expansion ofagricultural area will provide sufficientprotection to environmentally important areas.Brazil's policies need to take account of theimplicit trade-off between the economicbenefits and environmental costs ofagricultural growth in the Amazon region,while their design needs to reflect thedifficulties of policing such a vast area.

For many agricultural producers, the termsand availability of credit are also a majorconstraint. Commercial agri-businessestypically receive their payments in hardcurrency (mostly US dollars), which providesevidence of creditworthiness to lenders. Inmany cases, these companies do their ownlending to agricultural suppliers, either byproviding credit or financing inputs (such asfertiliser) directly. In Brazil, for example,soybean farmers often find it cheaper toobtain finance from the crushers.

The greatest difficulties arise for businessesthat are obliged to borrow on the domesticmarket. Although the economy has stabilisedin recent years, macroeconomic uncertaintystill has a disproportionate effect on less well-established companies without easy access to

Year XIV - Special edition - October 200515

overseas lenders. High real interest ratesmean that access to credit from banks isalmost prohibitive, despite governmentsubsidies. General credit subsidies riskcrowding out non-agricultural investmentmore than targeted subsidies to land reformrecipients and smallholders under thePRONAF programme.

Tax policies also have an important effect onproducers' opportunities. Under Brazil's ICMS(value added) tax system, each of thecountry's 26 states imposes its own taxes andexemptions. This distorts producers'incentives, while the system's complexityplaces an additional burden on taxpayers.

The shadow that hangs over attempts toimprove competitiveness, and to buildsuccessful agribusinesses around a corecomparative advantage in agriculture, is tradeprotection in important markets andsubsidised production and exports by rivalsuppliers. Some of the adverse impacts can becushioned by moves into products whereeffective demand is less constrained(e.g. tropical products), but these policiesnevertheless impose an important constrainton the agro-food sector's growth prospects.With supply-side improvements likely tocontinue, the need for further liberalisation oftrade in agricultural products becomes moreimportant.

The social challenges presented byagricultural development call for targetedadjustment policies and effective safety nets.

In addition to the need to continueimprovements in agricultural competitiveness,Brazil also faces a number of socialchallenges associated with agriculturaldevelopment. Agricultural employment fell by14% between 1992-93 and 2001-02. Thisdecline is not exceptional by internationalstandards, but it indicates particularly strongadjustment in the labour market, given that

the sector's share of national income wasmore or less constant over the same period.

Moreover, agricultural growth has made littleimpact on the problem of rural poverty. Morethan 60% of the rural population has anincome below an absolute poverty line of halfthe minimum wage, while income inequalityin rural areas has gone up over the lastdecade and the poorest have become poorer.Out-migration from rural areas may havehelped reduce rural poverty, but to a largeextent this has shifted the burden to urbanareas. Rural poverty is increasinglyconcentrated in the North and North East,where there is a heightened need for effectivedevelopment policies and social safety nets.

Poverty rates are influenced by twocompeting forces. On the one hand,economic growth at the national level helpsraise incomes, and generates demand-linkages throughout the economy. On theother hand, structural change poses a threat topoor producers who are progressively lessable to compete. The competitive pressuremay come from imports or from domesticpressures. Given that Brazil has little tariffprotection, the major challenge to lesscompetitive producers comes not from furtherliberalisation, but rather from structuralchange within the country, where traditionalproducers (often operating on a small scale)have experienced long-term price declinesbut not shared in the cost reductions thatgenerated them. Indeed, Brazil is becomingincreasingly competitive in a number ofproducts that have been important to smallscale farmers (e.g. dairy, maize); a positivedevelopment, but one that nevertheless putspressure on smallholders.

The key need is for targeted adjustmentpolicies. For some households, programmes toupgrade farming skills (e.g. through extension)may enable them to become competitivewithin the sector. At the same time, it isimportant to recognise that the long-term(inter-generational) future for most semi-

Year XIV - Special edition - October 2005 16

subsistence farm households lies outsideagriculture, so there is a parallel need formeasures that facilitate income diversificationand the exploitation of non-farm opportunities.Investments at the individual level, forexample through education and healthexpenditures, are important here, as arepolicies that foster rural development, such asinfrastructure development.

Many of the policies that improvecompetitiveness, or facilitate adjustment, fallwithin the general services element of thecalculation of total support to agriculture. Yetthis component of support has been falling atthe expense of producer support, mostlyprovided in the form of credit subsidies anddebt reduction. Moreover, the majority ofproducer support has not been targeted atpoorer agricultural households, while thepoorest of the rural poor are outside the scopeof several economy-wide social policies,particularly pensions.

Policies to improve commercial competitivenessand address social objectives need to takeaccount of the macroeconomic constraints thatbind policy makers. Neither improvements incompetitiveness nor long term poverty reductionare attainable without economic growth andstability, which in turn require fiscal disciplineand hence the adoption of well-targetedmeasures. Such policies have the potential tocreate a virtuous circle, with improvedcompetitiveness and enhanced human capitalsupporting faster economic growth.

In overall terms, Brazil has pursued essentialpolicy reforms that have benefited theagricultural sector and helped raise incomesand reduce poverty. A shift of support towardslonger term investments in areas such asinfrastructure, and research and extensionshould further enhance competitiveness, whilebetter targeting of agricultural and economy-wide social policies could enable agriculturaldevelopment to be more fully inclusive than ithas so far been.

Year XIV - Special edition - October 200517

This text was based on a presentation made atthe opening session of the Committee forAgriculture of the Organization for EconomicCo-operation and Development (OECD), inJune 2005, which held a debate on draft study“Review of Agricultural Policies in Brazil”,now published by that organization. Theobjective of the presentation was to highlightthe Brazilian delegation viewpoints on Brazilagriculture and agricultural policydevelopments, including social andenvironmental impacts.

The debate clearly demonstrated theinfluence of macroeconomic factors(monetary, fiscal and foreign exchangepolicies) and the limitations imposed byFederal Government fiscal constraints(balanced budgets requirements) to carry-outthe agricultural policy. Analysts, negotiatorsand policy makers in the field of internationalagricultural policy see a non evidentcontradiction between the outstandingBrazilian agricultural growth in the last fiveyears and the fact that Brazil has one of thelowest levels of farm support worldwide.OECD concluded that only 3% of gross farmreceipts in Brazil, in the period 2002-2004,were derived from government support.

This paper is divided in three parts: the firstpresents a brief summary of the Brazilianagricultural policies and its instruments; thesecond deals with issues on agriculture andenvironment with due considerations ofrecent concerns on the environmental impactof growth in soybeans production; the thirdpresents remarks concerning the Brazilianagricultural policy in the future.

Issues on Brazilagricultural policy

1. Brief history of thebrazilian agricultural policy2

Brazilian agricultural policy is based on twomain tools: credit and producers incomeguarantees. The first includes working capital,marketing and storage, and investment, andthe second one relays on a set of devicesdeveloped under the Minimum GuaranteedPrice Policy (PGPM) to support prices,guarantee producers income and ensurecomplementary food supply.

Table 1 presents the key points of theBrazilian agricultural policy which can betraced since its inception in 1931, when theConselho Nacional do Café [National CoffeeCouncil] and the Comissão de Defesa daProdução de Açúcar [Commission for theProtection of Sugar Production] were created.Afterwards, it was replaced by the InstitutoBrasileiro do Café (IBC) [Brazilian CoffeeInstitute] and the Instituto do Açúcar e doÁlcool (IAA)3 [Sugar and Alcohol Institute].Agriculture, mainly coffee, for many decadesgenerated most of the fiscal and foreignexchange revenues that enabled theimplantation of Brazil’s urban and industrialdevelopment model.

In sectors such as grains (cereals, oilseedsand fibers) and regional products (such assisal, jute and cashew nuts), the effectiveoutbreak of agricultural policy occurred in

1 Secretariat for Agricultural Policy of the Ministry of Agriculture, Livestock andFood Supply. This paper counted on the contribution of SPA-MAPA team.

2 A more complete analysis can be found in the paper “70 anos de PolíticaAgrícola no Brasil (1931-2001)”, by Carlos Nayro Coelho in Revista de PolíticaAgrícola, Year X, Jul-Aug-Sep 2001.

3 Both institutes were abolished in 1990.

Ivan Wedekin1

Year XIV - Special edition - October 2005 18

Elaboration: SPA-MAPA.

1931

1943

1945

1965

1966

1967

1987

1988

1991

1994

1995

1996

1997

1998

1999

2000

2003

2004

2005

National Coffee CouncilSugar Production Defense Commission

EGF-COV (Federal Government Loanswith Sell Option) extinction

Government Sell Option Contracts, Premium forCommercial Buyers (PEP) and Product DeliveryValue (VEP)

Marketing Credit Special Line (LEC)

CDA-WA and Private Sell Option Contract - PROP(Law 11076/04) and Purchase Option Contract

Table 1. Syntheses of the Brazilian Agricultural Policy.

Year XIV - Special edition - October 200519

1943, when the Comissão para Financiamentoda Produção (CFP) [Commission for ProductionFinancing] was established. This agency waslater (in 1990) transformed into the CompanhiaNacional de Abastecimento (CONAB) [NationalFood Supply Company], which arose from themerger of two companies controlled by theFederal Government: Companhia Brasileira deArmazenamento (Cibrazem) [NationalWarehousing Company] and the CompanhiaBrasileira de Alimentos (Cobal) [National FoodCompany].

In 1945 it was created the PGPM and its maindevices: the Aquisições do Governo Federal(AGF) [Federal Government Purchase], a sourceof direct intervention in the market, and theEmpréstimos do Governo Federal (EGF)[Federal Government Loans], credits formarketing and storage. The PGPM was modifiedin 1965 (Decree 57391) and underwent a deepreform in 1966 through the Decree-Law nº 79,whose characteristics remain in force.

The framework of preferential credit foragriculture was launched in 1965 under theSistema Nacional de Crédito Rural (SNCR)[National System of Rural Credit], by Law 4829,regulated by Decree 58380/66. The SNCR wasestablished once the Sistema FinanceiroNacional [National Financial System] was set inDecember 1964, which instituted the CentralBank (BACEN) and the National MonetaryCouncil (CMN). The CMN remains the decision-making body responsible for the mainagricultural policy measures. The Manual deCrédito Rural (MCR) [Rural Credit Manual]consolidated the guidelines of the SNCR,including the main types of credit: workingcapital, marketing and storage, and investment.The legislation defined rural producers and theircooperatives as public target, which haveaccess to credit at interest rates below thoseprevailing in the internal financial markets.Agroindustry firms may also have access to ruralcredit but always related to marketing creditoperations that benefit producers andcooperatives.

Rural financing development

Under Law 4829, which created the SNCR,the banks were obliged to reserve part of theirresources for rural credit, an exigibilidade4

which was regulated by the CMN in 1967.Current rule requires that 25% of cashdeposits in commercial banks must beinvested in agriculture. The non-fulfillment ofthis exigibilidade leads to the freezing of suchresources by the Central Bank, without anypayment to the financial institution.

In 1987, twenty years after the establishmentof these bank exigibilidade, a new source offunding was created – the Caderneta dePoupança Rural [Rural Savings Account],which was operated by Banco do Brasil,Banco do Nordeste do Brasil and Banco daAmazônia. The balance of deposits in Bancodo Brasil savings accounts is approximatelyUSD 12.6 billion. From the 1st of August 2005onwards, these three official banks mustcompulsorily offer 55% of these deposits tothe agricultural sector. The percentage ofcompulsory funding will grow by 5percentage points yearly until up to 65% onthe 1st of July, 2007.

Until 2004, the so-called Poupança Verde[Green Savings] was operated only by officialfederal banks. Private Banks and CaixaEconômica Federal (CEF) attracted resourcesfrom people through another type of savingsaccount, part of which is for the financing ofhome building. They are not allowed by lawto use those resources to finance agriculture,and official federal banks and cooperativebanks do not deal with savings for homebuilding financing. Private Banks areinterested in financing agriculture with part ofits savings deposits given that theseoperations have higher turnover and shorterterm, in comparison with real estatefinancing.

In March 2004, the Government allowed alsothe cooperative banks BANCOOB and

4 A certain share of banks obligatory sight deposits that can be allocated torural lending.

Year XIV - Special edition - October 2005 20

BANSICRED to deal with savings depositsunder the condition of investing 65% in ruralcredit. This opening of the rural savings marketfor cooperative banks rekindled the interest ofprivate banks facing difficulties in complyingwith home building exigibilidade.

The amendments of 1988 made in the BrazilianConstitution provided for the creation ofconstitutional funds for the development of theCenter-West (FCO), Northeast (FNE) and North(FNO) so as to carry fiscal resources toinvestment in these less-developed regions. Theconstitutional funds are important sources for thefinancing of agriculture and agro-industry. Overthe last two crop years, the three funds haveinvested in agriculture approximately USD 700million per year.

The first private instrument for agriculturalfinancing outside the SNCR, was the Cédulade Produto Rural (CPR) [Rural Product Note],created in 1994 by Law nº 8929. It is a note,issued by rural producers and cooperatives,which enables the financing of workingcapital, mainly for the purchase of agriculturalinputs. In addition to notes financed, acquiredor guaranteed by a bank, the market has alsoseen the rise of the so called “CPR degaveta”, which works mainly as a sort ofguarantee on commercial transactionsbetween rural producers and suppliers ofinputs, processing industries and foreign tradecompanies. The CPR-Financeira (CPR-F)[Financial CPR] was launched in 2000. Theoperation is settled in cash and thereto thereis no physical delivery of merchandise.

The Law5 that created CPR-F opened thedoors for an important source ofmodernization for the Brazilian agriculturecalled Moderfrota6, a program which financesthe agricultural machinery renewal.Moderfrota put forward a “family” of MAPA-

BNDES investment programs for ruralproducers and cooperatives. They rely onresources from the Fundo de Amparo aoTrabalhador (FAT) [Unemployement InsuranceFund] administered by the Banco Nacional doDesenvolvimento Econômico e Social[National Economic and Social DevelopmentBank] and contracted by financial agents7.

Between 1998 and 2003, MAPA launched 16new programs, which gave a new allure toproductive investment in agriculture.Breaking with monetary indexation habitude,all these programs work with fixed interestrates (from 8.75 to 12.75% per annum), longterm repayment (5 to 12 years) and costcompensation (equalização)8 by the NationalTreasury. The strong demand for agriculturalmachinery was also met by a line of creditcomplementary to Moderfrota, the BNDESFiname Agrícola Especial [Finame SpecialLine], for which interest rates is 13.95% perannum. After July 1st 2004, Moderfrota nolonger included cost compensation.

In the 2003-2004 Agriculture and LivestockPlan, the Government merged some programsand reduced their number from 16 to 8, and to 7in the following crop year. This rationalizationfacilitated the marketing and application offunds. Starting from the application of USD186 million in the 1999-2000 (Moderfrota -USD 114 million), the MAPA-BNDES programsreached a record of USD 1.9 billion in the2004-2005 crop, which ended in June, 2005.When added to other sources of funding(Finame Special Line, Constitutional Funds andRural Proger), investment credits provided toproducers reached USD 2.9 billion in the2004-2005 crop season.

Brazil is characterized by significantimbalances in the distribution of income onindividual, regional and sectorial levels. The

5 Provisional Decree 2117, of 1/10/2000, converted into Law 10200, of 14/2/2001.6 Program for Modernization of the Fleet of Agricultural Tractors and Associated Implements and Harvesters (Provisional Decree nº 2017-1, dated 2/17/2000,transformed into Art. 3º of Law nº 10200, dated 2/14/2001).

7 Finame Special Line (BACEN Resolution 2314/96) was the first step of BNDES in financing rural producers. The programs Prosolo (1998) and Proleite (1999) werecreated before Moderfrota.

8 Difference between the rate paid by producers and the costs with the remuneration of the FAT, BNDES and financial agents.

Year XIV - Special edition - October 200521

expansion of agriculture has had a beneficialeffect on the population residing in Brazil’sinterior. Nonetheless, the per capita income ofthe rural population is equivalent to 45% ofurban dwellers income.

Measures for the reduction of poverty arebeing implemented by several ministries andagencies, at the federal, state and locallevels. Brazilian agricultural policy has alsosought to promote the social and economicinclusion of producers and rural inhabitants.One important example is the ProgramaNacional de Fortalecimento da AgriculturaFamiliar (PRONAF) [National Program for theStrengthening of Family Agriculture], createdby Decree 1946/969. With a focus onsustainable rural development, the programinvolves market instruments (such as creditand insurance) and structural aspects(infrastructure, research, education).

From 2003 onwards, the emphasis has beenon increasing the volume of and facilitatingaccess to credit. In two years – between thecrops season of 2002-03 and 2004-05 – thePRONAF showed an exceptional growth: thenumber of operations rose from 926,000 to1.64 million, while the amount of creditgranted jumped from USD 660 million toUSD 2.3 billion.

The various macroeconomic stabilizationprograms implemented in the 1980s and1990s resulted in a rural debt crisis. Thedramatic situation was largely due to theincompatibility between the rate applied toadjust the outstanding debt and those used tocalculate minimum prices, which serve asreference in the formation of producerincomes. After a long and intense negotiation,the rural debt question was settled in threestages: Law nº 9138, of 1995, opened the firstphase of debt securitization; followed by therescheduling of debts above R$ 200,000 bythe Programa Especial de Saneamento deAtivos (PESA) [Program of Financial Assets

Rehabilitation], regulated by BACENResolution 2471/1998; and yet another stageby means of the Programa de Revitalizaçãode Cooperativas de Produção Agropecuária(RECOOP) [Program for the Revitalization ofAgricultural Production Cooperatives], underBACEN Resolution 2666/1999. It is estimatedthat the current stock of farm debt, originallycontracted with financial institutions, isapproximately USD 13 billion, with acompensation cost (equalização) whichrepresents the main share of FederalGovernment agricultural policy expenditures.

Market price and income support

The objective of the PGPM is to ensure anadequate income for producers andaccessible prices for consumers and tocomplement supply in regions where thedemand for certain products may exceedlocal supply. In order to achieve these goals,government intervention seeks to correctmarket failures, which are aggravated byBrazil’s continental dimensions and deficientinfrastructure.

The PGPM remained practically unchangedfrom the 1960s to the 1980s. The Preço deLiberação de Estoques (PLE) [Stock ReleaseSales Price] was set by the Agricultural Act in1992. It is a criterion used to define themarket government stocks sales price. It wasimplicit for the legislator that the governmentmarket intervention by means of stocks salemight be detrimental to the interestsof producers.

The fiscal crisis of the State forced theextinction of EGF-COV in 1996, whichcombined financing with sales option. Thisinstrument enabled the compulsory settlementof storage loans by delivery of the product tothe government, an eventuality which waslikely to occur in periods of high inflation.

The modernization of government marketintervention was initiated in 1997 so as tosustain farmers income, without necessarily

9 In 1999, the program's management was transferred from MAPA to the Ministryof Agrarian Reform, today Ministry of Agrarian Development.

Year XIV - Special edition - October 2005 22

including the purchase of goods andmaintenance of costly stocks by CONAB.

Sales Options Contracts for the sale ofagricultural products to the government is oneof the most important PGPM instruments. Astandard contract defines the date, locationand exercise price of the option. Thedifference between the price prevailing onthe market on the date of auction and theexercise price at a future date signals theupward trend in prices desired by the policymakers. In auctions organized by CONAB,rural producers and cooperatives – the targetpublic of the policy – purchase the right,subject to payment of a premium, to deliverthe product to the government if, on thecontracted date, market prices are below theexercise price. If the measure is efficient, inother words, if it helps market prices torecover, it will guarantee income toproducers, who will not exercise their options,thereby freeing the government from the needto use scarce funds in order to build up stocks.

By the Prêmio de Escoamento de Produto(PEP) [Premium for Commercial Buyers] andthe Valor de Escoamento de Produto (VEP)[Product Delivery Value], the governmentenables the transfer of products from regionswith excess production (and low producerprices) to other regions with supply deficits(especially North and Northeast). The PEPoperation occurs when the transferred productbelongs to the farmer or cooperatives. In thiscase, an auction defines the premium that thegovernment will grant to consumers for thepurchase of goods in the region with excessproduction, paying the minimum price to theproducer. In the VEP, the premium is paid toconsumers for the removal of public stocksdeposited in warehouses. In both cases, theauction opening premium, set by thegovernment, takes into account the productimportation parity in the destination region.

Established in 2003, the Linha Especial deCrédito à Comercialização (LEC) [SpecialCredit Line for Marketing] provides storage

credit using as parameter a price above theminimum price established by thegovernment, which serves as a reference forEGF contracts. This instrument has theadditional advantage of being simpler thanthe EGF.

The management of the PGPM is complexbecause it involves managerial,macroeconomic and fiscal issues. MAPASecretariat of Agricultural Policy isresponsible for defining the government’sintervention measures in agricultural markets.These policies are then carried out byCONAB. Annually, the federal budget sets outrevenue and expenditure forecasts andauthorizes a limited deficit for the executionof the PGPM, in the budget of the OperaçõesOficiais de Crédito (OOC) [Official CreditOperations], under the control of the NationalTreasury. Thereby, the effectiveness of marketinterventions depends on the size of theauthorized deficit and the generation ofrevenues from the sale of stocks. According tothe Fiscal Responsibility Law, no expendituremay be made without a correspondingavailability of resources in the budget.Considering that agricultural policy measuresmay affect the economy (price levels forexample), there is a need of coordination withFederal Government personnel in charge ofthe economic policy. It means that there is apermanent process of negotiation notrestricted to the need of ensuring resources toprovide price and income support toproducers.

Three outstandingagricultural policy phases

The last four decades of Brazilian agriculturalpolicy can be divided into three periods withmarkedly distinct characteristics. The firstphase, which lasted from 1966 to 1985, wasone of “Massive Intervention” by governmentin agriculture (Figure 1). There was a strongincrease in the supply of rural credit, reachingits peak in 1978, when the volume of

Year XIV - Special edition - October 200523

plunged from 85% of agricultural GDP in thelate 1970s to 29% in 1994. On the other hand,due to the big 1987 crop (a consequence ofCruzado Plan) the government providedmarket price support for up to 19% of thegrain production in 1988, by means of theMinimum Guaranteed Price Policy (PGPM).But the support fell down close do zero in theearly 1990s.

The third period – characterized by “LowInflation” – started with the Real Plan andpersists until today. This period is marked bythe almost complete depletion of traditionalagricultural policy instruments. In 1996, thesupply of rural credit fell to only 11% ofagricultural GDP and then was graduallyrecovered, reaching 25% in 2004. In thisperiod Government support to marketingremained between 2% and 5% of grainproduction.

preferential credit for rural producers wasequivalent to around 85% of agricultural GDP.By means of the PGPM, the governmentmarket price support to agricultural productsshowed a similar trend. The share of grainproduction benefiting from price supportmeasures rose from approximately 5% of totalproduction in the early 1970s to about 12% in1982. In addition to the accumulation of highlevels of stocks, government interventionincluded price controls and even fullregulation of an entire sector such as wheat.

From 1985 to 1994, agricultural policyreflected the “Debt Crisis and EconomicLiberalization”. The deep governmental fiscalcrisis and the measures taken to open up theeconomy, especially import tariffs cuts in theearly 1990s, caused a strong competitiveshock in the agricultural sector. The reductionin credit was enormous: in relative terms, it

Figure 1. Four decades of brazilian agriculture policy.Elaboration: SPA-MAPA.

Sources: BACEN, IBGE, CONAB.

Year XIV - Special edition - October 2005 24

In the 1965-85 period, about 80% of ruralcredit was derived from the government’smonetary budget, 12% came from bankingexigibilidades and 8% came from othersources (Figure 2). During the followingperiod, the 1990-94 “Debt Crisis”, thegovernment budget (National Treasury) felldrastically cut to 26% of total rural creditsupply. The worsening of public accountsobliged the government to modify the ruralcredit. In 1983, the CMN started to reduce theinterest rate implicit subsidy and adopted themonetary indexation of loans. In 1986,BACEN Conta de Movimento held in Bancodo Brasil was eliminated. It allowed thetransfer of high amount of resources from themonetary budget for rural credit. But what ismore impressive are the statistics for 2004,which show that the National Treasuryaccounted for only 4% of total rural creditsupply. Banking exigibilidades (41%) andrural savings (26%) became the two mainsources of rural credit. A point worthemphasizing is the redirection of rural credittowards productive investments. MAPA-BNDES programs represent 11% and theConstitutional Funds a further 6% of totalagricultural credit in 2004.

lines has jumped from USD 9.6 billion, inDecember 2002, to USD 23.7 billion inAugust 2005, an increase of 137%. In spite ofthe high interest rates prevailing in Brazil, thegovernment has decided to maintain theinterest rate of 8.75% for commercial farmersand up to 4% for small family farms(PRONAF).

There is a strong correlation between theincrease in grain planted area in recent yearsand the availability of investment credit foragriculture. In the 1999-2000 crop, the areaunder cultivation was 37.8 million hectares,which grew to 48.7 million in 2004-05.During the same period, rural investmentcredit rose from USD 900 million to a recordof USD 2.9 billion in the crop year that endedin June 2005 (Figure 3).

In recent years, there was a recovery of thelending to the agriculture sector and asubstantial improvement in the quality of credit.The rescheduling of agricultural debt approvedin the 1990s, along with exchange ratedevaluation and favorable conditions on worldcommodity markets, improved the agriculturalsector performance and reduced its credit risk.In December 2004, about 94% of total ruralcredit were classified as normal risk, e.g. withinthe four least risky levels (AA, A, B and C),according classification as defined by the CMN(Figure 4). By the end of August 2005, the shareof lendings classified as normal risk fell to 90%,a reflection of income crisis in the grain sector in2005, caused by an increase in the value ofnational currency and a crop lower than it wasexpected.

The challenge of guaranteeingprices and income

Empirical evidence demonstrates thatagricultural markets are much more volatilethan those for industrialized products. If this istrue for the world, in the case of Brazil thevolatility is even grater due to chronicinfrastructure deficiencies and ofmacroeconomic instability.

Figure 3. Planted area and agricultural investiment.Elaboration: SPA-MAPA.

Sources: CONAB, BNDES, BB, BNB, BASA

Corn is a good example of a volatile market. Inthe USA, the maximum annual price variationsare in a range of 20%, upwards or downwards.In Brazil prices reductions are frequentlyobserved from one year to the other and attainfrom 20% to 40%; and peaks of price changecan reach 60% in one year, as occurred in thesecond half of 2002 and 2003 (Figure 5).

In view of this instability and market failures,the demand for government intervention tostabilize producer prices and income is veryhigh in Brazil. The PGPM is established bylaw, but comes into conflict with another

more recent act called Fiscal ResponsibilityLaw, which prevents the government fromincreases in spending without the respectivebudgetary funding.

Last decade saw a strong reduction in theOfficial Credit Operations (OOC) budgetaryshare for the market price support. The budgethas fallen from about US$ 9 per produced ton ofgrain in 1997 and 1998, to less than US$ 0.90per ton in 2003 and 2004. It is an insignificantvalue when compared with grains averageprice of about US$ 200 per ton. The lack ofbudgetary funding is preventing an effectivepolicy of price stabilization, food supply andovercome agricultural market failures. Here isone of the greatest dilemmas faced by Brazilagricultural policy.

2. Agriculture and EnvironmentIn recent years, international press has givengreat emphasis to the Brazilian agriculture fortwo reasons. Firstly, it was due to productionand export increases, which allowed Brazil toachieve the largest trade surplus in the world,according to World Trade Organization (WTO)criteria. Secondly, because the pressure madeby environmentalists, especially regarding therapid expansion of soybeans cultivation.Competing international producers manifesttheir perplexity and concern about the factthat cultivated area in Brazil may expandsubstantially.

Indeed, the Brazilian agriculture potentialitiesrelated to the availability of land areimpressive. Brazil currently uses 48 millionhectares for annual or temporary crops and afurther 15 million hectares for permanentcrops. Cattle herd has reached 200 millionheads which occupy a pasture area of200 million hectares, showing a very low rate(0.9) of animals per hectare. In view oftechnological developments in livestockbreeding in the last two decades, it isestimated that 30 million hectares of pasturecould be shifted over to the production ofcrops without any adverse effects on meat

production. In addition, Brazil has a stock of106 million hectares of arable land that hasnot yet been exploited.

In other words, Brazilian agriculture isalready highly competitive and has a greatpotential for expansion because the ampleavailability of land (land prices are low inrelation to its international levels) and anenormous stock of technology related toagricultural production in tropical andsubtropical areas. Considering also theeconomy of scale advantages of bigger farmsand the prospects of logistic and transport costreductions, Brazil can increase strongly itsparticipation in the world agrofood market.Therefore, issues on the environmental impactof the Brazil agricultural growth are animportant aspect of the competitivenessamong major world agricultural producersand exporters.

Environment in Brazil is much more aquestion of law enforcement than policyconcerns. After May 2000, the Brazilianenvironmental legislation became even morerestrictive concerning land use by farmers.Out of the total farm area (exclusivepermanent preservation areas), the law for theLegal Amazon requires that the 80% of forestareas and 35% of cerrado areas shouldremains out of use. For other regions thisrequirement is 20%. Formerly, these figureswere 50%, 20% and 20%.

The impact of soybeans cultivation on theAmazon forest is small. Only 2.7% of theBrazilian soybeans are produced in the Northregion, and it does not necessarily come fromland originally covered by the Amazonrainforest. Soyabeans production representsonly 1.2% of the Legal Amazon area, out ofwhich 98% are in the States of Mato Grosso,Tocantins and Maranhão.

An analysis of soybeans production data bymunicipality, between 1990 and 2003, revealsthat its cultivations were increasinglyconcentrated in traditional producing areas.

Year XIV - Special edition - October 200527

The map shows the soybeans growth in Braziltakes a “Y” form (Figure 6). It starts in thesoutheast and northeast regions of Rio Grandedo Sul, passes through Santa Catarina, Paraná,São Paulo and reaches the Cerrado of MinasGerais. From this point onwards it splits into twobranches: westwards, including Goiás, MatoGrosso do Sul and Mato Grosso; and towardsthe northeast, encompassing the Cerrado ofWestern Bahia and, more recently, Tocantins,Maranhão and Piauí.

During the period under consideration,soybeans production increased from 20 millionto 52 million tons. However, the most importantproducing cities, responsible for 81% ofsoybeans planted area in 1990, remainedimportant in 2003, accounting for 63% of thetotal soybeans area. Production becameconcentrated in cities where soybeans were

already planted in 1990, and expanded towardsnew cities, most of them in the same region.

In addition to rigorous environmental legislation,technology has strongly contributed to thesustainability of brazilian agriculture. Oneexample of good practices in Brazil is the directtillage. Indeed, it is an example to the world.This technology spares land, reduces erosionand improves soil quality, especially with regardto microorganisms and the percentage oforganic material. It lessens the need to till thesoil and, therefore, the demand for capital andfuel, and also cuts the consumption of plantprotection products, thereby reducingenvironmental impacts and production costs.

In 1992, direct tillage was utilized in 2 millionhectares, about 4% of the grain planted area,and 22 million hectares in 2003, representing37% of total cultivated grain area in Brazil.

Figure 6. Soybeans expansion in Brazil.Elaboration: SPA-MAPA.

Source: IBGE.

Legal Amazondivision line

“Cerrado”division line

Year XIV - Special edition - October 2005 28

3. The future of agricultural policy

Macroeconomic restrictions

The nature of agricultural markets makesthem vulnerable to infrastructure deficienciesand dependent on macroeconomic policy-making. Brazil has been forced to live withhigh real interest rates, above 20% perannum, as registered 1998 and 1999 and inthe second half of 2002. Although real interestrates have fallen in recent years, Brazil is stilla world champion in terms of high realinterest rates, whose level was about 14% perannum in October 2005.

Such high levels of interest rates accentuatethe market failures and reduce demand,especially in harvest season, when a largevolume of product comes on the market.Consequently, market volatility is increased,to the detriment of farmers at the very momentin which they must market their crop.

In view of the high degree of insertion ofBrazilian agriculture in the internationalmarket, for the majority of farmers theirincome is the result of a combination ofinternational commodity prices and exchangerate. In this sense, the exchange rate is thekey variable for the agribusiness. Thedevaluation of the Brazilian currency whichbegan in 1999 stimulated agricultural growth insubsequent years. From 2004 onwards,however, there has been a continuousdownward trend in the exchange rate, from anaverage of R$ 3 per US dollar in the second halfof 2004 (inputs purchasing period for plantingthe 2004-05 crop), to around R$ 2.50 in thesecond quarter of 2005, when the crop is sold.This situation put an unexpected pressure on thebalance sheet of grain production in 2005. Thegross value of the production of the five maintypes of grain – rice, cotton, corn, soybeans andwheat – fell from USD 20.5 billion, in 2004, toan estimated USD 18.8 billion in 2005. The fallin prices is responsible for 83% of this reduction,while the remaining 17% is due to the reductionin crop size caused by the weather.

The deficiencies in infrastructure represent aprime example of how the “Brazil cost”affects agriculture, with a powerful effect onproducer’s income since agricultural andlivestock products typically have low unitvalue, increasing the relative share oftransportation and distribution expenses in thefinal price of goods in consuming markets.Under a situation that has dragged on formore than ten years, Brazil invested less than1% of GDP in transportation in 2004, and thevalue of interest rate payments wasequivalent to 7.4% of GDP.